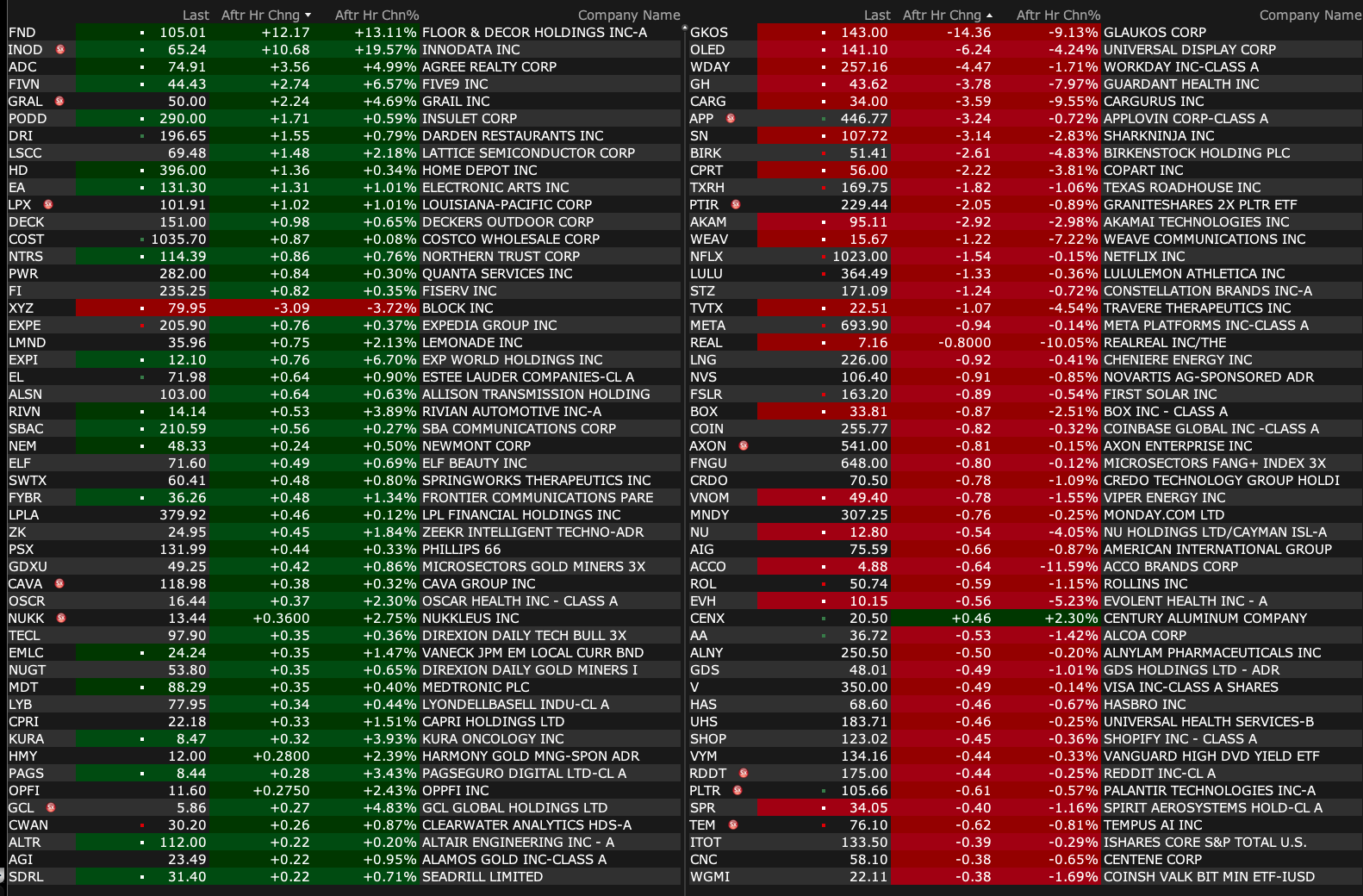

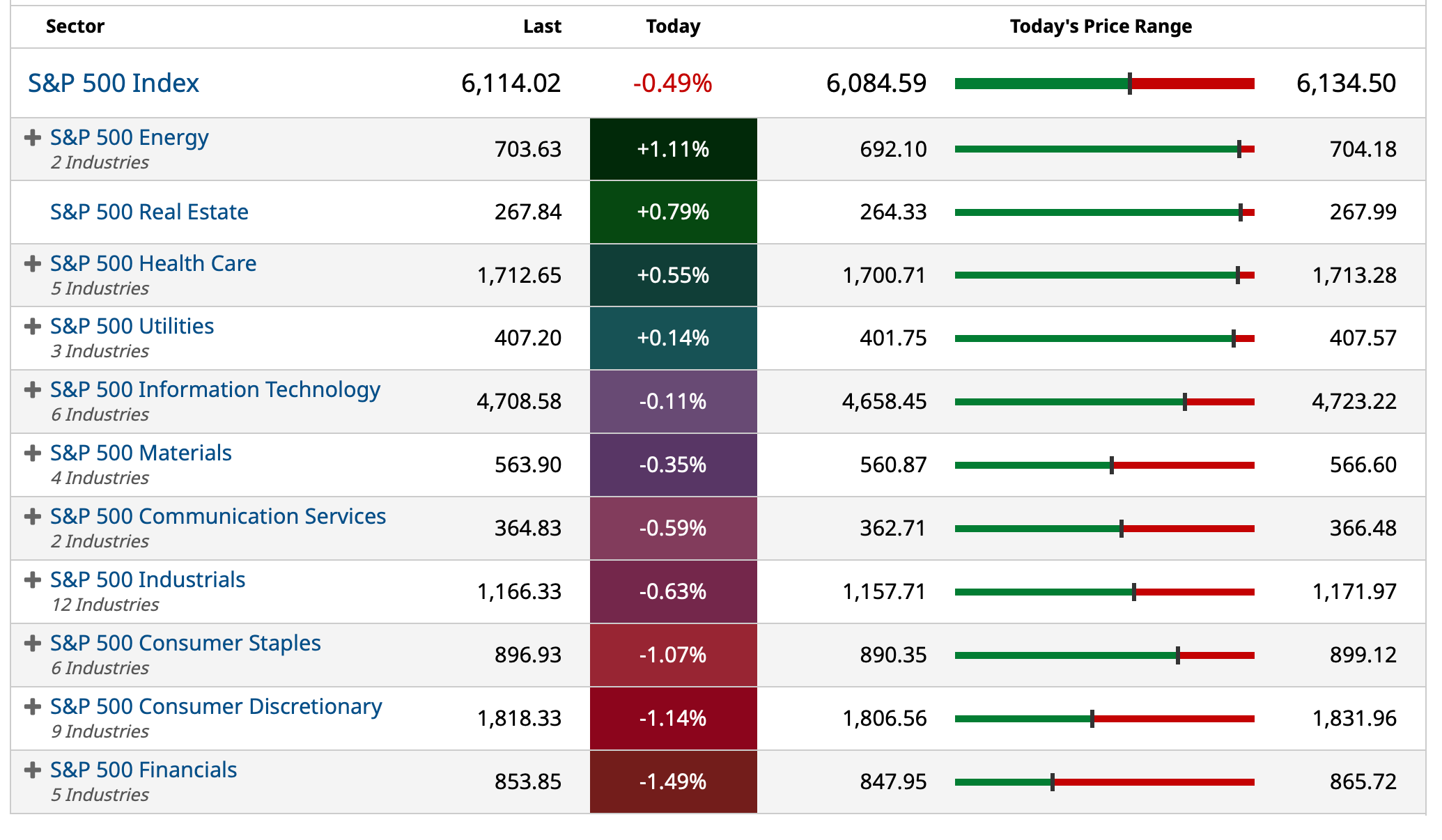

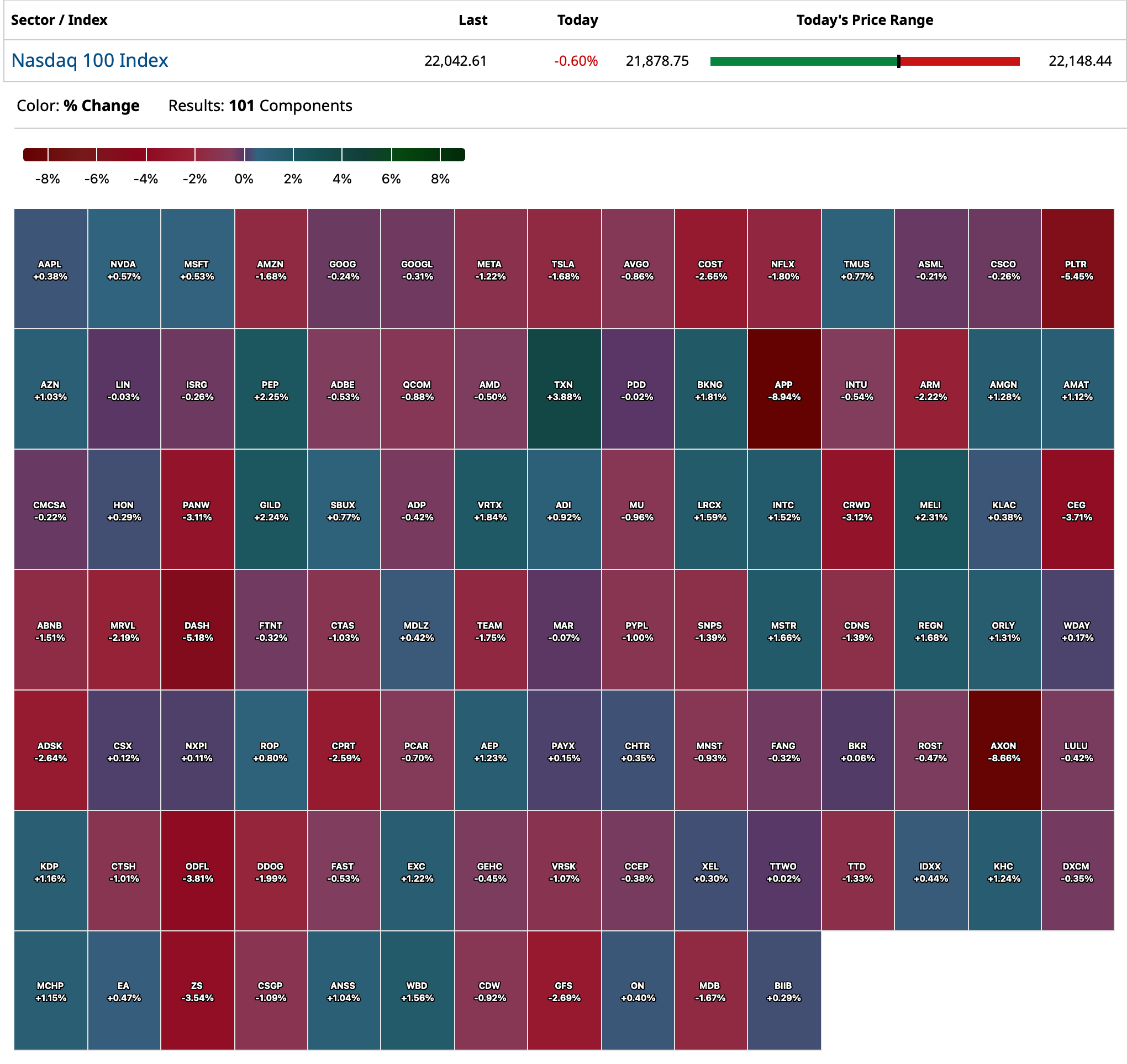

Thursday's After-Market Movers

At 4:11 p.m.:

BY Doug Kass · Feb 20, 2025, 5:02 PM EST

At 4:11 p.m.:

BY Doug Kass · Feb 20, 2025, 5:02 PM EST

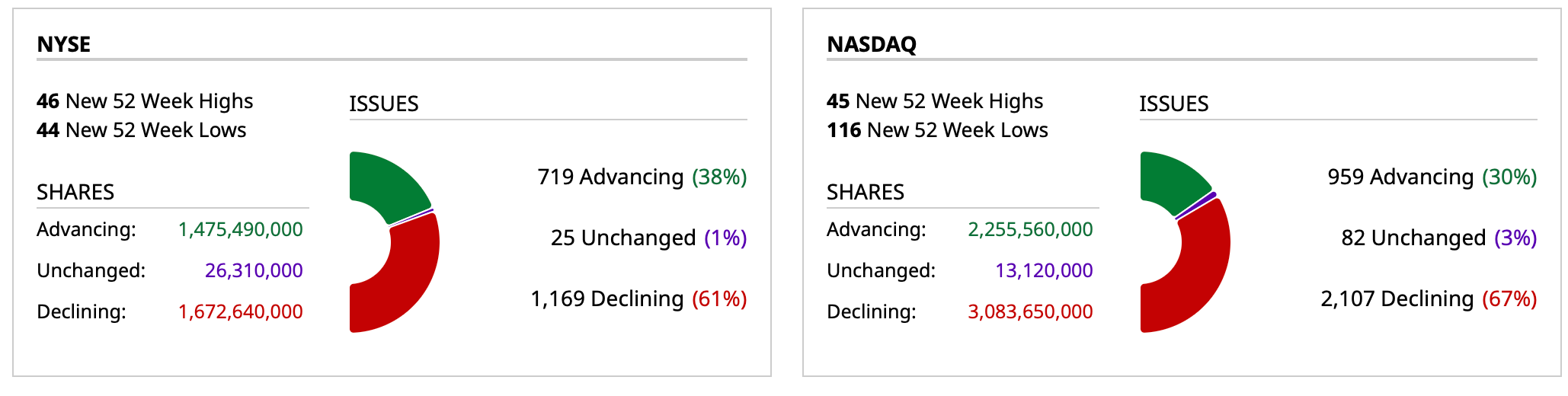

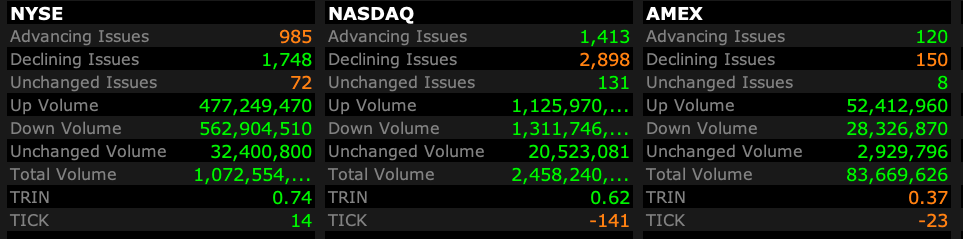

- NYSE volume 7% above its one-month average

- NASDAQ volume 5% below its one-month average

-VIX: up 1.18% to 15.45

BY Doug Kass · Feb 20, 2025, 4:54 PM EST

* I was wondering if I would ever see a down day.

* I sure hope The Dude makes the finals...

"One of those days, huh. A wiser fella than myself once said, "sometimes you eat the bar and sometimes the bar, well, he eats you"

"Is that some kind of Eastern thing?"

"Far from it"

- The Stranger, The Big Lebowski The Dude, The Stranger, The Bar

Thanks for reading my Diary today.

But I didn't like seeing Donny go. (But then I happen to know there is a little Lebowski on the way!)

Enjoy the evening.

Take 'er easy, Dude.

Be safe.

Catch you later down the trail.

BY Doug Kass · Feb 20, 2025, 3:30 PM EST

With S&P cash rallying to down only -31 handles, I have taken off some of my long Index common (which was held against short calls), so getting shorter again.

But baby steps.

BY Doug Kass · Feb 20, 2025, 3:18 PM EST

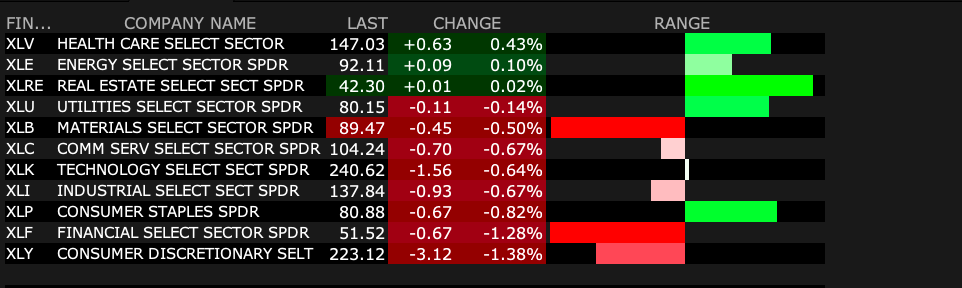

BY Doug Kass · Feb 20, 2025, 3:07 PM EST

View side-by-sides of Goldman Sachs GS, Citigroup C, JPMorgan Chase JPM:

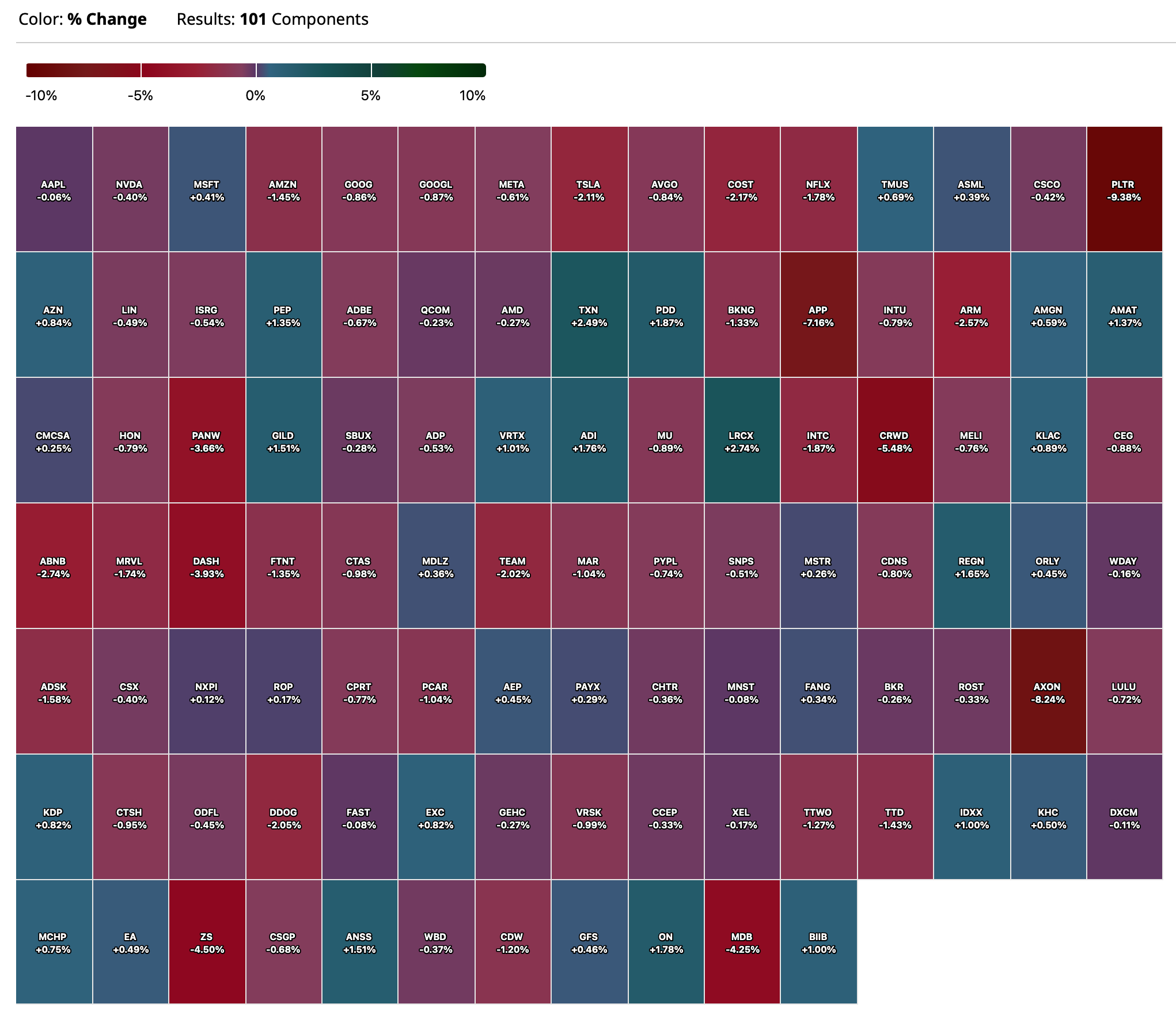

BY Doug Kass · Feb 20, 2025, 2:35 PM EST

Comments from Satya Nadella about AI.

A tweet about his comments first. (At some point you would think enthusiasm for this stuff is going to start falling faster than a turd from a tall moose):

Microsoft CEO Satya Nadella has cautioned against the hype surrounding AI,

comparing the current frenzy to the dot-com bubble. He said AI's long term

impact must be measured by its ability to drive global GDP growth rather than

arbitrary benchmarks. "If you're going to have this explosion, abundance,

whatever, commodity of intelligence available, the first thing we have to

observe is GDP growth". "Before I get to what Microsoft's revenue will look

like, there's only one governor in all of this. This is where we get a little

bit ahead of ourselves with all this AGI hype". He criticised the tech

industry's tendency to claim artificial general intelligence breakthroughs

without real world validation. "Us self-claiming some AGI milestone, that's

just nonsensical benchmark hacking to me". "The real benchmark is: the world

growing at 10%", which is just not happening. Nadella also addressed concerns

over reckless overbuilding in AI infrastructure, drawing parallels to the

dot-com boom. "There was a lot of money lost," he said, referring to the early

2000s tech crash. "Everybody's going to race... the only thing that's going to

happen with all the compute builds is the prices are going to come down," the CEO said.

BY Doug Kass · Feb 20, 2025, 1:20 PM EST

From Gary Marcus:

The primary lesson here is the same as in the early ChatGPT days: caveat emptor. No matter how good-looking the output, there are often subtle errors that most people wouldn’t catch.

The secondary lesson here is that the more excited people are about LLMs, the more I wonder how carefully they have examined the output.

Stepping back, the broadest observation is this. Grok 3 required training two new massive data centers operating full time for months, and 15x the compute of Grok 2 — yet all these kinds of errors feel awfully familiar.

If AI were (as it used to be, to some degree) a science, people would say: “Hey, we put half a trillion dollars into testing the idea of scaling and massive compute and something’s still not right, maybe we should try something else?” Instead, valuations just keep rising, results notwithstanding. At least for now.

BY Doug Kass · Feb 20, 2025, 12:52 PM EST

BY Doug Kass · Feb 20, 2025, 12:07 PM EST

I am out of all my financial stock shorts today except B. Riley RILY.

BY Doug Kass · Feb 20, 2025, 11:52 AM EST

BY Doug Kass · Feb 20, 2025, 11:44 AM EST

BY Doug Kass · Feb 20, 2025, 11:15 AM EST

BY Doug Kass · Feb 20, 2025, 10:55 AM EST

I covered the balance of my MS short at $134 (-$6.70)

BY Doug Kass · Feb 20, 2025, 10:52 AM EST

Bidding for individual cannabis equities across-the-board.

BY Doug Kass · Feb 20, 2025, 10:50 AM EST

keithfern

14 minutes ago

If WMT had disappointing results...and 75% of its market share gain over the last year came from households making over $100k...do we really think AAPL should be bought?

Shorting AAPL.

BY Doug Kass · Feb 20, 2025, 10:50 AM EST

I covered half of my ARKK (-$2 1/2)

BY Doug Kass · Feb 20, 2025, 10:43 AM EST

Adding to MSOS at $3.27.

BY Doug Kass · Feb 20, 2025, 10:38 AM EST

I covered the balance of my JPMorgan JPM at $272.86.

I plan to reshort on strength.

BY Doug Kass · Feb 20, 2025, 10:25 AM EST

I covered half of my JPM short at $273.52.

BY Doug Kass · Feb 20, 2025, 10:18 AM EST

I covered my GS short at $351.

BY Doug Kass · Feb 20, 2025, 10:12 AM EST

With S&P cash -58 handles I covered a bunch of my short Index calls on the whoosh lower.

BY Doug Kass · Feb 20, 2025, 10:07 AM EST

From Peter Boockvar:

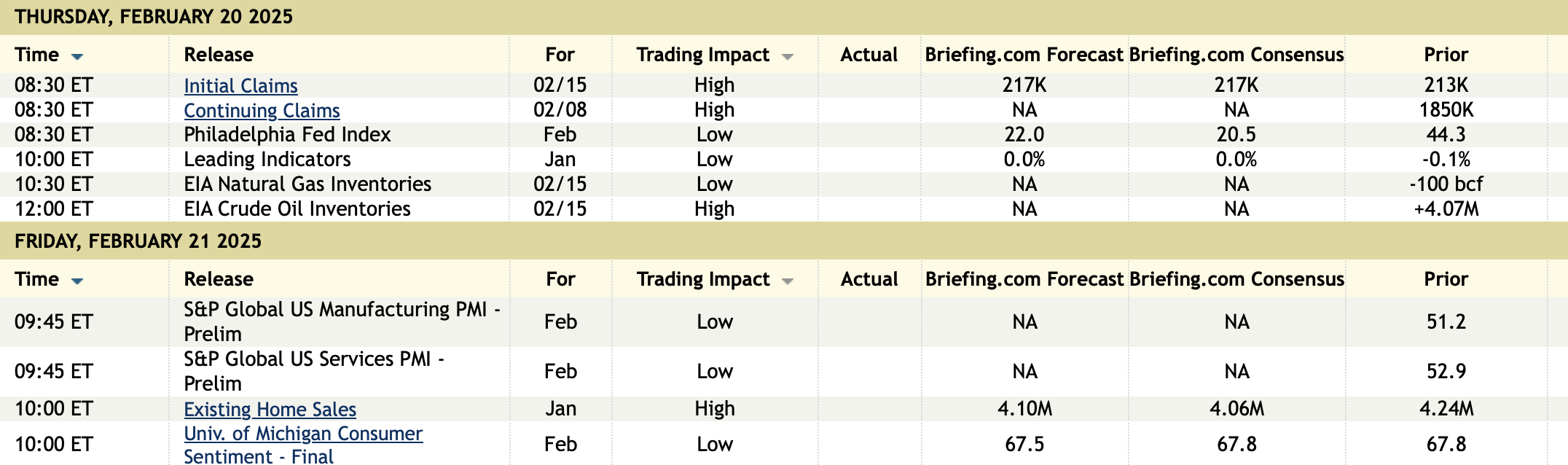

Initial jobless claims rose to 219k from 214k and that was 4k above the estimate. The 4 week average of 215k is down 1k w/o/w as a print of 223k drops out of the calculation. Continuing claims totaled 1.869mm as expected and still around the highest since November 2021.

By the way, the Washington, DC claims figure as of 2/14 is near a 2 yr high at 1,695 which compares to 473 in February 2020, as to be expected with the layoffs going on.

Outside of this, the story remains the same with the low level of firing's as measured here and the more subdued, but still good, pace of hiring's.

Following a positive print seen Tuesday in the NY manufacturing February index, the Philly regional index just out was +18.1, 4 pts above expectations and after the January spike to 44.3 and vs -10.9 in December. Also similar to the NY survey was the further rise in prices paid and prices received.

Those paid rose to 40.5 from 31.9 and that is the highest since October 2022. Prices received were up 3.2 pts m/o/m to the most since November 2022.

The internals otherwise were all over the place and best to compare with the 6 month average because of the month to month volatility. New orders at 21.9 is vs the 6 month average of 13.3 but backlogs at 1.4 is below the half yr average of 8.1. Inventories were just under zero at -.4 vs the average of 2.9. Employment at 5.3 is about in line with the average of 6.3 and the same with the workweek.

Also seen in the NY survey was the drop in the 6 month outlook and that happened here too with it dropping to 27.8 from 46.3. That's a 5 month low. Capital spending plans fell to a 6 month low.

Bottom line, as said on Tuesday with the NY index, I'm sure the outlook is clouded by the tariffs implemented on China and its impact and the likelihood of other tariffs coming elsewhere. At the same time, there is plenty of business optimism currently that the more than 2 yr recession is trying to find a bottom and the regulatory state will now ease the cost of doing business.

BY Doug Kass · Feb 20, 2025, 9:50 AM EST

With S&P cash -11 handles I added to my short calls.

BY Doug Kass · Feb 20, 2025, 9:39 AM EST

From Peter Boockvar:

To two big speculations that I've been hearing about over the past month, that being revaluing the price of gold that is marked currently at the US Treasury at $42 per ounce and also terming out US debt via more longer term debt issuance and maybe the speculation of having our foreign friends take some 100 year bonds, Treasury Secretary Scott Bessent had something to say to Bloomberg TV on both. On the latter with terming out our debt, "That's a long way off." On revaluing gold, "not what I had in mind" and he has no plans of visiting Fort Knox. He also mentioned wanting a strong dollar policy. No market response to Treasuries and gold but interesting to hear from him in light of all the speculation.

The yen is back to testing the 150 level vs the US dollar for the first time since early December and something we should all watch, especially as we approach the end of the Japanese fiscal year as of the end of March. More attractive yields in Japan at more than decade highs, with JGB's seemingly selling off every day (has rallied once since the end of January) and Japan still the largest holder of US Treasuries, more Japanese money might be in the process of being repatriated back home.

Post holidays and the rush to get goods, along with the continued Israel/Hamas truce which has kept the Houthi's quiet resulted in container shipping costs to fall for a 9th straight week by $269 w/o/w to $2,618 for the Shanghai to Rotterdam route. That price is the lowest since early January 2024. The Shanghai to LA cost fell to the lowest since December 2024 at $3,888, down by $504.

Speaking of the pull forward of orders at the end of last year, Taiwan exports in January fell 3% y/o/y vs the estimate of a gain of 2.7%. The Economic Ministry of Affairs though is still optimistic for this year saying "Demand will remain solid for our supply chain of advanced technologies in semiconductors and servers, supporting export orders growth momentum."

Reflecting a still tough macro backdrop for global manufacturing, the UK CBI February industrial orders figure was -28, though up 6 pts m/o/m and 2 pts above expectations. CBI said "The survey paints a downbeat picture of the manufacturing sector over the last three months, which can be attributed in part to low domestic business confidence following the Autumn Budget combined with a subdued international environment. Manufacturers expect to raise output in the quarter ahead. But with firms having rapidly run down stocks of finished goods, it's possible that the need to re-build inventories partly explains this rebound. Order books remain weak from a long-term perspective."

I'll add, as seen in many places in Europe, and in the US, it's been the services sector that has carried the economic day. The number is not typically market moving but the pound is just shy of a 2 month high, gilt yields are higher again while the FTSE 100 is down by .3%, though still up almost 7% year-to-date. There are still a lot of cheap stocks domiciled in the UK that we own.

With global manufacturing having been in a 2 yr+ recession, trucking the stuff has been too. JB Hunt spoke yesterday at a Barclays conference and said this:

"I think we're at 31, 32 months of dealing with this freight recession. And so I do feel like we're at the bottom. I do feel like we're at an inflection point." Let's hope.

Also, they continue to see pressure on rates with the lower volumes but higher insurance and claims costs are also pressuring margins.

From Walmart, whose stock is down sharply pre market but one that was trading at 38x earnings and leaving no room for error:

US comp sales grew by 4.6% "with positive growth in general merchandise." They guided to 3% to 4% net sales growth for FY '26 vs the consensus of 4%.

Also in Walmart US, "Comp sales growth led by transaction counts and unit volumes; share gains primarily from upper-income households." eCommerce sales rose 20% and "reflects strength in store-fulfilled pickup & delivery, advertising and marketplace."

Sales growth at Sam's Club was "led by food and health & wellness categories."

What Walmart delivers is value and convenience and if you can't deliver that, you are having a tougher retail time.

This is what Etsy said to that yesterday and whose stock fell 10%:

"Recent eCommerce growth has been skewed towards those that offer low prices and fast delivery and that's a game we're unlikely to win. We also recognize that consumers are shopping and spending their time differently with more competition than ever for mindshare."

From Carvana, whose stock is down as wholesale unit sales and margins were a touch light but after an incredible stock rebound:

"The strong demand we experience in the first three quarters of the year continued into the fourth quarter."

Wingstop stock, a very pricey one at about 65x earnings, fell 13% as comps disappointed and they mentioned heightened competition:

"QSR is promoting value heavily as a way to reverse their transaction trends." They also noted "the unseasonable weather in the southeast and the fires in California."

Analog Devices stock popped 10% yesterday as numbers were above the midpoint of their previous guide. They said "while we continue to operate in a challenging macro and geopolitical environment, our first quarter results and outlook for double-digit y/o/y growth in our 2nd quarter builds my confidence that 2025 will be a year of growth."

Finally, it is important to not just look at one stock market sentiment gauge and look at a bunch. If we look only at the individual investor AAII survey, we should all be bullish because they are mostly bearish. Bulls were little changed at 29.2, up .8 pts off the lowest level since mid January. The Bears last week rose to the most since November 2023 but fell back by 6.8 pts to 40.5. On the other hand, Investors Intelligence still has many more Bulls than Bears. Bulls clocked in at 49.2 from 46.8 and Bears fell to 25.4 from 29. We also saw over last weekend that the Citi Panic/Euphoria index is well into Euphoria land, back at multi year highs at .70, well above the Euphoria threshold of .41. I discount the AAII survey because it's so volatile and fickle.

BY Doug Kass · Feb 20, 2025, 9:37 AM EST

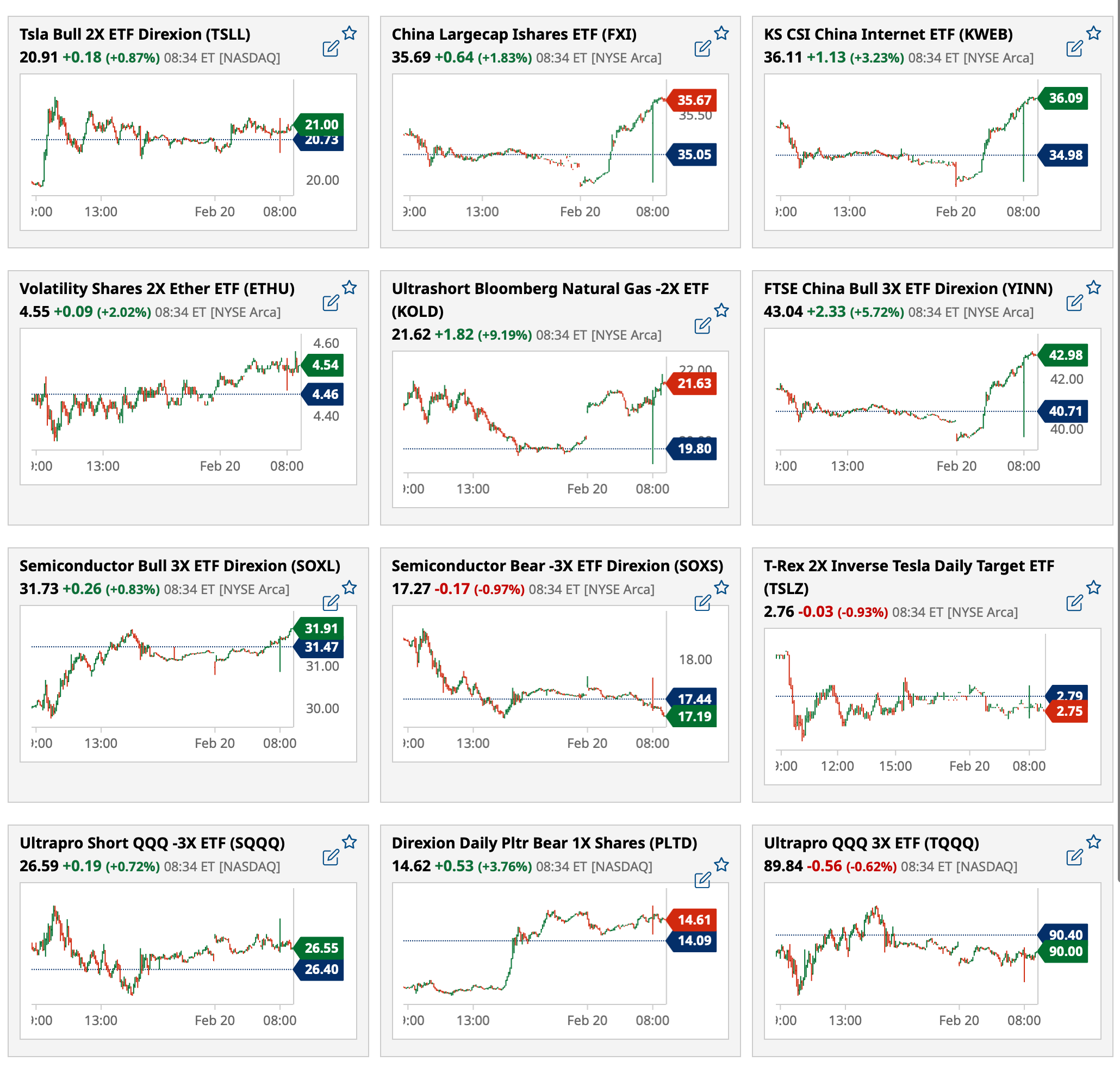

Most active premarket ETFs as of 8:39 a.m. ET:

BY Doug Kass · Feb 20, 2025, 9:15 AM EST

-BRTX +37% (receives FDA Fast Track Designation for BRTX-100 Chronic Lumbar Disc Disease Program)

-XOS +34% (Xos Hub listed on Federal GSA Schedule)

-MNDR +29% (secures $10M Funding to Expand AI-Powered Telehealth Solutions)

-HLF +26% (earnings, guidance)

-LUNG +21% (earnings, guidance)

-CWAN +18% (earnings, guidance)

-BABA +11% (earnings, guidance)

-MCW +11% (earnings, guidance)

-KLTR +10% (earnings, guidance)

-BMRN +8.2% (earnings, guidance)

-BAX +7.9% (earnings, guidance)

-GCI +7.1% (earnings, guidance)

-NRDS +6.9% (earnings, guidance)

-ALIT +6.1% (earnings, guidance; Chairman of Board to step down)

-PWR +6.1% (earnings, guidance)

-DARE +6.0% (Daré Bioscience and Theramex Announce Co-Development and Licensing Agreement for a Potential Biodegradable Long-Acting Contraceptive Implant)

-CRAI +5.9% (earnings, guidance)

-BHC +4.6% (earnings, guidance)

-DRS +3.9% (earnings, guidance)

-OEC +3.3% (earnings, guidance)

-SABR +3.2% (earnings, guidance)

-ATHM +3.1% (Haier Group to buy 41.9% of Company for ~$1.8B)

-ASMB +2.9% (reports Positive Interim Phase 1a Results from Clinical Trial Evaluating Long-Acting Helicase-Primase Inhibitor ABI-1179 in Development for Recurrent Genital Herpes)

-LAUR +2.9% (earnings, guidance)

-RELY +2.9% (earnings, guidance)

-VMEO -16% (earnings, guidance)

-TRUP -15% (earnings, guidance)

-TALK -13% (earnings, guidance)

-INBS -11% (prices $2.6M Public Offering of Common Stock at $2.00/shr)

-INSG -11% (earnings, guidance)

-U -9.3% (earnings, guidance)

-CVNA -8.8% (earnings, guidance)

-WMT -7.9% (earnings, guidance)

-ACVA -7.1% (earnings, guidance)

-DBRG -6.5% (earnings, guidance)

-FCN -6.0% (earnings, guidance)

-DNB -4.9% (earnings, guidance)

-BLDR -4.7% (earnings, guidance)

-GRAB -4.7% (earnings, guidance)

-VTLE -4.7% (earnings, guidance)

-PNST -2.7% (earnings)

BY Doug Kass · Feb 20, 2025, 9:06 AM EST

Premarket percentage movers at 8:35 a.m. ET:

BY Doug Kass · Feb 20, 2025, 8:55 AM EST

9:35 a.m.: Fed Bank of Chicago President Goolsbee (Voter) participates in a moderated question-and-answer session before the Chicagoland Chamber Mid-Market Chicago event, Chicago, IL

12:05 p.m.: Fed Bank of St. Louis President Musalem (Voter) speaks before the Economic Club of New York

2:30 p.m.: Fed Vice Chair for Supervision Barr (Voter) speaks on "Supervision and Regulation" at the Georgetown University Law Center, Washington, DC

5:00 p.m.: Fed Board Governor Kugler (Voter) speaks on "Navigating Inflation Waves While Riding on the Phillips Curve" before the 2025 Whittington Lecture event hosted by Georgetown University

BY Doug Kass · Feb 20, 2025, 8:43 AM EST

BY Doug Kass · Feb 20, 2025, 8:33 AM EST

"Don't focus on the macro. Look at WMT's chart. WalMart benefits from... "

- Panelist on CNBC (Final Trades, Two Weeks Ago)

Walmart WMT shares are -$9 in premarket trading after disappointing results.

From those uber-confident folks on Fin TV (many of whom have no serious investment process but a lot of "feel"):

Two Weeks Ago - Final Trades (CNBC) Final Trades: Cisco, UnitedHealth and Walmart

Belski Bullish on Walmart Final Trades: Cisco, UnitedHealth and Walmart

Three Stock Lunch (CNBC) 3-Stock Lunch: Walmart, SolarEdge and Bumble

Walmart Is Hitting on All Cylinders (CNBC) Walmart is hitting on all cylinders, says Loop Capital's Anthony Chukumba

Calls of the Day (CNBC) Calls of the Day: Starbucks, Uber, Lowe's, Walmart, Casey's General Store, AT&T and Charles Schwab

These actors will not likely take ownership of this investment boner.

Wash, rinse, repeat.

BY Doug Kass · Feb 20, 2025, 8:08 AM EST

* Cheerleading is not journalism...

Yesterday Palantir's PLTR stock fell by about -12% on news of Pentagon cuts and a modified stock sale plan from CEO Alex Karp. (I was short and covered into the schmeissing.)

I was critical of Karp's CNBC appearance (both in my Diary and on X) recently, which was nothing more than some "double talk" and a bunch of softball questions from complicit moderators.

That is the problem, Fin TV has become a platform for BS rather than a serious opportunity to discuss opportunities (and threats) to business models.

The Karp interview reminded me of CNBC's pathetic interview of Sam Bankman-Fried, weeks before it was discovered his company, FTX, was a Ponzi scheme.

I am not suggesting Palantir is a Ponzi scheme at all — it is not. I am critical of our business media which consistently fails to develop meaningful and value-added interviews.

A previous column of mine on softball throwing:

BY Doug Kass · Feb 20, 2025, 7:30 AM EST

BY Doug Kass · Feb 20, 2025, 7:25 AM EST

BY Doug Kass · Feb 20, 2025, 7:15 AM EST

I have covered my Walmart WMT short after disappointing results (-$9) at $95.50. This stock was universally admired over the last few days on Fin TV (more on that later!).

Why? The shares had momentum...

Wash, rinse, repeat.

BY Doug Kass · Feb 20, 2025, 7:04 AM EST

From Charlie:

BY Doug Kass · Feb 20, 2025, 6:55 AM EST

This is a valuable table for momentum-based short-term traders:

BY Doug Kass · Feb 20, 2025, 6:45 AM EST

Bonus — Here are some great links:

How Technical Analysis Helps Manage Risk

Cathie Is Back (Note: I recently shorted ARKK at around $57)

BY Doug Kass · Feb 20, 2025, 6:30 AM EST

From JPMorgan:

US: Futs are lower with both NDX/RTY futs underperforming after setting a new ATH yesterday. The potential for a pausing of the Fed’s QT helped a late-day rally and Trump says a bigger China trade deal is possible but says there is a shot clock for Ukraine to find a deal. Pre-mkt, Mag7 names are mixed with Semis lower, bond yields down 1-2bps with USD weaker. Cmdtys seeing strength in both Ags and Metals. The macro data focus is on Jobless Claims and the Leading Indicator Index; Bessent interview at 7am EST.

and...

EQUITY AND MACRO NARRATIVE: Yesterday was a relatively quiet day and the Fed Minutes release catalyzed action in both Treasuries and Equities. The confirmation that the Fed is paused is not new news but the possibility of pausing (or tapering) QT lead to lower bond yields and another move higher in stocks. I mentioned to several clients yesterday, “if you are looking for a reason to buy stocks, this probably is not it but we do prefer up-days to down days.” Less flippantly, if the Fed were to reduce/pause QT this would reduce/remove a liquidity drain which tends to be a positive for stocks. It is unclear if Equity investors would treat this similarly to QE where we tend to see vol suppression and then a subsequent move to lower quality names, e.g., ARKK over NDX. Separately, Trump mentioned wanting to do a bigger trade deal with China.

BY Doug Kass · Feb 20, 2025, 6:20 AM EST

From Hedgeye:

BY Doug Kass · Feb 20, 2025, 6:10 AM EST

* Of a CNBC-kind

* As I vividly recall the picks of WBD, MRNA, TTD, ELF and so many more

From Hedgeye:

BY Doug Kass · Feb 20, 2025, 6:05 AM EST

Wolf Street howls about the "drunken sailors."

BY Doug Kass · Feb 20, 2025, 5:55 AM EST

The S&P Short Range Oscillator slipped from 3.0% to 1.58%.

BY Doug Kass · Feb 20, 2025, 5:45 AM EST