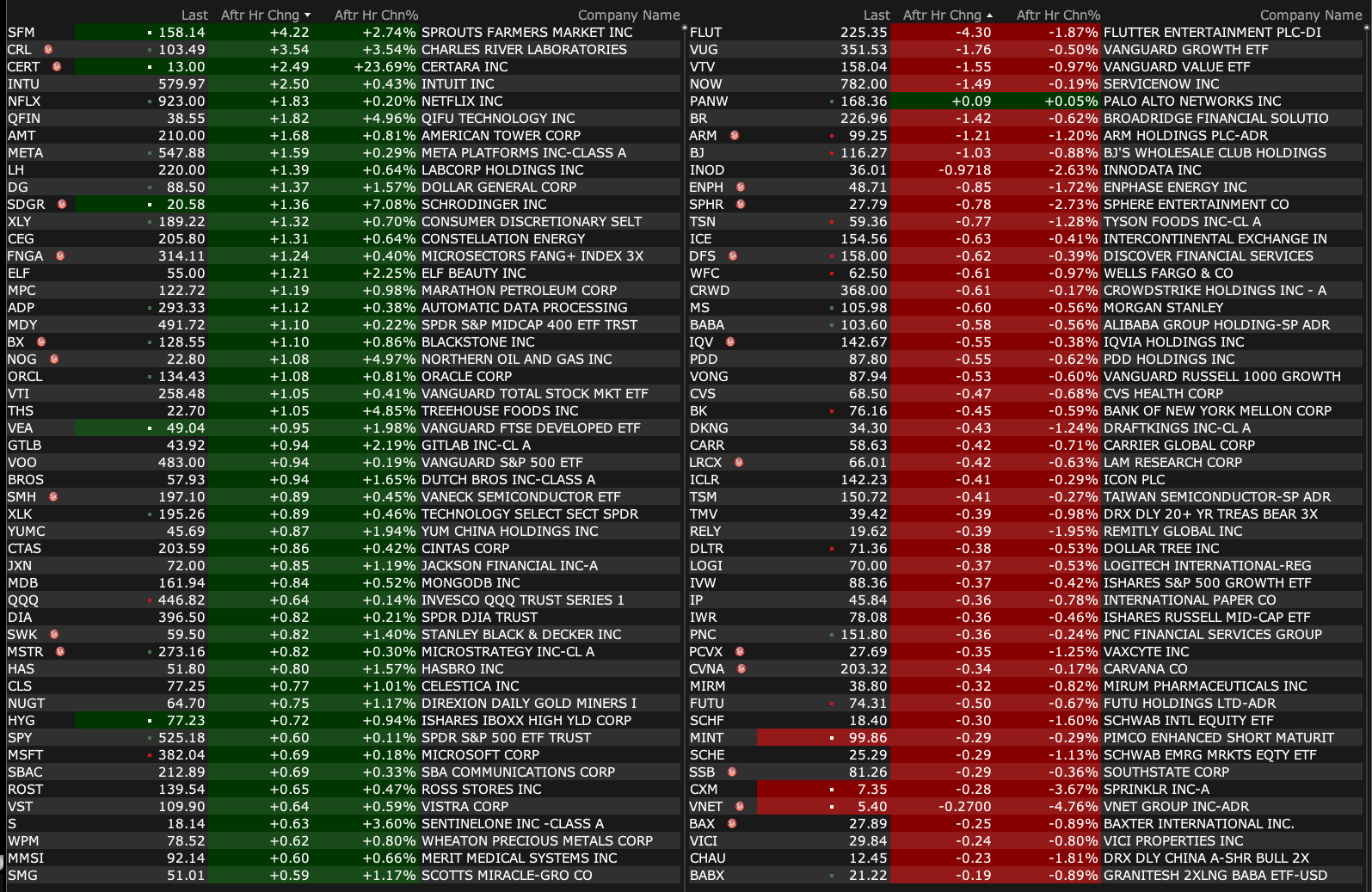

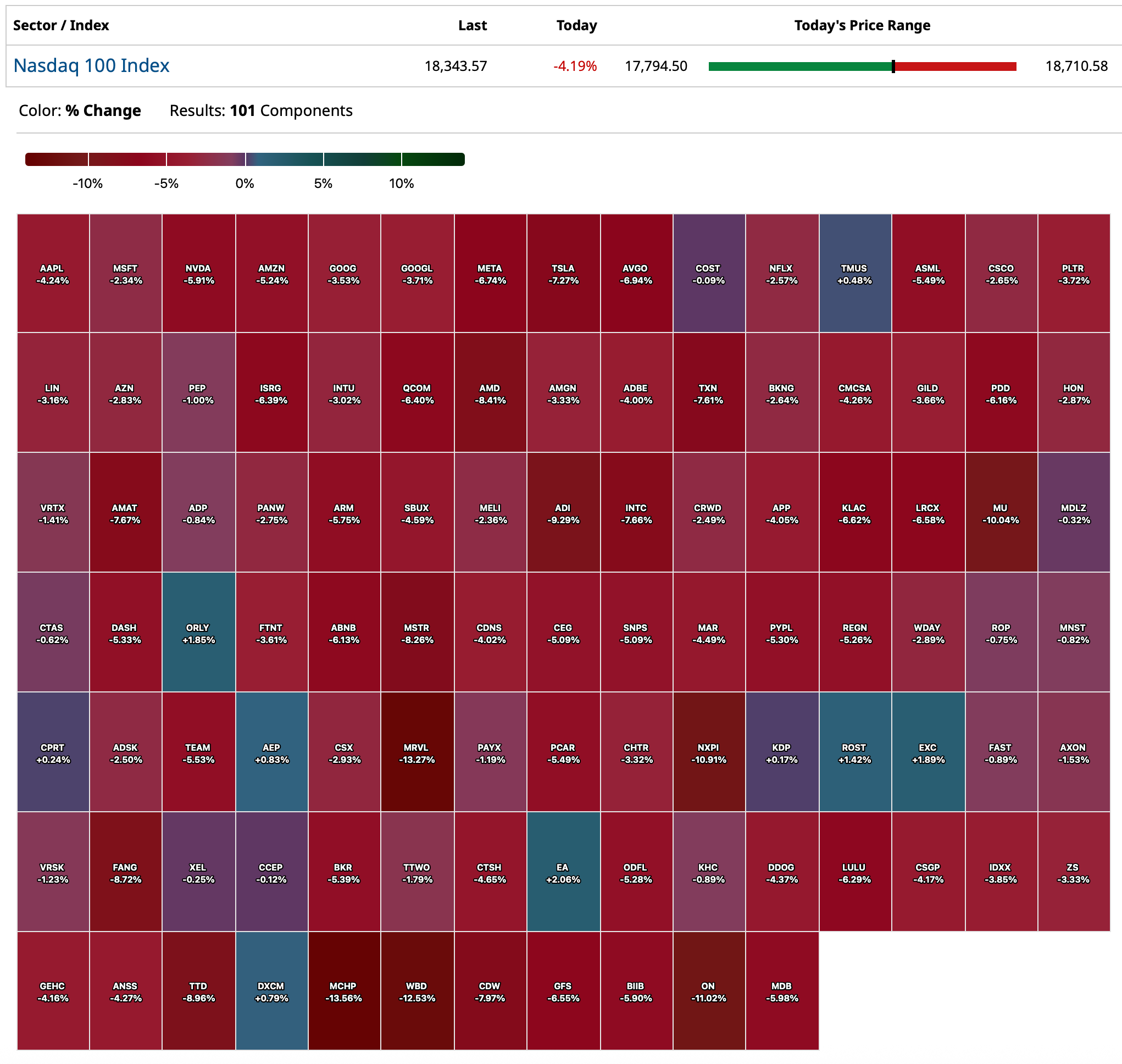

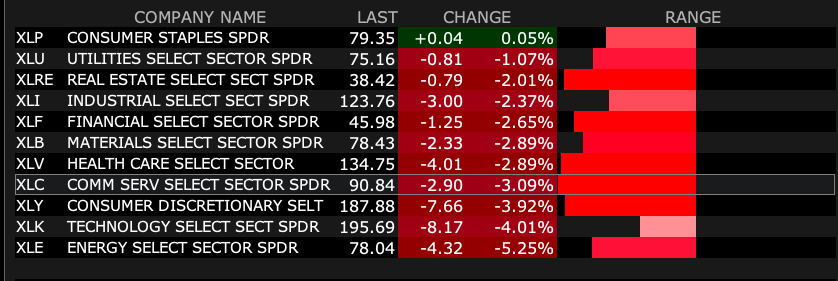

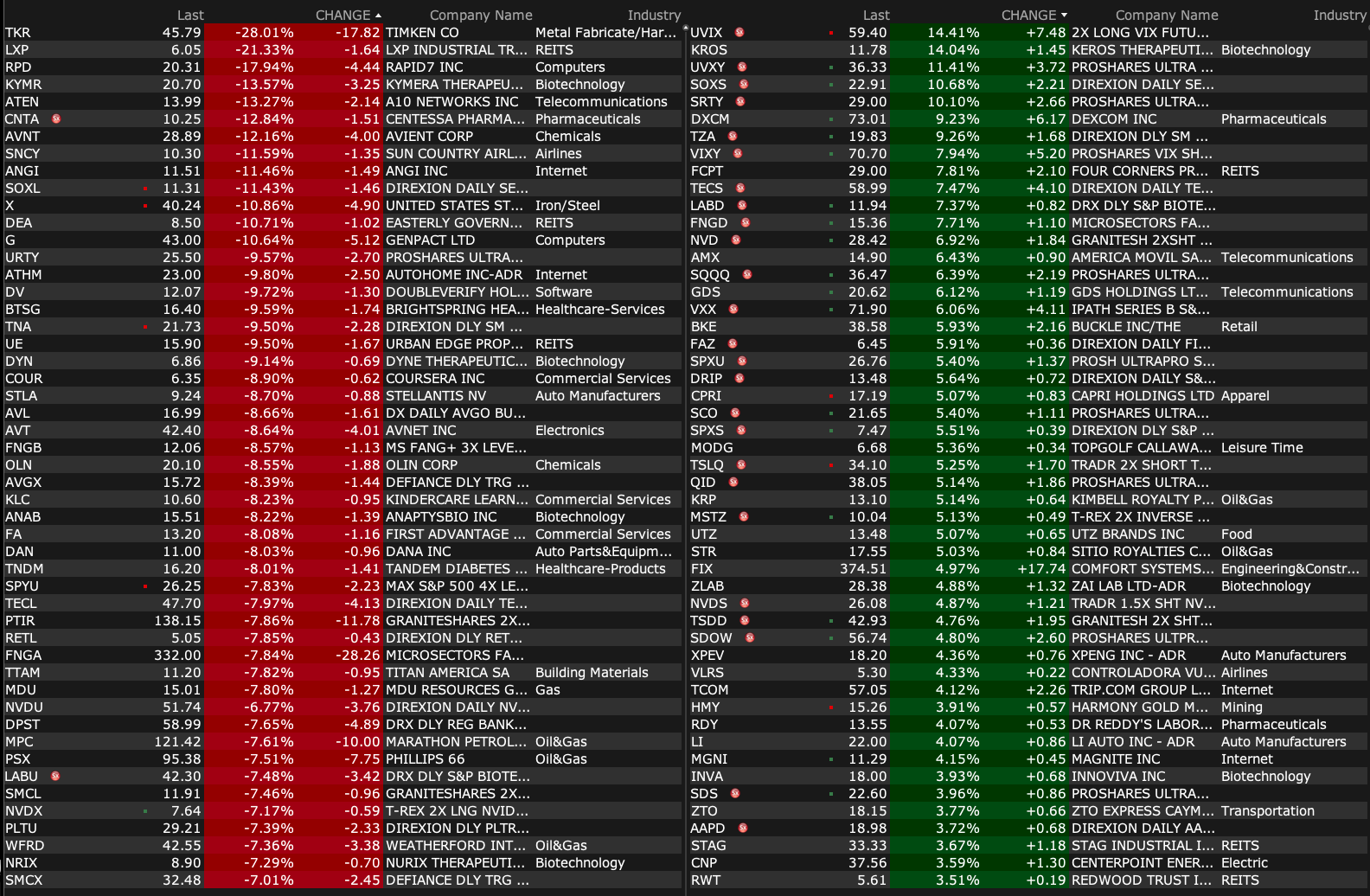

Thursday's After-Market Movers

As of 4:19 p.m.:

BY Doug Kass · Apr 10, 2025, 5:00 PM EDT

As of 4:19 p.m.:

BY Doug Kass · Apr 10, 2025, 5:00 PM EDT

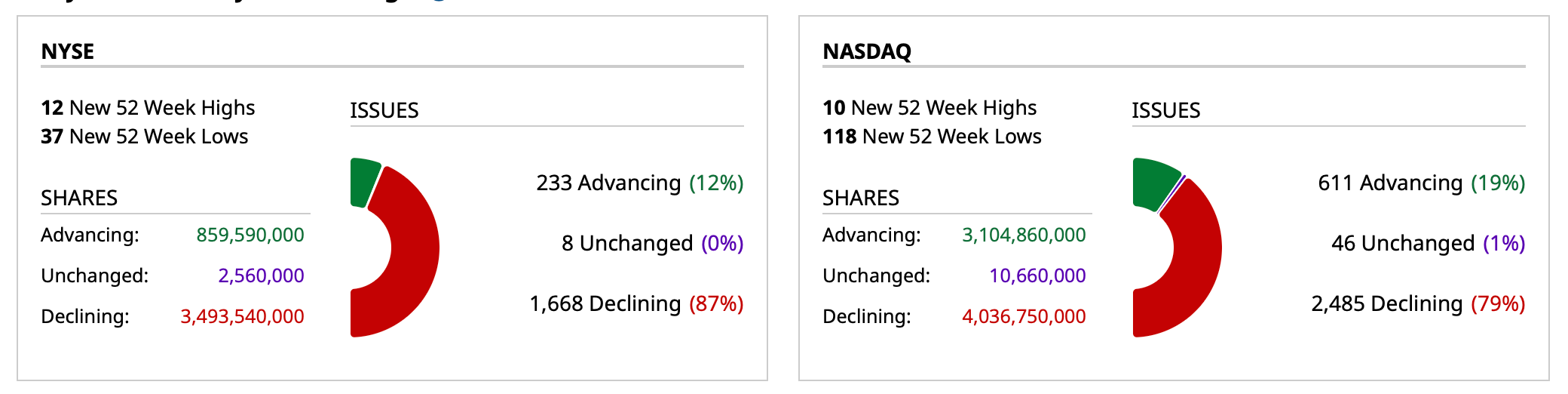

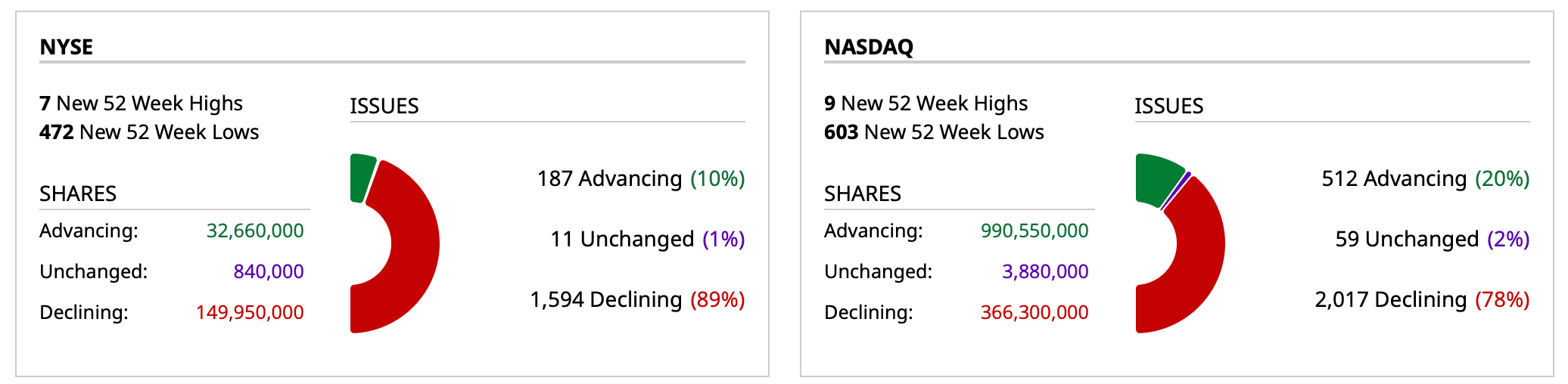

- NYSE volume 33% above its one-month average

- NASDAQ volume 44% above its one-month average

- VIX index: up 21.27% to 40.77

BY Doug Kass · Apr 10, 2025, 4:46 PM EDT

* The state of the bond market continues to deteriorate.

* Is the loss of U.S. safe haven status unfolding?

"There are blues you get from wimmin when you see 'em goin' swimmin'

And you haven't got a bathing suit yourself.

There are blues you get much quicker when you hide a lot of liquor

And your lady goes and swipes it off the shelf.

There are blues that come from waitin' on the dock, wondering if the boat is gonna rock,

And there's blues that come from gettin' in a taxicab and frettin'

Everytime you hit a bump and jump the clock.

There are blues you get from tryin' when you save a guy from dyin'

And he afterwards forgets you in his will.

But the blues much worse than this is when you're walkin' with the missus

And some chorus lady shouts, "Hello there Bill!"

But the blues that make me crazy mad and sorer than a bunion

'Till I feel like goin' out and stabbin' someone with an onion

Are the blues my naughty sweetie gives to me"

- Charles Russell McCarron, Blues My Naughty Sweetie Gives To Me

Bond prices just hit the day's low (TLT is lower by - $2.45) and yields have hit a high:

* The yield on the 10-year Treasury note is +1 basis point (and yields 4.40%).

* The yield on the 20-year Treasury bond is +7 1/2 basis points.

* The yield on the 30-year Treasury bond is +8 1/2 basis points (and yields 4.87%).

As El-Erian remarked in his tweet how the U.S. is losing its "safe haven" status:

Here is a further explanation of why U.S. rates are rising relative to other countries' rates:

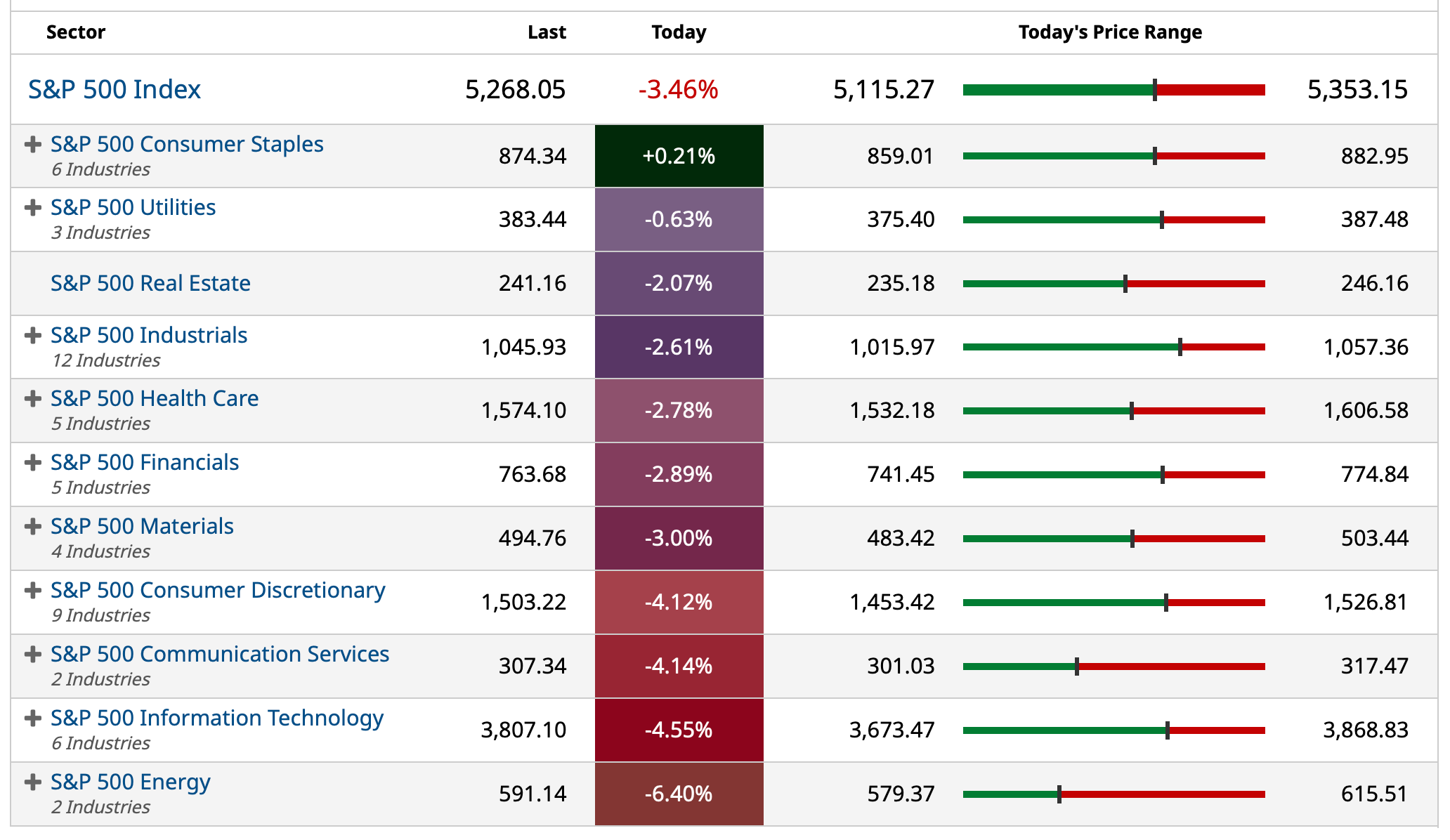

This helps to explain one important reason for the equity market's weakness today.

BY Doug Kass · Apr 10, 2025, 3:48 PM EDT

BY Doug Kass · Apr 10, 2025, 3:27 PM EDT

BY Doug Kass · Apr 10, 2025, 3:08 PM EDT

BY Doug Kass · Apr 10, 2025, 2:50 PM EDT

Housekeeping item.

WBD is -12% today I am covering some of my short at $8.03 (-$1.23).

BY Doug Kass · Apr 10, 2025, 2:41 PM EDT

Market structure issues in a leveraged system of capital asset categories (bitcoin, currency, commodities, equities and fixed income) dominated by passive investing (in turn controlled by algos and machines) are contributing to enormous volatility.

That volatility and its impact (on portfolios' "value at risk") is rendering trading particularly difficult — even for old graybeards like me.

Let's roll, but, as Phil Esterhaus said, "let's be careful out there."

BY Doug Kass · Apr 10, 2025, 2:15 PM EDT

From Peter Boockvar:

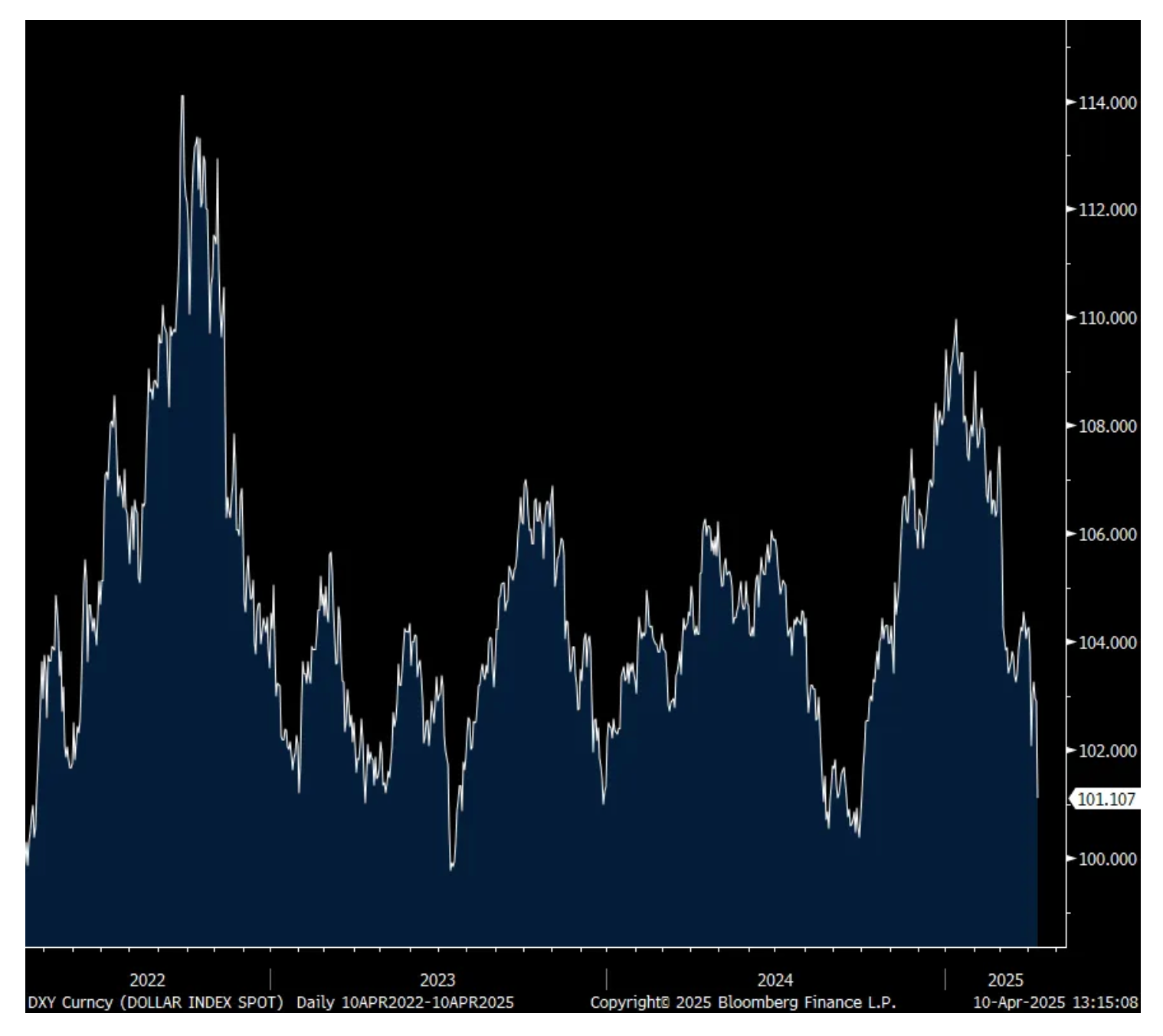

Very Good 30 yr auction after solid 10 yr, but dollar continues to break down

Because there is typically mostly 3 players in the 30 yr part of the yield curve, that being pension funds, insurance companies and those looking for the highest beta when betting on rates because of its long duration, I don’t pay as much attention to its auction results relative to the 10 yr but in light of everything going on, we have to take note.

The 30 yr bond auction was very good, following the great 10 yr yesterday and long yields are coming off their highs, though still up on the day. The yield of 4.813% was about 2.5 bps below the when issued pricing. The bid to cover of 2.43 though was only slightly above the 12 month average of 2.42. Direct and indirect bidders (I combine them because foreigners can use a US bank to buy at auction so it’s not clear who is a foreign buyer and who is not) totaled 88%, just above the one yr average of 85%.

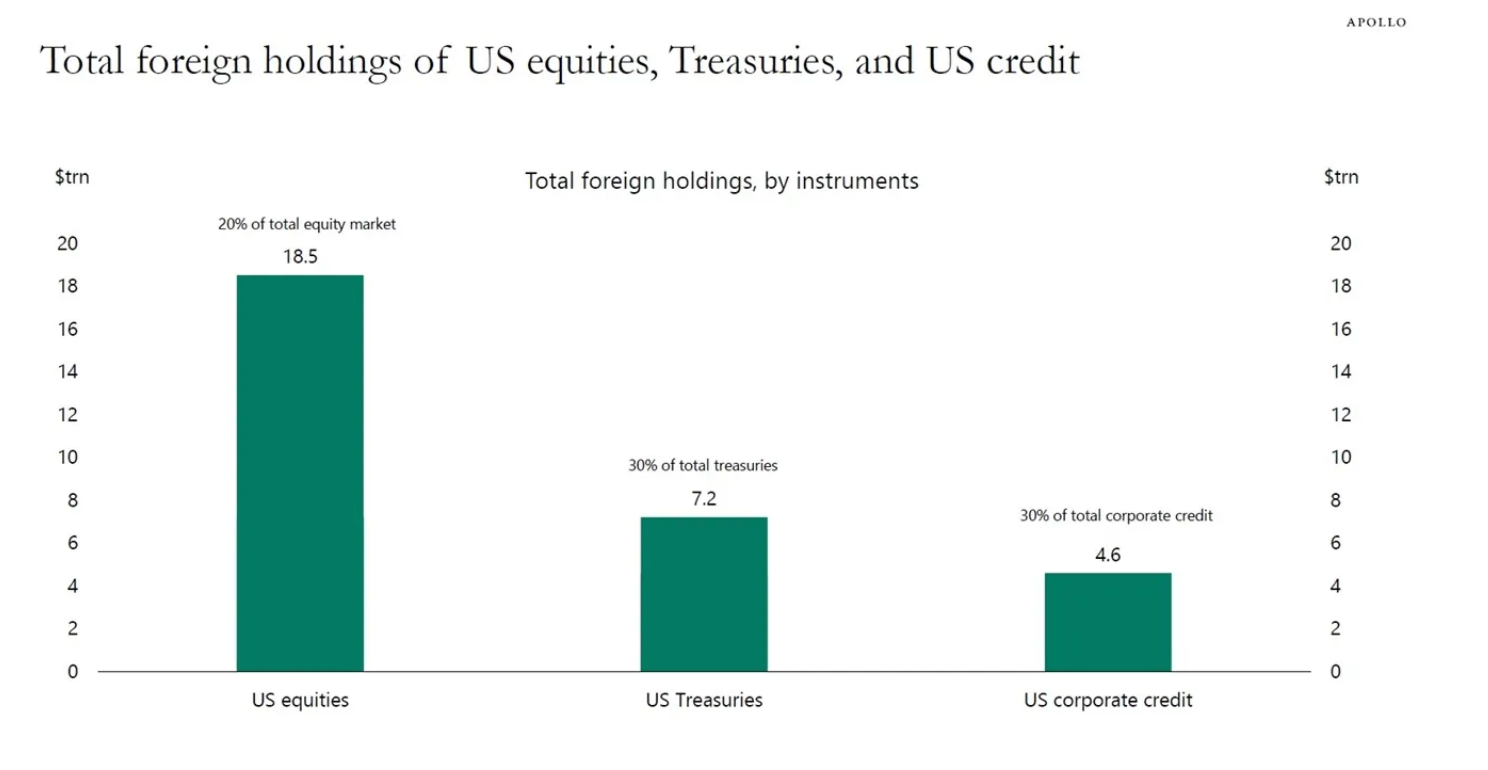

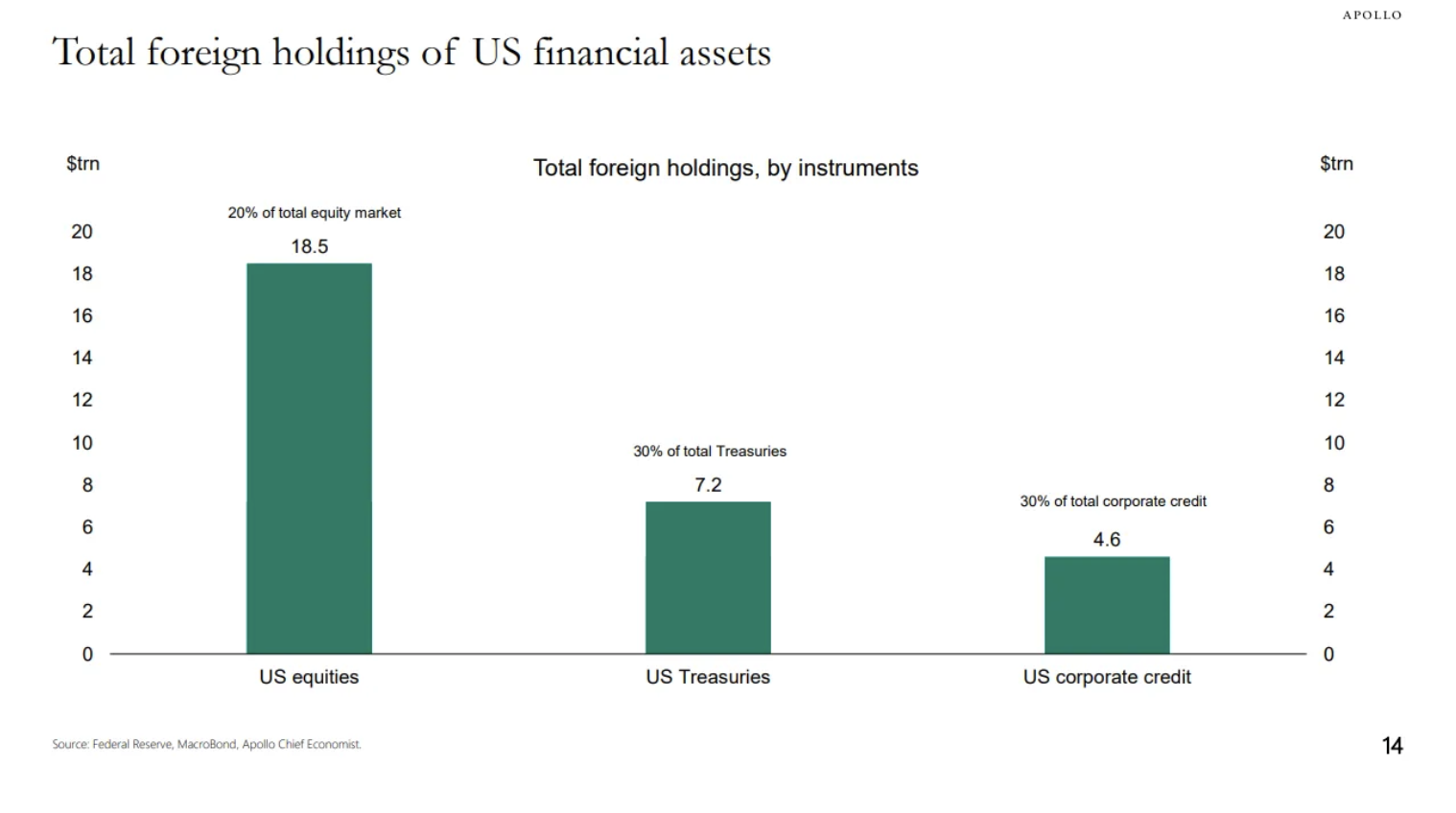

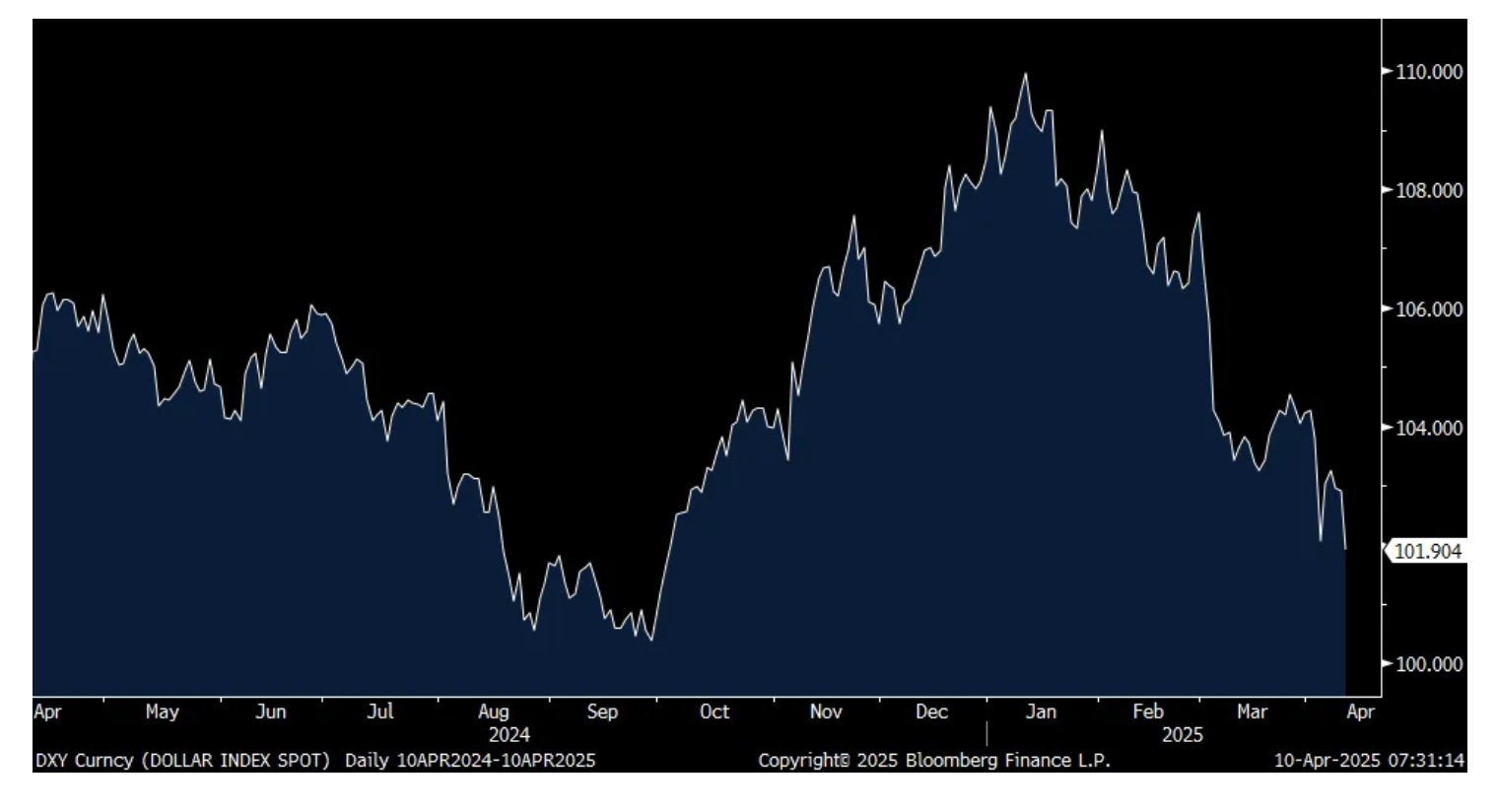

Bottom line, what stands out the most today is the continued weakness in the US dollar where the DXY is having its worst percentage day since November 2022 and nearing 100. The last time it broke 100 was in July 2023. This is happening obviously with US stock and long end bond weakness and this just smells of foreign flight from US assets. I include again the chart from Torsten Slok below measuring the foreign holdings of stocks and bonds, including corporates.

For every tick down in the US dollar, the more expensive these tariffs are going to be for us.

DXY

BY Doug Kass · Apr 10, 2025, 1:55 PM EDT

BY Doug Kass · Apr 10, 2025, 1:31 PM EDT

If you really want to get worried about the U.S. stock market, look at the multi-year chart of the Russell Index. (Tom Lee's favorite sector over the last 18 months.)

IWM is a proxy for economic sensitivity.

BY Doug Kass · Apr 10, 2025, 12:35 PM EDT

BY Doug Kass · Apr 10, 2025, 12:30 PM EDT

As I wrote in my opener, the administration is improvising on trade policy — and that's a slippery slope:

BY Doug Kass · Apr 10, 2025, 12:10 PM EDT

ocean20

Question for Doug. When you went in with all the long trades yesterday what percent were you long. Were you 100% long or still like 50/50 on base portfolio with the long trades. I am just trying to figure out my strategy . Its hard not to follow you in on the trades but I cant just follow and I know you dont ask us to just follow but I am trying to learn different strategies. Obviously your tactical thinking is very different if you were 50/50 with just adding 20 percent long trades than going 100% long. Let us know if you can.

Dougie Kass

that is irrelevant as my risk appetite is different than yours and yours is different than others

so providing an absolute level of exposure is meaningless

for example, what I may think is an aggressive long at 40% might seem defensive to a more aggressive trader (and vice versa)

what i did say i was at my highest net long in several years - that is relevant.

BY Doug Kass · Apr 10, 2025, 12:00 PM EDT

BY Doug Kass · Apr 10, 2025, 11:45 AM EDT

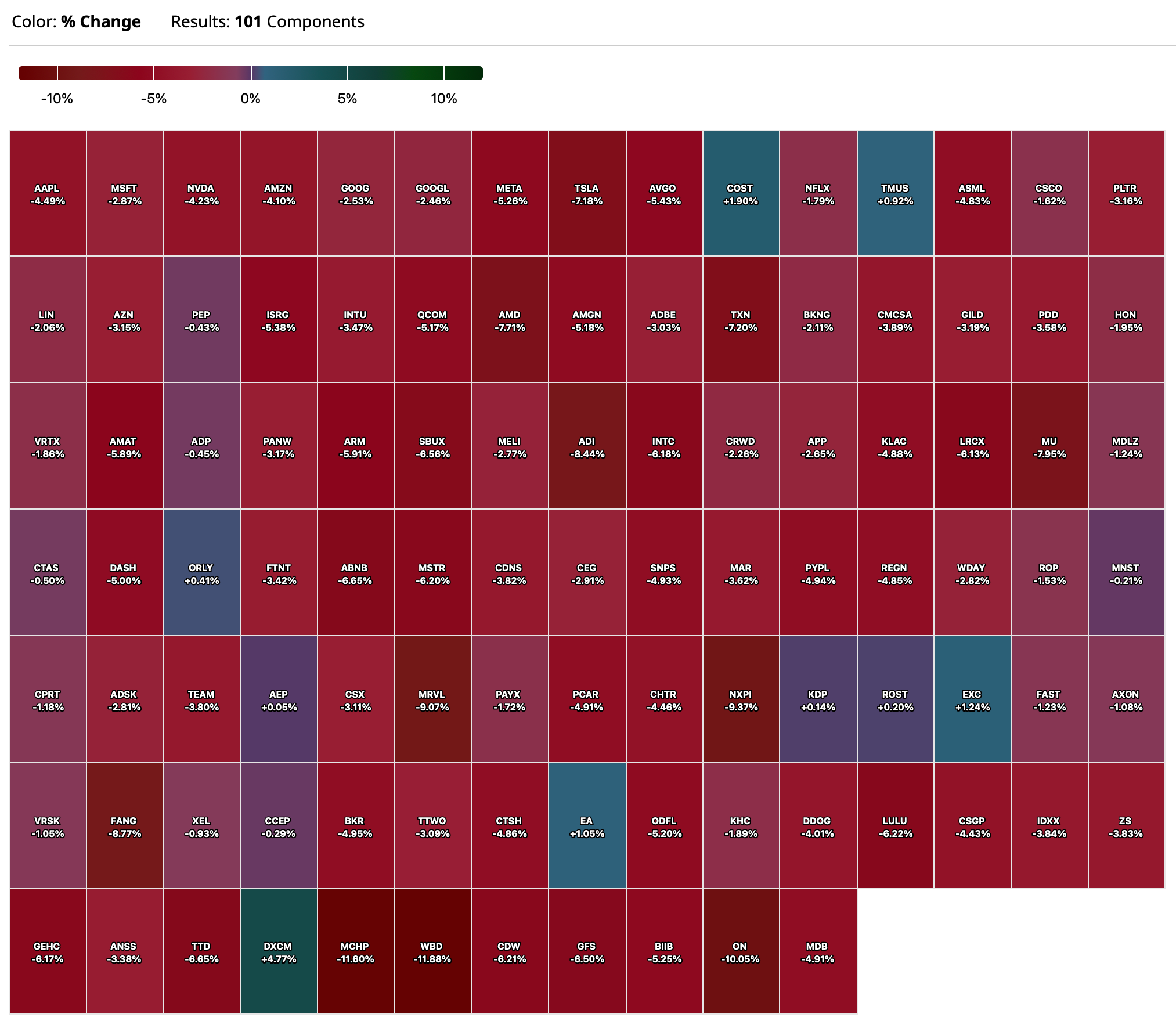

After a 93% up day:

BY Doug Kass · Apr 10, 2025, 11:35 AM EDT

- NYSE volume 6.4% above its one-month average;

- Nasdaq volume 67% above its one-month average;

- VIX index: + 17.25 to 39.42

BY Doug Kass · Apr 10, 2025, 11:25 AM EDT

Run don't walk to watch the two most honest and value added podcasters in the business - Guy, Carter and Dan - talk about the markets at 11 a.m. this morning.

And its Free.

Let's go to the tape! Stocks Sink After Trump Tariff Pause Sparks Historic Rally - YouTube

Who knows? They might even discuss my morning missive....

BY Doug Kass · Apr 10, 2025, 11:03 AM EDT

From Peter Boockvar:

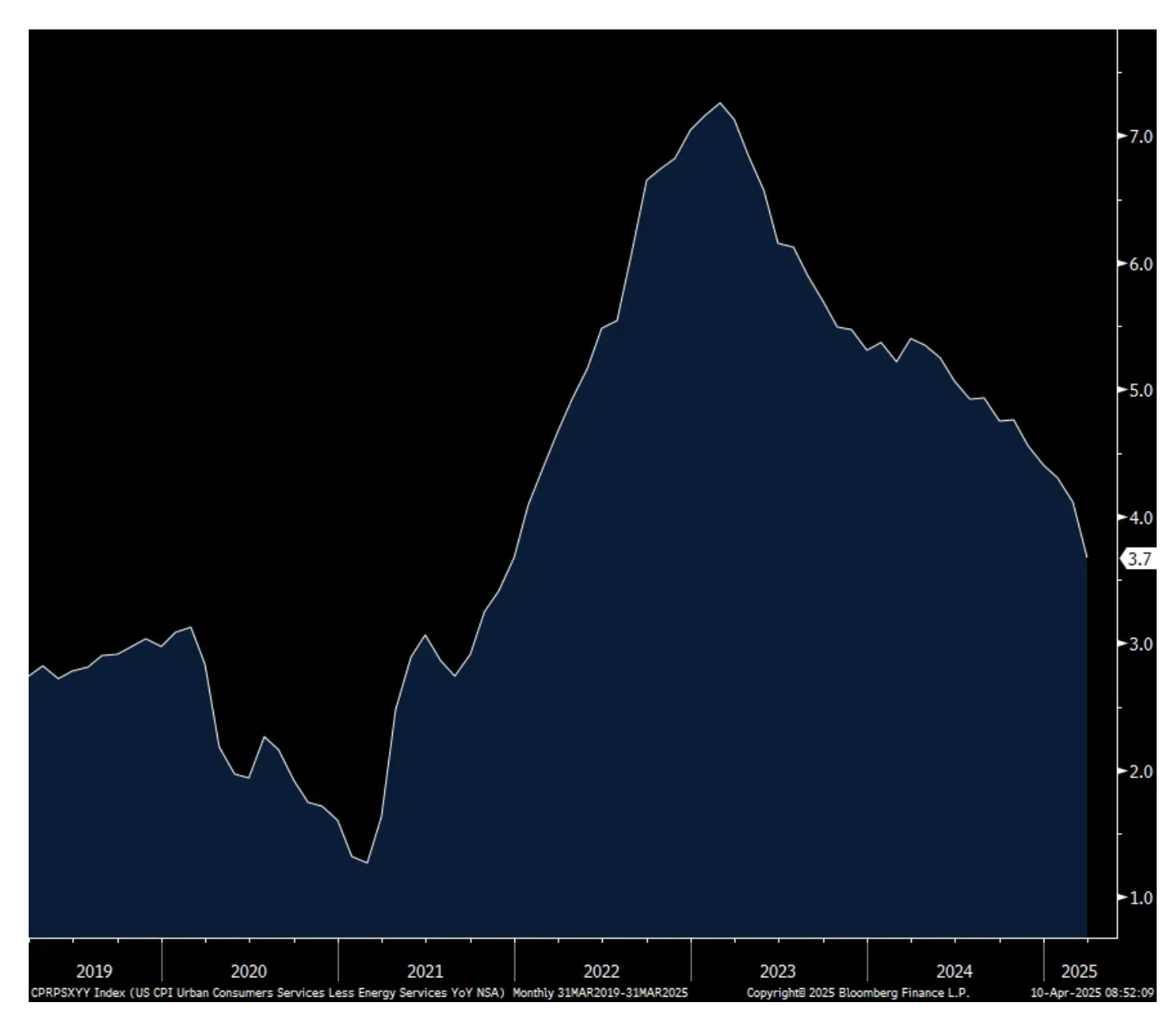

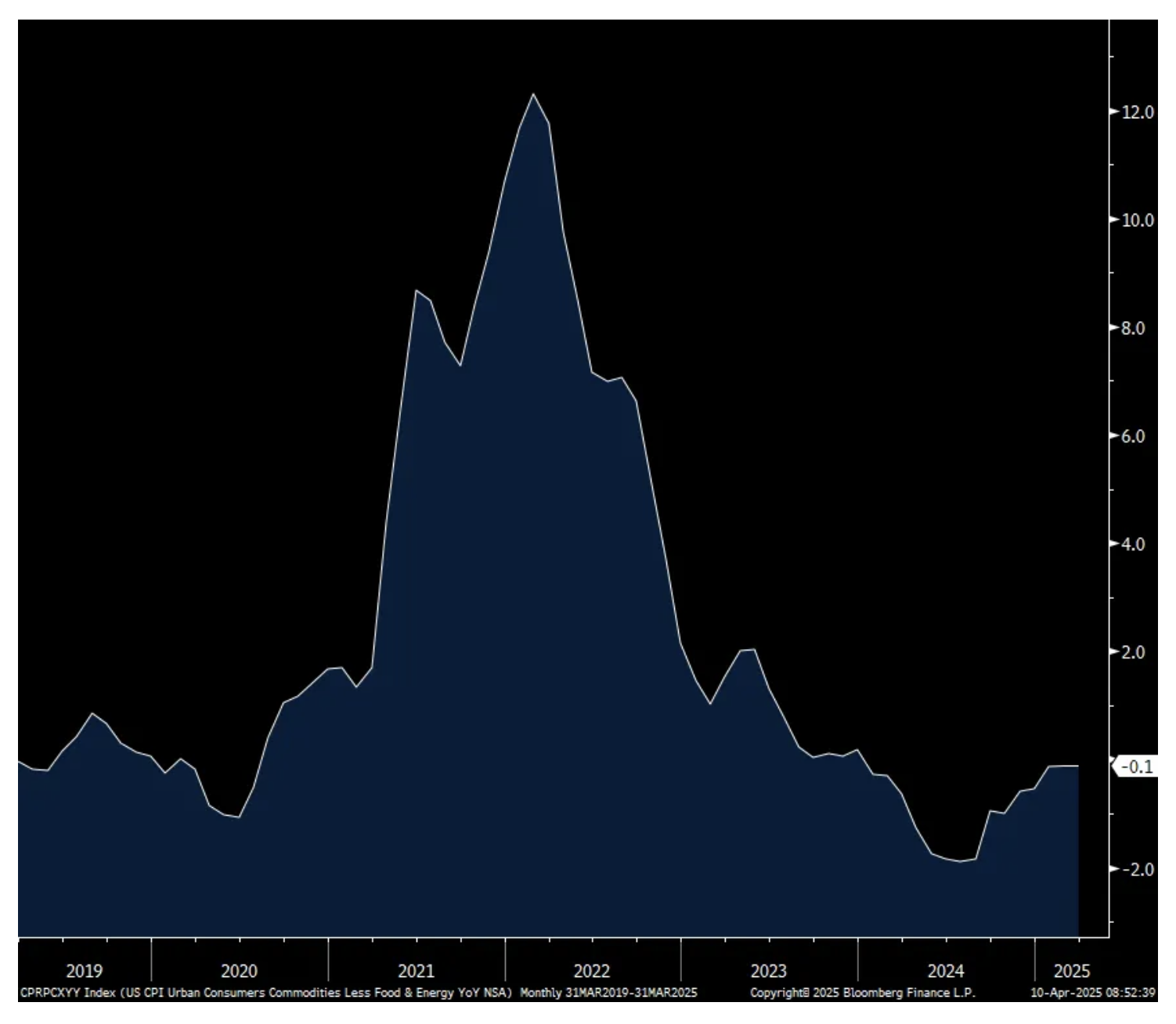

March CPI fell one tenth headline vs the estimate of a gain of one tenth. The core rate was higher by .1%, also two tenths below expectations. The y/o/y gains slowed to 2.4% headline and 2.8% core vs 2.8% and 3.1% in February. Weighing on the headline was the 2.4% drop in energy prices in part due to the drop in gasoline and fuel oil prices. Energy prices are down 3.3% y/o/y. Food prices in contrast rose by .4% m/o/m and by 3% y/o/y. ‘Food at home’ in particular was higher by .5% m/o/m and 2.4% y/o/y. ‘Food away from home’ saw a price gain of .4% m/o/m and 3.8% y/o/y.

Services ex energy prices were up just one tenth m/o/m and by 3.7% y/o/y, though still driving overall inflation. Rent growth remains overstated but also never reflected the real upside seen a few years ago. Owners’ Equivalent Rent rose .4% m/o/m and 4.4% y/o/y. Rent of Primary Residence was higher by .3% m/o/m and 4%. The former is a guess, the latter is real and the former should be scrapped from this calculation but the end result won’t be too much different. Medical care costs rose .2% m/o/m and 2.6% y/o/y but still WAY underestimating health insurance costs as here they were up .4% m/o/m and 3.1% y/o/y. Not reality. Dragging down service prices was the 5.3% drop in airline fares, maybe reflecting what Delta said yesterday about slowing demand. Hotel prices dropped a sharp 4.3% m/o/m and by 3.7% y/o/y. Also, finally there was a deceleration in auto insurance prices as they fell .8% m/o/m, though remain up by 7.5% y/o/y. Fixing a car saw prices up by another .8% m/o/m and by 4.8% y/o/y.

The goods side remains where the disinflation has taken place with core goods down by one tenth m/o/m after gains in the prior two months. They are unchanged y/o/y. After a rebound in used car prices over the prior 7 months, they fell by .7% m/o/m and are up just slightly y/o/y. New car prices have essentially flat lined over the past 3 months and also y/o/y. Apparel prices were up by .4% m/o/m but little changed y/o/y, up by .3%. Prices for things related to the home were unchanged m/o/m and down by .3% y/o/y. This includes everything from window and floor coverings, appliances, furniture, bedding, clocks, dishes, lamps, etc…

Bottom line, with goods prices flattish, though bottoming, and services inflation ex energy slowing to 3.7% y/o/y growth, the slowest since November 2021, overall inflation continues to decelerate. But of course this is all before the onslaught of tariffs and while there is a 90 day pause on the biggest of them, you can be sure there is a global rush to procure everything you can get your hands on which will push prices higher in the short term.

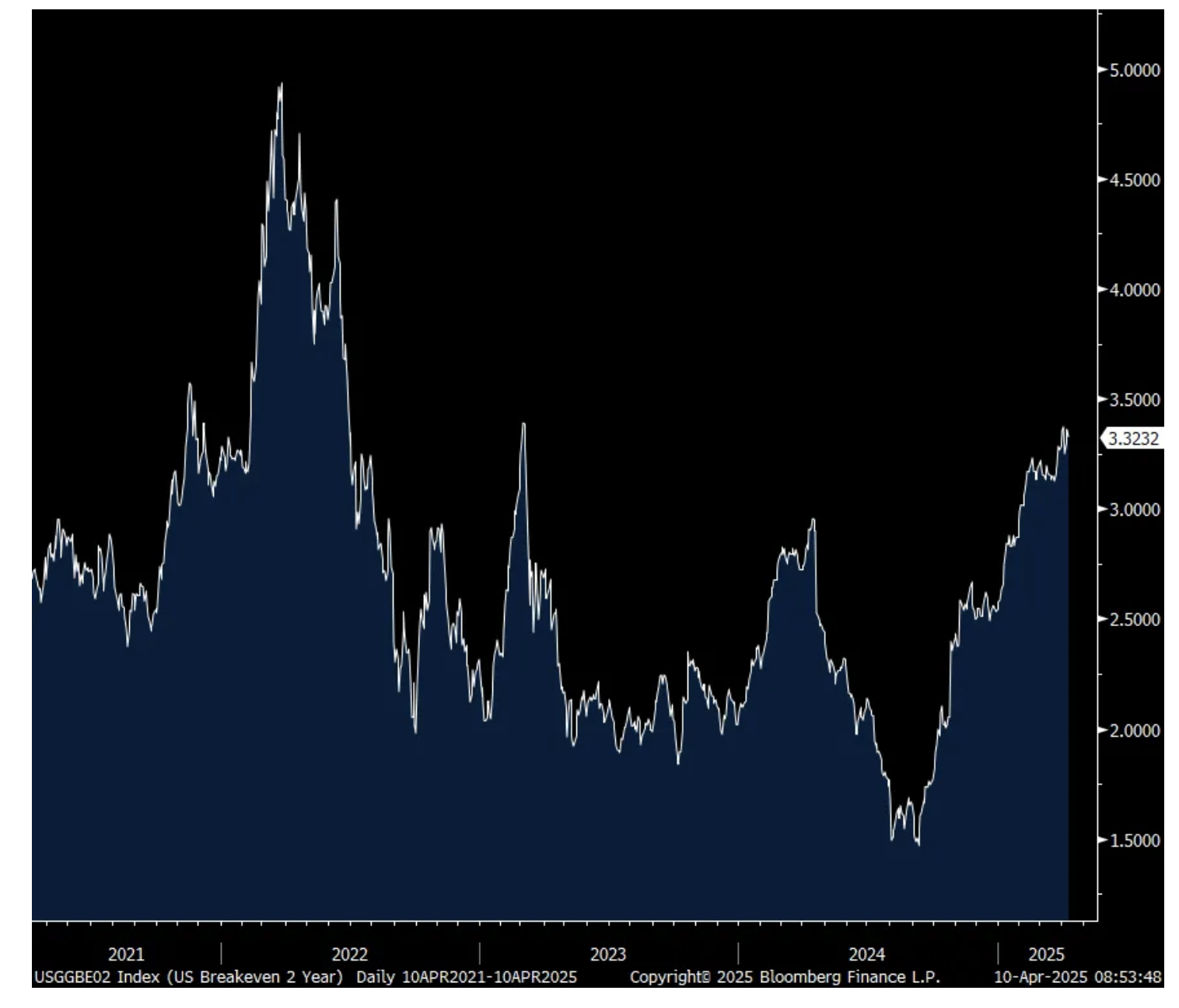

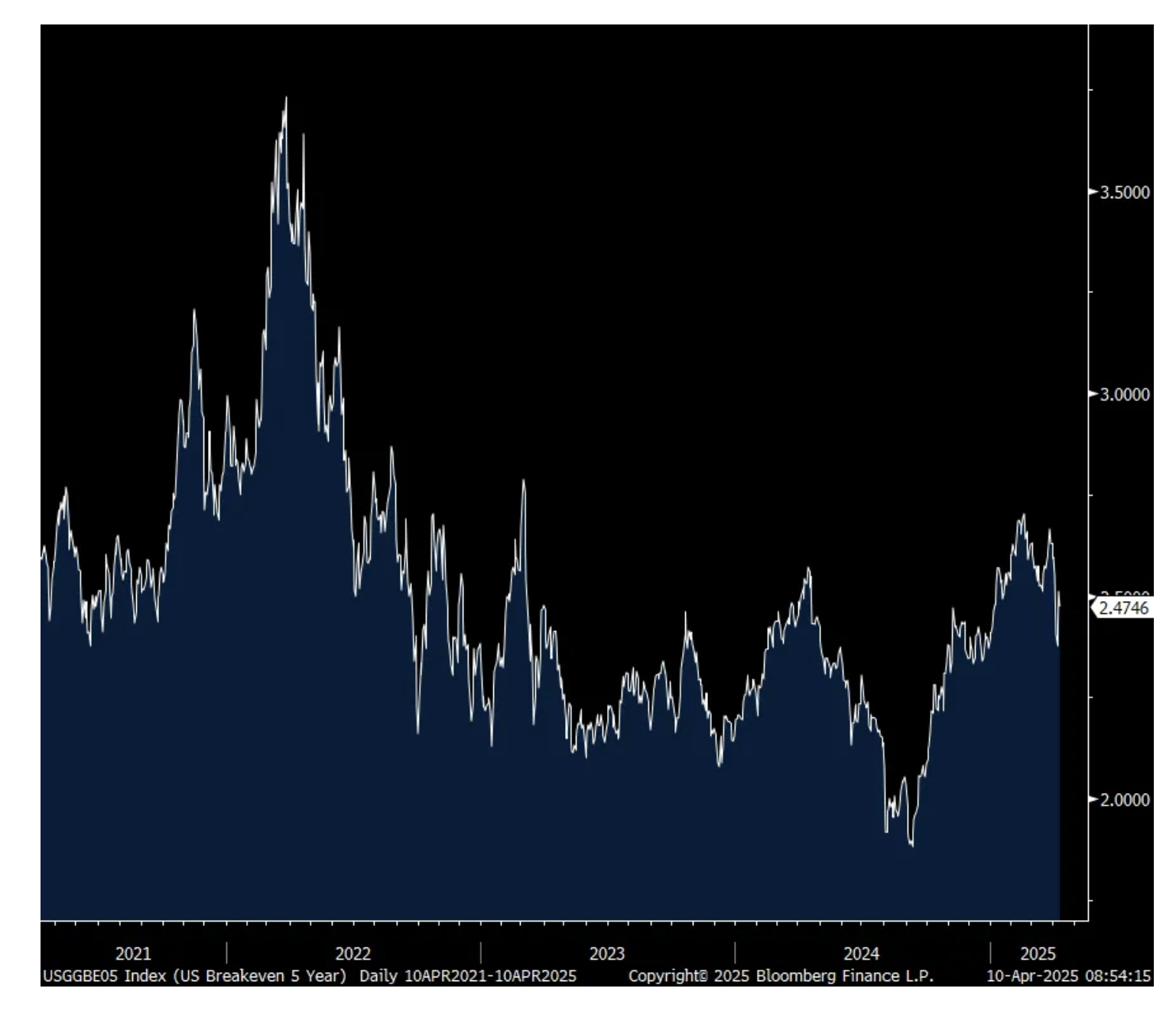

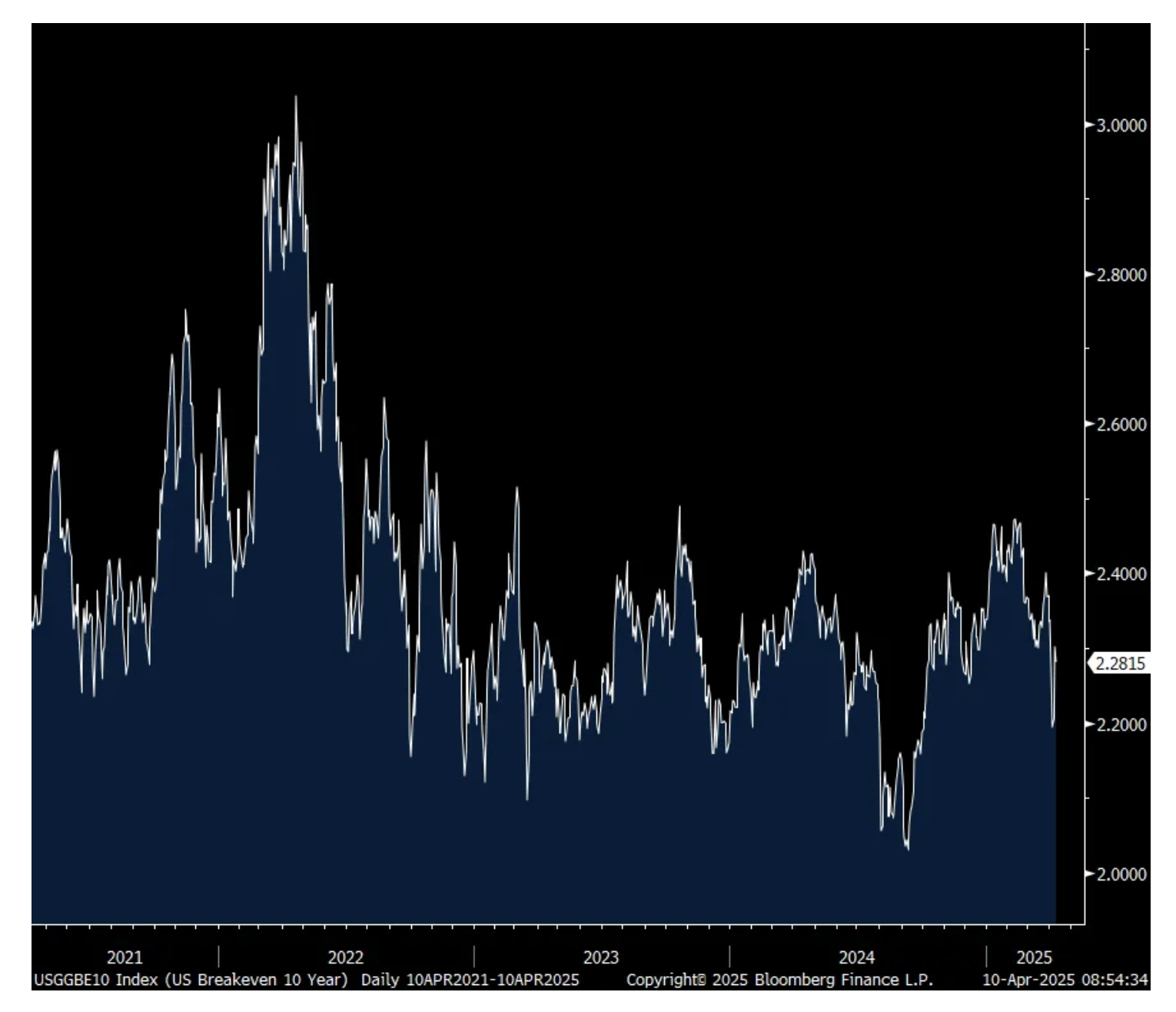

Reflecting the short term inflation worry but longer term calm is what is seen in the TIPS market with inflation breakevens. The 2 yr is at a two yr high but the 5s and 10s are much lower and chopping around.

The Treasury response to the data was mixed as the 2 yr yield fell 3 bps vs where it was right before the data after yesterday’s spike but the 10 yr yield is up 1 bp vs 8:29am est after the rise seen over the past 3 days.

Services ex Energy y/o/y

Core Goods y/o/y

2 yr Inflation Breakeven

5 yr Inflation Breakeven

10 yr Inflation Breakeven

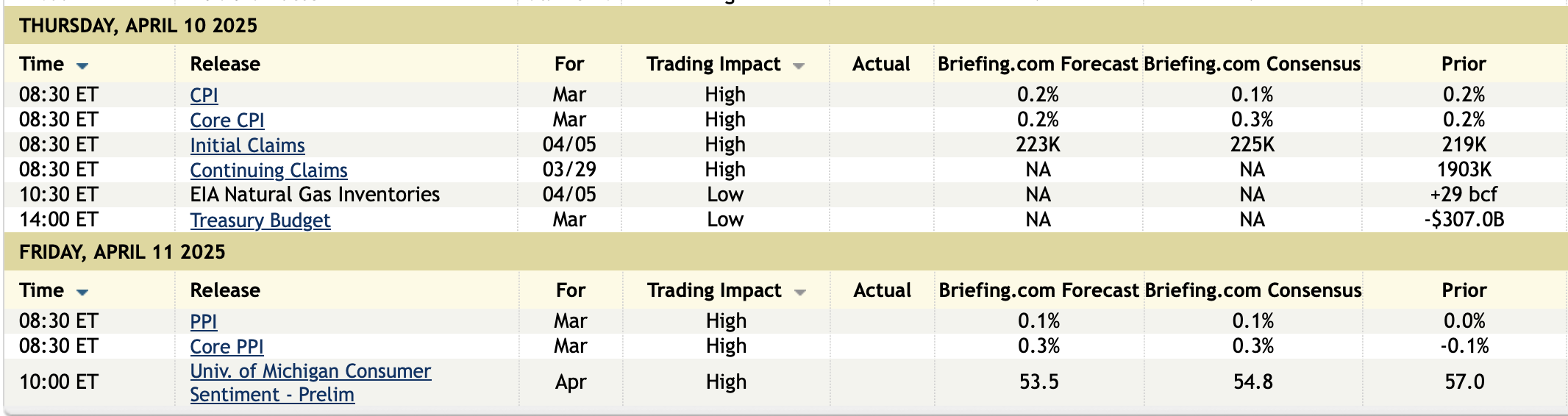

Initial jobless claims rose to 223k from 219k, though as expected and still remaining low, especially in light of everything going on. Continuing claims, delayed by a week and pre ‘Liberation Day’, totaled 1.85mm, down from 1.893mm in the week before. All eyes of course to what happens now post April 2nd, though now tempered, and with the drop in stocks.

BY Doug Kass · Apr 10, 2025, 10:55 AM EDT

From Peter Boockvar:

I think I'm going to have to buy a whiteboard for my office, with the magic marker and eraser, to keep track of both the tariffs we lay on the world, then take some off, and the retaliatory ones placed on us, and then maybe some removed.

It's of course great to see a time out called on the most egregious tariff threat we've seen so far, and that includes the 2018 experience, and we all hope that TRUE reciprocity is the end result with lower tariffs around the world. But what will come with the China tariffs and the 'negotiations' that follow?

I saw the story yesterday that some in Congress are preparing another bailout of American farmers because of the China tariffs placed on them, deja vu from the 2018-2019 bailout. I'd advise them to prepare one for dock workers on the West Coast if incoming trade with China really falters, which seems to be the intent.

I went to the websites of the Port of Los Angeles, Port of Long Beach and Port of Oakland to get a sense of the number of workers they employ, the broader worker impact on those they do business with and the exposure to China and broader Asia.

For the Port of LA, they employ about 1,000 workers on site at the docks but according to a Facts & Figures page they have, they impact 136,000 jobs in LA, which is 1 in 14 jobs in that city. In the broader five county region they influence 486,000 jobs which is 1 in 18 and for the entire US, they impact 1,400,000 jobs which is 1 in 113. Not surprisingly, their biggest trading partner is China, by far, as they are 3 times bigger than number two and three which is Japan and Vietnam. About 90% of its imports come from all of Asia.

The Port of Long Beach is the 2nd busiest US port behind the Port of Los Angeles. They directly employ about 500 people but claim to support 51,000 jobs in Long Beach, about 1 in 5, according to their website. In the five county Southern California region, they impact 576,000 jobs, or 1 in 20. And throughout the US, they claim that 2.6 million jobs "are related to Long Beach generated trade." But, I think that last stat includes the LA port. Who is their biggest trading partner? You guessed it, China, followed by Vietnam and Thailand.

China too is the biggest customer for the Port of Oakland and 74% of the incoming cargo is from Asia. In the press release I post below from 2023, the Port of Oakland Executive Director said "The Port of Oakland continues to be one of the region's leading employers, creating good-paying union jobs for local residents and families. These jobs are a critical contribution to the economic vitality and growth of communities in our region." They employ directly 470 people and support 98,345 jobs in the Northern California region from data I saw in this press release from September 2023 .

Here some more facts and figures.

Overall for these major California ports, they "carry approximately half of the nation's total container cargo volume" according to the Port of Oakland website.

As we debate the impact of foreign selling of US assets, here's another great chart from my friend Torsten Slok so we can see to what extent they own US stocks and bonds, including corporates.

Here was more from Delta in their earnings call:

"February and March reflected a much more challenging macro environment than anyone initially planned for. Coming into 2025, we are positioned for another year of strong growth. However, given broad economic uncertainty around global trade, growth has largely stalled. The impact has been most pronounced in domestic, and specifically in the main cabin, with softness in both consumer and corporate travel. While not immune in this environment, we do continue to see greater resilience in international and our diversified revenue streams, including premium and loyalty, reflecting underlying strength of our core consumer."

"Consumers remain cautious and corporate travel trends are choppy, with overall corporate volumes currently expected to be flattish over last year, similar to what we saw in March. Main cabin demand softness in both domestic and international is persisting, particularly in off-peak times...Internationally, approximately 80% of revenues are US point of origin, with bookings remaining strong for the peak summer period."

"In Canada, we have seen a significant drop off in bookings. In Mexico, it's kind of a mixed bag...And I think we will be looking at Canada and Mexico as places that we probably want to reduce our capacity levels as we move forward." I'll add, this certainly didn't need to happen.

Japan said its PPI for March rose .4% m/o/m, double the estimate and February was revised up by 2 tenths. Versus last year, wholesale prices are up 4.2% and we saw a jump in JGB yields with the 10 yr higher by 8 bps to 1.35%.

Reflecting likely the pull forward of ordering ahead of tariffs, Taiwan's trade data came in about twice expectations. Exports in March jumped 29%, well above the estimate of 14%. Imports were higher by 18.5% and vs the estimate of 8.1% growth. The TAIEX rebounded by 9.3% overnight but is still down 17.5% year to date after a strong few years prior. The Ho Chi Minh index by the way was higher by almost 7%, though still lower by 7.8% ytd. We remain bullish and long Vietnamese stocks.

China's March CPI was flattish, falling by .1% y/o/y and all led by lower food prices which dropped by 1.4% y/o/y. Prices ex food and energy were up by .5% y/o/y. PPI was down by 2.5% y/o/y vs the estimate of -2.3% as they remain challenged by the global manufacturing downturn and price competition. Though seeing no relief on tariffs, the Shanghai comp was up 1.2% and the Hang Seng rallied by 2% are is still up 3% ytd.

Finally, another look at the US dollar which reversed lower against the yuan today and is faltering again vs most other things with the DXY at the lowest level since early October.

DXY

BY Doug Kass · Apr 10, 2025, 10:35 AM EDT

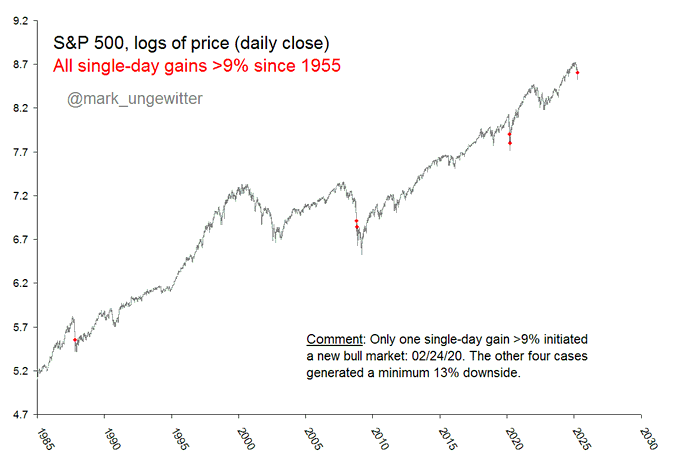

* We are likely in the early stages of a protracted Bear Market that started in late January

* Valuations remain inflated, consensus 2025-2026 S&P earnings per share and global GDP forecasts are too optimistic -- recession risks are probably still close to 50%

* The Federal Reserve is dug in a policy box

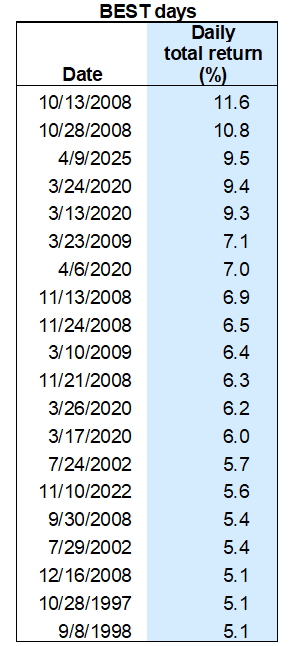

* Over history, the best daily returns are achieved during bear markets (see chart below) -- yesterday was probably no different than the previous bear market rallies

* We continue to view January, 2025 as an important market and Magnificent 7 top -- similar to the major market and Nifty Fifty tops experienced in January, 1974

* Improvisational fiscal policy (and changing goal posts of reciprocity with trading partners) driven by impulse, intuition and little analysis will likely weigh on consumer/corporate spending intentions and the global economy

* Make America Scammy Again -- "MASA"? Were people tipped off to yesterday's announcement? Action in the options market (and elsewhere in the markets) raise the issue of..."Who knew about the change in tariff policy?"

* We sold out most of our trading long rentals in the spectacular rally late on Wednesday

* Then there is the continuing China tariff situation...

* We would not be surprised by a possible retest of the recent lows

Most of The Best Daily Returns Since 1990 Have Occurred in Bear Markets

"A bull market tends to bail you out of all your mistakes. Conversely, bear markets make you pay for your mistakes."

- Richard Russell

Before you start reading today's opening missive, please consider my comments within the context of Warren Buffett's teachings:

"Market forecasters will fill your ear but will never fill your wallets." tt

I am not being humble, I am being honest. As I always write, I often make mistakes (I have the scars on my back to prove it!) and I am always in doubt. No hubris here -- as, unlike some (who are trying to sell a service) I don't have exaggerated pride or self confidence. I know, after all these decades, that Mr. Market exists to embarrass us all.

Over the last year I have claimed that we have unjustifiably been in A Bull Market in Certainty -- arguing that certainty of bullish outcomes (incorporated by the consensus and in a 23-times price earnings multiple) was unwise. Resultingly, up to late last week I maintained an ursine market view.

That began to change four days ago, as in the teeth of the vicious market decline I materially expanded my long exposure.

I got lucky on Tuesday (the day before Wednesday's "face ripper") in which I outlined the case ("A Bear Turns Short-Term Bullish") for a sharp and imminent rally within the context of a Bear Market.

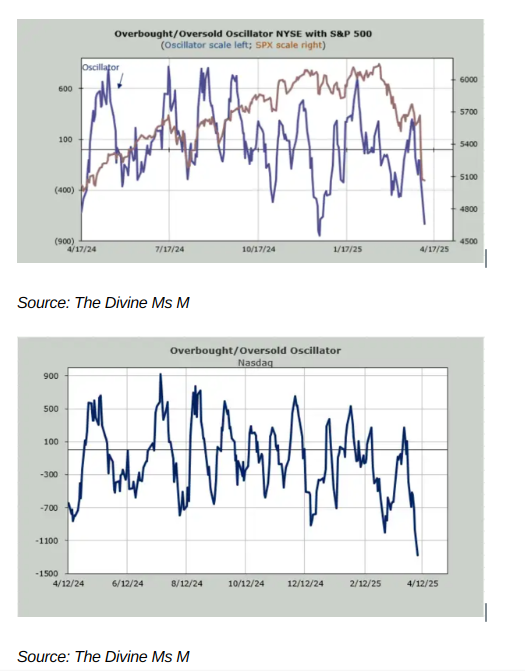

Besides a meaningful oversold and bearish sentiment extreme (manifested in the spike to 60 in the VIX, an oversold Oscillator, low relative strength index, prepondernce/unprecedented Bear/Bulls ratio and fearful sentiment surveys (CNN Fear & Greed etc.) -- the fast (and scary) weekend climb in interest rates and the rapid and deep capital destruction in our capital markets (over the last six weeks) were instrumental to our view of expecting a market rally.

But even more importantly, we saw the need and likelihood of a quick adjustment in tariff policy by the President. As we wrote on Tuesday:

Peak Tariff Concerns: We are almost certain that the hard line in the Trump administration apparent tariff's policies will be softened. As always, President Trump starts big in his threats. Any pause, easing or softening in policy (very likely) could reverse the recent downturn in sentiment in a backdrop of rising shorts, liquidation, emotional selling and near panic selling in certain individual stock prices (some of which have gotten back to great upside/downside opportunities for the first time in several years)

Here is our complete post (two days ago) which anticipated an imminent rally:

In the last two days I have shifted to the largest net long exposure I have had since the last half of 2023.As of the close, the S&P Index is -14% and the Nasdaq Index is -19% in 2025.At the worst levels Monday the S&P Index was -19%A (year to date), worse than the downside of about -15%E (vs. expected upside of only +5%E) that I projected at the beginning of this year.

Extreme Sentiment: With sentiment at a bearish extreme (as measured by the CNN Fear and Greed Index at "3"), the AAII bears/bulls, the VIX spiked to 60 (it's now back down to a still-elevated 43) and the extremely oversold S&P Short Range Oscillator (-8.7%) I was confident that the sentiment factors had turned extremely negative, perhaps providing a backdrop for taking on more long exposure.I can't lie, Jim Cramer's panicky expectation on Sunday of a "Black Monday" had some impact on my new-founded buying strategy! It was a manifestation of the market's pessimism.

Still Weak Technicals: While the technicals continue weak and somewhat ambiguous, the fundamentals were finally accepted to be deteriorating (as we have warned and feared).

Better Reaction to Bad News: And, Monday, equities rallied, even in the face of continued and stern tariff warnings from the president.

Peak Tariff Concerns: We are almost certain that the hard line in the Trump administration apparent tariff's policies will be softened. As always, President Trump starts big in his threats. Any pause, easing or softening in policy (very likely) could reverse the recent downturn in sentiment in a backdrop of rising shorts, liquidation, emotional selling and near panic selling in certain individual stock prices (some of which have gotten back to great upside/downside opportunities for the first time in several years). (Note: I added a number of new longs to my Watch List over the weekend.) As a consequence, we were very active on the buy side — throughout the entire morning weakness, adding further to the indices on each pullback...

As seen the chart I started this column with (above) and the chart that follows (note the large daily gains in red), the best rallies occur in bear markets and during crises -- in fact, bear market rallies of the order of magnitude that occurred on Wednesday (+9.5%) are more of a signpost of emerging economic and liquidity problems than indicative of a healthy stress-free global economy or capital market:

Here are some thoughtful observations from Dan Niles

Just for fun, I looked at the two big up days during The Financial Crisis -- October 13, 2008 (+11.6%) and October 28, 2008 (+10.8%). From the Oct. 13 close to the Oct. 14 intra-day peak was around +4%, then the market reversed and closed down. Unlike today so far, it opened strong that day.

From the 10/28 close the market moved up another +7.5% over the next 5 trading days before the bear resumed.

* A comprehensive, well thought out global tariff policy is far different than a transactional NYC real estate deal

* The U.S. has become, increasingly, an unreliable and undependable partner

* Global economic growth will suffer

A real estate deal in New York City is dissimilar to establishing global tariff policy.

The improvisational manner in which the President appeared to create and then alter tariff policy is disarming -- for our markets and for consumer and corporate sentiment and spending.

It is unclear that President Trump actually understands how international trade actually works:

Justin Wolfers posted on X: "It's an extraordinary question to have to ask you, but do you think Donald Trump actually understands how international trade actually works."

Finally, the rationale for tariff policy keeps changing. Remember when it was all about bringing manufacturing home? (That was two days ago!). Now its about negotiating deals.

Those two objectives are in tension. ("Is a company willing to build a factory in the U.S. if tariffs are likely to persist?")

Why would any company proceed with capital and spending plans in the face of the continued uncertainties of policy?

More domestic and global economic concerns:

* The odds of a recession are still about 50%

.* The Administration is not going to get "big" wins: Tariffs were low before this and if the President negotiates competently, they will be low again. Basically there is no gain. (We have seen this before when NAFTA got relabeled by the President in 2020, but the agreement really didn't change much).

* During the 90-day pause, the U.S. will still have the highest tariffs in the world, perhaps more than 10-times - 20-times that of most of our trading partners and roughly 10-times higher than it was before. These are still at or above the Depression-era Smoot-Hawley tariffs.

Execution risk is always challenged with rapidly rising volatility. Many leveraged players (think Long Term Capital, etc.), in particular, will not be able to navigate the journey and there will be casualties along the way:

Here are some questions I do not have the answer to, but, boy, I would love to know:

* What caused them to cave on the tariffs? Was it the equity markets, the Treasury (basis trade unwind)/debt markets and financial plumbing issues, or other?

* Are we in a better position now than we would have been in if we started with a more measured and negotiated approach to all of these issues? Or are we now worse off that we went down this path, and backed off, and now leverage has been lost as it shows we don’t have the stomach for a big and protracted fight?

* It was also amusing watching a 10-year auction at 4.43 being celebrated when it was sub 4.00% last week...

* Make America Scammy Again? (MASA) Was there foul play? Who knew about the 90- day pause in tariffs announcement ?

'

Once again, it seems more than one person trading stocks knew. The Nasdaq was up about +1.5% at about 10 a.m., when one would think it should have been pretty soft in the morning based on what went on overnight. Same guys in the basis trade (per first dash) would be the same people most likely to have the direct line to those dealing with the financial plumbing issues. Who knows, but the open Wednesday morning being pretty firm was interesting.

Take a closer look at the options market, with the calls that expired on Wednesday! Those that are wiser were probably buying straight equities (albeit on a levered basis):

There are a lot of other issues at play with the equity markets still, that have nothing to do with tariffs.

The AI/Mag 7 unwind, softer consumer, sticky inflation, credit markets (and rates still did not back off with the massive equity rally), valuation, still a general lack of confidence and confusion among consumers and company executives (who will still have no idea how the tariff thing will resolve and what to do in the interim), global instability, and a broken and self destructive political system that has more interest in destroying the other side than productive solutions.

Then there is the continuing tariff saga between the U.S. and China, which will likely remain unresolved for some time:

"We sail within a vast sphere, ever drifting in uncertainty, driven from end to end."

- Blaise Pascal

The events of this week are not growth or valuation friendly. Rather, they could trigger even greater instability.

The events of this week uncovered some of the market structure concerns (in a leveraged capital market system) that we have opined about over the last twelve months.

The events of this week underscore the risks of improvisational fiscal policy.

There remain downside risks to economic growth and upside risks to inflation.

We believe that a protracted Bear Market began two months ago. Similar to the top in The Nifty Fifty in January , 1974 a seminal rotation out of Mag7 began in late January, 2025.

Wednesday's rise in the S&P Index of +9.5% was the third best daily rise in history. Unfortunately and over history, most of the largest daily market rises occurred during bear markets.

Markets are constantly in a state of uncertainty and flux and money is made by discounting the obvious and betting on the unexpected.

The unexpected would be a retest of the recent market lows.

I would sell all rallies.

BY Doug Kass · Apr 10, 2025, 9:55 AM EDT

-PRFX +40% (expands into home energy management sector)

-LOVE +16% (earnings, guidance)

-KROS +14% (announces review of strategic alternatives)

-TLS +14% (awarded $5.8M Contract from US DoD to Support Defense Department’s Microwave Line of Sight Program)

-DXCM +9.2% (Dexcom G7 15 Day receives FDA Clearance)

-CDT +8.1% (announces up to $1M Share Repurchase Program)

-SXTP +6.8% (to discuss Babesiosis at Healing Lyme Summit)

-CPRI +5.1% (to buy Versace from Capri in deal valued at $1.38B)

-BCTX +4.1% (subsidiary BriaPro develops Novel Antibodies to Anti-Cancer Target B7-H3)

-PCYO -11% (earnings, color)

-X -11% (consistent with prior position President Trump says he doesn’t want US Steel sold to Japan)

-STLA -8.7% (reports revenue; ready to engage in talks with Italian unions to avoid 'unilateral actions' on employment levels and expects up to 2.8K voluntary job cuts)

-RCAT -7.8% (files to sell 4.72M shares in $30.0M registered direct offering)

-KMX -7.6% (earnings, guidance)

-STM -6.9% (earnings, guidance)

-GM -3.7% (UBS Cuts GM to Neutral from Buy, price target: $51 from $64)

-TSLA -3.5% (OpenAI files suit; Nissan Motor says planning to launch next generation autonomous driving technology)

-NKE -3.3% (hearing price target cut by Stifel due to tariff concerns)

-LAKE -3.1% (earnings, guidance)

-DAL -2.9% (downside momentum following earnings)

-STZ -2.6% (earnings, guidance; announces buyback program and signs agreement with The Wine Group to divest primarily mainstream wine brands and related facilities from its wine and spirits portfolio)

BY Doug Kass · Apr 10, 2025, 9:20 AM EDT

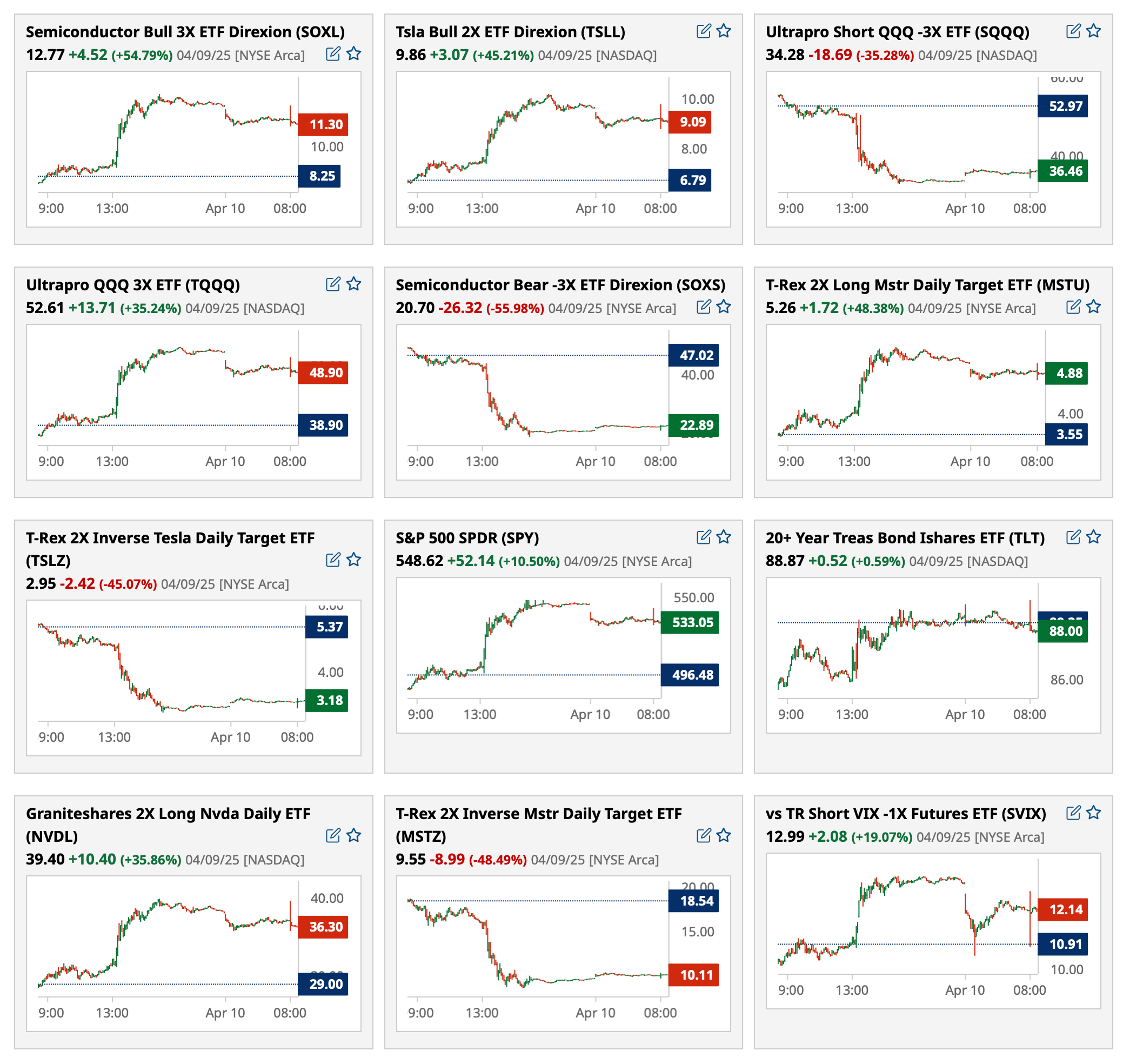

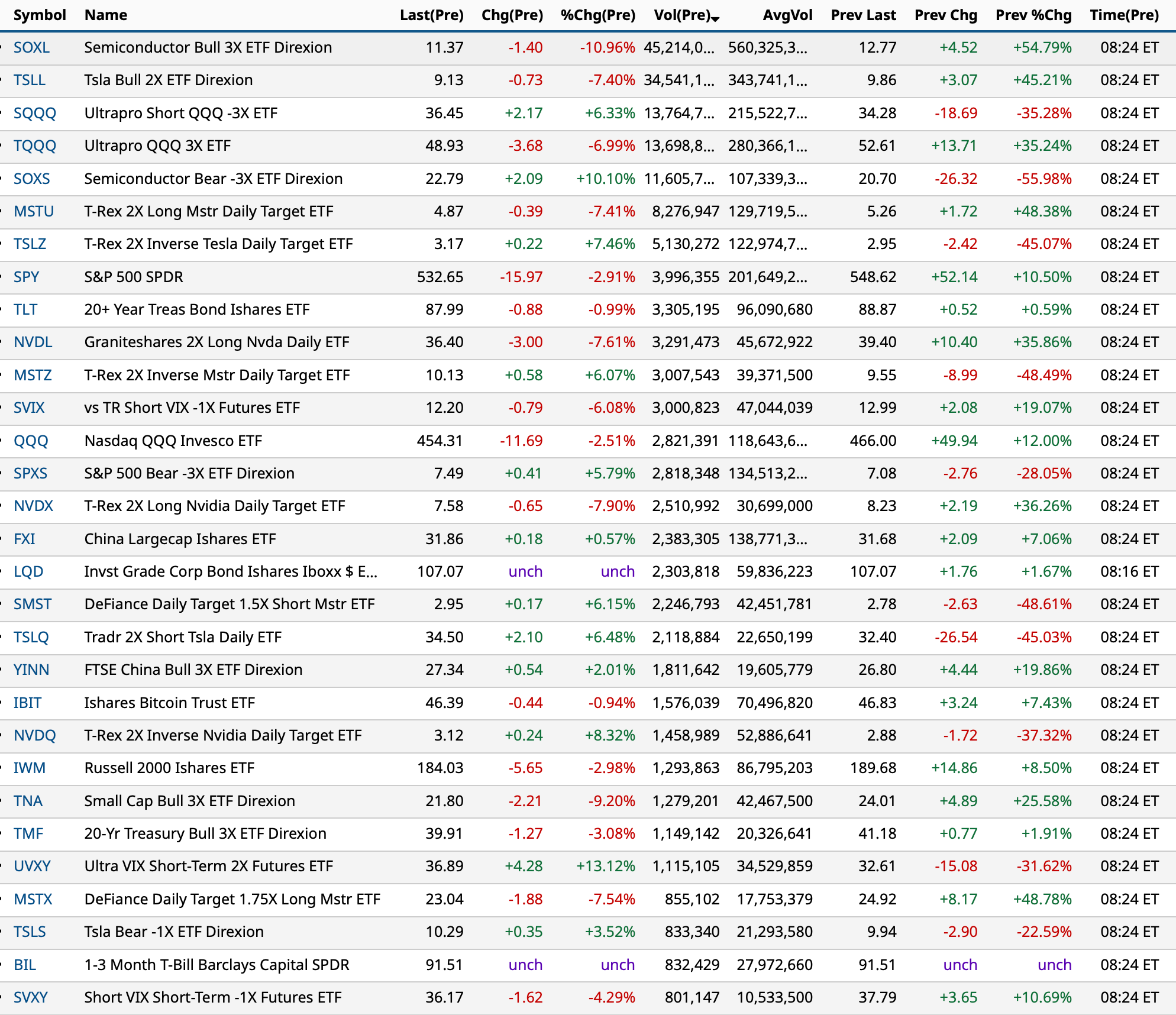

Most active premarket ETFs as of 8:24 a.m. ET:

BY Doug Kass · Apr 10, 2025, 9:10 AM EDT

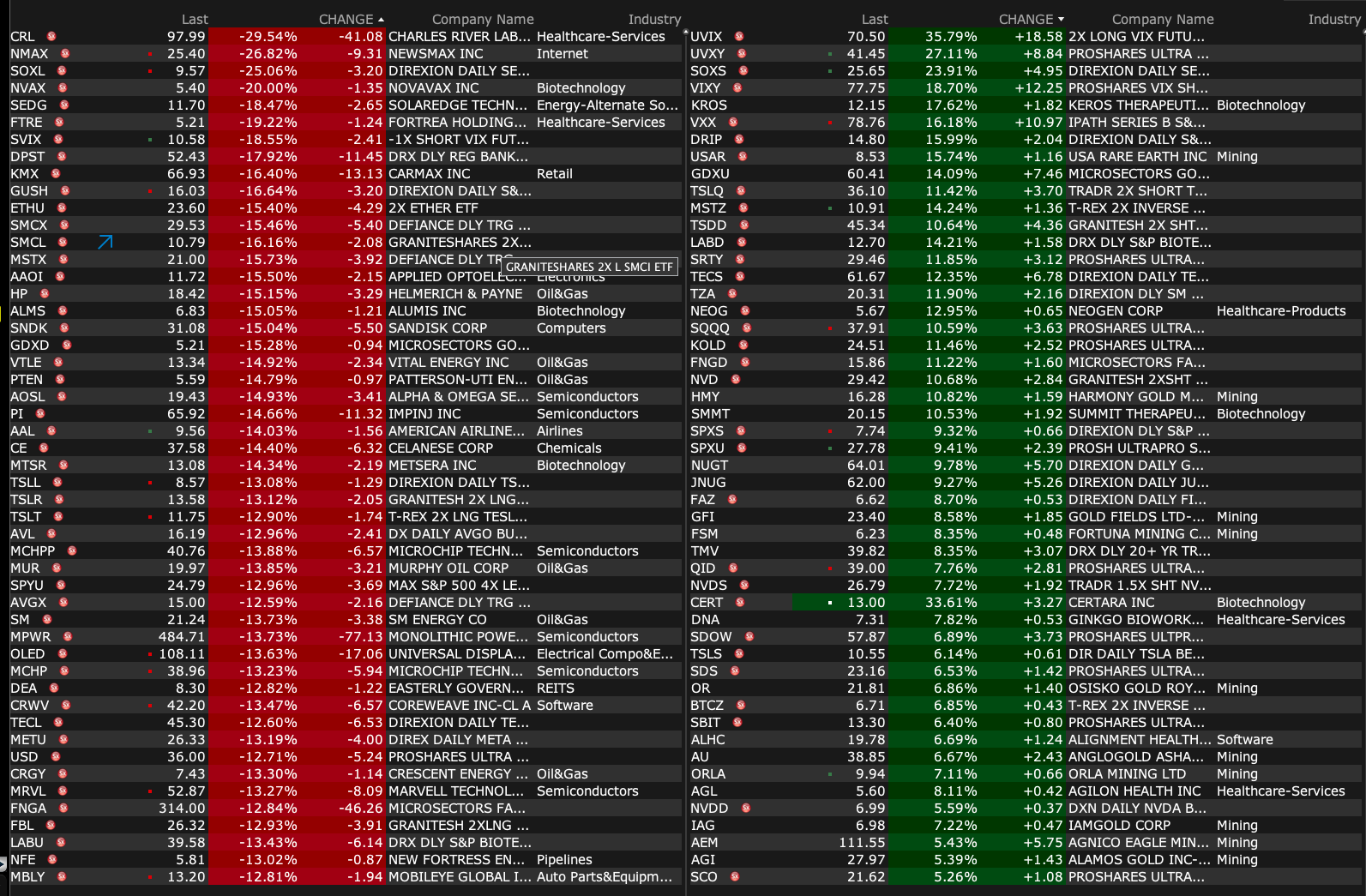

Premarket percentage movers at 8:43 a.m. ET:

BY Doug Kass · Apr 10, 2025, 8:58 AM EDT

BY Doug Kass · Apr 10, 2025, 8:11 AM EDT

8:30AM: Fed Bank of Richmond President Barkin (Non-Voter) speaks on "Driving Through the Economic Fog" and participates in a moderated question-and-answer session before the Talbot County Business Appreciation Summit sponsored by the Talbot County Chamber of Commerce, Easton, MD (No new text. No livestream. No media availability)

9:30AM: Fed Bank of Dallas President Logan (Non-Voter) gives welcome remarks before hybrid Outlook for North American Trade and Immigration event hosted by the Federal Reserve Bank of Dallas, Dallas, TX (Virtual access available)

10:00AM: Fed Board Governor Bowman (Voter) testifies on her nomination for Federal Reserve Vice Chair before the Senate Committee on Banking, Housing, and Urban Affairs, Washington, DC (Text available. Livestream at https://www.banking.senate.gov/)

10:00AM: Fed Bank of Kansas City President Schmid (Voter) speaks on the economic outlook and monetary policy before the Secured Finance Network Independent Finance Roundtable 2025, Kansas City, Mo (Text availability TBD. Audience Q&A expected. No separate media Q&A. Livestream planned)

12:00PM: Fed Bank of Chicago President Goolsbee (Voter) participates in a moderated question-and-answer session before the Economic Club of New York, NYC (Embargoed text TBD. Livestream)

2:00PM: Fed Bank of Philadelphia President Harker (Non-Voter) speaks on "Fintech" before the 2025 Fintech and Financial Institutions Research Conference, Philadelphia, PA (Livestream and advance text available. No Q&A)

4:00PM: Fed Bank of Boston Susan Collins (Voter) delivers the 2025 Razin Economic Policy Lecture hosted by the Georgetown University Center for Economic Research and the Economics Department, Washington, DC (Embargoed text available. Audience Q&A expected. No livestream. No media Q&A)

BY Doug Kass · Apr 10, 2025, 8:00 AM EDT

BY Doug Kass · Apr 10, 2025, 6:15 AM EDT

From Doomberg... As the Pieces Lie - Doomberg

BY Doug Kass · Apr 10, 2025, 6:05 AM EDT

BY Doug Kass · Apr 10, 2025, 5:55 AM EDT

The S&P Short Range Oscillator dropped from a high of -10.72% to -7.93%.

I sold out of all of my index positions (common and calls) yesterday.

BY Doug Kass · Apr 10, 2025, 5:45 AM EDT

One thing a lot of people (including myself) got wrong this week was thinking that Trump would be dug into the plan he revealed last Wednesday. In the end, he just watched Jamie Dimon on Maria Bartiromo's show and checked out the 10-year yield and then changed his mind.