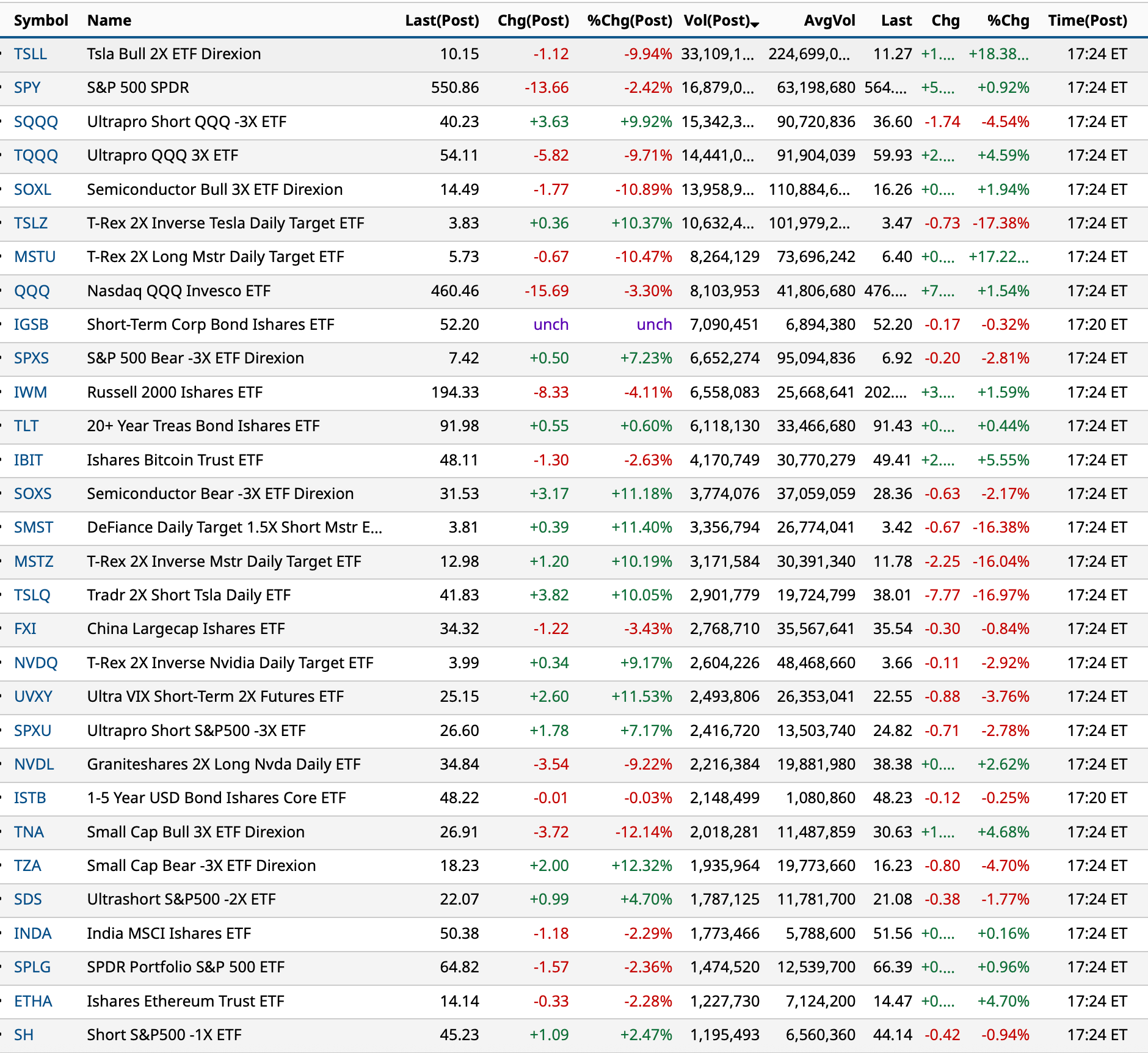

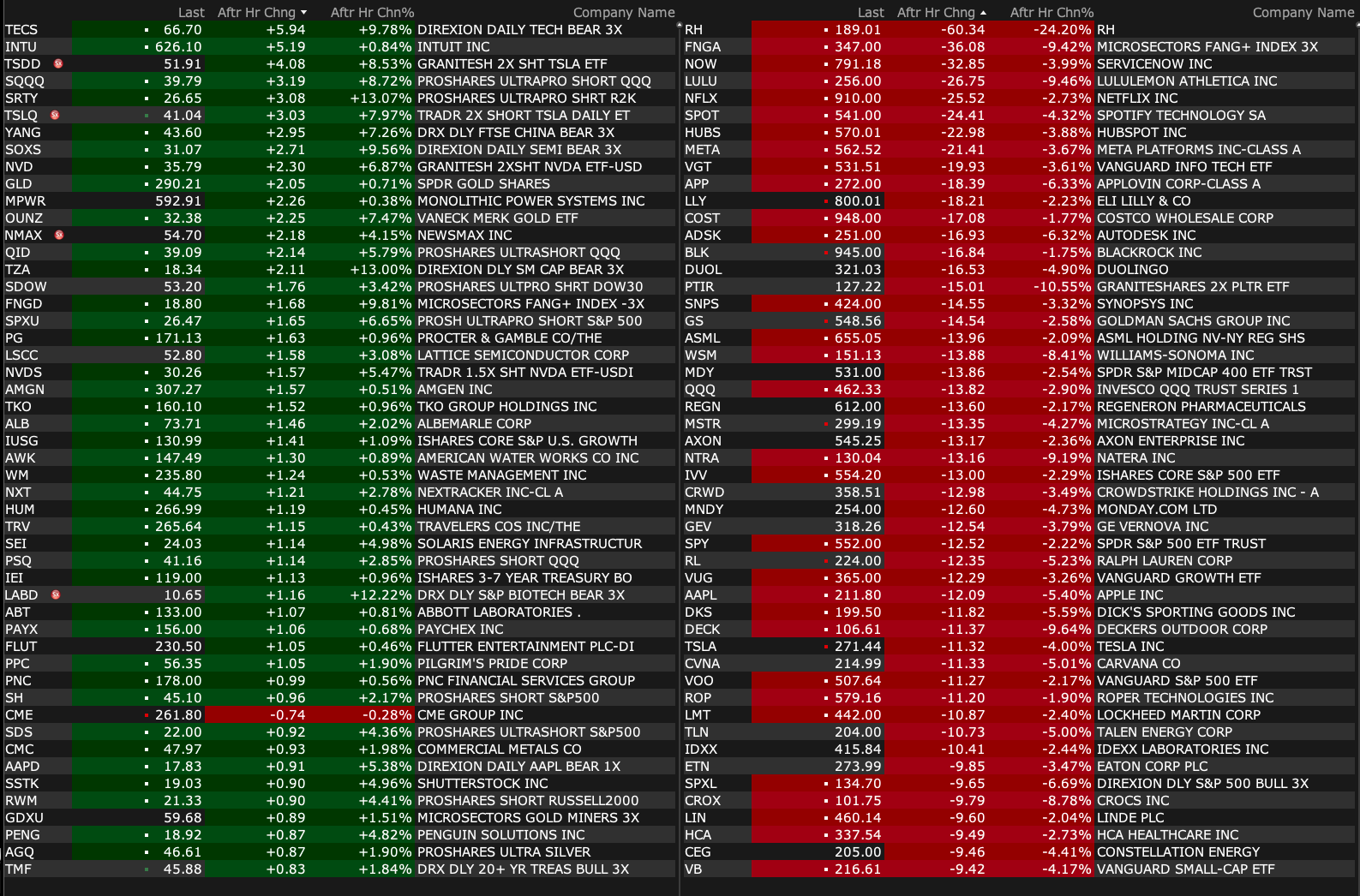

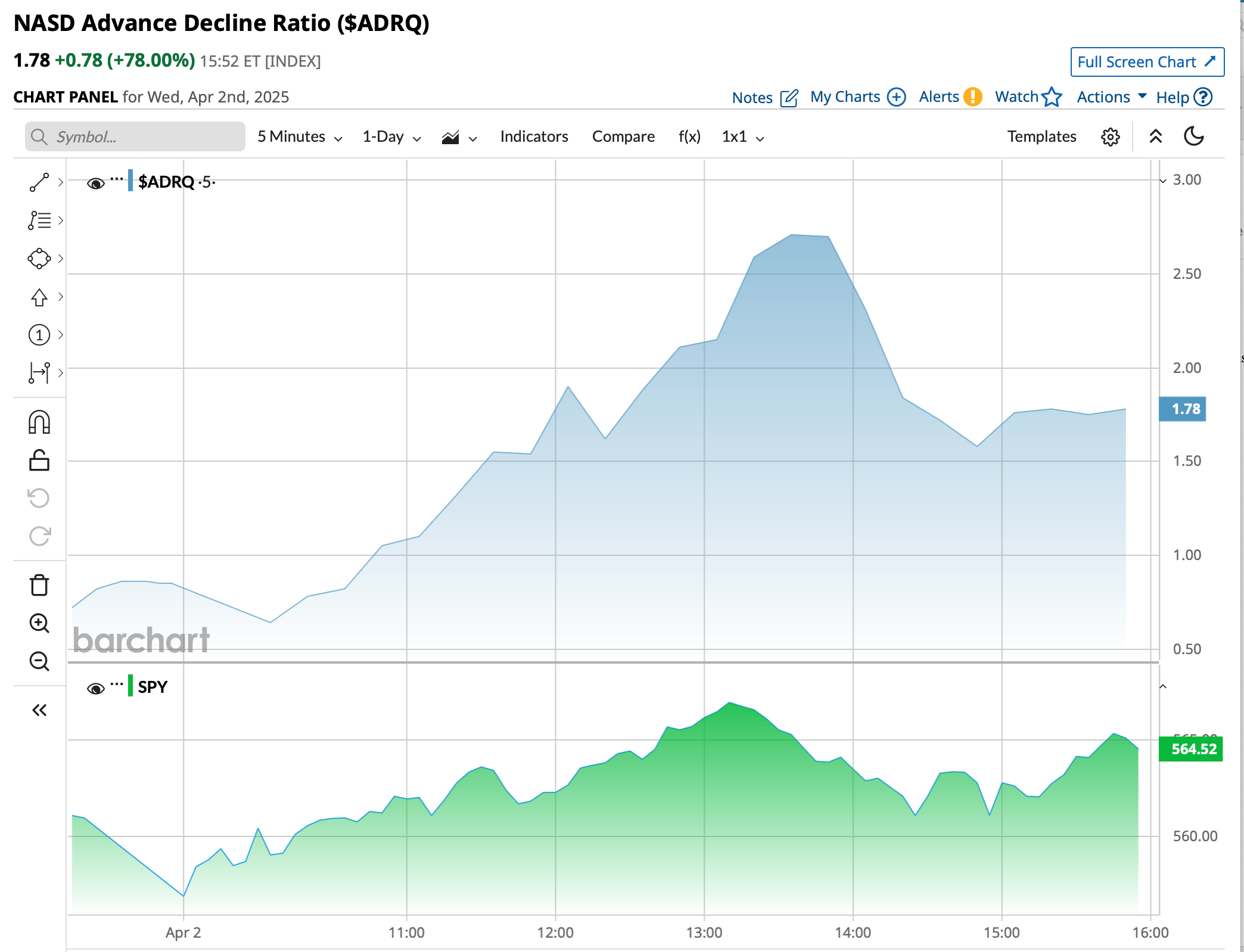

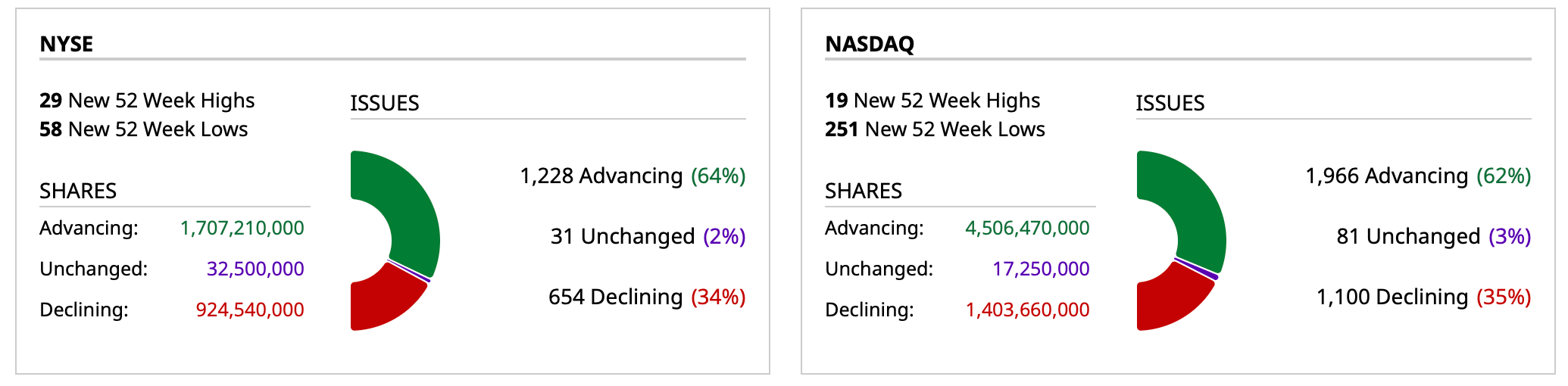

Most Active ETFs After Hours

As of 5:24 p.m.:

BY Doug Kass · Apr 2, 2025, 7:10 PM EDT

As of 5:24 p.m.:

BY Doug Kass · Apr 2, 2025, 7:10 PM EDT

I am adding to my second tranche of index common with S&P futures -205:

* SPY $545.09

* QQQ $455.75

BY Doug Kass · Apr 2, 2025, 6:57 PM EDT

As of 5:07 p.m.:

BY Doug Kass · Apr 2, 2025, 4:55 PM EDT

I am not back in office but I am buying SPY and QQQ at $552 and $463, respectively.

BY Doug Kass · Apr 2, 2025, 4:50 PM EDT

BY Doug Kass · Apr 2, 2025, 4:45 PM EDT

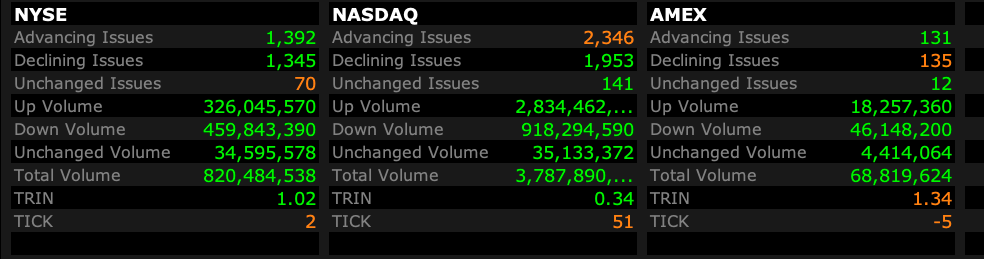

- NYSE volume 17% below its one-month average

- NASDAQ volume 28% above its one-month average

- VIX Index: + 0.05% to 21.6

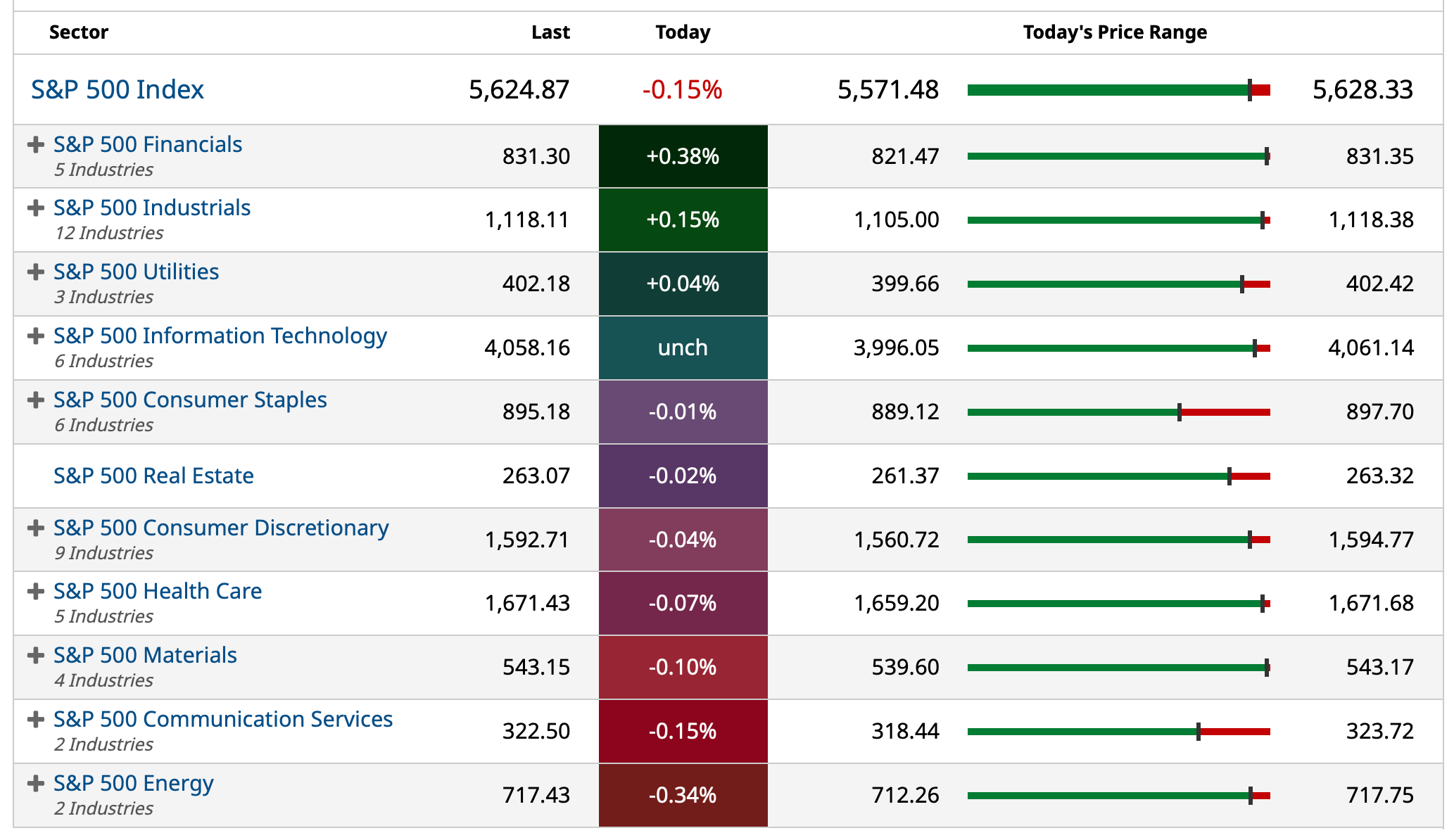

BY Doug Kass · Apr 2, 2025, 4:34 PM EDT

BY Doug Kass · Apr 2, 2025, 1:57 PM EDT

Wolf Street howls about how Musk crushed his own brand: Oh Elon! Tesla Deliveries Plunge as Musk Crushes One of the Most Successful Consumer Brands | Wolf Street

BY Doug Kass · Apr 2, 2025, 11:20 AM EDT

- NYSE volume 29% below its one-month average;

- Nasdaq volume 55% above its one-month average;

- VIX index: up 1.52% to 22.10

BY Doug Kass · Apr 2, 2025, 11:03 AM EDT

With S&P cash now +3 handles (that is a +63 reversal from the morning's lows) - I have sold out the technology buys made (in the hole) in premarket weakness.

For a nice profit.

As noted in an earlier column, this is the best trading market for dispassionate and opportunistic traders.

BY Doug Kass · Apr 2, 2025, 10:47 AM EDT

BY Doug Kass · Apr 2, 2025, 10:15 AM EDT

I have sold out my index common I bought in the hole - after the S&P futures moved from being -60 handles to only -15 handles.

Nice, quick profit.

Staying opportunistic.

BY Doug Kass · Apr 2, 2025, 10:00 AM EDT

From Peter Boockvar:

I believe the best outcome today at 4pm would be a tariff reciprocity agreement with our trading partners that would result in a net lowering of global tariffs. What would not be a welcome is an across the board global tariff on all US imports for the sole reason of needing to raise money to pay for the extension of the expiring tax cuts. While 'pay fors' will certainly be needed for the latter, I'd prefer spending cuts instead though there is no chance of finding enough.

Either way, it doesn't look like we'll get the finality on this issue even after today that so many of us want, particularly small and medium sized businesses that just don't have the same flexibility as larger ones to absorb any cost increases that they can't pass on.

I will say this, with tariffs such a big topic to pay attention to and it basically neutering the Fed and its monetary policy because of the inflation and economic confusion, I've talked less this year about the Fed than I've had for a long time. Refreshing but it's no fun talking about tariffs either.

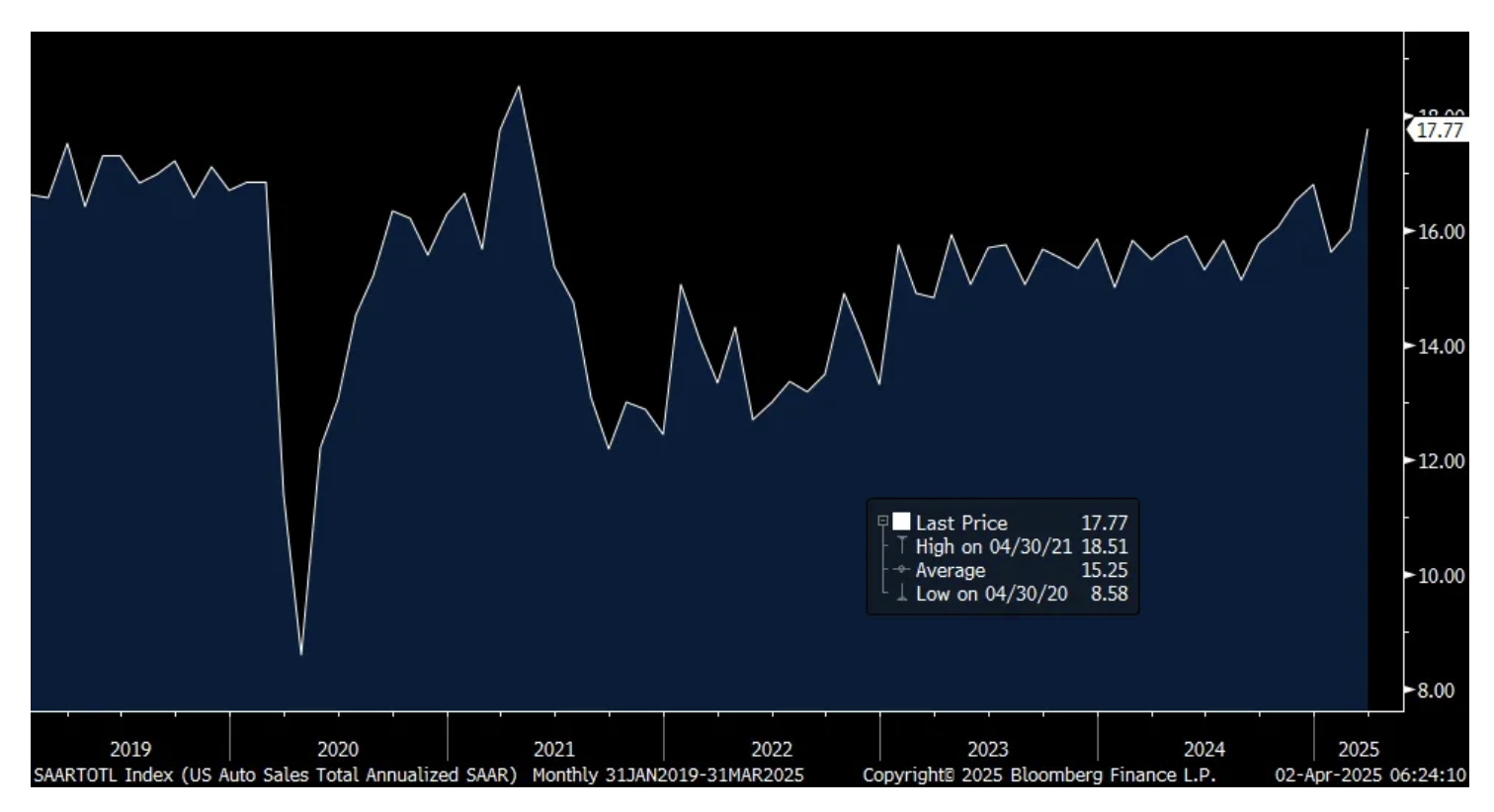

Reflecting the desire to buy a new car now as to avoid the inevitable price increase (whether on imports or a domestically made vehicle that imports their parts), vehicle sales in March jumped to 17.77mm at a seasonally adjusted annualized rate. That was well above the estimate of 16.2mm, vs 15.49mm in March 2024 and vs 17.5mm in March 2019.

Ward's Automotive said in response, "March sales were proof that US consumers are very much paying attention to tariffs...Buyers flocking to dealer lots to beat potential price increases, combined with some pre-tariff push by automakers raising deliveries to fleet customers lifted raw volume to over a 4 yr high, not to mention a rare double digit y/o/y gain. Regardless of any coming impacts from tariffs, March's booming results will cause lower volume in the 2nd quarter dur to the additional drain to dealer inventory that, based on industry norms, was already lean prior to the month."

Vehicle Sales

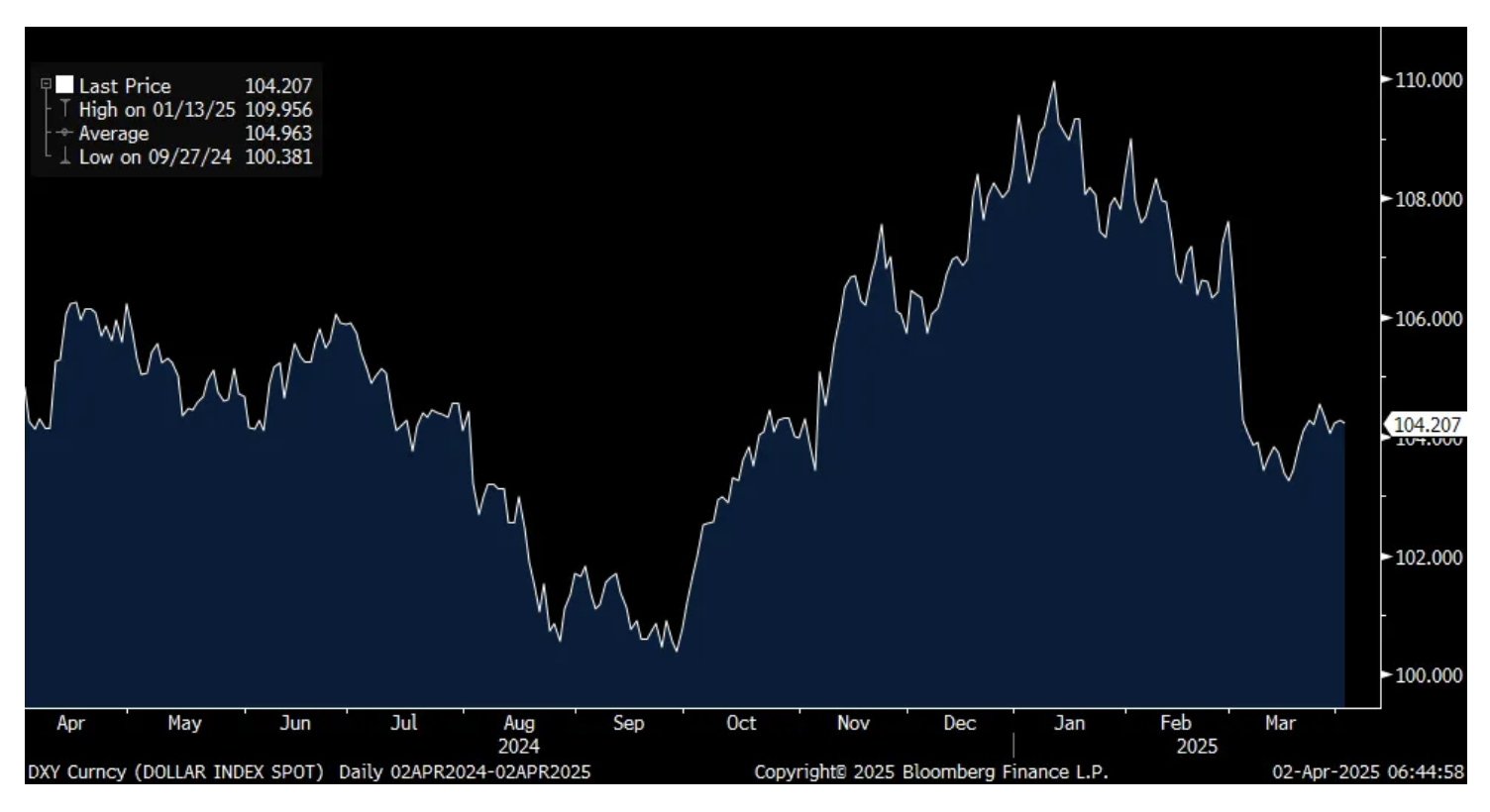

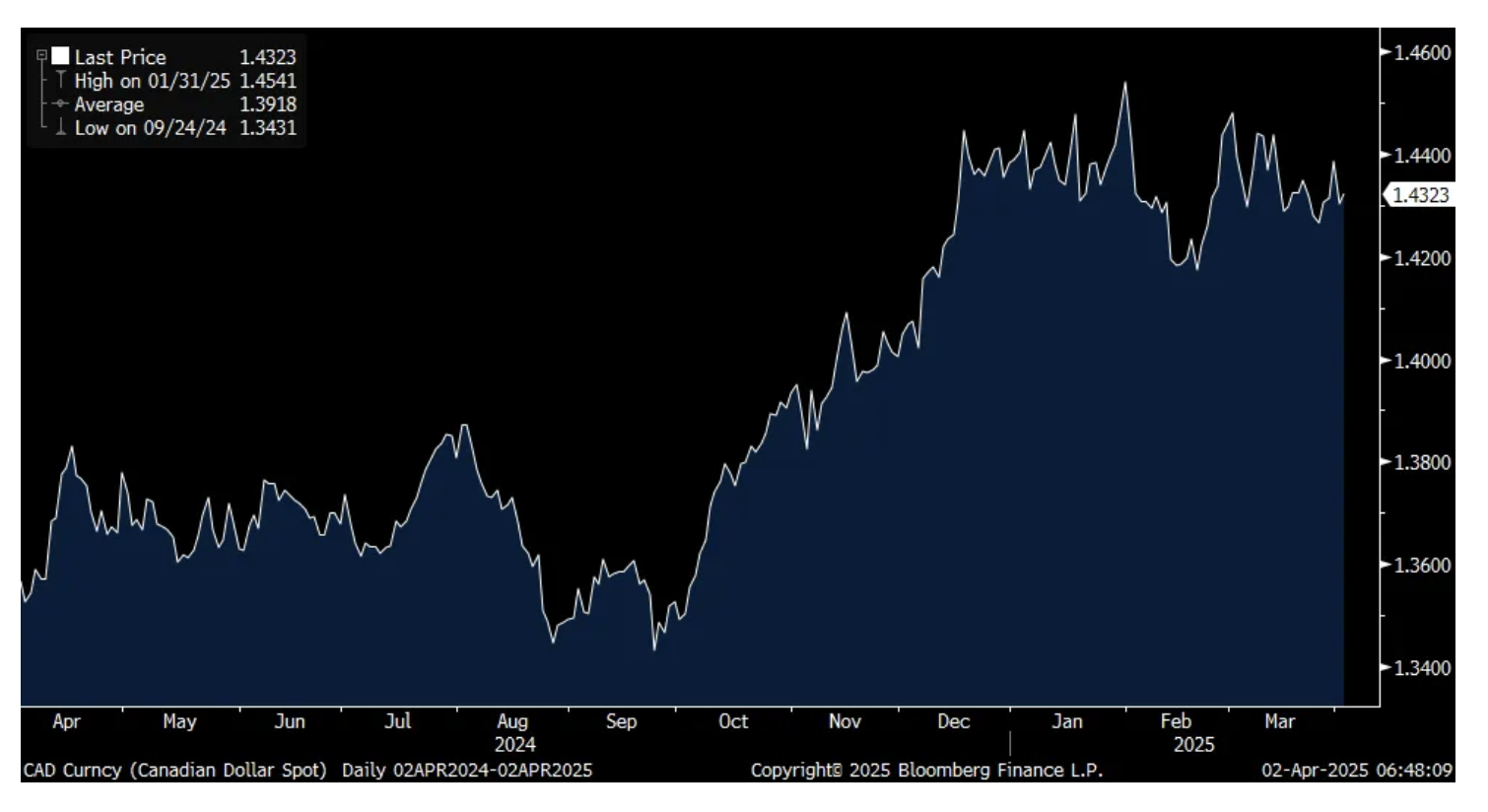

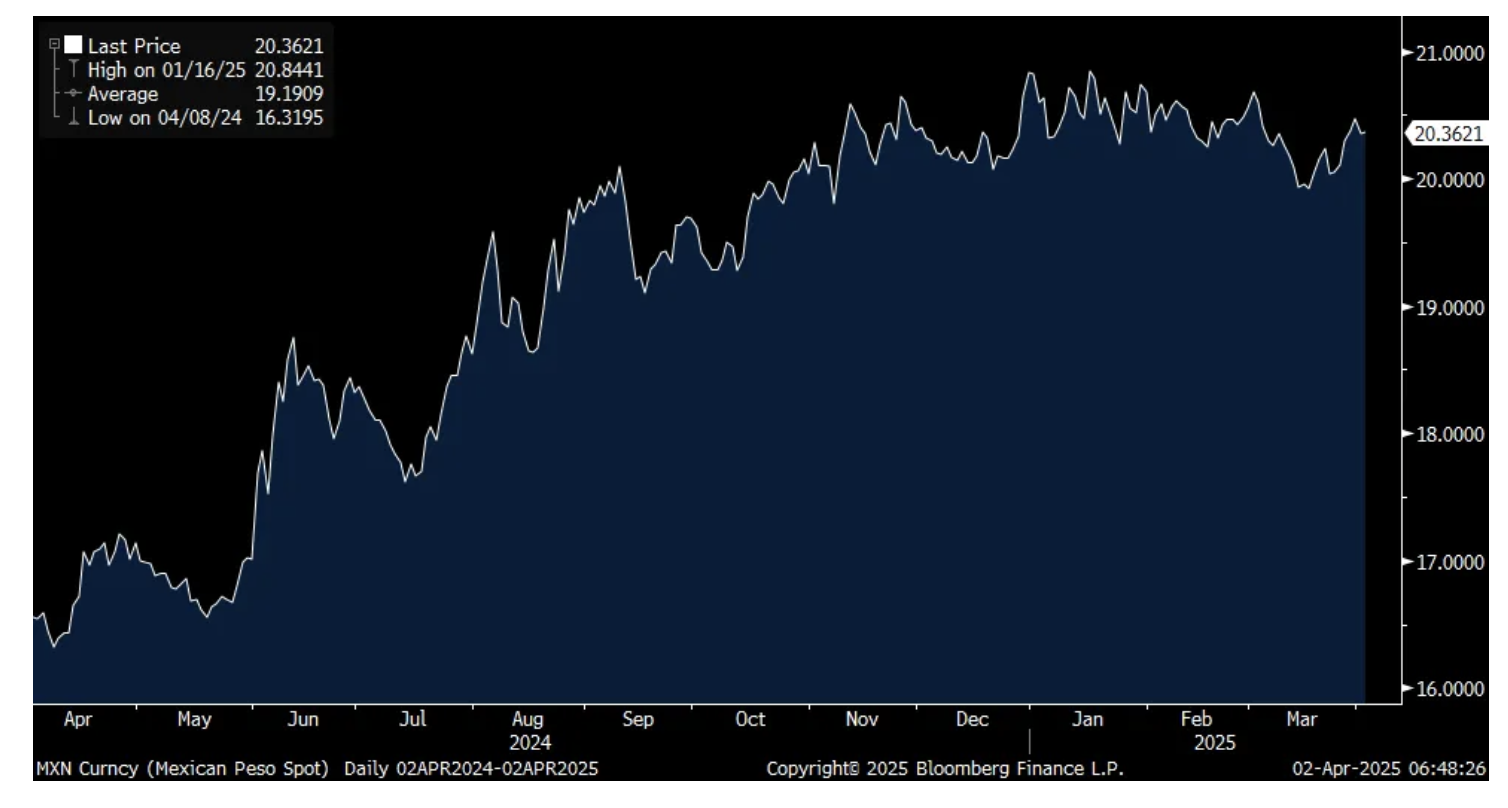

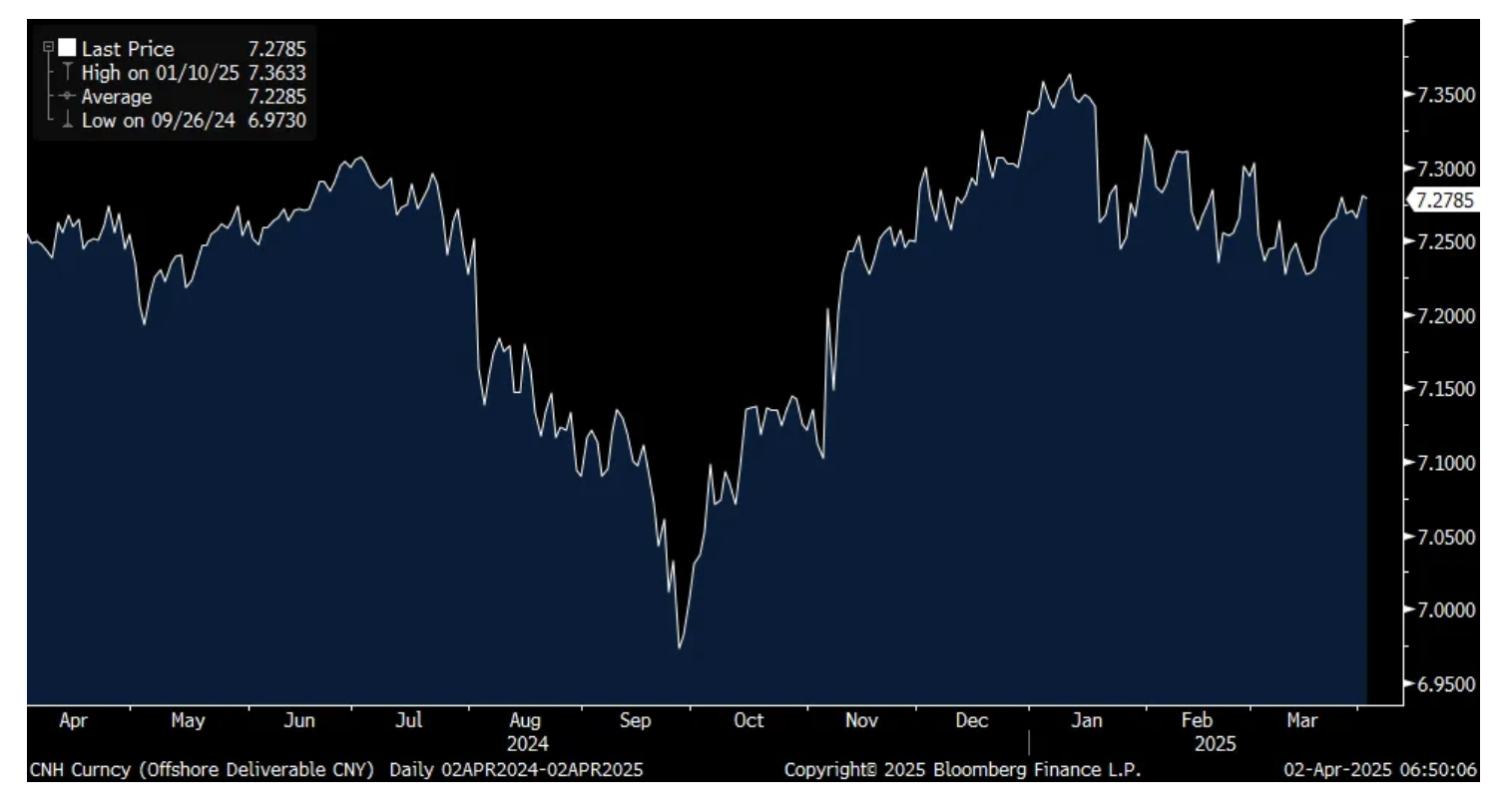

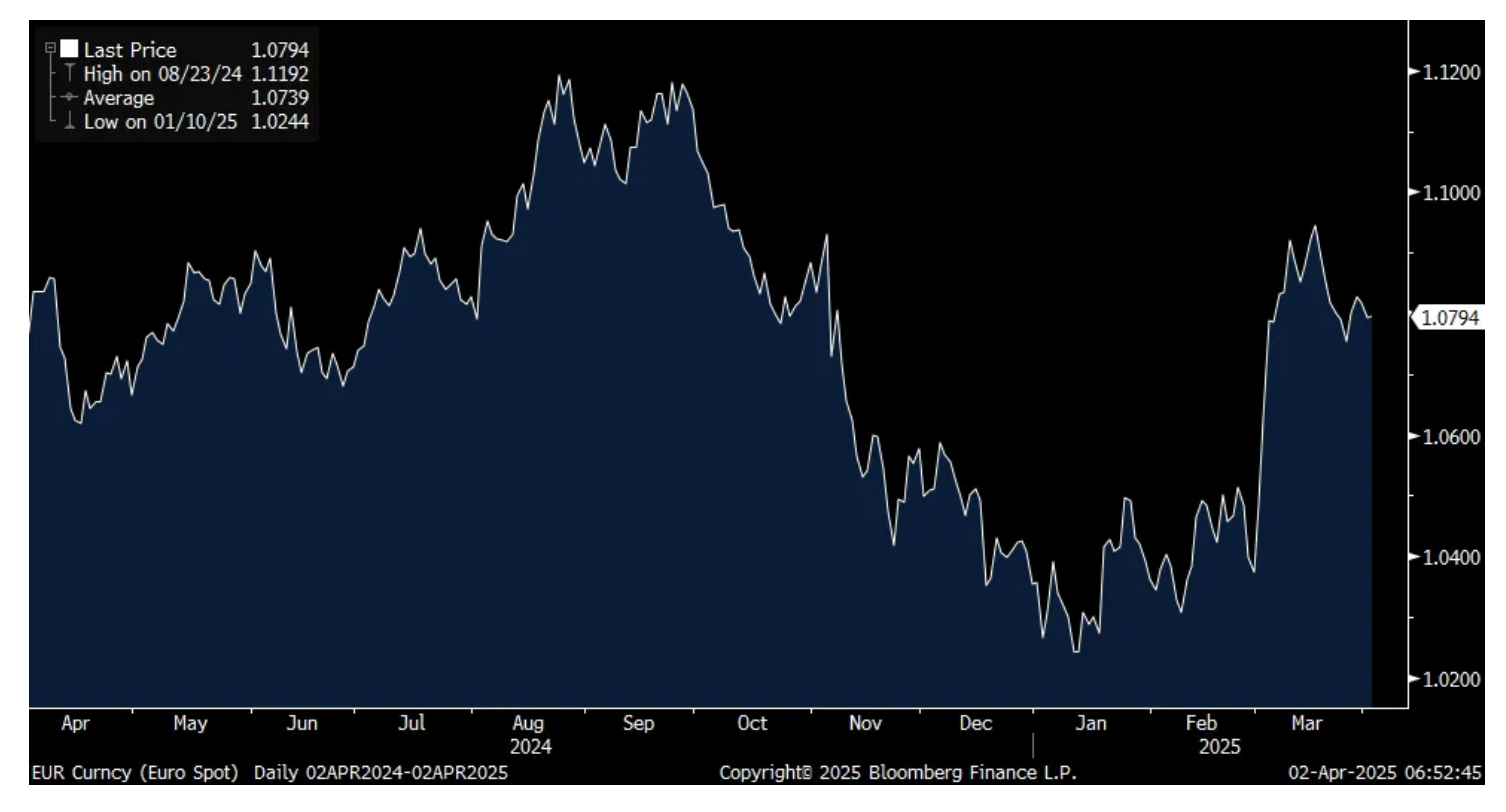

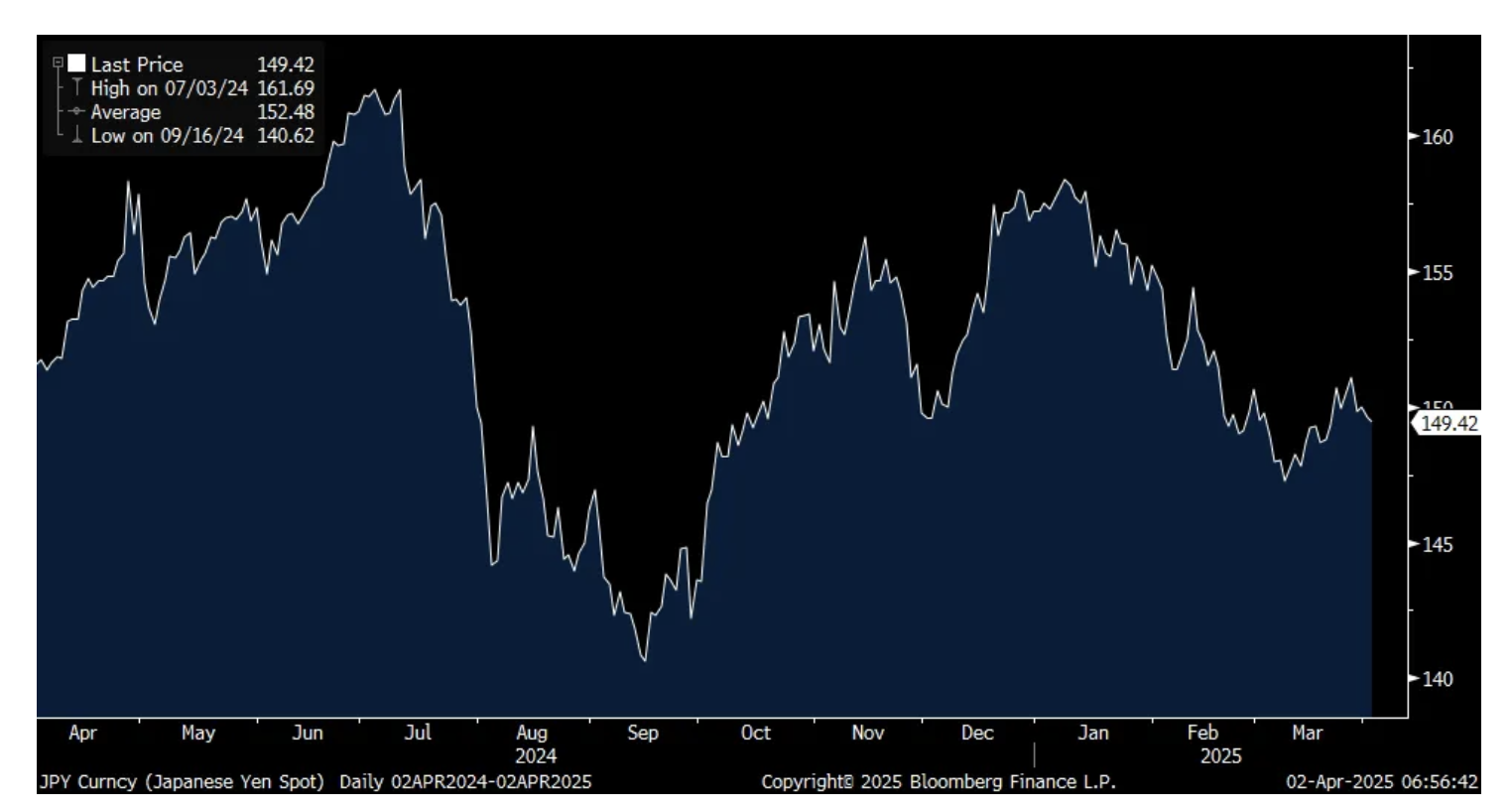

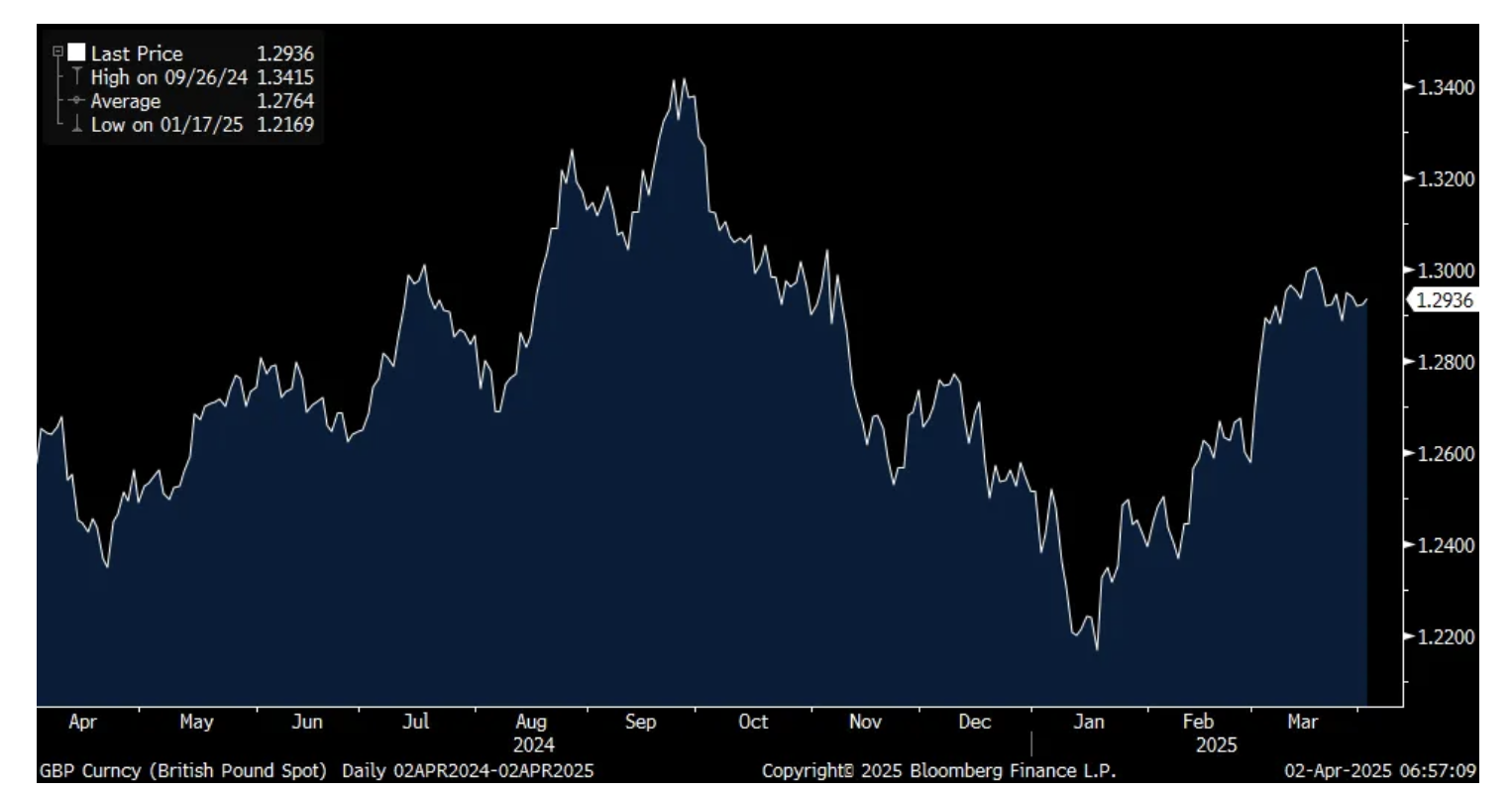

An economic key here for US importers is where the US dollar goes as it is a main input in calculating the extent at which any cost increase will be absorbed by the importer or the exporter. The euro/yen heavy DXY is just a touch above where it was the day before the election after the sharp rally post it. The Canadian dollar is the one that has gotten hit the most of our large trading partners as its trading at $1.43 vs $1.39 the Monday before the election (a US dollar buys more Canadian $s in this instance). The Mexican peso is just a touch weaker post election, though is down sharply over the past year. The offshore yuan is lower too at 7.278 vs 7.11 the day before the election ($1 gets more yuan). The euro is slightly down post election but well off its lows in reaction to the fiscal stimulus measures being taken in the region and I'll argue, as a result of Europeans selling the Mag 7 stocks. The British pound and Japanese yen are higher vs the US dollar post election.

DXY

CAD

MXN

CHN

EURO

YEN

Pound

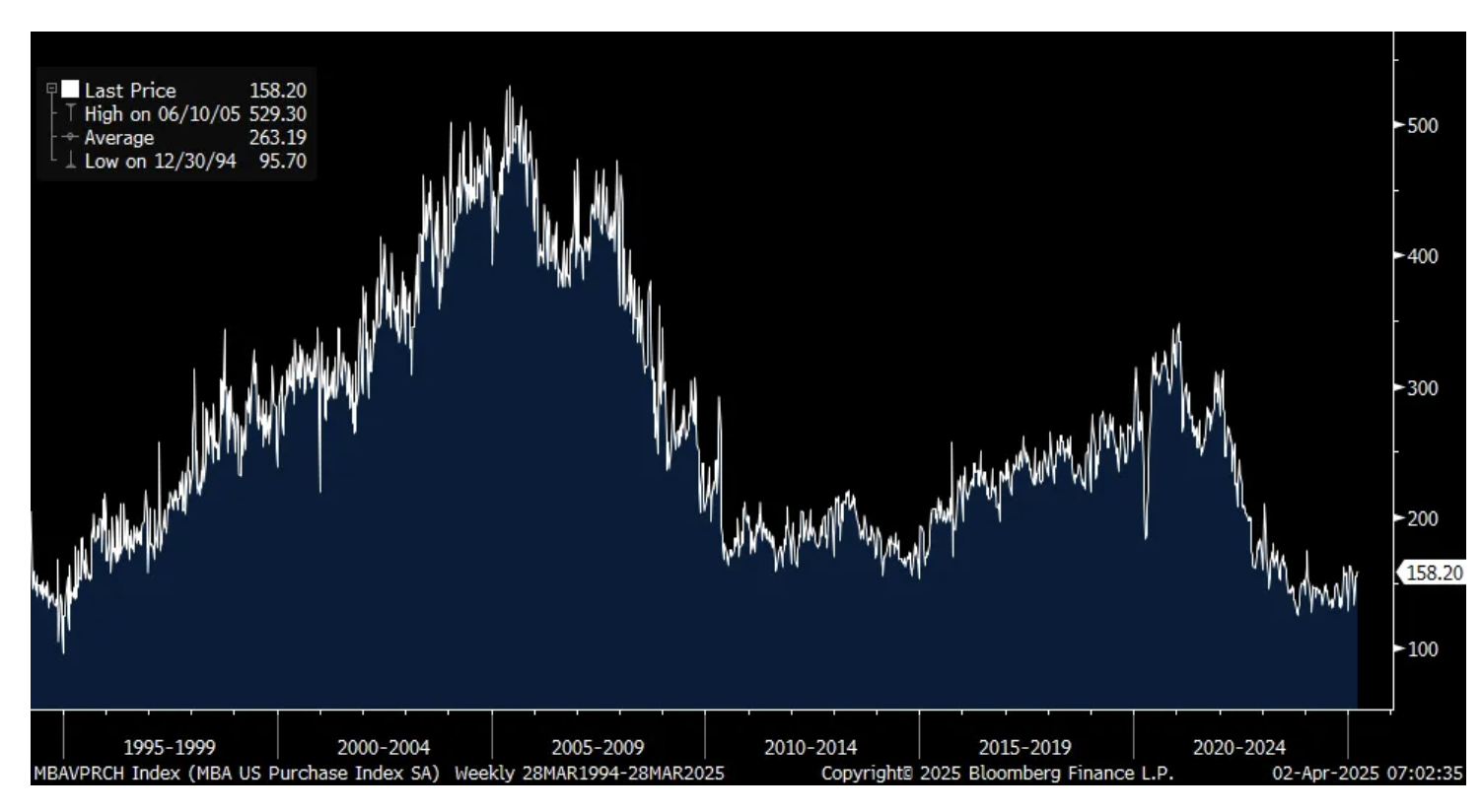

The average 30 yr mortgage rate was 6.70% for the week ended 3/28, little changed w/o/w. Purchases lifted by 1.5% but refi's fell by 5.6%, and down for a 3rd week. This is the key selling season as about half of all annual sales take place in this time frame but as seen in the chart below, purchase applications are still bouncing around 30 yr lows.

Purchase Applications.

BY Doug Kass · Apr 2, 2025, 9:53 AM EDT

Since I will be out of the office most of the morning and as I have aggressively been on the long side, here are today's "Things":

* Added reasonable size in the indexes: SPY $556.69 QQQ $468.07

* Increased tech holdings: AMZN $189.12, GOOGL $155.54, META $575, MSFT $378.31

* Increased financial holdings: C $69.72 BAC $41.06 WFC $70.47 AXP $268.50

BY Doug Kass · Apr 2, 2025, 9:48 AM EDT

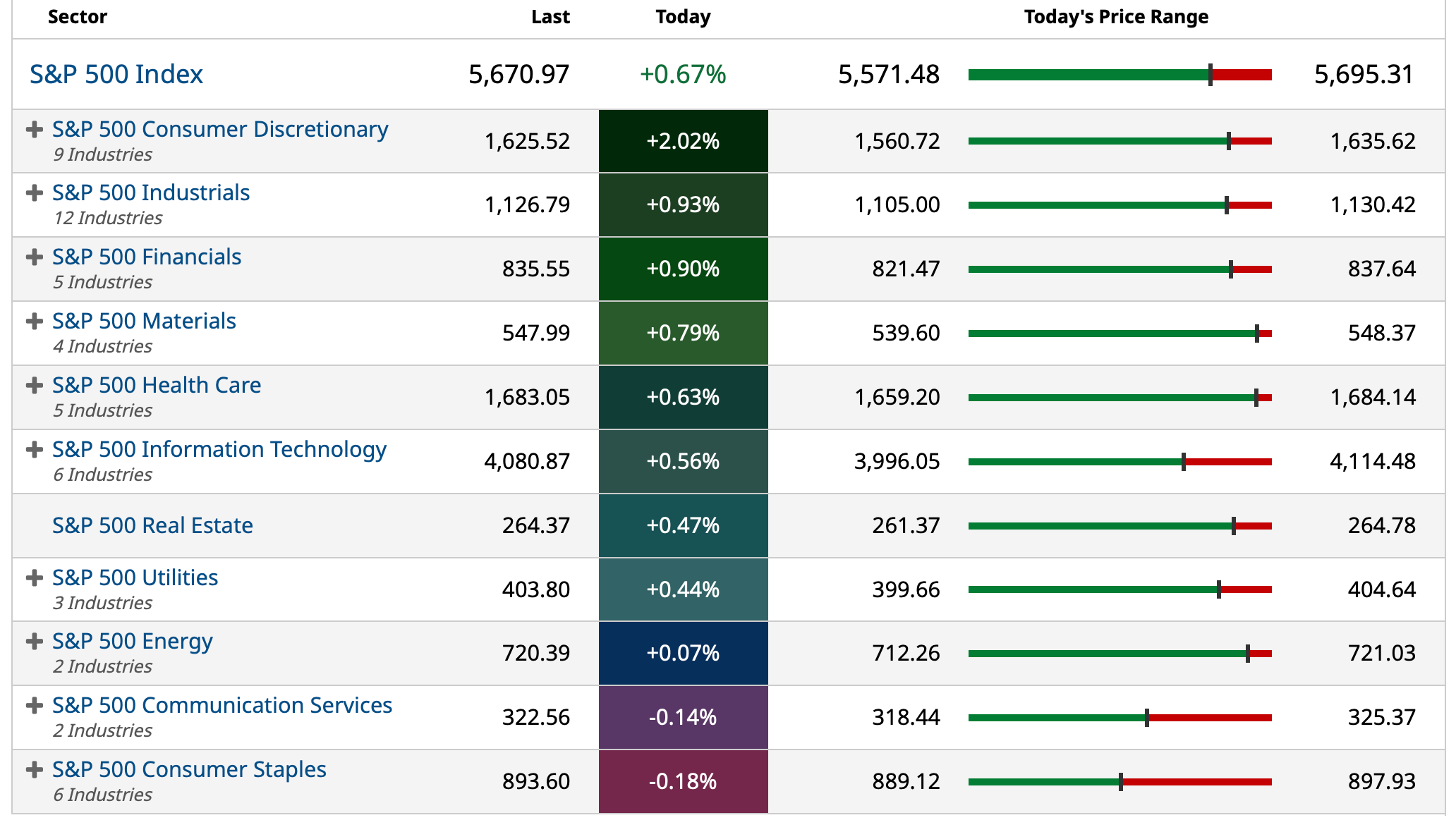

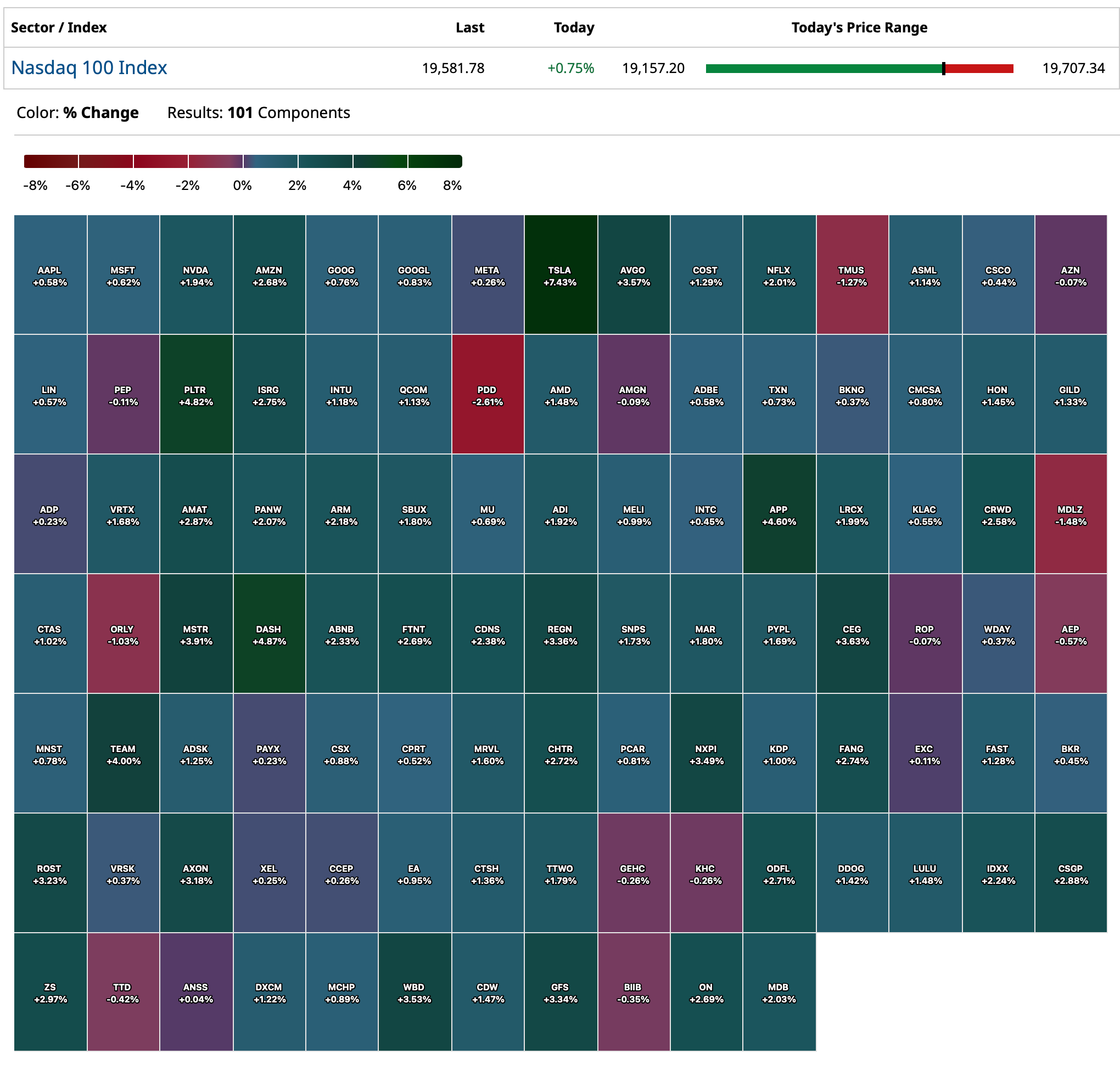

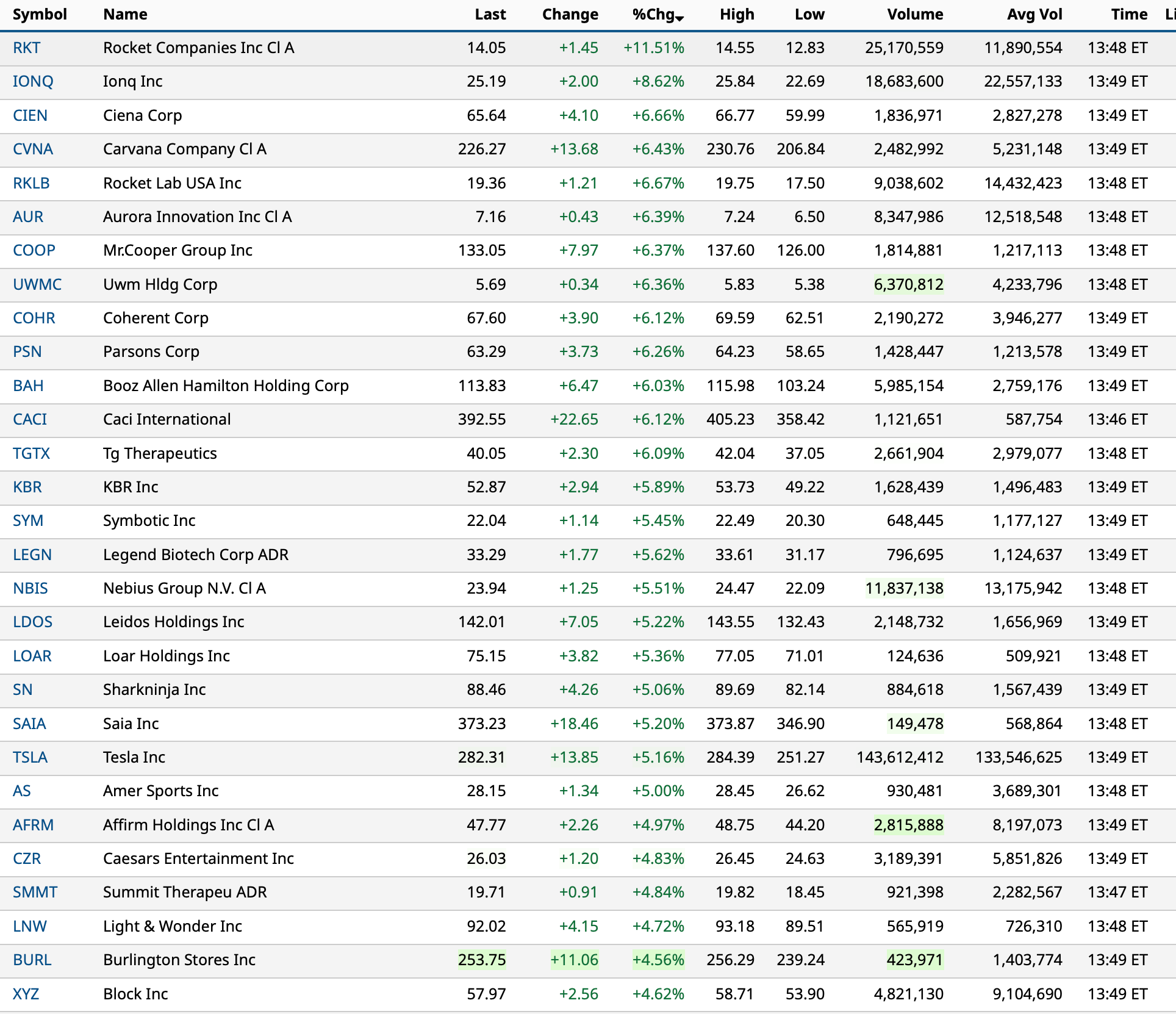

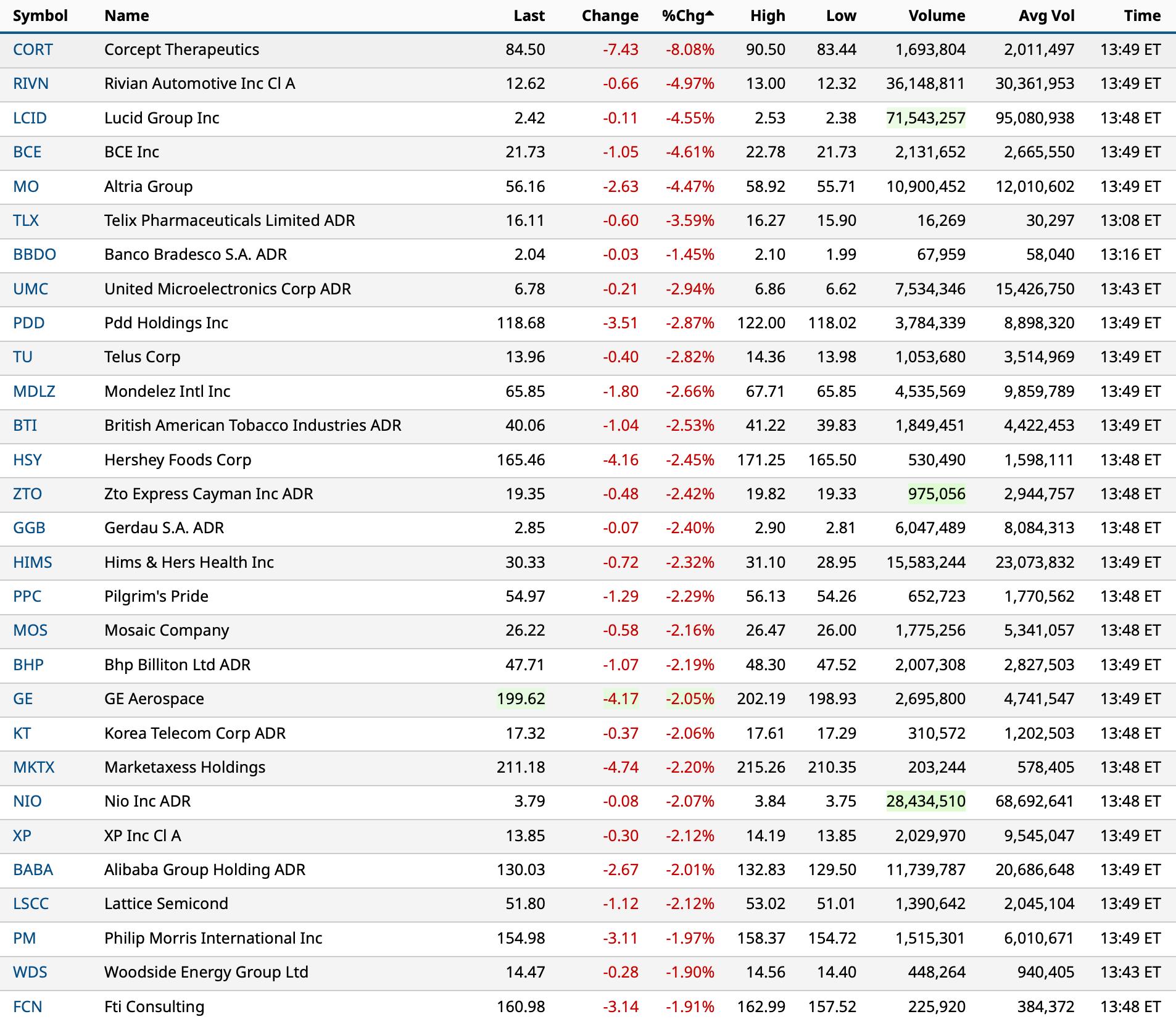

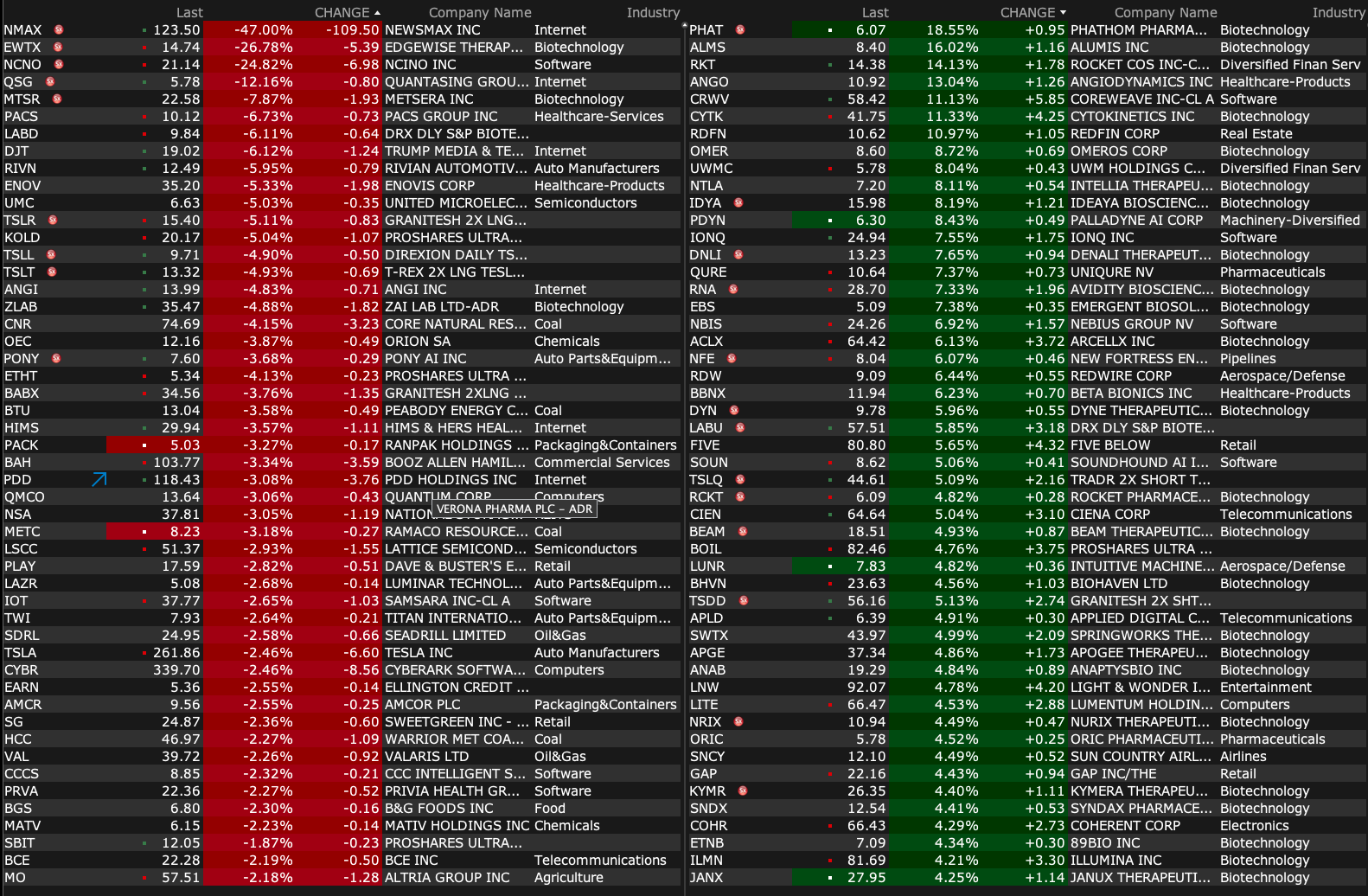

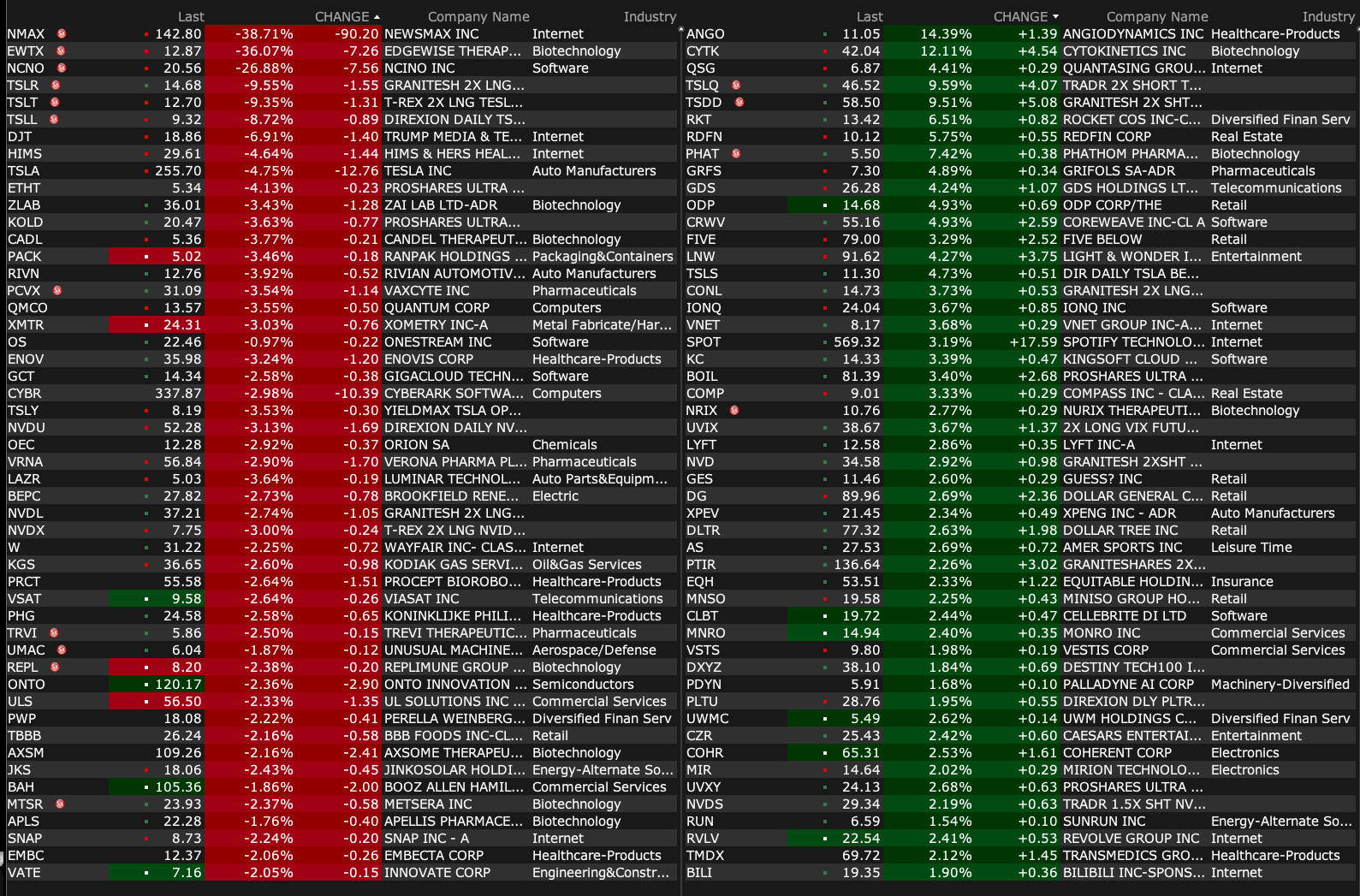

Percentage movers shortly after the open at 9:39 a.m. ET:

BY Doug Kass · Apr 2, 2025, 9:46 AM EDT

I have been more aggressive on the buy side (on weakness) in premarket trading than I have been for awhile.

I will do "Things Today" with stocks/prices shortly because I will be out most of the afternoon.

BY Doug Kass · Apr 2, 2025, 9:40 AM EDT

-QNRX +90% (announces additional positive ‘Whole Body’ clinical data from ongoing Pediatric Netherton Syndrome Study and approval to Initiate testing of a second pediatric patient)

-SBFM +50% (announces results of mRNA cancer therapy)

-ALLK +46% (enters into agreement to be acquired by Concentra Biosciences, LLC for $0.33/shr in cash)

-SPWH +36% (earnings, guidance)

-TTEC +24% (Special Committee completed review and preliminary value of TTEC, and is ready to consider, and engage with, CEO's $6.85/shr proposal)

-ANGO +14% (earnings, guidance)

-NRGV +12% (signs 10-year, >30GWh Licensee and Royalty Agreement with India’s SPML Infra to Manufacture and Deploy the B-Vault Battery Energy Storage Technology Platform for the Indian Market)

-HOTH +7.7% (announces preclinical data supporting the therapeutic potential of its lead Alzheimer's candidate, HT-ALZ, in improving cognitive function and reducing neuroinflammation in Alzheimer's disease)

-CATX +7.0% (insider purchases of $256K in common shares)

-BOLD +6.9% (files $400M mixed shelf)

-KLTO +6.8% (enters into Share Exchange Agreement with SkyBell Tech and subsidiary SB Security Holdings)

-WOOF +5.7% (CEO Anderson purchases 1.6M shares)

-GRFS +5.6% (Brookfield said to restart talks with the company regarding a possible offer)

-PAL +2.9% (acquires Brothers Auto Transport; financial terms not disclosed)

-ABOS +2.3% (showcases pTau217 Trial Screening Progress in Phase 2 ALTITUDE-AD Trial and Preclinical Research Methods at AD/PD 2025 and AAN Annual Meeting)

-AEHL -36% (announces 1-for-40 reverse stock split)

-NCNO -34% (earnings, guidance)

-EWTX -25% (two participants experienced serious adverse events of AF requiring cardioversion with one participant discontinuing treatment in EDG-7500 Phase 2 CIRRUS-HCM trial for obstructive and nonobstructive hypertrophic cardiomyopathy; prices 9.94M shares at $20.13/shr in $200M underwritten offering)

-NMAX -24% (weakness following strong IPO)

-BB -13% (earnings, guidance)

-DJT -8.1% (files to sell 8.4M shares; Holders file to sell additional stock and warrants)

-HCWB -5.7% (announces 1-for-40 reverse stock split)

-TLSA -5.7% (Johns Hopkins University commences dosing Nasal Foralumab in Phase 2 Multiple Sclerosis Clinical Trial)

-PLTR -3.2% (weakness ahead of ‘Liberation Day’ with concern over potential defense budget cuts)

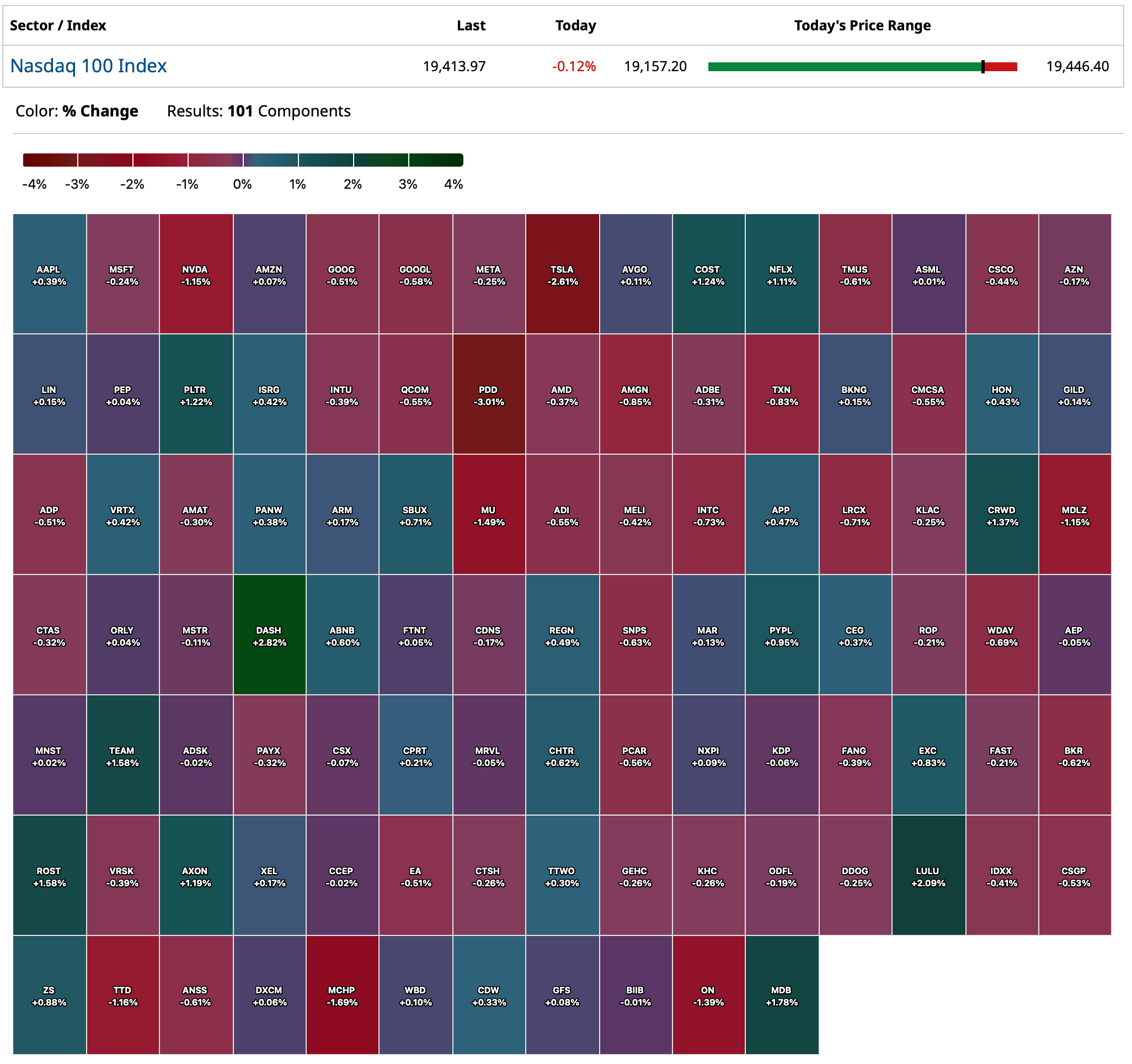

-TSLA -2.6% (reports prelim Mar China deliveries ahead of full Q1 delivery data)

BY Doug Kass · Apr 2, 2025, 9:29 AM EDT

From Peter Boockvar:

ADP said that in March 155k private sector jobs were added to payrolls, 35k more than expected and follows a print of just 84k in the month before (revised up by 7k). Small business picked up their hiring, particularly those with less than 20 employees, adding 52k people, compared to 43k for medium sized companies and 59k for the large ones (those with 500+ employees).

The service sector contributed 132k of the jobs with most coming from professional/business services (57k) and financial services (38k). Leisure/hospitality hired a net 17k, education/health added 12k and ‘information’ was a plus 3k. Trade/transportation/utilities shed 6k.

On the goods side, manufacturing hired 21k jobs which is in direct contrast to the soft data ISM employment component seen yesterday which fell further below 50 at 44.7 and where just 1 of 18 industries surveyed saw an increase in payrolls. Construction added 6k while ‘natural resources/mining’ lost 3k. That sector happened to be the one, primary metals, that ISM said added jobs.

With wages, ‘job stayers’ saw a pay increase of 4.6% vs 4.7% in February. Those changing jobs got a 6.5% raise on average vs 6.7% in the month before. These are still good pay gains but the pace is slowing, in part due to the high comparisons seen last year and a slowing quit rate.

From ADP, “Despite policy uncertainty and downbeat consumers, the bottom line is this: The March topline number was a good one for the economy and employers of all sizes, if not necessarily all sectors.” We’ll see Friday if the BLS agrees. The estimate for Friday’s private sector read is 135k.

The 3 month average is now 142k vs the 6 month average of 171k and the one year average of 155k. As markets respond to the BLS report and not ADP, Treasury yields are where they were at 8:14am est, lower again on the day with growing economic growth worries.

My bottom line, I just don’t see how job growth doesn’t slow down from here with the lack of much visibility.

BY Doug Kass · Apr 2, 2025, 8:59 AM EDT

Adding back to GOOGL, AMZN and the banks/selected financials in premarket weakness

BY Doug Kass · Apr 2, 2025, 8:44 AM EDT

BY Doug Kass · Apr 2, 2025, 8:38 AM EDT

Adding to:

* SPY $556.19

* QQQ $467.50

BY Doug Kass · Apr 2, 2025, 8:24 AM EDT

Love me two times, girl

One for tomorrow

One just for today

Love me two times

I'm goin' away

Love me one time

Could not speak

Love me one time

Yeah, my knees got weak

- The Doors, Love Me Two Times

I had a good day trading the indices on Tuesday — buying weakness and selling strength (two times). (See Greatest Trading Market just posted)

With S&P futures -35 handles (7:15 a.m.) I am back buying the indices:

* SPY $557.77

* QQQ $469.17

From yesterday:

With the S&P now +40 handles after being down by -48 handles this morning, I am selling calls against the (SPY) / (QQQ) purchases (in the hole) early this morning.

Good trade.

By Doug Kass Apr 1, 2025 12:25 PM EDT

BY Doug Kass · Apr 2, 2025, 7:45 AM EDT

* In a market with no memory from hour to hour.

We have entered a period of heightened uncertainty (in policy and economic/corporate profit expectations), which has produced the sort of volatile markets we haven't seen in years.

As an example, yesterday the S&P 500 Index initially fell by nearly -1%, rallied by almost +2%, fell by -1% and rallied +1% near the close. (Following that positive late-day momentum, S&P futures are -20 handles at 5:40 a.m.).

This is the greatest market for opportunistic and unemotional traders. It is time consumptive and intense and requires boldness, dispassion and strong risk management/control. (Ergo, it is not for most!)

But today's market is not so great for the buy-and-hold crowd.

I see no reason why this will not continue.

So, either relish in the opportunity (as I have tried to do with my index trading) or sit back with above-average cash reserves and be patient for long-term investment opportunities.

BY Doug Kass · Apr 2, 2025, 7:00 AM EDT

BY Doug Kass · Apr 2, 2025, 6:50 AM EDT

BY Doug Kass · Apr 2, 2025, 6:35 AM EDT

BY Doug Kass · Apr 2, 2025, 6:25 AM EDT

I will be giving a lecture from 2-5 p.m. today so my posts will be sparse this afternoon.

A heads up.

BY Doug Kass · Apr 2, 2025, 6:15 AM EDT

The S&P Short Range Oscillator is less oversold.

The Oscillator is now at -1.29% vs. -2.52%.

Note: From a short-term tactics purpose I often use the Oscillator as a guide.

When the Oscillator is less oversold (as it is now) or more overbought I tend to hold back and wait to take on rental longs only when the market is under pressure — and visa versa.

BY Doug Kass · Apr 2, 2025, 5:59 AM EDT

Wolf Street on "locked In" homeowners.

BY Doug Kass · Apr 2, 2025, 5:54 AM EDT