Boockvar's Succinct Summation of the Week’s Events

From Peter Boockvar:

Positives

1)A time out was called on slapping the uniquely defined, via internal math, reciprocal tariffs on the rest of the world.

2)March CPI fell one tenth headline vs the estimate of a gain of one tenth. The core rate was higher by .1%, also two tenths below expectations. The y/o/y gains slowed to 2.4% headline and 2.8% core vs 2.8% and 3.1% in February. Weighing on the headline was the 2.4% drop in energy prices in part due to the drop in gasoline and fuel oil prices. Energy prices are down 3.3% y/o/y. Food prices in contrast rose by .4% m/o/m and by 3% y/o/y. ‘Food at home’ in particular was higher by .5% m/o/m and 2.4% y/o/y. ‘Food away from home’ saw a price gain of .4% m/o/m and 3.8% y/o/y. Services ex energy prices were up just one tenth m/o/m and by 3.7% y/o/y, though still driving overall inflation. The goods side remains where the disinflation has taken place with core goods down by one tenth m/o/m after gains in the prior two months. They are unchanged y/o/y.

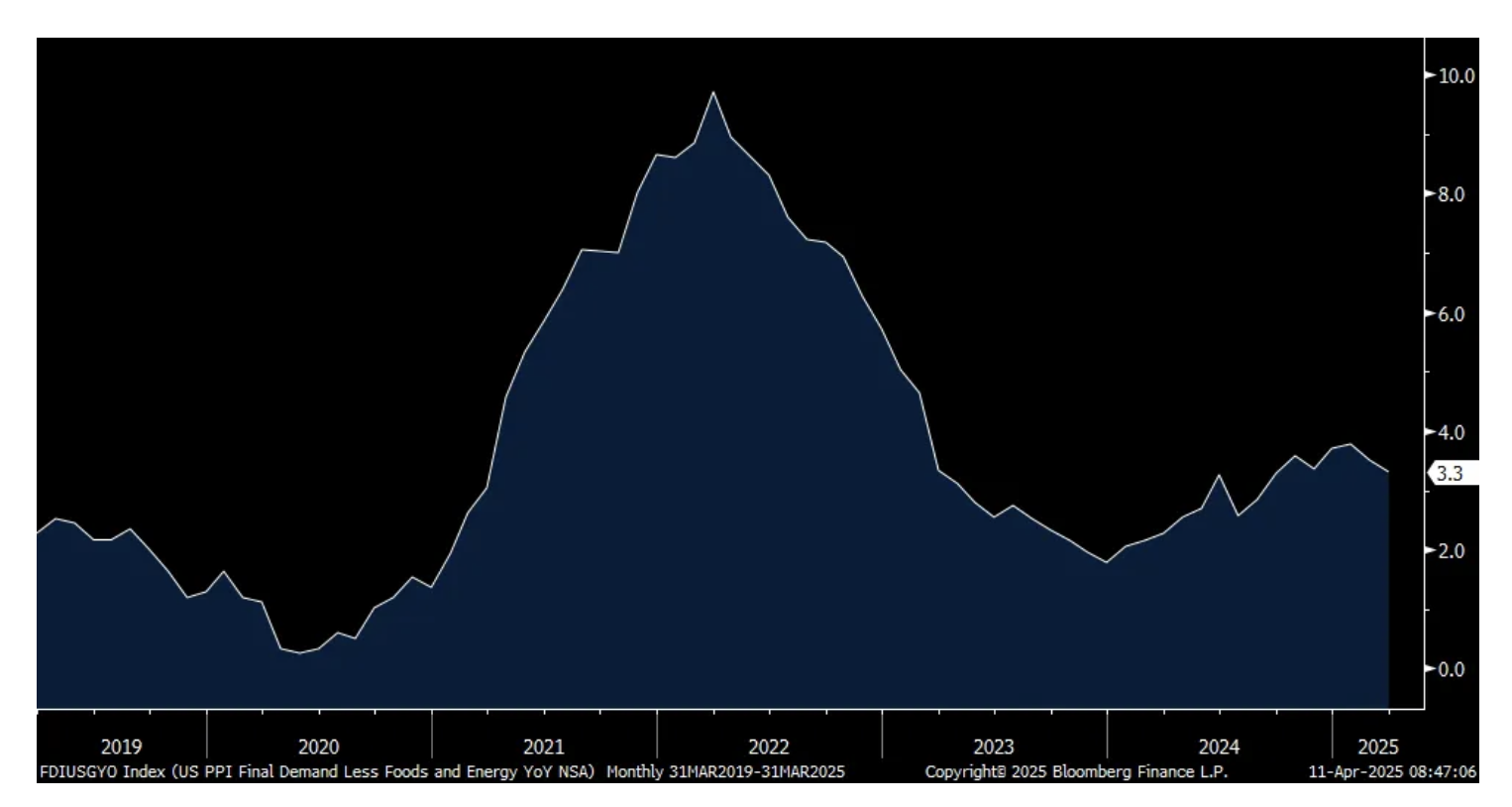

3)March PPI unexpectedly fell 4 tenths headline vs the estimate of a rise of 2 tenths after a one tenth gain in February which was revised up by one tenth. The core rate was lower by one tenth vs the forecast of up .3% but half of that was due to a higher revision by two tenths to February. If we take out trade too, the figure was actually as expected when including the upward revision to the month before. Versus last year, headline PPI was up 2.7%, the core rate by 3.3% and ex food, energy and trade by 3.5% vs 3.2%, 3.5% and 3.5% respectively in February.

4)Initial jobless claims rose to 223k from 219k, though as expected and still remaining low, especially in light of everything going on. Continuing claims, delayed by a week and pre ‘Liberation Day’, totaled 1.85mm, down from 1.893mm in the week before.

5)This will get completely reversed and then some this week with the jump in Treasury and mortgage rates but at least thru 4/4 purchase applications rose 9.2% w/o/w and refi’s were up by 35.3%.

6)From CarMax: In terms of their quarterly sales cadence, "December and January were very strong. February was a little softer, which we expected given that we had leap day last year. We also think February is slightly impacted by the delay of refunds. And what I mean there is, if you remember, probably halfway through February, refunds were off significantly y/o/y. Now, they caught up pretty much by the end of February, but I think it pushed a little bit into March, as well as we had some weather impacts. Then we get into March, and we saw a step up that was a little stronger than the fourth quarter comp, and it continued the whole month until the end of March where we saw some strength - some additional strength, which continued and then accelerated into the first few days of April, which obviously we're early into April right now. From a comp standpoint, first quarter to date, we're running high single digits." But the tariff pull forward will lead to a hangover thereafter.

7)The UK economy in February surprised to the upside with a .5% m/o/m growth rate, well better than the estimate of up .1%. Manufacturing production, services and construction all contributed to the growth. The manufacturing lift was likely pre-tariff planning.

8)Reflecting likely the pull forward of ordering ahead of tariffs, Taiwan's trade data came in about twice expectations. Exports in March jumped 29%, well above the estimate of 14%. Imports were higher by 18.5% and vs the estimate of 8.1% growth.

9)China's March CPI was flattish, falling by .1% y/o/y and all led by lower food prices which dropped by 1.4% y/o/y. Prices ex food and energy were up by .5% y/o/y.

10)The Reserve Bank of New Zealand cut its official cash rate by 25 bps as expected to 3.50% and the Reserve Bank of India did too by 25 bps to 6%.

Negatives

1)Ratcheting up the tariff battle with China better be resolved quickly as many will suffer on both sides if it does not.

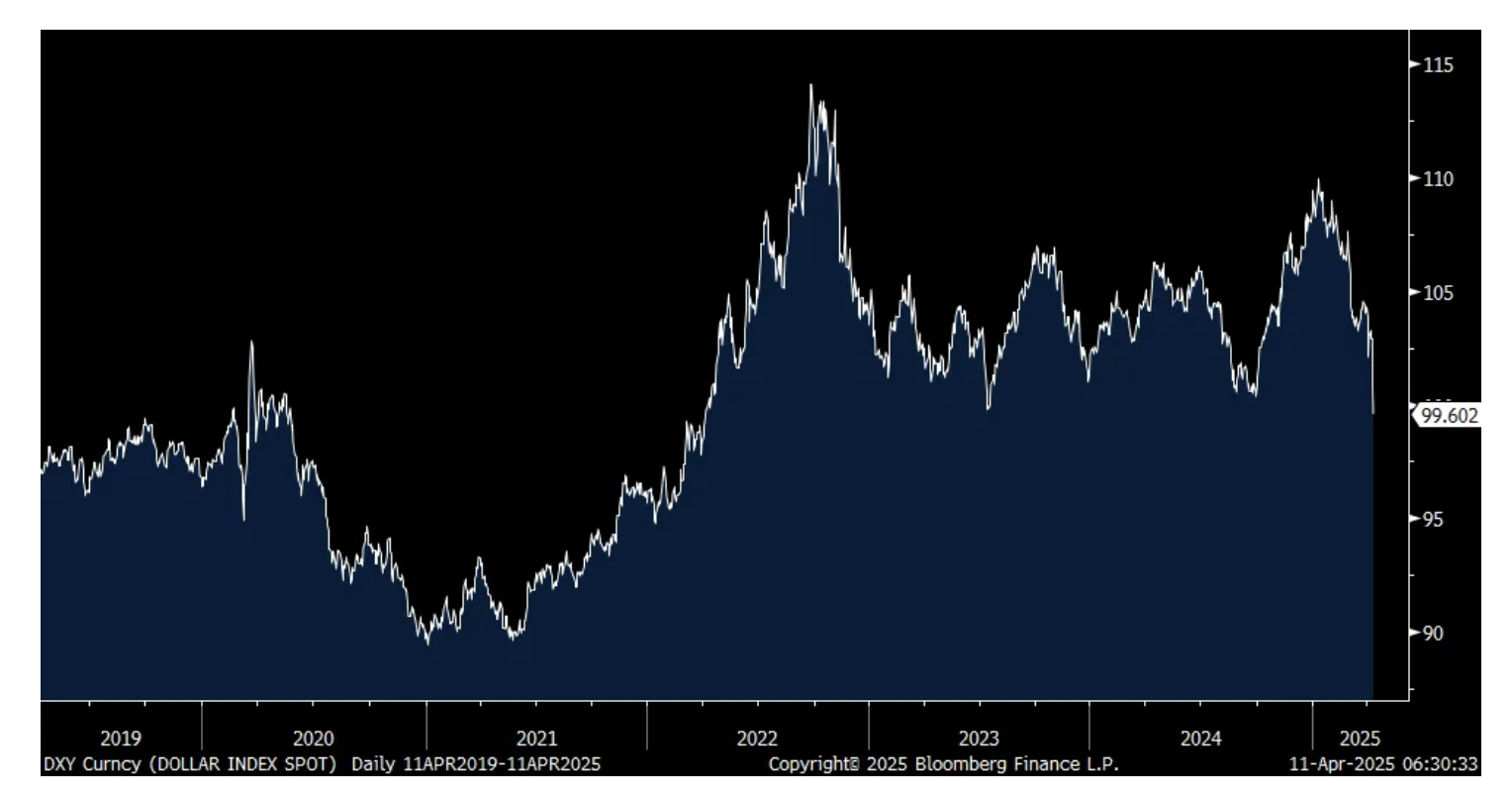

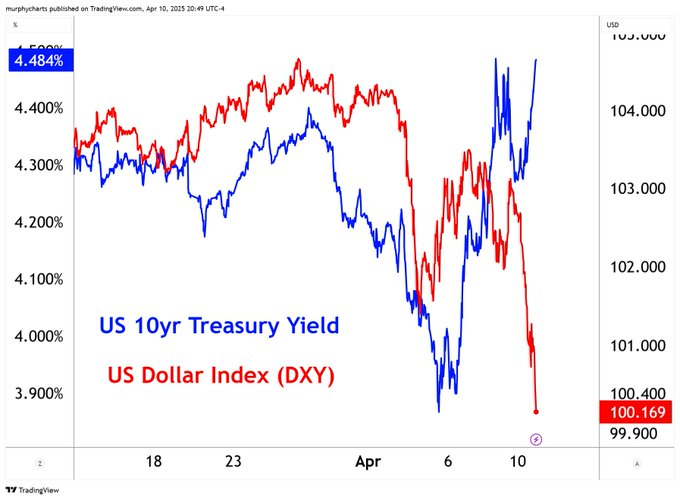

2)The US dollar tanks to almost a 2 yr low and Treasury yields spike with the 10 yr yield up 54 bps on the week as of this writing.

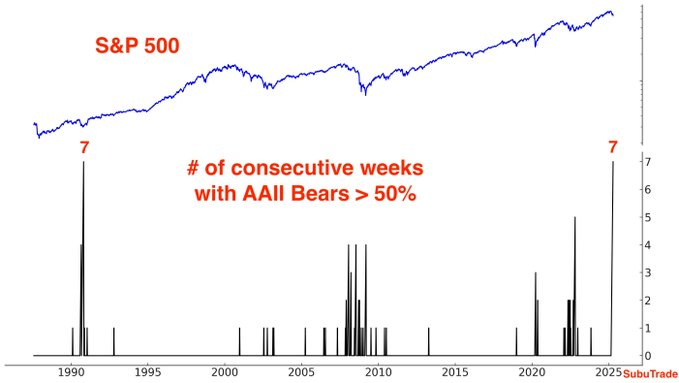

3)The preliminary April UoM consumer confidence index fell to 50.8 from 57 and 3 pts below expectations. The Expectations component fell to the lowest level since 1980 at 47.2. One yr inflation expectations jumped to 6.7% from 5% in March, 4.3% in February, 3.3% in January and vs 2.8% in December. The 5-10 yr view rose 3 tenths m/o/m to 4.4%. After plunging by 23 pts in March, employment expectations were unchanged m/o/m. The income component fell again to -4 from -2. Spending intentions fell across the board. Yes, the confidence of Democrats fell sharply again to 34.1 vs 91.4 in October but confidence for Independents keep falling too as well as for Republicans which dropped to 81.9 from 87.4, though still well above the pre-election level of 53.6. UoM said with regards to the overall figure, “This decline was, like the last month’s, pervasive and unanimous across age, income, education, geographic region, and political affiliation. Sentiment has now lost more than 30% since December 2024 amid growing worries about trade war developments that have oscillated over the course of the year. Consumers report multiple warning signs that raise the risks of recession: expectations for business conditions, personal finances, incomes, inflation, and labor markets all continued to deteriorate this month.” In maybe a good stock market contrarian indicator, 41% of people polled think stocks will be up in the coming 12 months, the lowest since March 2009, the market bottom then.

4)The NFIB small business optimism index for March fell to 97.4 from 100.7 and lower for a 3rd month. The bottom line from the NFIB and Bill Dunkelberg, "The implementation of new policy priorities has heightened the level of uncertainty among small business owners over the past few months. Small business owners have scaled back expectations on sales growth as they better understand how these rearrangements might impact them." Also of note, "The percent of small business owners reporting labor quality as the single most important problem for their business was unchanged from February at 19%, remaining the top issue, with taxes one point behind."

5)From CarMax: "I think over time, what could happen is that the used car prices will also go up. Now, the question is, how much will they go up, over what period of time? I think the other thing to think about on the tariffs that impacts our business, as well as anybody that sells used cars is just the parts piece. When it comes to reconditioning, the parts will be going up, and it just makes our work that much more important on the efficiencies that we're going after on cost of goods sold to offset those increases."

6)From Delta: "February and March reflected a much more challenging macro environment than anyone initially planned for. Coming into 2025, we are positioned for another year of strong growth. However, given broad economic uncertainty around global trade, growth has largely stalled. The impact has been most pronounced in domestic, and specifically in the main cabin, with softness in both consumer and corporate travel. While not immune in this environment, we do continue to see greater resilience in international and our diversified revenue streams, including premium and loyalty, reflecting underlying strength of our core consumer…Consumers remain cautious and corporate travel trends are choppy, with overall corporate volumes currently expected to be flattish over last year, similar to what we saw in March. Main cabin demand softness in both domestic and international is persisting, particularly in off-peak times...Internationally, approximately 80% of revenues are US point of origin, with bookings remaining strong for the peak summer period…In Canada, we have seen a significant drop off in bookings. In Mexico, it's kind of a mixed bag...And I think we will be looking at Canada and Mexico as places that we probably want to reduce our capacity levels as we move forward."

7)Japan said its PPI for March rose .4% m/o/m, double the estimate and February was revised up by 2 tenths. Versus last year, wholesale prices are up 4.2%.

8)China PPI was down by 2.5% y/o/y vs the estimate of -2.3% in March as they remain challenged by the global manufacturing downturn and price competition.

PPI news, watching core goods prices as reflection of tariffs

March PPI unexpectedly fell 4 tenths headline vs the estimate of a rise of 2 tenths after a one tenth gain in February which was revised up by one tenth. The core rate was lower by one tenth vs the forecast of up .3% but half of that was due to a higher revision by two tenths to February. If we take out trade too, the figure was actually as expected when including the upward revision to the month before.

Versus last year, headline PPI was up 2.7%, the core rate by 3.3% and ex food, energy and trade by 3.5% vs 3.2%, 3.5% and 3.5% respectively in February.

A 4% drop in energy prices weighed on the headline and is down 6.7% y/o/y. Food prices fell too, by 2.1% m/o/m helped by a 21% drop in eggs prices after the spikes seen in the two prior months. Food prices are still up 3.7% y/o/y.

Core goods prices, which in light of tariffs is now the key figure to watch, rose .3% m/o/m for a 2nd month and by 2.4% y/o/y.

Services prices, outside of food and energy, were the main reason for the PPI declines. Prices for transportation and warehousing services fell .6% was the main factor here as taking this out saw final demand for services prices rose .1%.

I do think there were some signs of pre tariff activity that showed up in terms of shipments. ‘Truck transportation of freight’ prices jumped .7% m/o/m and now up 3.6% y/o/y. ‘Air transportation of freight’ prices rose .5%. I did hear the story of Apple flying Iphones out of China to avoid tariffs but haven’t been able to confirm that. The prices of ‘rail transportation of freight, mail’ were unchanged from February but up 3.1% y/o/y.

Bottom line, we’ll take the inflation relief but who knows what the tariffs will look like in coming months and I’ll say again that the core goods figure within this data will be most important to watch as to what price is being absorbed at the producer level. Core goods prices within CPI will then tell us to what extent they are getting passed through to us.

Treasury yields are pretty much exactly where they were at 8:29am est as we all know today’s data is somewhat old news. The US dollar index is off its lows of 99 but still below 100.

The Art of War responds again to The Art of the Deal/DXY breaks below 100

The Art of War continues to stand up to The Art of the Deal and the battle between the two makes us all worse off. Elsewhere, the dollar continues to tank. With today's retaliation, and expressed as the last, China said "Given that American goods are no longer marketable in China under the current tariff rates, if the US further raises tariffs on Chinese exports, China will disregard such measures." The Commerce Ministry also said "It's become a joke" referencing the situation. As we import about $450b worth of goods from China, including Iphones as we know, that we can't easily replace and quickly, this has become a ridiculous situation.

If this fight with China doesn't end soon, Polymarket should start adding a prediction of an over/under on how many months before US shelves start emptying out. Because of all these risks, I think a deal happens soon and even Trump yesterday said he was hopeful.

Why isn't anything said about the trade surplus in US services of about $300b? Are we ripping everyone off? No, but we are now pissing them off. From a Bloomberg News article yesterday, "The number of Canadian resident return trips by automobile from the US plunged 31.9% in March from a year ago, Statistics Canada said Thursday. That's the third straight monthly decline and followed a 23% drop a month earlier."

Also, "The number of Canadian-resident return trips by air from the US also fell, decreasing 13.5% in March from the same month a year ago. On the other hand, return trips by Canadians from foreign countries other than the US rose 9.1%."

And, "Canadians make up the biggest group of tourists in the US. Last year, Canadian visitors generated $20.5 billion in spending in the US, according to the US Travel Association." Well, the US is about to start shrinking its trade surplus in services. https://www.bloomberg.com/news/articles/2025-04-10/canadian-car-trips-to-us-plunge-32-as-trump-threats-strain-ties

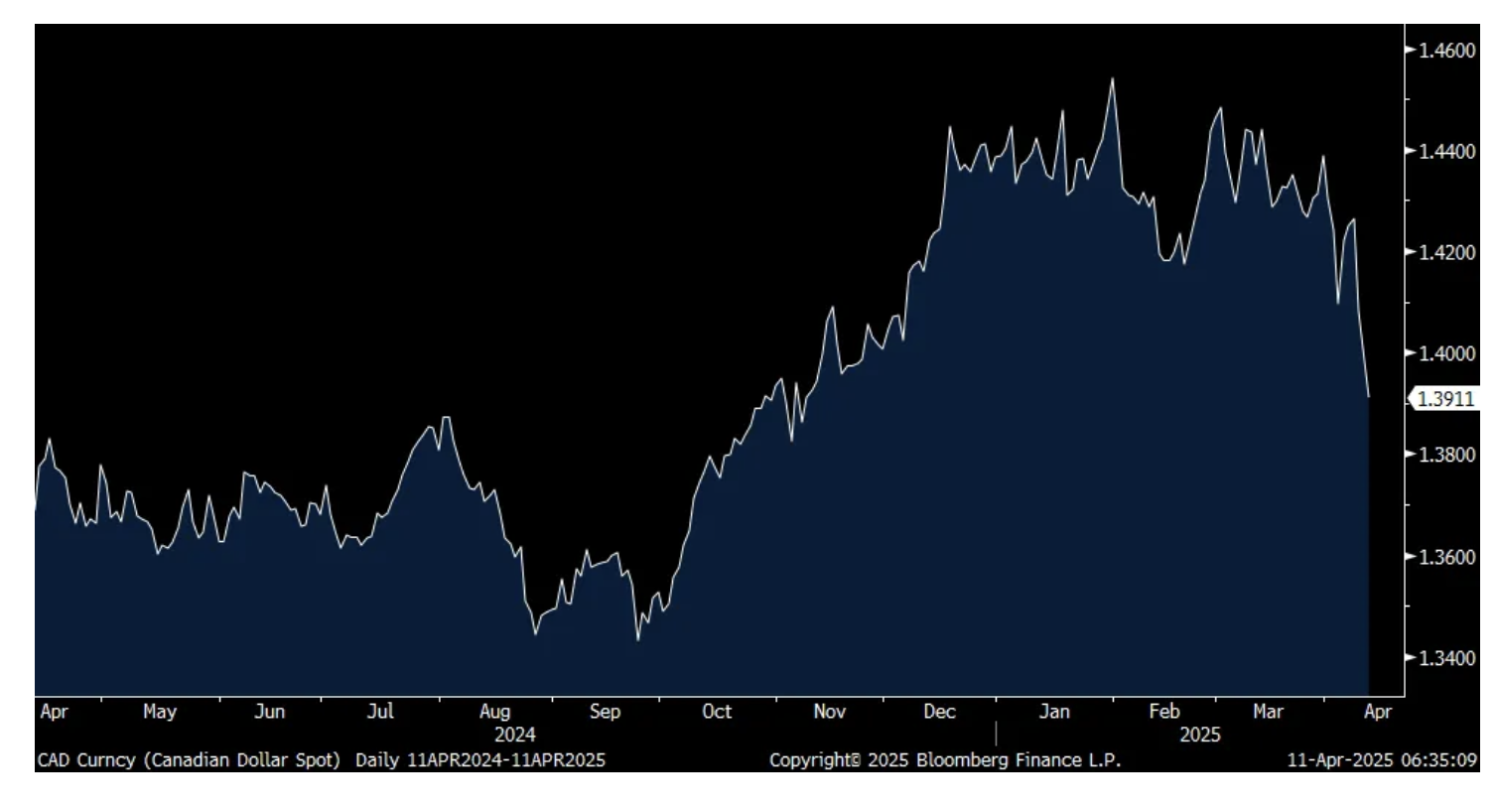

Back to the US dollar, I mentioned in the 30 yr auction note yesterday that it was on track for its worst percentage day decline since November 2022, falling by 2% in the DXY and is down another 1.2% today. Now below 100, it stands at its weakest level in three years. Specifically against the Canadian$, the US dollar has now lost all of its post election gains. What this means, other than being likely inflationary, is that US importers/consumers will continue to eat more of the tax impact of tariffs. I'm glad I locked in on Monday, before the US dollar selloff this week, the purchase of Toronto Blue Jay tickets from Ticketmaster Canada for a game in Toronto next month I'm going to with my buddy David Rosenberg.

It's hard not to think that with the trio of selling in long end Treasuries, stocks and the US dollar that foreign capital flight is happening. As I stated in February, I think this started with the foreign selling of the Mag 7 stocks, as DeepSeek killed that trade in terms of its outperformance and accelerated when the tariff war started. And with US Treasuries, if the US economy further slows and enters a recession, our budget deficit relative to GDP will go north of 10% and you'll see a real flood of supply just as others turn their back.

With regards to what China might be doing specifically with US Treasuries, we'll only see in hindsight but I wouldn't be surprised if they were selling any long paper duration they own and shifting to the short end of the yield curve to some degree.

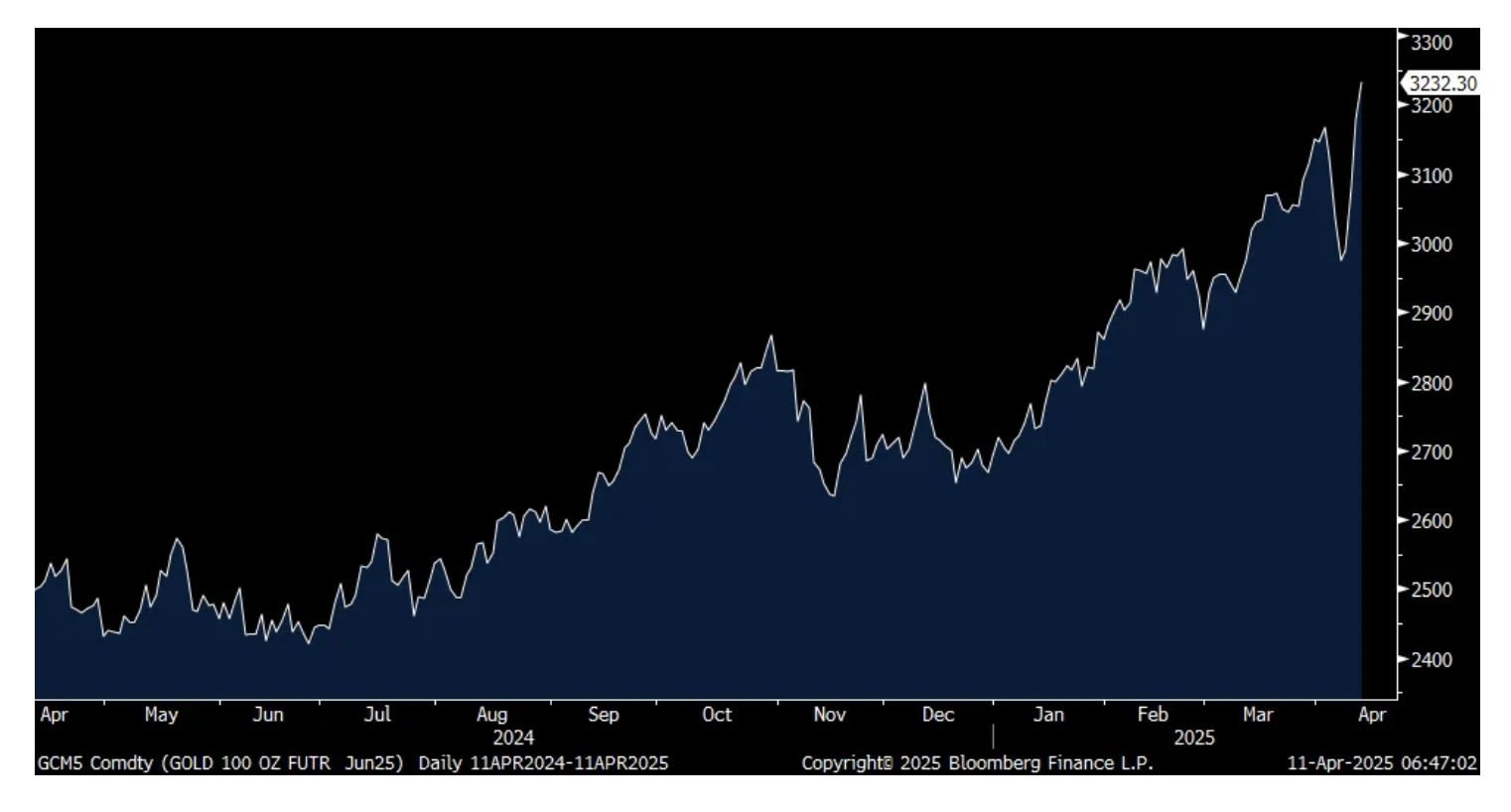

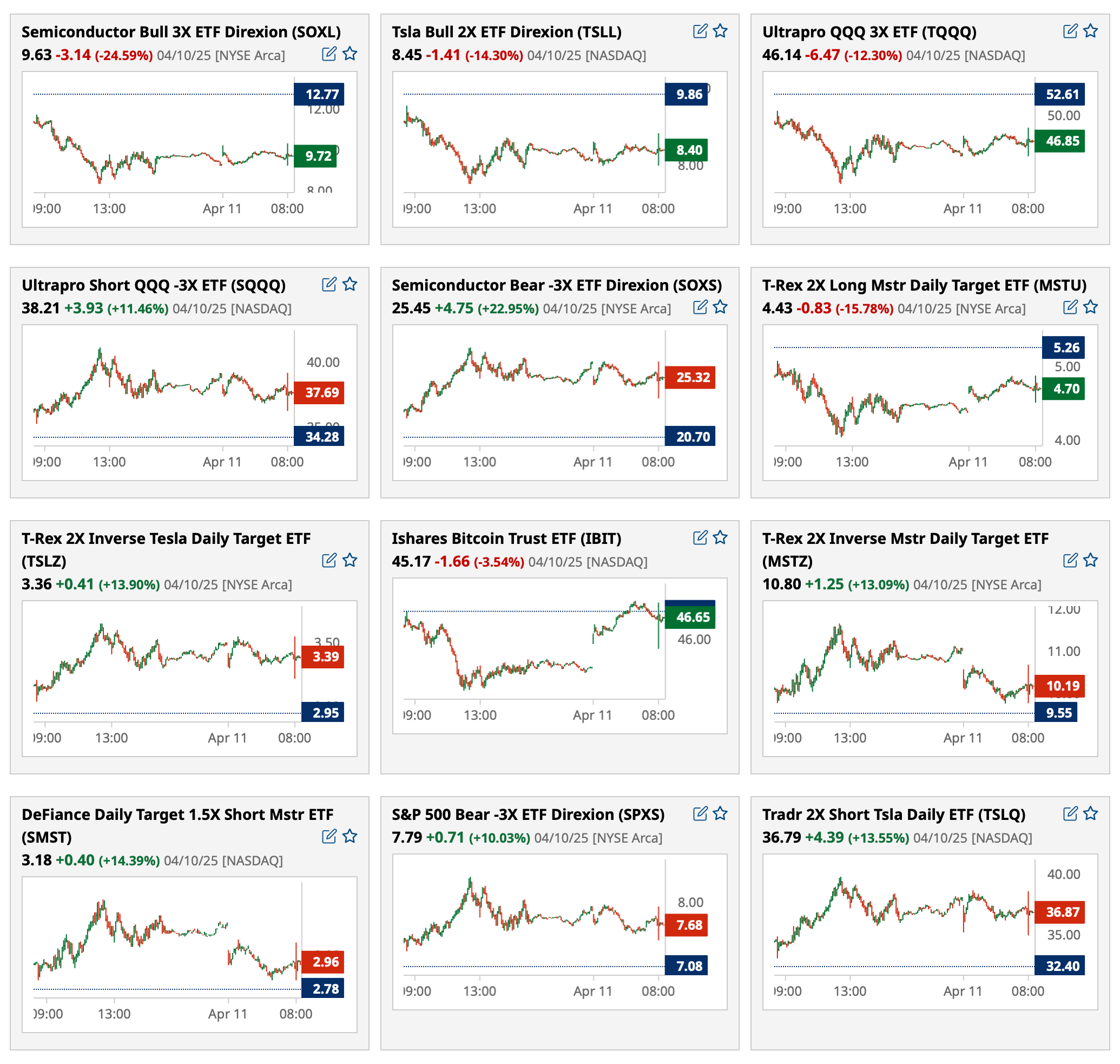

Gold is certainly the main beneficiary with it hitting another record high today. We remain long and positive and on silver and platinum too.

DXY

CAD

Gold

From CarMax whose stock fell 17% yesterday after its earnings report where comp growth of 5.1% missed the estimate of 6.8%:

They blame the comp miss on "having one less selling day, inclement weather, and a delayed start to this year's tax season." Last year was a Leap yr.

"Average selling price was flat y/o/y."

Their CarMax Auto Finance business saw a sequential improvement in its provision for loan losses which "reflects an additional quarter with a more normalized provision, along with the continuation of previous credit tightening."

In terms of their quarterly sales cadence, "December and January were very strong. February was a little softer, which we expected given that we had leap day last year. We also think February is slightly impacted by the delay of refunds. And what I mean there is, if you remember, probably halfway through February, refunds were off significantly y/o/y. Now, they caught up pretty much by the end of February, but I think it pushed a little bit into March, as well as we had some weather impacts. Then we get into March, and we saw a step up that was a little stronger than the fourth quarter comp, and it continued the whole month until the end of March where we saw some strength - some additional strength, which continued and then accelerated into the first few days of April, which obviously we're early into April right now. From a comp standpoint, first quarter to date, we're running high single digits."

I'll add, we of course have to wonder how much of the recent pick up in sales is pre tariff buying as if the supply of new cars will slip, used car buying will pick up. To this, in response to a question on the impact of tariffs, "I think certainly as new car prices go up, that'll put a bigger spread between late model used and new cars. Obviously, just the speculation of the tariffs and now the tariffs actually being out there, it's driven demand. I mean, you're seeing it in the franchise dealers. We're seeing it just based off of the step up that I just spoke to. I think it will push some folks into looking at used cars, late model used cars, which is interesting because that's what we're seeing a lot of interest in right now."

And, "I think over time, what could happen is that the used car prices will also go up. Now, the question is, how much will they go up, over what period of time? I think the other thing to think about on the tariffs that impacts our business, as well as anybody that sells used cars is just the parts piece. When it comes to reconditioning, the parts will be going up, and it just makes our work that much more important on the efficiencies that we're going after on cost of goods sold to offset those increases."

From Jamie Dimon:

"The economy is facing considerable turbulence (including geopolitics), with the potential positives of tax reform and deregulation and the potential negatives of tariffs and 'trade wars,' ongoing sticky inflation, high fiscal deficits and still rather high asset prices and volatility. As always, we hope for the best but prepare the Firm for a wide range of scenarios."

From Charlie Scharf at Wells Fargo:

"We support the administration's willingness to look at barriers to fair trade for the United States, though there are certainly risks associated with such significant actions. Timely resolution which benefits the US would be good for businesses, consumers, and the markets. We expect continued volatility and uncertainty and are prepared for a slower economic environment in 2025, but the actual outcome will be dependent on the results and timing of the policy changes."

What I'm curious with both banks and the ones we'll hear from next week, is to what extent are businesses tapping credit lines for 'just in case' scenarios?

From the Fastenal press release, a major distributor of stuff sold to the manufacturing and industrial end markets:

"results reflected contribution from improved customer contract signings over the past 12 months, which was partially offset by sluggish underlying business activity." They did see strength "with warehousing and storage, and data center customers, which was partially offset by declining sales with resellers."

The UK economy in February surprised to the upside with a .5% m/o/m growth rate, well better than the estimate of up .1%. Manufacturing production, services and construction all contributed to the growth. The manufacturing lift was likely pre-tariff planning.

Here's a funny childhood story that I produce annually to take us all into this weekend's Palm Sunday and next weekend's Easter holiday:

I'm reminded at this time every year (by my famous artist sister Debbie) of a true story that occurred in the late 1950s when I was about 10 years old.

When I was in fourth grade at my Long Island, N.Y., elementary school, the students were notified of a "special assembly" to be held that afternoon.

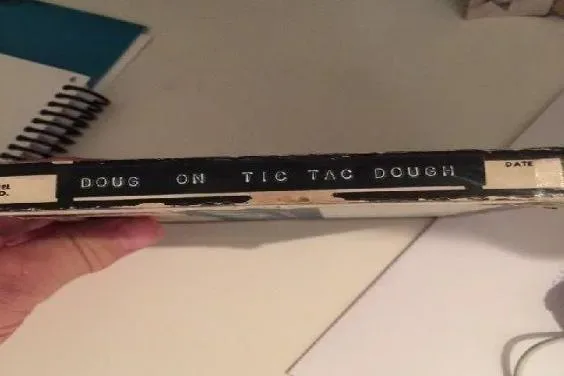

When we all arrived in the auditorium, there was a woman on the stage in a chair who explained that she was an NBC representative for a TV quiz show called Tic-Tac-Dough, which aired at that time in New York on Channel 4.

She went on to explain that Tic-Tac-Dough, the predecessor show to Hollywood Squares (which used the same concept), was looking for two students to represent Long Island on the show during Christmas vacation week. (Adults participated on the show the rest of the year.)

She began to ask the students questions, but I was shy and never raised my hand. But in response to a question, my buddy Jo Anne Zerillo raised her hand and said she didn't know the answer but "The Professor" (my nickname then!) might. She pointed at me.

I answered the question and then another, and was notified that I had been selected along with my friend and classmate Carrie Spivak to represent our area on Tic-Tac-Dough.

Jack Barry, a fellow Long Islander and a Wharton graduate (as I would later be), was the host and (along with Dan Enright) the show's producer.

If you remember Jack Barry, it's probably because his production company was responsible for the scandal-ridden game show Twenty One. It turns out that Charles Van Doren and champion Herb Stempel were provided with answers to Twenty One's questions in advance after principal advertiser Geritol complained that the unrigged production was dull and boring.

Barry's production company later created other game shows like Dough Re Mi, Winky Dink and You (reputedly the world's first-ever interactive TV program), the fabulously successful Concentration and the long-running Joker's Wild.

I went on Tic-Tac-Dough several weeks later and won my first six games, breaking a record for the show.

But in the seventh game, I selected the box "Holidays" and was asked by Jack Barry to name the Sunday before the Easter holiday. He went on to say that the holiday was the name of a tree.

The music played in the background and after waiting about 10 or 15 seconds, Mr. Barry asked if I knew the answer.

I thought long and hard, but had no idea of the answer. So I figured I should take a shot and guess the answer, as I already knew the holiday had the name of a tree in it.

Under pressure from Mr. Barry, I said: "Dogwood Sunday."

As the words came out of my mouth, I could hear my mother and Grandma Koufax (who were in the audience) gasp. My mom, clear as day, said, "Oh, no!" (I can still hear her words as if it were yesterday.)

I instantly knew it was the wrong answer and said — I swear I did! — "No, Mr. Barry. It's Redwood Sunday!"

Jack Barry, was in front of a pyramid of empty Crest toothpaste boxes that were stacked up in preparation for a commercial later on in the show. (The "Look Ma, No Cavities!" commercial was initially aired on Tic-Tac-Dough.)

Barry then said, "Doug, I am sorry. That is the wrong answer. The correct answer is Palm Sunday. Haven't you ever heard of Palm Sunday, the Sunday before Easter?"

I immediately said — remember, this was live television — "No, Mr. Barry. I never heard of Palm Sunday. I am Jewish."

Barry, who was also Jewish, fell over laughing right into the boxes of Crest toothpaste, which all fell down into a mess.

I hope you enjoyed the story about Dogwood — er, I mean, Redwood — Sunday.

I will never forget the experience, and I have the tape of the week's appearances to prove it. (My office has been listening to them all day).

In this holiday spirit, I want to be the first to wish a Happy Dogwood Sunday, Holy Week and Happy Easter to my family, all of my friends, subscribers, contributors, editors, and the entire TheStreet Pro management team!

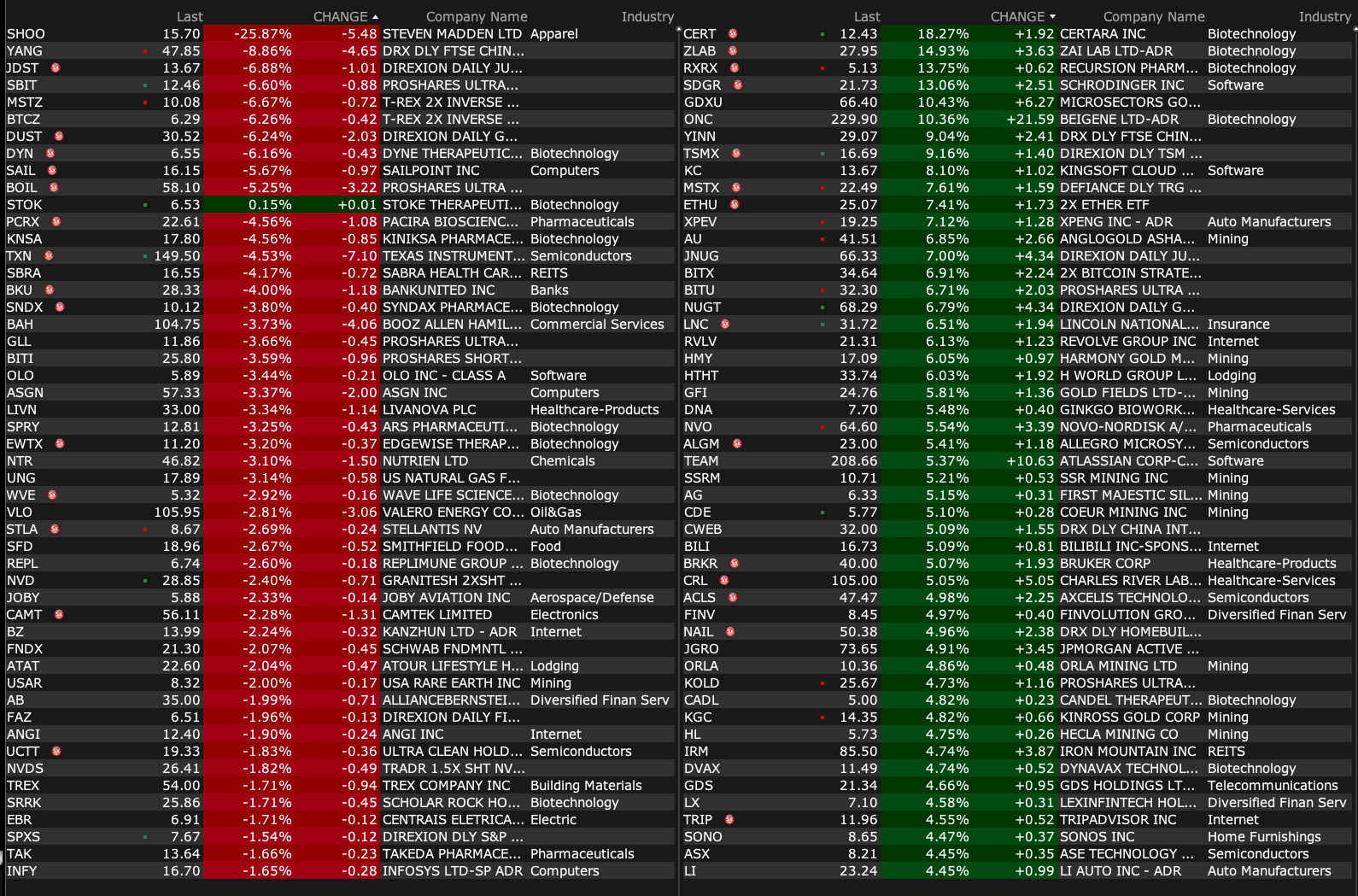

-SLP +20% (US FDA plans to phase out animal testing requirement for monoclonal antibodies and other drugs, in favor of AI-based computational models of toxicity and cell lines and organoid toxicity testing in a laboratory setting)

-CERT +18% (US FDA plans to phase out animal testing requirement for monoclonal antibodies and other drugs, in favor of AI-based computational models of toxicity and cell lines and organoid toxicity testing in a laboratory setting)

-IPA +15% (highlights alignment of proprietary AI-driven platform LENSai with FDA's shift to non-animal testing methods)

-RXRX +14% (US FDA plans to phase out animal testing requirement for monoclonal antibodies and other drugs, in favor of AI-based computational models of toxicity and cell lines and organoid toxicity testing in a laboratory setting)

-VERO +8.4% (files to sell $1.5M registered direct offering of common stock price at the market under NASDAQ rules at $4.06/shr)

-VERV +7.3% (receives FDA Fast Track designation for VERVE-102 for hyperlipidemia and high lifetime cardiovascular risk)

-ARGX +4.8% (US FDA approves VYVGART Hytrulo Prefilled Syringe for Self-Injection in Generalized Myasthenia Gravis and Chronic Inflammatory Demyelinating Polyneuropathy)

-FSM +4.3% (announces sale of Yaramoko Mine, Burkina Faso for $130M aggregate in cash)

-NEM +3.6% (UBS Raised NEM to Buy from Neutral, price target: $60 from $50)

-HII +3.0% (Goldman Sachs Raised HII to Buy from Sell, price target: $234)

-LHX +2.6% (Goldman Sachs Raised LHX to Buy from Sell, price target: $263)

-AXP +2.2% (Tier1 firm Raised AXP to Buy from Neutral, price target: $274 from $325)

-BLK +1.8% (earnings)

Downside:

-TXN -4.7% (China Semiconductor Industry Association (CSIA) reportedly says some chipmakers are exempt from retaliatory US tariffs based on location of fabrication)

8:00 a.m. ET: Fed Bank of Minneapolis President Kashkari (Non-Voter) on CNBC Squawk Box;

9:00 a.m.: Fed Bank of Boston President Collins (Voter) is interviewed on "Yahoo! Finance."

10:00 a.m.: Fed Bank of St. Louis President Musalem (Voter) speaks on the U.S. economy and monetary policy and participates in moderated conversation before the Arkansas State Bank Department's 29th Annual Day with the Commissioner, Hot Springs, AR (In person and virtual access option. Text anticipated. No media availability);

11:00 a.m.: Fed Bank of New York President Williams (Voter) speaks on the economic outlook and monetary policy before the Puerto Rico Chamber of Commerce (Text and moderated Q&A expected. Venue TBA)NONE