Friday's Closing Market Stats

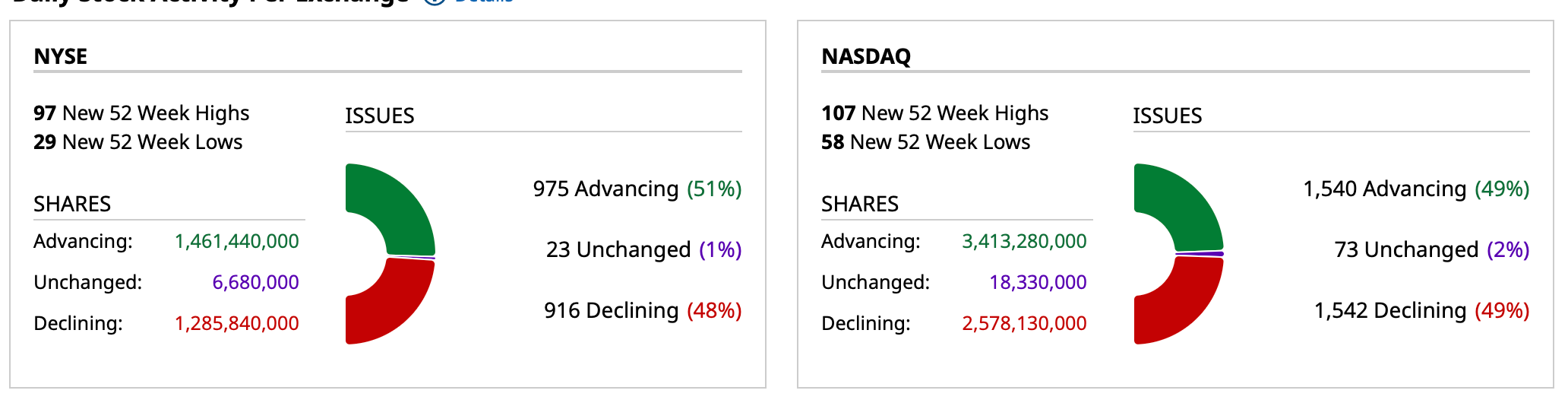

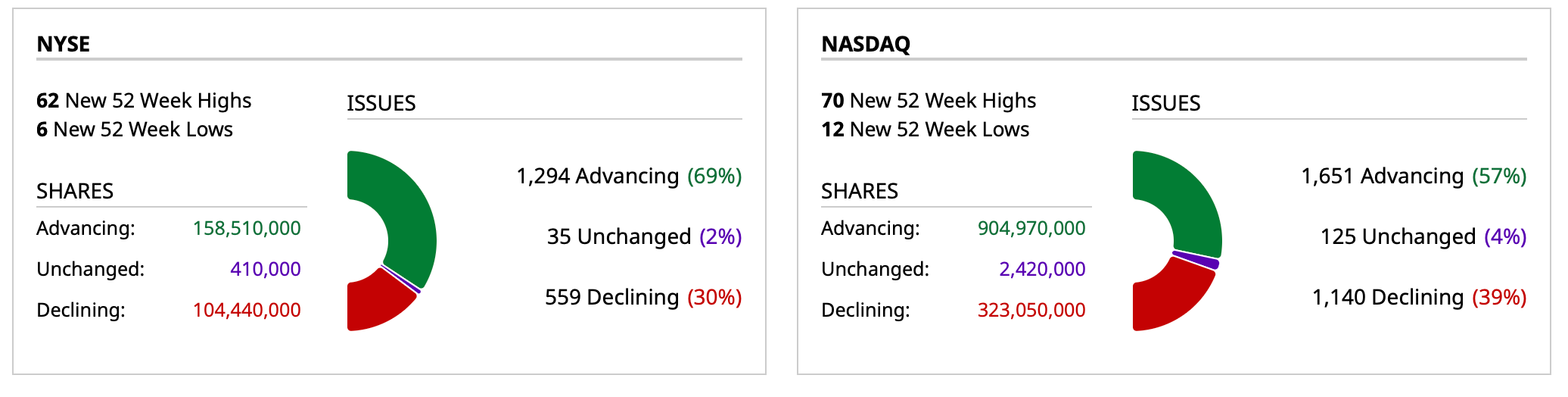

Breadth

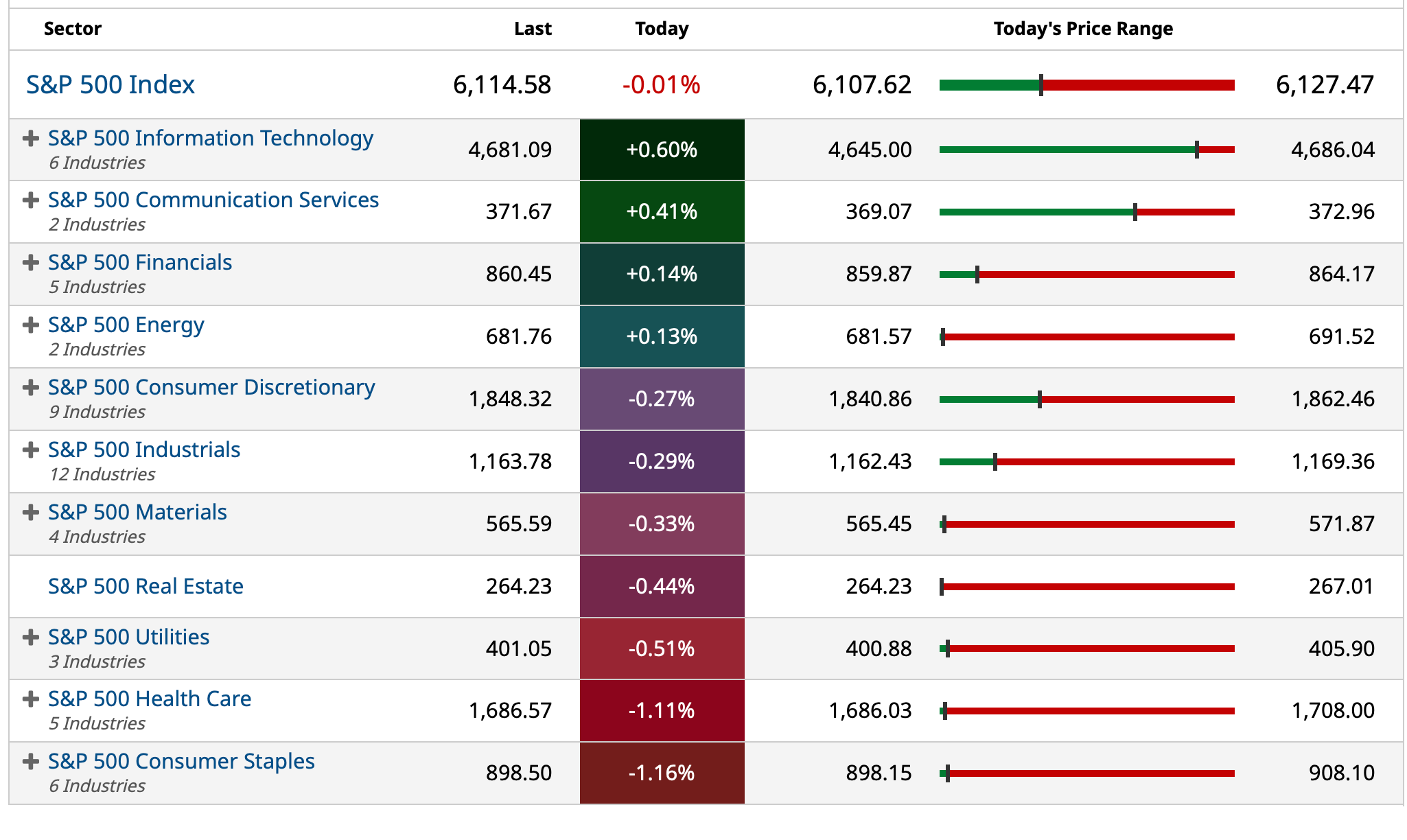

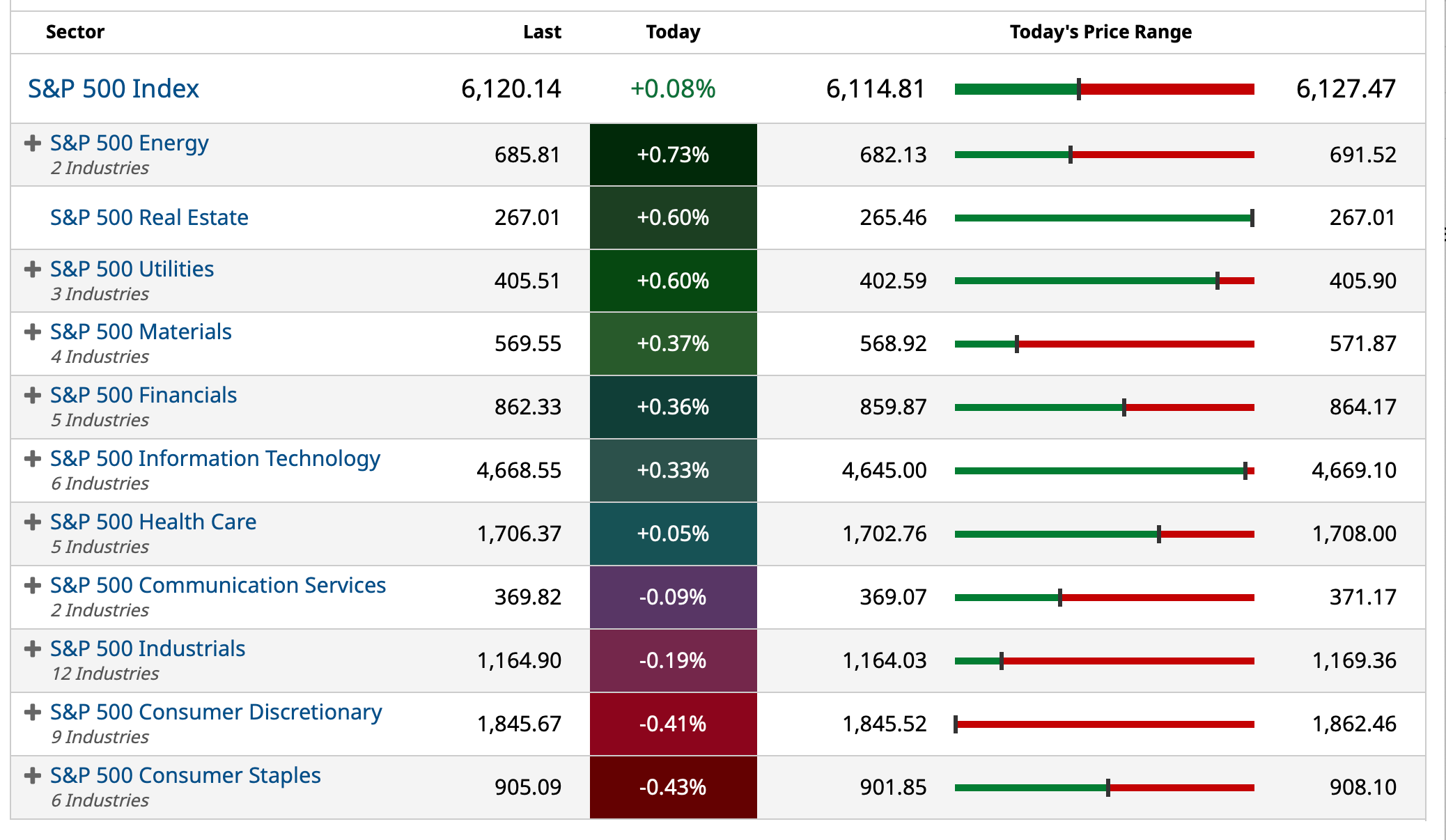

S&P 500 Sectors

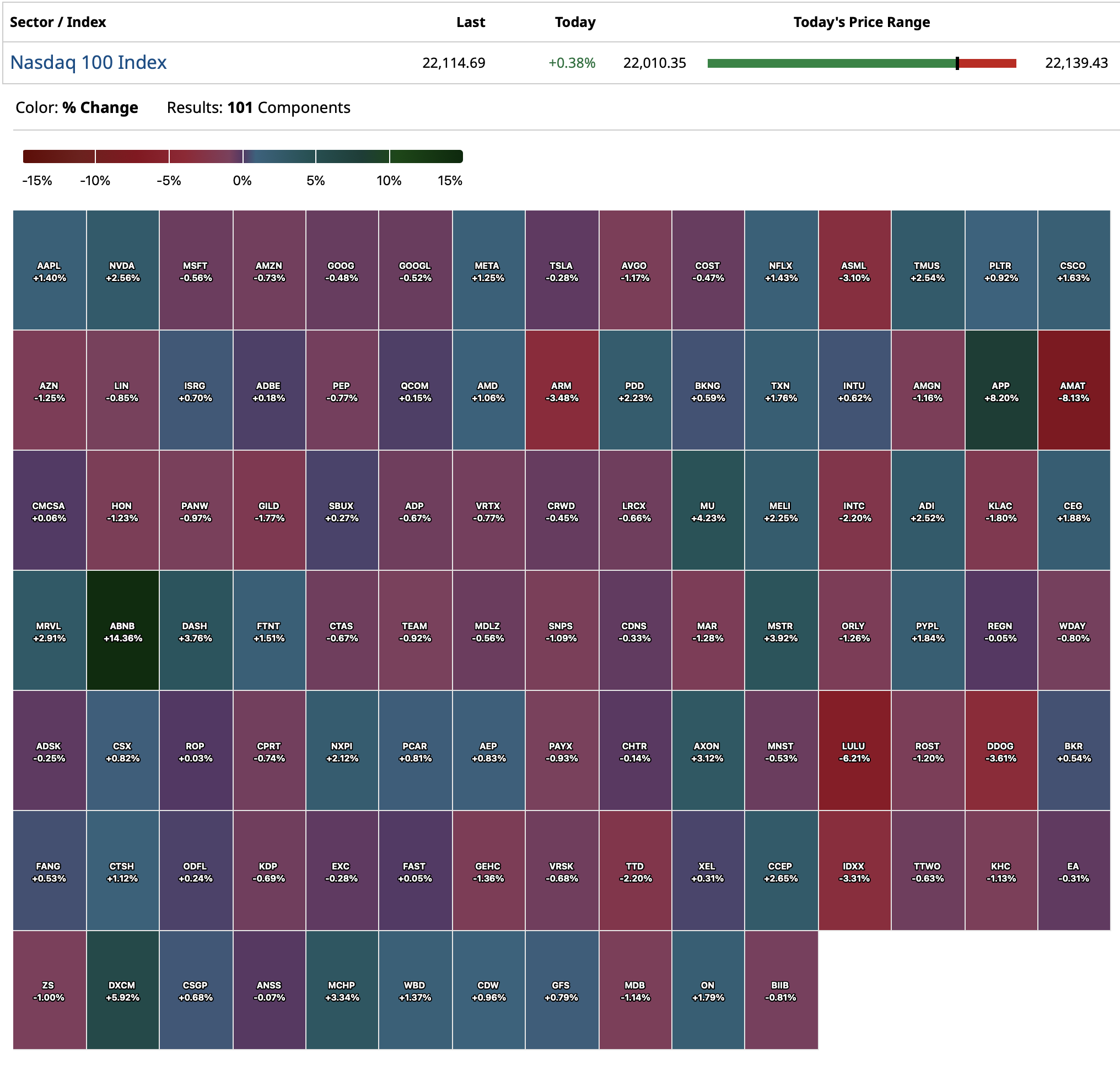

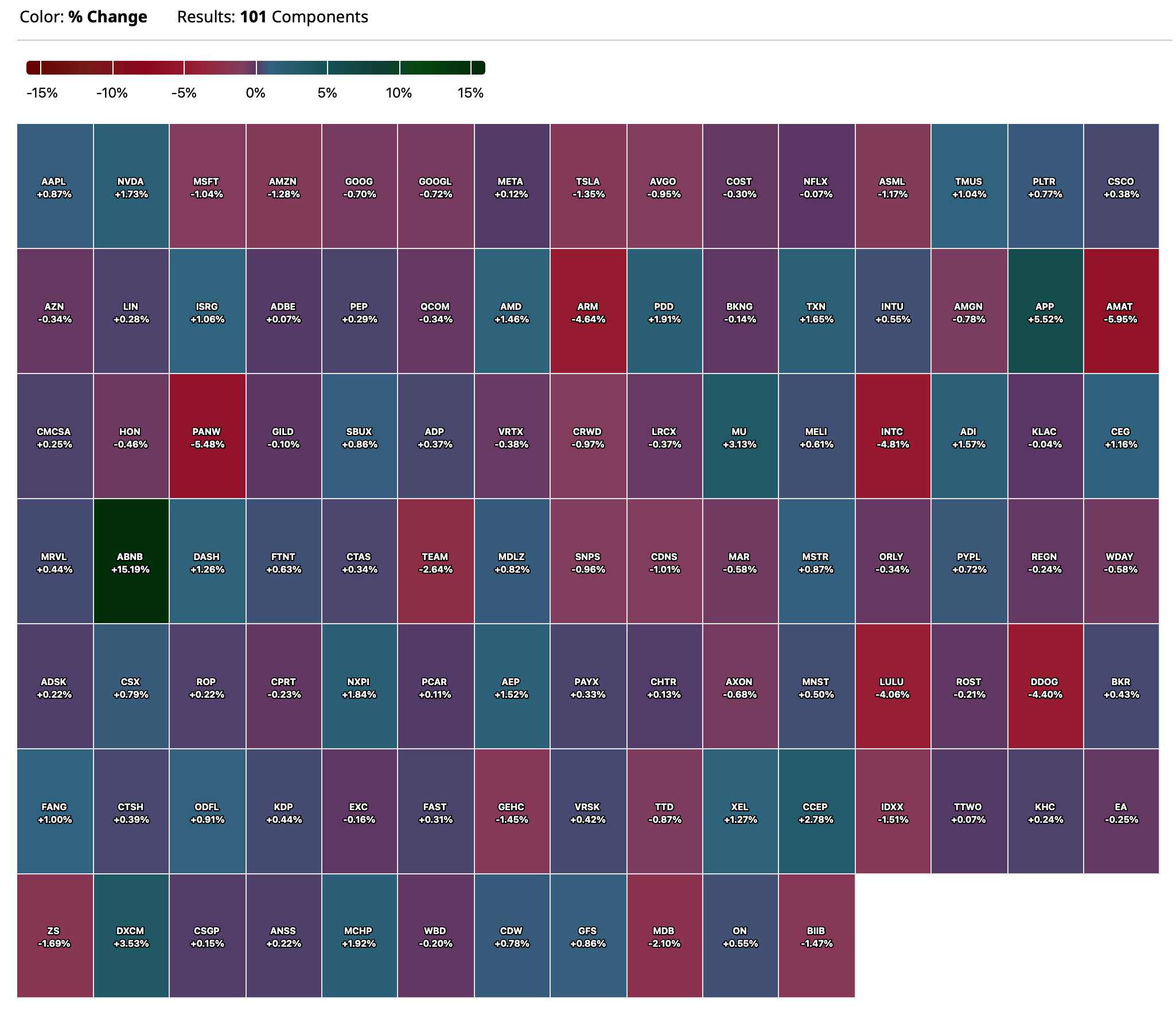

Nasdaq 100 Heat Map

BY Doug Kass · Feb 14, 2025, 4:50 PM EST

BY Doug Kass · Feb 14, 2025, 4:50 PM EST

To all our subscribers, editors and contributors — Happy Valentine's Day!

BY Doug Kass · Feb 14, 2025, 3:00 PM EST

I have taken a starter short position in ARKK at $66.60.

BY Doug Kass · Feb 14, 2025, 2:35 PM EST

BY Doug Kass · Feb 14, 2025, 2:21 PM EST

With S&P cash +6 handles I am adding to my short Index calls and selected individual shorts.

BY Doug Kass · Feb 14, 2025, 2:10 PM EST

I will be on a research call from 1:45 PM to about 2:30 PM.

BY Doug Kass · Feb 14, 2025, 2:00 PM EST

Scott Galloway's No Mercy No Malice: "Elon Musk, Welfare Queen"

BY Doug Kass · Feb 14, 2025, 1:00 PM EST

From Barron's - "The Dot-Com Bubble Burst 25 Years Ago, AI Could Be Next."

BY Doug Kass · Feb 14, 2025, 12:40 PM EST

After today's additional shorts, I am now at my largest net short exposure in a number of months.

BY Doug Kass · Feb 14, 2025, 12:30 PM EST

- NYSE volume is 2% below its one-month average;

- Nasdaq volume is 17% above its one-month average

- VIX: down 0.46%to 15.03

BY Doug Kass · Feb 14, 2025, 12:15 PM EST

BY Doug Kass · Feb 14, 2025, 12:02 PM EST

BY Doug Kass · Feb 14, 2025, 11:48 AM EST

BY Doug Kass · Feb 14, 2025, 11:25 AM EST

From Peter Boockvar:

Positives,

1) Initial jobless claims fell to 213k from 220k and that was 3k below expectations while last week was revised up by 1k. The 4 week average is now 216k vs 217k last week. Continuing claims, delayed by a week in its reporting, fell to 1.85mm from 1.872mm but still around 3 1/2 year highs.

2) When including the slight upward revision to December, January import prices were as expected. On a y/o/y basis, import prices are up 1.9% and by 1.2% y/o/y ex food and fuels. The stronger dollar is helping to keep a lid on import prices.

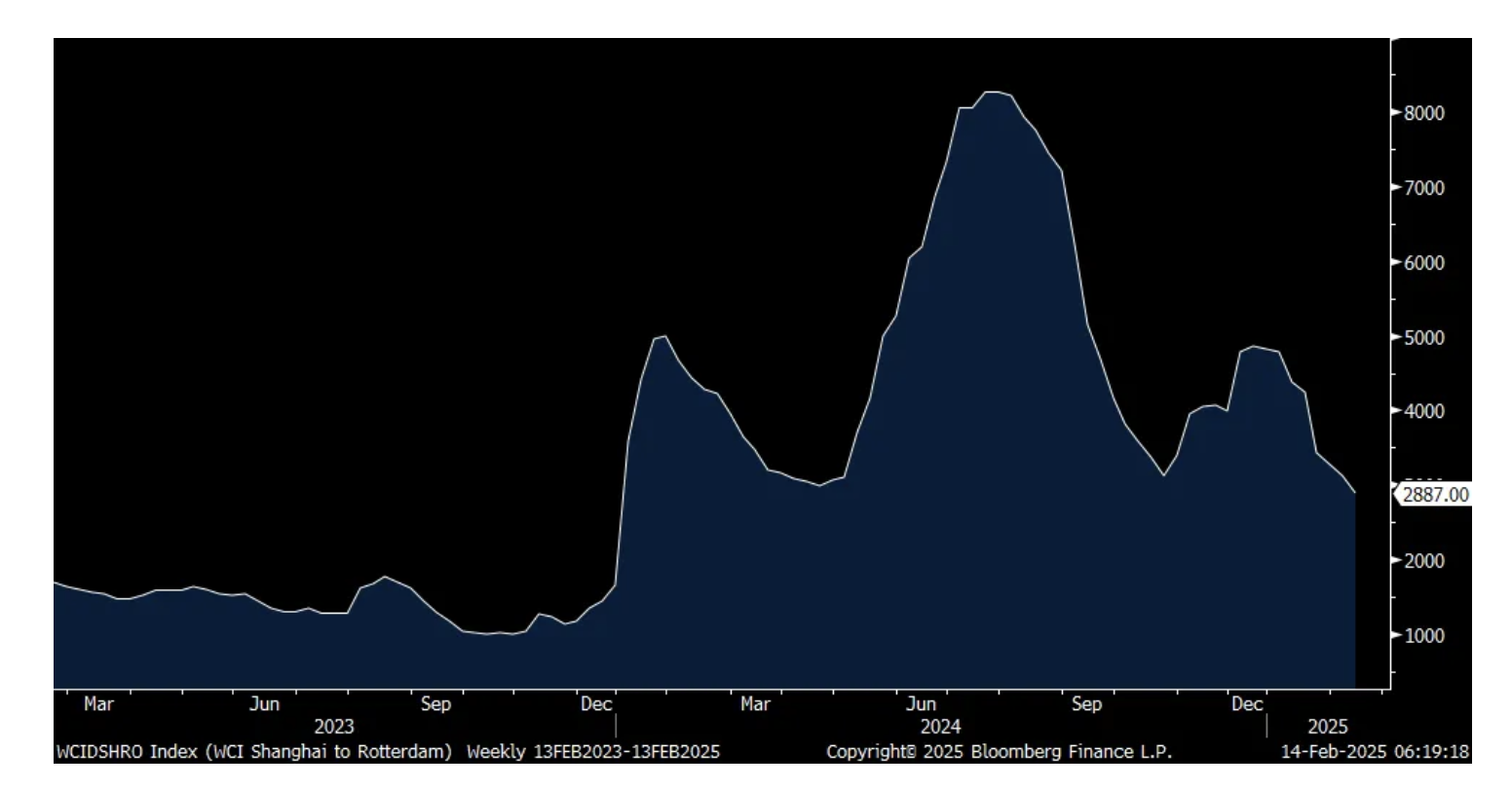

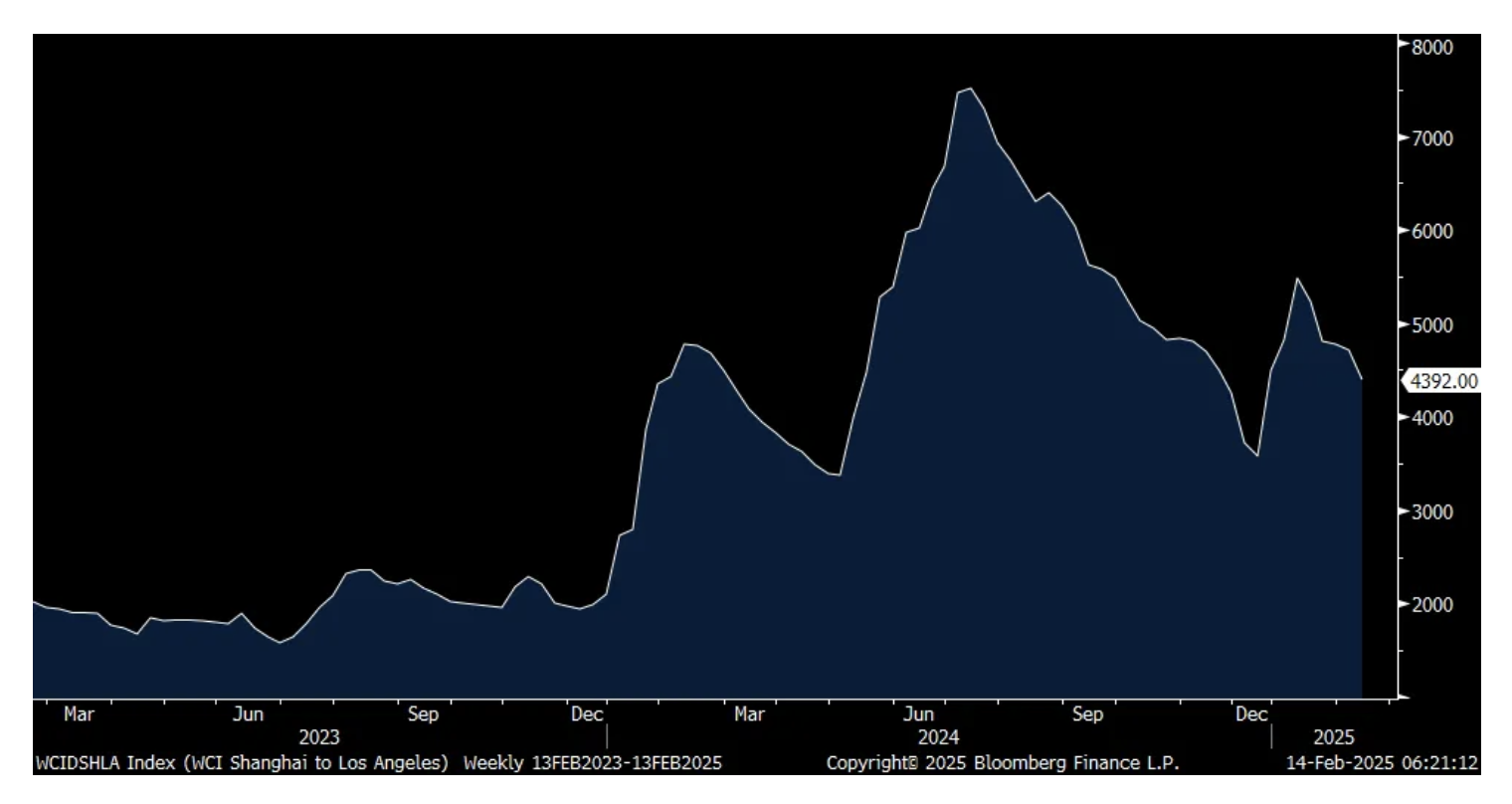

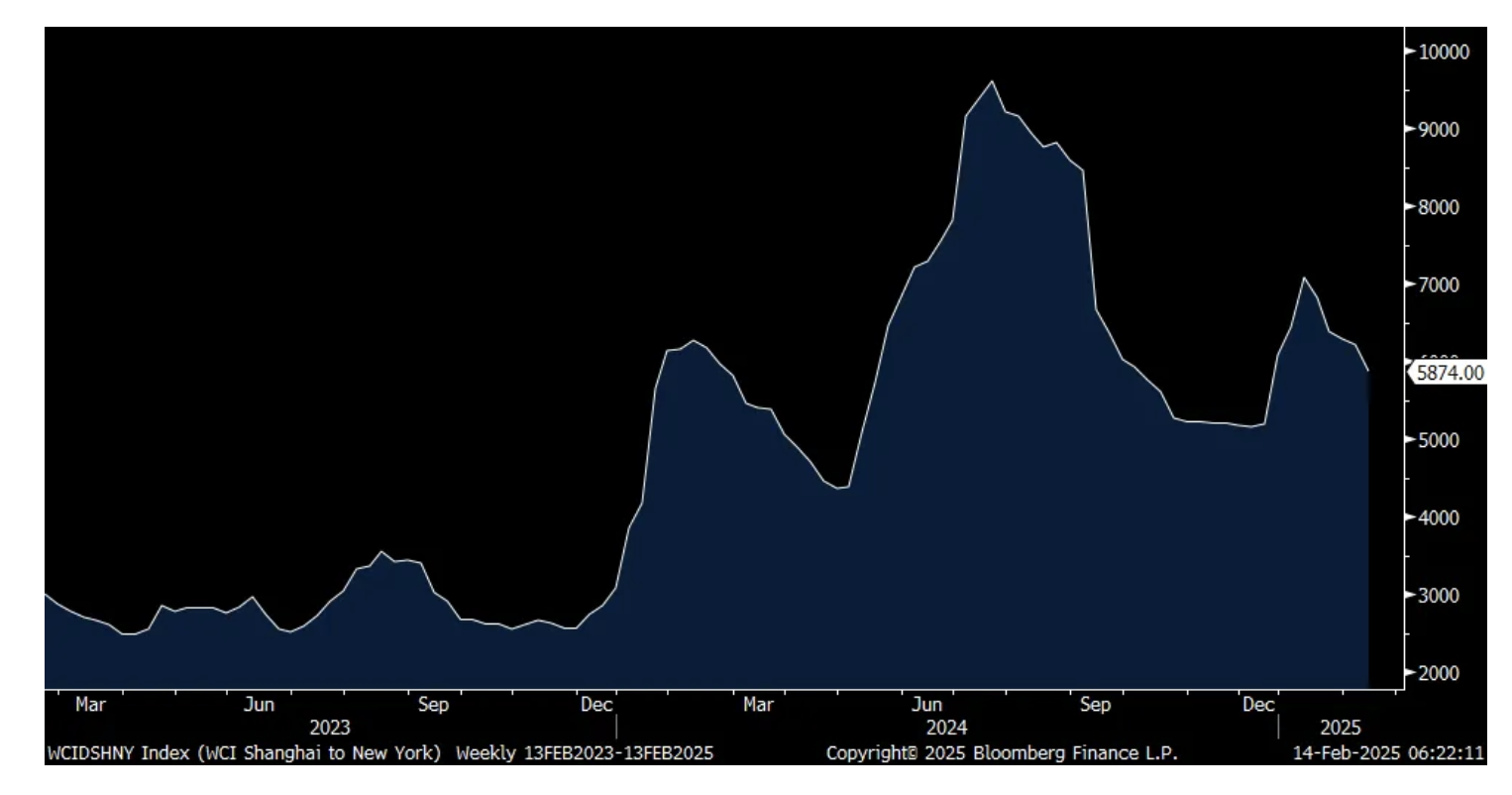

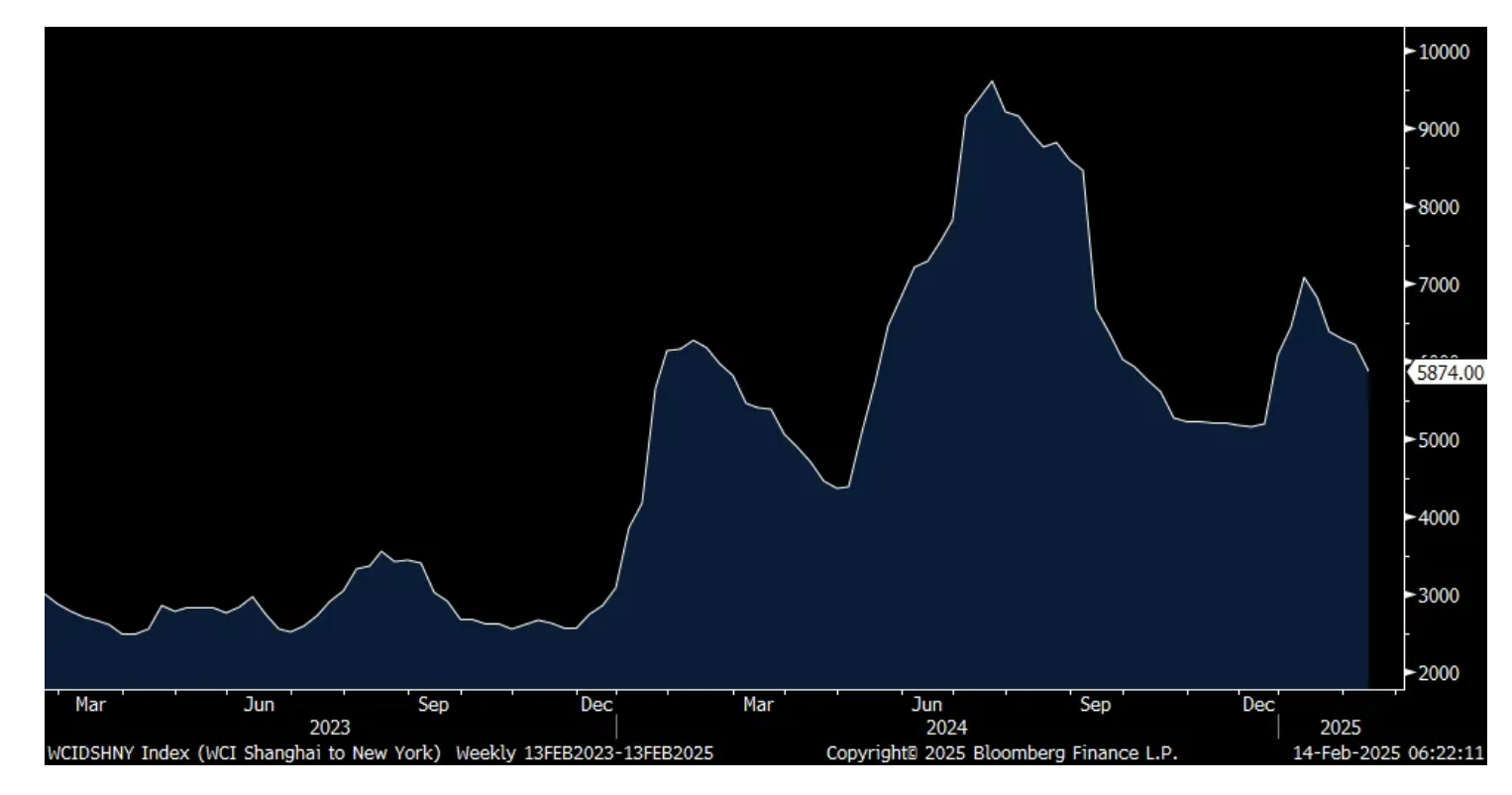

3) The Shanghai to Rotterdam trip for a 40 foot container now costs $2,887, which is down for an 8th straight week and to the lowest level since the beginning of 2024. Shanghai to LA costs $4,392, down from its highs but not as much as the Rotterdam route as it is at the lowest since December 2024 and still more than double where it was in January 2024. The Shanghai trip to NY is also more than double the January 2024 level, currently at $5,874 and just at a multi week low.

4) Refi's rose 9.6% w/o/w and up by 33% y/o/y.

5) From McDonald's: "Throughout November and December, we saw sequential improvement in baseline traffic performance, including slightly positive comp guest count growth for the month of December and had a positive comp guest comp gap to most near end competitors for the 4th quarter. These results were driven by our marketing efforts to amplify traffic drivers."

6) From Wendy's: "In the US, our traffic and dollar growth outpaced the QSR burger category. Growth was led by the success of our collaboration with Paramount, celebrating SpongeBob's 25th anniversary."

7) From Wynn Resorts: "Yet another record year of adjusted property EBITDAR, including another annual record in Las Vegas...Excluding Super Bowl weekend, all of our key volume metrics are up y/o/y. Looking further out, we already have our budgeted group and convention room nights for 2025 on the books at healthy ADRs, and transient booking demand over the last two weeks has been extremely robust. When coupled with a calendar that is once again chock full of large demand drivers in the market, the setup for 2025 feels good."

8) From MGM Resorts: On tough comps, revenues and adjusted EBITDAR did fall y/o/y but "December occupancy and ADRs were still up single digits y/o/y." And, "December slot handle and slot win were an all time record level for any month in our history."

9) From Expedia: "Our fourth quarter results exceeded our expectations, with room nights, gross bookings and revenue all growing double-digits. This top line strength reflects our continued strong execution, along with better than expected travel demand...Travel demand remained healthy in Q4, despite price increases in hotels, vacation rentals and air. Like last quarter, international demand was stronger than the US with booked room nights growing high single digits in the US, low double digits in Europe and high teens in the rest of the world."

10) From Penske Automotive: "In our US retail automotive operations, we experienced a surge in traffic post election...During the quarter, 33% of the new units sold in the US were sold at MSRP, demonstrating continued strength in demand."

11) From AutoNation: "Premium Luxury segment achieved beyond its typically strong seasonal performance, growing unit sales by 12% from a year ago, with particular strong performance in some of the upper end vehicle brands."

12) From Airbnb: "we ended the year on a strong note. Nights and experiences booked accelerated in Q4 to 12%, making it the highest y/o/y growth quarter of 2024." And, "we're excited about the strong demand we continue to see early in 2025."

13) From Herc Holdings: "For 2025, we're seeing continued strength in its signals for mega projects and LNG, data centers, semiconductors, along with strength in healthcare, education, and infrastructure."

14) From Hermes: Q4 revenue was up 18% "With good performance in America and robust growth in the other regions in 2024...France plus 13% and Europe plus 19% recorded strong progressions sustained by robust demand. Japan plus 23% benefited from sustained and regular growth carried by the fidelity of its local customers. Asia excluding Japan up 7% had a remarkable progression thanks to sales up in all of the countries of the zone. America plus 15% confirms an excellent performance."

15) From Kering: "From a sales perspective, as I shared on our last earnings call in October, we were seeing healthy demand trends in line with seasonal patterns. While interest rates increased sharply through the quarter, activity held up with impressive consistency through year end...I am pleased that this sales success was achieved with only a modest increase in incentives needed to address the impact of higher interest rates." In Asia, "Asia Pacific recovered in Q4, down 24%, a 6 percentage point upswing compared to Q3. Mainland China, Hong Kong and Macau led this sequential recovery...Finally, rest of the world was up 5% in Q4, fueled by Middle East and to a lesser extent Latin America."

16) From Cisco: "We continue to see very strong momentum in service provider and cloud, with product orders up 75%, driven by triple digit growth in webscale. Three of the top six webscalers each grew orders in the triple digits, and two of the six each grew more than 50%. This shows our increasing relevance to this high growth customer market as they scale their infrastructure for AI."

17) From Taylor Morrison: "From a sales perspective, as I shared on our last earnings call in October, we were seeing healthy demand trends in line with seasonal patterns. While interest rates increased sharply through the quarter, activity held up with impressive consistency through year end...I am pleased that this sales success was achieved with only a modest increase in incentives needed to address the impact of higher interest rates."

18) From Coca Cola: "I think the overall consumer environment is pretty stable in the sense that there's good economic growth on a broad based view around the world, and that includes both the developed and the emerging markets. If I look at the developed markets, whilst it is absolutely true that the lower income segments in the US and perhaps more notably, in Europe and Western Europe, are under disposable income pressure and have been in '24 and quite possibly will continue for some part of '25. The rest of the consumer base is actually still gaining in terms of disposable income and is spending, maybe spending a little more in the US, North America than Western Europe...And similarly in the emerging markets, yes, it's a little more volatile in ups and downs, but in aggregate, again, you see pretty robust or enduring consumer demand. In the quarter, we saw India rebound, we saw China get a bit better, the Middle East got a bit better, they're still doing pretty well in Latin America. A little softer perhaps in South Africa, but overall, we see continued robustness and growth across consumers that we need to respond to with all the strategies that we have."

19) From Cousins Properties: For Class A properties, "Fundamentals are improving. The existing supply of office buildings is declining as older buildings are converted or torn down and new construction is almost non-existent. At the same time, leasing demand is accelerating. During the fourth quarter, leasing volume nationwide reached a new post-pandemic peak for the third consecutive quarter, and net absorption was positive for the first quarter since 2021."

20) From Marriott: "The US and Canada saw its best quarterly RevPAR growth for the year, with fourth quarter RevPAR rising over 4%, primarily driven by a higher ADR (average daily room rate) . The drop in occupancy around November's US election was not as severe as we had anticipated, with demand accelerating quickly after the election. International RevPAR rose over 7% in the quarter, driven by a 4% rise in ADR and a 2 percentage point gain in occupancy." Leisure travel was strong but business transient saw the "lowest growth quarter of the year due to fewer group events in the US around November's election and a decline in group RevPAR in Greater China."

21) From Lattice Semiconductor: "Looking ahead, as you heard during last quarter's earnings call, we expect more of a U-shaped recovery in 2025. We are very pleased to be guiding our Q1 EPS above the current consensus estimates in a quarter when other companies in our industry are expecting a guide down."

22) The UK economy in December unexpectedly expanded by .4% m/o/m vs the estimate of up .1% and this helped to lift Q4 to an increase of .1% q/o/q vs the forecast of down .1%. It was mostly government spending though that drove the growth as there was no contribution from household spending and business investment declined.

Negatives,

1) January CPI rose .5% headline m/o/m and .4% core, both above the estimate of a gain of .3% for each. The y/o/y gains rose to 3% and 3.3% vs 2.9% and 3.2% in the prior month respectively. Food prices jumped .4% m/o/m and 2.5% y/o/y. In particular, ‘food at home’ saw a .5% price gain m/o/m and up 1.9% y/o/y. Egg prices skyrocketed by 15.2% m/o/m and 53% y/o/y, as it’s all over the news as we know. Prices for ‘food away from home’ rose .2% m/o/m and 3.4% y/o/y. Energy prices were up 1.1% m/o/m after a 2.4% m/o/m gain in December driven by a 1.8% price gain for ‘utility gas services’ with the colder weather and higher natural gas prices. Fuel oil prices jumped by 6.2% and gasoline prices were up by 1.8% all in the month alone. Services inflation ex energy was a culprit here too, rising .5% m/o/m and 4.3% y/o/y. Core goods prices rose .3% m/o/m, though still flat y/o/y.

2) January PPI rose .4% headline m/o/m and .3% core about as expected (in isolation) but that wasn’t the only news because December was revised up sharply (annual revisions) with the headline rate up by .5% instead of .2% initially. The core rate was revised to a gain of .4% from .1%. This brings the y/o/y gain in January to 3.5% and a core rate of 3.6% vs 3.5% and 3.7% in December respectively. Energy prices rose 1.7% m/o/m after a 2.2% rise in the month before though remain flat y/o/y. Diesel fuel in particular drove this along with jet fuel. Food prices jumped 1.1% m/o/m and by 5.5% y/o/y. Eggs by the way saw a price gain of 44% from December. Core goods prices continue to show signs of bottoming, rising .1% m/o/m (no more disinflation for months now) and by 2% y/o/y. On the services side, prices rose .3% m/o/m and 4.1% y/o/y.

3) Core retail sales in January, that had rougher weather than the past few January’s and of course the fires in LA, fell .8% m/o/m which was much below expectations of a .3% gain. This follows a .8% rise in December.

4) The Manheim Used Vehicle Index is at its highest level since October 2023. Their January index rose .4% m/o/m and .8% y/o/y. "While it's not yet spring, wholesale values increased more than we usually see in the month of January, with particular strength at the end of the month...Currently, retail days' supply at used dealerships sits nine days lower than last year, and we are just now on the cusp of starting the spring wholesale market."

5) After a very optimistic response in November and December to the Trump win, the NFIB small business optimism index slipped back a bit in January to 102.8 from 105.1 and vs 101.7 in November though still well above the 93.7 in October. There were slight pullbacks in most of the categories. The one that stands out was the 7 pt drop in the 'Increased Capital Spending' category after the jump in the two prior months. Also, the average rate paid on a loan was 9.4% vs 8.7% in December. For perspective, it averaged 6.2% over the past 20 years. The bottom line from the NFIB, "Overall, small business owners remain optimistic regarding future business conditions, but uncertainty is on the rise. Hiring challenges continue to frustrate Main Street owners as they struggle to find qualified workers to fill their many open positions. Meanwhile, fewer plan capital investments as they prepare for the months ahead."

6) Purchase applications fell for a 3rd straight month, down by 2.3% w/o/w.

7) From McDonald's: "the QSR industry remained challenged and our performance in 2024 fell short of our expectations. Pressure on spending persists, in particular with two significant cohorts of our consumer base, low income and families, particularly in Europe."

8) From Wendy's: On helping them with creating accurate forward guidance they used "multiple third party forecasts for both food away from home and industry traffic. These indicate that consumer spending for food away from home is expected to remain pressured, and traffic in the QSR burger category is expected to be flat to down 1% compared to last year. Our 2025 outlook does not include any impact from new tariffs."

9) From Penske Automotive: "Although we've done a great job working with our OEMs to manage BEV (battery EV) inventory to be more closely aligned with customer demand, the majority of BEV unite still require significant discounting. In Q4, the average discount on a BEV from MSRP was nearly $6,900 per unit."

10) From Herc Holdings: They expect the positive parts of their business to "offset the persistent weakness in interest rate sensitive local markets."

11) From Ryder: "In terms of market assumptions, we're expecting a muted growth environment in 2025, reflecting freight market conditions. The top end of our 2025 forecast range assumes continued contractual earnings growth and a very modest improvement in rental demand later in the year. We expect to see typical seasonal patterns in rental most of the year and slightly better than seasonal trends later in the year, reflecting an anticipated slow freight recovery."

12) From Masco: On guidance, "For the North America repair and remodel market, we expect the market to be roughly flat. For international markets, we expect the markets in aggregate to be down low single digits." Taking out a divestiture, "We expect our sales to be roughly flat to up low single digits."

13) From Ford: On the tariff threats and those implemented, "So far, what we're seeing is a lot of cost, a lot of chaos.

14) From American Express: In giving guidance, "I think Q1's expectations are too high." In part due to "the strength of the US dollar is a headwind to our growth. And the dollar is a bit stronger now than it was in late December."

15) From Edgewell: They also talked about the FX headwind. They described "an external environment that has become increasingly more volatile and uncertain. Largely driven by the strengthening of the US dollar. Organic net sales were down slightly vs last year, but in line with our expectations with a sequential improvement over recent trend...Consumers remain resilient and at the same time cautious. Though in our categories, which are mostly non-discretionary and everyday use, we see no material signs of purchasing hesitancy nor trade down behavior. Having said that, the US wet shave and sun care categories remain highly competitive and promotional."

16) From Coty: "The Q2 reported sales reflected the further slowing of the mass beauty market, particularly color cosmetics, together with continued headwinds in the APAC region, particularly China, travel retail Asia and Australia." They also cited pressure in their "Consumer Beauty US."

17) From ON Semiconductor: "As for the market environment, demand declined late in the quarter and continued into January...Regional revenue declined sequentially except North America, which remained flat with Japan seeing the sharpest decline. Q/o/q declines were driven primarily by our non-core market segments. Amid a backdrop of end market softness and geopolitical uncertainty, inventory digestion persists across our key end markets."

18) From Newell: "Turning to 2025, we expect the macroeconomic backdrop to be dynamic. Lower income consumers remain under pressure from the cumulative impact of inflation over the last several years. The recent substantial appreciation of the US dollar, along with evolving tax policies and potential tariffs and trade regulations in the US, contribute to a fluid and complex operating environment."

19) Japanese January PPI rose 4.2% y/o/y, up from 3.9% in December and above the estimate of 4%. That's the quickest pace since June 2023.

BY Doug Kass · Feb 14, 2025, 11:15 AM EST

From Peter Boockvar:

Core retail sales in January, that had rougher weather than the past few January’s and of course the fires in LA, fell .8% w/o/w which was much below expectations of a .3% gain. This follows a .8% rise in December.

Not included in the core, auto sales fell a sharp 2.8% in January m/o/m and building materials were lower for a 4th straight month, down by 1.3%.

Elsewhere, e-commerce sales fell a notable 1.9% m/o/m, and of course can’t be blamed on weather. Sales also fell for furniture, electronics, clothing and sporting goods. On essentials, like food/beverage and health/personal care, sales fell too, by a touch m/o/m. Department stores saw a gain in sales as did restaurants/bars.

Bottom line, this was a pretty weak report with sales declines almost across the board, even for online sales which of course can’t be blamed on weather as said and I can’t quantify the impact of the LA fires. Bigger picture, we know full well by now the two lane consumer highway that exists with the upper income spender in the fast lane and the lower to middle income one in the slow lane.

US treasuries are rallying in response with the 10 yr yield back below 4.50% at 4.48% after getting to nearly 4.65% intraday on Wednesday after the CPI print.

When including the slight upward revision to December, January import prices were as expected. On a y/o/y basis, import prices are up 1.9% and by 1.2% y/o/y ex food and fuels. The stronger dollar is helping to keep a lid on import prices.

BY Doug Kass · Feb 14, 2025, 9:59 AM EST

* After 15 minutes of trading!

MSFT, GOOGL and AMZN rolling over...

SPYs over QQQs

BY Doug Kass · Feb 14, 2025, 9:54 AM EST

Sluggish domestic economic growth coupled with prickly inflation - what I call slugflation - is around the corner:

BY Doug Kass · Feb 14, 2025, 9:48 AM EST

I added to short index calls on higher opening.

BY Doug Kass · Feb 14, 2025, 9:38 AM EST

From Peter Boockvar:

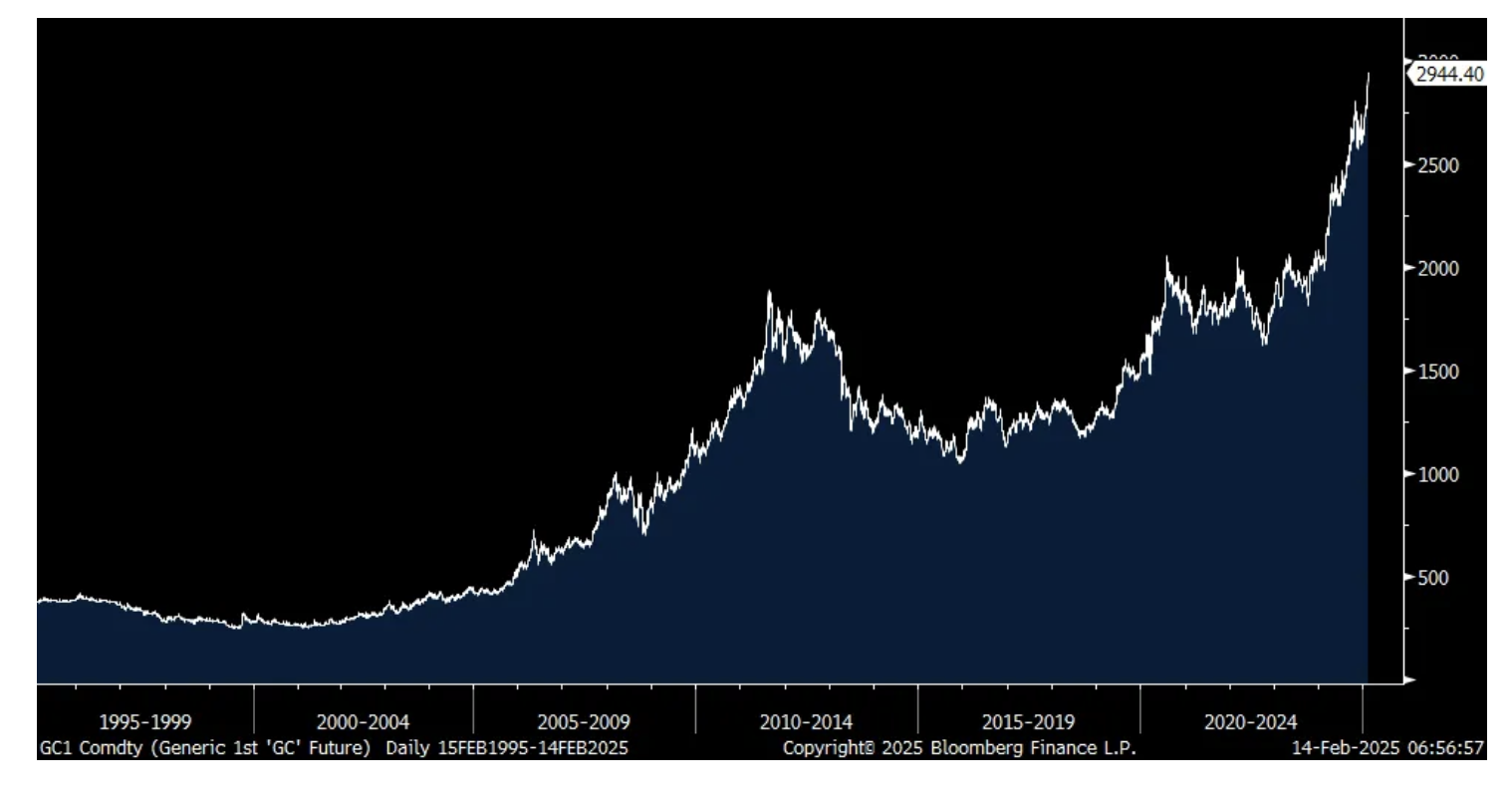

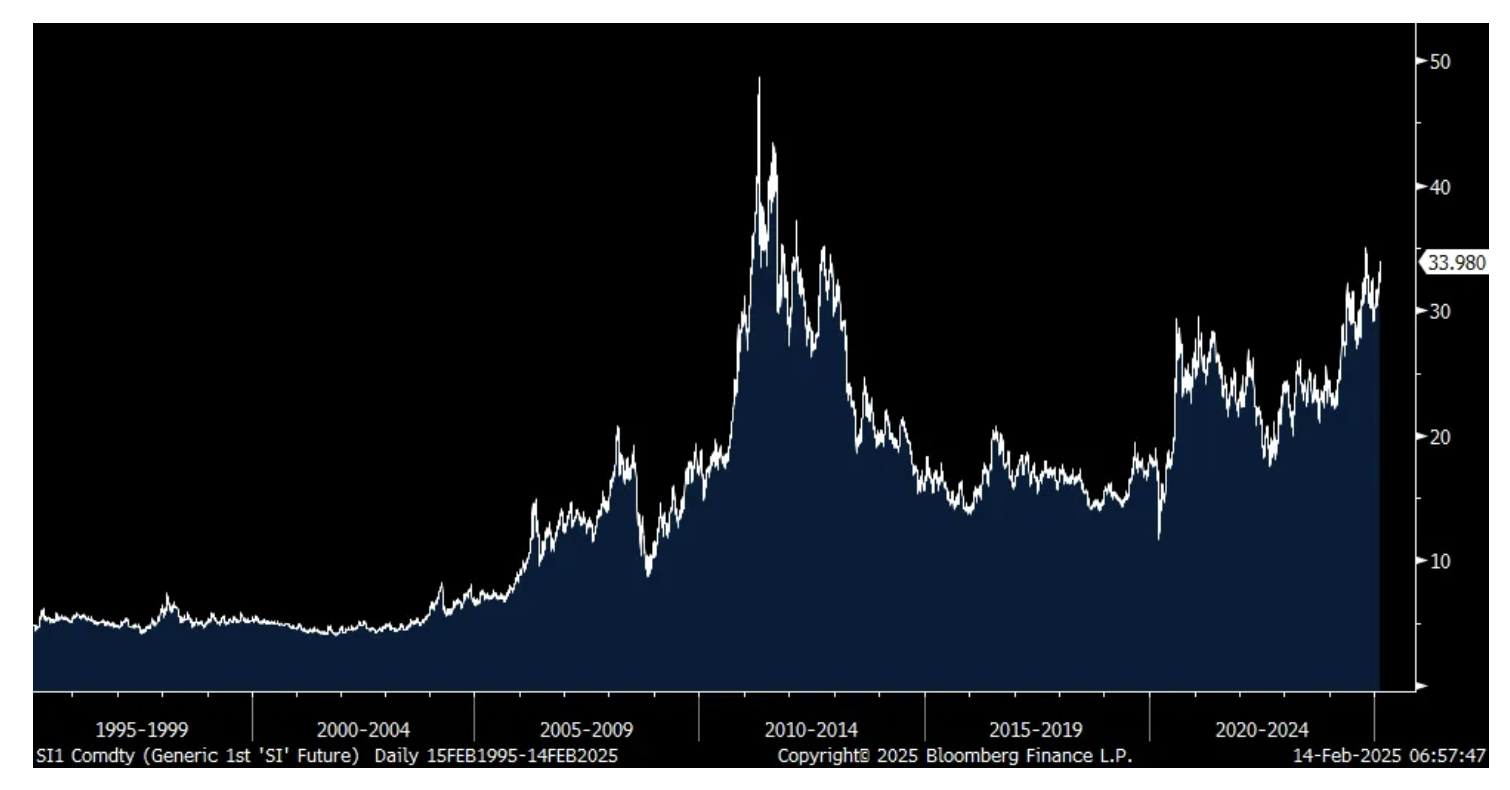

Another record high in gold today and silver is playing some catch up, though is still well off its record high. We remain bullish and long of both (platinum too). So, while the US dollar has been strong against most fiat currencies, it has been very weak against gold, the 5000 year old non-fiat currency. The gold miners are finally playing some catch up too but remain very inexpensive. I include in a chart below the gold/silver price charts of the known ETF gold holdings and it still remains well off its 2020 peak when western investors decided to sell gold and buy bonds that finally had a yield again. Consider this possible dry powder.

Silver

Total known ETF holdings of gold in ounces

It's been a few weeks since I updated for you the price of container shipping and they continue to fall post the Israeli/Hamas cease fire that the Houthi's are adhering to also, for now. It is also post the year end rush to get stuff delivered before any tariffs are implemented. The Shanghai to Rotterdam trip for a 40 foot container now costs $2,887, which is down for an 8th straight week and to the lowest level since the beginning of 2024. Shanghai to LA costs $4,392, down from its highs but not as much as the Rotterdam route as it is at the lowest since December 2024 and still more than double where it was in January 2024. The Shanghai trip to NY is also more than double the January 2024 level, currently at $5,874 and just at a multi week low.

From what I heard from Maersk and Hapag-Lloyd is that both are still avoiding the Red Sea until they have more certainty on the staying power of the ceasefire and what the Houthi's will do.

Shanghai to Rotterdam

Shanghai to LA

Shanghai to NY

With very little else going on I'll get to the earnings calls of note.

From Wendy's:

"In the US, our traffic and dollar growth outpaced the QSR burger category. Growth was led by the success of our collaboration with Paramount, celebrating SpongeBob's 25th anniversary." I remember those SpongeBob days.

On helping them with creating accurate forward guidance they used "multiple third party forecasts for both food away from home and industry traffic. These indicate that consumer spending for food away from home is expected to remain pressured, and traffic in the QSR burger category is expected to be flat to down 1% compared to last year. Our 2025 outlook does not include any impact from new tariffs."

Also, "we've started the year facing some overall industry traffic headwinds exacerbated by significant weather events across the country. The good news is we do expect Q1 to be the trough."

Lastly, "Obviously, consumers are still looking for value."

From Airbnb whose stock is up sharply pre market:

"we ended the year on a strong note. Nights and experiences booked accelerated in Q4 to 12%, making it the highest y/o/y growth quarter of 2024." And, "we're excited about the strong demand we continue to see early in 2025."

They are also negatively impacted by the strong dollar. They expect Q1 revenue growth of 4% to 6% y/o/y "or 7% to 9% when excluding FX headwinds."

"to answer your question in terms of quantifying the Q4 demand, I would say, obviously, we benefited from organic tailwinds across the industry." They also said they benefited from other 'product optimizations.'

From Hyatt Hotels, whose stock was down 9% yesterday as they missed EBITDA expectations for the quarter and in its guidance:

"We continue to see high end consumers prioritizing travel as RevPAR growth was strongest among our luxury brands in both the quarter and for the full year. Leisure transient rooms revenue increased approximately 4% in the quarter and for the full year, revenue increased approximately 1%...transient pace for the first quarter of 2025 is up in the high single digits compared to the first quarter of 2024."

"Group rooms revenue was flat in the quarter and was up 5% when adjusting for the timing of the Jewish holidays in October and the US elections in November. Looking ahead, 2025 group pace for the US full service managed properties is up 7% compared to 2024 with average rate accounting for over half of the increase."

"Business transient customers remained our strongest growth segment, delivering revenue growth of 10% in the quarter. We continue to see our large corporate customers back on the road and we experienced an increase in both demand and average rate in the quarter."

From Wynn Resorts, a stock I own:

"Yet another record year of adjusted property EBITDAR, including another annual record in Las Vegas."

"Excluding Super Bowl weekend, all of our key volume metrics are up y/o/y. Looking further out, we already have our budgeted group and convention room nights for 2025 on the books at healthy ADRs, and transient booking demand over the last two weeks has been extremely robust. When coupled with a calendar that is once again chock full of large demand drivers in the market, the setup for 2025 feels good."

Their Boston property "set a new all time property record for slot revenue."

In Macau, EBITDA was down 1% y/o/y but up 11% sequentially. They referred to the market as still competitive "but stable."

From Penske Automotive:

"In our US retail automotive operations, we experienced a surge in traffic post election...During the quarter, 33% of the new units sold in the US were sold at MSRP, demonstrating continued strength in demand." On the other hand, "Although we've done a great job working with our OEMs to manage BEV (battery EV) inventory to be more closely aligned with customer demand, the majority of BEV unite still require significant discounting. In Q4, the average discount on a BEV from MSRP was nearly $6,900 per unit."

Helping their non BEV business is that Penske is about 77% premium in the US and we know this is the best part of the market. In the UK they are 95% premium with brands like Mercedes, BMW, Porsche and Land Rover and "we see that those brands are maintaining the growth, which certainly helps us."

From Herc Holdings, the equipment rental company benefiting from some big trends and getting hurt by others:

"For 2025, we're seeing continued strength in its signals for mega projects and LNG, data centers, semiconductors, along with strength in healthcare, education, and infrastructure." They expect this and some other things to "offset the persistent weakness in interest rate sensitive local markets."

From Hermes on the luxury side of retail:

Q4 revenue was up 18% "With good performance in America and robust growth in the other regions in 2024...France plus 13% and Europe plus 19% recorded strong progressions sustained by robust demand. Japan plus 23% benefited from sustained and regular growth carried by the fidelity of its local customers. Asia excluding Japan up 7% had a remarkable progression thanks to sales up in all of the countries of the zone. America plus 15% confirms an excellent performance."

BY Doug Kass · Feb 14, 2025, 9:30 AM EST

-VRPX +72% (confirms Positive Results with US Army with Probudur for Combat Care Study)

-NUS +24% (earnings, guidance)

-MTNB +18% (agrees to acquisition of preferred stock and appointment of Dr. Robin L. Smith to the Board of Directors)

-ABNB +14% (earnings, guidance; plans to invest $200-250M towards launching and scaling new businesses to be introduced later this year)

-CELZ +14% (announces Mid-Term Follow-up Study Data Reporting Significant Reduction in Opioid Use by Chronic Lower Back Pain Patients Undergoing StemSpine Procedure using AlloStem)

-ROKU +14% (earnings, guidance)

-PCOR +11% (earnings, guidance)

-ELME +9.8% (earnings, guidance; Board initiates formal evaluation of strategic alternatives)

-AXL +8.6% (earnings, guidance)

-GME +8.5% (said to be mulling investment into Bitcoin and other crypto)

-ALLO +7.1% (announces Publication of Durable Response Data from Phase 1 ALPHA/ALPHA2 Trials of the Allogeneic CAR T Cemacabtagene Ansegedleucel/ALLO-501 in Relapsed/Refractory Large B-Cell Lymphoma in the Journal of Clinical Oncology)

-DKNG +5.4% (earnings, guidance)

-GT +4.9% (earnings, guidance)

-ANTE +4.5% (terminates previously announced share prepurchase agreement for 15.1M shares)

-HASI +3.8% (earnings, guidance; raises dividend and appoints new CFO)

-THS +3.7% (earnings, guidance)

-NMRK +3.3% (earnings, guidance)

-DXCM +2.9% (earnings, guidance)

-INFA -35% (earnings, guidance)

-IFRX -24% (prices 8.3M shares at $2.00/share [includes pre-funded warrants])

-KN -15% (earnings, guidance)

-ISSC -12% (earnings)

-LGCY -11% (earnings)

-TWLO -8.5% (earnings, guidance)

-GDDY -6.7% (earnings, guidance)

-CPS -6.3% (earnings, guidance)

-AMAT -4.9% (earnings, guidance)

-PANW -4.4% (earnings, guidance)

-DVA -9.4% (earnings, guidance; Berkshire sold ~203K shares on Feb 11th under terms of share repurchase between the two companies)

-CLW -6.4% (earnings)

-MRNA -3.4% (earnings, guidance)

-JTAI -3.1% (flyExclusive to acquire Jet.AI's spun off aviation business in an all-stock transaction)

-UPST -3.0% (to offer up to $500M of stock under shelf)

-AEE -2.8% (earnings, guidance)

-SXT -2.6% (earnings, guidance)

-COIN -2.1% (earnings, guidance)

BY Doug Kass · Feb 14, 2025, 9:23 AM EST

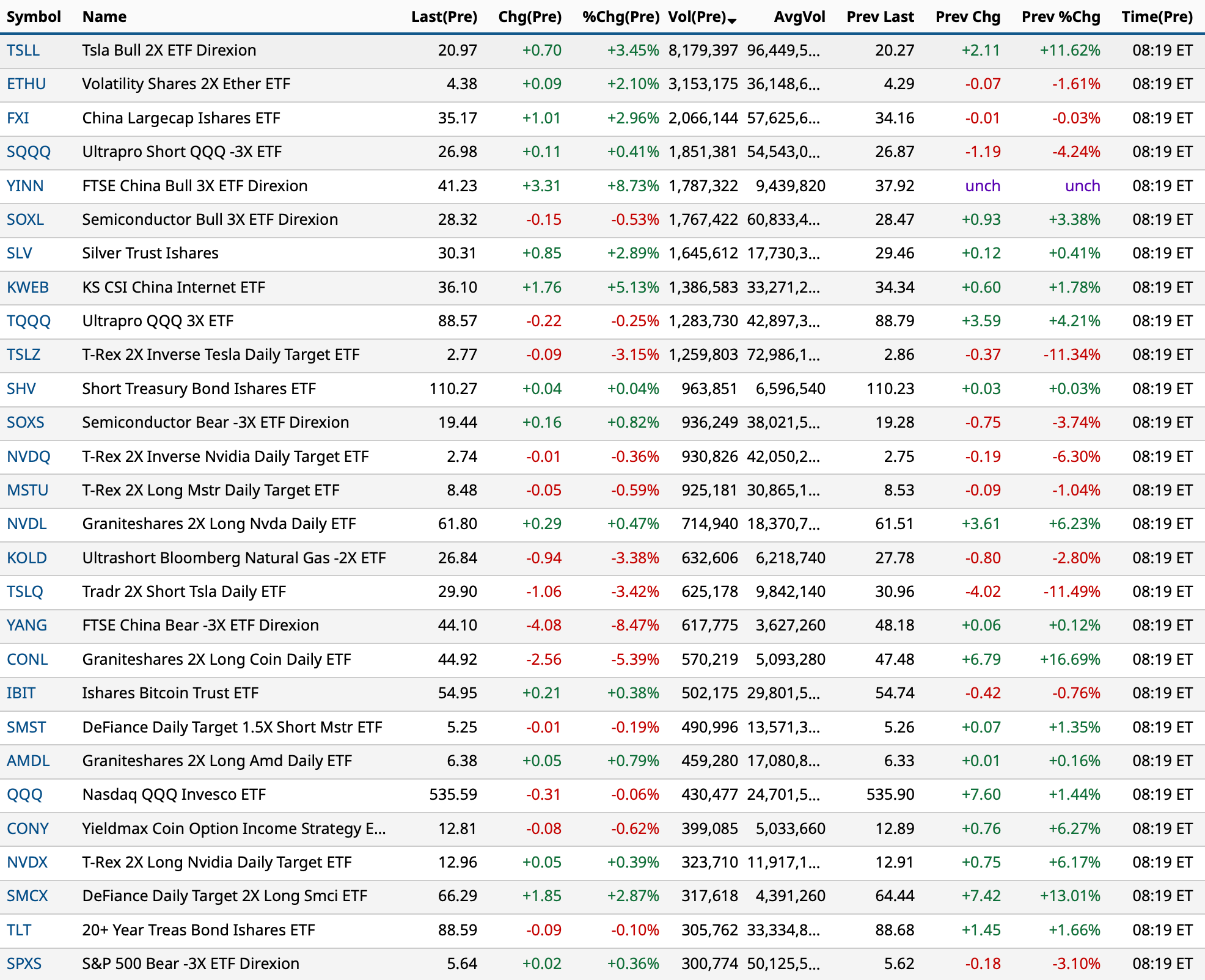

Most active premarket ETFs as of 8:19 a.m.:

BY Doug Kass · Feb 14, 2025, 9:13 AM EST

Premarket percentage Movers at 8:38 a.m. ET:

BY Doug Kass · Feb 14, 2025, 8:59 AM EST

BABA's BABA CEO is critical of technology's large capital spending frenzy (where have you heard that before?):

BY Doug Kass · Feb 14, 2025, 8:47 AM EST

BY Doug Kass · Feb 14, 2025, 8:33 AM EST

BY Doug Kass · Feb 14, 2025, 8:21 AM EST

BY Doug Kass · Feb 14, 2025, 7:55 AM EST

From my pal Larry McDonald:

BY Doug Kass · Feb 14, 2025, 7:35 AM EST

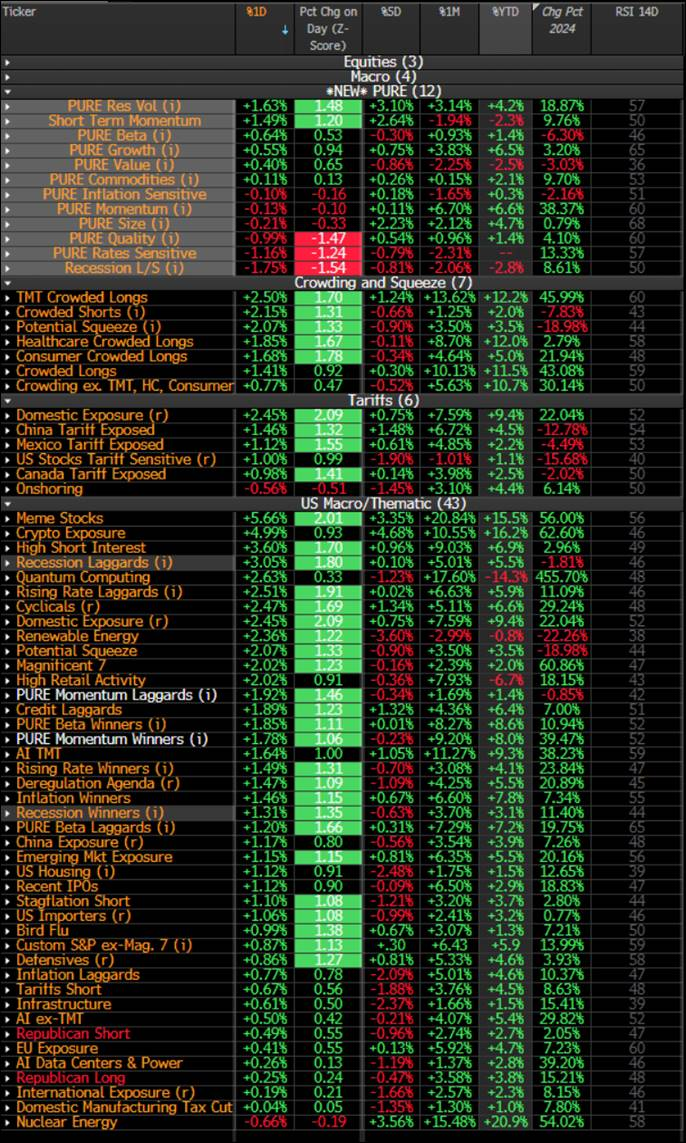

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Feb 14, 2025, 7:20 AM EST

From JPMorgan:

US: Futs are mostly flat. Mag 7 are mostly flat to slightly lower, with the exception of TSLA’s +1.6% gain pre-market. Yields are 1-2bp lower; USD is lower. Commodities are mixed: base metals are lower, while ags are higher. House Budget Committee advanced a budget resolution yesterday, a major first step towards Trump’s legislative agenda (THE HILL). Today, key macro focus will be Retail Sales: Feroli expects Retail Sales to decline 0.7% MoM with the control group advancing by 0.5% MoM.

and...

EQUITY AND MACRO NARRATIVE: Stocks finished higher yesterday led by Tech; TSLA (+5.8%), AAPL (+2.0%) and NVDA (+3.2%) all staged a rally, with almost all D1 baskets finished in the green. The softer reading on several key PPI components (particularly for those that are important to PCE) and the absence of immediate implementation on tariffs supported equities rally yesterday. Thematically, we have seen some short squeezing with High Short Interest baskets adding 3.6% (1.7z). Yields managed to erase all of post-CPI spike given yesterday’s PPI print points to a softer PCE on Feb 28 and now the expected date for the next Fed cut has been moved back October from December (post CPI).

Today, key macro focus will be Retail Sales: Feroli expects Retail Sales to decline 0.7% MoM with the control group advancing by 0.5% MoM. Into this weekend, Ukraine ceasefire negotiations will remain the central focus for investors given the expectation of US presenting Ukraine ceasefire plan at the Munich Security Conference this weekend.

BY Doug Kass · Feb 14, 2025, 7:10 AM EST

BY Doug Kass · Feb 14, 2025, 7:00 AM EST

Bonus — Here are some great links:

BY Doug Kass · Feb 14, 2025, 6:45 AM EST

BY Doug Kass · Feb 14, 2025, 6:35 AM EST

BY Doug Kass · Feb 14, 2025, 6:25 AM EST

The S&P Short Term Oscillator is approaching neutral — now at 0.44 vs. 0.53.

BY Doug Kass · Feb 14, 2025, 6:15 AM EST

Wolf Street howls about America's "drunken sailors."

BY Doug Kass · Feb 14, 2025, 6:05 AM EST

BY Doug Kass · Feb 14, 2025, 5:55 AM EST

BY Doug Kass · Feb 14, 2025, 5:45 AM EST