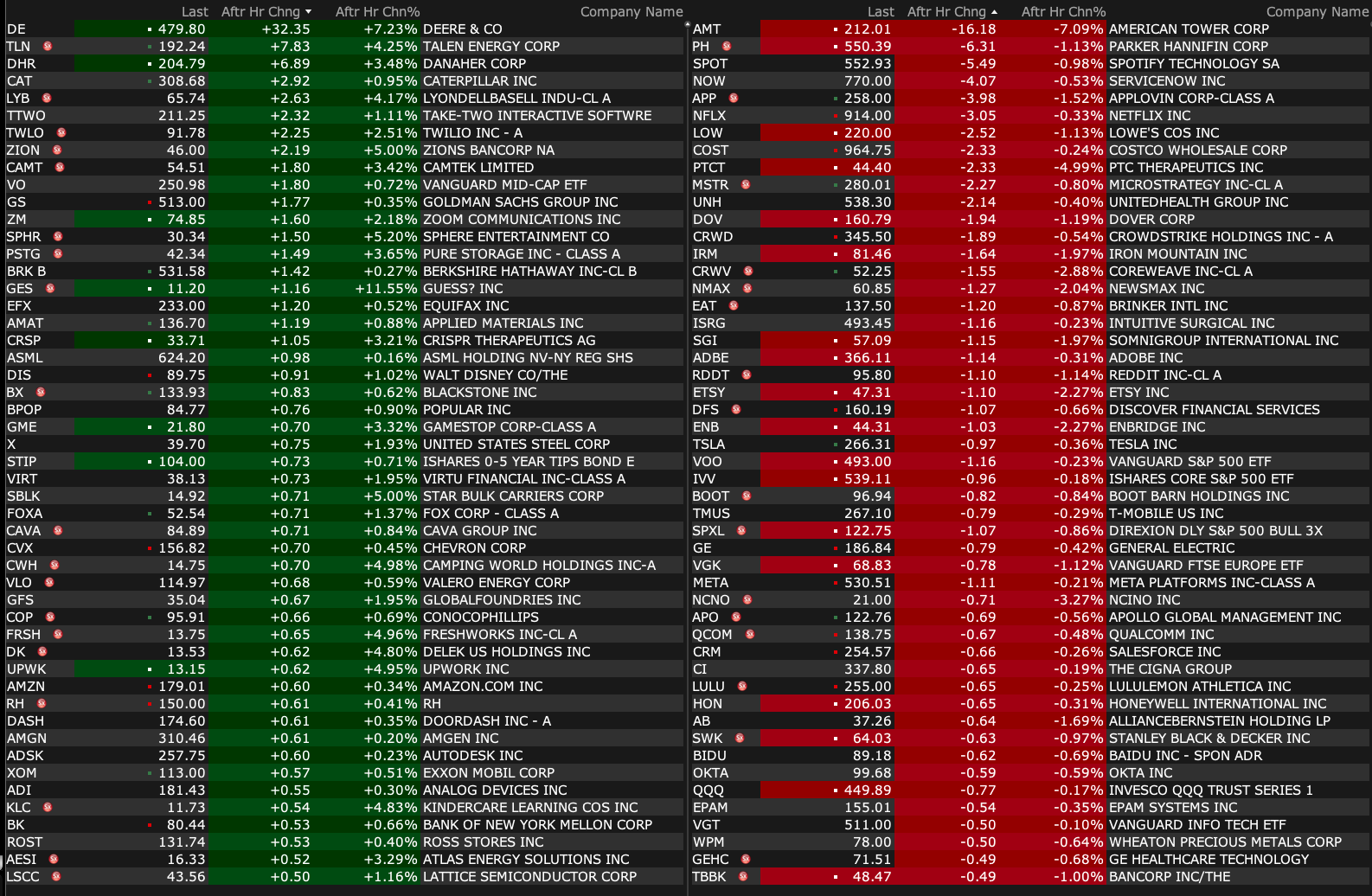

Thursday's After-Market Movers

As of 4:25 p.m.:

BY Doug Kass · Apr 3, 2025, 4:55 PM EDT

As of 4:25 p.m.:

BY Doug Kass · Apr 3, 2025, 4:55 PM EDT

- NYSE volume 55% above its one-month average

- NASDAQ volume 25% above its one-month average

- VIX index: up 37.47% to 29.57

BY Doug Kass · Apr 3, 2025, 4:41 PM EDT

S&P cash is now at 5400, which is my approximate "fair market value" that I have held for some time.

BY Doug Kass · Apr 3, 2025, 3:58 PM EDT

Here are some of today's "Things":

* Indices: I added to SPY at $545.89 and QQQ at $458.09.

* Financials: I added to APO at $124.03, AXP at $252.63, BAC at $39.60, BX at $133.99, C at $67.634, MS at $110.23 and WFC at $68.28.

* Technology: I added to AMZN at $184.79, MSFT at $373.58, GOOGL at $152.70 and META at $553.45

* New long: Purchased SBUX at $88.87.

* I shorted KO at $73.36.

BY Doug Kass · Apr 3, 2025, 3:22 PM EDT

Wolf Street howls about drunken sailors.

BY Doug Kass · Apr 3, 2025, 2:59 PM EDT

BY Doug Kass · Apr 3, 2025, 2:50 PM EDT

Back in the saddle.

BY Doug Kass · Apr 3, 2025, 2:45 PM EDT

I have a lunch board meeting and will out between noon and 2 p.m.

BY Doug Kass · Apr 3, 2025, 12:00 PM EDT

- NYSE volume is 57% above its one-month average;

- Nasdaq volume is 29% above its one-month average;

- VIX index is up 26.41% to 27.19

BY Doug Kass · Apr 3, 2025, 11:45 AM EDT

Morgan Stanley MS price target lowered to $125 from $129 at JPMorgan JPMorgan lowered the firm's price target on Morgan Stanley to $125 from $129 and keeps a Neutral rating on the shares. The firm adjusted forecasts to mark-to-market for quarter-end and reduced investment bank fee forecasts.

Goldman Sachs GS price target lowered to $614 from $625 at JPMorgan JPMorgan analyst Kian Abouhossein lowered the firm's price target on Goldman Sachs to $614 from $625 and keeps an Overweight rating on the shares. The firm adjusted forecasts to mark-to-market for quarter-end and reduced investment bank fee forecasts.

Wells Fargo WFC price target lowered to $73.50 from $82 at JPMorgan JPMorgan lowered the firm's price target on Wells Fargo to $73.50 from $82 and keeps a Neutral rating on the shares as part of a Q1 earnings preview for the large-cap banks. The firm expects the tariffs announcement will increase concerns about the impact on the economy and pressure markets overall. Banks would be impacted with a fallout on investment banking, consumer spending, and loan growth plus wealth management, the analyst tells investors in a research note. JPMorgan points out consumer spending started to slow in Q1, which would impact economic growth, and inflation could rise with tariffs. It cut estimates, noting there is potential for further cuts based on the full impact of tariffs.

Citi C price target lowered to $75.50 from $85.50 at JPMorgan JPMorgan lowered the firm's price target on Citi to $75.50 from $85.50 and keeps a Neutral rating on the shares as part of a Q1 earnings preview for the large-cap banks. The firm expects the tariffs announcement will increase concerns about the impact on the economy and pressure markets overall. Banks would be impacted with a fallout on investment banking, consumer spending, and loan growth plus wealth management, the analyst tells investors in a research note. JPMorgan points out consumer spending started to slow in Q1, which would impact economic growth, and inflation could rise with tariffs. It cut estimates, noting there is potential for further cuts based on the full impact of tariffs.

Bank of America BAC price target lowered to $43.50 from $49.50 at JPMorgan JPMorgan lowered the firm's price target on Bank of America to $43.50 from $49.50 and keeps an Overweight rating on the shares as part of a Q1 earnings preview for the large-cap banks. The firm expects the tariffs announcement will increase concerns about the impact on the economy and pressure markets overall. Banks would be impacted with a fallout on investment banking, consumer spending, and loan growth plus wealth management, the analyst tells investors in a research note. JPMorgan points out consumer spending started to slow in Q1, which would impact economic growth, and inflation could rise with tariffs. It cut estimates, noting there is potential for further cuts based on the full impact of tariffs.

BY Doug Kass · Apr 3, 2025, 11:30 AM EDT

New position: Long SBUX $88.90 (-$10)

BY Doug Kass · Apr 3, 2025, 11:02 AM EDT

I covered more BOOT short at $93.20 (-$21 on the day).

BY Doug Kass · Apr 3, 2025, 11:00 AM EDT

BY Doug Kass · Apr 3, 2025, 11:00 AM EDT

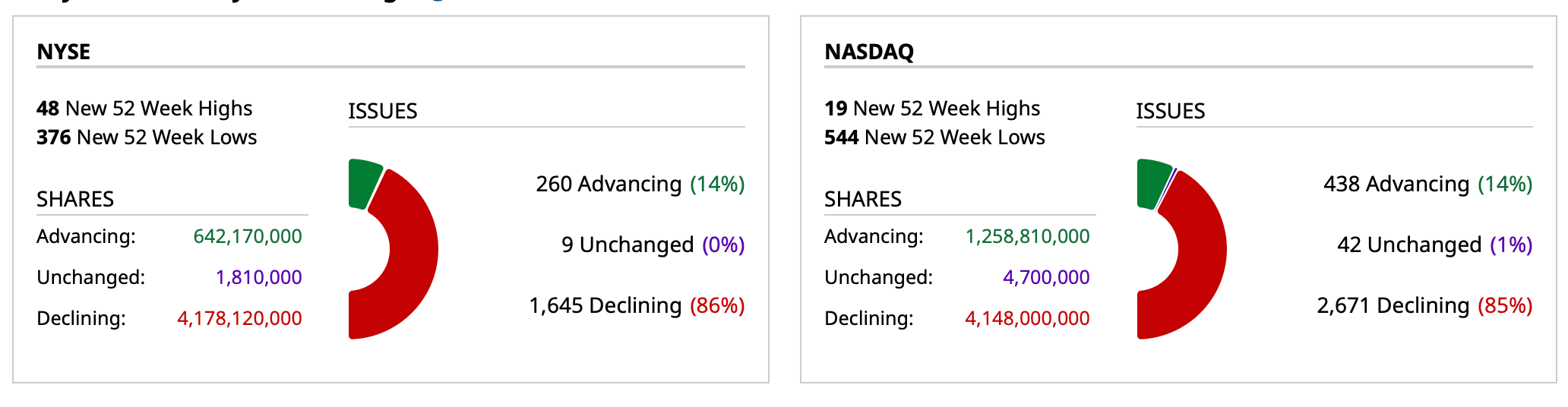

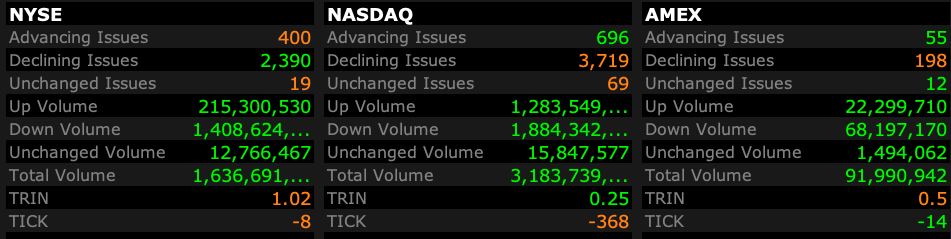

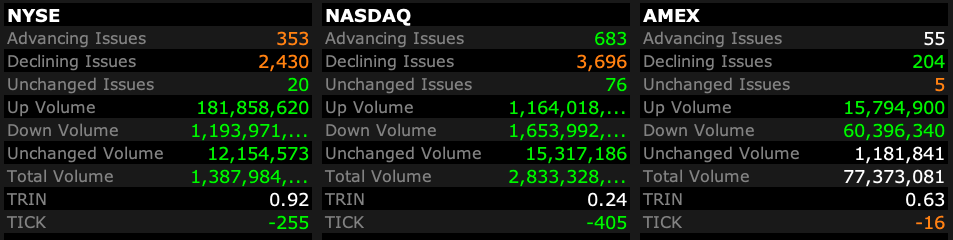

Breadth at 10:24 a.m. ET:

BY Doug Kass · Apr 3, 2025, 10:40 AM EDT

BY Doug Kass · Apr 3, 2025, 10:29 AM EDT

Buying APO $123.85, KKR $104.37 and BX $133.91

BY Doug Kass · Apr 3, 2025, 10:13 AM EDT

BY Doug Kass · Apr 3, 2025, 10:05 AM EDT

* We have been strongly critical of the bullish mantra (which lacked critical investment process) like the "cash on the sidelines" argument and the new paradigm of higher valuations.

* We entered the tariff event well positioned (with a very large cash position).

* Wrong-footed fiscal (and trade) policy was consistently a concern of mine... and the "not ready for prime time players" did not disappoint.

* We thrive on volatility and uncertainty - trading and investing unemotionally with a calculator in hand (measuring for a "margin of safety" and reward vs. risk)

* We aggressively purchased Index positions (SPY/QQQ into the waterfall in equities throughout the evening) as the ratio of upside reward v downside risk has measurably improved in the last 12 hours.

* We are likely now at or near maximum pain stemming from the tariff proposal.

"Never buy at the bottom and always sell too soon." - Jesse Livermore

We saw this coming -- wayward fiscal, tax and monetary policy were the foundation blocks to our ursine market view.

The only thing investors hate more than uncertainty is chaos - and the Administration's tariff tax proposals underscored the likely chaos more than the continued uncertainty.

A small group of "not ready for prime time players" in the Administration have resulted in a (self inflicted) shot into the foot of the world equity markets. The impact on an already wounded consumer, worsening economic/profit expectations and the already broken technical bearings of the stock market were exacerbated and felt in the after hours yesterday, when, at one point, the S&P Index futures reversed lower by nearly 300 handles (or -5%) in a matter of 60 minutes. We now wait for a renegotiation phase between the U.S. and our trading partners. There will be a lot of telephone calls in the next few weeks. We believe the market's reaction has been extreme, as we do not expect a worsening in trading relationships as our baseline expectation.

Though the delivery of the tariff policy was extraordinarily simplistic and blunt, our core case is that trading nations get quickly to the negotiating table for fear of dire global economic ramifications.

I agree with Peter Boockvar, who writes this morning:

As the tariff presentation shown yesterday was not a serious attempt at accuracy as rather than show the actual tariffs placed on US imports, it instead reflected the trade deficit we have with that particular country divided by their exports, it's now obvious that the very high reciprocal tariff threats thrown out yesterday will all be negotiated to something much lower. Hopefully.

And once the administration begins to show signs of cooperation, equity markets will stabilize and likely rally back a bit.

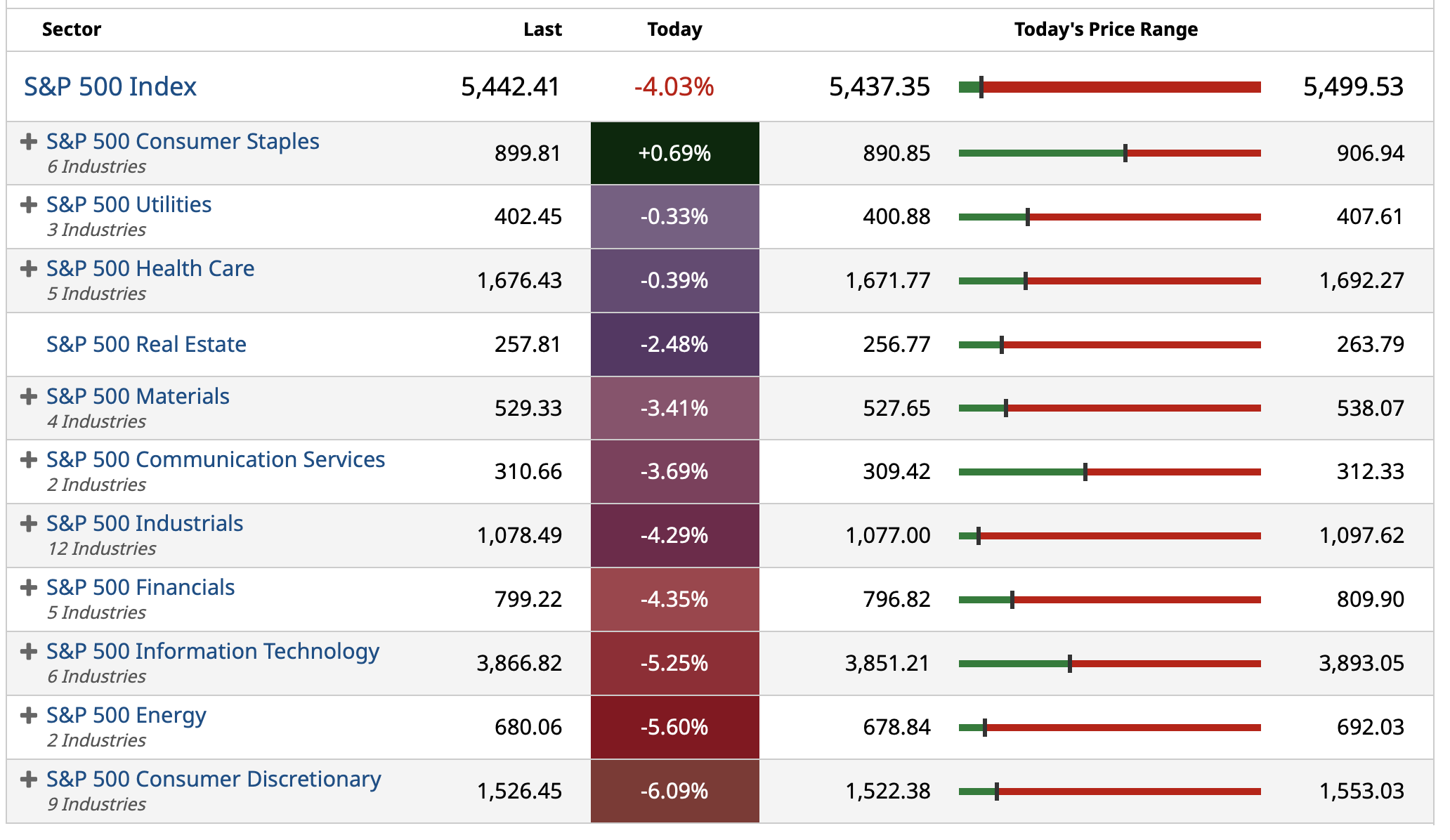

I have expected a 2025 S&P range of between 10% to 15% to the downside and only about 5% to the upside. With the after-hours carnage, the S&P Index is down by more than 8% and the Nasdaq is approximately 13% lower.

Ergo reward v risk has become more attractive.

Tactically, I entered the tariff event very liquid, having sold all of my Index exposure and even much of my technology exposure into yesterday afternoon's free fall:

Tactically, we invest and trade opportunistically without emotion. As the decline in the after hours intensified and reward vs. risk has shifted to better entry points -- I began to reestablish trading long rentals in the indexes:

Once again The Oracle of Omaha is on the top of the heap, with record cash reserves (of nearly $325 million) and having pared his largest investment holding, Apple, near its all-time high:

"Be fearful when others are greedy and greedy when others are fearful."

- Warren Buffett

I would also add something that another pal, Byron Wien, once mentioned to me:

"Disasters have a way of not happening."

- Byron Wien

Fasten your seat belts.

BY Doug Kass · Apr 3, 2025, 9:45 AM EDT

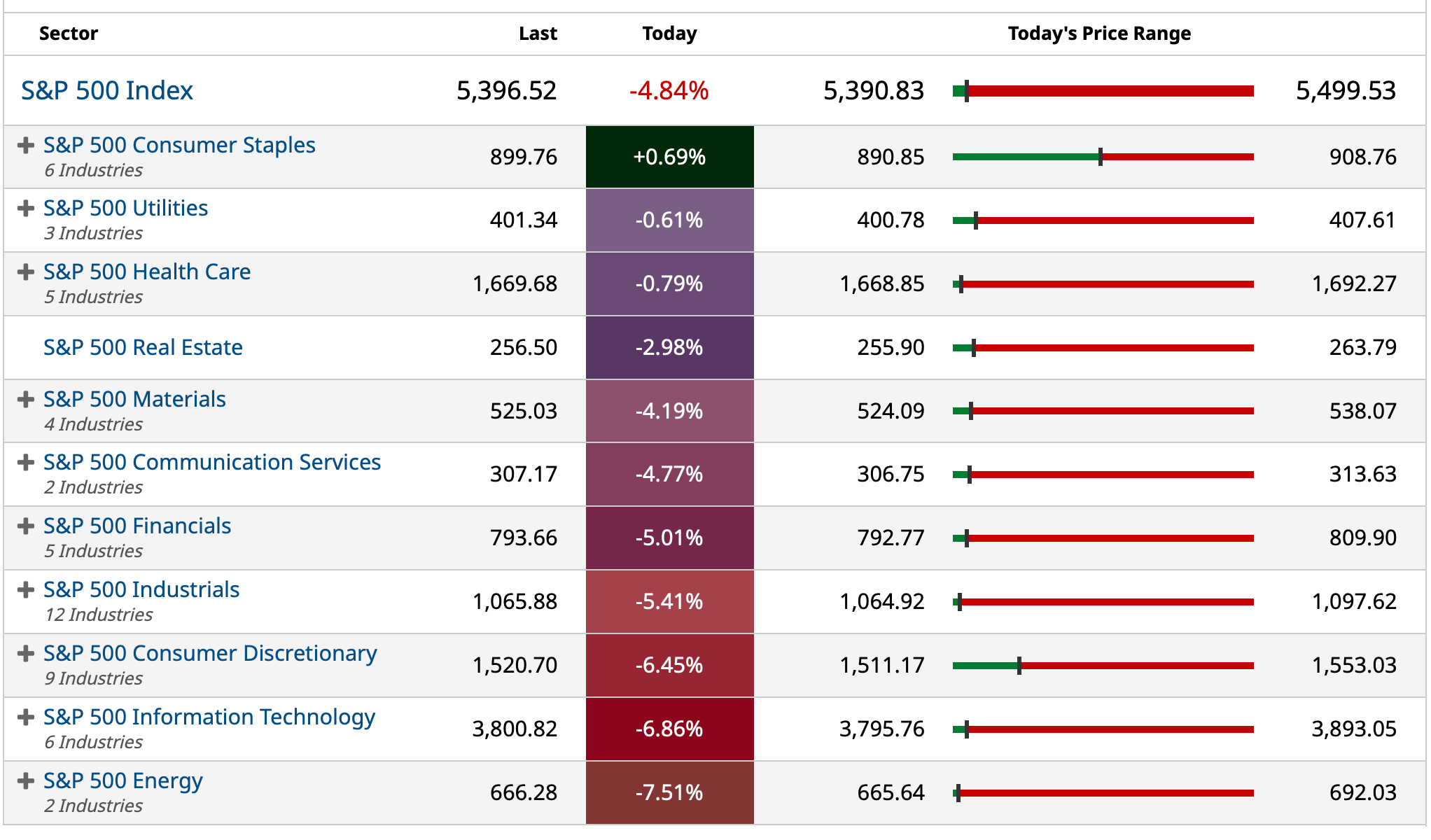

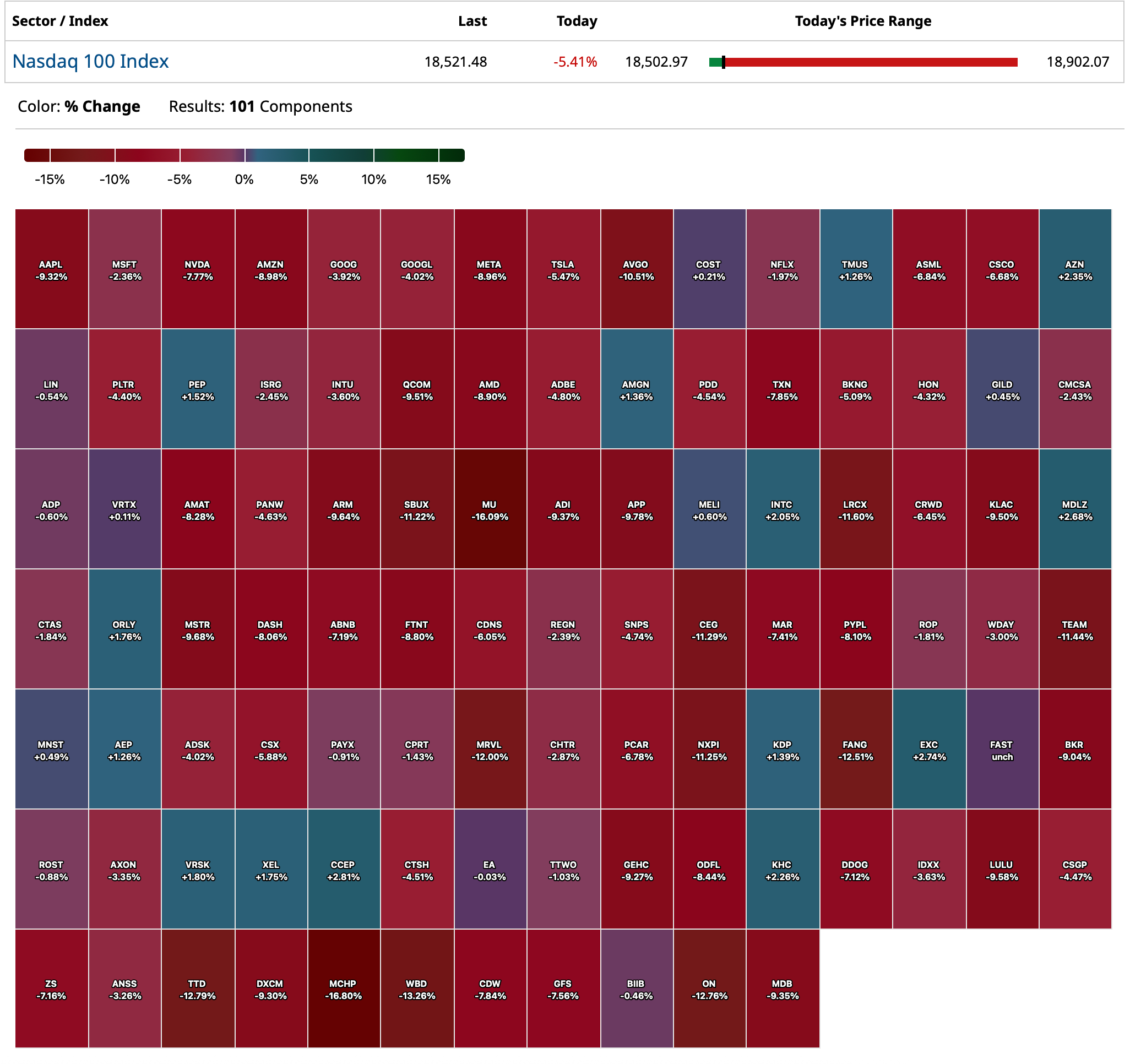

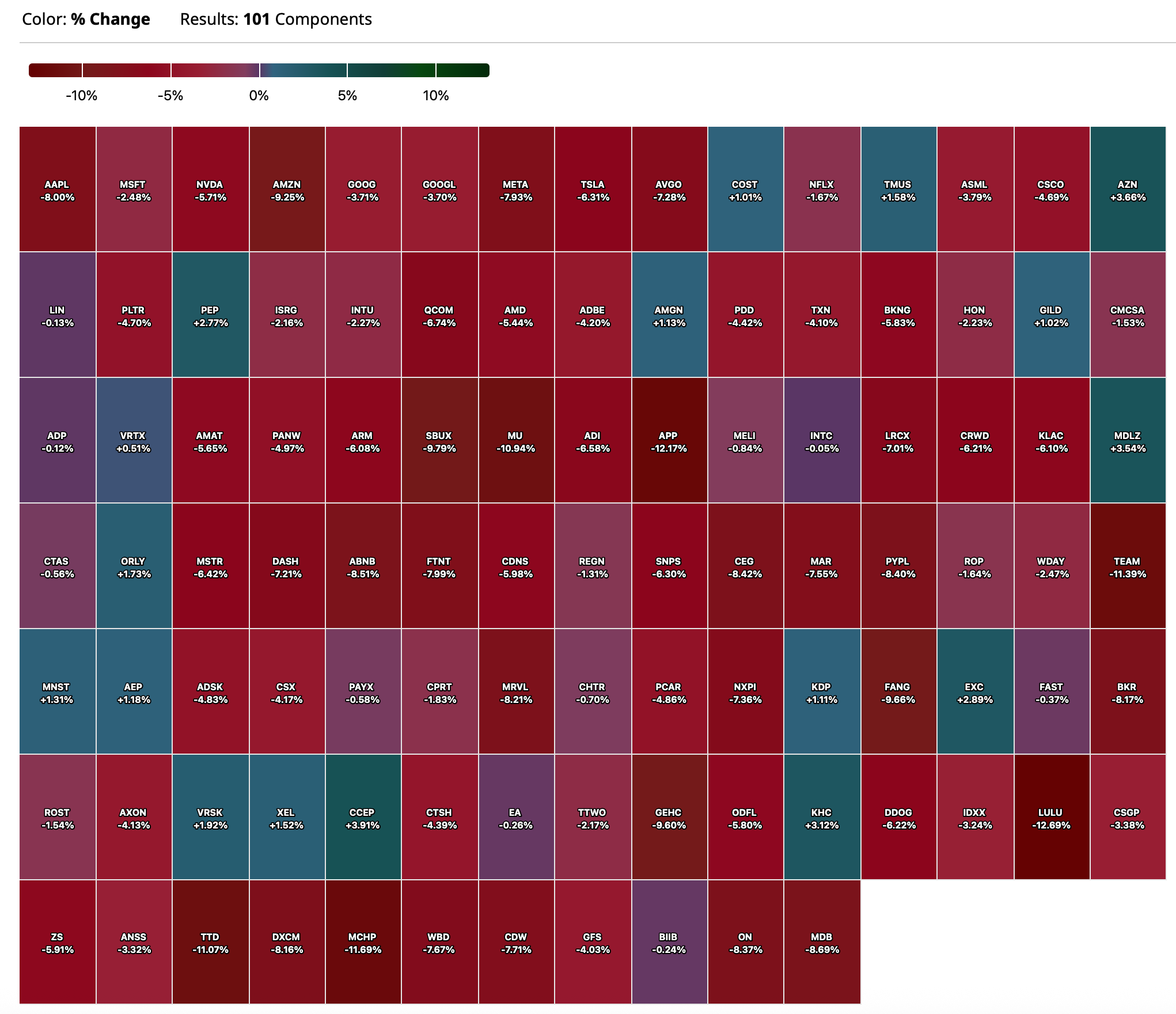

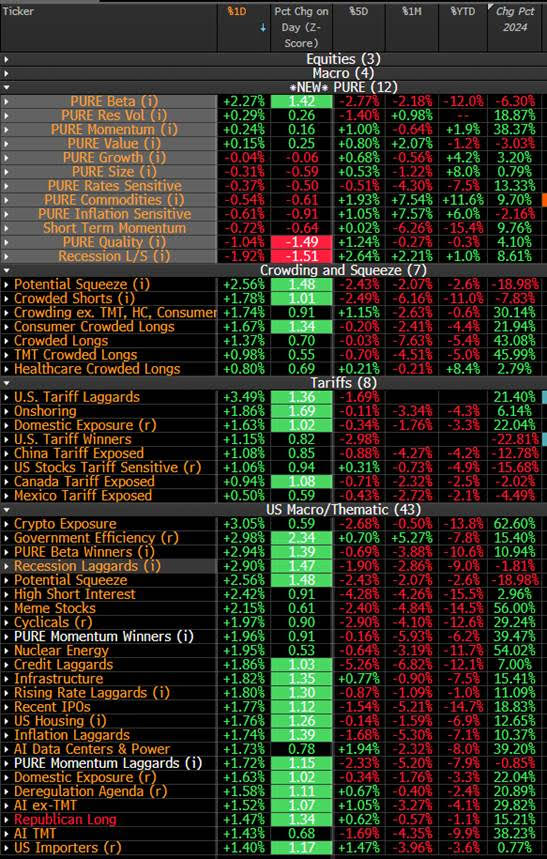

This table is a valuable resource for momentum-based short term traders:

BY Doug Kass · Apr 3, 2025, 9:30 AM EDT

-LW +3.9% (earnings, guidance; engaged AlixPartners, a leading global business advisory firm, to assist the Company in evaluating opportunities for near- and long-term value creation and cost savings)

-RH -30% (earnings, guidance)

-FIVE -18% (US tariff announcement)

-DECK -14% (US tariff announcement)

-BBY -12% (CitiGroup Cuts BBY to Neutral from Buy, price target: $70)

-NKE -11% (US tariff announcement)

-LYFT -10% (Tier1 firm Cuts LYFT to Underperform from Buy, price target: $10.50 from $17.50)

-AAPL -7.6% (US tariff announcement)

-HPQ -7.3% (US tariff announcement)

-MSM -7.1% (earnings, guidance)

-AMZN -6.2% (US tariff announcement)

-NTLA -6.0% (plans to submit BLA for ATTRv-PN by 2028)

-TSLA -5.9% (US tariff announcement)

-NVDA -5.8% (US tariff announcement)

-WMT -5.5% (US tariff announcement)

-DG -5.2% (US tariff announcement)

-LSTR -5.2% (cuts guidance, citing significant supply chain fraud)

-PDD -5.2% (to invest CNY100B over next three years on transforming and upgrading platform merchants)

-SMH -4.7% (US tariff announcement)

-FDX -3.7% (US tariff announcement)

-MSFT -2.6% (US tariff announcement)

-UPS -2.5% (US tariff announcement)

-GM -2.4% (US tariff announcement)

-F -2.0% (US tariff announcement)

BY Doug Kass · Apr 3, 2025, 9:23 AM EDT

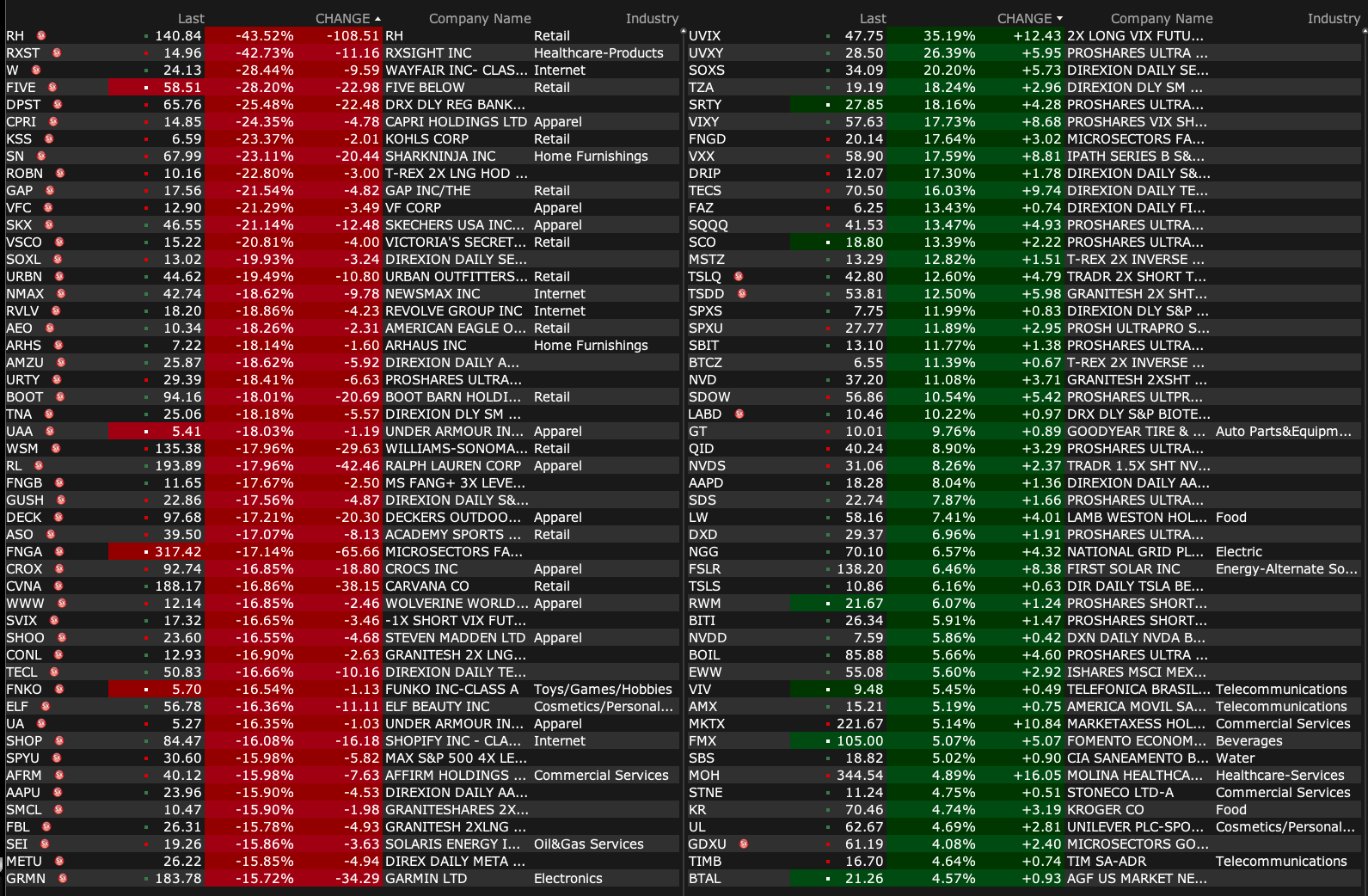

Premarket percentage movers at 8:34 a.m. ET:

BY Doug Kass · Apr 3, 2025, 9:17 AM EDT

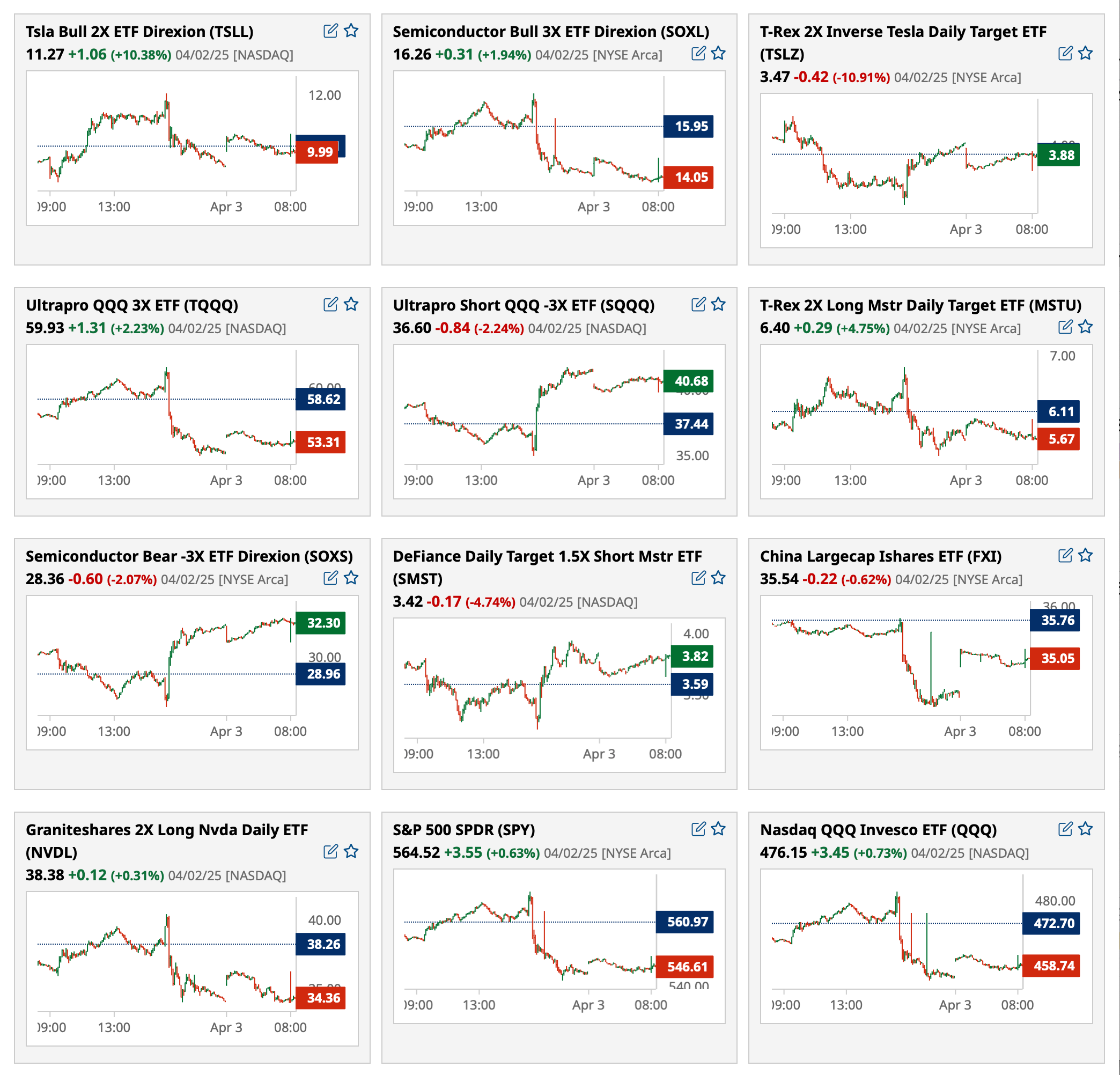

Most active premarket ETFs as of 8:14 a.m. ET:

BY Doug Kass · Apr 3, 2025, 9:10 AM EDT

BY Doug Kass · Apr 3, 2025, 9:00 AM EDT

From Peter Boockvar:

I remind again, if you don't see a daily comment from me, please check your spam.

As the tariff presentation shown yesterday was not a serious attempt at accuracy as rather than show the actual tariffs placed on US imports, it instead reflected the trade deficit we have with that particular country divided by their exports, it's now obvious that the very high reciprocal tariff threats thrown out yesterday will all be negotiated to something much lower. Hopefully.

A simple example of why a trade deficit can be a good thing for both transacting parties. Walmart has a huge trade deficit with China as they import so many items sold in US stores and export to them very little other than what is need for some stores they have in China. That large trade deficit for Walmart benefits both them and China tremendously and the US consumer does as well via affordable items. The belief that a trade deficit is bad is completely flawed.

This all said, the hope that clarity and finality to tariffs would be seen yesterday, that of course is not the case as this will all continue on. And maybe it does work out in terms of negotiated settlements with our trading partners with an overall reduction in tariff rates (outside of the broad 10% tax rate on all imports) but until then,this current approach is going to literally freeze global trade. I bolded for emphasis.

Regardless of what you or I think, the stock market again obviously doesn't like it, again, and if the S&P 500 breaks further from here, the odds of an economic recession will continue to trend to 100% as we all know that upper income spending has been a major economic support and will certainly buckle if stocks do. This at the same time that the goal is to slow the rate of government spending which is desperately needed but has negative short term economic implications as said here now many times.

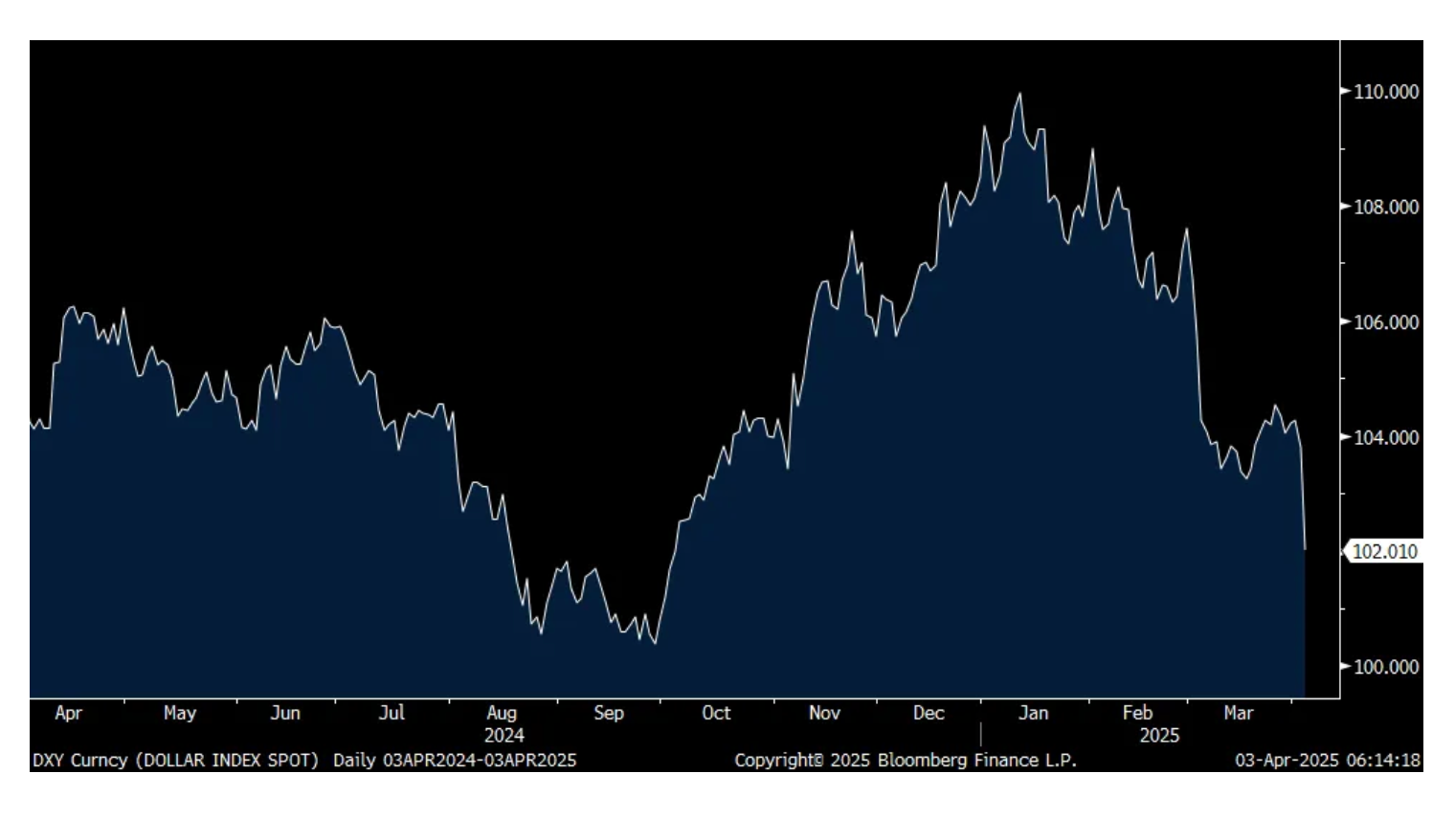

What is very notable today and creates even more pain for US importers that will be paying these tariffs is the US dollar is getting slammed. The euro/yen heavy DXY is down a large 1.7%, the biggest one day decline since November 2022 and to the weakest level since October 2024. The Canadian $ and Mexican peso are rising too while the yuan is flattish. The weaker the dollar gets, the more we, the US, are going to pay for these tariffs.

DXY

RH (Restoration Hardware) is down sharply this morning, both in response to their earnings, and due to the foreign sourcing they do.

From Gary Friedman, the CEO:

"While we expect a higher risk business environment this year due to the uncertainty caused by tariffs, market volatility, and inflation risk, we believe it's important to separate the signal from the noise. The fact is, we've been operating in the worst housing market in almost 50 years. For context, in 1978, there were 4.09 million existing homes sold when the US had a population of 223 million. Contrast that to 2024, where 4.06 million existing homes sold with a population of 341 million, and it illuminates just how depressed the housing market has been this past year. Despite that fact, we are performing at a level most would expect in a robust housing market."

A lot of question and comments on all the tariffs and its impact of course and Gary said they'll manage it as best they can. He also said "I wouldn't want to compete with us in times like these. No one is going to outwork us. No one is going to out think us. No one is going to out create us, out innovate us."

This was great from him too in response to a question about the 32% tariff on Indonesia where they have some production. "I mean, you figure out how to be more efficient. You figure out how to work better. Humans, I like to say humans without deadlines are useless, right? We're no good without deadlines. We're not good without pressure. It's why the great athletes perform in the playoffs, not necessarily their best in the regular season. Although Steph Curry did have 12 threes and 52 points last night, I was happy about that, but it's getting close to the playoffs and it was against one of their rivals, right? So you see we're kind of one of those teams. Like we're great in the playoffs. We're great under pressure. And humans generally are better under pressure."

The March China Caxin services index rose to 51.9 from 51.4 and above the estimate of 51.5. On the outlook from here, "Market optimism was maintained. The indicator for expectations of future activity measured lower than February but remained in expansionary territory. Service providers were hopeful about future policy support at home. However, some expressed concerns over a potentially deteriorating global trade environment."

Singapore's March PMI rose to 52.7 from 51 while Hong Kong's fell to 48.3 from 49.

I'm sure all of this changes in light of yesterday.

BY Doug Kass · Apr 3, 2025, 8:45 AM EDT

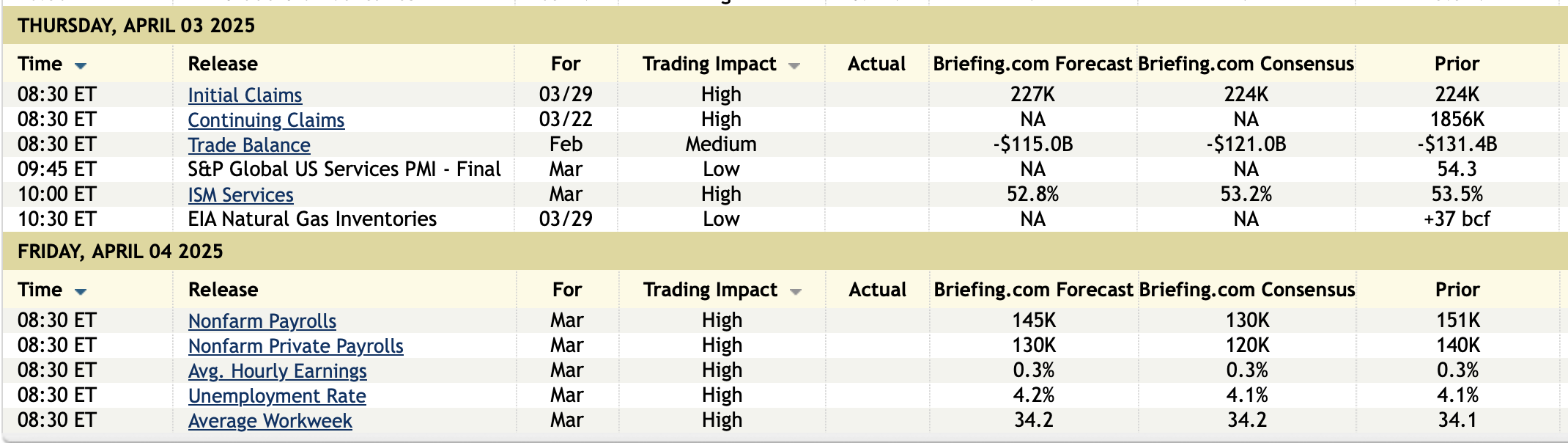

BY Doug Kass · Apr 3, 2025, 8:30 AM EDT

BY Doug Kass · Apr 3, 2025, 8:15 AM EDT

* Written after the close on Wednesday.

* Shared by me without comment.

BY Doug Kass · Apr 3, 2025, 8:05 AM EDT

S&P futures are now -190 handles (7:32 a.m.):

* Added to indices: SPY $545.89 and QQQ $458.09.

* Added to technology: META $565.41, MSFT $372.77, AMZN $184.24, GOOGL $153.41.

* Added to financials: WFC $69.32, BAC $40.55, C $68.96.

BY Doug Kass · Apr 3, 2025, 7:55 AM EDT

BY Doug Kass · Apr 3, 2025, 7:45 AM EDT

Dougie Kass

I have repeatedly commented in the Comments Section that buying any sector (and that importantly includes "Generational Multipliers") is a poor strategy unless one calculates and superimposes decisions regarading "margin of safety" and upside reward v downside risk.

Many in our Comments have not agreed, especially as it related to technology (AMZN, MSFT, GOOGL, META. NVDA etc).

Too many forgot how it felt to own Mag7 at the recent bear market low in late 2021 - instead they were buoyed by the ascent of late 2022 to the end of 2024.

I hope that the recent drop in the share prices of Mag7 is instructive as to how important entry points are.

BY Doug Kass · Apr 3, 2025, 7:36 AM EDT

* Here is my shocked face — the plethora of technicans are now confidentally negative."

Bonus — Here are some great links:

BY Doug Kass · Apr 3, 2025, 7:15 AM EDT

BY Doug Kass · Apr 3, 2025, 7:05 AM EDT

BY Doug Kass · Apr 3, 2025, 6:55 AM EDT

BY Doug Kass · Apr 3, 2025, 6:45 AM EDT

Added to indices on premarket weakness:

* SPY $545.81

* QQQ $458.01

BY Doug Kass · Apr 3, 2025, 6:35 AM EDT

I am buying back technology (that I sold yesterday afternoon) (MSFT, GOOGL, AMZN) and financials (C, BAC, WFC) in premarket weakness.

BY Doug Kass · Apr 3, 2025, 6:25 AM EDT

BY Doug Kass · Apr 3, 2025, 6:15 AM EDT

BY Doug Kass · Apr 3, 2025, 6:05 AM EDT

The S&P Short Range Oscillator remained modestly over sold (-1.35%).

But the figure is an illusion as it was determined at 4 p.m. on Thursday.

Tonite's reading, accounting for the after-hours drop, will likely be much more oversold.

BY Doug Kass · Apr 3, 2025, 5:55 AM EDT

BY Doug Kass · Apr 3, 2025, 5:45 AM EDT

* SPY $544.27

* QQQ $454.90

BY Doug Kass · Apr 2, 2025, 8:43 PM EDT