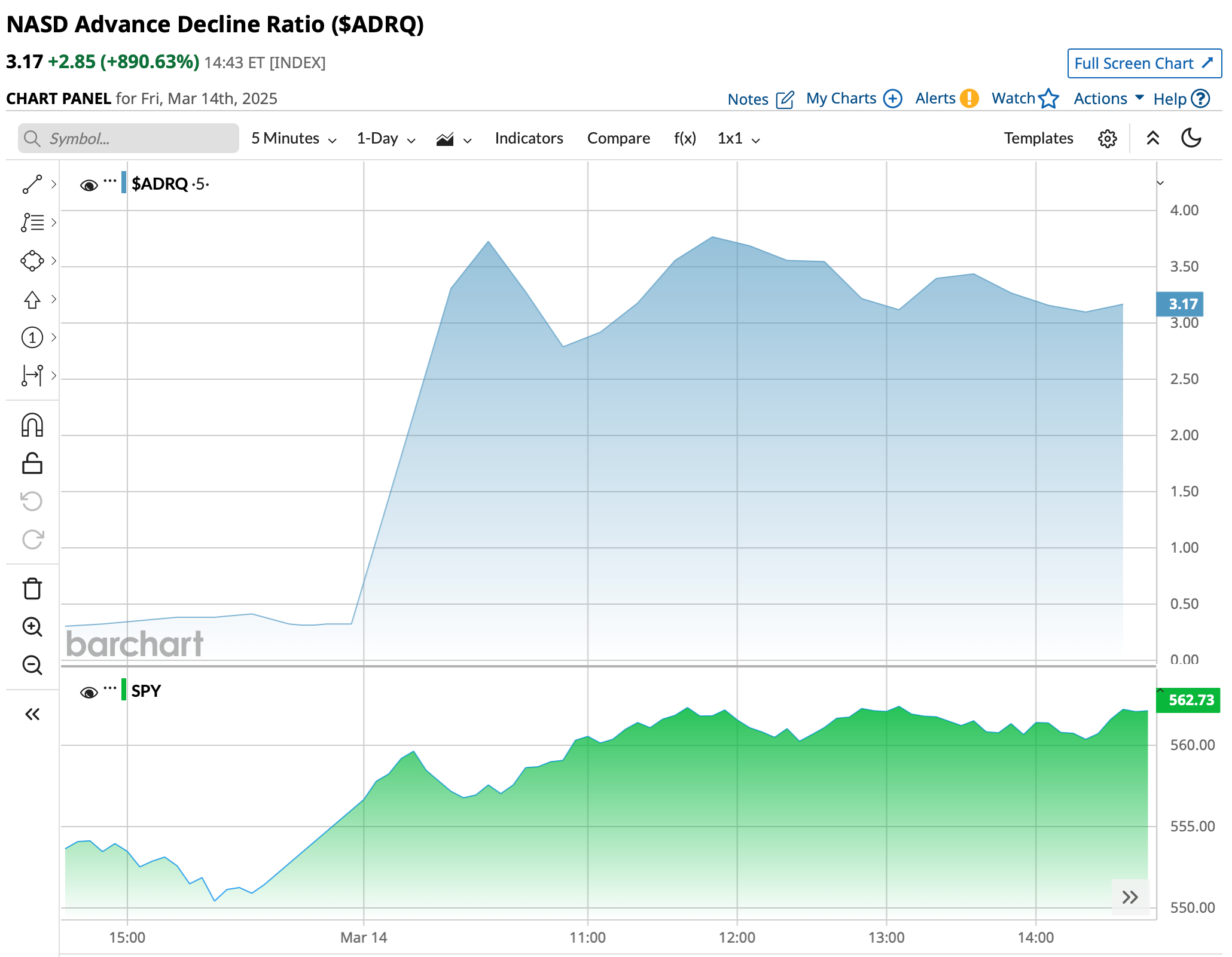

Friday's Closing A/D Intraday vs. SPY

NASD Closing Advance-Decline Intraday (blue) vs. SPY (lower green chart):

BY Doug Kass · Mar 14, 2025, 4:45 PM EDT

NASD Closing Advance-Decline Intraday (blue) vs. SPY (lower green chart):

BY Doug Kass · Mar 14, 2025, 4:45 PM EDT

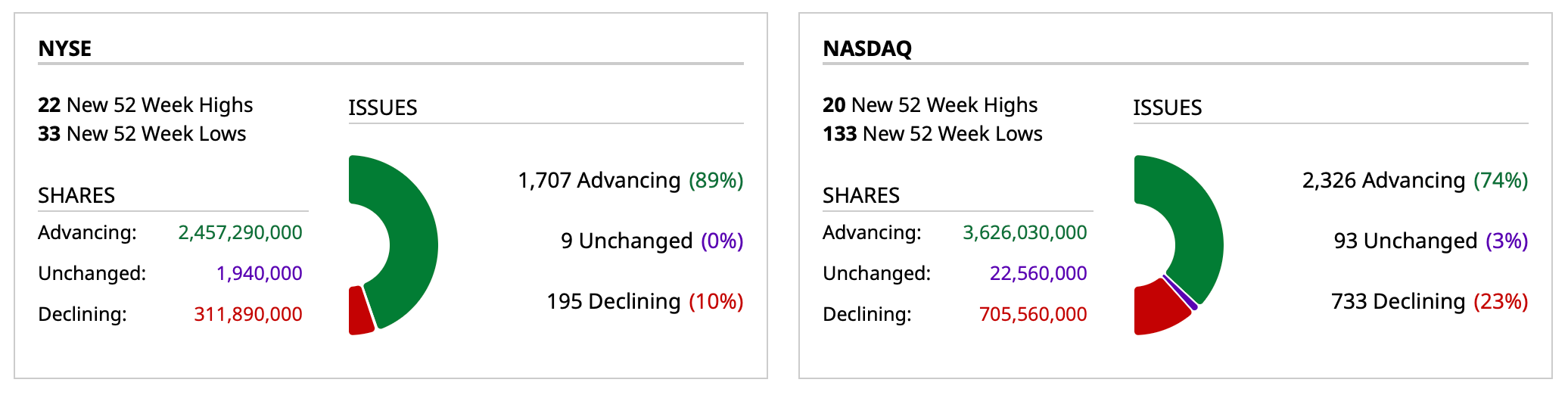

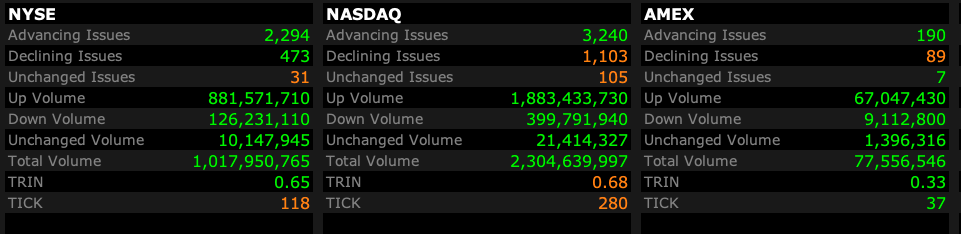

- NYSE volume 13% below its one-month average

- NASDAQ volume 12% below its one-month average

- VIX index: Down 11.68% to 21.78

BY Doug Kass · Mar 14, 2025, 4:34 PM EDT

From Peter Boockvar:

Positives,

1) The February CPI rose by .2% headline and core with both one tenth below expectations. These are off .5% and .4% gains for each in January. The y/o/y gains are 2.8% and 3.1% respectively vs 3% and 3.3% in the month prior. Energy prices were up by .2% m/o/m and down .2% y/o/y. Food prices were higher by .2% m/o/m and 2.6% y/o/y with eating out driving the increase. ‘Food away from home’ prices were up .4% m/o/m and 3.7% y/o/y though ‘food at home’ saw no price gain m/o/m but up 1.9% y/o/y. Services inflation ex energy prices grew by another .3% m/o/m and by 4.1% y/o/y. Core goods prices continue to show signs of bottoming out, up by .2% after a .3% rise in January and are unchanged y/o/y.

2) The February PPI was unchanged. That was well below the estimate of a .3% increase but mostly offset by a two tenths upward revision to January to a .6% gain from .4% initially. The core rate was lower by one tenth m/o/m vs the estimate of up .3%, partly mitigated by also a two tenths upward revision to January to up .5%. Versus last year, headline PPI is still up 3.2% y/o/y vs 3.7% in the month before. The core rate is higher by 3.4% vs 3.8% in January.

3) Initial jobless claims totaled 220k, down 2k w/o/w and below the estimate of 225k. Continuing claims fell to 1.87mm from 1.897mm.

4) Wage growth remains pretty good as the Atlanta Fed released its February wage growth tracker which rose 4.3% y/o/y vs 4.1% in January, 4.2% in December and 4.3% in November. For a 'job switcher', wages were higher by 4.8%, the same pace seen in January. For a 'job stayer', they accelerated to 4.4% growth vs 4.1% in the three prior months.

5) The number of job openings in January totaled 7.74mm, up from 7.51mm in December which was revised down by about 100k. This compares with 8.03mm in November and 7.62mm in October. The hiring rate was 3.4% and December was revised up to the same level from 3.3% initially. For perspective, 3.2% matches the lowest since 2013 not including Covid. The quit rate did rebound to 2.1% vs 1.9% in the two prior months.

6) With a further drop in mortgage rates to an average of 6.67%, purchase applications rose 7% w/o/w after a 9.1% rise in the week before that followed four weeks in a row of declines. Refi's were higher by 16.2% w/o/w after jumping by 37% last week.

7) From Oracle: "this was our strongest booking quarter ever by a large margin...Speaking of data centers, we marked a milestone this quarter as we crossed into triple digits with our 101st cloud region coming online."

8) From Dick’s Sporting Goods: On their customer and clarifying their muted guidance, "We are not seeing a weaker consumer now. We're coming off a fantastic Q4. Our guidance merely reflects the fact that there's so much uncertainty in the world today in the geopolitical environment, macroeconomic environment, we are just being appropriately cautious. And I would give you a couple of other data points about our consumer and why we actually feel optimistic. Our consumer has proven that in times of stress and uncertainty, that they are leaning into outdoor, being outside going for a run or walk, or play, watch team sports, it's become much more of a necessity than a discretionary item. And it makes sense because it is a way for people to find calm in an otherwise uncertain timeframe."

9) From Vivid Seats: They mentioned the "long term secular growth trends in live events...Additionally, we are seeing that consumers increasingly prioritize spending on live experiences over goods, and artists touring more and more. While 2024 saw muted growth relative to the record setting growth seen in 2022 and 2023, 2025 looks to potentially return to industry expansion consistent with its long term trajectory."

10) From Viking Cruises: "2025 is shaping up to be a great year. Also demand for our core products remain strong. As of February '25, we were already 88% booked for the year, with $5.3 billion of advanced bookings. These are 26% higher than the 2024 season at the same point in time."

11) Here was the bottom line for why the Bank of Canada cut its base rate by another 25 bps to 2.75% as expected. "While economic growth has come in stronger than expected, the pervasive uncertainty created by continuously changing US tariff threats is restraining consumers' spending intentions and businesses' plans to hire and invest. Against this background, and with inflation close to the 2% target, Governing Council decided to reduce the policy rate by a further 25 bps." They also said this, which is revealing too ahead of the Fed meeting next week. "Monetary policy cannot offset the impact of a trade war. What it can and must do is ensure that higher prices do not lead to ongoing inflation."

12) Base pay in Japan in January rose 3.1% y/o/y, up from 2.6% in December and that is the quickest pace of gain since 1992.

13) The main reason for the .7% y/o/y drop in February CPI in China was the 3.3% decline in food prices. Ex food and energy saw prices lower by one tenth y/o/y, essentially unchanged, aka price stability.

Negatives

1) The very politically divided initial March UoM consumer confidence index fell to 57.9 from 64.7 and that was below the estimate of 63 and the weakest since November 2022. Most of the drop came from the Expectations component which declined by 10 pts m/o/m. The Current Conditions index was lower by a more modest 2.2 pts m/o/m. Also of note, one year inflation expectations jumped to 4.9% from 4.3% and that is the highest since November 2022. The 5-10 yr crystal ball guess went to 3.9% from 3.5%, a level last seen in early 1993. The employment component plummeted by 20 pts to just 50 with those seeing ‘more unemployment’ rising by 15 pts to 66, the most since February 2009 at the depths of the Great Recession. The income component went negative with more respondents now expecting lower income compared to those seeing more. The percentage of those expecting that family income will exceed inflation over the coming 5 years fell to just 25.5%, the lowest since this question was first asked in 1997. Spending intentions were mixed with the drop in mortgage rates likely helping to lift by 2 pts those that think it’s a Good Time to Buy a House but after dropping by 6 pts last month. Intentions to buy a major appliance also rose by 4 pts but declined by 20 pts in February. Vehicle intentions sunk again, by 7 pts to the lowest level since November 2022. Not surprisingly, “Many consumers cited the high level of uncertainty around policy and other economic factors.” And obviously tariffs are a big focus. “Last month, about 40% of consumers spontaneously mentioned tariffs during interviews, and this month, 48% did so. This figure includes the 44% of Independents who referenced tariffs, showing that these concerns are not limited to Democrats in opposition to Trump.”

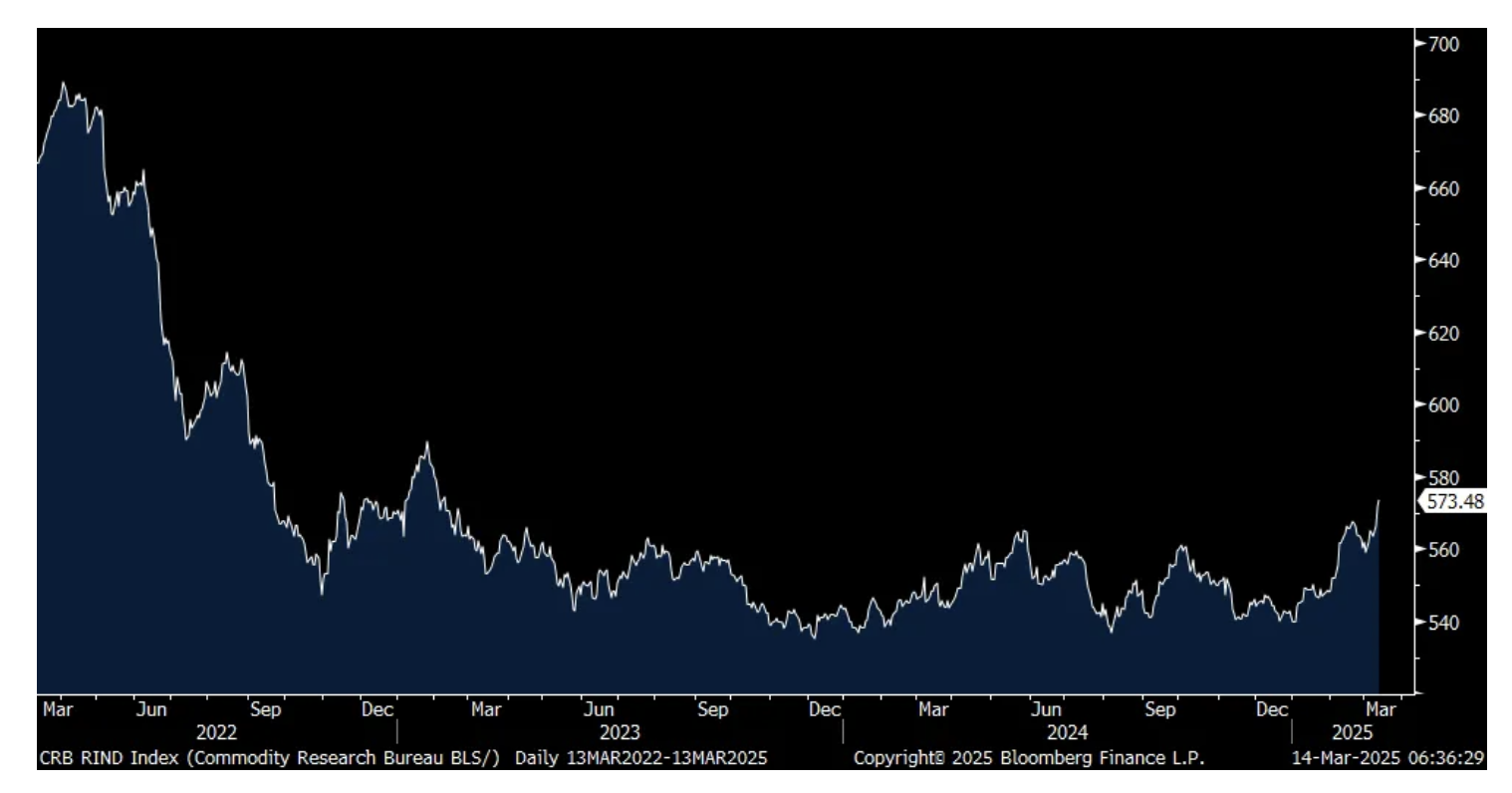

2) The CRB Raw Industrials index closed at a 2 yr high.

3) From the NY Fed’s Consumer Expectations Survey: "Mean unemployment expectations - or the mean probability that the US unemployment rate will be higher one year from now - jumped 5.4 percentage points to 39.4%, its highest reading since September 2023. The increase was broad based across age, education, and income groups." On the credit side for consumers, "Perceptions of credit access compared to a year ago showed a larger share of households reporting it is harder to get credit, and a smaller share reporting it is easier. Expectations for future credit availability deteriorated considerably in February." And, "The average perceived probability of missing a minimum debt payment over the next three months increased by 1.3 percentage points to 14.6%, the highest level since April 2020." To the concerns above, "The share of households expecting a worse financial situation in one year from now rose to 27.4%, the highest level since November 2023."

4) The NFIB optimism index for February fell 2.1 pts m/o/m to 100.7 and down for a 2nd month. It's though still well above the October, pre-election, level of 93.7. The NFIB said "Small business owners have experienced uncertainty whiplash over the last four months with the Uncertainty Index falling from October's 110 reading to 86 in December and then back up to 104." The bottom line from the NFIB, "Uncertainty is high and rising on Main Street, and for many reasons."

5) From Delta: They lowered their y/o/y revenue guidance to growth of 3% to 4% from its initial guidance of 7% to 9%, along with trimming margin and eps guidance and said "The outlook has been impacted by the recent reduction in corporate confidence caused by increased macro uncertainty, driving softness in Domestic demand. Premium, international and loyalty revenue growth trends are consistent with expectations and reflect the resilience of Delta's diversified revenue base."

6) From Southwest Airlines: They are lowering their Q1 revenue per available seat mile (RASM) growth rate to a "range of 2% to 4% on capacity down approximately 2%, both on a y/o/y basis. They blame part of this on "less government travel, and a greater impact from the California wildfires than originally estimated." But also this, "The remainder of the decrease is primarily attributable to softness in bookings and demand trends as the macro environment has weakened."

7) From American Airlines: "the revenue environment has been weaker than initially expected due to the impact of Flight 5342 and softness in the domestic leisure segment, primarily in March."

8) From American Eagle: "2025 has started off softer than anticipated. First quarter to date sales have been impacted by a less robust consumer environment and cold weather. For the year, ongoing consumer uncertainty and changes in the operating landscape, including tariffs and a strengthening US dollar, are also creating factors for us to navigate. Against this backdrop, we currently expect full year revenue and operating income to be down relative to last year."

9) From Dollar General: "Our customers continue to report that their financial situation has worsened over the last year as they have been negatively impacted by ongoing inflation. Many of our customers report that they only have enough money for basic essentials with some noting that they have had to sacrifice even on the necessities. As we enter 2025, we are not anticipating improvement in the macro environment, particularly for our core customer."

10) From Ulta Beauty: "Turning now to our outlook for 2025. The operating environment continues to be dynamic. And as we navigate ongoing consumer uncertainty, we believe it is prudent to take a cautious approach to our guidance for fiscal 2025."

11) From Kohl’s: "from a macro perspective, you see a pretty decent bifurcation among income level. We don't see it too much geographically per se, but when you look at income level, if you're making less than $50k, that consumer is pretty constrained from a discretionary standpoint. If you're making less than $100k, it's also pretty challenging. And you see that very clearly in numbers. And obviously we hear the inflation numbers. We know they're coming down to 2% to 3%, but they're still pretty elevated particularly from a grocery and rent perspective over the last few years because they haven't actually deflated. And, I'm not sure wages have kept up with that...You definitely see that in them, they're seeking out value. You see it in the mix of the product we're selling, you see it in the promotions that we are doing. They're definitely seeking value."

12) From Alcoa: "We do see the tariffs creating uncertainty with our customers right now. Some customers are rushing to secure supply ahead of the tariffs, while others are playing wait and see, to see how the final tariff structure will exist. As a result, this quarter, we do have more uncertainty in both our revenue and our working capital that is more than normal. Overall though, we're expecting a very strong first quarter."

13) The UK economy unexpectedly contracted in January by one tenth m/o/m vs the estimate of slight growth of one tenth. Weakness in manufacturing and construction led the decline. There was modest growth in the services side of their economy, particularly in retail.

14) In China, the 2.2% decline in producer prices is more a symptom of the manufacturing challenges that China is having, along with the rest of the world.

BY Doug Kass · Mar 14, 2025, 3:01 PM EDT

Professor Scott Galloway's No Mercy/No Malice:

BY Doug Kass · Mar 14, 2025, 2:45 PM EDT

This is not good for Apple AAPL and it's different than yesterday's bad AI integration news.

I remain short despite the share price decline.

BY Doug Kass · Mar 14, 2025, 2:29 PM EDT

BY Doug Kass · Mar 14, 2025, 2:00 PM EDT

From Peter Boockvar:

Yes, politics are an influence here (the world is upside down as Dems hate tariffs/taxes but Repubs are fine with them) but a very stagflationary outlook/mood

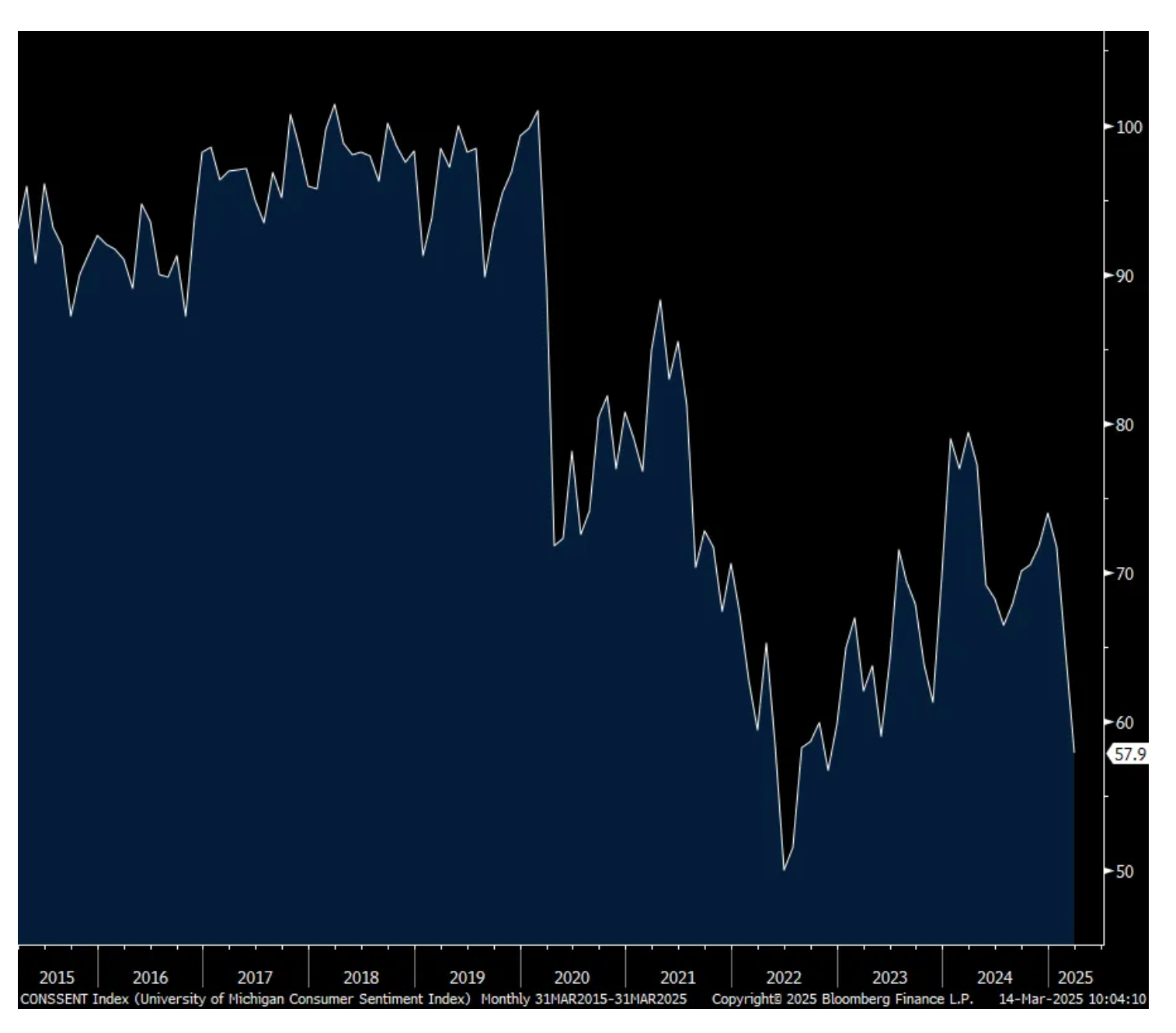

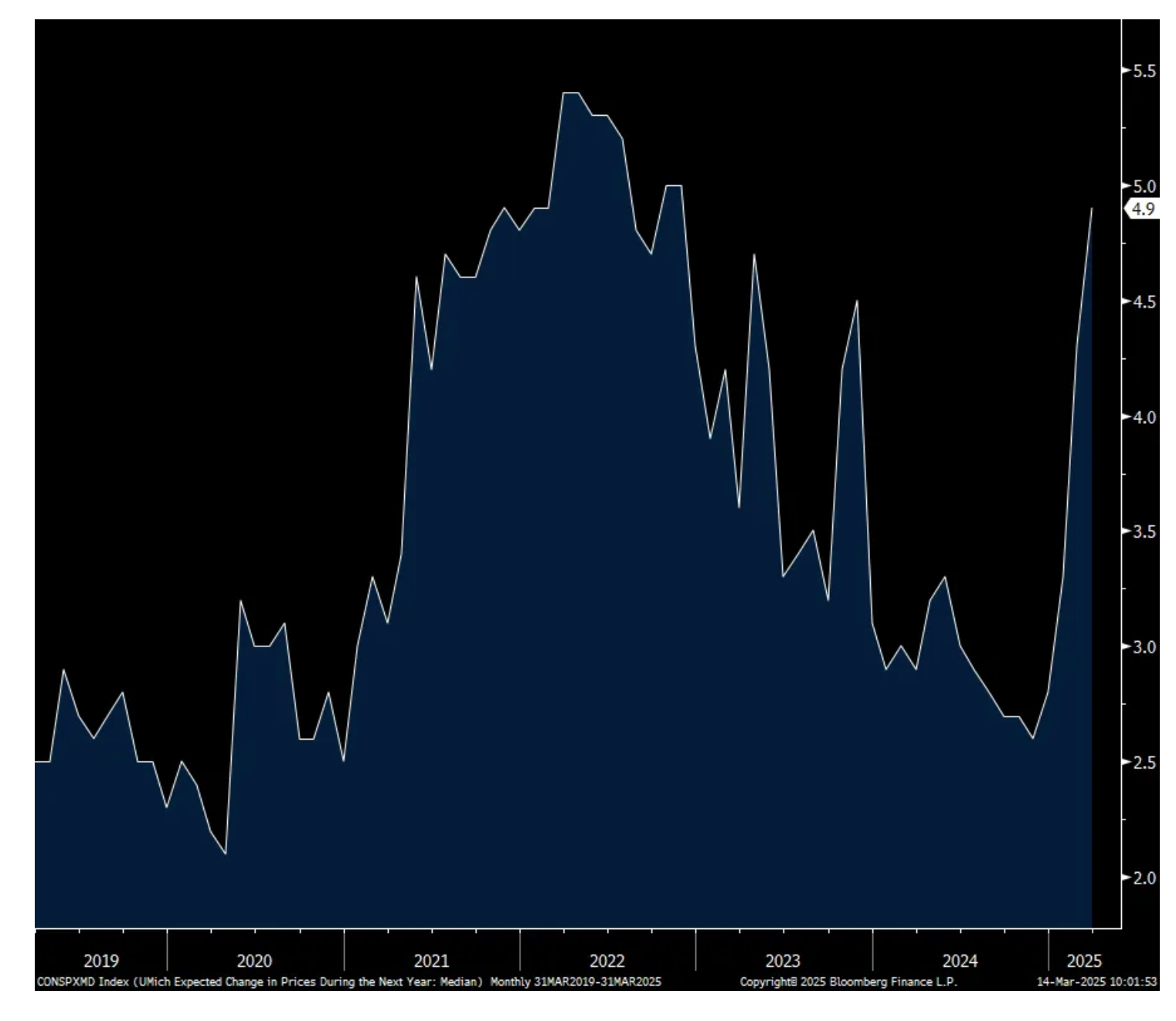

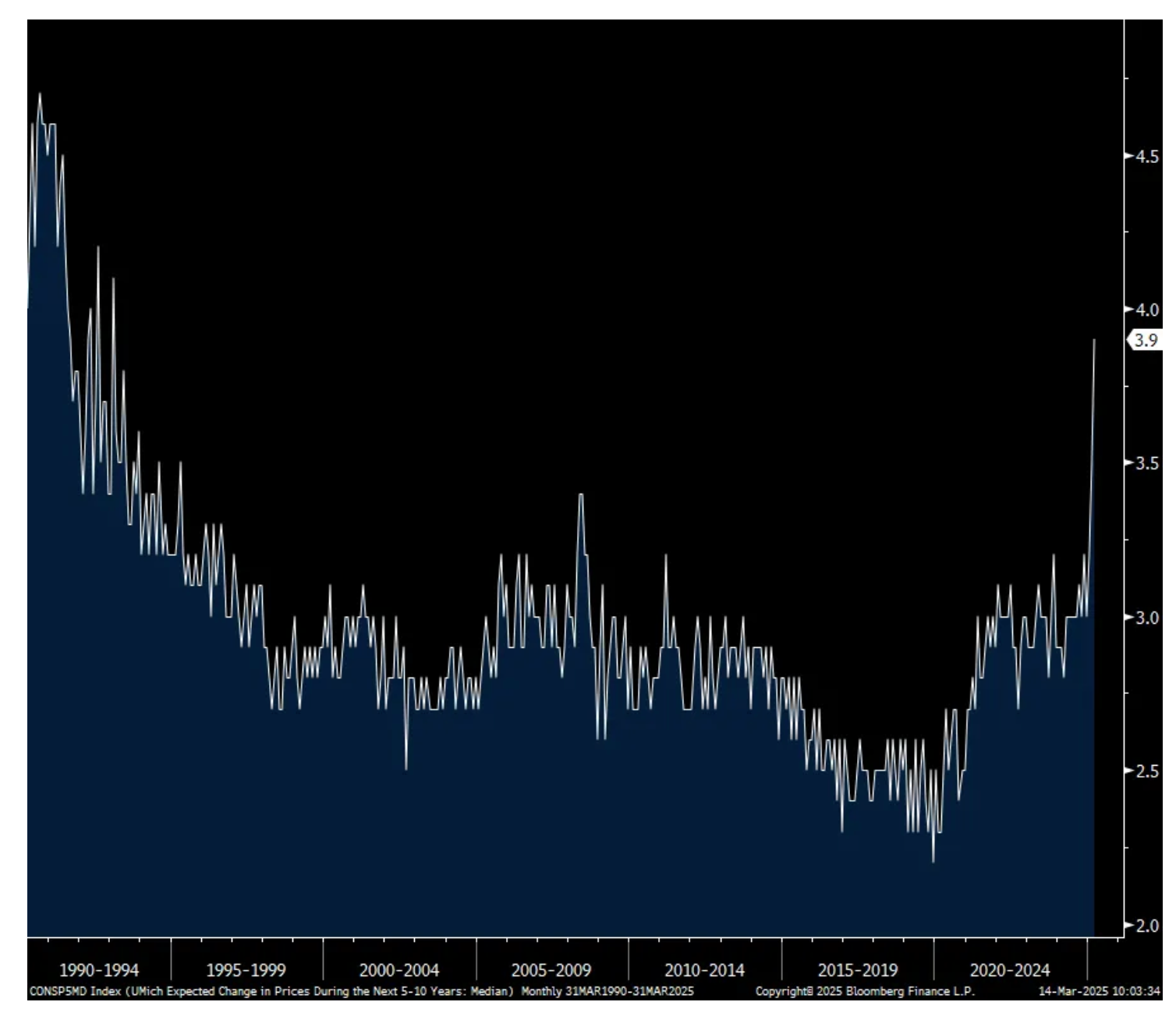

The very politically divided initial March UoM consumer confidence index fell to 57.9 from 64.7 and that was below the estimate of 63 and the weakest since November 2022. Most of the drop came from the Expectations component which declined by 10 pts m/o/m. The Current Conditions index was lower by a more modest 2.2 pts m/o/m. Also of note, one year inflation expectations jumped to 4.9% from 4.3% and that is the highest since November 2022. The UoM specifically said “This month’s rise was seen across all three political affiliations.” The 5-10 yr crystal ball guess went to 3.9% from 3.5%, a level last seen in early 1993.

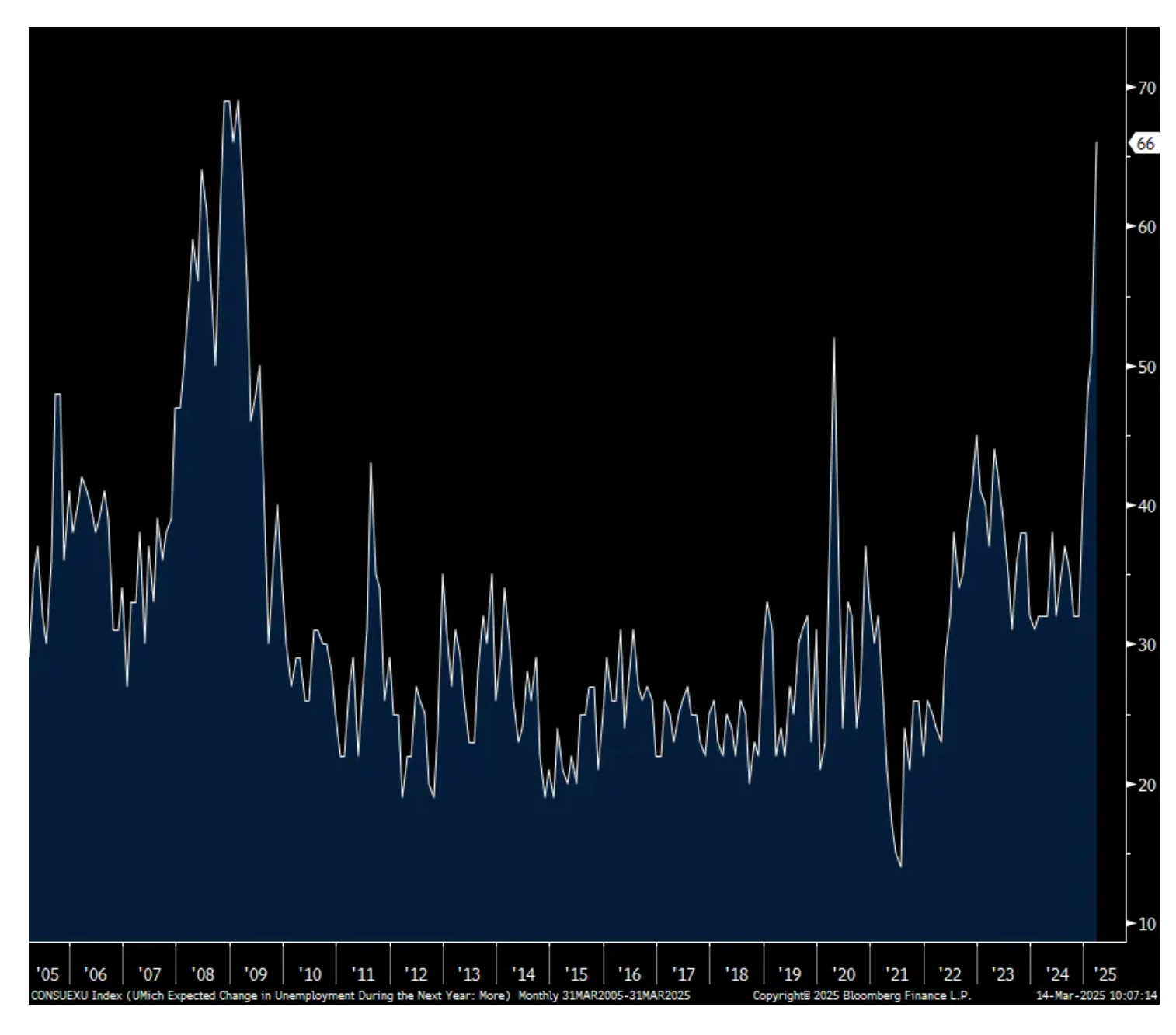

It’s not just worries about inflation but growing concerns with the labor market. The employment component plummeted by 20 pts to just 50 with those seeing ‘more unemployment’ rising by 15 pts to 66, the most since February 2009 at the depths of the Great Recession. The income component went negative with more respondents now expecting lower income compared to those seeing more.

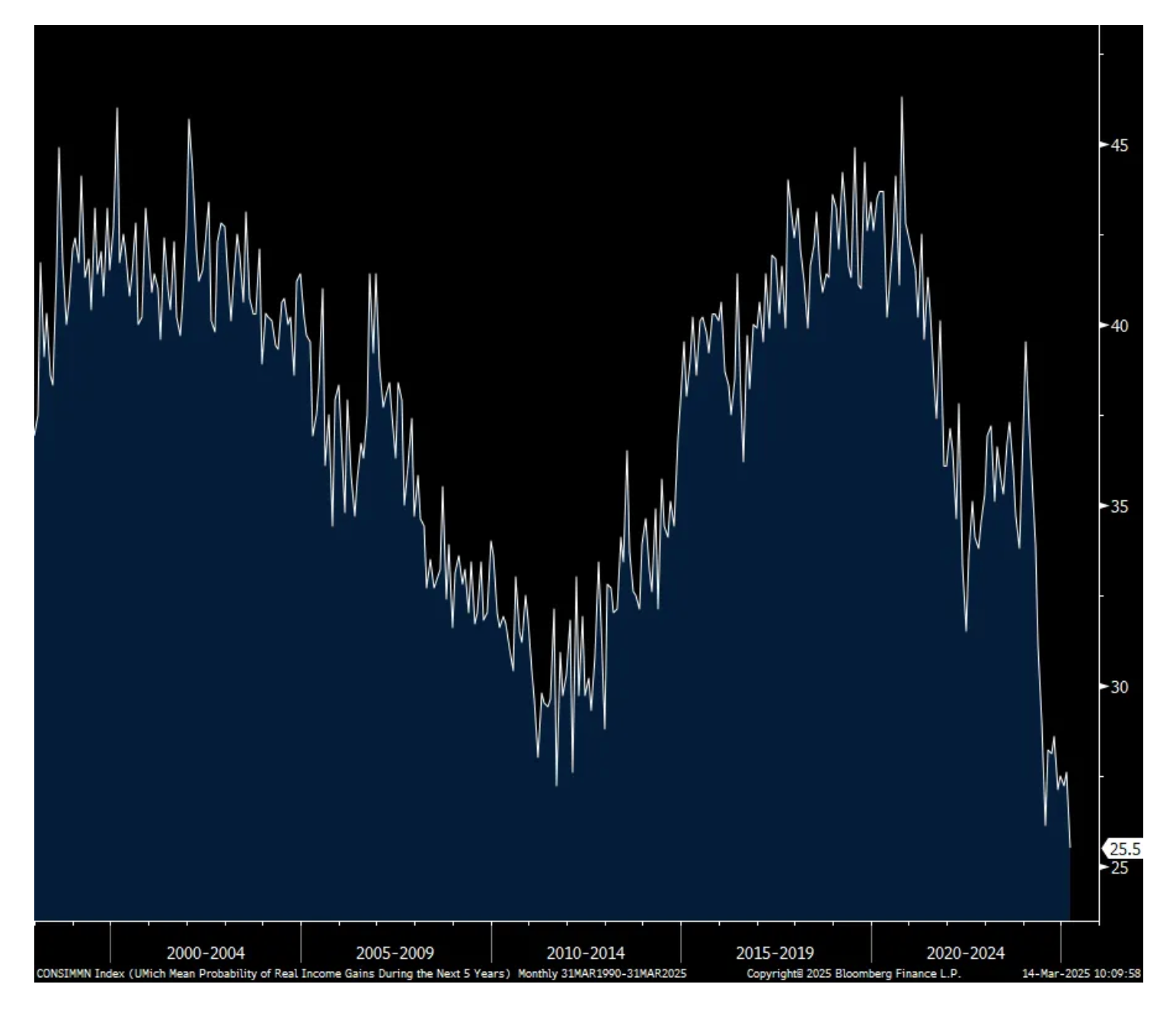

The percentage of those expecting that family income will exceed inflation over the coming 5 years fell to just 25.5%, the lowest since this question was first asked in 1997.

Spending intentions were mixed with the drop in mortgage rates likely helping to lift by 2 pts those that think it’s a Good Time to Buy a House but after dropping by 6 pts last month. Intentions to buy a major appliance also rose by 4 pts but declined by 20 pts in February. Vehicle intentions sunk again, by 7 pts to the lowest level since November 2022.

One’s politics continues to be a major influence on the data as sentiment dropped the most for Democrats, down about 10 pts m/o/m at 41.4. For perspective, it’s now down 50 pts since pre-election. In contrast, the mood among Republican consumers at 83.9 (down 2.8 pts m/o/m) compares with 53.6 in October 2024. It’s worth pointing out though that the Expectations component among Republicans fell by 11 pts m/o/m. Confidence among Independents dropped by 5.4 pts m/o/m to 57.2 which compares with 65.8 in October.

Overall, the UoM said the confidence declines were “seen consistently across all groups by age, education, income, wealth, political affiliations, and geographic regions.”

On that drop in the main Expectations component, it fell “across multiple facets of the economy, including personal finances, labor markets, inflation, business conditions, and stock markets.”

Not surprisingly, “Many consumers cited the high level of uncertainty around policy and other economic factors.” And obviously tariffs are a big focus. “Last month, about 40% of consumers spontaneously mentioned tariffs during interviews, and this month, 48% did so. This figure includes the 44% of Independents who referenced tariffs, showing that these concerns are not limited to Democrats in opposition to Trump.”

I’ll add this, you really know the world is upside down when Democrats are vehemently against tariffs which are otherwise known as taxes and some Republicans are all for them.

Consumer confidence figures are typically not market movers after what was a very stagflationary consumer outlook.

UoM

One yr Inflation Expectations

5-10 yr Inflation Expectations

Those That Expect More Unemployment

Percent of Those Expecting Family Income to Exceed Inflation Over Next 5 yrs

BY Doug Kass · Mar 14, 2025, 12:45 PM EDT

I had a great week so I am going out for lunch with some pals.

Back in a few!

BY Doug Kass · Mar 14, 2025, 12:30 PM EDT

With S&P futures +103 handles I am taking a bunch of my trading long rentals off.

Staying with core positions.

BY Doug Kass · Mar 14, 2025, 12:17 PM EDT

I have collapsed my Index common long and short calls.

No position.

BY Doug Kass · Mar 14, 2025, 11:55 AM EDT

BY Doug Kass · Mar 14, 2025, 11:30 AM EDT

- NYSE volume is 18% below its one-month average;

- Nasdaq volume is 17% below its one-month average

- VIX: down 7.54% to 22.80

BY Doug Kass · Mar 14, 2025, 11:13 AM EDT

BY Doug Kass · Mar 14, 2025, 10:48 AM EDT

My favorite sector to "play" if we are approaching a tradeable rally would be private equity stocks which we initiated yesterday afternoon:

* Value is what you might be getting.,,

If you are looking for a sector that might rally hard into an up move, check out the charts of (KKR) , (BX) and (APO) .

I was previously short private equity at much higher levels.

I initiated trading long rentals in KKR at $108.18, BX at $136.10 and APO at $129.11.

Mar 13, 2025 2:18 PM EDT

BY Doug Kass · Mar 14, 2025, 10:27 AM EDT

From Peter Boockvar:

Gold has finally gotten above the $3,000 level, albeit slightly, and it's done it without much help from the western investor. I define 'help' and 'western' by looking at the ETF holdings of gold that investors usually use to own their gold, outside of physical holdings or mining stocks. At 86.4mm ounces of holdings, while off the lows of 80.5mm a year ago, is still well below the 2020 high of 110.67mm ounces. The main buying continues to be foreign central banks and governments and I'm confident that the western buyers of gold will catch up and remains sort of fresh buying powder. We remain long and bullish gold to say again. I mentioned silver the other day too and it's just $1 from the highest level since October 2012.

As for the CRB raw industrials index that I now keep mentioning and where gold and silver are not a part of, it rose another .3% yesterday to a fresh 2 yr high and is up 2.4% just over the past two weeks.

Total Known ETF Holdings of Gold

CRB Raw Industrials Index

Silver

These were comments from some of the retailers that reported yesterday, particularly Dollar General and Ulta Beauty, and it remains clear that a portion of the US population continues to be challenged financially.

From Dollar General:

They grew comps by 1.2% in the quarter "and was driven entirely by growth of 2.3% in average transaction amount. This included relatively even contributions from increases in average unit retail price per item and average items per transaction. This growth was partially offset by a decline of 1.1% in customer traffic during the quarter, which was impacted by ongoing financial pressures of our core consumer as well as lapping the strong traffic increase of 3.7% from Q4 of 2023."

"The comp sales increase was driven entirely by growth in our consumable category and was partially offset by declines in our seasonal home and apparel categories." Thus, needs were the main priority of spend and less so on discretionary.

"Our customers continue to report that their financial situation has worsened over the last year as they have been negatively impacted by ongoing inflation. Many of our customers report that they only have enough money for basic essentials with some noting that they have had to sacrifice even on the necessities. As we enter 2025, we are not anticipating improvement in the macro environment, particularly for our core customer."

From Ulta Beauty who guided lower by whose stock is rebounding pre market:

"The competitive environment in beauty has never been more intense. For the first time, we lost market share in the beauty category in 2024." Of their competitive challenges, "Some of them are external, while others we own."

"Looking forward, we remain optimistic about the strength and resilience of the beauty category. We are mindful that consumers are navigating a dynamic macro environment, but we continue to expect healthy consumer engagement in beauty."

"Turning now to our outlook for 2025. The operating environment continues to be dynamic. And as we navigate ongoing consumer uncertainty, we believe it is prudent to take a cautious approach to our guidance for fiscal 2025."

From G III Apparel, the clothes maker with brands via licenses like Tommy Hilfiger, Calvin Klein, DKNY and Donna Karan:

They reported earnings that were good but with guidance mixed "in light of what was and continues to be a very challenging operating environment."

The UK economy unexpectedly contracted in January by one tenth m/o/m vs the estimate of slight growth of one tenth. Weakness in manufacturing and construction led the decline. There was modest growth in the services side of their economy, particularly in retail. Nothing market moving here but highlighting the sluggish business activity in the UK, though it has outperformed many of its European peers. And, its service sector has done much better than manufacturing as we know.

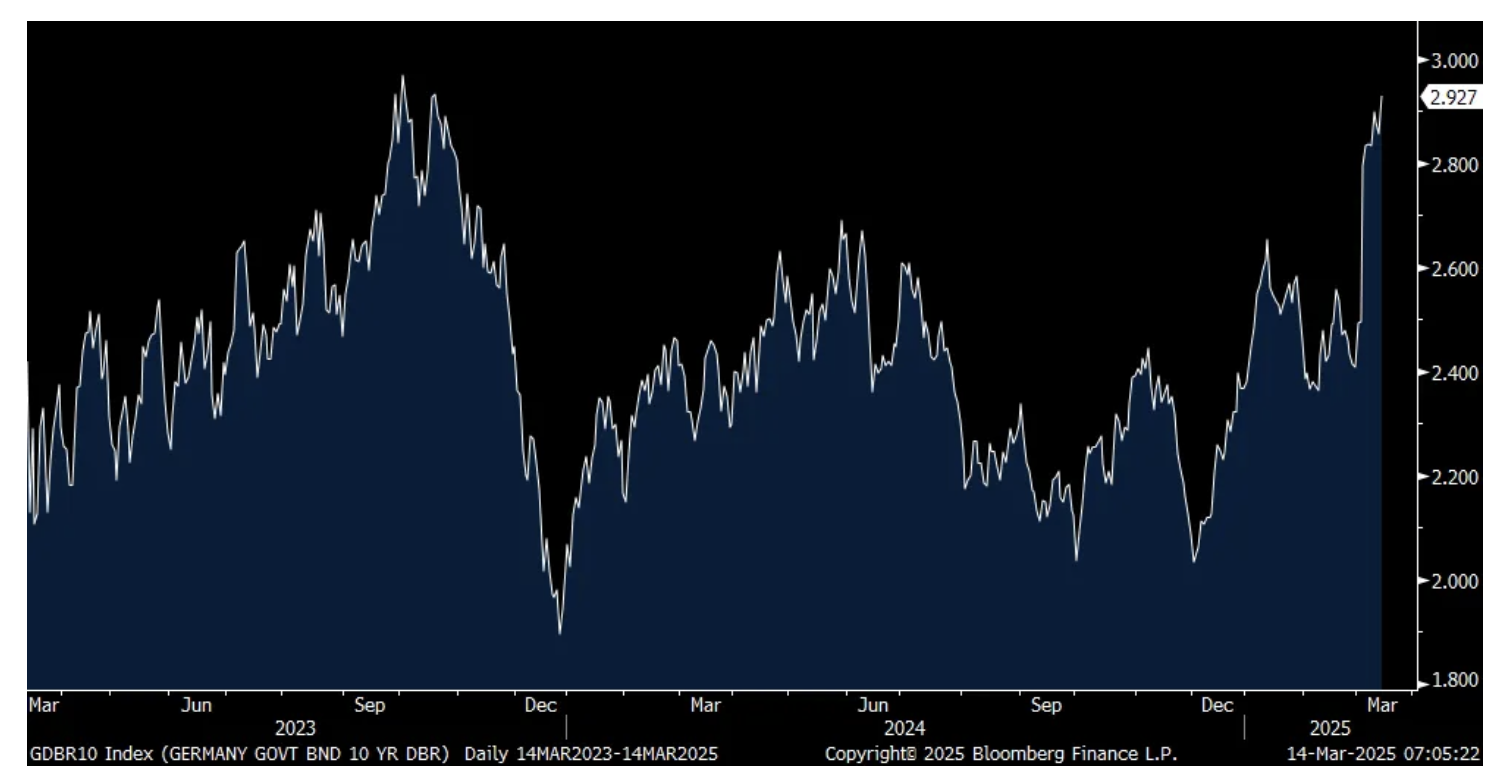

European bond yields are higher again across the region with the German 10 yr bund yield in particular rising by another 7 bps to 2.92%, the highest since October 2023. The reason today is that it looks like the new Merz government has made a deal with the Green party (the one holdout) to implement his fiscal plan. The euro is higher as well as is the DAX which is up 15% year to date.

German Bund 10 yr Yield

BY Doug Kass · Mar 14, 2025, 9:33 AM EDT

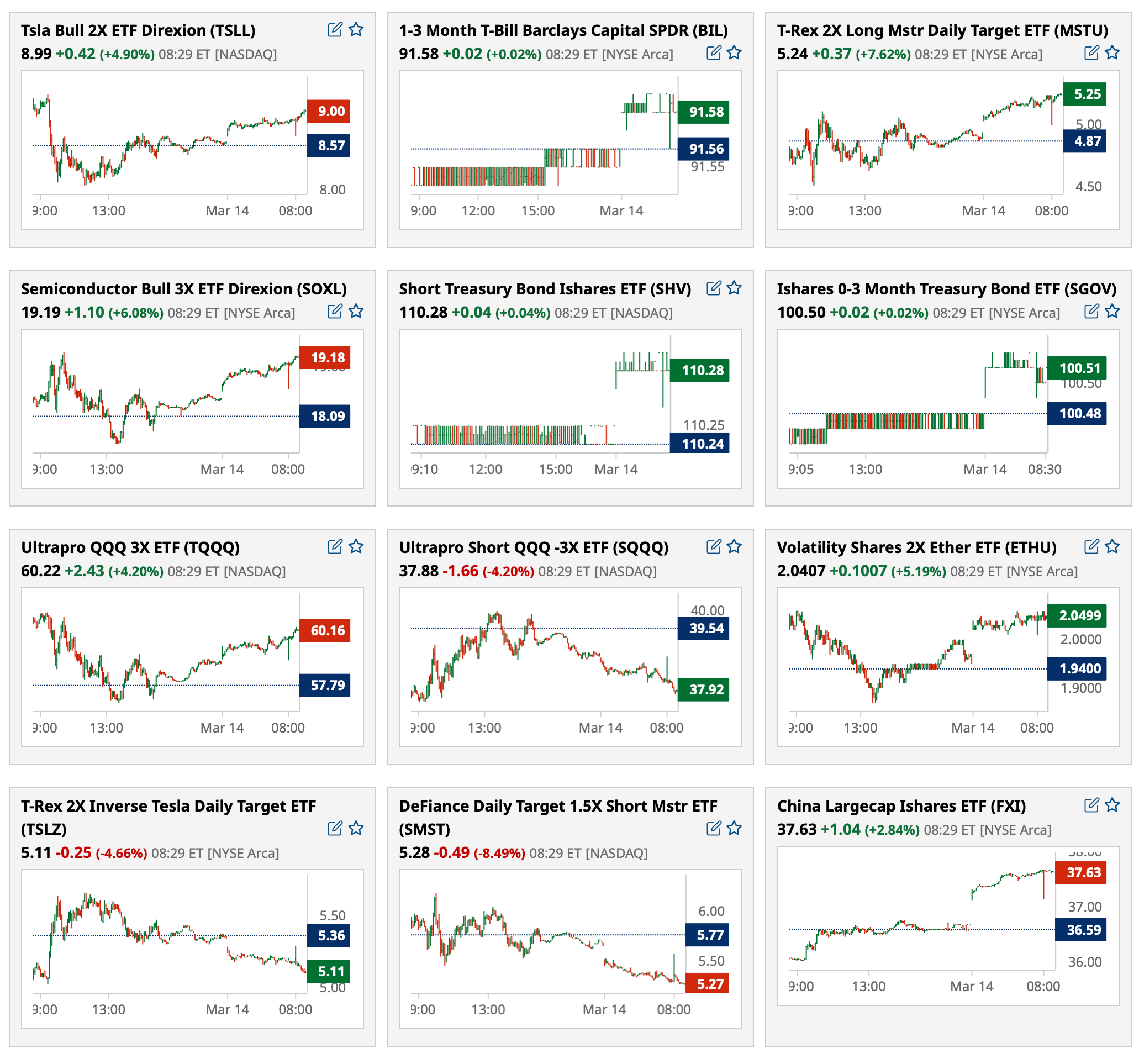

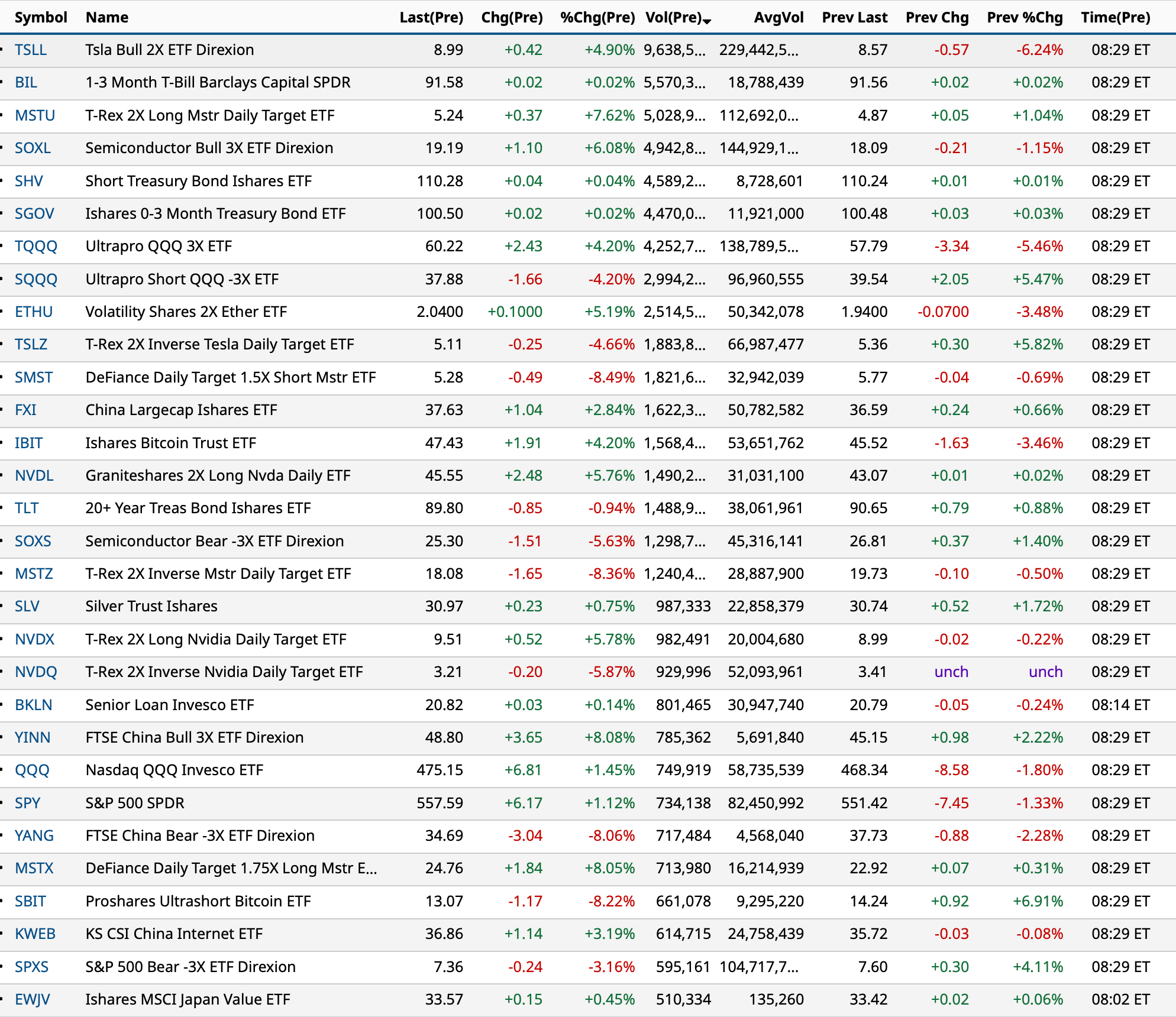

Most active premarket ETFs as of 8:29 a.m. ET:

BY Doug Kass · Mar 14, 2025, 9:23 AM EDT

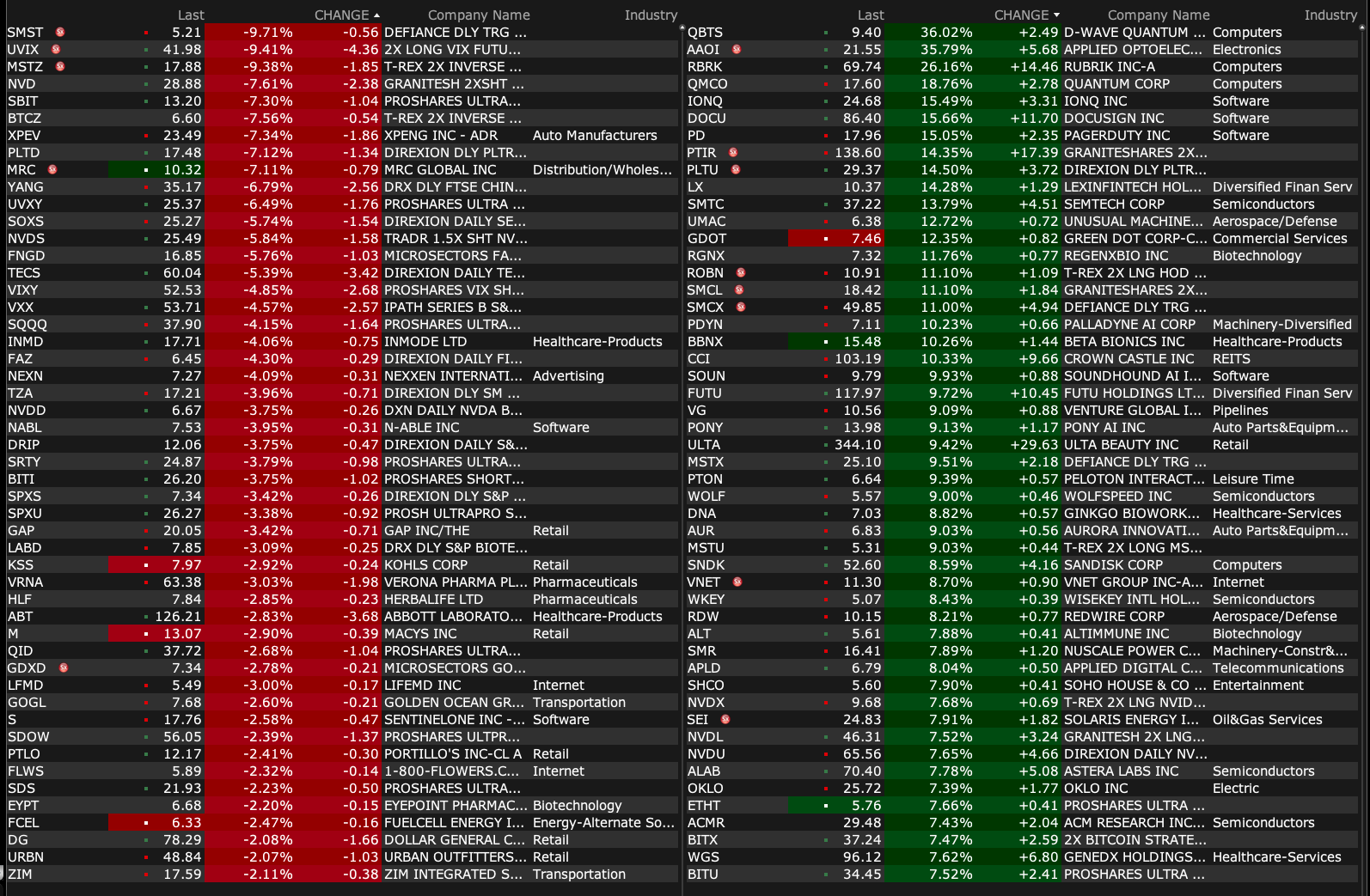

Premarket percentage movers at 8:49 a.m. ET:

BY Doug Kass · Mar 14, 2025, 9:17 AM EDT

-RDUS +109% (to be acquired by Toyota Tsusho America, Inc for $30.00/shr in cash)

-AAOI +53% (entered warrant transaction agreement with Amazon to purchase up to 7.9M shares)

-RBRK +18% (earnings, guidance)

-BZFD +15% (earnings, guidance)

-KINS +12% (earnings, guidance)

-SMTC +12% (earnings, guidance)

-GOGO +11% (earnings, guidance)

-PRPL +10% (earnings, guidance; announces review of strategic alternatives)

-PSQH +10% (earnings)

-DOCU +9.1% (earnings, guidance)

-AMIX +7.3% (advances toward U.S. clinical trials in 2025 with completed integration of Apex 6 Generator for Transvascular Ablation)

-ULTA +5.9% (earnings, guidance)

-JD +5.3% (US listed Chinese stock strength)

-CCI +5.2% (earnings, guidance; to sell Fiber Segment to EQT and Zayo for $8.5B)

-BKE +4.0% (earnings)

-PD +4.0% (earnings, guidance)

-PDD +3.9% (US listed Chinese stock strength)

-CMG +3.0% (Loop Capital Raised CMG to Buy from Hold, price target: $65)

-XPOF -27% (earnings, guidance)

-AIRS -17% (earnings)

-STRO -16% (earnings)

-NAYA -15% (announces a 1:12 reverse stock split, effective Mar 18th)

-GRWG -12% (earnings, guidance)

-SKLZ -9.8% (earnings)

-ATYR -8.4% (earnings)

-LI -4.0% (earnings, guidance)

-AVD -3.2% (earnings, guidance)

-ZUMZ -2.2% (earnings, guidance)

-TBCH -2.0% (earnings, guidance)

BY Doug Kass · Mar 14, 2025, 9:12 AM EDT

JPMorgan failed to warn about the overvalued stock market.

But after the fall, this is their confident communique:

I have been buying JPM aggressively over the last few days.

BY Doug Kass · Mar 14, 2025, 9:05 AM EDT

From JPMorgan:

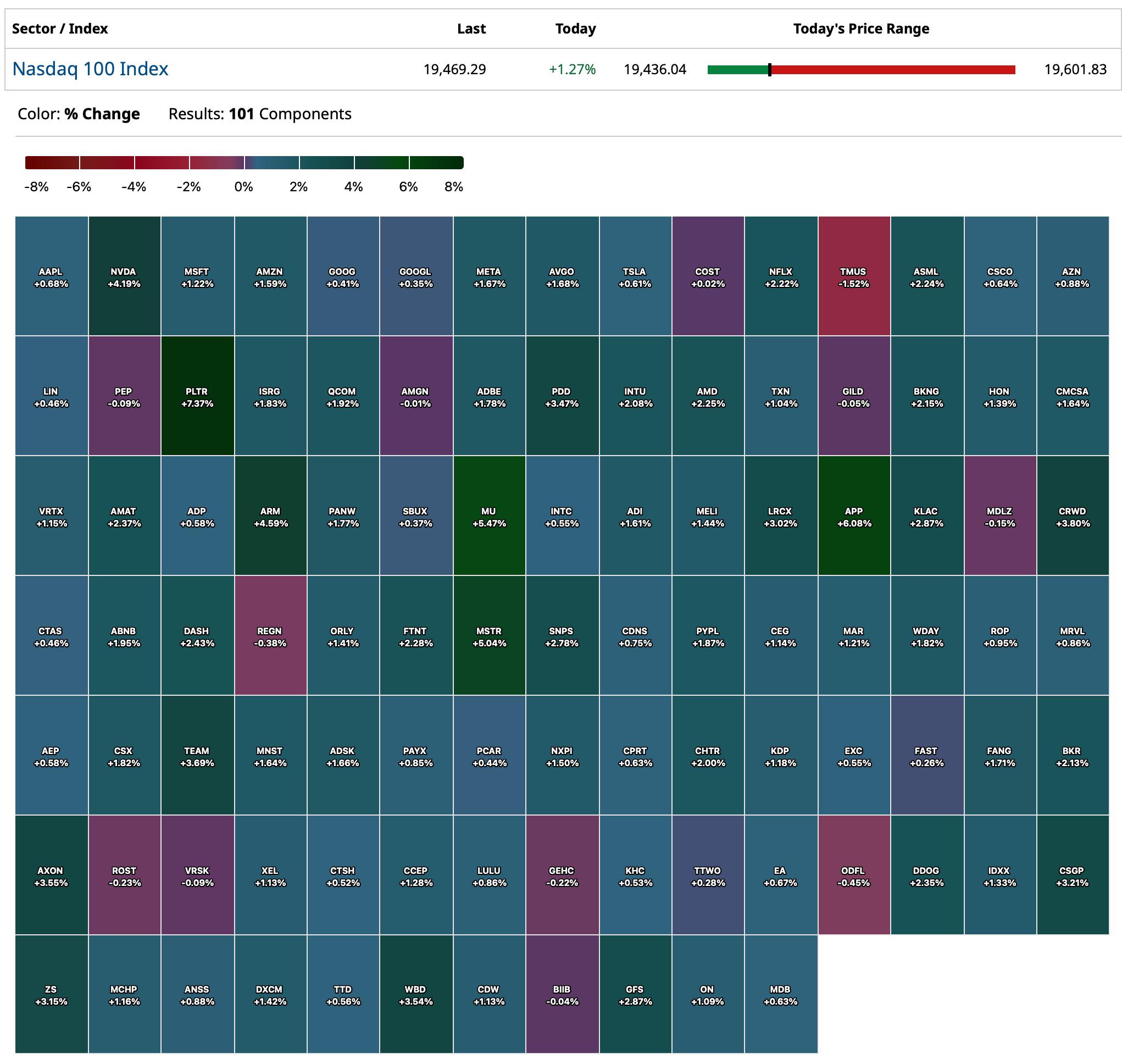

US: Futs are higher led by both NDX and RTY. Mag 7 are mostly outperforming les by NVDA (+1.8%), META (+1.6%) and TSLA (+1.5%). Bond yields are 1-3bp higher this morning; USD is higher. Commodities are higher led by Oil (WTO +1.0%) and Iron (+1.5%). Since yesterday’s close, there has been some positive developments on macro policies: meeting between Lutnick and Ontario’s Ford was viewed as positive; the US government managed to avoid the shutdown. Internationally, China will hold a press briefing next Monday to outline some additional measures boost consumer; Japan announced the largest pay hike in over three decades (+5.36% average pay gain and +3.84% base pay vs. 3.8% JPMe vs. 3.7% last year), a positive catalyst for consumption growth.

and...

EQUITY AND MACRO NARRATIVE: Yesterday, stocks faced a selloff amid another tariff headlines indicating that Trump has now added Europe as a major tariff target. While yesterday’s morning session showed some stabilization, this quickly dissipated as Trump threats to impose a 200% tariff on alcohol products from EU. As of Thursday’s close, a government shutdown will likely be avoided as Senate Dem leader Chuck Schumer said he won’t block Republican funding bill despite divisions within the party (NBC). Immediately reaction in rates was moderate as avoiding the shutdown has been largely priced in by rates and equities investors. On recession probabilities, chart below shows that how global markets are seeing higher recession probability vs. pre-inauguration. Notably, equities has overshot credit markets recession expectation. We think this is likely due to the fact that we came in this year with an above-trend GDP growth and robust economic fundamentals, the current recession concerns arising from political uncertainty over fundamental deterioration. In addition, Nikos tells (here) us that “The recent US equity market correction appears to be more driven by equity quant fund position adjustments and less driven by fundamental or discretionary managers reassessing US recession risks.”

BY Doug Kass · Mar 14, 2025, 8:55 AM EDT

* About Warren and Berkshire....

BY Doug Kass · Mar 14, 2025, 8:45 AM EDT

There continues to be no shortage of chatter about the government-spend side of things, which is obviously significant. In his latest must-read report, Jared Woodard, Bank of America's Research Investment Committee head, writes that the U.S. has never been more government-dependent: It relies on government for 85% of job growth, 33% of all spending and -- worst of all -- 6%-7% budget deficits, all of which are at record highs (excluding crisis and war).

But it still seems to me the consumer side of the equation is not getting the attention it deserves. I'm talking about the consumer spend outside of the spending from government employees or related entities. Just the average Joe.

The rule of thumb is to never bet against the U.S. consumer, but if you did for the last few months, you would have been right. It might not have been Keynesian economics that did the trick post World War II, it may just have been that Americans felt great all of the sudden and had also underspent for about the prior 15 years coming out of the Great Depression, so there was a fair bit of catch up.

What if we are going through the opposite of that now? People just feel like garbage due to all the political toxicity, stress, and wars, on top of being overspent and over consumed? And the U.S. government doesn’t have a balance sheet left to deal with any of this.

I am not a huge believer in Keynesian economics. In fact, as opposed to separating out government spend from gross domestic product, one could even argue you could give it a negative number, given all of its unintended consequences.

This is a good article with regard to the history of government spend and its implications: https://www.zerohedge.com/economics/get-government-out-gdp. Even if you believe in Keynesian economics, however, it was never supposed to be this way. Government was meant to spend to plug the hole in bad times and then run a surplus in the good times. Not complicated. What we have now is far from that. Spend, spend, spend, and it has exploded since Covid.

Here are some more blurbs on the state of the U.S. consumer. A Wall Street Journal article from Tuesday and a snippet from Macro-Strategy. I would add Dick’s Sporting Goods to the list, they chunked it a few days ago too. It feels like there is just a broad slowing in consumer demand, for the time being at least:

The WSJ reports that U.S. consumer spending is declining across all income levels. Wage growth is also slowing across all income groups. The article says its not all about tariffs, but rather a broader sense of uncertainty as many have less hard cash on hand. Checking and savings deposits across all income levels have declined over the 12-month period through February and are getting closer to inflation-adjusted 2019 levels. Wage growth for all income groups has slowed over the past year, and inflation adjusted debt balances are starting to surpass pre-pandemic levels.

As highlighted in Absolute and Relative Growth and Decline, U.S. domestic money supply is still below its 2022 high, although it has been climbing marginally. All that we have seen over the last few years is that money that had already been created in 2020 and 2021 has realigned within the domestic and international economy and financial markets (velocity increasing), funding the U.S. deficit and asset price appreciation. That is now exhausted. The growth in the velocity of money has started to turn down. Without an increase in monetary growth from the present 3% – 4% level, nominal GDP growth – (MV = PT) - will disappoint.

BY Doug Kass · Mar 14, 2025, 8:00 AM EDT

Another one from Bramo (on the subject of credit spreads that I touched on during the week):

BY Doug Kass · Mar 14, 2025, 7:55 AM EDT

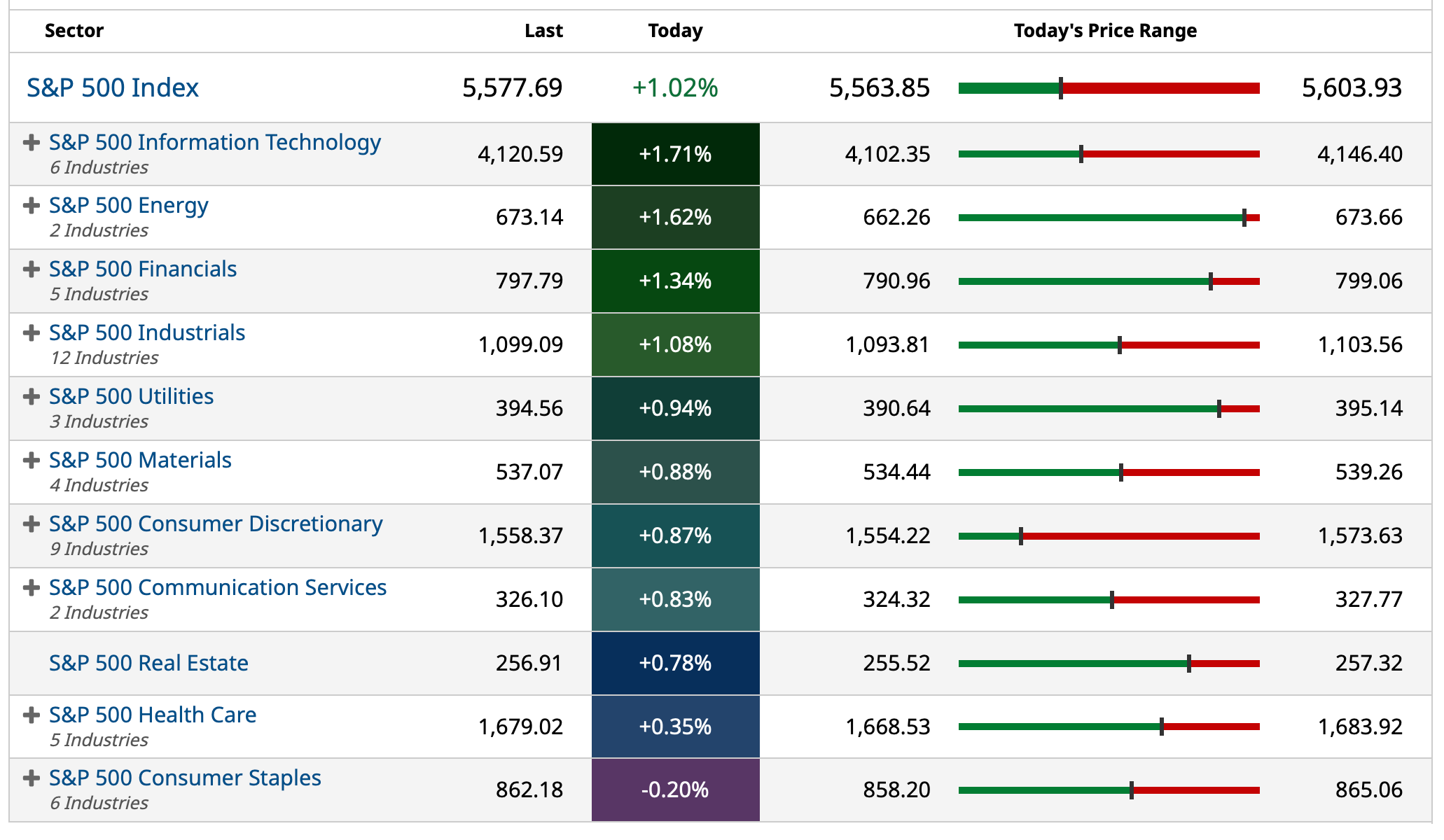

This table is a valuable resource for momentum-based short term traders:

BY Doug Kass · Mar 14, 2025, 7:50 AM EDT

"You will continue to suffer if you have an emotional reaction to everything that is said to you.

True power is sitting back and observing things with logic. True power is restraint. If words control you that means that everyone else can control you. Breathe and allow things to pass."

- Warren Buffett, The Oracle of Omaha

And from Keith McCullough, The Oracle of Stamford:

BY Doug Kass · Mar 14, 2025, 7:48 AM EDT

"What's this stuff? Some cereal.... Let's get Mikey, he won't eat it - he hates everything.

He likes it, hey Mikey!"

- Life Cereal TV Commercial Life Cereal Mikey Likes It Commercial HD - YouTube

BY Doug Kass · Mar 14, 2025, 7:45 AM EDT

BY Doug Kass · Mar 14, 2025, 7:41 AM EDT

* Again, for emphasis, see how negative the technicians have become - a possible bullish contrarian indicator!

"There's no fever like Gold fever."

- Richard Russell

Bonus - here are some great links:

Don't Fight the Trend Don't fight the trend 📉

Is The S&P In a Bear Market? 01 Arthur CreateASize Landscape - 15s

Selling in US Growth Continues Selling in US Growth Continues

Three Fonzis We're Gonna be like Three Little Fonzies Here

Can The Luck of the Irish Change the Markets? Almanac Trader — Can Luck O’ the Irish Stem the Tide? S&P 500 Up 23...

BY Doug Kass · Mar 14, 2025, 7:32 AM EDT

BY Doug Kass · Mar 14, 2025, 7:25 AM EDT

* Bramo and McDonald...

BY Doug Kass · Mar 14, 2025, 7:14 AM EDT

In my recent market update I wrote that 2025 will look very different than 2024:

BY Doug Kass · Mar 14, 2025, 6:55 AM EDT

From Jazzy Jeff Hirsch:

Almanac Trader — Can Luck O’ the Irish Stem the Tide? S&P 500 Up 23...

BY Doug Kass · Mar 14, 2025, 6:45 AM EDT

BY Doug Kass · Mar 14, 2025, 6:35 AM EDT

BY Doug Kass · Mar 14, 2025, 6:25 AM EDT

From Wally:

BY Doug Kass · Mar 14, 2025, 6:15 AM EDT

I continue to grow (tactically) more bullish based on sentiment and my assessment of reward vs. risk in individual stocks after the fall.

The S&P Short Range Oscillator moved to a greater oversold (confirming above) from -6.0% to -6.5%.

BY Doug Kass · Mar 14, 2025, 6:05 AM EDT

Wolf Street howls about cash not being trash.

BY Doug Kass · Mar 14, 2025, 5:55 AM EDT

BY Doug Kass · Mar 14, 2025, 5:46 AM EDT