Positives,

1) Initial jobless claims were little changed w/o/w at 224k vs 225k (revised up by 2k) . That was about as expected. Continuing claims fell to 1.856mm, down from 1.881mm and below the estimate of 1.886mm.

2) The March US manufacturing and services composite PMI rose to 53.5 from 51.6. It was all led though by the services sector which rose to 54.3 from 51 while manufacturing fell back below 50 at 49.8 from 52.7.

3) Personal income rose .8% m/o/m which was double the estimate, partly offset by a 2 tenths downward revision to January. Private sector wages/salaries in particular rose .5% m/o/m and by 3.2% y/o/y vs 3.9% in January. Transfer payments continue to drive the headline income beat with a 2.2% m/o/m gain after a 1.8% jump in the month before. Medicaid payments especially were up sharply within this. Combine both income and spending and the savings rate rose to 4.6% from 4.3% and that is the most since June 2024 but still pretty low.

4) Pending home sales in February rose 2% m/o/m after a 4.6% drop in January and a 4.2% decline in December which took this index to a record low since it started. That was just above the estimate of up 1%. The gain was led almost entirely by the 6.2% increase in sales in the South which followed a 9.2% fall in the month before (blame the weather?) . Sales fell in the West and Northeast and were up slightly in the Midwest. The NAR said it as it is, “Despite the modest monthly increase, contract signings remain well below normal historical levels.”

5) New home sales in February totaled 676k, about as expected and up from 664k last month.

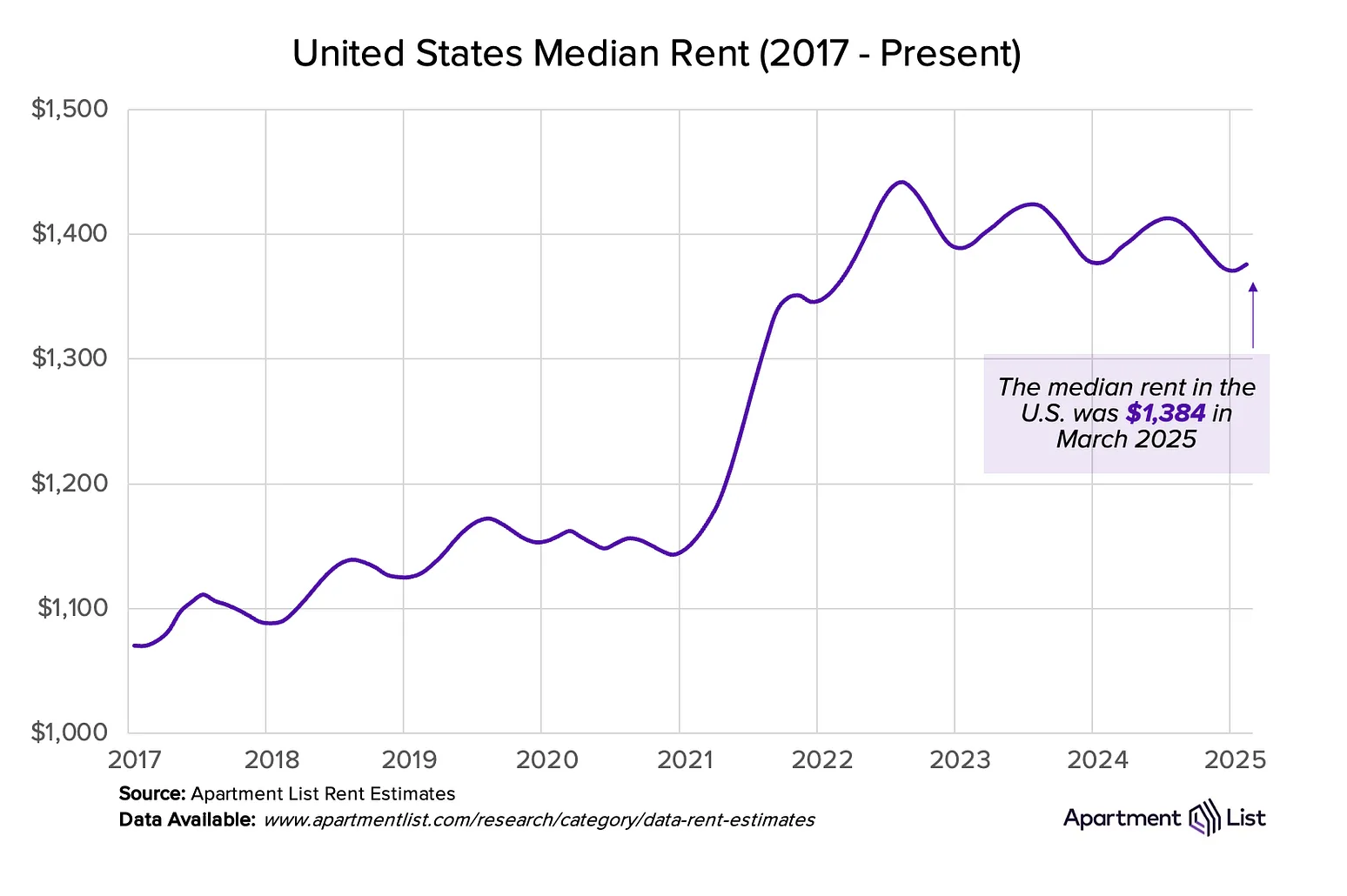

6) The Apartment List National Report for March and said its new rent index rose .6% m/o/m, up for a 2nd month and helped by seasonality. The index though is still down .4% y/o/y "but is slowly inching back toward positive territory." The supply side continues to be the issue with rent growth, particularly in the Sunbelt states with the vacancy rate rising to 6.9%, up one tenth m/o/m. Austin is the softest market. They said "2024 saw the most new apartment completions since the mid-1908s, and with 750k units still in the construction pipeline, the supply boom has runway to continue this year."

7) Within the durable goods report, core shipments, which get plugged into GDP, jumped by .9%, well above the estimate of up .2%. This is likely due to the rush to get product before tariffs but will lift Q1 GDP estimates.

8) From Carnival: "We achieved a robust 7.3% yield increase, smashing our yield guidance on top of last year's 17% yield improvement. Both ticket and onboard equally outperformed on very strong close-end demand, which speaks to the strength of our consumer…For the full year, and despite heightened macroeconomic and geopolitical volatility since providing our December guidance, we are taking up yields by .5 pt to 4.7% based on our strong first quarter results while affirming yield expectations for the remainder of the year."

9) France and Spain released its preliminary March CPI figures and they were both less than expected.

10) The UK had good news with its February retail sales data which rose 1% m/o/m ex auto fuel, well better than the estimate of down .5%, partly offset by a 5 tenths downward revision to January. The growth was broad based.

11) In the UK, headline CPI rose 2.8% y/o/y, 2 tenths less than expected while the core rate was higher by 3.5%, one tenth under the estimate and vs 3.7% in January. The inflation issue in the UK continues to be the services side where prices rose 5% y/o/y, the same pace seen in the month before and one tenth above the consensus. The ONS said slower clothing price gains helped to slightly cool inflation on the goods side.

12) Economic confidence has risen in Germany with the new Chancellor and release of the 'debt brake'. The March IFO business confidence index rose to 86.7 from 85.3 as expected but is now at the best level since July 2024, though still dancing along the bottom. Most of the lift off the lows has come in the Expectations component as Current Conditions are still muted. The IFO said succinctly, "German businesses are hoping for a recovery."

13) CPI in February in Australia was up 2.4% y/o/y vs the forecast of 2.5%. The trimmed mean rate which is what the RBA looks at the most was up by 2.7%, also one tenth less than expected.

14) Australia's PMI index lifted to 51.3 from 50.6 with both components higher m/o/m and with both above 50.

15) India's PMI held strong at 58.6 vs 58.8 with manufacturing at 57.6 and services at 57.7.

16) The European PMI was mixed as manufacturing rose to 48.7 from 47.6, though still below 50 while services slipped to 50.4 from 50.6. S&P Global had some interesting insight, "Just in time with the beginning of spring we may see the first green shoots in manufacturing. While we should not be carried away by a single data point, it is noteworthy that manufacturers expanded their output for the first time since March 2023. It's also encouraging, that the index output has risen for three months straight. This is complemented by a much softer fall in new orders and employment. One could pour some cold water on this development arguing that it's the temporary tariff-related import boom from the US which has driven the improvement in manufacturing. However, given the will of Europe, to invest heavily in defense and infrastructure - in Germany a corresponding historical fiscal package has been approved only last week - hope for a more sustained recovery seems well founded."

17) The UK PMI rose 1.5 pts m/o/m to 52 with all the help coming from services which rose to 53.2 from 51. Manufacturing softened further to just 44.6 from 46.9.

Negatives,

1) Headline PCE in February rose by .3% as expected but the core rate was higher by .4%, one tenth above the estimate. Prices rose 2.5% y/o/y headline and 2.8% ex food and energy vs 2.5% and 2.6% in the month before respectively. Service prices were up 3.5% y/o/y while goods prices were up by .4% y/o/y, higher for a 2nd month after a string of declines.

2) Personal spending was a bit light as it grew by .4% m/o/m, one tenth less than expected and follows a 3 tenths drop in January which was revised down by one tenth. These are nominal figures so soft on a REAL basis.

3) Reflecting the major pull forward of orders ahead of tariffs, the US goods trade deficit in February was a huge $147.9b vs $155.6b in January and compared to ‘just’ $104b in November. This also compares to about $90b in January and February in 2024. The estimate was $139b.

4) Non-defense capital goods ex aircraft orders in February unexpectedly fell by .3% m/o/m vs the estimate of a gain of .2% and follows a .9% rise in January (revised up by one tenth) . They are now down 1.2% y/o/y.

5) A reminder that cuts in government spending, while desperately needed long term, will result in near term economic weakness, Bloomberg News reports the termination by the DOD of a software contract with Oracle. Across governmental agencies, assume this is now happening every week in various shapes and sizes.

6) I’m all for the US producing more autos in the US and bringing back manufacturing jobs but I don’t believe the current plan will be a net benefit to the economy of the US, the risks over a multi year period are huge and the retaliation is going to hurt.

7) The comments from the Dallas Fed’s monthly energy survey are worth a read, https://www.dallasfed.org/research/surveys/des/2025/2501#tab-comments.

8) Purchase applications for the week ended 3/21 were flattish for a 2nd week, up by .7% w/o/w while refi's fell by 5.3%, down for a 2nd week after a sharp rise in the two weeks prior. The average 30 yr mortgage rate held at 6.71%.

9) Good for homeowners but not for first time buyers or most of the industry that relies on housing turnover, the national home price index for January from S&P CoreLogic which rose .6% m/o/m and by 4.1% y/o/y.

10) The March Consumer confidence index from the Conference Board fell to 92.9 from 100.1, just below the estimate and at the lowest level since January 2021. Most of the decline was led by the Expectations component which dropped almost 10 pts m/o/m. The Present Situation was lower by 3.6 pts from February. One year inflation expectations are now at 6.2%, up from 5.8% last month and 5.2% in the month before “as consumers remained concerned about high prices for key household staples like eggs and the impact of tariffs” said the Conference Board. The answers to the labor market questions were little changed m/o/m but did soften last month. And, expectations over the coming 6 months for the labor market continues to deteriorate with those seeing ‘more jobs’ falling 2.1 pts to the lowest level since August 2024. Expectations for income also weakened, declining by 2.5 pts sequentially to the lowest since June 2024. Spending intentions were mixed. Bottom line, not surprisingly, “Comments on the current Administration and its policies, both positive and negative, dominated consumers’ write-in responses on what is affecting their views of the economy. Write-in responses also showed that inflation is still a major concern for consumers and that worries about the impact of trade policies and tariffs in particular are on the rise. There were also more references than usual to economic and policy uncertainty.”

11) The March Richmond manufacturing index fell back under zero at -4 from +6 in February. Prices paid and received jumped sharply m/o/m. Also of note, the 6 month outlook for the prices paid annualized percent change went from 4.6% to 7.2%. For those received, to 4% from 3.2%.

12) The March Philly non-manufacturing index fell sharply to -32.5 from -13.1 and is now negative for 5 straight months.

13) From Lululemon: "As you have seen, we started this year with several compelling new product launches, but we also believe the dynamic macro environment has contributed to a more cautious consumer. In fact, based on a survey we conducted earlier this month in conjunction with Ipsos, consumers are spending less due to increased concerns about inflation and the economy. This is manifesting itself into slower traffic across the industry in the US in quarter one, which we are experiencing in our business as well."

14) From Dollar Tree: "In recent weeks, many retailers reported that customers, particularly middle income customers, are shifting towards alternatives that present value. Dollar Tree is also seeing middle income shoppers who make up about half of our customer base focusing more on value. At the same time, we are seeing stronger demand from higher income customers, who increasingly see Dollar Tree as a cost effective source for an expanding range of products. This trade-in has helped to offset other headwinds."

15) From Winnebago: "As expected, soft retail and growing macroeconomic uncertainty continue to create a challenging sales environment across the outdoor recreation industry in our second quarter. Consequently, we remain intently focused on the factors in our control." With guidance, they did lower their revenue and eps range "largely driven by the reduction in consumer confidence and consumer sentiment."

16) From Oxford Industries: "In December, we said that we were expecting a strong holiday selling season. That expectation turned into reality as the consumer did in fact show up to buy their loved ones and friends the gifts that they really wanted from the brands that they love...As we moved into January, we experienced a moderation in demand, which we attribute to the recent pattern of consumers retreating when there isn't a reason to spend, combined with a deterioration in consumer sentiment. As a result, January was not as strong as December, with comps down 3%. This negative trend accelerated in the beginning of fiscal 2025, with comps of negative 9% in February...We believe the choppiness in demand we experienced towards the end of fiscal 2024 is likely to continue in the near term."

17) From Paychex: "Turning to the macro environment, the pace of US job growth has moderated from the robust levels observed coming out of the pandemic but has been relatively stable during the past year and in line with historical averages. Our customer employment levels were a little softer than expected in the third quarter and likely impacted by weather related challenges and devastating fires in California, as well as lower bonus checks than last year and our expectations. Year-to-date, our checks per client have been flat compared to the prior year, suggesting relatively stable US labor market conditions."

18) From McCormick: "There is increasing consumer uncertainty and concern over returning to more inflation, and this has impacted consumer sentiment, particularly in the last month. This prolongs the consumer context of 2024, where consumers, especially lower income consumers, are more cautious, exhibiting more value seeking behavior and tightening their budgets as many are worried about the future, job security and rising costs. We are seeing this not just in the US but across our key markets."

19) From KB Homes: "Consumers are continuing to cope with affordability concerns and uncertainties around macroeconomic and geopolitical events. As a result, consumer confidence has declined sequentially each month for the past several months and homebuyers are moving more slowly in making their purchase decisions. While longer-term housing market conditions remain favorable, driven by demographics and an undersupply of homes, demand at the start of the spring selling season has been more muted than we have seen over the past few years. As a result of this softer selling environment, we are lowering our revenue guidance for fiscal 2025."

20) The March CPI in the city of Tokyo, which is a good read on the national number, was up 2.9% y/o/y, two tenths above the estimate with a 2.2% gain ex energy and food, 3 tenths higher than anticipated.

21) The March manufacturing and services composite index for Japan fell to 48.5 from 52 with continued softness in manufacturing at 48.3 vs 49 and a big drop in services to 49.5 from 53.7. Inflation pressures were apparent too as "cost pressures remained elevated in March, with overall input costs rising sharply across both monitored sectors, leading to a solid rise in selling prices. Strong inflation, coupled with concerns over labor shortages, an ageing population, subdued client spending and increased uncertainty over the international trade environment dampened optimism around the outlook. Notably, overall confidence regarding future business activity dipped to the lowest since August 2020 at the end of the first quarter."

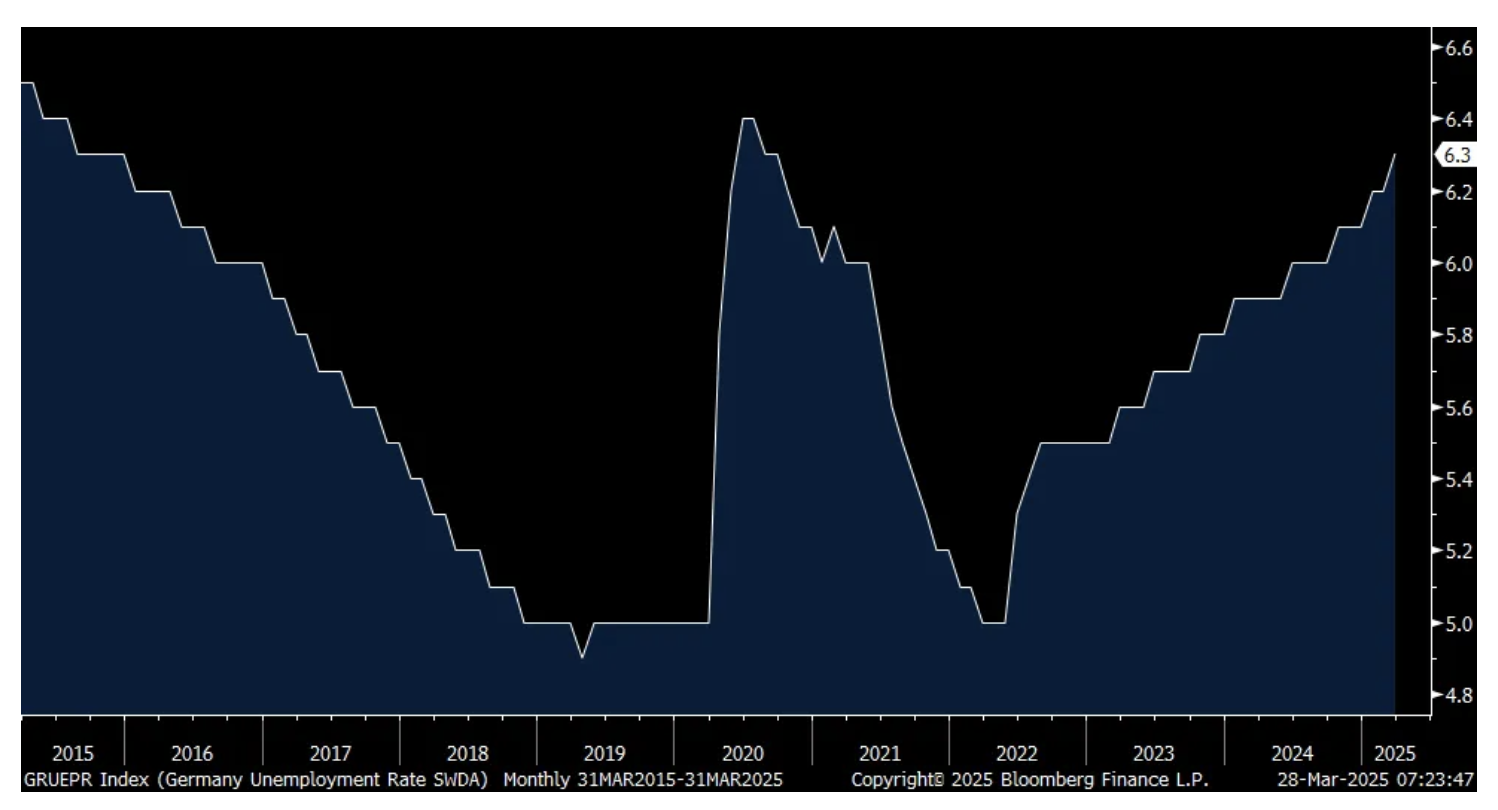

22) German unemployment rose by 26k people in March and that was well above the estimate of up 10k. Their unemployment rate rose one tenth to 6.3% and that is just one tenth from matching the lockdown highs in 2020.

23) The March Eurozone Economic Confidence index which fell to 95.2 from 96.3 where there was an expected gain to 96.7. That's the lowest since December. Manufacturing confidence actually improved m/o/m but was offset by declines in services, retail and with consumer confidence.