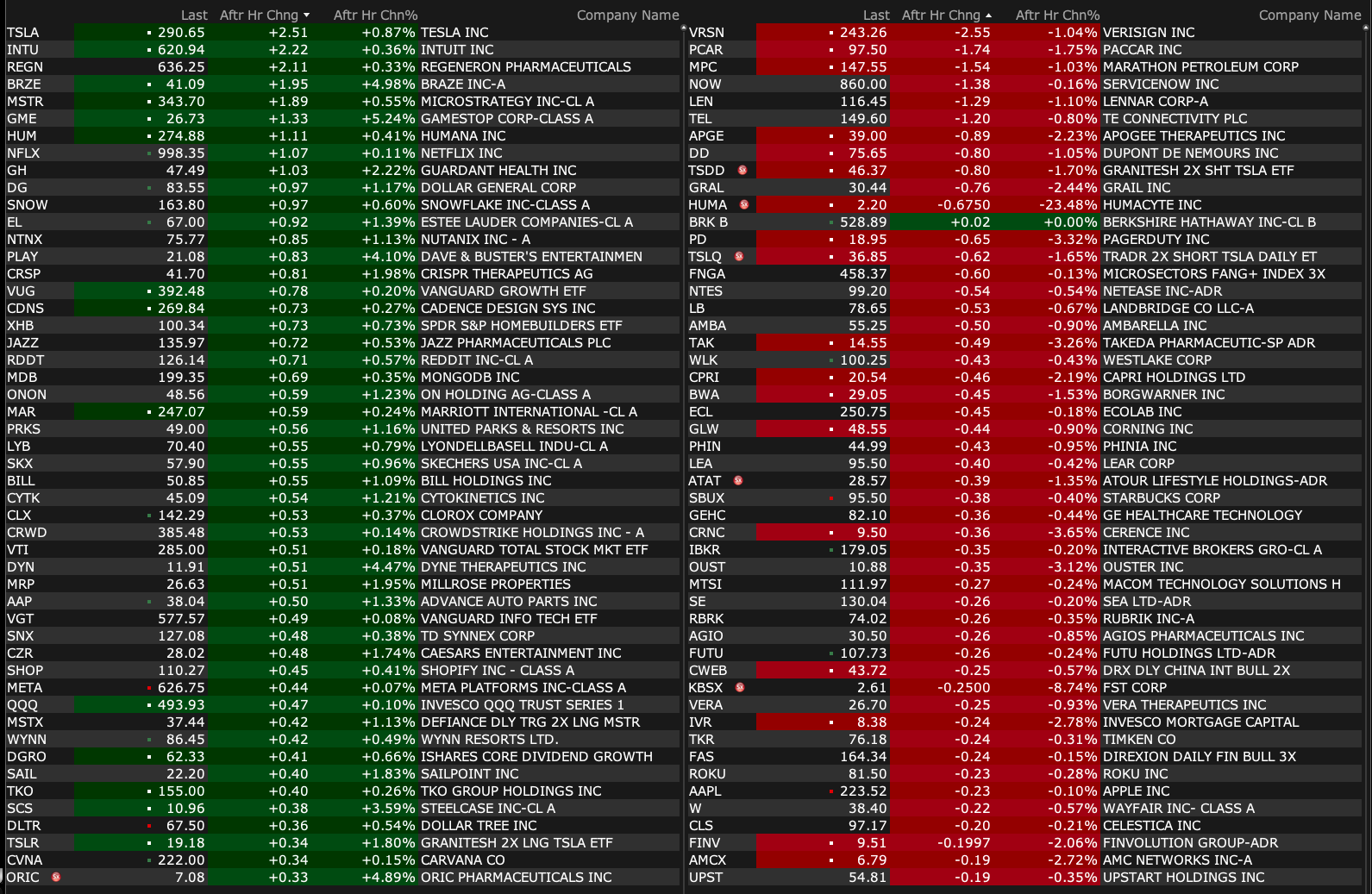

Tuesday's After-Hours Movers

As of 4:18 p.m.:

BY Doug Kass · Mar 25, 2025, 4:55 PM EDT

As of 4:18 p.m.:

BY Doug Kass · Mar 25, 2025, 4:55 PM EDT

BY Doug Kass · Mar 25, 2025, 4:35 PM EDT

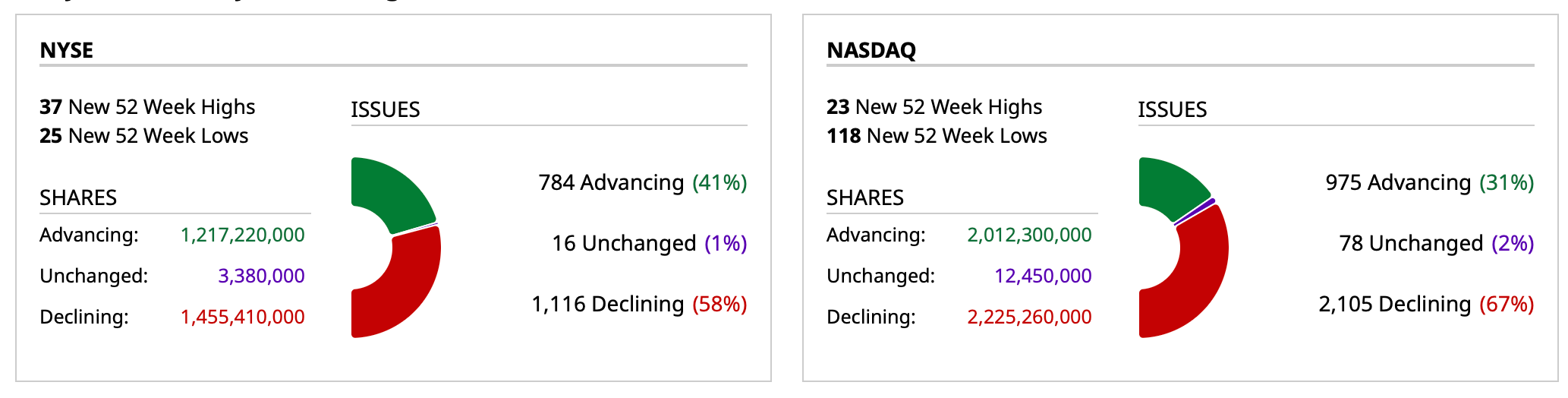

- NYSE volume 23% below its one-month average

- NASDAQ volume 15% below its one-month average

- VIX index: down 2.29% to 17.08

BY Doug Kass · Mar 25, 2025, 4:26 PM EDT

Based on my five scenarios (from very negative to very positive and attaching multiples to that distribution) I expect the S&P index to be down between five and ten percent for the full year.

It is my continued view that there is upside to about +5% (year over year), but my thinking remains that the high might have been already made in late January.

On the downside I see risk (for 2025) to be about -10% to -15% for the S&P.

Despite the anticipated and relatively narrow trading range there will be plenty of long and short opportunities on the road to the end of the year.

BY Doug Kass · Mar 25, 2025, 3:00 PM EDT

BY Doug Kass · Mar 25, 2025, 2:38 PM EDT

Keep your portfolios and children away from short-term stock predictions (and that includes mine!), which only serve to make fortune tellers look good:

BY Doug Kass · Mar 25, 2025, 2:30 PM EDT

All-time high in the price of copper:

BY Doug Kass · Mar 25, 2025, 2:20 PM EDT

* Still playing small ball...

No trades, save two tranches of shorting the indices on the gaps (of fifteen to twenty handles higher).

Gun to my head, we head down shortly.

BY Doug Kass · Mar 25, 2025, 2:05 PM EDT

From Bramo:

BY Doug Kass · Mar 25, 2025, 1:40 PM EDT

BY Doug Kass · Mar 25, 2025, 1:29 PM EDT

Posted without comment:

BY Doug Kass · Mar 25, 2025, 1:05 PM EDT

From Steph:

BY Doug Kass · Mar 25, 2025, 12:25 PM EDT

BY Doug Kass · Mar 25, 2025, 12:10 PM EDT

Long-term investment short CHGG just hit a 52-week low and is now over -95% from our cost basis.

BY Doug Kass · Mar 25, 2025, 11:55 AM EDT

From Peter Boockvar:

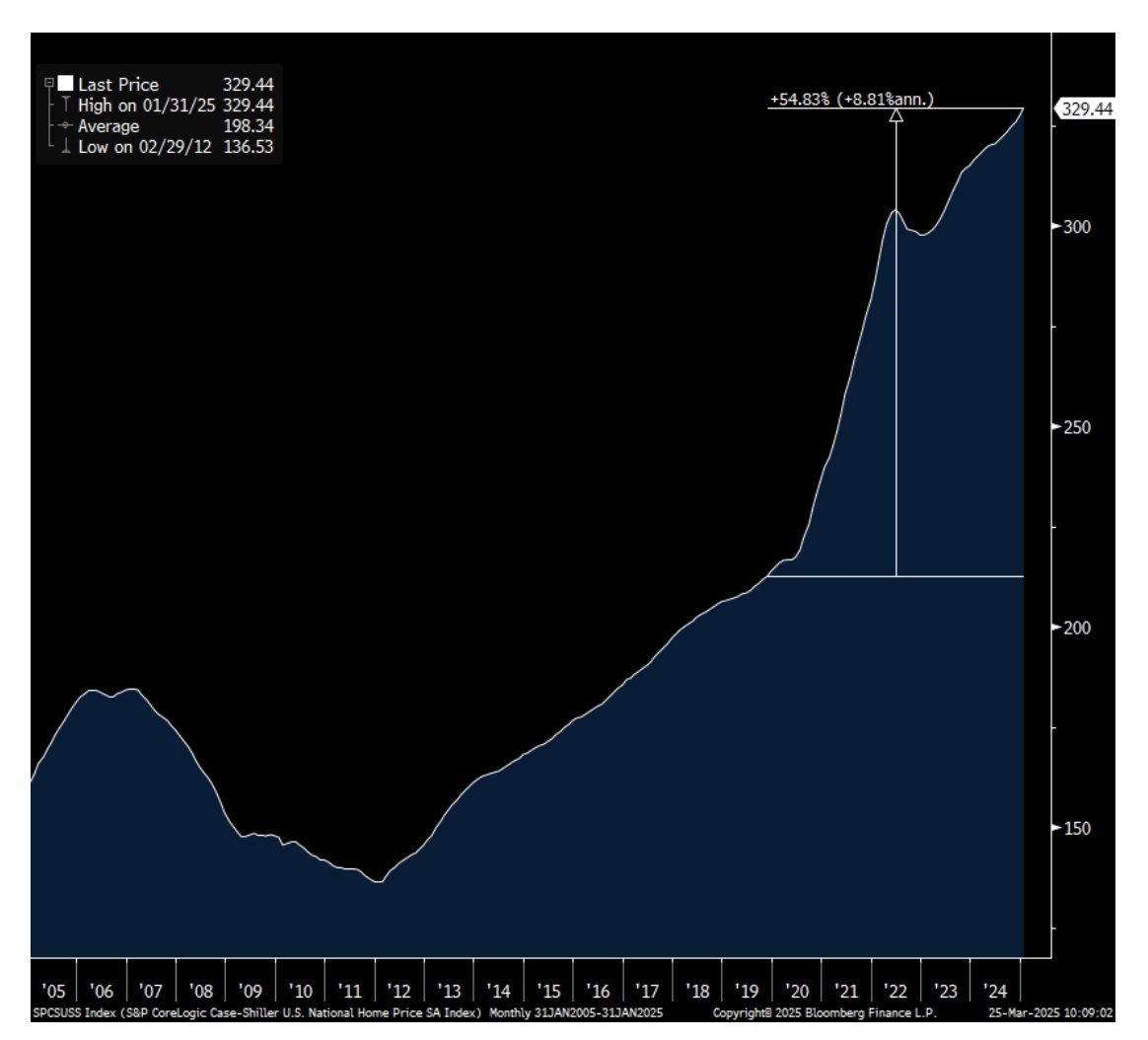

Somewhat dated but persistent nonetheless is the national home price index for January from S&P CoreLogic which rose .6% m/o/m and by 4.1% y/o/y. Versus last year the gains were led by NY with a 7.8% increase followed by Chicago up 7.5% and Boston by 6.6%. Lagging is where a lot of the new building as taken place such as in Tampa (down 1.5%), Dallas, Denver and Atlanta.

S&P Global broke down the trailing 12 months into two parts and said most of the gains came in the first half of the year with prices falling by .7% in the 2nd half “as high mortgage rates and affordability constraints weighed on buyer demand and market activity.”

On the supply side, “Inventory constraints remain a challenged, particularly in legacy metro areas, where limited new construction continues to restrict supply.”

The explain for the strength in NY and Chicago is maybe reflecting “more normalized valuations relative to frothier regions, along with continued urban recovery trends post pandemic. On the other hand, Sunbelt markets that experienced sharp run ups earlier in the cycle - like Tampa and Phoenix - have seen the most pronounced slowdowns.”

Stretching this out, the national home price index is up an unbelievable 55% since February 2020. Going back even further to the early 2000’s, the boom and bust that followed, the recovery and then the last 5 years that included massive MBS Fed buying and boy did the Federal Reserve mess around with the cost of shelter to the detriment of many but to the delight of those owning.

S&P CoreLogic Home Price Index

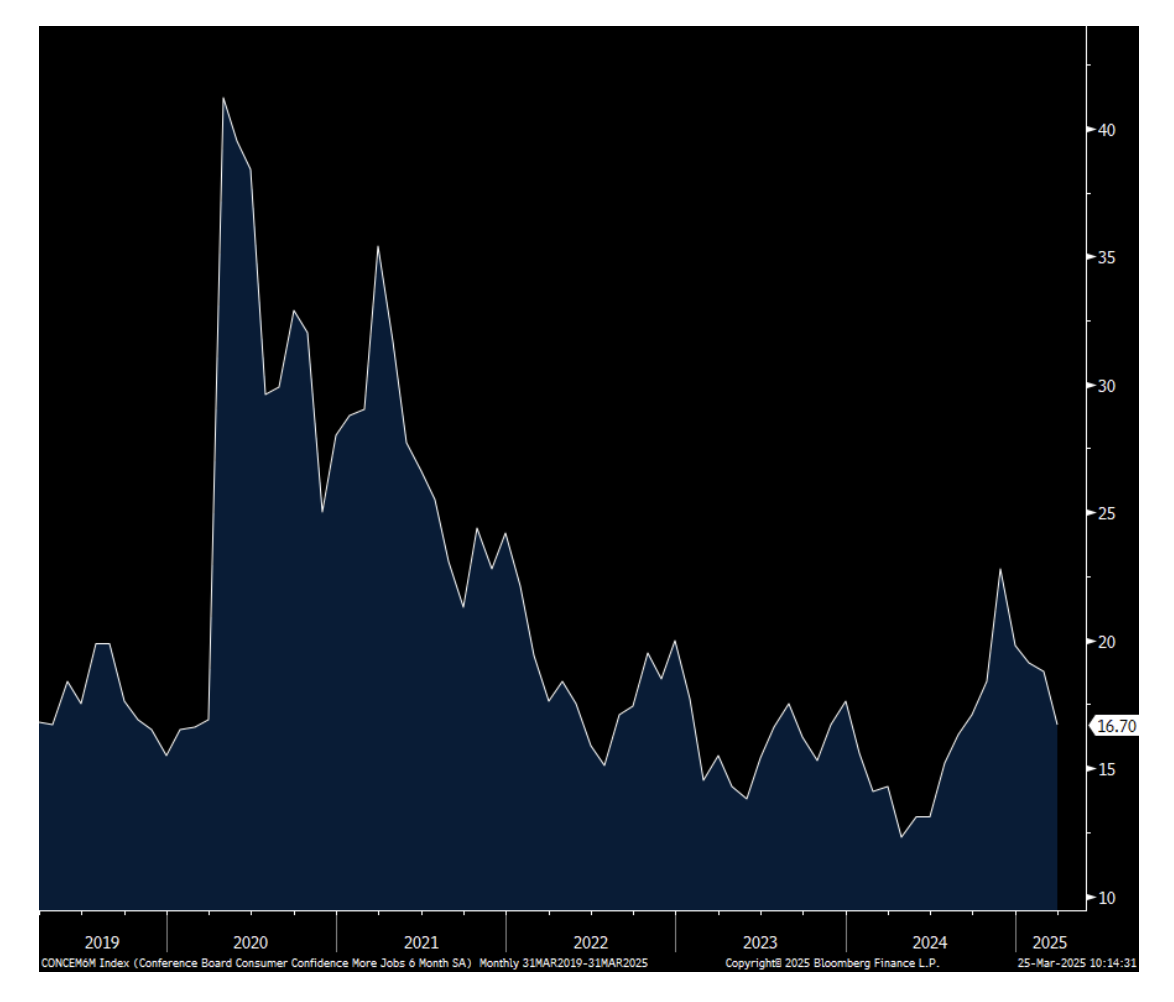

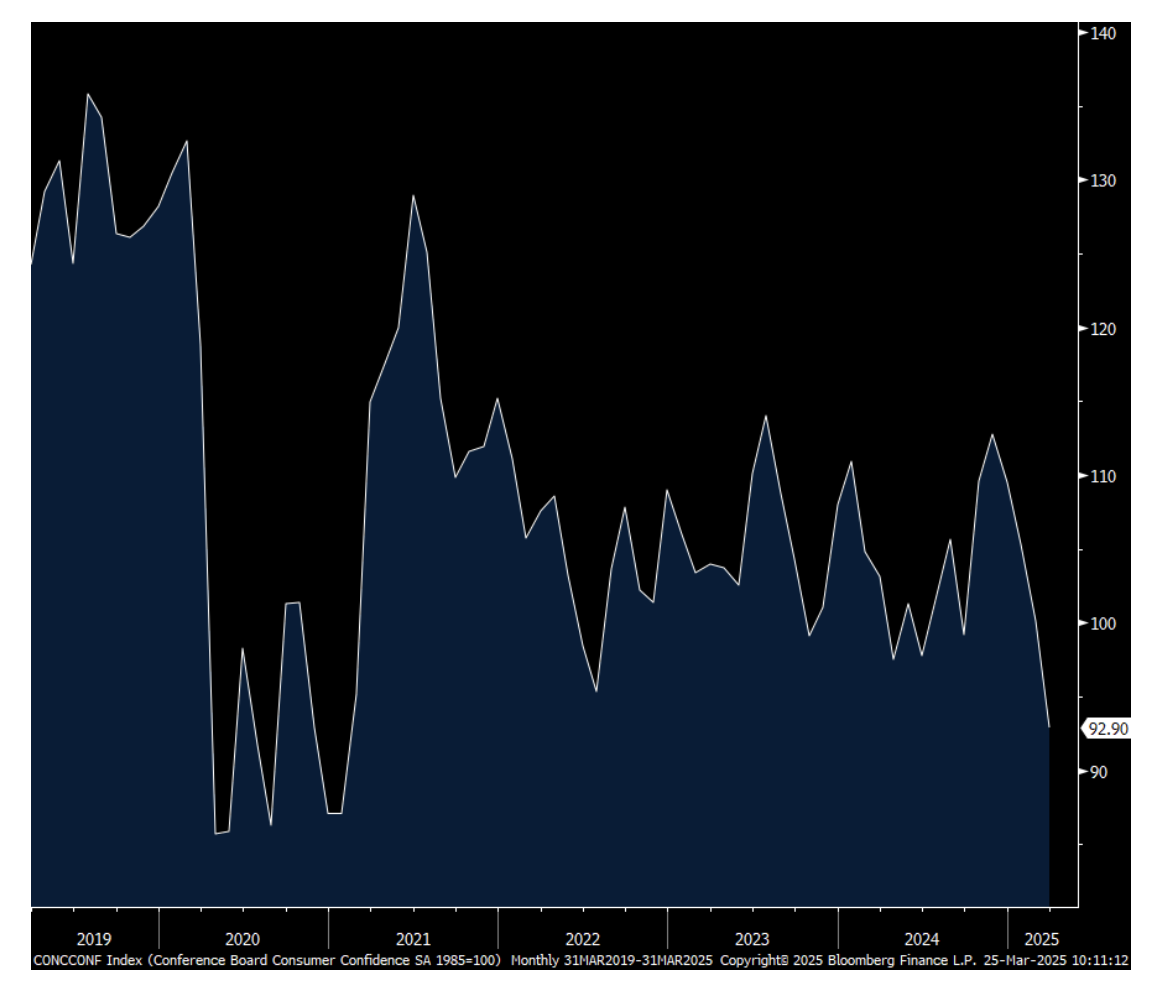

The March Consumer confidence index from the Conference Board fell to 92.9 from 100.1, just below the estimate and at the lowest level since January 2021. Most of the decline was led by the Expectations component which dropped almost 10 pts m/o/m. The Present Situation was lower by 3.6 pts from February. One year inflation expectations are now at 6.2%, up from 5.8% last month and 5.2% in the month before “as consumers remained concerned about high prices for key household staples like eggs and the impact of tariffs” said the Conference Board.

The answers to the labor market questions were little changed m/o/m but did soften last month. And, expectations over the coming 6 months for the labor market continues to deteriorate with those seeing ‘more jobs’ falling 2.1 pts to the lowest level since August 2024. Expectations for income also weakened, declining by 2.5 pts sequentially to the lowest since June 2024.

On that last point, the Conference Board said “consumers’ optimism about future income - which had held up quite strongly in the past few months - largely vanished, suggesting worries about the economy and labor market have started to spread into consumers’ assessments of their personal situations.”

Spending intentions to buy a vehicle fell to match the lowest since April 2023. They were flattish for buying a home, up by .1 pt. For major household items, they ticked up “which may reflect plans to buy before impending tariffs lead to price increases.” Vacation plans rose.

The Conference Board doesn’t break out their respondents by political party but we have to assume there is a wide divide as seen in the UoM survey. Demographically, confidence rose for those under the age of 35 but fell for those aged above, particularly the 55 and over category. Income wise, confidence deteriorated for those making under $125k and rose slightly for those making more.

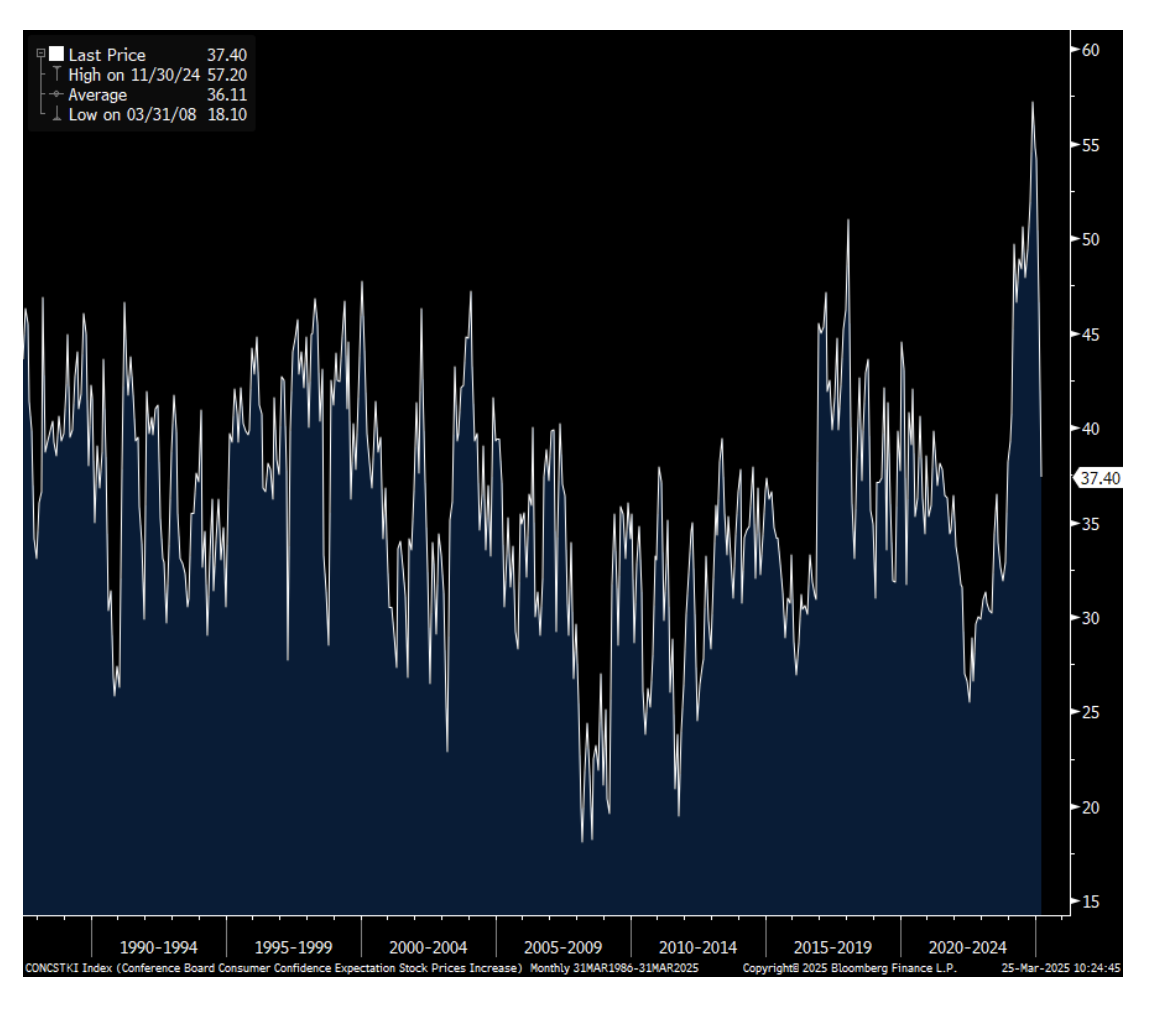

Remember back in November when 57.2% of respondents thought the stock market would rise in the coming 12 months, the highest since that question was first asked in 1987? That percentage in March is down to 37.4%, actually in line with the long term average.

Bottom line, not surprisingly, “Comments on the current Administration and its policies, both positive and negative, dominated consumers’ write-in responses on what is affecting their views of the economy. Write-in responses also showed that inflation is still a major concern for consumers and that worries about the impact of trade policies and tariffs in particular are on the rise. There were also more references than usual to economic and policy uncertainty.”

Consumer Confidence

Expectations for "More Jos"

Percent of those Expecting Higher Stock Prices in Coming 12 months

New home sales in February totaled 676k, about as expected and up from 664k last month. As heard from KB Homes and others, making a home sale has to include more discounts and incentives because of the high price and still very elevated mortgage rates.

Finally, the March Richmond manufacturing index fell back under zero at -4 from +6 in February. Prices paid and received jumped sharply m/o/m.

Also of note, the 6 month outlook for the prices paid annualized percent change went from 4.6% to 7.2%. For those received, to 4% from 3.2%.

Bottom line, as with the NY and Philly surveys, manufacturing visibility in terms of ones order book and costs has to be very limited right now.

BY Doug Kass · Mar 25, 2025, 11:45 AM EDT

Some sell-side chatter on several of my holdings:

Freshpet price target lowered to $145 from $160 at Piper Sandler Piper Sandler analyst Michael Lavery lowered the firm's price target on Freshpet to $145 from $160 and keeps an Overweight rating on the shares. The firm notes the company's revenue growth has slowed in recent weeks, driven by notably slower growth with lower- and middle-income consumers, which it expects to persist near-term.

Morgan Stanley price target raised to $129 from $124 at JPMorgan JPMorgan analyst Kian Abouhossein raised the firm's price target on Morgan Stanley to $129 from $124 and keeps a Neutral rating on the shares.

Goldman Sachs price target raised to $625 from $605 at JPMorgan JPMorgan raised the firm's price target on Goldman Sachs to $625 from $605 and keeps an Overweight rating on the shares.

BY Doug Kass · Mar 25, 2025, 11:35 AM EDT

BY Doug Kass · Mar 25, 2025, 11:25 AM EDT

NYSE volume is 27% below its one-month average;

Nasdaq volume is even with its one-month average;

VIX index is down 0.29% to 17.43

BY Doug Kass · Mar 25, 2025, 11:15 AM EDT

From Anthony:

BY Doug Kass · Mar 25, 2025, 11:05 AM EDT

* Still playing "small ball..."

I've added to very small Index short, with S&P cash up 20 handles:

* SPY $576.19

* QQQ $493.20

BY Doug Kass · Mar 25, 2025, 10:57 AM EDT

BY Doug Kass · Mar 25, 2025, 10:55 AM EDT

BY Doug Kass · Mar 25, 2025, 10:45 AM EDT

From JPMorgan:

US: Futs are lower as we saw investors taking some profits from yesterday’s rally. Mag 7 are all lower pre-market: NVDA -0.7% and TSLA -0.7%. Bond yields are 1-3bp higher. Commodities are mostly higher led by precious metals (silver) and oil. Today, we will receive consumer confidence at 10am ET. Feroli see consumer confidence to print 95.0 vs 94.0 survey vs. 98.3 prior.

and..

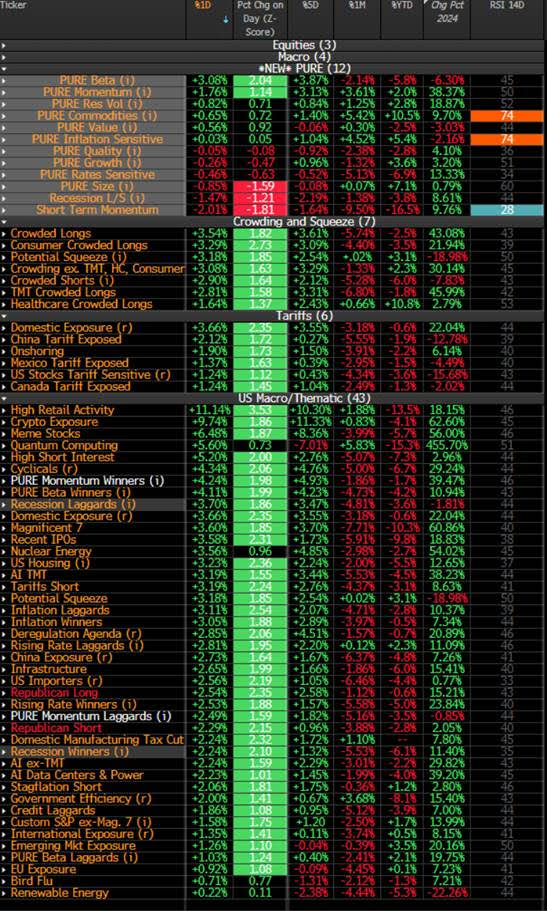

EQUITY AND MACRO NARRATIVE: Yesterday, we saw a full risk-on rally with nearly 85% of the stocks finishing higher, given a combination of short-squeezing (High Short Interest +5.2%) and crowded longs/Mag 7 being brought back after weeks of selloff. The rally was mostly driven by weekend headlines on Trump’s tariffs being more “targeted,” along with further comments from Trump that they may give “a lot of countries breaks on tariffs.”

BY Doug Kass · Mar 25, 2025, 10:21 AM EDT

BY Doug Kass · Mar 25, 2025, 10:00 AM EDT

* You could say I am now on the dark side of the road...

It ain't no use to sit and wonder why, babe

If'n you don't know by now

And it ain't no use to sit and wonder why, babe

It'll never do somehow

When your rooster crows at the break of dawn

Look out your window and I'll be gone

You're the reason I'm a-traveling on

But don't think twice, it's all right

- Bob Dylan, Don't Think Twice It's All Right

Next Monday I will complete my 28th year writing for TheStreet.

I am not sure if anyone in this line of work has written for one entity for so long.

My estimate is that I have written more than thirty million words since 1997 in my Diary.

So it ain't no use in calling out my name, gal Like you never done before

And it ain't no use in calling out my name, gal

I can't hear you anymore

I'm a-thinking and a-wonderin' walking down the road

I once loved a woman, a child, I'm told

I give her my heart but she wanted my soul

But don't think twice, it's all right

- Bob Dylan and Eric Clapton (one of my favorite versions)

My friendships established (the old ones like Smails, Mikey, Johnny The Greek and the new ones like TechNova, MasterHedge, Robbo, etc.) and the conversations we have had have been a good enough reason to travel on with all you between 4 AM and 6 PM nearly every trading day.

When the rooster crows at the break of dawn, well, you are all the reason I have been traveling on for these many years.

This morning I just wanted to say, thanks. And I hope I didn't waste your precious time...

"All I can do is be me, whoever that is."

- Bob Dylan

BY Doug Kass · Mar 25, 2025, 9:30 AM EDT

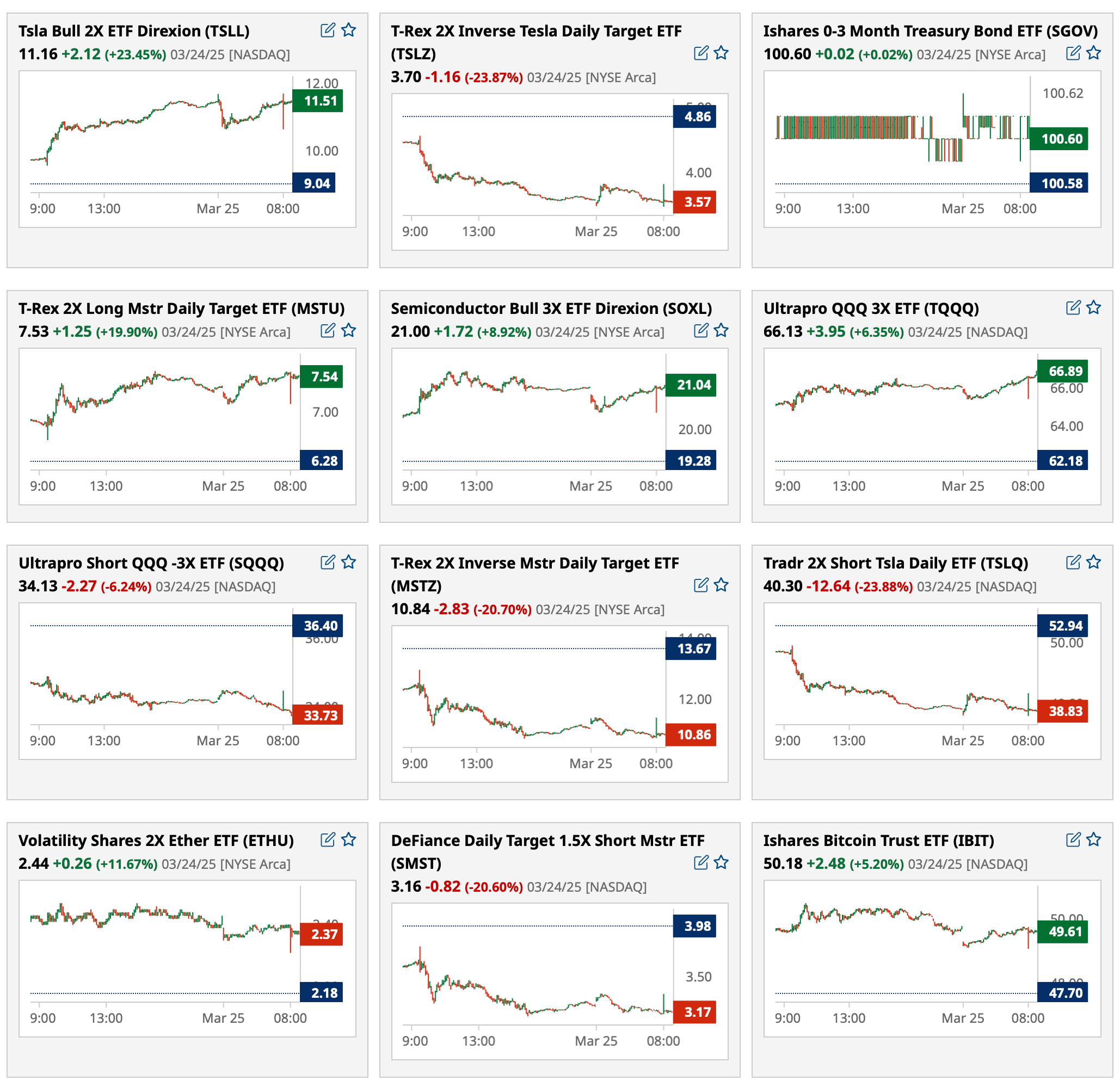

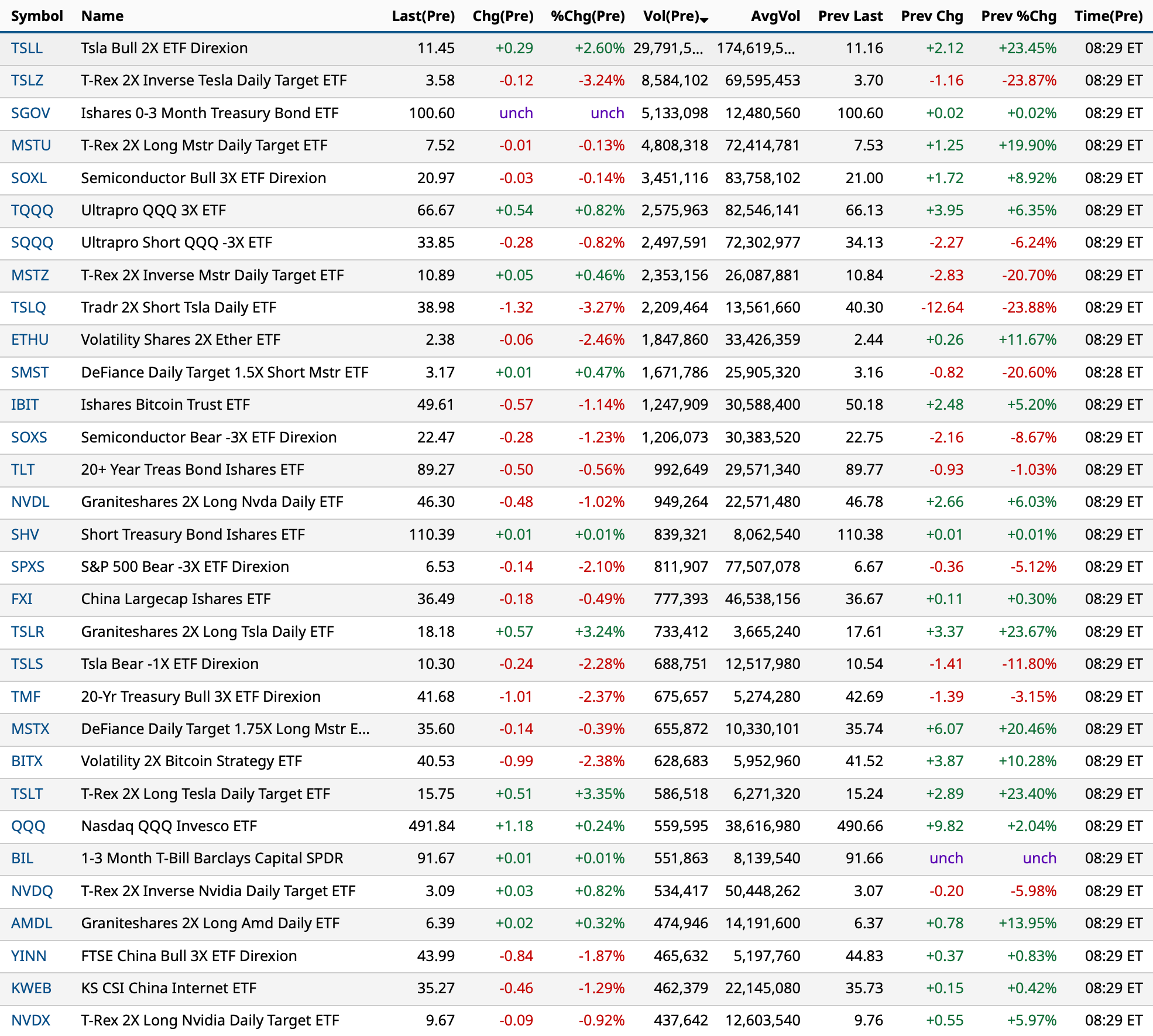

Most active premarket ETFs at 8:29 a.m. ET; SPY & QQQ not even in the top 24:

BY Doug Kass · Mar 25, 2025, 9:15 AM EDT

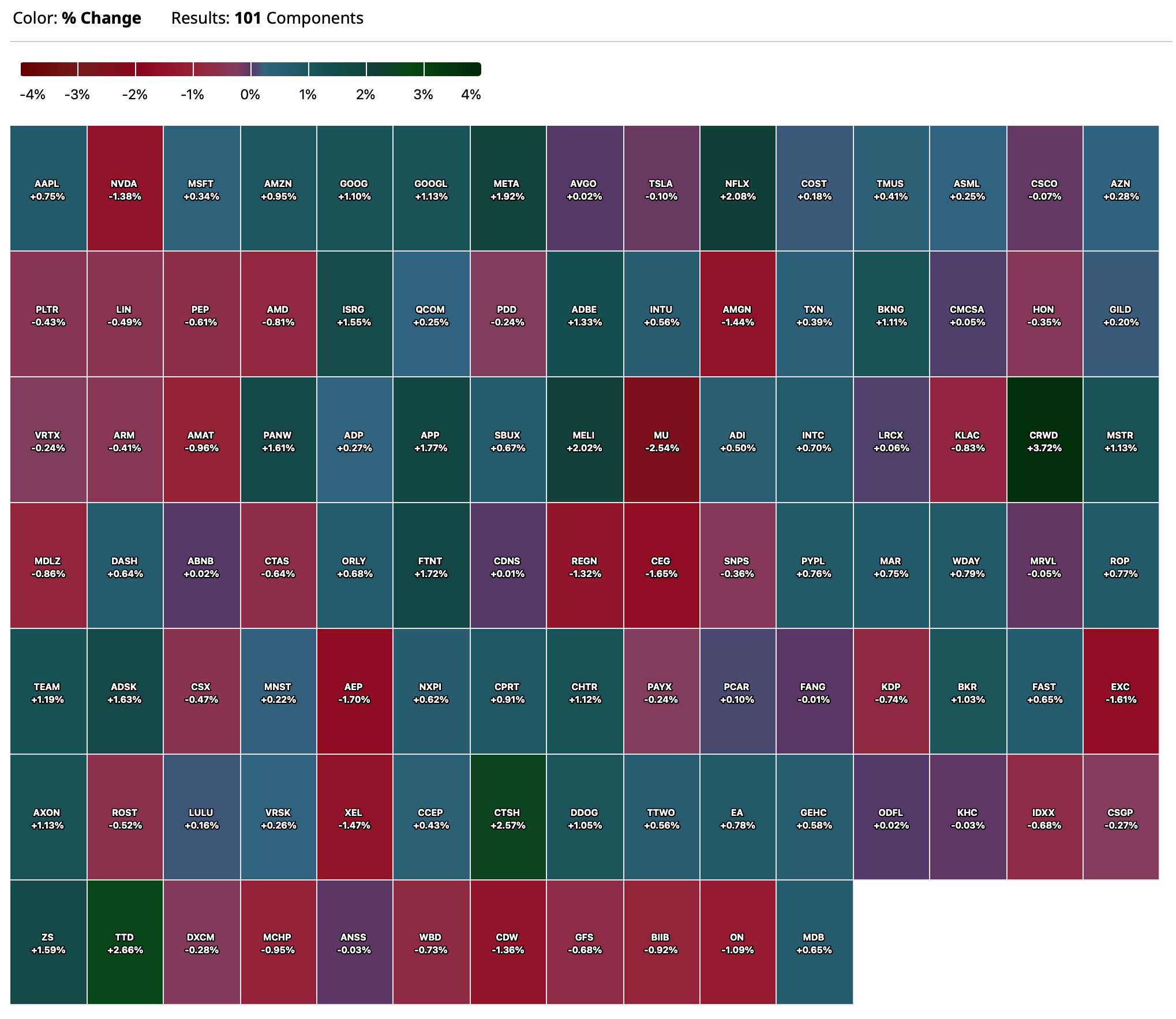

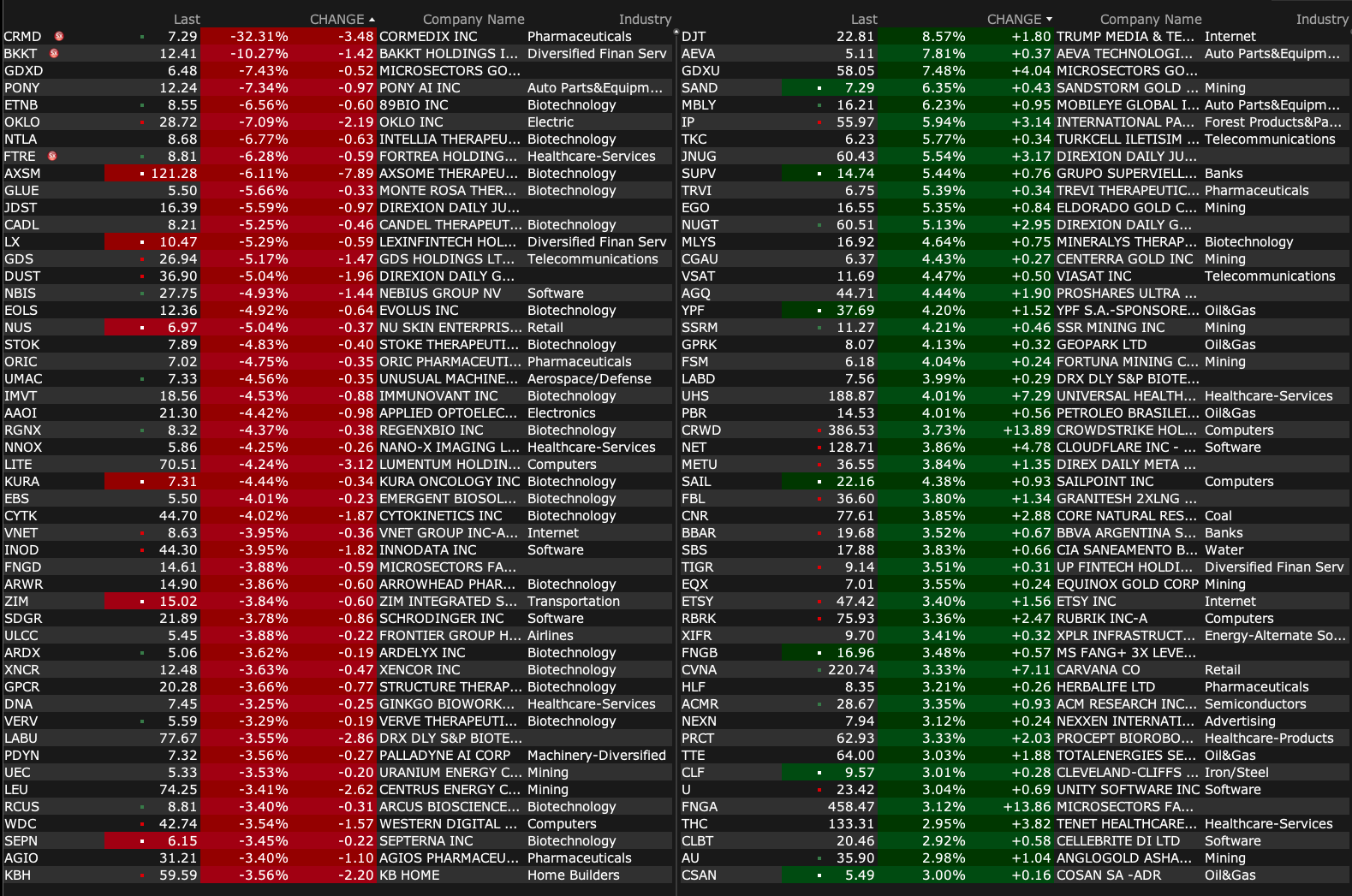

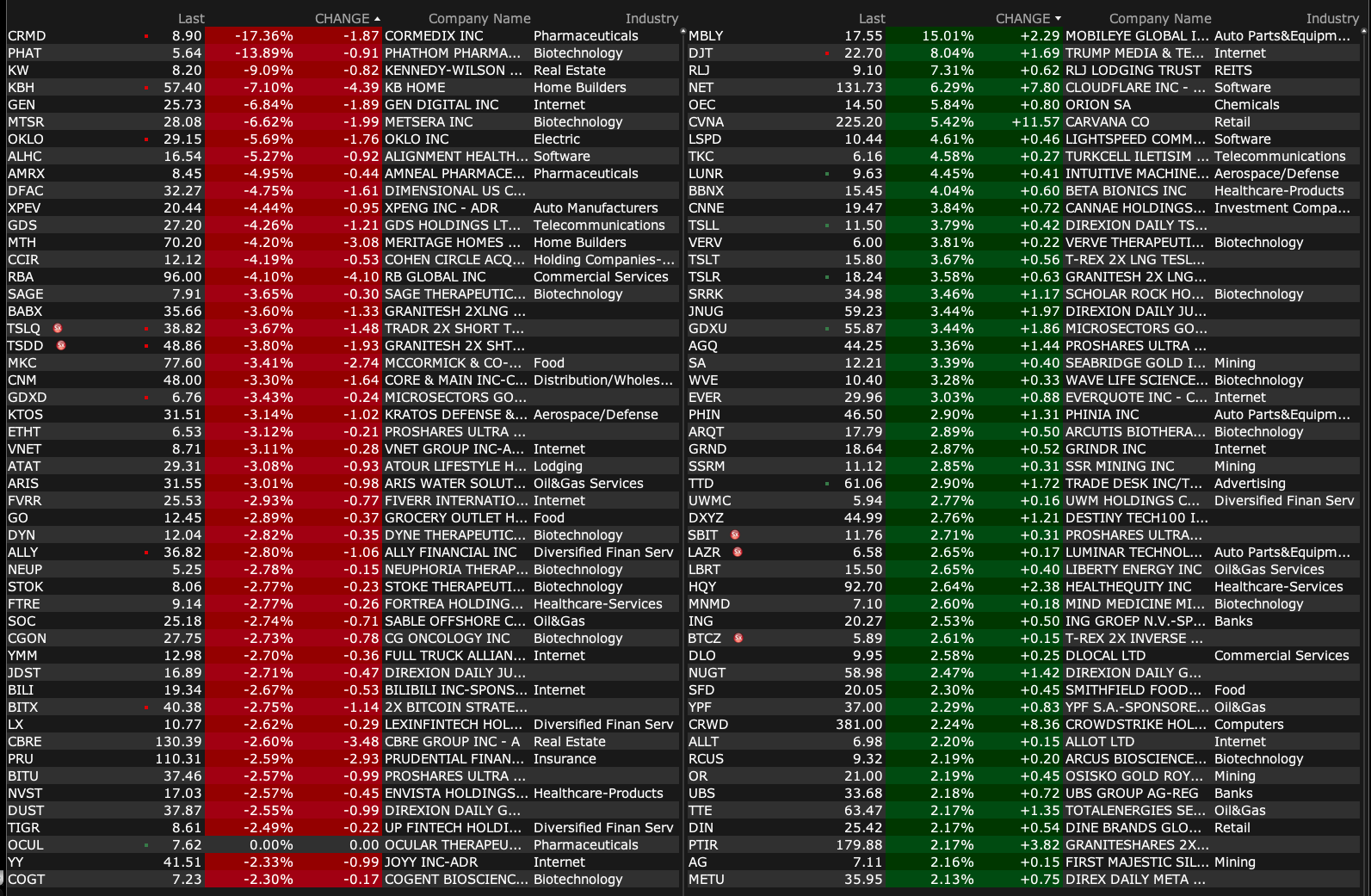

Premarket percentage movers as of 8:47 a.m. ET:

BY Doug Kass · Mar 25, 2025, 9:05 AM EDT

-TNON +351% (US FDA clears Catamaran SIJoint Fusion System for new indication to Augment Spinal Fusion)

-MBLY +13% (Volkswagen Group cooperates with Valeo and Mobileye to enhance driver assistance in future MQB vehicles up to Level 2+ (“enhanced partially automated driving”) in its upcoming vehicle portfolio)

-PSIX +12% (earnings)

-DJT +9.0% (intends to partner with Crypto.com to launch ETFs)

-ATNM +8.7% (announces Supply Agreement with Eckert & Ziegler for Ac-225 Radioisotope to Support Comprehensive Development Activities; to host investor call to highlight clinical programs)

-XAIR +8.7% (subsidiary NeuroNOS secures $2.0M in Funding to Advance Development of an Innovative Autism Therapy)

-NET +5.5% (Tier1 firm Raised NET to Buy from Underperform, price target: $160)

-CVNA +5.3% (Morgan Stanley Raised CVNA to Overweight from Equal Weight, price target: $280)

-FUFU +4.5% (earnings)

-SRRK +3.5% (US FDA Grants Priority Review for BLA and EMA Accepts MAA for Apitegromab as treatment for Spinal Muscular Atrophy)

-ILMN +2.3% (reportedly Board Chairman Stephen MacMillan retiring from Board; Current board member Scott Gottlieb will become Chairman and Activist investor Keith Meister will join the Board)

-CRWD +2.0% (BTIG Raised CRWD to Buy from Neutral, price target: $431)

-KALV +2.0% (announces early completion of enrollment in KONFIDENT-KID Pediatric HAE Trial)

-MURA -48% (provides update on Phase 3 ARTISTRY-7 Trial of Nemvaleukin in combination with KEYTRUDA (pembrolizumab) in patients with Platinum-Resistant Ovarian Cancer; based on overall survival data observed in interim analysis in platinum-resistant ovarian cancer, Mural will not progress trial to final analysis)

-PROP -20% (prices 8.6M common share secondary offering)

-UNF -10% (Cintas acquisition discussion with UniFirst Corp. 'terminated')

-OKLO -6.7% (earnings; identified a material weakness in our internal control over financial reporting in the area of complex and infrequent accounting, which could impact earnings report)

-CNM -5.3% (earnings, guidance; announces executive leadership changes)

-KBH -5.0% (earnings, guidance)

-GNLX -3.6% (Genelux and Newsoara Announce Positive Preliminary Phase 1b/2 Data of Olvi-Vec in Advanced Small-Cell Lung Cancer)

-MKC -3.4% (earnings, guidance)

-KZR -3.3% (earnings, guidance; announces topline results from PORTOLA Phase 2a trial evaluating Zetomipzomib for treatment of patients with autoimmune hepatitis)

-DFLI -3.1% (earnings, guidance)

-ALLY -2.6% (BTIG Cuts ALLY to Sell from Neutral, price target: $30)

-PONY -2.5% (earnings)

-BOLT -2.4% (earnings)

-ATAT -2.3% (earnings, guidance)

-AEP -2.1% (files to sell $2B public offering of common stock with a forward component; prices 19.6M shares at $102/shr)

-EPAC -2.0% (earnings, guidance)

BY Doug Kass · Mar 25, 2025, 8:55 AM EDT

From Peter Boockvar:

By now I'm sure you've heard about the concept of the "Mar-a-Lago Accord," a reworking of the financial system with the US dollar at the center of it. Well, the whole idea came from a paper that the current Chair of the White House Council of Economic Advisors, Stephen Miran, wrote last November and with the help of Zoltan Pozsar. The paper was titled "A User's Guide to Restructuring the Global Trading System."

In Miran's mind, "The root of the economic imbalances lies in persistent dollar overvaluation that prevents the balancing of international trade, and this overvaluation is driven by inelastic demand for reserve assets. As global GDP grows, it becomes increasingly burdensome for the United States to finance the provision of reserve assets and the defense umbrella, as the manufacturing and tradeable sectors bear the brunt of the costs."

Also in the paper, he advocates tariffs and the "possible implementation schemes" and how it will influence the dollar now (should go higher) and thereafter (will be an attempt to get it lower). He also gives his idea about strong arming foreign holders of US Treasuries to take 100 year bonds in return for the holdings they have and a defense security guarantee we will give them. And the concept of revaluing the 8,000 tons of gold that the US Treasury/Fed holds was also raised by Miran and even the possibility of selling some of it.

In the paper he said "As currency accords are typically named after resorts where they are negotiated, like Bretton Woods and Plaza, with some poetic license I'll describe the potential agreement in the Trump Administration as others have done as the prospective "Mar-a-Lago Accord."

As to what it would do, "Such a Mar-a-Lago Accord gives form to a 21st Century version of a multilateral currency agreement. President Trump will want foreigners to help pay for the security zone provided by the United States. A reduction in the value of the dollar helps create manufacturing jobs in America and reallocates aggregate demand from the rest of the world to the U.S. The term-out of reserve debt helps prevent financial market volatility and the economic damage that would ensue. Multiple goals are accomplished with one agreement."

Miran in the paper made it a point to say "This essay is not policy advocacy...My analysis reflects only my own views, not those of anyone on President Trump’s team or Hudson Bay Capital" but when he took his new position we all assumed these policy steps were on the docket and all of this has created quite a stir (I first mentioned it last month after Jillian Tett talked about this in an FT article which came soon after I was with Zoltan Pozsar at a conference in which he laid out a lot of this) when it was first released but greater focus over the past few months as tariffs have taken center stage in terms of policy and we've seen big rallies and declines in the US dollar.

I bring this all up because as he said in the paper that this was "not policy advocacy" he repeated that in an interview with Bloomberg yesterday. In an answer to the question "Can you tell me how much of this is in the works?"

He said "So I'm glad you brought that up because this paper seems to have taken on a life of its own, against all my intents. Look, I'm pretty clear in that paper that it's a catalog of available options and you know, it's a recipe book and I'm trying to evaluate how useful or not useful or easy or difficult those various receipes are to make. Some of them are easy, some are tough, some are filling, satisfying meals and some will leave you hungry again in a half an hour. And my goal in that paper was to provide an evaluation of options so that a cost benefit analysis of risks and rewards so that whoever was making the decision, sort of could have that available if helpful. To be clear, I'm not the chef, right? The President is the chef and he's been very clear, very clear that he's focused on fair and reciprocal tariffs. He couldn't be clearer. And so anybody who's anybody who's thinking that something that I included in a catalog in November is the source of what the policy agenda is now, I think that's wrong."

So if the US dollar is theoretically supposed to rise with the implementation of tariffs but the ultimate goal is to have it drop thereafter, is this Accord going to happen Miran was asked?

He said "Could it be something that is entertained down the road? Sure it could, but right now the president is focused on tariffs."

Here is a link to the original paper he wrote which many of you I'm sure have seen.

From KB Homes and their earnings call:

"Consumers are continuing to cope with affordability concerns and uncertainties around macroeconomic and geopolitical events. As a result, consumer confidence has declined sequentially each month for the past several months and homebuyers are moving more slowly in making their purchase decisions. While longer-term housing market conditions remain favorable, driven by demographics and an undersupply of homes, demand at the start of the spring selling season has been more muted than we have seen over the past few years. As a result of this softer selling environment, we are lowering our revenue guidance for fiscal 2025."

Economic confidence has risen in Germany with the new Chancellor and release of the 'debt brake'. The March IFO business confidence index rose to 86.7 from 85.3 as expected but is now at the best level since July 2024, though still dancing along the bottom. Most of the lift off the lows has come in the Expectations component as Current Conditions are still muted. The IFO said succinctly, "German businesses are hoping for a recovery." Improvement in manufacturing confidence led the m/o/m increase with also a lift in services, trade and construction.

The euro is up, bund yields are lower and stocks in the DAX continue to rally. I think there is a growing chance that the ECB holds rate policy unchanged in April.

Global bond yields though are rising too as any dilution to the upcoming Trump tariffs would be well received economically speaking and why the US 10 yr yield is back to 4.35-.36% and the 2 yr yield is back above 4%.

German IFO

BY Doug Kass · Mar 25, 2025, 8:42 AM EDT

BY Doug Kass · Mar 25, 2025, 7:53 AM EDT

* Another lesson learned.. stay independent of view and do your own homework.

For about six months we had a hefty short position in homebuilders. The group, because of strong absolute and relative stock price performance, was admired by the "talking heads" who know everything about price and nothing about value.

Since then the stocks have gone from heroes to goats.

Yesterday KB Home KBH whiffed and lowered guidance:

From briefing.com:

KB Home misses by $0.08, misses on revs, deliveries decreased 9%; Lowers FY25 housing revenue and housing gross profit margin guidance (61.78 +2.03)

We saw this coming and I made a mistake in covering my homebuilding shorts too early.

Mea culpa.

BY Doug Kass · Mar 25, 2025, 7:38 AM EDT

There were several reasons behind my reshorting of the indices on Monday.

Besides the developing overbought (from oversold) market, the declining volume (on higher prices) was a feature of yesterday's sharp ramp higher:

As I mentioned during the day:

Today's volume is weak, accompanied by only 3-1 up/down volume.

Ten days ago I purchased equities (at the height of the tariff concerns) but I have been peeling off on strength.

My guess is that we can move up only a bit longer — maybe mid-to-late week.

I would short more aggressively on that final move (were it to occur), but, given the plethora of uncertainties I am playing (and plan to continue to play).... Small Ball.

By Doug Kass Mar 24, 2025 2:20 PM EDT

BY Doug Kass · Mar 25, 2025, 6:40 AM EDT

Bonus — Here are some great links:

Stocks Rarely Peak in February

BY Doug Kass · Mar 25, 2025, 6:25 AM EDT

The S&P Short Range Oscillator has flipped back to overbought — at 1.35% vs. -1.58%.

Late yesterday morning I began to reshort the indices:

I just reshorted the indices after the climb from Friday morning's lows:

* (SPY) $573.68

* (QQQ) $490.01

By Doug Kass Mar 24, 2025 11:42 AM EDT

BY Doug Kass · Mar 25, 2025, 6:15 AM EDT

BY Doug Kass · Mar 25, 2025, 6:05 AM EDT

Wolf Street howls about the SPAC implosion.

BY Doug Kass · Mar 25, 2025, 5:55 AM EDT

BY Doug Kass · Mar 25, 2025, 5:45 AM EDT