Wednesday's After-Hours Movers

At 4:15 a.m.:

BY Doug Kass · Mar 26, 2025, 4:37 PM EDT

At 4:15 a.m.:

BY Doug Kass · Mar 26, 2025, 4:37 PM EDT

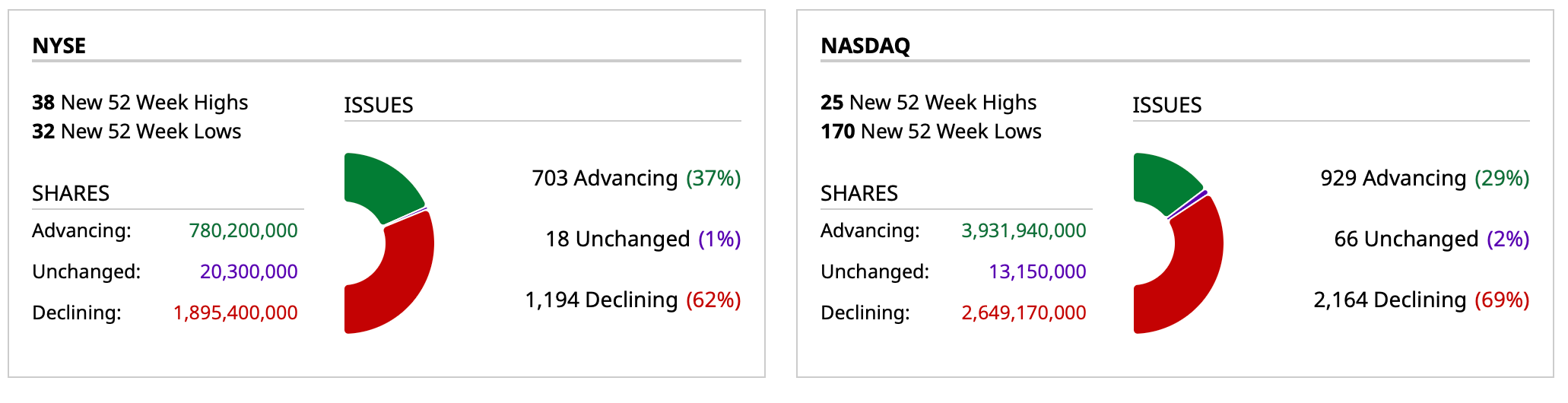

- NYSE volume 24% below its one-month average

- NASDAQ volume 29% above its one-month average

- VIX index: up 7% to 18.35

BY Doug Kass · Mar 26, 2025, 4:21 PM EDT

BY Doug Kass · Mar 26, 2025, 3:55 PM EDT

BY Doug Kass · Mar 26, 2025, 3:47 PM EDT

* I have now published about 80 "Tales." Generally all of then have cautioned about the outlook for NVDA's shares.

* During that interim interval (since last June) NVDA common shares have performed poorly (absolutely and relatively)

BY Doug Kass · Mar 26, 2025, 3:37 PM EDT

To recap, I expected a tradeable three-to seven-day rally from the recent lows and that is exactly what we got.

As posted, we went net long into the whoosh lower and sold into the strength (and on a scale) earlier this week.

Also as posted, I am now playing "small ball" — with a low gross and net and with plenty of cash reserves.

I expect the market, with a plethora of uncertainties, to be very volatile (and "newsy") — ideal for dispassionate and opportunistic traders but not so great for the buy-and-hold crowd.

BY Doug Kass · Mar 26, 2025, 3:20 PM EDT

I added to cannabis equities just now: MSOS at $2.43, CRLBF at $0.62, VRNOF at $0.605, CURLF at $0.867, GTBIF at $5.52, TCNNF at $3.72.

Last night GLASF reported fantastic results. I am adding to this name as well at $4.72. The conference call was exceptional.

BY Doug Kass · Mar 26, 2025, 2:42 PM EDT

I just covered some more of my shorts: ROAD $77.99 and BOOT $106.42.

BY Doug Kass · Mar 26, 2025, 2:35 PM EDT

BY Doug Kass · Mar 26, 2025, 2:30 PM EDT

No trades today, save the short cover of the indices.

BY Doug Kass · Mar 26, 2025, 2:21 PM EDT

BY Doug Kass · Mar 26, 2025, 1:25 PM EDT

* And more are coming tomorrow morning...

BY Doug Kass · Mar 26, 2025, 1:06 PM EDT

And the proximate cause for the market's slide in the last few minutes:

BY Doug Kass · Mar 26, 2025, 12:10 PM EDT

BY Doug Kass · Mar 26, 2025, 11:45 AM EDT

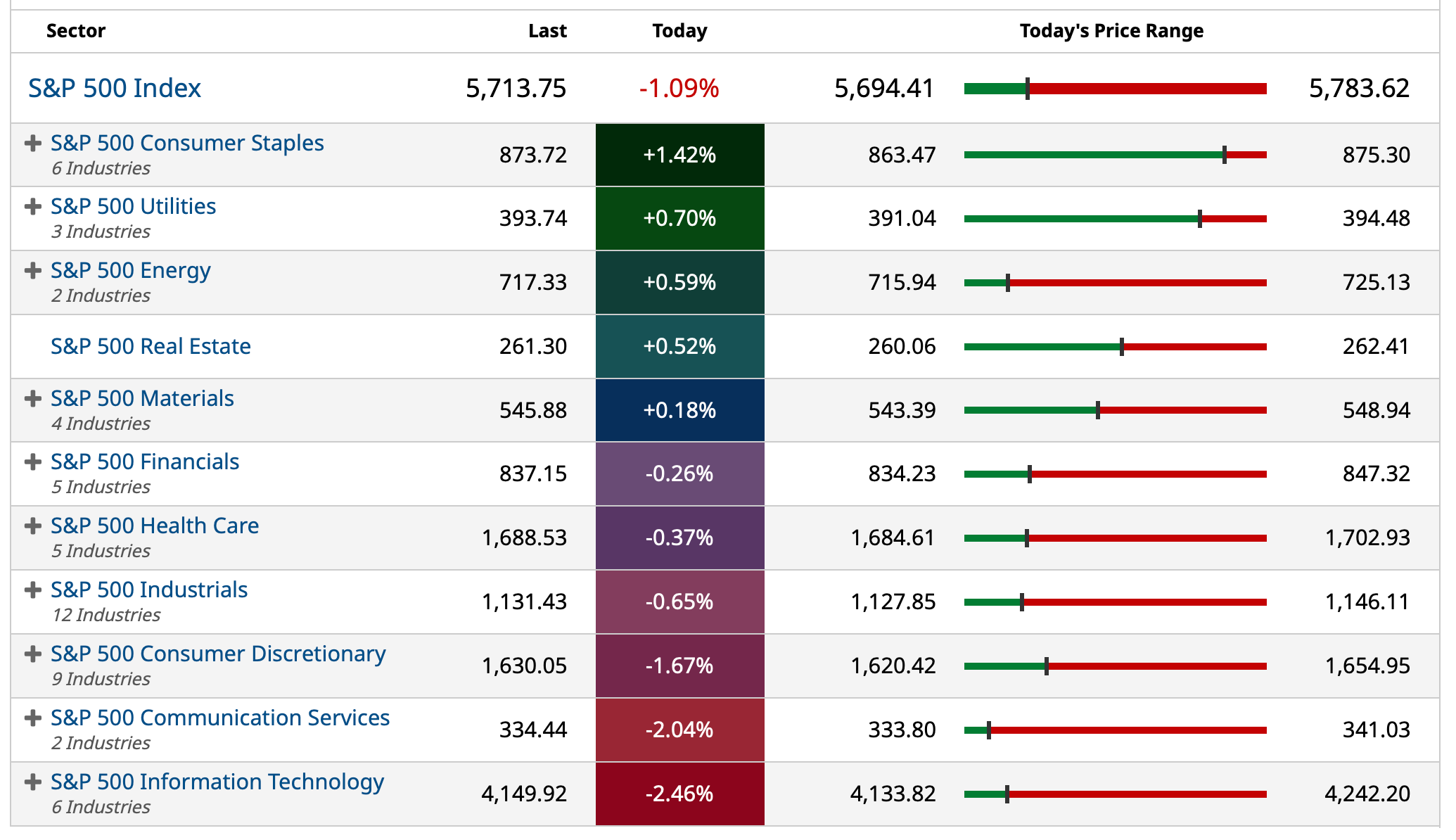

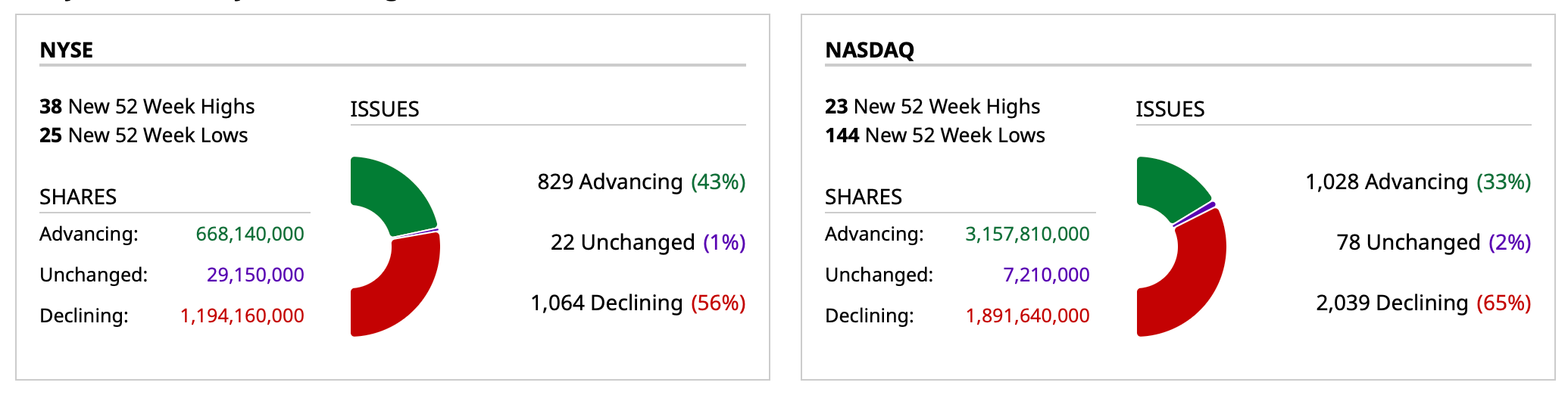

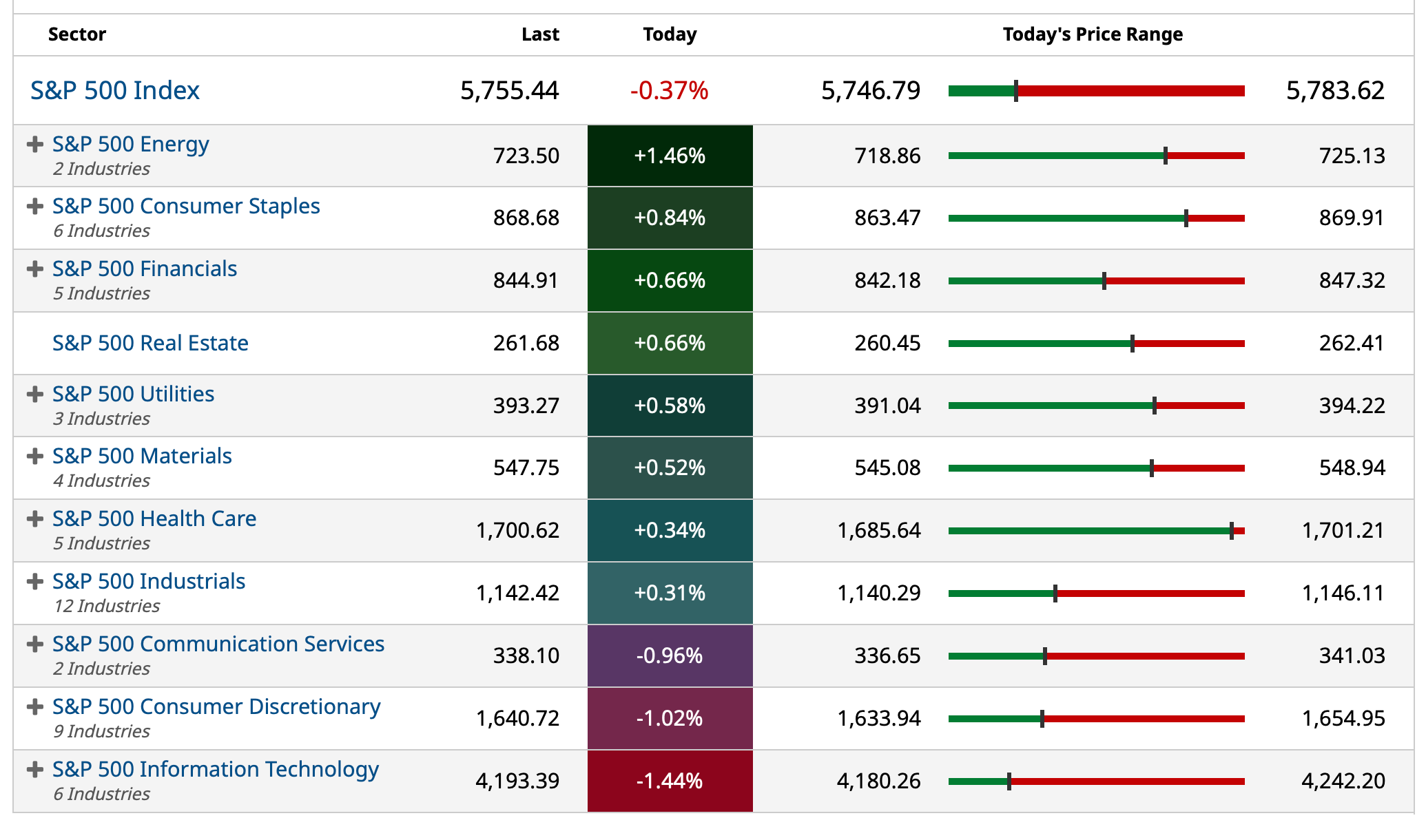

The clear rotation into finance and energy is conspicuous today.

BY Doug Kass · Mar 26, 2025, 11:30 AM EDT

BY Doug Kass · Mar 26, 2025, 11:20 AM EDT

- NYSE volume 32% below its one-month average;

- Nasdaq volume 23% above its one-month average;

- VIX index: up 2.68% to 17.61

BY Doug Kass · Mar 26, 2025, 11:05 AM EDT

From Peter Boockvar:

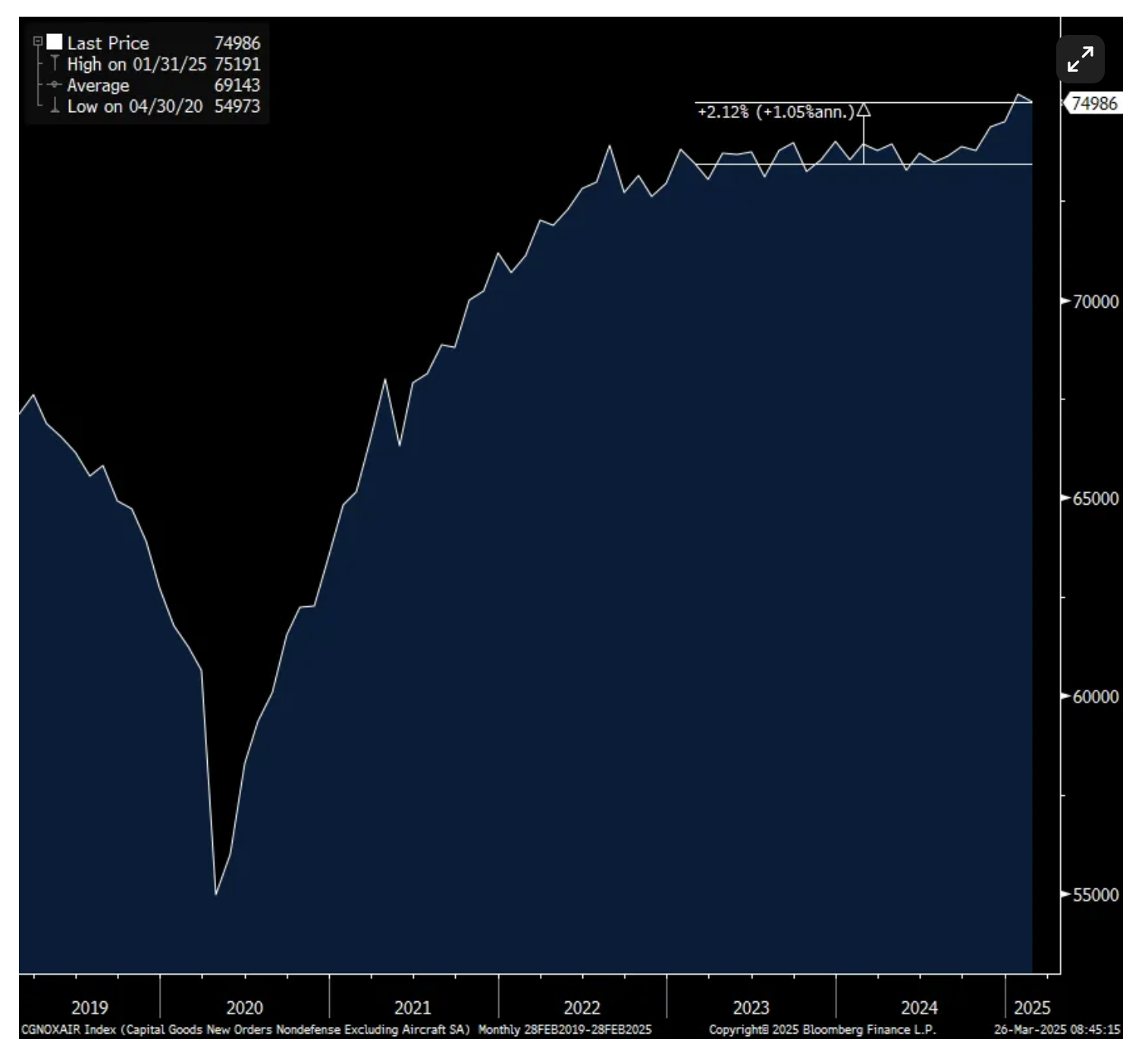

Non defense capital goods ex aircraft orders in February unexpectedly fell by .3% m/o/m vs the estimate of a gain of .2% and follows a .9% rise in January (revised up by one tenth). They are now down 1.2% y/o/y.

Vehicles/parts orders did rebound by 4% but after 4 months of declines and are still down 2.7% y/o/y. Orders were flat for computers/electronics after a 1.8% rise in the month before. Orders for electrical equipment, which has been a bright spot over the past six months with data center buildouts, were up 2% m/o/m. Orders were little changed for machinery and rose for both primary and fabricated metals.

Core shipments, which get plugged into GDP, jumped by .9%, well above the estimate of up .2%. This is likely due to the rush to get product before tariffs but will lift Q1 GDP estimates.

Bottom line, about every single regional manufacturing sector seen has reflected a drop in capital spending plans due to the lack of business visibility and today’s durable goods orders is hard data confirming the soft.

Also, with regards to CapEx, I’ve argued that most over the past few years has been allocated to anything related to AI with the biggest dollars spent by big cap tech as we know. CapEx elsewhere has been much more muted. To quantify, over the past 2 years, core durable goods orders are up in TOTALITY by just 2.1% in nominal terms, so about a 1% increase per year.

Core Durable Goods Orders in Dollars

BY Doug Kass · Mar 26, 2025, 10:45 AM EDT

SPY is nearing Monday's intraday low of $572.02:

BY Doug Kass · Mar 26, 2025, 10:35 AM EDT

BY Doug Kass · Mar 26, 2025, 10:20 AM EDT

I have just covered my Index shorts:

* SPY $573.49

* QQQ $489.44

BY Doug Kass · Mar 26, 2025, 10:05 AM EDT

* But baby if I'm the bottom you're the top...

"At words poetic, I'm so pathetic

That I always have found it best

Instead of getting 'em off my chest

To let 'em rest unexpressed

I hate parading my serenading

As I'll probably miss a bar

But if this ditty is not so pretty

At least it'll tell you how great you are.

"You're Mahatma Gandhi

You're the top

You're Napoleon brandy

You're the purple light of a summer night in Spain

You're the National Gallery, you're Garbo's salary

You're cellophane."

- Cole Porter, You're The Top

While these previous price patterns/charts are obviously vague, should not be taken literally and basically BS, it's always fun to make the comparison. The 2025 Nasdaq pattern is very similar to 2022 (when the index broke 17,500) — so technically speaking, 21,000 is an important spot:

Here is the way Ella Fitzgerald saw it — and here is the way I currently see it:

"You're the Nile

You're the Tow'r of Pisa

You're the smile

On the Mona Lisa

I'm a worthless check, a total wreck, a flop

But if, baby, I'm the bottom

You're the top."

- Cole Porter, You're The Top

Equities have recovered smartly from last week's lows and, as we and others anticipated, a knee-jerk higher has commenced.

At the bottom, we were deeply oversold — but the S&P Short Range Oscillator is now back into overbought.

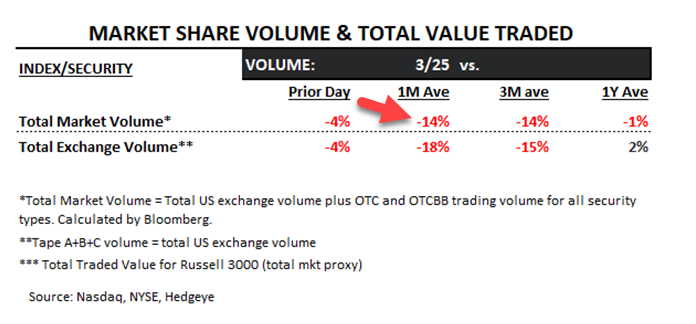

Thus far, especially over the last two trading sessions, the rally in stocks has been unsupported by higher volume. Just the opposite (very low volume) has followed:

Most bulls and technicians are interpreting the recent climb in equities as another opportunity to "buy the dip."

Away from the less important technicals, the fundamentals are deteriorating. One of the foundations of our bear case was that 2025 S&P consensus EPS estimates were too elevated.

Indeed, over the last few weeks, first-half 2025 domestic economic real GDP growth projections have been significantly lowered — and so have corporate profit estimates (the previous consensus forecasts of +14% growth in S&P EPS was a pipedream).

In summary, my interpretation is less favorable and my 2025 market view is unchanged.

Based on my five scenarios (from very negative to very positive and attaching multiples to that distribution) I expect the S&P index to be down between five and ten percent for the full year.

It is my continued view that there is upside to about +5% (year over year), but my thinking remains that the high might have been already made in late January.

On the downside I see risk (for 2025) to be about -10% to -15% for the S&P.

Despite the anticipated and relatively narrow trading range there will be plenty of long and short opportunities on the road to the end of the year.

By Doug Kass Mar 25, 2025 3:00 PM EDT

BY Doug Kass · Mar 26, 2025, 9:30 AM EDT

-SURG +70% (earnings, guidance)

-THTX +34% (receives FDA Approval for EGRIFTA WR\ (Tesamorelin F8) to Treat Excess Visceral Abdominal Fat in Adults with HIV and Lipodystrophy)

-PLTK +14% (Tier1 firm Raised PLTK to Buy from Underperform, price target: $6.50 from $6)

-WVE +14% (positive Phase 2 FORWARD-53 data for WVE-N531, demonstrating significant muscle health improvements in boys with Duchenne Muscular Dystrophy)

-GME +12% (earnings; Board has unanimously approved an update to its investment policy to add Bitcoin as a treasury reserve asset)

-PRM +8.7% (UBS Raised PRM to Buy from Neutral, price target: $14)

-ABOS +6.7% (completes enrollment of ALTITUDE-AD, a Phase 2 Clinical Trial of Sabirnetug (ACU193) in Early Alzheimer’s Disease)

-ZH +6.7% (earnings)

-ABBV +6.4% (showcases early pipeline and scientific advances in oncology at AACR Annual Meeting 2025)

-LVO +5.0% (notes it exceeded 1.4M subscribers and ad-supported users, fueled by its Tesla partnership)

-SMMT +4.9% (CitiGroup Raised SMMT to Buy from Neutral, price target: $35)

-PAYS +4.8% (earnings, guidance)

-CHWY +4.7% (earnings, guidance)

-CRVS +4.3% (earnings)

-GLBE +4.3% (Morgan Stanley Raised GLBE to Overweight from Equal Weight, price target: $46)

-CTAS +3.9% (earnings, guidance)

-SAIL +3.7% (earnings, guidance)

-WOR +2.8% (earnings)

-DLTR +2.4% (confirms to divest Family Dollar to Brigade Capital and Macellum for $1.01B; earnings, guidance)

-PYXS +2.3% (to present new preclinical data supporting development of First-In-Concept ADC targeting EDB+FN in tumor microenvironment at AACR 2025)

-INTT +2.0% (long-term guidance ahead of Investor Day)

-HUMA -30% (prices 25M shares at $2/share)

-VNRX -11% (prices $2.3M Registered Direct Offering at $0.55/shr)

-PRTS -5.3% (earnings; evaluating strategic alternatives in response to inbound interest)

-GWRS -4.4% (prices 2.8M common share offering at $10/shr)

-REE -2.6% (announces increase in previously announced Registered Direct Offering to $36.4M with pricing of additional $9.4M at premium to market at $4.25/shr)

BY Doug Kass · Mar 26, 2025, 9:25 AM EDT

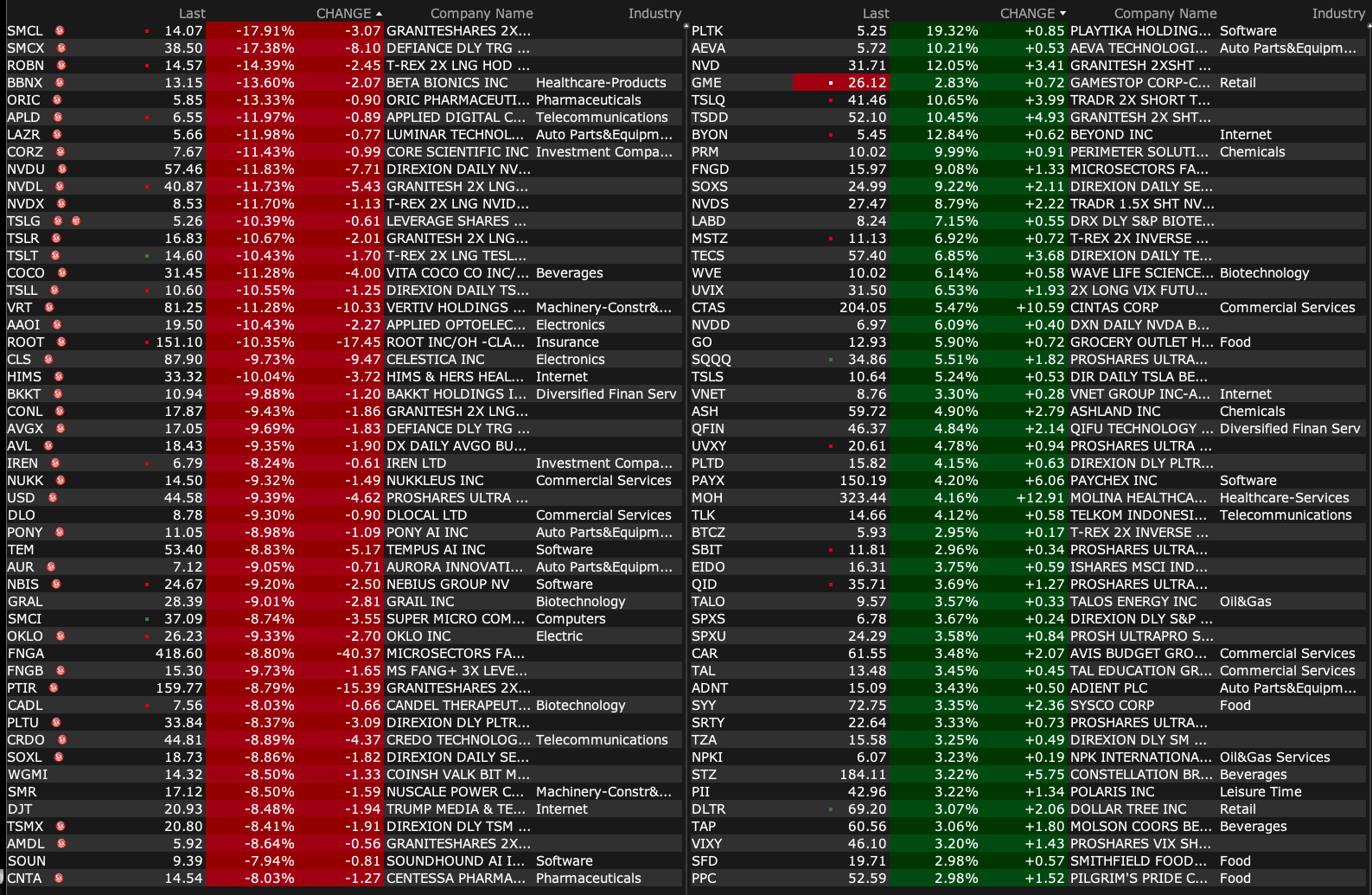

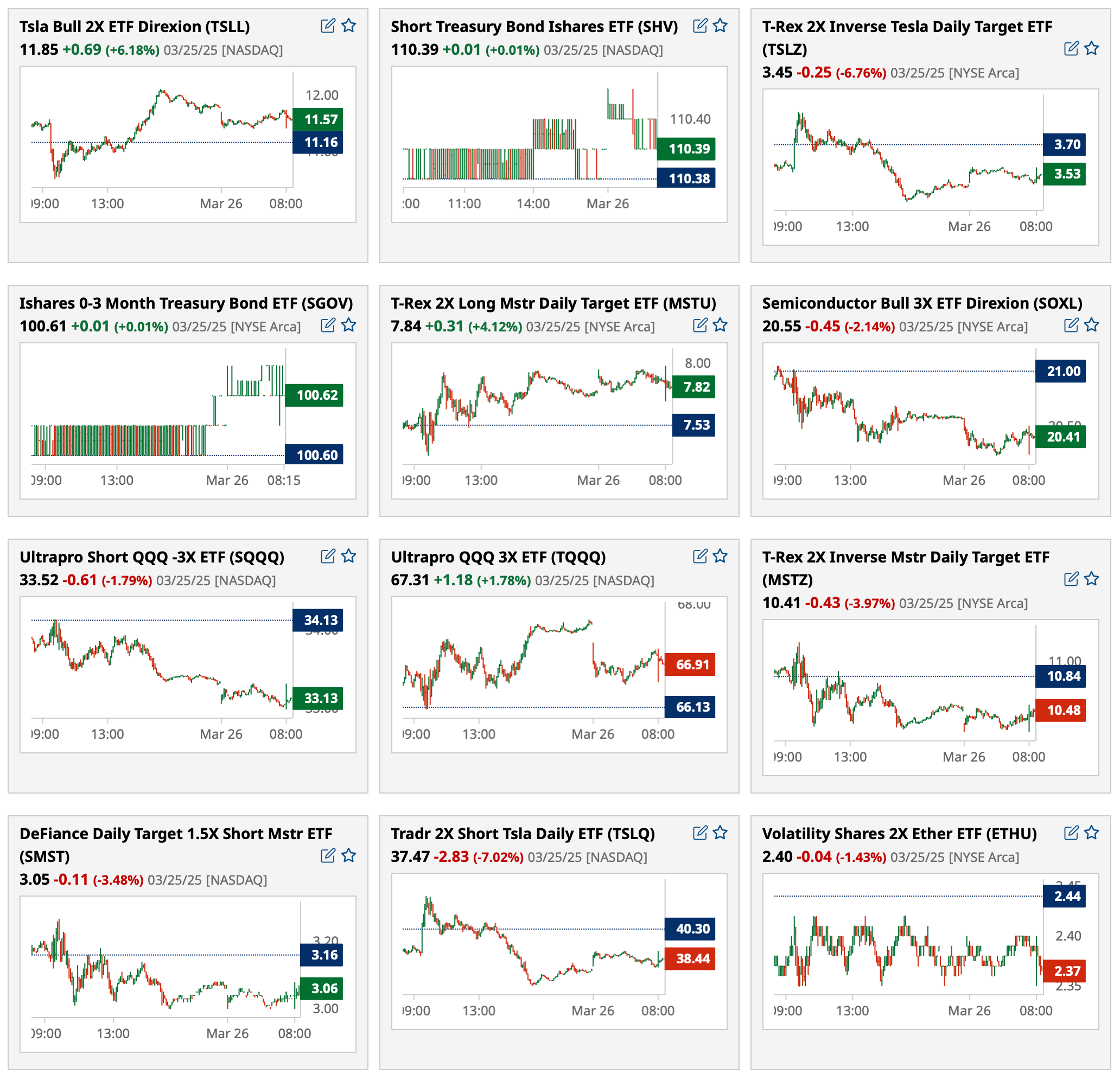

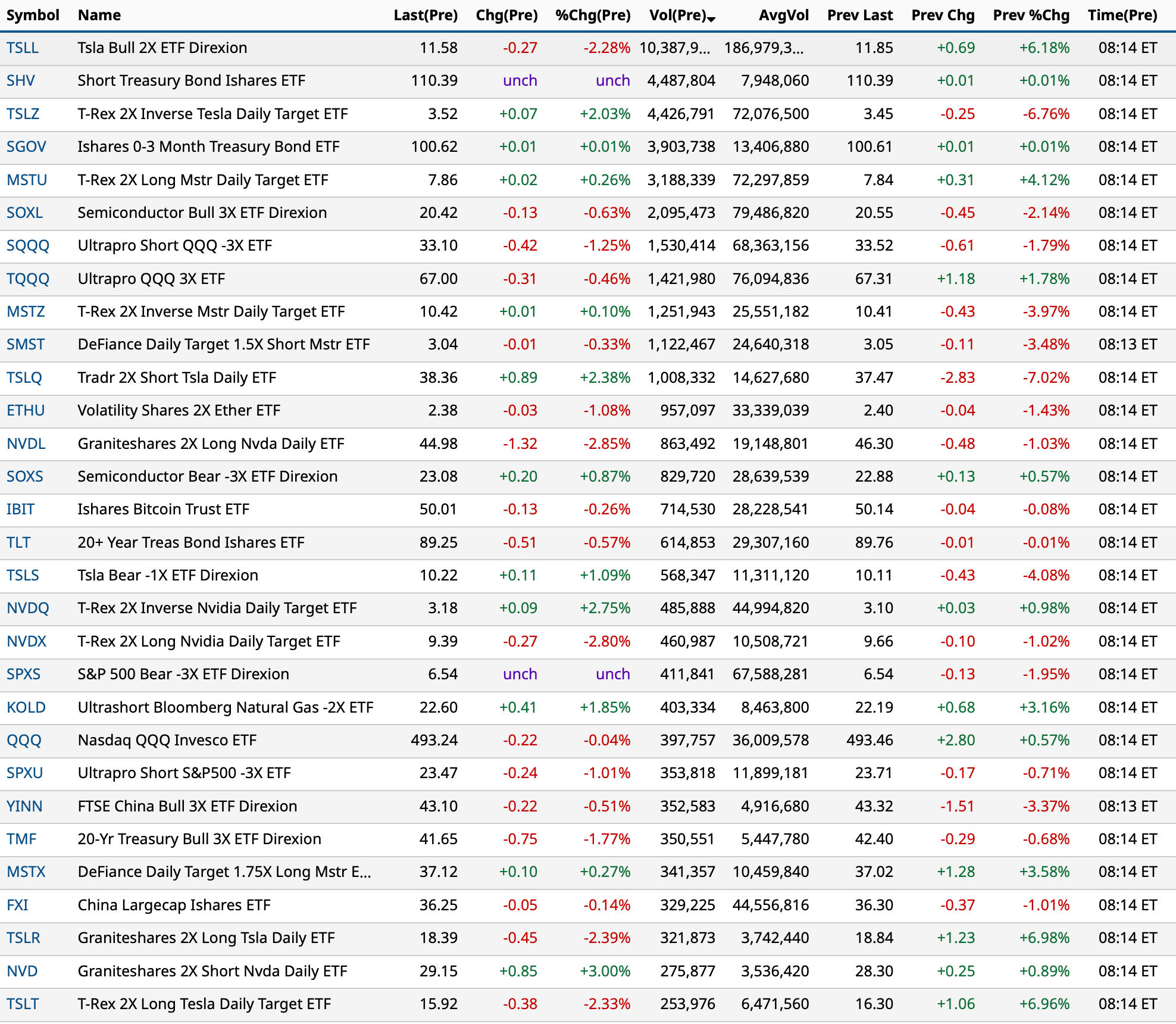

These two charts show the most active premarket ETFs at 8:14 a.m. ET; SPY doesn't even make top 30 ranking. Highly leveraged ETFs outrank QQQ by 21 spots.

BY Doug Kass · Mar 26, 2025, 9:12 AM EDT

Premarket percentage movers as of 8:35 a.m. ET:

BY Doug Kass · Mar 26, 2025, 9:05 AM EDT

BY Doug Kass · Mar 26, 2025, 8:55 AM EDT

BY Doug Kass · Mar 26, 2025, 8:45 AM EDT

From Peter Boockvar:

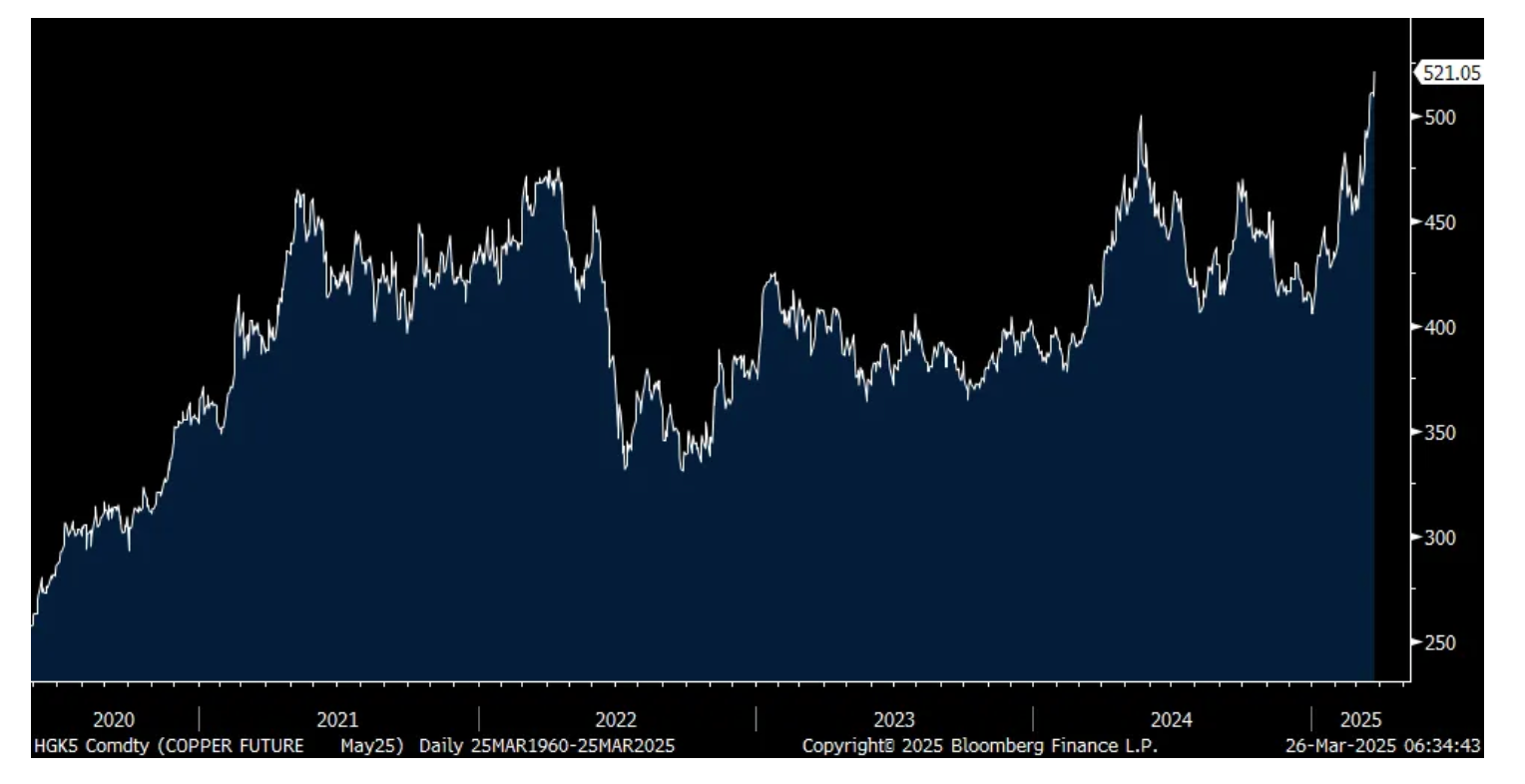

I understand dressing down some of our trading partners for egregious tariffs they place on US exports and the desire to threaten/implement reciprocal tariffs in order to encourage them to lower their tariffs. What I don't understand is putting a tariff on an imported item that we don't and will never produce enough of in the US. I say this because of the new copper tariff proposed which would follow steel and aluminum. According to Google Gemini, we import about 44% of our copper needs. I'll add that copper is just about the most industrial metal in the world in terms of its breadth of crucial uses, including in housing. According to the International Copper Association, "One ton of copper brings functionality to 40 cars, powers 100,000 mobile phones, enables operations in 400 computers and distributes electricity to 30 homes." Among many other things. Would it be nice to produce all of it here so as not to rely on anyone? Sure, but not remotely realistic.

Copper today is at a fresh record high in response

Conventional wisdom has it that just a little bit of inflation, about 2% give or take, is a good thing and god forbid prices actually go down, aka deflation. I've spent endless energy pushing back against the belief that all deflation is bad with the best example being technology products where a massive industry has been created and our lives have changed for the better because of ever lower prices with ever better advancements. That IBM PC desktop that cost $2,000 in 1981 would be about $4,800 today if the price went up 2% per year. Instead, you can pay less than $2,000 today for a computer that is as powerful as a mainframe computer was back then.

The Bank of Japan has spent decades trying to create inflation even though their populace has benefited from a stable cost of living over this time frame. So what happens when the BoJ is now successful in generating higher inflation? Yesterday Bloomberg News has a story that says "Japanese Prime Minister Shigeru Ishiba is planning measures to ease the impact of inflation on consumers...The government spokesman pointed to a range of existing policy efforts, including cash handouts to low income households and regional governments, and releasing emergency rice stockpiles to curb soaring rise prices."

Further, "The cost of living crunch has been a major challenge for Ishiba's minority government, fueling public discontent over the ruling parties' handling of economic policies while strengthening opposition parties' calls for spending and tax cuts."

We also heard from Governor Ueda today in the BoJ's semi-annual report they release. In it he said "Our projection is that the underlying price trend will broadly reach 2% in the second half of our outlook period. Of course monetary policy can be adjusted in line with that outlook, but if the trend overshoots, we would adjust policy more strongly." He went on to say specifically, "Underlying inflation is gradually accelerating. Still, it's not quite in the narrow range of around 2%, there's a bit of distance."

He says this like it is a good thing. It is not. Japan is an aging population where many senior citizens are getting just .50% interest rate or less on their bank savings accounts vs inflation running well above that.

We saw CPI for February in Australia and it was up 2.4% y/o/y vs the forecast of 2.5%. The trimmed mean rate which is what the RBA looks at the most was up by 2.7%, also one tenth less than expected but yields rose in Australia and the Aussie$ is higher after the Australian government said the debt supply they are issuing this year is more than previously expected.

CPI stats were reported for the UK too today for February. Headline CPI rose 2.8% y/o/y, 2 tenths less than expected while the core rate was higher by 3.5%, one tenth under the estimate and vs 3.7% in January. The inflation issue in the UK continues to be the services side where prices rose 5% y/o/y, the same pace seen in the month before and one tenth above the consensus. The ONS said slower clothing price gains helped to slightly cool inflation on the goods side.

With no surprises, though still persistent inflation, gilt yields are lower as is the British pound and UK inflation breakevens are unchanged while the FTSE 100 is flattish. UK stocks remain cheap, particularly big oil there which we are long and continue to trade at a notable discount to its US peers.

McCormick & Co makes spices, seasonings and flavorings that go into so many things we eat. This is what they said on their earnings call yesterday of note:

"total organic sales increased by 2%, primarily driven by volume and product mix growth, and partially offset by pricing, in line with our expectations." With pricing specifically, "In the Americas, price declined due to price gap management plans that were implemented in the second quarter of 2024 and a targeted incremental promotion related to seasonal recipe mixes." We know consumer product companies, particularly in food, pushed a lot of price higher over the past few years that resulted in falling volumes that they are now responding to with lower prices or less increases for some.

Overseas though, they raised prices further "to cover rising commodity costs and still maintained volume momentum."

"For the year to go, we expect price in our Global Consumer segment to be flat."

Here is what they said on the macro, "There is increasing consumer uncertainty and concern over returning to more inflation, and this has impacted consumer sentiment, particularly in the last month. This prolongs the consumer context of 2024, where consumers, especially lower income consumers, are more cautious, exhibiting more value seeking behavior and tightening their budgets as many are worried about the future, job security and rising costs. We are seeing this not just in the US but across our key markets."

"At the same time, we are all witnessing shifts in consumer preferences. They are becoming more health conscious, and this trend is continuing to gain momentum. They are cooking at home more often and increasingly shopping the perimeter for protein and produce."

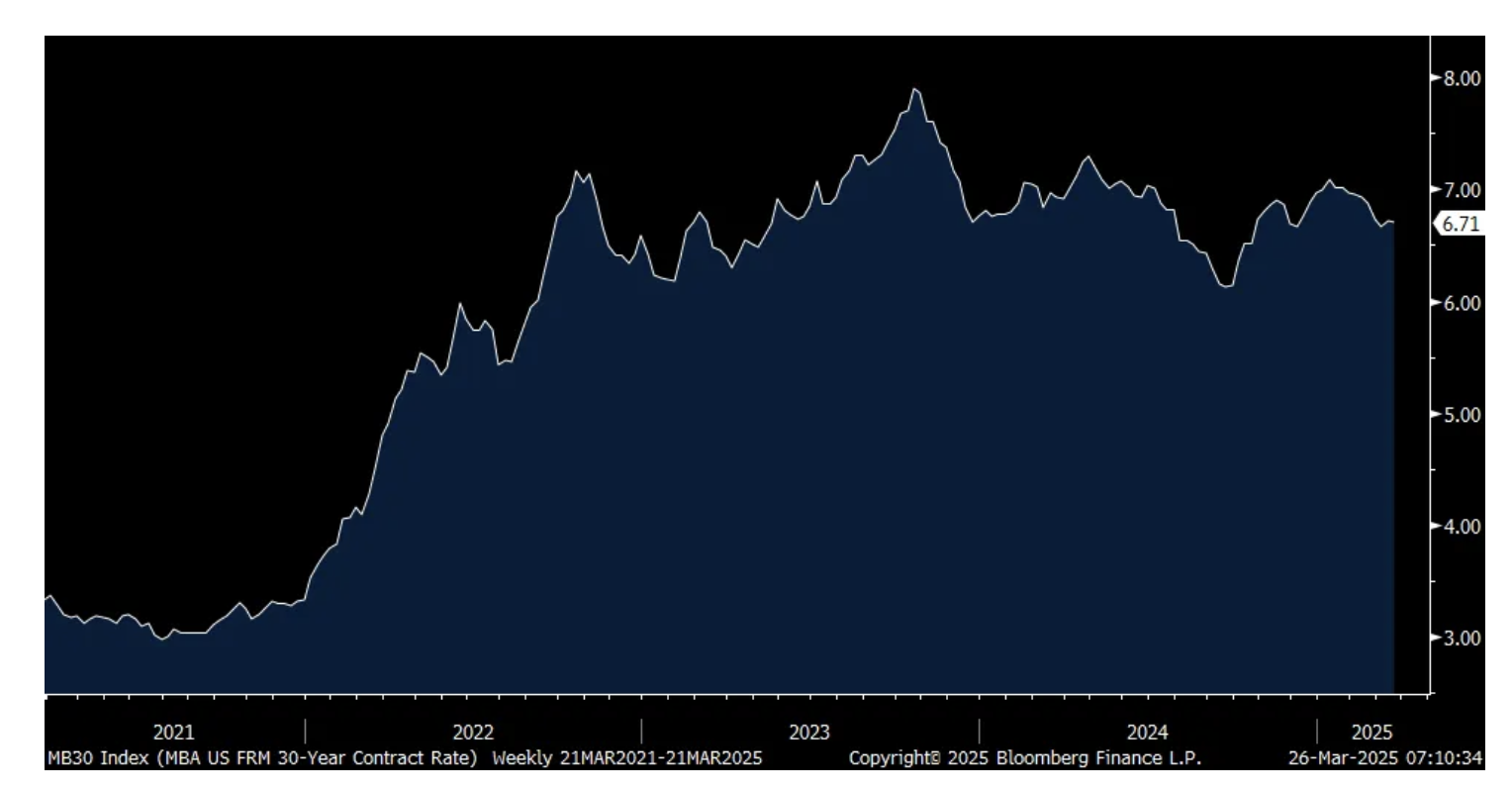

Finally, purchase applications for the week ended 3/21 were flattish for a 2nd week, up by .7% w/o/w while refi's fell by 5.3%, down for a 2nd week after a sharp rise in the two weeks prior. The average 30 yr mortgage rate held at 6.71%, off its highs for sure but still elevated which combined with a 50% rise in home prices over the past 5 years, the affordability challenge for many first time buyers remains acute.

Average 30 yr Mortgage Rate

BY Doug Kass · Mar 26, 2025, 8:33 AM EDT

* On the consumer...

BY Doug Kass · Mar 26, 2025, 7:50 AM EDT

* After being optimistic at the top of the 2025 market and pessimistic at the bottom of this year's market, optimism now reigns in technical analysis land...

Bonus — Here are some great links:

April Is the Second-Best Month

BY Doug Kass · Mar 26, 2025, 6:40 AM EDT

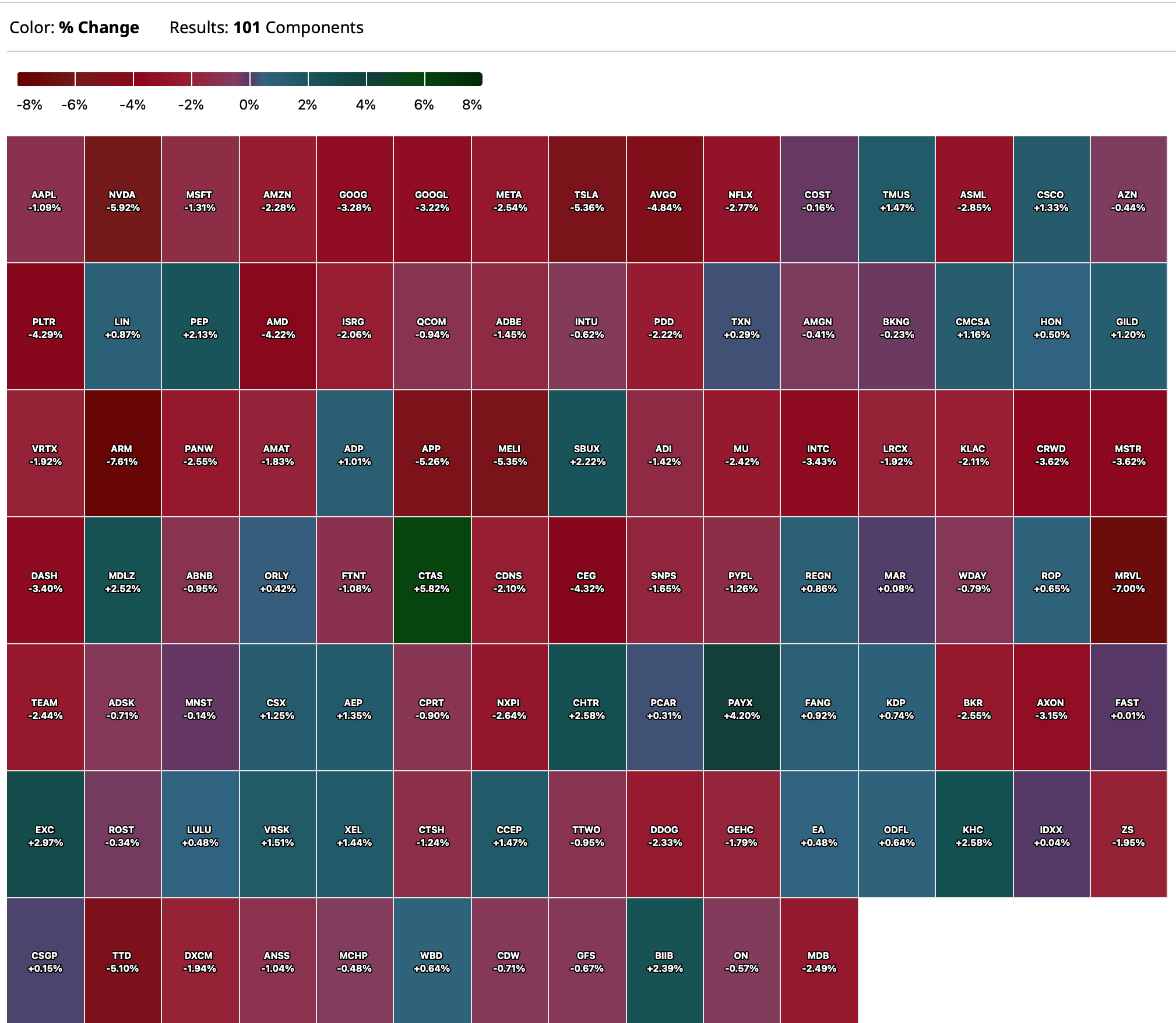

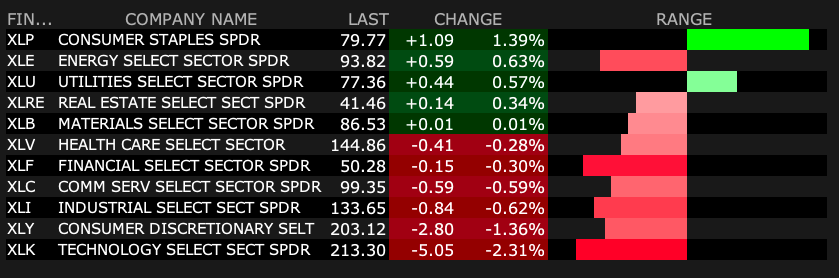

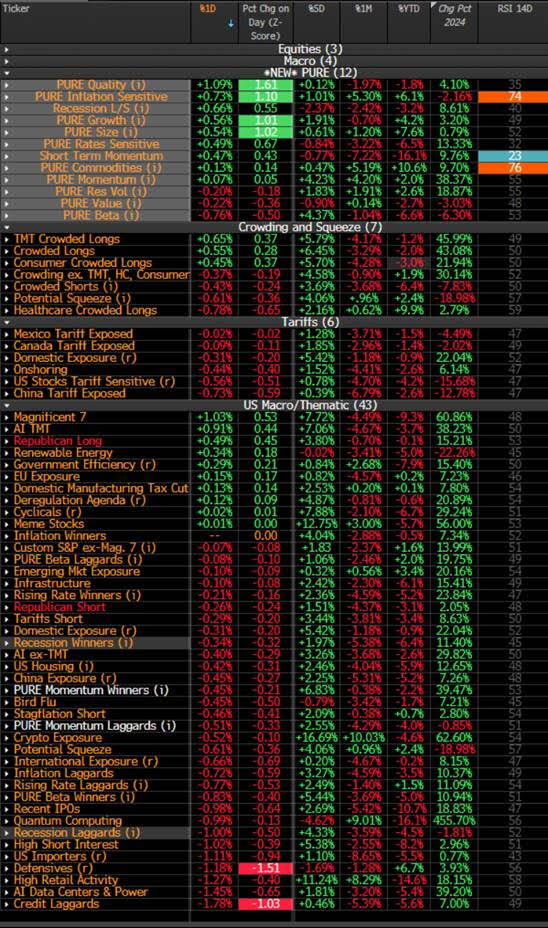

This is table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Mar 26, 2025, 6:25 AM EDT

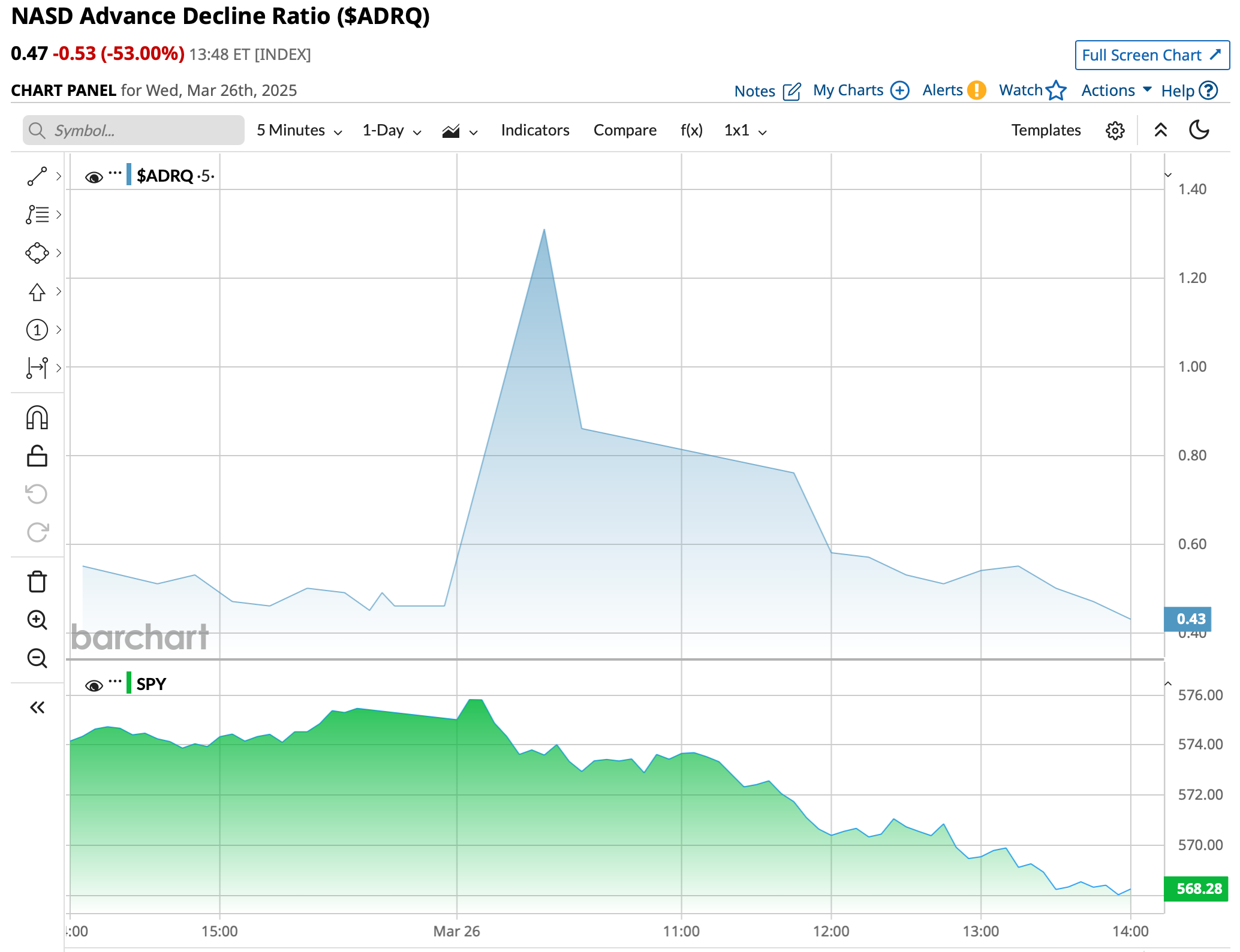

Another day of higher prices and lower volume:

BY Doug Kass · Mar 26, 2025, 6:15 AM EDT

BY Doug Kass · Mar 26, 2025, 6:05 AM EDT

From JPMorgan:

US: Stocks finished mixed; NDX led while RTY lagged. Mag 7 continued yesterday’s recovery with most of the stocks finishing +1% higher (TSLA +3.5%, while NVDA -59bp amid AI comments from BABA). The underlying price actions were worse than index level, with more than 55% of SPX stocks finishing lower today. The major downside surprise on consumer confidence (the Expectation Index at 12-year-low) led to a broad selloff in retailers (JPM Retail Index -1.4%)

and..

EQUITY AND MACRO NARRATIVE: Overall, macro data (sharp drop in consumer confidence) and corporate comments (particularly BABA’s concerns on AI spending bubbles) were not helpful for stocks, but the continuous recovery in Mag 7 helped the price actions on the index level.

BY Doug Kass · Mar 26, 2025, 5:55 AM EDT

The S&P Short Range Oscillator became more overbought at 1.85% vs. 1.35%.

BY Doug Kass · Mar 26, 2025, 5:45 AM EDT