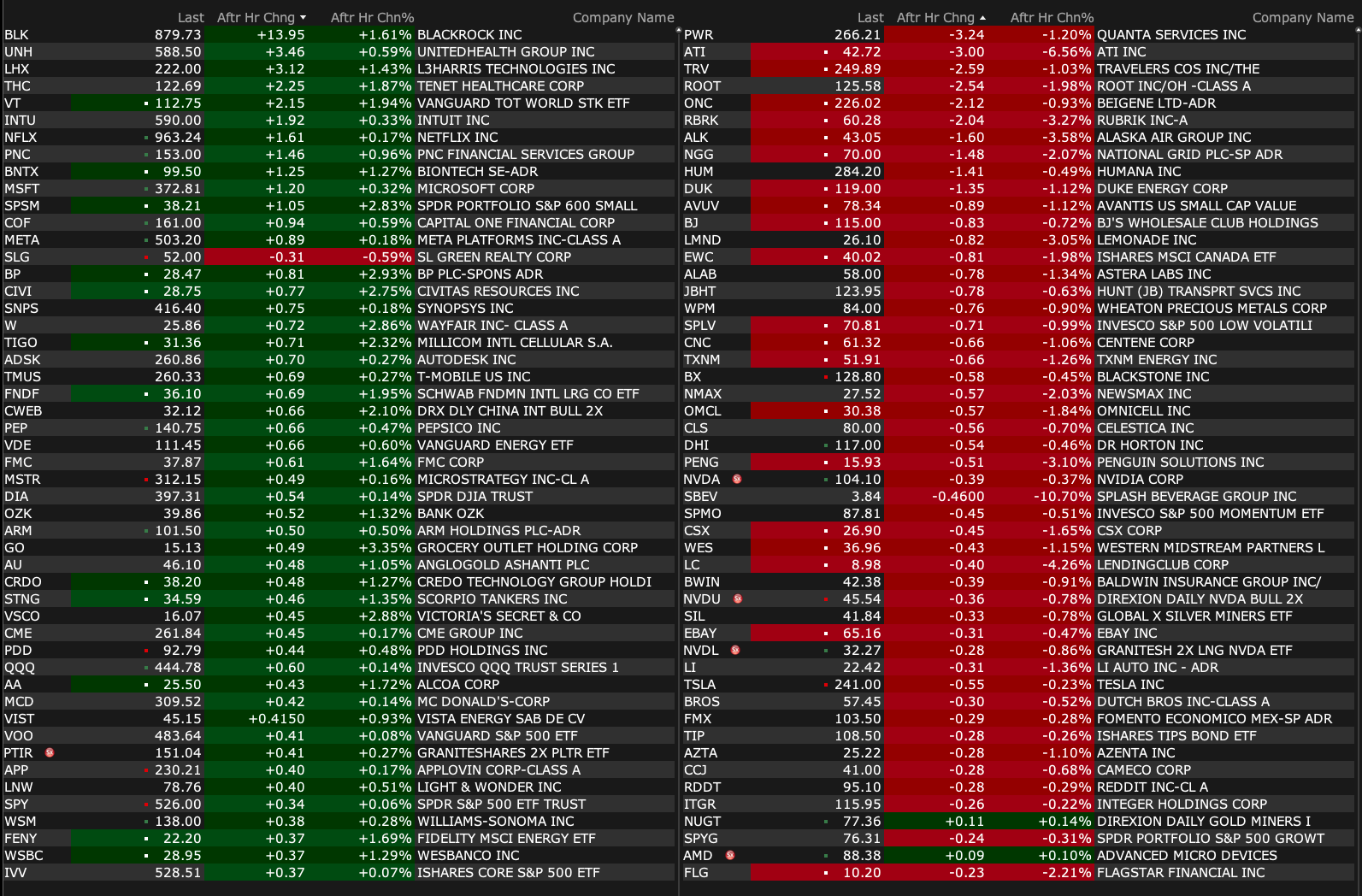

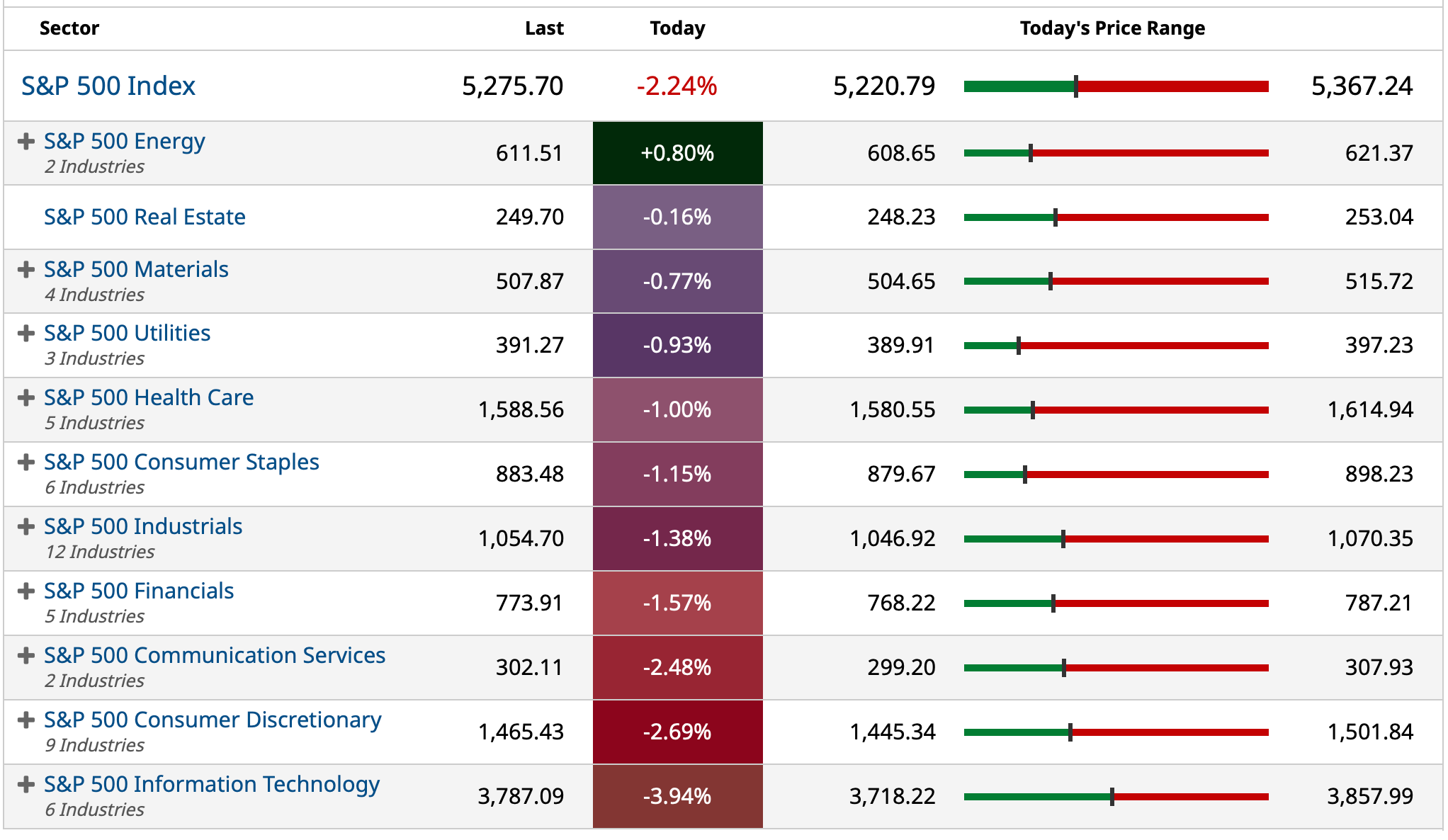

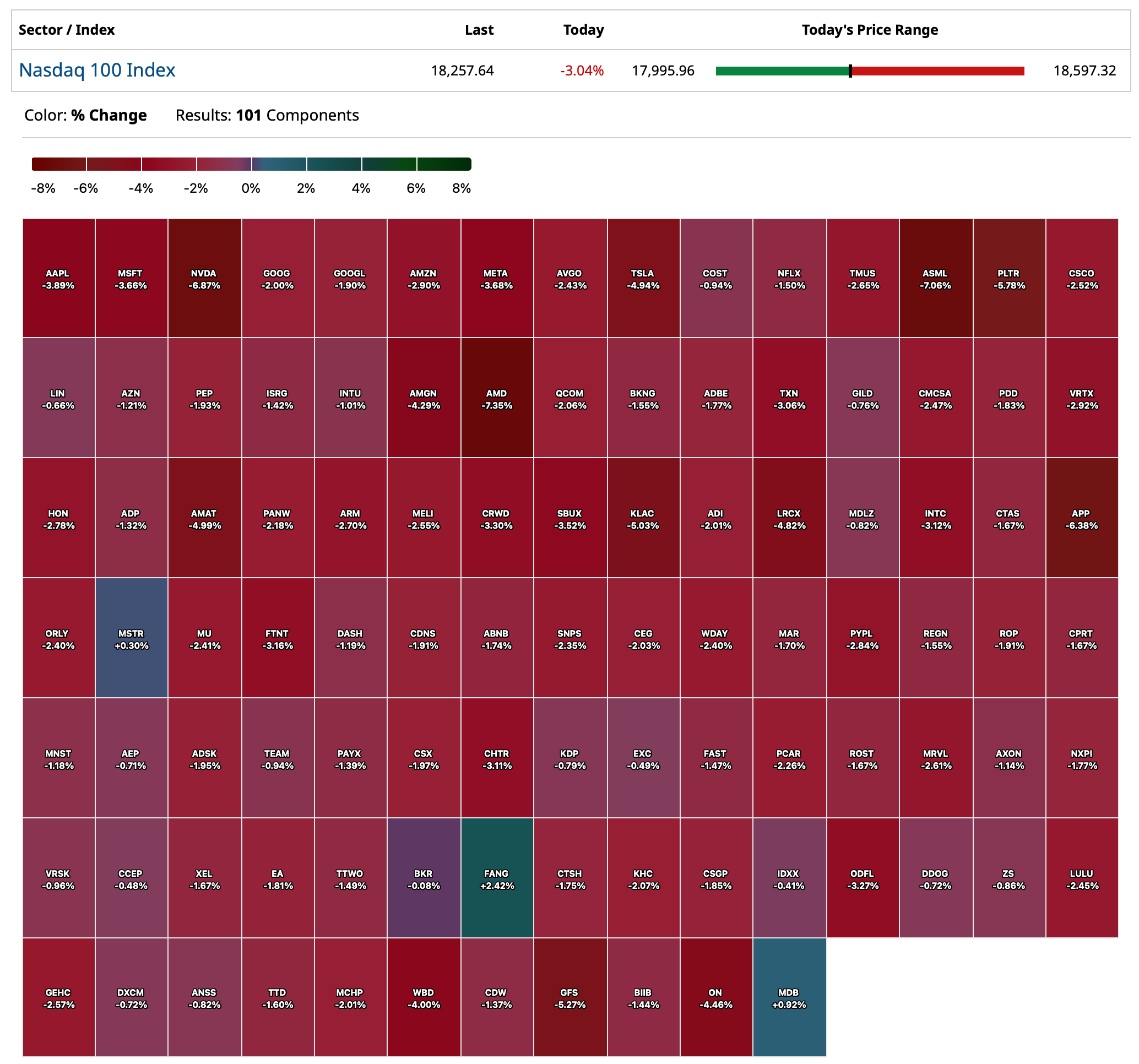

Wednesday's After-Hours Movers

At 4:22 p.m.:

BY Doug Kass · Apr 16, 2025, 4:45 PM EDT

At 4:22 p.m.:

BY Doug Kass · Apr 16, 2025, 4:45 PM EDT

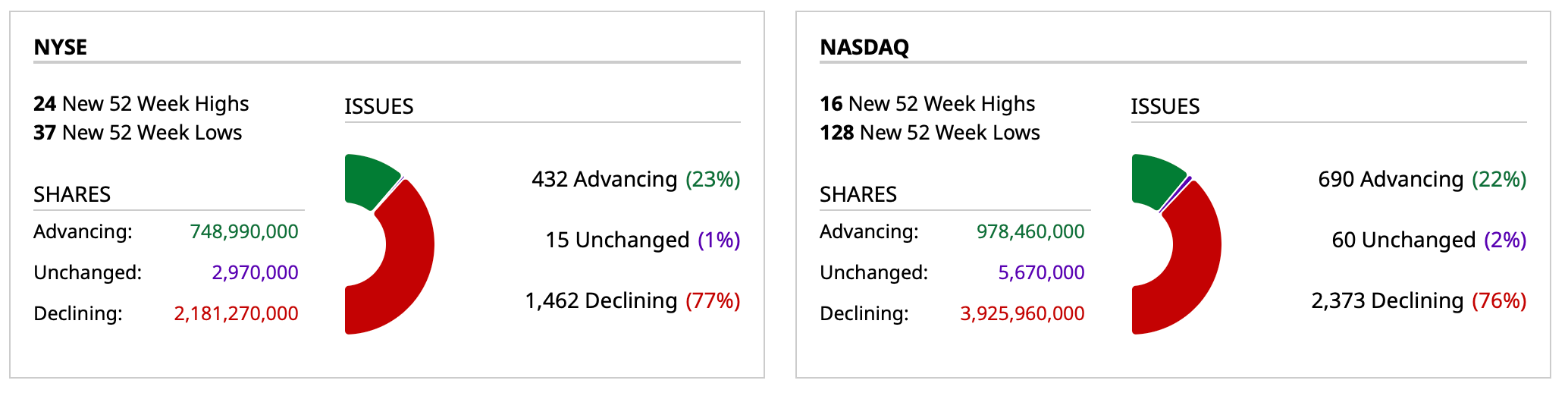

- NYSE volume 23% below its one-month average

- NASDAQ volume 14% below its one-month average

- VIX index: up 8.37% to 32.64

BY Doug Kass · Apr 16, 2025, 4:36 PM EDT

BY Doug Kass · Apr 16, 2025, 3:49 PM EDT

I'm back buying private equity shares: APO at $123.81, BX at $127.75 and KKR at $100.91.

BY Doug Kass · Apr 16, 2025, 3:44 PM EDT

BY Doug Kass · Apr 16, 2025, 3:15 PM EDT

This might be a significant and positive development for cannabis.

BY Doug Kass · Apr 16, 2025, 3:05 PM EDT

From Peter Boockvar:

"Life moves pretty fast" said Ferris Bueller, quoted by Jay Powell

While this could change, Powell in his just released speech is reflecting his bias to protect us first against inflation rather than the labor market being his main focus right now. He believes you need the former in order to help the later. He said, “without price stability, we cannot achieve the long periods of strong labor market conditions that benefit all Americans.”

Basically the Fed is telling us, when we review what Powell just said and what Susan Collins said last week, is that the first help we could get from them would be more liquidity based if markets freeze up rather than rate cuts to help the economy, as of now.

That said, I believe he’s overly optimistic on the state of the US economy currently, referring to it as “still in a solid position” though he does acknowledge the slowing going on, as will be seen for Q1 and the threats from tariffs.

He did add some levity to his speech in Chicago by quoting in his concluding paragraph “that great Chicagoan Ferris Bueller” who “once noted, ‘Life moves pretty fast.’ And then, “For the time being, we are well positioned to wait for greater clarity before considering any adjustments to our policy stance.”

As seen, stocks went to the lows of the day as he likely disappointed anyone hoping for a rate cut sooner rather than later. The 2 yr yield though at 3.80-.81% is about where it was right before the speech was out. Rate cut odds for the June meeting stands at 60%, so call it about a coin toss as of today.

BY Doug Kass · Apr 16, 2025, 2:26 PM EDT

Alibaba BABA is down by -$5 as chatter about a Trump delisting of Chinese companies circulates in the whisper circuit.

A good sale five days ago:

Also sold (BABA) (I had averaged down) at $105.60 for a near $2 profit.

Position: None

By Doug Kass Apr 11, 2025 12:47 PM EDT

BY Doug Kass · Apr 16, 2025, 1:25 PM EDT

META looks like it may now break a double top on the daily chart.

BY Doug Kass · Apr 16, 2025, 1:20 PM EDT

From Dan Niles:

BY Doug Kass · Apr 16, 2025, 1:08 PM EDT

I have taken a trading long rental in IWM at $185.74.

BY Doug Kass · Apr 16, 2025, 12:16 PM EDT

I added to RSP at $163.45.

I added to technology.

BY Doug Kass · Apr 16, 2025, 12:02 PM EDT

I don't even know what Jim Cramer means (regarding Nvidia NVDA as a meme stock):

BY Doug Kass · Apr 16, 2025, 11:52 AM EDT

BY Doug Kass · Apr 16, 2025, 11:20 AM EDT

From Peter Boockvar:

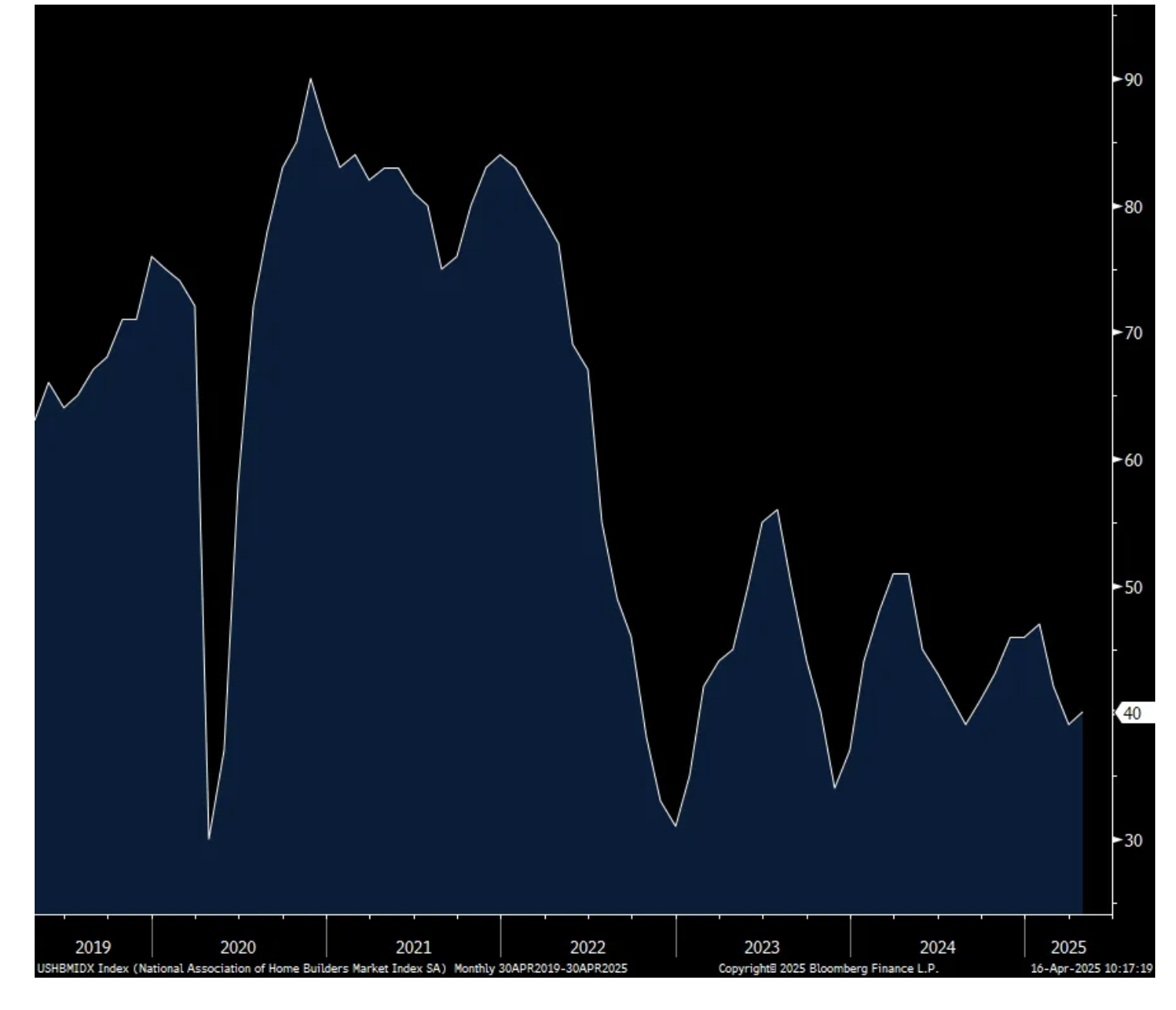

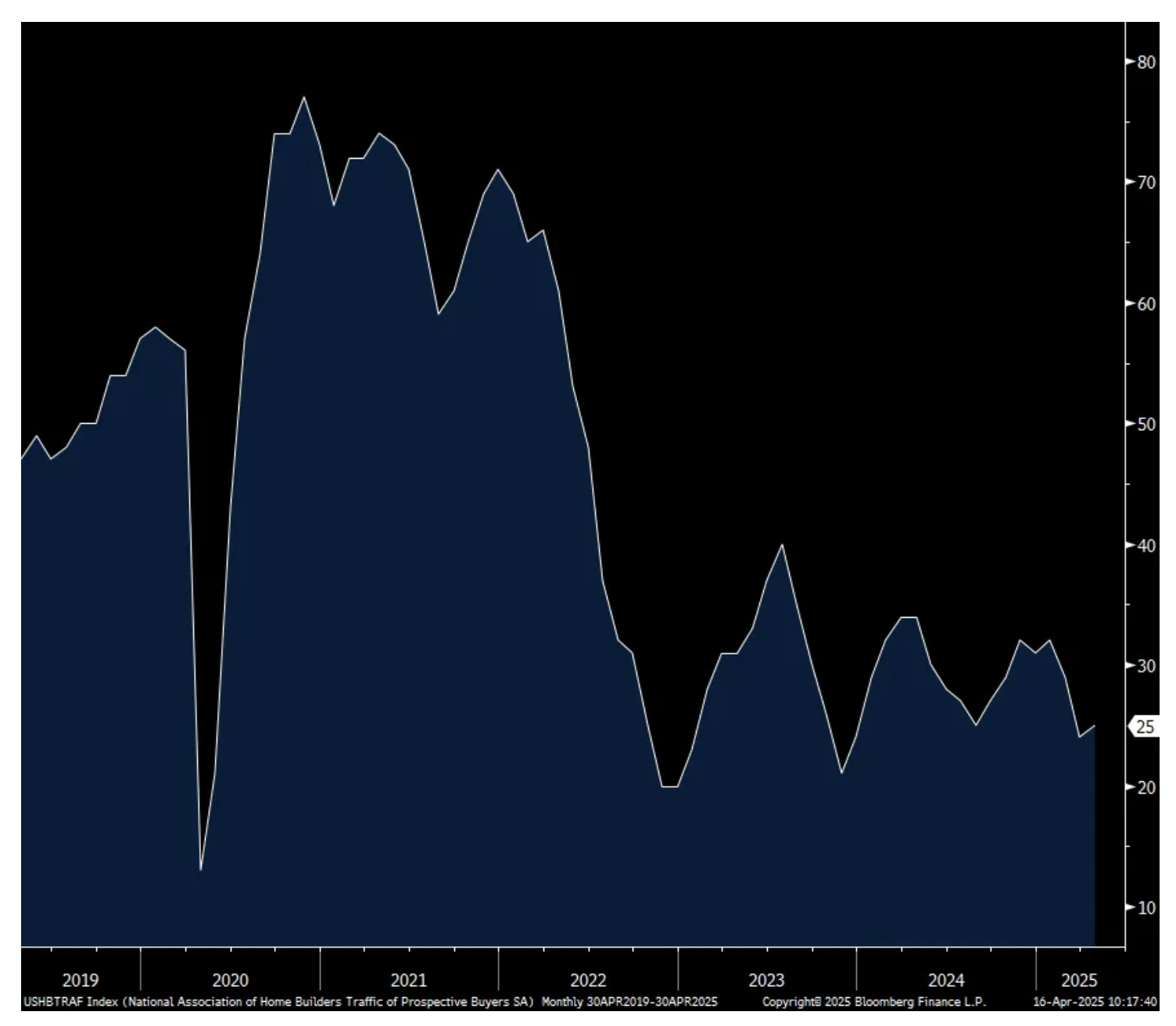

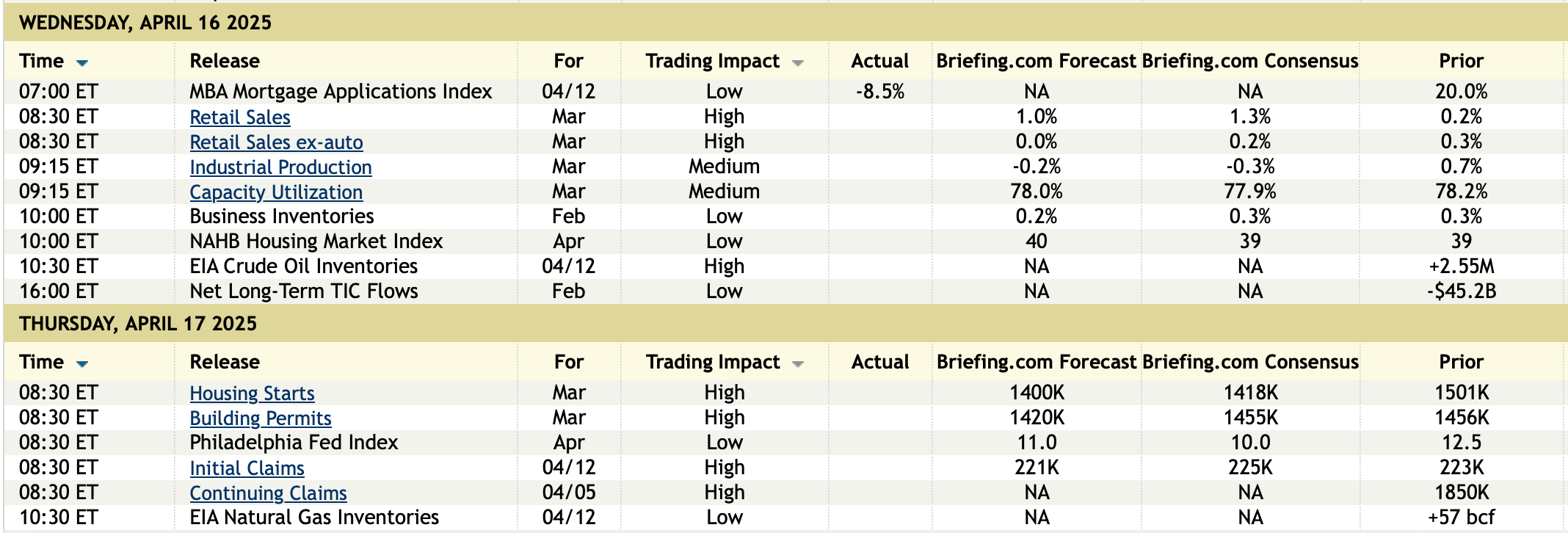

The April NAHB home builder sentiment index rose 1 pt m/o/m to 40 but remaining well below 50. The estimate was for a 1 pt drop to 38. While the Present Situation rose 2 pts to 45, the Expectations component was down by 4 pts to 43, the lowest since November 2023. Prospective Buyers Traffic was 25, up 1 pt but half the level of the 50 breakeven.

The press release from the NAHB was littered with tariff talk. While the April headline got a slight lift as “The recent dip in mortgage rates may have pushed some buyers off the fence in March, helping builders with sales activity,” builder visibility is clear as mud and business is getting more costly. “At the same time, builders have expressed growing uncertainty over market conditions as tariffs have increased price volatility for building materials at a time when the industry continues to grapple with labor shortages and a lack of buildable lots.”

More, “Policy uncertainty is having a negative impact on home builders, making it difficult for them to accurately price homes and make critical business decisions. The April data indicates that the tariff cost effect is already taking hold, with the majority of builders reporting cost increases on building materials due to tariffs.”

To what extent and by how much? “When asked about the impact of tariffs on their business, 60% of builders reported their suppliers have already increased or announced increases of material prices due to tariffs. On average, suppliers have increased their prices by 6.3% in response to announced, enacted, or expected tariffs. This means builders estimate a typical cost effect from recent tariff actions at $10,900 per home.”

No bottom line from me needed as the comments above from the NAHB speak for themselves.

NAHB

Prospective Buyers Traffic

BY Doug Kass · Apr 16, 2025, 11:15 AM EDT

Chart from 10:04 a.m. ET:

BY Doug Kass · Apr 16, 2025, 11:00 AM EDT

From Peter Boockvar:

Core retail sales in March rose .4% m/o/m, two tenths below expectations but offset by a three tenths upward revision to February to a gain of 1.3%. Clear evidence of a buying rush ahead of tariffs was apparent as auto/parts sales jumped by 5.3% after two months of declines. Building material sales were higher by 3.3% m/o/m.

Elsewhere, sales for furniture fell by .7% but electronics sales rose by .8%. Clothing sales rose .4% m/o/m after declines in the two prior months. We’ll see if sock sales pop in April. Sporting goods sales jumped by 2.4% as we enter spring time. Department stores sales dropped by .3% and down by 5.5% y/o/y as this sales outlet continues to struggle. Sales at restaurant/bars rebounded by 1.8% after an .8% drop in February. Online retail sales were flattish, up one tenth but still up 6.1% y/o/y. Sales at miscellaneous stores like pet, dollar, flower, convenience, etc… saw a .7% m/o/m sales gain and by 6.7% y/o/y.

As for the necessities, health/personal care sales rose .7% m/o/m and by 6.4% y/o/y. Food/beverage saw sales up by .2% m/o/m and .6% y/o/y.

Bottom line, as higher prices start to kick in with autos, we’ll see slower sales of them after this rush to buy. As for the broader view, this data is before the April 2nd news, both tariff on, off and a step towards 145% on China so I assume we’ll get a further lift in pull forward buying and then the hangover. Either way, there remains a bifurcation of sales between upper income consumers and the lower end as we all well know. And all eyes on that upper income spender and how they process the declines in their stock portfolios and how that is expressed in their consumption.

BY Doug Kass · Apr 16, 2025, 10:50 AM EDT

DK

Doug Kass

STAFF

4 minutes ago

I remain bearish, if I didnt make it clear!!!

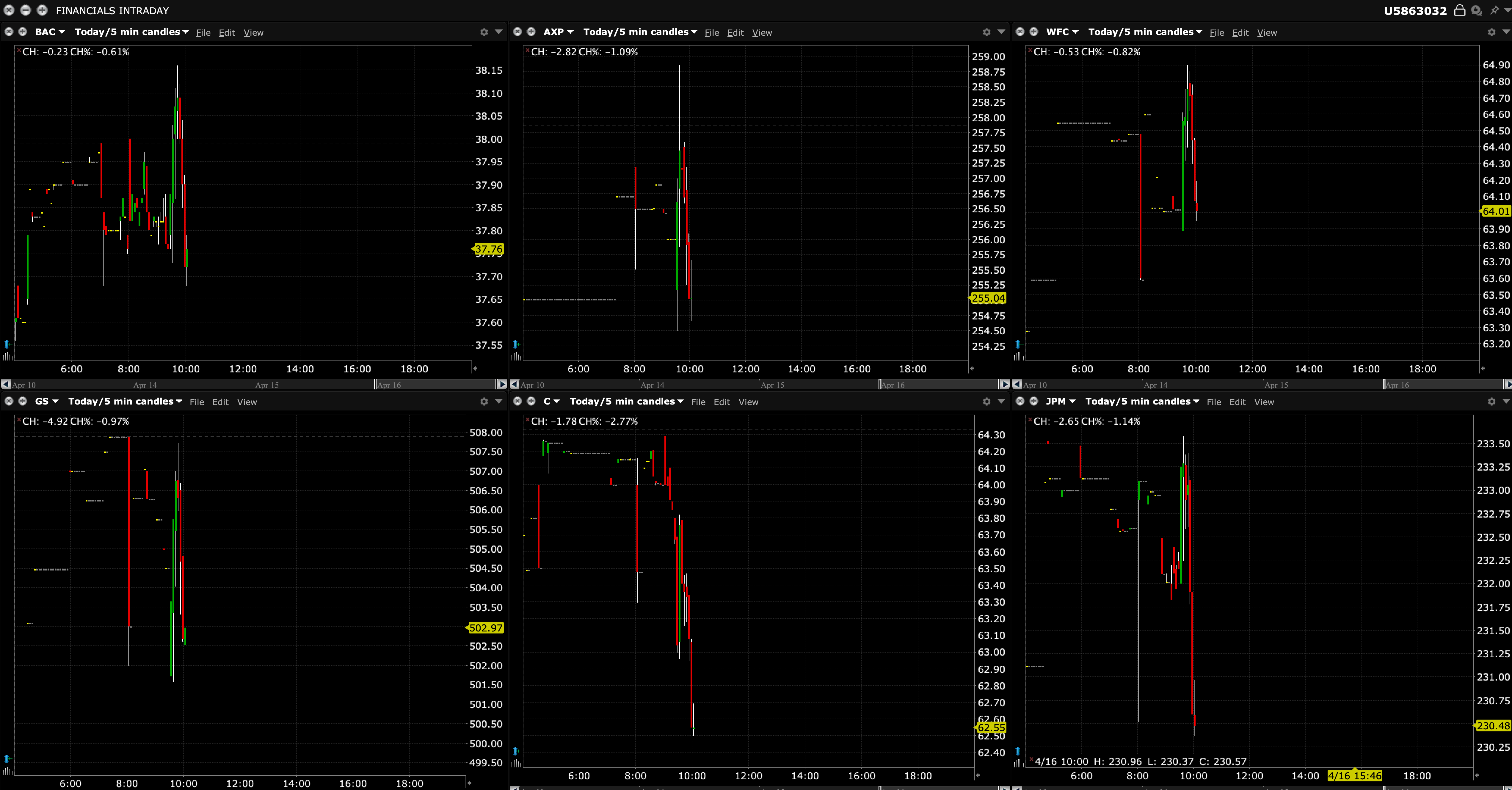

If the market loses the financials (I am long), katie bar the doors.

BY Doug Kass · Apr 16, 2025, 10:33 AM EDT

I just went long RSP at $162.86.

BY Doug Kass · Apr 16, 2025, 10:28 AM EDT

Here are today's things:

* Added to technology: AMZN $176.82 GOOGL $153.405 META $510.06 MSFT $378.89

* Sold SPY puts and calls for May ($530-kind)

BY Doug Kass · Apr 16, 2025, 10:21 AM EDT

BY Doug Kass · Apr 16, 2025, 10:19 AM EDT

New short CoreWeave CRWV down by another two beaners today (to $38.15).

From Monday:

I am short (CRWV) at $45.66

More later this week on the name.

Position: Short CRWV VS.

By Doug Kass Apr 14, 2025 9:51 AM EDT

BY Doug Kass · Apr 16, 2025, 10:19 AM EDT

Adding more aggressively to my short straddles/strangles.

BY Doug Kass · Apr 16, 2025, 10:14 AM EDT

BY Doug Kass · Apr 16, 2025, 10:02 AM EDT

On banks and NVDA:

Citi price target lowered to $79 from $84 at Truist Truist lowered the firm's price target on Citi to $79 from $84 and keeps a Buy rating on the shares as part of a broader research note on large-cap updating the firm's models following Q1 earnings. The firm's revisions reflect modest downward adjustments to EPS, incorporating more conservative run rates on certain fee revenue lines and slightly higher provisioning, the analyst tells investors in a research note. Truist sets its price targets lower on a combination of slightly lower EPS estimates and more conservative valuation multiples, reflecting the increased uncertainty and risks associated with the current macro environment, the firm added.

Citi price target lowered to $77 from $83 at Piper Sandler Piper Sandler lowered the firm's price target on Citi to $77 from $83 and keeps an Overweight rating on the shares following quarterly results and updated guidance. The firm cites its new EPS estimates offset by the recent decline in bank equity valuations. Piper's 2025 EPS goes from $7.29 to $7.35, and its 2026 EPS goes from $8.94 to $9.20.

Bank of America price target lowered to $47 from $50 at Truist Truist lowered the firm's price target on Bank of America to $47 from $50 and keeps a Buy rating on the shares as part of a broader research note on large-cap updating the firm's models following Q1 earnings. The firm's revisions reflect modest downward adjustments to EPS, incorporating more conservative run rates on certain fee revenue lines and slightly higher provisioning, the analyst tells investors in a research note. Truist sets its price targets lower on a combination of slightly lower EPS estimates and more conservative valuation multiples, reflecting the increased uncertainty and risks associated with the current macro environment, the firm added.

Bank of America price target lowered to $42 from $45 at Piper Sandler Piper Sandler analyst R. Scott Siefers lowered the firm's price target on Bank of America to $42 from $45 and keeps a Neutral rating on the shares following quarterly results and updated guidance. The firm cites lower bank equity valuations. Piper's 2025 EPS goes from $3.61 to $3.67, though its 2026 EPS goes from $4.09 to $4.03.

KR price target lowered to $138 from $169 at Oppenheimer Oppenheimer lowered the firm's price target on KKR to $138 from $169 and keeps an Outperform rating on the shares as part of a Q1 preview for the alternative asset managers. These companies have the best business models in financial services and perhaps in any industry, the analyst tells investors in a research note.

Blackstone Mortgage price target lowered to $18.50 from $20 at JPMorgan JPMorgan lowered the firm's price target on Blackstone Mortgage to $18.50 from $20 and keeps a Neutral rating on the shares as part of a Q1 preview for the mortgage real estate investment trusts. Lower short-term rates provide incremental credit relief for borrowers in the form of lower financing costs, but may signal an elevated risk of recession, which could pressure occupancy and rent growth rates and make final resolution of troubled assets more difficult, the analyst tells investors in a research note. The firm says elevated macro uncertainty and a more "two sided risk/reward outlook tempers" its conviction on the MREITs.

PNC Financial price target lowered to $178 from $179 at Morgan Stanley Morgan Stanley analyst Betsy Graseck lowered the firm's price target on PNC Financial to $178 from $179 and keeps an Underweight rating on the shares. PNC reported a 4% EPS beat, mainly on lower provision, and fiscal year guidance was reiterated, the analyst noted following the company's Q1 earnings report.

Cantor says Nvidia Q1 revenue remains intact with only two weeks left After Nvidia filed an 8-K noting that its Q1 results will now include up to $5.5B of charges associated with H20 products and the U.S. Governments decision to require licenses to export to China, Cantor Fitzgerald sees "a fairly major hit" to EPS, which at "first blush" the firm thinks is now likely tracking closer to 76c than the consensus of 93c. However, Q1 revenues remain intact with only two weeks left and the firm still thinks revenues will be "a beat, though smaller" than the ones seen in the prior seven quarters. While it now appears investors need to derisk Nvidia completely from serving 20% of the AI market in China, the stock was trading down 6% on the news and the firm would be buyers on weakness as it reiterates an Outperform rating and $200 price target on Nvidia, which remains the analyst's "Top Pick."

Nvidia H20 restrictions 'more abrupt' than Morgan Stanley expected After Nvidia filed an 8K to disclose that the U.S. government has enacted new licensing requirements for shipments of the H20 product, "and any other circuits achieving the H20's memory bandwidth, interconnect bandwidth, or combination thereof," to China or companies headquartered in China and said it will see up to $5.5B in inventory charges in the April quarter, Morgan Stanley analyst Joseph Moore noted that this is not a ban, it is a licensing requirement, but argues that the inventory writedown suggests that the company is "not optimistic about being granted licenses." The firm expected H20 to be restricted by export controls, but stopped shipments "effective immediately" is a bit more abrupt and disruptive than expected and the large inventory writedown is "a cautionary signal," the analyst added. While the firm is trimming estimates for the next couple of quarters to remain conservative, it says Nvidia remains its top pick in semis with an Overweight rating and $162 price target on the shares.

Nvidia price target lowered to $160 from $200 at BofA BofA lowered the firm's price target on Nvidia to $160 from $200 and keeps a Buy rating on the shares. For U.S. chip vendors, the firm expects Q1 results to beat as their original outlook was likely conservative and as tariff related pull-ins created a better demand environment, the analyst tells investors in an earnings preview for the group. However, the firm lays out scenarios where a "modest" tariffs equate to a 4%-6% sales hit on average for the group and where "deeper" tariffs in "a dire scenario" equate to sales decline of 9% and 12% in calendar year 2025 and 2026 on average. In a modest tariff scenario, the EPS hits could be 12%-13%, added the firm, which lower targets across its semis coverage to reflect growing uncertainty.

BY Doug Kass · Apr 16, 2025, 9:53 AM EDT

Adding back to AMZN, GOOGL, MSFT and META (I had sold down the positions on strength a week or so back).

BY Doug Kass · Apr 16, 2025, 9:51 AM EDT

And the beat goes on:

I add to cannabis positions daily.

Investment, not a trade (see me in a year!).

BY Doug Kass · Apr 16, 2025, 9:50 AM EDT

BY Doug Kass · Apr 16, 2025, 9:35 AM EDT

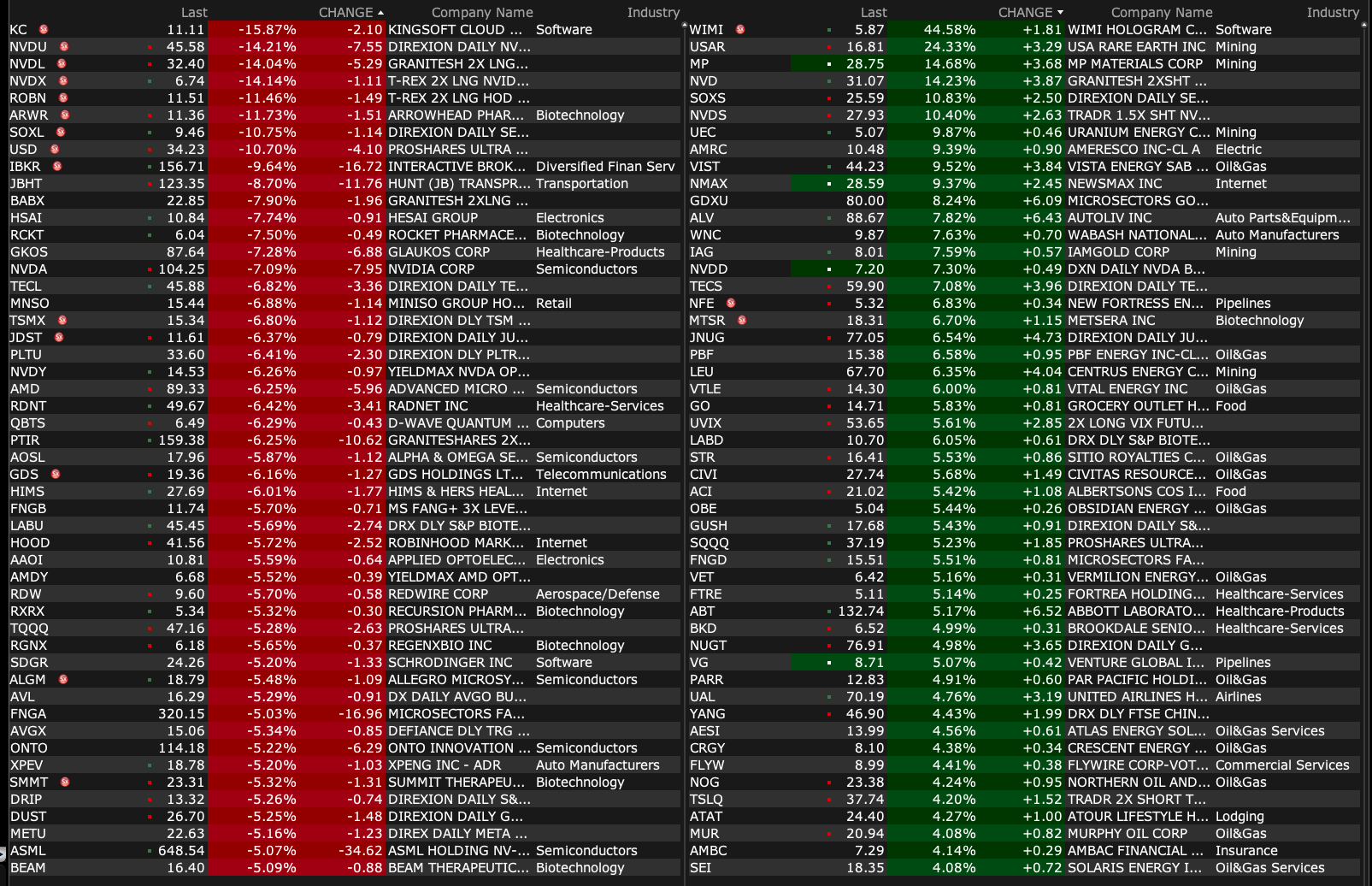

Premarket percentage movers at 8:53 a.m. ET:

BY Doug Kass · Apr 16, 2025, 9:26 AM EDT

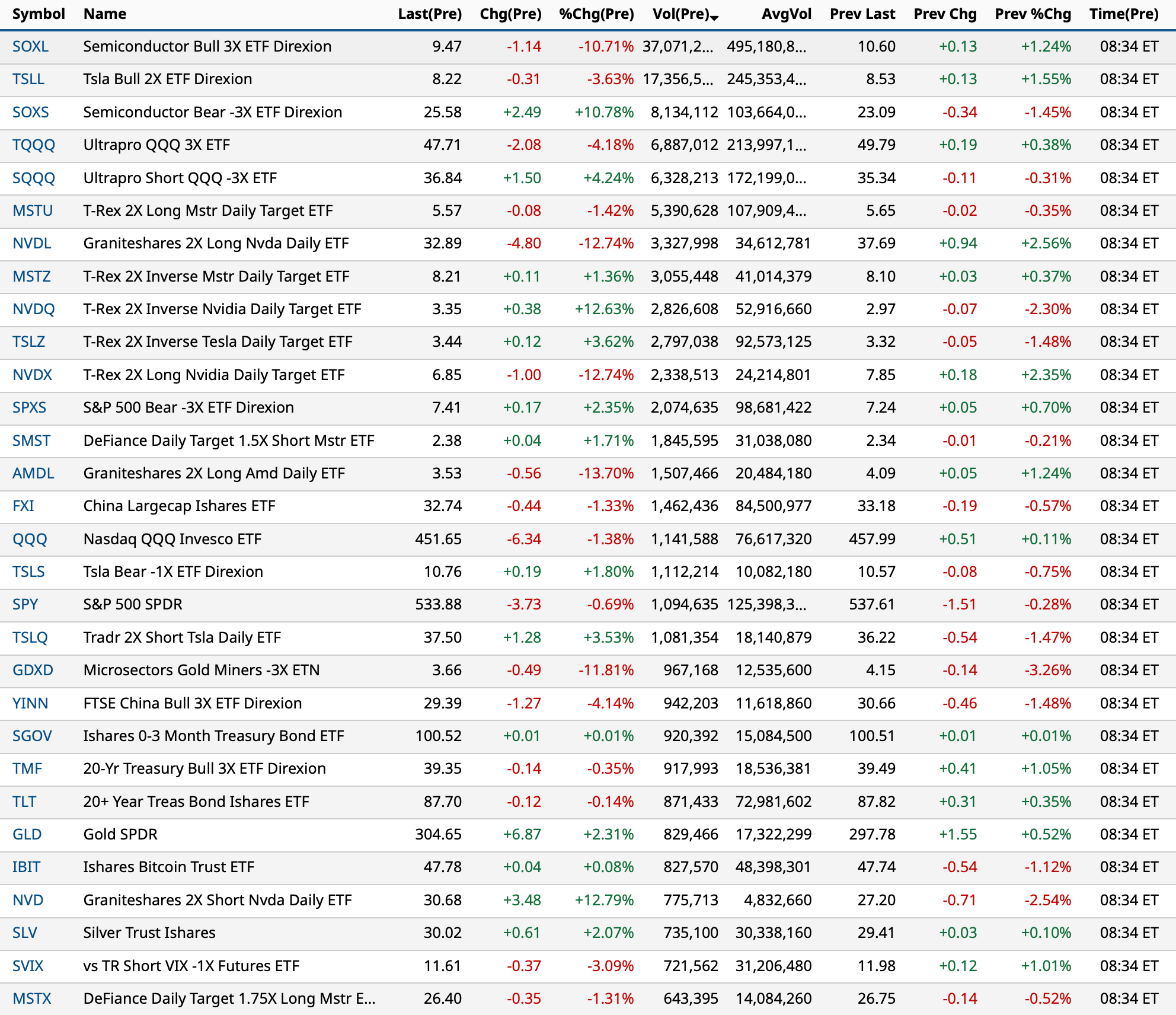

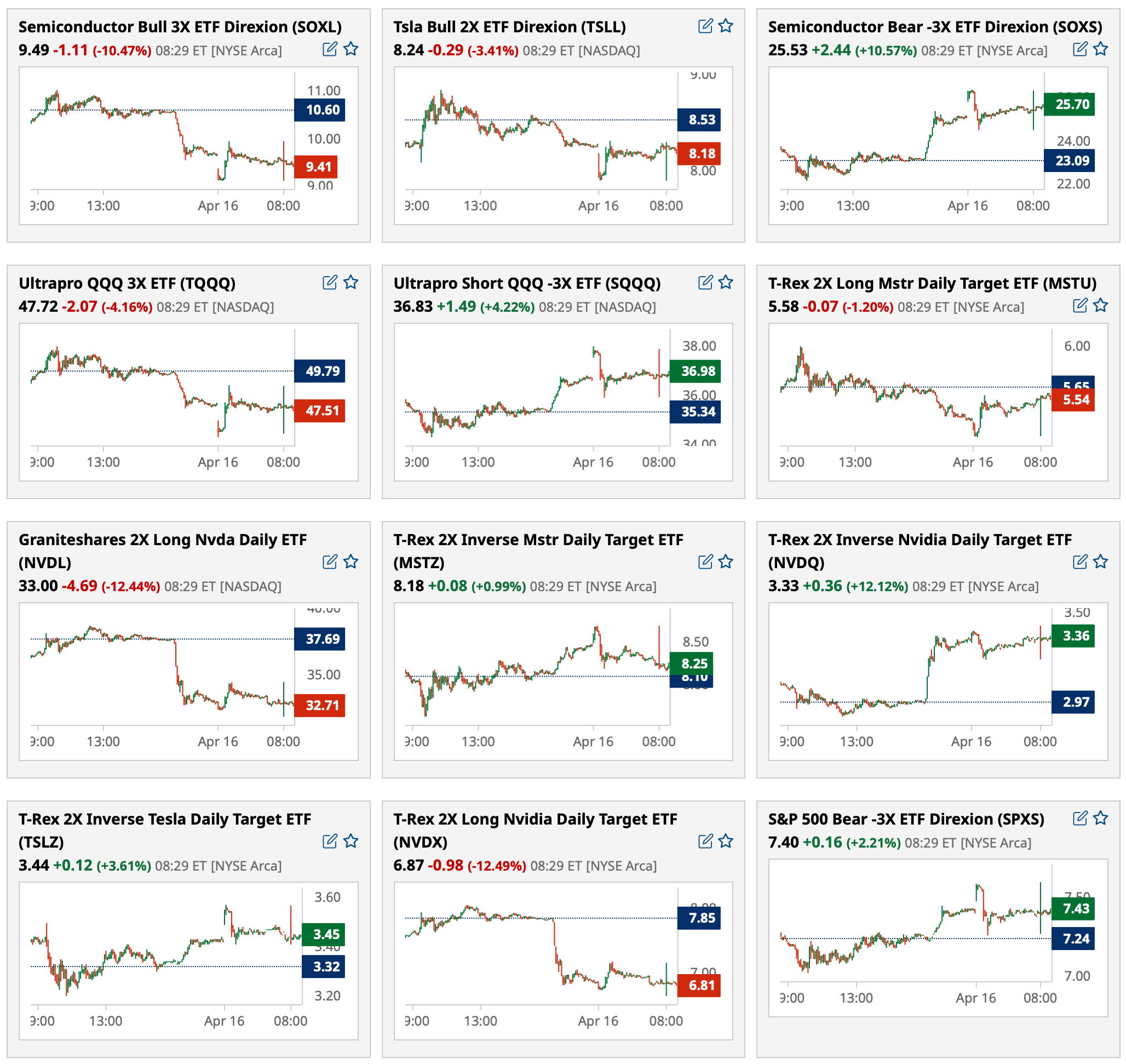

Most active premarket ETFs as of 8:34 a.m. ET:

BY Doug Kass · Apr 16, 2025, 9:16 AM EDT

-ICAD +70% (to be acquired by RadNet in an all stock deal)

-HTZ +17% (Pershing Square discloses ~12.7M share holding as of Dec 31, 2024)

-ALV +7.5% (earnings, guidance)

-UAL +6.3% (earnings, guidance)

-MOV +5.3% (earnings)

-TRV +2.5% (earnings; raises dividend)

-PGR +2.1% (earnings)

-KC -11% (files to sell public equity offering of 18.5M ADSs and concurrent private placement to Kingsoft Corp.)

-IBKR -6.6% (earnings)

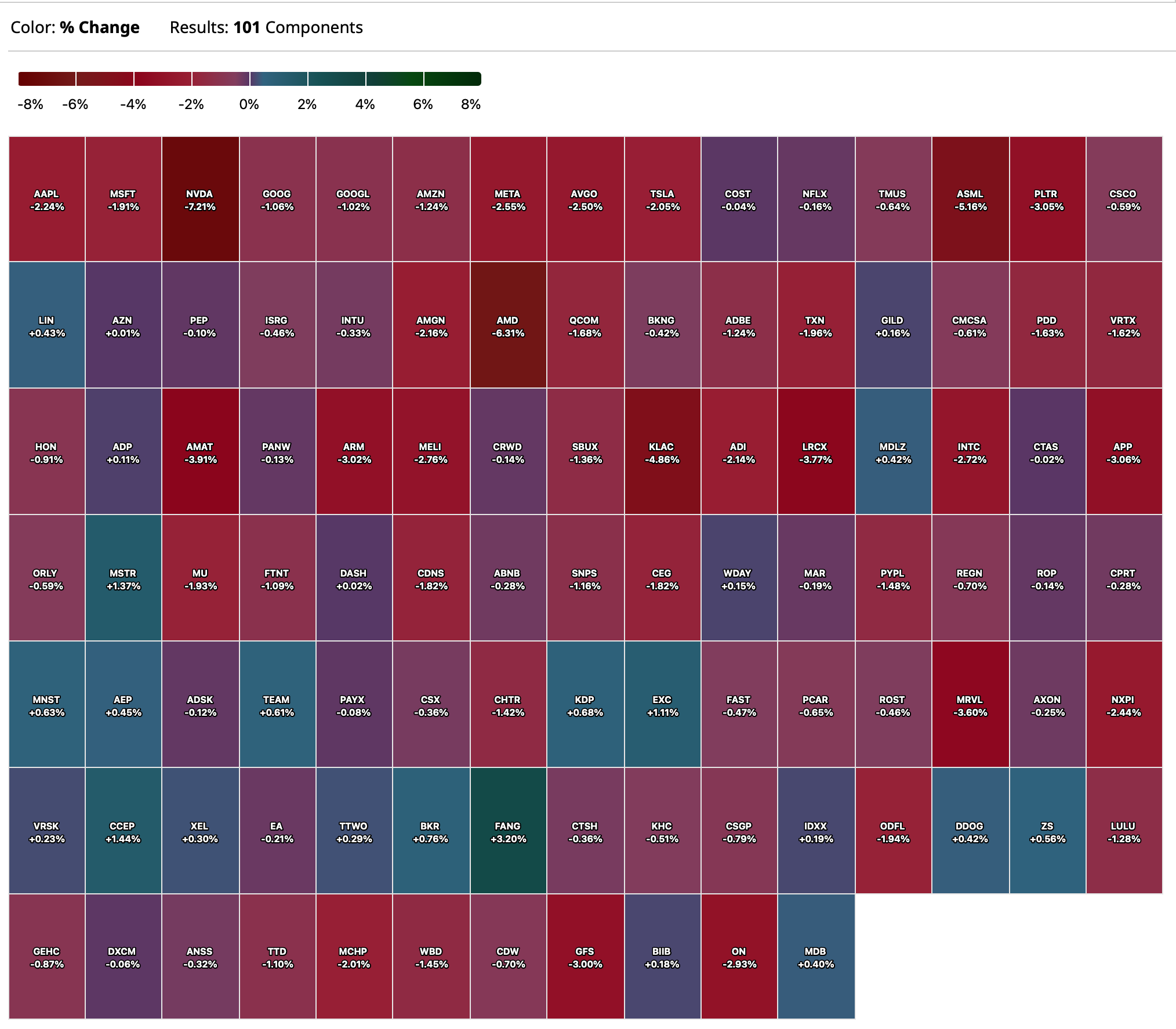

-NVDA -6.3% (US government informed Company it requires a license "for the indefinite future" for export to China for its H20 integrated circuits and any other circuits achieving the H20’s memory bandwidth, interconnect bandwidth, or combination thereof; Expects $5.5B charges in Q1:2026 associated with H20 products)

-JBHT -6.0% (earnings, guidance)

-WIT -5.3% (earnings, guidance)

-ASML -3.9% (earnings, guidance)

-TSM -3.2% (reportedly planning a 3% 4nm OEM quotation hike at its US plant as TSMC's current US factory has limited 4nm production capacity)

-OMC -2.4% (earnings)

-MRTN -2.1% (earnings)

-TSLA -2.0% (said to halt plans to ship Cybercab and semi parts from China; could disrupt Tesla's plan to start mass production of these models)

BY Doug Kass · Apr 16, 2025, 9:06 AM EDT

BY Doug Kass · Apr 16, 2025, 9:00 AM EDT

douglas cassel

40 minutes ago

I sold down a very large position in NVDA due in part to Doug K's campaign, but mainly due to it's poor price behavior. I am presently at a level Doug K would describe as tag ends. My question now is what do people feel the fair value is?Doug K's implication is that the AI revolution will fail, and NVDA impressive growth will stop. However, this is a minority view. Even many skeptics feel that AI spending will continue, if at a reduced level. What price would people get back in?

DK

Doug Kass

STAFF

Just Now

The nature of these cycles is that it ends with a dramatic diminution in profitability (orders, sales, cash flow, operating income) - by the time it is clear the stock will likely be down dramatically from the highs and from current levels.It is, to me, a no touch. And this in and of itself has material impact on the markets/averages. I have now written 84 columns on NVDA since the first half of the year. Mine remains a minority view.Until it becomes a majority view.

BY Doug Kass · Apr 16, 2025, 8:49 AM EDT

Noon: Fed Bank of Cleveland President Hammack (Non-Voter) speaks on "Fed 101" and participates in a moderated question-and-answer session before event, "Columbus Metropolitan Club Weekly Forum: Insights from Cleveland Fed President Beth Hammack," Columbus, OH (Audience Q&A expected. Livestream at https://www.youtube.com/channel/UCTagQr-YfniHI8C5nVH2d9w);

1:30 p,m.: Fed Chair Powell speaks about the economic outlook at the Economic Club of Chicago, Chicago, IL (Text available. Q&A from moderator. Webcast at https://www.youtube.com/@EconomicClubChicago);

7:00 p.m.: Fed Bank of Kansas City President Schmid (Voter) speaks on the economy and community banking in moderated conversation with Federal Reserve Bank of Dallas President Lorie Logan before a Global Perspectives event hosted by the Federal Reserve Bank of Dallas and the Dallas Citizens Council, Dallas, TX (Livestream available. Audience Q&A expected. No Logan/Schmid texts. No Logan/Schmid media Q&A) https://www.dallasfed.org/research/perspectives/2025/25schmid

BY Doug Kass · Apr 16, 2025, 8:38 AM EDT

From Peter Boockvar:

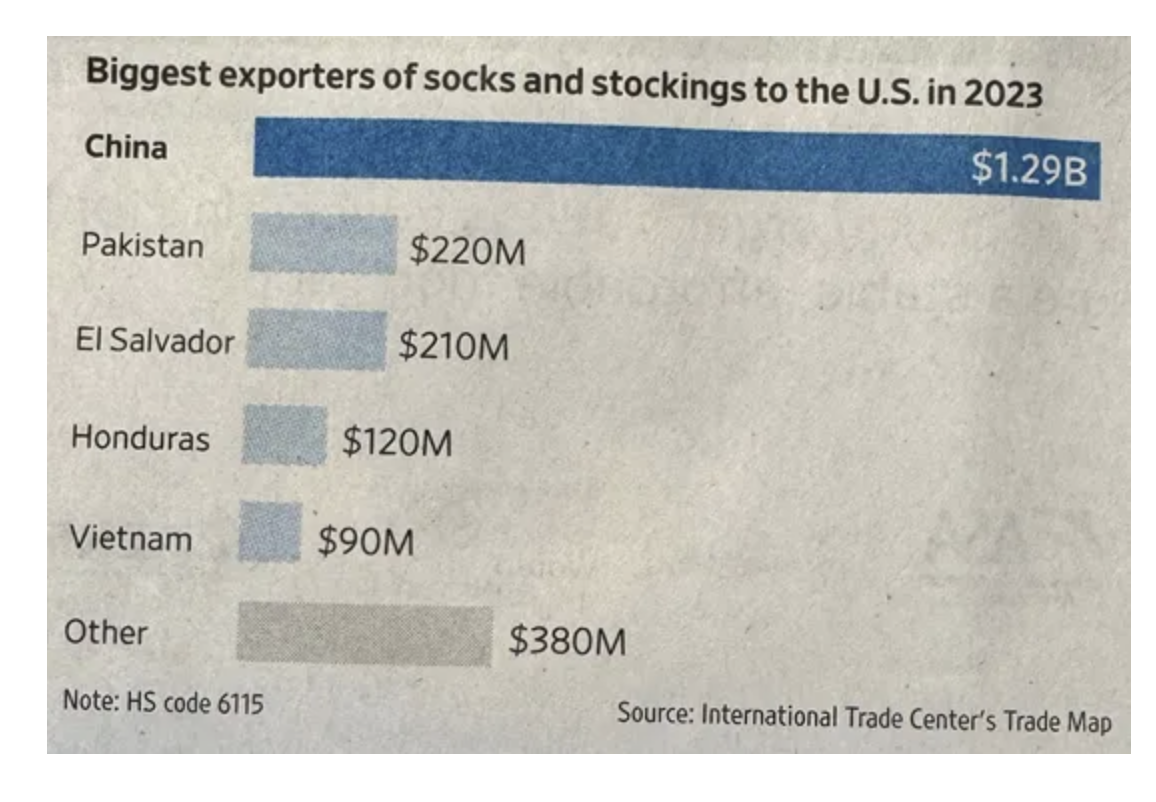

I wasn't being facetious last week when I talked about the possibility of shortages in coming months in the US of products we import from China, or used to import from China. I found this chart in yesterday's WSJ about our 'dependence' on China for socks. The article was titled, "At China's Wholesale Hub, US Orders Have Suddenly Halted. One Example: Socks."

Now I'm not that familiar with the supply chains of Pakistan, El Salvador and Honduras but I'm going to guess that it will take quite some time for them to ramp up enough manufacturing capabilities to fill the gap of China, because it is quite the gap. I'd thus expect some empty store shelves of socks coming our way. Get yours while you can. (From the Wall Street Journal:)

I saw another lawsuit filed on Monday against DJT and something we all have to watch out for because an adverse ruling for him would obviously have big implications for the markets and economy. The Liberty Justice Center issued a press release saying they have "filed a lawsuit challenging the Trump Administration's authority to unilaterally issue the 'Liberation Day' tariffs, which are devasting small businesses across the country. The lawsuit argues that the Administration has no authority to issue across-the-board worldwide tariffs without Congressional approval." They are representing 5 owner-operated businesses "who have been severely harmed by the tariffs and highlights the human and economic toll of unchecked executive power."

It mentioned the President's use of the International Emergency Economic Powers Act (IEEPA) to justify the use of tariffs. "But under that law, the President may invoke emergency economic powers only after declaring a national emergency in response to an 'unusual and extraordinary threat' to national security, foreign policy, or the US economy originating outside of the United States. The lawsuit argues that the Administration's justification - a trade deficit in goods - is neither an emergency nor an unusual or extraordinary threat. Trade deficits have existed for decades, and do not constitute a national emergency or threat to security. Moreover, the Administration's imposed tariffs even on countries with which the US do not have a trade deficit, further undermining the administration's justification."

Bottom line according to the Senior Counsel at the Liberty Justice Center, "No one person should have the power to impose taxes that have such vast global economic consequences. The Constitution gives the power to set tax rates - including tariffs - to Congress, not the President."

And I'm now seeing that California is filing its own suit today with a similar claim.

Here was the lay of the global land from Jane Fraser at Citi:

"In terms of the macro environment, I am not going to try to predict the unpredictable. While our corporate and consumer clients are resilient and in good financial health, the world is in a wait-and-see mode and is facing a more negative macro outlook than anyone had anticipated at the beginning of the year. And we know that prolonged uncertainty generally hurts confidence."

"The changes underway globally will go beyond trade and tariffs. In the US, for example, regulation and tax policy are all likely to look different in a year's time. And these changes will not only have economic impact, but geopolitical and cultural ones as well."

"We appreciate the administration taking a fresh look at regulations across all industries to unlock growth. We welcome the changes being discussed in our own industry to place more focus on material financial risks and to make it easier for banks to contribute to economic growth and to improve client service. When all is said and done and these longstanding trade imbalances and other structural shifts are behind us, the US will still be the world's leading economy and the dollar will remain the reserve currency."

From Bank of America:

"going more to what our customer data shows, it shows that the money moving across all our consumer spending methods, debit and credit cards, ACH, checks written, Zelle, etc... All that aggregate shows it grew at about a 4.4% pace in the first quarter of 2025 compared to the first quarter of 2024...you can note that consumer spending has been consistently growing y/o/y, but during last year, it actually slowed a bit, especially in the summer and picked back up in the fall. That resulted in the 4th quarter of '24 over the 4th quarter of '23 being about a 4% pace and that pace has continued."

And, "That pace has also continued through the first part of April. We note that some retailers may say that their sales are slower and others are picking up, and it really reflects the change in consumer spending behavior. But in the aggregate, the consumer keeps pushing money into the economy." I'll add, we'll of course see whether the consumer buying right now is being front loaded ahead of tariff induced price increases, particularly for socks.

"As we look at our business side and what our business clients are telling you, in the current setting, they remain profitable, liquid and have strong results. They all look ahead and worry about the same things that you hear reflected in your conversations with them also. So, we continue to watch for signs of the environment actually changing."

On the commercial loan side, they grew a solid 7% y/o/y, and ex CRE was 9%. They attribute some of this growth from just adding more loan officers and doing more international business. Also of note, "We noted a modest increase in revolver utilization during the quarter, as clients navigate the current environment." If the economy does roll over, expect many more companies to tap credit/revolver lines.

Their net charge off rate was flat with Q4. "Near term, we don't expect much change in net charge-offs, as you can see improvement in both early and late-stage delinquencies from the fourth quarter. That tells us that net charge-offs could even be a touch lower next quarter on the consumer side."

JB Hunt is looking down after earnings:

"As a general overview, our results for the quarter came in as expected and on the better side of the guidance range we had provided last quarter. That said, seasonally lower volume and rate pressure, coupled with inflationary cost headwinds, more than offset our cost control and productivity improvements and weighed on margins vs the prior year period."

With the 'inflationary cost headwinds', they particularly cite "noticeable increases in insurance premiums for the 3rd consecutive year."

They mentioned a "continuation of a tough operating environment across the industry."

They also said "the truckload market loosened as the quarter progressed. This suggests truckload capacity continues to exceed demand."

"Our customers continue to plan for multiple what if scenarios, but most of them are waiting for the dust to settle to determine how tariffs might influence and change their short and long-term business strategies. As part of this scenario planning process, some customers are considering ways to alter supply chain freight flows and/or their country of origin sourcing, but these changes will be part of a much longer decision process."

Finally, "Demand for big and bulky products remains muted with relatively weak demand for furniture, exercise equipment, and appliances. That said, demand in our fulfillment network was positive, driven by off-price retail trends."

From the United Airlines press release:

"In response to the current demand environment, United is removing 4 percentage points of scheduled domestic capacity starting in the third quarter of 2025. United is also continuing to make prudent adjustments to the utilization rate of its fleet, including ongoing reductions in off-peak flying on lower demand days. The airline expects to continue this approach into the 4th quarter of 2025."

In response to the 20 bps jump in the average 30 yr mortgage rate to 6.81%, purchase applications fell by 4.9% w/o/w after rising by 9.2% in the week before. Refi's popped by 35% last week and fell by 12.4% this week. The bottom line remains in the US housing market that it is somewhat frozen with the pace of existing home sales trending at 30 yr lows with affordability and supply being big problems. That said, supply has been building with new homes in certain overbuilt markets and prices are finally softening.

China's economy grew by 5.4% y/o/y in Q1, two tenths above the estimate with particular strength in retail sales and industrial production while housing remained weak. While their economy will certainly be hit by the 145% tariffs on about $440b of exports to US, their reliance on the US markets has been shrinking for years.

BY Doug Kass · Apr 16, 2025, 8:25 AM EDT

BY Doug Kass · Apr 16, 2025, 7:32 AM EDT

BY Doug Kass · Apr 16, 2025, 7:21 AM EDT

From Sanford Bernstein:

Last night NVIDIA disclosed that the US government will require a license for H20 shipments into China, Hong Kong, Macau, and other D:5 countries. The company is taking a $5.5B charge in FQ1 for inventory, purchase commitments, and reserves. They did not update guidance for the quarter (which ends on April 27).

The action came as a surprise especially given reports last week of an H20 reprieve following a Trump dinner Jensen supposedly attended, and recent news of substantial US AI investments by the company. Clearly the Trump rug remains in full effect...We believe the impact of a full H20 wipeout is probably ~30 cents or so at current levels (not enormous in the grand scheme of things), China accounted for ~$17B in revenue for the company in FY25, the largest ever on an absolute basis but only ~13% of revenue (the smallest % in over a decade) (Exhibit 1, Exhibit 2). This revenue also included gaming, networking, and auto; we believe the H20 portion was ~$12B or so, roughly ~30cents of EPS (Exhibit 3), not trivial but not enormous in the grand scheme of things. Banning the H20 makes little sense to us; could some licenses be granted? H20 performance is low, well below already-available Chinese alternatives (Exhibit 4); a ban essentially simply hands the Chinese AI market over to Huawei. We shall see if any licenses are granted (and to be fair the license requirement is supposed to address risks of H20s diverted to Chinese supercomputers so it is possible that some customers could get them after vetting), but the charge suggests NVIDIA is taking a conservative view.

The new license requirements seem to also apply to other products that have similar bandwidth characteristics. We do not know what this might imply for China AI products from competitors, but it seems a reasonable bet that similar licenses will be needed. But we also wonder if new products could be made that would not require licenses (i.e. H20 equivalents with lower memory/interconnect bandwidth capabilities) though we don’t know how suitable such a part might be.

What about the AI diffusion rules? Beyond the H20, The Biden Administration's AI diffusion rules are set to go into place on May 15. These rules would require NVIDIA’s non-US customers to obtain a license to purchase more than a small amount of AI parts (Exhibit 5). While we believe these rules are ultimately manageable, we do not know how long it will take to process and obtain appropriate licenses, and (if the rules are put into place) theregulations have the potential to impact FQ2 and 2H outlook as a result. We would have thought that the chance of actual implementation was small, but after imposing the H20 license requirement we are now no longer so sure.

So now what? We still believe that overall AI demand from more mainstream customers remains strong, and AI infrastructure in general seems to be more insulated from immediate tariff effects given Mexico USMCA compliance of much of the hardware as well as (presumably) the strategic nature of the industry with substantial US buildouts coming. But we admit the H20 announcement was disappointing especially given recent newsflow suggesting potential for a more positive resolution.

BY Doug Kass · Apr 16, 2025, 6:50 AM EDT

BY Doug Kass · Apr 16, 2025, 6:35 AM EDT

ASML Holding ASML with a miss on bookings — will put a pall over AI equities today.

BY Doug Kass · Apr 16, 2025, 6:25 AM EDT

The S&P Short Range Oscillator continues its steady to decline from a deeply oversold condition.

Now at -3.71% vs. -4.17%, it is down from double-digit oversold a week ago.

BY Doug Kass · Apr 16, 2025, 6:15 AM EDT

Wolf Street howls about Nvidia NVDA (I have been howling for almost ten months!)...

BY Doug Kass · Apr 16, 2025, 6:05 AM EDT

BY Doug Kass · Apr 16, 2025, 5:55 AM EDT