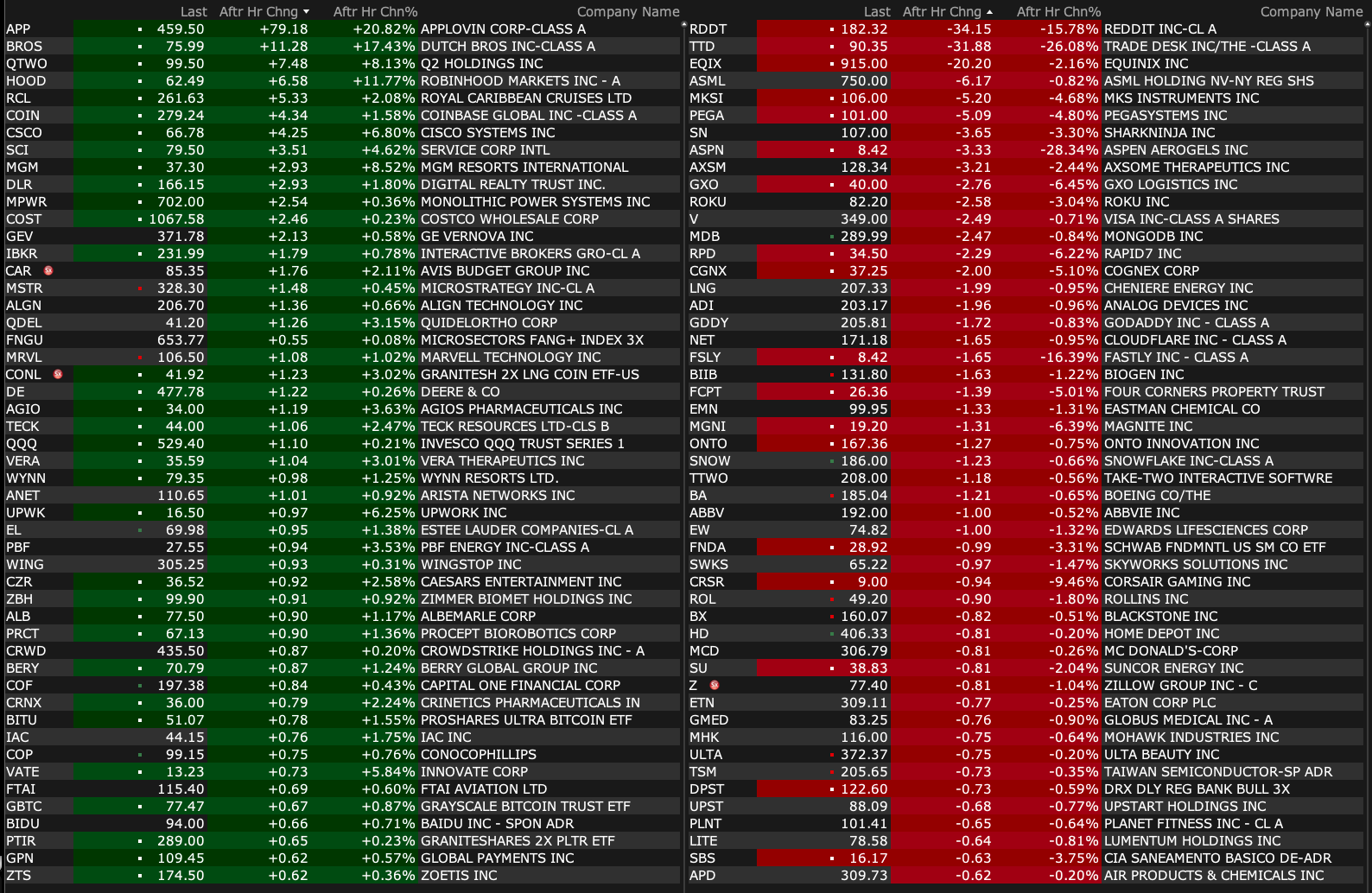

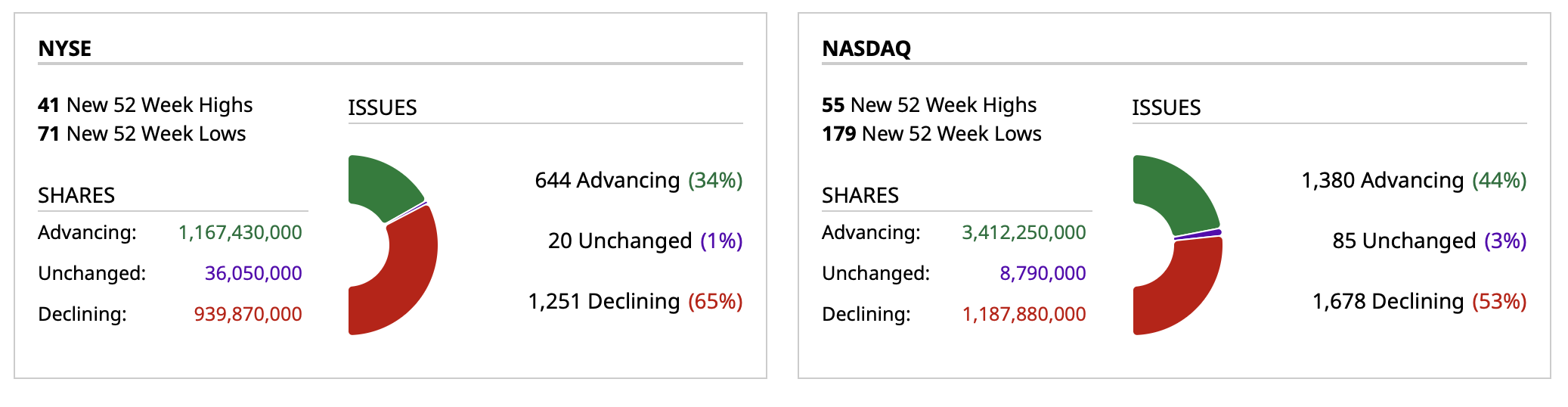

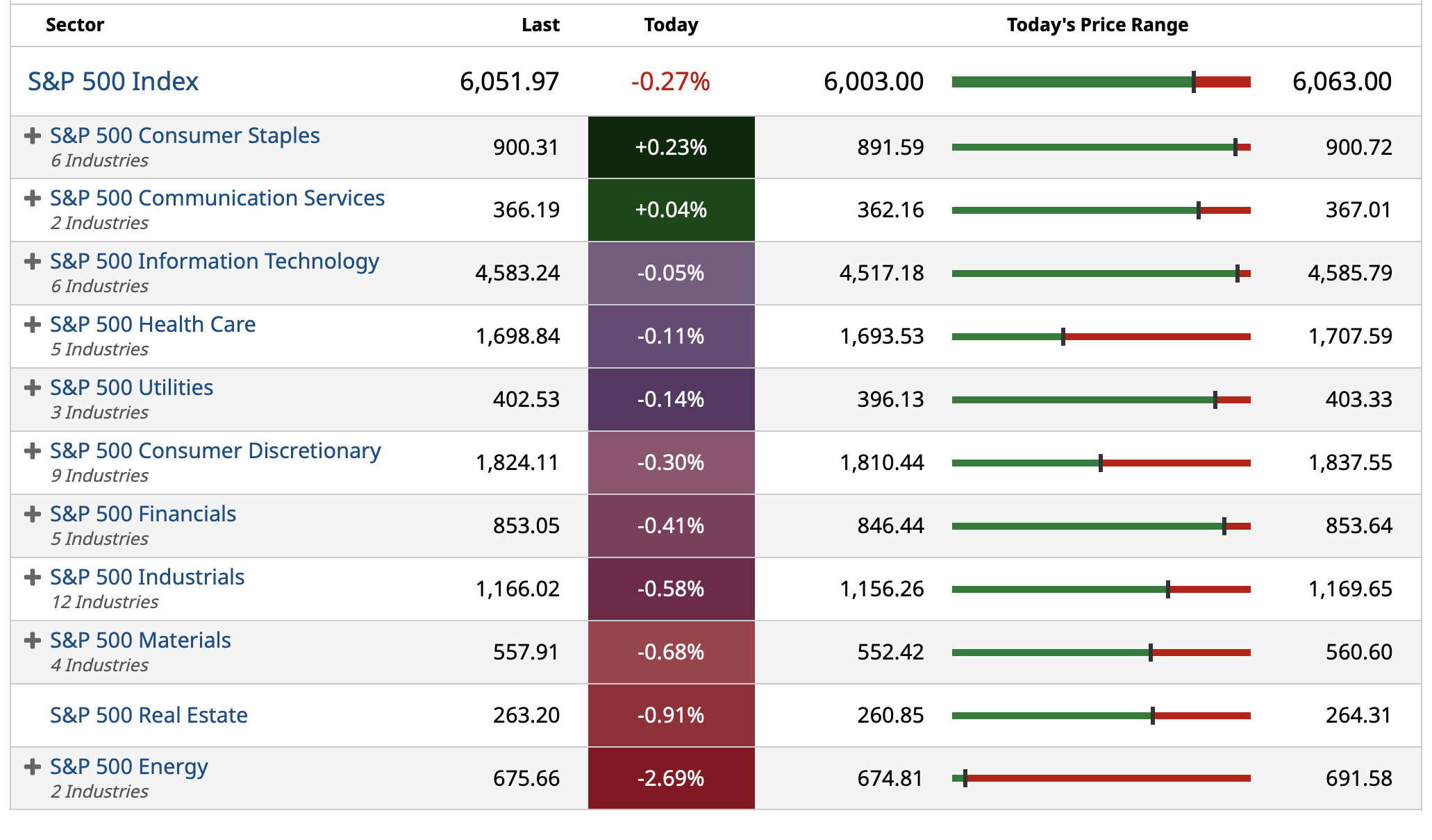

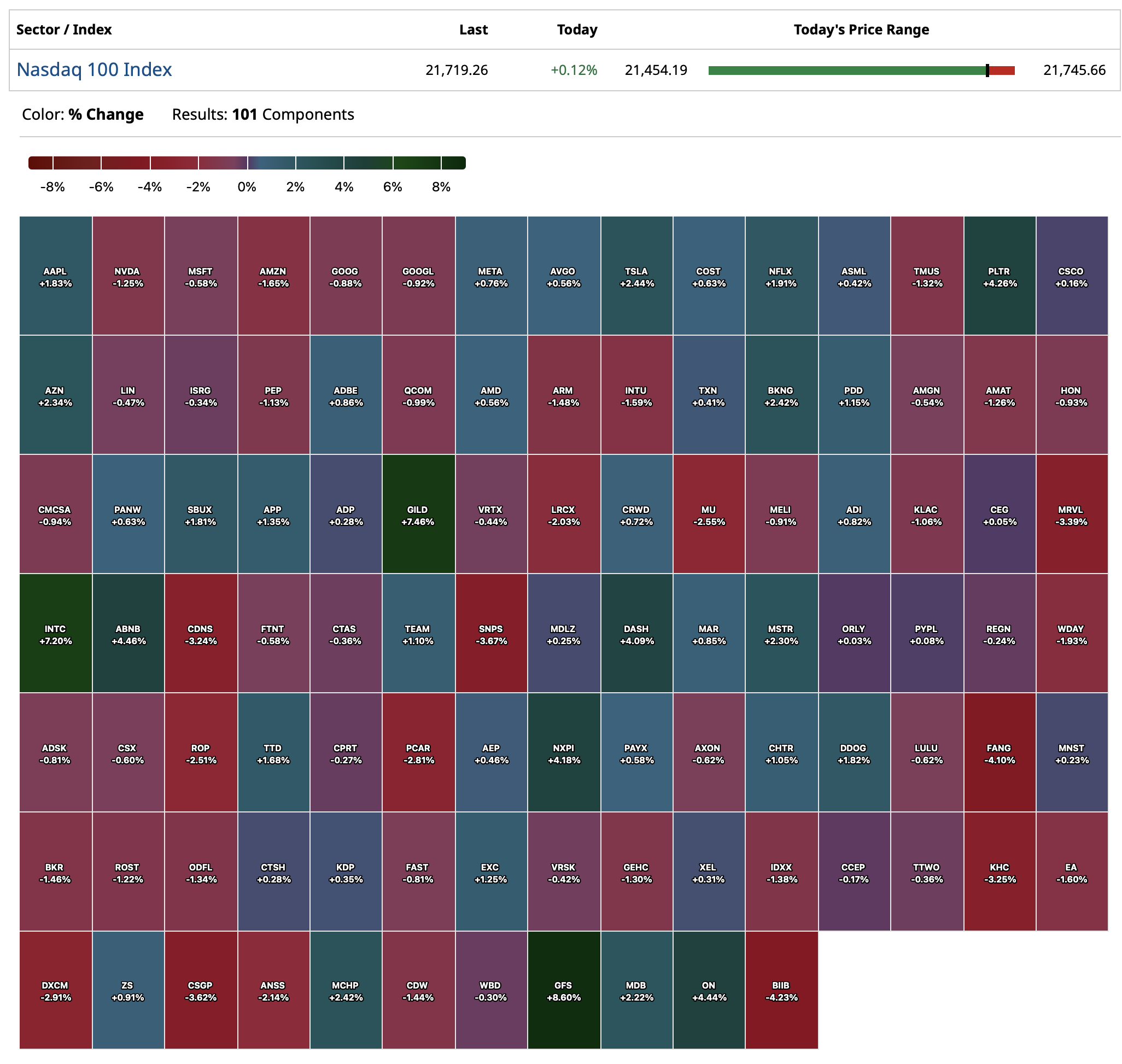

Wednesday's After-Hours Movers

At 4:48 p.m.:

BY Doug Kass · Feb 12, 2025, 5:10 PM EST

At 4:48 p.m.:

BY Doug Kass · Feb 12, 2025, 5:10 PM EST

BY Doug Kass · Feb 12, 2025, 4:55 PM EST

From Peter Boockvar:

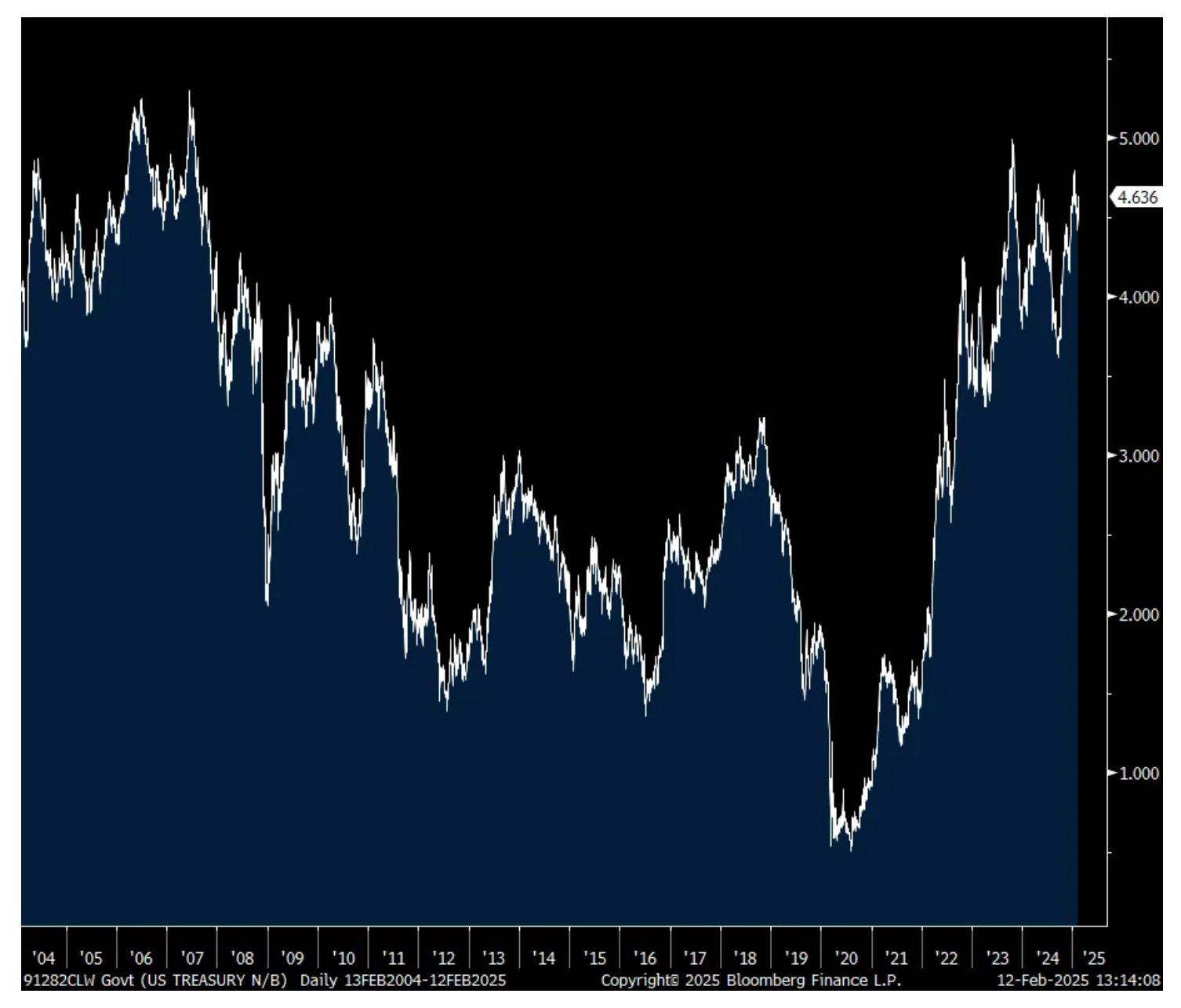

On the heels of the CPI report, the benchmark 10 yr note auction was a bit weak. The yield of 4.632% was about 1 bps above the when issued pricing. The bid to cover of 2.48 was just below the one year average of 2.53. Direct and indirect bidders took 85% of the auction which is about in line with the 12 month average.

Bottom line, the 10 yr yield didn’t move much in response as it is already up 10 bps post CPI print. The 2 yr remains 9 bps above where it was at 8:29am est. Powell also just wrapped up his two day Congressional visit and its clear that he’s stuck in limbo with rates and not by choice but by the reality of the data and policy, for now.

10 yr chart dating back 20 years

BY Doug Kass · Feb 12, 2025, 1:50 PM EST

Apropos to my Moderna post from this morning.

Moderna MRNA was the bell of the ball 3-4 years ago, just like AI is now.

Back then I was screaming about Moderna's share price (and, to some degree, its efficacy) like I am screaming about AI now. Nobody wanted to listen then, like nobody wants to listen now.

I guess in the case of Moderna, there is a little bit of an excuse, because people were scared (perhaps wrongfully driven by media and political hype, yes Covid was an issue, but not nearly the issue it was portrayed as being, especially if younger and healthier), and wanted something to believe in. If people weren’t so traumatized by the media and politicians, maybe they would have looked a little harder at the underlying data and also believed a little more in the human immune system, which has kept us alive as a species for a few hundred thousand years.

There is no such excuse for AI. All the data is out there, if you just want to look.

It was the same thing with Moderna and Covid policy.

All the scientists that had nothing to gain from Moderna and Covid (no financial interests, not positioning themselves to be TV or Twitter personalities, not positioning themselves to make money from big pharma, not positioning themselves for a government/regulatory job, not on Pfizer’s PFE board, not a venture capitalist loading up on biotech investments for their fund, etc.) were telling you the stuff would never really work in the way we were being told it would work, and that it also had very real and very negative side effects for many, and also had the potential to do all sorts of unknown bad things to your body, heart, and immune system.

All you had to do was look, it was not hard to figure out that the whole Moderna and Covid thing was entirely overdone.

AI is no different. All the people positioned to make money from it (Sam Altman, Nvidia NVDA, the venture capitalists, the public companies invested in it, Wall Street. pushing it, the TV pundits, etc.), are all telling you AI is the Moderna for the future of the world. The hard scientists, not trying to position themselves to make money from it, are telling you it does not work nearly in the way we are being told, and its potential is far more limited.

Hopefully, AI turns out better for the world than Covid and Moderna did.

The world is now overburdened with debt, inflation, and all sorts of other societal damage and tension born out of the way Covid was handled and all the political tension and divisiveness that emerged.

BY Doug Kass · Feb 12, 2025, 1:15 PM EST

BY Doug Kass · Feb 12, 2025, 12:55 PM EST

sturner

I know its probably just me, but this market's reaction to the following is stunning: (1) inflation is not dead and is becoming retrenched in core; (2) in 60 days, the 10-Year has moved from 4.2% to 4.63%; (3) regardless of your political leanings, dramatic shifts in tariff application are destabilizing which should have an impact on multiples; (4) earnings among the current leaders have not been that good and yet investments has been accelerated - you get the picture. This is actually quite amazing to this observer.

Dougie Kass

it is not stunning to me.... bull markets die hard. (i have been selling the rips but covering the dips - not really sticking with a big net short exposure)

i am very slowly reshorting today's rally.

patience young jedi.

BY Doug Kass · Feb 12, 2025, 12:45 PM EST

I have an out of town meeting tonight, so I will be leaving at about 3 this afternoon.

I will be returning around noon tomorrow (but I will be posting early in the morning).

BY Doug Kass · Feb 12, 2025, 12:30 PM EST

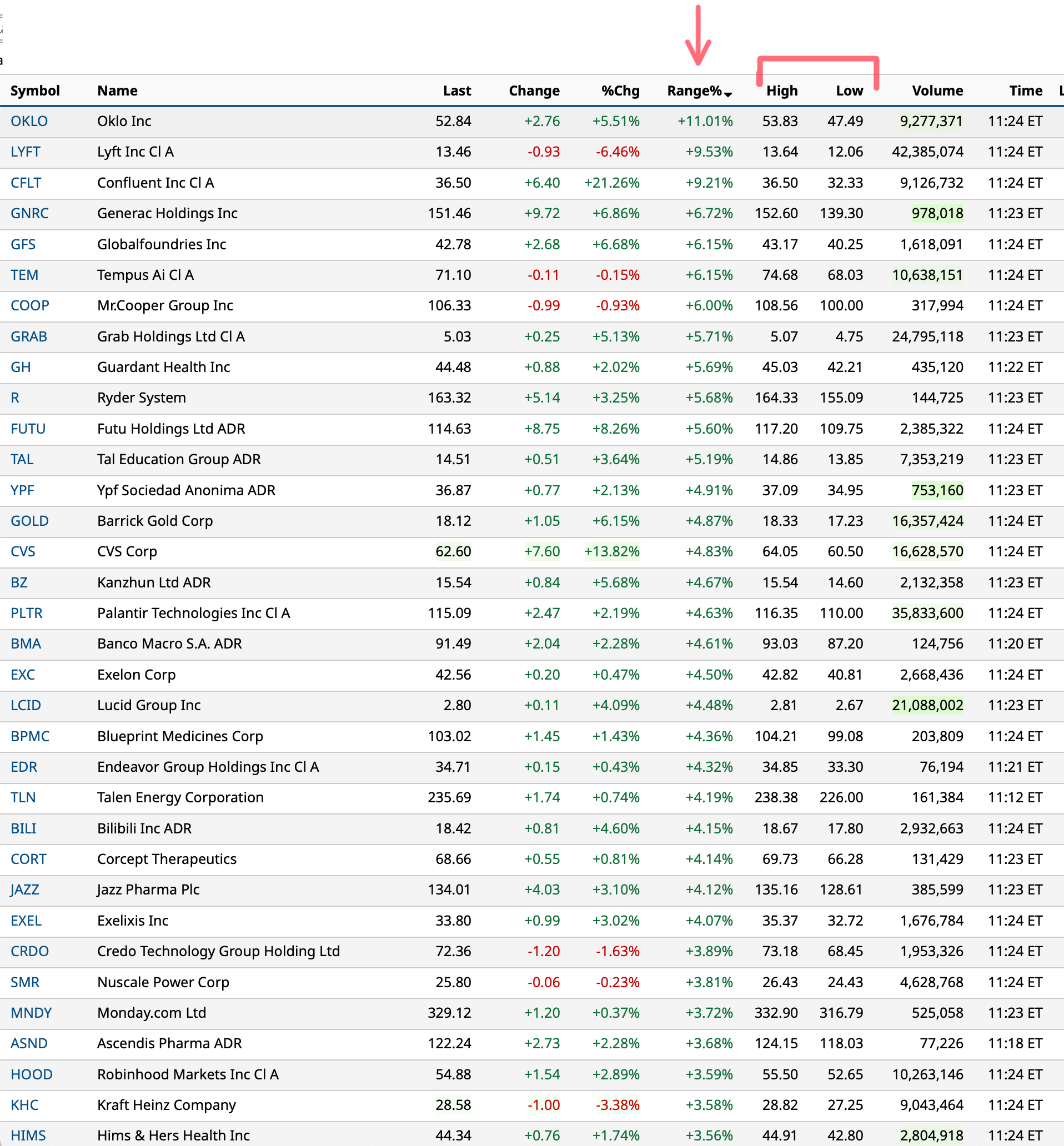

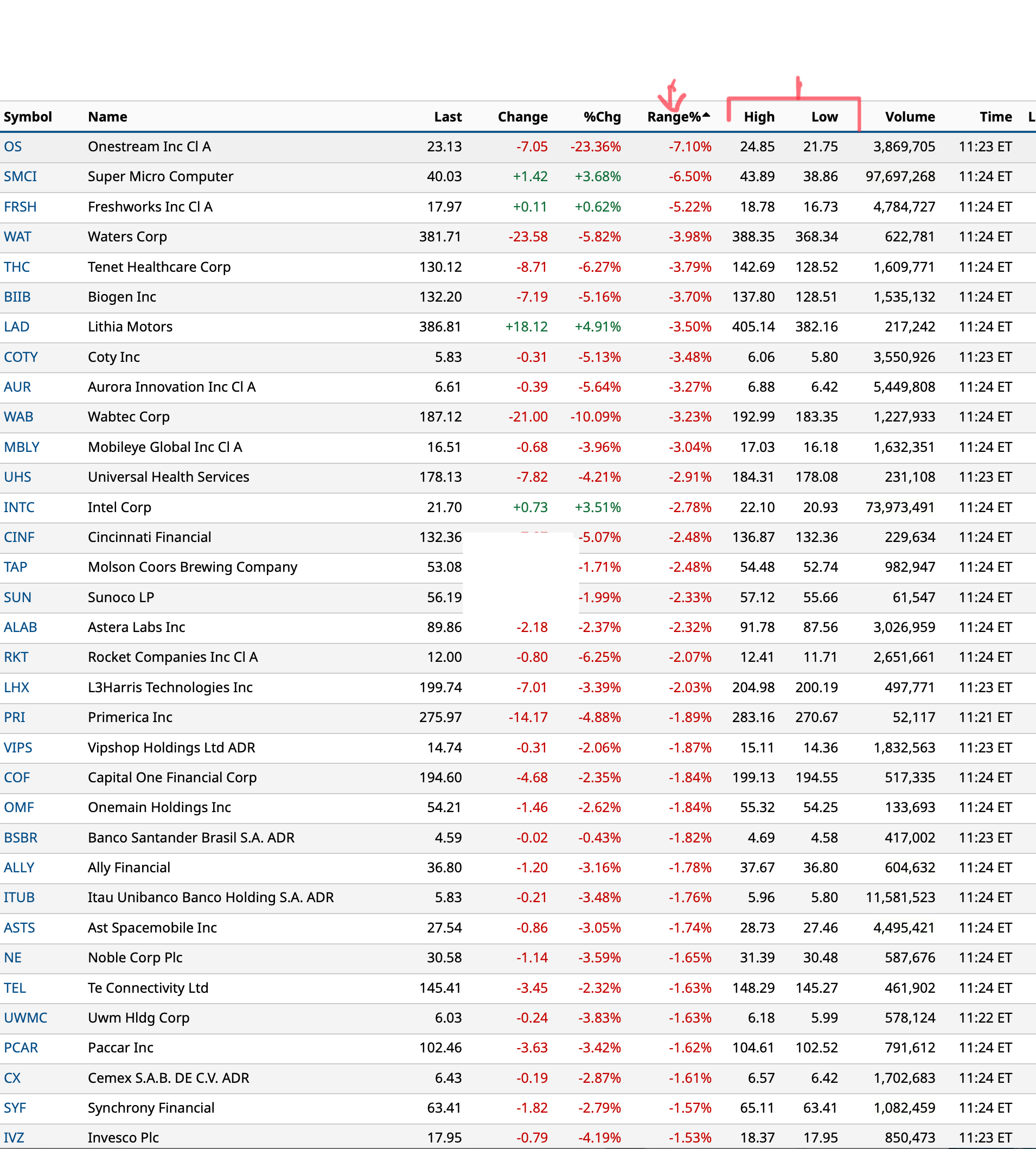

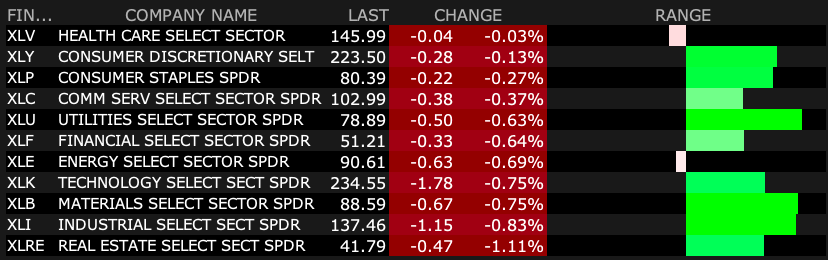

Large-cap stocks with biggest % range (day high - day low):

BY Doug Kass · Feb 12, 2025, 12:00 PM EST

* RSP (equal weighted S&P) -0.82%

* SPY -0.57%

* QQQ -0.32%

BY Doug Kass · Feb 12, 2025, 11:53 AM EST

I have added to my Starbucks SBUX short at $111.06.

BY Doug Kass · Feb 12, 2025, 11:40 AM EST

BY Doug Kass · Feb 12, 2025, 11:30 AM EST

BY Doug Kass · Feb 12, 2025, 11:13 AM EST

From Peter Boockvar:

January CPI rose .5% headline m/o/m and .4% core, both above the estimate of a gain of .3% for each. The y/o/y gains rose to 3% and 3.3% vs 2.9% and 3.2% in the prior month respectively. Food prices jumped .4% m/o/m and 2.5% y/o/y. In particular, ‘food at home’ saw a .5% price gain m/o/m and up 1.9% y/o/y. Egg prices skyrocketed by 15.2% m/o/m and 53% y/o/y, as it’s all over the news as we know. Prices for ‘food away from home’ rose .2% m/o/m and 3.4% y/o/y. Energy prices were up 1.1% m/o/m after a 2.4% m/o/m gain in December driven by a 1.8% price gain for ‘utility gas services’ with the colder weather and higher natural gas prices. Fuel oil prices jumped by 6.2% and gasoline prices were up by 1.8% all in the month alone.

Services inflation ex energy was a culprit here too, rising .5% m/o/m with another .3% rise in owners’ equivalent rent and up 4.6% y/o/y. Rent of Primary Residence was also up .3% m/o/m but its y/o/y rate slowed to 4.2%. That remains above the blended rent gains I’ve seen from the publicly traded multi family REITS of about 2% but also includes single family rentals which are running above that. With regards to the other big component, medical care, prices rose .1% m/o/m and 2.8% y/o/y. Health insurance in particular saw prices up .7% and 4% y/o/y. Please find me a health insurance policy that only costs 4% more than last year.

We’ve seen all the airlines talking about cutting capacity and that continues to flow thru into higher prices as airline fares jumped another 1.2% in the month after a 3% spike in December. They are higher by 7.1% y/o/y. Hotel prices gained 1.7% m/o/m after a .7% drop in December and a 3.1% rise in November. They are up 1.9% y/o/y. Another problem continues to be insurance and repair as auto insurance prices popped by 2% in the month and by 11.8% y/o/y. Vehicle maintenance prices rose by .5% m/o/m and 5.9% y/o/y.

We know goods prices is where almost all of the disinflation has taken place but maybe that is bottoming out as core prices rose .3% m/o/m, though still flat y/o/y. Used car prices (I pointed out the recent lift in the Manheim index) jumped 2.2% in the month after an .8% rise in December and 1.3% gain in November. New car prices on the other hand were flat m/o/m. I’ll say again, we are now 5 yrs with below 2019 levels of new car sales which means less used car inventory. On the disinflation side, apparel prices dropped by a sharp 1.4% in the month, though still up .4% y/o/y. Prices related to home furniture/appliances/supplies fell .2% m/o/m and .9% y/o/y.

Bottom line, we get some inflation relief one side (slowing rents) but then get kicked from somewhere else with the end result being inflation that just can’t break below 3% (if one looks at CPI instead of PCE).

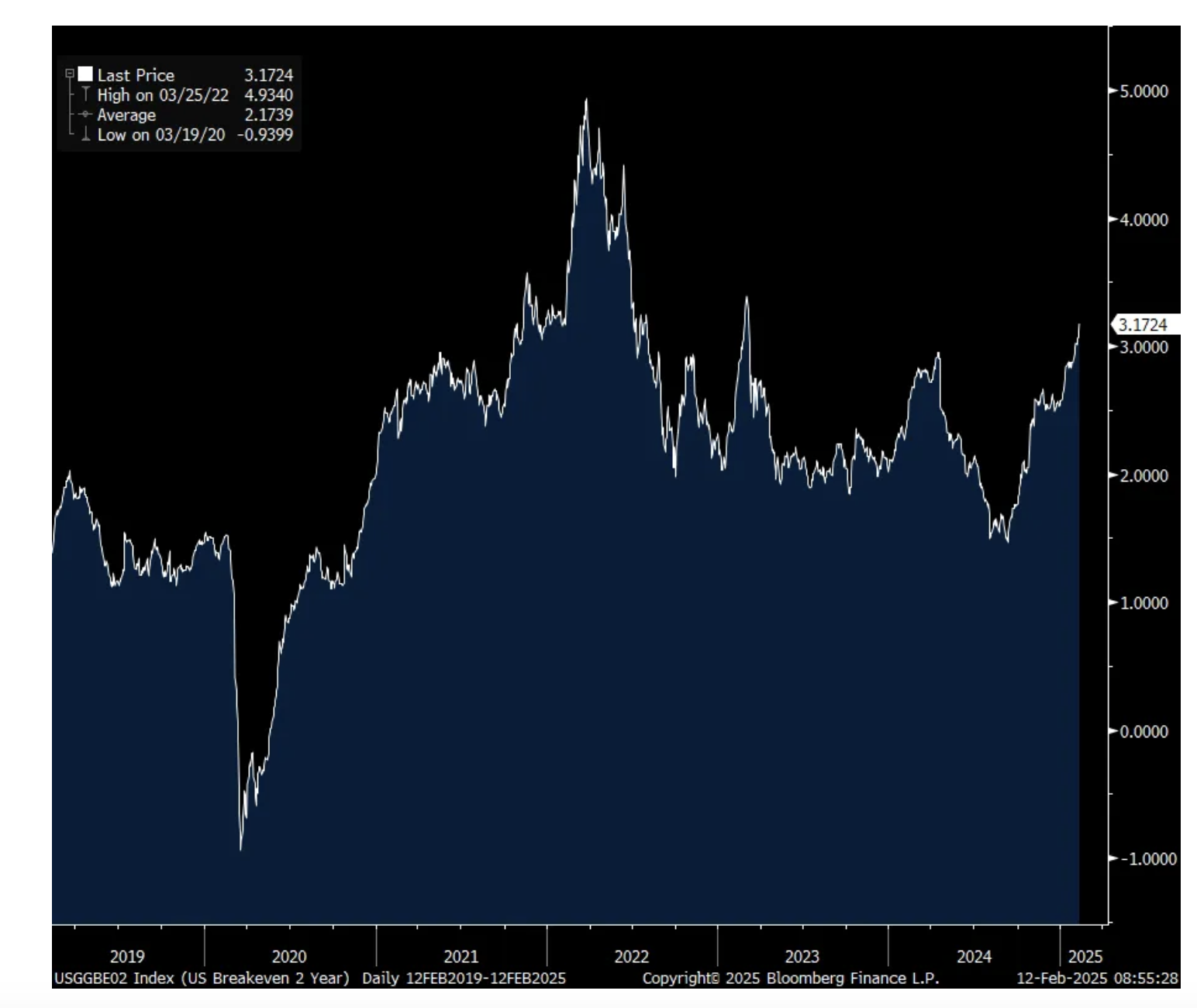

The market response is as you should expect it to be on the hot numbers. The 2 yr inflation breakeven is jumping by another 5 bps to 3.17%, the highest since March 2023. The 5 yr breakeven is higher by 3.5 bps to 2.72%, also around a 2 yr high. The 10 yr breakeven is up by 2.5 bps to 2.49%, the highest since October.

With regards to bond yields, the 2 yr yield at 4.37% is up 9 bps post number and the 10 yr yield is higher by 10 bps at 4.63%.

Powell will again today repeat yesterday’s testimony and him saying they are not in a hurry to cut rates continues to sink in after today’s figures.

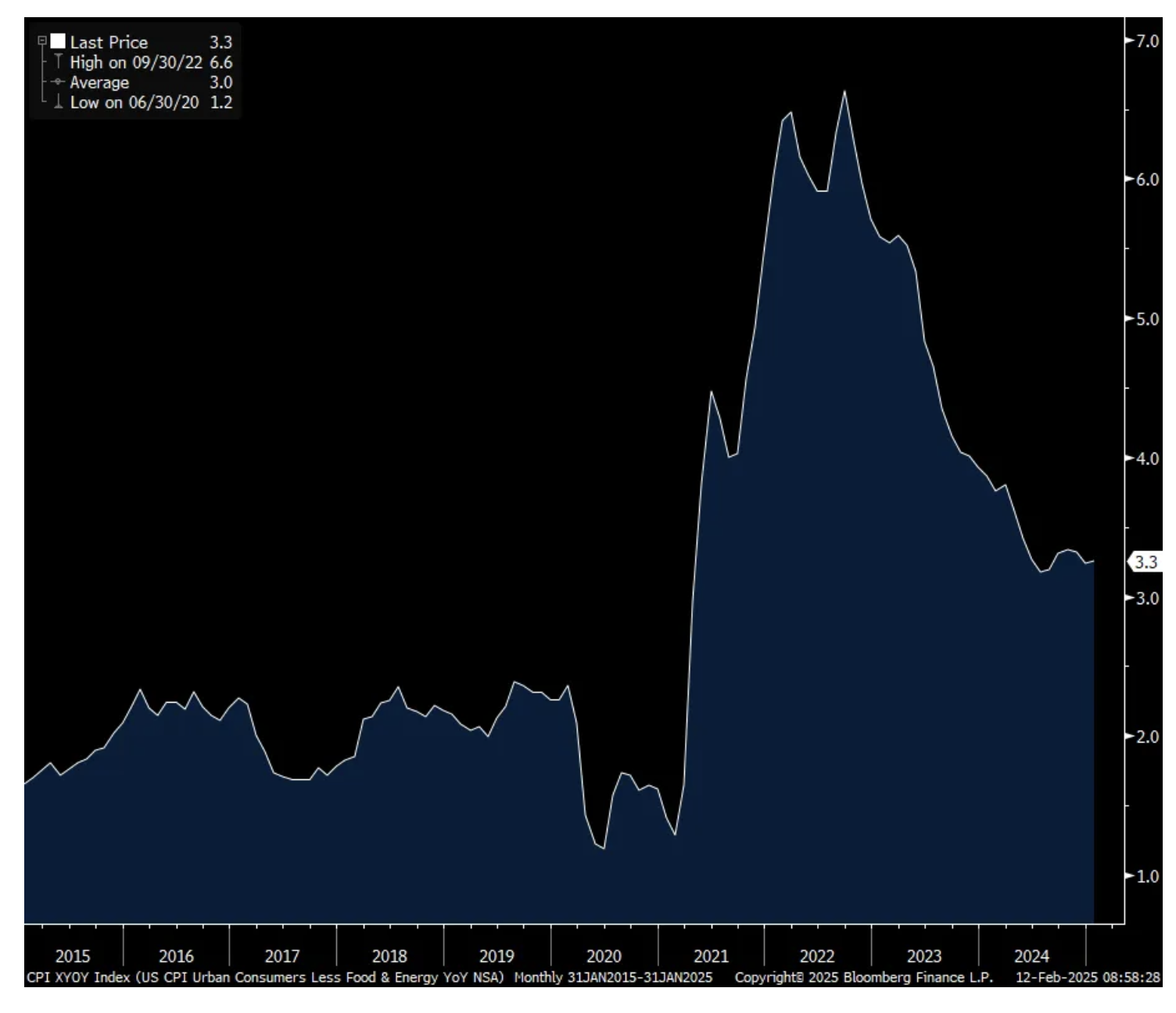

Core CPI y/o/y

2 yr Inflation Breakeven

BY Doug Kass · Feb 12, 2025, 10:59 AM EST

I added to my JPM short at $274.81.

Adding to MSOS (I am on the bid side) and purchased more TCNNF and GTBIF.

BY Doug Kass · Feb 12, 2025, 10:49 AM EST

douglas cassel

12 minutes ago

Doug K appears to have been right, at least for now. Even if his slugflation is short in duration, there is still a market transition happening. The valuations and long term uptrends are certainly at risk. For active and talented short term traders, this is a major opportunity. However, for the less gifted traders among us, some really hard choices present themselves.

Hold, be brave and double down, or sell and wait?

For me, I have been trimming around the edges for a while now, but still am taking losses in long term holdings. I am at my core levels in many stocks that have rewarded me for years. I have stop prices, but wonder if I will regret selling truly great companies in the long term. I sold a bunch of AAPL in 2008, probably my dumbest decision ever.

Bonds seem like a loser here, interest rates can go up a lot more.

Crypto is the most difficult. If Kass, Meisler, and Buffet are correct, bad market times will reduce liquidity in the risk assets, and lead to very bad times for crypto. On the other side, if the theory behind the non-inflationary aspects of crypto are correct, this might be the best time toown them, especially BTC. The endlessly depreciating dollar will lose even more credibility against a limited supply currency. Someone is swimming naked, and the tide is going out, we will see whom this might be.

Most know my feelings about gold, and in any case, it is difficult for me to have it be a large part of any portfolio.

So honor my stops, wait and see, and separate hope from reality. Try not to go down too far on any ship. Easier said than done.

BY Doug Kass · Feb 12, 2025, 10:45 AM EST

Next short tranche (Index calls) with S&P cash only -28 handles.

BY Doug Kass · Feb 12, 2025, 10:37 AM EST

keithfern

14 minutes ago

Dougie Kass is one year older

Entering the years supposedly golder

To us he remains the market wizard

With knowledge and smarts - in good weather or a blizzard

Benefits abound when you listen to DK

Most days we finish and say "hurray!"

To many more years with Dougie as our guide

We all stand to benefit - always enjoying the ride!

Dougie Kass

STAFF

Just Now

love

BY Doug Kass · Feb 12, 2025, 10:28 AM EST

From Peter Boockvar:

Coincidentally, just days after the 25% tariffs on all imports of steel and aluminum, the big auto maker CEO's spoke yesterday at the Wolfe Research Auto, Auto Tech and Semiconductor conference. Jim Farley in particular was not shy chiming in on both the threatened tariffs on Canada and Mexico that were pulled back and the new ones just implemented. He also had something to say about the IRA.

"There's a global street fight in the auto industry right now between electrification, zone electric architectures, and of course, kind of the emergence of the Chinese as a global force in our industry. And I think President Trump has talked a lot about making our US auto industry stronger, bringing more production here, more innovation in the US. And if his administration can achieve that, it would be one of the most signature accomplishments."

"So far, what we're seeing is a lot of cost, a lot of chaos. If you look at the tariffs, let's be real honest, long term, a 25% tariff across the Mexico and Canadian border will blow a hole in the US industry that we have never seen. And frankly, it gives free reign to South Korean and Japanese and European companies that are bringing 1.5 million to 2 million vehicles into the US that wouldn't be subject to those Mexican and Canadian tariffs. So, it would be one of the biggest windfalls for those companies ever. Meanwhile, we're USMCA compliant with almost all of our content, finished vehicles and components going across the borders to have that kind of size of tariff would be devastating."

On the impact from the new steel and aluminum tariffs, which we know the auto industry is a heavy user of. For Ford, "So in steel, we get 90% of that from the US. We get about 10% from Canada and nothing meaningful from Mexico. Aluminum also is not that impacted for us."

But, "The reality is, though, our suppliers have international sources for aluminum and steel. So that price will come through and there may be a speculative part in the market where prices come up because the tariffs are even rumored. So we'll have to deal with it. And that's what I'm talking about, cost and chaos. It's like a little here, a little there. A couple of weeks or a couple of months of vehicles crossing the border, components crossing the border, that's going to be a tariff. This is what we're dealing with right now."

On the possible repeal of the IRA, "We've already sunk capital, even though we've rationalized it in battery production and assembly plants all through Ohio, Michigan, Kentucky and Tennessee. And many of those jobs will be at risk if the IRA is repealed, big parts of it is repealed." I'll add, industry policy rarely works and just because other countries employ it doesn't mean we should.

Finally, Jim Farley said, "So, that's why tomorrow I'm going to DC. It's the second time I've been there in three weeks because they need to understand that there's a lot of policy uncertainty here."

Mary Barra, the CEO of GM also spoke at the conference and she seemed to be more measured in her answer addressing the tariff question:

"As you talk about tariffs specifically, since virtually the day that the potential tariffs were announced, so late November, early December, we started doing scenario planning and looking at what are the different things we can change, we can move, we can respond...We know the steps we could take, and we think we can mitigate 30% to 50% of tariffs without deploying capital. And then of course, if tariffs are longer, there's additional things that we've studied that we know we can do from a capital efficient way."

This is what Coca Cola CEO James Quincy said on what he's seeing with the consumer, and a stock we own:

"I think the overall consumer environment is pretty stable in the sense that there's good economic growth on a broad based view around the world, and that includes both the developed and the emerging markets. If I look at the developed markets, whilst it is absolutely true that the lower income segments in the US and perhaps more notably, in Europe and Western Europe, are under disposable income pressure and have been in '24 and quite possibly will continue for some part of '25. The rest of the consumer base is actually still gaining in terms of disposable income and is spending, maybe spending a little more in the US, North America than Western Europe."

"And similarly in the emerging markets, yes, it's a little more volatile in ups and downs, but in aggregate, again, you see pretty robust or enduring consumer demand. In the quarter, we saw India rebound, we saw China get a bit better, the Middle East got a bit better, they're still doing pretty well in Latin America. A little softer perhaps in South Africa, but overall, we see continued robustness and growth across consumers that we need to respond to with all the strategies that we have."

Cousins Properties, a major Class A office REIT with properties in the fast growing sunbelt cities like Austin, Charlotte, Tampa, Atlanta, Nashville, and Phoenix:

"Fundamentals are improving. The existing supply of office buildings is declining as older buildings are converted or torn down and new construction is almost non-existent. At the same time, leasing demand is accelerating. During the fourth quarter, leasing volume nationwide reached a new post-pandemic peak for the third consecutive quarter, and net absorption was positive for the first quarter since 2021."

Also, "private capital markets remain challenging for office. Asset level debt and equity is limited and expensive. Many private equity investors have legacy issues in their existing portfolios and remain on the sidelines. Conversely, the public markets show meaningful signs of improvement. Liquidity has grown in the unsecured debt markets and spreads have tightened materially. Office share prices have begun to rebound. This creates a compelling investment opportunity for Cousins as private and public markets valuations finally converge."

The bottom line from them, "the office market remains highly bifurcated. There is little to no leasing demand or capital for commodity and older vintage properties. Values for these properties are resetting, so they can be reimagined or demolished, this process is now underway. At the same time, the lifestyle office market is improving. New construction is at historic lows, while leasing demand is accelerating. The market is rebalancing and a shortage of premium lifestyle space is not far off."

Marriott's stock was down 5.4% yesterday and said this:

We know travel is a bright spot in the US economy. "The US and Canada saw its best quarterly RevPAR growth for the year, with fourth quarter RevPAR rising over 4%, primarily driven by a higher ADR (average daily room rate). The drop in occupancy around November's US election was not as severe as we had anticipated, with demand accelerating quickly after the election. International RevPAR rose over 7% in the quarter, driven by a 4% rise in ADR and a 2 percentage point gain in occupancy."

Leisure travel was strong but business transient saw the "lowest growth quarter of the year due to fewer group events in the US around November's election and a decline in group RevPAR in Greater China."

From AutoNation whose fourth quarter included the Fed rate cuts (which started at the end of Q3) which flows into loan rates but also a rise in long term rates:

"last quarter I mentioned some trends that we found encouraging, including the reduction in interest rates, helping to improve affordability and lift demand for both new and used vehicles. And actions we were seeing from a number of our OEM partners to balance demand and production, either through initiatives to make vehicles more affordable or adjusting inventory levels by moderating production, and these were well received. And both trends played out and contributed to our fourth quarter results."

"Sales were particularly strong for hybrid vehicles and battery electric vehicles."

And, pointing to the strength in the upper income consumer, "Premium Luxury segment achieved beyond its typically strong seasonal performance, growing unit sales by 12% from a year ago, with particular strong performance in some of the upper end vehicle brands."

From Masco, the maker of home improvement and building construction products like Delta faucets:

In plumbing supplies, "While the industry continues to show signs of stabilization, it remains choppy and has not yet pivoted to sustained growth."

In paints, pro paint sales were up high single digits and DIY paint sales were down mid single digits.

On guidance, "For the North America repair and remodel market, we expect the market to be roughly flat. For international markets, we expect the markets in aggregate to be down low single digits. Taking out a divestiture, "We expect our sales to be roughly flat to up low single digits."

In the cliche category of 'lunch is not free,' I read a Bloomberg New piece yesterday that said "UK taxpayers will end up paying 150 billion pounds to cover the total losses incurred by the Bank of England on its quantitative easing program. The scale of the losses, which would pay for Britain's entire defense budget for two and a half years, was revealed in the BoE's Asset Purchase Facility Report for the final quarter of 2024." The BoE bought about 900 billion pounds of gilts between 2009 and 2021 and has been selling them off over the past few years. They, along with their central bank peers, mugged themselves with missing inflation and the sharp rise in rates that followed.

The bar is very high for QE to begin again.

BY Doug Kass · Feb 12, 2025, 10:17 AM EST

* Back shorting on the rally off of the lows...

Dougie Kass

STAFF

12 minutes ago

With S and P cash rallying to -38 handles I am back shorting Index calls and moving off my delta neutral (long common, short calls) back into very small net short in Indices.

BY Doug Kass · Feb 12, 2025, 10:10 AM EST

* Where is the honesty, accountability and contrition in the business media?

* Where are the Tim Russerts on financial TV?

* (To me) issues of integrity: Morgan Stanley's Mike Wilson ... and one more conspicuous example of a wrong footed recommendation (Moderna MRNA from $459 to $31), which was never followed up

"Today's move is very logical, though its up +15% (to $459.share)... Despite the move itis the cheapest stock in my portfolio based on current and prospective earnings. (To the person that has ridden the stock up, is today the time to buy more?... "It depends on your risk profile, it can go up another five fold from here."

and, several months earlier (after its first decline)...

"It's (Moderna) my biggest position ever. ($325/share)... To sell it on this news, with their platform, really speaks to the market.... The fundamentals are getting better every single day. It's a long-term play and its a moment in time, and I am happy to have it as my largest position. I added more this morning.... This will be the first $1 trillion healthcare company, period, full stop, end of story."

- CNBC Panelist (2021)

Bulls, bears... alike.

"They" always want to appear correct in view -- regardless of being wrong (present company included!).

Fin TV commentators are unquestioning -- they become accomplices to panelists and commentators who too conveniently forget about recent investment boners and strategic/tactical inaccuracies in favor of new narratives that they have been consistently correct in view -- perhaps because they want to maintain access to these "sources" who may have eviscerated the wealth of viewers (but are not contrite).

Let's first go the Mike Wilson tape! Morgan Stanley's Mike Wilson: Markets are likely to be choppy for the next 3-6 months - YouTube

Or how about this "uber" confident statement (please listen to the hubris) by another financial TV panelist who saw Moderna becoming the first $1 trillion healthcare company three years ago.

Let's go to these tapes, also:

* Moderna ($459) Hits An All Time High

* Moderna ($345) Will Become the First $1 Trillion Health Care Company

* Defending Moderna (2021) and Buying More ($320, -$25) (Steve Weiss defends his position on Moderna as shares plunge)

* Again, Defending Moderna (2021) and Buying The Dip ($285, -$65/share): Steve Weiss defends his position on Moderna as shares plunge

Moderna's market cap today, three years later, is about $13 billion (quite a far distance from $1 trillion!) and its share price is -92% ($450/share to $30/share) since the panelist pushed it has his favorite equity.

You would expect a follow up, a mea culpa but, no.

Crickets about this "pick" -- favoring the emphasis over the winners.

In the main, I prefer the words of Warren Buffett, "praise by individual, criticize by category," to direct criticism. But sometimes we need an air-clearing rant.

I question those in the business media not as ad hominem and out of disrespect or based on an inherent hatred. Rather, it is because I yearn for the facts, I appreciate honesty and I feel accountability is at the essence and is the obligation of the business media as their viewers "depend" and seek the advice of those on the public platform of Fin TV.

"It's a simple question, sir."

- Tim Russert, Meet The Press

I yearn for the honesty of Tim Russert's "Meet The Press," where people were terrified to go on the show. Everyone knew Tim was prepared with the facts and nothing but the facts. He would go back to his panelists' previous quotes and challenge his guest on those facts and not by his opinions.

More lessons learned.

BY Doug Kass · Feb 12, 2025, 9:36 AM EST

10:00 a.m.: Fed Chairman Powell delivers semiannual monetary policy testimony before the House Financial Services Committee;

12:00 noon: Fed Bank of Atlanta President Bostic (Non-Voter) speaks on the economic outlook in a moderated conversation before the Atlanta chapter of the National Association of Corporate Directors, Atlanta, GA

5:05 p.m.: Fed Board Governor Waller (Voter) speaks on "Stablecoins" before event, "A Very Stable Conference: Stablecoin Infrastructure for Real World Applications," San Francisco, CA

**CONGRESSIONAL HEARINGS: 10:00 a.m.: Senate Health, Education, Labor and Pensions Committee hearing

BY Doug Kass · Feb 12, 2025, 9:31 AM EST

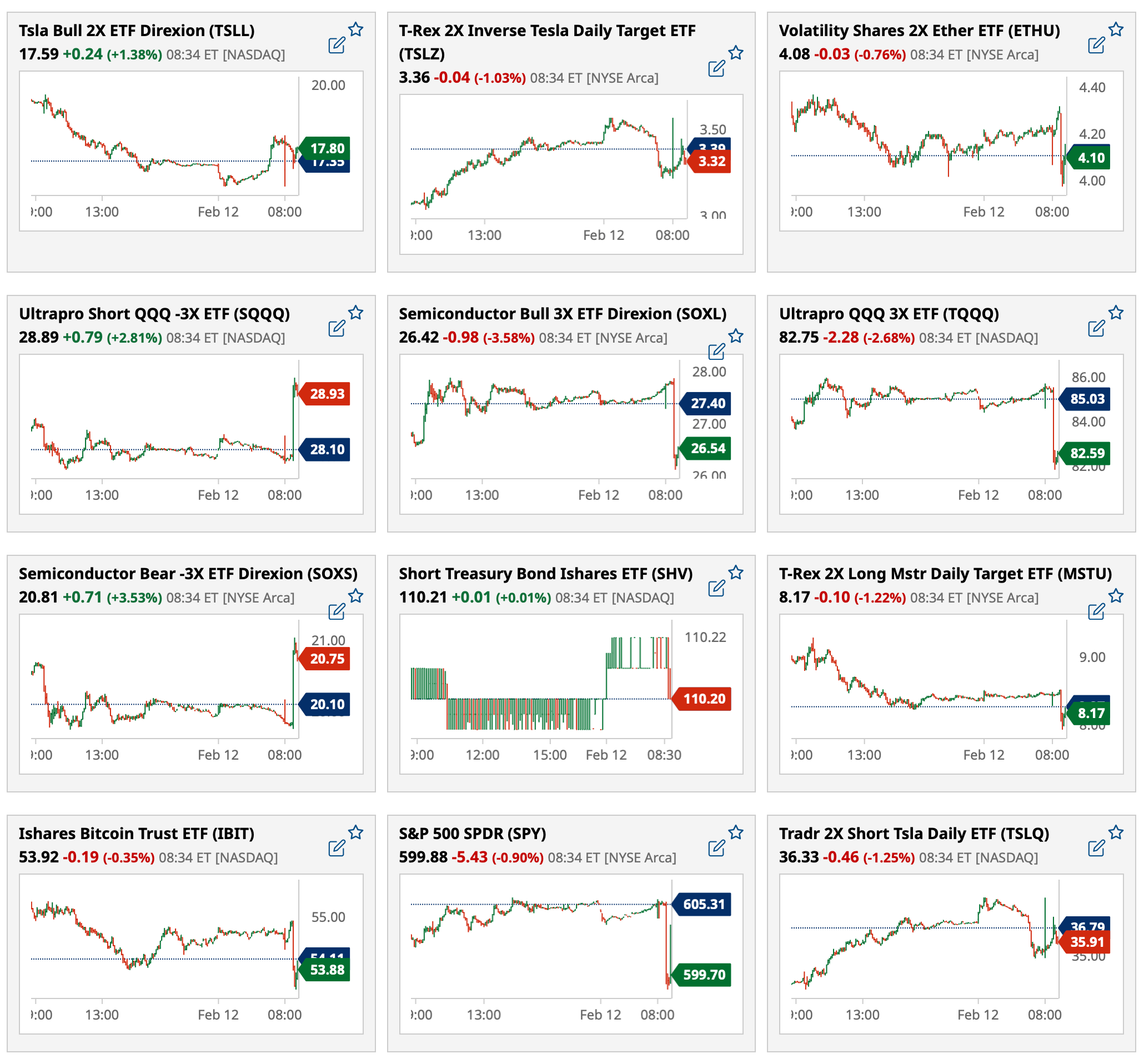

Most active premarket ETFs as of 8:44 a.m. ET:

BY Doug Kass · Feb 12, 2025, 9:19 AM EST

-XLO +119% (collaborates with AbbVie, includes Option Agreement to Develop Novel Tumor-Activated Immunotherapies; Xilio will receive $52.0M in total upfront payments, including a $10.0M equity investment)

-UPST +26% (earnings, guidance)

-MCY +20% (earnings)

-CFLT +14% (earnings, guidance)

-SMCI +14% (earnings, guidance; files to sell $700M of New 2.25% Convertible Senior Notes Due 2028 and Amendments to Existing 0.00% Convertible Senior Notes Due 2029; delays 10Q filing)

-CVS +9.4% (earnings, guidance)

-RDFN +9.2% (Zillow and Redfin partner making Zillow the exclusive provider of multifamily rental listings (properties with 25 or more units) on Redfin and its sites, Rent.com and ApartmentGuide.com)

-LAD +7.1% (earnings, guidance)

-PBI +7.1% (earnings, guidance)

-FRSH +6.4% (earnings, guidance)

-DASH +6.2% (earnings, guidance)

-TMHC +5.4% (earnings, guidance)

-EW +4.4% (earnings, guidance)

-SWTX +4.3% (strength following receiving FDA approval for Mirdametinib for treatment of children and adults with NF1-PN)

-ANGI +4.1% (earnings, guidance)

-MIR +3.9% (earnings, guidance)

-GNRC +3.8% (earnings, guidance)

-ALKS +3.1% (earnings, guidance)

-R +2.1% (earnings, guidance)

-VLN +2.0% (adopts a Share Repurchase Program of up to $15M)

-SPIR -52% (intends to seek additional equity or debt financing due to delay in Maritime sale; Has substantial doubt to continue as going concern)

-ATOM -41% (earnings)

-STAA -38% (earnings, guidance)

-SMWB -26% (earnings, guidance)

-OS -21% (earnings, guidance)

-TDC -17% (earnings, guidance)

-RGS -15% (earnings)

-LYFT -14% (earnings, guidance)

-BL -13% (earnings, guidance)

-ALSN -9.3% (earnings, guidance)

-WAT -8.7% (earnings, guidance)

-VRT -7.9% (earnings, guidance)

-WAB -6.8% (earnings, guidance)

-ZG -6.6% (earnings, guidance)

-KHC -5.5% (earnings, guidance)

-ZWS -4.5% (prices 7.75M shares for selling stockholder [Ice Mountain] at $35/share)

-CAR -2.8% (earnings)

-KRG -2.5% (earnings, guidance)

-IE -2.4% (prices upsized offering of 10.3M shares at $5.85/shr for gross proceeds ~$60M)

-MLM -2.1% (earnings, guidance)

BY Doug Kass · Feb 12, 2025, 9:09 AM EST

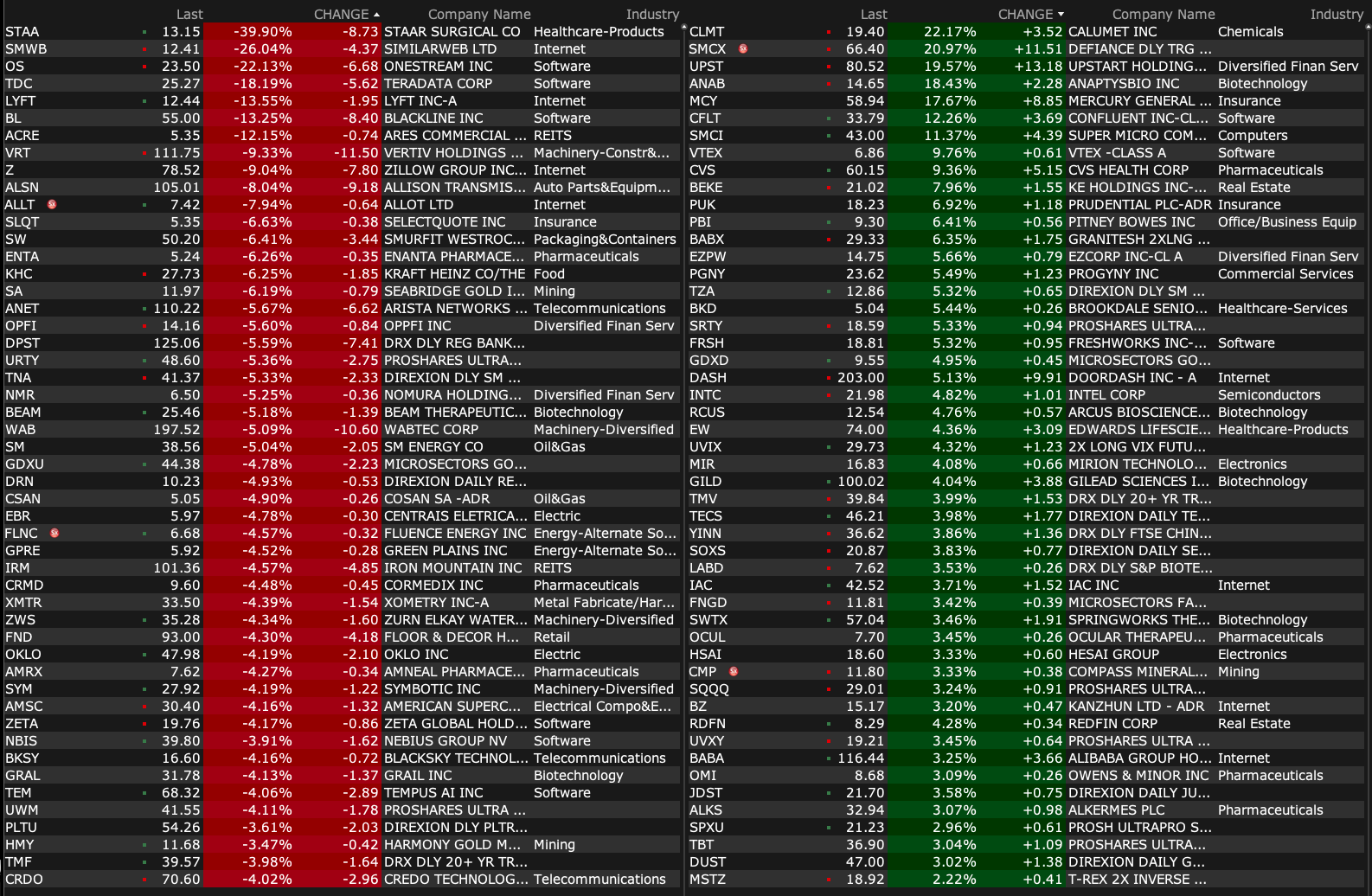

Premarket percentage movers at 8:43 a.m. ET:

BY Doug Kass · Feb 12, 2025, 8:55 AM EST

On the hot inflation number (which was my baseline expectation) I purchased SPY and QQQ common against my short Index calls:

* SPY $599.14

* QQQ $522.21

Ergo, I have a buy write on.

This was very profitable.

BY Doug Kass · Feb 12, 2025, 8:40 AM EST

BY Doug Kass · Feb 12, 2025, 8:15 AM EST

Charts and technical analysis lose their usefulness with changing market structure:

BY Doug Kass · Feb 12, 2025, 8:05 AM EST

Well, I don't know why I came here tonight

I've got the feeling that something ain't right

I'm so scared in case I fall off my chair

And I'm wondering how I'll get down the stairs

Clowns to the left of me

Jokers to the right

Here I am, stuck in the middle with you

Yes, I'm stuck in the middle with you

And I'm wondering what it is I should do

It's so hard to keep this smile from my face

Losing control, yeah, I'm all over the place

- Stealers Wheel, Stuck In The Middle With You

BY Doug Kass · Feb 12, 2025, 7:55 AM EST

BY Doug Kass · Feb 12, 2025, 7:45 AM EST

* Tesla's share price has fallen from $485 (in mid-December, 2024) to $322 (down by another -$6 in premarket trading) this morning.

* Read on... its no wonder!

* And more skeptical comments on AI and some "More Tales of Nvidia"

This article on Tesla TSLA self-driving is interesting.

Elon Musk is about to masterfully move the goalpost on Tesla Full Self-Driving

I guess the company finally figured out their massive investment in AI to do it will not work, so they have resorted to an old-fashioned belt-and-suspenders approach to develop a product that might barely suffice in a limited fashion in small geo-fenced markets. Probably includes lidar and everything else Waymo has done, as well as actual humans supporting it in the background. Heck, if they had humans driving these things around with a joystick like a drone, I would not be surprised!

Ultimately, businesses figure out their massive investments in AI are not panning out, and then they pivot to something else. It just takes time. At least Tesla is finally figuring it out:

Here is a bit more of an explanation from me as to why AI has failed at full self-driving for Tesla. The proof is in the pudding, which is why Tesla is finally now pivoting to an entirely different approach.

It is the "long tail" problem; you need actual common sense and the ability to think to deal with the real world, where you encounter an exponential number of situations you have not seen before.

This is the "now I've seen everything" approach. The big AI players are trying to convince everyone that you can just train reinforcement learning on enough data (millions of hours of video of driving) so that you've literally trained on everything that will possibly happen. That is just BS.

A teenager takes about 20 hours to learn to drive, not 20 million. It took me about zero. It is not hard. Whatever they're doing now, it is not going to work. Throwing everything into a giant sequence to sequence generator algorithm is not how it's going to get done.

The fact that AI cannot drive a car, which is one of the easiest things to do, speaks volumes. There are strict rules of the road. It is not complicated. If A, do B. But the slightest variance, which happens all of the time, AI just cannot cope. It is not hard for a human to figure out what to do when there is slight variance, but for the AI, not even close, and it fails. Human lives should not be trusted to a roll of the dice in these situations.

Driving a car is actually a lot simpler, and a lot more rules based, than a lot of the things we are being told AI will be able to do, like thinking and language and all sorts of other stuff. No chance. Tesla has finally figured that out, probably after a billion dollars down the tube. Thus the pivot.

Watch what they do, not what they say.

From the article, they are not even close with AI:

As of the latest data, Tesla FSD v13 is achieving about 500 miles between critical disengagement while Tesla’s own stated goal to be safer than humans is to surpass miles between collision with human drivers, which is at 700,000 miles, according to NHTSA.

BY Doug Kass · Feb 12, 2025, 7:00 AM EST

BY Doug Kass · Feb 12, 2025, 6:10 AM EST

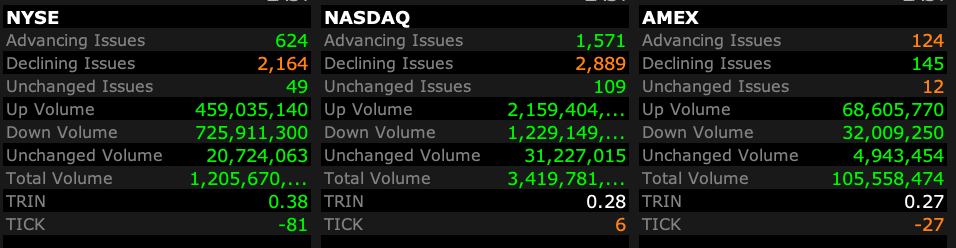

The S&P Short Range Oscillator rose modestly — from 0.87% to 1.11%.

BY Doug Kass · Feb 12, 2025, 5:45 AM EST