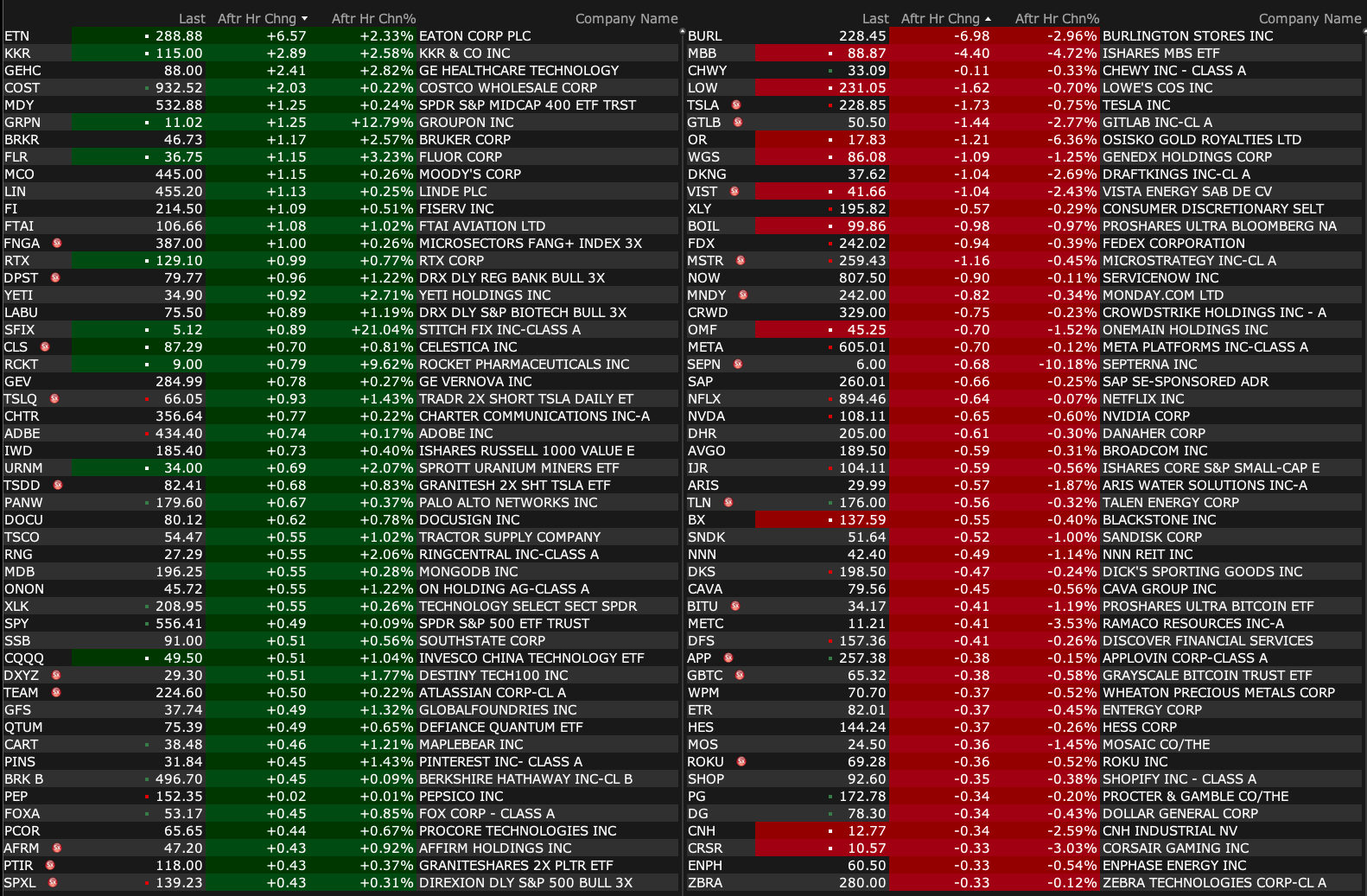

Tuesday's After-Hours Movers

At 4:26 p.m.:

BY Doug Kass · Mar 11, 2025, 5:00 PM EDT

At 4:26 p.m.:

BY Doug Kass · Mar 11, 2025, 5:00 PM EDT

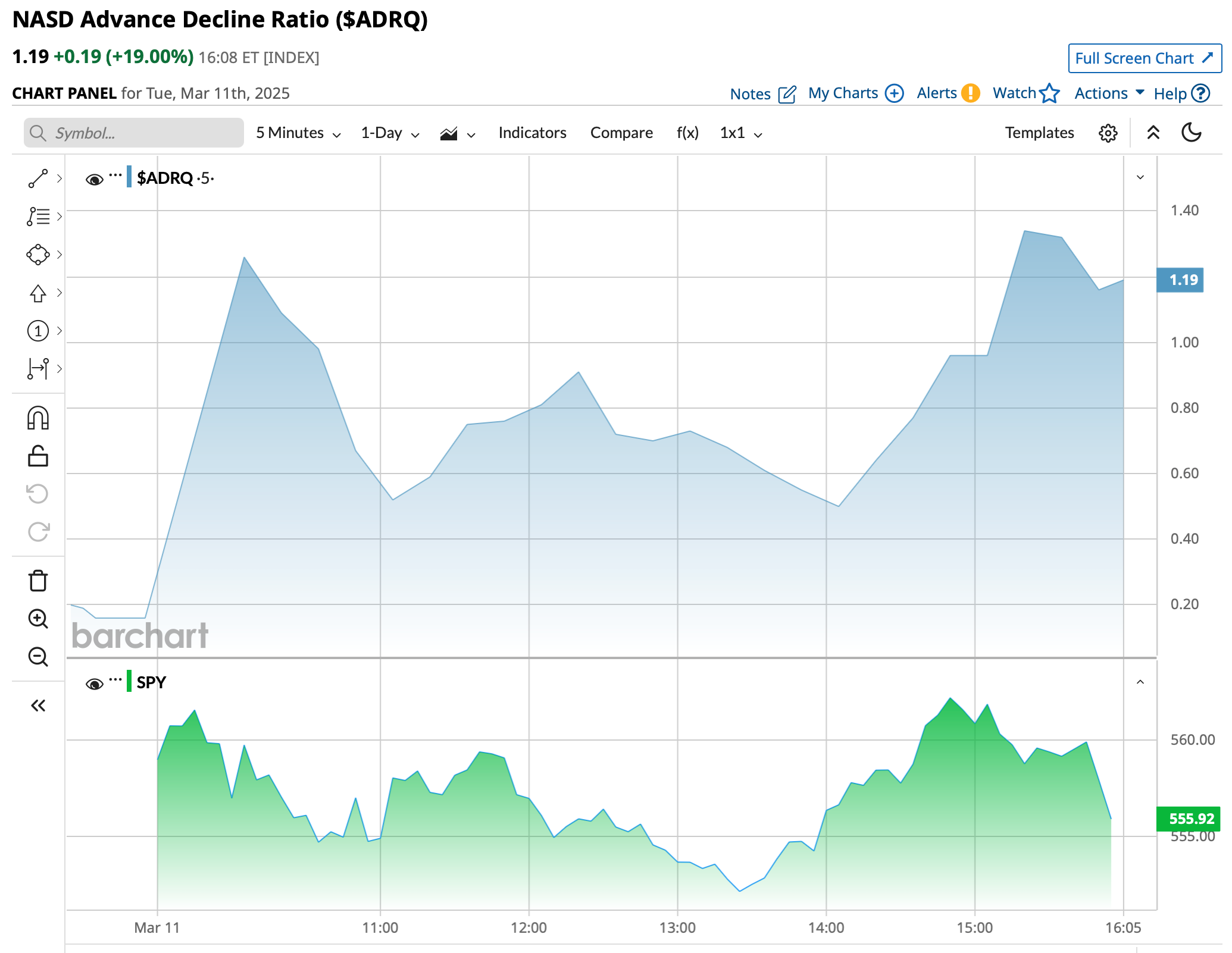

Through closing:

BY Doug Kass · Mar 11, 2025, 4:47 PM EDT

- NYSE volume 28% above its one-month average

- NASDAQ volume 7.85B shares, 16% above its one-month average

- VIX: down 3.37% to 26.92

BY Doug Kass · Mar 11, 2025, 4:38 PM EDT

BY Doug Kass · Mar 11, 2025, 3:44 PM EDT

BY Doug Kass · Mar 11, 2025, 3:20 PM EDT

Sixteen years ago I made my "Generational Bottom" call on CNBC's The Kudlow Report.

Here is a Wall Street Journal article that covered that call.... The Pros Who Called the '09 Bottom - WSJ

Here is Business Insider coverage of my call.. Kass Calls the Bottom - Business Insider

Interestingly, my friends at CNBC took down the video.

Here is my surprised face!

BY Doug Kass · Mar 11, 2025, 3:05 PM EDT

BY Doug Kass · Mar 11, 2025, 2:50 PM EDT

I am at the largest net long position since Q3 2023.

BY Doug Kass · Mar 11, 2025, 2:40 PM EDT

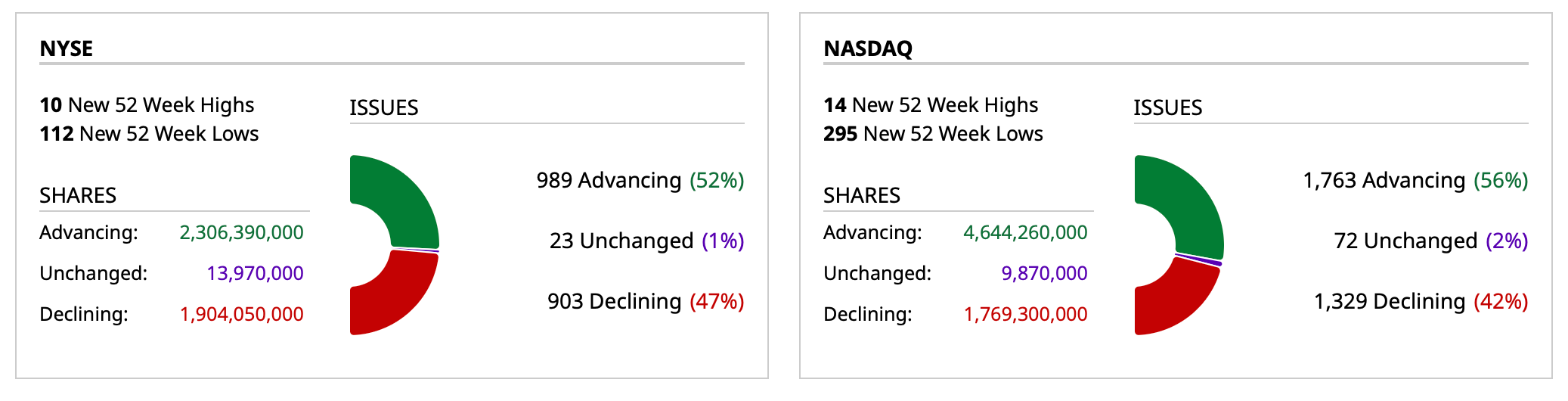

Another volatile day, with more moves than a short stop batting .110!

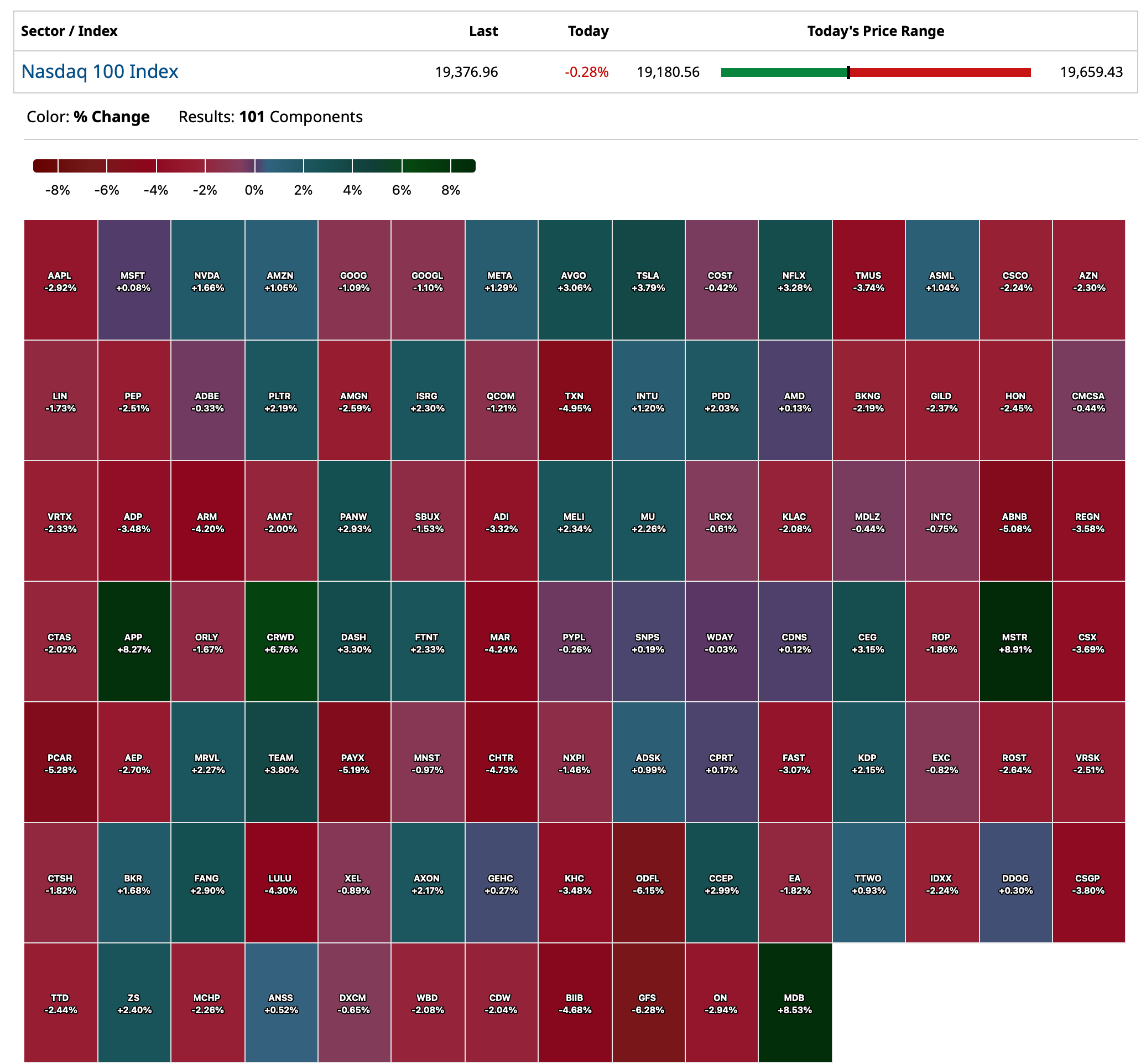

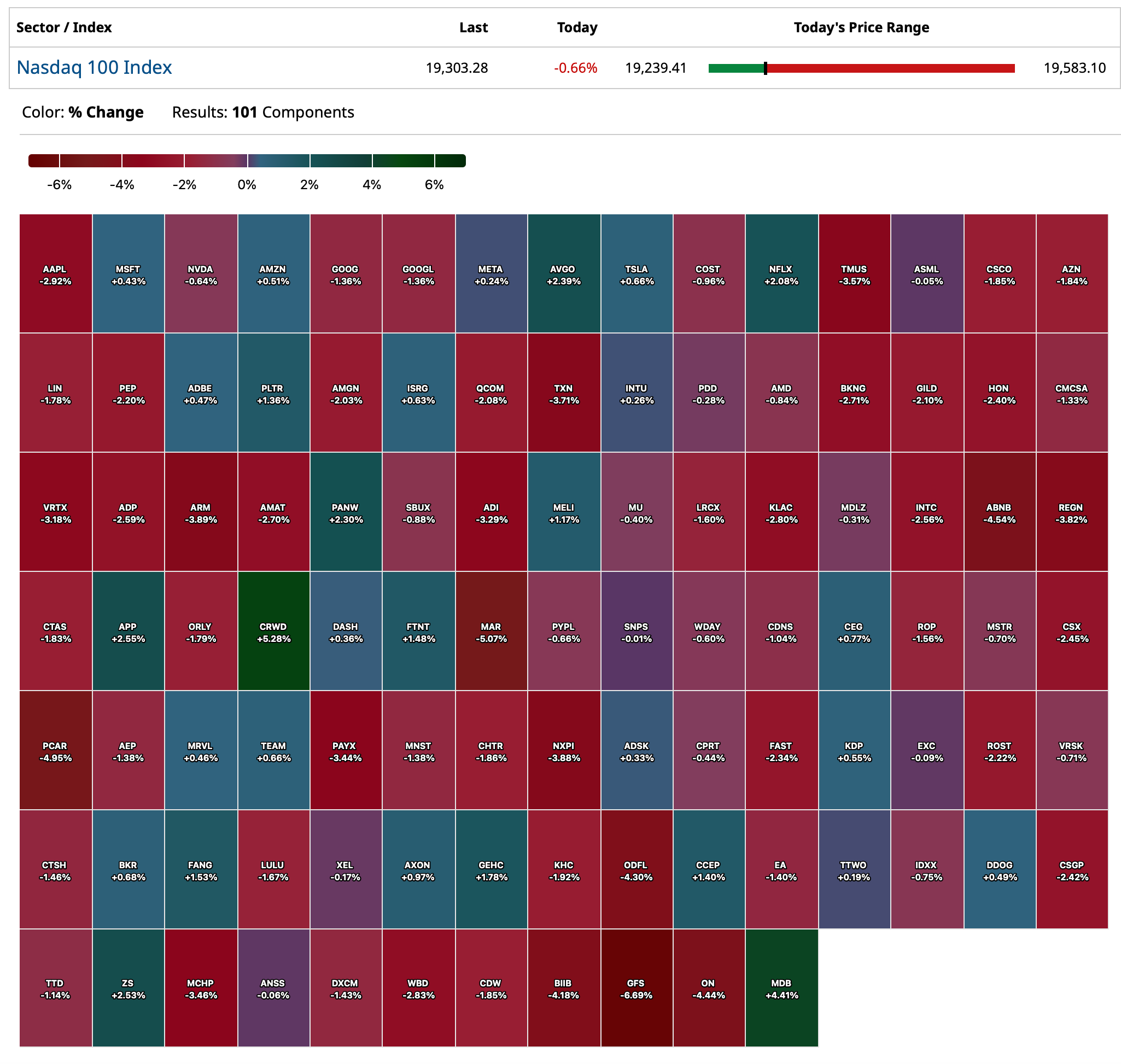

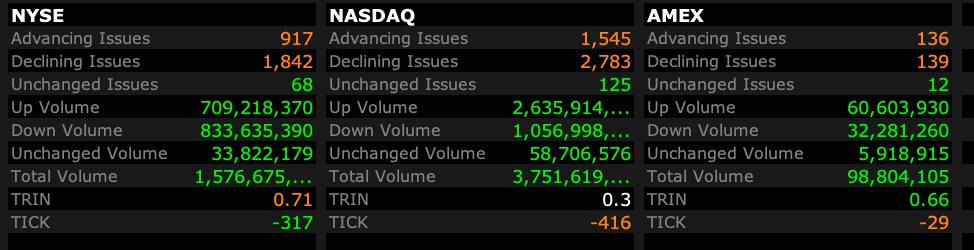

Market breadth is quite weak (2-1 negative on the NYSE, 1.5-1 negative on the Nasdaq):

At 2:15 p.m. the S&P Index is -32 handles (erasing 2/3 of the decline at the nadir only an hour or so ago!).

Here are today's "Things":

* Added to SPY at $556.86 and QQQ at $471.39 longs.

* Added to the following financial longs: AXP at $256.88, GS at $528.33, BAC at $39.44, JPM at $227.92, MS at $111.36 and WFC at $66.10.

* In technology we purchased more AMZN at $195.12, GOOGL at $163.02.

* Purchased more MSOS at $2.75.

* Covered much of my PEP short at $152.69.

BY Doug Kass · Mar 11, 2025, 2:30 PM EDT

BY Doug Kass · Mar 11, 2025, 2:03 PM EDT

BY Doug Kass · Mar 11, 2025, 1:39 PM EDT

From Charlie!

BY Doug Kass · Mar 11, 2025, 1:26 PM EDT

As of 12:44 p.m.:

BY Doug Kass · Mar 11, 2025, 1:05 PM EDT

I added to Amazon AMZN at $195.50.

BY Doug Kass · Mar 11, 2025, 12:57 PM EDT

BY Doug Kass · Mar 11, 2025, 12:52 PM EDT

Another index buy tranche:

* SPY $554.96

* QQQ $470.57

BY Doug Kass · Mar 11, 2025, 12:48 PM EDT

One feature of my market forecast that I felt fairly certain of has been the strong likelihood of rising volatility.

Let's walk through a vivid example.

Go to the SPY menu for the $558 straddle (calls/puts) that expire tomorrow.

Add the price of the call ($4.78) and the price of the put ($5.15) and divide by $558 (the exercise price) and you can see that the market is suggesting close to a two percent move in the next 1 1/2 trading sessions (by Wednesday's close)!

Now, that's vol!!

BY Doug Kass · Mar 11, 2025, 12:16 PM EDT

Cost basis of index longs today:

* SPY $557.83

* QQQ $471.93

BY Doug Kass · Mar 11, 2025, 11:39 AM EDT

BY Doug Kass · Mar 11, 2025, 11:35 AM EDT

I've added to GOOGL at $164.22.

BY Doug Kass · Mar 11, 2025, 11:31 AM EDT

From Peter Boockvar:

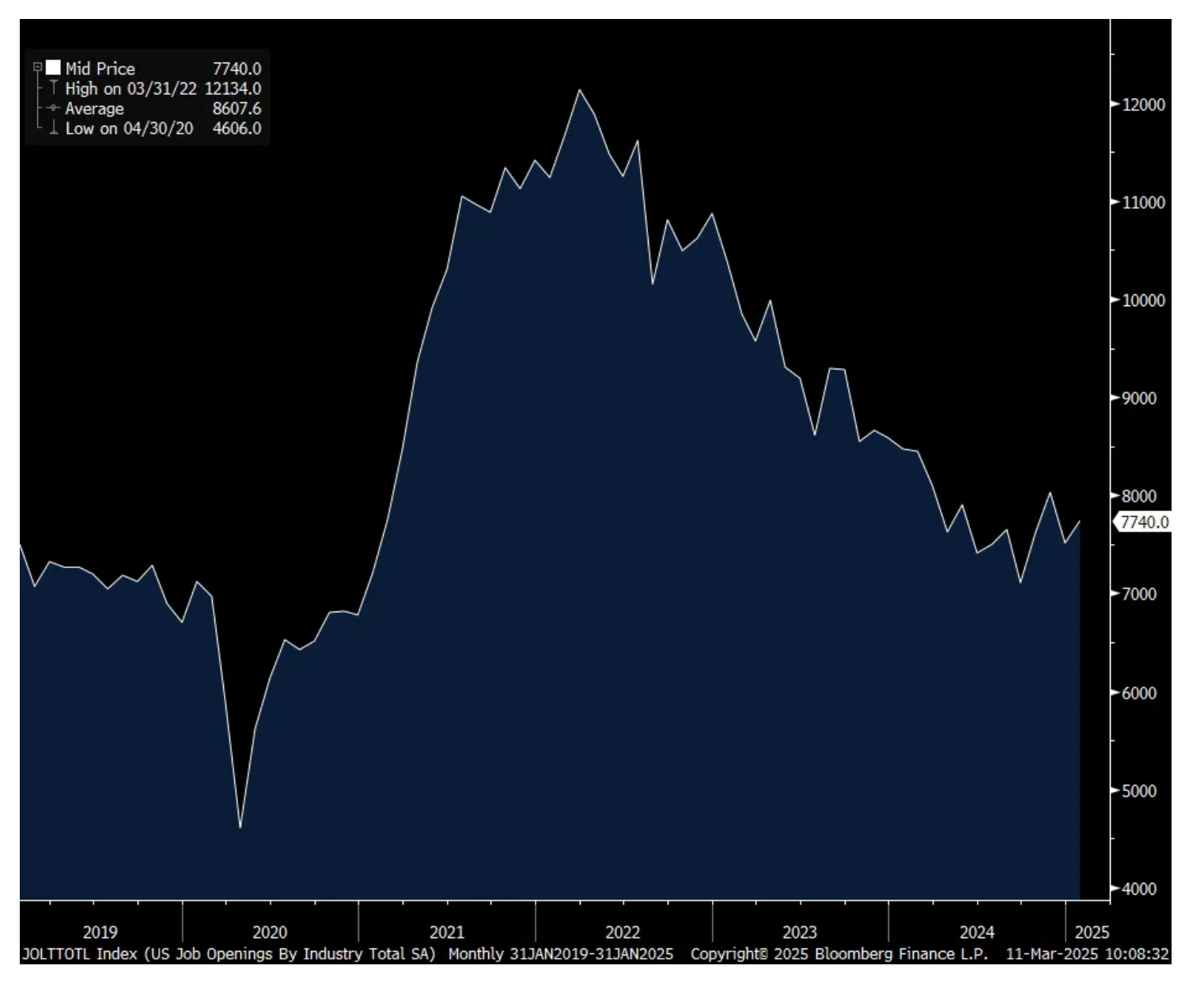

The number of job openings in January totaled 7.74mm, up from 7.51mm in December which was revised down by about 100k. This compares with 8.03mm in November and 7.62mm in October.

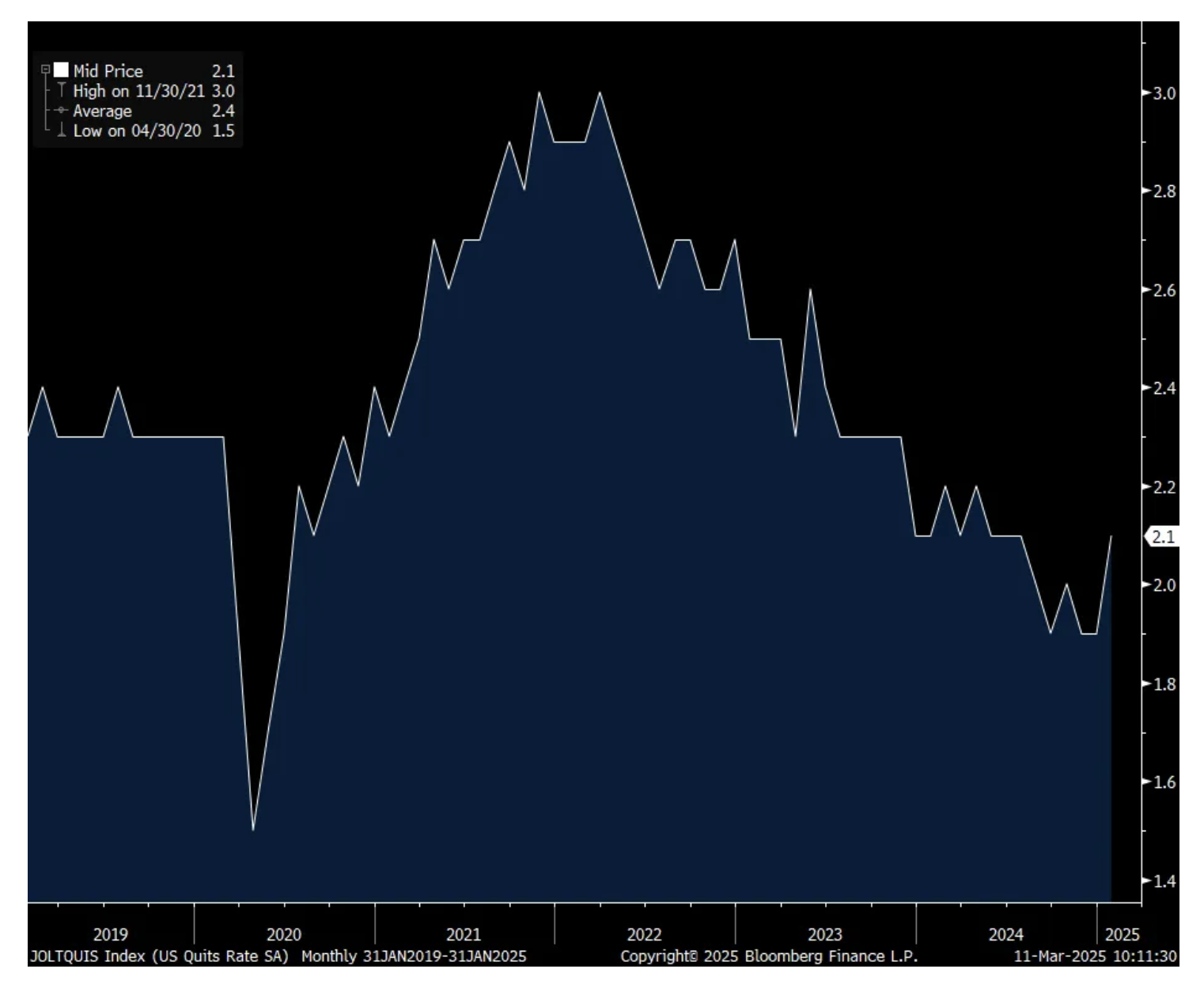

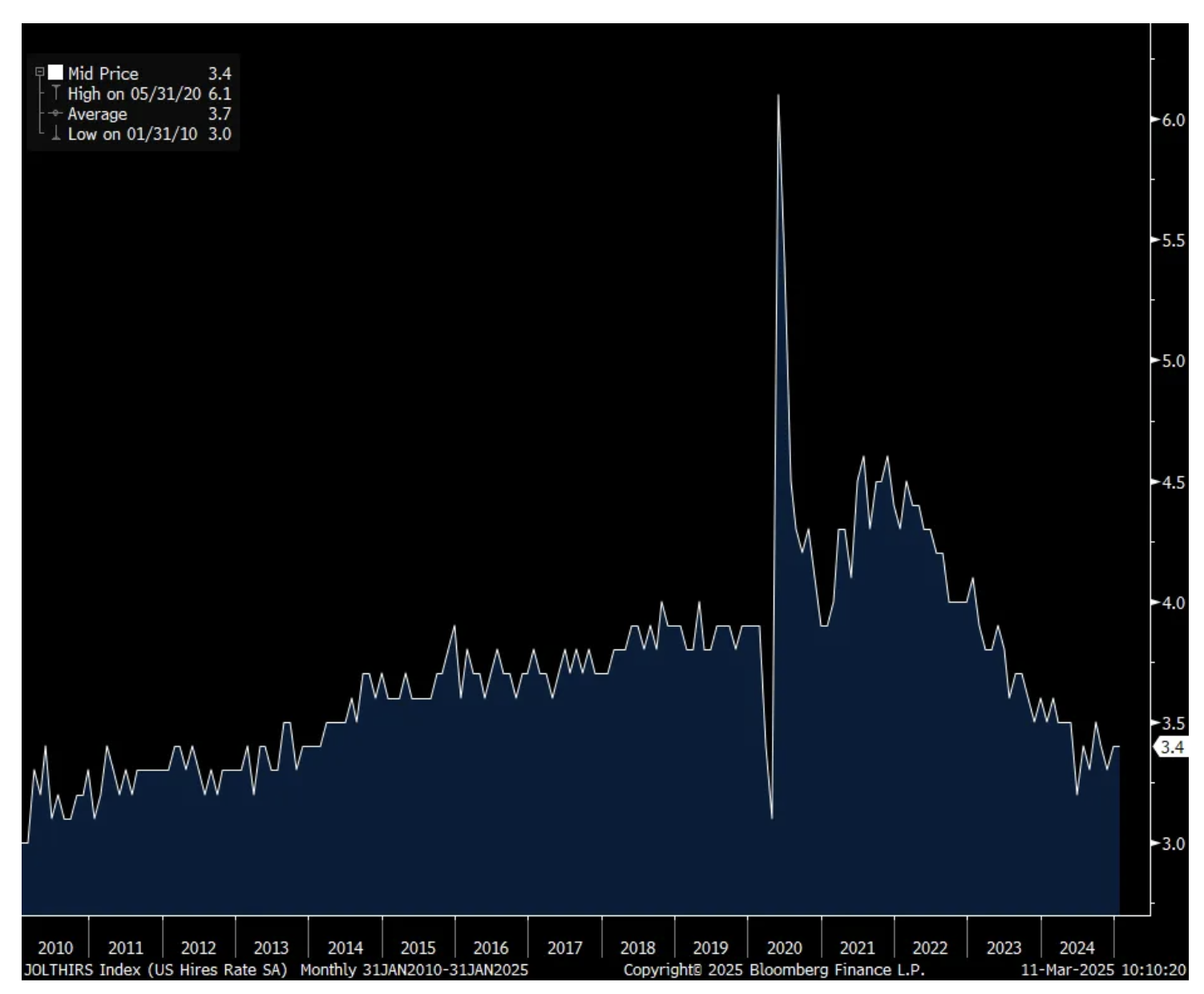

The hiring rate was 3.4% and December was revised up to the same level from 3.3% initially. For perspective, 3.2% matches the lowest since 2013 not including Covid. The quit rate did rebound to 2.1% vs 1.9% in the two prior months.

Because of the work from home phenomenon and ability to source workers from anywhere, the job openings data today does not have the same complexion as pre Covid as the same job can sometimes be listed multiple times. So, I prefer to watch the trajectory of job openings rather than the absolute figure and after a steady decline since 2022, we’re now sort of flattening out. This said, a lot has changed in February and March so far with respect to all the tariffs, markets and the consumer mood (as heard from the airlines yesterday and today) and I’d regard January jobs data as old news.

Job Openings

Hiring Rate

Quit Rate

BY Doug Kass · Mar 11, 2025, 11:15 AM EDT

Added to financials across the board.

Price recap in "Things" later today. (Too many to type out and I am trading actively)

BY Doug Kass · Mar 11, 2025, 10:56 AM EDT

I covered a lot of Monday's PEP shorts ($159.34) just now at $152.69.

From yesterday:

BY Doug Kass · Mar 11, 2025, 10:31 AM EDT

I added to SPY $557.01 and QQQ $470.97 on whoosh lower just now.

BY Doug Kass · Mar 11, 2025, 10:12 AM EDT

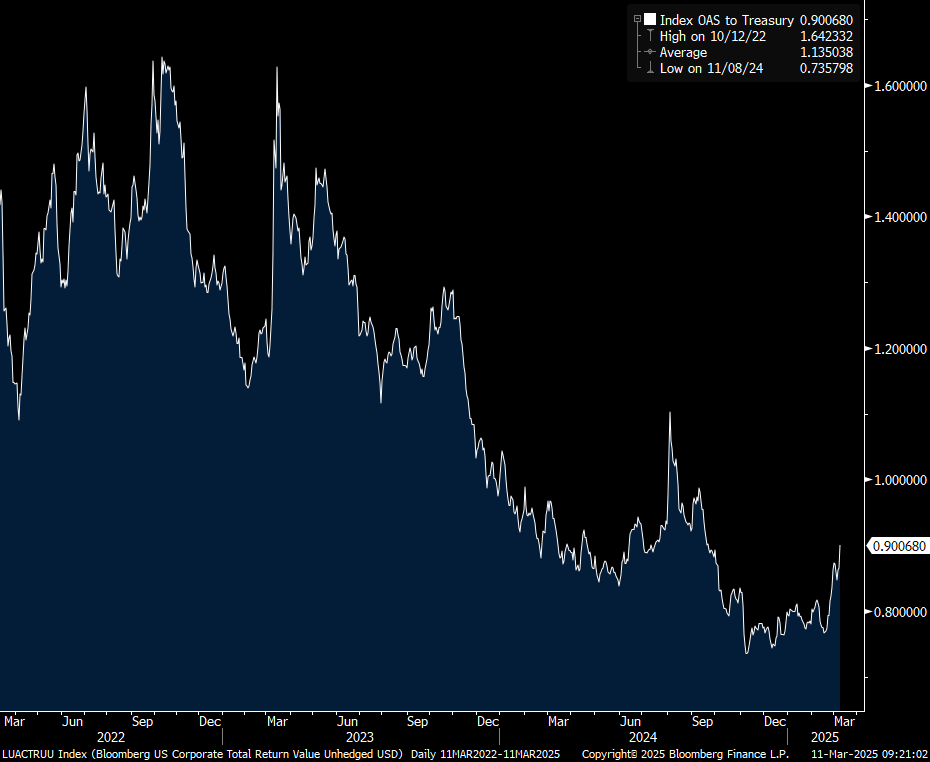

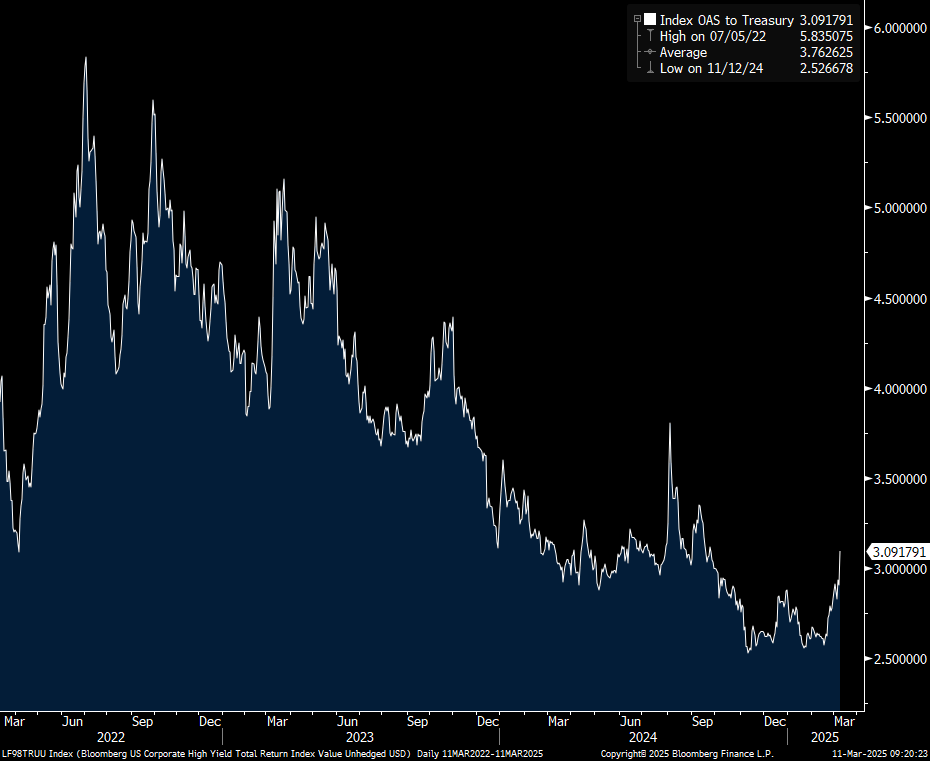

Another factor that has led me to play the long side (on the profound weakness) is that credit spreads, though up a bit from the lows, are still relatively stable:

High Yield

Source: Peter Boockvar

IG

BY Doug Kass · Mar 11, 2025, 9:50 AM EDT

Added to:

* SPY $558.71

* QQQ $471.86

BY Doug Kass · Mar 11, 2025, 9:40 AM EDT

From Peter Boockvar:

It's easy to blame the tariffs and scattershot approach being employed for the decline in the stock market but it's broader than that. I argued last month (February 18th to be exact) that the AI tech trade was over in terms of their stock market dominance and it's become clear of that, with the DeepSeek news in January being a key catalyst for that, along with the unclear revenue drivers all this spend will generate. Also, we now have multiple compression also being a notable part of the stock performance as earnings growth slows. You lose the special 7 stocks, which at its peak made up about 35% of the S&P 500, you are without a net in the broader market unless the baton is immediately passed to someone else.

I also said then, "In a way, the big 7 have become its own reserve currency where foreigners around the world have parked their money in and kept a bid under the US dollar." Well, we've seen the US dollar tank along with the big 7 stocks. And many international stock markets have done great instead and where we remain bullish and long of. To this point that the selloff is not just worries about tariffs, the Mexican stock market is up for the year by 4.5% and the Canadian market is down only slightly, by 1.4%.

My point here is, and I'll say again, a regime change is taking place in the markets and what used to work is not going to work from here anywhere to the same degree. The stock market has a history of handing the baton over to other things and now seems to be one of those times.

I also want to point out that we are also possibly losing the massive fiscal influx into the US economy that I've talked about here and Treasury Secretary Bessent referred to last week as needed 'detox.' The nearly 7% budget deficit as a % of GDP was also a big boost to corporate earnings and profit margins. I need to add now too, the other big leg holding up the US economy has been upper income spending, as we know, helped by a record net worth for those that own stocks and their homes. Thus, we lose the stock market right now, you can be sure upper income spending will falter. You want to debate the odds of a recession? you need to have an opinion on the S&P 500.

Southwest Airlines is repeating pretty much what Delta said last night in response to the now cloudy economic outlook. This morning they are lowering their Q1 revenue per available seat mile (RASM) growth rate to a "range of 2% to 4% on capacity down approximately 2%, both on a y/o/y basis. They blame part of this on "less government travel, and a greater impact from the California wildfires than originally estimated." But also this, "The remainder of the decrease is primarily attributable to softness in bookings and demand trends as the macro environment has weakened."

This is what Delta said last night in its 8k:

They lowered their y/o/y revenue guidance to growth of 3% to 4% from its initial guidance of 7% to 9%, along with trimming margin and eps guidance and said "The outlook has been impacted by the recent reduction in corporate confidence caused by increased macro uncertainty, driving softness in Domestic demand. Premium, international and loyalty revenue growth trends are consistent with expectations and reflect the resilience of Delta's diversified revenue base."

From American Airlines too:

"the revenue environment has been weaker than initially expected due to the impact of Flight 5342 and softness in the domestic leisure segment, primarily in March."

Of note in yesterday's NY Fed's Consumer Expectations Survey where inflation expectations were little changed, they said this on the labor market:

"Mean unemployment expectations - or the mean probability that the US unemployment rate will be higher one year from now - jumped 5.4 percentage points to 39.4%, its highest reading since September 2023. The increase was broad based across age, education, and income groups." Also, the quit rate fell to the lowest since July 2023.

On the credit side for consumers, "Perceptions of credit access compared to a year ago showed a larger share of households reporting it is harder to get credit, and a smaller share reporting it is easier. Expectations for future credit availability deteriorated considerably in February."

And, "The average perceived probability of missing a minimum debt payment over the next three months increased by 1.3 percentage points to 14.6%, the highest level since April 2020."

To the concerns above, "The share of households expecting a worse financial situation in one year from now rose to 27.4%, the highest level since November 2023."

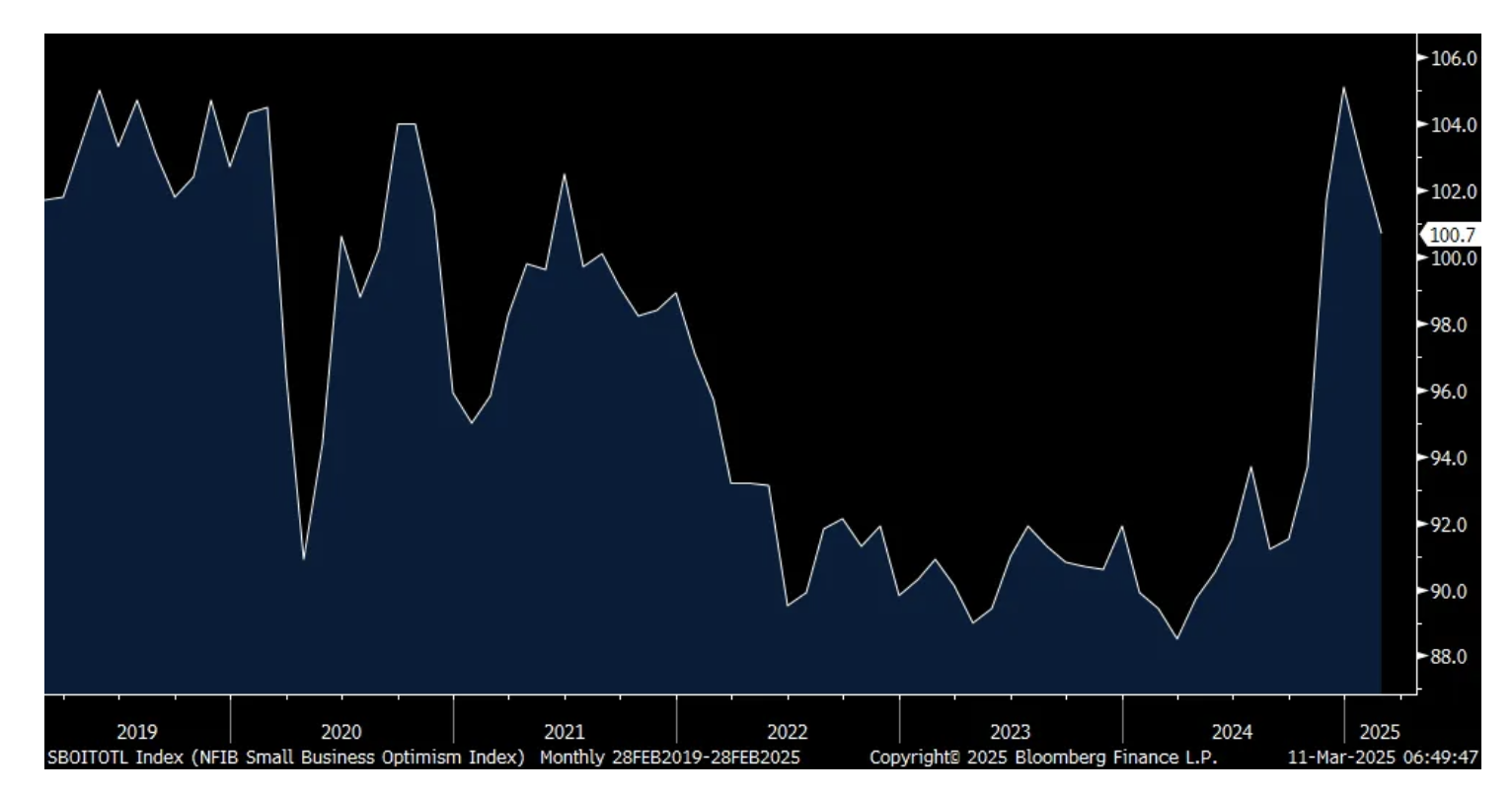

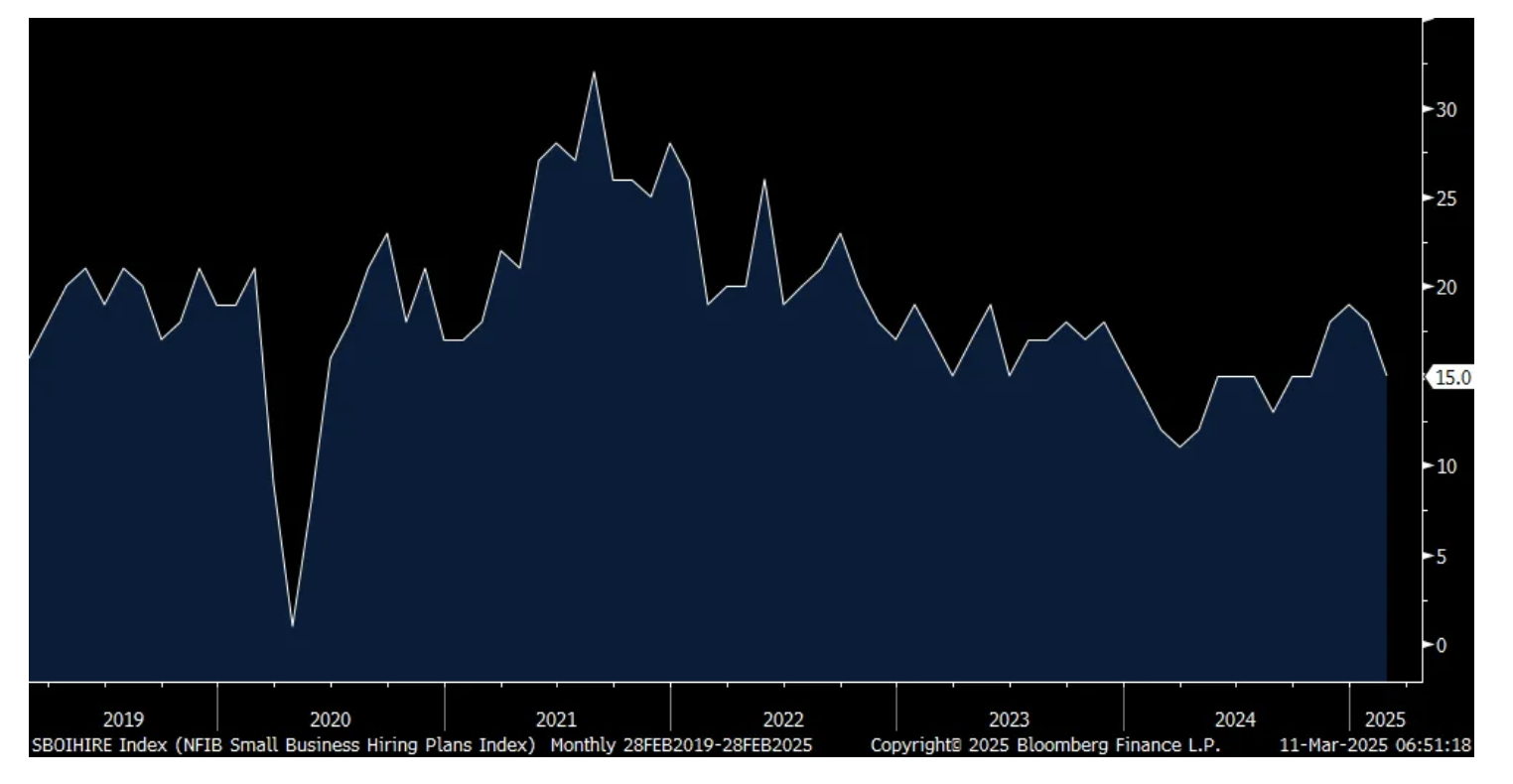

Now with respect to small business confidence, the NFIB optimism index for February fell 2.1 pts m/o/m to 100.7 and down for a 2nd month. It's though still well above the October, pre-election, level of 93.7.

The key internals to highlight, Plan to Hire fell 3 pts to 15%, matching the lowest level since August 2024. Current compensation was unchanged but future comp plans eased by 2 pts.

Of particular note, and most likely in response to the tariffs, Higher Selling Prices jumped by 10 pts to 32%, the highest since May 2023. The NFIB said "this is the largest monthly increase since April 2021, and the third highest jump in the survey's history." Capital spending plans fell 1 pt after dropping 7 pts in January.

Those that Expect a Better Economy fell 10 pts but still is well above zero at 37% vs the -5% it was at in October. Those that Expect Higher Sales and that it's a Good Time to Expand also fell m/o/m. The average rate paid on a loan dropped to 8.8% from 9.4%.

The NFIB said "Small business owners have experienced uncertainty whiplash over the last four months with the Uncertainty Index falling from October's 110 reading to 86 in December and then back up to 104."

As for the top business issue, 'labor quality' has now surpassed inflation by 3 pts, though the NFIB still said "Inflation remains a major problem."

The bottom line from the NFIB, "Uncertainty is high and rising on Main Street, and for many reasons." I'm sure tariffs and the threats of them are the main reason.

NFIB Small Business Optimism Index

Plan to Hire

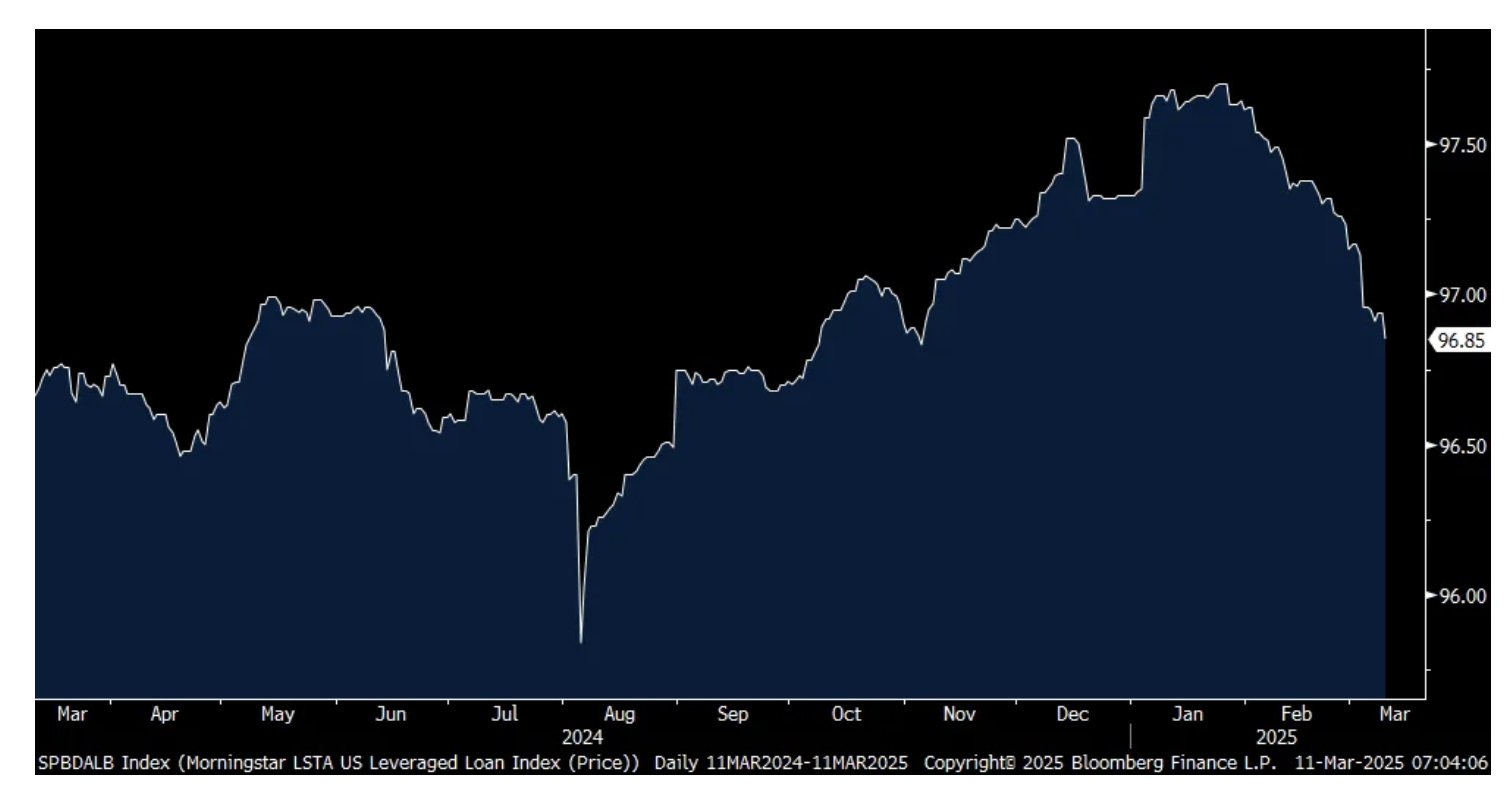

Before I get to some earnings calls, here is a chart of the LSTA leveraged loan index which includes floating rate debt. So, on expectations of more Fed rate cuts, these loans become less attractive at the same time the credits, lower end of totem pole, lose luster with worries over economic growth.

LSTA Index

From Oracle who is benefiting from their Cloud/AI data center business:

"this was our strongest booking quarter ever by a large margin...Speaking of data centers, we marked a milestone this quarter as we crossed into triple digits with our 101st cloud region coming online."

Some interesting comments from Mission Produce, a maker of fruit, particularly avocados, and whose stock symbol is AVO:

The price of avocados has made the news and they said "We realized segment growth of 32% vs the prior year, reflecting a 5% increase in avocado volumes sold and a 25% increase in per unit avocado selling prices relative to the prior period. The combination of volume, growth during a period of heightened pricing clearly indicates the resiliency of consumer demand for the category, despite the broader impacts from the inflation that consumers continue to absorb."

Also, "Our blueberry segment also contributed nicely...We see tremendous long term growth in blueberries as consumer preferences shift towards healthy, convenient snacking options."

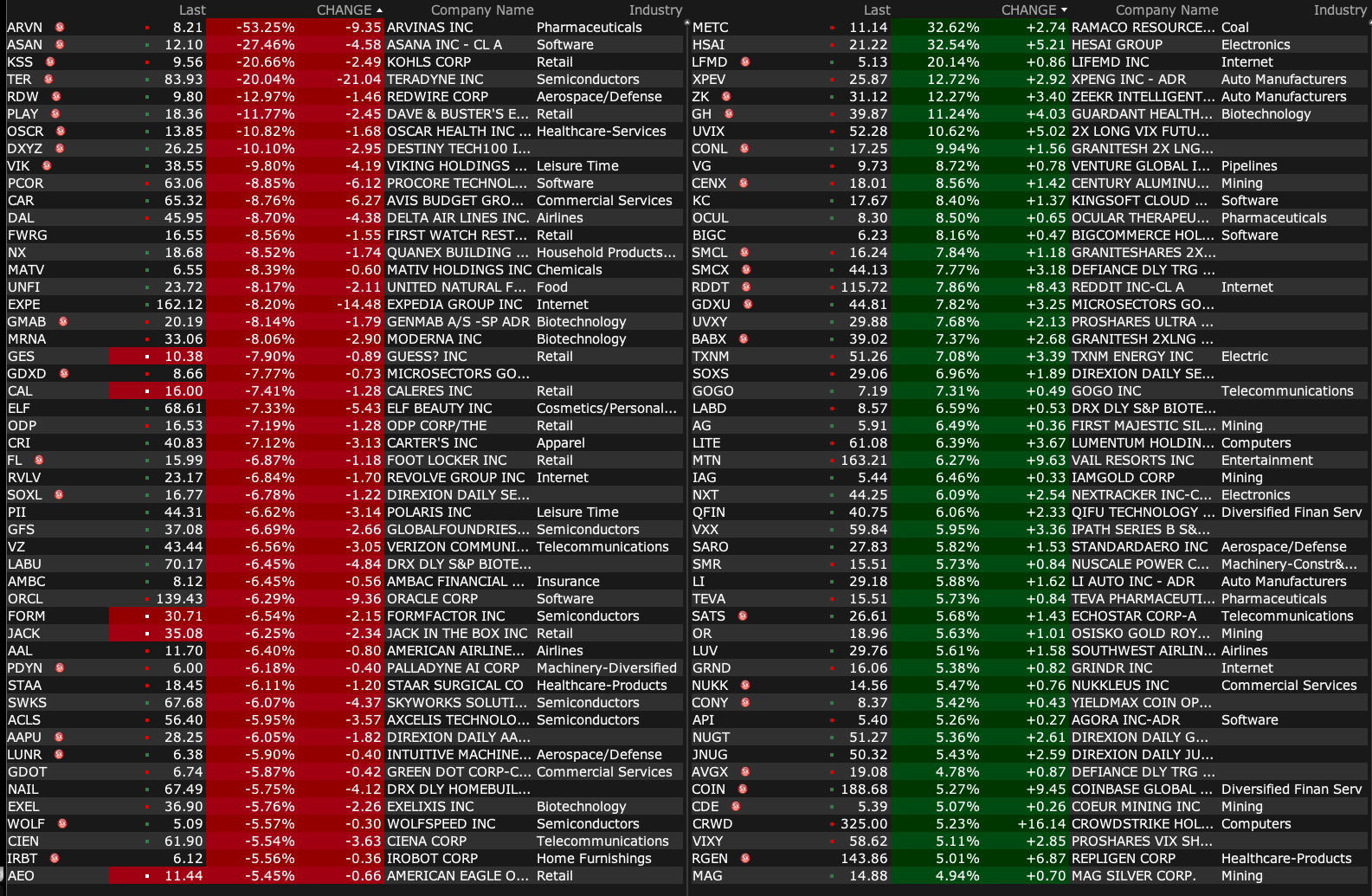

BY Doug Kass · Mar 11, 2025, 9:35 AM EDT

-SNOA +52% (secures Extensive U.K. Regulatory Clearances of Key Wound Care and Dermatology Products by the Medicines & Healthcare Products Regulatory Agency (MHRA))

-TNON +41% (receives Approval for Notice of Allowance from the European Patent Office)

-BVS +27% (earnings, guidance)

-MYO +26% (earnings, guidance)

-ONDS +24% (Ondas Autonomous Systems partners with Palantir to enhance drone platform scalability)

-LFMD +21% (earnings, guidance)

-MNTS +17% (Momentus & Solstar Space announce strategic partnership for On-Demand Communication for Space Systems)

-LUV +10% (trims guidance; to introduce a new, Basic fare on its lowest priced tickets purchased on or after May 28, 2025, in advance of offering assigned seating and extra legroom options)

-XPEV +9.4% (said to consider investing up to $13.8B on humanoid robots)

-TXNM +8.4% (said to explore sale after getting takeover interest)

-PAY +7.4% (earnings, guidance)

-HSAI +7.1% (earnings, guidance; announced new exclusive design win with a leading European OEM)

-WATT +6.2% (updates 2025 growth trajectory, raised $13.4M YTD)

-HLLY +5.0% (earnings, guidance)

-ELV +4.8% (affirms guidance)

-MTN +4.8% (earnings, guidance)

-UNFI +4.7% (earnings, guidance)

-JBLU +4.3% (adjusts guidance)

-SARO +4.2% (earnings, guidance)

-KFY +3.9% (earnings, guidance)

-VXRT +3.8% (announces Clinical Trial Initiation of Norovirus Oral Pill Vaccine Candidate)

-COIN +3.2% (secures registration in India; plans to launch initial retail services later this year)

-NNE +2.9% (confirmed as Reactor Designer of KRONOS MMR by U.S. Nuclear Regulatory Commission)

-ILMN +2.5% (guidance)

-KFY +2.4% (earnings, guidance)

-FWRG +2.2% (earnings, guidance)

-UAL +2.2% (guidance)

-ARVN -36% (Arvinas and Pfizer Phase3 VERITAC-2 Clinical Trial did not reach statistical significance in improvement in PFS in the intent-to-treat (ITT) population)

-NPWR -34% (pressured by project Permian uncertainty)

-ASAN -24% (earnings, guidance)

-RDW -16% (earnings, guidance)

-KSS -14% (earnings, guidance)

-FCEL -10% (earnings, guidance; files to offer $205M shares)

-FERG -7.5% (earnings, guidance)

-AVO -6.9% (earnings, guidance)

-MYPS -5.3% (earnings, guidance)

-DKS -4.8% (earnings, guidance)

-STKS -4.2% (earnings, guidance)

-DAL -4.1% (cuts guidance)

-VZ -3.5% (Q1 color provided at DB conference)

-EXPE -2.0% (airlines cuts forecasts)

-ORCL -2.0% (earnings, guidance)

BY Doug Kass · Mar 11, 2025, 9:23 AM EDT

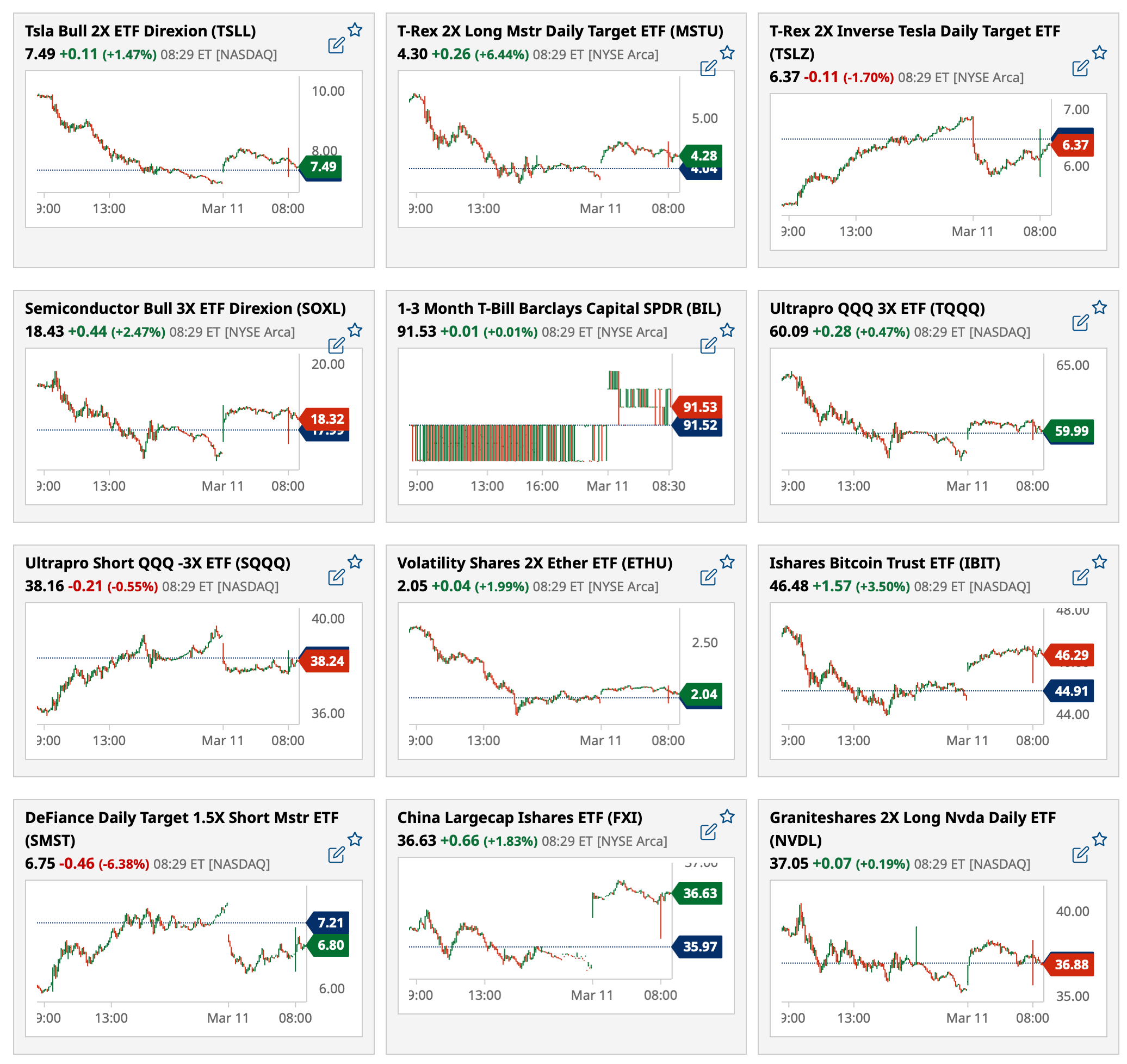

Most active premarket ETFs as of 8:34 a.m. ET:

BY Doug Kass · Mar 11, 2025, 9:12 AM EDT

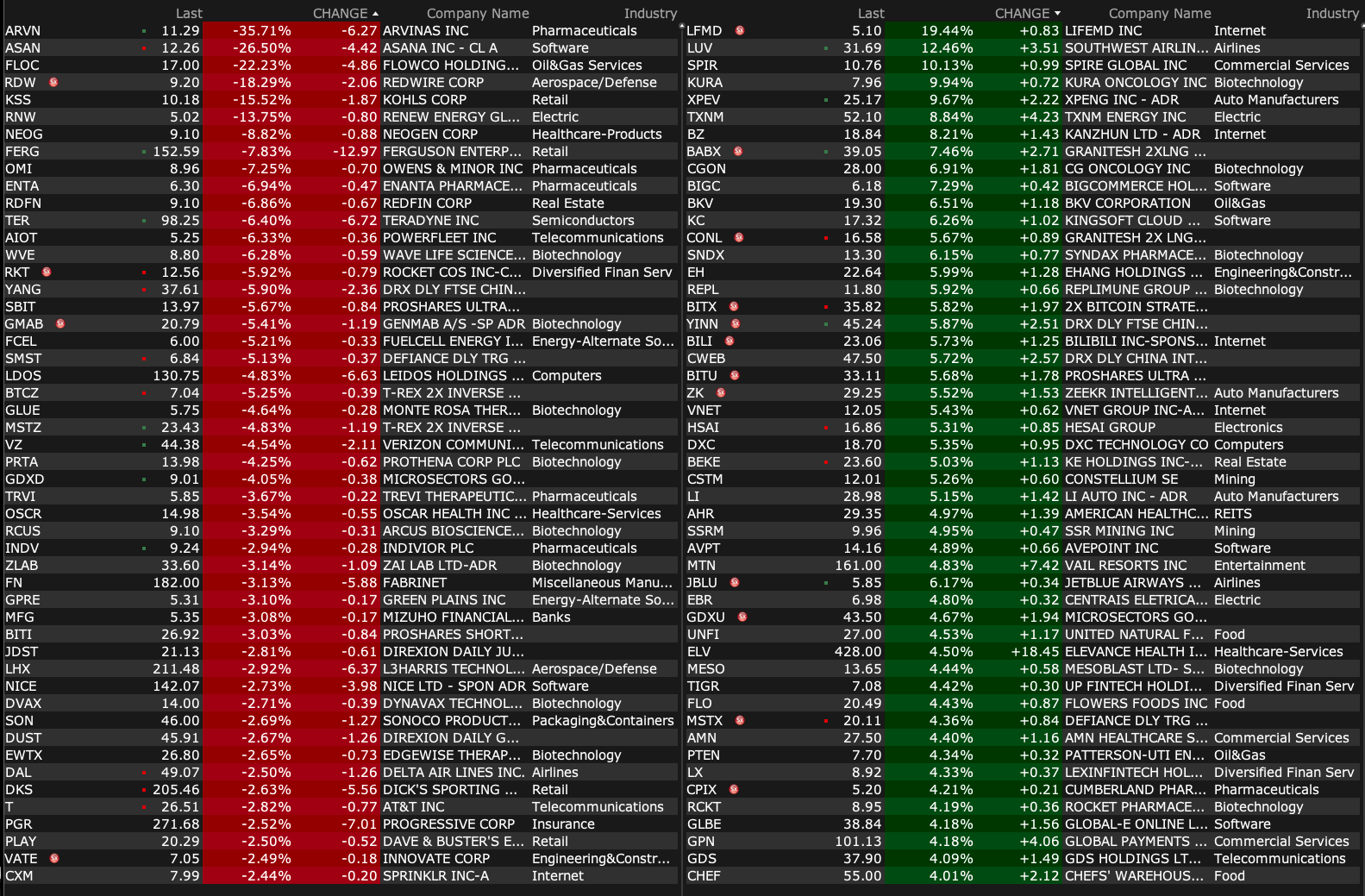

Premarket percentage movers at 8:51 a.m. ET:

BY Doug Kass · Mar 11, 2025, 9:00 AM EDT

* On being committed...

I am not a perma-anything.

I obviously got aggressive on the (trading) long side into the teeth of Monday's decline and the fear/selling of panicky and stunned market participants.

Besides a deepening oversold (see the S&P Oscillator's climb), Monday produced a record level of put buying:

I was dispassionate in buying as it is all about numbers (reward vs. risk/margin of safety) to me — not emotion.

Indeed history shows the timing might be good:

As of Monday's close, year to date the S&P 500 is -5% (it was +4% a few days ago) and the Nasdaq is -10% (it was +3% a few days ago). So, the decline in the senior averages has been swift and deep.

Remember I had previously estimated that the S&P index would see an approximate high of +5% and could fall -10% to -15% (precision not intended) in 2025. Therefore, the current reward vs. risk is now uninteresting but not as poor as it was in February before the averages' dramatic fall from grace (when I characterictized downside to be 2x to 3x upside).

That said, many equities have fared poorly for some time and some value is now emerging.

For those that didn't see my trade recap here it is:

On second thought, here is a quick and abbreviated "Things I Did Today":

* Short sales: (PEP) $159.34 and (KO) $73.19.

* Short covers: (AAPL) $225.73, (ROAD) $66.01, (BOOT) $101.10.

* Buys: (MSFT) $380.05, (GOOGL) $163.96, (AXP) $259.57, (META) $588.97, (GS) $529.28, (MS) $111.09, (C) $66.79, (JPM) $231.19, (AMZN) $194.11, (HOOD) $37.3, (WFC) $66.22 and (BAC) $39.71.

* Bought the Indices (SPY) / (QQQ) , but not done yet. (SPY $564.01 and QQQ $478.10 at)

By Doug Kass Mar 10, 2025 3:57 PM EDT

Working for the GOAT Lee Cooperman reverberated in my work ethic and process.

I had the office next to Lee at Omega Advisors. I felt I had to get into work before him. Since his work day started at about 6:15 a.m., I got in very early.

* Lee taught me to work hard. My days, running Seabreeze Partners and writing my Diary on TheStreet Pro, routinely start at 4 a.m. I am not lying because the time of publication is listed on each column I contribute.

* Lee taught me to go belly to belly with company managements I am long or short. He inculcated in me the need to know my companies as well as the CFO. This continues to this day. My working day is not watching the screens, it is talking to managements.

* Lee taught me that opportunities must be taken, no matter at what time of day. Case in point, last night I worked until midnight as the volatility in the S&P and Nasdaq futures was wild. At one point (and I was buying SPY), S&P futures were -53 handles. This morning they have reversed to being up by nearly +20 handles — that's a more than one percent move (from the evening's futures lows) to take advantage of. I also added to Robinhood HOOD and Amazon AMZN last night. HOOD was down by -$2 from the close, while AMZN was -$3. Robinhood's shares are now +$3 from last night's buy and Amazon's shares are up from $191 to $195.40.

Seabreeze profited from this extra work and commitment.

I tell my hedge fund investors that I may not always be right about the markets, but there is no one that works as hard as I (and our team) does for them. Last night was an example of my commitment to my Limited Partners.

The same applies, I hope, to our subscribers.

BY Doug Kass · Mar 11, 2025, 8:15 AM EDT

DocMarc

19 minutes ago

Dougie, I rarely see you shorting the small caps. Is there a reason?

Also, are the equities you bought yesterday for a trade? Are you expecting a dead-cat bounce in the indices since you holding index shorts?

DK

Dougie Kass

STAFF

16 minutes ago

i want to stick to large and dominant companies that have deep moats, doc.

but i do own smaller caps, i dont just publish which ones because they are generally speculative.

BY Doug Kass · Mar 11, 2025, 8:00 AM EDT

BY Doug Kass · Mar 11, 2025, 7:48 AM EDT

"The only person you can trust in your life is your mom. The first 3 letters of Momentum are M-O-M"

- Ralph Acampora

Bonus - here are some links:

Bull or Bear.. Why It Matters Bull or Bear. Why it Matters?

Semis Being Bad is Not Bad For the Markets https://www.youtube.com/watch?si=SV8ier_66lOy8xi-&v=gJLiGVhGZME&feature=youtu.be

The SOL Is Setting The SOL is Setting

The Nasdaq 25 Years Later Bespoke | My Research

BY Doug Kass · Mar 11, 2025, 7:15 AM EDT

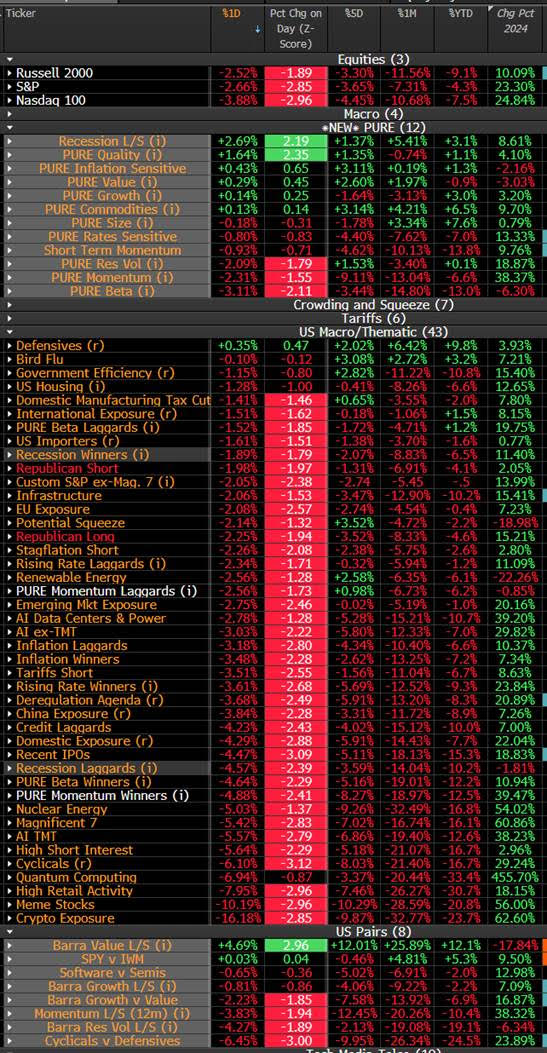

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Mar 11, 2025, 6:52 AM EDT

From JPMorgan:

US: Futs are higher, with both NDX and RTY outperforming. Across the JPM Trading Desk like participating in this bounce higher but it may be short-lived unless trade policy is crystallized. Delta’s earnings, calling out uncertainty for hitting guidance may increase expectations for Trump to establish the Trump Put in Eqy mkts. Trump may also visit China in April, potentially to do a trade deal’ as second summit in the US in June is in discussion. Pre-mkt, Mag7 are all higher ex-AAPL with Semis, Financials, and Int’l Eqy ADRs also poised to outperform. Bond yields are mixed as the yield curve twists flatter and USD is weaker. The cmdty complex is strong across all 3 complexes with precious metals the standout. Today’s macro data focus is on JOLTS data and Small Business Optimism (future hiring plans are a leading indicator for NFP).

and...

EQUITY AND MACRO NARRATIVE: Yesterday, felt like the first signs of panic in this sell-off that enters its third week. Mag7 entered a bear market with the index down 20.3% from all-time highs set in December. The SOX Index is 19.5% below its January highs and ARKK is -28.6% from its ATH set in Feb. Momentum is down 14% from its Feb highs, in line with previous unwinds. Given the magnitude of moves yesterday, a bounce is increasingly likely and is likely a tradeable bounce, but we remain of the view that all rallies should be sold.

BY Doug Kass · Mar 11, 2025, 6:42 AM EDT

The S&P Short Range Oscillator slipped deeper into oversold to -4.92% from -3.47%.

Now you know why, in part, I got aggressive on the long side in my trading during the teeth of the decline on Monday.

BY Doug Kass · Mar 11, 2025, 6:35 AM EDT