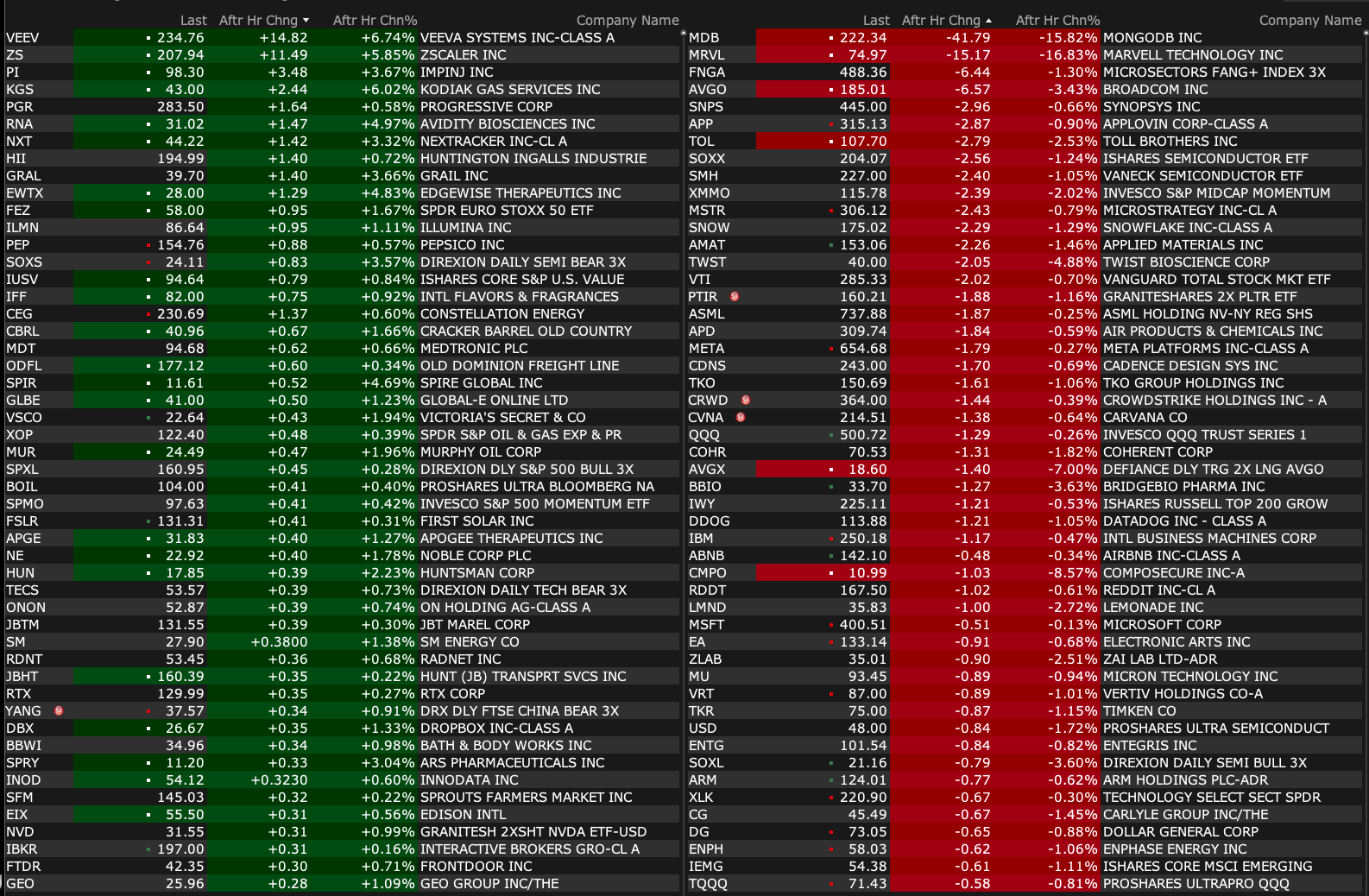

Wednesday's After-Hours Movers

As of 4:22 p.m.:

BY Doug Kass · Mar 5, 2025, 4:47 PM EST

As of 4:22 p.m.:

BY Doug Kass · Mar 5, 2025, 4:47 PM EST

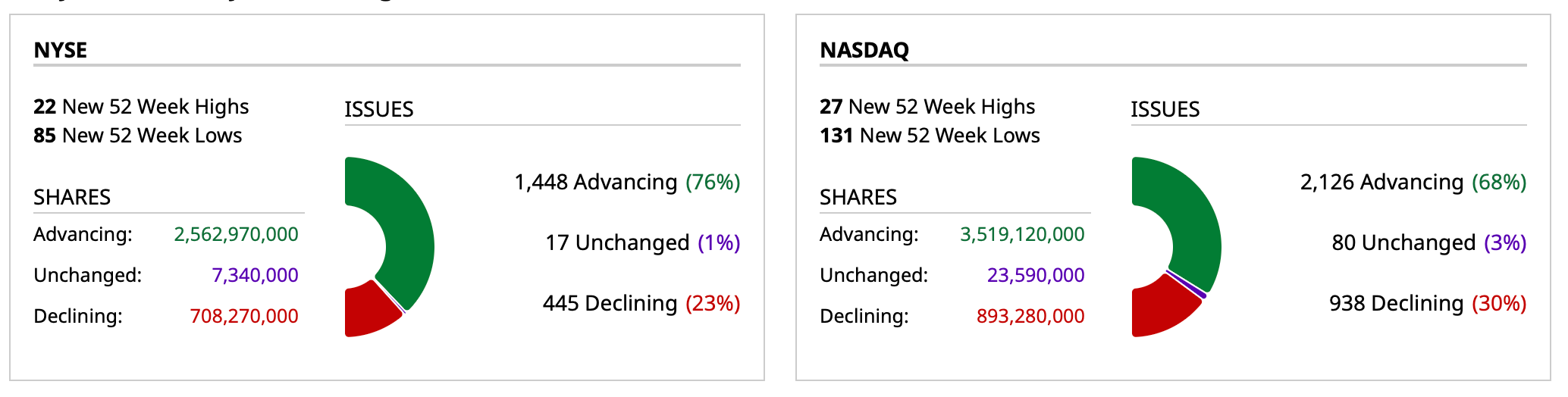

- NYSE volume 9% above its one-month average

- NASDAQ volume 3% below its one-month average

- VIX index: down 6.93% to 21.88

BY Doug Kass · Mar 5, 2025, 4:35 PM EST

Investment short Sleep Number SNBR misses on sales again.

The share price is down another -$1.50 (or -13%) in post-market trading.

Here is the full release.

Sleep Number Corporation - Sleep Number Announces Fourth Quarter and Full Year 2024 Results

BY Doug Kass · Mar 5, 2025, 4:08 PM EST

* On the ramp...

Selling more SPY $584.32 and QQQ $502.56 with the lift of S&P futures close to +80 handles.

BY Doug Kass · Mar 5, 2025, 3:36 PM EST

Another very volatile day.

Up, down, up, down, very up.

Again, great for opportunistic traders... not so much for the buy-and-hold crowd.

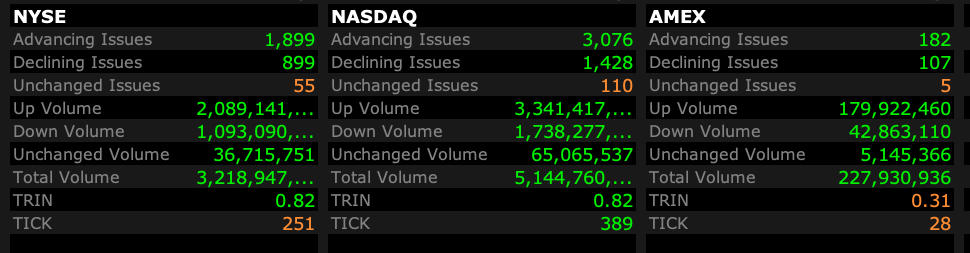

Breadth on both the NYSE and Nasdaq are about 2-1 positive (and steadily improved during the day):

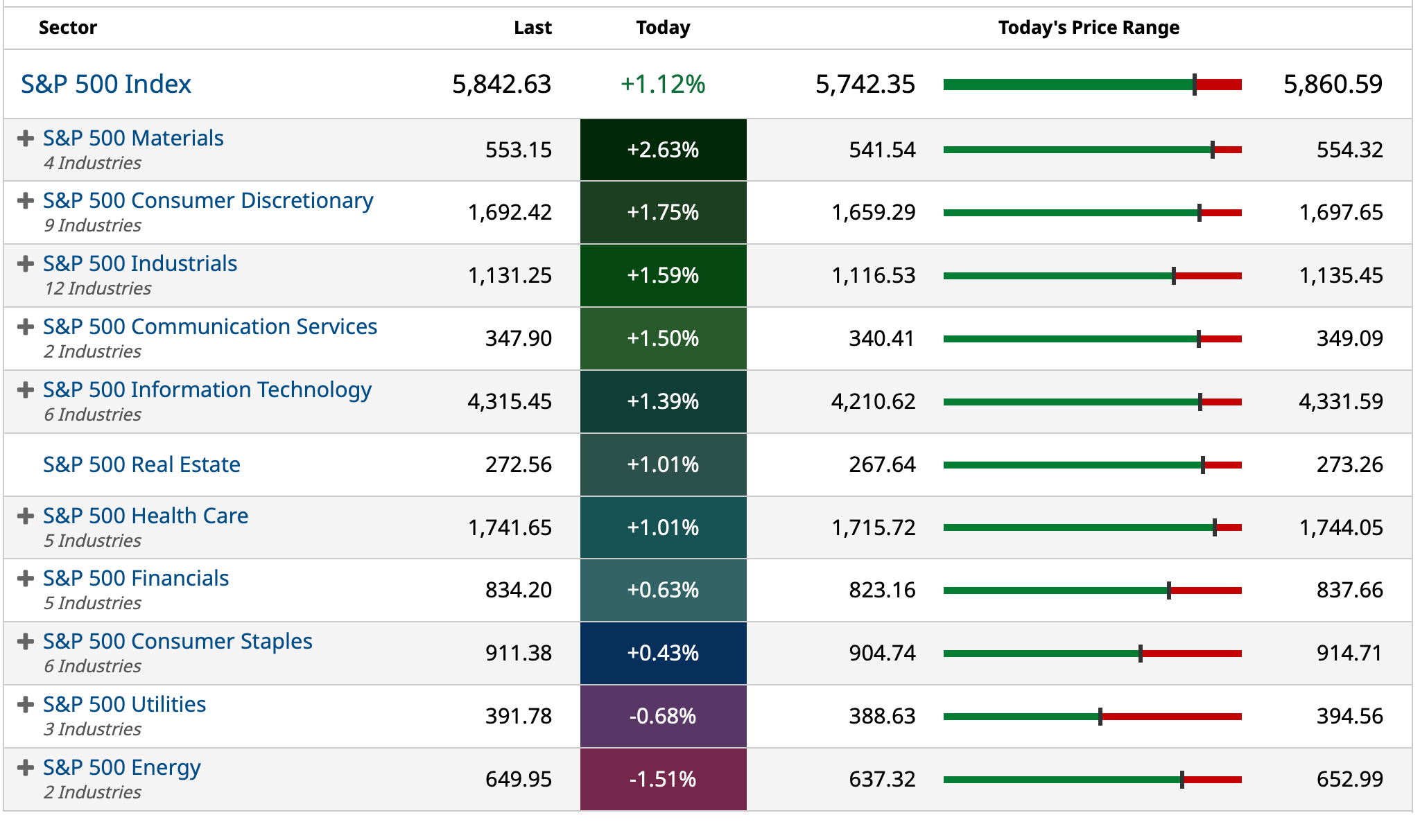

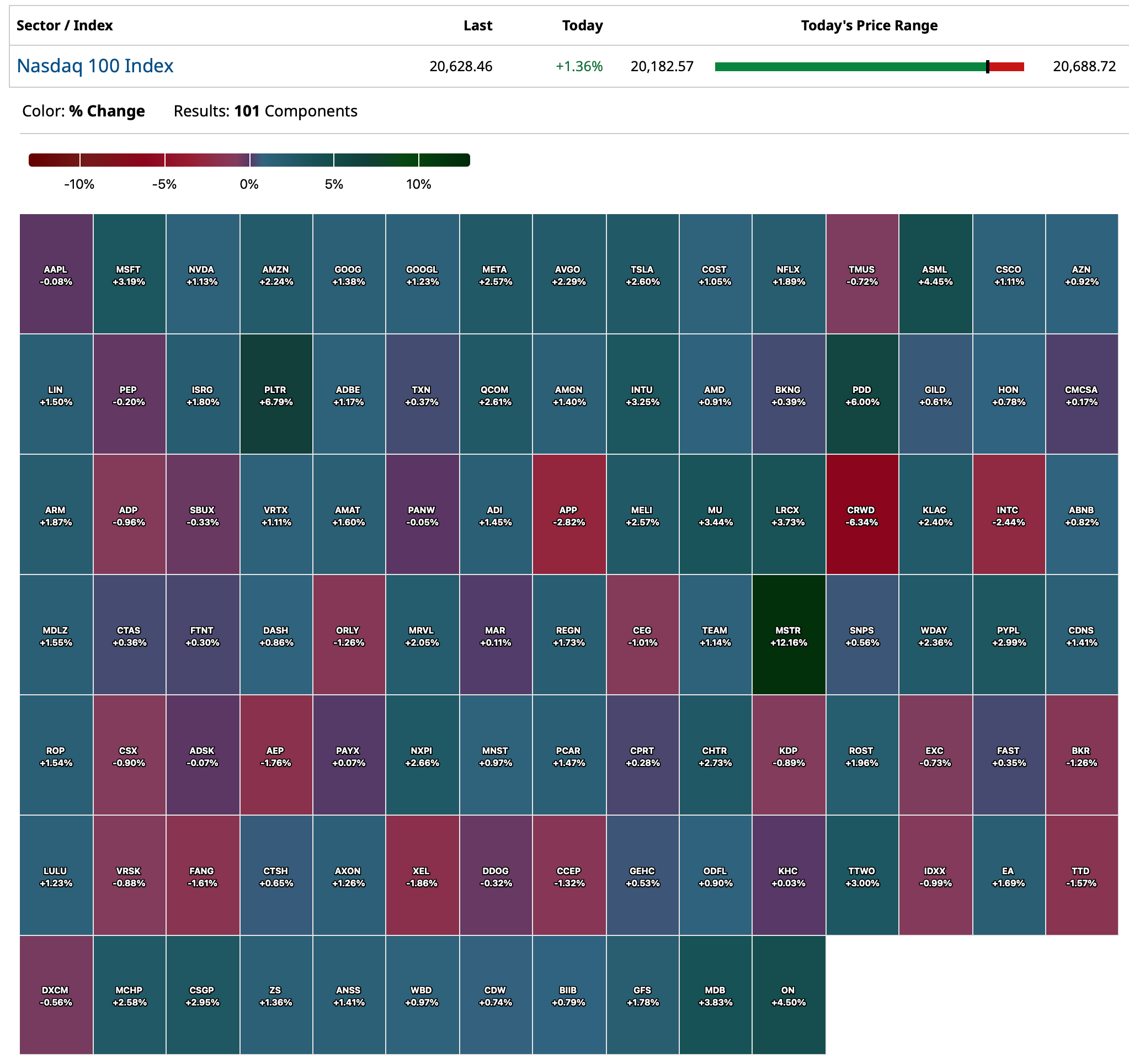

At 2:45 PM the S&P Index is up by +67 handles.

Here are the things I did today:

* I actively traded SPY/QQQ common — three profitable trades.

* Added to MSOS at $2.80, AYRWF at $0.265, CURLF at $1.04, GTBIF at $6.60 and TSNDF at $0.39.

* Shorted AAPL at $236.02.

BY Doug Kass · Mar 5, 2025, 3:00 PM EST

With the S&P Index +51 handles I have moved from delta-adjusted neutral to slightly net short Indices.

This has been quite a move off of support when the S&P cash was -37 handles a brief time ago.

BY Doug Kass · Mar 5, 2025, 2:10 PM EST

Since today's MRKT CALL with EY, Guy and Dan was particularly rich in data and observations, I wanted to pass on a recording of it!

But more importantly, I wish EY from SOFI (Liz Young Thomas) a great rest of her pregnancy and a wonderful/effortless birth of her first child ("the next Warren Buffett") ahead.

Let's go to the tapes. What To Buy If Tariff Wars Reverse

BY Doug Kass · Mar 5, 2025, 2:00 PM EST

* This is BEFORE tariffs (!)...

BY Doug Kass · Mar 5, 2025, 1:50 PM EST

BY Doug Kass · Mar 5, 2025, 12:44 PM EST

TechNova

Tariffs : These Tariffs if left in place, amount to the largest Tax imposed on US businesses in over 30 years.

Given compressed margins, I expect the vast majority of this Tax to be passed on to the consumer.

This will have a chilling effect on Consumer Confidence and GDP.

I have mentioned this at the start of my PIVOT notices.

There will be no choice but to lower interest rates, there will be no choice but to rain cash on people, there will be no choice but to debase our currency, and there will be no choice but to Balloon our Fiscal Deficit.

Donnie calls himself "The King of Debt". Now that he is King, why would he change the full moniker?

NOTE : The world spent millions disarming Germany after 2 wars, now Trump is rushing its re-armement just as we witness the largest rise in the AFD party in Germany since WWII.

BY Doug Kass · Mar 5, 2025, 12:30 PM EST

* Ideal for opportunistic traders who are unemotional.

* Not so great for the buy/hold crowd.

The S&P has rapidly rallied from -35 handles to up small on the auto tariff delay. (Get used to this volatility and lack of predictability!)

I just sold out the trading long rentals (purchased a few minutes ago) for a profit:

* SPY $576.93

* QQQ $494.36

I am back delta-adjusted neutral in the Indices.

From 11:30 AM:

As I wrote in my opener today, I expect a test of yesterday's lows.

In the case of (SPY) , we are now within $2 of that test. ( (QQQ) s are $5 higher than the Tuesday lows.)

The oversold is growing and I just added to my Index long trading rentals:

* (SPY) $574.21

* (QQQ) $492.67

Position: Long SPY common (M), QQQ common (M); Short SPY calls (M), QQQ calls (M)

By Doug Kass Mar 5, 2025 11:25 AM EST

BY Doug Kass · Mar 5, 2025, 12:11 PM EST

* Winnebago continues to be a "No Drama" short...

The shares of investment short WGO are down by another -$2.50/share today at $34.80 (and below the 52-week high of $73 and at a new one year low)!

Vince: "That's what good actors do, they listen. Right, Johnny?

Johnny: "What?”

No Drama.

BY Doug Kass · Mar 5, 2025, 11:50 AM EST

As I wrote in my opener today, I expect a test of yesterday's lows.

In the case of SPY, we are now within $2 of that test. (QQQs are $5 higher than the Tuesday lows.)

The oversold is growing and I just added to my Index long trading rentals:

* SPY $574.21

* QQQ $492.67

BY Doug Kass · Mar 5, 2025, 11:25 AM EST

* The general lack of "predictability" in policy (and in turn, economic growth) is rising.

* We continue to expect this year's market to be much different than last year's market.

* I estimate that downside market risk is roughly 2-3x upside market reward.

* My 2025 forecast for a 10% to 15% drop in the S&P Index remains intact.

Since mid-February, equities (led by large-cap technology and the Magnificent Seven) have begun to roll over, consistent with my expectation that January 2025 may mark the top in equities for the year (and analogous with the January 1973 peak in the broader market and the end to The Nifty Fifty leadership/dominance and cycle):

The several-week rotation away from large-cap tech (and The Magnificent 7) is growing more conspicuous. Through Tuesday the Mag 7 is -10% (year-to-date) or double the decline of the Nasdaq Index and compared to only a couple percentage drop in the S&P 500 Index.

As noted recently (below) I believe the market is on a path for a 10-15% decline this year. (Note: Precision is not intended!)

The expected downturn will not likely come in a straight line. It is my view that machines and algos will exaggerate moves up and down, contributing to a sawtooth pattern lower.

I might be wrong but this is my baseline expectation upon which I tactically manage my hedgefund, Seabreeze Partners.

Responding to the market selloff, fear and negative investor sentiment has risen over the last few weeks:

Fear and Greed Index - Investor Sentiment | CNN

With seven out of the last eight days lower for the S&P Index, the CNN Fear & Greed Index highlighting "Extreme Fear" (above), the S&P Short Range Oscillator moving to a deeper oversold (-5.12%) and the S&P Index hitting (at their nadir Tuesday morning) an important support line, I was not surprised (and I took a small trading long rental in the Indices!) that stocks exhibited a powerful reversal higher Tuesday afternoon (and in stock futures this morning):

I do not expect the recovery in stocks (seen in the last 12 hours) to be long lasting or the start of another leg in the bull market that we have witnessed over the last two years.

My multiple concerns are now well known — stubborn inflation and sluggish economic growth ("slugflation"), fiscal and monetary policy risks, elevated valuations, rising geopolitical threats, etc.

We can now add the Trump administration's agenda and policy impact on inflation, economic growth and the Federal Reserve's policy decisions. Specifically, I am concerned about the poorly thought out and current implementation of tariffs, which will serve to raise prices, slow economic activity, increase unemployment, worsen inequality, diminish productivity and raise global tensions.

I am fearful that the lack of predictability of current economic (and tariff) policy, in and of itself, may contribute to delayed capital and consumer spending — and even slower economic growth than I currently anticipate.

Finally, as noted in the nearly 70 columns in my "More Tales From Nvidia" series (since June 2024), I expect AI capital spending to go through a digestive phase this year. So, with their outsized market weightings, the averages will likely be adversely impacted. Already six of the seven Mag 7 companies have reduced first-quarter 2025 revenue guidance. I anticipate cuts in Mag 7 EPS estimates for the second half of 2025.

Here is a mid-February recap of my 2025 market outlook:

* Updating my market outlook...

What goes up must come down

Spinning Wheel got to go 'round

Talkin' 'bout your troubles

It's a cryin' sin

Ride a painted pony

Let the Spinning Wheel spin

You got no money, you got no home

Spinning Wheel all alone

Talkin' 'bout your troubles and you

You never learn

Ride a painted pony

Let the Spinning Wheel turn

- Blood, Sweat and Tears, Spinning Wheel

I continue to be deeply skeptical of the market's advance and I am maintaining our cautious investment strategy in the belief that equities are braced for a decline this year.

We believe that we are close to 2025's high in the averages and that downside is now roughly 3x the upside.

Investors should now be fearful of the excessive market optimism.

Nine days before the 1929 stock market crash that led to the Great Depression, Dr. Irving Fisher, an economist at Yale University, famously said (at the Purchasing Agents Association Dinner in New York City):

“Stock prices have reached what looks like a permanently high plateau.”

Fisher's prediction is considered one of the most notorious stock market forecasts of all time. The market's crash cost Fisher much of his wealth as well as his academic reputation.

Coincident with two back-to-back +20% annual returns in the S&P Index, a developing and confident bullish market narrative has emerged — which is eerily reminiscent of Dr. Fisher's 1929 comments:

"Increasingly, at least from my perspective, the U.S. stock market's new valuation range (after 30 years its probably misleading to continue calling it new) appears to be permanent."

- The Daily Chartbook

Despite the near universal optimism in investor sentiment (as expressed in historically low cash reserves and most classical metrics and valuations above the 95% tile) there are rarely new eras — excesses are never permanent.

As noted last month, I remain of the view that we are not in a new (and permanently high) valuation paradigm for equities and that an important top in the U.S. stock market may be close at hand:

December marked the beginning of what we expect to be a lower-trending market accompanied by rising volatility.

We expect 2025 to look far different than 2024.

While we predominantly focus on an assessment of reward vs risk on individual stocks — if we were forced to hazard a precise forecast we would project only about a five percent upside and a ten to fifteen percent downside for the S&P 500 Index in 2025.

Today's commentary will explain why heady valuations are rarely a good launching pad for higher stock prices.

We will explore and summarize some of our fundamental near and intermediate-term concerns.

We will compare today with early 1973 (which marked the end of the Nifty Fifty era) and produced years of subpar returns for the major market averages. Then, we will highlight some longer-term existential market threats that few discuss, but that have a reasonable chance of emerging.

Finally, we will explain why the numerous uncertainties and headwinds provide a fertile basis for investors to prosper (absolutely and on a relative basis) in searching for asymmetric investment opportunities — and why a top-heavy, technology-led market (which has not broadened) has already begun to deliver some developing long opportunities with upside rewards that dwarf downside risks.

As I also recently wrote:

Many of our fundamental concerns (growing policy (fiscal and monetary) risks, sticky inflation, slowing economic growth and rising interest (higher for longer)) are finally beginning to be accepted by investors — at a point in time in which valuations are elevated and consensus corporate profit estimates seem too optimistic. We are increasingly more confident that stocks will correct to more attractive levels than exist right now — at which time we can begin to accumulate selected stocks that meet our investing criteria and standards.

BY Doug Kass · Mar 5, 2025, 10:02 AM EST

Given the oversold condition, I have taken another trading long rental in the indexes:

* SPY $576.75

* QQQ $494.10

BY Doug Kass · Mar 5, 2025, 9:44 AM EST

Adding to MSOS, Terrascend (TSNDF) and GTBIF.

BY Doug Kass · Mar 5, 2025, 9:40 AM EST

BY Doug Kass · Mar 5, 2025, 9:40 AM EST

* According to Steve Rattner...

BY Doug Kass · Mar 5, 2025, 9:30 AM EST

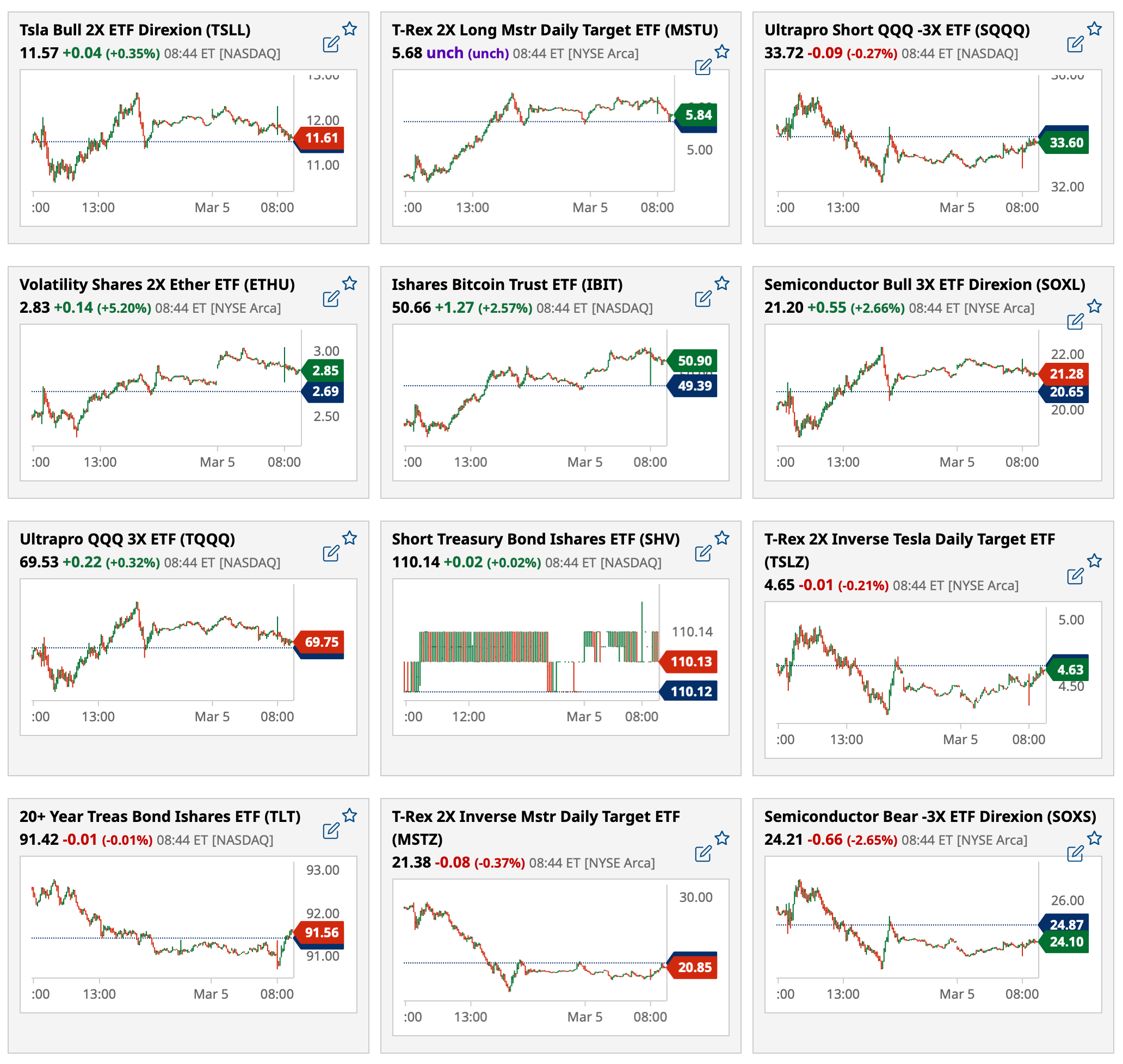

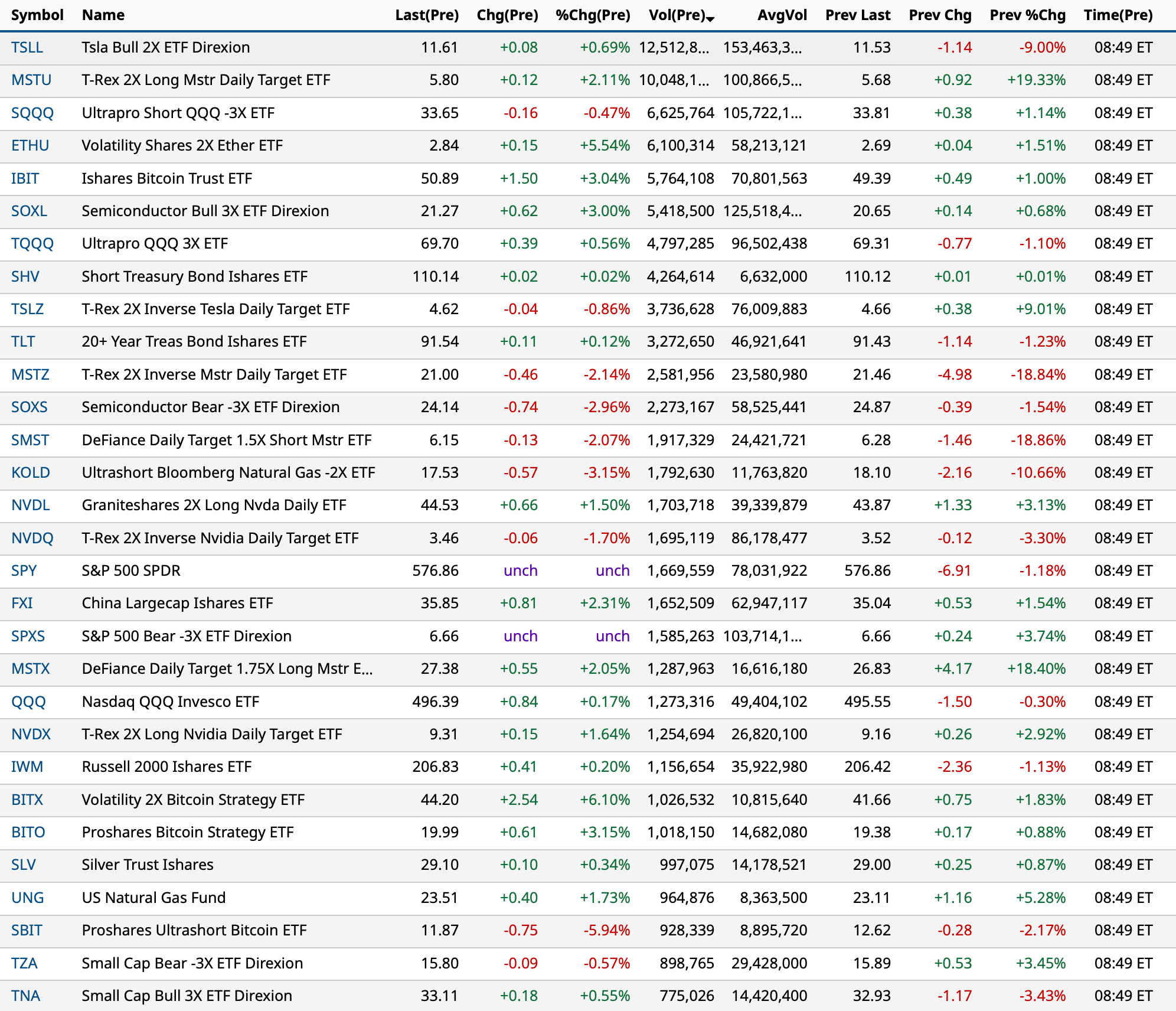

Most active premarket ETFs as of 8:49 a.m. ET:

BY Doug Kass · Mar 5, 2025, 9:26 AM EST

BY Doug Kass · Mar 5, 2025, 9:20 AM EST

-CMRX +69% (to be acquired by Jazz at $8.55/shr in cash)

-TENX +15% (expands Phase 3 LEVEL Program, advancing two TNX-103 (Oral Levosimendan) Registrational studies for treatment of PH-HFpEF; announces $25M Private Placement at $6.04/shr)

-CDXC +11% (earnings, guidance)

-CTOS +10% (earnings, guidance)

-HII +10% (strength off President Trump comments to potentially create Office of Shipbuilding)

-MRNA +8.3% (CEO bought 160K shares at avg price of $31.22/shr)

-STLA +8.1% (President Trump suggests potential tariff ‘carve outs’ for auto industry; momentum from EU relaxing CO2 laws)

-GSL +6.2% (earnings)

-REVG +6.2% (earnings, guidance)

-GM +5.3% (President Trump suggests potential tariff ‘carve outs’ for auto industry)

-CERO +4.5% (new poster to highlight preclinical data of CER-1236 in ovarian cancer)

-NVO +4.5% (introduces NovoCare Pharmacy, lowering cost of all doses of FDA-approved Wegovy (semaglutide) to $499/month and offering easy home delivery for cash-paying patients)

-SCCO +4.3% (copper prices rise after Trump comments that imports of copper could be subject to 25% tariff)

-EOSE +4.1% (earnings, guidance)

-FCX +3.7% (copper prices rise after Trump comments that imports of copper could be subject to 25% tariff)

-SWIM +3.7% (earnings, guidance)

-FLNC +3.6% (Mizuho Securities Initiates FLNC with Outperform, price target: $8)

-PR +3.6% (Susquehanna Raised PR to Net Positive from Net Neutral, price target: $20)

-ACI +3.4% (to replace AZPN in S&P MidCap 400 Index)

-ATRO +3.4% (earnings, guidance)

-BF.B +2.8% (earnings, guidance)

-ANET +2.4% (UBS Raised ANET to Buy from Neutral, price target: $115)

-CIFR +2.4% (reports Feb BTC production)

-F +2.2% (President Trump suggests potential tariff ‘carve outs’ for auto industry)

-GEV +2.2% (Guggenheim Securities Raised GEV to Buy from Neutral, price target: $380)

-CARR +2.1% (partners with Google Cloud to Strengthen Grid Resilience with AI-Powered Home Energy Management Systems; JPMorgan Chase and Co Raised CARR to Overweight from Neutral, price target: $78)

-CUTR -40% (files for Chapter 11 bankruptcy)

-AVAV -22% (earnings, guidance)

-ORN -12% (earnings)

-THO -9.1% (earnings, guidance)

-ANF -7.8% (earnings, guidance)

-CRWD -7.4% (earnings, guidance)

-CPB -6.6% (earnings, guidance)

-CRDO -6.3% (earnings, guidance)

-BOX -6.2% (earnings, guidance)

-SMRT -5.4% (earnings)

-SSYS -2.7% (earnings, guidance)

-FL -2.4% (earnings, guidance)

BY Doug Kass · Mar 5, 2025, 9:20 AM EST

BY Doug Kass · Mar 5, 2025, 9:15 AM EST

Premarket percentage movers as of 8:24 a.m. ET:

BY Doug Kass · Mar 5, 2025, 8:55 AM EST

BY Doug Kass · Mar 5, 2025, 8:45 AM EST

"Where you want to be is always in control, never wishing, always trading, and always, first and foremost protecting your butt."

- Paul Tudor Jones

Bonus - here are some great links:

Decision Time Decision Time

Rotation vs Distribution Rotation vs Distribution

Today's Number is 2021 The Daily Number 💯 Tuesday, March 4, 2025

Post Election Years Plague Republicans Almanac Trader — Post-Election Years Plague Republicans

Technical Tuesdays

BY Doug Kass · Mar 5, 2025, 8:35 AM EST

This brief post is apropos to my criticism of the (often) superficial company commentary on the business media.

The conversations on Apple AAPL continue to be superficial.

Yes, Apple generates amazing yearly free cash flow. But I have emphasized that the sizeable company buybacks have depleted Apple's net cash (gross cash less debt) over the last year (during much of the period I have been short).

The (lazy) business media's "talking heads" have done little balance sheet analysis, instead dwelling on the aggressive capital allocation strategy (of buying back stock) without observing the simple fact that buybacks have depleted the company's cash hoard.

BY Doug Kass · Mar 5, 2025, 8:20 AM EST

BY Doug Kass · Mar 5, 2025, 8:10 AM EST

Summary of Wall Street Journal's observations:

· Doubled down on tariffs

· Pushing to stop the RU/UKR war

· Selling DOGE efforts

· Biden blame

· Democratic resistance

· Ramping up mass deportations

· A night of theatrics

BY Doug Kass · Mar 5, 2025, 8:00 AM EST

From JPMorgan:

US: Futs are higher following Lutnick comments that a compromise on Canadia/Mexican tariffs could be announced today; Trump’s speech double-down on tariffs but did not refute Lutnick’s comments. The US/UKR mineral deal appears to be moving forward. There appears to be an off-ramp for China; China began announcing its stimulus measures at its NPC. Pre-mkt, All 7 of Mag7 are higher and Semis are bid into MRVL earnings. Bond yields are flat, USD is weaker and cmdtys are mixed. Energy is lower, Ags higher, and precious over base. Today’s macro data focus is on ISM-Srvcs, Factory Orders, Mtge Applications, and ADP.

and...

EQUITY AND MACRO NARRATIVE: Oh No. Whippy. Squeezy. We’re Sooo Back … these are some of the phrases during yesterday’s session which saw the SPX trade in a 2.3% range, including a substantial decline into the bell from a previously positive position. From a sector perspective, TMT was the key driver of the index and some of the Delta One baskets that led are tied to the Retail Investors such as Crypto, High Short Interest, AI, and its ancillary plays. The rationale for the moves is tied to an improved outlook in the Europe, a US/UKR mineral rights deal as a ceasefire proxy, or that Trump is likely to reopen the door to tariff negotiations starting with the Thursday call with Mexico’s Sheinbaum.

Has anything changed since we flipped bearish ~24 hours ago? Maybe. We are at the beginning of Trade War 2.0 and with Trump’s tariff study coming due on April 1 we make see blanket tariffs enacts shortly thereafter. The current tariffs are part of an executive order to combat an economic emergency; in that order is an ‘escalation clause’ pushing Trump to increase tariffs on any country that retaliates against the US. This is a long-winded way of saying that we (US Mkt Intel) expect this portion of the trade war to last until, at least, mid-April.

· WHAT WOULD MAKE YOU BULLISH AGAIN? (i) a de-escalation of the Trade War and removal/reduction of tariffs. Post-mkt, there was an interview with Lutnick that offered both strong words for tariff targets but also a potential off-ramp. First, he said that he thinks Trump will meet Mexico and Canada in the middle on tariffs, which could be announced as soon as today. Second, Lutnick says that if USMCA rules are followed that Trump would consider relief. Next, he mentioned that with China the US is not engaged in a Trade War but a Drug War which suggests that if fentanyl production falls. Lastly, he mentions that April 2 is about reciprocal tariffs and achieving fairness. (ii) if macro data inflects higher after the imposition of tariffs. This does not include today’s ISM-Srvcs or Friday’s NFP promise. (iii) if the Trump Put was activated yesterday. The positive press headlines came with the SPX falling towards 5,740 or ~6.5% below ATHs and Lutnick’s comments drove futures higher post-mkt; (iv) if we found a bottom in TMT/Mag7. While we had yet to see a full positioning flush, we had seen TMT much close to the end of its sell-off.

· WHAT WOULD MAKE YOU MORE BEARISH? We have already seen the negative impact that policy/trade uncertainty has had on both household and corporate spending, so it seems likely that we see a larger magnitude of this over the next month. Keep an eye on the unemployment rate, layoffs, WARN notices, etc. If we start to see the unemployment rate rising rapidly, then that likely which push the market back into the ‘Recession Playbook’ which dominated the first half of yesterday’s session. In case you missed it, we have reposted the bearish hypothesis a few sections below.

BY Doug Kass · Mar 5, 2025, 7:50 AM EST

BY Doug Kass · Mar 5, 2025, 7:43 AM EST

Importantly, the S&P Short Range Oscillator jumped from -3.16% to -5.12%, moving deeper into the oversold.

BY Doug Kass · Mar 5, 2025, 5:45 AM EST

Join us on spaces at 11am ET to talk charts and more! x.com/i/spaces/1Mnxn…