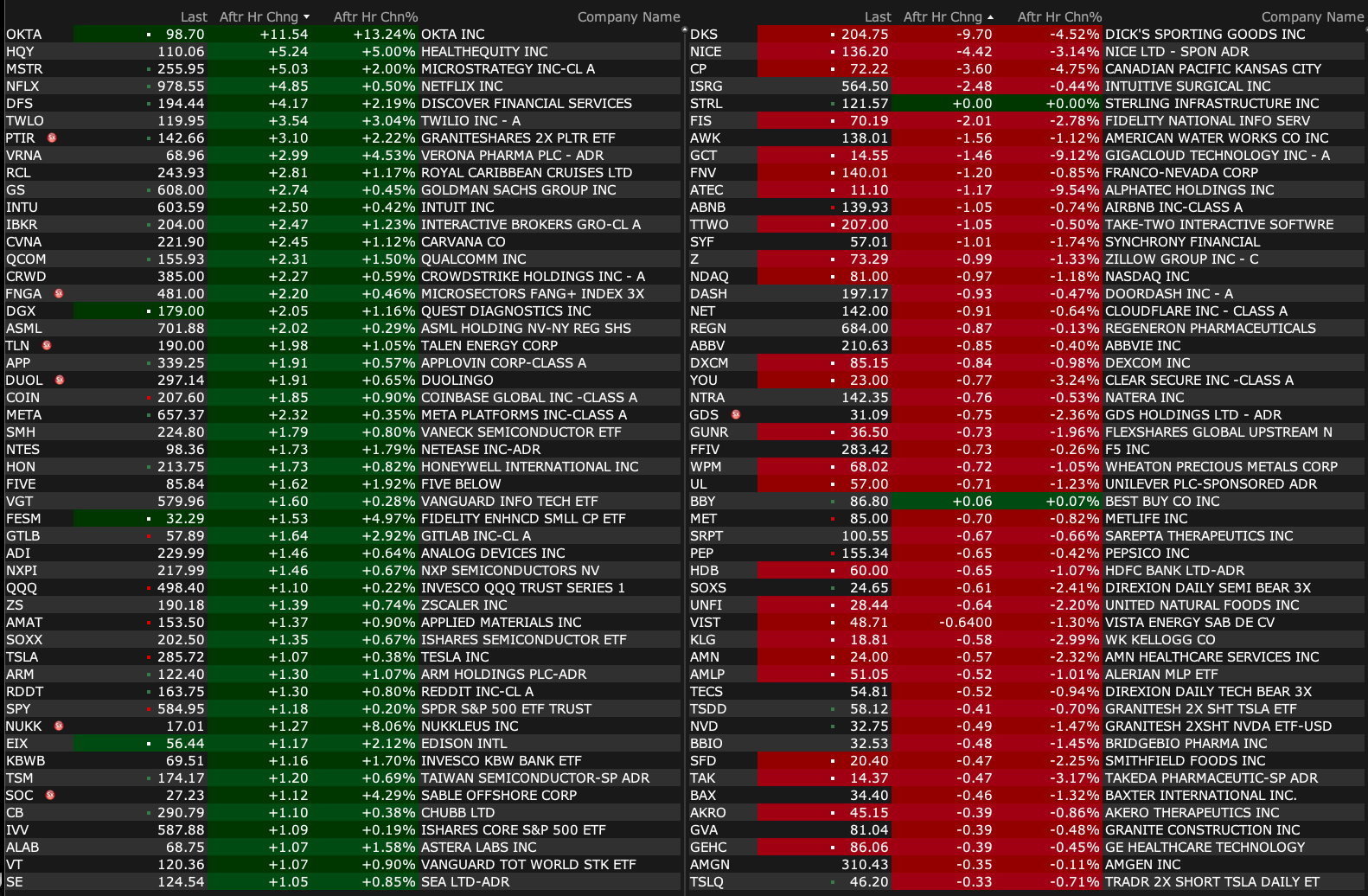

Monday's After-Hours Movers

As of 4:20 p.m.:

BY Doug Kass · Mar 3, 2025, 5:07 PM EST

As of 4:20 p.m.:

BY Doug Kass · Mar 3, 2025, 5:07 PM EST

BY Doug Kass · Mar 3, 2025, 4:56 PM EST

BY Doug Kass · Mar 3, 2025, 4:25 PM EST

BY Doug Kass · Mar 3, 2025, 3:48 PM EST

BY Doug Kass · Mar 3, 2025, 3:37 PM EST

With S&P cash -98 handles I have added to trading long rental in SPY at $583.92 and QQQ at $498.83.

BY Doug Kass · Mar 3, 2025, 3:15 PM EST

BY Doug Kass · Mar 3, 2025, 3:10 PM EST

With S&P cash -76 handles (and down a quick 37 handles in 15 minutes) I have added to longs in SPY at $586.64 and QQQ at $501.01.

BY Doug Kass · Mar 3, 2025, 3:05 PM EST

Another very volatile day.

Up, down, up down.

Again, great for opportunistic traders... not so much for the buy-and-hold crowd.

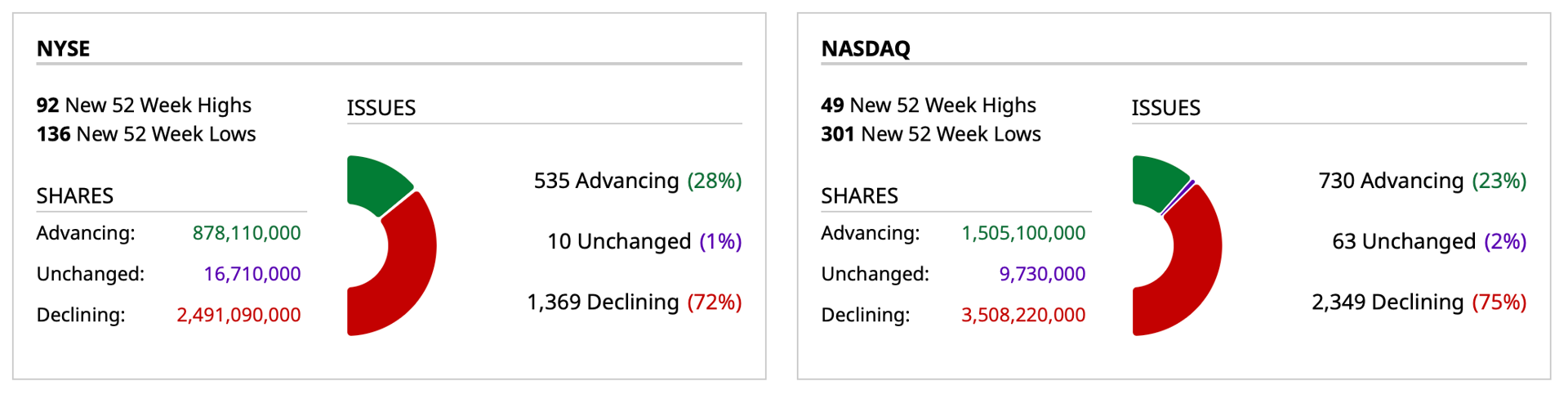

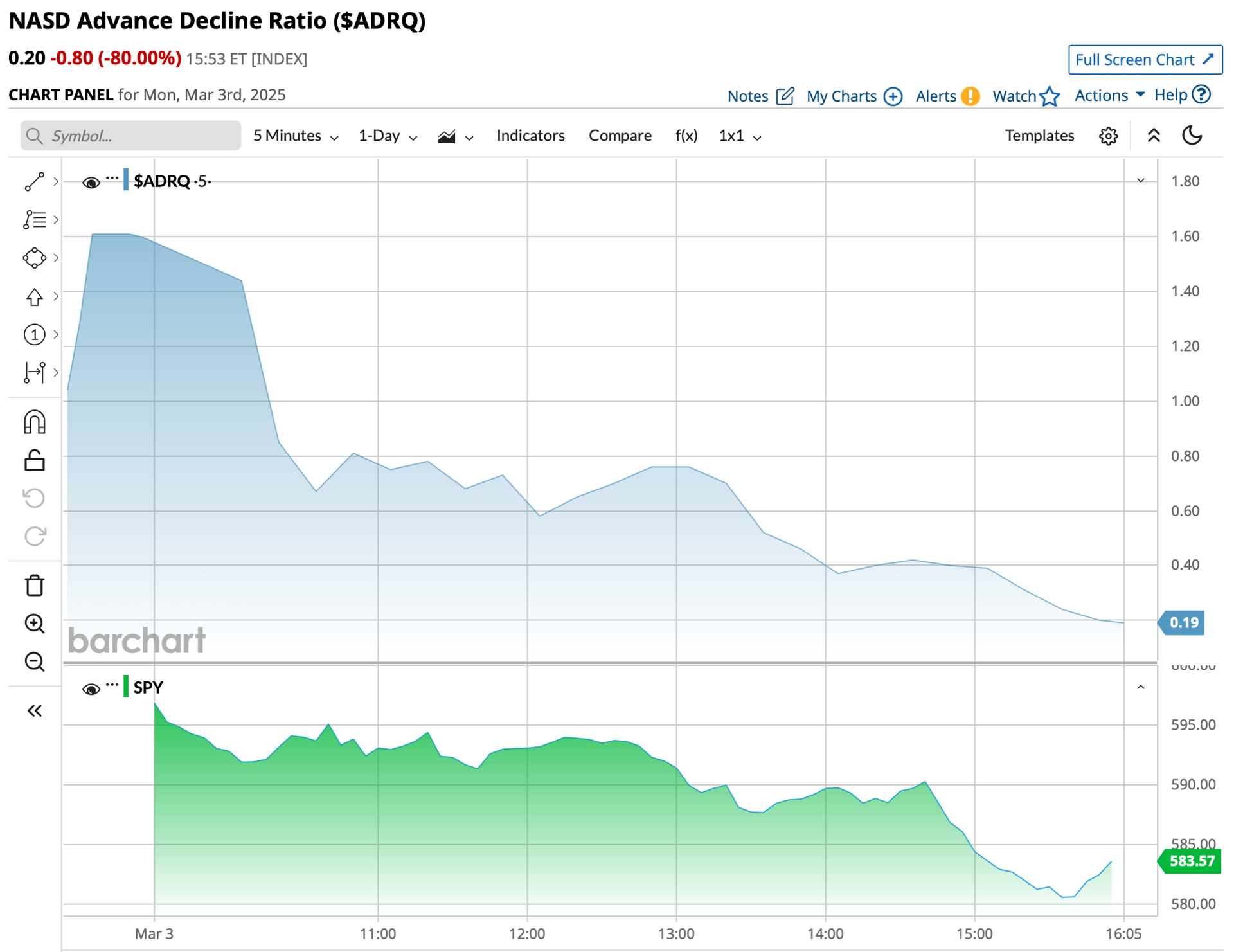

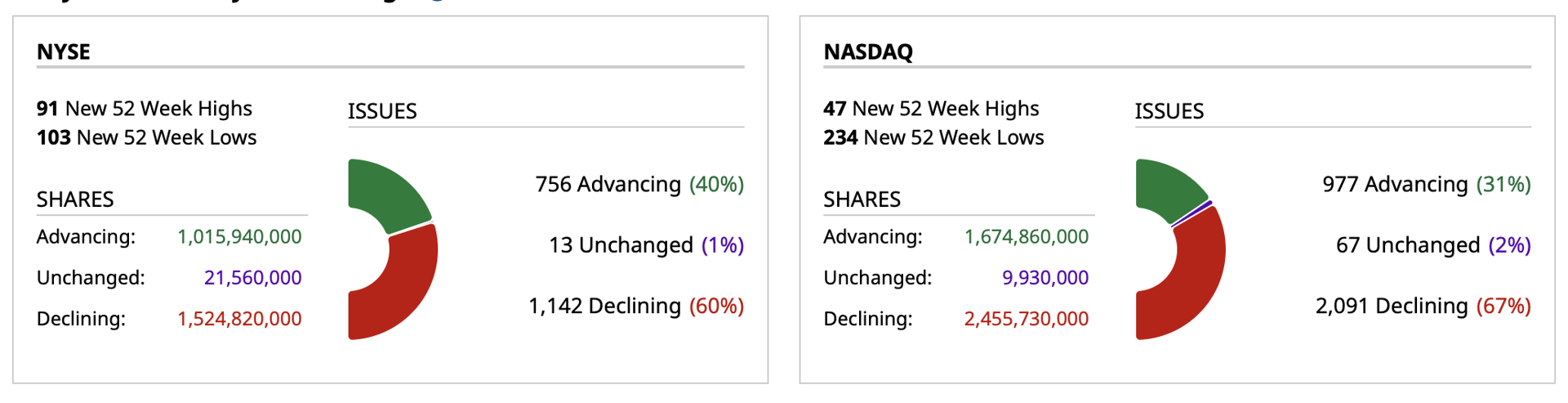

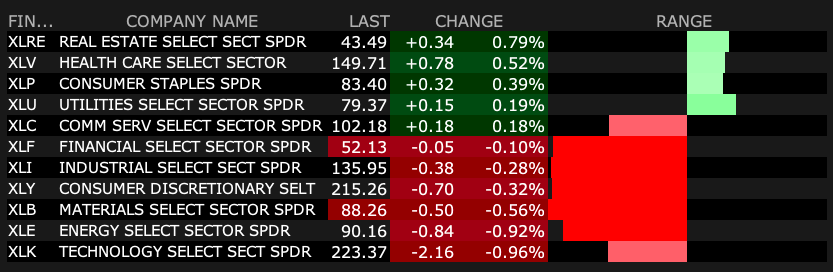

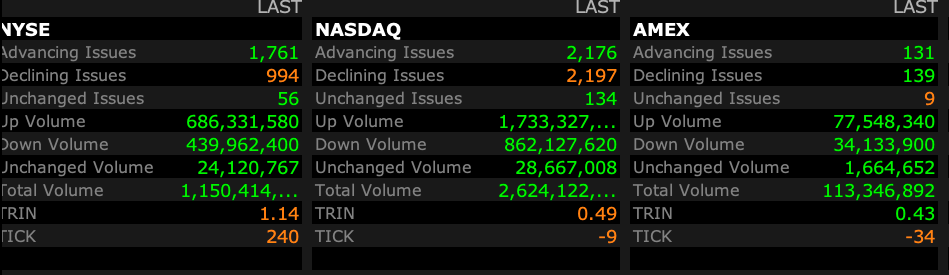

Breadth on the NYSE is around -1.5 decliners for every 1.0 advancer and about 2-1 negative on the Nasdaq:

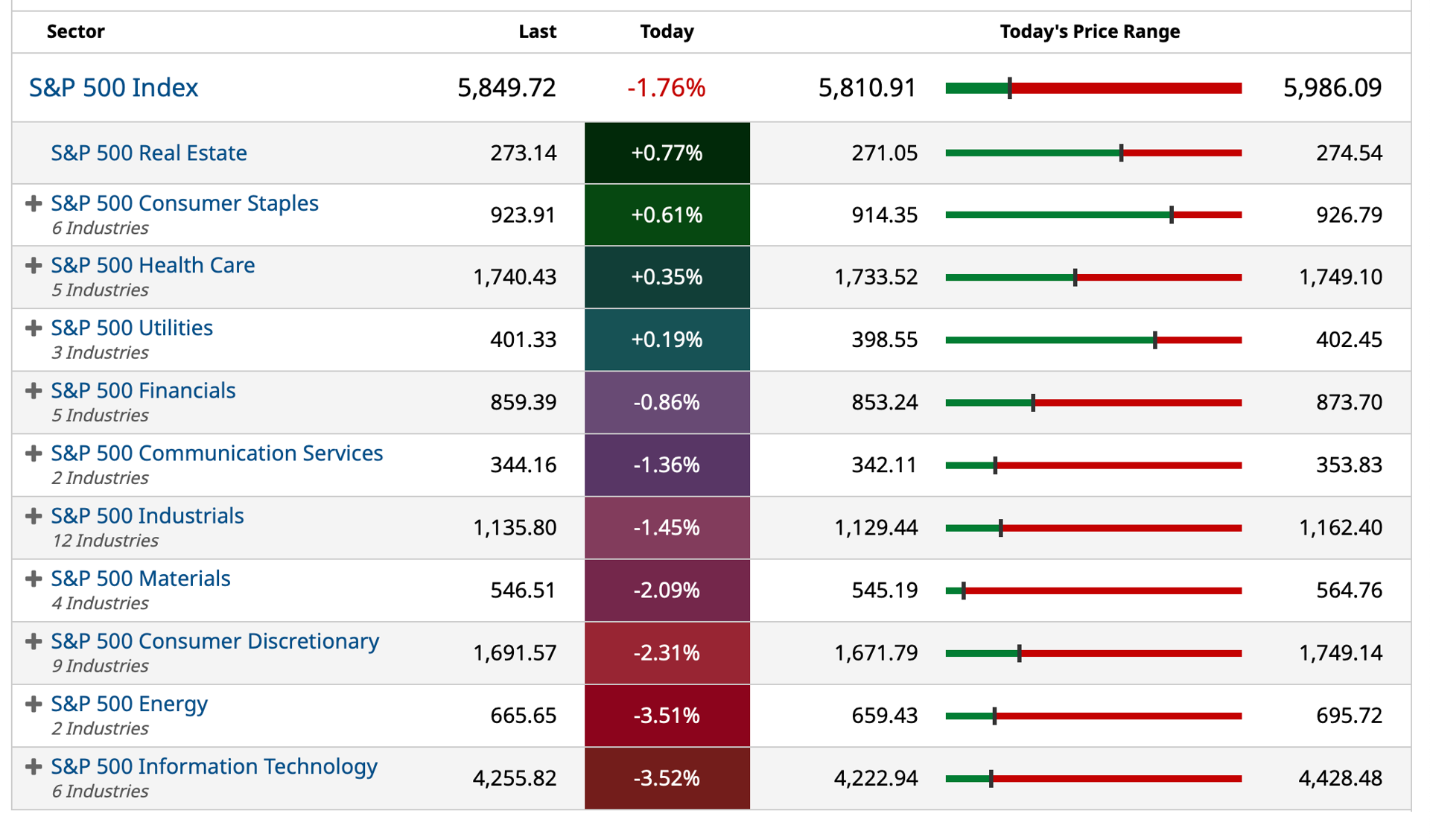

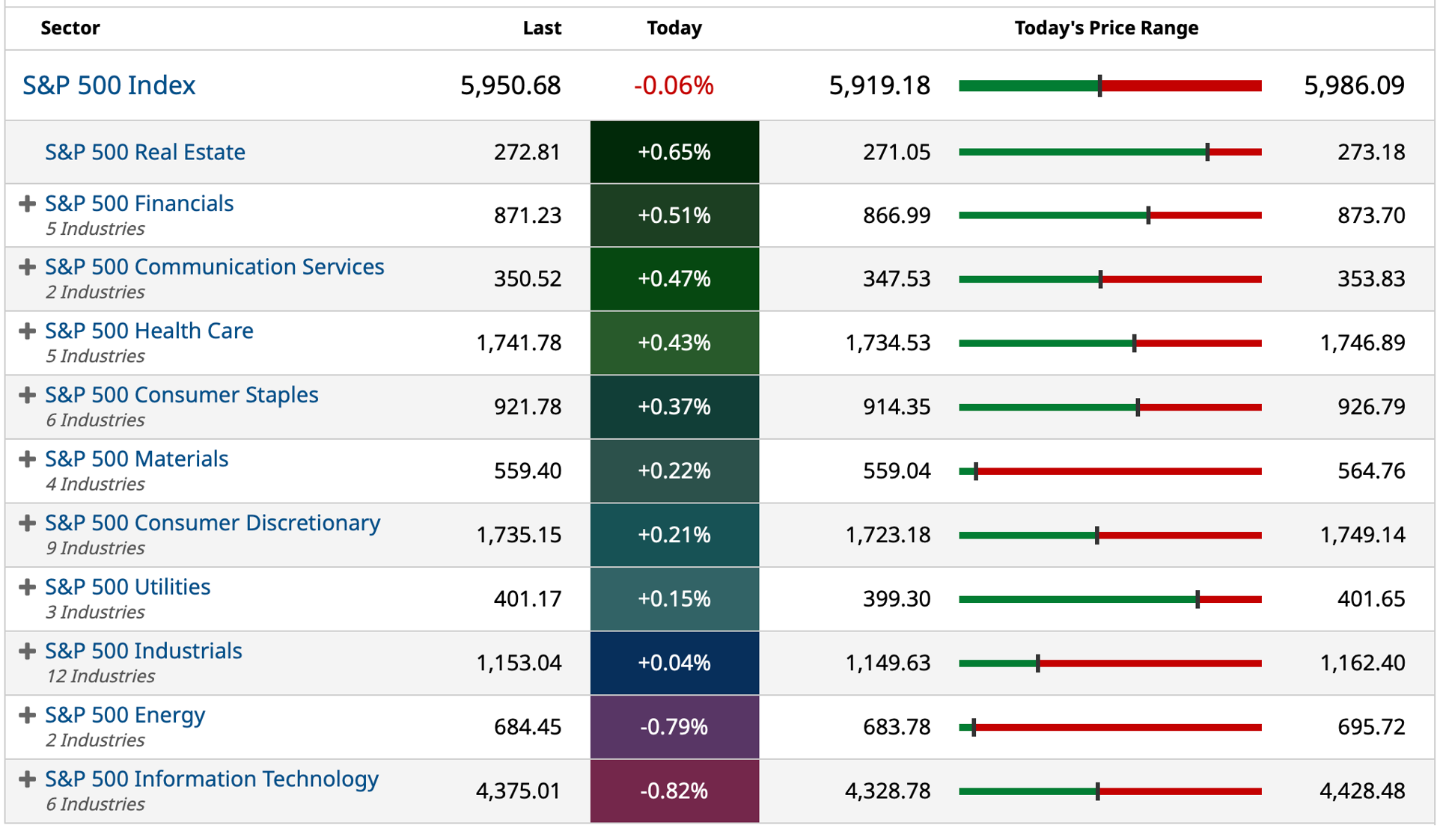

At 2:35 PM the S&P Index is down by -46 handles.

Here are the things I did today:

* I shorted SPY and QQQ very early in the morning:

* (SPY) $597.28

* (QQQ) $512.09

I covered these shorts in the early afternoon for nice gains:

* (SPY) $591.18

* (QQQ) $505.45

* I (phew!) took a long trading rental in SPY and QQQ:

With S&P cash -58 handles I have taken a small trading LONG rental in the Indices:

* (SPY) $588.06

* (QQQ) $502.64

* I added to MSOS at $3.09, TSNDF at $0.49 and VRNOF at $0.79.

* I shorted Berkshire BRK.B at $516.80 and covered a few hours later under $510.

BY Doug Kass · Mar 3, 2025, 3:00 PM EST

* From last week...

BY Doug Kass · Mar 3, 2025, 2:51 PM EST

BY Doug Kass · Mar 3, 2025, 2:35 PM EST

BY Doug Kass · Mar 3, 2025, 2:25 PM EST

I covered my Berkshire BRK.B trading short rental under $510 for a quick, seven dollar profit from this morning.

BY Doug Kass · Mar 3, 2025, 2:15 PM EST

With S&P cash -58 handles I have taken a small trading LONG rental in the Indices:

* SPY $588.06

* QQQ $502.64

BY Doug Kass · Mar 3, 2025, 1:59 PM EST

From Peter Boockvar:

If you're making stuff, you're trying to figure out the tariff impact

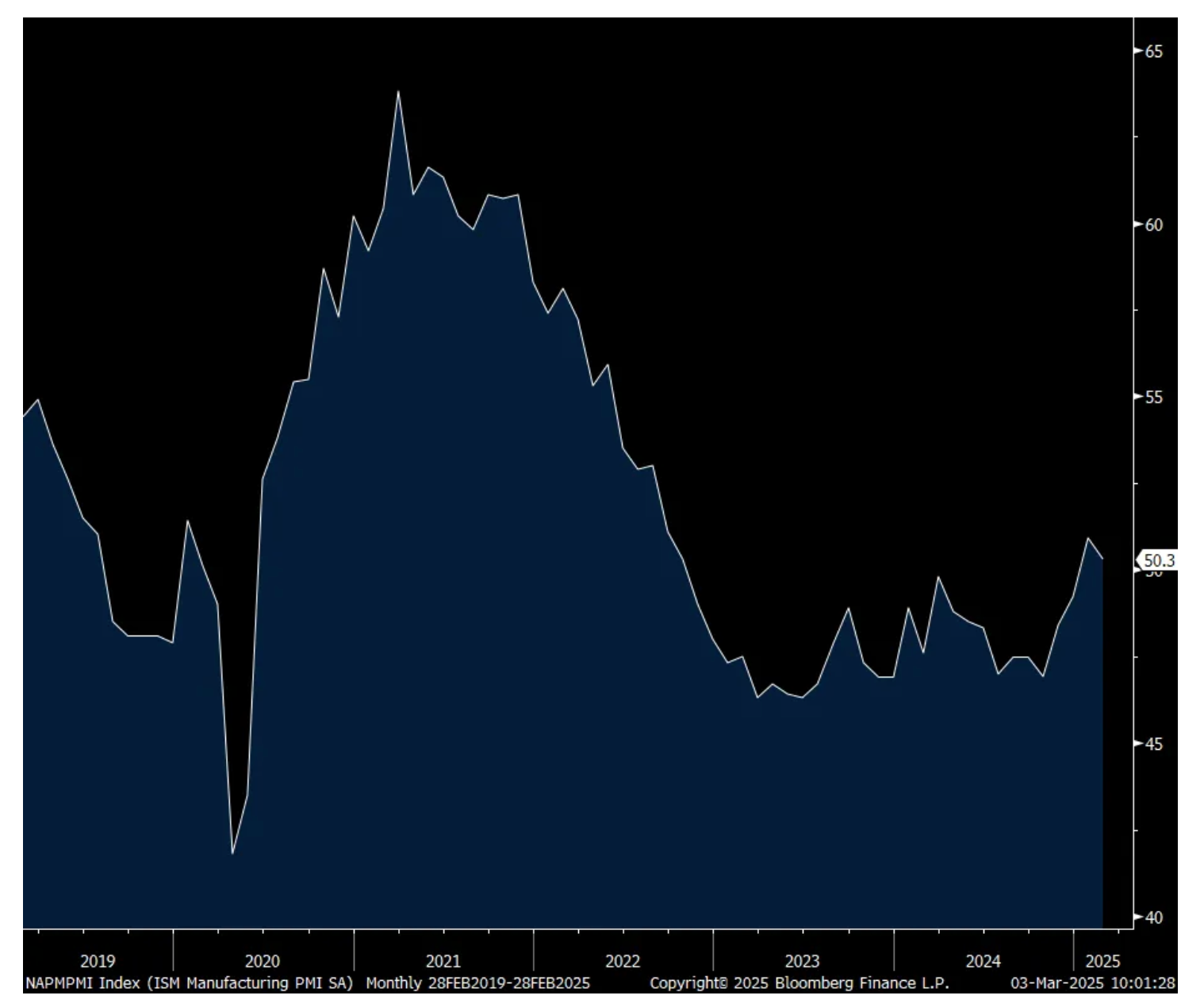

The February ISM manufacturing index was 50.3, down from 50.9 in January and just below the estimate of 50.7 but at least holding the 50 level for a 2nd month after 26 months below 50. After 3 months above 50, new orders fell 6.5 pts to 48.6. Backlogs remained below 50 but less so at 46.8, up 1.9 pts.

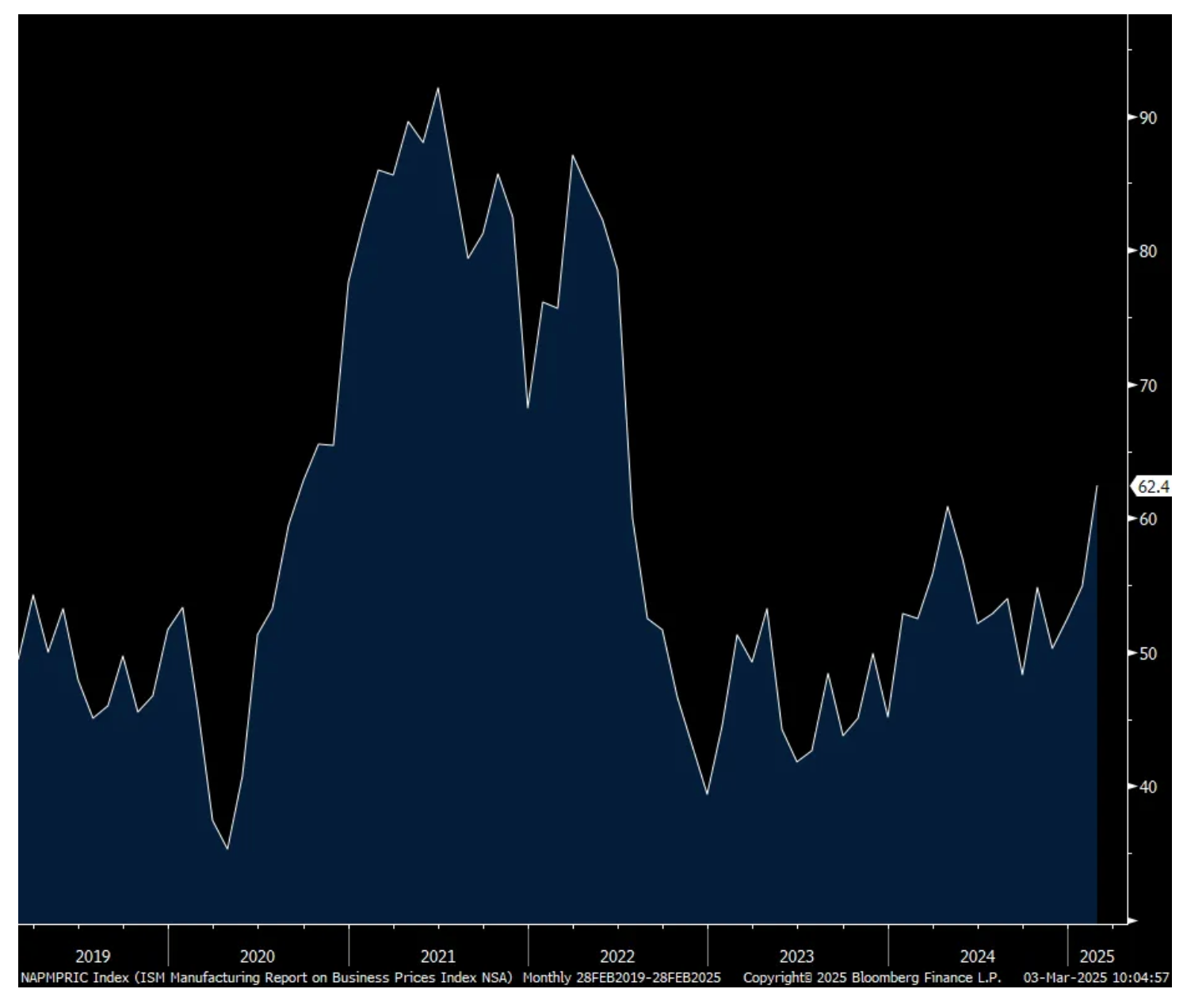

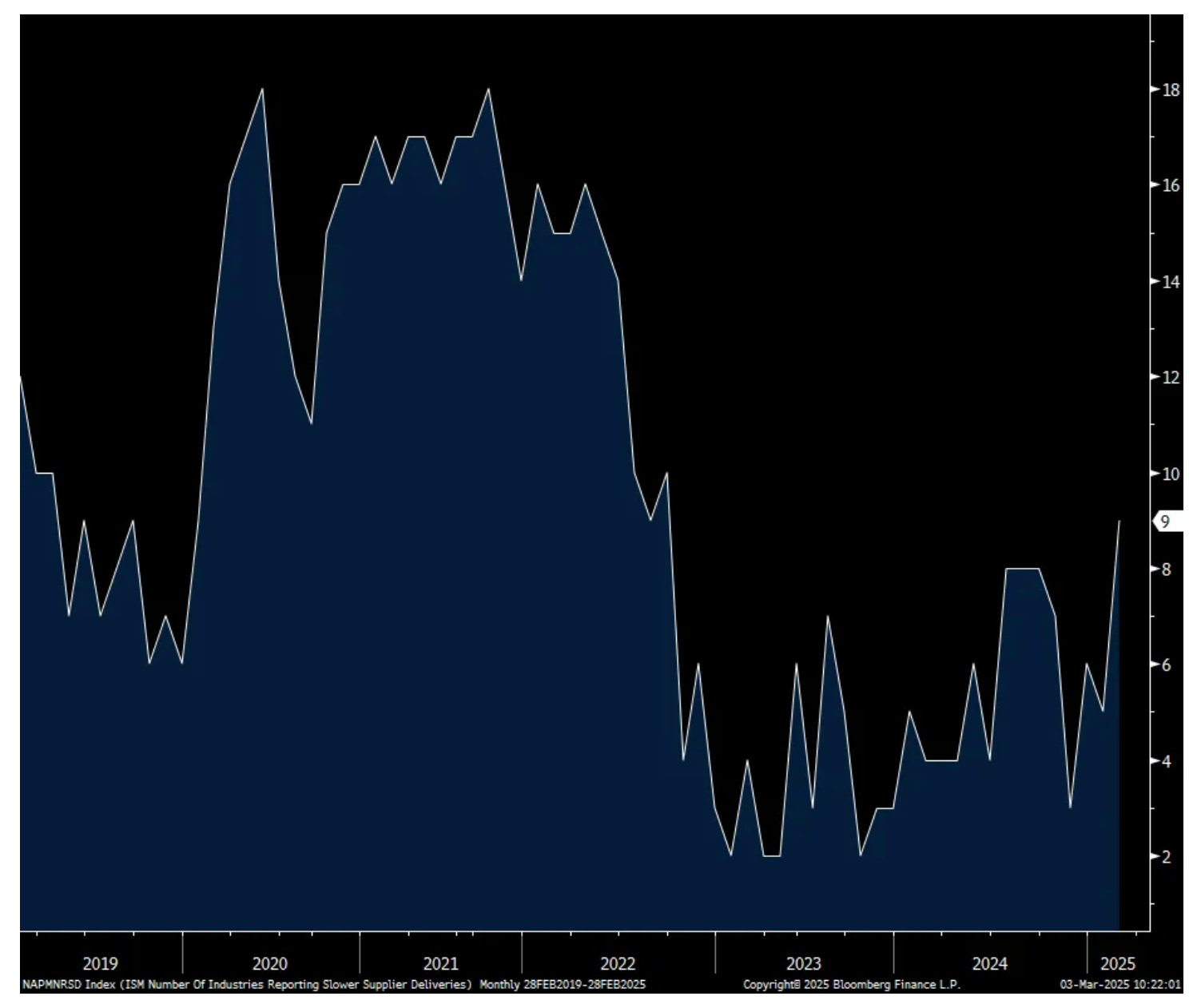

We had a rush of imports as seen with Friday’s goods data in January and the February inventory number here rose 4 pts to 49.9, though not above 50. And likely there has been some supply chain/shipping delays as supplier deliveries roes 3.6 pts to 54.5 (means slower deliveries), the highest since August 2022. Prices paid jumped by 7.5 pts to 62.4, the most since June 2022. 14 industries said they paid more vs 11 in January and 7 in December. Specifically, “Mill materials (steel, aluminum and copper), food elements, plastics and natural gas registered increases similar to the prior month. The plastics increase reversed a decline.” And, 31% of companies reported higher prices in February, compared to 21% in January.”

With supplier deliveries, 9 industries experienced slower times, the most since September 2022.

With that drop in new orders, “Panelists noted a weakening level of demand performance…Orders have also been impacted by discussions of which party will pay for potential tariff costs, causing a slowing in order placement. In addition, there is diminished confidence not only in additional interest rate cuts, but also the decline in long term rates, affecting durable goods and construction activity.”

Employment dropped by 2.7 pts to 47.6 after a brief stint above 50 last month. The ISM said, “Panelists are continuing to release employees as the business environment becomes more unclear.” Export orders fell 1 pt to 51.4, but remaining above 50 “as panelists’ comments cited Chinese stimulus impacts and potential counter tariffs levied by Beijing and Europe.”

While the headline figure fell, the breadth improved as 10 industries saw growth (the most since April 2023) vs 8 in January while 5 said their sector contracted vs 8 in January. The balance saw no change.

Here is what the ISM said on all of the above, “Demand eased, production stabilized, and destaffing continued as panelists’ companies experience the first operational shock of the new administration’s tariff policy. Prices growth accelerated due to tariffs, causing new order placement backlogs, supplier delivery stoppages and manufacturing inventory impacts. Although tariffs do not go into force until mid-March, spot commodity prices have already risen about 20%.”

Bottom line, as reminded here many times, the 2018-2019 tariff battle put US manufacturing into a recession that eventually led to the Fed rate cuts in the summer of 2019. Just as this sector was showing signs of bottoming, companies need to now deal with a whole new set of tariffs that throws mud in the gears of their business. Yes, some will benefit, but I believe more will be hurt.

Here are comments the ISM included in its press release from businesses in a variety of industries and just about everyone is talking tariffs and its influence.

“The tariff environment regarding products from Mexico and Canada has created uncertainty and volatility among our customers and increased our exposure to retaliatory measures from these countries.” [Chemical Products]

“Customers are pausing on new orders as a result of uncertainty regarding tariffs. There is no clear direction from the administration on how they will be implemented, so it’s harder to project how they will affect business.” [Transportation Equipment]

“Tariff impact has been minimal to overall manufacturing and raw material supply. Limits on U.S. government spending in key organizations like the Food and Drug Administration, Environmental Protection Agency and National Institutes of Health are delaying some orders.” [Computer & Electronic Products]

“Inflation and pricing pressure continue to drive uncertainty in our 2025 outlook. We are seeing volume impacts due to pricing, with customers buying less and looking for substitution options.” [Food, Beverage & Tobacco Products]

“The incoming tariffs are causing our products to increase in price. Sweeping price increases are incoming from suppliers. Most are noting increases in labor costs. Vendors are indicating open capacity. Inflationary pressures are a concern. Our company is working diligently to see how the new tariffs will affect our business.” [Machinery]

“Business is still slow, but some indications of improved demand are six to nine months out. Steel and scrap costs are increasing, and it’s too early to tell how high they will go.” [Fabricated Metal Products]

“New orders continue to be strong after picking up in December. The uncertainty about tariffs keeps us cautious on spending, despite the strong sales right now.” [Electrical Equipment, Appliances & Components]

“Management now has us running scenarios to project tariff impacts to our business. They want numbers in 24 hours on variables that equate to a wild guess. Interesting times we live in.” [Nonmetallic Mineral Products]

“Internal analysis ongoing about impact of tariffs, but nothing concrete yet. General business conditions remain tepid; outlook on the durables side growing more pessimistic with growing domestic inventories of automobiles.” [Plastics & Rubber Products]

“Customer volumes seem to be better than 2024. However, customers are still very hesitant to commit to long-term volumes due to the market uncertainty caused by proposed tariffs on steel/aluminum imports.” [Primary Metals]

ISM Mfr’g

Prices Paid

Number of Industries Seeing Slower Deliveries

BY Doug Kass · Mar 3, 2025, 1:15 PM EST

BY Doug Kass · Mar 3, 2025, 1:05 PM EST

BY Doug Kass · Mar 3, 2025, 12:55 PM EST

* Governments should not be in the asset speculation business.

I am wondering how this Trump/Crypto thing can even be legal.

It seems like the type of thing that needs congressional approval/budget approval.

* Where are we gonna get the money?

* I thought we are supposed to be cutting expenses and addressing the deficit?

* Shouldn’t they DOGE the crypto reserve?

Then again, Musk/Tesla owns bitcoin, so maybe we shouldn't be suprised.

This one I don’t get.

Something tells me it is hot air, for some odd reason. Does not seem like there is any meat on the bone to this one. No specific details, no nothing. We shall see, but I think a good chance it is B.S.

The response in price already has been less than one would have thought, so there is probably a fair bit of skepticism out there. The last thing I want is for the government to be buying any assets — crypto, equities, commercial real estate, or a car company or anything like that. It our money.

If President Trump feels like the U.S. government has too much money, send me a check and I will decide how to spend or invest it. This whole thing is anti-capitalist and anti-small government. Governments also tend to be about the worst allocators of capital in history. They should not be in the asset speculation business.

BY Doug Kass · Mar 3, 2025, 12:20 PM EST

As of 11:45 a.m.:

BY Doug Kass · Mar 3, 2025, 12:10 PM EST

BY Doug Kass · Mar 3, 2025, 12:05 PM EST

Dougie Kass

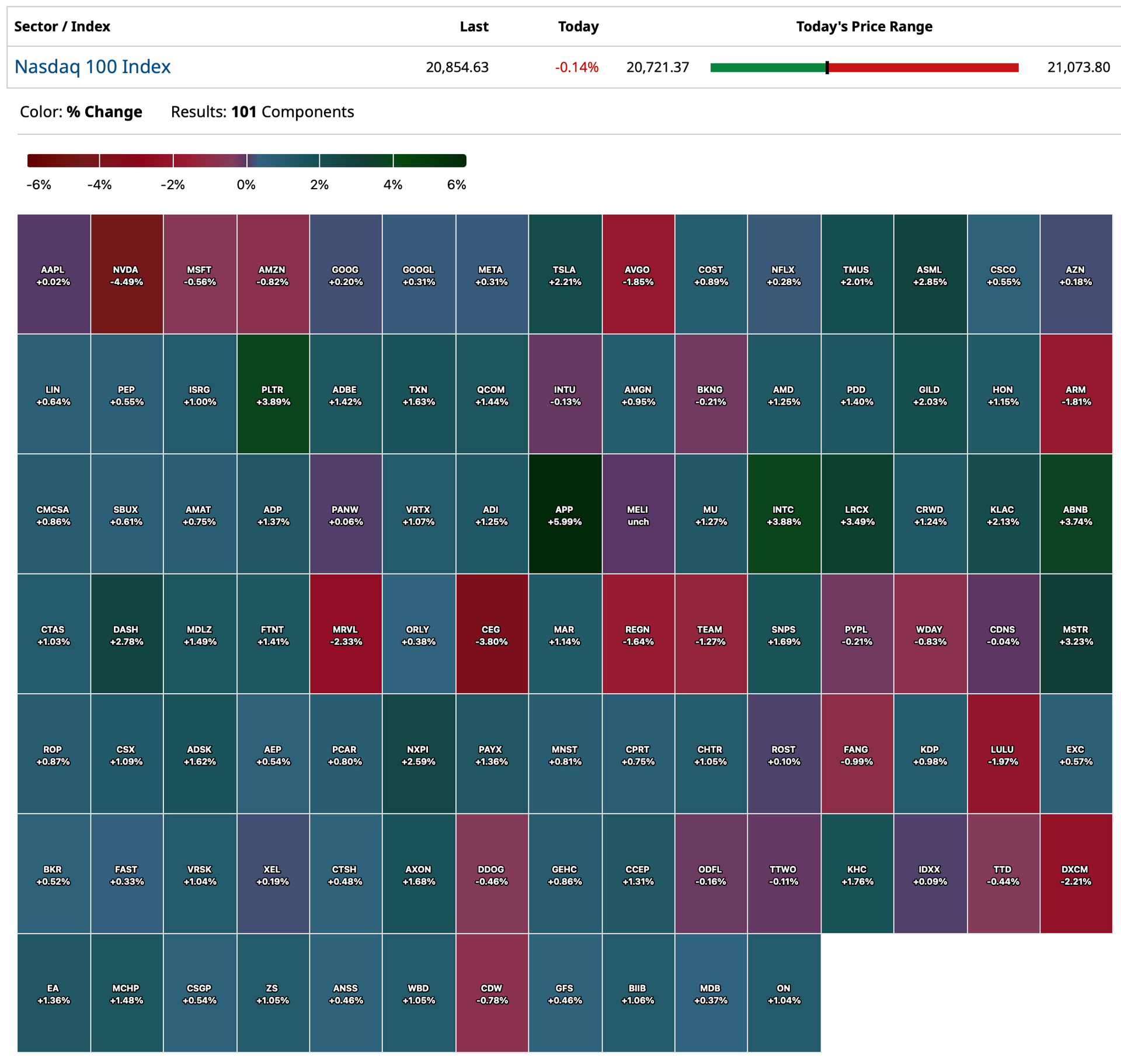

Like clockwork when the "generational compounders" are flying (higher) we get comments about the religion of buy/hold Mag 7. Those comments are self congratulatory and critical of those that have missed "the trade."

But when the stocks roll over - as they appear to be doing over the last six weeks - nothing but crickets.

As for me I write negatively about NVDA almost daily - and regardless of whether the share price is up or down.

And I will continue to.

BY Doug Kass · Mar 3, 2025, 11:55 AM EST

Whiff of Stagflation in the ISM Survey

The ISM manufacturing PMI was terrible in several respects — orders and employment sagged but prices spiked sharply. Tariffs were cited across the board as a major obstacle to growth. The Administration would be well advised to tread cautiously, but that is likely a case of wishful thinking since many on the Trump Team are fanatical when it comes to the foreign trade file.

BY Doug Kass · Mar 3, 2025, 11:42 AM EST

- NYSE volume 9% above its one-month average;

- Nasdaq volume 8% below its one-month average

- VIX: up 1.17% to 19.86

BY Doug Kass · Mar 3, 2025, 11:15 AM EST

*From our Comments Section...

douglas cassel

1 hour ago

Doug K. I generally agree about NVDA being overpriced, and have substantially cut back a long held, and profitably position. However, I must chime in that Gary Marcus, the ChatGPT critic, is far from an unbiased source. He has been on a mission to criticize AI from the get go, and seems to be making a career of it.

He could be right, but his bias must be addressed.

DK

Dougie Kass

STAFF

1 hour ago

on the other hand are the entire sell side of research, jim cramer et al

i try to offer a contrarian view that is rarely presented

i think that has value

even though you dont have to agree

DC

douglas cassel

57 minutes ago

The point is that "experts" do not always offer opinions in good faith. It does indeed happen on both sides, especially when money is involved. Part of our job is to sort out the truth from the noise.

DK

Dougie Kass

STAFF

58 minutes ago

since I started the series in june 2024 nvda has been a material underperformer.

BY Doug Kass · Mar 3, 2025, 10:45 AM EST

Small trading short rental in Berkshire Hathaway BRK.B $516.80.

High RSI (Relative Strength Index) very overbought.

Tactical trade.

BY Doug Kass · Mar 3, 2025, 10:26 AM EST

I covered this morning's Index shorts:

* SPY $591.18

* QQQ $505.45

From early this morning;

I entered today delta neutral on Indices (long common, short calls).

I moved back into a small Index short by just selling some common:

* (SPY) $597.28

* (QQQ) $512.09

Position: Long SPY common (M), QQQ common (M); Short SPY calls (M), QQQ calls (M)

Mar 3, 2025 7:11 AM EST

BY Doug Kass · Mar 3, 2025, 10:18 AM EST

BY Doug Kass · Mar 3, 2025, 9:58 AM EST

From Peter Boockvar:

Keep an eye on the US dollar index as chart wise it's looking like the right shoulder of a classic head and shoulders top.

DXY

The data focus today is on February global manufacturing with a slew of PMI's being released ahead of the US ISM at 10am est. I'd call it all a very mixed bag.

China's state sector focused manufacturing PMI hovered around 50 at 50.2, up 1.1 pts m/o/m. So did the non-manufacturing figure at 50.4 vs 50.2. The private sector Caixin China manufacturing print was 50.8 from 50.1. The Lunar New Year always distorts the January/February numbers. Caixin said, "Overall, the market showed clear signs of recovery, with manufacturers launching new products." And, "Optimism among manufacturing entrepreneurs continued to grow. The gauge for future output expectations rose close to its historical average, matching a level last seen in November. Entrepreneurs had relatively high hopes for future market supply and demand."

There were some caveats though in the commentary. "China's economy still faces significant challenges, with rising uncertainties in employment and household income constraining efforts to boost domestic demand and stabilize the economy."

Elsewhere, the final Japan one (we already saw the preliminary one) was 49 vs 48.7. Australia's was 50.4 vs 50.2. Taiwan's rose to 51.5 from 51.1. Vietnam's was at 49.2 from 48.9 and it was below 50 too in Malaysia at 49.7, though up 1 pt. Thailand's increased 1 pt to back above 50 at 50.6. Indonesia was at 53.6 from 51.9 while the Philippines fell to 51 from 52.3. India's final February print was 56.3 from 57.7 and still outperforming all of its global peers.

Here were some other notable comments from some countries.

On Taiwan, "Taiwan's manufacturing sector was revitalized in February, posting faster increases in key factory health barometers such as production, output, purchasing and inventories...February's growth in new factory orders also appears to reflect diverse strength across the customer base, with panelists reporting domestic and overseas markets like Europe and the US as sales drivers."

On Vietnam, "Manufacturers in Vietnam reported subdued demand conditions again in February, with the sector struggling to gain momentum in 2025 so far. On a more positive note, firms were increasingly optimistic about the future path of output, although confidence was often based on hopes that economic conditions was often based on hopes that economic conditions will be stable in the months ahead."

On Japan, "The near term outlook remains clouded, as firms continued to work through backlogs of work at a solid rate, a sign that new order inflows are not enough to sustain production. Moreover, confidence in the year ahead outlook weakened from that seen in January to the lowest since mid 2020, as firms highlighted the potential downside risks of US protectionist trade policies and a slower than anticipated economic recovery."

On India, "Robust global demand continued to boost growth in the Indian manufacturing sector, which increased its purchasing activity and employment. Business expectations also remained very strong, with nearly one-third of survey participants foreseeing greater output volumes in the year ahead. Although output growth slowed to the weakest level since December 2023, overall momentum in India's manufacturing sector remained broadly positive in February."

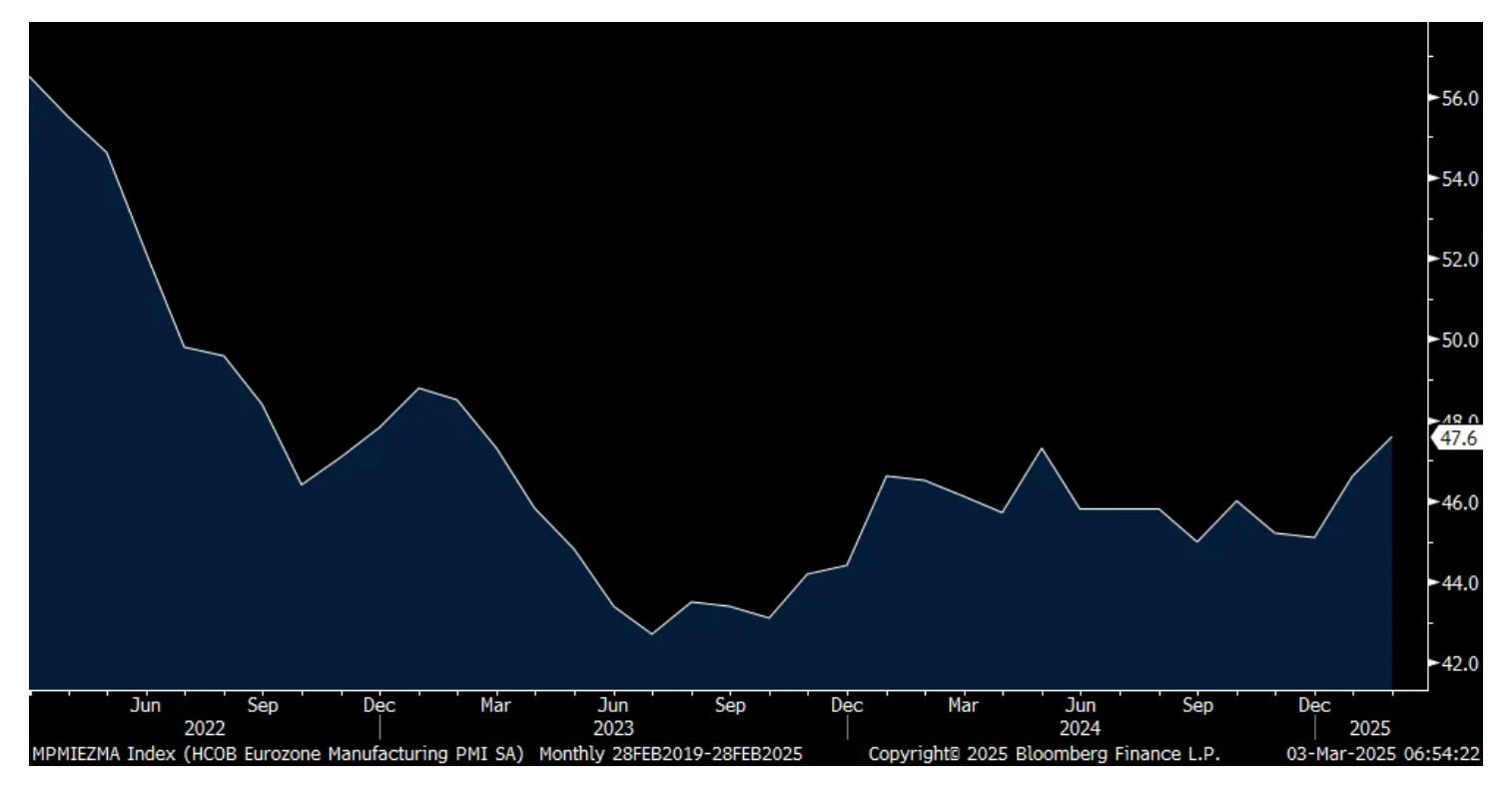

Europe continues to have its manufacturing challenges and its final manufacturing PMI was 47.6, up .3 pts from the initial figure and up 1 pt from January. It was last above 50 in June 2022. Germany at 46.5, France at 45.8 and Italy at 47.4 all were a drag and even Spain's softened at 49.7 from 50.9 in January and it's the first time below 50 for them since January 2024.

S&P Global is seeing the glass as maybe half full though for Europe. They said "the PMI hints that the manufacturing sector might be finding its footing. New orders are falling at the slowest pace since May 2022, and production is edging closer to stabilizing. So, after almost three years of recession, we could see a bit of growth in the coming months."

At least on the defense side, the coming flood of spending is certainly going to help anyone touching that space and defense stocks in Europe today are all trading higher again today.

Stagflation remains a problem as "Cost pressures facing Eurozone factories intensified midway through the first quarter as the rate of input price inflation quickened to a six month high." It's more a margin hit though as "The latest data implied that these greater expenses were absorbed by companies as output charges were discounted marginally since January."

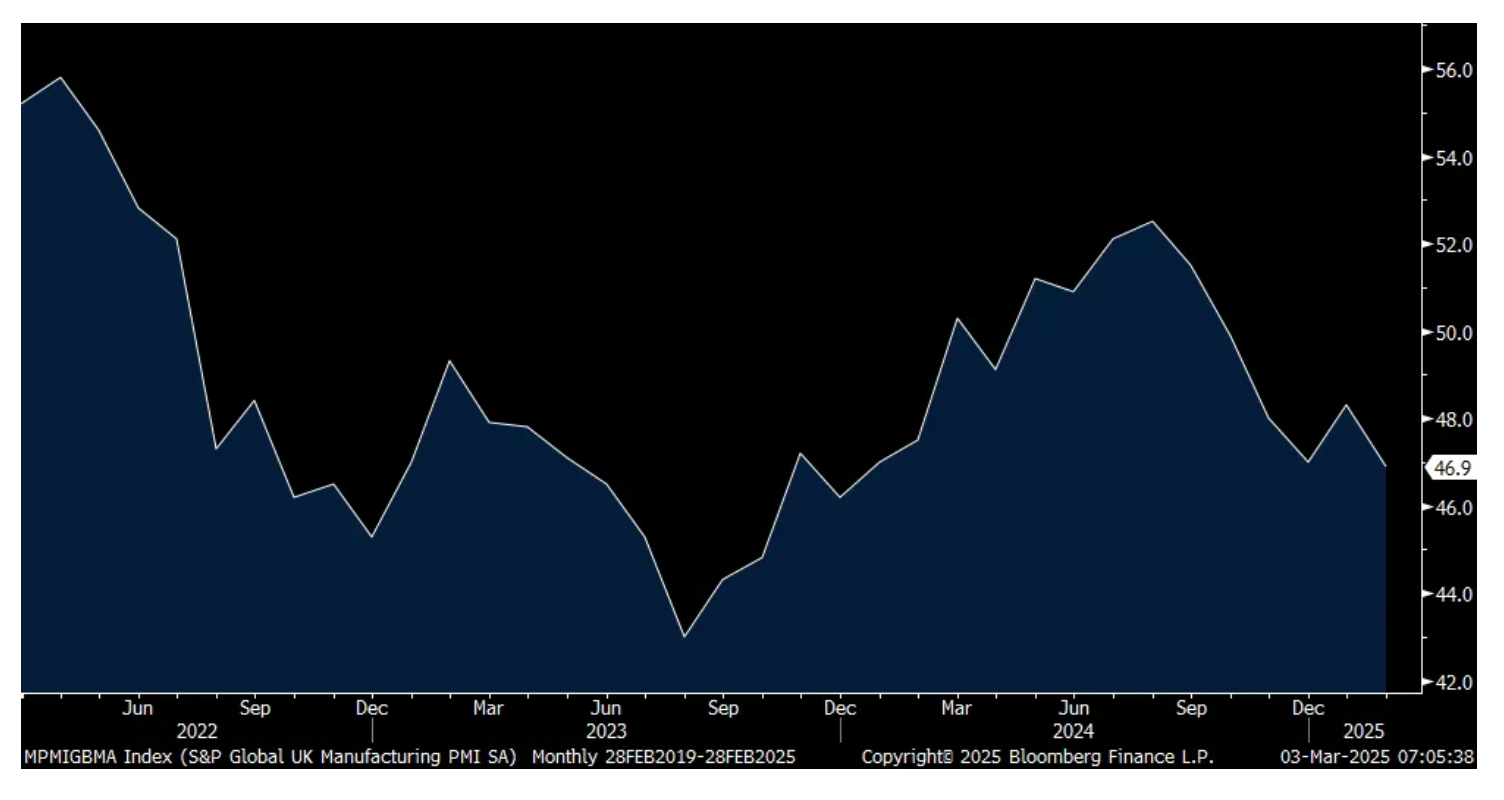

The final UK manufacturing PMI was 46.9, down from 48.3 in January and the lowest since December 2023. S&P Global said "Weak demand, low client confidence and rising cost pressures are accelerating the downturns in output and new orders, while the Autumn Budget's changes to the national minimum wage and employer NICs are driving up inflation fears and intensifying the downward trend in staff headcounts. The pace of manufacturing job losses is currently running at a rate not seen since the pandemic months of mid 2020."

Stagflation remains the word here too and through the entire supply chain, as "Underlying price pressures continued to climb in February, with rates of inflation in input costs and output charges both accelerating...Selling prices meanwhile rose to the greatest extent since April 2023, reflecting the pass through of current and expected cost increases to clients, higher staff costs and increased tax burdens."

Eurozone Mfr'g PMI

UK Mfr'g PMI

Speaking of inflation in the Eurozone, the February CPI rose 2.4% y/o/y, one tenth more than expected, though down from 2.5% in January. The core rate at 2.6% was also one tenth above the estimate but down one tenth from the month before. The ECB meets on Thursday and is fully expected to cut rates again to 2.50% which would essentially put its REAL rate at zero.

With the likely huge increase in defense spending and possibility of a bottoming in the region's economy with hopes of economic liberalization too, the ECB is playing with fire getting so easy again with inflation supposedly their sole mandate. The 5 yr 5 yr euro inflation swap is higher by 4 bps to 2.08% in response to the slightly higher inflation print, though well off its 12 month high of 2.39%.

The possibility that this could be the last rate cut for a while has the euro higher and bond yields up across the region.

BY Doug Kass · Mar 3, 2025, 9:40 AM EST

-ALGM +17% (said to be drawing takeover interest from ON Semi, which has been working with advisers in recent months to pursue Allegro)

-UPXI +15% (unit Quantum Hash has signed LoI acquire a 2MW operating facility, its biggest initiative into the Cryptocurrency industry to date)

-NUVB +11% (secures up to $250M in Non-Dilutive Financings from Sagard Healthcare Partners)

-NXL +8.1% (receives Notice of Allowance from the United States Patent and Trademark Office (USPTO) for its patent application titled “Alternating Current Dynamic Frequency Stimulation Method for Opioid Use Disorder (OUD) and Substance Use Disorder (SUD)”)

-INTC +6.0% (reportedly Nvidia and Broadcom are testing Intel's 18A manufacturing process, signaling early confidence in its advanced chip-making capabilities)

-CLDX +5.7% (presents Positive Preclinical Data from Inflammatory Bispecific Antibody Program CDX-622 at AAAAI 2025)

-PLTR +3.6% (momentum)

-SGRY +3.6% (earnings, guidance)

-MOS +3.1% (JPMorgan Chase and Co Raised MOS to Overweight from Neutral)

-TSLA +3.1% (reiterating as ‘Top Pick’ in US Autos at Morgan Stanley)

-DRH +2.8% (affirms FY25 guidance)

-AVGO +2.4% (reportedly Nvidia and Broadcom are testing Intel's 18A manufacturing process)

-CMG +2.4% (Morgan Stanley Raised CMG to Overweight from Equal Weight, price target: $70)

-AMPL +2.1% (Needham initiates coverage with ‘Buy’ rating)

-ME -32% (CEO Wojcicki offers to take private at $0.41/shr after New Mountain no longer interested in participating in a potential acquisition)

-FTRE -16% (earnings, guidance)

-RC -14% (earnings; cuts dividend)

-NABL -7.4% (earnings, guidance)

-ADT -5.5% (Apollo files to sell 70M shares; Board authorizes concurrent 20M share repurchase)

-CMRX -5.3% (to pause enrollment in US portion of ACTION study during NDA review period)

-NABL -3.7% (earnings, guidance)

-LUV -2.1% (JPMorgan Chase and Co Cuts LUV to Underweight from Neutral, price target: $25)

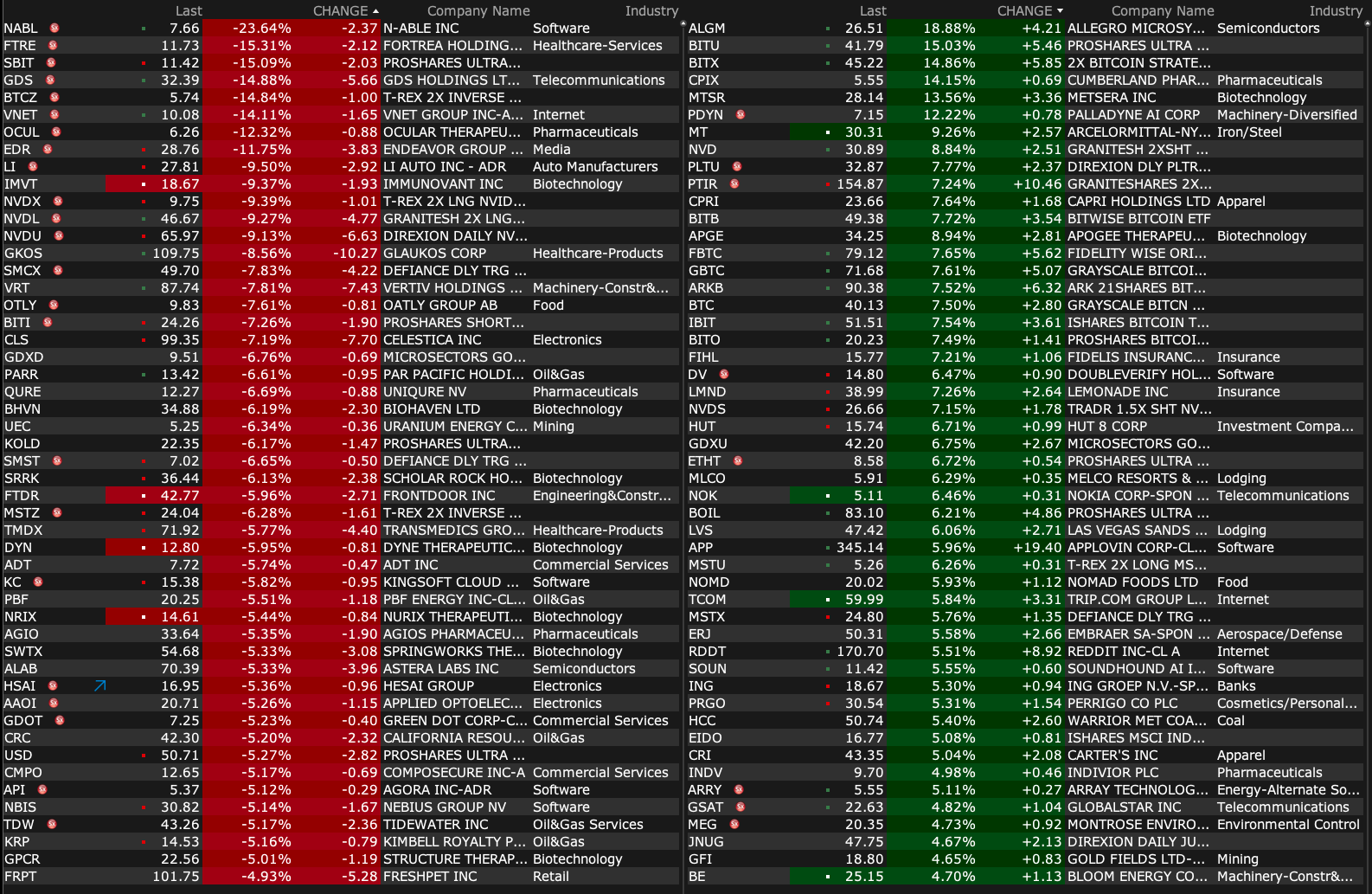

BY Doug Kass · Mar 3, 2025, 9:15 AM EST

As of 8:19 a.m.:

BY Doug Kass · Mar 3, 2025, 8:57 AM EST

At 8:39 a.m.:

BY Doug Kass · Mar 3, 2025, 8:48 AM EST

* Misleading economic data get us into trouble... often!

The header of course refers to the famous quote by Mark Twain, implying that statistics can be manipulated to present a misleading picture, essentially acting like a lie...

On Friday night I saw this regarding expected Q1 2025 GDP from the Atlanta Fed:

https://www.atlantafed.org/-/media/documents/cqer/researchcq/gdpnow/realgdptrackingslides.pdf

That "august" body revised from +2.3% expected down to -1.5% expected, a ~4% delta. This is about the sharpest change over a short period of time, with no big exogenous event or shock, that I can remember. This is the equivalent of an aircraft carrier somehow being able to turn like a motorcycle. I cannot tell how much of the revision is due to G, and how much is due to softening consumer spend (they are both related), and how much is other factors (home sales, etc). The markets (debt and equity) seem to be sniffing this one out, especially the debt markets. Granted, we are still early in the data cycle. I would be surprised if it is this bad, but who knows.

Who knows what GDP will turn out to be, but it is one more example of a somewhat poor and misleading economic statistic. I think poor and misleading economic statistics get us into trouble, often.

Obviously, if the G goes down it is a problem for the economy. The problem becomes bigger when G going up is what was propping the economy up to begin with. Nobody should have thought things were as good as they looked, because a fair bit of it was the G. Politicians do this for a reason, and they should not be rewarded for trying to buy votes and elections.

Digging a hole and filling it back up increases G over the short term, but is harmful over the mid-to longer term. Hiring regulators increases G over the short term, is harmful to businesses and the economy over the mid-to longer term. You could take everyone that is making cars and put them to work at the DMV for the same salary. Nobody would have cars, but GDP stays the same.

We might want to start looking more closely at GDP without the G, and employment without the G. These numbers exist, but policy makers seem to ignore them.

Post Script: The economic statistics problem is made worse when the numbers are fraudulent. I have long expressed cynicism regarding the methodology underpinning inflation numbers. Recently, it appeared the employment numbers (in addition to being a lot of government) were outright fraudulent, probably for political reasons. We saw what happened with the massive downward revisions at the end (which might not have been enough). This garbage cannot be allowed to happen, ever again. There is a human tendency, even when knowing data is no good, to go along with what it implies, if it is convenient and expedient to do so, for political, career, or other reasons (gutless).

BY Doug Kass · Mar 3, 2025, 8:00 AM EST

15x more expensive. For this?

Does not work. And investors in Open AI (and the others) should be marking down their investments post haste, in my view.

I cannot imagine any of this is consistent with any investment hypothesis, nor can Meta META giving them the boot be good news either (from Gary Marcus):

BY Doug Kass · Mar 3, 2025, 7:35 AM EST

I entered today delta neutral on Indices (long common, short calls).

I moved back into a small Index short by just selling some common:

* SPY $597.28

* QQQ $512.09

BY Doug Kass · Mar 3, 2025, 7:11 AM EST

Bonus — Here are some great links:

Jazzy Jeff Hirsch on the First Day of March

BY Doug Kass · Mar 3, 2025, 7:00 AM EST

BY Doug Kass · Mar 3, 2025, 6:45 AM EST

BY Doug Kass · Mar 3, 2025, 6:35 AM EST

From Bramo:

BY Doug Kass · Mar 3, 2025, 6:25 AM EST

BY Doug Kass · Mar 3, 2025, 6:15 AM EST

"Market opinions are like assholes. Everyone has one."

- Lee Cooperman

Even Goldman Sachs appears to want Twitter "clicks" and "follows:"

BY Doug Kass · Mar 3, 2025, 6:05 AM EST

Wolf Street howls about oil... vey:

BY Doug Kass · Mar 3, 2025, 5:55 AM EST

The S&P Short Range Oscillator grew slightly more oversold at -1.89% vs. 1.56%.

BY Doug Kass · Mar 3, 2025, 5:45 AM EST