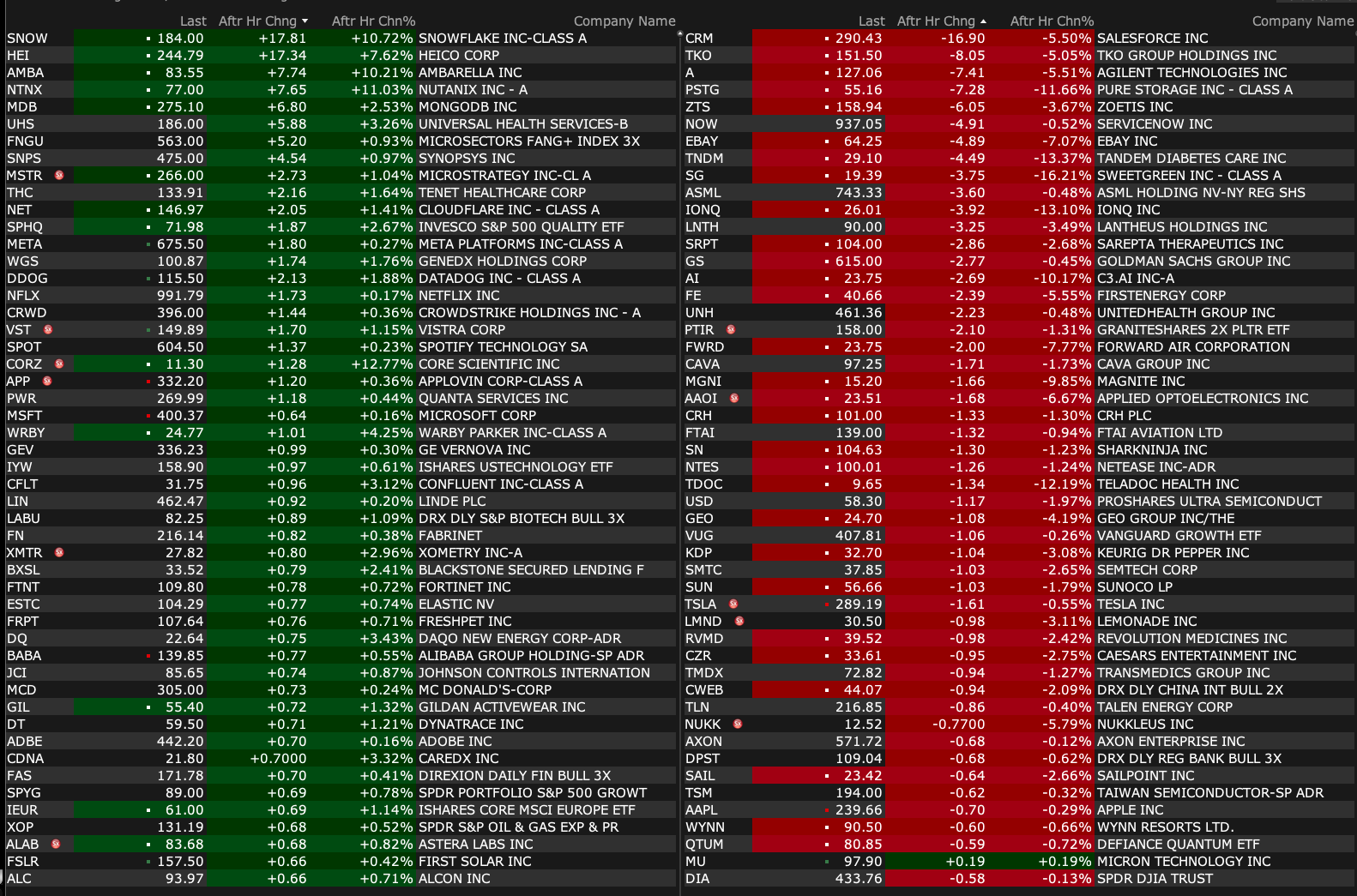

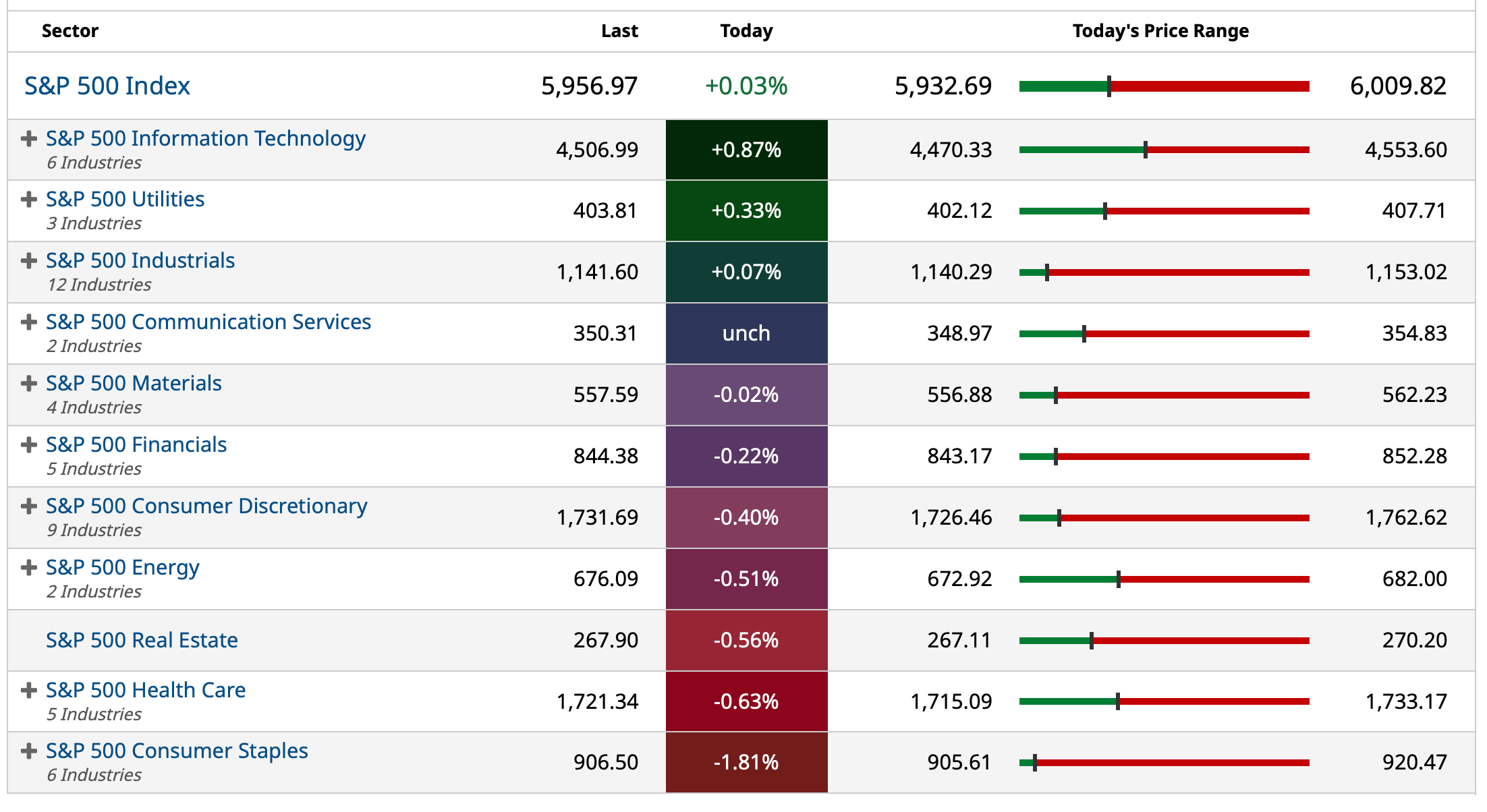

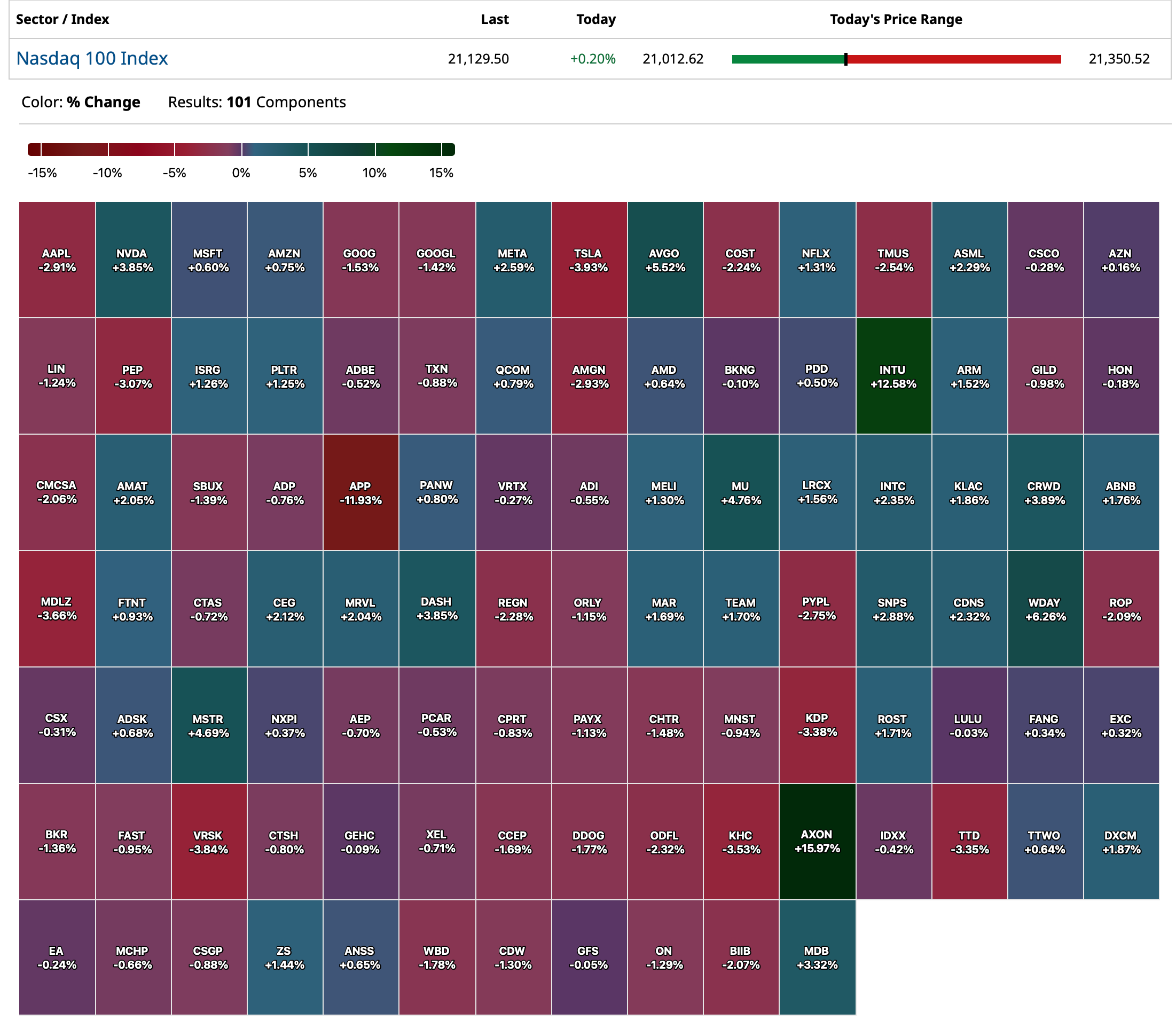

Wednesday's-After Hours Movers

As of 4:29 p.m.:

BY Doug Kass · Feb 26, 2025, 4:32 PM EST

As of 4:29 p.m.:

BY Doug Kass · Feb 26, 2025, 4:32 PM EST

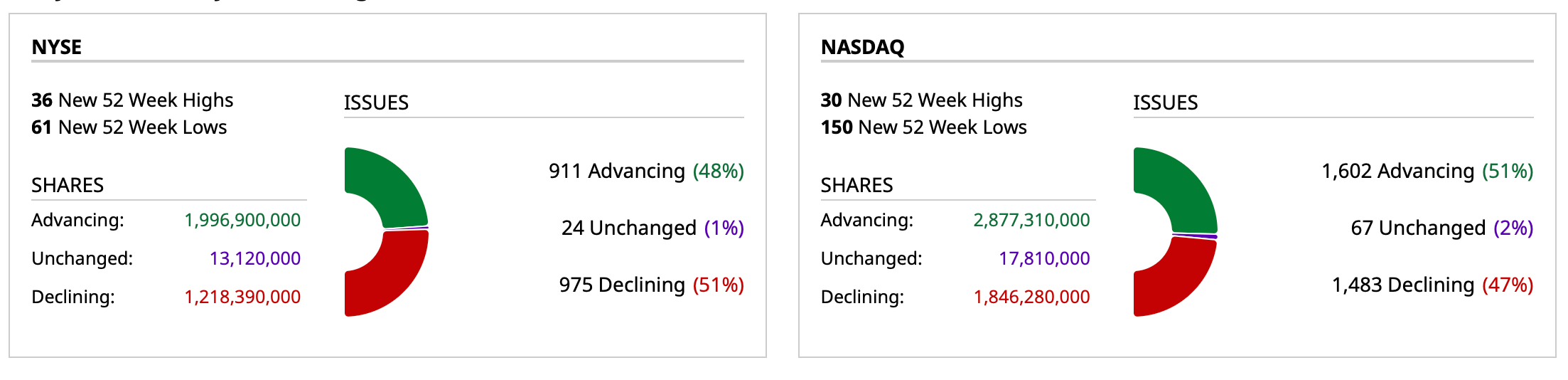

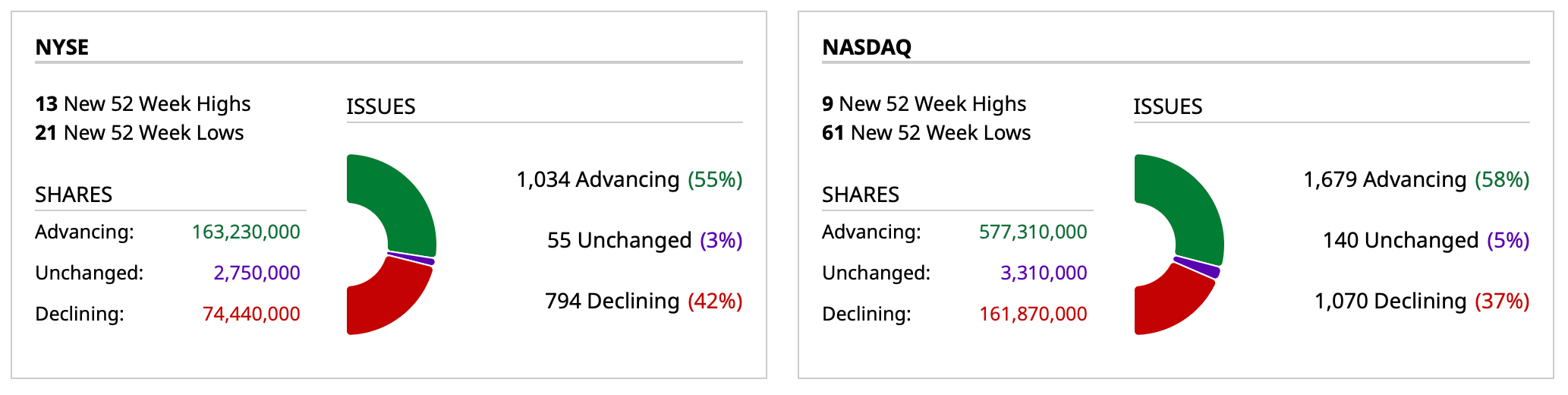

- NYSE volume 6% above its one-month average

- NASDAQ volume 11% below its one-month average

- VIX down 1.75% to 19.09

BY Doug Kass · Feb 26, 2025, 4:18 PM EST

BY Doug Kass · Feb 26, 2025, 3:29 PM EST

Enjoy the rest of the day and Nvidia's NVDA EPS beat (and higher guide).

We are in a new regime of higher volatility — consider your VAR (value at risk) and invest and trade accordingly.

Thanks for reading my Diary.

Be safe.

BY Doug Kass · Feb 26, 2025, 3:00 PM EST

Housekeeping item.

I covered my Apple AAPL short at $239.82.

I plan to re-short strength.

BY Doug Kass · Feb 26, 2025, 2:36 PM EST

From Peter Boockvar:

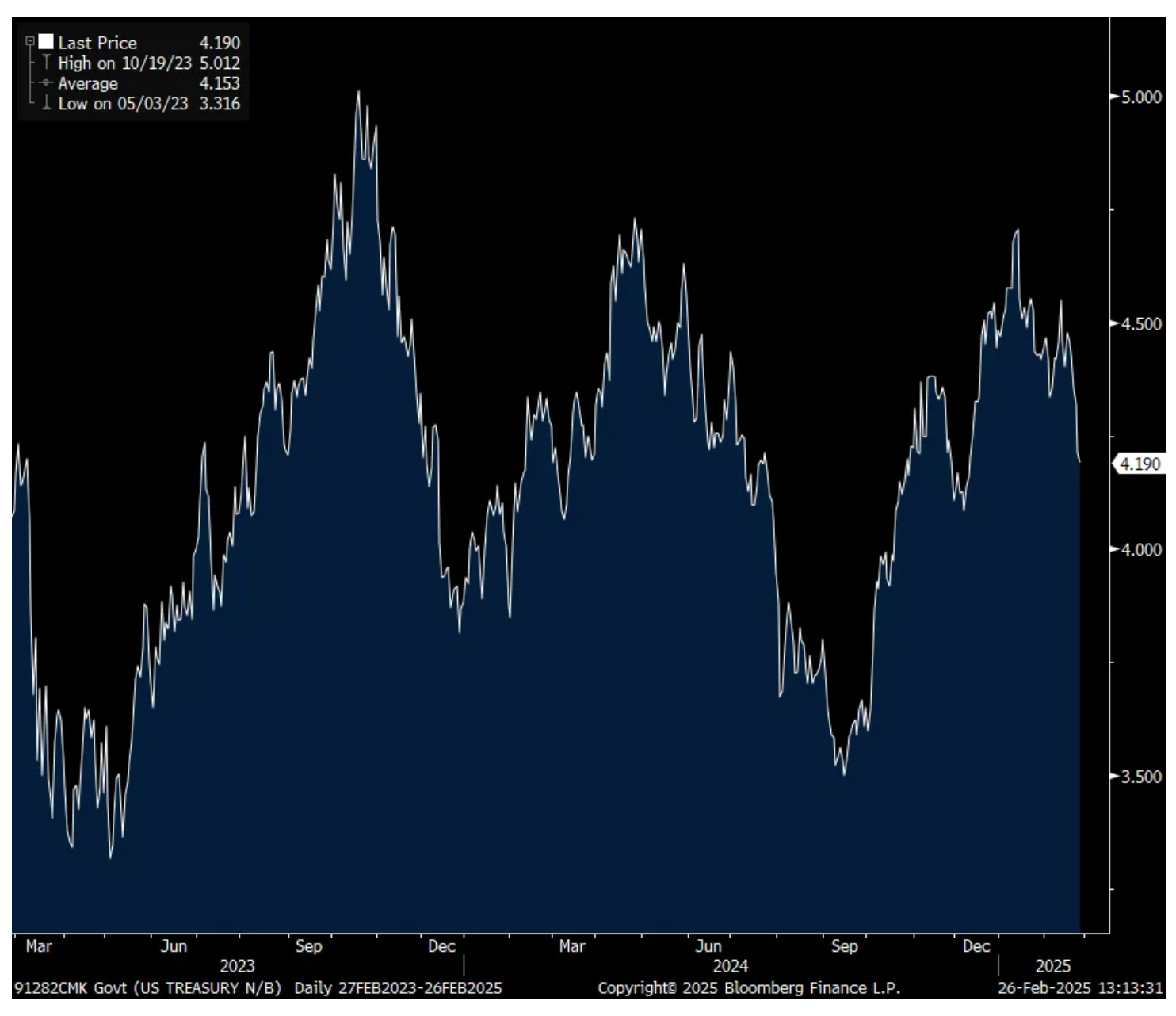

Bessent and the Treasury had a good issuance week

The just seen good 7 yr note auction caps a good week for Scott Bessent and the US Treasury in his issuance of 2s, 5s and today’s 7 yr. The yield of 4.194% was about 1 bp below the when issued pricing. The bid to cover of 2.64 was a touch above the one year average of 2.61. And, direct and indirect buyers took 91% of the auction, near the recent highs.

Bottom line, we’ve seen a really nice rally in US Treasuries across the curve and we all speculate why. I attribute it to a few things. While the economic data hasn’t really changed much, the imbalance is still obvious with all of the strength coming from upper income spenders, AI spend and everything related to the government. Softness has been seen elsewhere. But now we have the likelihood that government spending is likely to slow in its trajectory and tariffs too will negatively impact economic growth.

Inflation expectations haven’t fallen nearly as much as the drop in nominal yields as seen in the breakevens which points to more growth concerns than the belief that inflation will fall much from here. Maybe the tariff influence separating the two.

I also want to point to the shakiness in the Mag 7 trade that I think is coming to an end as I’ve said many times now. As the whole world has piled into these stocks, and I literally mean the entire world, this is a really big deal if I’m right because if it leads to an eventual market correction, that upper income spending pillar will get shaky legs. Hopefully, the investing dollars will just find other things to buy instead of dragging everything lower. That said, upper income savers will continue to benefit from interest income with interest rates staying high for a while still.

7 yr Auction

BY Doug Kass · Feb 26, 2025, 2:25 PM EST

I'm back to delta-adjusted neutral on the Indices.

BY Doug Kass · Feb 26, 2025, 2:01 PM EST

I covered today's SPY/QQQ shorts on the whoosh lower:

* SPY $595.31

* QQQ $515.79

From earlier this trading session:

* Still baby steps...

Sold more Index longs:

* (SPY) $599.07

* (QQQ) $518.28

Position: Long SPY common M QQQ common M, Short SPY calls M QQQ calls M

By Doug Kass Feb 26, 2025 10:39 AM EST

BY Doug Kass · Feb 26, 2025, 1:09 PM EST

I have to give a talk about the markets to a group later today so I will be leaving at around 3:30 p.m. (missing the Nvidia NVDA excitement).

I also won't be publlishing "Things" column until tomorrow morning.

BY Doug Kass · Feb 26, 2025, 12:20 PM EST

TechNova

A tiring response to Dougie's "Why HODL?"

Love you to pieces Dougie, but you rail on CNBC hosts constantly for their fickle arguments and for shilling nonsense.

If I wore your arguments in this post as garments on the street, I would be arrested for indecent exposure given how thin they are.

With much love.

Dougie Kass

I think it is great that you made so much money.

Mine is a brief column which provides what I believe to be clear observations about the security of crypto.

Nothing more, nothing less.

I am not short bitcoin.

If I was certain in view (or could analyze the asset class) I would be short.

I can not analyze (and produce an intrinsic value calculuation) and I am not short.

I rail on several CNBC idiots because they have no process (and not fickle arguments), they make decisions on feel.

They entertain by memorizing sound bytes (observed thru the rear view mirror) and not by doing research - they are entertainers who get paid and they couldnt get jobs in a serious hedge fund with their limited body of knowledge about the markets, sectors and individual companies.

BY Doug Kass · Feb 26, 2025, 11:56 AM EST

BY Doug Kass · Feb 26, 2025, 11:30 AM EST

- NYSE volume is 1% above its one-month average;

- Nasdaq volume is 18% below its one-month average;

- VIX index: down 5.92% to 18.28

BY Doug Kass · Feb 26, 2025, 11:15 AM EST

PEP is -$4.60 to $151.85.

I reshorted yesterday:

I'm back shorting PepsiCo (PEP) at $157.56.

Position: Short PEP (VS)

P

Feb 25, 2025 1:26 PM EST

BY Doug Kass · Feb 26, 2025, 10:55 AM EST

* Still baby steps...

Sold more Index longs:

* SPY $599.07

* QQQ $518.28

BY Doug Kass · Feb 26, 2025, 10:39 AM EST

Another Comments Section exchange:

skeptcl

22 minutes ago

Hmmmm

maybe I am wrong but how does Jensen come on CNBC tonight after the call w a shitty guide

DK

Dougie Kass

STAFF

Just Now

I know for a fact that "Meet" Bret Jensen will be in a certain dive bar on Atlantic Avenue in Delray Beach at that time.

Oh, that Jense!

That's very different... Never mind! Nevermind - Emily Litella

BY Doug Kass · Feb 26, 2025, 10:15 AM EST

BY Doug Kass · Feb 26, 2025, 10:05 AM EST

From Peter Boockvar:

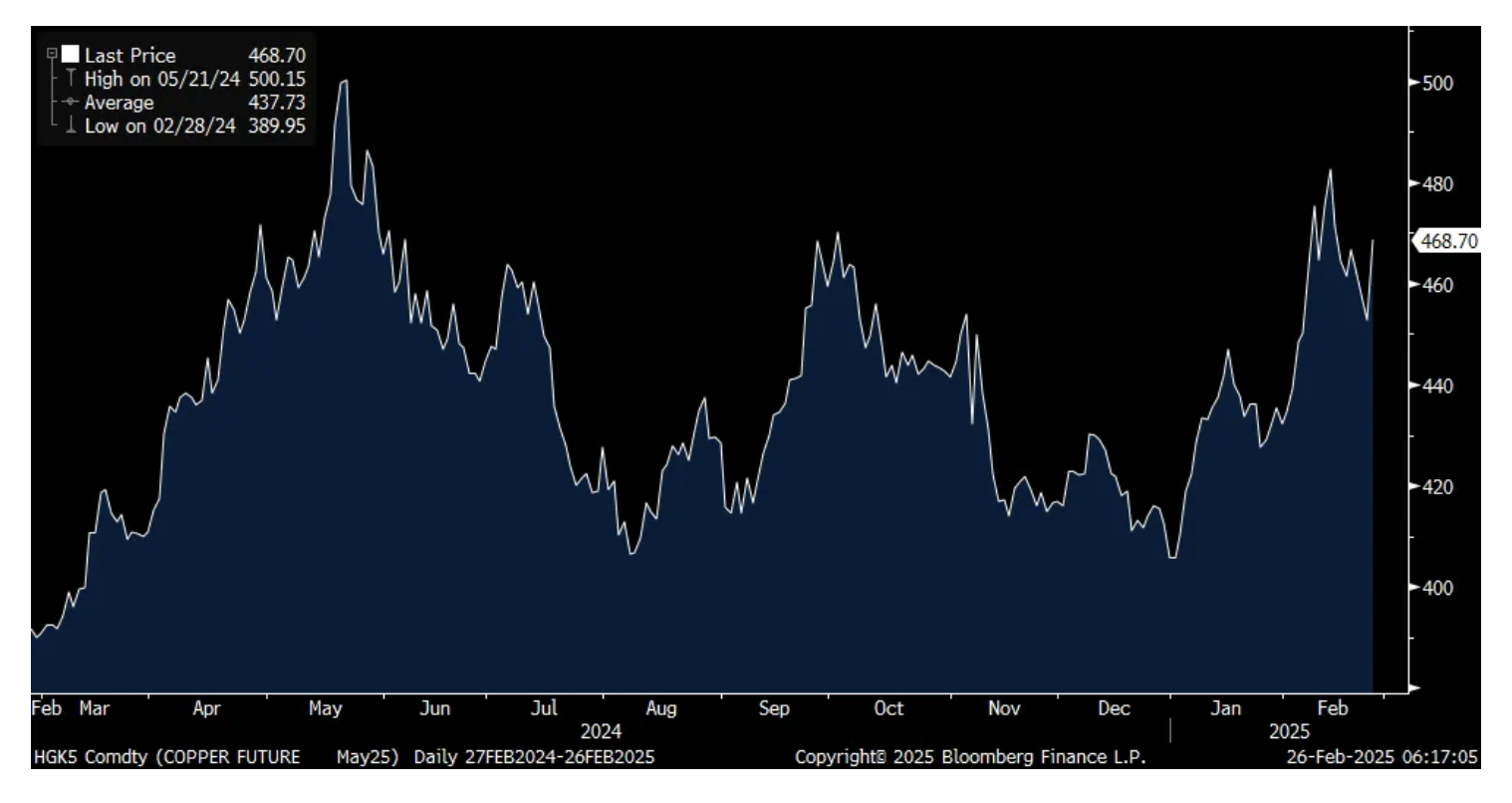

Let's start again with the possible impact of tariffs. Copper is jumping by 3.5% after it was said yesterday that the Commerce Department was going to look into putting tariffs on imported copper in order to defend US production.

The Alcoa CEO speaking yesterday at the BMO Metals, Mining & Critical Minerals conference said this on the impact of possible aluminum tariffs on Canada and Mexico:

"So the tariff situation is dynamic, is the term that I would use...but our current view is that we will have a stacked tariff system from metal coming from Canada into the US. Now, I say Canada, I'm not that focused on Mexico simply because so much of our operations are in Canada and so much of the metal comes for the US from Canada."

"Currently the US is short 4 million metric tons on an annual basis of aluminum. We import, the US imports that from Canada largely, which is 2.8 million metric tons of the 4 million metric tons short, and the other 1.2 million metric tons from different parts of the world."

Between the tariff on aluminum of 25% and a separate 10% on energy and critical minerals, "Our view is that currently those two tariffs would stack for a 35% net tariff coming from Canada. We think that's a particularly bad outcome for a number of reasons and I'll highlight some of them. But first of all, if there is a differential tariff between Canada and the rest of the world, that will incent or motivate metal to go from Canada into Europe, and potentially pull metal from the rest of the world, Middle East and India, into the US. You will literally see ships passing each other that have the exact same products coming from Europe and coming into Canada. And it really makes very little sense."

"I don't have updated numbers for a 35% tariff, but we have a view that a 25% tariff will destroy about 20,000 direct US aluminum industry jobs and could result in 80,000 indirect jobs being eliminated in the US. So we view it's bad for the US."

Copper

Speaking of the labor market, ZipRecruiter is my go to quarterly earnings call as Ian Siegel tells us about the state of things. He called out a year ago the slowdown in job growth from the robust recovery pace in 2023.

Some product improvements helped lift web traffic in Q4 by 15% and "We made these advancements while facing a difficult hiring environment. Seasonally adjusted hires have declined on a y/o/y basis for 28 consecutive months, surpassing the Great Recession of 2008. Fueling the decline is a steep drop in people quitting their jobs. The Quits Rate remains near its lowest level since 2015, excluding the onset of the Covid pandemic."

"Despite the protracted labor market downturn, we enter 2025 with cautious optimism from both internal and external indicators. The NFIB's Small Business Optimism index in December posted its highest reading since October of 2018, which can be a leading indicator for employer hiring plans. There are other encouraging underlying signs internally, such as an uptick in employer account reactivations."

However, "Despite these positive signals, business uncertainty lingers over employer hiring plans."

"Quarterly paid employers were 58,000, representing an 18% decrease vs Q4 '23 and an 11% decrease sequentially. The y/o/y and q/o/q decreases are primarily reflective of reduced demand from SMBs, which comprise the majority of our quarterly paid employers, and the continued uncertainty and volatility of the labor market."

Some more color from Home Depot in their earnings call:

"we saw greater engagement in home improvement spend, despite ongoing pressure on large remodeling projects...In addition, we also saw incremental sales as a result of the ongoing hurricane recovery efforts. However, the higher interest rate environment continues to pressure larger remodeling projects."

"Additionally during the quarter, we continued to see our customers trading up for new and innovative products. Big ticket comp transactions, or those over $1,000, were up .9% compared to the fourth quarter of last year. We were pleased with the performance we saw in categories such as appliances, building materials and lumber."

"However, we continue to see softer engagement in larger discretionary projects for customers that typically use financing to fund the project, such as kitchen and bath remodels...both Pro and DIY comp sales were positive, with Pro outpacing the DIY customer."

From Jack in the Box, whose stock fell almost 8% yesterday after their Q2 guide was soft:

"As with others in the industry, traffic and macro pressures persist, so it likely won't come as a surprise to hear that there are more headwinds than tailwinds for us, thus far in the second quarter. We are running negative quarter-to-date and expect a negative Q2 same store sales result for both brands." They also own Del Taco.

From Cava, who similar to Chipotle, are outperforming their QSR competitors with 21.2% comp gains "driven by traffic growth of 15.6%." Their business seems to lie right now in the sweet spot in between quick service and casual dining:

"It is clear that our unique value proposition, the quality and relevance of our Mediterranean cuisine, the convenience of our multi channel format, and the experiences we provide across our physical and digital channels is meeting the moment for the modern consumer."

Wage growth rose 4% for its employee base.

Also, "as of January 2025, we implemented an approximate 1.7% in restaurant menu price adjustment and at this time we have no plans for further price increases this year."

From Krispy Kreme whose stocked got hit hard yesterday as they dealt with a major cybersecurity attack and weak guidance:

With regards to the first quarter guide, "we've seen consumer softness. We're also seeing an impact from weather in the Southeast and fires in California."

Later in the call they said something similar, "It has been a choppy start of the year in our traditional retail locations in the US and those freezing temperatures and wildfires but we also see the value conscious consumer under pressure."

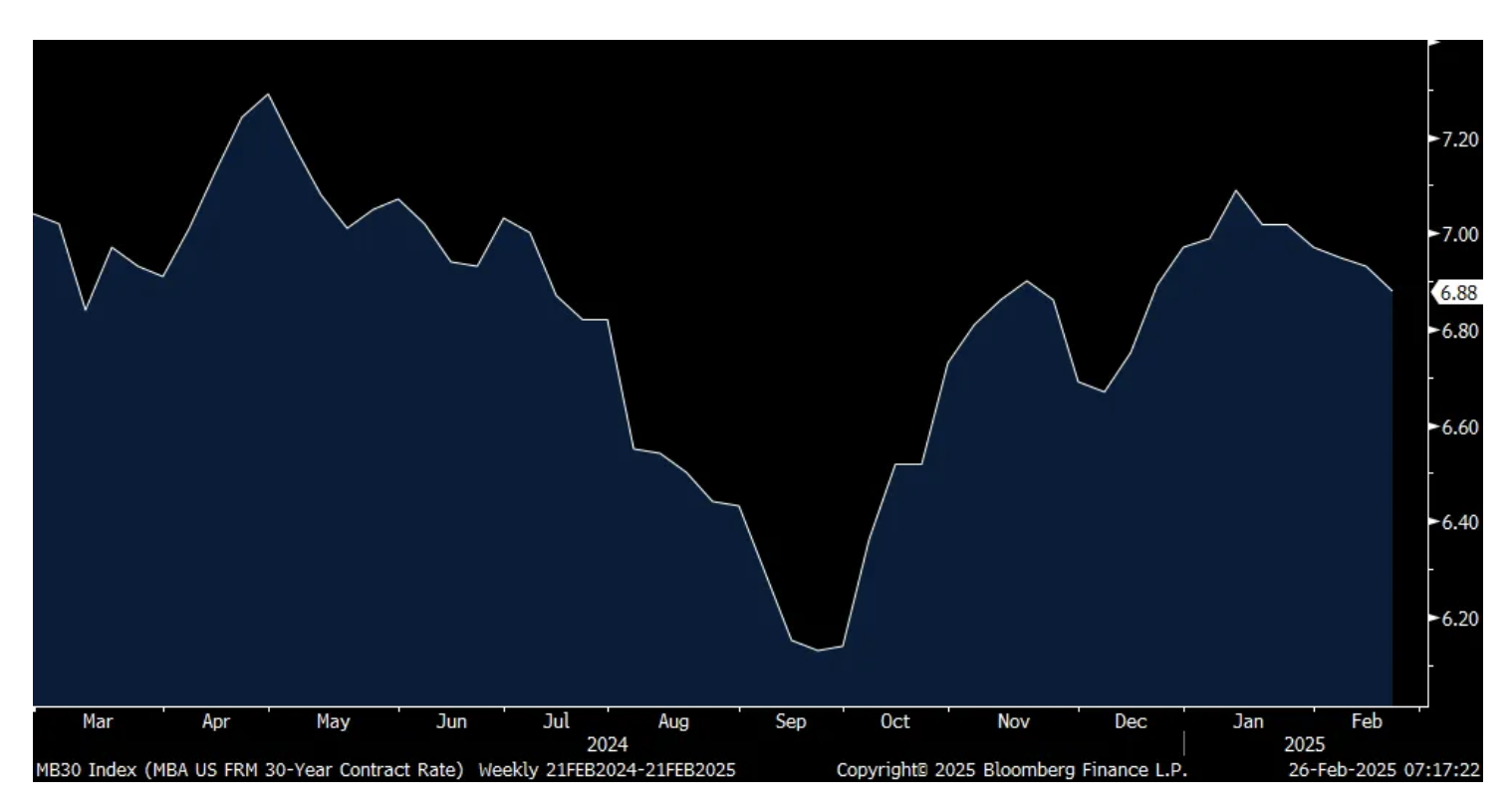

The lowest mortgage rates in two months at an average of 6.88% did not help mortgage applications for the week. Purchases were flat, up .2% after four weeks in a row of declines. Refi's were down by 3.6% w/o/w. With home prices up 52% in 5 years, the purchase market is going to need more than just a 20-30 bps drop in mortgage rates to spur buying. The market really needs more supply and maybe lower home prices to stimulate demand.

Average 30 yr Mortgage Rate

The Bank of Thailand followed the Bank of Korea with a 25 bps rate cut and to 2.00% but was unexpected and don't expect another cut anytime soon as they said, "Our policy space is not much...The bar will be high next time." They expect 2.5% economic growth this year.

German consumer confidence in March deteriorated again as the GfK index fell to -24.7 from -22.6. That's the weakest since April 2024 and below the estimate of -21.6. The report said "Consumer climate has been stagnating at a low level since the middle of last year. There is still a great deal of uncertainty among consumers and a lack of planning security." We'll see what happens in coming months, quarters with a new government in place.

French consumer confidence in February rose 1 pt m/o/m to a four month high at 93. For perspective, it was at 105 in February 2020.

German Consumer Confidence

BY Doug Kass · Feb 26, 2025, 9:47 AM EST

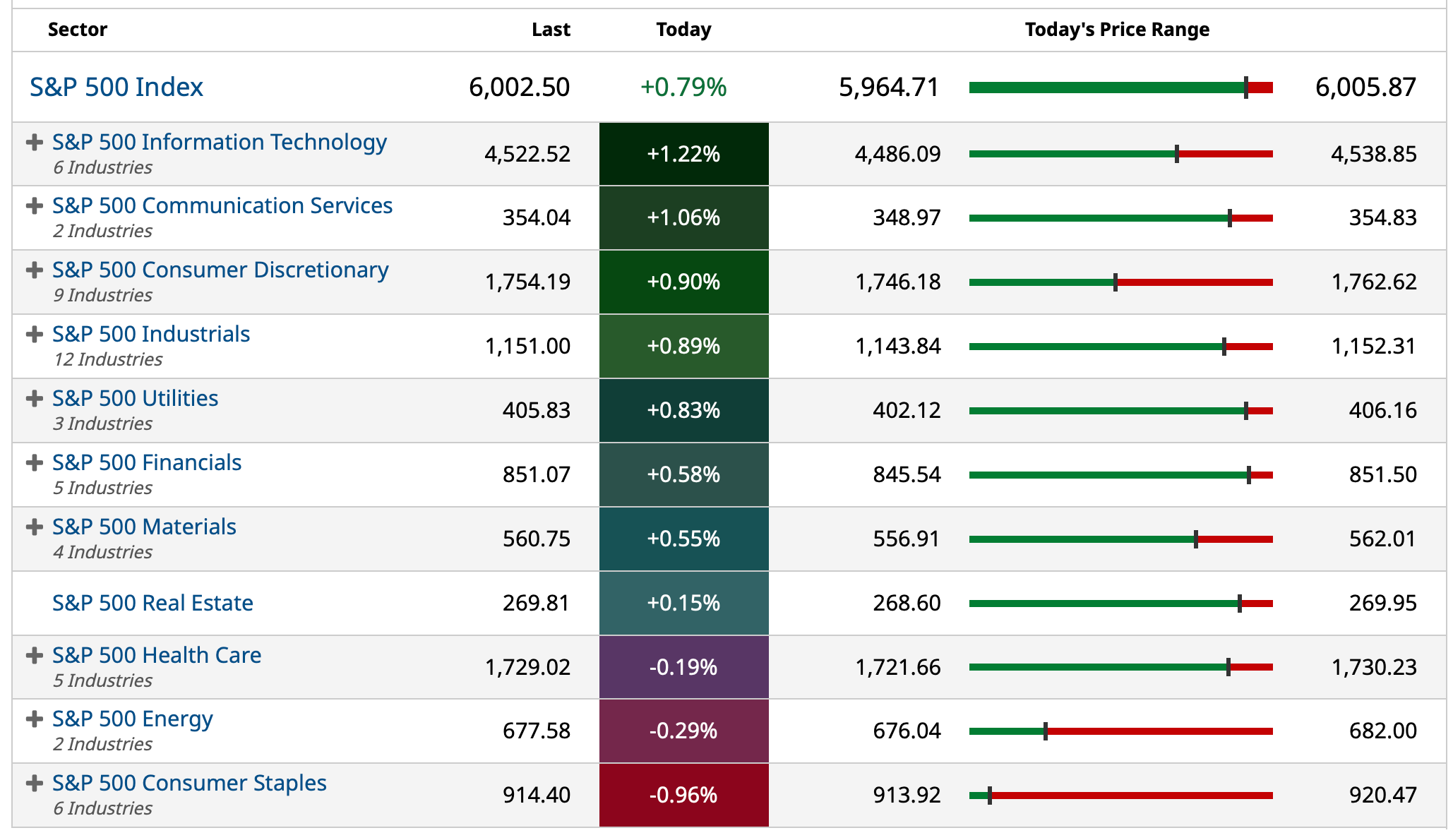

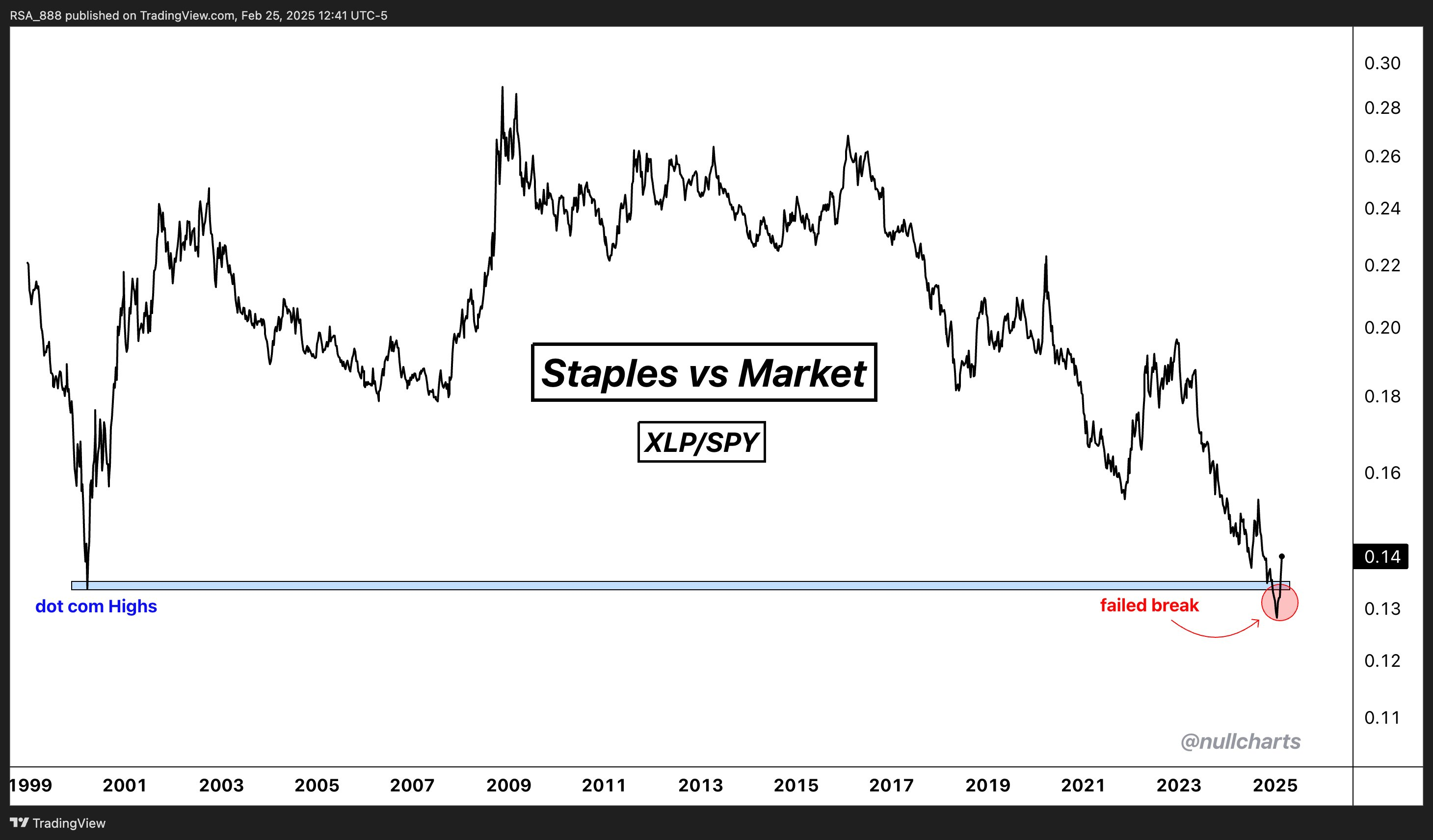

Based on history, strength in consumer staples equities (stocks like PG, KO, PEP, etc.) is an indicator that broader market weakness may lie ahead.

Of late, staples have been conspicuously strong. Consider these two charts on that sector:

XLP: Consumer Staples

XLP vs. SPY

Postscript: "Beware the Ides of March” is a line from William Shakespeare's play Julius Caesar. It is a warning to be careful on March 15, the day of the Ides of March, when Julius Caesar was assassinated.

BY Doug Kass · Feb 26, 2025, 9:30 AM EST

I added to MSOS at $3.13.

BY Doug Kass · Feb 26, 2025, 9:28 AM EST

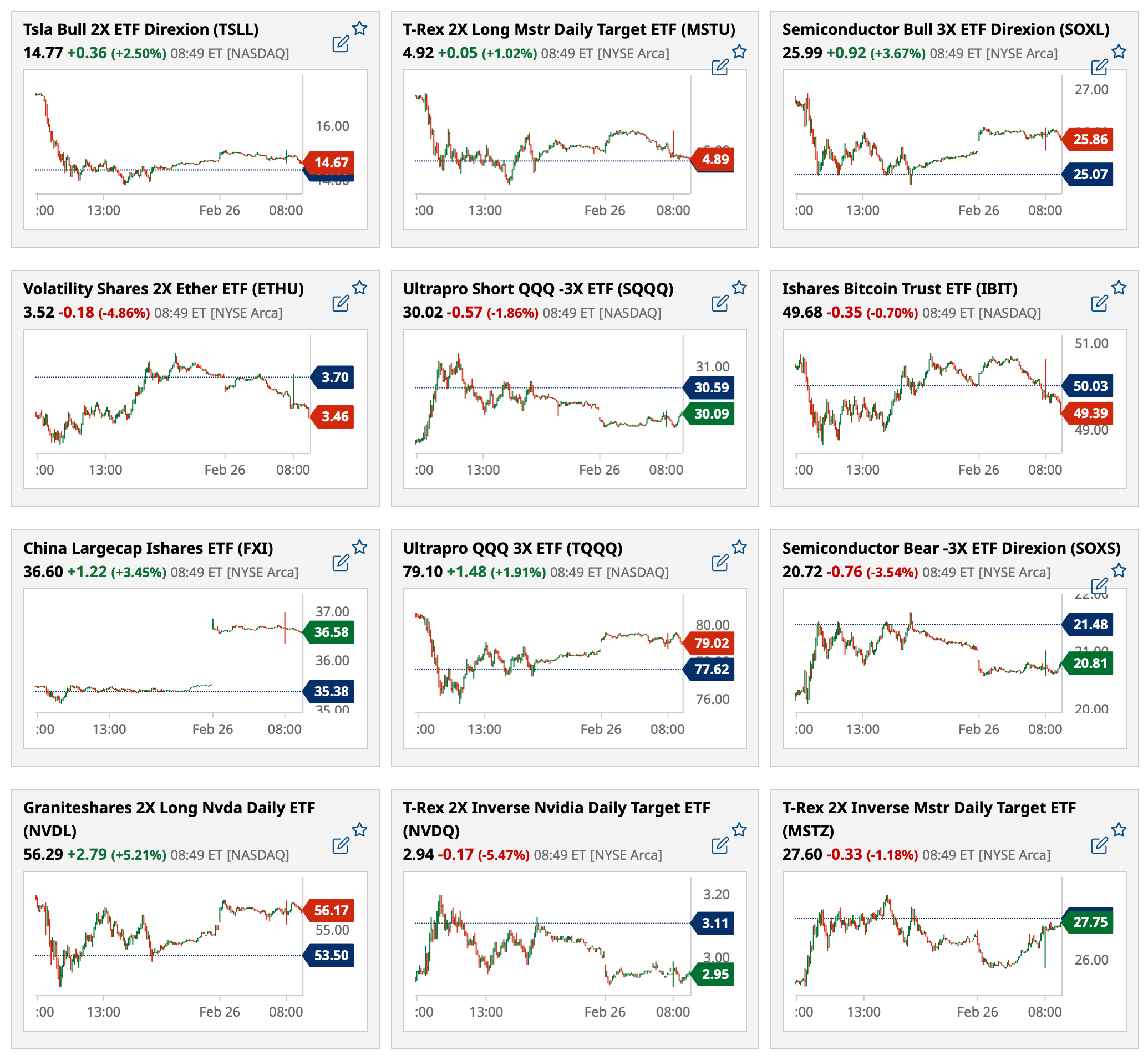

Most active premarket ETFs as of 8:54 a.m. ET:

BY Doug Kass · Feb 26, 2025, 9:23 AM EST

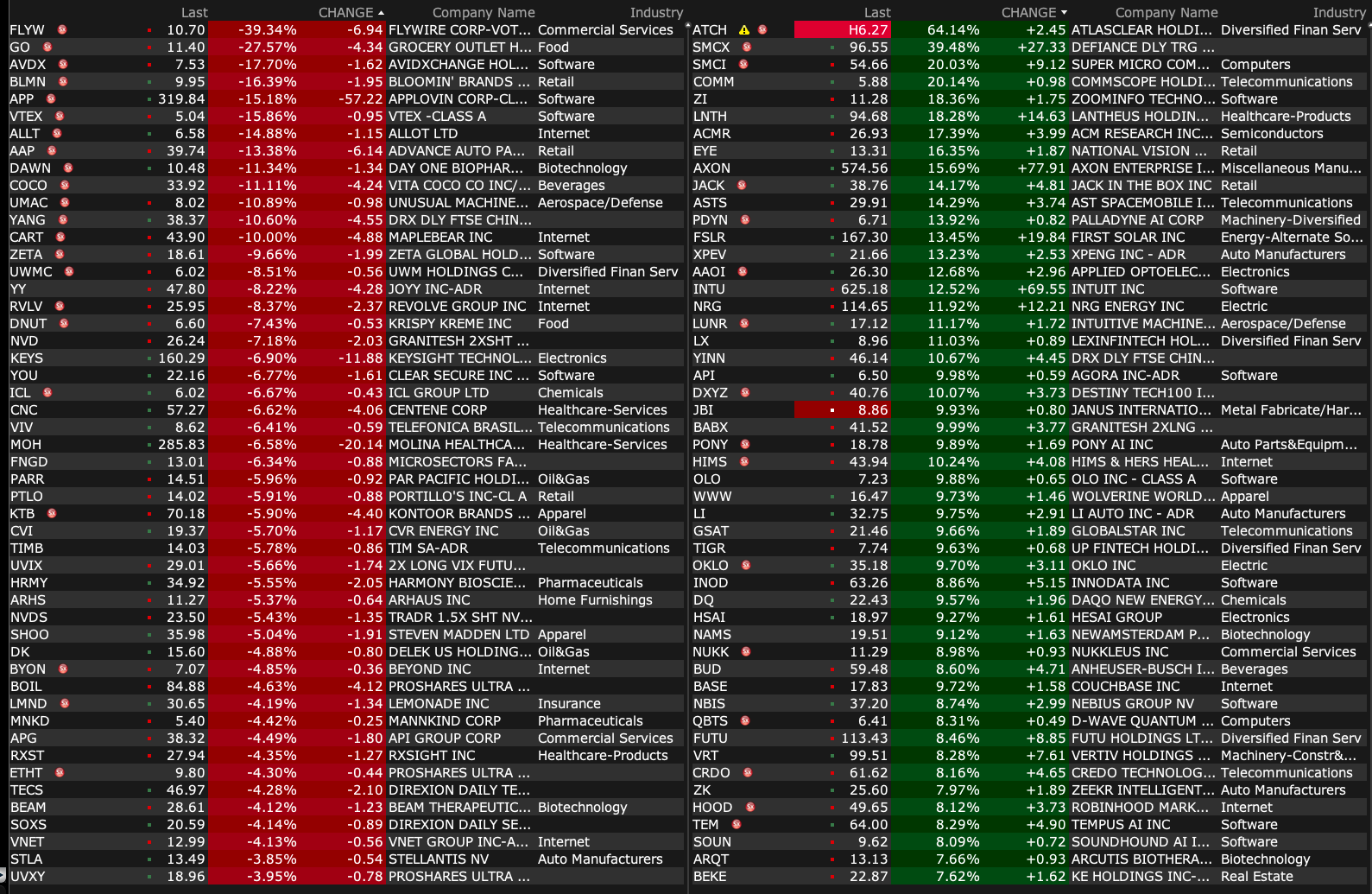

-SMCI +22% (earnings)

-ZI +20% (earnings, guidance)

-PRCH +19% (earnings, guidance)

-SEZL +17% (earnings, guidance)

-OLO +15% (earnings, guidance; files indeterminate mixed shelf)

-AXON +13% (earnings, guidance)

-INVX +12% (earnings, guidance)

-CCCS +11% (earnings, guidance)

-JACK +11% (earnings, guidance)

-WDAY +10% (earnings, guidance)

-BUD +8.6% (earnings, guidance)

-INGN +8.4% (earnings, guidance)

-INTU +8.4% (earnings, guidance)

-BLZE +6.5% (earnings, guidance)

-MASI +6.2% (earnings, guidance; files mixed shelf of indeterminate amount)

-CPNG +5.5% (earnings, guidance)

-VLN +4.9% (earnings, guidance)

-WWW +4.3% (Director purchases $536K in common stock)

-GM +3.6% (approves new share repurchase plan of $6B, including $2B ASR; raises quarterly dividend from $0.12 to $0.15/shr)

-LOW +3.6% (earnings, guidance)

-BCO +2.7% (earnings, guidance)

-TJX +2.3% (earnings, guidance)

-FLYW -34% (earnings, guidance)

-GO -26% (earnings, guidance)

-SINT -22% (announces $5M Private Placement Priced At-the-Market under Nasdaq Rules at $3.45/shr)

-AGL -19% (earnings, guidance)

-AVDX -15% (earnings, guidance)

-DNA -15% (earnings, guidance)

-LMND -13% (earnings, guidance)

-OSUR -12% (earnings, guidance)

-XPEL -12% (earnings, guidance)

-CART -7.8% (earnings, guidance)

-VTEX -6.9% (earnings, guidance)

-SPT -6.2% (earnings, guidance)

-NKGN -5.2% (shareholders approve amendment to effect between 1-for-2 and 1-for-20 reverse stock split)

-LCID -4.2% (earnings, guidance)

-UTHR -3.5% (earnings)

-AAP -3.2% (earnings, guidance)

-KEYS -2.9% (earnings, guidance)

-UWMC -2.7% (earnings, guidance)

-SPNT -2.5% (prices ~4.1M shares at $14.00/shr in secondary offering)

-SWX -2.0% (earnings, guidance)

BY Doug Kass · Feb 26, 2025, 9:15 AM EST

"It means setting small, reasonable goals for yourself- one tiny step at a time."

-What About Bob? Baby Steps - YouTube

Next short tranche (but taking baby steps):

* SPY $597.53

* QQQ $517.68

Remember:

"The best psychiatrist in the world is the one inside you."

Uh, oh:

"Vacation? That's a month - what if I need you."

BY Doug Kass · Feb 26, 2025, 8:55 AM EST

douglas cassel

3 minutes ago

Answer to Doug K's question

The table below shows the average returns of the Bitcoin index over the last periods.

Period Average annualised return Total return

Last year 150.9% 150.9%

Last 5 years. 63.5% 1,067.5%

Last 10 years 86.7% 51,259.5%

DK

Dougie Kass

STAFF

Just Now

the historical price action is meaningless to me

investment wisdom is always 20/20 when viewed in the rear view mirror

historical returns provide no predictive value to future returns in bitcoin or in any other asset class

BY Doug Kass · Feb 26, 2025, 8:50 AM EST

BY Doug Kass · Feb 26, 2025, 8:37 AM EST

TBA: Fed Bank of Richmond President Barkin (Non-Voter) speaks on "Inflation Then and Now" before the Northern Virginia Chamber of Commerce. (Time, other details TBA);

Noon: Fed Bank of Atlanta President Bostic (Non-Voter) participates in conversation on the economic outlook and housing before the Urban Land Institute's annual Housing Opportunity Conference, Atlanta, GA (Livestream available. Audience Q&A expected.No media Q&A. No embargoed text)

BY Doug Kass · Feb 26, 2025, 8:25 AM EST

Knowledge@Wharton on the Fed and Inflation.

BY Doug Kass · Feb 26, 2025, 8:15 AM EST

As of 7:33 a.m.:

BY Doug Kass · Feb 26, 2025, 8:05 AM EST

* Riddle me this, Mooch...

Given the facts below I would like bitcoin bulls to explain the case for HODL.

Stated simply, I do not understand the fascination with crypto when it can be stolen at the blink of an eye by a global army of hackers. (Based on recent price weakness, I think the markets might finally be figuring this one out!)?

Consider these series of recent events In North Korea:

* Hackers stole Ethereum tokens worth around $1.5 billion on Sunday in the largest-ever known heist of any kind — by far.

* Crypto sleuths traced the stolen coins to wallets linked to North Korea's state-linked Lazarus Group, suggesting that North Korea probably more than doubled its 2024 cryptocrime haul of $650 million in just one attack.

* North Korea uses its crypto heists to fill state coffers and fund its weapons programs, and these proceeds will buy Pyongyang quite a lot of nuclear kit. Coincidentally, this haul of $1.4 billion is exactly what Janes estimates North Korea's total annual defense budget to be.

BY Doug Kass · Feb 26, 2025, 7:30 AM EST

We all know that most of technical analysis is reactionary and not anticipatory.

After being uber-confident in bullish view, the comments from the technically inclined (below) have changed...

My approach, like it or leave it, is to be anticipatory — buying stocks that sell at discounts to intrinsic value and shorting stocks that are at a premium to my calculus of intrinsic value.

Neither is right or wrong. There are many ways to skin the market's cat!

As we say in harness racing, "Horses for courses"...

Bonus — Here are some great links:

March Is Typically Seasonally Weak

BY Doug Kass · Feb 26, 2025, 7:10 AM EST

In yesterday's whoosh lower I went delta-adjusted neutral in Indices (long common SPY/QQQ, short calls SPY/QQQ).

With S&P futures +32 handles this morning (6:50 a.m.) I am taking off (small) some of my long Indices:

* SPY $597.38

* QQQ $517.36

BY Doug Kass · Feb 26, 2025, 6:59 AM EST

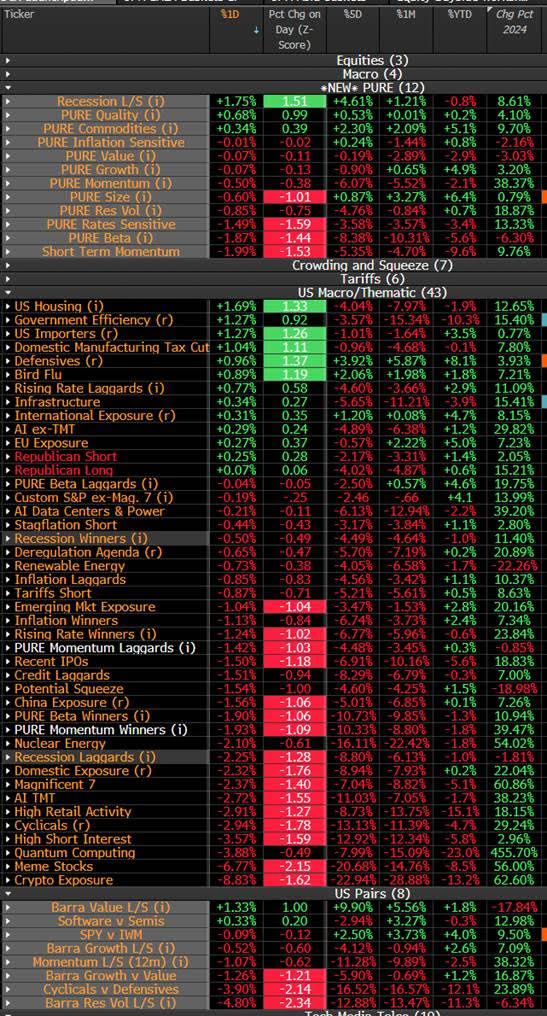

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Feb 26, 2025, 6:55 AM EST

From JPMorgan:

US: Futs are higher as the market awaits NVDA earnings after today’s close. Pre-mkt, Mag7 names are all higher ex-AAPL and NVDA +2.6% aiding the bid for Semis. Bond yields are 1-2bps higher but will little reaction to the House passing the blueprint for the next budget that is likely to materially increase the deficit. The global risk-on tone is not extending to cmdtys where there is weakness across all 3 complexes.

and...

EQUITY AND MACRO NARRATIVE: The SPX fell 47bps, part of a four-day losing streak, its first of the year, with the index giving back 3.1% after setting an all-time high last Wednesday.

BY Doug Kass · Feb 26, 2025, 6:45 AM EST

BY Doug Kass · Feb 26, 2025, 6:35 AM EST

* Listen up, Dan Ives...

"Nvidia's management cannot really say anything all that new or conclusive that would push investors head first back into AI semis and hardware related longs that to me just want to go lower on a unwind of all the retail and momentum froth... We are still early days in this DE-RISK, MOMO UNWIND. Not saying the ‘AI keg party’ is officially over. But it sure is coughing up a lot of foam and beer [is] getting warm. Many names just got over-bought."

- Mizuho Analyst Jordan Klein

BY Doug Kass · Feb 26, 2025, 6:25 AM EST

The S&P Short Range Oscillator remains modestly oversold at -1.16% vs. -0.82%.

BY Doug Kass · Feb 26, 2025, 6:08 AM EST

Wolf Street howls about the FDIC.

BY Doug Kass · Feb 26, 2025, 5:59 AM EST