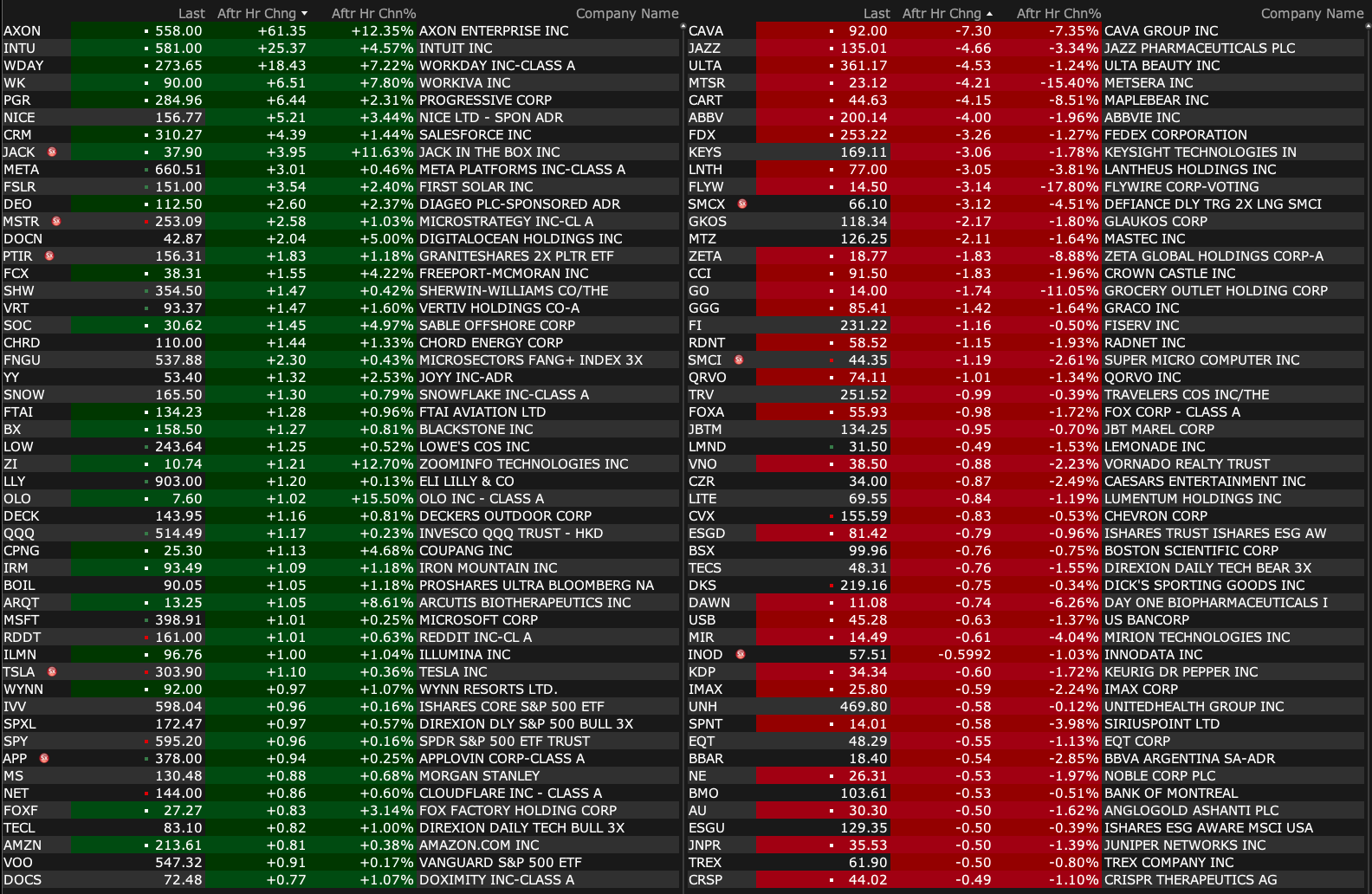

Tuesday's After-Hours Movers

At 4:28 p.m.:

BY Doug Kass · Feb 25, 2025, 4:45 PM EST

At 4:28 p.m.:

BY Doug Kass · Feb 25, 2025, 4:45 PM EST

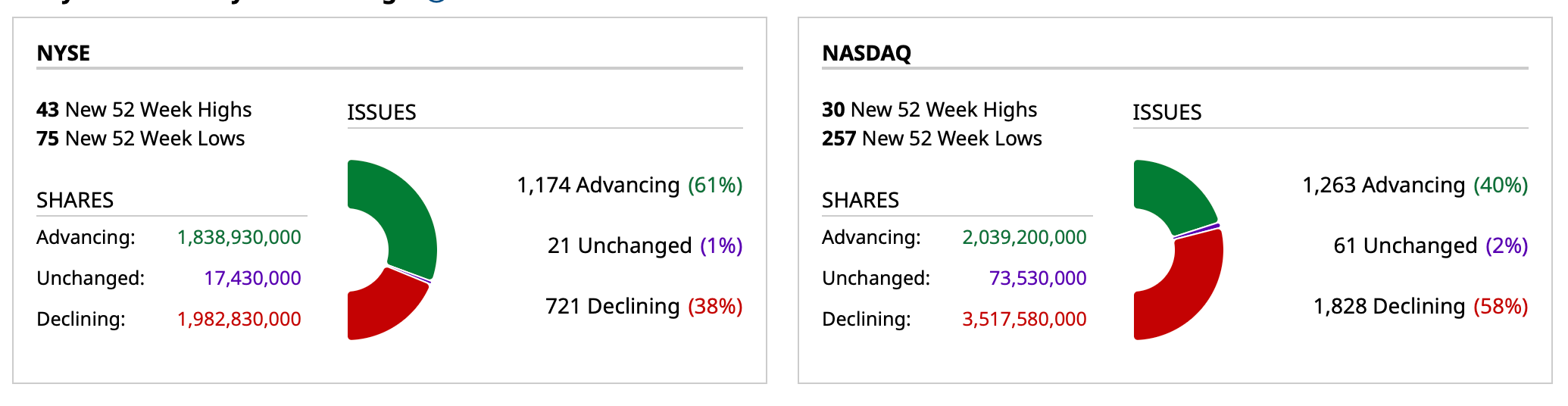

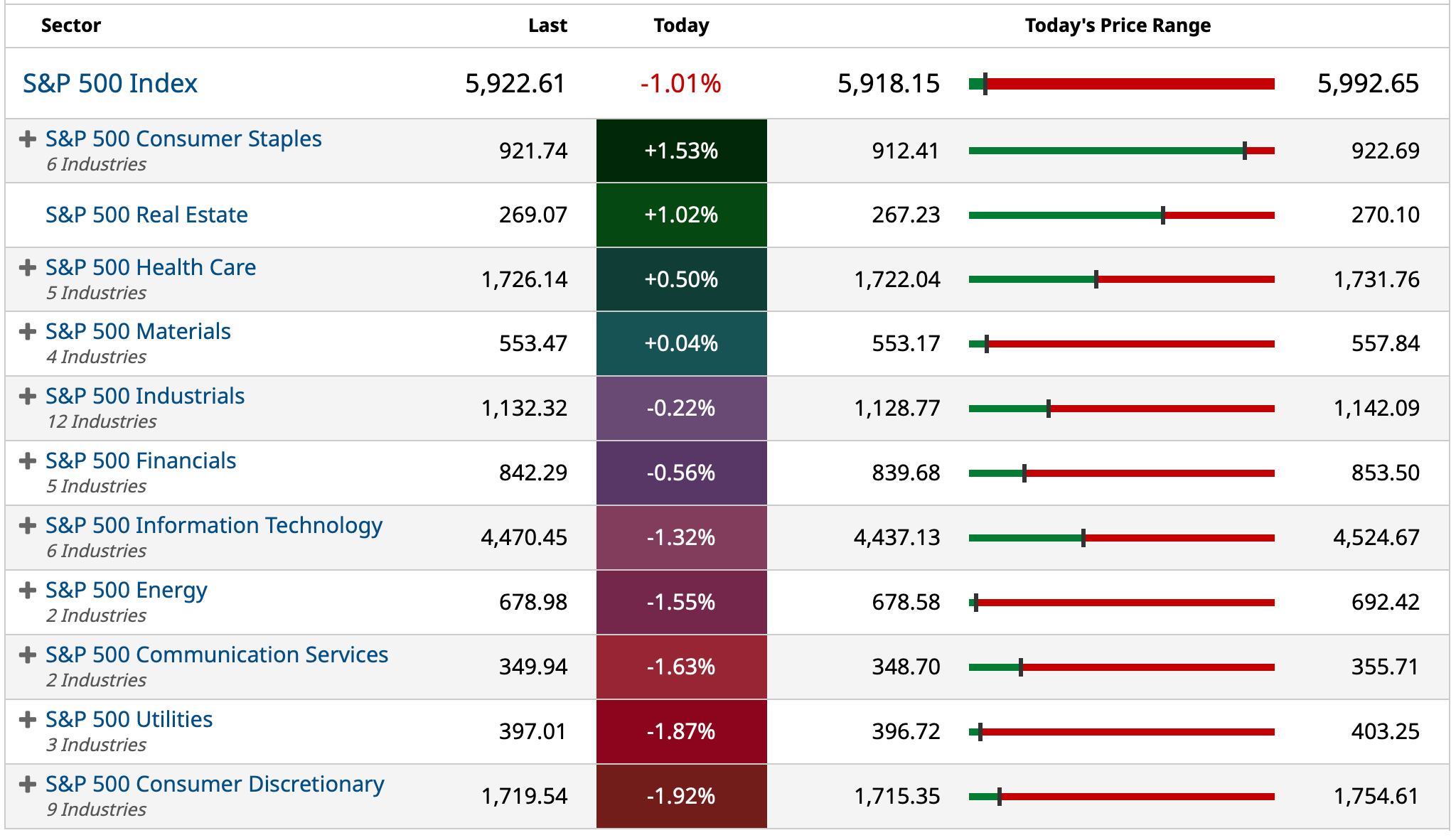

- NYSE volume 15% above its one-month average

- NASDAQ volume 1% above its one-month average

- VIX Up 2.37% to 19.43

BY Doug Kass · Feb 25, 2025, 4:35 PM EST

BY Doug Kass · Feb 25, 2025, 3:35 PM EST

Another volatile day.

Again, great for opportunistic traders... not so much for the buy-and-hold crowd.

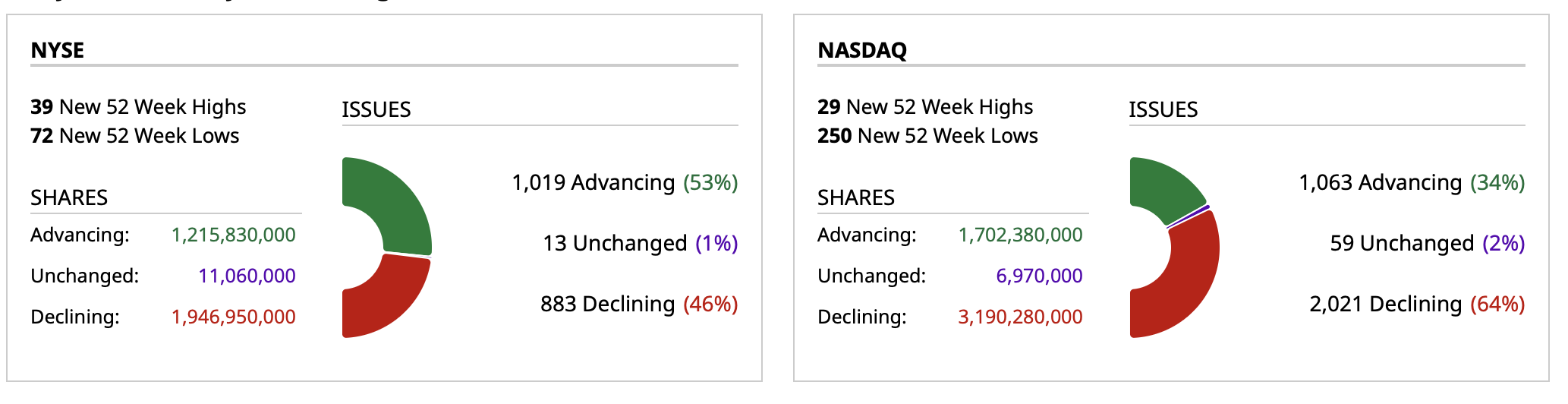

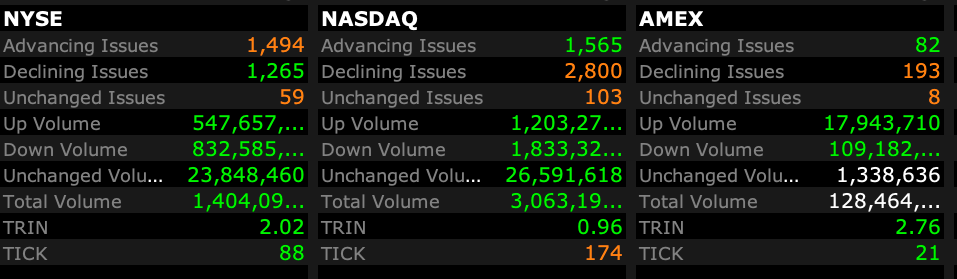

Breadth on the NYSE is slightly positive, but 2-1 negative on the Nasdaq:

At 3:15 PM the S&P Index is down by -21 handles.

Here are the things I did today:

* Back and forth in the Indices (common and calls traded), all nicely profitable. (I go out delta neutral on my Index positions).

* I continue to add to cannabis — MSOS $3.21, GTBIF $6.85, AYRWF $0.38, TCNNF $4.20 and TSNDF $0.56.

* Day traded a slug of Amazon AMZN — bought at $206.68 and sold at $211.41.

* Covered a portion of investment short INTU (-$12 on day) at $555.11.

* Shorted more PEP $157.56 and KO $71.50.

BY Doug Kass · Feb 25, 2025, 3:27 PM EST

* The Zen of Caddyshack.

* We remain short MSTR.

"Let me tell you a little story. I once knew a guy could have been a great golfer, could have gone pro. he just needed a little time to practice. Instead he decided to go to college instead. At the end of his fourth year in his last semester he got kicked out of college. You know for what for? Night putting with the fifteen year old daughter of the Dean. You know who that guy was Danny? That guy was Mitch Cumsteen, my roommate. Good guy. Don't be obsessed with your desires, Danny."

- Ty Webb, Caddyshack Caddyshack (1980) Thank You Very Little

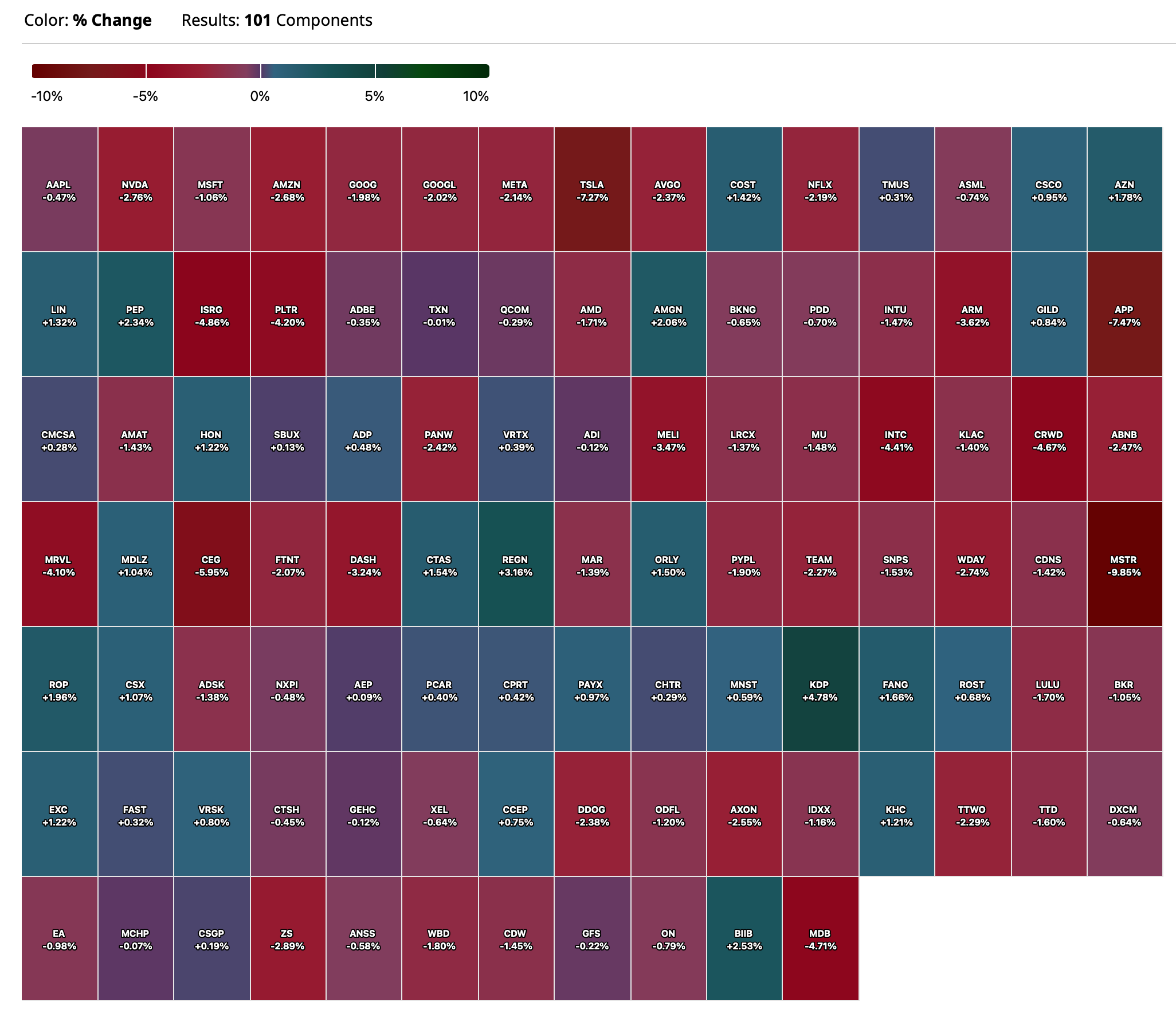

Remember the incessant interviews, adulation and softballs thrown at MicroStrategy MSTR Chairman Michael Saylor on Fin TV over the last two months?

Now look at the shares of MSTR — down another $33/share to $249 (and down from $540 in November).

"The Zen philosopher, Basho, once wrote, 'A flute with no holes, is not a flute. A donut with no hole, is a Danish.'"

Thank you very little Fin TV. Bitcoin on the move as Michael Saylor speaks in Miami

BY Doug Kass · Feb 25, 2025, 3:00 PM EST

This one I didn't expect.

I paid, on average today, $206.68 for a slug of Amazon AMZN.

I am selling (just what I bought today) at $211.41. (The shares traded as low as $204.16 this morning!)

BY Doug Kass · Feb 25, 2025, 2:54 PM EST

Two cannabis podcasts from my pal Shadd Dales.

and...

I add to MSOS daily.

And, more importantly, best of luck in the delivery and birth of Shadd's sidekick Anthony Varrell today!

BY Doug Kass · Feb 25, 2025, 2:31 PM EST

BY Doug Kass · Feb 25, 2025, 2:15 PM EST

I'm back shorting PepsiCo PEP at $157.56.

BY Doug Kass · Feb 25, 2025, 1:26 PM EST

Sold SPY at $594.46 and QQQ at $514.85 purchased earlier.

From this morning:

With S&P cash -64 handles I am taking a small long rental in the Indices:

* (SPY) $590.74

* (QQQ) $510.73

Position: Long SPY common (M), QQQ common (M); Short SPY calls (M) QQQ calls (M)

By Doug Kass Feb 25, 2025 10:49 AM EST

BY Doug Kass · Feb 25, 2025, 12:51 PM EST

As of 12:20 p.m.:

BY Doug Kass · Feb 25, 2025, 12:40 PM EST

From Peter Boockvar:

Home prices up 52% over past 5 years/Eggs and tariffs matter/Cloudy mfr'g outlook

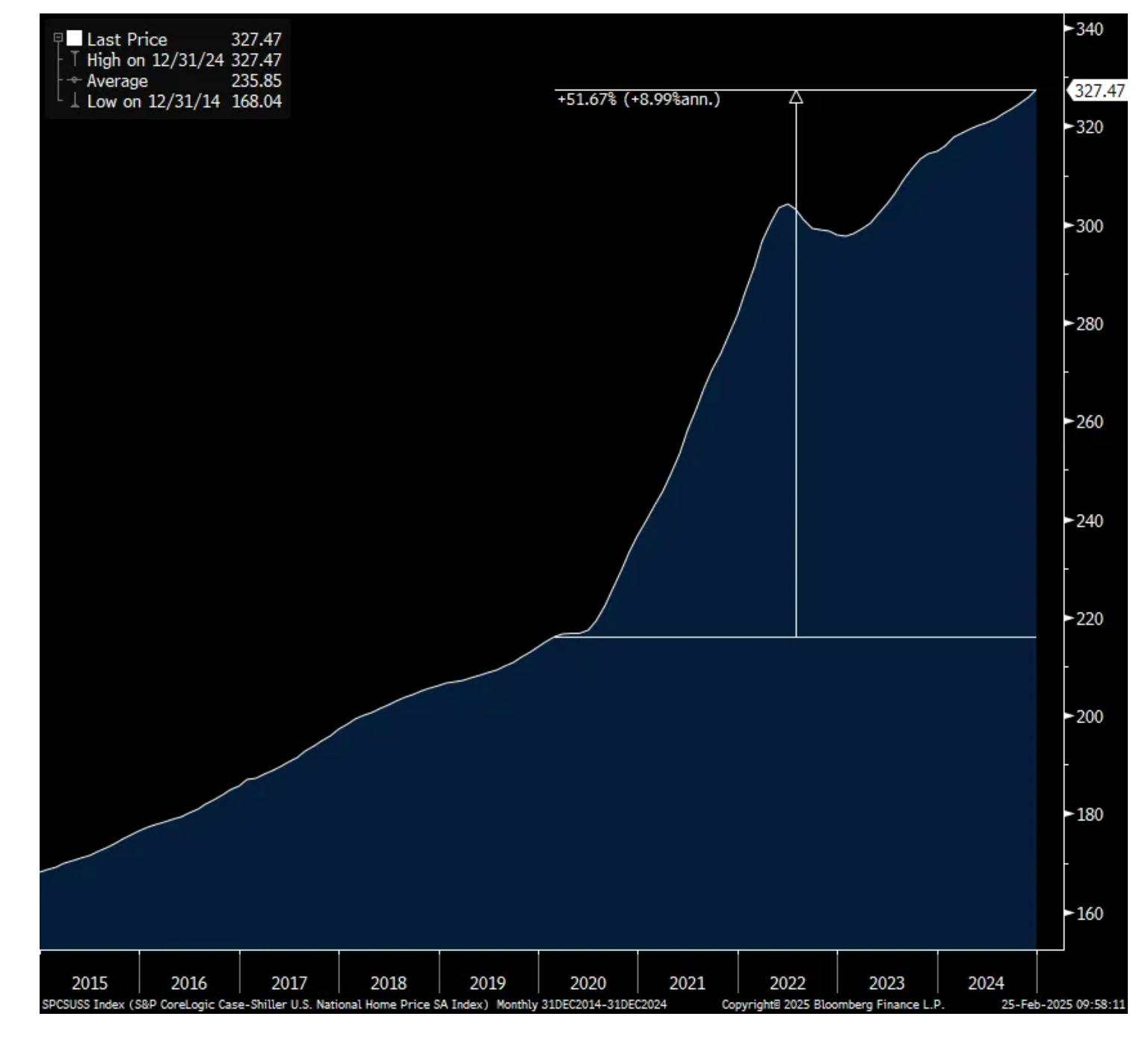

In December, the S&P CoreLogic home price index saw a 3.9% y/o/y increase and continues to be a major affordability problem for the first time buyer who is not playing with ‘house’ money. For perspective, since February 2020 when the Fed was on the cusp of going hog wild with monetary easing, including massive purchases of MBS, this index is up 52%.

If this was included in CPI instead of owners’ equivalent rent which was up ‘only’ 27%, we would have seen double digit inflation in 2022.

Home Price Index

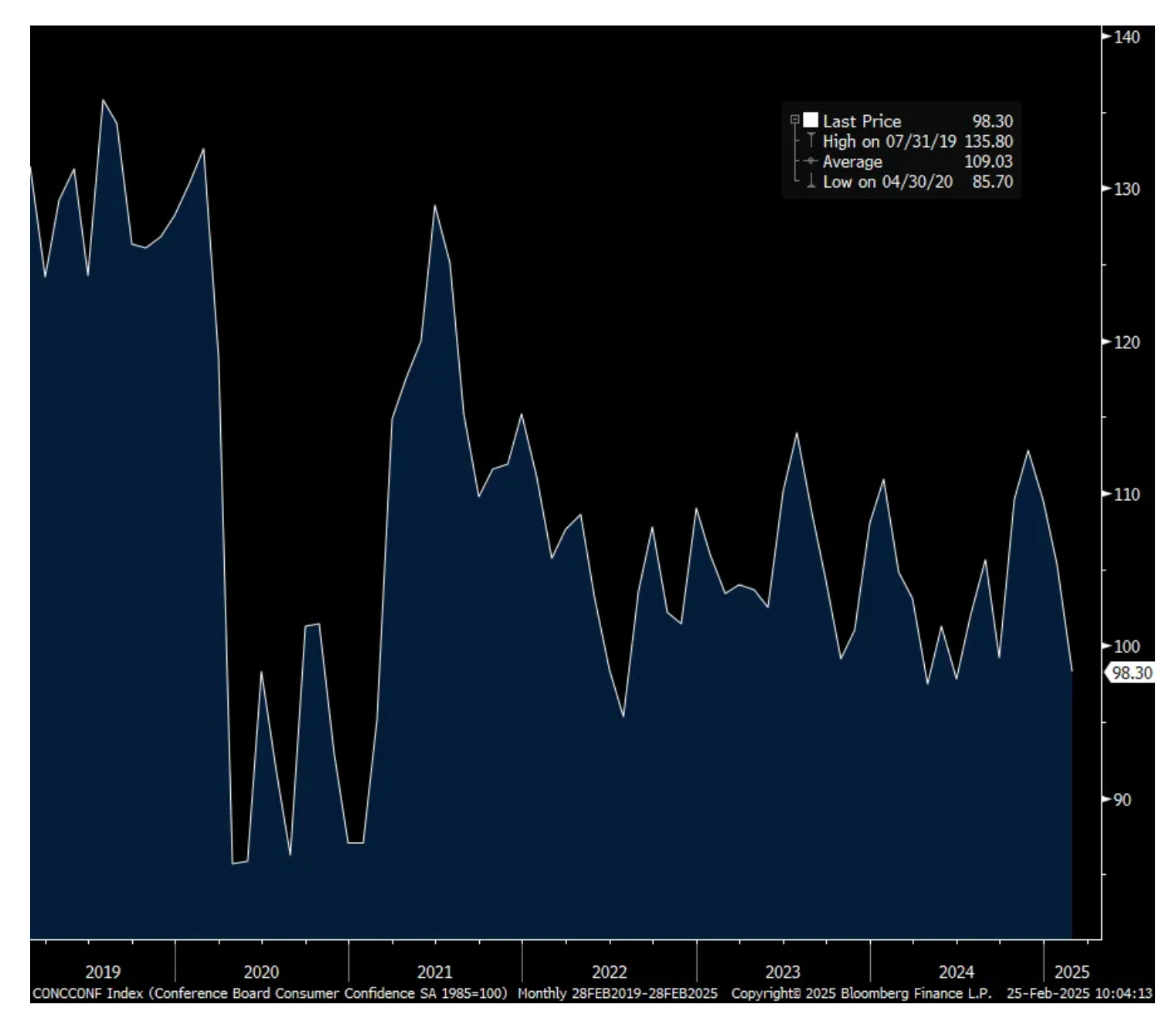

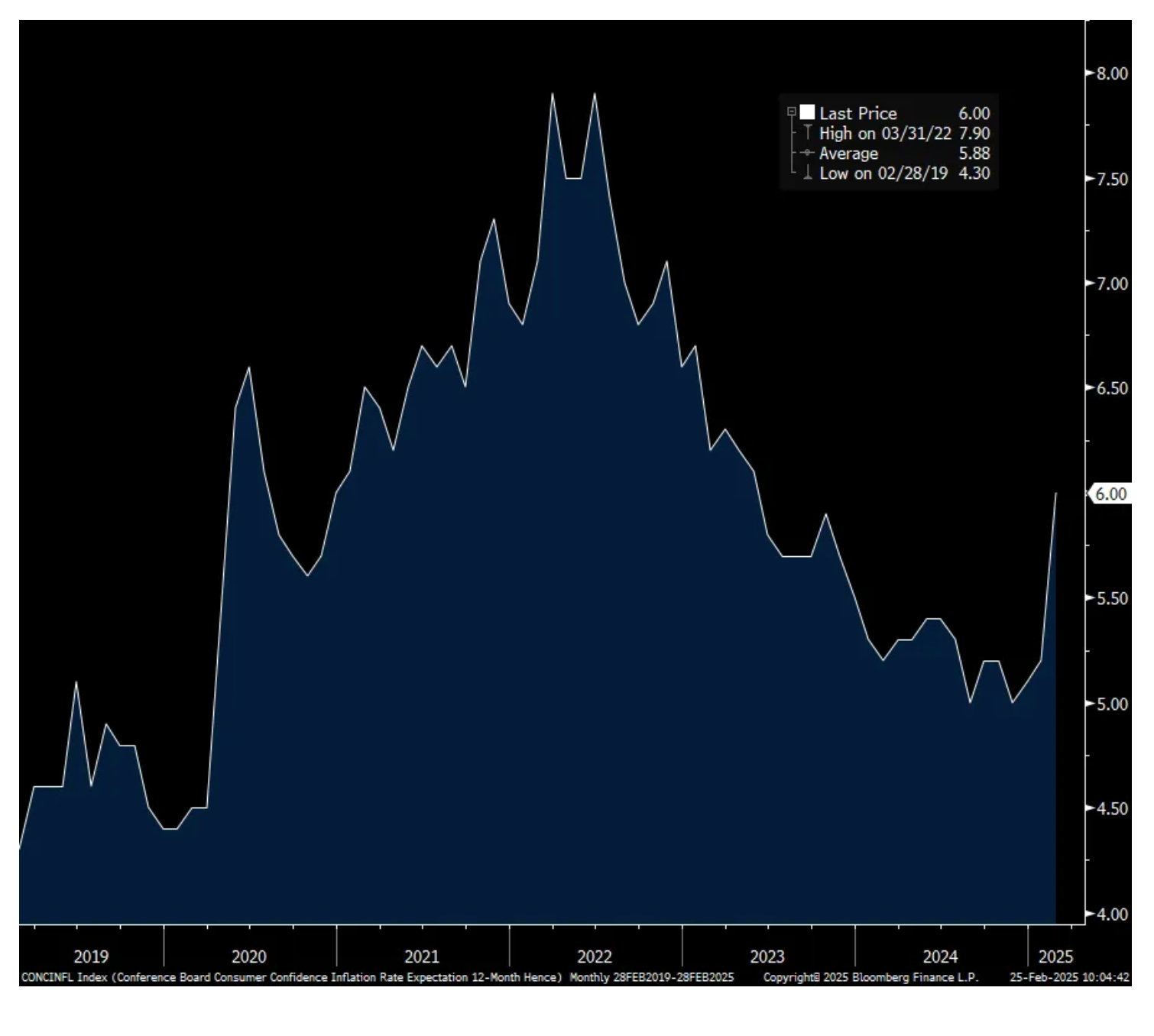

On the heels of the politically slanted UoM consumer confidence index, the February consumer confidence index from the Conference Board fell to 98.3 from 105.3. Almost all of the decline was in the Expectations component which fell almost 10 pts m/o/m while the Present Situation was lower by 3.4 pts. As seen in the UoM, there was a jump in one yr inflation expectations, to 6% from 5.2% and that is the highest since May 2023.

With that inflation expectations pop, the Conference Board said “This increase likely reflected a mix of factors, including sticky inflation but also the recent jump in prices of key household staples like eggs and the expected impact of tariffs. References to inflation and prices in general continue to rank high in write-in responses, but the focus shifted towards other topics. There was a sharp increase in the mentions of trade and tariffs, back to a level unseen since 2019.”

The answers to the labor market questions slipped with those Plentiful falling .5 pt to a 5 month low. Hard To Get was up by 1.8 pts to a 4 month high. Those that expect ‘more jobs’ in the coming six months fell .7 pts to 18.4, matching the lowest since September. Income expectations were little changed.

Spending intentions were mixed with a drop in vehicles but a rise in home buying (up by .6 pts after falling by .7 pts last month). They were mixed to little changed for major household items.

In terms of age, confidence fell across the board and for income, most notably for those making more than $125k and between $25-35k.

Bottom line, I don’t have a political breakdown for you here but assume there are similarities to the UoM survey. That said, while tariffs may be a one time price reset, we have a US consumer base that has PTSD over inflation, particularly lower to middle income consumers that don’t want ANY further price increases from here.

Consumer Confidence

One yr Inflation Expectations

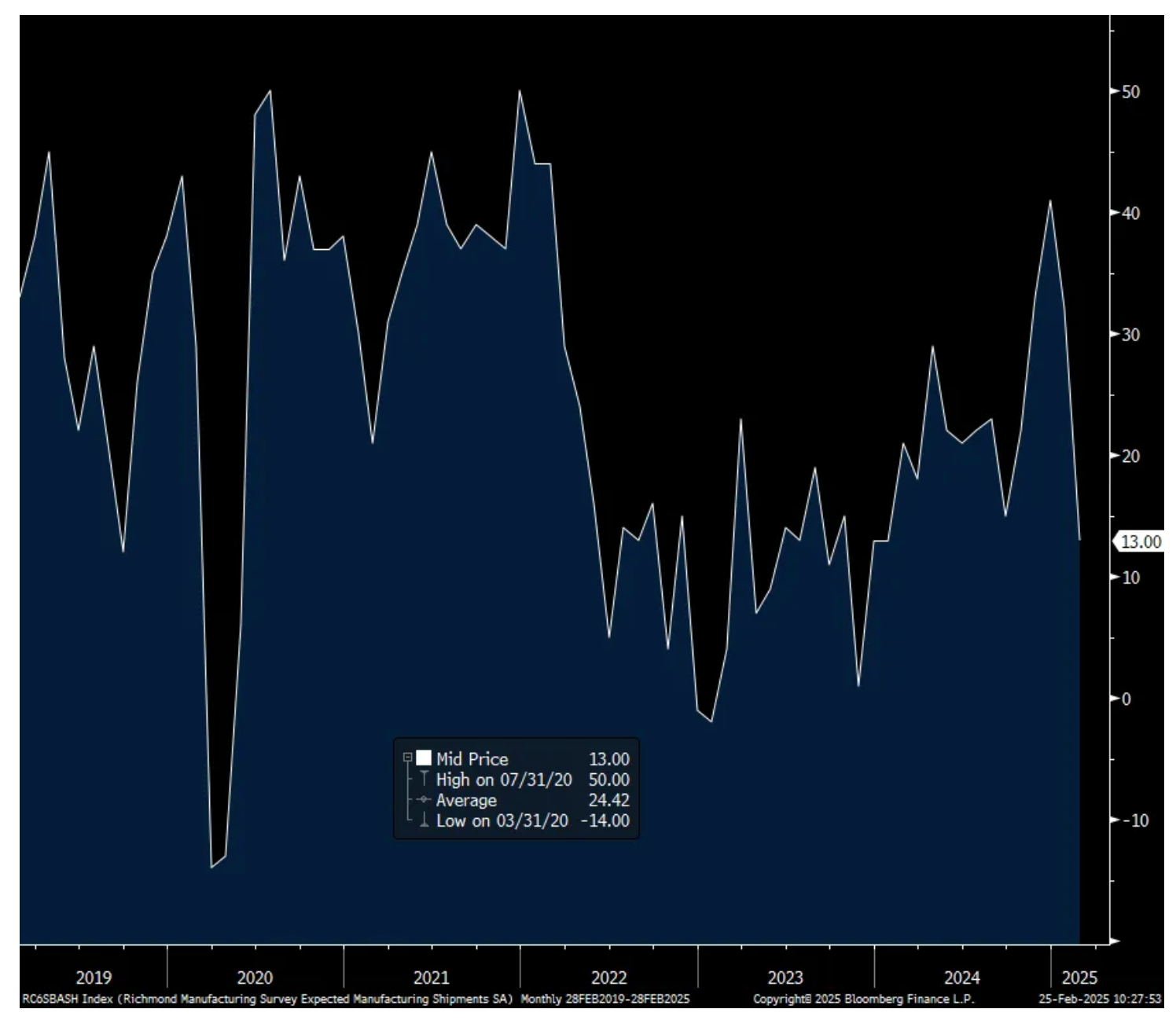

Finally today, after two positive reads from the NY and Philly manufacturing indexes and the negative Dallas figure, the just reported Richmond index rose to +6 from -4. The Richmond region is now in focus because of DOGE and whatever spending cuts impact the DC metro area along with the tariff issue that all manufacturers are dealing with.

While the headline number was better, economic worries clearly showed up in the 6 month outlook figures. Shipments fell to 13 from 32, new orders dropped to 8 from 31, backlogs fell to 3 from 17, employment plunged to 1 from 12 and expectations for both prices paid and received were higher with the former at the highest level since November 2022.

Bottom line, the common theme in all the regional manufacturing numbers seen so far is obvious, most are worried about the impact of tariffs with the Richmond region also focused on the DOGE influence with government a key customer, particularly in defense in the Richmond area.

6 month Shipments outlook

BY Doug Kass · Feb 25, 2025, 12:30 PM EST

BY Doug Kass · Feb 25, 2025, 12:10 PM EST

I'm buying more Amazon AMZN at $205.77 and JOE at $45.74.

BY Doug Kass · Feb 25, 2025, 11:51 AM EST

BY Doug Kass · Feb 25, 2025, 11:45 AM EST

Investment short Intuit INTU is -$12 and hit a 52-year low this mornning.

Covering some at $555.11.

BY Doug Kass · Feb 25, 2025, 11:40 AM EST

* Hmmmm....

Fear and Greed Index - Investor Sentiment | CNN

And as the S&P Short Range Oscillator flashes an emerging oversold:

The S&P Short Range Oscillator stays in modest oversold ground — at -0.82% vs. -1.42%.

Position: Long SPY common (M), QQQ common (M); Short SPY calls (M), QQQ calls (M)

By Doug Kass Feb 25, 2025 6:50 AM EST

BY Doug Kass · Feb 25, 2025, 11:31 AM EST

BY Doug Kass · Feb 25, 2025, 11:28 AM EST

From Peter Boockvar:

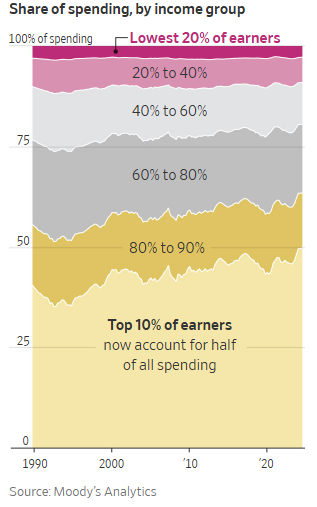

"The US economy Depends More Than Ever on Rich People"

I've mentioned here many times my belief that the strength in the US economy has rested on three pillars, with lackluster growth most everywhere else. One, upper income spending, two, anything related to AI spend including data center construction, and three, anything related to local, state and federal government spending, whether that is related to infrastructure, the Chips Act, the IRA, Medicare, Medicaid and transfer payments. We're obviously on watch with the third factor in light of the scrutiny of government spending but the WSJ yesterday had a great chart in case you didn't see it on how influential upper income spending is on total consumer spending.

The article was titled "The US Economy Depends More Than Ever on Rich People." It said "The top 10% of earners - households making about $250,000 a year or more - are splurging on everything from vacations to designer handbags, buoyed by big gains in stocks, real estate and other assets. Those consumers now account for 49.7% of all spending, a record in data going back to 1989, according to an analysis by Moody's Analytics. Three decades ago, they accounted for about 36%."

What this means is that the direction of the stock market and other asset prices will be the swing factor on maintaining this level of spend. And you can be sure, this income cohort (along with investors around the world) is most likely heavily invested in the Mag 7, appropriately so for many years but something I believe as stated here over the past few weeks, something that should be reassessed as to the extent of that exposure in terms of looking for future returns from here.

https://www.wsj.com/economy/consumers/us-economy-strength-rich-spending-2c34a571

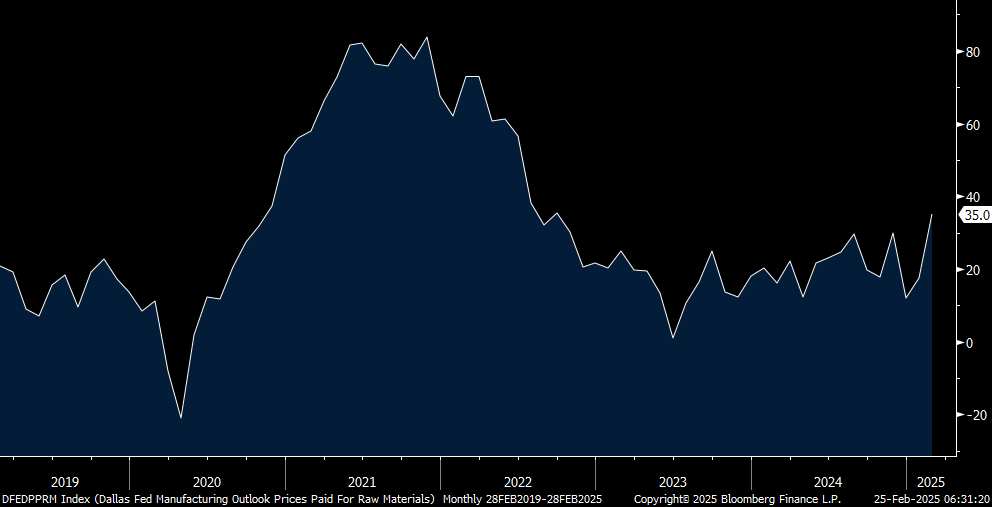

Following the above zero prints in both the NY and Philly manufacturing indexes seen last week, the February Dallas regional survey fell back below zero at -8.3 from +14.1 in January and under the estimate of +6.4. Seen though in those two surveys was a similar jump in the Dallas figure in prices paid which doubled from 17.5 to 35 and that is the highest since September 2022. Also seen in the NY and Philly surveys was the drop in the 6 month business outlook. The same can be said for the Dallas one as it dropped to just 7.7 from 35.5 and well below the 6 month average of 22.8. Capital spending plans slipped as well.

The comments from companies in a variety of industries were littered with concerns over tariffs and likely explains the drop in business optimism. The most telling comment was this, "With some of the new Buy America changes and tariffs incoming, we are looking at closing the business." That was from a company in the computer/electronics industry.

Chemical manufacturing

The dynamic tariff situation is one for us to follow and seek to understand. The approach to improve export tariffs for U.S. companies seeking to deliver goods in foreign countries is good, and we believe the current tactic of reciprocal tariffs could drive improvement for U.S. export competitiveness.

Tariff threats and uncertainty are extremely disruptive.

Computer and electronic product manufacturing

Keep lowering interest rates, please.

The overall effects of administrative change have stalled consumer and customer spending.

We are uncertain as to the full impact of tariffs related to our business. We procure parts from overseas. We have lost business opportunities for production of goods that goes to other countries as a result of tariffs. We may see new opportunities for products built elsewhere for companies who wish to shift manufacturing to the U.S. to avoid tariffs. There is much uncertainty at the moment as to how this will shake out.

With some of the new Buy America changes and tariffs incoming, we are looking at closing the business.

We are seeing broad signals of demand cyclically recovering. Personal electronics, communications equipment and enterprise business are now several quarters into a cyclical recovery. We are seeing industrial and automotive inventories cleaned out, and our revenues are returning to consumption.

Fabricated metal product manufacturing

We are starting to see old requests for quotations starting to receive purchase orders. We are still having issues filling positions.

We are still in a low-volume period but are holding steady as we’ve flexed down capacity and costs accordingly.

Food manufacturing

President Trump’s freeze on government contracts has had a dramatic impact on us. USAID [United States Agency for International Development] is our major customer. That aside, it needed to happen.

The current political environment under President Trump has increased the uncertainty of the consumer market. As a food manufacturer, we have noticed small customers are struggling (unable to pay bills on time), and the larger national customers have reduced their purchases. Imposing tariffs on our major trading partners will lead to higher consumer prices. The items we import are preparing to raise prices. I have more uncertainty about the future business/consumer environment than ever before in my 40 years of operating businesses.

The back-and-forth tariff talk has been very stressful, but it has not been disruptive so far.

Immigration laws and raids [are affecting our business].

Machinery manufacturing

We are experiencing up-and-down waves. Hopefully, it will pick back up now that the election is over.

The phone is ringing. There's some trepidation about inflation and tariff impact, but we have confidence that orders are about to come. More importantly, our industry feels better in general about where our country is going as a whole. The direction provides hope for the long term, even if the cash register is not rattling quite yet.

Last month was our best month in over a year. We are seeing much more business activity and expect this trend to continue. We are finally seeing a bright future for our business.

Miscellaneous manufacturing

Sales volumes have been trending downward in the last 28 months. We have cut hours to 36 per week, and it is not enough to get profitable. Next week, we are cutting further to 32 hours and laying off three people. The uncertainty in tariff threats and general chaos of another Trump presidency is weighing heavy on our business. All customers are decreasing or pushing out orders—taking a wait-and-see posture. Automotive OEM [original equipment manufacturer] and aftermarket represents 72 percent of our sales. The outlook from automotive OEM is that production should begin to pick up in second quarter 2025, but no firm increases have been promised. The outlook is bleak.

Nonmetallic mineral product manufacturing

It is very hard to plan. Interest rates? Tariffs? Wow.

Paper manufacturing

Currently it is very slow, and we started reduced production hours in the plant. Orders are also very slow. A price increase in the industry has been delayed 30 days due to softness.

Plastics and rubber products manufacturing

Customers, vendors and ourselves are all trying to get ahead of anticipated global trade challenges. It is stressing capacities, especially with production personnel.

Primary metal manufacturing

The proposed 25 percent tariffs on steel imports will directly and favorably improve the bottom line as a domestic steel manufacturer. However, uncertainty is sky high.

It is A Tale of Two Cities. February was down compared with January, but our outlook remains positive due to the 25 percent Section 232 tariff on aluminum. This tariff is expected to slow the influx of foreign aluminum from Mexico and other countries. Currently, a significant amount of aluminum is being dumped into the U.S. market, with many countries subsidizing their exports to gain a competitive edge. The bottom line: If the tariffs remain in place, they will benefit our industry. However, if they are reversed, many companies in our sector will struggle to survive.

Production improvements are directly related to capital expenditures in 2024 and continuing in 2025. Raw materials are expected to increase due to impending tariffs.

Printing and related support activities

It's so weird how we are slow as molasses right now, yet a year ago, we were very busy at this time. I'm very worried about the possible tariffs affecting some of our material costs, which we will have no choice but to pass along to our customers. This is a terrible policy decision and hopefully will not be very long lived.

Textile product mills

No major change from January. We made the decision a few months ago to purchase more inventory than usual, and the negative cash impact of making this larger purchase was worth minimizing uncertainty about future pricing and impacts of tariffs. (We import from overseas.)

Transportation equipment manufacturing

The new tariffs will have a big impact on the demand for our products. This applies primarily to the 25 percent on goods from Mexico. The impact of the additional 25 percent for steel and aluminum will also be detrimental to demand, the extent of which is still being evaluated.

The Trump tariff situation is creating uncertainty about our future material costs later this year.

I was expecting a pickup in business activity in third quarter 2025 and now think it will be first quarter 2026.

Prices Paid in Dallas Mfr'g index

From Home Depot who beat estimates, including with US comps but slightly lowered its fiscal year comp guidance and said eps growth should be negative y/o/y:

"Our fourth quarter results exceeded our expectations as we saw greater engagement in home improvement spend, despite ongoing pressure on large remodeling projects." We await the earnings call for more color.

From the Domino's Pizza earnings call:

"As we look ahead to 2025, we believe the combination of pressured consumer spending and a value driven QSR marketplace will continue."

"The delivery comp was impacted by continued macro and competitive pressures that put pressure on our low-income consumers...Traffic was flat for the quarter, which was partially driven by a slight headwind as a result of New Year's Eve timing."

From Cleveland Cliffs:

"Our results in 2024 were a consequence of the worst steel demand environment since 2010 (ex Covid). Cleveland Cliffs is an American steel company, designed to supply high-end manufacturers producing things in the US. That said, for the first time, the number of cars sold in the US that were produced abroad and imported into the US surpassed the number of cars sold that were produced domestically. With this decline in domestic automotive production, and too much imported steel from abroad that drove unsustainably low steel prices, Cliffs was deeply impacted. As a steel producer equipped to supply high-end steel - like automotive exposed parts, among others - we by design carry a higher fixed cost structure, and we are more impacted than others when markets are weak."

And why CEO Lourenco Goncalves wants tariffs on imports. "Since January 20th, President Trump has made clear that proper enforcement of our trade laws and a supportive industrial policy prioritizing manufacturing in the US are both being implemented."

The Bank of Korea cut its base rate by 25 bps to 2.75% as expected. And the Governor blessed the current market expectations of two to three more cuts this year as their economic expectations is for just 1.5% growth this year. A reason for that was tariff worries. "The outline of Trump's tariff policies has now largely taken shape, and that prompted the downgrade from January."

BY Doug Kass · Feb 25, 2025, 11:11 AM EST

I am adding to my Coca-Cola KO short at $71.50.

Buying more Amazon AMZN at $206.85.

BY Doug Kass · Feb 25, 2025, 10:55 AM EST

With S&P cash -64 handles I am taking a small long rental in the Indices:

* SPY $590.74

* QQQ $510.73

BY Doug Kass · Feb 25, 2025, 10:49 AM EST

My Amazon AMZN position moves to medium sized with a purchase at $207.78.

BY Doug Kass · Feb 25, 2025, 10:31 AM EST

With S&P cash -45 handles I am now at a neutral delta-adjusted position in the Indices.

I accomplished this by adding to SPY at $592.80 and QQQ at $513.55.

From yesterday:

With S&P cash +14 handles I am moving off my delta-adjusted Index neutral position by selling out some of my (SPY) $601.22 and (QQQ) $525.32 longs.

From earlier:

With S&P cash only +9 handles (and down from +36 handles earlier) I have moved to a delta adjusted neutral position in the indexes.

Position: Long SPY common M QQQ common M; Short SPY calls M QQQ calls M

By Doug Kass Feb 24, 2025 9:49 AM EST

Position: Long SPY common (S/M), QQQ common (S/M); Short SPY calls (M), QQQ calls (M)

By Doug Kass Feb 24, 2025 12:31 PM EST

BY Doug Kass · Feb 25, 2025, 10:27 AM EST

Some of my names from the sell-side:

Chegg CHGG price target lowered to $1 from $1.25 at Morgan Stanley Morgan Stanley analyst Josh Baer lowered the firm's price target on Chegg to $1 from $1.25 and keeps an Underweight rating on the shares. Q1 guidance "meaningfully missed consensus," which is likely to cause material negative consensus estimate revisions in 2025 and beyond, the analyst tells investors. The firm lowered its "Street low" estimates, driving its decreased price target, the analyst noted following earnings.

Freshpet FRPT price target lowered to $140 from $170 at Truist Truist lowered the firm's price target on Freshpet to $140 from $170 but keeps a Buy rating on the shares after its Q4 earnings miss and Q&A with its management. The company has seen a slowdown in pet food category over the past few months which factored into its decision to not raise the 2027 goal, though its forecast will prove conservative, the analyst tells investors in a research note. Truist adds however that Freshpet has managed the business to avoid supply chain constraints by moderating A&P spend over the past few years, and the firm does not see meaningful sales outperformance in 2025 for the same reason.

Elanco ELAN reports Q4 adjusted EPS 14c, consensus 15c Reports Q4 revenue $1.02B, consensus $1.01B. "Elanco delivered a strong finish to 2024, achieving our sixth consecutive quarter of organic constant currency revenue growth - with Q4 up 4% - and building momentum as we head into 2025," said CEO Jeff Simmons. "For the year we grew in both Pet Health and Farm Animal, in our top five product franchises, and in nine of our top 10 countries, all on an organic constant currency basis, demonstrating the broad-based strength of our diverse portfolio. We exceeded our innovation revenue target for 2024 and raised the goal for 2025, with six potential blockbuster products now launched and reinforcing our confidence in mid-single digit organic constant currency revenue growth this year. We generated over half a billion dollars of operating cash flow in 2024, doubling from the prior year through working capital discipline. Employee engagement is at a four-year high and our teams are already off to a fast start in 2025, focused on delivering a successful year and creating long-term value."

Elanco sees 2025 adjusted EPS 80c-86c, consensus 90c Sees 2025 revenue $4.45B-$4.51B, consensus $4.53B. "We are focused on accelerating organic constant currency revenue growth for 2025, with continued efforts to improve our earnings potential and leverage profile," said Todd Young, CFO. "As we navigate a dynamic macroeconomic backdrop, we remain confident in the underlying drivers of the 2025 outlook provided during the November earnings call. The only adjustment we have made is for incremental currency headwinds using rates from earlier this month. We expect 2025 adjusted EBITDA to be more back half weighted than our historical cadence, with the stronger dollar and as our strategic investments in global launches drive the expected ramp for innovation revenue contributions."

BY Doug Kass · Feb 25, 2025, 10:15 AM EST

"Any market will gain respectability if it goes up high enough and any market will lose respectability if it goes down enough."

- Arnold Van Den Berg

Bonus - here are some great links:

See A Little, See Alot See a little....see a lot.

Streaky Bespoke | My Research

Turn, Turn, Turn Almanac Trader — A Time For Market Patience Turn Turn Turn

Crypto Bulls Are Running out of Arguments Crypto Bulls Are Running Out of Arguments

Can Nvidia Save the Market? Can Nvidia Save The Market? - by Aaron

BY Doug Kass · Feb 25, 2025, 9:52 AM EST

I bought small JOE under $46.

BY Doug Kass · Feb 25, 2025, 9:49 AM EST

Sole trade today - added to MSOS at $3.25.

I have multiple research calls this morning.

BY Doug Kass · Feb 25, 2025, 9:40 AM EST

-DOCN +17% (earnings, guidance)

-PGEN +14% (US FDA grants Priority Review for PRGN-2012 BLA for treatment of Adults with Recurrent Respiratory Papillomatosis)

-SEE +13% (earnings, guidance)

-EPRX +11% (announces Positive Data from RESOLVE Phase 1b/2a Trial of EP-104GI for Treatment of Eosinophilic Esophagitis)

-ITRI +10% (earnings, guidance)

-ALLT +9.8% (earnings)

-XPRO +9.8% (earnings, guidance)

-YY +9.8% (Baidu acquires JOYY's Live Streaming Business in China for $2.1B)

-PTLO +7.6% (earnings, guidance)

-BEAM +4.5% (earnings)

-CADL +4.3% (Final Survival Data from Randomized Controlled Phase 2 Clinical Trial of CAN-2409 in Non-Metastatic Pancreatic Cancer showed notable improvement in estimated median overall survival of 31.4 months)

-BOOM +3.7% (earnings, guidance)

-AWI +2.9% (earnings, guidance)

-KDP +2.6% (earnings, guidance)

-PYPL +2.3% (earnings, guidance)

-FANG +2.2% (earnings, guidance)

-CHGG -24% (earnings, guidance)

-HIMS -22% (earnings, guidance)

-MPLN -14% (earnings, guidance)

-SRE -12% (earnings, guidance)

-DNUT -11% (earnings, guidance)

-UCTT -9.9% (earnings, guidance)

-TCOM -9.2% (earnings)

-CRI -7.8% (earnings, guidance)

-SHLS -6.5% (earnings, guidance)

-ZM -3.8% (earnings, guidance)

-NOVT -3.4% (earnings, guidance)

-O -2.9% (earnings, guidance)

-ELAN -2.8% (earnings, guidance; enters agreement with Medgene to Commercialize Highly Pathogenic Avian Influenza Vaccine in Dairy Cattle)

-MIDD -2.8% (earnings)

-XHR -2.5% (earnings, guidance)

-AS -2.1% (earnings, guidance)

BY Doug Kass · Feb 25, 2025, 9:13 AM EST

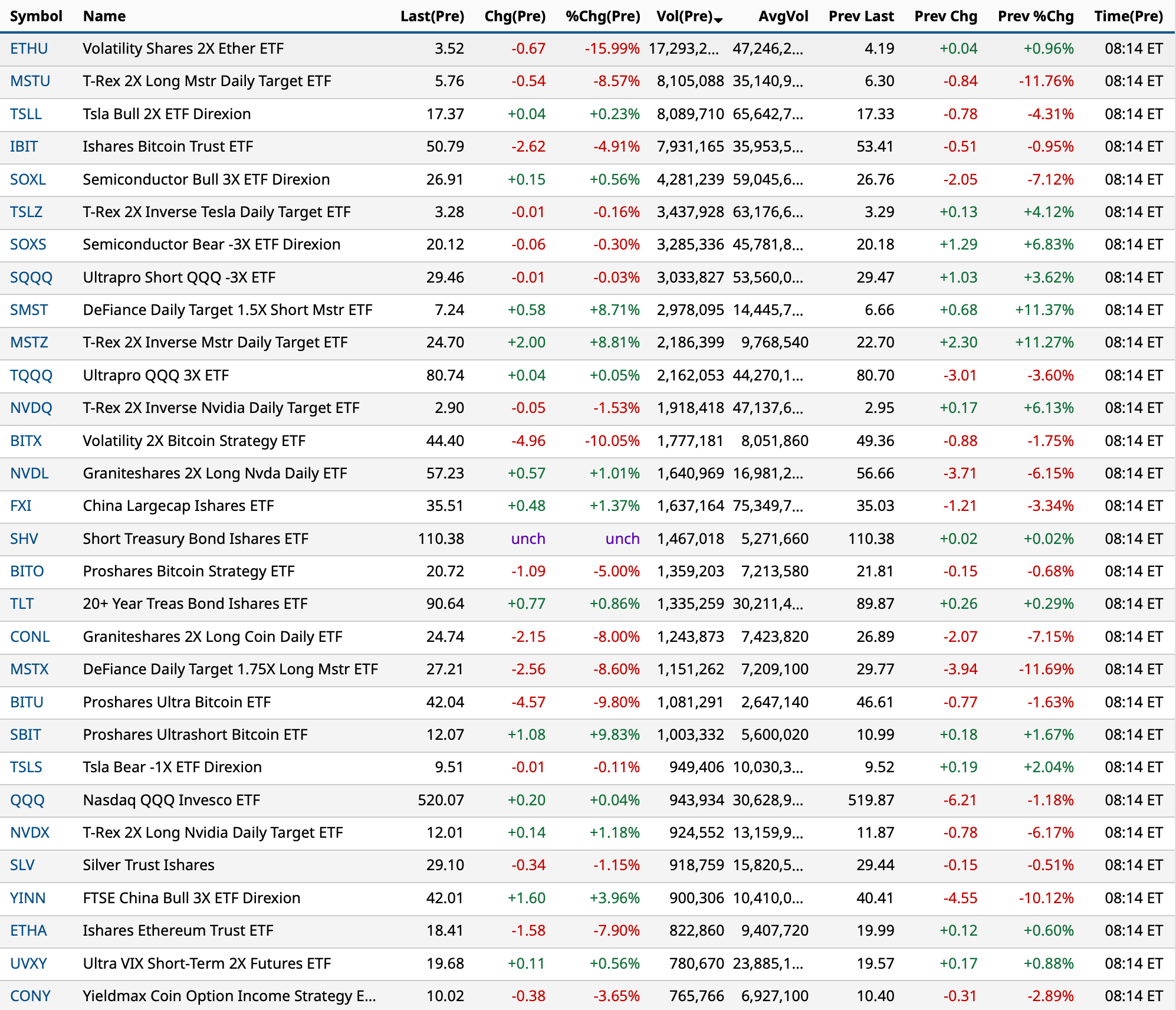

Most active premarket exchange-traded funds as of 8:14 a.m. ET:

BY Doug Kass · Feb 25, 2025, 9:07 AM EST

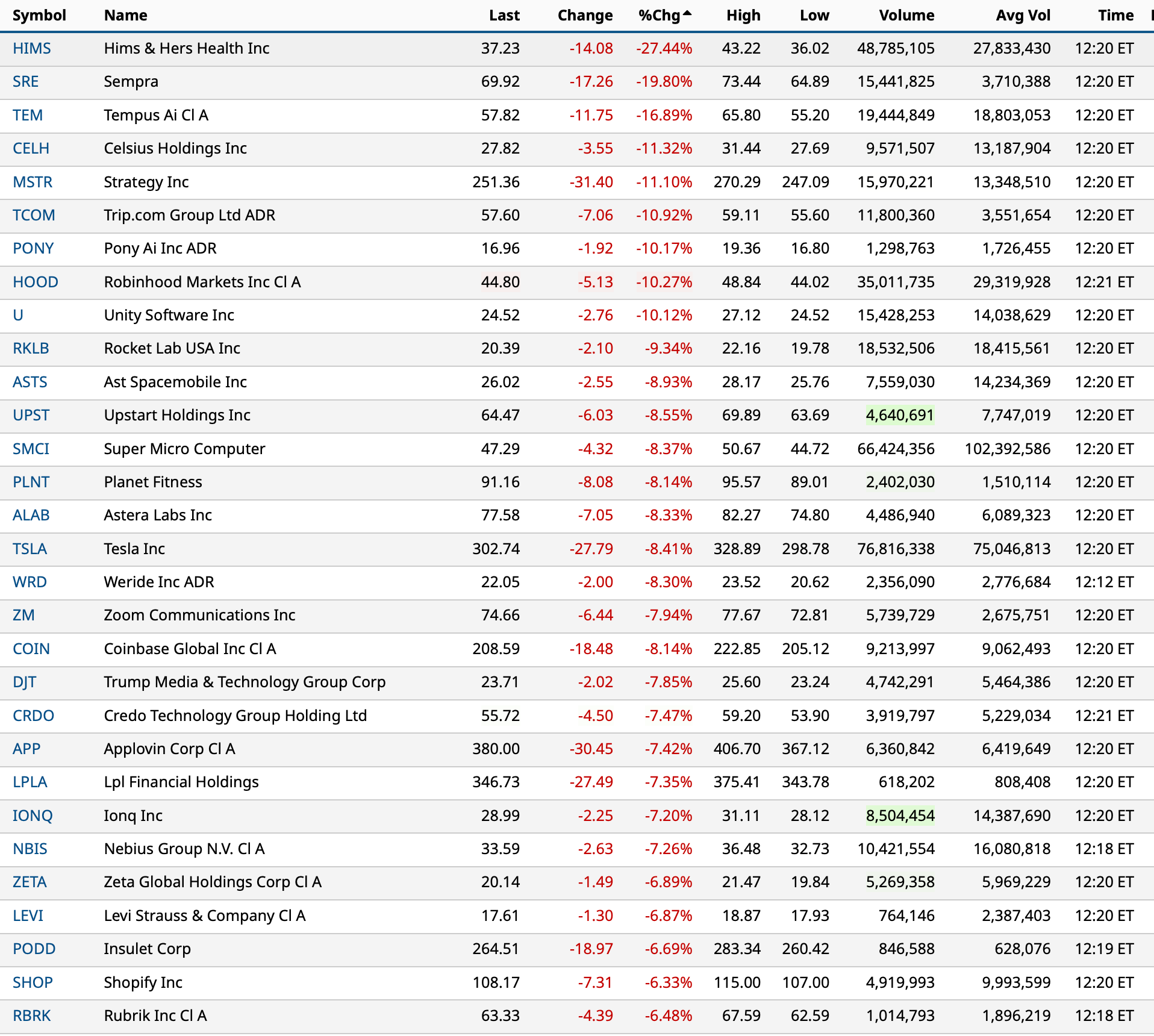

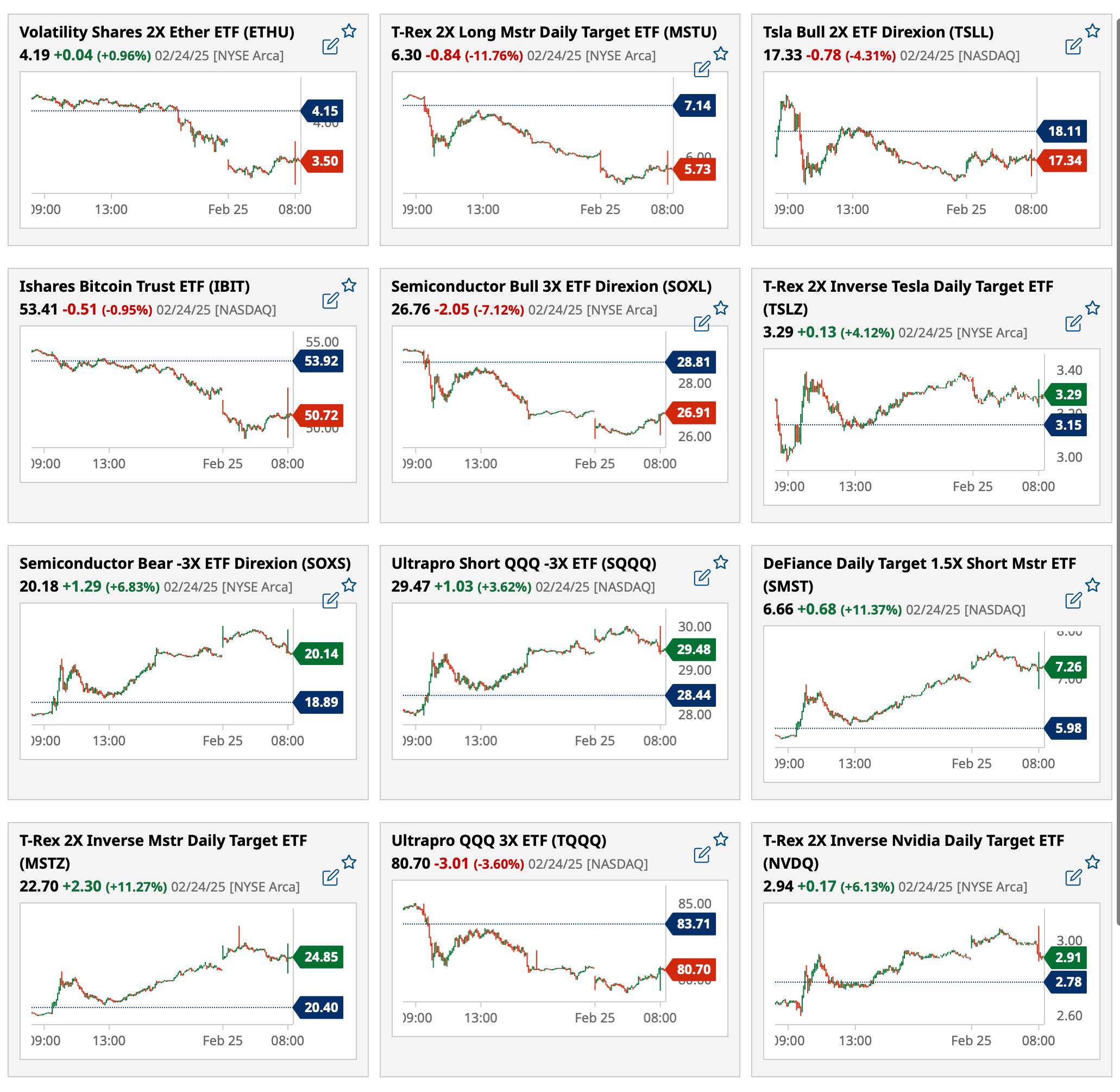

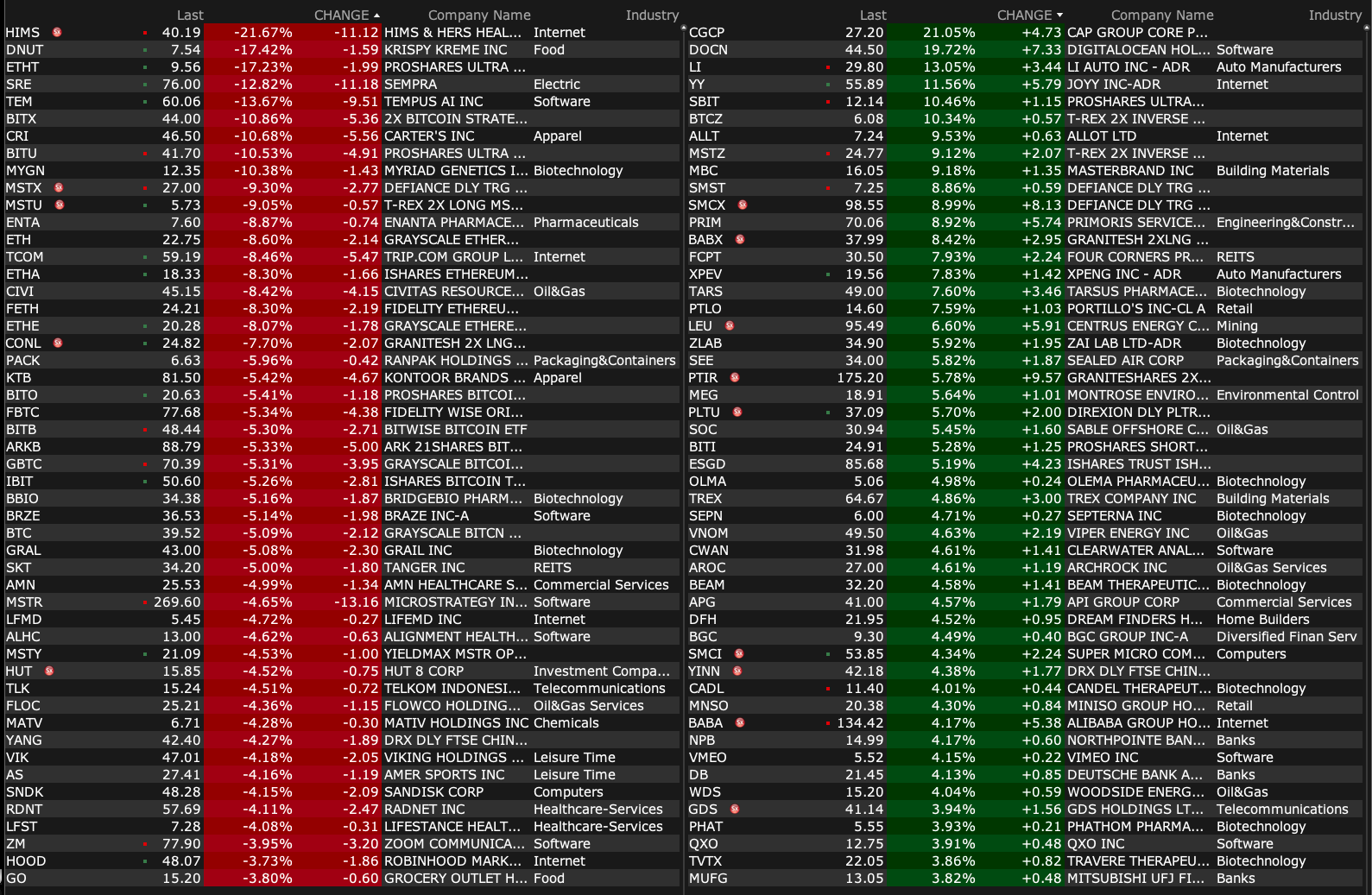

Premarket percentage movers at 8:33 a.m. ET:

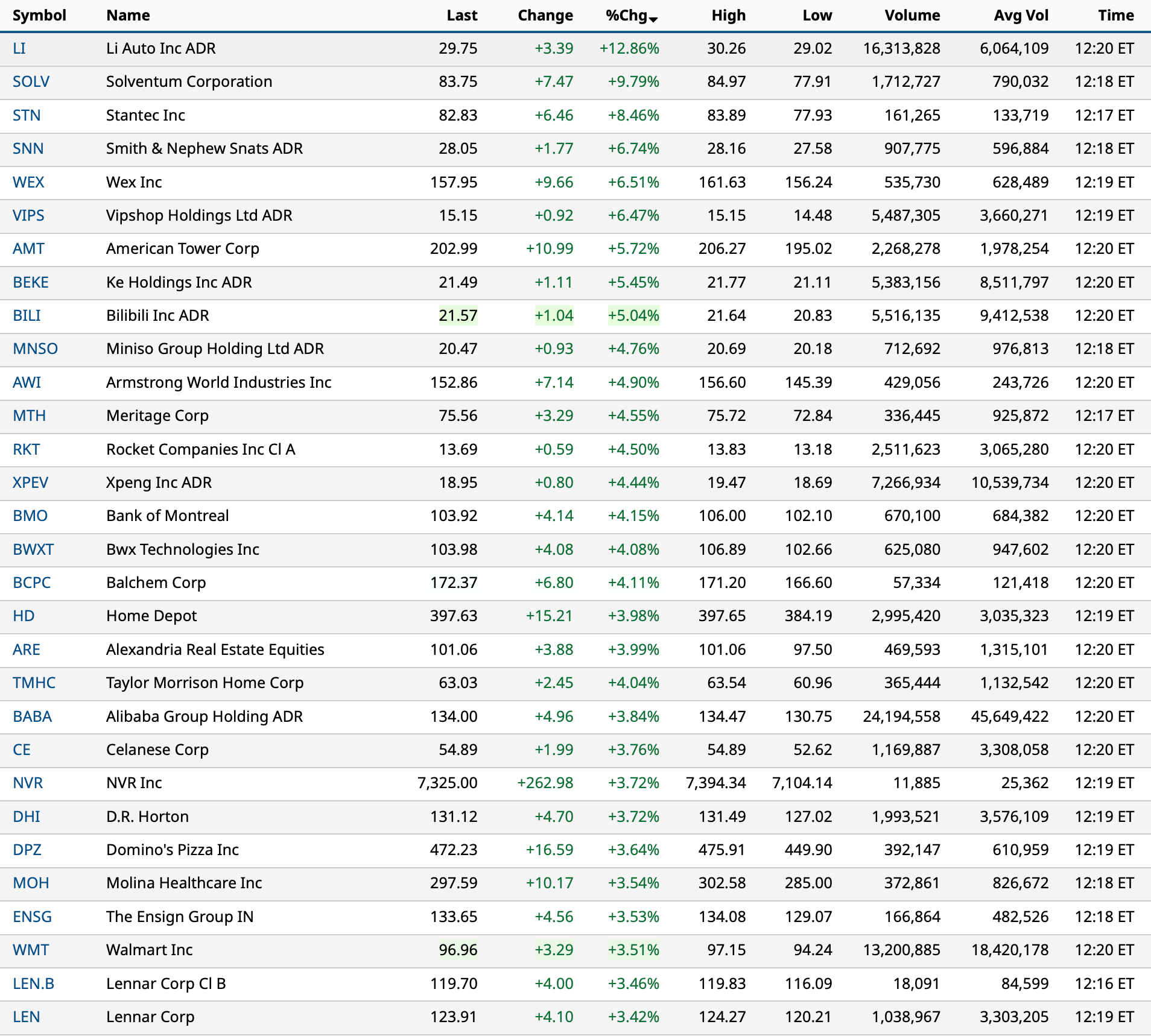

BY Doug Kass · Feb 25, 2025, 8:47 AM EST

This is a valuable table for momentum-based short-term traders:

BY Doug Kass · Feb 25, 2025, 8:35 AM EST

From JPMorgan:

US: Futs are lower as the risk-off behavior continues; SPX futs are outperforming NDX/RTY. Trump said that CAN/MEX tariffs would be implemented on-time. Pre-mkt, Mag7 names are lower with NVDA -1.6% and Semis under pressure as the battle over chips appears to escalate. Bond yields are lower 5-6bps and USD is flat. Cmdtys are mostly lower with crude/gasoline higher. Today’s macro data focus is on Housing, regional Fed activity indicators, and Consumer Confidence.

and...

EQUITY AND MACRO NARRATIVE: Trade war headlines are dominating markets as investors await NVDA/AVGO earnings to see if the AI/TMT trade can get back on track. In a relatively light macro data week, Consumer Confidence is one to watch today given its ties to spending and fears over the state of the Consumer. Our view is that the consumer, and corporations, remain in good shape but that policy uncertainty is delaying spending and capex decisions.

BY Doug Kass · Feb 25, 2025, 8:25 AM EST

4:20AM: Fed Bank of Dallas President Logan (Non-Voter) speaks before the 2025 BEAR (Bank of England Agenda for Research) Conference: "The Future of the Central Bank Balance Sheet," London

11:45AM: Federal Reserve Vice Chair for Supervision Barr (Voter) speaks on "Financial Stability" before an event hosted by the Yale Program on Financial Stability, New Haven, CT

1:00PM: Fed Bank of Richmond President Barkin (Non-Voter) speaks on "Inflation Then and Now" before the Rotary Club of Richmond, Richmond, VA

BY Doug Kass · Feb 25, 2025, 8:15 AM EST

Also today:

8:30AM: Philly Fed Non-Manufacturing Activity (February)

8:55AM: Johnson Redbook Retail Sales Reports (w/e 2/22)

BY Doug Kass · Feb 25, 2025, 8:06 AM EST

In late January our channel checks suggested that Elanco Animal Health ELAN may miss the quarter. I sold 95% of my common position, holding on to a small (out of the money) call option (which expired worthless on Friday). Our analysis differed from several sell-side brokerages who reiterated their buy recommendations recently:

Our channel checks for Elanco (ELAN) are a bit disappointing.

I was hopeful that the company would meet Street expectations, but that now appears challenging.

Though the quarter is not reported until February 24 (four weeks away), discretion is the better part of valor and I have sold most of my common holdings.

However, I am keeping my calls (as the pet company remains a bonafide takeover candidate).

By Doug Kass Jan 29, 2025 9:43 AM EST

Today the company reported poor results, as expected, and offered up weak guidance (relative to expectations).

Here is the company's fourth-quarter release.

BY Doug Kass · Feb 25, 2025, 7:28 AM EST

The S&P Short Range Oscillator stays in modest oversold ground — at -0.82% vs. -1.42%.

BY Doug Kass · Feb 25, 2025, 6:50 AM EST

BY Doug Kass · Feb 25, 2025, 6:39 AM EST

BY Doug Kass · Feb 25, 2025, 6:36 AM EST