The Outlook Now Could Be Far Different Than Many Expect

After forecasting a rally and even expecting a possible "face ripper" this week the outlook, to me, is likely far different than many expect after today's fireworks.

I will put my words to pen by 6 a.m.

You might be surprised.

Thanks for reading my Diary and enjoy the evening.

In a Fox Business interview, Jamie Dimon reiterates that sticky inflation won't go away as fast as people thought: Probably a recession is likely outcome and has not seen defaults but he is expecting them:

* Current market environment doesn't compare to global financial crisis (GFC); banking system not very leveraged

* Not yet seen defaults, but expecting them; typically doesn't pay attention to anecdotal evidence, but what we're hearing from CEOs is real, they are cutting back and planning for recession

* Fair to say that trade has been unfair especially when it comes to non-tariff barriers (NTBs)

* Reiterates tariffs will raise inflation and lower growth; volatility is serious

* If one want to calm the market, announce some trade deals

* Taking calm approach to markets; could get worse if we don't make progress quickly - Watching closely to see how 10-year Treasury auction goes today

* Seeing a lot of deleveraging from hedge funds and other players in the bond markets

* In bigger picture, any trade deal should bring U.S. closer to allies to offset alliance between Russia and China

* We can bring manufacturing back to U.S., using land grants and specifics for pharmaceutical and defense

* Have put some headcount controls in place, but not forcing cuts; this isn't because company isn't doing well, it's to avoid complacency

* Trade is extremely complicated; the sooner the better we get to some deals

* We've already lost a couple of bond deals to overseas following the U.S. tariffs

* Believes we could be growing at 3% per year if we could get our own house in order; We should be striving for that

Can this really be happening?/One business of many on the brink if tariff rates don't drop/Delta on travel

China is not backing down as they just hiked their tariff on US goods to 84%. This is getting so ridiculous that it's hard to believe it's actually happening between the two largest economies that make up almost $50 Trillion of global GDP, almost half of the world, let alone a tariff war against the whole world.

If you have any idea as to what a 'China deal' would look like, please let me know because I have no idea. Will it be just a repeat of the 2018 deal where China might buy more soybeans and/or LNG? All I know is the deals that will have to be had as each day nothing gets done is the bailout, AGAIN, of American farmers and all the small businesses who don't have the ability nor the agility in shifting supply chains away from China anytime soon. Ask anyone who procures product from China supply chains and I'd argue that most would say it is the most efficient, productive, reliable source of what they need.

Tainting our global brand is becoming more apparent in the weaker US dollar, except vs the yuan, and the drastic selloff again in US Treasuries. Yes, some of the Treasury selloff I'm sure is further unwind of the hedge fund basis trade (which was long Treasuries and short futures and which I saw yesterday that Torsten Slok estimated the trade to be as large as $800b) but watching interest rates go higher and the US dollar lower at the same time is the historical financial reaction seen in 3rd world countries.

When I saw last Thursday night's lawsuit against Trump to stop his use of the International Emergency Economic Powers Act of 1977, I was hopeful there would be a lot more of these which result in some court putting a stop to this. What I read from a Bloomberg News story yesterday instead was very disconcerting. The article was titled, "Top US Retailers Balked at Challenging Trump Tariffs in Court."

Deborah White, general counsel for the Retail Industry Leaders Association said that 'those efforts had been put on hold' as she said "given the current climate, the members of our groups were unwilling to proceed despite the heightened economic uncertainty caused by the various shifting EO's and pronouncements." Keep in mind that members of this group include big retail hitters like Home Depot, AutoZone, Target, Best Buy and others.

What was really alarming was this, "White said more than 30 other groups RILA contacted had also balked at suing over the tariffs. As of Tuesday afternoon, no industry group has filed a legal challenge." The article did cite the New Civil Liberties Alliance suit from last Thursday but another reason why more suits aren't being filed, the article said "In her email, White also noted the potential challenge of finding law firms willing to bring suits over tariffs in light of Trump's attacks on some of the biggest names in the legal profession." She said "Given the multiple EO's that have been lodged at law firms, it's not clear which firms would be willing to do so," she said. That is scary I have to say.

Finally, "White expressed hope that 'another plaintiff might pick up the mantle,' allowing RILA members to 'observe from a distance.' " Anyone, anyone? https://www.bloomberg.com/news/articles/2025-04-08/top-us-retailers-balked-at-challenging-trump-tariffs-in-court

With respect to small businesses and the crisis that has been created, here was an anecdote from Reuters yesterday in an article titled "Clothing retailers delay orders, freeze hiring as tariffs hit." It said "These businesses, much like Nike and Lululemon, face an impossible choice: offset the cost of tariffs by raising prices by some 40% - potentially cratering sales - or absorb the cost increase and further strain already - thin profit margins. Unlike their bigger rivals, however, the smaller clothing and shoemakers lack vast supply chains, making them highly dependent on Vietnam and China."

They cite a particular business, Day Owl, a 6 yr old NY based company that makes backpacks in Vietnam. They have paused orders. The CEO Ian Rosenberger said, "Unless there's a deal to significantly lower Vietnamese tariffs," he "estimates Day Owl has 30 days before it folds. But with a production cycle of about 100 days, waiting much longer risks missing the crucial back-to-school shopping season." Rosenberger said, "The damage is already significant enough to be an existential threat," and adding that 'his seven employees have been asking if they should prepare to be out of a job.'

What's the price impact?, "Rosenberger said tariffs would increase his duty to $22 from $5, prompting him to increase the price of his top-end bag to $212 from $155." I'll add this, multiply this situation countless times around the country and what many small businesses are facing all because of the flawed, nonsensical economic belief that a trade deficit is inherently bad.

I want to mention the Fed again here and what their possible response can be because it is not a free lunch if they start cutting, though each day that goes by with this they might have to bail out something in the financial system. For this, I'll focus on one thing though, the impact on the upper income household. As they own most of the stocks, they are losing a lot of money but if the Fed starts to cut rates, they will start losing interest income too and if stocks don't rally in response to those cuts, it will be a double whammy. Something to keep in mind as again I'll say that this cohort has helped tremendously in carrying the growth of the US economy over the past few years.

This is what Delta said in their earnings release today:

"With broad economic uncertainty around global trade, growth has largely stalled. In this slower-growth environment, we are protecting margins and cash flow by focusing on what we can control. This includes reducing planned capacity growth in the 2nd half of the year to flat over last year while actively managing costs and capital expenditures."

Also, "Given the lack of economic clarity, it is premature at this time to provide an updated full-year outlook."

The Reserve Bank of New Zealand cut its official cash rate by 25 bps as expected to 3.50% and the Reserve Bank of India did too by 25 bps to 6%.

Long rates though in New Zealand skyrocketed by 21 bps, seemingly what we're seeing in the US. They jumped 15 bps in Australia.

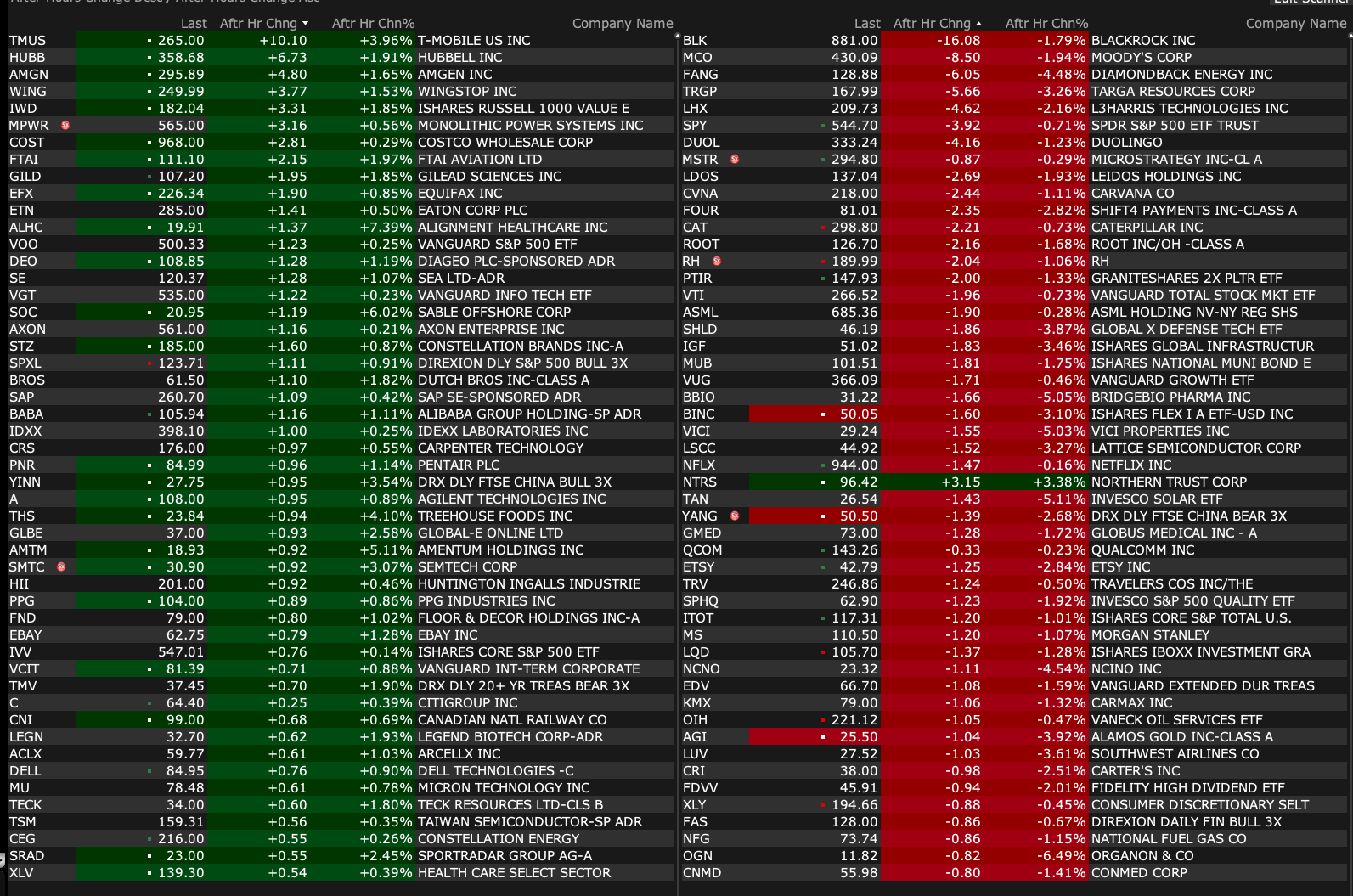

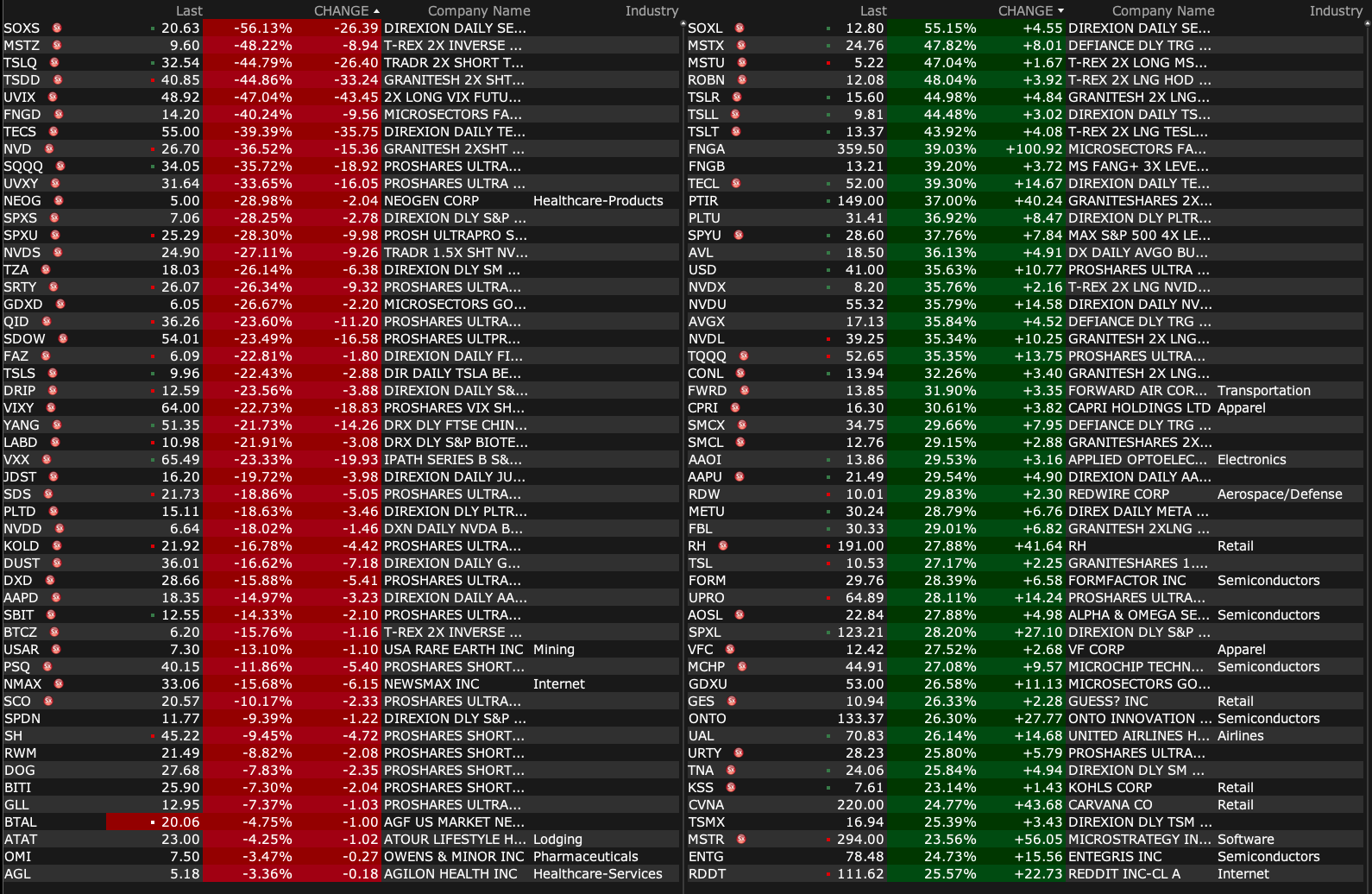

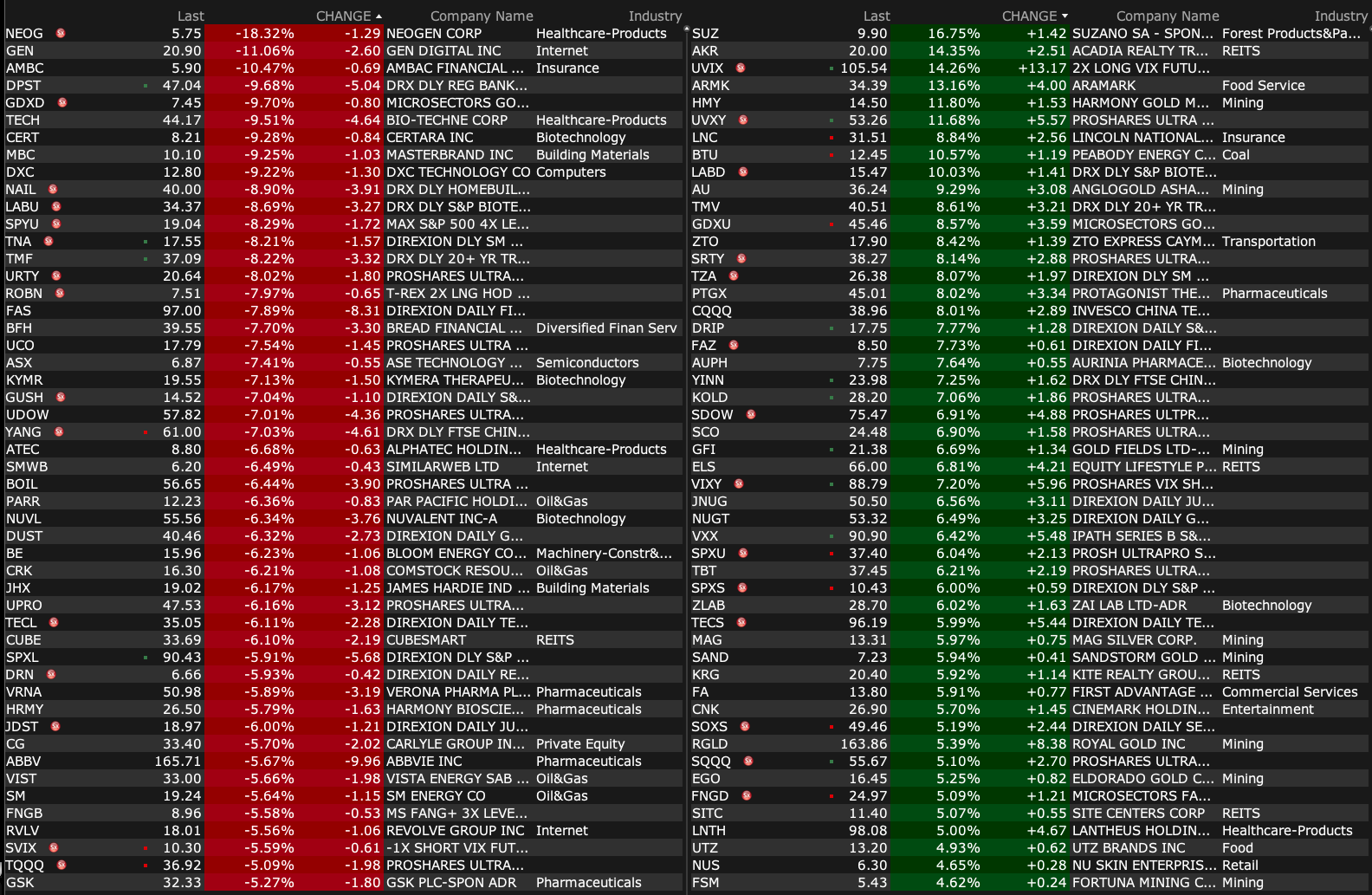

-BTU +13% (bullish Trump Administration commentary on coal)

-LNC +11% (Bain Capital to acquire a 9.9% ownership stake in Lincoln for aggregate consideration of $825M)

-CING +9.1% (receives $3M grant from private foundation to accelerate development of anxiety asset CTx-2103)

-MBOT +7.9% (releases results from pivotal clinical trial, achieving 100% Robotic Navigation Success for the LIBERTY Endovascular Robotic System)

-GRCE +5.4% (announces alignment with the FDA supporting the planned NDA Submission for GTx-104NDA Submission anticipated Q2 Calendar 2025)

-AEHR +4.7% (earnings; withdraws guidance due to tariff uncertainty)

-EU +4.2% (divests New Mexico assets to Verdera Energy Corp)

Downside:

-VINC -51% (announces Termination of Letter of Intent and Board Authorization to pursue wind-down activities)

-CALM -5.0% (earnings, buyback announcement; reaches Definitive Agreement to acquire ready-to-eat egg product and breakfast food company Echo Lake Foods, Inc. for $258M cash)

-AMGN -4.5% (weakness following Trump announcement that pharma tariffs are coming shortly)

-PFE -4.5% (weakness following Trump announcement that pharma tariffs are coming shortly)

-LLY -3.8% (weakness following Trump announcement that pharma tariffs are coming shortly)

-F -2.7% (hearing Bernstein SocGen Group Cuts F to Underperform from Market Perform, price target: $7)

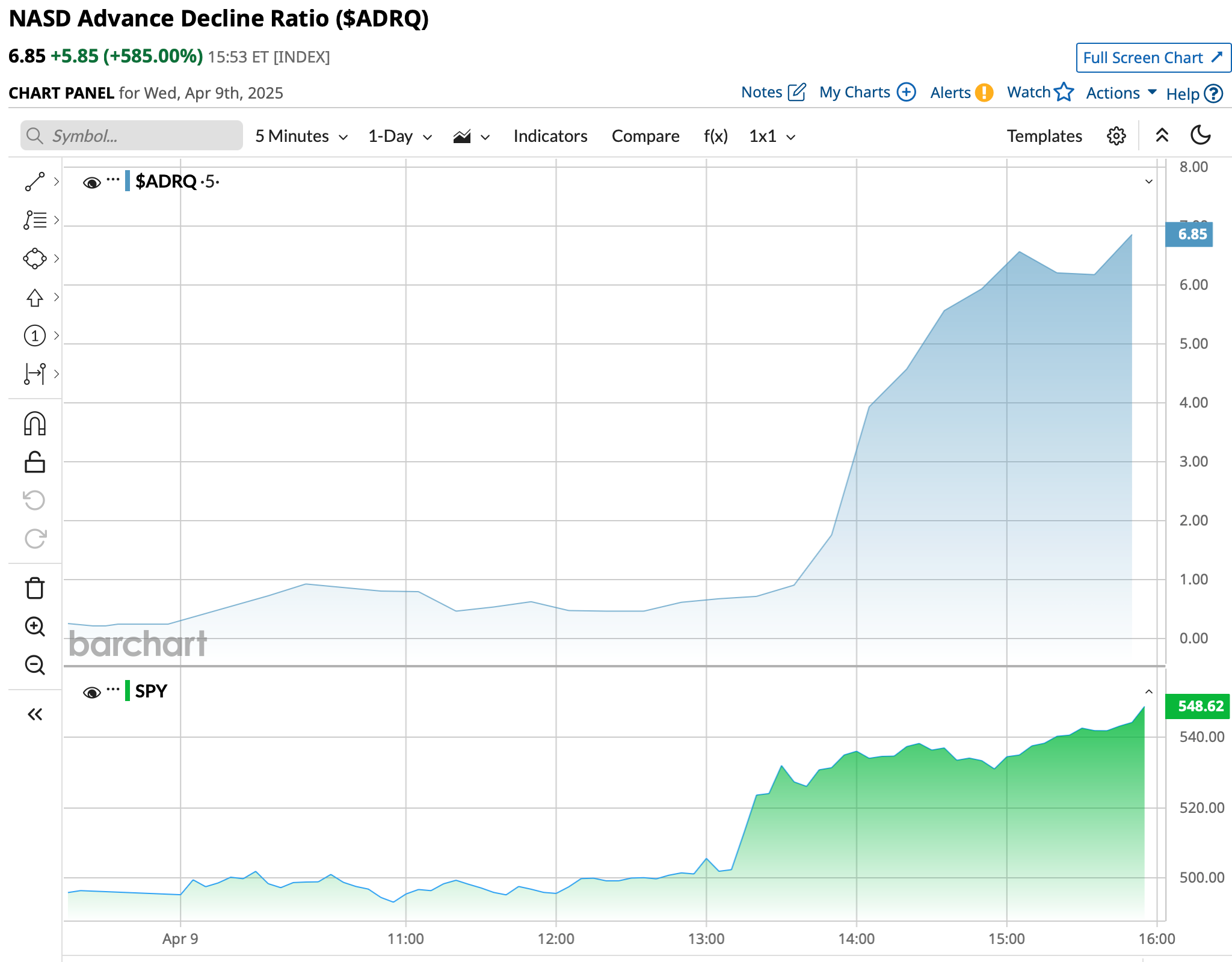

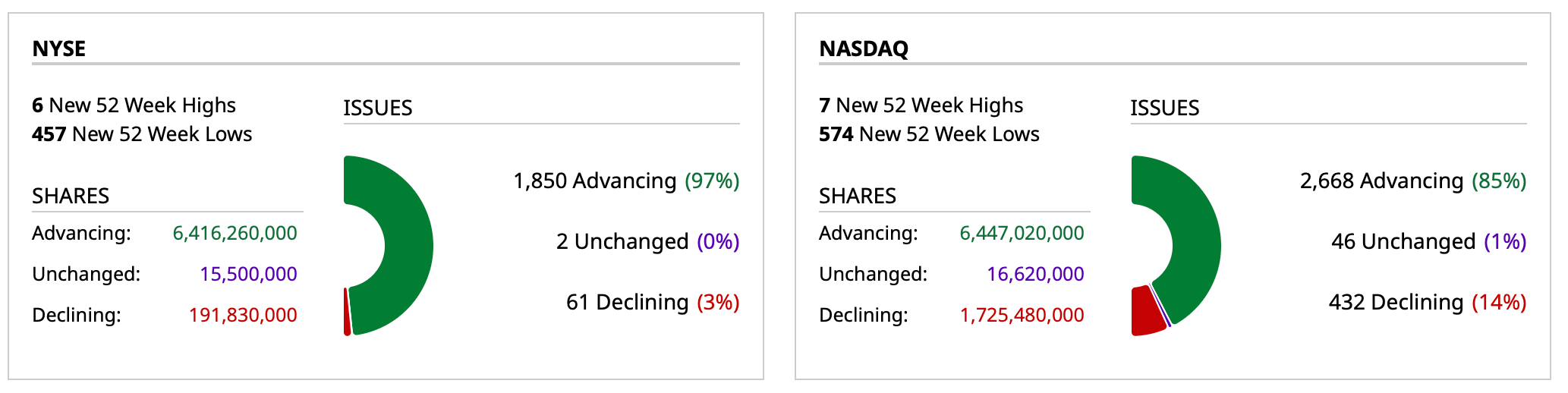

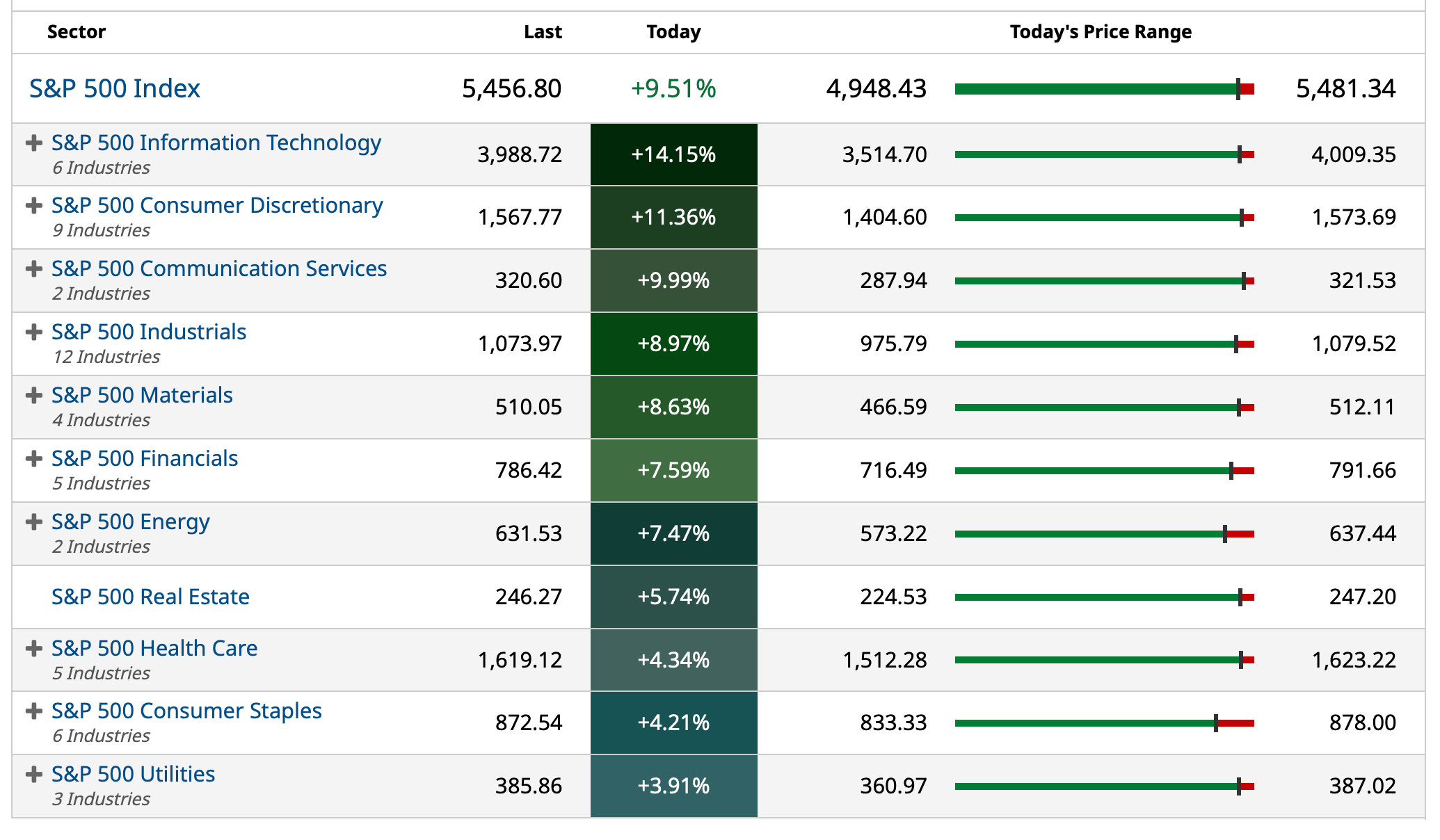

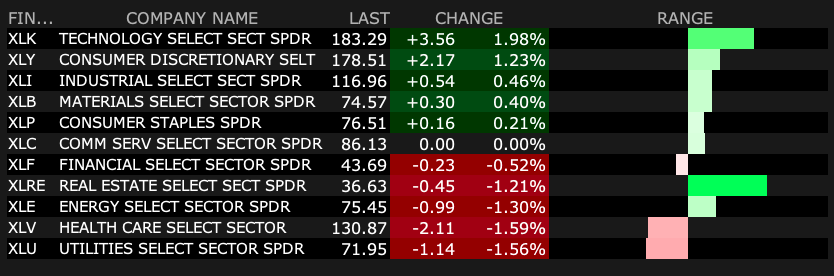

* President Trump, stocks and bonds melted down last night but have rallied in recent hours...

I have warned about market structure for over twelve months.

I have also warned about a clueless Trump administration — an administration that improvises and rarely analyzes (and that fails to "game out" scenarios) — that has no concept or idea what knock-on effects of policy are.

It is an administration that is off the rails and our capital markets are now paying the price for the trade uncertainties associated with an extreme tariff policy.

NAFTA, which established a free-trade zone among only three countries (Canada, Mexico, and the United States), aiming to eliminate tariffs and other trade barriers, and was later replaced by the USMCA, took nearly two years to finalize.

What happens when fifty plus countries try to resolve tariff disputes with our country when the administration has no real stated plan?

Today, despite his protestations, Trump appears to have no real integrated tariff plan — he is shooting from the hip and risking global economic panic:

At least to this observer (I am not being political, I am being observational), it is more than concerning that policy is being guided by our president.

Here are some excerpts of a Trump speech last night — not only is it uninspiring but it hysterical, emotional and full of falsehoods:

Back to my market structure concerns, which have now been realized.

Leveraged risk parity and other volatility control funds have been aggressively selling BOTH equities and bonds in the last few weeks.

Unlike during The Great Decession (2007-09) and during Covid, as stocks have cratered so have bonds as economic growth, massive deficit spending, the U.S. debt load and the sharp and quick drop in stocks have resulted in forced selling of bonds and the return of the bond vigilantes:

Perhaps equally important is the fear that the seizing up of trade means that foreigners will not be as supportive of our Treasury market - a knock-off impact of the administration's not thoughtful and ignorant trade policy. After all who needs to hold onto U.S. dollars and Treasuries if you are not trading with the U.S.?

During The Great Decession and as Covid spread, equities fell by a negative wealth effect of between five and ten billion dollars in each event. But on those two occasions, more than half of that lost value was made up by higher bond prices.

Not so in 2025 — as correlations, because of many reasons mentioned here, have broken down (with regard to fixed income, currency and equities).

Investors are now selling what they can — and the bond market is liquid. This is something Gundlach warned about on CNBC on Monday.

With equities -20% or so year to date, there has been no offset in portfolios from an appreciation in bond prices —they, too are down, year to date.

I watched my screen most of the night.

Bond prices cratered (at one point TLT was -$3) and bond yields leaped by 30 basis points (now up by only six basis points in yield):

The longer the uncertainty continues on trade policy, the more consequential will be the damage done to our markets and global economic health (from an intermediate-term standpoint).

The pity is that this all was self-manufactured and should never have happened.

A feckless and fatuous Trump administration has shot itself in the foot and our capital markets and the global economy has been hospitalized.