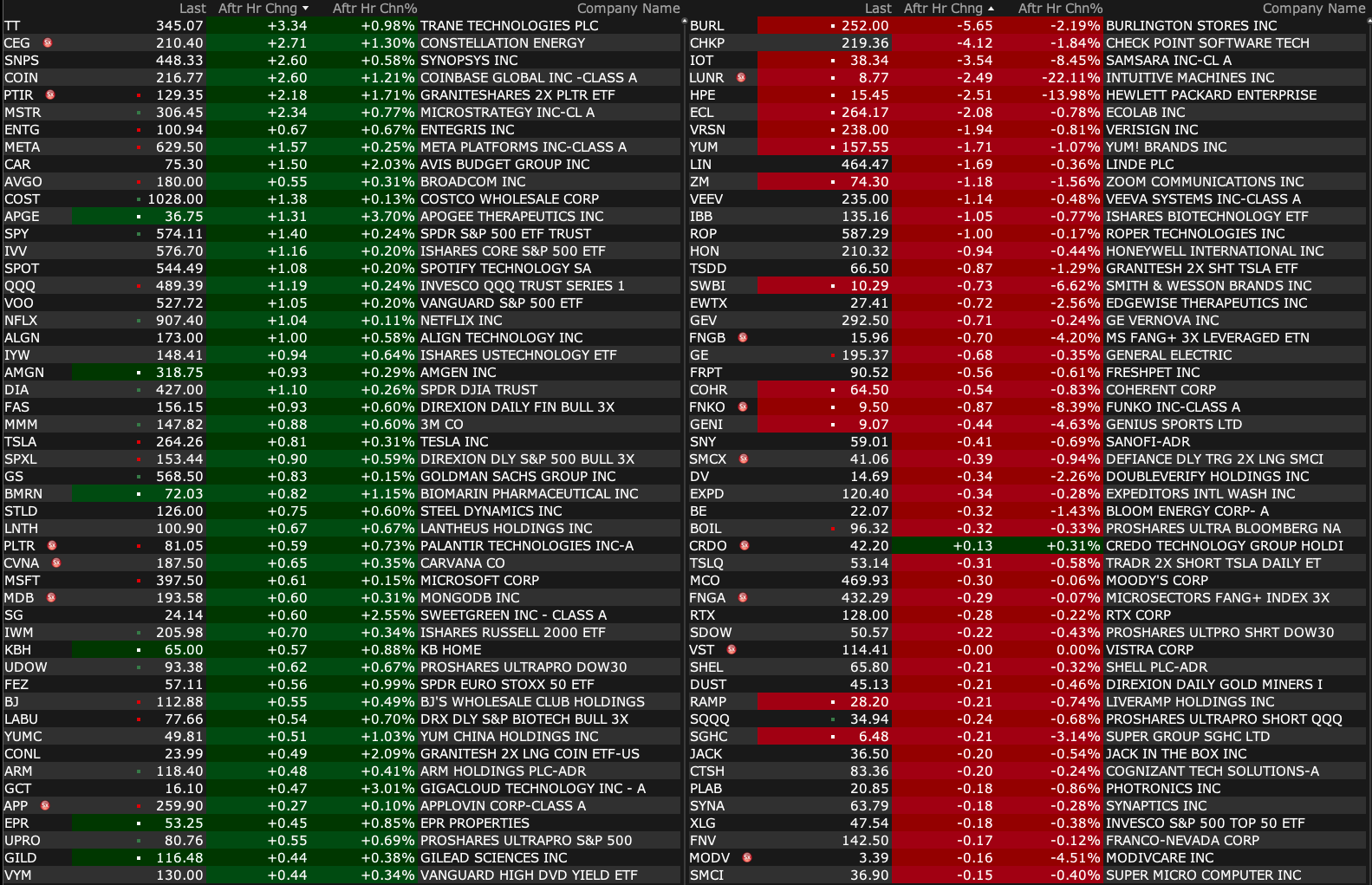

Thursday's After-Hours Movers

As of 4:12 pm ET:

BY Doug Kass · Mar 6, 2025, 4:50 PM EST

As of 4:12 pm ET:

BY Doug Kass · Mar 6, 2025, 4:50 PM EST

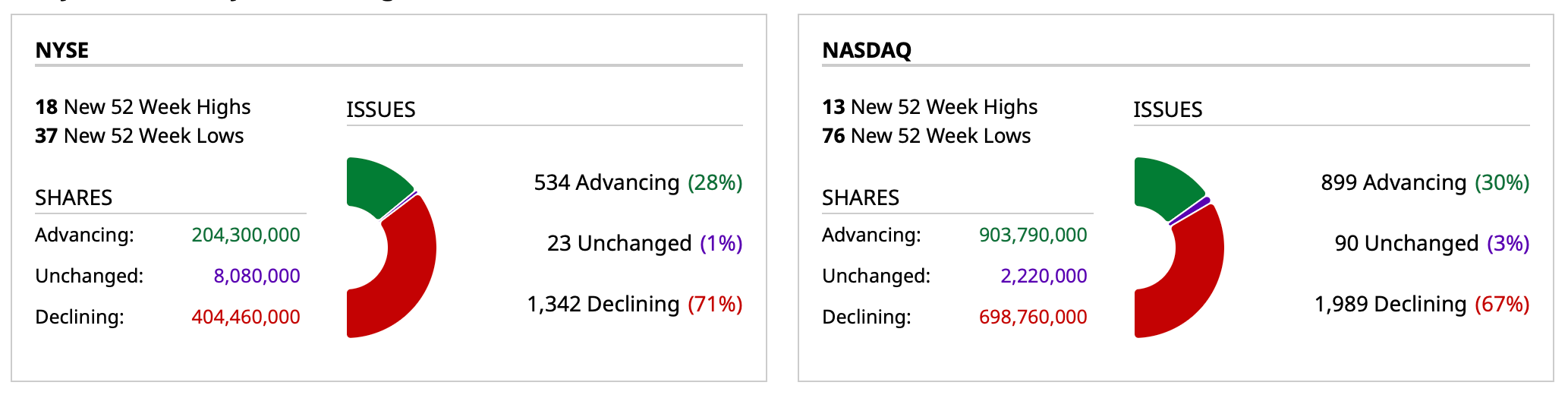

- NYSE volume 11% above its one-month average

- NASDAQ volume 3% below its one-month average

- VIX index: up 14.73% to 25.16

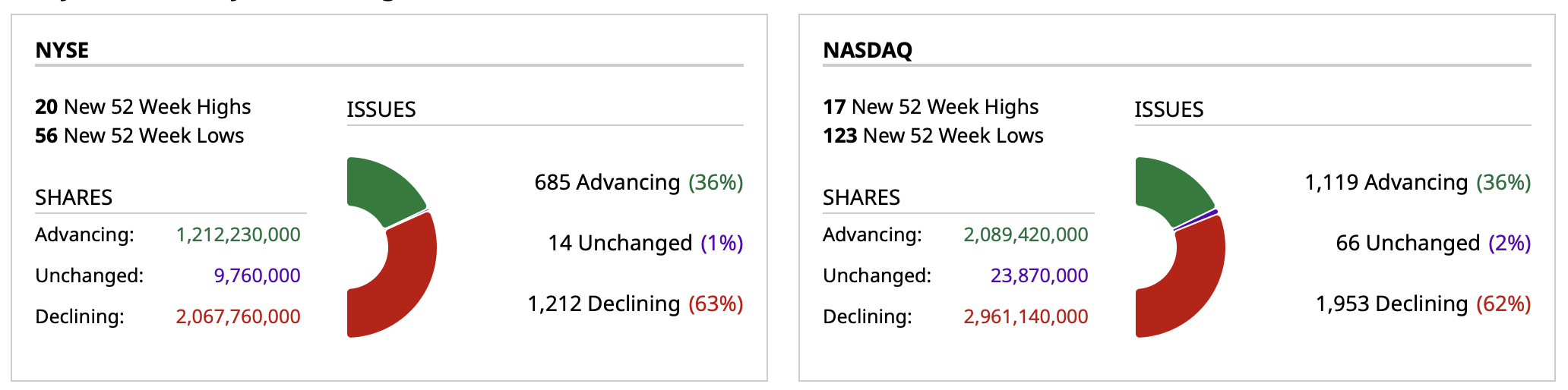

Closing Breadth

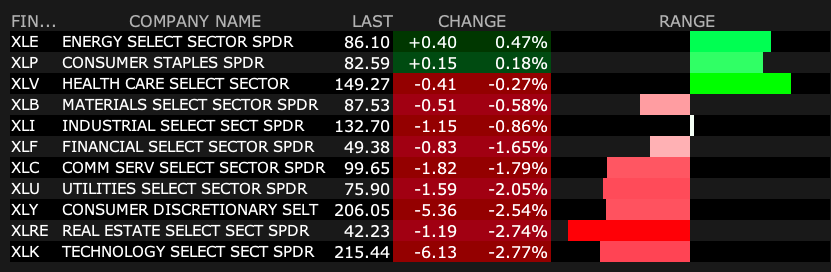

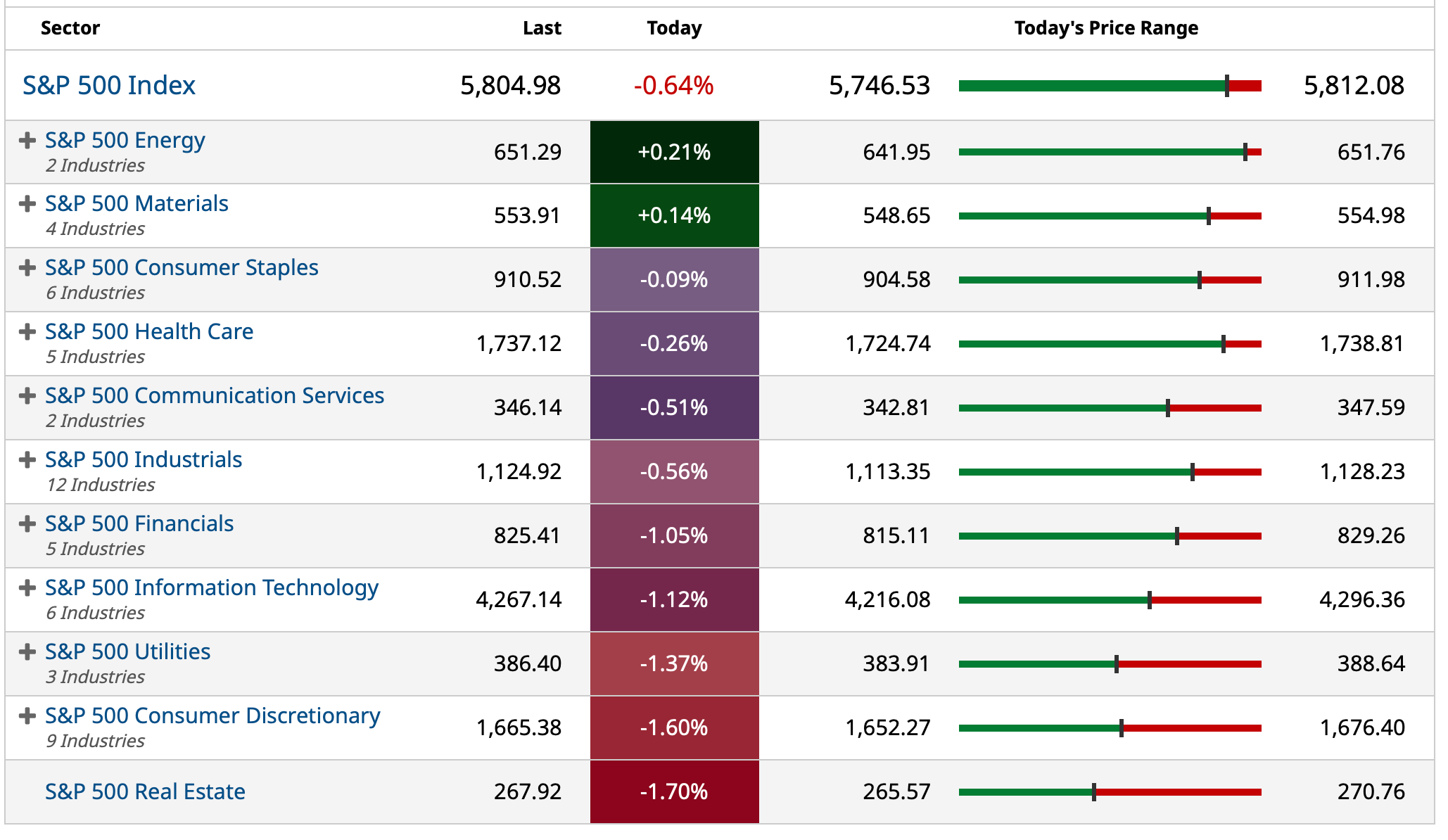

S&P 500 Sector ETFs

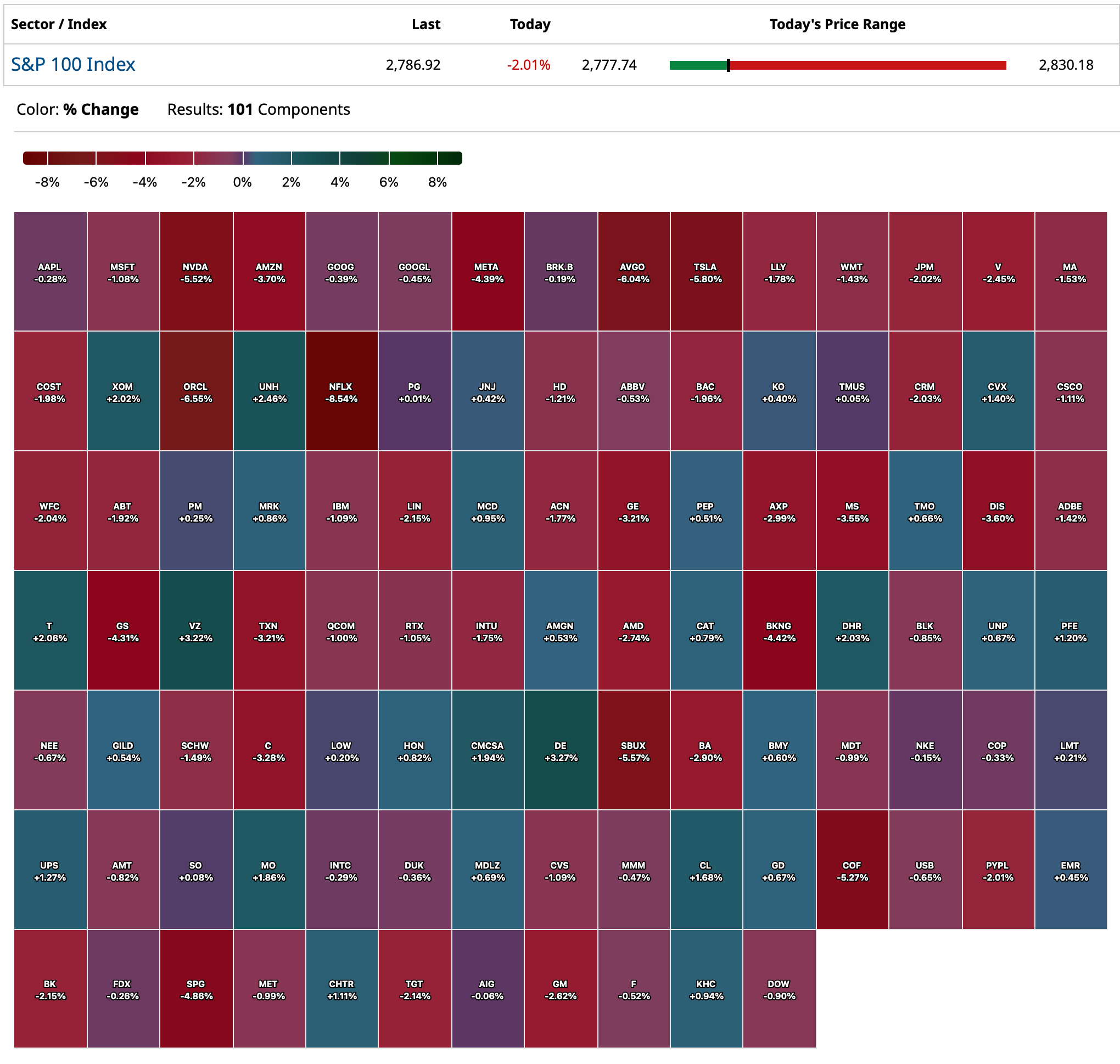

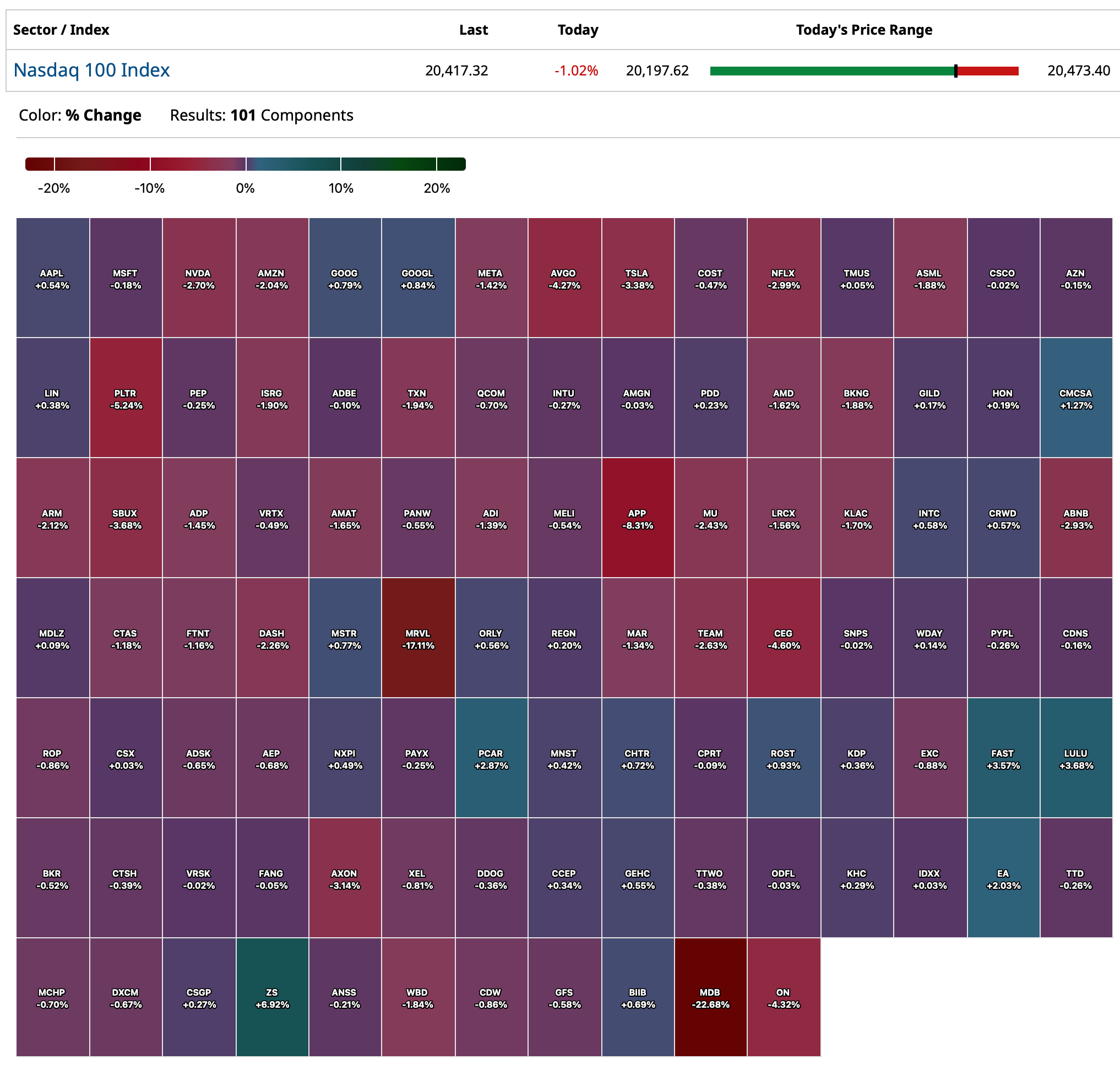

Nasdaq 100 Heat Map

BY Doug Kass · Mar 6, 2025, 4:40 PM EST

AVGO had excellent numbers.

This should make my index trading long rentals, made late in the day, profitable tomorrow.

More later.

BY Doug Kass · Mar 6, 2025, 4:25 PM EST

BY Doug Kass · Mar 6, 2025, 4:20 PM EST

Investment short Sleep Number SNBR is -42% today after the bad miss and lowered guidance.

BY Doug Kass · Mar 6, 2025, 4:05 PM EST

At $199.45, moved to medium-sized in Amazon AMZN

BY Doug Kass · Mar 6, 2025, 3:51 PM EST

With the oscillator moving to a larger oversold and SPY on support ($572-ish), I took the following long trading rentals in the indices:

* SPY $571.86

* QQQ $487.47

BY Doug Kass · Mar 6, 2025, 3:35 PM EST

Getting my sea legs back.

BY Doug Kass · Mar 6, 2025, 3:20 PM EST

I have covered my Starbucks SBUX short at $106.60 (-$5.50).

BY Doug Kass · Mar 6, 2025, 12:37 PM EST

BY Doug Kass · Mar 6, 2025, 11:55 AM EST

I sold my trading long rentals purchased earlier to move back to delta neutral on limited: SPY $578.19; QQQ $497.56

BY Doug Kass · Mar 6, 2025, 10:39 AM EST

Investment short SNBR is now -20% in premarket after the miss (see below):

Investment short Sleep Number (SNBR) misses on sales again.

The share price is down another -$1.50 (or -13%) in post-market trading.

Here is the full release.

Sleep Number Corporation - Sleep Number Announces Fourth Quarter and Full Year 2024 Results

By Doug Kass

Short SNBR VS

Mar 5, 2025 4:08 PM EST

BY Doug Kass · Mar 6, 2025, 9:45 AM EST

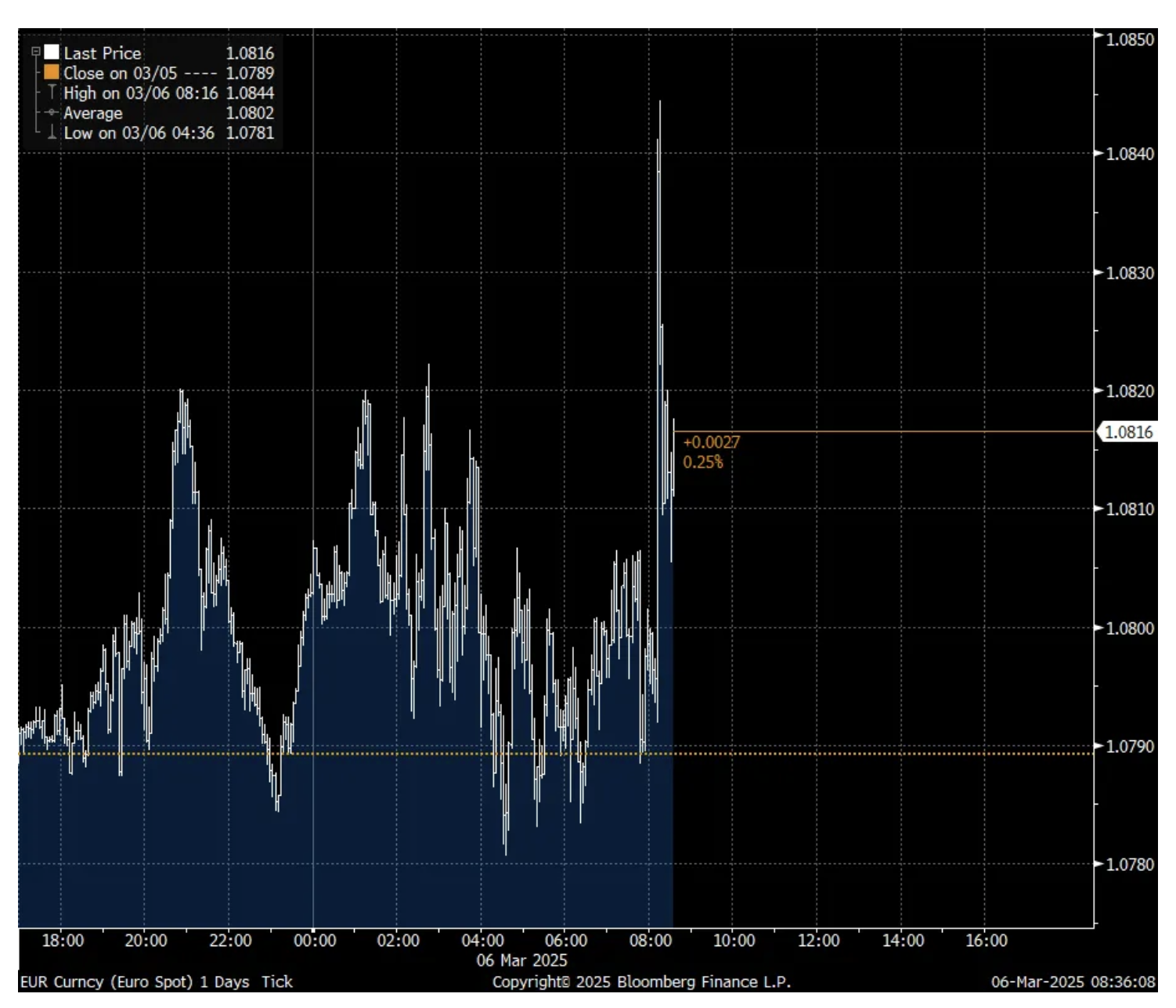

From Peter Boockvar:

While the ECB cut rates again to 2.50%, bringing its REAL rate to about zero in the face of what could be the biggest fiscal expansion in Europe seen in a while, they are hinting at a pause by saying that the rate level now is “becoming meaningfully less restrictive.” On that comment, the euro initially rallied but gave it back as seen below, though still up on the day. We’ll soon hear what Lagarde has to say at her press conference.

Euro Intraday

The Challenger February jobs report saw the number of cuts totaling 172,017 which is the most for the month of February since 2009 and the most over a 12 month period since July 2020. They said “Private companies announced plans to shed thousands of jobs last month, particularly in Retail and Technology. With the impact of the DOGE actions, as well as canceled government contracts, fear of trade wars, and bankruptcies, job cuts soared in February.”

In that headline figure, about 62k came from the federal government “from 17 different agencies.”

It’s not all bad as hiring plans rose in February by almost 35k and that is the most for a February since 2022. Entertainment/leisure drove most of the hiring, adding 28k.

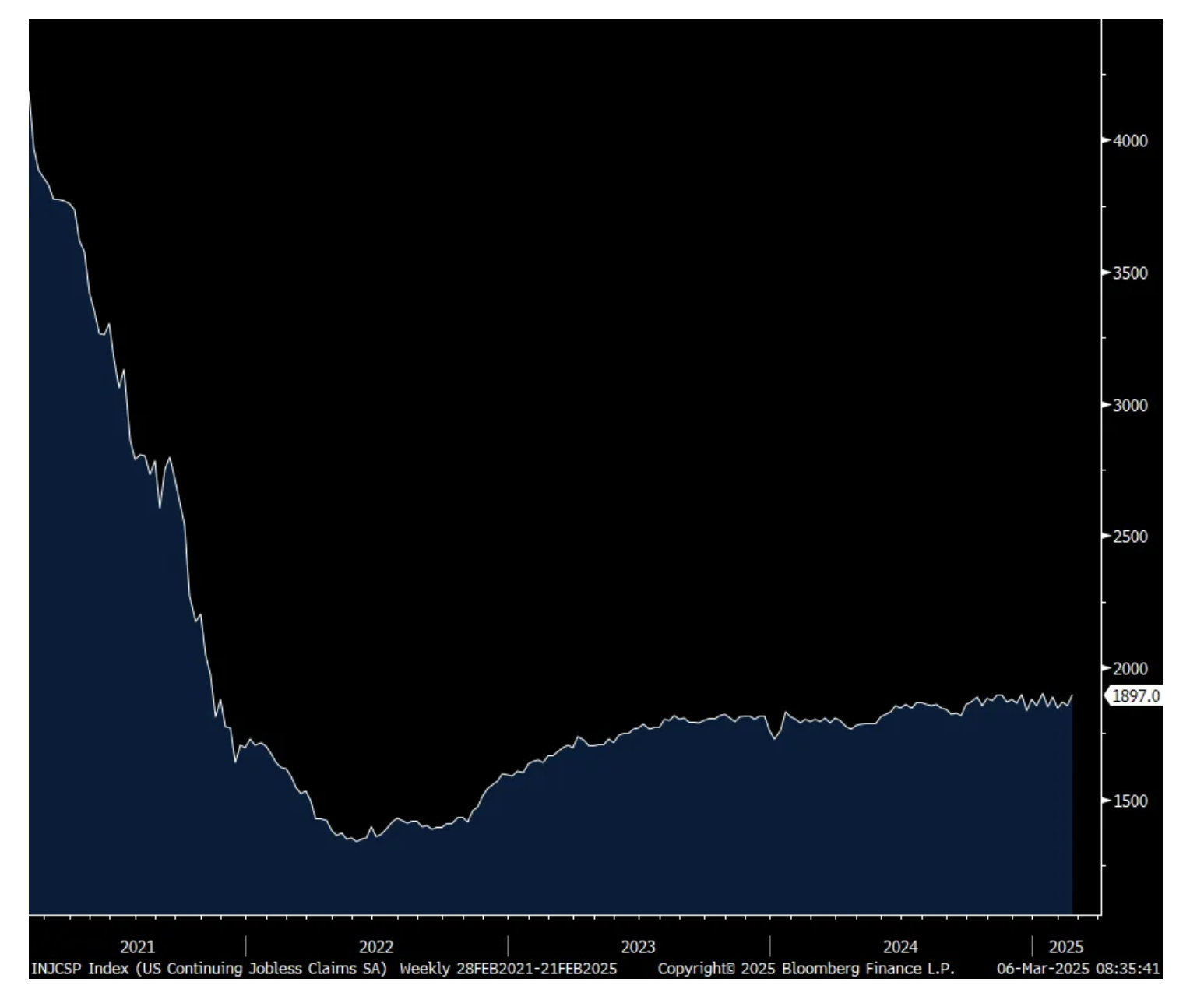

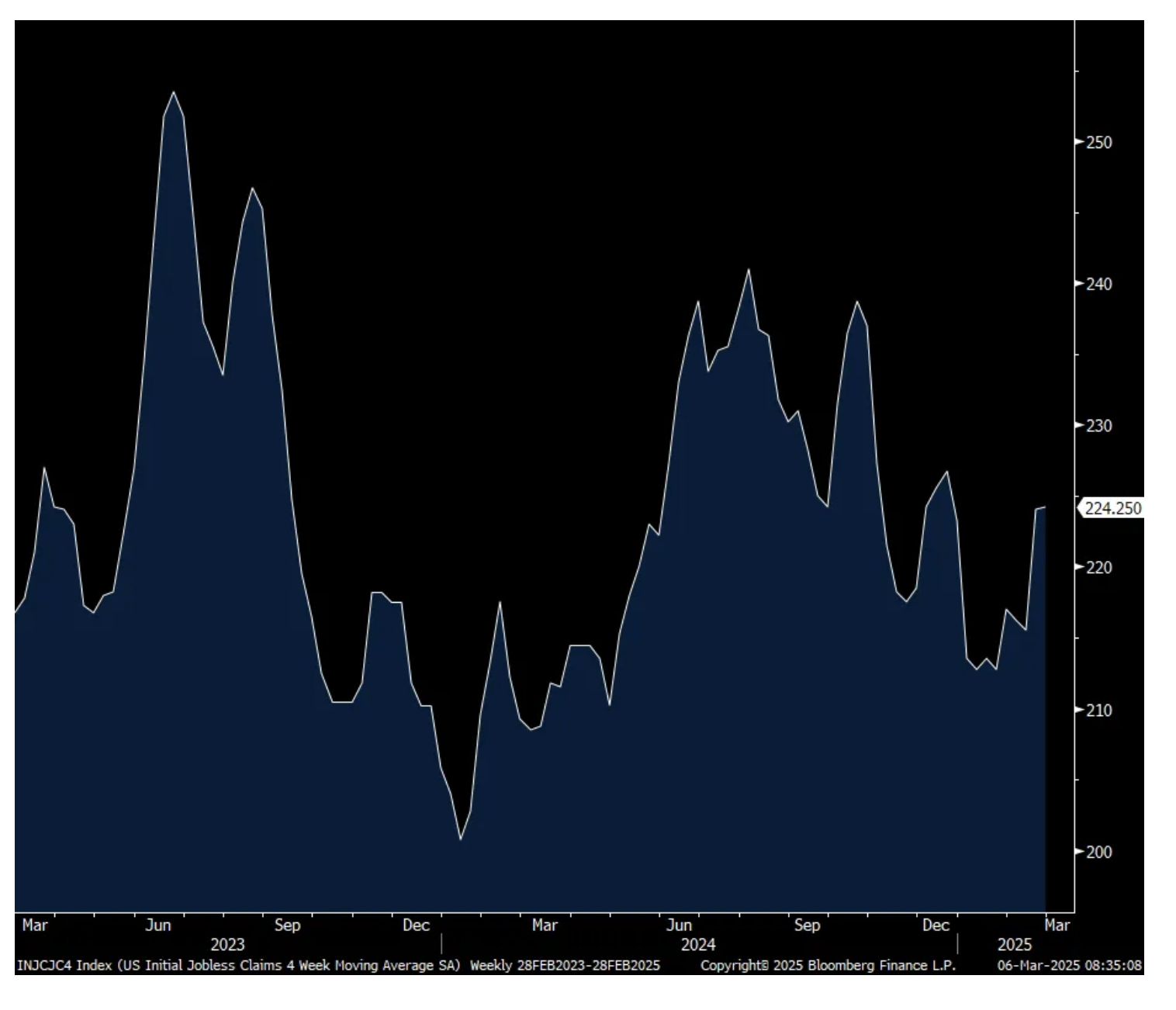

Initial claims fell back to 221k from 242k last week which we know was a bigger than expected rise. The estimate was 233k. Smoothing this out put the 4 week average at 224k from the same 224k last week. Continuing claims, delayed by a week, rose by 42k to 1.897, back to the highest since November 2021.

Initial claims in DC specifically fell by 383k w/o/w but assume the rise in continuing claims reflect the big jump in 3 out of the 4 prior weeks in initial claims.

Bottom line, the labor market seems to be at a really interesting moment as the economic front car window has gotten more cloudy.

4 Week Avg Initial Claims

Continuing claims

BY Doug Kass · Mar 6, 2025, 9:35 AM EST

-KITT +17% (to acquire SeaTrepid International for $16M)

-TH +14% (confirms secured 5-year lease and services contract with CoreCivic to reactivate Dilley, Texas facility)

-TREE +14% (earnings, guidance)

-BURL +12% (earnings, guidance)

-IHRT +12% (CEO, Chair Pittman buys 200K common shares)

-LSH +12% (files to sell convertible debt financing for up to $4.5M)

-FLUX +9.9% (receives first purchase order for lithium-ion battery packs from large US medical supply company)

-CBRL +9.2% (earnings, guidance)

-CRMT +9.2% (earnings)

-CLSD +8.0% (announces Successful End-of-Phase 2 Meeting with the FDA and Alignment on Phase 3 Plans for Suprachoroidal CLS-AX in Wet AMD)

-ALGM +7.9% (confirms receipt of proposal from Onsemi of $35.10/shr cash offer)

-CXW +6.9% (announces resumption of operations at South Texas Family Residential Center in Dilley, Texas)

-VEEV +6.0% (earnings, guidance)

-IDCC +5.6% (raises Q1guidance)

-JD +5.1% (earnings, color)

-VXRT +4.3% (Phase 2 challenge study of an oral pill norovirus vaccine candidate expected to initiate in 1H25)

-ZS +2.9% (earnings, guidance)

-SPRY +2.6% (receives US FDA NDA Supplemental 1 approval for neffy 1 mg (epinephrine nasal spray) for Type I Allergic Reactions, Including Anaphylaxis, in Pediatric Patients Weighing 15 to < 30 Kilograms)

-PRTH +2.0% (earnings, guidance)

-BKSY -20% (earnings, guidance)

-MDB -19% (earnings, guidance)

-MRVL -18% (earnings, guidance)

-SNBR -15% (earnings)

-VRME -14% (earnings; files to sell $15.8M in stock)

-LPSN -13% (earnings, guidance)

-ONL -13% (earnings, guidance)

-RGTI -10% (earnings)

-GRND -9.6% (earnings, guidance)

-HIMS -8.2% (TDOC adds GLP-1 Self-Pay Option to Comprehensive Weight Care)

-GMS -7.0% (earnings, guidance)

-EDIT -5.9% (earnings)

-CMPO -5.6% (earnings, guidance)

-DSGX -5.3% (earnings)

-M -5.3% (earnings, guidance)

-YEXT -5.2% (earnings, guidance)

-TTC -3.2% (earnings, guidance)

-VSCO -3.2% (earnings, guidance)

-NVO -2.8% (CEO: Not immune to US tariffs; moving towards producing US product in-country)

-TSLA -2.7% (hearing price target cut at Baird)

BY Doug Kass · Mar 6, 2025, 9:13 AM EST

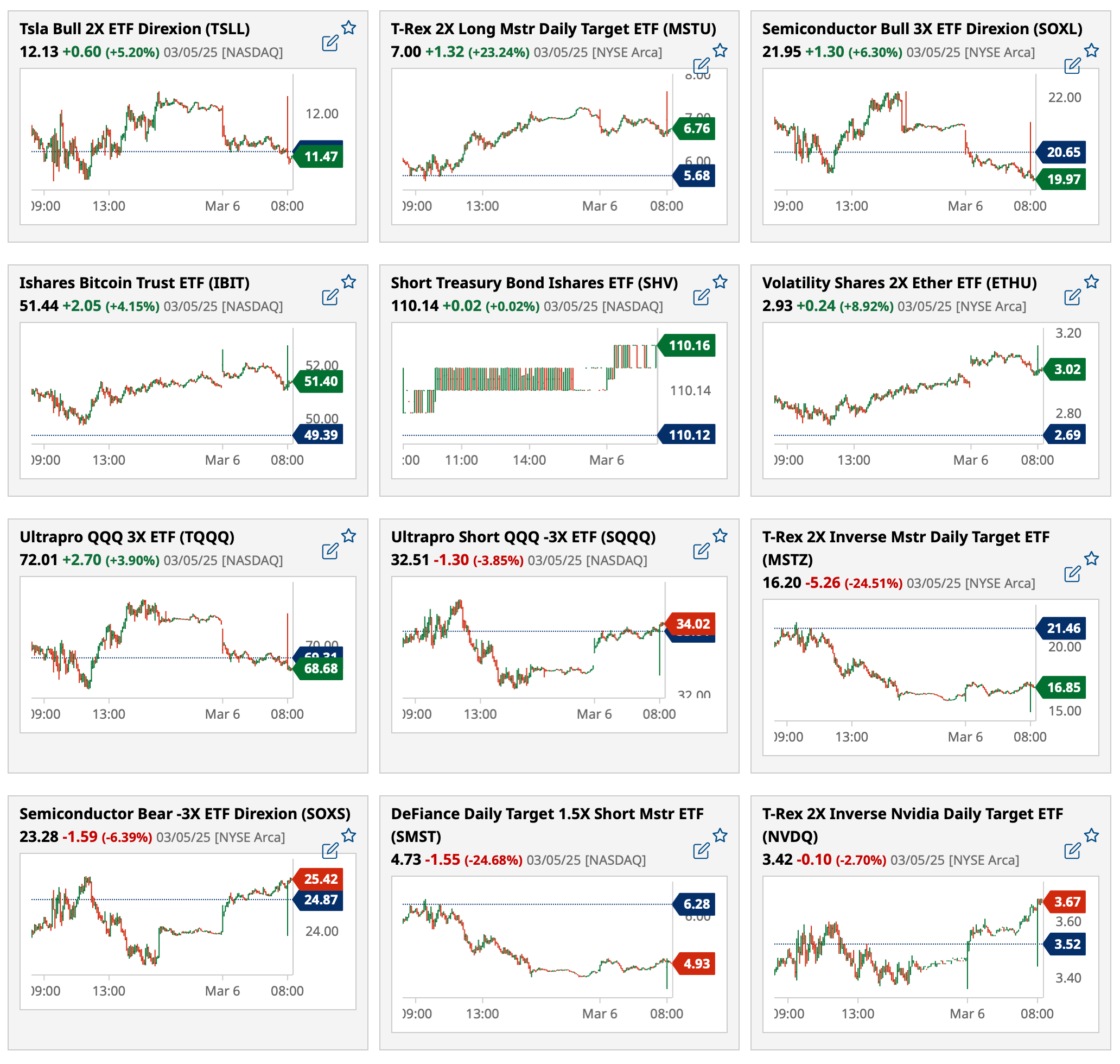

Most active premarket ETFs at 8:14 a.m. ET:

BY Doug Kass · Mar 6, 2025, 9:05 AM EST

Premarket percentage movers at 8:31 a.m. ET:

BY Doug Kass · Mar 6, 2025, 8:50 AM EST

8:45 a.m.: Fed Bank of Philadelphia President Harker (Non-Voter) speaks on "Economic Education" before the National Association of Economic Educators 2025 Spring Professional Development Conference, Philadelphia, PA

3:30 p.m.: Fed Board Governor Waller (Voter) speaks on the economic outlook before the Wall Street Journal CFO Network Summit, NYC

1:00 p.m.: The Federal Reserve Board, Office of the Comptroller of the Currency and the Federal Deposit Insurance Corporation host a virtual meeting to receive public comments consistent with the Economic Growth and Regulatory Paperwork Reduction Act of 1996 (EGRPRA) about their regulations that may be outdated, unnecessary, or unduly burdensome;

7:00 p.m.: Fed Bank of Atlanta President Bostic (Non-Voter) participates in a conversation on the economic outlook with some focus on the Birmingham region, Birmingham, AL

BY Doug Kass · Mar 6, 2025, 8:35 AM EST

BY Doug Kass · Mar 6, 2025, 8:05 AM EST

I will be attending a business conference between 11 a.m. and 2 p.m. today.

BY Doug Kass · Mar 6, 2025, 7:45 AM EST

BY Doug Kass · Mar 6, 2025, 7:25 AM EST

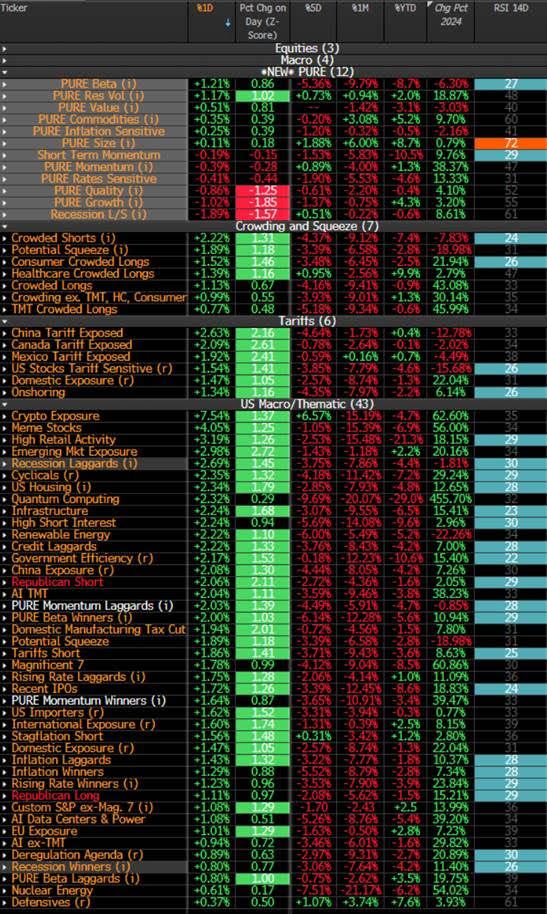

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Mar 6, 2025, 7:15 AM EST

From JPMorgan:

US: Futs are lower led by Tech. Mag 7 are underperforming: NVDA (-1.8%), TSLA (-1.6%) and META (-1.5%) pre-market. 10y is +2.5bp higher while 2y is -1.5bp lower this morning; USD is lower. Commodities are mixed: oil saw small gain (+0.5%) after yesterday’s selloff; basic metals are rallying this morning, while precious metals are lower. Since yesterday’s close, the equity weakness was not contributed by single catalyst but more due to a number of macro uncertainties (the auto tariffs delay will not resolve the tariffs risks; more evidence of sentiment impacts from Beige book) and rotation to international stocks. Today, we will hear from AVGO on AI outlooks; MRVL fell -15% post earnings release yesterday (after-market) despite numbers are mostly in line with expectation.

and...

EQUITY AND MACRO NARRATIVE: Stocks finished higher yesterday on the back of Lutnick’s comments on potential relief on Canada/Mexico tariffs, but markets have given back most of the gains this morning. While Tuesday’s tariff comments “meet in the middle” were initially interpreted as potentially lowering tariff risk, Lutnick’s Bloomberg interview and the 1PM White House press briefing yesterday both commented on keeping the 25% level but having exceptions (such as autos) from the tariffs. Stocks rallied on the back of eased tariff pressure yesterday afternoon. Does this ease any tariff risks in the near-term? We don’t think so. While equities seem to be more optimistic on lower tariff risks, we still face a high level of uncertainty: (i) the auto tariffs is only delayed, not fully excluded; (ii) Canadian officials commented on “Canada won’t scrap tariffs unless all US levies are lifted” suggested potential further escalation; (iii) the April 2 reciprocal tariffs have been reiterated by both the press briefing and Lutnick’s comments. Outside tariffs, the progress on reconciliation bill has not been successful: CBO reports found that “Republicans can’t achieve their goal of slashing $2 trillion in federal spending over the next decade without cutting Medicaid” (THE HILL).

Beyond US equities, we saw outperformance in both EMEA and APAC. Tuesday’s NPC in China boosted the China Tech sector (KWEB +7% yesterdsay). JPM Economist Haibin Zhu pointed out that the policy targets from the NPC so far have been largely in line with consensus, but price actions suggest more optimism around China growth and tech revival.

BY Doug Kass · Mar 6, 2025, 7:00 AM EST

Bonus —Here are some great links:

BY Doug Kass · Mar 6, 2025, 6:45 AM EST

Continuing the tactics of buying extreme weakness and selling extreme strength in a "sawtooth pattern (lower)."

I have taken a long trading rental in the Indices with S&P futures -71 handles:

* SPY $576.28

* QQQ $495.24

BY Doug Kass · Mar 6, 2025, 6:35 AM EST

* We have no long positions in energy the sector...

It was the majority view, in fact a near unanimous view in the business media (and elsewhere), that energy stocks were the ideal "value play" and would benefit from a rotation out of Mag 7.

This clearly has not proven to be the case:

Indeed, many energy stocks (like OXY, XOM, CVX, SLB, etc.) fell through the bottom of their recent trading ranges and have broken down conspicuously in trading yesterday.

Given the uncertain trajectory of domestic economic growth and the uncertain energy policy of the current administration I feel it is too early to place a bet on energy stocks — despite the apparent values (as measured by most traditional metrics).

We have no long positions in the energy sector at the current time.

BY Doug Kass · Mar 6, 2025, 6:25 AM EST

The S&P Short Range Oscillator remains oversold at -5.00% vs. -5.12%.

In an oversold like this, I am (tactically) inclined to buy weakness (as I did early this morning, covering my Index shorts with S&P futures -60 handles).

Here is the issue — we are oversold, but is it still in a bull phase (and long-term uptrend) or are we in a developing bear phase where the uptrend will be violated?

As noted in yesterday's opener (and market outlook) I think it is the latter.

BY Doug Kass · Mar 6, 2025, 6:10 AM EST

I got shorter (in SPY/QQQ) in the ramp late yesterday afternoon.

As noted in my tweet (4:32 a.m.) early this morning I have covered those shorts and moved back to delta neutral in my Index positions:

BY Doug Kass · Mar 6, 2025, 5:59 AM EST

* S&P futures are -60 handles at 4:45 a.m...

Several of my trader friends, who like me, get up early, are asking why stock futures are so weak.

Besides some uninspiring post-market EPS releases I suspect this is contributing to the overall weakness:

* Microsoft MSFT has withdrawn from some of its commitments with CoreWeave ahead of the cloud company's IPO.

From Bloomberg: Microsoft Reduces Commitments to CoreWeave Ahead of IPO: FT - Bloomberg:

Microsoft Corp. has withdrawn from some of its commitments with cloud computing provider CoreWeave due to delivery issues and missed deadlines, the Financial Times reported on Thursday.

New Jersey-based CoreWeave, which provides data center technology, filed for an initial public offering this week that could raise about $4 billion and is expected to target a valuation greater than $35 billion, Bloomberg News has reported. Microsoft is by far its largest customer, but it has walked away from some agreements over delivery issues and missed deadlines, the FT said, citing unnamed people familiar with the situation.

Nvidia Corp. also has a close relationship with CoreWeave, holding a stake in the startup and also counting it as a major customer for its AI-focused GPUs. Representatives of Microsoft and Nvidia declined to comment for the FT.

The relationship with Microsoft is a closely watched factor as CoreWeave builds toward its IPO. The Windows maker and AI data center operator accounted for 62% of CoreWeave’s revenue in 2024, according to the startup’s disclosures. Changes in demand from Microsoft could adversely affect CoreWeave’s business, the company said in its S-1.

Here is more from Reuters: Microsoft withdrew some CoreWeave agreements over delivery issue, FT reports | Reuters

BY Doug Kass · Mar 6, 2025, 5:45 AM EST