From Peter Boockvar:

Positives

1) The market is closed for the next two days.

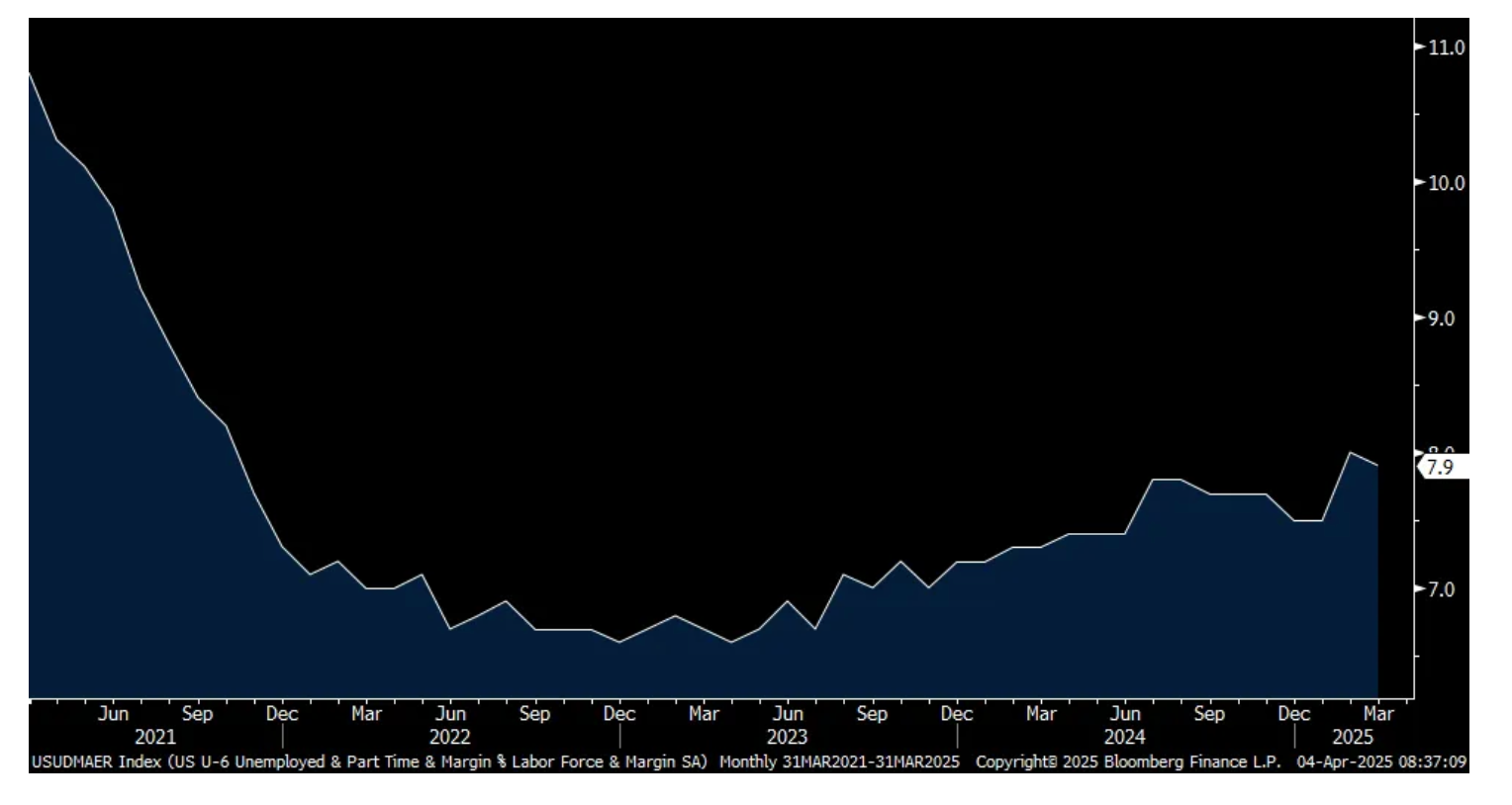

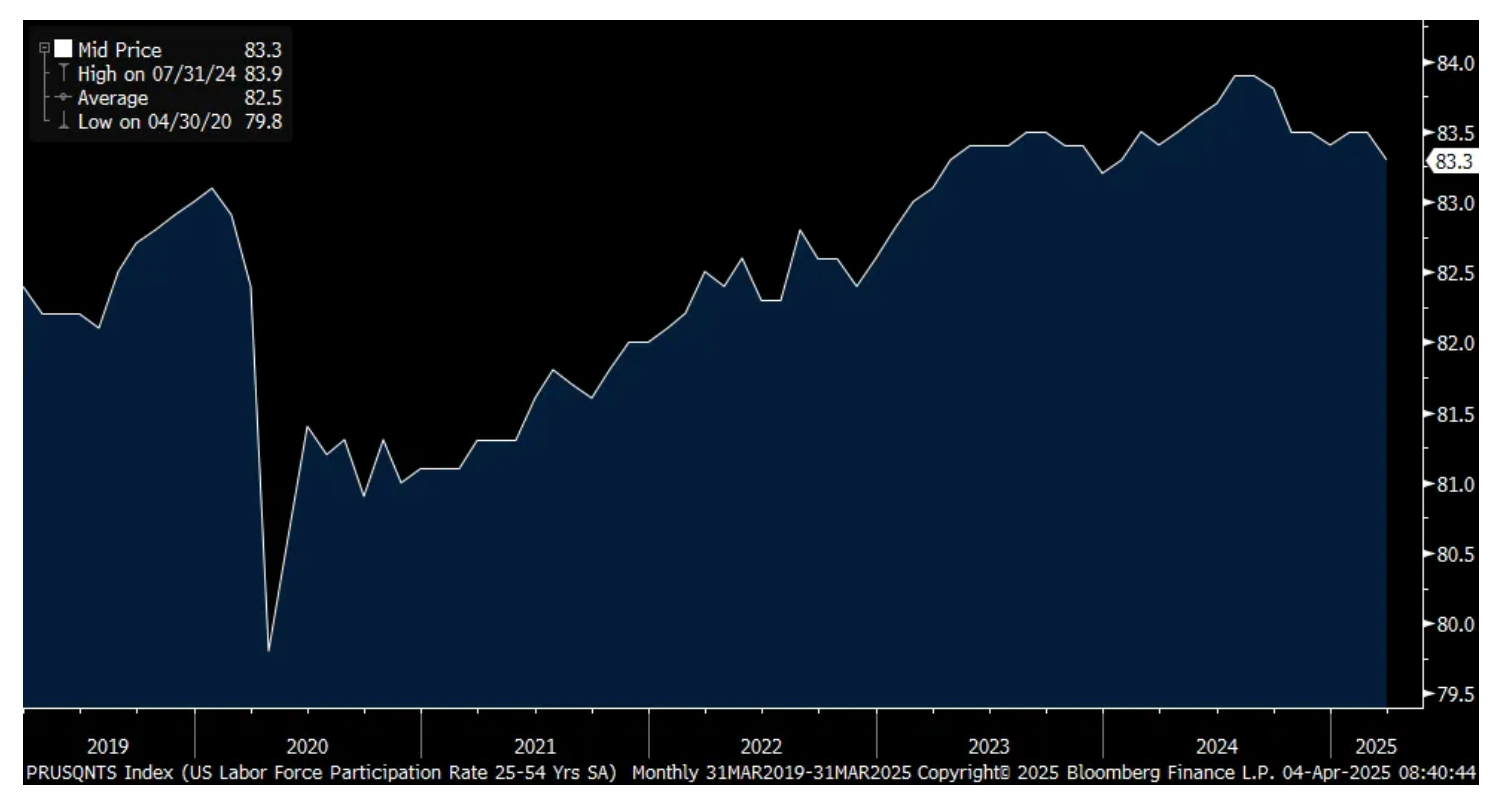

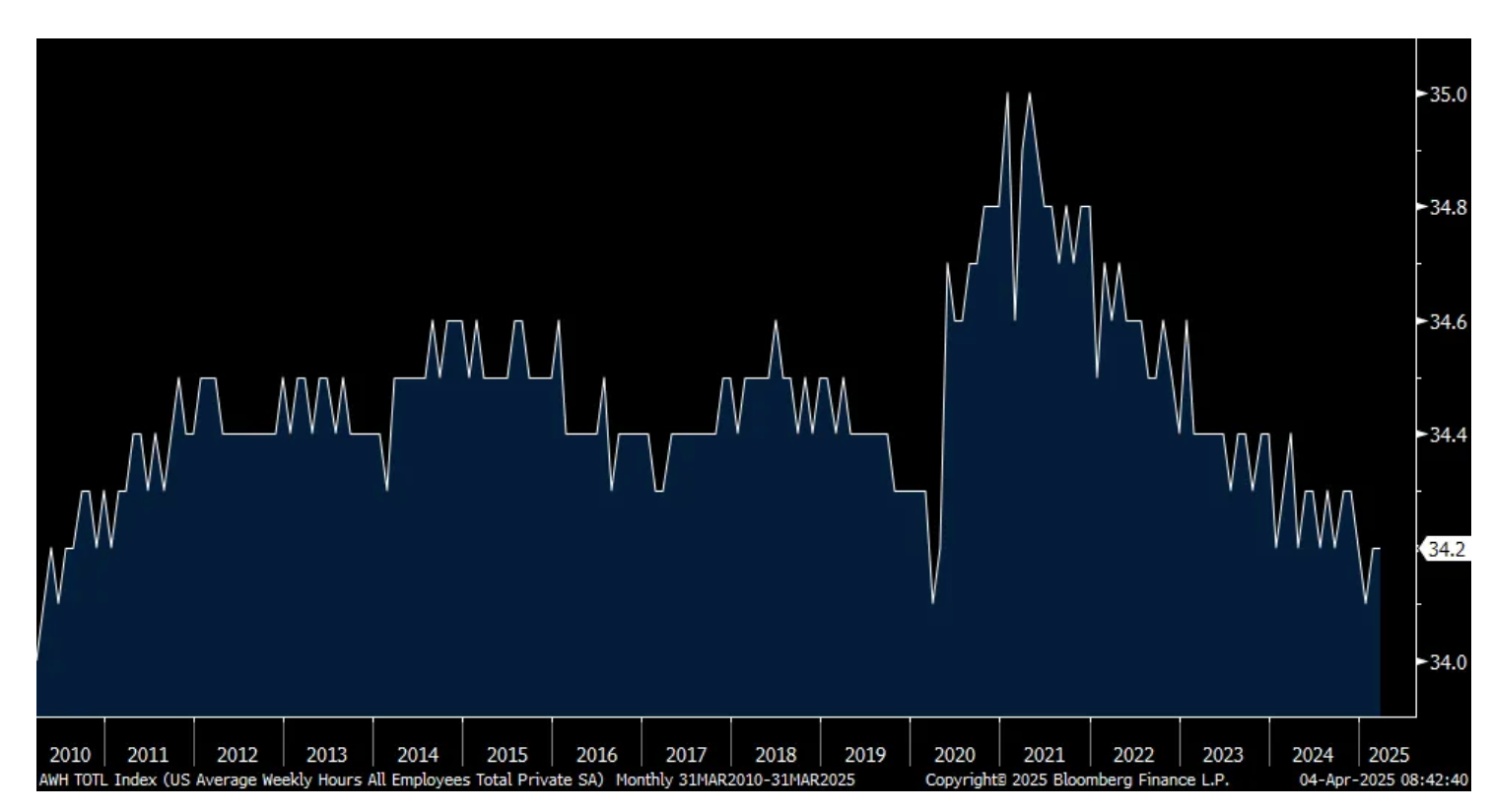

2) In the last jobs report before the global trade earthquake of April 2nd saw 228k net jobs added in March, well above the estimate of 140k with about half of that offset by a downward revision of 48k combined in the prior two months. The household survey saw a job gain of 201k which because it was just below the 232k person rise in the size of the labor force, the unemployment rate ticked up by one tenth to 4.2%. The all in U6 rate which jumped by 50 bps to 8% in February to a multi year high fell one tenth to 7.9%. The participation rate rose one tenth to 62.5% after falling by two tenths last month. The key 25-54 yr olds though saw a drop of two tenths to 83.3% which is the lowest since December 2023. Hours worked was 34.2 for a 2nd month after touching 34.1 in January which was the lowest since 2010 not including Covid. Average hourly earnings were up by .3% m/o/m as expected though the prior month was revised down by one tenth and was up by 3.8% y/o/y. Combining hours worked and hourly wages puts the weekly earnings up by .3% m/o/m after a 5 tenths gain last month and higher by 3.2% y/o/y.

3) Initial jobless claims fell to 219k from 225k and 6k below expectations.

4) The average 30 yr mortgage rate was 6.70% for the week ended 3/28, little changed w/o/w. Purchases lifted by 1.5%.

5) Reflecting the desire to buy a new car now so as to avoid the inevitable price increase, vehicle sales in March jumped to 17.77mm at a seasonally adjusted annualized rate. That was well above the estimate of 16.2mm, vs 15.49mm in March 2024 and vs 17.5mm in March 2019. We’ll of course have a hangover in the coming months.

6) From PVH: "In a challenging macro, we delivered another year of strong profitability in North America, drove sequential improvements in our wholesale order books in Europe while improving our quality of sales, and we achieved our third consecutive year of growth in Asia Pacific, on a constant currency basis."

7) China's March manufacturing Caixin index rose to 51.2 vs 50.8. They said "Manufacturers saw their promotional efforts pay off as the market improved. In March, output grew for the 17th straight month and at the fastest pace in four months, while the subindex for total new orders stayed in expansionary territory for the 6th straight month. The overseas demand growth momentum recorded in February was extended, with the indicator for new export orders rising to the highest point since last April." Also, "Businesses remained optimistic. The majority of surveyed companies expressed confidence in the near term economic outlook, although some remained cautious over a potential escalation in global trade tensions."

8) The March China Caixin services index rose to 51.9 from 51.4 and above the estimate of 51.5. On the outlook from here, "Market optimism was maintained. The indicator for expectations of future activity measured lower than February but remained in expansionary territory. Service providers were hopeful about future policy support at home. However, some expressed concerns over a potentially deteriorating global trade environment."

9) China's economy improved very slightly in March if looking at the state sector focused PMI data. The manufacturing index was 50.5, up from 50.2 and while barely above 50, that is the best read in a year. The non-manufacturing component which includes both services and construction was up .4 pts m/o/m to 50.8. That's the highest since last May.

10) Vietnam’s March PMI rose to 50.5 from 49.2. Australia’s was up to 52.1 from 50.4.

11) The March Eurozone manufacturing final PMI was tweaked to 48.6 from 48.7 initially but up 1 pt from February and the highest level since January 2023.

12) March CPI in the Eurozone rose 2.2% y/o/y as expected and vs 2.3% in February. The core rate was higher by 2.4% vs 2.6% in the month before and one tenth below expectations. This is all before the fiscal spending is about to ramp up in Europe, particularly on defense but also infrastructure in Germany. Services inflation continues to be the main driver of inflation, higher by 3.4% y/o/y while non-energy industrial goods prices were up just .6%.

13) German February retail sales rose by .8% m/o/m vs the estimate of no change. Food, non-food and online retail all drove the increase after a .7% increase in January which was revised up by 5 tenths.

14) The Reserve Bank of Australia kept its policy rate unchanged at 4.10% as expected. The usually hawkish Governor Michele Bullock did not lean in any one direction.

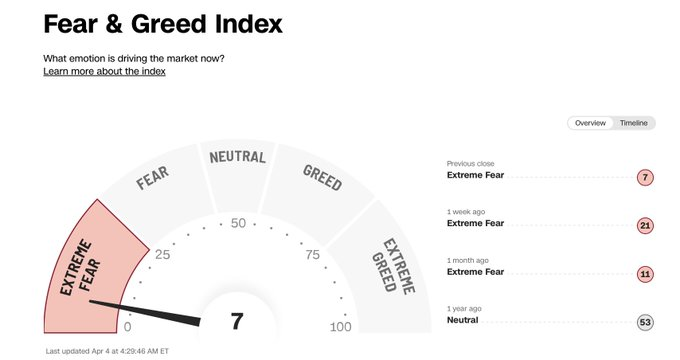

15) From a contrarian standpoint, the CNN Fear/Greed index is down to just 4 and ranges from 0-100.

Negatives

1) With the opportunity for a legitimate attempt to convince foreign countries to lower their tariffs in line with what we have on them, so called reciprocity and a benefit to the whole world, we instead get 5th grade math in a formula that results in insane levels of tariffs on all of our trading partners. It begs the following questions, Do we really want to lower global tariff rates? Do we instead want to have high ones as to encourage production back home (though who knows if it comes and some will move overseas) ? Do we want to raise a lot of money via higher tariffs or do we want lower ones instead in the aggregate in order to achieve fairness?

2) We’ve seen a large amount of wealth destruction in just two days and multiple IPOs canceled. Any help with tariffs from a stronger US dollar has slipped away too, for now.

3) Continuing claims rose back above 1.9mm at 1.903mm, up from 1.847mm.

4) Job openings in February, thus dated data, totaled 7.568mm. That’s 90k below expectations and down from 7.762mm in January. The hiring rate held at 3.4% for a 3rd month and the quit rate was unchanged at 2%. The DOGE cuts are slightly reflected here as there are 138,000 federal government job openings vs 132k in January and 138k in December. In October it was 142,000.

5) The March ISM services index fell to 50.8 from 53.5. In terms of industry breadth, 10 saw growth vs 14 in February. The bottom line from the ISM, “There has been a significant increase this month in the number of respondents reporting cost increases due to tariff activity. Despite an increase in comments on tariff impacts and continuing concerns over potential tariffs and declining governmental spending, there was a close balance in near-term sentiment, between panelists with good outlooks and those seeing or expecting declines.”

6) The March ISM manufacturing index fell back under 50 to 49 after two months above and just below the estimate of 49.5. Overall breadth softened a touch with 9 industries seeing growth vs 10 last month. Those seeing a contraction totaled 7 vs 5 in the month before. One saw no change.

7) Refi's fell by 5.6%, and down for a 3rd week.

8) From MSC Industrial: "there remains hesitancy and caution among our customer base around future production levels due to tariff uncertainty, potentially looming inflation, and sustained high interest rates…in pricing, we've taken select tariff related price increases in late March and will continually evaluate additional moves as warranted."

9) From RH: "While we expect a higher risk business environment this year due to the uncertainty caused by tariffs, market volatility, and inflation risk, we believe it's important to separate the signal from the noise. The fact is, we've been operating in the worst housing market in almost 50 years. For context, in 1978, there were 4.09 million existing homes sold when the US had a population of 223 million. Contrast that to 2024, where 4.06 million existing homes sold with a population of 341 million, and it illuminates just how depressed the housing market has been this past year.”

10) Some manufacturing PMI’s: Taiwan 49.8 vs 51.5, South Korea 49.1 vs 49.9, Thailand 49.9 vs 50.6, and Japan 48.4 vs 49.

11) The UK March manufacturing index was revised to a still weak 44.9 from 46.9 in February.