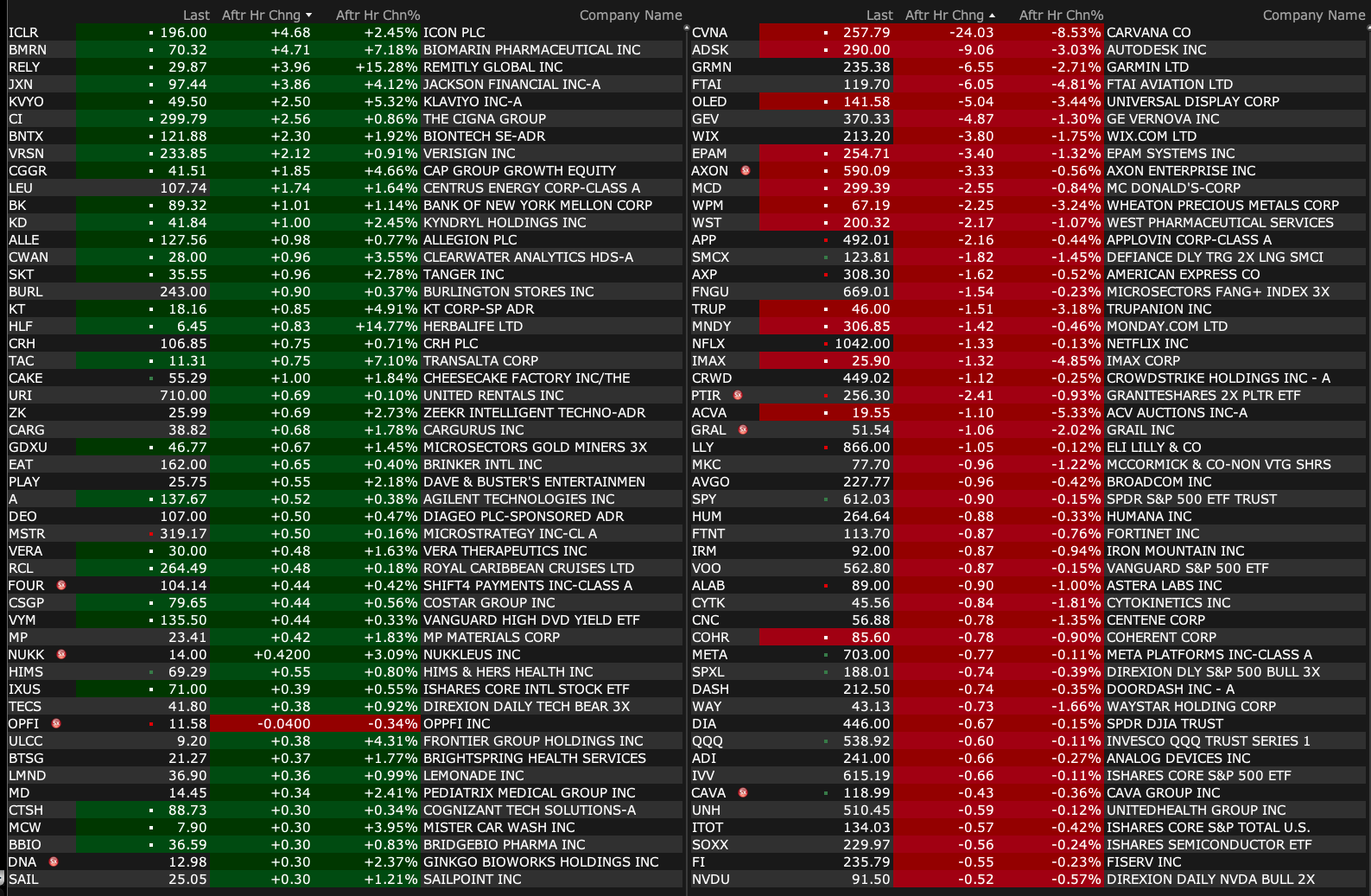

Wednesday's After-Hours Movers

As of 4:18 p.m.:

BY Doug Kass · Feb 19, 2025, 4:59 PM EST

As of 4:18 p.m.:

BY Doug Kass · Feb 19, 2025, 4:59 PM EST

BY Doug Kass · Feb 19, 2025, 4:49 PM EST

- NYSE volume 3% above its one-month average

- NASDAQ volume 5% above its one-month average

- VIX: down 0.78% to 15.23

BY Doug Kass · Feb 19, 2025, 4:39 PM EST

Thanks for reading my Diary today.

I hope you found my output helpful in your trading and investing decisions.

Enjoy the evening.

Be safe.

BY Doug Kass · Feb 19, 2025, 4:15 PM EST

* Of a Palantir-kind...

BY Doug Kass · Feb 19, 2025, 3:55 PM EST

I'm out of my Palantir PLTR short at $110.80.

This morning, I had shorted more PLTR at $123.13.

BY Doug Kass · Feb 19, 2025, 3:46 PM EST

Fourth cannabis buy today as I added to Green Thumb Industries GTBIF at $6.75.

BY Doug Kass · Feb 19, 2025, 3:19 PM EST

From Peter Boockvar:

The Fed also commented on the balance sheet and talked about some re-calibration of how they would manage their balance sheet once QT ended (we have no idea though when that will be) and also slowing QT around the debt ceiling discussions. This could also be a reason why yields dipped a bit.

“A number of participants also discussed some issues related to the balance sheet. Regarding the composition of secondary-market purchases of Treasury securities that would occur once the process of reducing the size of the Federal Reserve's holdings of securities had come to an end, many participants expressed the view that it would be appropriate to structure purchases in a way that moved the maturity composition of the SOMA portfolio closer to that of the outstanding stock of Treasury debt while also minimizing the risk of disruptions to the market. Regarding the potential for significant swings in reserves over coming months related to debt ceiling dynamics, various participants noted that it may be appropriate to consider pausing or slowing balance sheet runoff until the resolution of this event.”

BY Doug Kass · Feb 19, 2025, 3:06 PM EST

From Peter Boockvar:

The bottom line with the just released minutes from the FOMC meeting three weeks ago, they will sit and wait before cutting again. I say ‘cut’ because it still seems like they have an easing bias and maybe why yields came down a touch after the release.

To this, they said, “In discussing the outlook for monetary policy, participants observed that the Committee was well positioned to take time to assess the evolving outlook for economic activity, the labor market, and inflation, with the vast majority pointing to a still-restrictive policy stance. Participants indicated that, provided the economy remained near maximum employment, they would want to see further progress on inflation before making additional adjustments to the target range for the federal funds rate.”

“In discussing risk-management considerations that could bear on the outlook for monetary policy, a majority of participants observed that the current high degree of uncertainty made it appropriate for the Committee to take a careful approach in considering additional adjustments to the stance of monetary policy. Factors mentioned by participants as supporting such an approach included the reduced downside risks to the outlook for the labor market and economic activity, increased upside risks to the outlook for inflation, and uncertainties concerning the neutral rate of interest, the degree of restraint from higher longer-term interest rates, or the economic effects of potential government policies.”

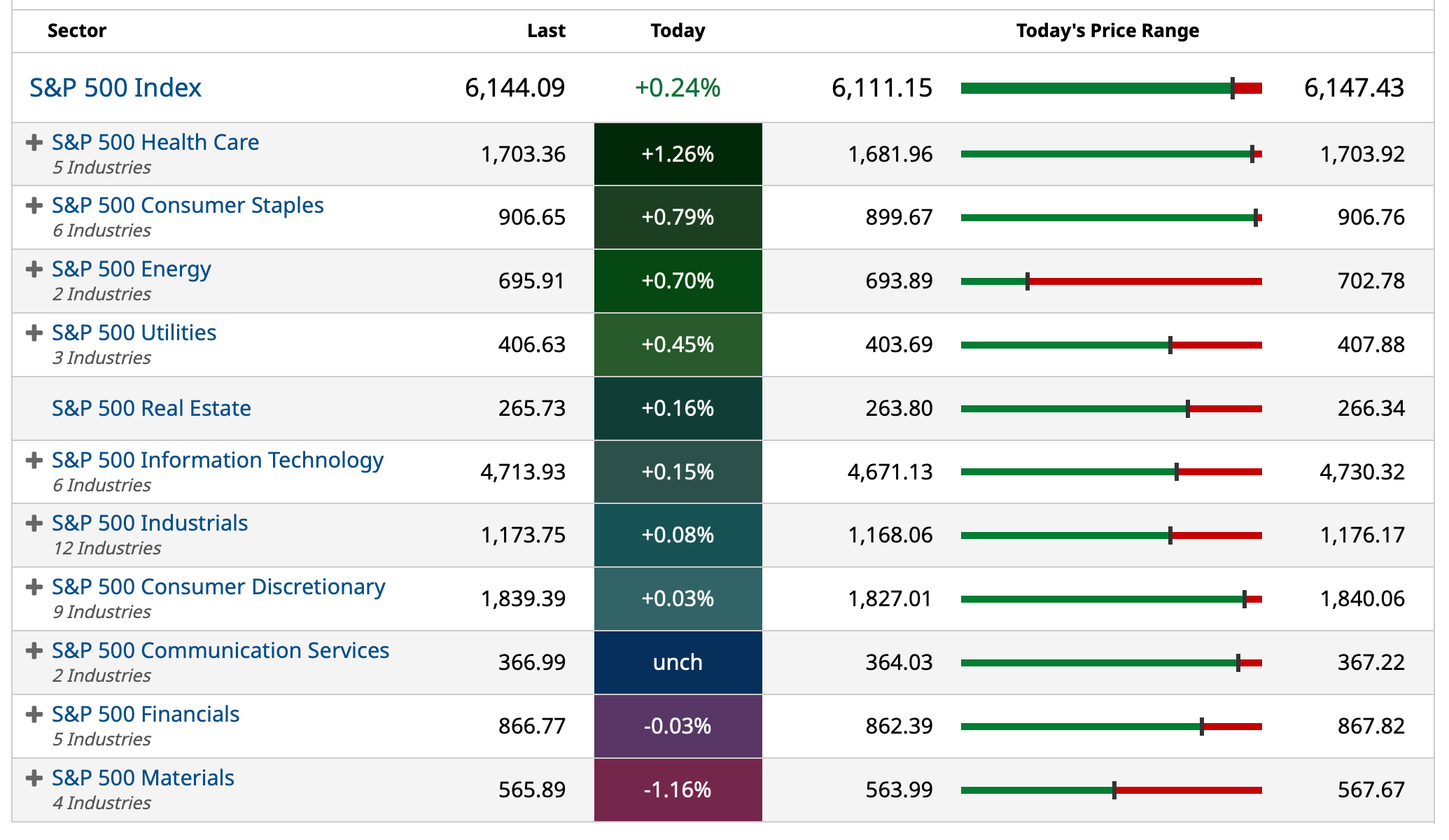

BY Doug Kass · Feb 19, 2025, 2:49 PM EST

All things being considered, a quiet day thus far.

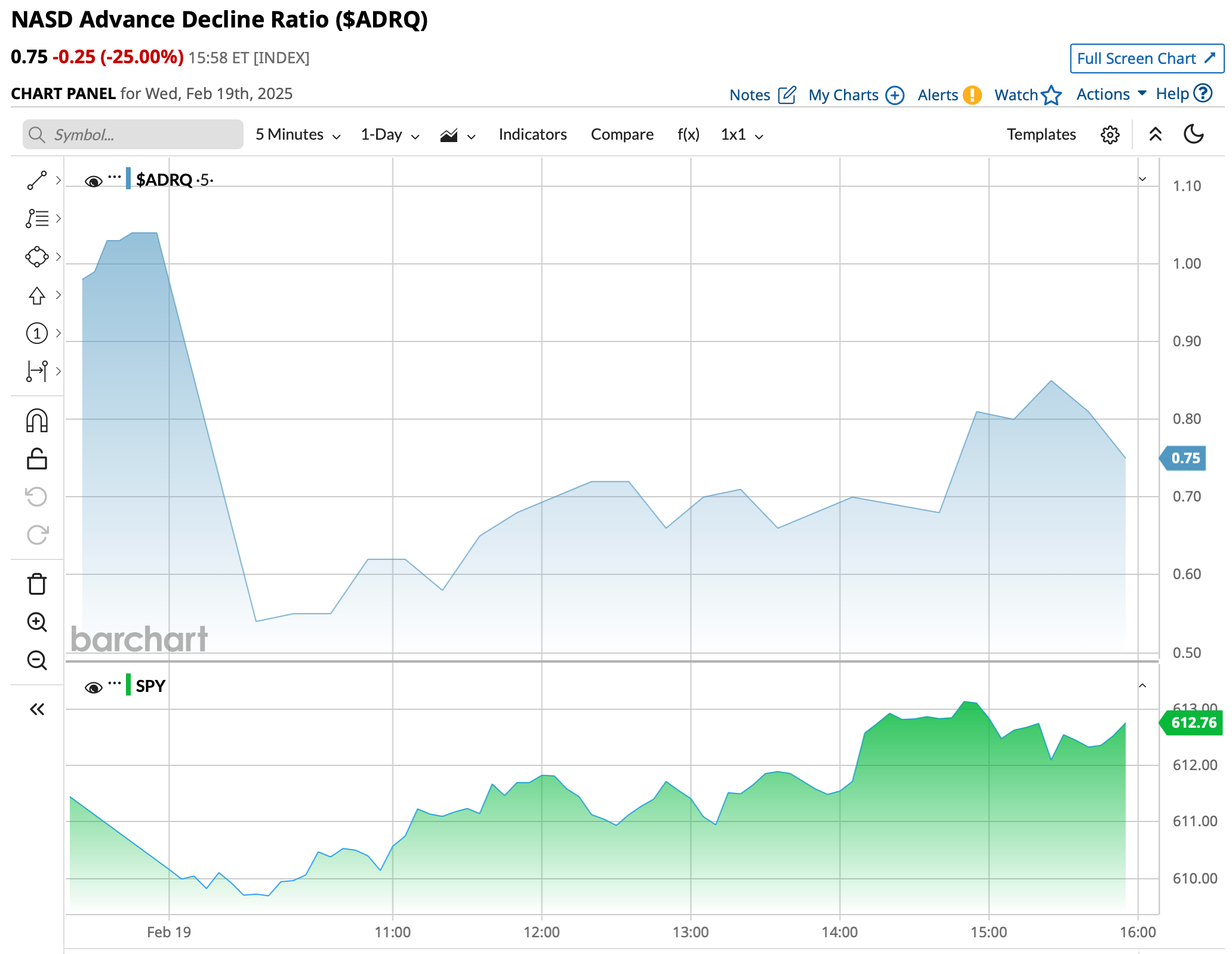

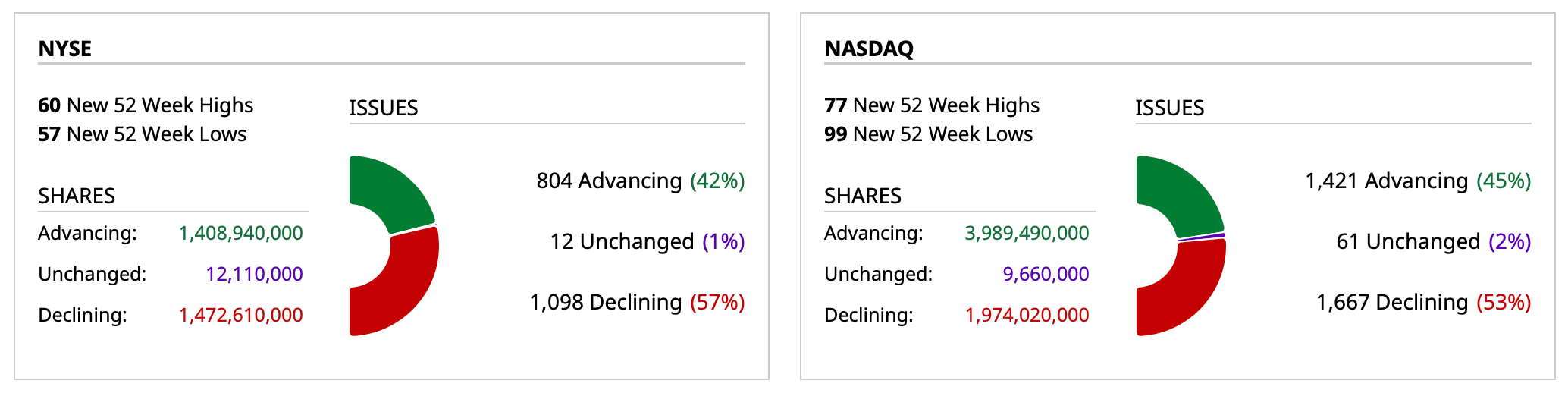

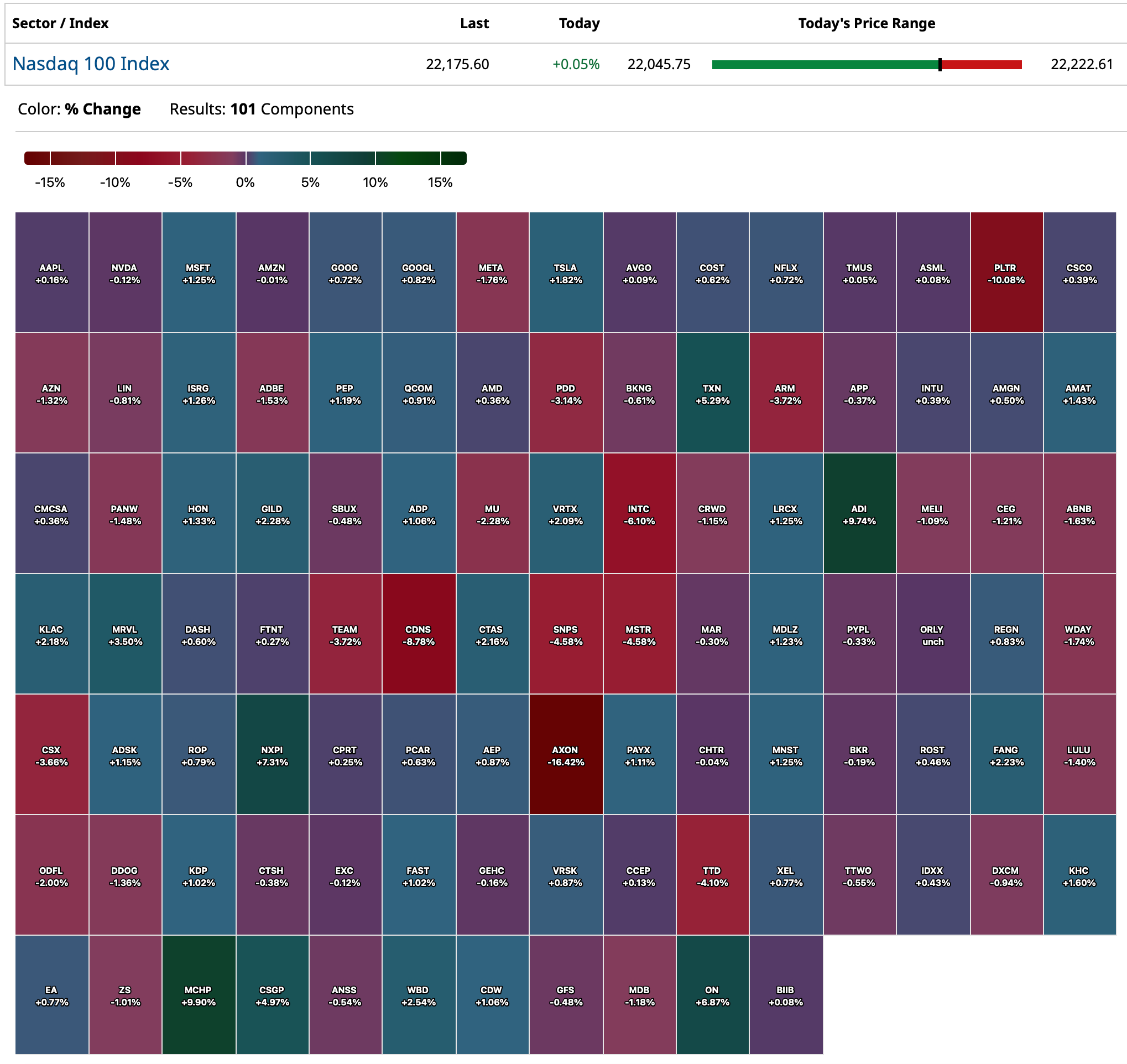

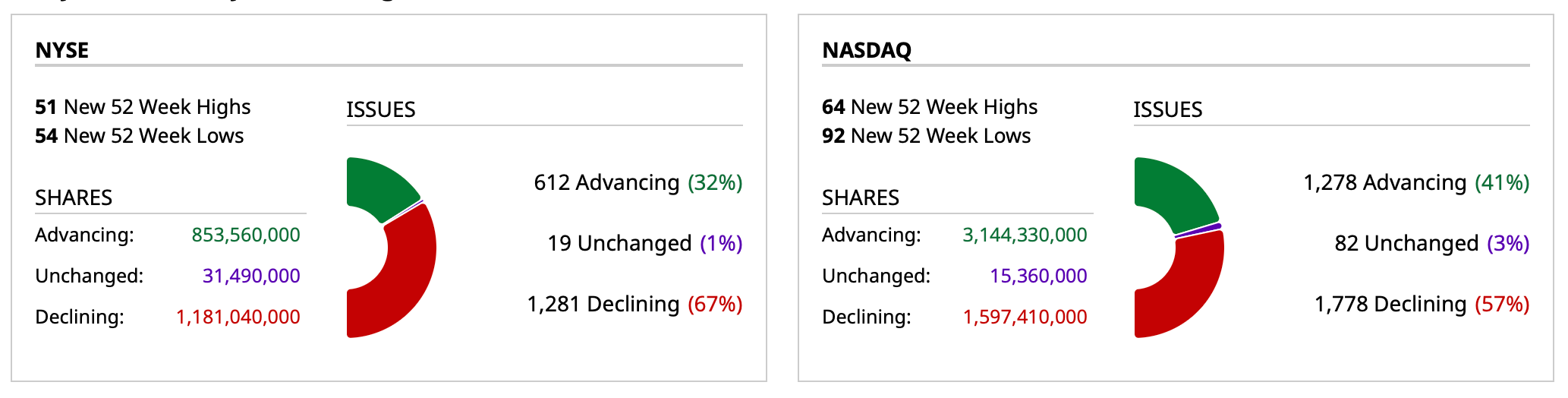

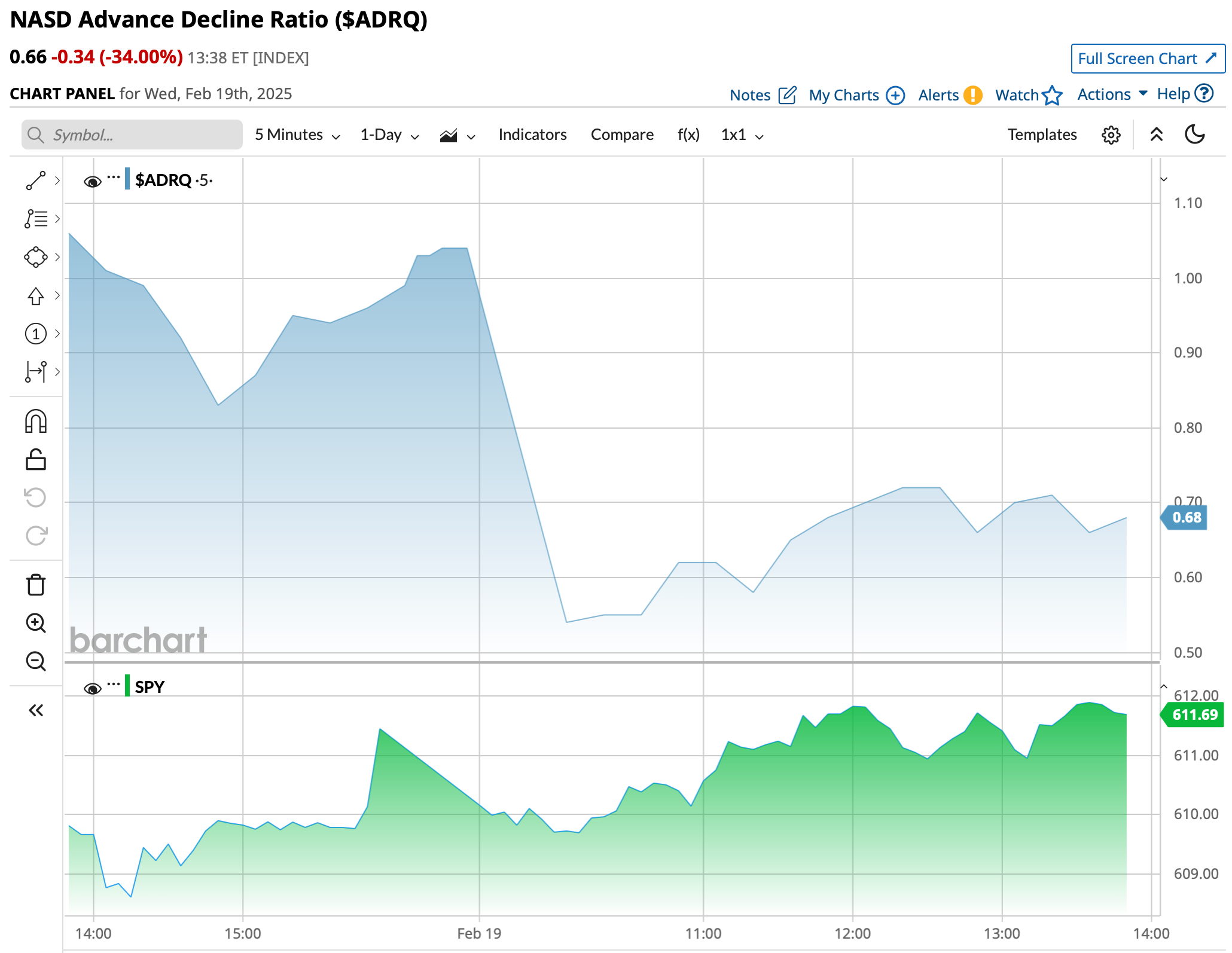

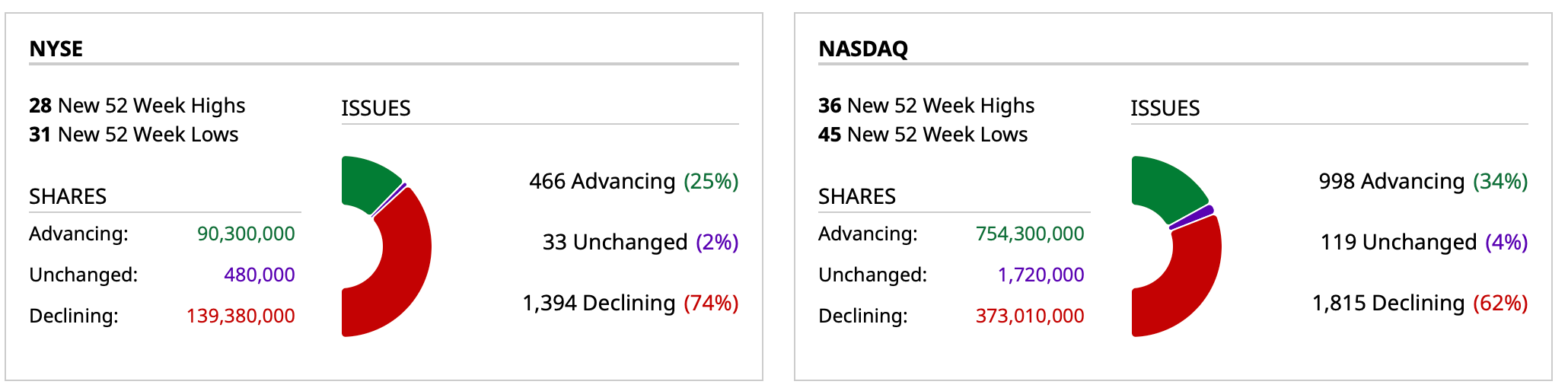

Breadth stinks, but that isn't new.

However, the advance/decline line is lackluster despite the rally off of the lows:

At 2:15 p.m. S&P cash is +3 handles. The RSP (equal weighted S&P) is -0.01% and IWM is -0.46%.

Not much trading as I had calls with three companies throughout the day.

Here are today's "Things":

* Three separate Index call shorts with S&P cash down 9, down 3 and unchanged.

* Added to MSOS at $3.22, TCNNF at $4.15 and TSNDF at $0.51.

* Sold BABA at $125.41 — out of name.

* Shorted more JPM at $280.04 and PLTR at $123.13.

BY Doug Kass · Feb 19, 2025, 2:30 PM EST

BY Doug Kass · Feb 19, 2025, 1:22 PM EST

jpiper

In the interests of transparency, why don't you just use the actual % the stock is of your portfolio? This should be a readily available number. This would be much more transparent than using L, S, M to determiine size, then somehow determining whether it is speculative or not, and then having your subscriber somehow determine how to make his trade somehow consistent with your own. Not to mention consistent with your commentary.

Dougie Kass

Reasonable question and I will give you a direct answer.

Everyone has a different risk appetite and many have different time frames.

As a result, giving percentages out (L, M and S) is far more descriptive and informative to the reader.

That is because what is large to a conservative investor is different from a large to an aggressive investor. We know where a L investment stands, we dont know what a 5% investment stands (because it means different things to different investors with differing risk profiles).

Also, mine is not a recommended list. I am showing you what stocks, why and at what price I am executing my trades and investments. I dont know anyone on our site that shows specific weightings (VL, L, M, S and VS) as I do - but I might be mistaken.

BY Doug Kass · Feb 19, 2025, 1:10 PM EST

* And keep them holy...

Six months ago homebuilder stocks were the rage — on the shows, in the sell-side research reports and in the business media.

Look at the charts since last summer...

That weakness may come to a chart near you!

BY Doug Kass · Feb 19, 2025, 12:25 PM EST

Housekeeping item.

I sold my Alibaba BABA at $125.41 for a sizeable gain.

BY Doug Kass · Feb 19, 2025, 12:07 PM EST

S&P cash bounces back to even. I'm adding further to short Index calls.

BY Doug Kass · Feb 19, 2025, 11:43 AM EST

From Charlie:

BY Doug Kass · Feb 19, 2025, 11:25 AM EST

- NYSE volume is 3% below its one-month average;

- Nasdaq volume is 7% above its one-month average

- VIX is up 2.41% to 15.72

BY Doug Kass · Feb 19, 2025, 11:15 AM EST

With S & P cash -9 handles I am adding to my short Index call position.

BY Doug Kass · Feb 19, 2025, 11:06 AM EST

calbear23

51 minutes ago

Dougie, do you have a stop loss on MSOS?

J

jpiper

4 minutes ago

Dougie doesn't use stops. And he's bullish on this name. Although there seems to be some question as to size. i dumped mine yesterday.

DK

Dougie Kass

STAFF

Just Now

agree, i dont use stop losses. i have weighted the position where i want it given its speculative nature.

there is no question about size.

large in a conservative equity is different than large in a speculative equity - that is familiar ground of investment management theory.

for similar reasons (and asymmetry of reward v risk) large in shorts is substantially smaller than large in longs...

And so on and so on and scooby-dooby-dooby

...Sly & The Family Stone - Everyday People (Official Video) - YouTube

BY Doug Kass · Feb 19, 2025, 11:00 AM EST

BY Doug Kass · Feb 19, 2025, 10:50 AM EST

With the Oscillator moving back from neutral to overbought, I expanded my individual equity short positions this morning.

BY Doug Kass · Feb 19, 2025, 10:42 AM EST

BY Doug Kass · Feb 19, 2025, 10:25 AM EST

From Peter Boockvar:

Housing starts in January totaled 1.366mm, below the estimate of 1.390mm and down from 1.515mm in December and vs 1.305mm in November and 1.344mm in October.

Single family starts fell back under one million at 993k from 1.084mm in the month before. Multi family starts were 373k vs 431k in December and 284k in November. They are much more volatile month to month relative to single family.

As for the forward looking permits, they were flat m/o/m with single family at 996k, no change from December. Multi family permits were 487k vs 486k in the prior month.

For perspective, the single family start count of 993k is about in line with the 12 month average of 1.012mm, the 2 yr average of 981k and 3 yr average of 989k. With multi family, the 373k figure compares with a one yr average of 355k, 2 yr average of 412k and the 3 yr average of 455k. It peaked at 627k in April 2022 so we can see the slowdown currently underway after record deliveries in 2024, particularly in the sunbelt.

Bottom line, the housing market needs more single family supply to mitigate the affordability challenges faced by many first time buyers but the price for that new home is itself an affordability challenge. With multi family, the permit pace of 487k is almost half the peak of 813k in February 2023 and points to a continued slowing pace of new supply after the delivery flood seen in 2024.

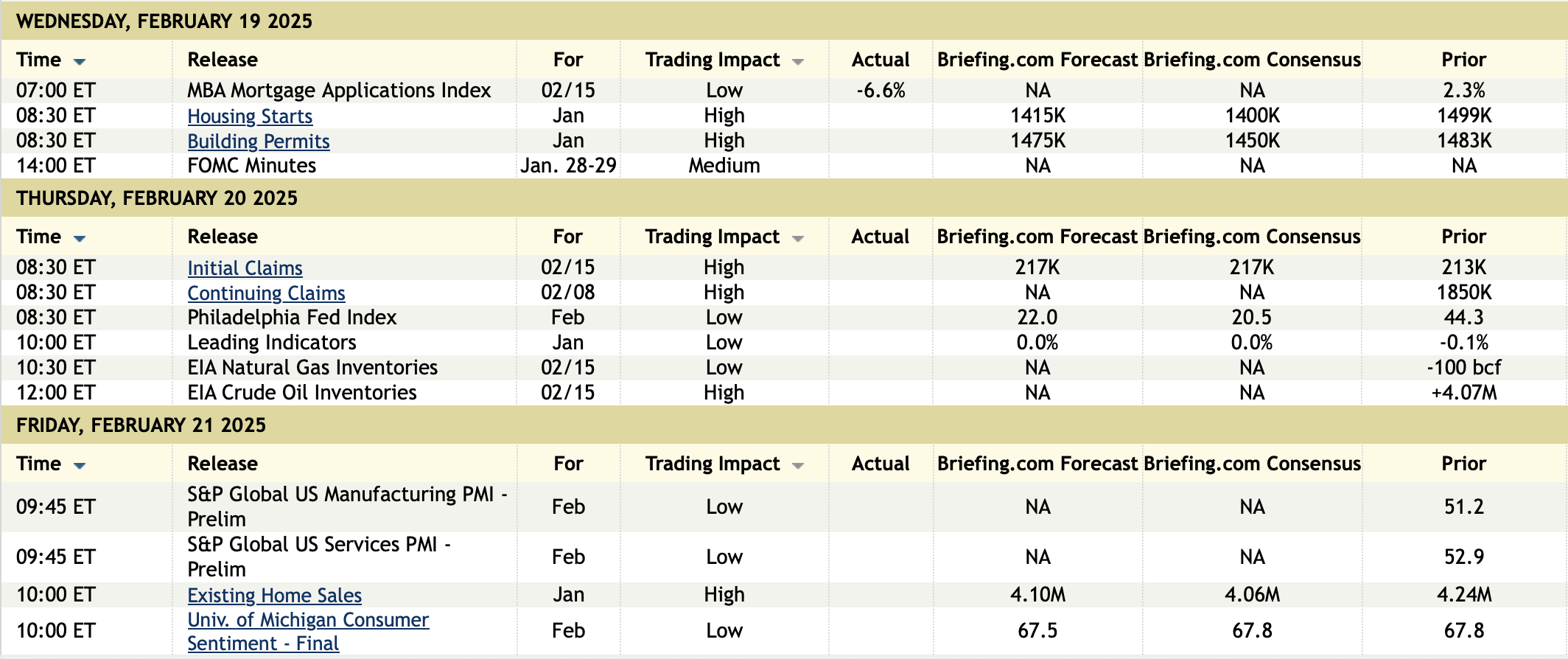

BY Doug Kass · Feb 19, 2025, 10:10 AM EST

Kdog88

Good morning Dougie…..did Rosie suggest what fair value of the S&P should be with real rates at 2%? Thanks.

Reply

Dougie Kass

STAFF

11 minutes ago

From Rosie:

"This is how crazy overvalued the S&P 500 is. The current 22x forward P/E multiple only makes rational sense in an environment where the 10-year TIPS yield is close to 0.2%, not 2.0%. We ran some regressions on the multiple against the real risk-free rate, and the equation spits out a fair-value 15.4x forward P/E multiple. We then went deep into the history books and found that when real rates were at today’s level, the multiple averaged out to be 16.6x. Valuations aren’t exactly a timing tool, and the market can be in a mania or price bubble for up to two years, rarely longer than that. It’s just useful to know that at this stage of the market cycle, investors jumping in now is akin to chasing nickels in front of a steamroller."

BY Doug Kass · Feb 19, 2025, 9:58 AM EST

BY Doug Kass · Feb 19, 2025, 9:45 AM EST

-SEDG +22% (earnings, guidance)

-ALZN +15% (completes Novel Head Coil by Tesla for Measuring Brain Structure Lithium Levels in Five Upcoming Phase II Clinical Trials at Massachusetts General Hospital)

-ROCK +8.1% (earnings, guidance)

-APPN +8.0% (earnings, guidance)

-GRMN +7.0% (earnings, guidance)

-SMCI +6.7% (momentum)

-ANRO +5.7% (announces U.S. Patent Granted Covering ALTO-300 as a Treatment for Patients with Major Depressive Disorder Characterized by an Electroencephalogram Biomarker)

-ENLT +5.0% (earnings, guidance)

-XFOR +4.8% (agrees to distribution and commercialization of XOLREMDI (mavorixafor) with taiba rare in WHIM Syndrome in Select Middle East Countries)

-ADI +4.6% (earnings, guidance)

-IONS +4.5% (earnings, guidance)

-POAI -19% (files to sell 363.3K shares at $1.50/shr in private placement)

-CE -15% (earnings, guidance)

-PERI -11% (earnings, guidance)

-PRG -11% (earnings, guidance)

-WWW -11% (earnings, guidance)

-FOUR -9.5% (earnings, guidance; to acquire specialty payment and tech provider serving luxury brands Global Blue for $7.50/shr cash)

-HRMY -9.2% (affirms FY25 Rev; received FDA refusal for pitolisant in treating idiopathic hypersomnia)

-GLBE -9.1% (earnings, guidance)

-WING -7.9% (earnings, guidance)

-ETSY -7.5% (earnings, guidance)

-CLVT -6.6% (earnings, guidance)

-KRYS -4.7% (earnings, guidance)

-LPX -4.6% (earnings, guidance)

-DEC -3.8% (launches 8.5M share underwritten offering)

-HHH -3.6% (confirms receipt of Revised Unsolicited Proposal from Pershing Square)

-APG -3.3% (earnings, guidance)

-CSGP -3.3% (earnings, guidance)

-OSW -3.2% (earnings, guidance)

-TOL -3.2% (earnings, guidance)

-CDNS -2.5% (earnings, guidance)

BY Doug Kass · Feb 19, 2025, 9:23 AM EST

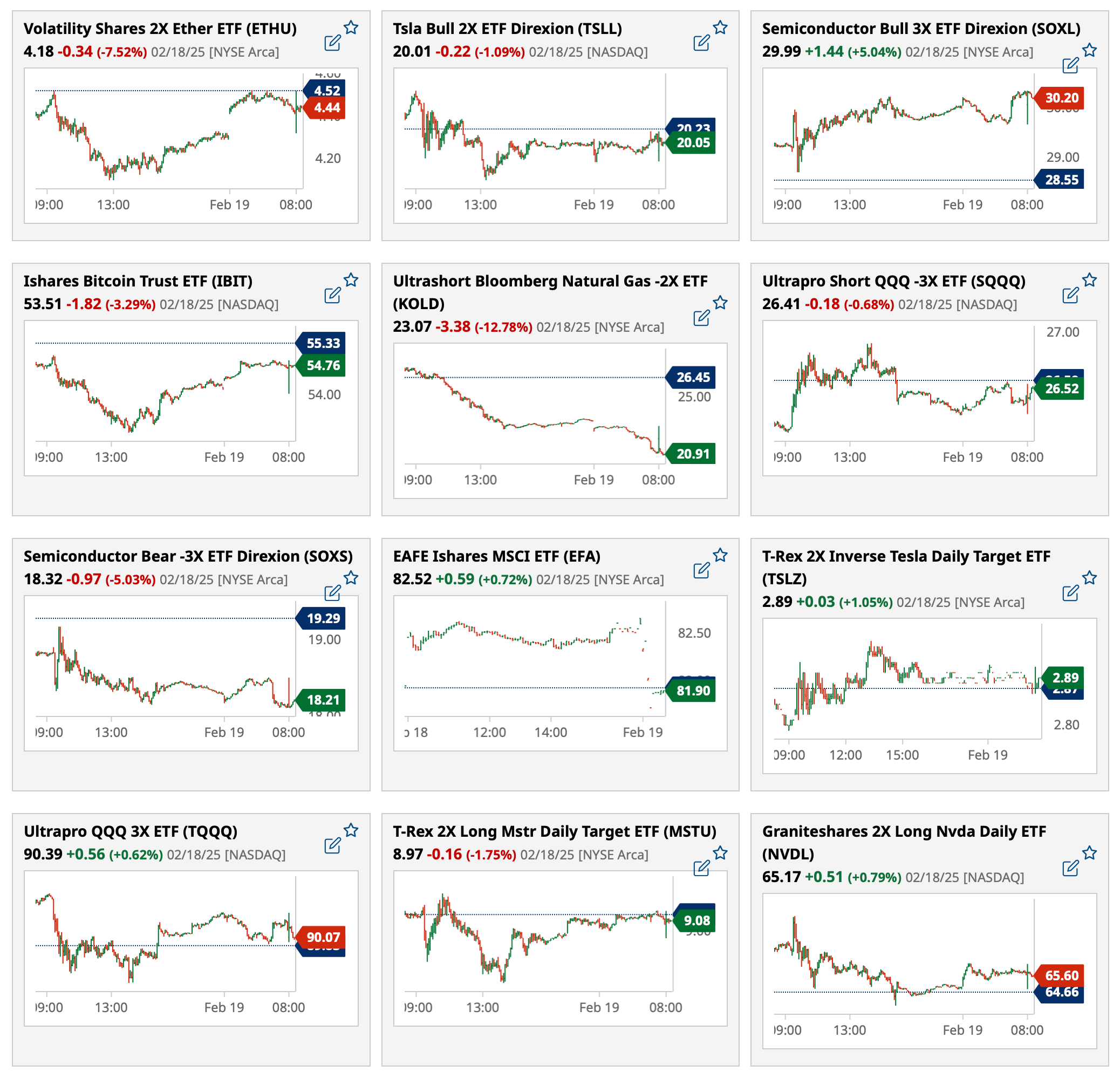

Most active premarket ETFs at 8:14 a.m. ET:

BY Doug Kass · Feb 19, 2025, 9:12 AM EST

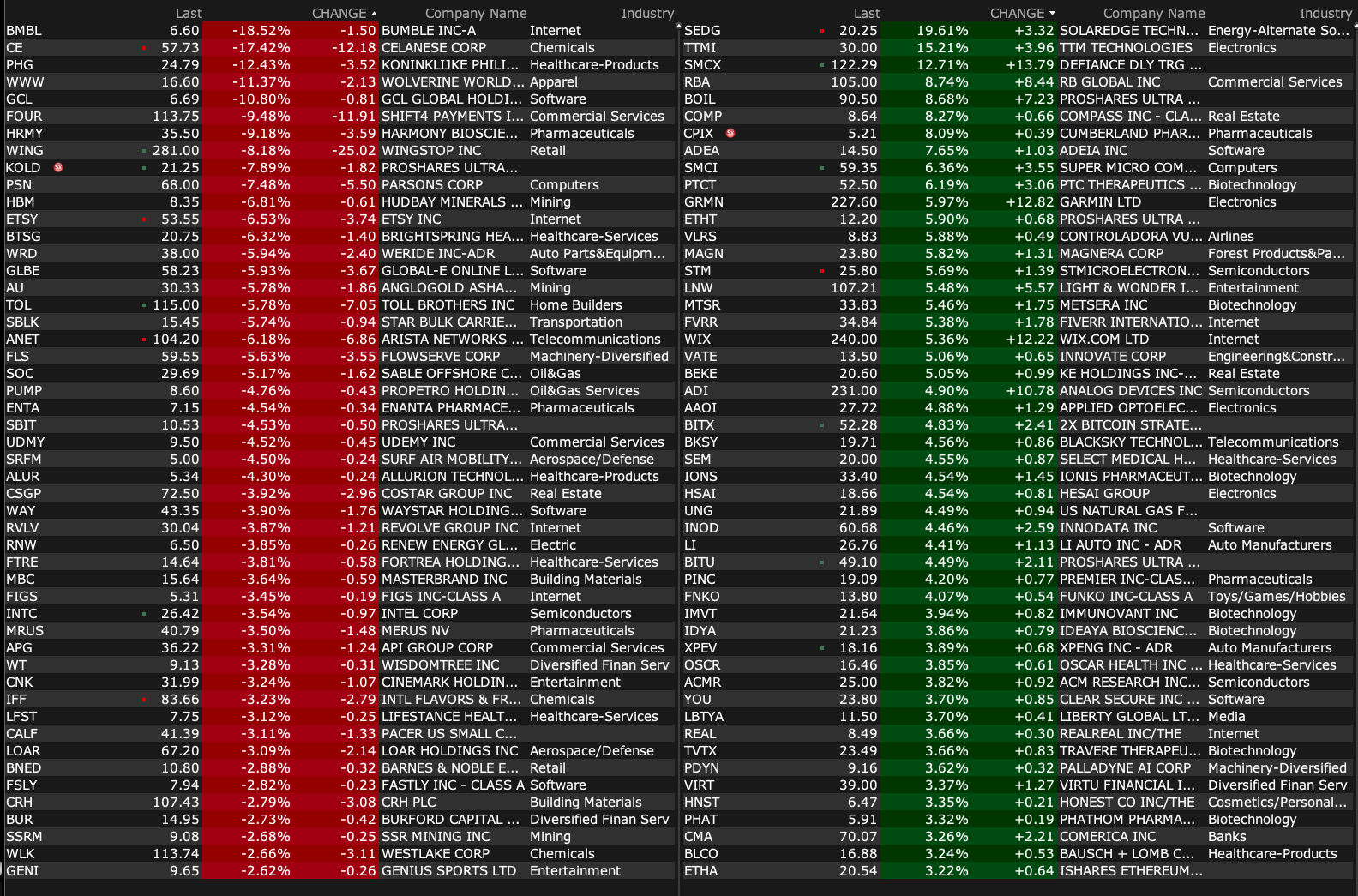

Premarket percentage movers at 8:35 a.m. ET

BY Doug Kass · Feb 19, 2025, 9:00 AM EST

BY Doug Kass · Feb 19, 2025, 8:56 AM EST

Yesterday I wrote about gold versus bitcoin:

I wonder when they find the vault depleted, if they blame Auric Goldfinger or Bob Menendez?

Is the price of gold going to rip after this one?

Nobody seems to have noticed, but for about the last three months gold is materially outperforming bitcoin.

Gold is making new highs and bitcoin is off its highs and stuck and is at the same price from late November last year:

https://www.dailymail.co.uk/news/article-14403697/gold-reserve-doge-audit-fort-knox-elon-musk.html

Feb 18, 2025 7:35 AM EST

Today, my pal Larry McDonald follows up and chimes in:

BY Doug Kass · Feb 19, 2025, 8:46 AM EST

From Peter Boockvar:

We know goods prices have been where most of the disinflation has taken place to the point where they are flattish y/o/y, the pace at which they were seen in the decades leading into Covid. Staying down though is the key. With used cars specifically you've heard me many times talk about the below trend amount of inventory because five years after Covid, new car sales are still trending below 2019. In case you didn't see this article in yesterday's WSJ titled "Why There is No Relief Ahead for High Used Car Prices" they said "Used-vehicle shoppers are finding stubbornly high prices at the dealership lot - if they can find a car at all...The number of vehicles coming back to dealers with expiring three year leases will drop 23% this year, to a decade low, according to Cox Automotive. It isn't expected to bounce back until 2027, forecasts show." https://www.wsj.com/business/autos/why-there-is-no-relief-ahead-for-high-used-car-prices-8d7617be?mod=itp_wsj. We are not yet in the inflation clear when looking out the next few years, and as I highlighted yesterday too with rents that are moderating still now but should shift higher again late this year and in 2026.

Also on the pricing front that caught my eye was in chemicals. This was from the Huntsman conference call yesterday:

After talking about the potential tariffs and how they are planning on managing through them, "The second shift we are seeing is around recent price announcements in many of our products...I think Huntsman remained incredibly disciplined with respect to pricing. We previously announced lost volume due to this. We've stated on past calls that demand needs to return before pricing picks up. As we have reported in the past few quarters we've seen volumes improve as de-inventorying has ceased and demand has tepidly returned. I believe that we're seeing some early signs of recovery in pricing and margins return."

"As of today, we are seeing publicly reported polymeric MDI prices in China at a three year high. Huntsman has also announced a series of price increases in North America as well. Again, as publicly reported, we have seen others pushing for similar actions. It is challenging to say if these actions will be successful and how soon and to what segments they will stick. However, as we sit here today, it is fair to say that there are more positive than negative movements in the MDI industry. My personal feeling is that MDI was one of the first major chemical chains to drop and may well be among those that show signs of recovery earlier than other chains."

According to Google Gemini, "Methylene diphenyl diisocyanate (MDI) is a highly reactive chemical used to make polyurethane materials."

The industry is not out of the woods though. Celanese, a chemical company on the specialty side, is down sharply pre market after they reported yesterday. In their release they said "Persistently weak global demand in critical end-markets like automotive, paints, coatings, construction and industrials caused headwinds throughout the year." And they also said they expect "the sequential demand and pricing challenges experienced in the fourth quarter to be largely unchanged in the first quarter."

Specifically on the residential construction side, Toll Brothers is down pre market as they missed delivery numbers and said this:

"Although demand has remained healthy in many of our markets and particularly at the higher end, affordability constraints and growing inventories in certain markets are pressuring sales - especially at the lower end. We continue to strategically manage our pricing, incentives and spec starts on a community-by-community basis to best match local selling conditions and to appropriately balance pace and price."

With respect to broader construction trends in the US, the January Architecture Billings Index remained well below 50, though rose 1 pt to 45.6 m/o/m. All four of their components are below 50 which consists of commercial/industrial, industrial, multi family residential and mixed practice. The chief economist there said "Stubborn inflation, persistently high interest rates, and labor concerns continue to weigh on the willingness of owners and developers to move ahead with construction projects. Architecture firms have been moving to right size their operations in response to softer market conditions. There was a net loss of 1,400 positions at architecture firms nationally in 2024, and firm employment has declined by a total of 4,100 positions since the post pandemic peak in June 2023."

Also, tariffs are a worry of the industry, particularly in residential construction has heard from the NAHB yesterday in their home building survey. "Uncertainty on the tariff front helped push builders' expectations for future sales volume down to the lowest level since December 2023. Incentive use may also be weakening as a sales strategy as elevated interest rates reduce the pool of eligible buyers."

"With 32% of appliances and 30% of softwood lumber coming from international trade, uncertainty over the scale and scope of tariffs has builders further concerned about costs" said the NAHB.

Affordability challenges continues to be seen in the weekly mortgage applications data as purchases fell by 5.9% w/o/w, down for a 4th straight month to the lowest since early January. Refi's were down by 7.3% w/o/w but after rising by 9.6% in the week before.

From Vulcan Materials, the aggregates maker, which continues to have some mixed end markets. They are benefiting from public sector spending but subject to the slowdown in private residential construction, offset by data center growth:

"Over the last year, trailing 12 months, highway starts have increased by another $7 billion to $122 billion...Additionally, $45 billion of funding initiatives were passed at the state and local level in recent election cycle to spur additional transportation in local states."

On the other hand, "Affordability and elevated interest rates remain headwinds for residential construction activity."

But, "Recent trends in both warehouse starts and data centers have been encouraging. Trailing 12 month warehouse starts, the largest category in private non-residential construction have continued to flatten out to pre-pandemic levels after a precipitous drop from historic highs throughout 2023."

"Current planned data center activity in our markets remains robust."

Fluor Corp is benefiting from government help and data centers too. "On the semiconductor front, based upon our project performance, a major semiconductor manufacturer in Arizona has awarded Fluor more tool installation work." I'm guessing it was TSMC. "Growing our experience in tool installed scopes, like this one, positions us well for future semiconductor opportunities in the US."

"In addition, we've recently signed a master agreement with a leading technology provider and have received initial data center work under this agreement."

They are also exposed to the metals and mining business. "For 2025, we see a continued focus by our clients on developing additional capacity for key resources, including copper, green steel, lithium and iron ore."

And infrastructure too as they are building out I-635 LBJ project in Texas and an LAX automated people mover project.

I'm pointing out all of the above to highlight again the mixed and uneven pace of US economic growth where most of the strength is coming from government spending and incentives, AI spend and upper income spending and it's much more choppy elsewhere.

More on the choppy side. This was from Expeditors International yesterday, the freight broker:

"We continue to have limited visibility going forward. It is extremely difficult to predict the impact to global air supply and demand that may result from actions such as the anticipated US elimination of certain de minimis exemptions. So, too, whether recessed Red Sea hostilities will lead to resumed ocean transit via that route remains to be seen. Geopolitical words and actions are driving disruption at a faster pace than we can ever recall, and national policies regarding tariffs and other similar measures are highly unclear in many countries around the globe."

Quickly overseas. Following the RBA rate cut the other day, the Reserve Bank of New Zealand cut 50 bps to 3.75% as expected.

Of note in China, home prices continued to fall in January but the pace of declines are still slowing giving hope that a bottom is near.

Japan said its January exports rose 7.2% y/o/y, about in line with the estimate of 7.7% while imports jumped by 16.7%, almost double the estimate of up 9.3%. What was front loaded and what was not ahead of possible tariffs is unknown in this data.

In the UK, January CPI rose 3%, above the estimate of 2.8% and up from 2.5% in December. The core rate was higher by 3.7% y/o/y but as expected vs 3.2% in the month before with services inflation growing by 5%. The wholesale data, both input and output prices, were above expectations. In response, the 10 yr inflation breakeven is higher by 2.6 bps to 3.54% but flat on the year. Gilt yields are higher but European bond yields are higher across the board as are global yields, again.

BY Doug Kass · Feb 19, 2025, 8:38 AM EST

* This morning...

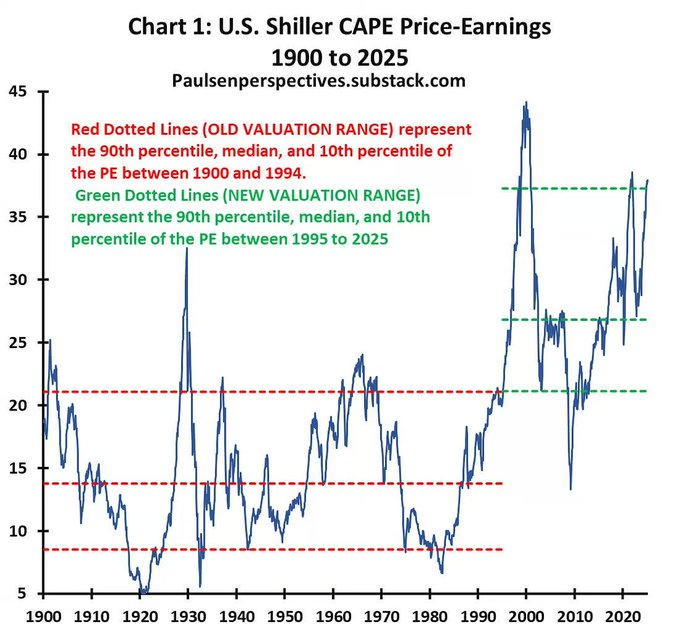

S&P 500 Seems to Think Real Interest Rates Are 0.2% Instead of 2.0% (Same Digits but in the Wrong Order)

BY Doug Kass · Feb 19, 2025, 8:23 AM EST

BY Doug Kass · Feb 19, 2025, 8:16 AM EST

BY Doug Kass · Feb 19, 2025, 8:05 AM EST

I shorted more (very small) Palantir PLTR in the premarket this morning:

BY Doug Kass · Feb 19, 2025, 7:53 AM EST

For those that didn't see this update yesterday afternoon, I wanted to repost:

* Updating my market outlook...

What goes up must come down

Spinning Wheel got to go 'round

Talkin' 'bout your troubles

It's a cryin' sin

Ride a painted pony

Let the Spinning Wheel spin

You got no money, you got no home

Spinning Wheel all alone

Talkin' 'bout your troubles and you

You never learn

Ride a painted pony

Let the Spinning Wheel turn

- Blood, Sweat and Tears, Spinning Wheel

What follows is a short compilation of recent commentary in my Daily Diary on TheStreet Pro and comments delivered to my investors at my hedge fund, Seabreeze Partners:

I continue to be deeply skeptical of the market's advance and I am maintaining our cautious investment strategy in the belief that equities are braced for a decline this year.

We believe that we are close to 2025's high in the averages and that downside is now roughly 3x the upside.

Investors should now be fearful of the excessive market optimism.

Nine days before the 1929 stock market crash that led to the Great Depression, Dr. Irving Fisher, an economist at Yale University, famously said (at the Purchasing Agents Association Dinner in New York City):

“Stock prices have reached what looks like a permanently high plateau.”

Fisher's prediction is considered one of the most notorious stock market forecasts of all time. The market's crash cost Fisher much of his wealth as well as his academic reputation.

Coincident with two back-to-back +20% annual returns in the S&P Index, a developing and confident bullish market narrative has emerged — which is eerily reminiscent of Dr. Fisher's 1929 comments:

Despite the near universal optimism in investor sentiment (as expressed in historically low cash reserves and most classical metrics and valuations above the 95% tile) there are rarely new eras — excesses are never permanent.

As noted last month, I remain of the view that we are not in a new (and permanently high) valuation paradigm for equities and that an important top in the U.S. stock market may be close at hand:

December marked the beginning of what we expect to be a lower-trending market accompanied by rising volatility.

We expect 2025 to look far different than 2024.

While we predominantly focus on an assessment of reward vs risk on individual stocks — if we were forced to hazard a precise forecast we would project only about a five percent upside and a ten to fifteen percent downside for the S&P 500 Index in 2025.

Today's commentary will explain why heady valuations are rarely a good launching pad for higher stock prices.

We will explore and summarize some of our fundamental near and intermediate-term concerns.

We will compare today with early 1973 (which marked the end of the Nifty Fifty era) and produced years of subpar returns for the major market averages. Then, we will highlight some longer-term existential market threats that few discuss, but that have a reasonable chance of emerging.

Finally, we will explain why the numerous uncertainties and headwinds provide a fertile basis for investors to prosper (absolutely and on a relative basis) in searching for asymmetric investment opportunities — and why a top-heavy, technology-led market (which has not broadened) has already begun to deliver some developing long opportunities with upside rewards that dwarf downside risks.

As I also recently wrote:

Many of our fundamental concerns (growing policy (fiscal and monetary) risks, sticky inflation, slowing economic growth and rising interest (higher for longer)) are finally beginning to be accepted by investors — at a point in time in which valuations are elevated and consensus corporate profit estimates seem too optimistic. We are increasingly more confident that stocks will correct to more attractive levels than exist right now — at which time we can begin to accumulate selected stocks that meet our investing criteria and standards.

By Doug Kass Feb 18, 2025 12:50 PM EST

BY Doug Kass · Feb 19, 2025, 7:30 AM EST

BY Doug Kass · Feb 19, 2025, 7:15 AM EST

From the keen-sighted Keith at Hedgeye:

The market doesn't care right now but if I and others are correct in view, it will — in the fullness of time.

BY Doug Kass · Feb 19, 2025, 6:55 AM EST

BY Doug Kass · Feb 19, 2025, 6:40 AM EST

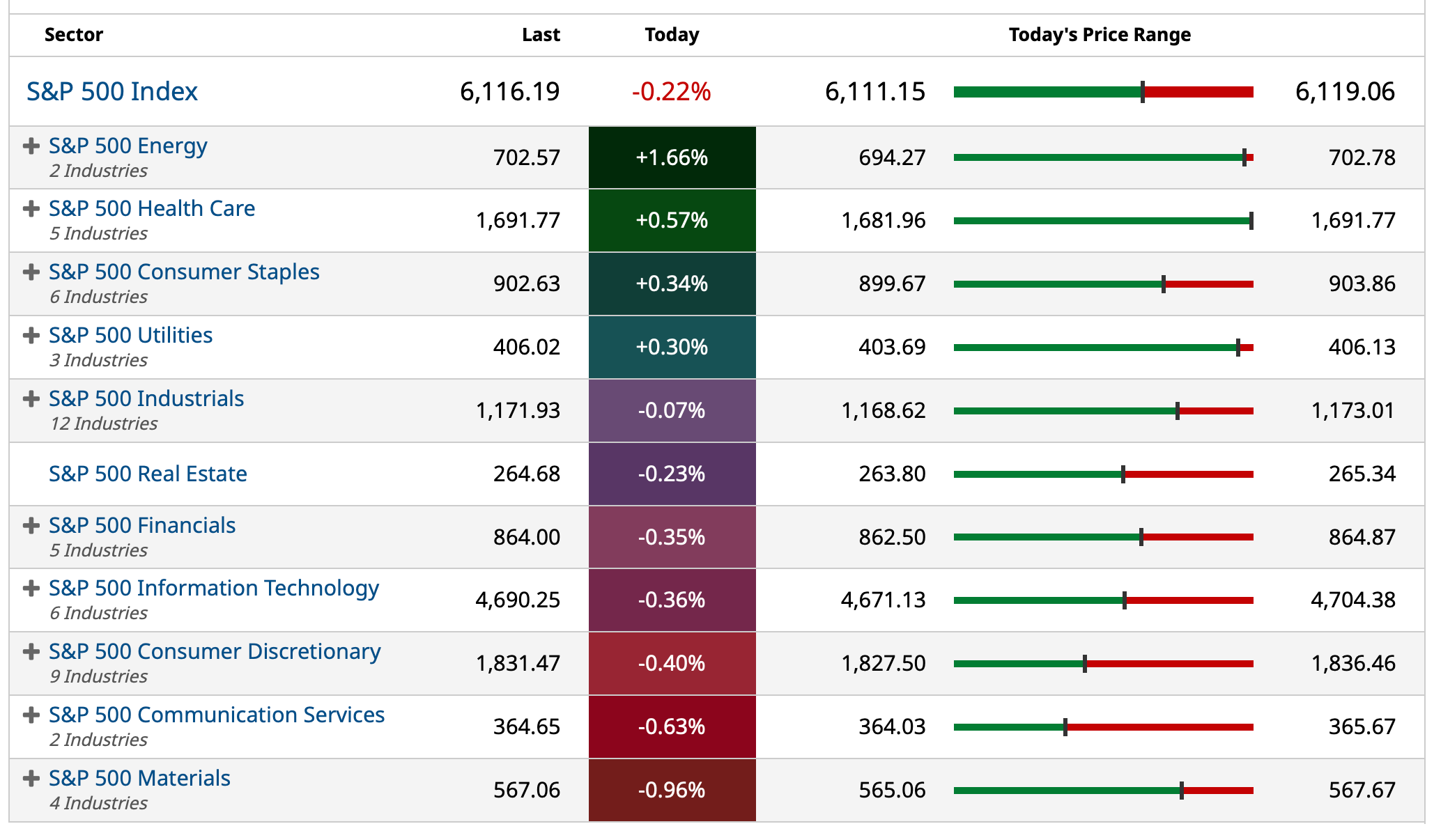

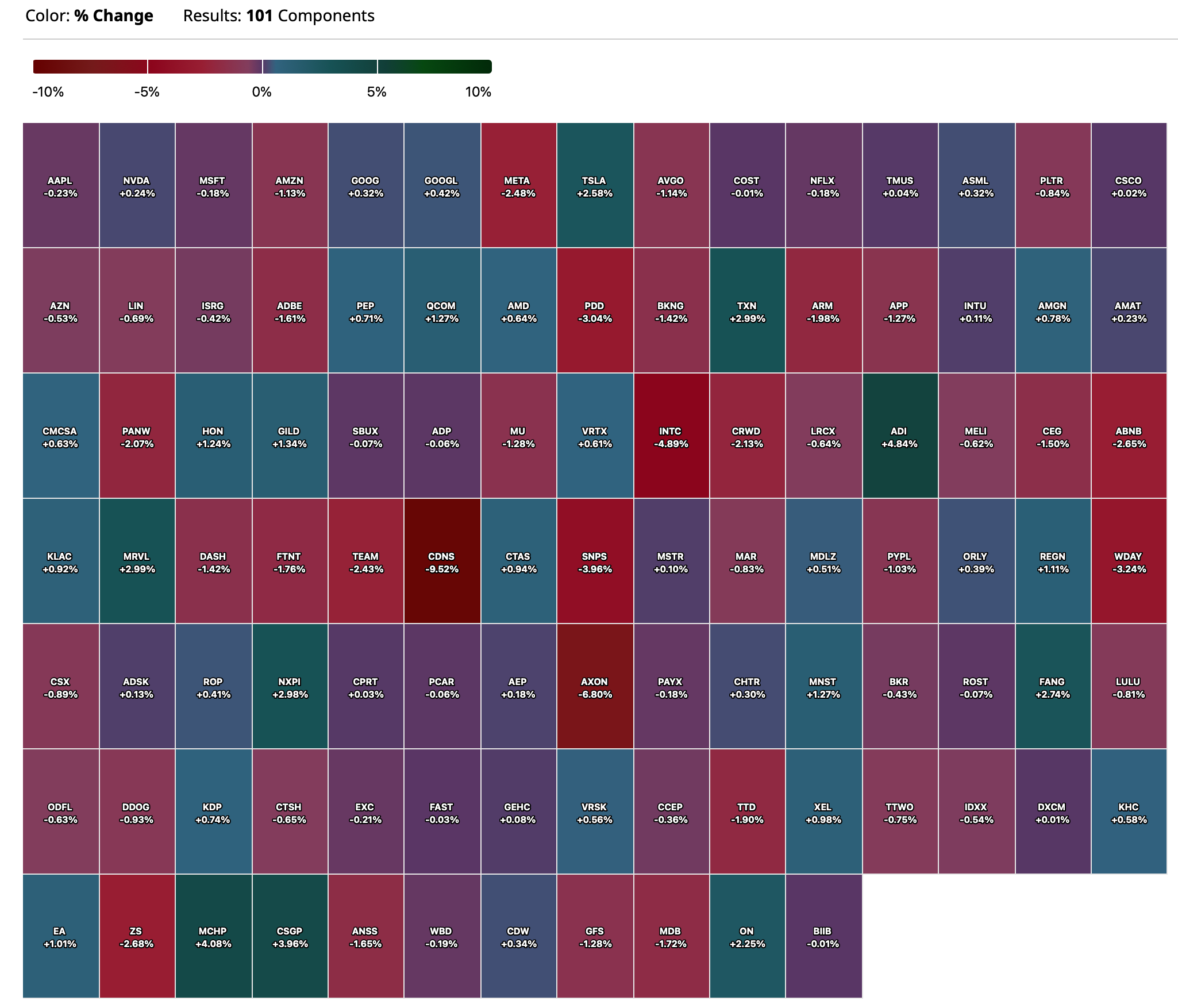

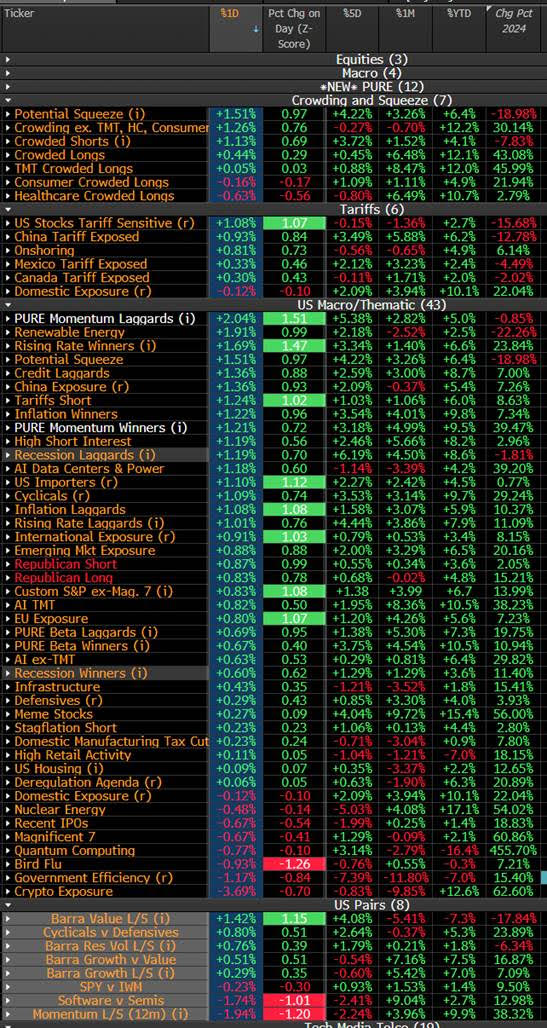

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Feb 19, 2025, 6:25 AM EST

From JPMorgan:

US: Futs are lower, having flipped negative following the hawkish UK inflation print and bond yields move higher; this follows new ATHs for SPX, NDX. Trump raises the specter of 25% tariffs on Autos and Pharma, both coming ~April 1. The Trump Admin will also keep Biden-era rules on M&A. Pre-mkt, Mag7 names are mixed with Semis seeing some profit-taking. The yield curve is twisting steeper as USD appreciates. Cmdtys are stronger despite the USD move. Today’s macro data focus will be on Housing data and the Fed Minutes.

and...

EQUITY AND MACRO NARRATIVE: Yesterday, was a quiet start to the holiday-shortened week. Stocks closed higher with RTY leading and NDX lagging. 70% of SPX stocks closed higher with major underperformers coming from Mag 7 (MTA -2.8%, AMZN -0.9%). JPM TMT trader Stuart Humphrey tells us that: “While we have not seen any supply [of MegaCap Tech] here, we've seen some covering/outright demand in other parts of TMT - we have seen LO demand in Semicaps (which have been most recently a relative short on China exposure), as well as some buying in higher-quality large cap software (have seen this demand here all year), and honestly have been better to buy in most semis ex-AVGO. For what it's worth this seems to be a consistent theme across the street per our conversations.”

BY Doug Kass · Feb 19, 2025, 6:15 AM EST

The S&P Short Range Oscillator has risen from 1.76% to 3.00% — thus, much more overbought.

BY Doug Kass · Feb 19, 2025, 6:05 AM EST

BY Doug Kass · Feb 19, 2025, 5:55 AM EST

BY Doug Kass · Feb 19, 2025, 5:45 AM EST

Who is confirming that gold wasn’t stolen from Fort Knox? Maybe it’s there, maybe it’s not. That gold is owned by the American public! We want to know if it’s still there.

As a U.S. senator I’ve tried repeatedly to get into Fort Knox Fort Knox: “You can’t come to Fort Knox.” Me: “Why?” Fort Knox: “It’s a military installation.” Me: “I’m a senator; I go to military bases all the time.” Fort Knox: “You still can’t come. Because, you can’t.”