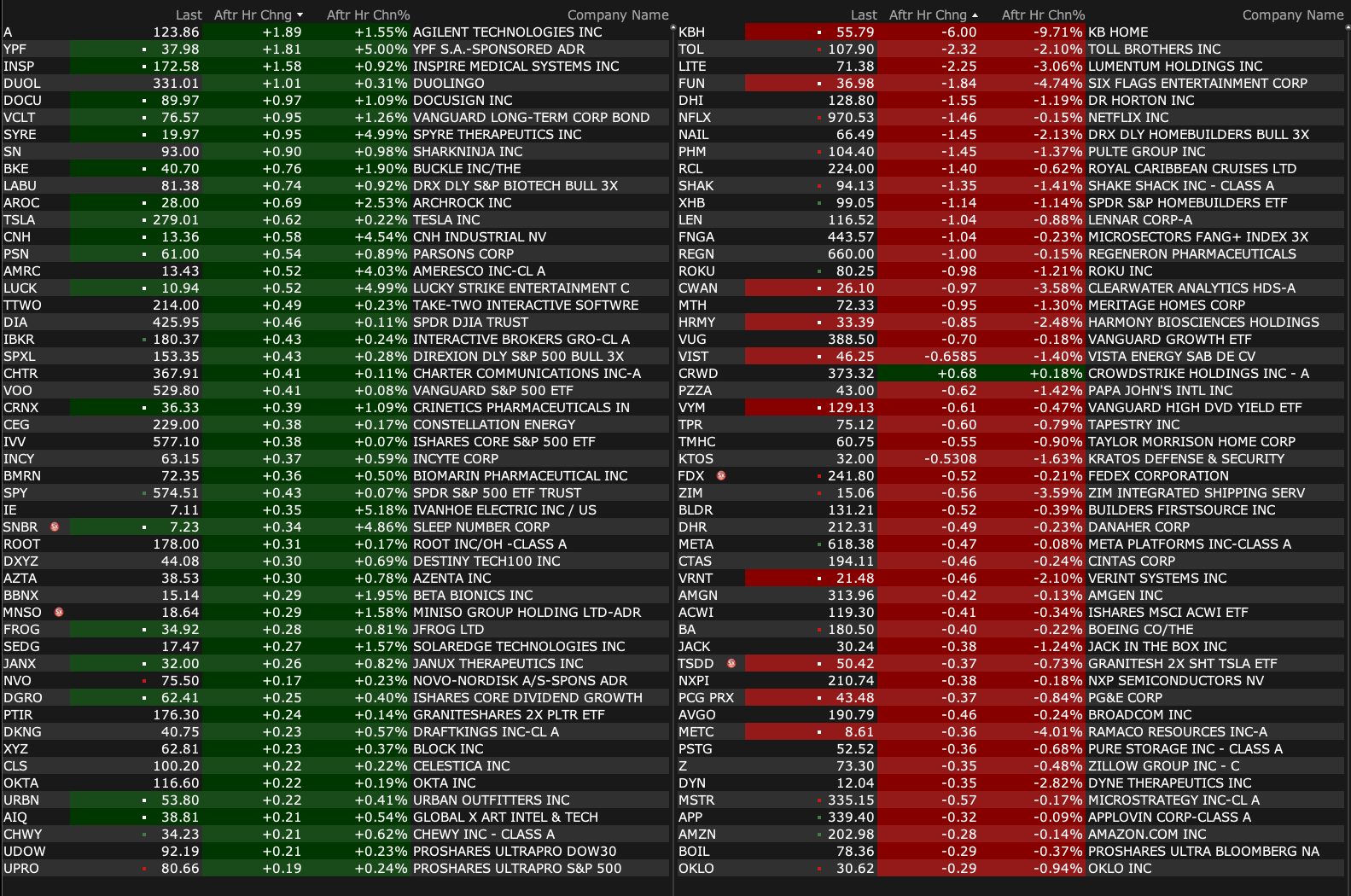

Monday's After-Hours Movers

As of 4:19 p.m., with homebuilders topping decliners after KBH miss:

BY Doug Kass · Mar 24, 2025, 4:35 PM EDT

As of 4:19 p.m., with homebuilders topping decliners after KBH miss:

BY Doug Kass · Mar 24, 2025, 4:35 PM EDT

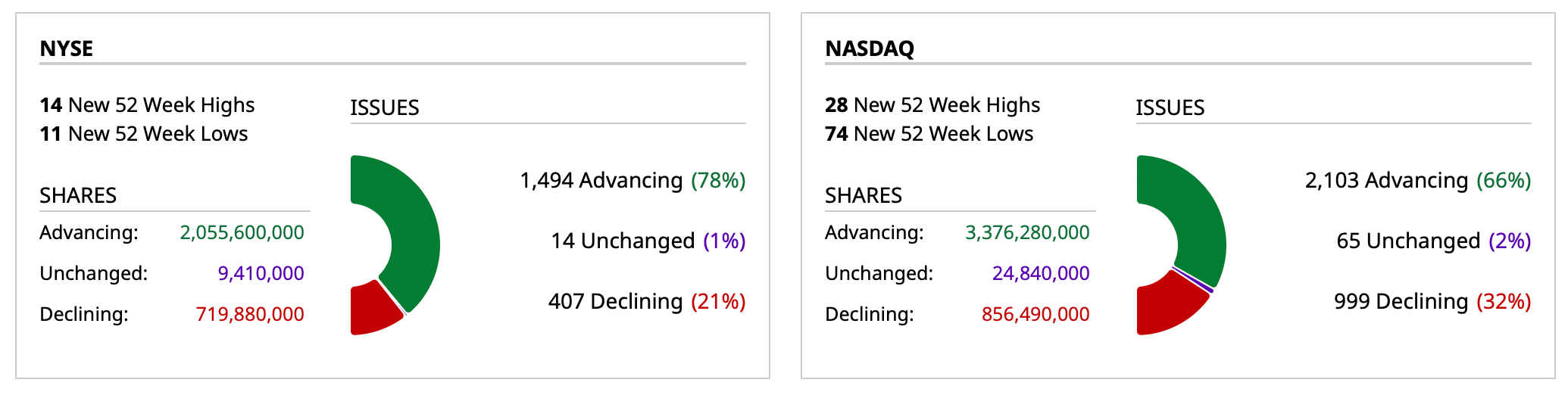

- NYSE volume 26% below its one-month average

- NASDAQ volume 14% below its one-month average

- VIX index: down 9.28% to 17.49

BY Doug Kass · Mar 24, 2025, 4:23 PM EDT

BY Doug Kass · Mar 24, 2025, 3:16 PM EDT

Wolf Street howls about services activity and cost pressures in the domestic economy.

BY Doug Kass · Mar 24, 2025, 2:36 PM EDT

Today's volume is weak, accompanied by only 3-1 up/down volume.

Ten days ago I purchased equities (at the height of the tariff concerns) but I have been peeling off on strength.

My guess is that we can move up only a bit longer — maybe mid-to-late week.

I would short more aggressively on that final move (were it to occur), but, given the plethora of uncertainties I am playing (and plan to continue to play).... Small Ball.

BY Doug Kass · Mar 24, 2025, 2:20 PM EDT

BY Doug Kass · Mar 24, 2025, 12:58 PM EDT

From Peter Boockvar:

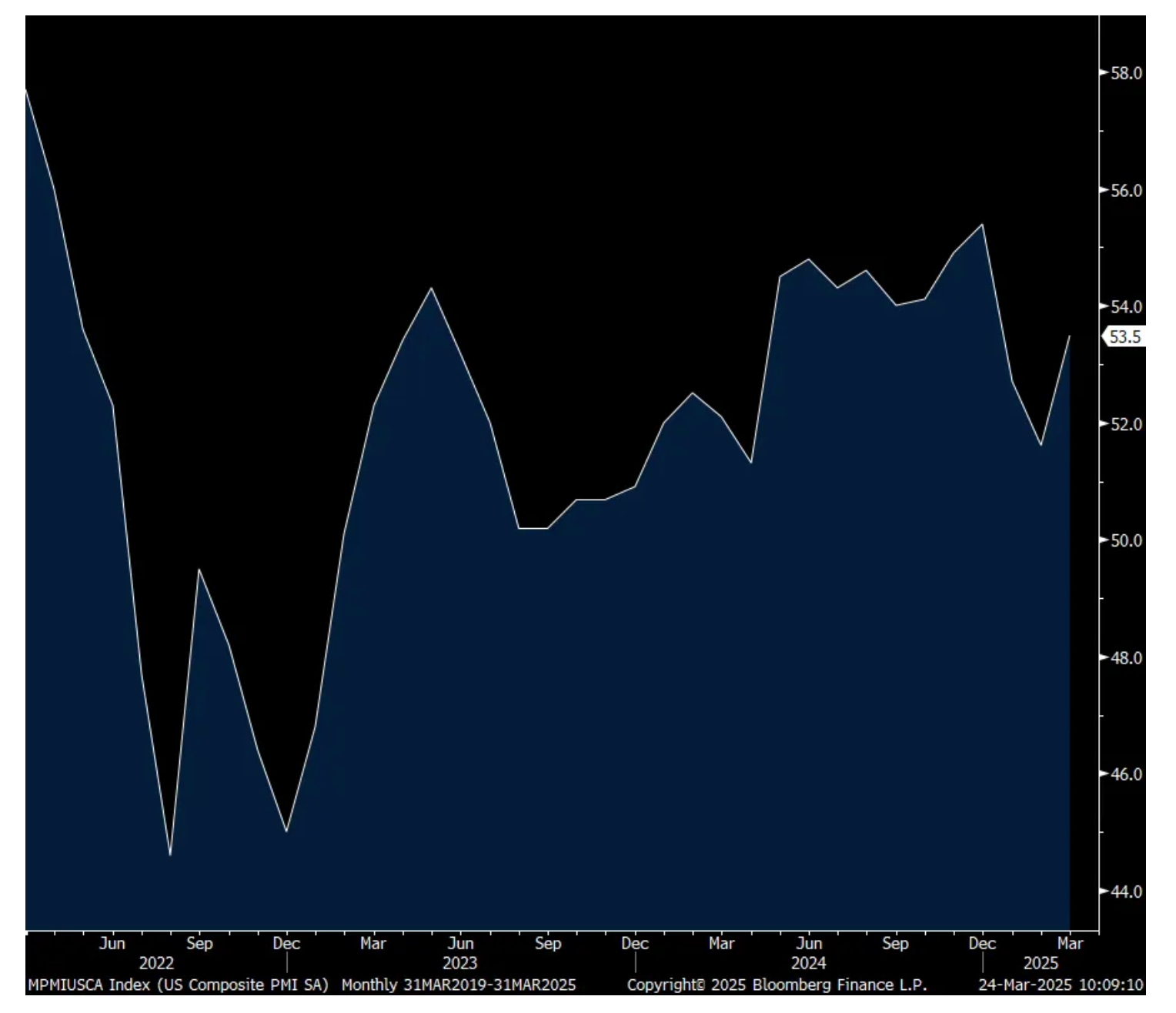

US PMI rundown, the front windshield is foggy

The March US manufacturing and services composite PMI rose to 53.5 from 51.6. It was all led though by the services sector which rose to 54.3 from 51 while manufacturing fell back below 50 at 49.8 from 52.7.

The big thing to understand is the S&P Global US services component DOES NOT include retail trade (and wholesale too) for some reason and where we know the situation has been very mixed. The ISM services index DOES include it.

With manufacturing, growth “fell back into decline after the front running of tariffs had temporarily boosted factory output in the first two months of the year.”

On services, “some of the March upturn in services was reportedly due to business picking up after adverse weather conditions had dampened activity across many states in January and February, which could prove a temporary bounce.”

Specifically on the labor market, “The upturn was led by renewed hiring in the service sector. However, even here the rate of job creation was marginal, and much weaker than at the turn of the year. Some companies reported job losses due to sluggish demand plus a wariness to hire due to the uncertain outlook.”

“Manufacturers in particular reported concerns over payroll numbers and rising costs, cutting headcounts for the first time since last October.”

Overall with expectations from here, “Business confidence in the outlook has also darkened, souring further from the buoyant mood seen at the start of the year to one of the gloomiest readings seen over the past three years, largely caused by growing worries over negative impacts from recent policy initiatives from the new administration. Most widely cited were concerns about the impact of Federal spending cuts and tariffs.”

As for the inflationary impact of tariffs, the PMI saw “a further sharp rise in costs as suppliers pass tariff-related price hikes on to US companies. Firms’ costs are now rising at the steepest rate for nearly two years, with factories increasingly passing these higher costs onto customers.”

With services though, “inflation remains relatively subdued, but this reflects the need to keep prices low amid weak demand, which will harm profits.”

Bottom line, with the exclusion of retail trade, I feel like the services PMI from S&P Global is not complete. On the manufacturing side, the survey as read was distorted by the positioning around tariffs. We know manufacturing has been under pressure for more than 2 years now. As seen with the outlook commentary, we should not be surprised right now that business visibility is very cloudy.

Treasury yields are higher with the 10 yr at 4.32% vs 4.30% right before the data release as the market focused on the headline PMI beat. The 2 yr yield is back to 4% vs a 3.95% close on Friday. Part of the weakness too is certainly optimism that the reciprocal tariffs will be more focused rather than scattershot.

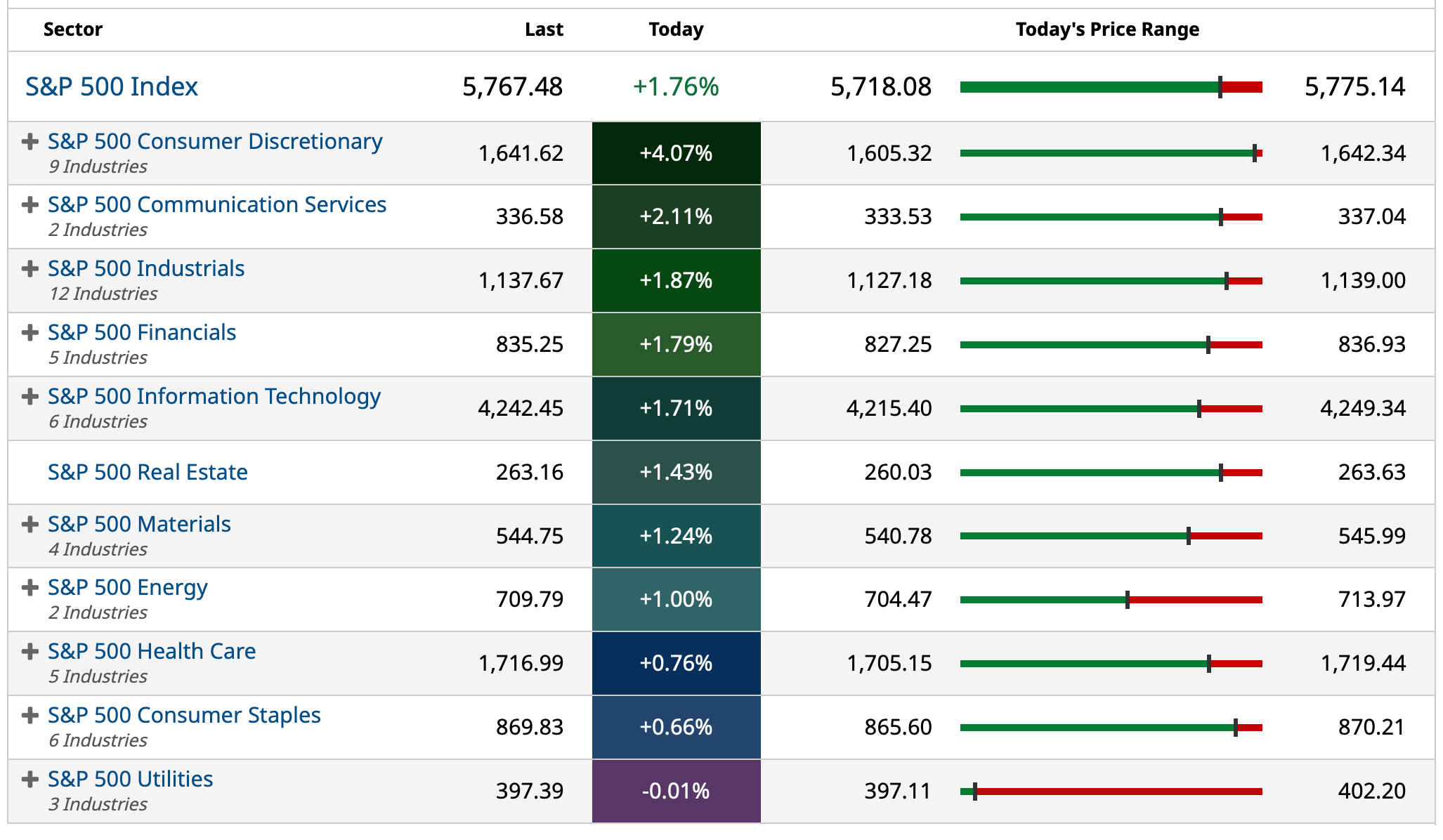

US Mfr’g and Services PMI

BY Doug Kass · Mar 24, 2025, 12:40 PM EDT

BY Doug Kass · Mar 24, 2025, 12:02 PM EDT

I lost all of my JOE and most of my FRPT on Friday's option expiration (I was short calls).

I plan to buy back St. Joe on any weakness and to add back to Freshpet on the same!

BY Doug Kass · Mar 24, 2025, 11:50 AM EDT

I just reshorted the indices after the climb from Friday morning's lows:

* SPY $573.68

* QQQ $490.01

BY Doug Kass · Mar 24, 2025, 11:42 AM EDT

- NYSE volume is 26% below its one-month average;

- Nasdaq volume is 9% below its one-month average;

- VIX index: down 4.36% to 18.44

BY Doug Kass · Mar 24, 2025, 11:05 AM EDT

BY Doug Kass · Mar 24, 2025, 9:30 AM EDT

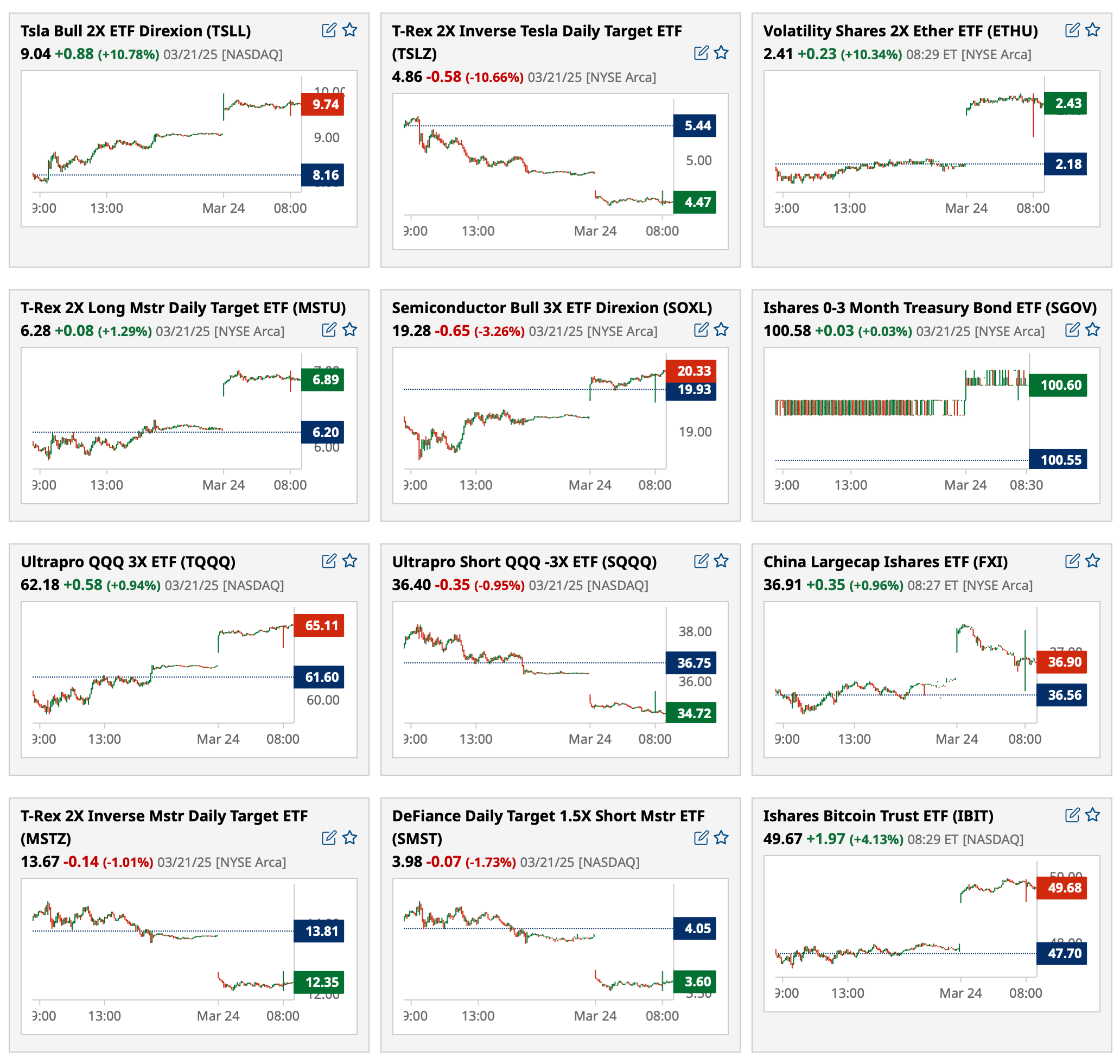

Most Active Premarket exchange-traded funds as of 8:34 a.m. ET:

BY Doug Kass · Mar 24, 2025, 9:21 AM EDT

-AZEK +23% (James Hardie to acquire US outdoor living manufacturer AZEK at $56.88/shr for a total $8.75B in cash and shares)

-GRRR +12% (confirms intention to acquire shares by Company and insiders)

-PMNT +8.8% (wholesale bookings up 30% for new Autumn/Winter 2025 Luxury Ski & Outerwear Collection)

-LUNR +6.5% (earnings, guidance)

-CTRI +6.1% (announces ~$500M in multi-year customer awards)

-UCAR +6.0% (announces Joint Venture with SUSCO, targeting Thailand's EV infrastructure boom)

-OKLO +5.9% (begins Pre-Application Readiness Assessment with US Nuclear Regulatory Commission (NRC) for Aurora Powerhouse license at Idaho National Laboratory)

-BMEA +4.9% (Icovamenib treatment in patients with Severe Insulin-Deficient Diabetes led to a significant improvement in Pancreatic Beta-cell function with a 53% mean increase in C-peptide levels 3 months after last dose)

-HOFT +4.6% (to exit Georgia Distribution Center; preliminarily expects to record net charges in FY25 $1.6-2.0M and FY26 $3.0-4.0M related to the Savannah exit)

-PINS +4.3% (Guggenheim Securities Raised PINS to Buy from Neutral, price target: $40)

-TSLA +4.1% (to release Full Self Driving (FSD) feature in China after approval process is completed)

-VSAT +4.1% (Deutsche Bank Raised VSAT to Buy from Hold, price target: $15)

-DNB +3.7% (enters into a Definitive Agreement to be acquired by Clearlake Capital Group at equity valuation $4.1B)

-W +3.2% (momentum)

-BRBR +2.6% (Morgan Stanley Initiates BRBR with Overweight, price target: $84)

-BA +2.0% (Acting FAA Administrator: believe Boeing is on right track)

-NVDA +2.0% (Malaysia Trade Min Aziz: Malaysia to crack down on Nvidia chip flows under pressure from the US)

-ME -43% (initiates Voluntary Chapter 11 process to maximize stakeholder value through court-supervised sale process; CEO Anne Wojcicki resigns, effective immediately)

-JHX -11% (James Hardie to acquire US outdoor living manufacturer AZEK at $56.88/shr for a total $8.75B in cash and shares)

-SMST -9.6% (files to sell 27M shares at expected offering price $28-36/shr)

-MDAI -6.5% (raises up to $15M of debt financing)

-GMAB -3.6% (to vigorously defend alleged claims of trade secret misappropriation by AbbVie Inc.)

-NVO -2.3% (United Labs International enters exclusive license agreement with Novo Nordisk for UBT251; expands Wegovy $499-per-month offering to additional cash-paying patients via the Wegovy savings offer)

-LNSR -2.2% (to be acquired by Alcon for $14/shr in cash)

BY Doug Kass · Mar 24, 2025, 9:13 AM EDT

Premarket percentage movers as of 8:51 a.m.:

BY Doug Kass · Mar 24, 2025, 9:00 AM EDT

From Peter Boockvar:

In light of the press reports on what the April 2nd tariffs might look like (targeted maybe but only in terms of the number of countries the tariffs will be applied to rather than targeted in terms of overall dollar size), whatever it looks like and regardless if one agrees with the application or not, let's hope that it's then done so businesses, households and investors can at least have some visibility from all of this and can plan around them.

Not much of a US dollar response as the DXY is down .15% and is still near giving back all of its post election gains. Specifically, the Canadian dollar and the Mexico peso are up a touch while the Chinese offshore yuan is flat in response today. Since the election, the Canadian dollar and Chinese yuan are really the only two currencies that are notably down vs the US dollar. The rest are mostly flat, including the Mexican peso.

I've argued that the real moves in the US dollar index have been more influenced by the foreign flows in and out of the Mag 7 stocks as they became a global reserve asset. In case you didn't see, on Friday in the BoA Flow Show, Michael Hartnett said while US stocks saw the biggest inflow of 2025 ($34.1b); "but note past 2 weeks have seen biggest foreign selling of US stocks since Mar '23" and that with Europe stocks: "biggest inflow since May '17, and 4th largest ever ($4.3b)." Investors have discovered other choices. We continue to have specific international equity exposure in Europe, Japan, Hong Kong, Singapore, Vietnam and most recently Brazil. Emerging market local currency bonds we own as well. And there are plenty of cheap, value stocks in the US that have been kicked to the curb that we own and like, including commodity stocks in oil/gas, uranium, precious metals, ag and industrial metals.

Bottom line, that playbook that worked so well over the past few years by mostly owning 7 US stocks and some other ones here and there (like utility and electrification stocks that were a play on AI), throw it in the garbage as a new one is being written. There should be nothing profound about that by the way as changing cycles and leadership in markets has been going on since the history of markets.

Ahead of the US manufacturing and services March PMI at 9:45am est, some foreign figures came out. The composite index for Japan fell to 48.5 from 52 with continued softness in manufacturing at 48.3 vs 49 and a big drop in services to 49.5 from 53.7. Inflation pressures were apparent too as "cost pressures remained elevated in March, with overall input costs rising sharply across both monitored sectors, leading to a solid rise in selling prices. Strong inflation, coupled with concerns over labor shortages, an ageing population, subdued client spending and increased uncertainty over the international trade environment dampened optimism around the outlook. Notably, overall confidence regarding future business activity dipped to the lowest since August 2020 at the end of the first quarter."

Australia's PMI index in contrast lifted to 51.3 from 50.6 with both components higher m/o/m and with both above 50.

India's PMI held strong at 58.6 vs 58.8 with manufacturing at 57.6 and services at 57.7.

The European PMI was mixed as manufacturing rose to 48.7 from 47.6, though still below 50 while services slipped to 50.4 from 50.6. S&P Global had some interesting insight, "Just in time with the beginning of spring we may see the first green shoots in manufacturing. While we should not be carried away by a single data point, it is noteworthy that manufacturers expanded their output for the first time since March 2023. It's also encouraging, that the index output has risen for three months straight. This is complemented by a much softer fall in new orders and employment. One could pour some cold water on this development arguing that it's the temporary tariff-related import boom from the US which has driven the improvement in manufacturing. However, given the will of Europe, to invest heavily in defense and infrastructure - in Germany a corresponding historical fiscal package has been approved only last week - hope for a more sustained recovery seems well founded."

With inflation on the services side, "Both input costs and selling prices are rising at a slower pace compared to recent months. Lower input cost inflation points to less pressure from wages which are a key ingredient of input costs in the labor intensive services sector." In manufacturing, "price increases for both selling and purchasing remain moderate, helped along by declining energy costs."

The UK PMI rose 1.5 pts m/o/m to 52 with all the help coming from services which rose to 53.2 from 51. Manufacturing softened further to just 44.6 from 46.9. On that manufacturing weakness, the sector "experienced severe headwinds to demand from rising global economic uncertainty and potential US tariffs. Weak international demand resulted in the fastest decline in manufacturing export sales since August 2023. Moreover, manufacturers reported the steepest downturn in production volumes for nearly one and a half years."

With the services rise, "Some service providers commented on a tentative turnaround in demand conditions, especially for consumer services." They specifically cited financial services as one of them.

On inflation, "Services providers recorded a much steeper rise in input prices than manufacturers, largely reflecting intense wage pressures and efforts by suppliers to pass on higher payroll costs. Manufacturers also noted that vendors had sought to pass on greater employment costs and rising raw material prices (especially metals)."

The markets response to the European data has bonds down slightly, currencies rising (in part due to the April 2nd tariff stories) and stocks up.

The one earnings conference call to go through is from Carnival where we know cruising is still doing well:

"We achieved a robust 7.3% yield increase, smashing our yield guidance on top of last year's 17% yield improvement. Both ticket and onboard equally outperformed on very strong close-end demand, which speaks to the strength of our consumer."

"For the full year, and despite heightened macroeconomic and geopolitical volatility since providing our December guidance, we are taking up yields by .5 pt to 4.7% based on our strong first quarter results while affirming yield expectations for the remainder of the year."

"We're generating demand well in excess of our very limited inventory remaining, which has been driving strong pricing for the remainder of the year, while also building demand for future years. In fact, we're at historical high prices across all core programs for 2025 and all quarters of the year, while booking volumes for 2026 sailings and beyond taken during the first quarter also reached an all time high. We were very well positioned going into wave this year and we exited with over 80% of the year on the books at higher prices and with a booking curve that is still the farthest out on record."

I will add this as we debate what the Fed will do with short term interest rates. Savers, particularly baby boomers, have benefited hugely from higher interest income with higher rates. That has gotten chipped away somewhat by 100 bps since last September and if the Fed starts cutting again, while good for some borrowers, will negatively impact interest income.

Take $1mm of savings as an example, when the fed funds rate was at its peak prior to the September 50 bps rate cut, it was generating about $50k of pre-tax income. That is now about $40k. Further cuts could be the price of a cruise and a canceled vacation.

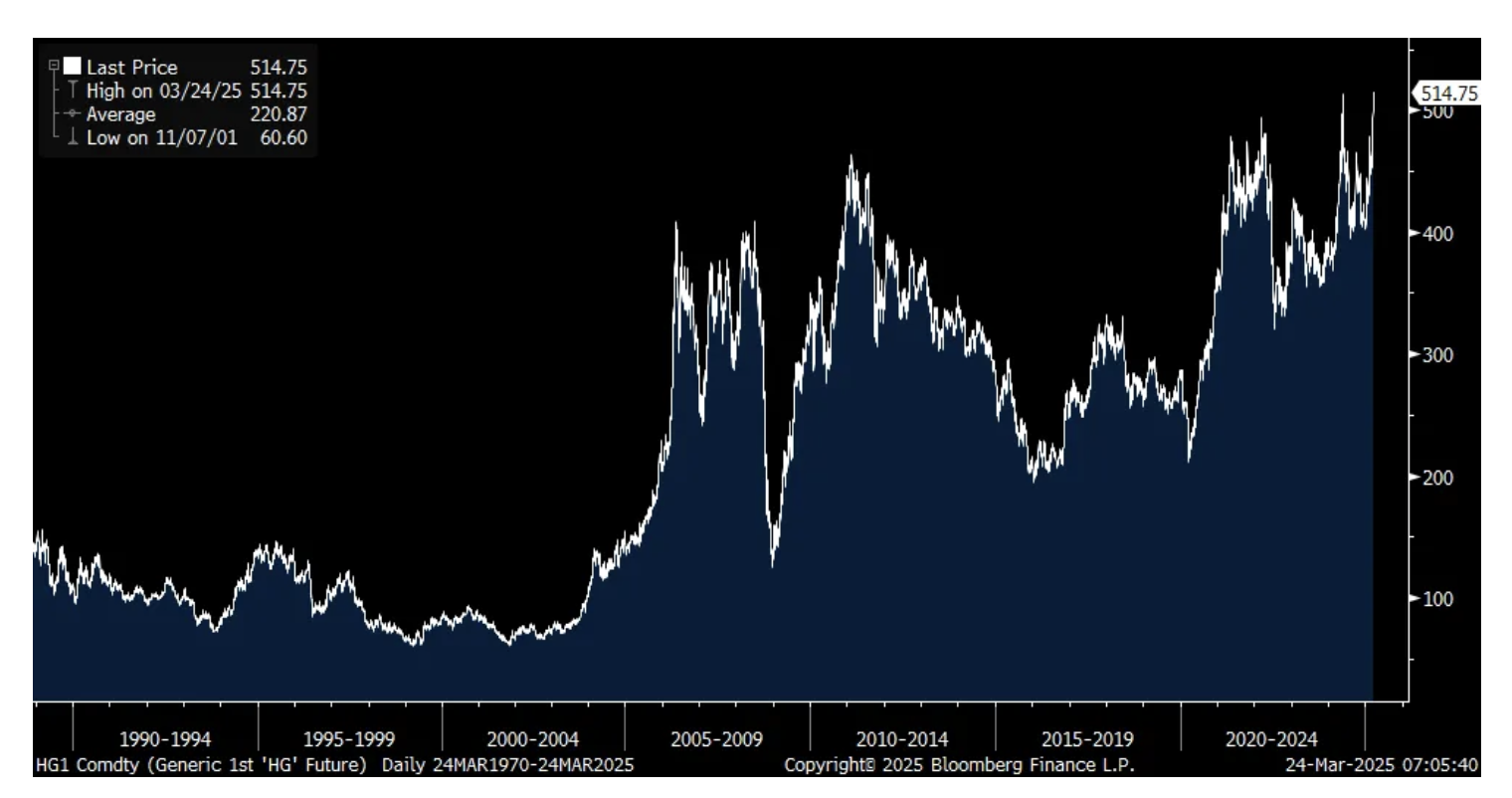

Lastly, here is a fresh chart on copper for the continuous contract and is at a fresh record high today.

BY Doug Kass · Mar 24, 2025, 8:37 AM EDT

BY Doug Kass · Mar 24, 2025, 8:15 AM EDT

BY Doug Kass · Mar 24, 2025, 8:00 AM EDT

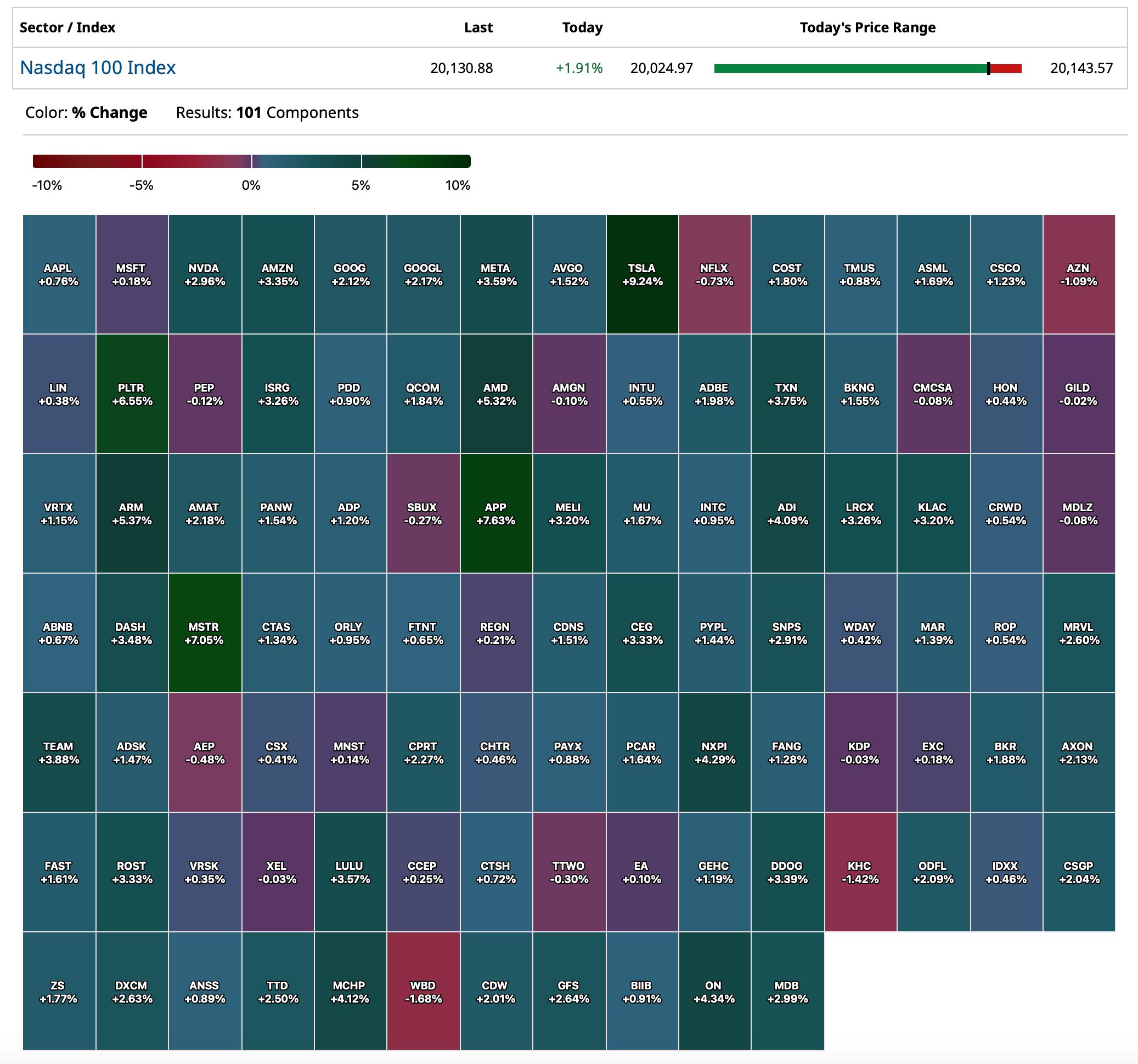

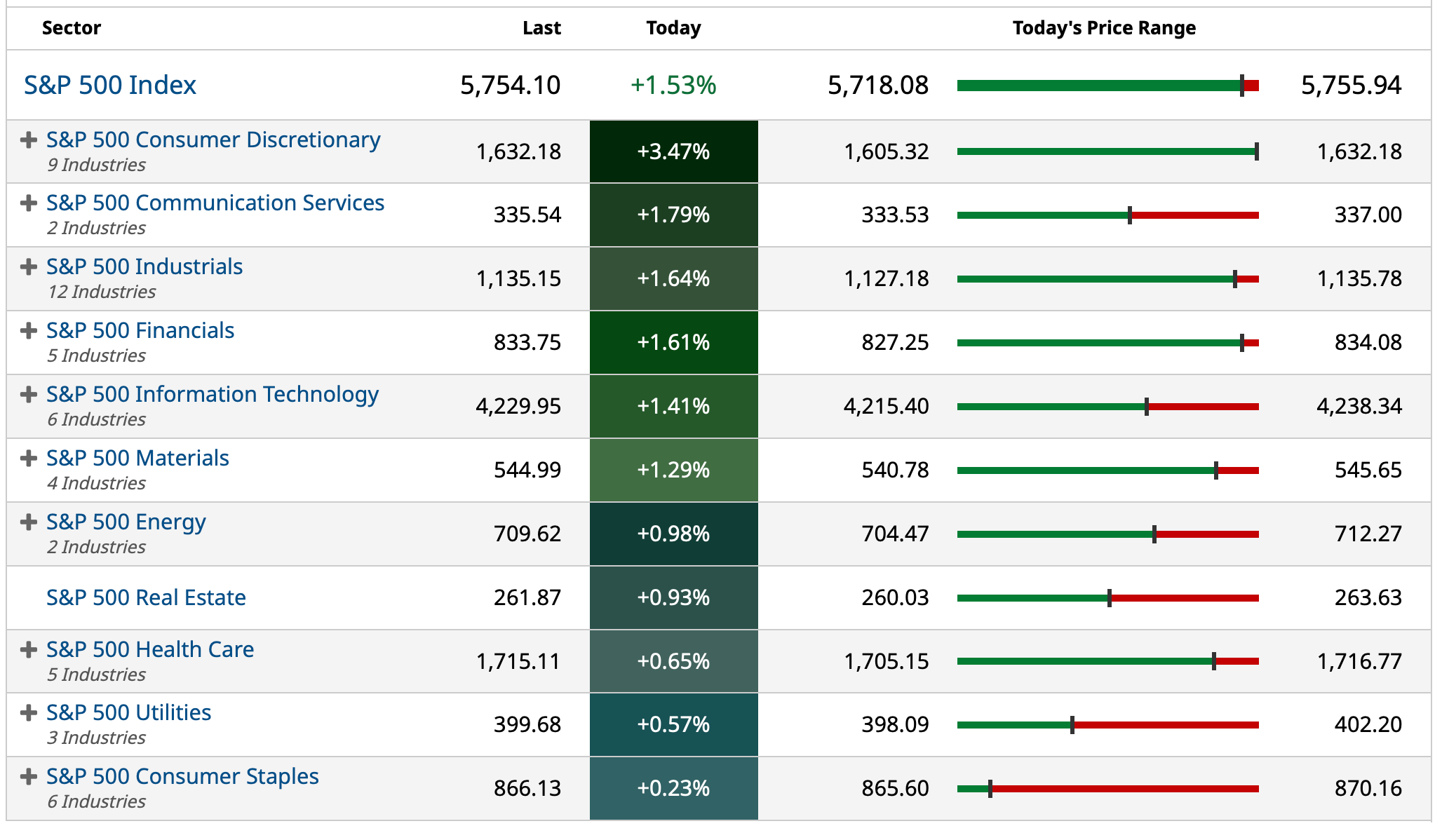

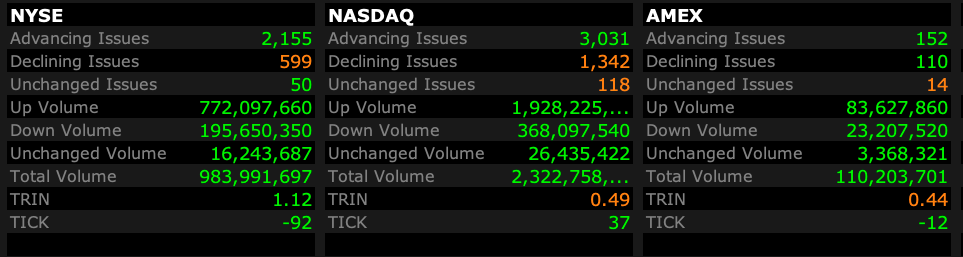

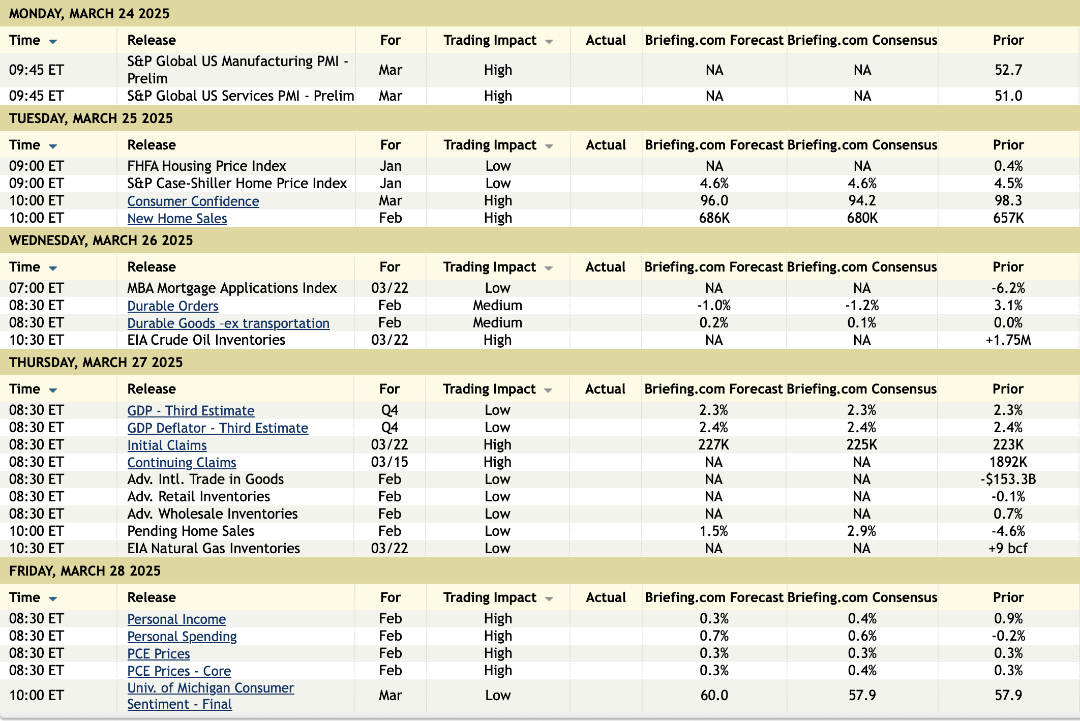

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Mar 24, 2025, 7:50 AM EDT

From JPMorgan:

US: Futs are higher. Over the weekend, the most noticeable headline from the White House was a BBG article (here) suggesting that Trump’s April 2 tariff package may be more “targeted” than feared. All of Mag 7 are higher this morning led by TSLA (+3.8%), META (+2.1%) and AMZN (+1.5%). Bond yields are 2-4bp higher. Commodities are mostly lower this morning, with Aluminum and Copper being down 1.4% and 0.8%, respectively. This week, the key macro focus will be flash PMIs (today) and PCE (Friday), with investors anticipating major tariff announcement next Wednesday (April 2).

and...

EQUITY AND MACRO NARRATIVE: Last week, SPX ended the four consecutive weekly losses and finished the week with a moderate 51bp gain. Energy, Financials and Health Care are among the top performing sectors. Macro data this week were mostly better-than-feared: core Retail Sales beat expectations, but headline level failed to recover from January decline; the rest of macro data was largely mixed. Equities staged a risk-on rally on Wednesday, partially thanks some positive aspects of the FOMC (QT slowing) and positioning. Earnings reports this week were mostly underwhelming, particularly for FDX, MU, NKE. Headlines from Washington were largely muted throughout the week. Over the weekend, the biggest headline came from a BBG article (here) suggesting that Trump’s April 2 tariff package may be more “targeted” than feared. The article notes that “… list of target countries may not be universal, and that other existing tariffs, like on steel, may not necessarily be cumulative, which would substantially lower the tariff hit to those sectors.” This week, the key macro focus will be flash PMIs (Monday) and PCE (Friday), with investors anticipating major tariff announcement on April 2 (next Wednesday).

BY Doug Kass · Mar 24, 2025, 7:40 AM EDT

BY Doug Kass · Mar 24, 2025, 7:30 AM EDT

Citigroup aggressively cuts price targets for many financials — AXP, MS, GS, BAC, etc.

BY Doug Kass · Mar 24, 2025, 7:20 AM EDT

BY Doug Kass · Mar 24, 2025, 7:10 AM EDT

Doomberg on "Full Tank."

BY Doug Kass · Mar 24, 2025, 7:00 AM EDT

As you will read below, most technicians like the action of the last few days. Why? Because they failed to break down! And that's how they roll:

Bonus — Here are some great links:

BY Doug Kass · Mar 24, 2025, 6:45 AM EDT

More on the fading consumer:

How can someone that needs to do buy now pay later for a burrito be a good credit risk? I hesitate to think about what they collateralize this with?

If this is what it has come to in order to keep the U.S. consumer afloat, oh boy:

BY Doug Kass · Mar 24, 2025, 6:35 AM EDT

I have a board meeting from 10 a.m. to noon today.

BY Doug Kass · Mar 24, 2025, 6:25 AM EDT

BY Doug Kass · Mar 24, 2025, 6:15 AM EDT

BY Doug Kass · Mar 24, 2025, 6:05 AM EDT

From Bramo:

BY Doug Kass · Mar 24, 2025, 5:55 AM EDT

The S&P Short Range Oscillator is at -1.58% vs -0.8%, so it's modestly oversold.

BY Doug Kass · Mar 24, 2025, 5:45 AM EDT