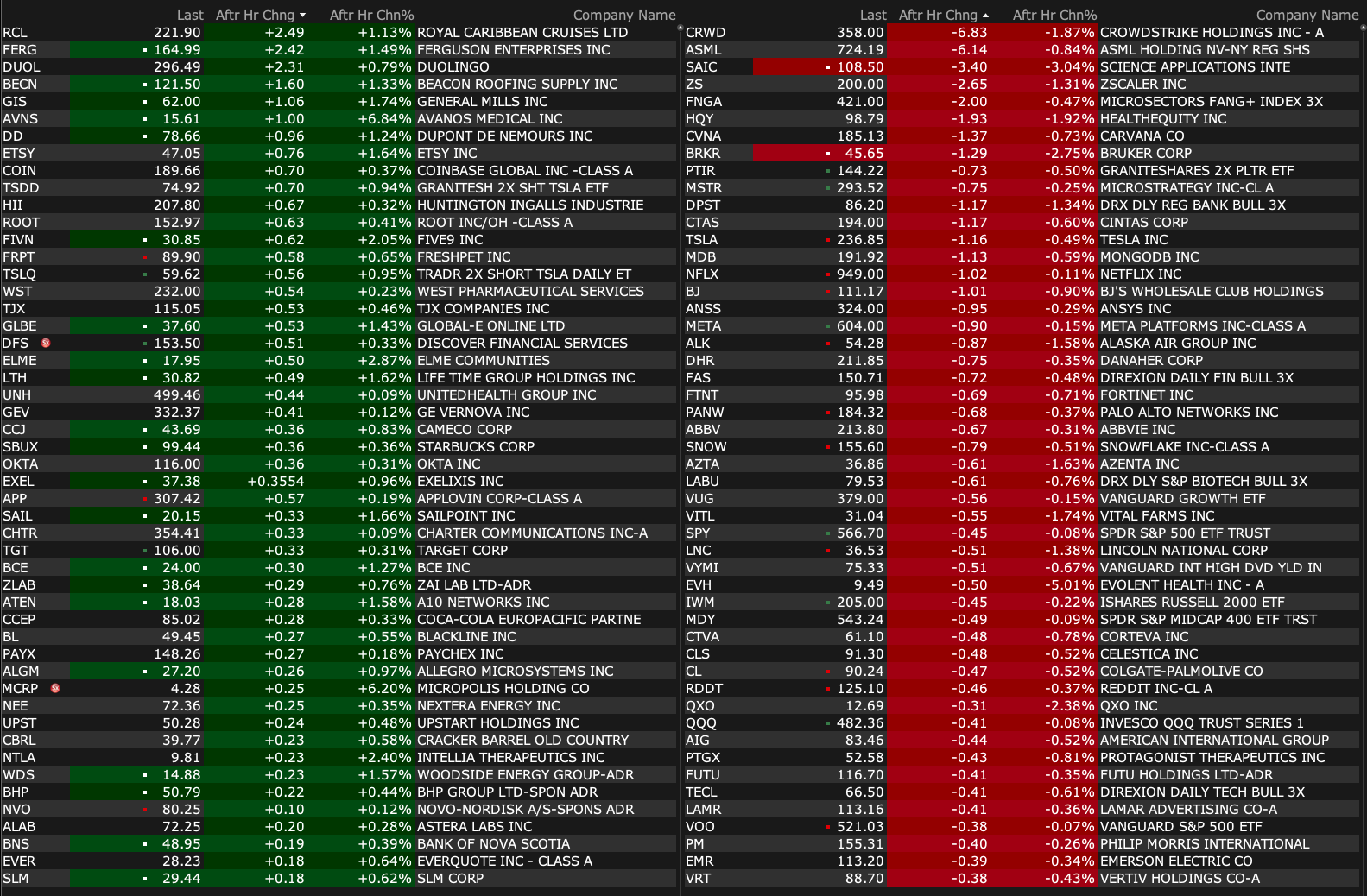

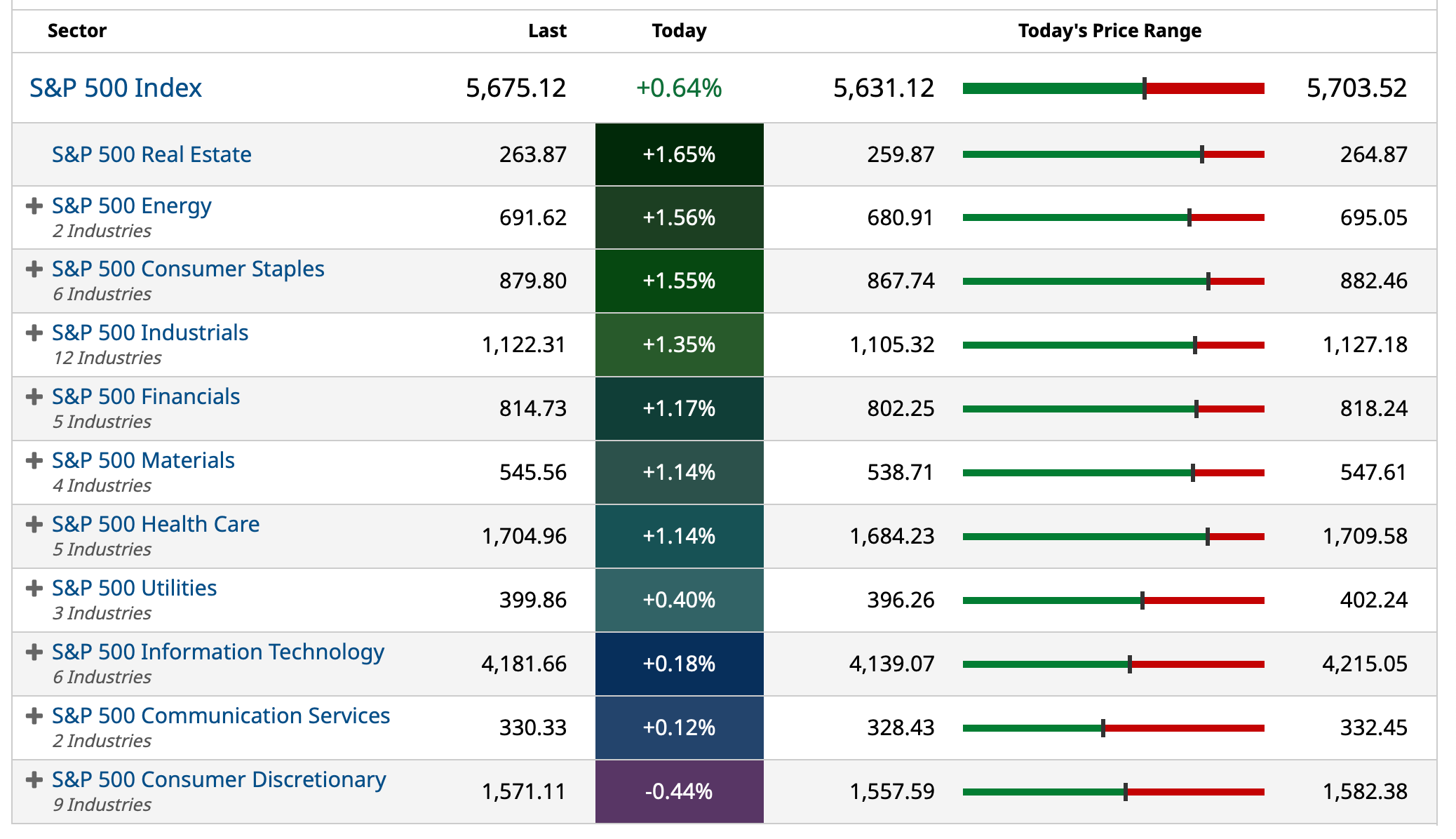

Monday's After-Hours Movers

At 4:20 p.m.:

BY Doug Kass · Mar 17, 2025, 5:00 PM EDT

At 4:20 p.m.:

BY Doug Kass · Mar 17, 2025, 5:00 PM EDT

BY Doug Kass · Mar 17, 2025, 4:48 PM EDT

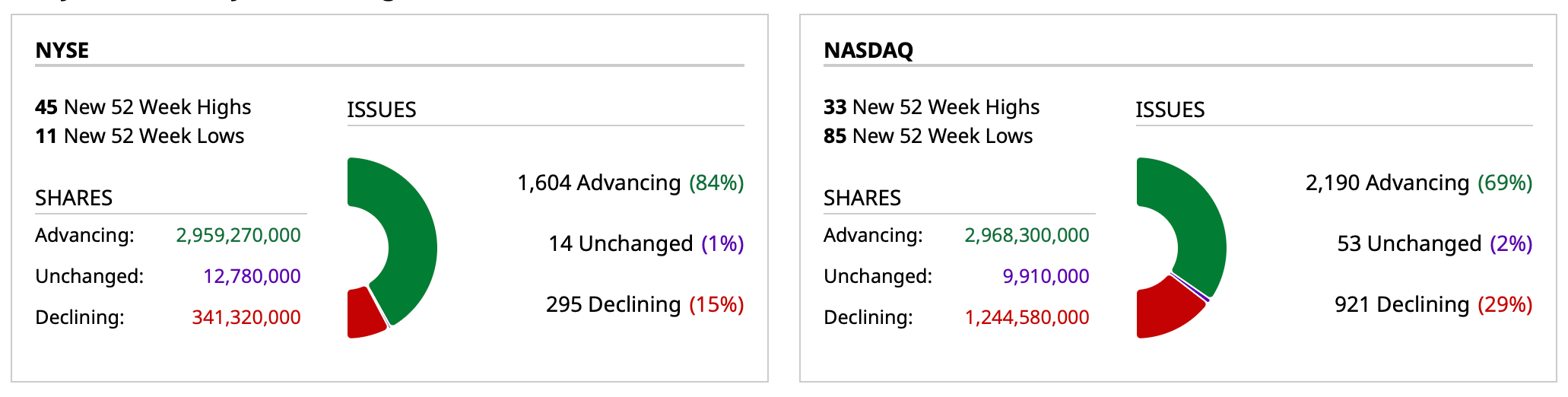

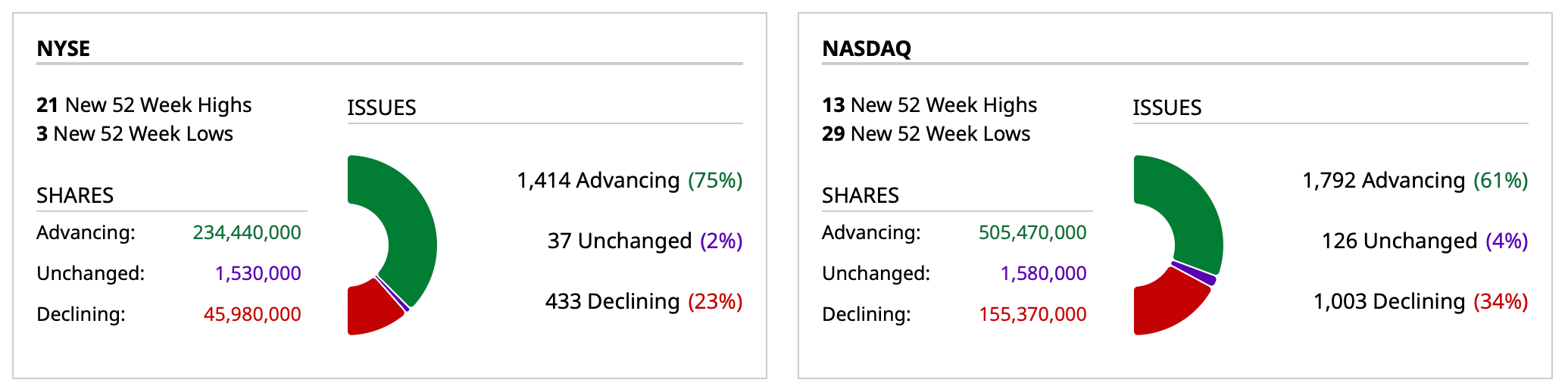

- NYSE volume 11% below its one-month average

- NASDAQ volume 22% below its one-month average

- VIX index: down 5.79% to 20.51

BY Doug Kass · Mar 17, 2025, 4:37 PM EDT

* I have added to my Apple AAPL short today at $214.60.

Interesting. Monopoly Round-Up: The Week Everyone Realized Apple Is Decaying

BY Doug Kass · Mar 17, 2025, 2:44 PM EDT

I have a 4 p.m. meeting outside of the office.

I will be leaving at around 3:30 p.m. to travel to the meeting.

BY Doug Kass · Mar 17, 2025, 2:20 PM EDT

We own a broad swath — from Thursday's buys.

BY Doug Kass · Mar 17, 2025, 2:02 PM EDT

BY Doug Kass · Mar 17, 2025, 1:50 PM EDT

BY Doug Kass · Mar 17, 2025, 1:38 PM EDT

BY Doug Kass · Mar 17, 2025, 1:30 PM EDT

I have been busy:

BY Doug Kass · Mar 17, 2025, 1:05 PM EDT

BY Doug Kass · Mar 17, 2025, 12:56 PM EDT

BY Doug Kass · Mar 17, 2025, 12:16 PM EDT

BY Doug Kass · Mar 17, 2025, 12:02 PM EDT

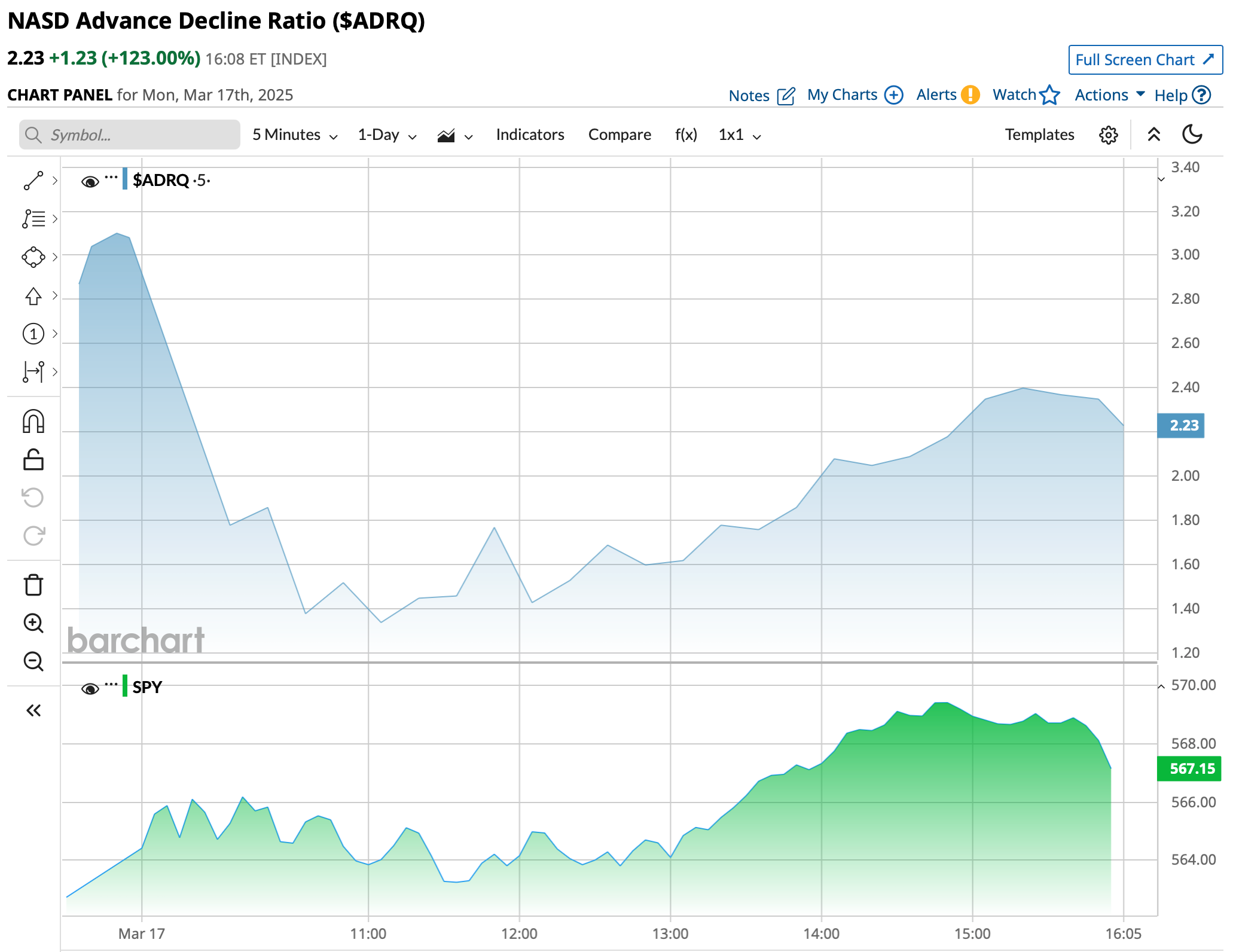

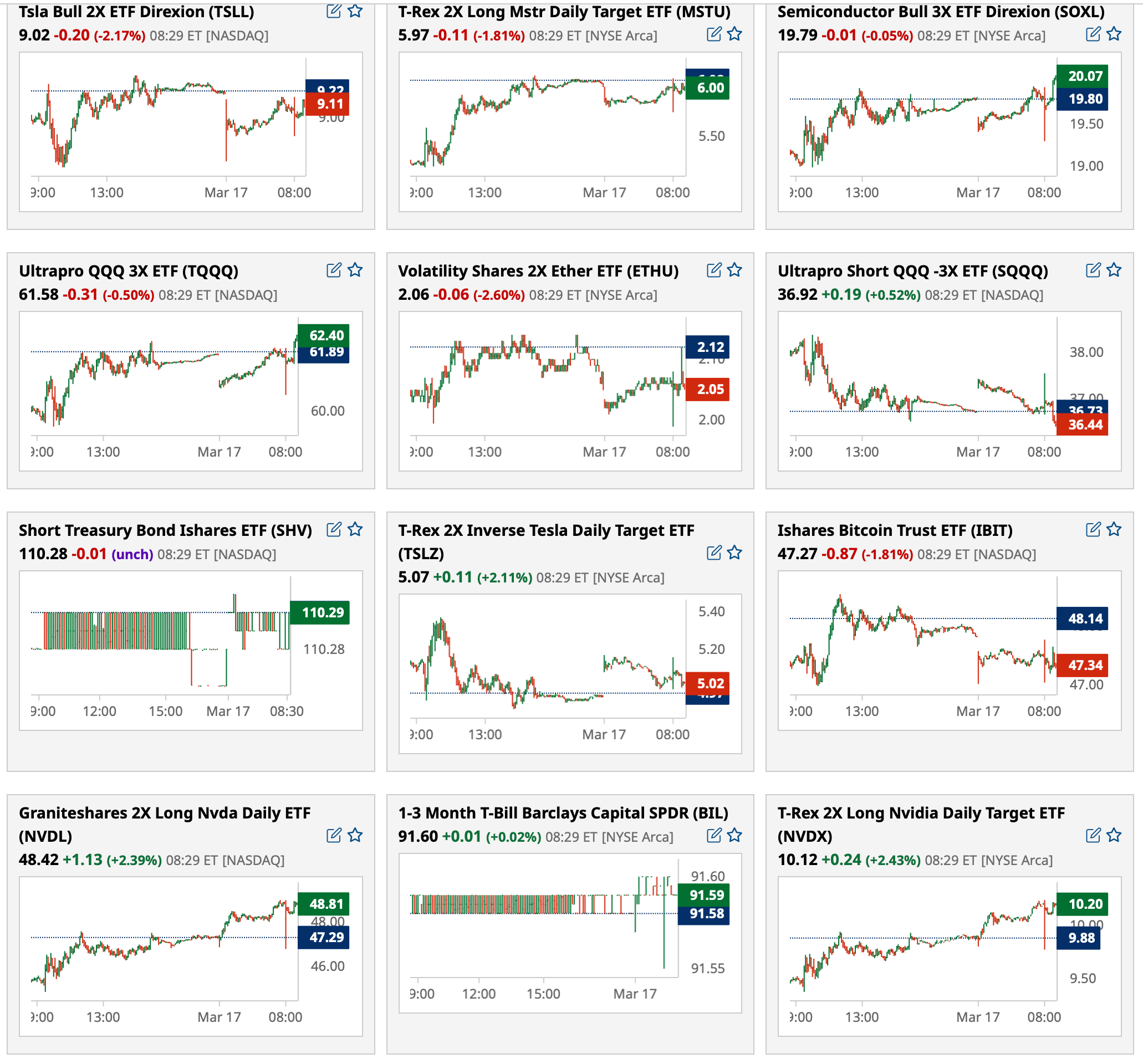

Intraday graphs from 11 a.m. ET

BY Doug Kass · Mar 17, 2025, 11:28 AM EDT

BY Doug Kass · Mar 17, 2025, 11:17 AM EDT

NYSE volume 10% below its one-month average;

Nasdaq volume is 26% below its one-month average;

VIX index is down 3.95% to 20.91.

BY Doug Kass · Mar 17, 2025, 11:05 AM EDT

BX, a buy last week, is the "world's fair."

BY Doug Kass · Mar 17, 2025, 10:18 AM EDT

BY Doug Kass · Mar 17, 2025, 10:15 AM EDT

From Peter Boockvar:

Core retail sales upside but really mixed under the hood/Mfr'g recession rolls on but with even less visibility now

Core retail sales in February rose 1% m/o/m, well above the estimate of up .4%. It though follows a 1% drop in January which was revised down from an initial .8% fall. Core sales y/o/y were basically flat in February, up by .3%. Auto sales, not included in the core figure, fell by .4% m/o/m after a drop of 3.7% in January. Building materials, not captured either, saw a .2% rise but after four straight months of declines. Food services are not included too and sales at restaurants/bars dropped by 1.5% m/o/m.

The internals elsewhere were really mixed, notwithstanding the headline strength. Driving that core figure was mainly online retailing where sales rose 2.4% m/o/m, though after dropping by a like amount in January. Also, necessities outperformed with health/personal care sales higher by 1.7% m/o/m after a 1.1% fall in the month before. Also, food/beverage sales grew by .4% m/o/m.

Sales fell for electronics, clothing, sporting goods, department stores, and other miscellaneous stores. Sales of furniture were flat.

Bottom line, as stated, necessities won out, along with e-commerce, with mostly weakness elsewhere. Sounds a lot like what we've heard from a variety of retailers and consumer product companies.

Continuing on with the manufacturing recession, the March NY index fell to -20 from+5.7. New orders went to -14.9 from +11.4 while backlogs were negative too at -2.0. Employment was below zero for the 4th month in the past five and the workweek was negative for the 4th straight month. Delivery times were a bit better but prices paid and received rose even further. Prices paid at 44.9 is 15 pts above its 6 month average and those received at 22.4 is almost 10 pts above.

Also of note, the 6 month business outlook fell to 12.7 from 22.2 and vs 36.9 in the month prior. Cap Ex plans weakened too and is now at a 6 month low.

Bottom line, whether one agrees with the tariff path or not, how can any manufacturer, whether they source product overseas or not, whether they sell internationally or not, have any visibility with what is going on?

BY Doug Kass · Mar 17, 2025, 10:06 AM EDT

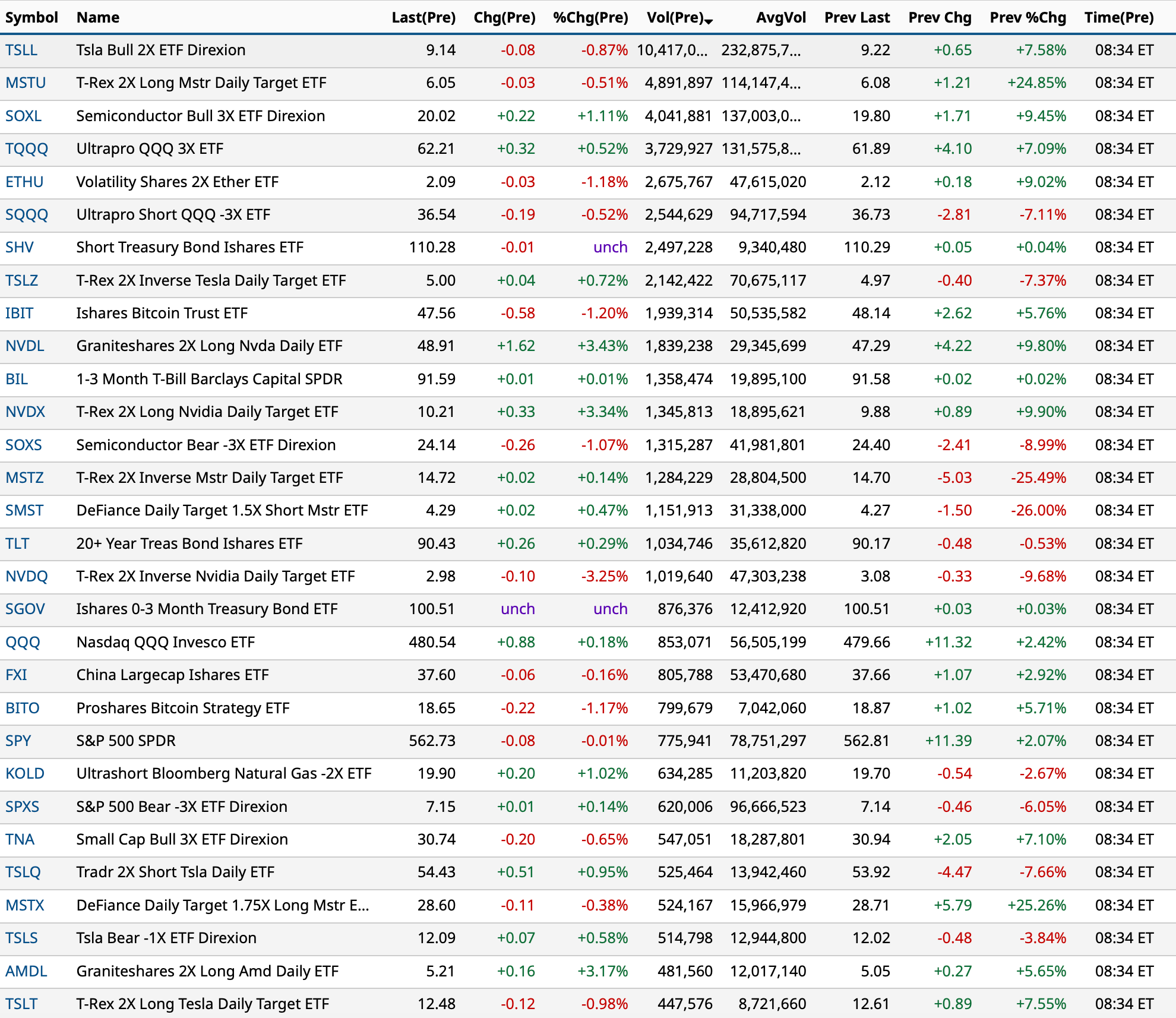

Most active premarket ETFs as of 8:34 a.m. ET:

BY Doug Kass · Mar 17, 2025, 9:21 AM EDT

Premarket percentage movers at 8:55 a.m.:

BY Doug Kass · Mar 17, 2025, 9:10 AM EDT

-GES +25% (receives Going-Private Proposal from WHP Global at $13/shr)

-SAIC +8.8% (earnings, guidance)

-SCNX +8.7% (FDA approves new dosage form of losartan Arbli for treatment of hypertension in adults and children 6+ years old)

-WLDS +8.7% (expands to Next-Gen Neural Interaction for everyday life after securing patent in the United States)

-NIU +7.7% (earnings, guidance)

-DTIL +7.1% (announces Clearance of Investigational New Drug Application by the U.S. FDA for First-in-Class PBGENE-HBV Designed to Eliminate Root Cause of Chronic Hepatitis B)

-CVM +6.7% (Head and Neck Cancer Registration Study Protocol Clears FDA Review; In Talks with Potential Partners Interested in Commercialization of Multikine)

-ANTE +4.5% (enters into Non-Binding Investment Letter of Intent with LLP STH Corp to Develop a 130MW Liquid-cooled Bitcoin Mining Farm in Kazakhstan)

-NCLH +3.8% (JPMorgan Chase and Co Raised NCLH to Overweight from Neutral, price target: $30)

-ASLE +3.7% (to repurchase ~6.428M shares from Leonard Green & Partners at $7.00/shr)

-X +3.3% (DOJ filed motion to extend CFIUS deadline from April 24th to May 12th)

-BANC +2.6% (announces $150M stock repurchase program)

-ANET +2.3% (added to JPM Analyst Focus List)

-INCY -15% (weakness following Phase 3 STOP-HS clinical trial data)

-AFRM -9.5% (rival Klarna reaches Walmart agreement)

BY Doug Kass · Mar 17, 2025, 9:02 AM EDT

From Peter Boockvar:

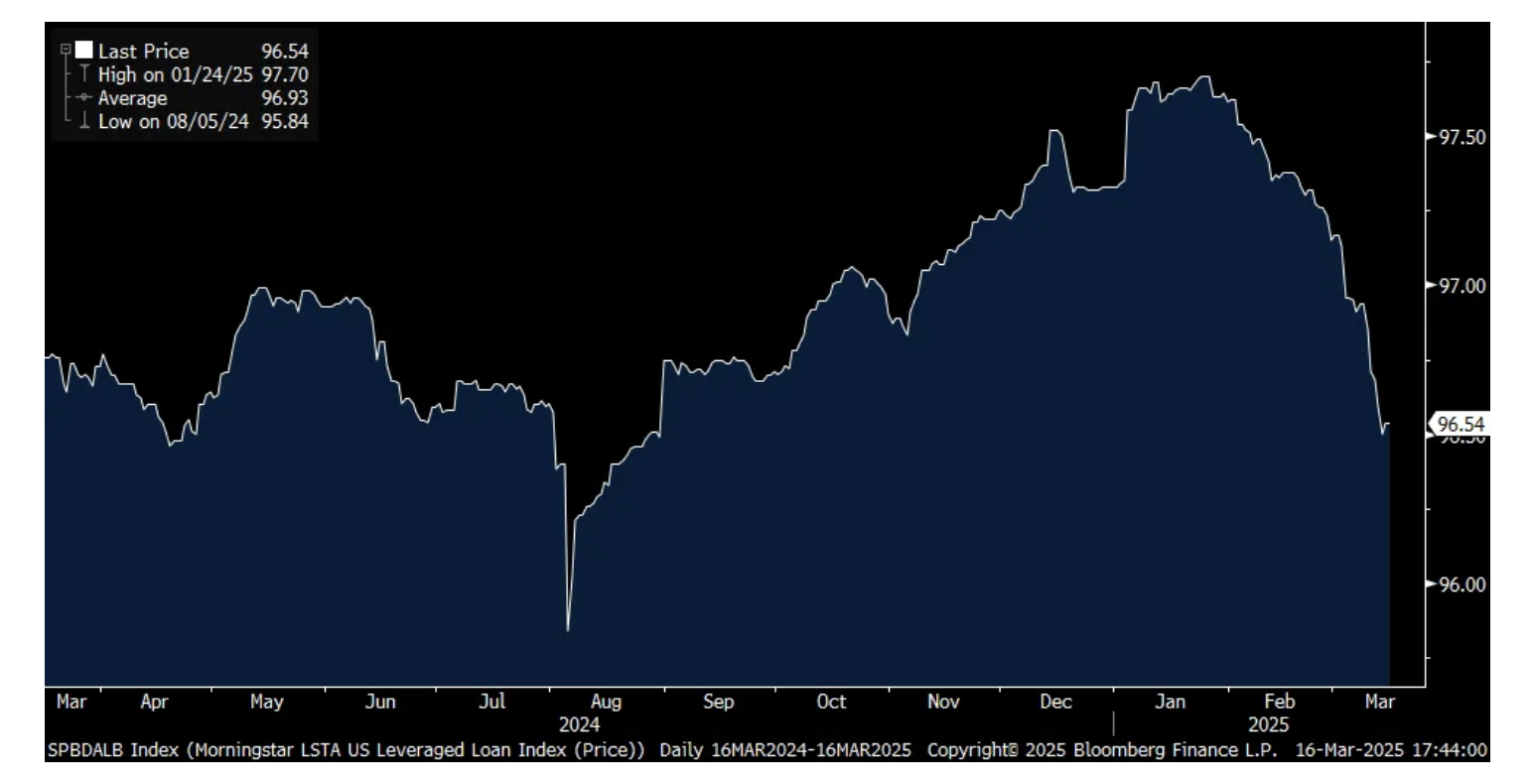

With the extraordinary amount of money piling into private credit (I get countless deal offerings emailed to me on a daily basis) I continue to have my eye on the LSTA Leveraged loan index as a marker on pricing. As private credit is essentially just a loan that used to be made by a bank (and indirectly still is if a bank is lending money to a private credit firm to underwrite loans) but instead resides in the non financial center, it's still subject to the same economic vagaries that should garner greater scrutiny when economic concerns grow. Keep in mind, for every low double digit return advertised by private credit is a borrower having to pay low double digits for that loan or something close if a bit of leverage is used to lift returns.

LSTA Leveraged Loan Index

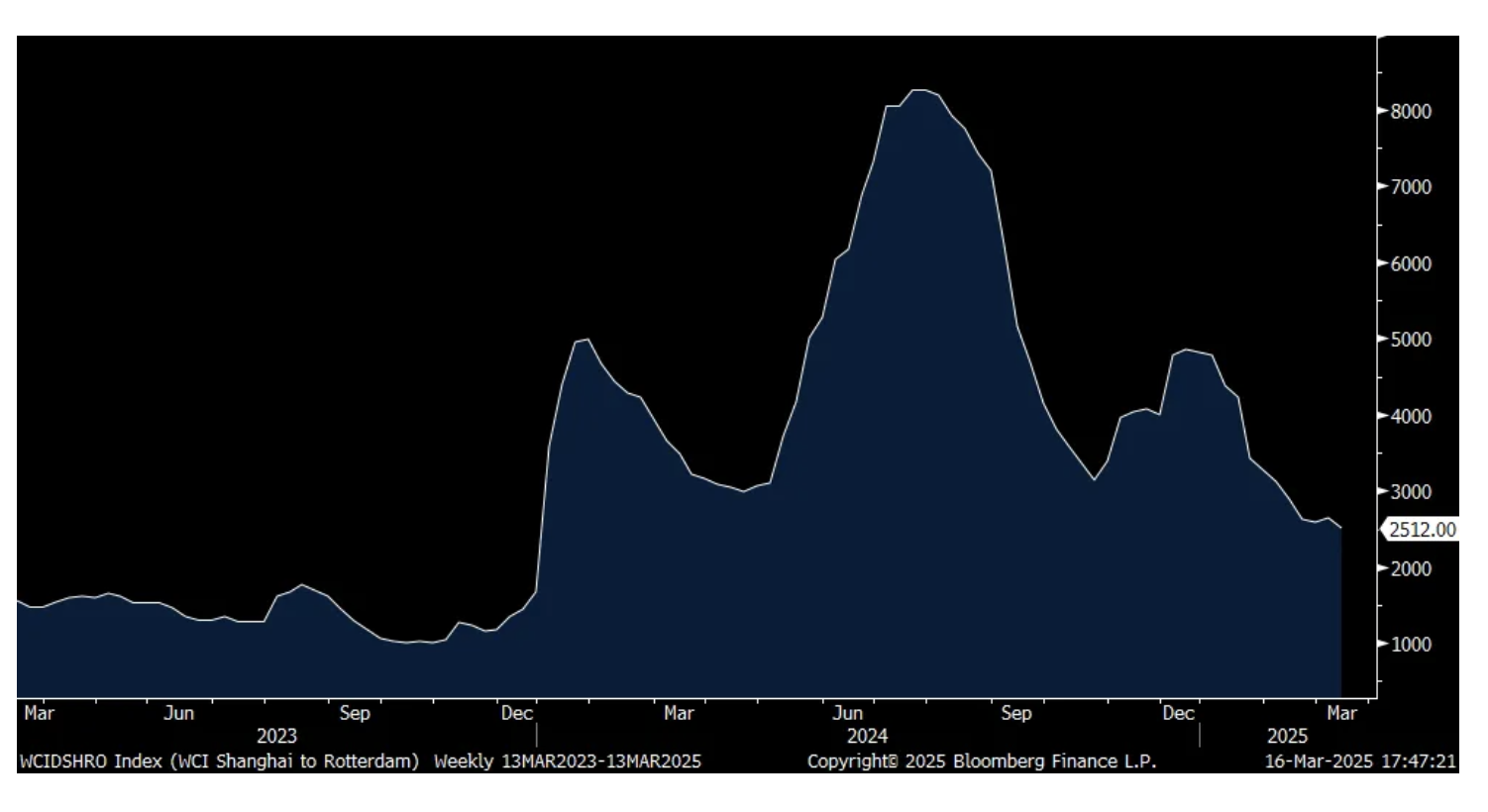

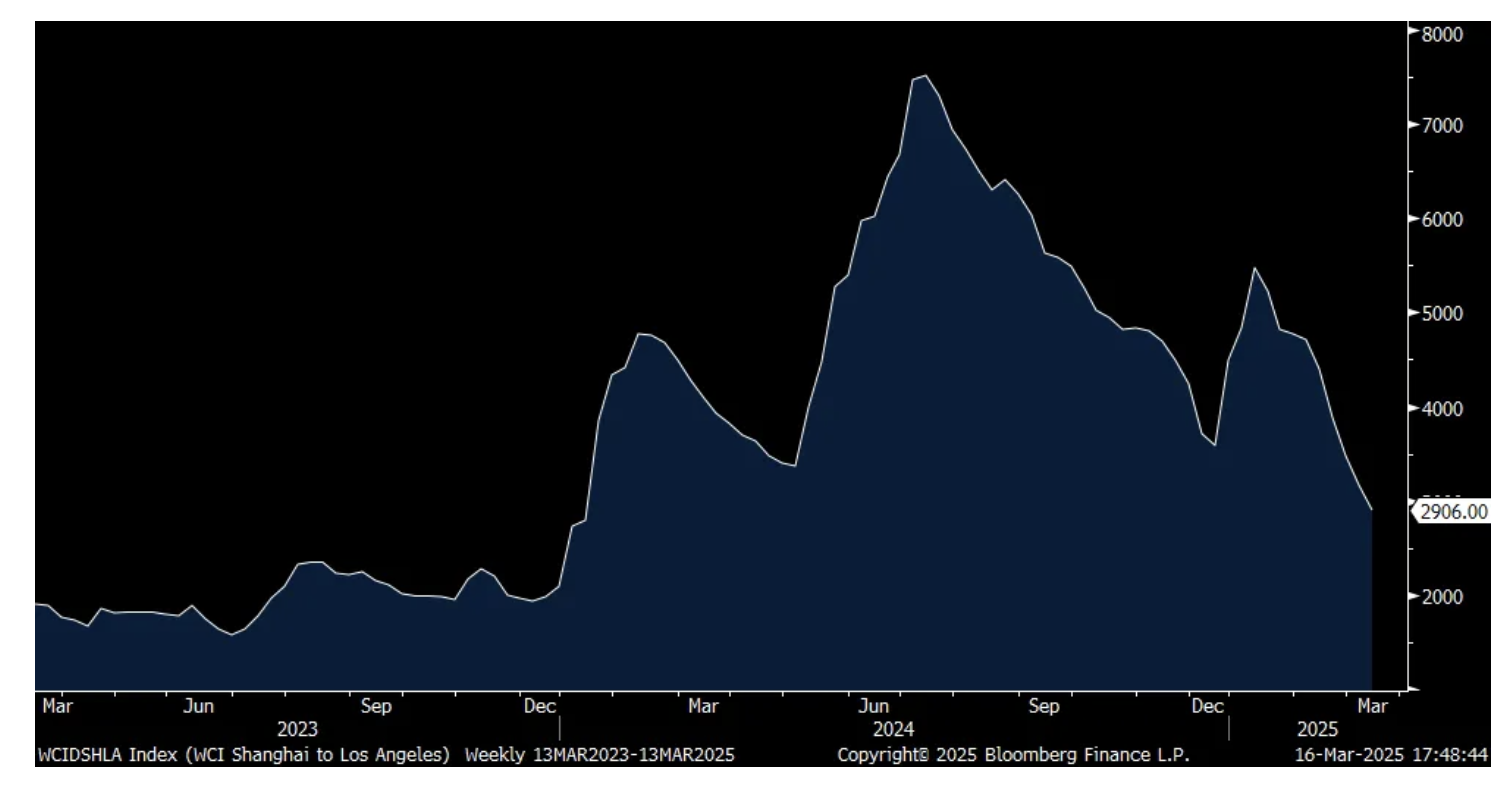

With the US bombing the Houthi's in an attempt to finally destroy their strangle hold on the Red Sea, here was an update from last week's World Container Index. The Shanghai to Rotterdam route fell in price to the lowest level since late December 2023 at $2,512 for a 40 foot container. The Shanghai to LA trip is down to $2,906, the cheapest since early January. So, for the following weeks/quarters, either we've destroyed their capabilities or this situation gets more messy.

Shanghai to Rotterdam:

Shanghai to LA

The Bank of Japan won't raise rates again this week but they have every reason to keep on hiking at some point this year, especially after Rengo, the largest labor union in Japan negotiated a pay increase for its members of 5.5% on average in the annual Shunto discussions. That's the fastest pace of gain since 1991 and follows the trajectory we've been seeing in the monthly base pay data. There are more deals Rengo will put in place so that's an initial tally of what's been done so far but a precedent is being set.

As for the last few weeks there has been stories about robust wage gains to be realized in these negotiations, there wasn't much of a market move today with JGB yields and the yen little changed. The Nikkei rallied about 1%, though is still down about 6% year to date. We remain long Japanese stocks.

China unveiled another comprehensive 'plan' to boost its economy, this time mostly focusing on consumption. It was a 30 point strategy focusing on everything from making child care more affordable to trying to boost wages (via higher minimum wages), further efforts to stabilize the stock market along with housing. I believe the key with encouraging more consumer spending is putting a floor under the housing market and home prices and at this point, time is the only real cure.

After the 2.1% rally in the Hang Seng on Friday, it was up another .8% today and is higher by 20.4% year to date. It is by far outperforming the S&P 500 since December 2023 and still only trades at about 11x earnings. We continue to be long and bullish on some names there.

China also reported January/February (to account for the distortion of the Lunar New Yr) combined data and property continues to be the soft spot with home prices and sales continuing to fall but the pace has definitely slowed. Year to date retail sales were up 4%, about as expected but helped by 'cash for clunkers' type incentives on some items and which I'm never a fan of as it's only temporary the boost. Industrial production exceeded expectations.

With the 8:30 and 10am economic data today including the first March industrial figure in the NY Empire manufacturing survey, retail sales and home builder sentiment, my ability to comment will depend on the quality of the wifi on my soon to be flight.

BY Doug Kass · Mar 17, 2025, 8:47 AM EDT

Per below I should add when public companies are fessing up, which they are loathe to do, you know there is an issue. Especially when the commentary lines up with the economic data.

In sports I often dispense with the nerd data and go with what my eyeballs tell me about a player (dumb nerd stats somehow indicate a player is good when they are batting .200 and can’t field). When the nerd stats align with the eyeballs, you are generally on to something.

How much of this is due to the consumer being over-consumed (having bought about all they need since Covid except for food, which oddly is softening too due to trade down), how much of this is due to the consumer having less income and a strained balance sheet, and how much of this is due to general loss of confidence and the consumer being traumatized, fatigued, and exhausted by politicians and the media, is beyond me. But this last factor exists and is overlooked.

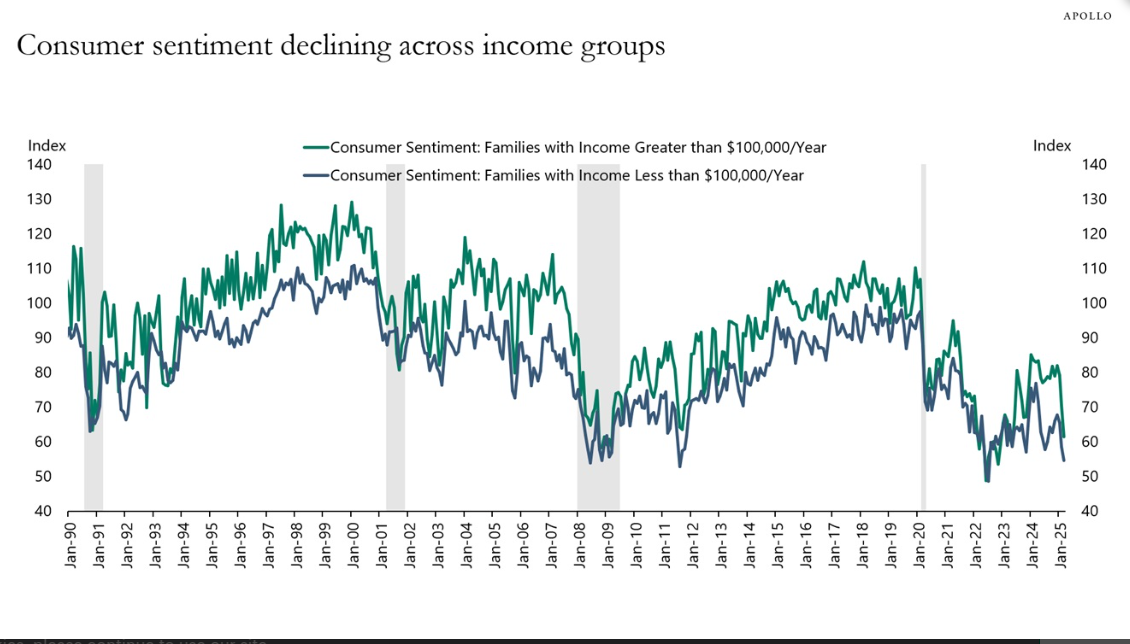

From Apollo's Dr. Torsten Slok:

March 16, 2025

Consumer Sentiment Deteriorating Rapidly

The March survey of consumer sentiment from the University of Michigan shows the following:

Consumer sentiment is declining rapidly both for households making more than $100,000 and less than $100,000 (see the first chart).

Consumer worries about losing their jobs are at levels normally seen during recessions (see the second chart).

A record-high share of consumers think business conditions are worsening (see the third chart).

Households’ income expectations are declining (see the fourth chart).

Inflation expectations are rising at an unprecedented speed (see the fifth chart).

The bottom line is that consumer sentiment is deteriorating at an alarming rate.

For the rest, click here.

And from me, on Friday:

There continues to be no shortage of chatter about the government-spend side of things, which is obviously significant. In his latest must-read report, Jared Woodard, Bank of America's Research Investment Committee head, writes that the U.S. has never been more government-dependent: It relies on government for 85% of job growth, 33% of all spending and -- worst of all -- 6%-7% budget deficits, all of which are at record highs (excluding crisis and war).

But it still seems to me the consumer side of the equation is not getting the attention it deserves. I'm talking about the consumer spend outside of the spending from government employees or related entities. Just the average Joe.

The rule of thumb is to never bet against the U.S. consumer, but if you did for the last few months, you would have been right. It might not have been Keynesian economics that did the trick post World War II, it may just have been that Americans felt great all of the sudden and had also underspent for about the prior 15 years coming out of the Great Depression, so there was a fair bit of catch up.

What if we are going through the opposite of that now? People just feel like garbage due to all the political toxicity, stress, and wars, on top of being overspent and over consumed? And the U.S. government doesn’t have a balance sheet left to deal with any of this.

I am not a huge believer in Keynesian economics. In fact, as opposed to separating out government spend from gross domestic product, one could even argue you could give it a negative number, given all of its unintended consequences.

This is a good article with regard to the history of government spend and its implications: https://www.zerohedge.com/economics/get-government-out-gdp. Even if you believe in Keynesian economics, however, it was never supposed to be this way. Government was meant to spend to plug the hole in bad times and then run a surplus in the good times. Not complicated. What we have now is far from that. Spend, spend, spend, and it has exploded since Covid.

Here are some more blurbs on the state of the U.S. consumer. A Wall Street Journal article from Tuesday and a snippet from Macro-Strategy. I would add Dick’s Sporting Goods to the list, they chunked it a few days ago too. It feels like there is just a broad slowing in consumer demand, for the time being at least:

The WSJ reports that U.S. consumer spending is declining across all income levels. Wage growth is also slowing across all income groups. The article says its not all about tariffs, but rather a broader sense of uncertainty as many have less hard cash on hand. Checking and savings deposits across all income levels have declined over the 12-month period through February and are getting closer to inflation-adjusted 2019 levels. Wage growth for all income groups has slowed over the past year, and inflation adjusted debt balances are starting to surpass pre-pandemic levels.

As highlighted in Absolute and Relative Growth and Decline, U.S. domestic money supply is still below its 2022 high, although it has been climbing marginally. All that we have seen over the last few years is that money that had already been created in 2020 and 2021 has realigned within the domestic and international economy and financial markets (velocity increasing), funding the U.S. deficit and asset price appreciation. That is now exhausted. The growth in the velocity of money has started to turn down. Without an increase in monetary growth from the present 3% – 4% level, nominal GDP growth – (MV = PT) - will disappoint.

Position: None.

By Doug Kass Mar 14, 2025 8:00 AM EDT

BY Doug Kass · Mar 17, 2025, 8:31 AM EDT

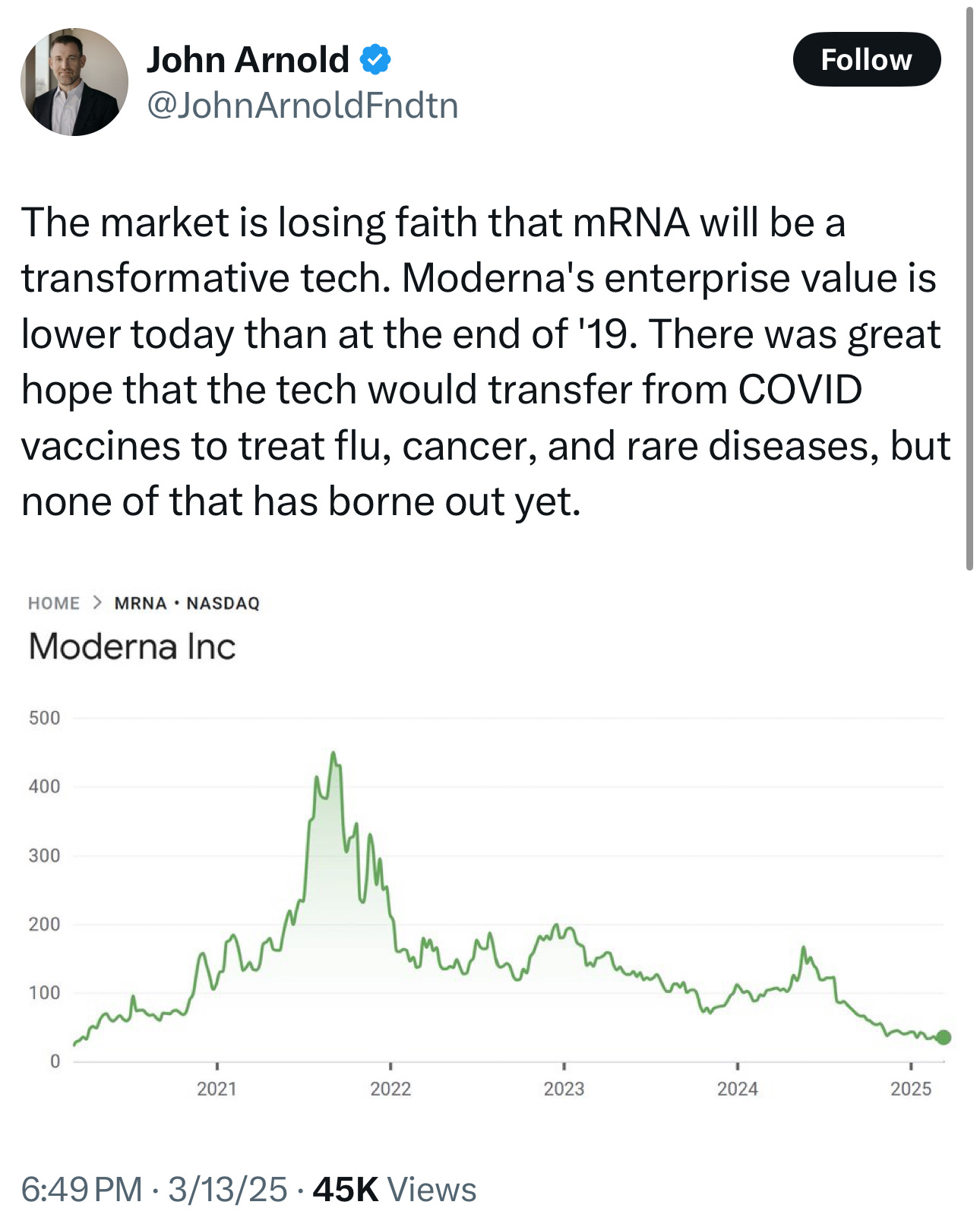

*Comparing AI to mRNA...

How different will artificial intelligence be? My belief is there will ultimately be more value to the AI product than the mRNA product (less than useless in my view), but at the same time more value will be destroyed due to the greater amount of excess capital that has been committed too early to the AI space (when the tech wasn’t there) than to the mRNA space, where substantially less capital was committed (although still a lot in absolute terms just relatively dwarfed by what has gone on in AI).

They always sell you the sun and the moon, oftentimes you only get the Dead Sea!

BY Doug Kass · Mar 17, 2025, 8:15 AM EDT

BY Doug Kass · Mar 17, 2025, 8:00 AM EDT

BY Doug Kass · Mar 17, 2025, 7:45 AM EDT

Citigroup lowers its price target on Occidental Petroleum OXY from $56 to $51.

BY Doug Kass · Mar 17, 2025, 7:35 AM EDT

BY Doug Kass · Mar 17, 2025, 7:25 AM EDT

BY Doug Kass · Mar 17, 2025, 7:15 AM EDT

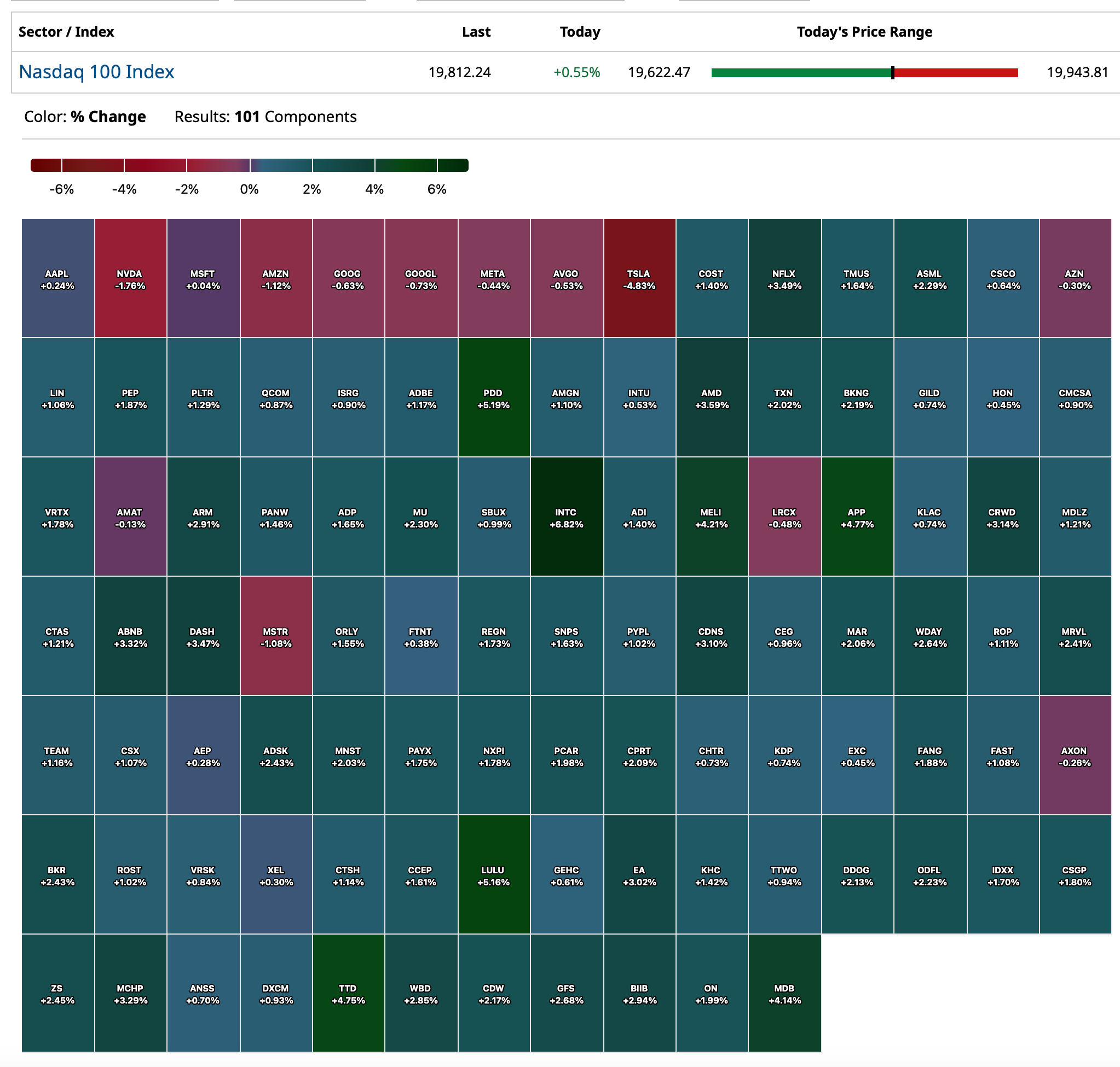

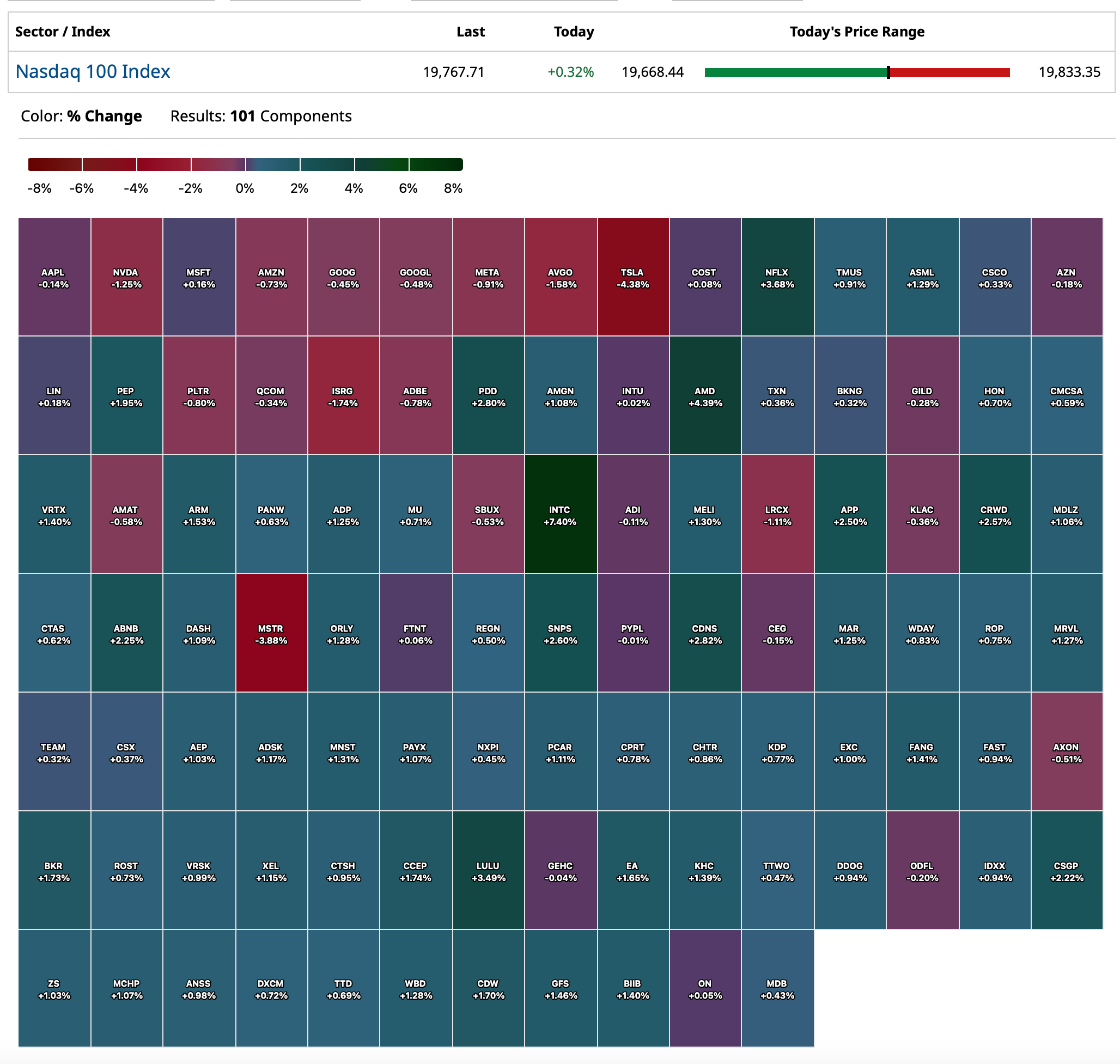

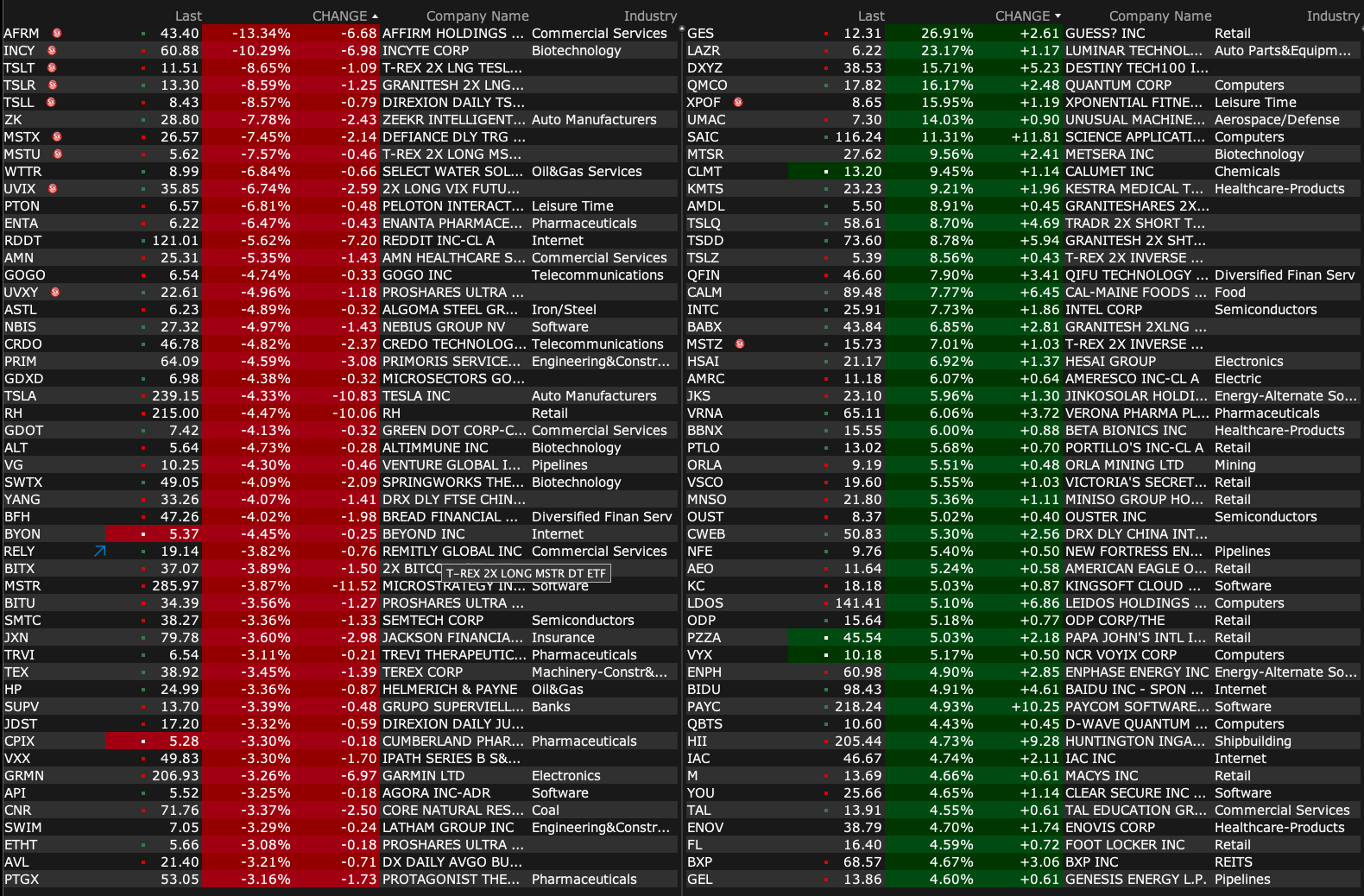

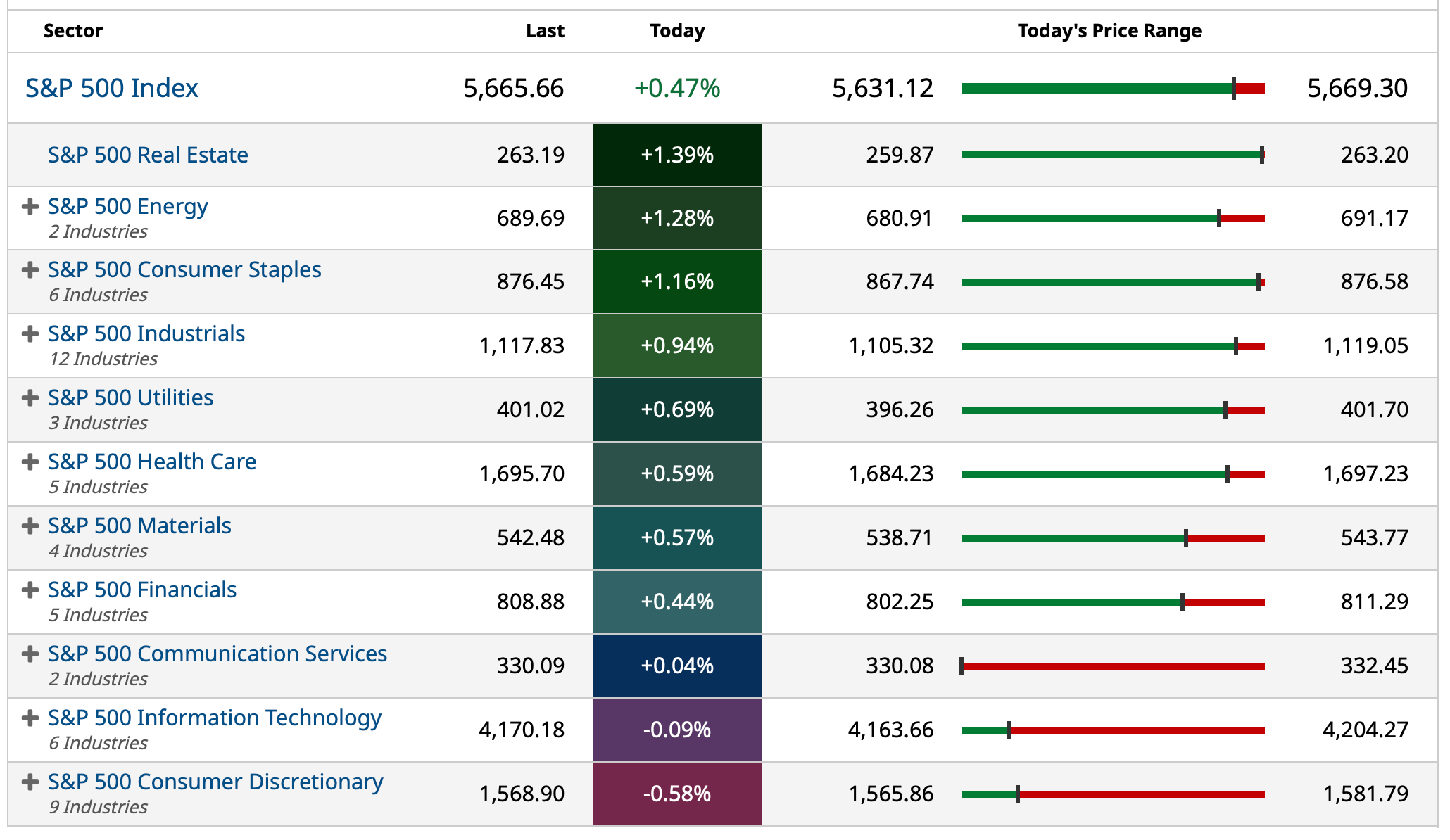

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Mar 17, 2025, 7:05 AM EDT

BY Doug Kass · Mar 17, 2025, 6:55 AM EDT

From JPMorgan:

US: Futs are lower to start the week as the market digests trade war news and the Trump Put remains absent. RU/UKR ceasefire news is having a muted impact. Pre-mkt, Mag7 names are all lower ex-NVDA, and most Semis are under pressure. Bond yields are lower as the curve bull flattens and the USD is flat. Cmdtys are bid higher led by Ags and Energy. Today’s macro data focus is on Retail Sales where a stronger number may give the market comfort in trying to create a relief rally and the Fed on Weds could be supportive too.

and...

EQUITY AND MACRO NARRATIVE: Last week, the SPX fell 2.3% its fourth consecutive weekly loss and the index sits 7.8% below its all-time highs. NDX underperformed on the week, dragged by Mag7, though Semis outperformed as did the RTY. The 10Y yield moved up 1bps with DXY flat. Commodities added 11bps and marks the 5th weekly gain out of the last 6 weeks, adding 2.7% to the BCOM Index. The drivers continue to be a combination of positioning, including factor unwinds, trade and economic uncertainty, valuation, and a broadening of the rally to international Equities. Also, given the absence of both a Trump Put and a Fed Put, markets have declined very rapidly stoking hopes for an equally aggressive bounce.

BY Doug Kass · Mar 17, 2025, 6:45 AM EDT

BY Doug Kass · Mar 17, 2025, 6:35 AM EDT

I had mentioned relatively quiet credit spreads as a potentially positive market influence, but spreads are now widening more:

BY Doug Kass · Mar 17, 2025, 6:25 AM EDT

BY Doug Kass · Mar 17, 2025, 6:15 AM EDT

BY Doug Kass · Mar 17, 2025, 6:05 AM EDT

Wolf Street howls about the state of the housing market.

BY Doug Kass · Mar 17, 2025, 5:55 AM EDT

The S&P Short Range Oscillator remains in oversold at -5.95% vs. -6.5%.

BY Doug Kass · Mar 17, 2025, 5:39 AM EDT