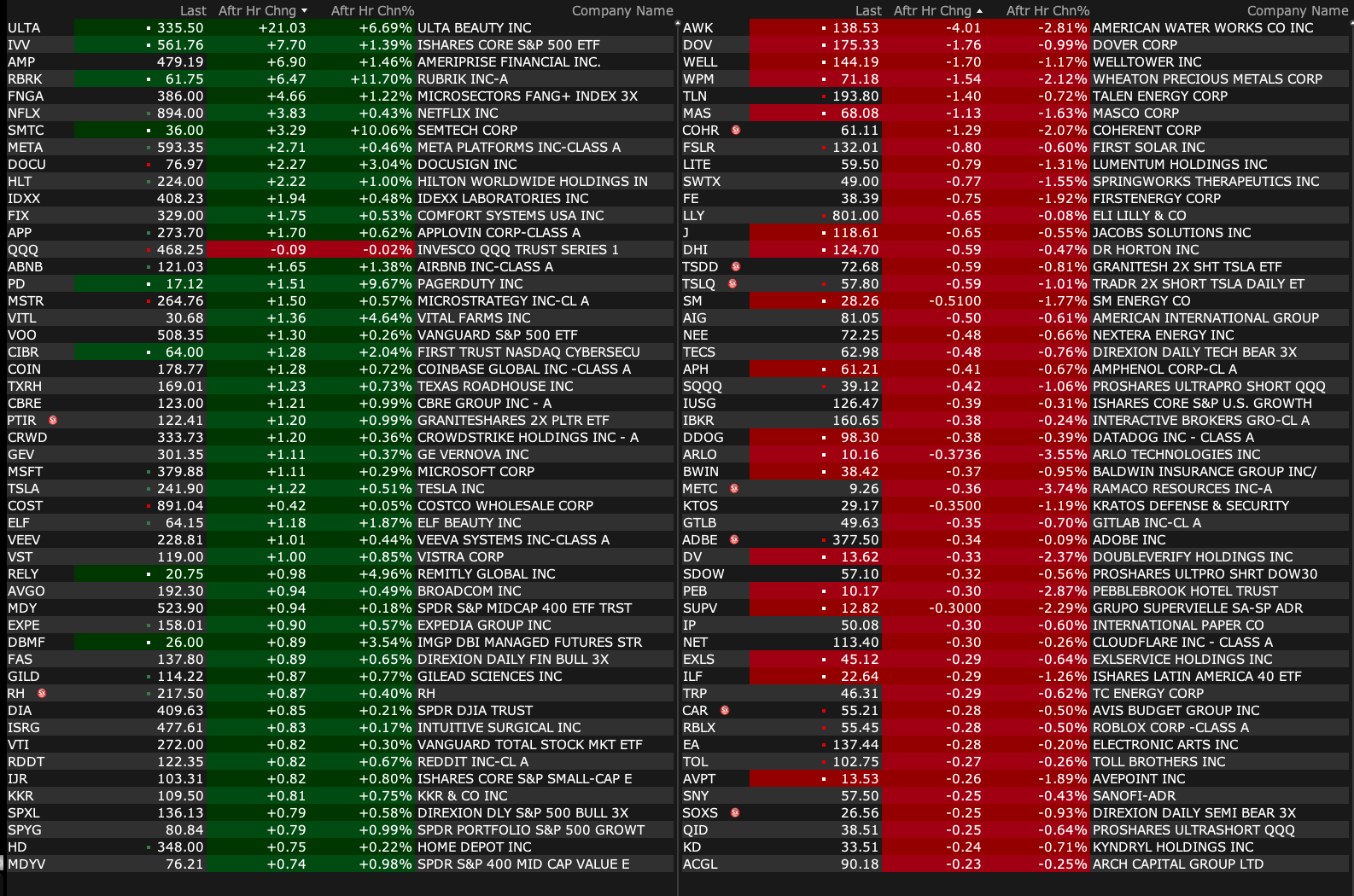

Thursday After-Hours Movers

At 4:26 p.m.:

BY Doug Kass · Mar 13, 2025, 4:42 PM EDT

At 4:26 p.m.:

BY Doug Kass · Mar 13, 2025, 4:42 PM EDT

BY Doug Kass · Mar 13, 2025, 4:37 PM EDT

* The Peter and Guy show...

BY Doug Kass · Mar 13, 2025, 3:09 PM EDT

I had tagends left in a winner, Freshpet FRPT after selling considerably higher.

I am back buying at $86.32.

From November 2024:

Freshpet (FRPT) is +$20 (off of the big EPS beat). Selling some more at $153.65. Down to tagends.

By Doug Kass Nov 4, 2024 2:47 PM EST

BY Doug Kass · Mar 13, 2025, 2:55 PM EDT

* Value is what you might be getting.,,

If you are looking for a sector that might rally hard into an up move, check out the charts of KKR, BX and APO.

I was previously short private equity at much higher levels.

I initiated trading long rentals in KKR at $108.18, BX at $136.10 and APO at $129.11.

BY Doug Kass · Mar 13, 2025, 2:18 PM EDT

I have aggressively bought the whoosh.

BY Doug Kass · Mar 13, 2025, 2:14 PM EDT

The decline is accelerating, with S&P cash now -85 handles.

I was fearful of market structure issues — and now with the momentum reversed — we are seeing the reprecussions when everyone is on the same side of the boat.

I am continuing to buy financials and selected technology.

BY Doug Kass · Mar 13, 2025, 1:28 PM EDT

BY Doug Kass · Mar 13, 2025, 12:15 PM EDT

MRKT CALL started at 11 a.m. with Guy and Dan.

I consider this podcast as a must view daily as the conversation is very real and full of substance. Dan often provides some interesting options ideas and Guy is just damn entertaining. And, unlike many, they take ownership of their mistakes.

Did I mention its free?

Let's go to the tape. Is It Finally Time To Buy The Mag7 Stocks? - YouTube

I just got a shout out from the boyz!

BY Doug Kass · Mar 13, 2025, 11:55 AM EDT

BY Doug Kass · Mar 13, 2025, 11:45 AM EDT

I have a board meeting at 4 p.m. today that I have to drive to.

I will be leaving at around 3 p.m. today.

BY Doug Kass · Mar 13, 2025, 11:35 AM EDT

BY Doug Kass · Mar 13, 2025, 11:25 AM EDT

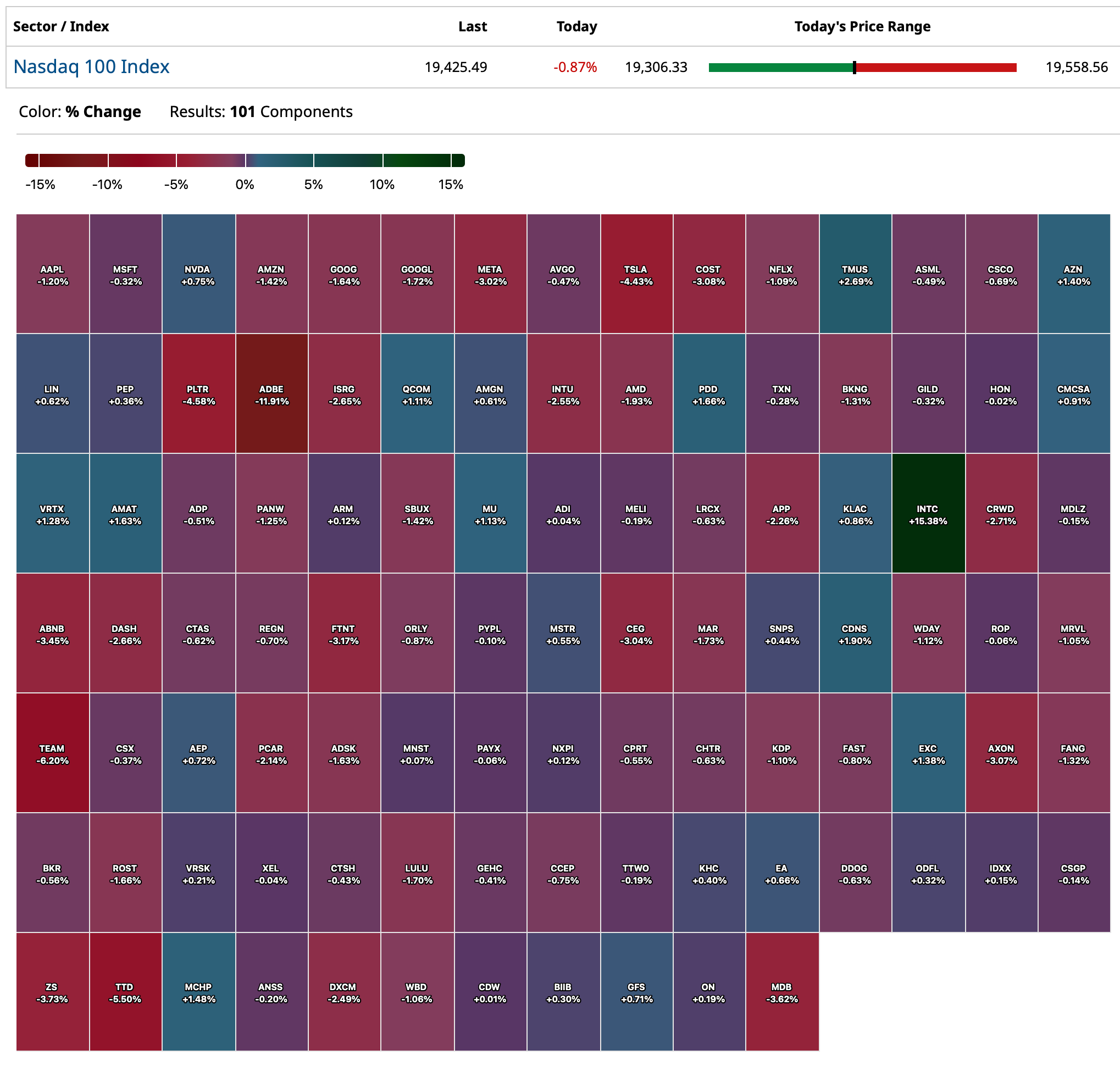

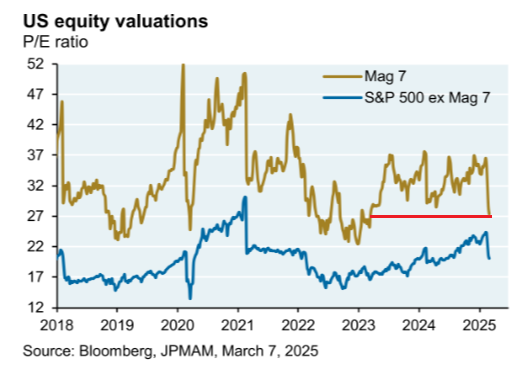

Very quickly Mag 7 becomes interesting on a valuation basis:

BY Doug Kass · Mar 13, 2025, 11:10 AM EDT

Here are this morning's "things":

* Added to SPY $556.08 and QQQ $473.21

* Added to financials: GS $529.18 and JPM $226.20

* Added to technology: AMZN $196.34, GOOGL $164.18, META $601.51, MSFT $381.01

* Purchased more JOE $44.68 and TSNDF $0.46

BY Doug Kass · Mar 13, 2025, 10:17 AM EDT

BY Doug Kass · Mar 13, 2025, 10:05 AM EDT

BY Doug Kass · Mar 13, 2025, 9:55 AM EDT

From Peter Boockvar:

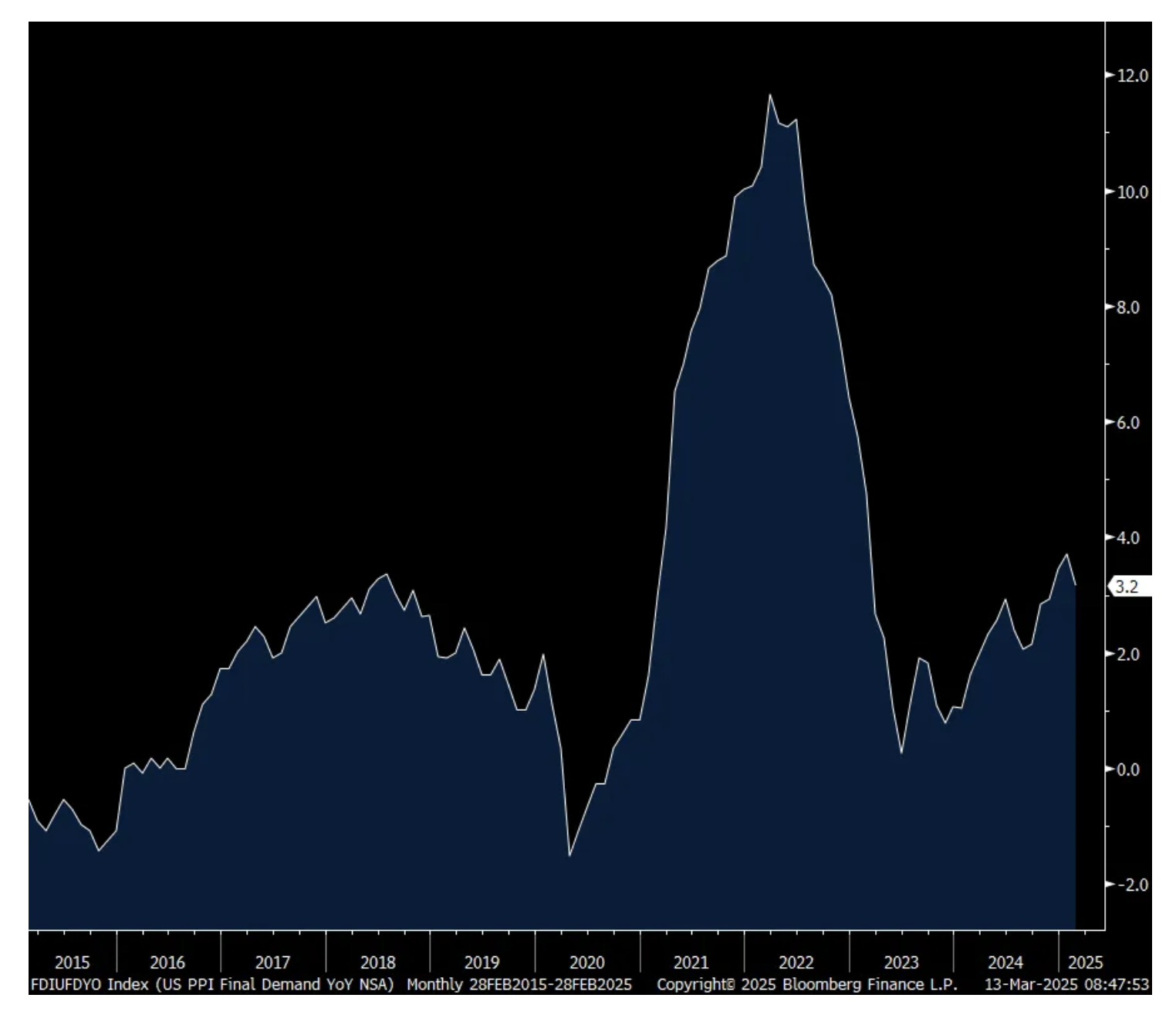

The February PPI was unchanged. That was well below the estimate of a .3% increase but mostly offset by a two tenths upward revision to January to a .6% gain from .4% initially. The core rate was lower by one tenth m/o/m vs the estimate of up .3%, partly mitigated by also a two tenths upward revision to January to up .5%. Versus last year, headline PPI is still up 3.2% y/o/y vs 3.7% in the month before. The core rate is higher by 3.4% vs 3.8% in January.

The drag on the headline figure was the 1.2% drop in energy prices and which are down 3.7% y/o/y. Food prices though were higher by 1.7% m/o/m and by 5.9% y/o/y, in part due to higher egg prices, up 54% y/o/y. Goods prices ex food and energy were up by .4% m/o/m and continuing to point to a bottoming in goods prices. They are up now 2.1% y/o/y and this is before the tariffs and the recent jump in commodity prices.

Services were also a drag on inflation, particularly at the core and that was because of a 1% fall in the ‘trade’ category. The BLS said “Over 40% of the February decline in prices for final demand services is attributable to margins for machinery and vehicle wholesaling, which decreased 1.4%.” Prices also fell for food/alcohol retailing, autos/parts retailing, apparel/footwear/accessories retailing, chemicals, residential real estate loans (likely due to lower mortgage rates). On the other hand, healthcare costs rose, particularly for ‘inpatient care’ and ‘hospital outpatient care.’

Bottom line, markets are extrapolating out the components here that plug into the PCE and the healthcare pieces all saw gains and likely explains why Treasury yields are slightly higher post PPI release. Also, we know this data is pre tariff implementation and the 2% rise in the CRB raw materials index over the past 2 weeks and by 5.6% year to date. Inflation breakevens are unchanged after the jump yesterday.

The inflation outlook is getting more and more complicated. We have reasons to expect further deceleration, particularly on the rent side and other consumer facing product lines as demand seems squishy but seemingly persistent underlying cost pressures that producers might have to eat themselves though will try their best not to all alone.

Headline PPI y/o/y

BY Doug Kass · Mar 13, 2025, 9:45 AM EDT

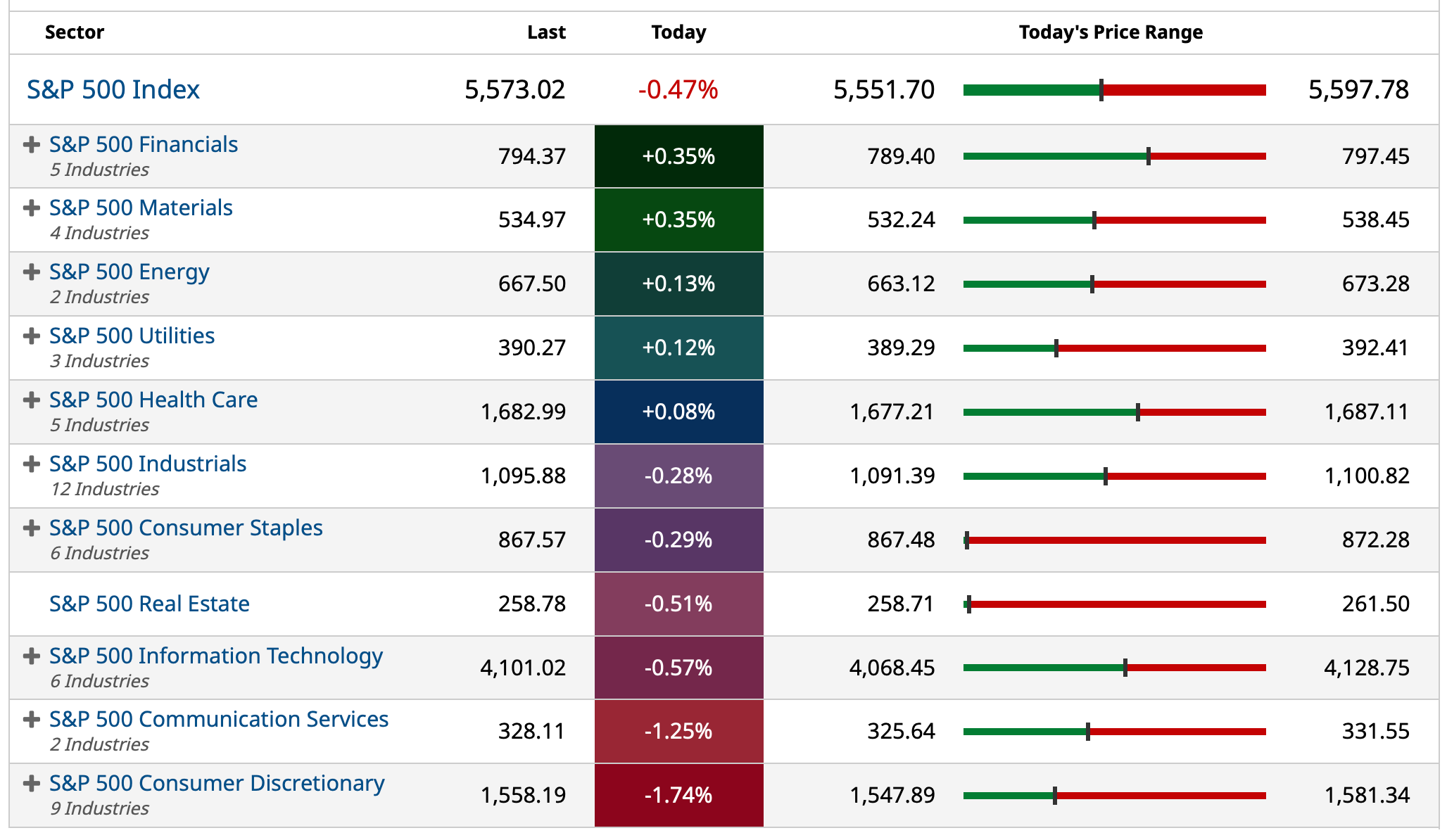

I'm adding to financials.

BY Doug Kass · Mar 13, 2025, 9:39 AM EDT

From Peter Boockvar:

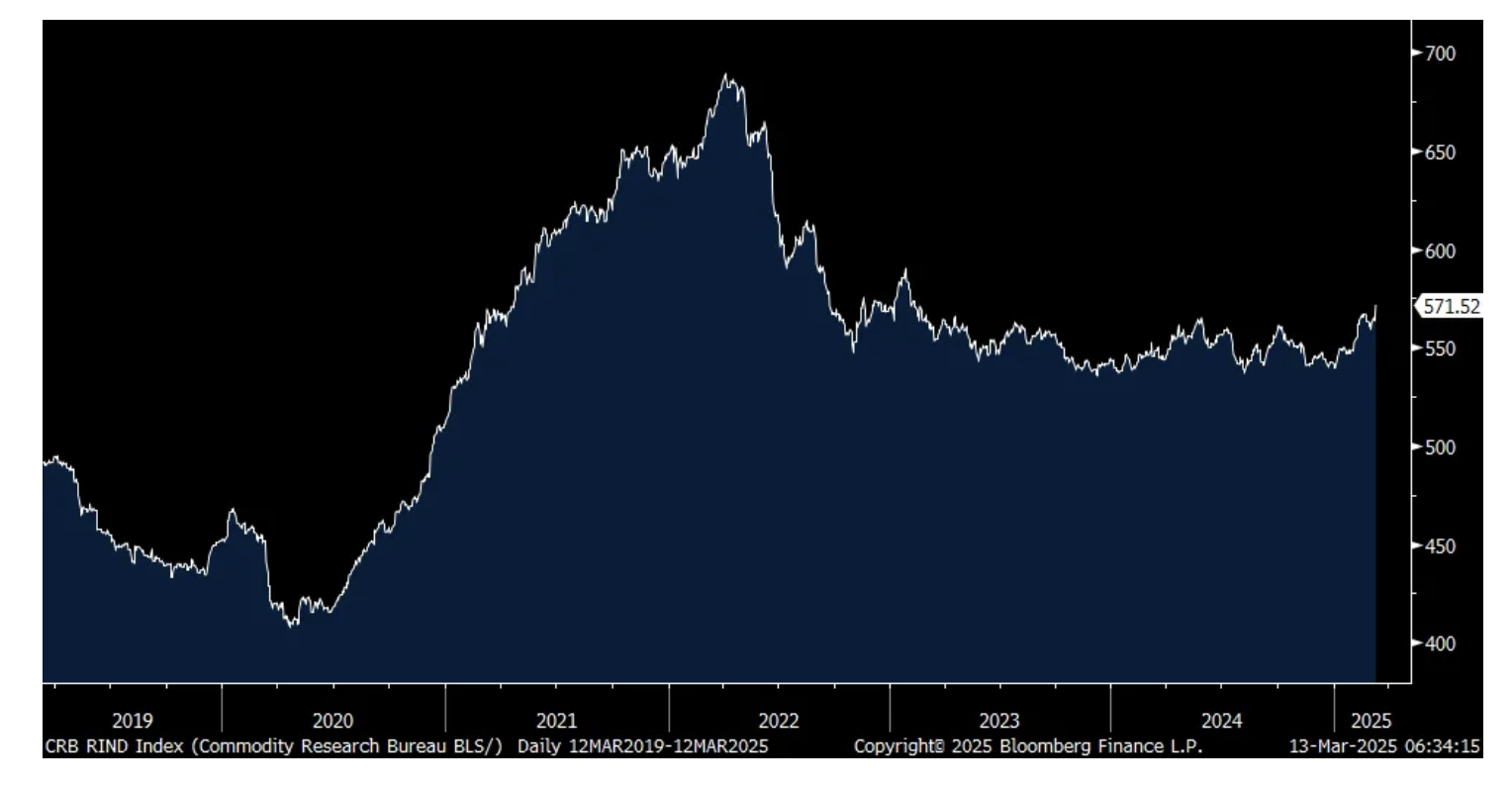

Post CPI and ahead of PPI, with the help of tariffs and the scramble to procure raw materials ahead of them, the CRB raw industrials index, what's a really bullish forming chart I showed yesterday, rose another 1% by days end to the highest level since February 2023. While still well off its highs of 2022, the direction is now up. We remain bullish and long commodities like gold, silver and platinum and commodity stocks in mining, oil/gas, uranium, and fertilizers.

Some of the 13 components in this index include everything from copper, steel scrap, tin, zinc, burlap, cotton and rubber.

CRB Raw Industrials index

Specifically with aluminum, Alcoa said this yesterday at a conference:

"We do see the tariffs creating uncertainty with our customers right now. Some customers are rushing to secure supply ahead of the tariffs, while others are playing wait and see, to see how the final tariff structure will exist. As a result, this quarter, we do have more uncertainty in both our revenue and our working capital that is more than normal. Overall though, we're expecting a very strong first quarter."

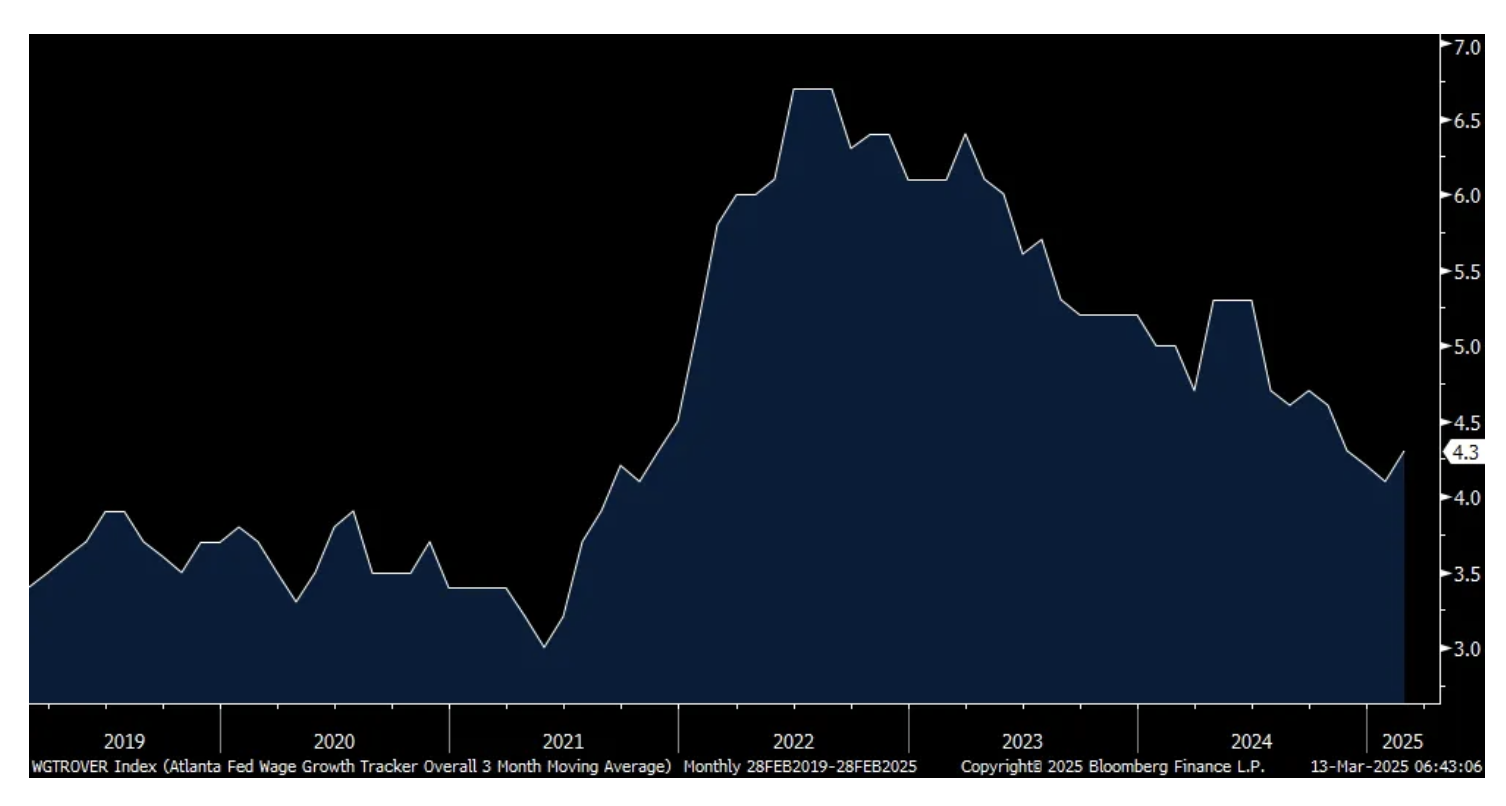

Meanwhile, wage growth remains pretty good as the Atlanta Fed released its February wage growth tracker which rose 4.3% y/o/y vs 4.1% in January, 4.2% in December and 4.3% in November. For a 'job switcher', wages were higher by 4.8%, the same pace seen in January. For a 'job stayer', they accelerated to 4.4% growth vs 4.1% in the three prior months.

Bottom line, as seen in the chart below, there has definitely been a deceleration in the pace of wage growth, though part of this is tougher comps. For perspective, wage growth pre-Covid was in the 3.5-4% range.

Atlanta Wage Growth Tracker

Here was the bottom line for why the Bank of Canada cut its base rate by another 25 bps to 2.75% as expected yesterday. "While economic growth has come in stronger than expected, the pervasive uncertainty created by continuously changing US tariff threats is restraining consumers' spending intentions and businesses' plans to hire and invest. Against this background, and with inflation close to the 2% target, Governing Council decided to reduce the policy rate by a further 25 bps."

They also said this, which is revealing too ahead of the Fed meeting next week. "Monetary policy cannot offset the impact of a trade war. What it can and must do is ensure that higher prices do not lead to ongoing inflation."

From Vivid Seats, the ticket reseller, highlighting the strength of live events:

They mentioned the "long term secular growth trends in live events...Additionally, we are seeing that consumers increasingly prioritize spending on live experiences over goods, and artists touring more and more. While 2024 saw muted growth relative to the record setting growth seen in 2022 and 2023, 2025 looks to potentially return to industry expansion consistent with its long term trajectory."

From American Eagle Outfitters:

"2025 has started off softer than anticipated. First quarter to date sales have been impacted by a less robust consumer environment and cold weather. For the year, ongoing consumer uncertainty and changes in the operating landscape, including tariffs and a strengthening US dollar, are also creating factors for us to navigate. Against this backdrop, we currently expect full year revenue and operating income to be down relative to last year."

From Dollar General who just reported:

They guided to a comp gain range that was in line with current estimates. In the quarter, they saw "growth in the consumables category, partially offset by declines in each of the seasonal, home products, and apparel categories." In other words, consumers spent more on needs, less on wants.

This was from MMM on Tuesday at a JPM conference that I though was worth mentioning:

"So as we went through February, we saw good order trends continuing right up until the end of February. In fact, the February month was up y/o/y in terms of orders really across the businesses. Our backlog from end of January from the beginning of the year and through February continues to build...So we're seeing good order patterns."

However, "But what we're seeing now is a bit of more of an elongation in the sell-out. So, a lot of the orders are coming in more for sales into the 2nd quarter." They anticipated some challenges this year and tightened up cost controls "So while we're seeing our sales be a little bit light in the quarter, our eps should be slightly better than what we previously expected."

To the question of whether the good January and February orders were more influenced by ordering ahead of expected tariffs, "It could be that for sure. We've signaled that. We've talked to people that as tariffs start to take hold...So, there's a lot of concern on the horizon about tariffs. And people like us are talking about what we're going to do in terms of pricing. And we've signaled that to distributors. So there could be some pre-buy that's happening. I'm not sure that's the primary driver. I do believe it's just general caution across our consumer base in placing orders, given what might be happening in the macro."

Shifting to stock market sentiment, a few weeks ago we saw the big jump in Bears and the plummet in the number of Bulls as surveyed by the AAII index. Yesterday, and for a 2nd week, the Investors Intelligence survey has gotten pretty bearish too. Bulls fell to just 27.6% from 36.7% in the prior week and 44.3% in the week before that. Bears jumped to 34.5% from 28.3% last week and vs 24.6% in the week prior. Today's AAII update has the Bulls at 19.1, down .2 pts and Bears at 59.2, up by 2.1 pts (after falling by 3.5 pts last week and jumping by 20 pts in the week before that). The CNN Fear/Greed at 21 has lifted over the past week from 17 one week ago but it's still in the 'Extreme Fear' category.

Bottom line, sentiment has us set up perfectly for a tradable rally so it better happen or else some bigger worries are taking over.

BY Doug Kass · Mar 13, 2025, 9:35 AM EDT

Added to GOOGL on the opening ($167.49).

BY Doug Kass · Mar 13, 2025, 9:35 AM EDT

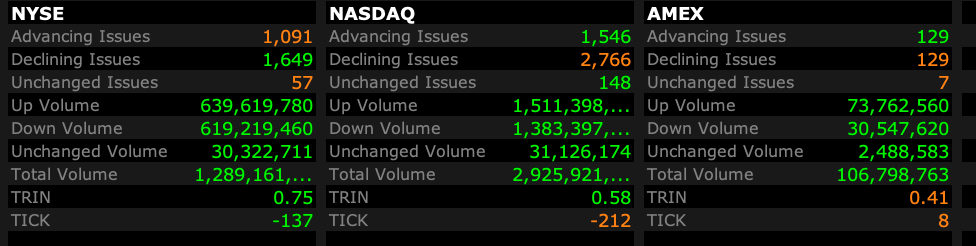

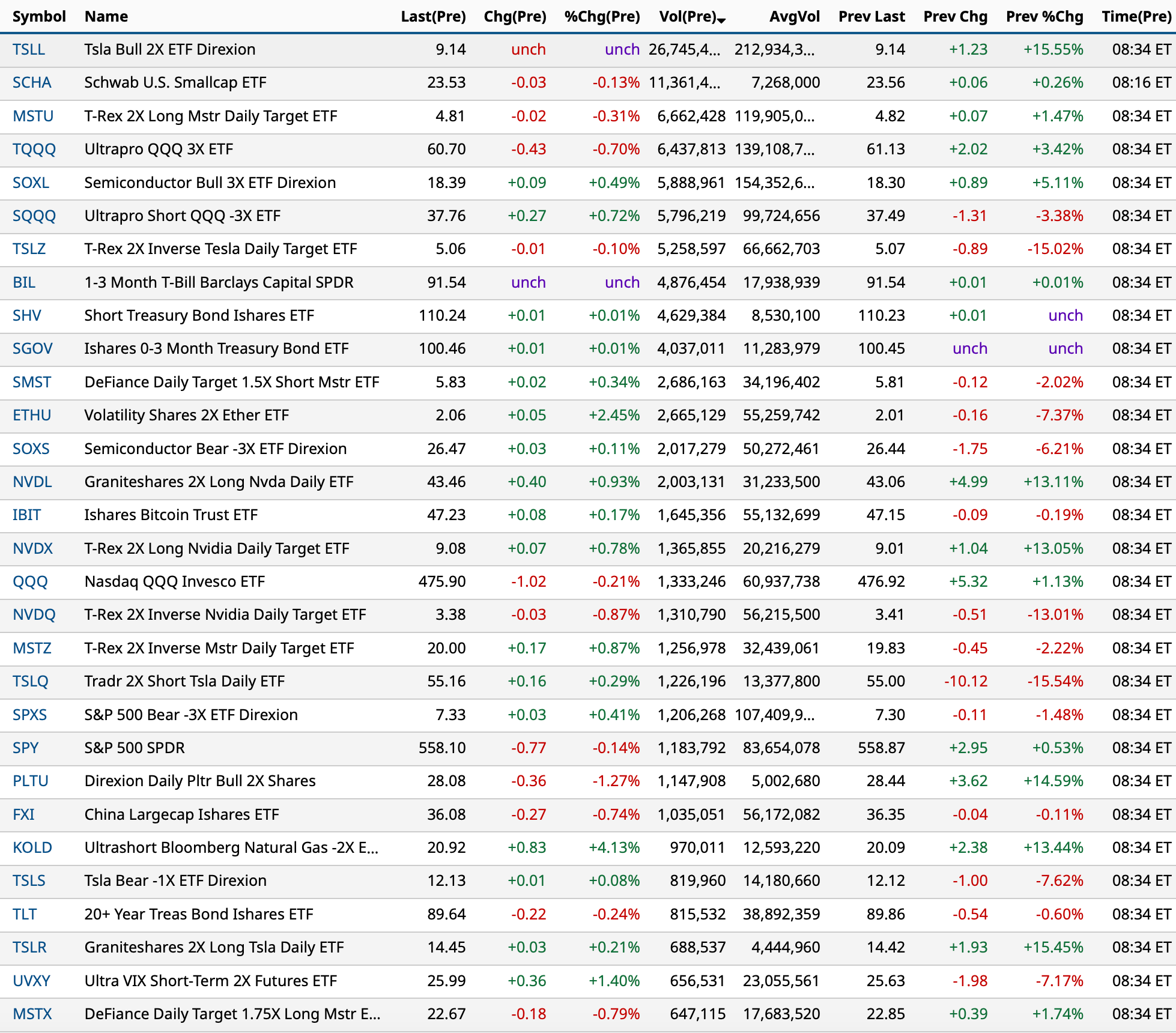

Most Active premarket exchange-traded funds as of 8:34 a.m.:

BY Doug Kass · Mar 13, 2025, 9:23 AM EDT

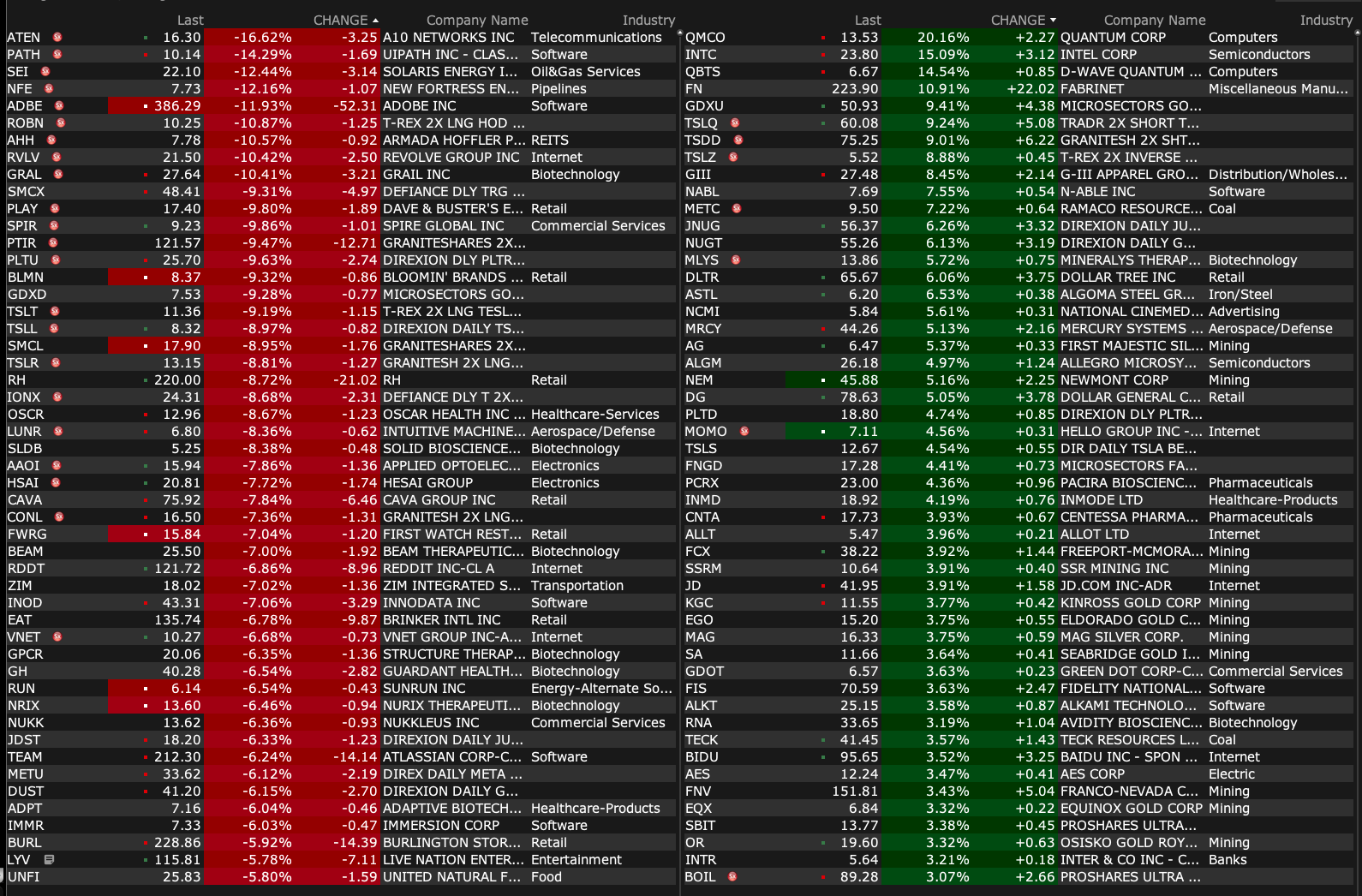

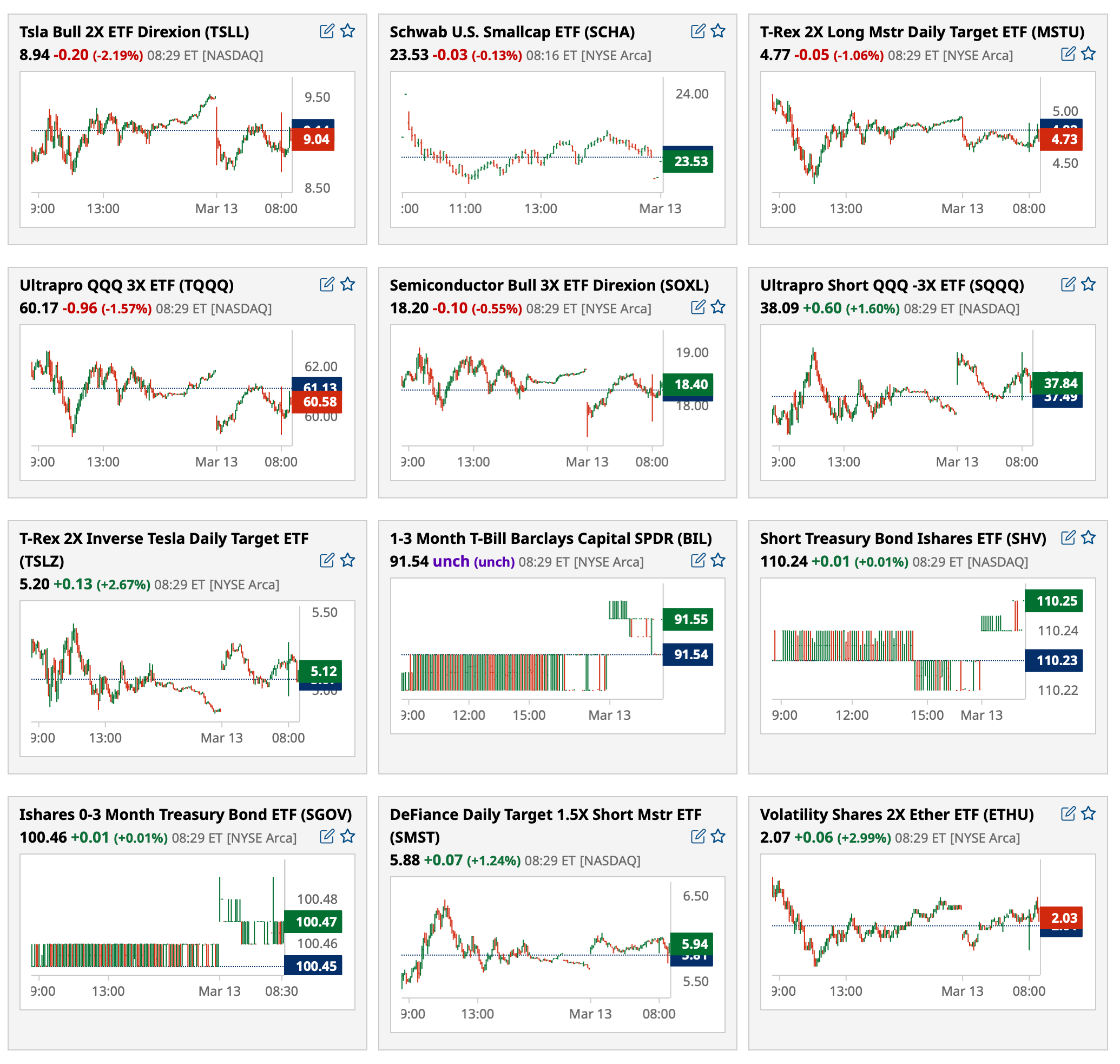

Premarket percentage movers chart from 8:50 a.m. ET:

BY Doug Kass · Mar 13, 2025, 9:12 AM EDT

-CRVO +22% (Chardan Capital Markets Raised CRVO to Buy from Neutral, price target: $14)

-MGTX +18% (earnings; to receive $200M in upfront cash consideration; enters strategic collaboration with Hologen AI to expedite Phase 3 development of AAV-GAD for Parkinson’s Disease and industrialize Proprietary Manufacturing Process)

-AVAH +17% (earnings, guidance)

-INTC +11% (appoints Lip-Bu Tan as Chief Executive Officer, effective immediately; Tier1 firm Raised INTC to Neutral from Underperform, price target: $25 from $19)

-FN +10% (warrant issue to Amazon to acquire up to ~381.9K ordinary shares; cuts Q3 guidance)

-GIII +10% (earnings, guidance)

-BBW +8.8% (earnings, guidance)

-DG +7.9% (earnings, guidance)

-BRLT +7.0% (earnings, guidance)

-EBS +4.1% (reinforces commitment to expanding access to NARCAN Nasal Spray by supporting organizations with New Opioid Overdose Preparedness Programs)

-RBOT +3.4% (appoints Sarah Romano as CFO, effective Apr 1st)

-NABL +2.7% (guidance ahead of Investor Day)

-ADTX -28% (1-for-250 reverse stock split)

-ULY -22% (earnings; announces 1-for-12 reverse stock split)

-PATH -19% (earnings, guidance; announced the acquisition of Peak, an AI-native company)

-NOVA -16% (said to prepare restructuring talks that could include bankruptcy filing; hearing CitiGroup Cuts NOVA to Neutral from Buy)

-S -14% (earnings, guidance)

-CMTL -13% (earnings)

-ATEN -11% (prices offering of $200M of 2.75% convertible senior notes due 2030)

-BTMD -11% (earnings, guidance)

-AEO -9.4% (earnings, guidance)

-PCAR -6.3% (weakness off vehicle emissions rule reversal)

-ADBE -6.2% (earnings, guidance)

-CMI -3.2% (weakness off vehicle emissions rule reversal)

BY Doug Kass · Mar 13, 2025, 9:00 AM EDT

BY Doug Kass · Mar 13, 2025, 8:55 AM EDT

On the cooler inflation number I added to my Index longs:

* SPY $557.58

* QQQ $475.43.

BY Doug Kass · Mar 13, 2025, 8:43 AM EDT

BY Doug Kass · Mar 13, 2025, 8:40 AM EDT

My old professor, Dr. Thomas Kuhn Thomas Kuhn - Wikipedia (author of "The Structure of Scientific Revolutions" would be proud:

BY Doug Kass · Mar 13, 2025, 8:35 AM EDT

BY Doug Kass · Mar 13, 2025, 8:23 AM EDT

BY Doug Kass · Mar 13, 2025, 8:10 AM EDT

From October 2024:

I Call BS to the 'Cash on the Sidelines' Argument (Part Trois)

BY Doug Kass · Mar 13, 2025, 8:00 AM EDT

BY Doug Kass · Mar 13, 2025, 7:50 AM EDT

BY Doug Kass · Mar 13, 2025, 7:40 AM EDT

* In three weeks technicians go from giddy to woe is me.

* Call it the "rear view mirror"...

Bonus — Here are some great links:

BY Doug Kass · Mar 13, 2025, 7:25 AM EDT

We have an oversold S&P Oscillator, a low RSI consistent with previous market bottoms, S&P stocks vs. moving average at similar bear market lows, CNN Fear & Greed in "Extreme Fear" and now this:

BY Doug Kass · Mar 13, 2025, 7:15 AM EDT

"Compounding is hard because a bad month can feel longer than a good decade."

- Morgan Housel

BY Doug Kass · Mar 13, 2025, 7:05 AM EDT

This is a valuable chart for momentum-based short-term traders:

BY Doug Kass · Mar 13, 2025, 6:55 AM EDT

BY Doug Kass · Mar 13, 2025, 6:45 AM EDT

Charlie Munger:

BY Doug Kass · Mar 13, 2025, 6:35 AM EDT

From JPMorgan:

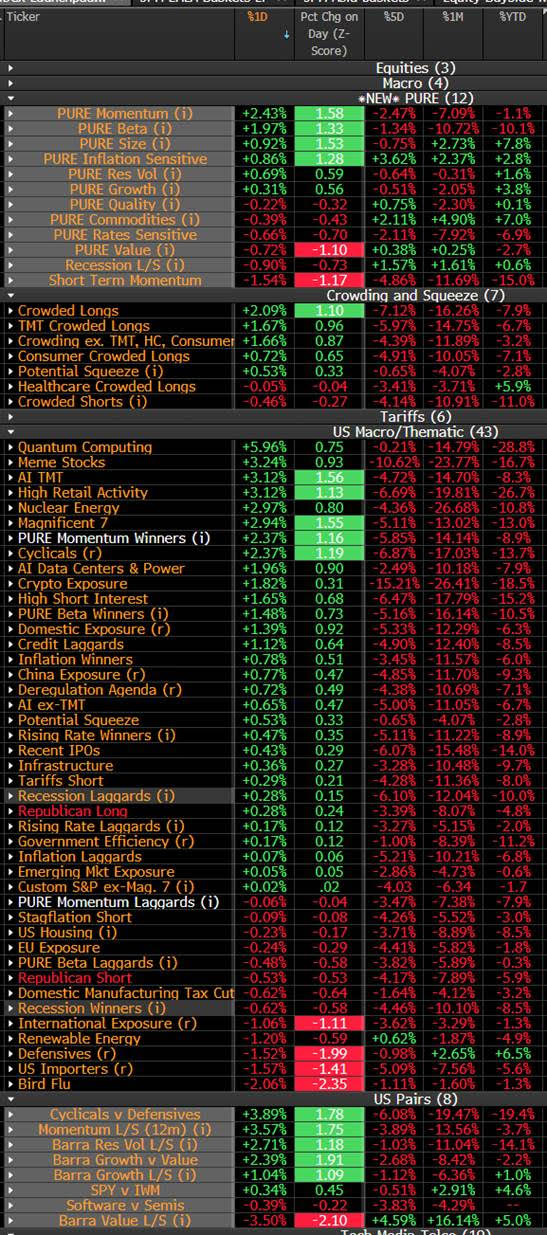

US: Stocks closed higher led by Tech. We saw a short relief rally post dovish CPI print, which helped ease some stagflation fears, but the bigger driver of this benign price action was the lack of geopolitical/tariffs headlines today. Overall, we saw the recent underperformers (cyclicals, Tech, Mag 7) staged a rally today. Thematically, Crowded Longs, AI TMT, Mag 7, and Cyclicals were the best performing baskets, while Defensives lagged.

and...

EQUITY AND MACRO NARRATIVE: Stocks finished higher, but off intraday highs, amid the dovish CPI surprise that helped ease some concerns on stagflation. Overall, the bigger contributor of today’s stable price action was the lack of major Trump/tariffs headlines: we still heard potential retaliatory tariffs from Europe and Canada, but the lack of Trump’s comments or further escalation (so far) helped stabilize prices in the afternoon session. On the reconciliation process, last night, the House passed a funding bill (to September 30) to avert the March 14 government shutdown with a largely party-line 217-213 vote. BBG headline (here) came out today suggests that Senate Dem leader Chuck Schumer and his party will block the GOP spending bill and urged the GOP to accept a Dem plan to provide 30 days of interim funding instead.

BY Doug Kass · Mar 13, 2025, 6:25 AM EDT

The S&P Short Range Oscillator grew slightly more oversold. It's now at -6.00% vs. -5.97%.

BY Doug Kass · Mar 13, 2025, 6:15 AM EDT

BY Doug Kass · Mar 13, 2025, 6:05 AM EDT

The percentage of S&P components above their moving averages joins the Oscillator, the CNN Fear & Greed gauge and RSI as being at important junctures:

BY Doug Kass · Mar 13, 2025, 5:55 AM EDT

S&P futures are -34 handles as I write this (430 a.m.).

Adding to my gross long exposure. Here are my early buys:

* SPY $555.95

* QQQ $473.51

* AMZN $197.34

* GOOGL $165.45

* MSFT $379.86

BY Doug Kass · Mar 13, 2025, 5:45 AM EDT