Blame it on the bossa nova With its magic spell Blame it on the bossa nova That he did so well Oh, it all began with just one little dance But soon it ended up a big romance Blame it on the bossa nova The dance of love

You might want to blame the market decline on the Bossa Nova, but I blame it on market structure risks I have warned about for twelve months.

Market Structure Favors the Bold Now

As I often write, I am repeatedly wrong and always in doubt.

That said, there is something — in this world of investment uncertainty — that I am almost certain about!

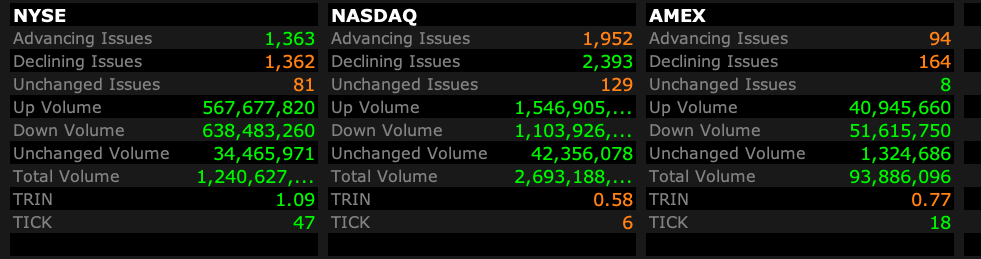

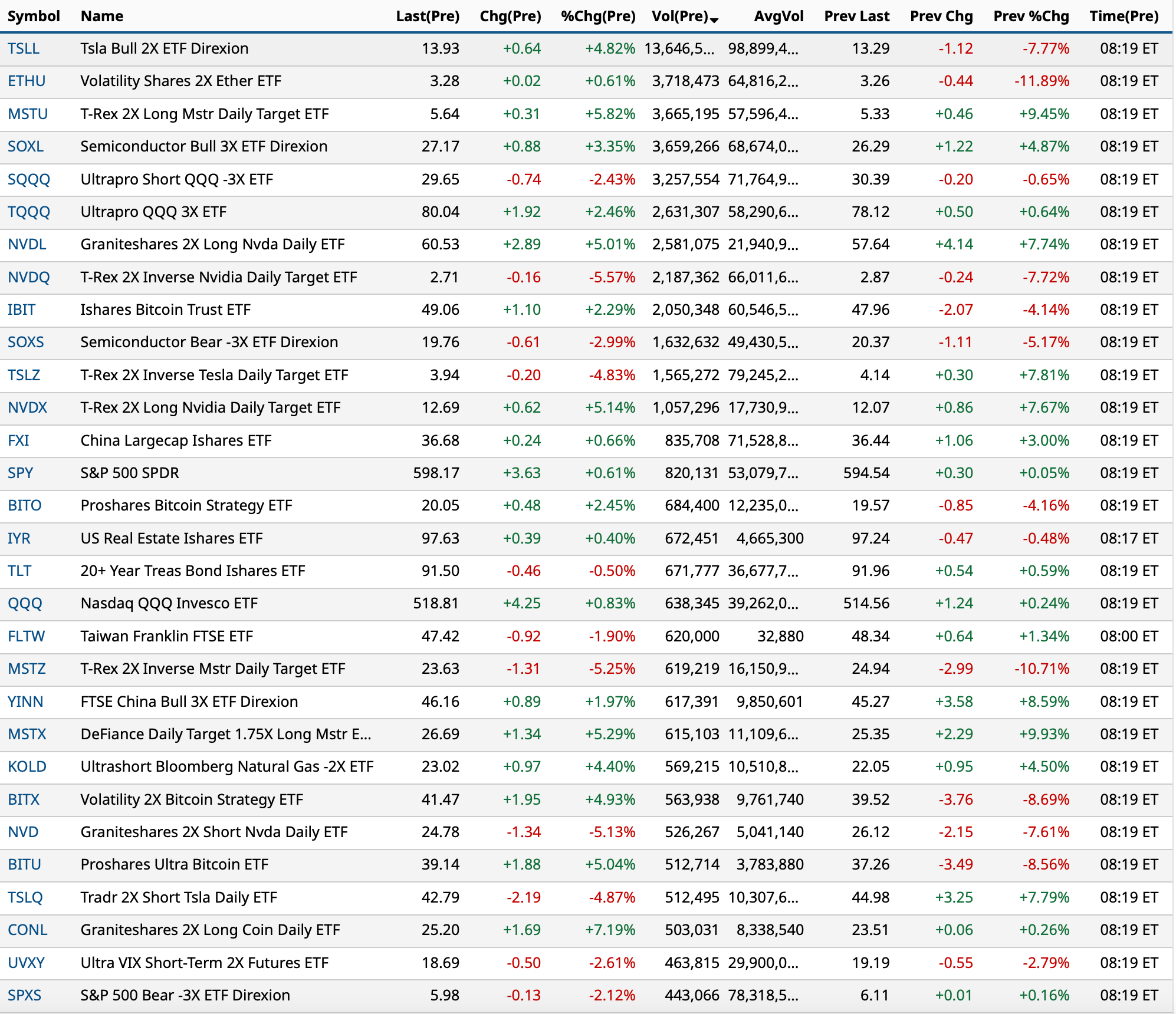

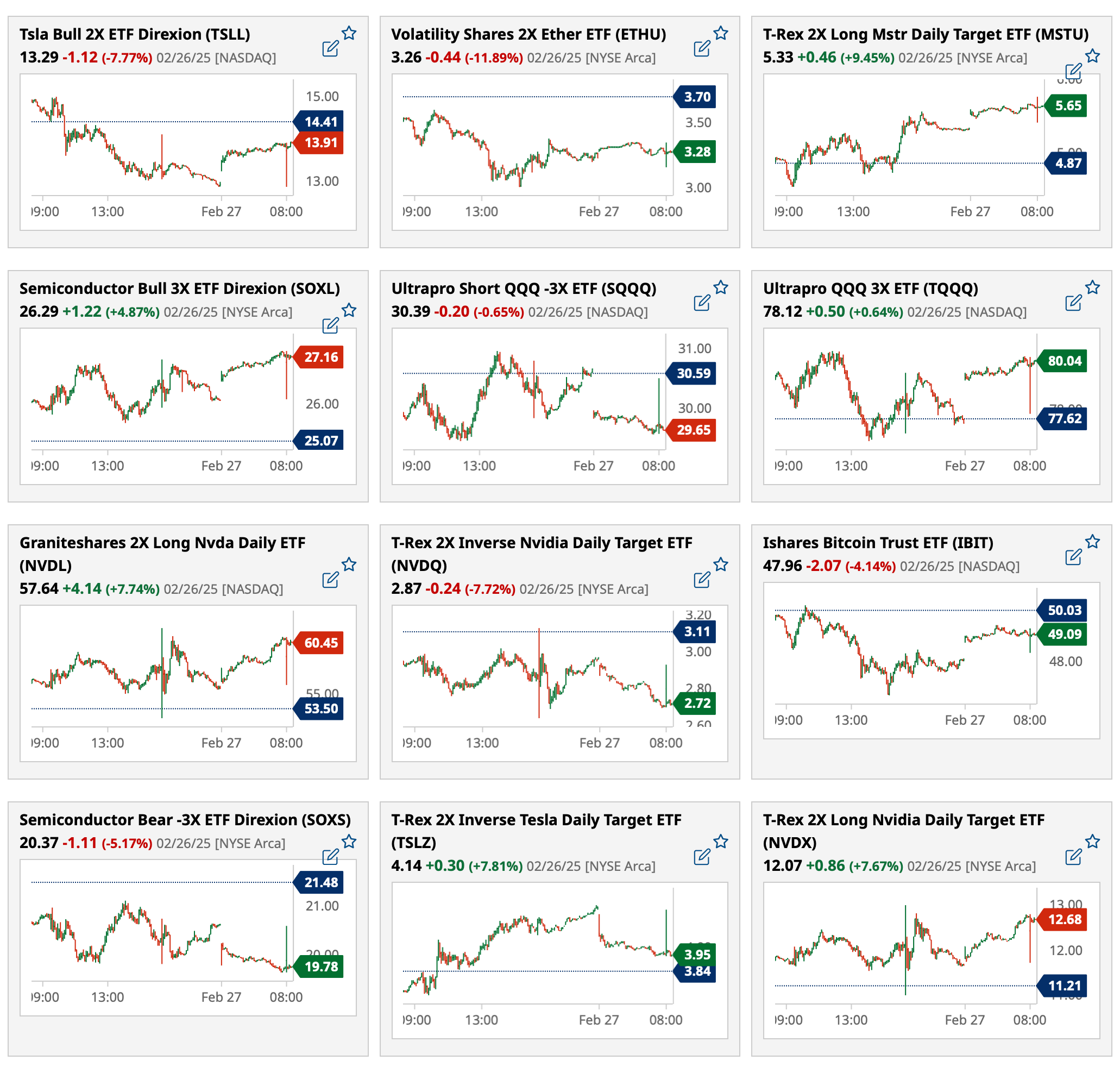

The dominance of machines — in which momentum (in both ways) is accentuated by products and strategies that worship at the altar of momentum — is producing many more trading and investment opportunities.

These days, the preponderance of passive investing (over active investing) is often taking selected equities to "artificial levels" with greater frequency.

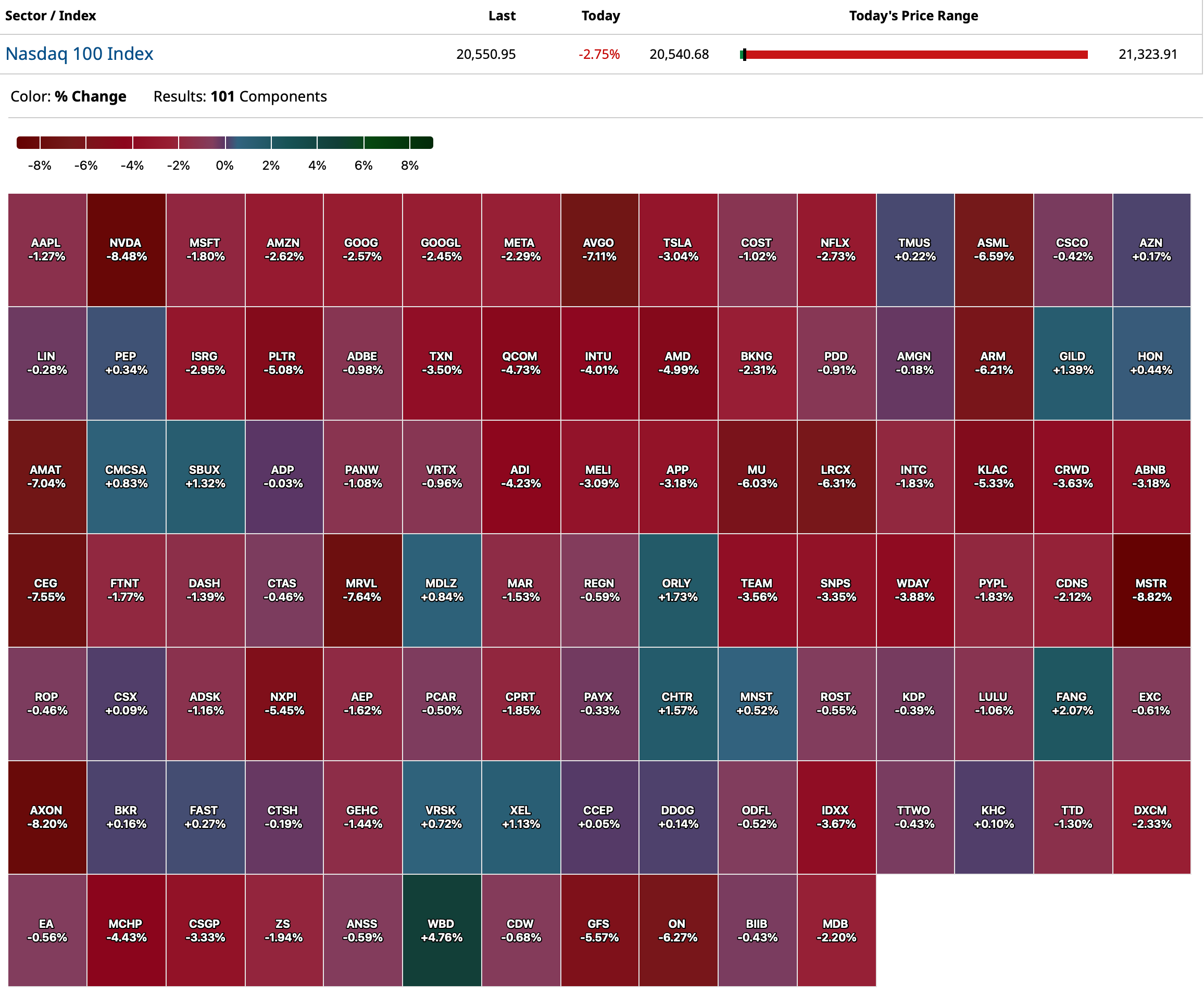

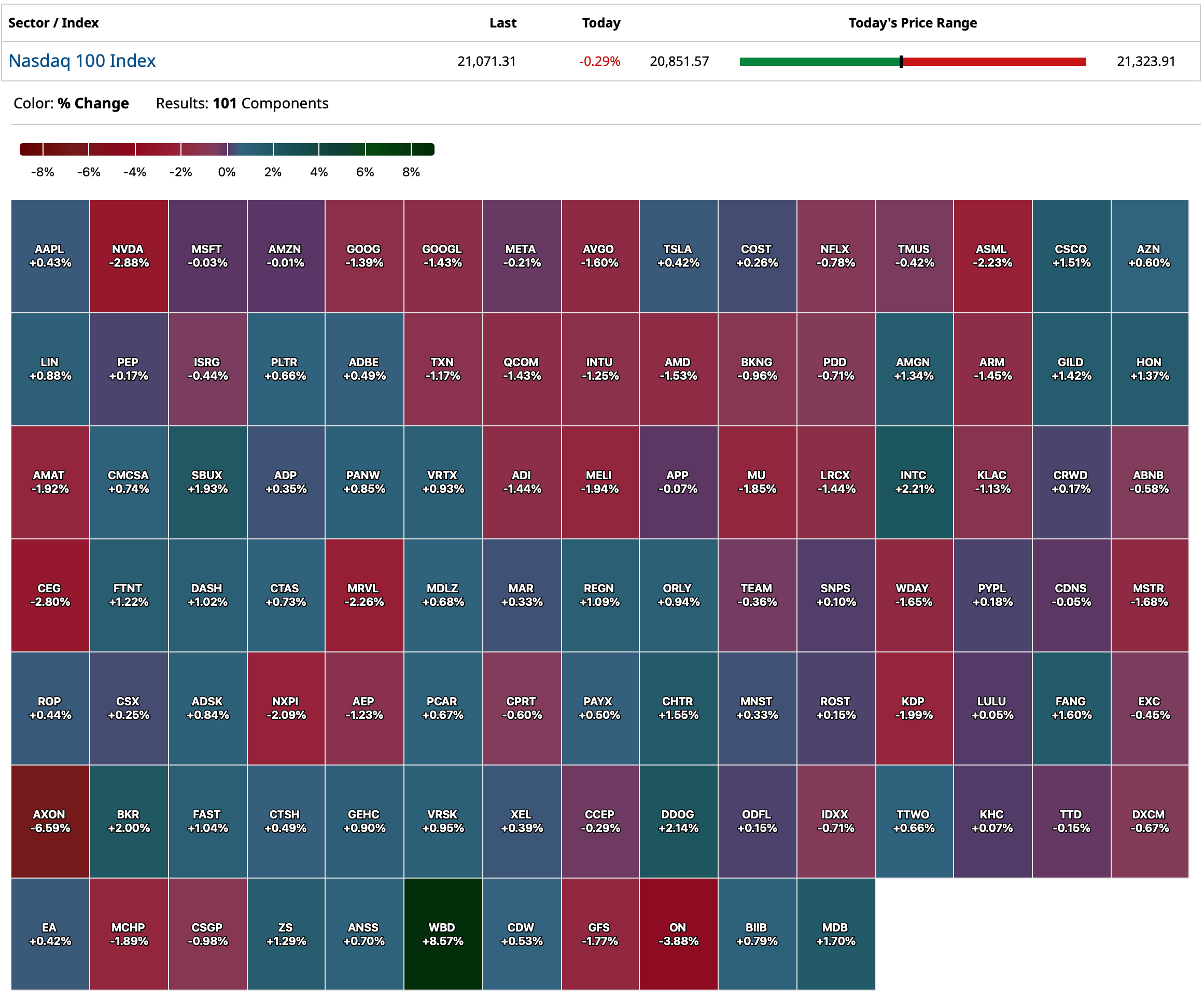

Arguably, several recent examples of this sort of rapid/random/extreme price movement were seen this week when Palantir (PLTR) and JPMorgan Chase (JPM) climbed vertically to new highs — and then over the last two trading days have fallen back badly (despite a modest drop in the overall market).

The positive about this is that if one is bold and has a sense of a company's "intrinsic value" one can capitalize (long AND short).

However, this sort of opportunistic trading/investing requires one to be dispassionate. It also means, that "fighting" the temporary and often short-lived price momentum in sectors and in individual stocks requires an "averaging in" strategy (something I have been discussing this week in the Comments Section of my Diary).

It also means that sector rotation could become more rapid and extreme.

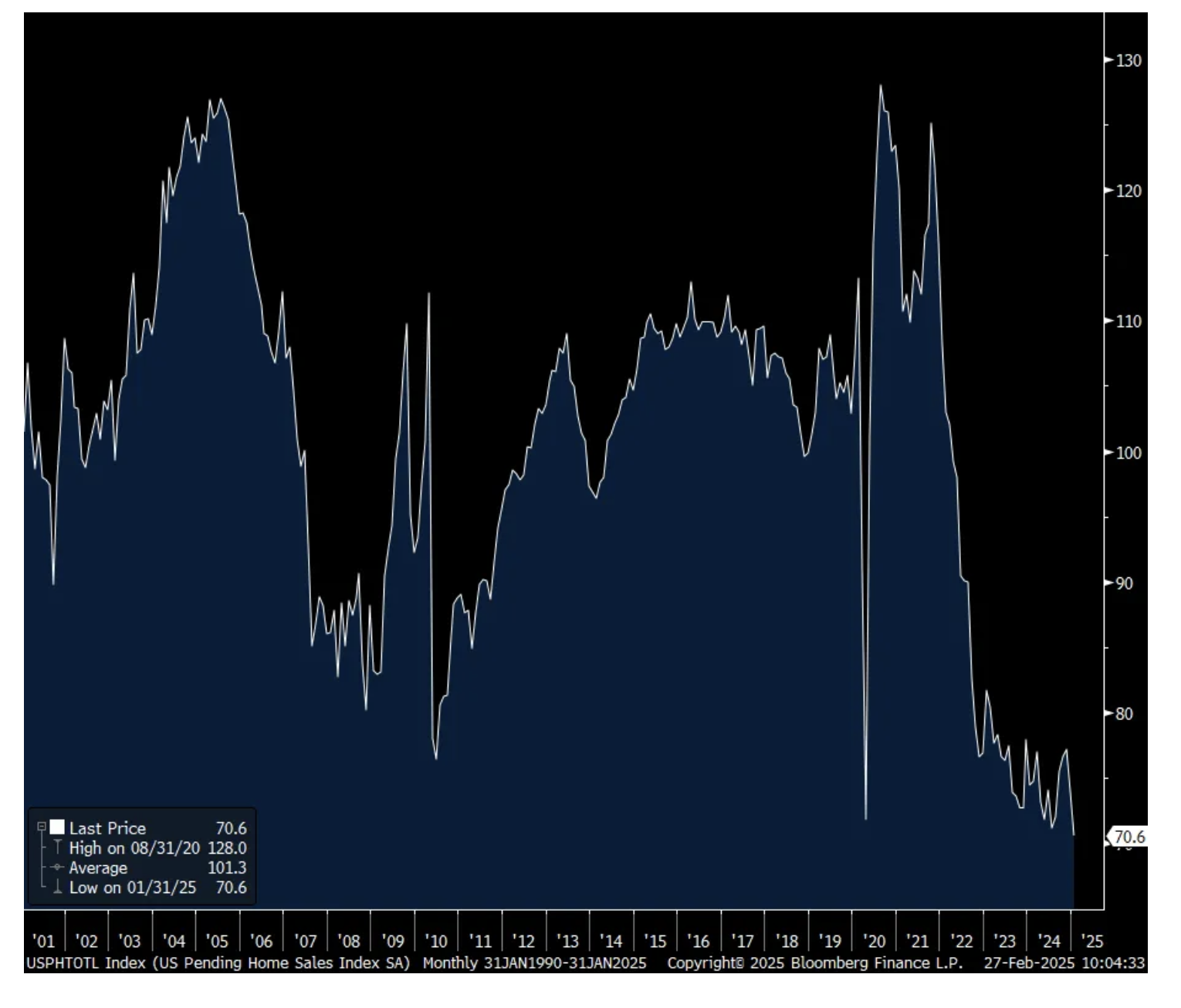

January Pending home sales, measuring contract signings of existing homes, fell 4.6% m/o/m, worse than the estimate of down .9% and follows a 4.1% decline in December. The index have now fallen below the Covid low and stands at the lowest level since this index first began in 2001.

The NAR tried to blame the possibility of “the coldest January in 25 years” in hindering sales which I think is nonsense. In fact, sales rose in the Northeast and fell the most in the South. Reality speaking, they got this right “it’s evident that elevated home prices and higher mortgage rates strained affordability.”

Sentiment check/Claims jump in DC/Q1 GDP estimates need to be trimmed but future orders better

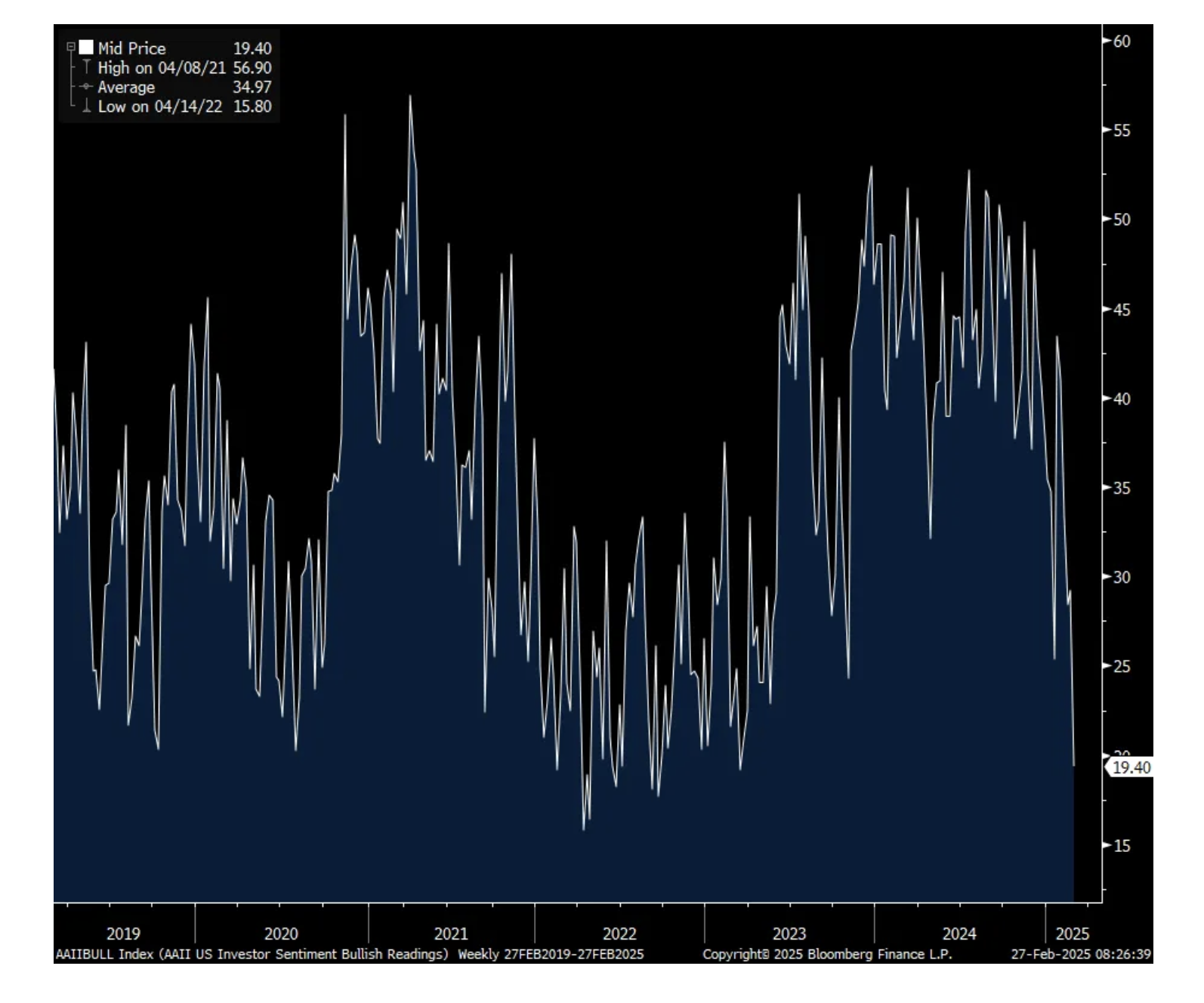

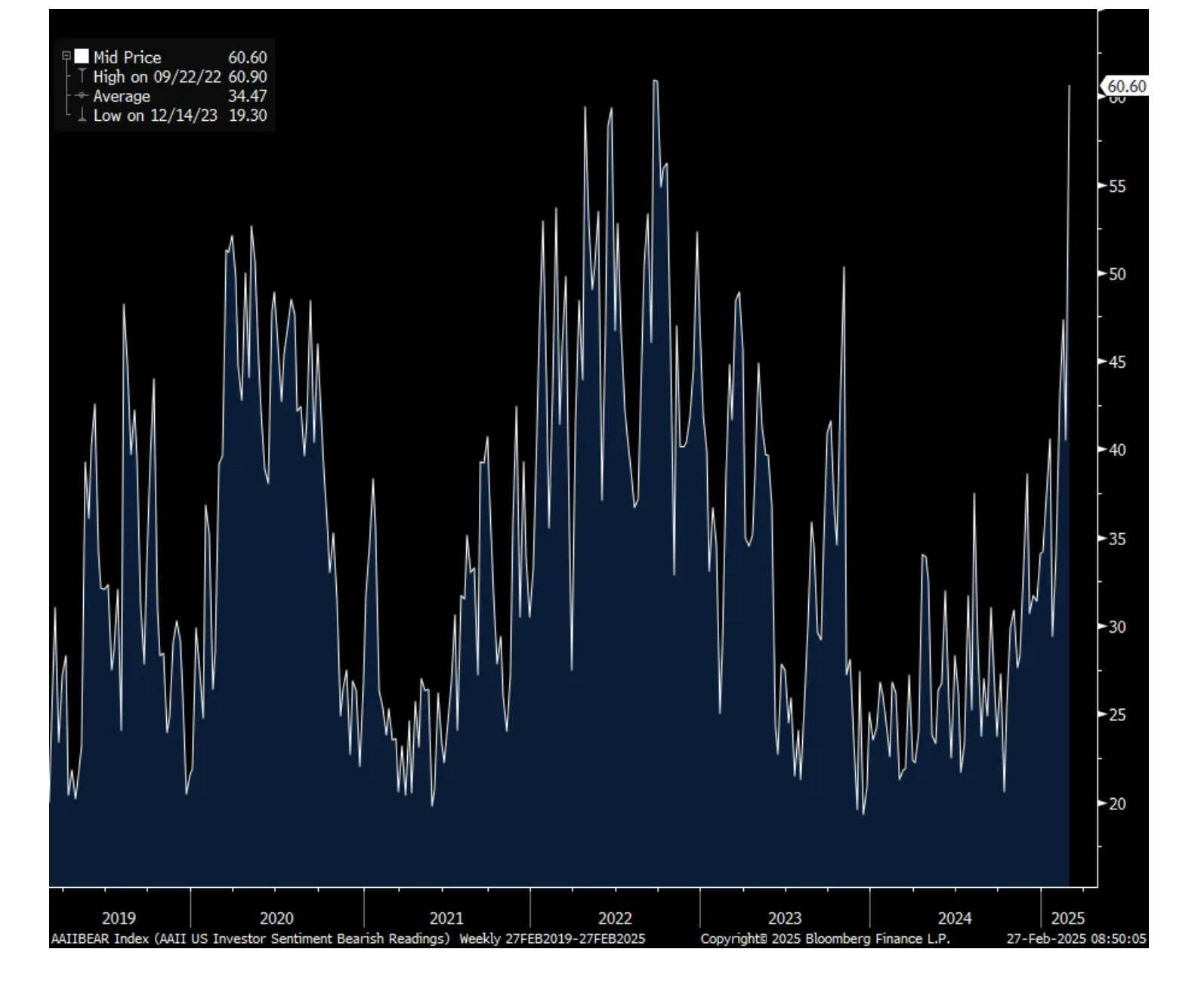

I forgot to mention stock market sentiment earlier and will right now as the AAII survey has gotten extremely bearish. Bulls fell to just 19.4, down 8.4 pts w/o/w and to the lowest since March 2023. Bears jumped to 60.6, the most since September 2022 around the market lows. In contrast, the less volatile, less fickle Investors Intelligence survey still has many more bulls than bears though a bit less so w/o/w. Bulls fell to 44.3 from 49.2 with all going to the Correction side as Bears dropped to 24.6 from 25.4.

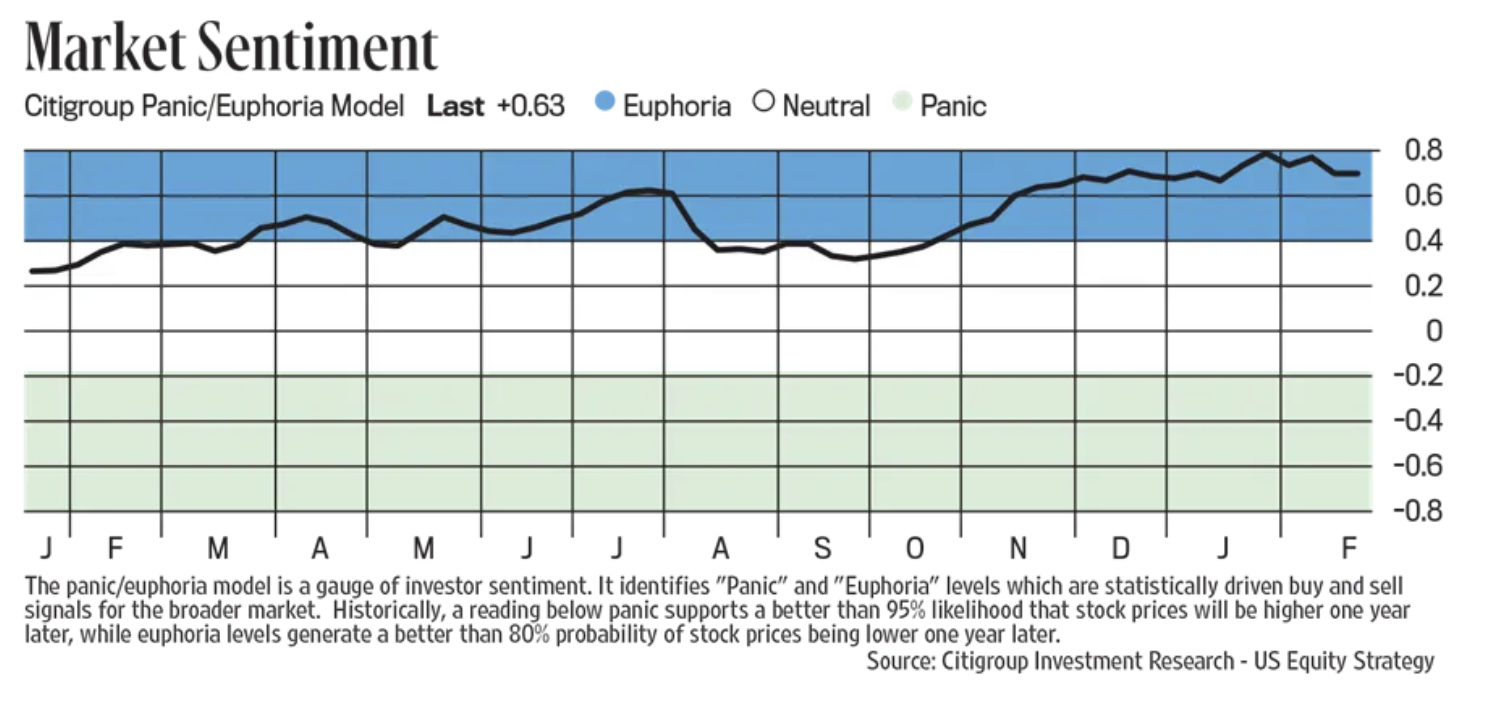

The Citi Panic/Euphoria index is off the Euphoric highs but still deep in Euphoria land at .63. On the other hand, the CNN Fear/Greed index is at just 21, in Extreme Fear, down from 45 one week ago.

Bottom line, don’t just rely on one sentiment gauge for your guide as it seems really mixed right now. More reliable is when they all lean too much in one direction.

Bulls

Bears

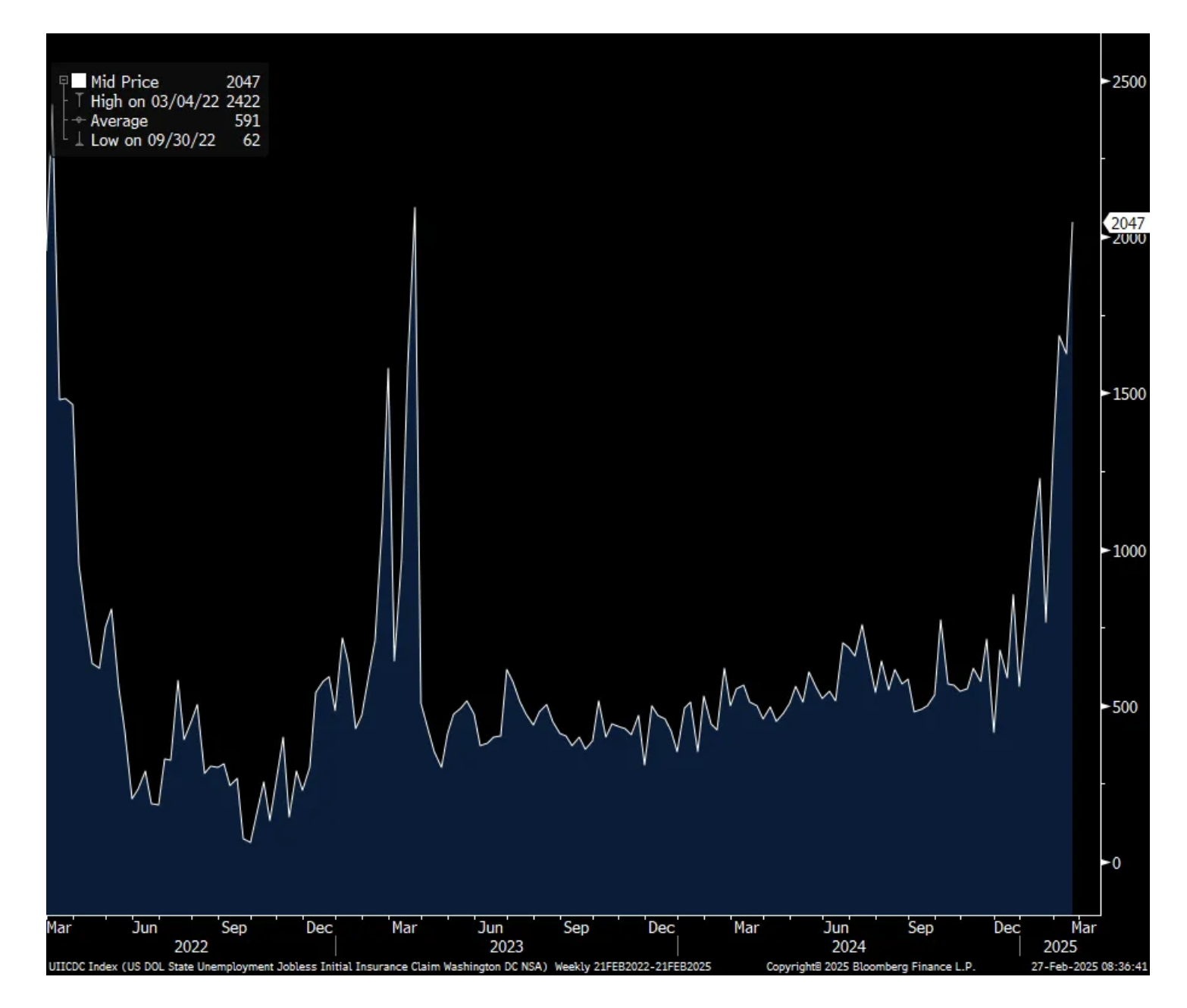

Initial jobless claims for the week ended 2/22 jumped to 242k from 220k and that was 21k more than anticipated. We might have the influence of President’s Day but no way explains all of this (see below). The 4 week average rose to 224k from 216k. Continuing claims fell by 5k after a rise of 22k last week. They stand at 1.862mm, still around the highest since November 2021.

Not surprisingly, claims are rising more rapidly in the DC metro area. In DC specifically, they rose by 421k and as seen in the chart, it stands out. However, they did fall in Maryland and Virginia and keep in mind that many government workers will be getting severance thru September and might not have filed yet.

DC Jobless Claims

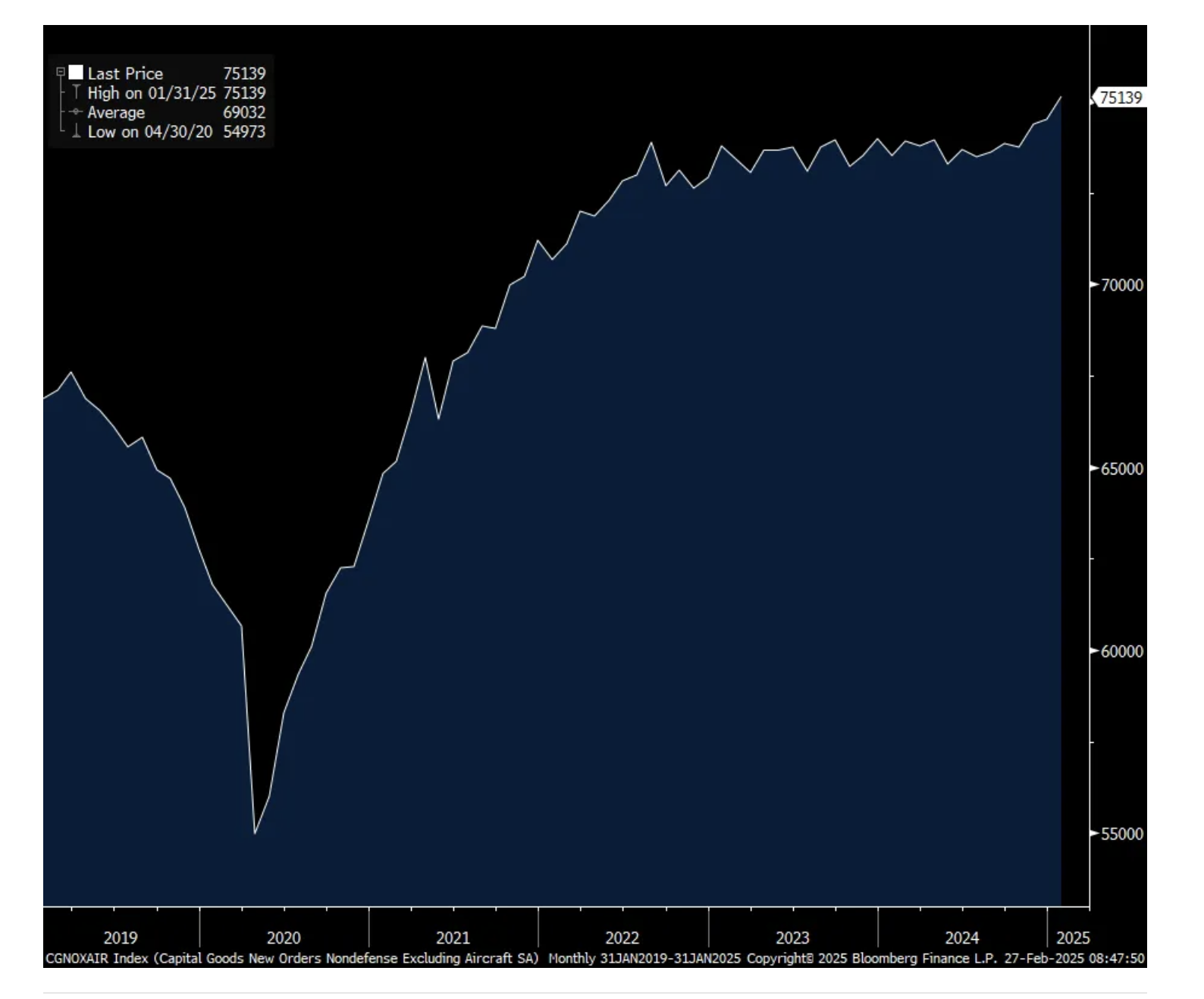

Core durable goods orders in January rose .8% m/o/m, well above the estimate of up .3%, partly offset by a 2 tenths downward revision to December. The negative though and a flow thru to Q1 GDP is that shipments of core orders declined by .3% instead of rising by .3% as forecasted and December was revised down by 2 tenths. So expect a GDP estimate cut in response.

Orders were best seen in computers/electronics, rising by 1.7% m/o/m and in primary metals by 1%. They fell by 1.2% for fabricated metals and were flattish for electrical equipment and machinery. For autos, orders fell for the 4th straight month and is down 3.8% y/o/y which is worth noting.

Bottom line, a mixed report with shipments weak but orders better. Overall, as seen in the chart below, capital spending ex AI has pretty much flat lined over the past few years. As for the early February anecdotes too, in each of the regional manufacturing surveys, capital spending plans have fallen and I have to believe that is in response to the cloudiness created by tariffs.

7:30 a.m.: Federal Reserve Bank of Richmond President Barkin (Non-Voter) speaks on "Inflation Then and Now" before the Fayetteville Cumberland Economic Development, Fayetteville, NC (No livestream. No media Q&A. No new text -- repeat of Feb. 25 speech)

9:15 a.m.: Fed Bank of Kansas City President Schmid (Voter) speaks on the economy before morning plenary at the U.S. Department of Agriculture 101st Agricultural Outlook Forum, "Meeting Tomorrow's Challenges, Today." Arlington, VA (Livestream available. Text TBD. Audience Q&A expected. No separate media Q&A);

10:00 a.m.: Federal Reserve Vice Chair for Supervision Michael Barr speaks on "Novel Activity Supervision" before the Bank and Fintech Arrangements Tech Sprint event, Washington, DC (Text available. Q&A from moderator);

11:45 a.m.: Fed Board Governor Bowman (Voter-Hawk) speaks on "Community Banking" before the Fort Hays State University Robbins Banking Institute Lecture Series (Text available. No Q&A);

1:15 p.m.: Fed Bank of Cleveland President Hammack (Non-Voter) speaks on "Financial Stability" before the Columbia University/Bank Policy Institute: 2025 Bank Regulation Research Conference, Columbia University School of International and Public Affairs, International Affairs Building, NYC (Text available. No livestream. Audience Q&A expected. No media availability);

3:15 p.m.: Fed Bank of Philadelphia President Harker (Non-Voter) speaks on the economic outlook before the Lyons Economic Forecast, presented by the University of Delaware's Center for Economic Education and Entrepreneurship, Newark, DE (Text and livestream available. Audience Q&A expected. No media Q&A)

Boockvar on More to Buy Than Nvidia, Earnings Comments

From Peter Boockvar:

Luckily, the market is finding other things to buy/Interesting earnings comments

Another great quarter from Nvidia and a raise in guidance but rather pedestrian for both relative to expectations and another Mag 7 stock losing its juice. Not an indictment of the company, just on the stock with its robust but slowing growth. Luckily, the market has found other stocks to buy.

From Nvidia:

"Post training and model customization are fueling demand for Nvidia infrastructure and software as developers and enterprises leverage techniques such as fine-tuning, reinforcement learning, and distillation to tailor models for domain specific use cases...The scale of post training and model customization is massive and can collectively demand orders of magnitude more compute than pre-training. Our inference demand is accelerating, driven by test time scaling and new reasoning models like Open AI's o3, DeepSeek-R1, and Grok 3."

"From a geographic perspective, sequential growth in our data center revenue was strongest in the US, driven by the initial ramp of Blackwell. Countries across the globe are building their AI ecosystems and demand for compute infrastructure is surging." And, "With respect to geographies, the takeaway is that AI is software, it's modern software, it's incredible modern software, but it's modern software."

I'll add, and why from an AI provider standpoint, the competition will only get more intense, the products will only get more commoditized and the users, like you and me, will end up being the biggest beneficiaries.

Salesforce focused on its agentic product in its call but whose stock is down pre market:

"I really think that we have something incredible to talk about. And, obviously, this was the quarter of Agentforce."

"Agentforce is revolutionizing how our customers work by bringing AI powered insights and actions, directly into the workflow across the customer 360 applications. This is driving strong growth across our portfolio."

Here is the but, "However, the adoption cycle is still early as we focus on deployment with our customers. As a result, we are assuming a modest contribution to revenue in fiscal '26. We expect the momentum to build throughout the year driving a more meaningful contribution in fiscal '27."

Overall revenues grew 9% y/o/y. "From an industry perspective, in Q4, health and life sciences, communications and media both performed well. While tech and manufacturing, automotive and energy were more measured."

They are being negatively impacted, like others, by the stronger dollar. "And even since our last earnings call that movement has driven an incremental $200 million headwind to fiscal '26 revenue."

Away from tech and on to the consumer.

From EBAY whose stock is down after lowering guidance:

They talked about FX headwinds too, by 40 bps.

"And I'd say with the macro environment it continues to be dynamic as it was through '24. I'd say demand in the US has been more resilient with trends in the UK and Germany still relatively weaker amid lower consumer confidence and lower GDP growth there."

"I would say the more affluent customers, our luxury businesses continue to perform well, handbag. I talked about collectibles being double digit growth right now. And so I think it's more the less affluent consumer who is pressured in this environment." Obviously something we continue to hear.

From TJX, one who focuses on that value seeking customer:

"Our sales, profitability and earnings per share were all well above our expectations. I am particularly pleased that our overall comp sales growth of 5% was driven by strong consistent comp increases of 4% or above at each of our divisions. Further, our comp sales growth across all of our divisions was once again driven by an increase in customer transactions. Clearly, our great values, gifting assortment and freshness of our mix resonated with our shoppers during the holiday season."

Also of note, "our fiscal '26 guidance assumes a small negative impact in the first half of the year from the current China tariffs on merchandise that we were committed to when these tariffs went into place."

Similar to Walmart, they are drawing customers from all demographics. "We saw nice increases in both our below 100k and above 100k income demographic areas."

And key also to their success is that they are taking market share from other retailers. "Home would be one of the more obvious ones where either business that had a home business as part of it or home only have closed."

From Sweetgreen who missed numbers and lowered guidance:

Comps grew 4% in the quarter. "This consisted of a 4% benefit from menu price increases and flat traffic and mix."

"Extreme weather in January and February affected guest traffic across approximately 60% of our fleet. The LA wildfires, while not causing physical damage to our locations, significantly disrupted operations. Given that the LA market represents nearly 15% of our revenue, the temporary closures and ongoing shifts in customer behavior have created a near term headwind."

From Bloomin' Brands that owns Outback Steakhouse, Carrabba's Italian Grill, Fleming's Steakhouse, and Bonefish Grill and whose stock was down 17% yesterday:

"the reality is that we are currently not succeeding...although our fourth quarter results were within our expected guidance range, we underperformed the industry and lost share as defined by Blackbox by 260 bps on sales and 410 bps on traffic."

Labor inflation was 3.2% as we continue to experience inflationary pressure on wages. Restaurant operating expense inflation was low single digits with additional costs from higher insurance and legal expenses."

In their guidance, "We expect commodities inflation to be between 2.5% and 3.5%, driven in large part by beef inflation. We expect labor inflation to be between 4% and 5%."

On the consumer "I would say we're seeing a choppy environment. And we're seeing a choosy consumer, but we see that more in the short term. And what I mean by that is, in terms of choppiness, we are definitely seeing some impact from weather, geopolitical issues, calendar shifts."

"As far as the choosiness of the consumer, we are seeing some check management with especially those households under about $100,000. We saw that in terms of appetizer mix, beverage attachments, and desserts that were a little bit lower than the fourth quarter. As far as the long term trends, I still feel really good about it. We saw really robust sales that Thursday, Friday, Saturday of Valentine's Day. And what we are finding is, when we meet the consumer where they're at with the right abundant value, they will make the visit and they'll visit more frequently." Again, that word, VALUE.

On to a big ticket item like an RV, from Camping World:

"Early indications of 2025 continue to show a consumer that is focused on affordability and value price units both on the new and used side."

"We never like to directly cite weather as a factor. It's no surprise that February weather patterns have been erratic, but once the weather broke, we were very pleased by the pent up demand we experienced. As this past weekend was one of the best sales weekends in our history, regardless of the month."

"If the 10 yr Treasury yield continues to stabilize and reduce, we expect to see additional retail finance rate relief for our customers, allowing them to take on more unit, while maintaining a monthly payment that fits their budget."

The data point overseas of note was the February Eurozone Economic Confidence index which rose 1 pt m/o/m to 96.3 but as seen in the chart below, continues to flat line and below its pre Covid trend. Internally, the gain was led by a 1.3 pt gain in manufacturing to a less negative figure. Consumer confidence rose too while partly offset by a drop in confidence in the services and construction sectors. Retail was unchanged m/o/m. Nothing market moving here with bond yields slightly higher after Spain also reported in line inflation stats, up 2.9% y/o/y. The euro is lower and stocks are mostly down, though doing great ytd as we know.

Europe is a really interesting place to watch in the coming years as they ramp up spending on defense and we'll see to what extent, if any, they start to ease the pressure of the EU regulatory state that many are now raising as a big impediment to economic growth.

I expect the outstanding results at Trulieve TCNNF and Green Thumb GTBIF (I have added to both almost daily) should result in a bid for MSOS (adding there too) today.

US: Futs are higher post-NVDA, though the stock’s reaction is a bit muted with the stock +1.3% pre-mkt. The balance of Mag7 are higher, Semis and Fins also stronger. Bond yields are up 5bps from 2s to 30s with USD poised to have its strongest day in 5 session. Cmdtys are weaker ex-Energy; WTI remains below $70/bbl. Today’s macro data focus is on Durable/Cap Goods and Jobless data. EU and HSTECH are weaker today, is this the beginning of a rotation back to US TMT?

and...

EQUITY AND MACRO NARRATIVE:NVDA is undoubtedly the main feature for this week, but I thought it worth flagging a potential bearish signal before posting Trading Desk color on NVDA, AI Capex, Data Centers, and the Consumer.

POTENTIAL BEARISH SIGNAL

With the focus on NVDA, you may have missed 3M / 10Y spread inverted, after setting a 52-week high on Jan 14. This spread dis-inverted on Dec 13, 2024. This may be the bond market expressing a stagflationary view. Why? For some of the same reasons we have seen the recent pullback: economic soft patch exacerbated by policy uncertainty but with a guarantee of tariffs, which will both hurt growth and increase inflation, we could see a negative outcome for the US. The key is whether the 25% tariffs on Canada and Mexico stick since that would likely push both economies into a recession. Those are our two largest trading partners and if they are in a recession, with a new tariff regime, then anticipate economic forecasts to be cut materially and downward EPS revisions, too. That said, it is far too early to sound the alarm but definitely a situation to monitor especially if this eventually spreads to 2s/10s; though it was a false flag from 2022 – 2024, I am not sure that the market will be as willing shrug that off a second time.