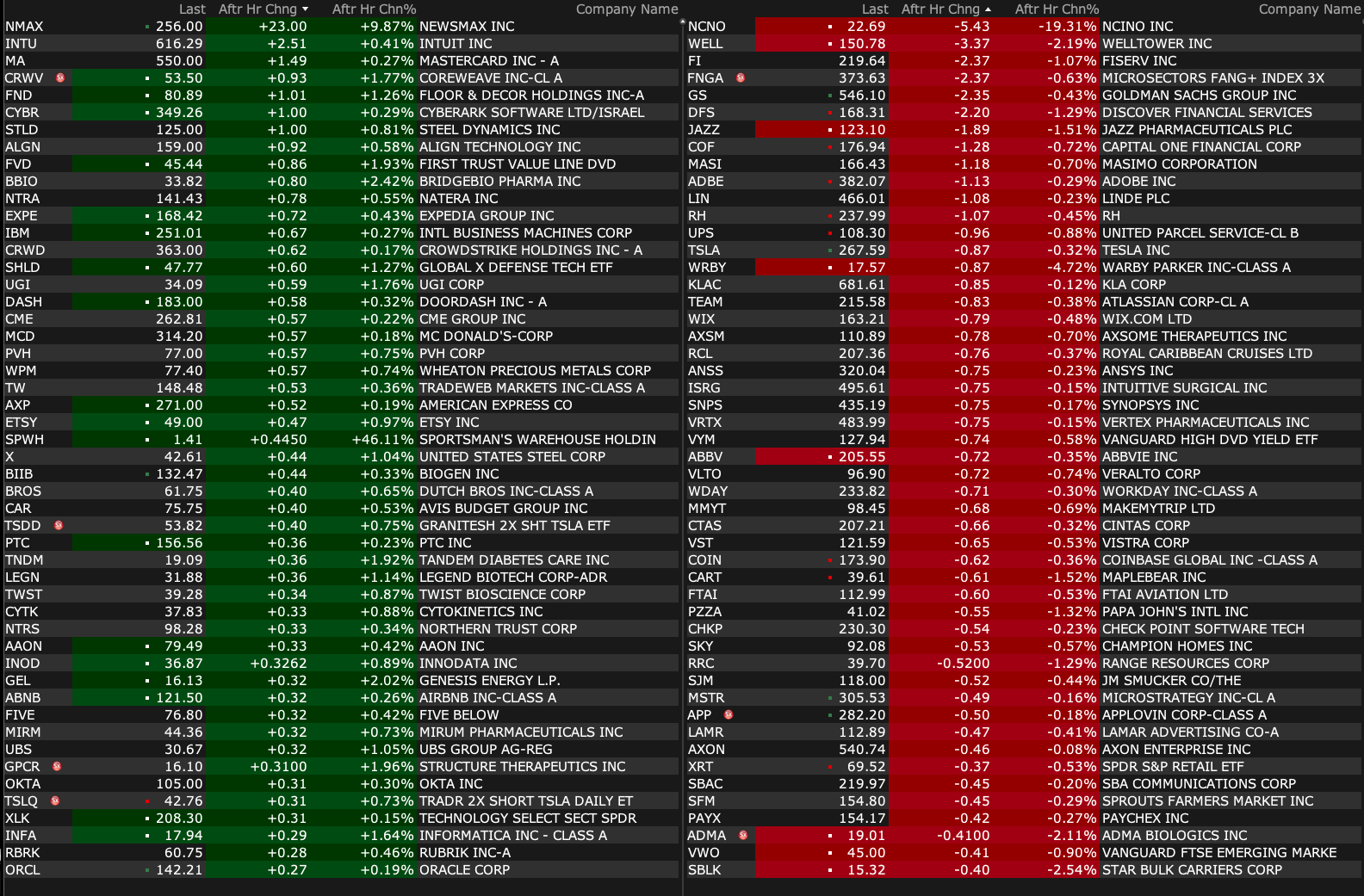

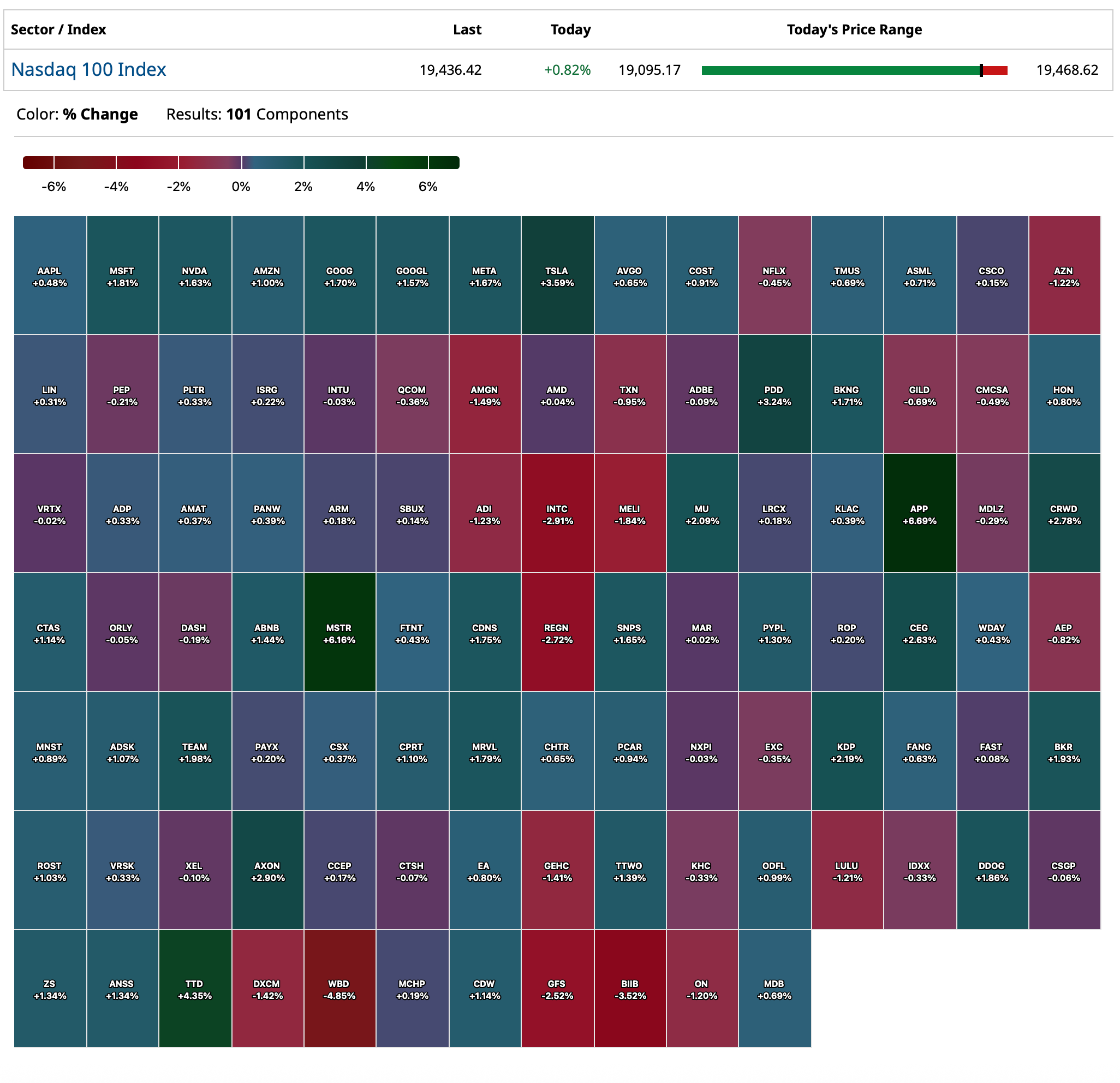

Tuesday's After-Hours Movers

At 4:20 p.m.:

BY Doug Kass · Apr 1, 2025, 4:55 PM EDT

At 4:20 p.m.:

BY Doug Kass · Apr 1, 2025, 4:55 PM EDT

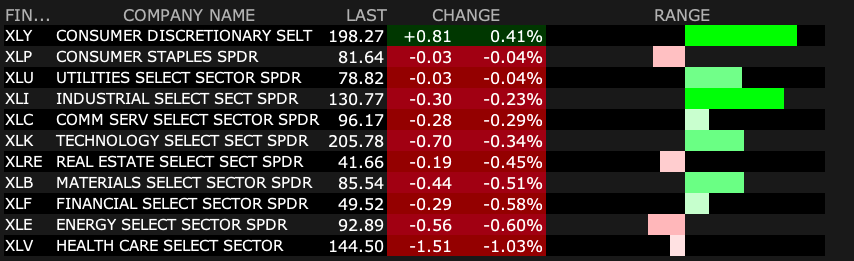

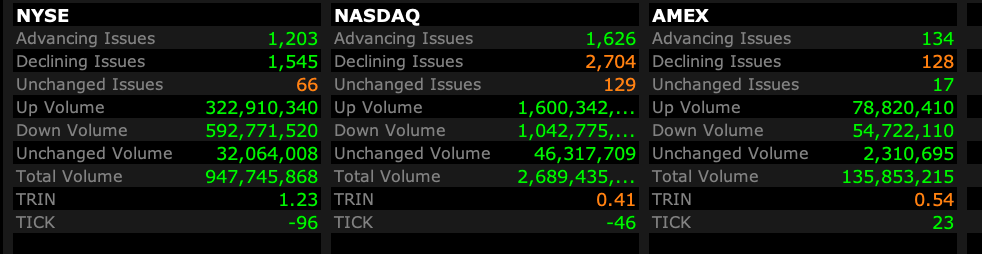

BY Doug Kass · Apr 1, 2025, 4:46 PM EDT

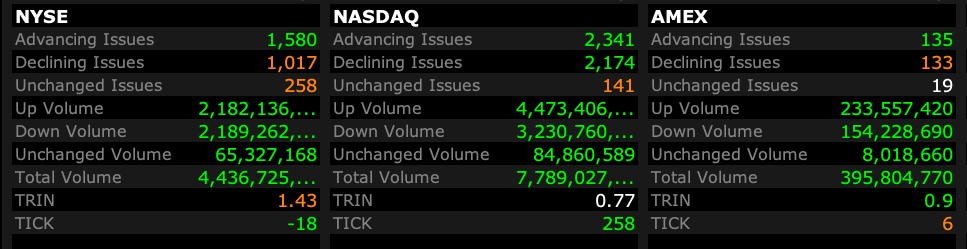

- NYSE volume 12% below its one-month average

- NASDAQ volume 6% above its one-month average

- VIX index: down 2.29% to 21.77

BY Doug Kass · Apr 1, 2025, 4:35 PM EDT

My old pal, Macke Truck on 5 Rules for a Bear Market:

BY Doug Kass · Apr 1, 2025, 2:50 PM EDT

TechNova

BTC : A follow up to my post last night after the market close.

I mentioned that the reason I did not agree with my Crypto Analyst friend that was calling for BTC at $50K is that Donnie and Team will need to rain money on people to prevent what may actually turn into a Depression.

You may remember the Amazing DOGE Dividend checks that were going to be made based on the Non-Existent Trillions in Savings, well, now we have the Tariffs Dividend Checks on the Non-Existent Trillions in Revenue.

Make no mistake.

Wether it is fake DOGE checks, or fake Tariffs checks, Checks will be written, and we will expand the debt to cover them.

Donnie is already talking about large disbursements to farmers AGAIN, because he ruined their trade routes AGAIN.

Between checks, checks and more checks. The debt will balloon.

I expect BTC to sniff this out before Equities do.

Separately:

Let's think about this. We Tariff American Citizens. They pay the Tax. Then we issue Checks, based on the Tariffs, back to American Citizens.

Since the bottom half of Americans pay most of the Sales Taxes and Tariffs (they consume a larger portion of their income), and we will then re-distribute their money to all Americans... is that not the textbook definition of Wealth Re-distribution? Wasn't that something we blamed the Dems for?

BY Doug Kass · Apr 1, 2025, 2:02 PM EDT

BY Doug Kass · Apr 1, 2025, 1:25 PM EDT

I will be leaving at about 3 p.m. today as I have an appointment with an allergist.

BY Doug Kass · Apr 1, 2025, 1:15 PM EDT

With volatility high and predictability low in a "newsy" setting I am still playing "small ball."

BY Doug Kass · Apr 1, 2025, 12:55 PM EDT

* Informative...

BY Doug Kass · Apr 1, 2025, 12:49 PM EDT

BY Doug Kass · Apr 1, 2025, 12:35 PM EDT

With the S&P now +40 handles after being down by -48 handles this morning, I am selling calls against the SPY/QQQ purchases (in the hole) early this morning.

Good trade.

BY Doug Kass · Apr 1, 2025, 12:25 PM EDT

I'm adding to Coca-Cola KO short at last sale.

BY Doug Kass · Apr 1, 2025, 12:10 PM EDT

BY Doug Kass · Apr 1, 2025, 11:40 AM EDT

MRKT CALL — rich in humility, value-added research and actionable ideas — with my pals Dan and Guy.

Be there or be square!

And it's free.

Let's go to the tape. Traders Brace for Tariff Tantrum

BY Doug Kass · Apr 1, 2025, 11:27 AM EDT

From Peter Boockvar:

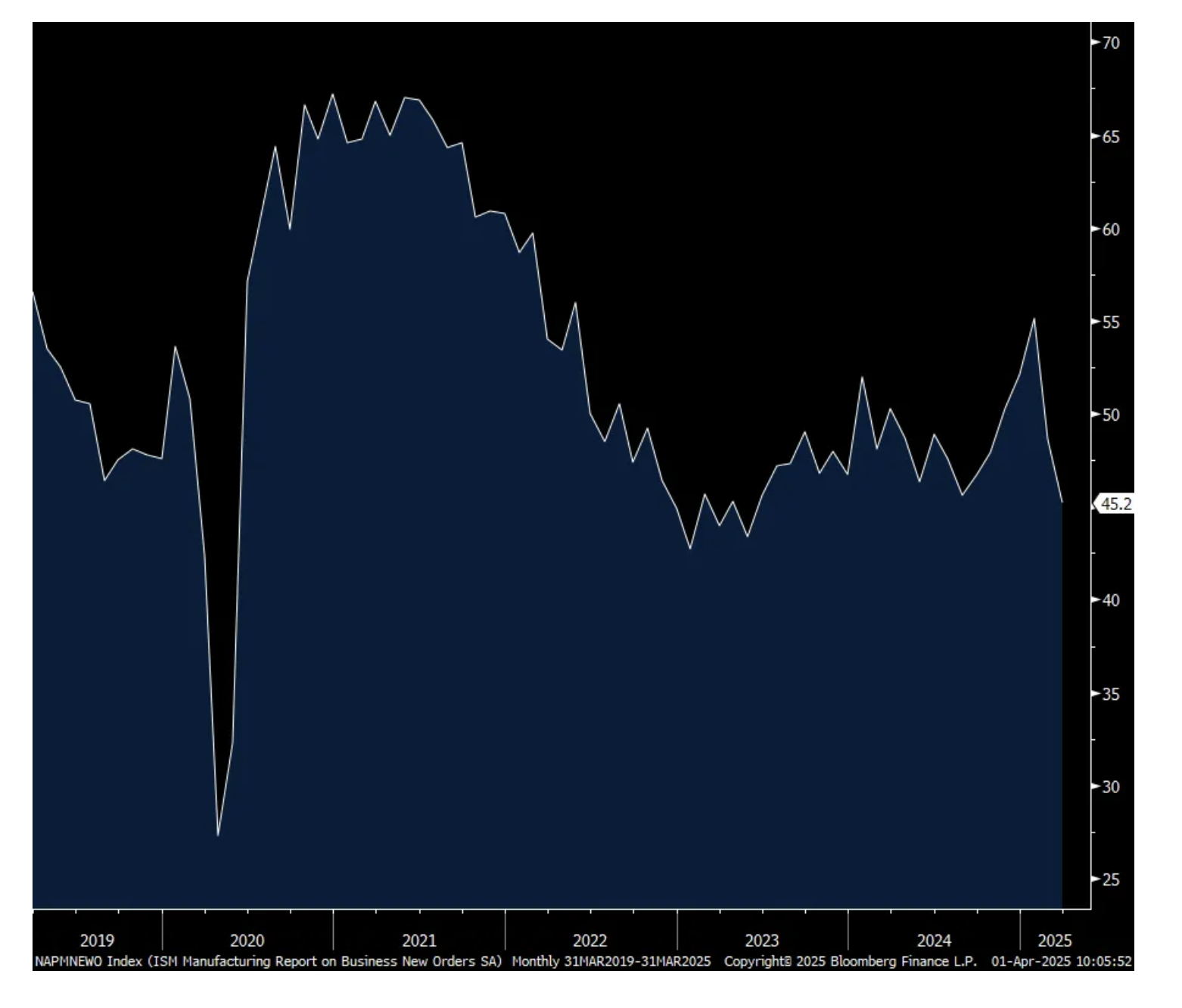

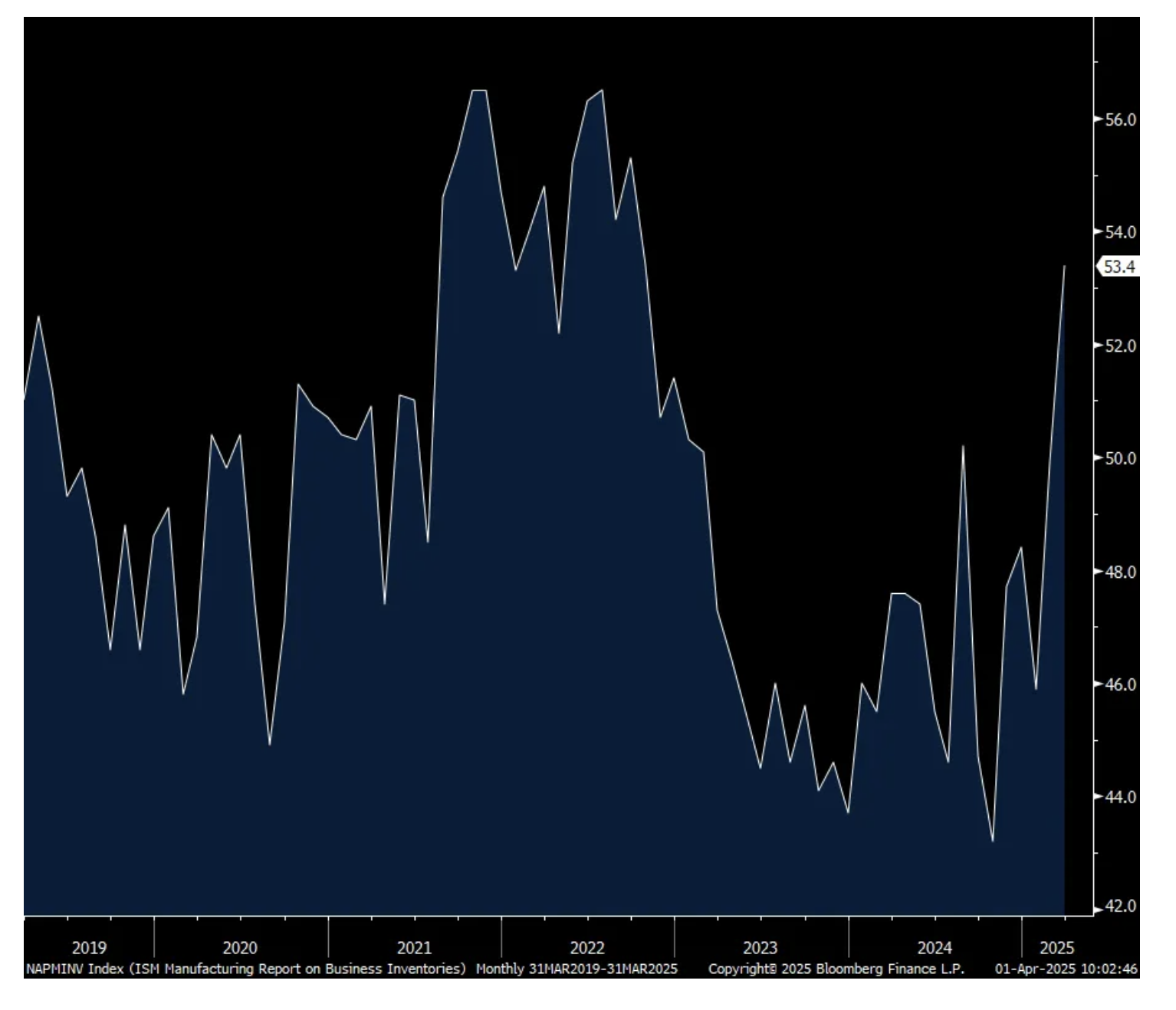

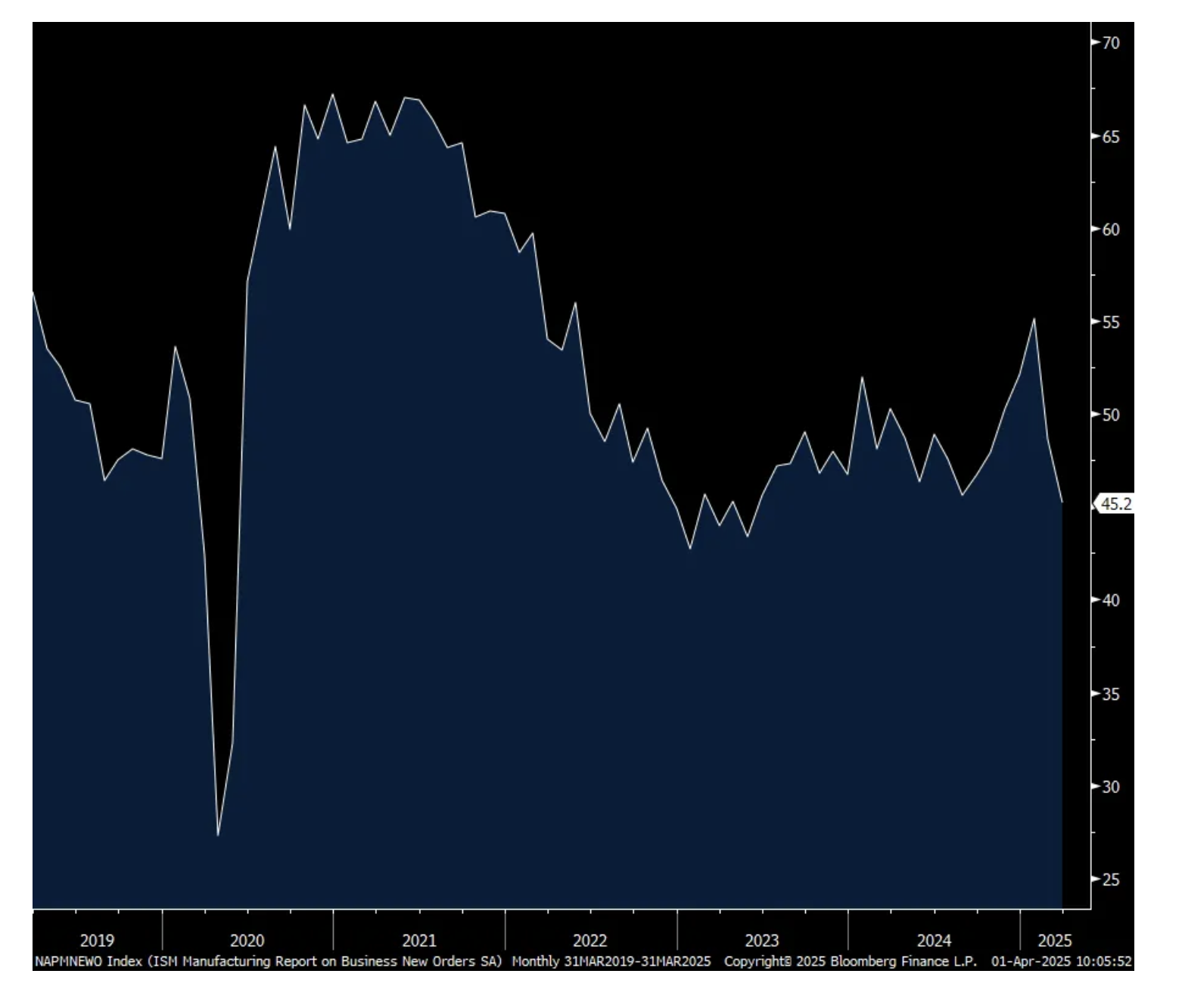

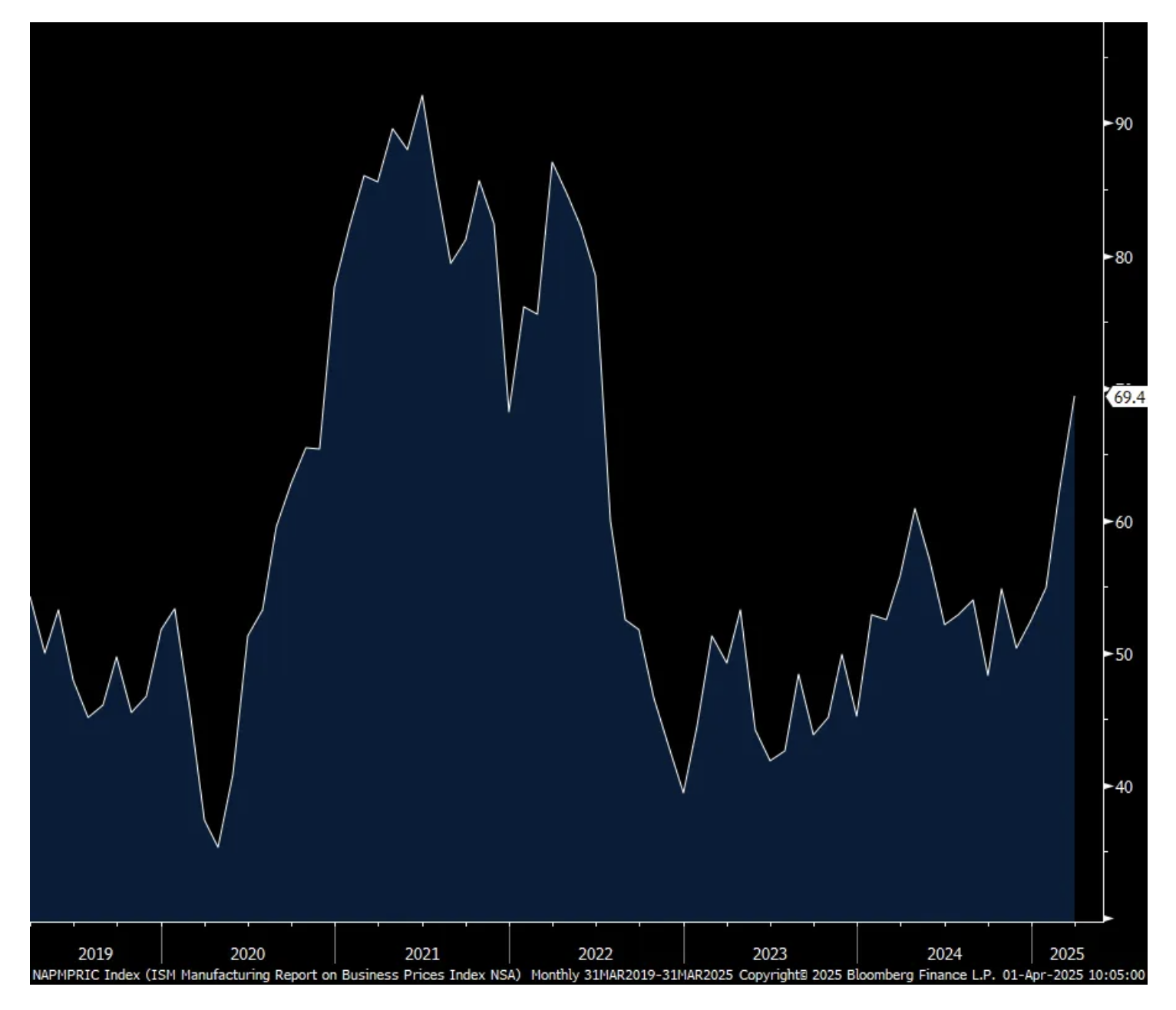

The March ISM manufacturing index fell back under 50 to 49 after two months above and just below the estimate of 49.5. The internals were pretty interesting.

Assuming that the first two months of the year included a bunch of tariff front loading, the March aftermath had inventories rising to 53.4 from 49.9 and that’s the highest since September 2022. New orders touched 55.1 in January and stand at 45.2 in March. Combining the two I guess is the definition of ‘pull forward’ or maybe companies are not seeing the growth they anticipated as we entered the year. Ahead of the jobs data this week, the employment component fell to 44.7 from 47.6 and that’s the lowest since September.

Export orders also dropped back below 50 at 49.6 from 51.4 and prices paid jumped by 7 pts to 69.4 and that is the highest since June 2022. Supplier deliveries fell 1 pt but after rising by 3.6 pts last month. The higher this figure is, the slower the deliveries and vice versa.

Regarding inventories, ISM said “Manufacturing inventories expanded in March, as panelists’ companies continue to pull forward (advance) deliveries of materials in an attempt to minimize the financial impacts of potential tariffs.”

With new orders, ISM said “Orders continue to slow, as discussions about who will pay for potential tariff costs are the prime topic of negotiations between buyers and sellers.”

On the labor market, “Freezing and attrition were the primary tools used for the 2nd straight month, in lieu of the more dramatic and costly layoff process.” There was just ONE industry of 18 surveyed that saw a rise in employment and that was in ‘primary metals’ and we can assume helped by the rise in prices.

Pushing prices paid higher was “driven by dramatic increases in steel and aluminum prices as a result of recently deployed tariffs. Corrugate, copper and plastic resins have all experienced price growth as companies move to minimize their exposure to foreign made goods, causing domestic prices to rise amid new demand.” 15 of 18 industries surveyed paid higher prices.

Overall breadth softened a touch with 9 industries seeing growth vs 10 last month. Those seeing a contraction totaled 7 vs 5 in the month before. One saw no change.

To the point above about 2025 growth rates not being realized year to date, a respondent in the chemical industry said this, “Complex markets saw a surge in volume buying in anticipation of 2025 being slightly better than 2024. In March, however, all markets saw a slowdown, with fear and inventory stocking to hold through a potential crisis.”

The rest of the comments are littered with tariff talk.

Bottom line, just as there was hope that manufacturing was bottoming, the challenges continue with a new set of concerns.

ISM Mfr’g

New Orders

Prices Paid

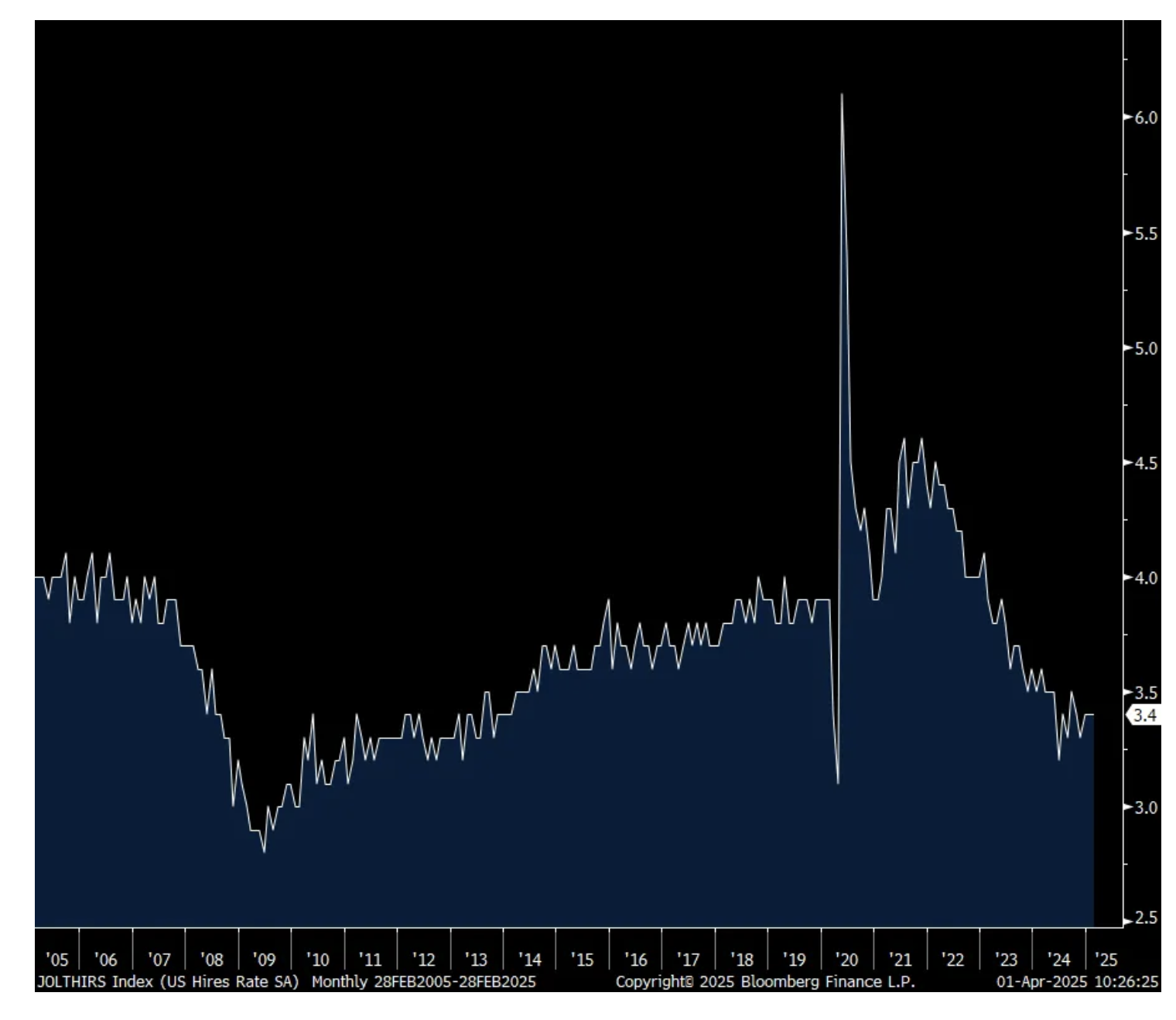

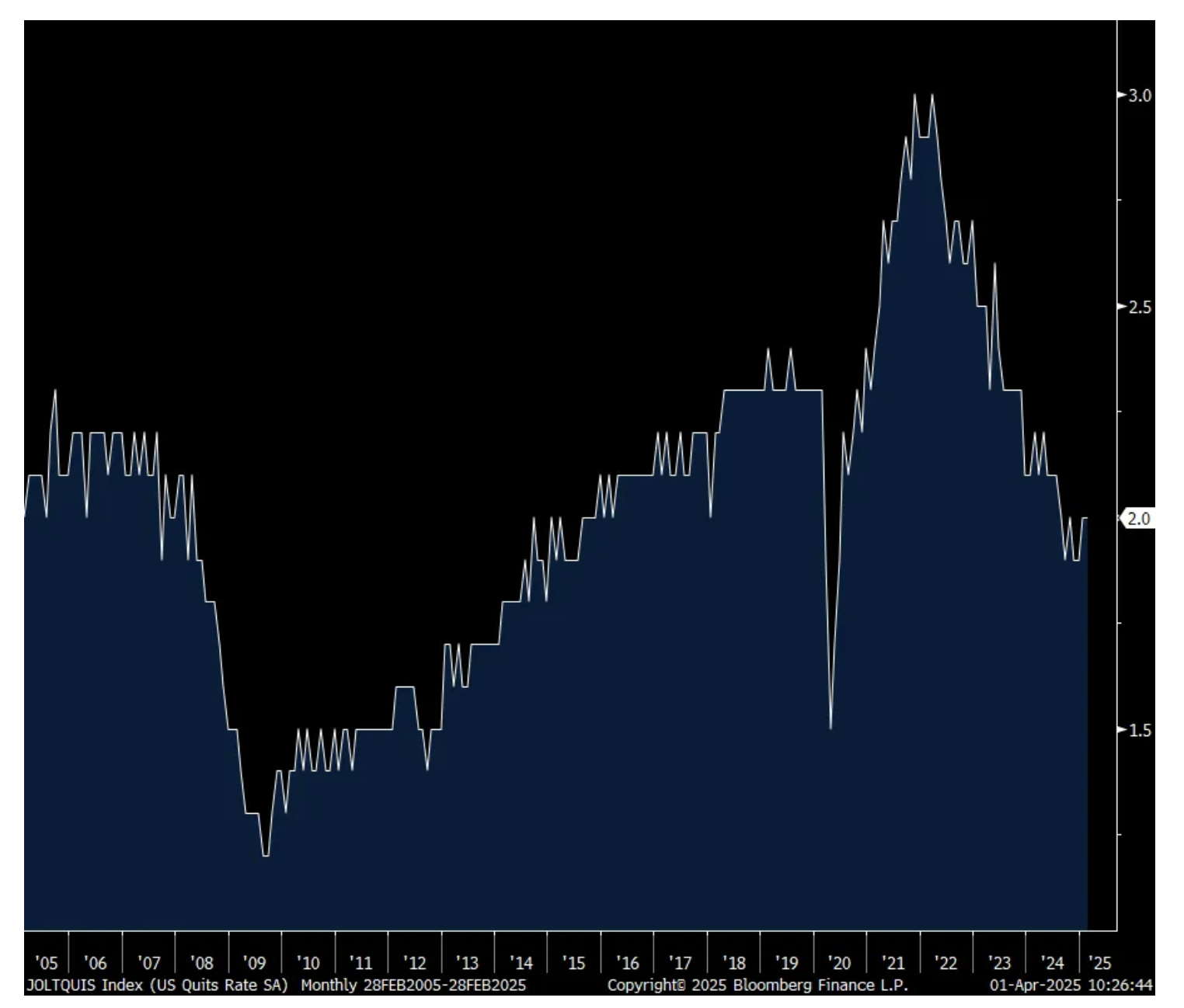

Job openings in February, thus dated data, totaled 7.568mm. That’s 90k below expectations and down from 7.762mm in January. The hiring rate held at 3.4% for a 3rd month and the quit rate was unchanged at 2%.

The DOGE cuts are slightly reflected here as there are 138,000 federal government job openings vs 132k in January and 138k in December. In October it was 142,000.

With job data in the days ahead, nothing market moving here.

Job Openings

Hiring Rate

Quit Rate

BY Doug Kass · Apr 1, 2025, 11:12 AM EDT

* SPY $554.63

* QQQ $465.37

BY Doug Kass · Apr 1, 2025, 10:33 AM EDT

The RSP (equal weighted S&P Index) is -0.84%.

This is keeping me from buying back much of what I sold into yesterday afternoon's rally.

That said I am picking (very small) in AMZN $189.46, GOOGL $156.08, GS $535.46, BAC $41.09, WFC $70.39 and C $69.50 - with he S&P futures -35 handles.

BY Doug Kass · Apr 1, 2025, 10:20 AM EDT

From Peter Boockvar:

I'll say again, the political world is really upside down when you have Democrats blasting tariffs which are taxes and you have Republicans embracing them. I'll give another Grateful Dead quote, "The sky was yellow and the sun was blue" from Scarlet Begonias. I know it is more nuanced than that with the possibility that foreigners would pay more of the tariff/tax via product discounts and/or US dollar strength but you get my point.

I am very sympathetic to the reciprocity angle to even out and hopefully lower global tariffs in the aggregate with other countries and I want to see more US manufacturing jobs too but the former is seemingly easier to figure out than the latter in terms of both negotiation and clear results. The latter is a 'fingers crossed' that it works with any results only years in the future. Otherwise, using tariffs mostly just to raise revenue and believing that it will lower the US budget deficit relative to GDP, there is one lesson we should all have learned over MANY decades and that is regardless of tax rates, both high and low, tax revenue as a percent of GDP has averaged about 17%. It is spending where our finances have gone off the rails and where it currently sits at about 24% vs a long term average closer to 20%. Finally, we've likely only seen the beginning of retaliatory tariffs on us if what we see tomorrow is more than just reciprocity. EC President Ursula von der Leyen said today, "We do not necessarily want to retaliate" but, "If necessary we have a strong plan to retaliate and will use it."

Either way, may tomorrow bring whatever tariffs we will see so companies and households can all adjust.

On the global travel side, the impact of tariffs is already here. Air Canada had its annual meeting yesterday and Bloomberg News is reporting that the airline is seeing "a 10% decline in bookings for transborder flights between Canada and the US for the April to September period compared to last year." "Am I concerned?," Chairman Vagn Sorensen said in a response to a question from a shareholder during Monday's meeting. "Yes, definitely, I'm concerned."

The CEO of Accor, the big European based hotel company with a variety of brands across the price spectrum like Fairmont, Delano, Mondrian, Novotel, Raffles, Sofitel, SLS and Swisshol, was on Bloomberg TV today and said vacationers are "deciding to change destination, to go to Canada instead of going to America, to go to South America or Egypt." He said bookings from Europe to the US are down 25% this summer.

While we have a large trade deficit in goods, we have a large surplus when it comes to services, particularly travel.

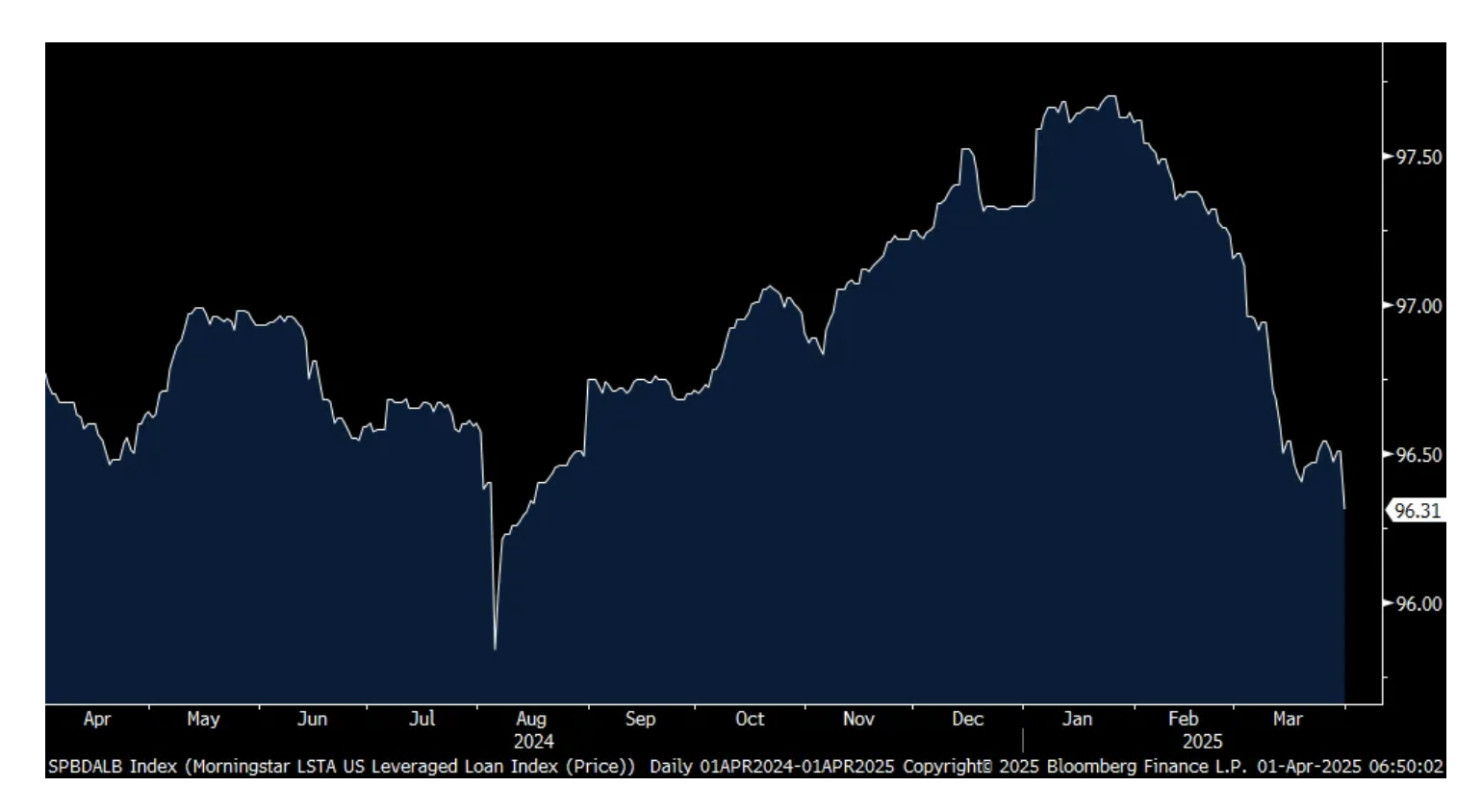

Here is a quick credit check, the LSTA leveraged loan index closed yesterday at the lowest since mid August 2024. I watch this index each day and is reflecting both expectations of more Fed rate cuts where this is floating rate debt and the credit quality of credits would be considered 'junk.'

LSTA Leveraged Loan Index

From PVH with brands like Calvin Klein and Tommy Hilfiger among others and whose stock is popping higher this morning with better than expected earnings and full year guidance:

"In a challenging macro, we delivered another year of strong profitability in North America, drove sequential improvements in our wholesale order books in Europe while improving our quality of sales, and we achieved our third consecutive year of growth in Asia Pacific, on a constant currency basis."

Ahead of the March US ISM report today, a bunch of manufacturing PMI's came out from overseas and they were mixed but all hovering around 50.

China's Caixin 51.2 vs 50.8

Taiwan 49.8 vs 51.5

Vietnam 50.5 vs 49.2

South Korea 49.1 vs 49.9

Thailand 49.9 vs 50.6

Final Japan 48.4 vs 49

Final Australia 52.1 vs 50.4

Specifically from Caixin on China's private sector manufacturers, "Manufacturers saw their promotional efforts pay off as the market improved. In March, output grew for the 17th straight month and at the fastest pace in four months, while the subindex for total new orders stayed in expansionary territory for the 6th straight month. The overseas demand growth momentum recorded in February was extended, with the indicator for new export orders rising to the highest point since last April."

Also, "Businesses remained optimistic. The majority of surveyed companies expressed confidence in the near term economic outlook, although some remained cautious over a potential escalation in global trade tensions."

The March Eurozone manufacturing final PMI was tweaked to 48.6 from 48.7 initially but up 1 pt from February and the highest level since January 2023. The UK read was revised to a still weak 44.9 from 46.9 in February.

Under the hood from S&P Global on the lift, "Things are looking up...A significant part of this movement may have to do with the frontloading of orders from the US ahead of the tariffs, which means some backlash is to be expected in the coming months. However, given the geopolitical developments, there is also increasing speculation that the defense sector will expand significantly over the next few years, with direct and indirect positive effects on the industry."

Also out of Europe was March CPI which rose 2.2% y/o/y as expected and vs 2.3% in February. The core rate was higher by 2.4% vs 2.6% in the month before and one tenth below expectations. This is all before the fiscal spending is about to ramp up in Europe, particularly on defense but also infrastructure in Germany. Services inflation continues to be the main driver of inflation, higher by 3.4% y/o/y while non-energy industrial goods prices were up just .6%.

After cutting its deposit rate to 2.5%, essentially a real rate of zero, it's looking more possible that the ECB takes a pause in April. Bloomberg News yesterday reported that "Several ECB officials are still wavering on whether to cut interest rates next month, according to people familiar with the matter, suggesting the meeting remains far more open than investors are betting." With all the fiscal spending about to come, they should pause.

Growth worries are dominating sovereign bond yields for a 2nd day with yields across the region lower and that is spilling over to another drop in US Treasury yields.

Finally, the Reserve Bank of Australia kept its policy rate unchanged at 4.10% as expected. The usually hawkish Governor Michele Bullock did not lean in any one direction on what comes next and likely why Australian yields and the Aussie$ are little changed. They did talk tariffs in their release by saying "Recent announcements from the United States on tariffs are having an impact on confidence globally and this would likely be amplified if the scope of tariffs widens, or other countries take retaliatory measures."

Also, "Geopolitical uncertainties are also pronounced. These developments are expected to have an adverse effect on global activity, particularly if households and firms delay expenditures pending greater clarity on the outlook."

And why they are non-committal?, "Inflation, however, could move in either direction." Yes it could.

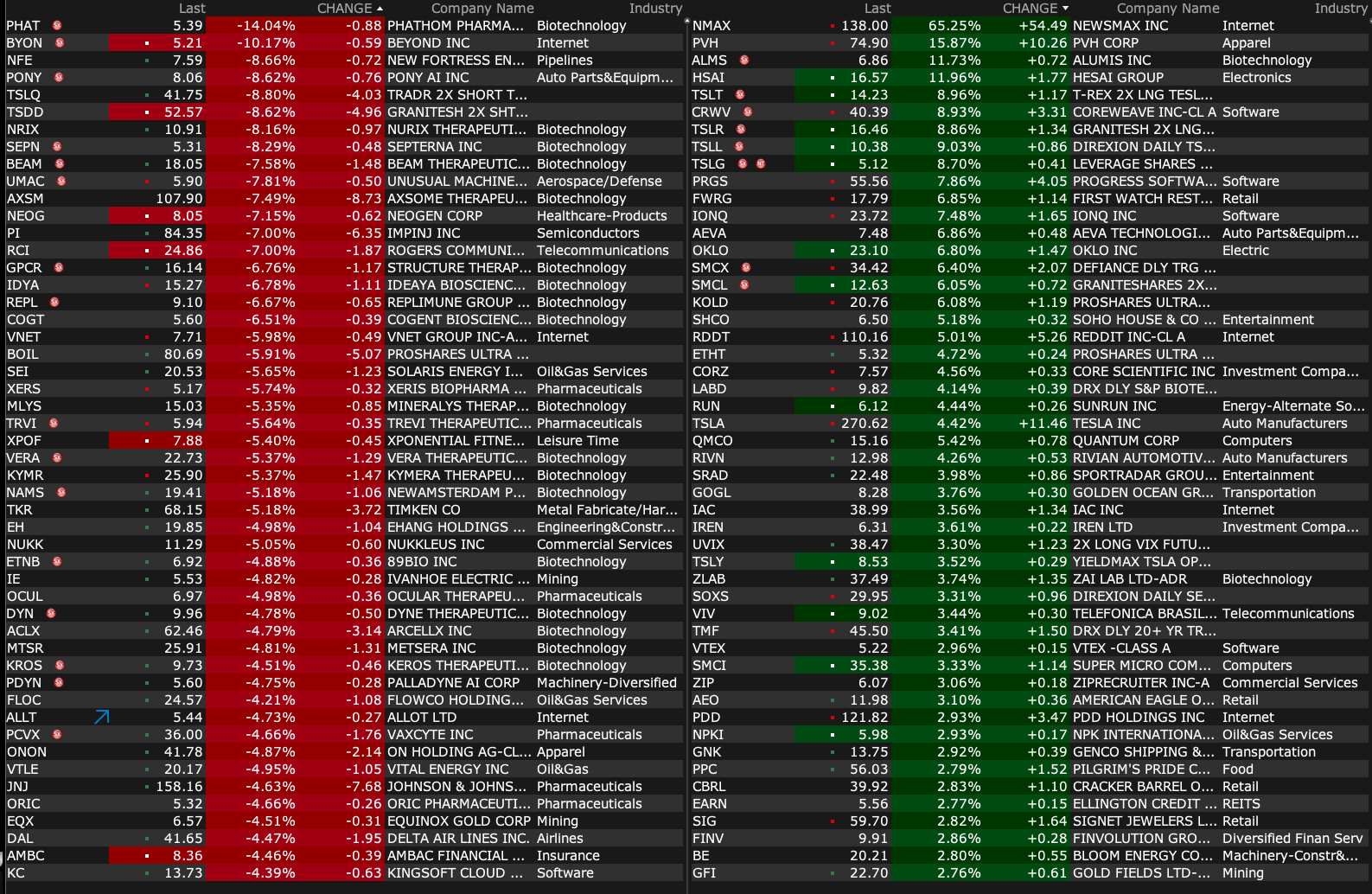

BY Doug Kass · Apr 1, 2025, 9:35 AM EDT

-SATX +67% (MDA Space to buy SATX for ~$193M)

-NUTX +48% (earnings)

-CSAI +28% (earnings)

-TLPH +19% (earnings, guidance)

-PVH +15% (earnings, guidance; announces stock repurchase)

-PSTV +12% (files to withdraw common stock and pre-funded warrant offering of indeterminate amount)

-XAGE +11% (earnings)

-TNXP +10% (launches TONIX ONE, a Fully-Integrated Digital Platform Designed to Help Patients Better Understand and Manage Their Migraine Condition)

-CMPX +9.2% (Tovecimig (CTX-009) Meets Primary Endpoint in the Ongoing Randomized Phase 2/3 Study in Patients with Biliary Tract Cancer)

-MVST +8.6% (earnings, guidance)

-PRGS +7.2% (earnings, guidance; files mixed shelf of indeterminate amount)

-CADL +3.9% (announces Publication of Phase 1b Clinical Trial Data on the Combination of CAN-2409 and Nivolumab plus Standard of Care in Newly Diagnosed High-Grade Glioma Patients)

-SHAK +3.7% (Hearing Loop Capital Raised SHAK to Buy from Hold, price target: $127)

-CGTX +3.4% (presents Results at AD/PD 2025 Showing Impact of Zervimesine (CT1812) on Alzheimer’s Disease Processes)

-IONQ +3.3% (announces IonQ Forte Enterprise)

-KDP +2.0% (Morgan Stanley Raised KDP to Overweight from Equal Weight, price target: $40)

-MSTR +2.0% (Monness Crespi Cuts MSTR to Sell from Hold, price target: $220)

-CMBM -43% (delays annual report; reports prelim Q4 earnings)

-LPRO -16% (earnings, guidance)

-ULBI -7.3% (earnings)

-EE -5.9% (prices upsized ~6.96M shares at $26.50/shr for gross proceeds $184M (prior $150M))

-JNJ -3.7% (confirms the U.S. Bankruptcy Court for the Southern District of Texas denied the request by subsidiary Red River Talc LLC (“Red River”) to confirm its proposed prepackaged bankruptcy plan)

-GRYP -2.9% (earnings)

-AXSM -2.5% (reports topline results of PARADIGM phase 3 proof-of-concept trial of Solriamfetol in Major Depressive Disorder (MDD) with and without Excessive Daytime Sleepiness (EDS))

-GRRR -2.5% (earnings)

-LUV -2.4% (Jefferies Cuts LUV to Underperform from Hold, price target: $28)

-DAL -2.0% (Jefferies Cuts DAL to Hold from Buy, price target: $46)

-AAL -1.9% (Jefferies Cuts AAL to Hold from Buy, price target: $12)

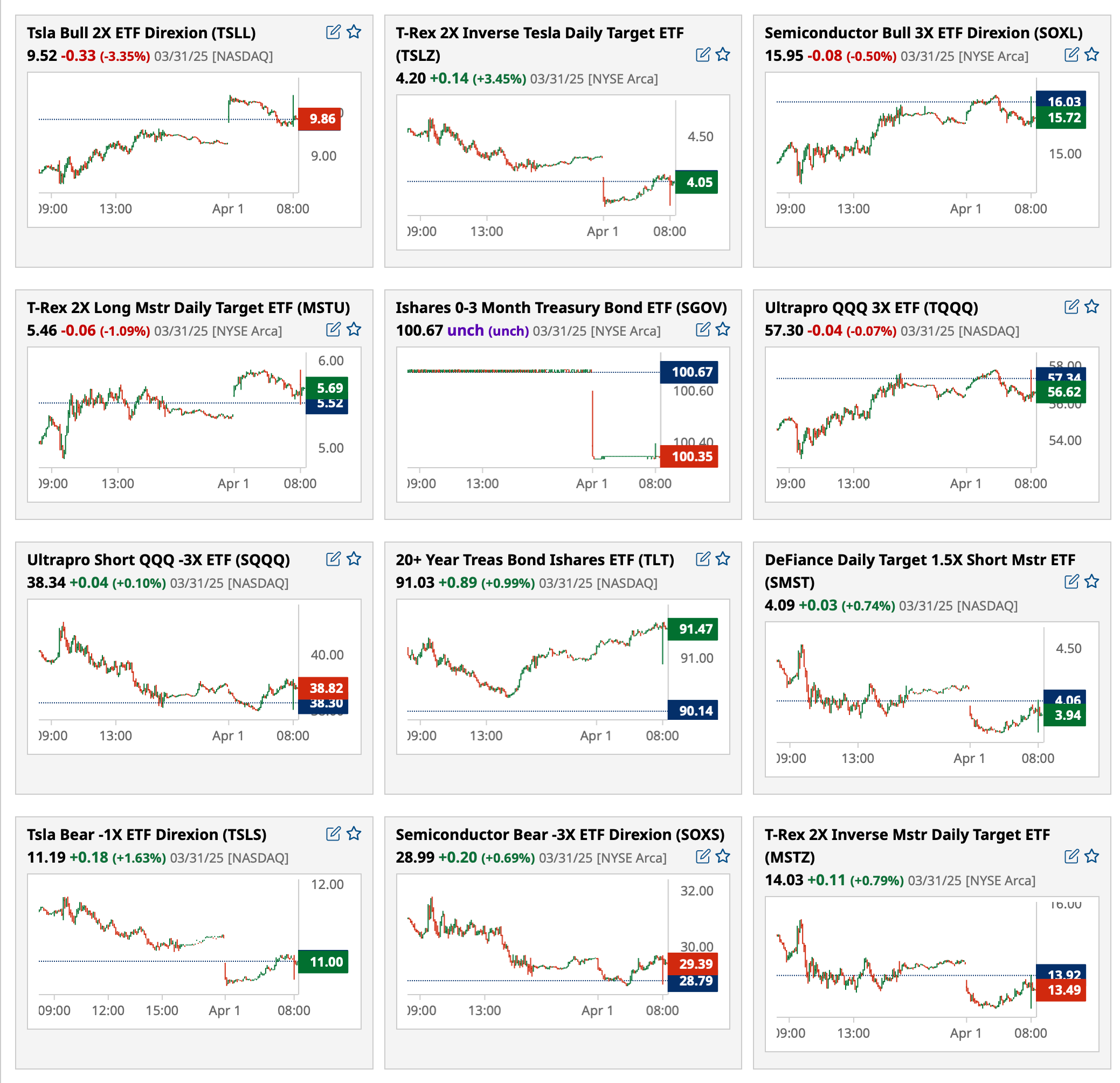

BY Doug Kass · Apr 1, 2025, 9:25 AM EDT

Most active premarket ETFs as of 8:09 a.m. ET:

BY Doug Kass · Apr 1, 2025, 9:15 AM EDT

Premarket percentage movers at 8:29 a.m. ET:

BY Doug Kass · Apr 1, 2025, 9:05 AM EDT

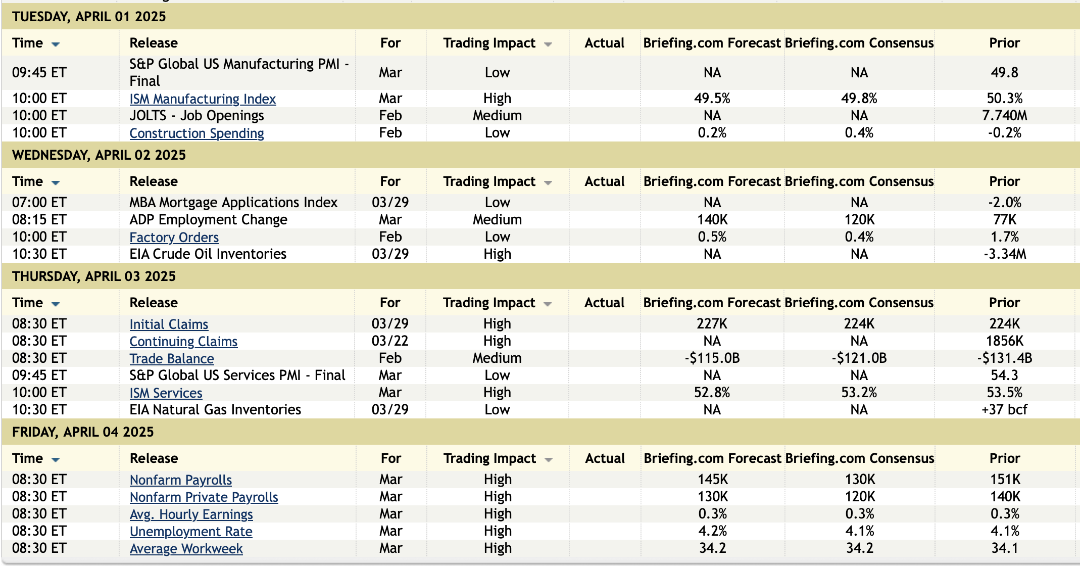

BY Doug Kass · Apr 1, 2025, 8:55 AM EDT

BY Doug Kass · Apr 1, 2025, 8:42 AM EDT

BY Doug Kass · Apr 1, 2025, 8:35 AM EDT

BY Doug Kass · Apr 1, 2025, 8:25 AM EDT

BY Doug Kass · Apr 1, 2025, 8:15 AM EDT

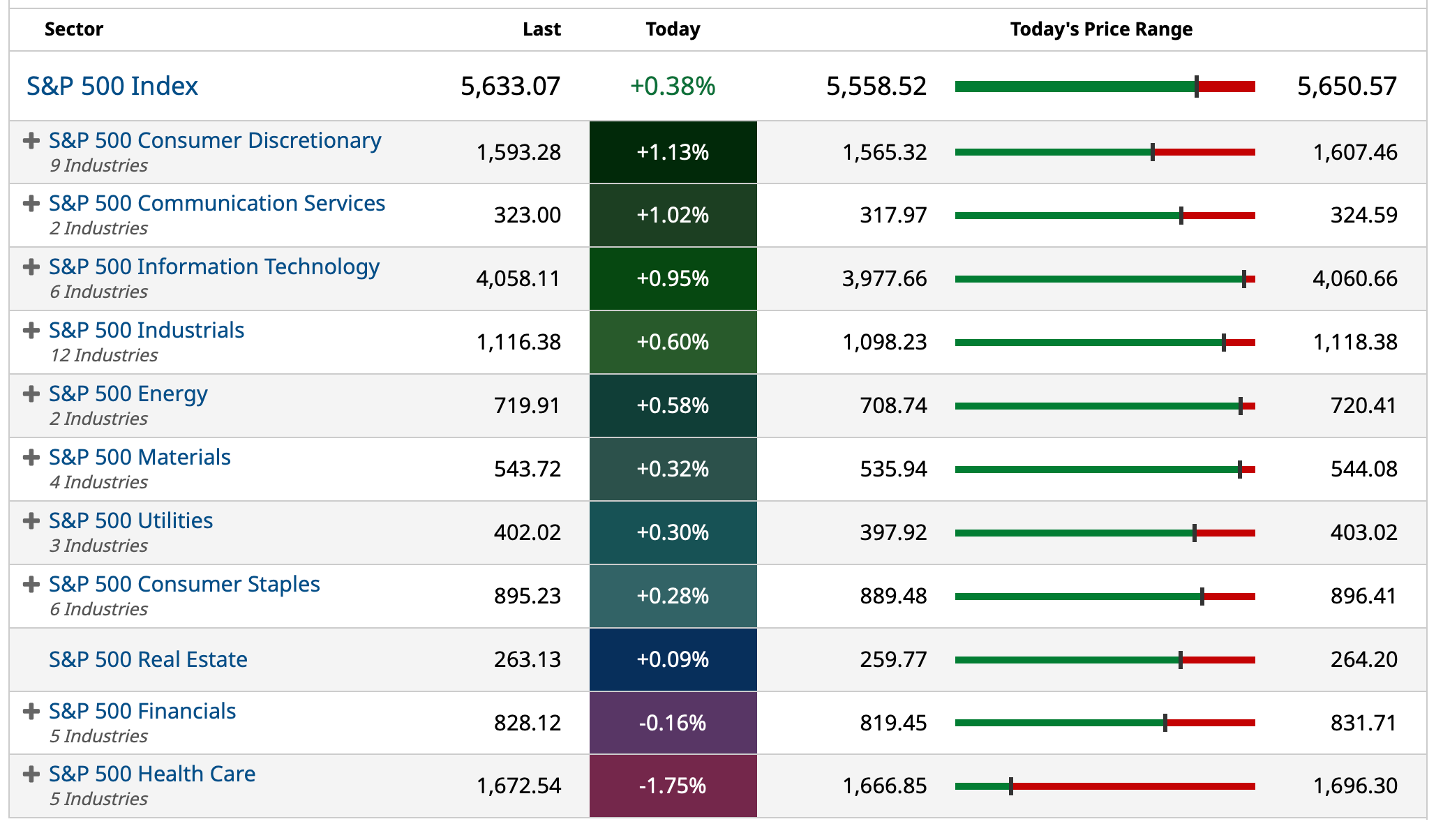

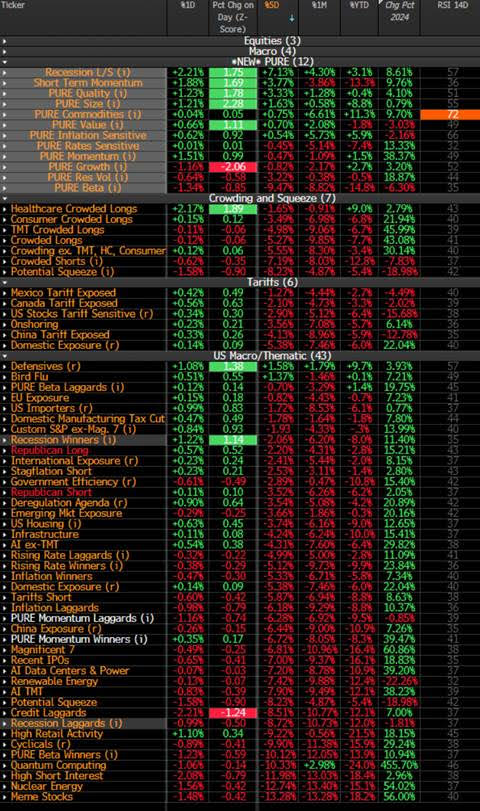

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Apr 1, 2025, 8:05 AM EDT

From JPMorgan:

US: Futs are higher. Pre-mkt, Mag 7 are mostly higher led by TSLA +3.7% and NVDA +1.3%. Bond yields are 0-3bp lower and USD is lower. Commodities are mostly flat this morning with base metals declining (copper -0.9%). Overnight, headlines were largely light, with geopolitical tension and trade policy remaining uncertain. Trump seems to dial back his criticism on Putin, per BBG article (here). We will receive ISM-Mfg this morning: Feroli expects the Index to print 48.0 vs. 49.5 survey vs. 50.3 prior.

and...

EQUITY AND MACRO NARRATIVE: Yesterday, despite the selloff pressure in the morning amid tariff escalation from weekend headlines, equities managed to rebound with SPX closing in the green. We share our tactical thoughts on tariffs ahead of Wednesday’s announcement below:

US MKT INTEL TARIFFS THOUGHTS AHEAD OF WEDNESDAY – we published below on March 31st. Below is the excepts from the note and you may fine the full note here

US MARKET INTEL VIEW – we remain Tactically Bearish. We think the policy uncertainty is the dominant factor in the markets and that neither the Trump Put nor Fed Put activate in the near-term. Further, we see downward pressure on the soft economic data though hard data is likely to remain resilient, potentially putting a floor on the next US downdraft. One potential event that could break the bearish outlook is the announcement of a trade deal, or framework of one, with a G7 country ahead of the announcement, e.g. US/UK deal could allow the market to look through tariffs on places such as the EU and/or Japan.

BY Doug Kass · Apr 1, 2025, 7:55 AM EDT

BY Doug Kass · Apr 1, 2025, 7:45 AM EDT

BY Doug Kass · Apr 1, 2025, 7:35 AM EDT

BY Doug Kass · Apr 1, 2025, 7:25 AM EDT

I tried to get a borrow on Newsmax (NMAX) early this morning when the shares were $110.

I could not get a borrow.

Like Trump Media DJT was (at higher prices), this is one of the more interesting short setups I have seen in a long time — but the volatility and difficulty to borrow preclude implementation for 99.9% of traders.

BY Doug Kass · Apr 1, 2025, 7:15 AM EDT

BY Doug Kass · Apr 1, 2025, 7:05 AM EDT

Bought back some index (common) on reversal from +10 handles to -23 handles in S&P futures (coincident with the tariffs news release):

* SPY $556.14

* QQQ $466.52

BY Doug Kass · Apr 1, 2025, 6:55 AM EDT

Bonus — Here are some great links:

The First Day of the Second Quarter Is Typically Strong

BY Doug Kass · Apr 1, 2025, 6:41 AM EDT

BY Doug Kass · Apr 1, 2025, 6:31 AM EDT

This news release likely is the reason for the fall from positive to negative in stock futures:

Trump aides draft tariff plans that experts say could hurt the economy - The Washington Post

BY Doug Kass · Apr 1, 2025, 6:21 AM EDT

BY Doug Kass · Apr 1, 2025, 6:15 AM EDT

The expectation of the big market on close order, helped me with my intraday trading tactics — as here is what I wrote late yesterday afternoon:

As noted earlier this morning (see below) the potential for a large reallocation trade out of bonds and into equities was present given the dramatic underperformance of stocks vs. fixed income.

I suspect the afternoon rally has been a front run of the reallocation trade and might be about done ...

From the AM:

Keep in mind that today is quarter end — and the substantial outperformance of bonds vs. equities means that a large asset allocation out of fixed income and into stocks could occur at the close of trading.

By Doug Kass Mar 31, 2025 7:50 AM EDT

Position: None

By Doug Kass Mar 31, 2025 3:49 PM EDT

BY Doug Kass · Apr 1, 2025, 6:05 AM EDT

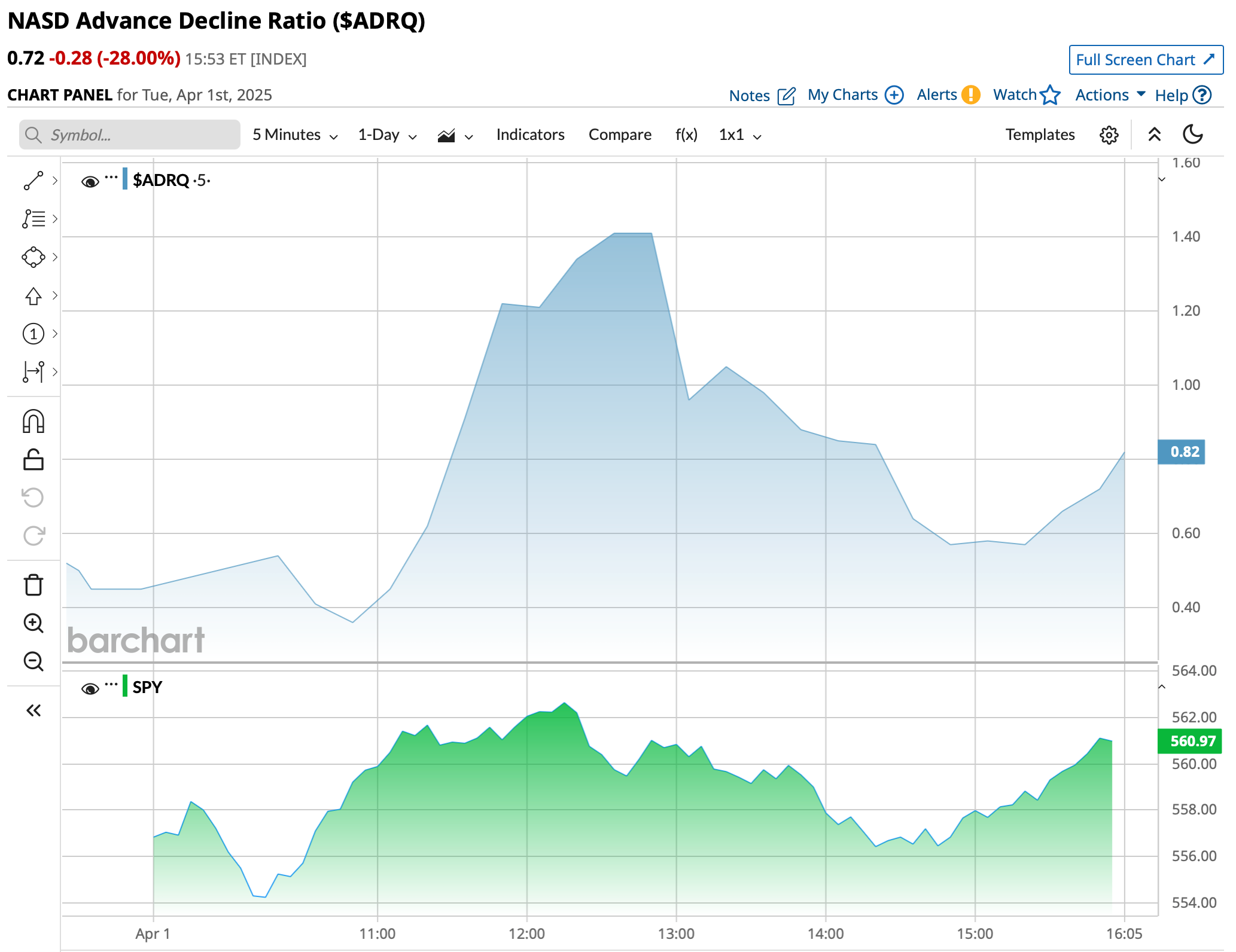

The S&P Short Range Oscillator moved to more oversold at -2.52% vs. -1.00%.

BY Doug Kass · Apr 1, 2025, 5:55 AM EDT

BY Doug Kass · Apr 1, 2025, 5:45 AM EDT