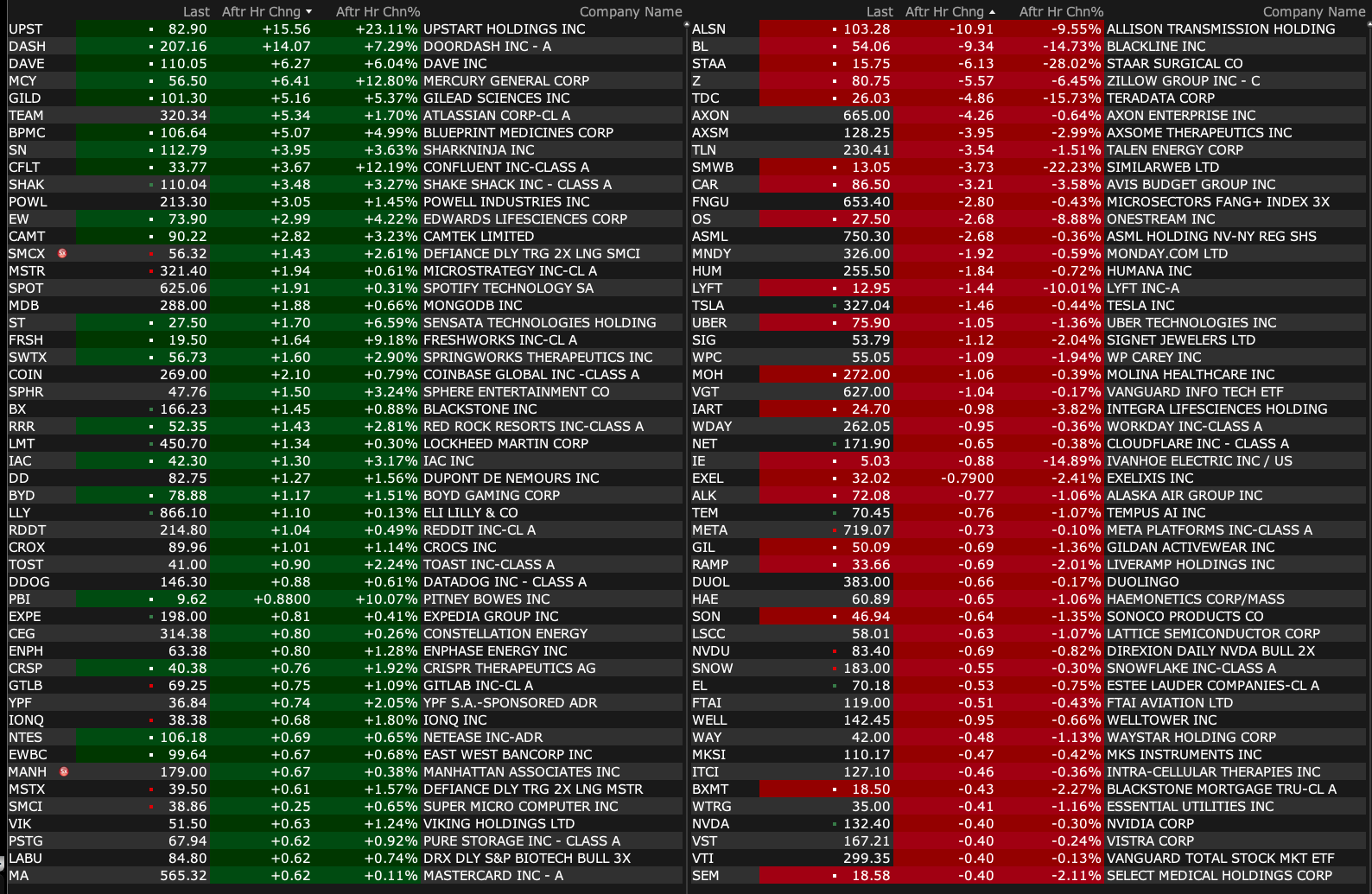

Tuesday's After-Hours Movers

At 4:30 p.m.:

BY Doug Kass · Feb 11, 2025, 4:51 PM EST

At 4:30 p.m.:

BY Doug Kass · Feb 11, 2025, 4:51 PM EST

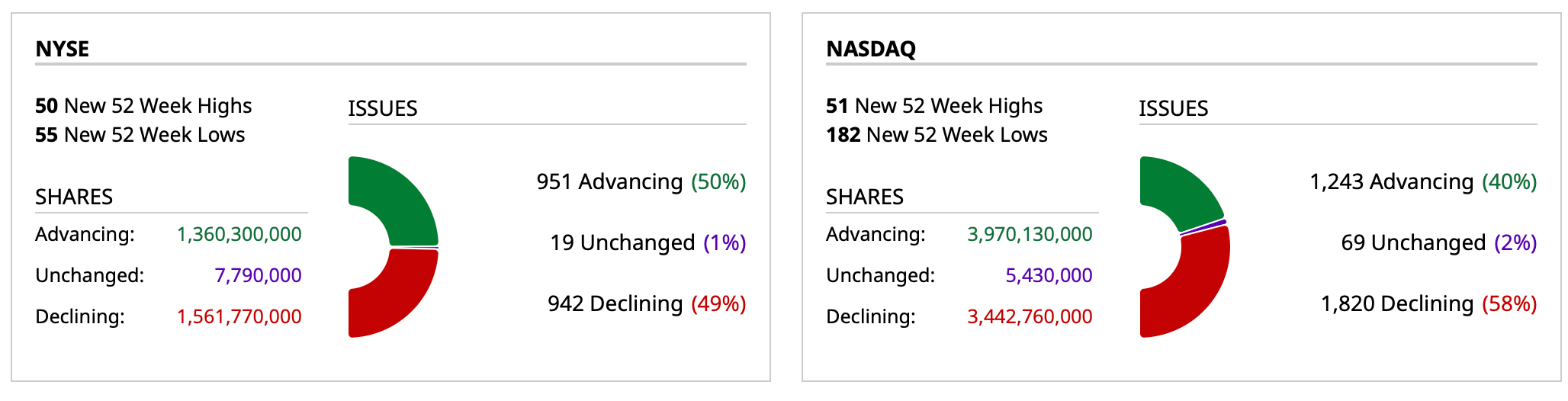

- NYSE volume 2% below its one-month average

- NASDAQ volume 28% above its one-month average

BY Doug Kass · Feb 11, 2025, 4:37 PM EST

* Let's play ball (thanks Chicago Cubs!)

Once again, the market had more intraday moves than a shortstop batting .110 today!

It's a terrific market for opportunistic and disciplined traders not so great for the buy-and-hold crowd.

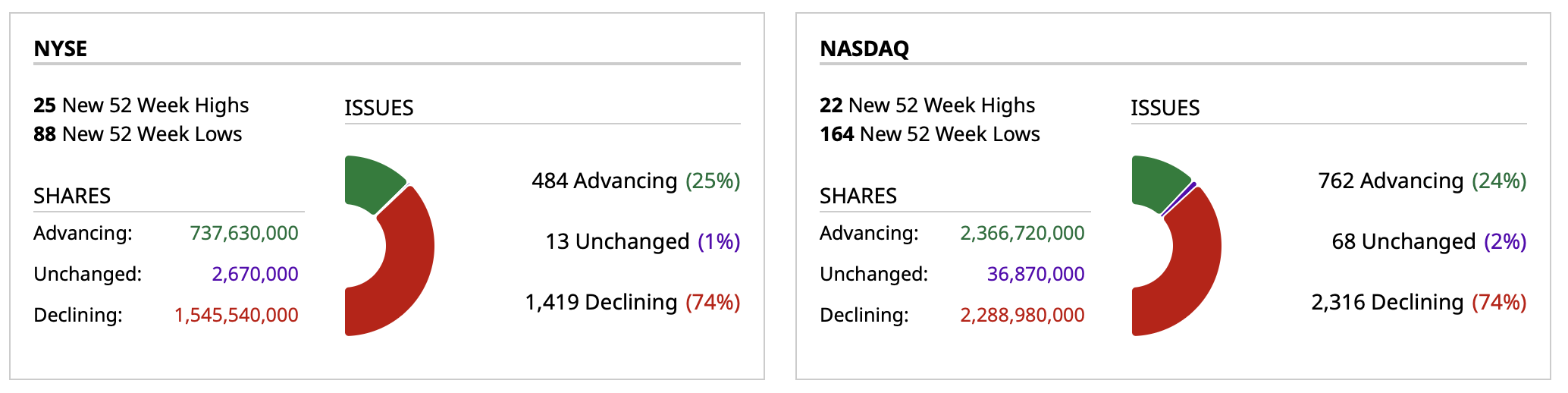

Breadth is weak but improved from earlier in the morning. However, the advance/decline line showing breadth (upper graph) isn't keeping up with the advance of the SPY (lower graph):

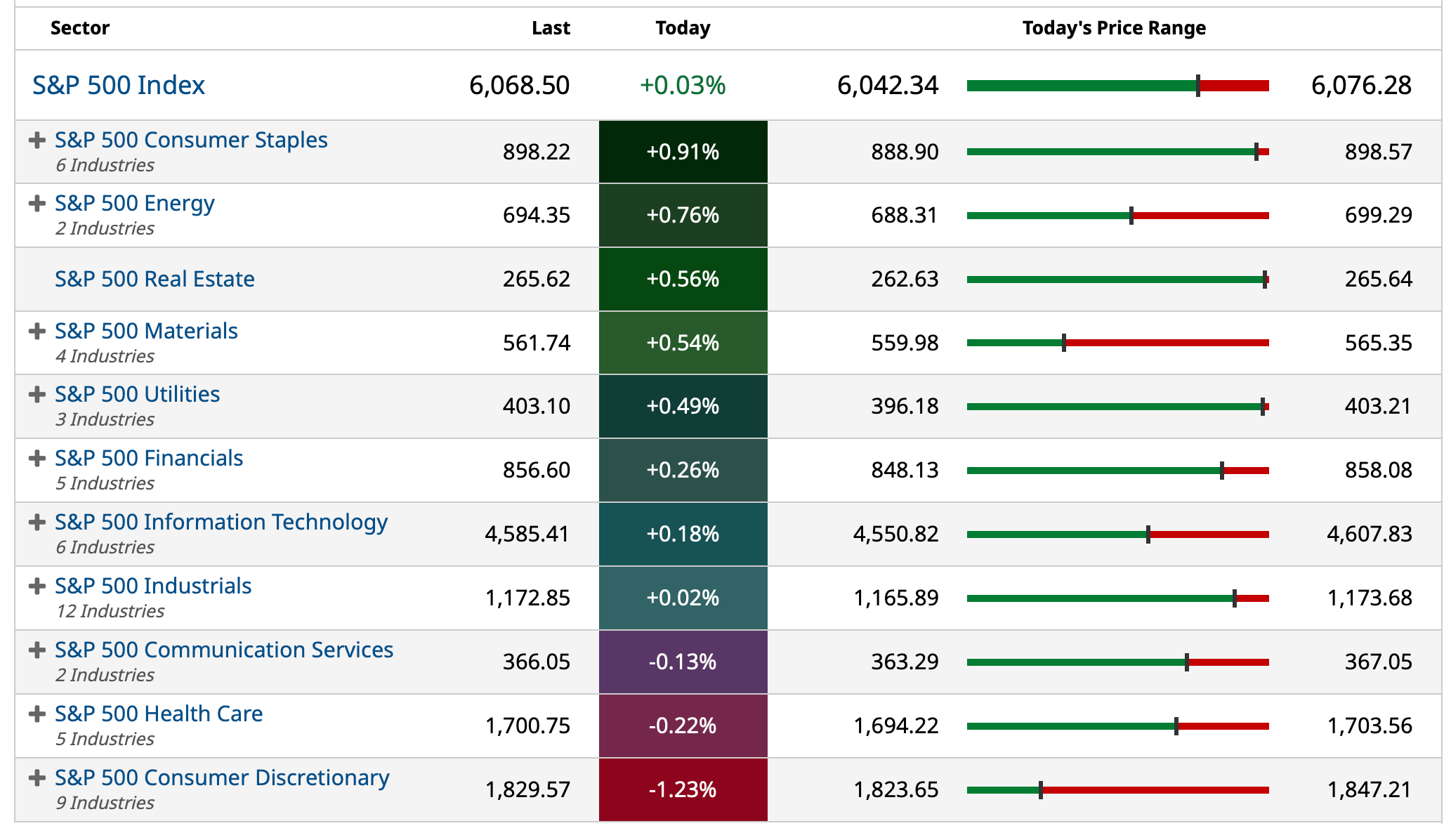

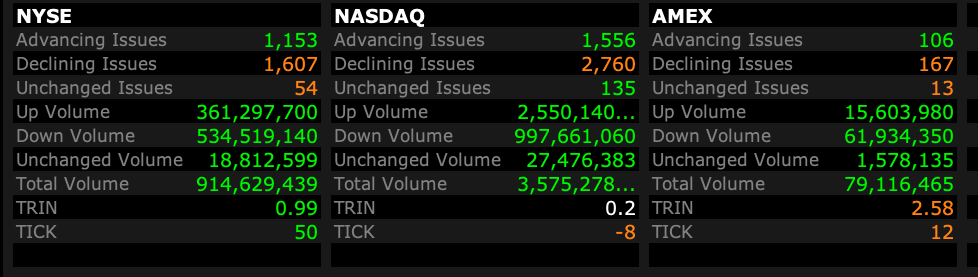

At 3:30 p.m. S&P cash is +3 handles (skewed positively by Apple AAPL and JPMorgan Chase JPM and the equal weighted S&P Index RSP is down by 0.11% and IWM is -0.66%:

Here are today's "Things":

* I actively (and profitably) traded Index common and calls — covering on weakness and shorting on strength.

* I added to MSOS $3.48 and CURLF $1.44 and TCNNF $4.71.

* I shorted JPM $275.35.

BY Doug Kass · Feb 11, 2025, 3:44 PM EST

Strength in JPMorgan Chase JPM and Apple AAPL are blurring what is an "uninspiring tape.

BY Doug Kass · Feb 11, 2025, 3:08 PM EST

I'm adding to my JPMorgan Chase JPM short at $274.50 and with S&P cash +4 handles I am shorting more SPY and QQQ calls.

I have also taken off my SPY and QQQ common (longs) at $606.05 and $528.58 (so getting more short).

BY Doug Kass · Feb 11, 2025, 2:07 PM EST

MRKT CALL with the boyz - Guy Adami and Dan Nathan.

Be there or be square.

Let's go to the tape! MRKT Call - Tuesday, February 11th

BY Doug Kass · Feb 11, 2025, 1:29 PM EST

I have a friend taking me for my birthday lunch.

I will be out from noon to 1:30 today

BY Doug Kass · Feb 11, 2025, 11:35 AM EST

- NYSE volume is 8% below its one-month average;

- Nasdaq volume is 45% above its one-month average;

BY Doug Kass · Feb 11, 2025, 11:26 AM EST

BY Doug Kass · Feb 11, 2025, 11:15 AM EST

* At 11 a.m.:

While markets have rallied smartly (in the aggregate) from the morning lows I will make the same cautious remark - it is not broadening.

Consider that:

* RSP (equal weighted S and P Index) -0.24%

* IWM 0.40%

I am scaling further into shorts.

BY Doug Kass · Feb 11, 2025, 11:06 AM EST

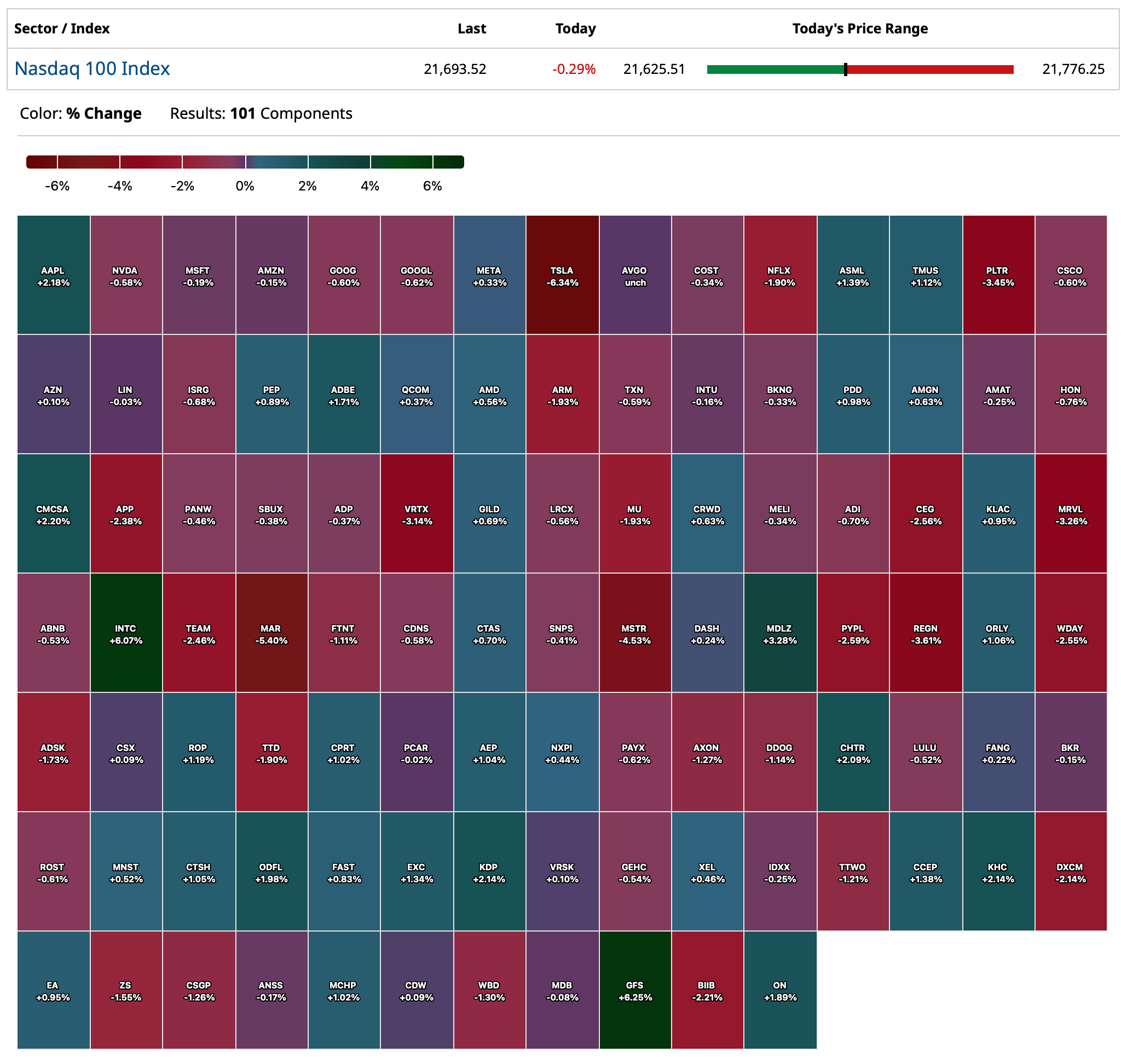

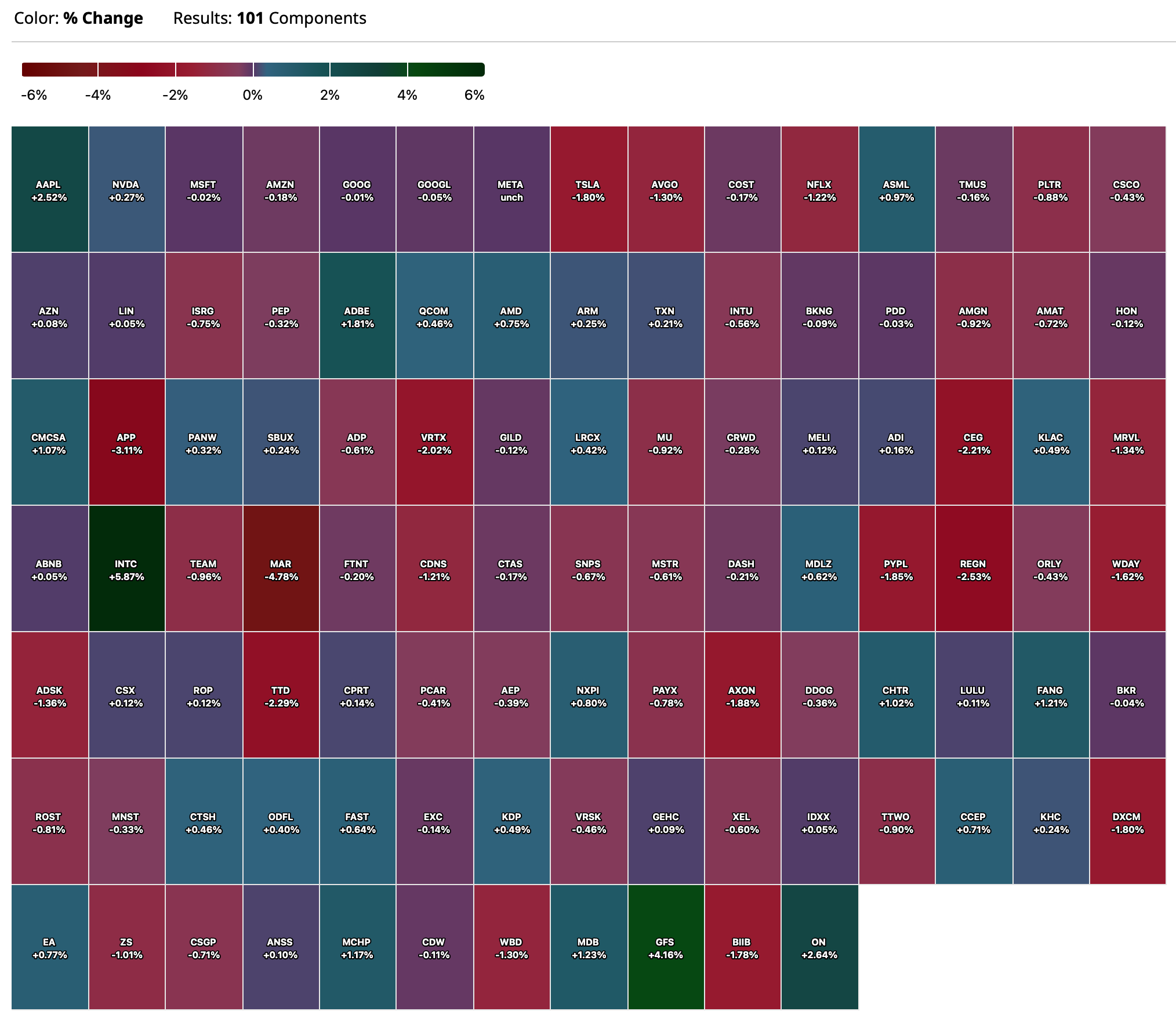

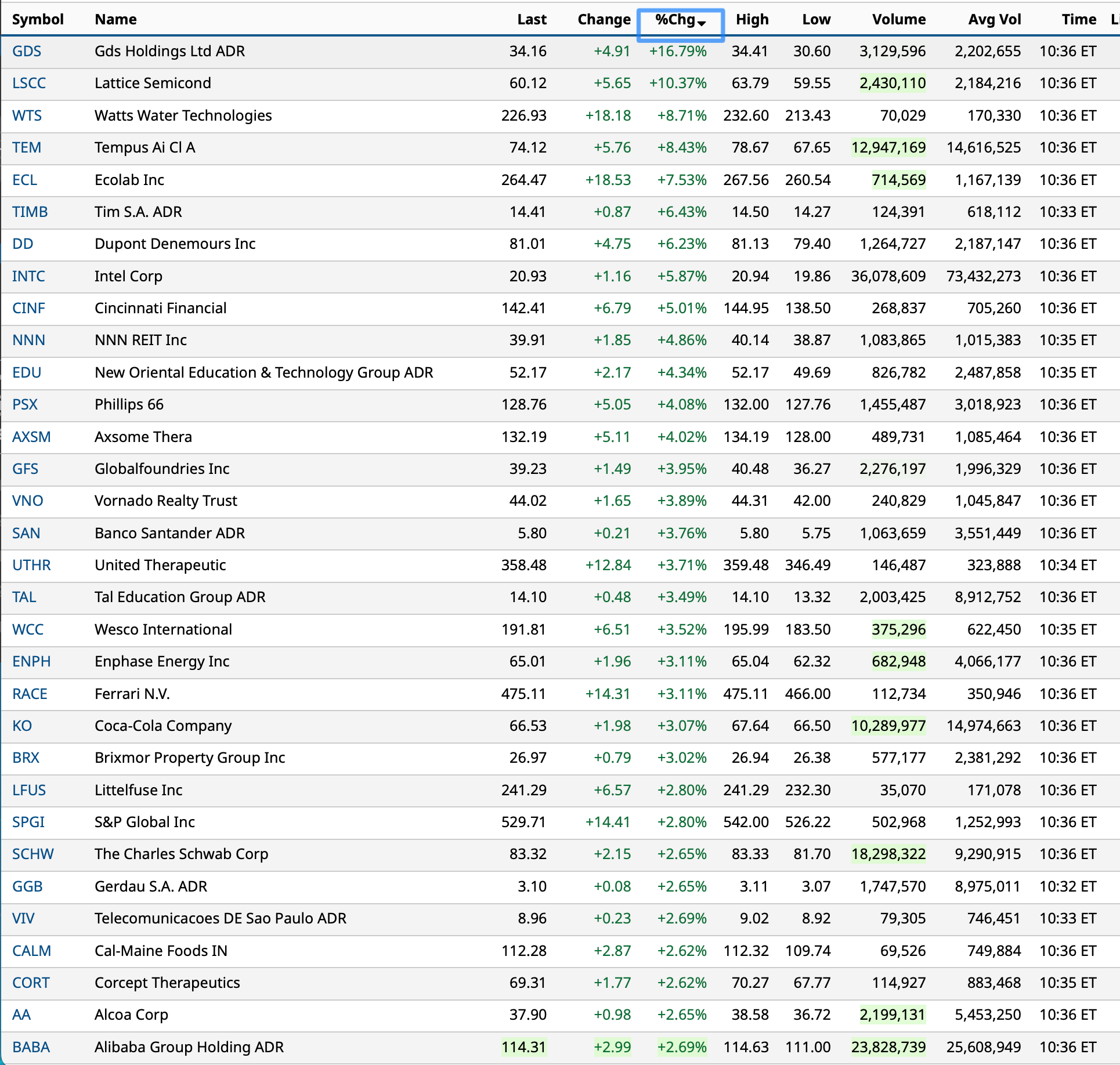

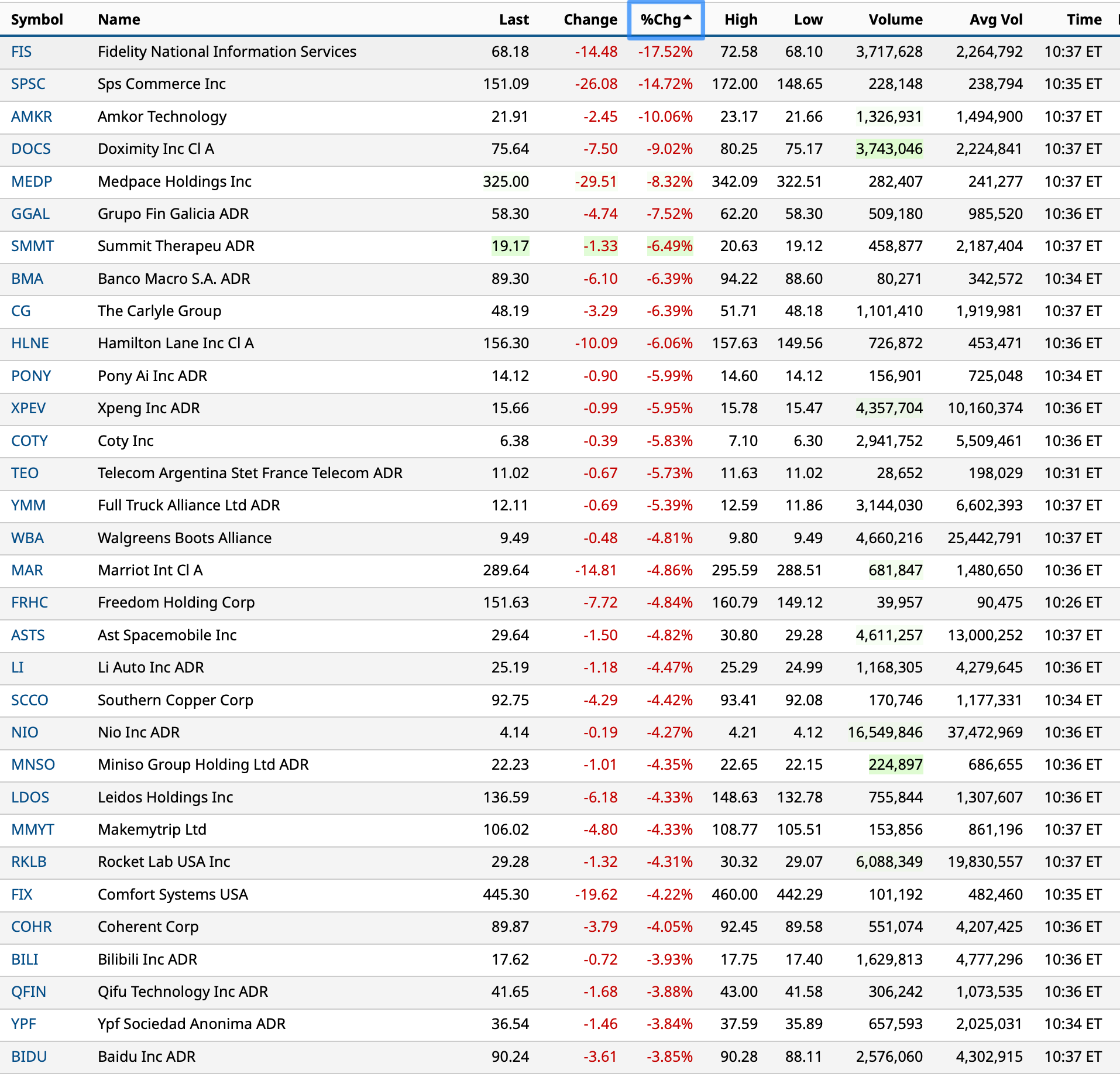

Large-cap stocks: percent gainers, percent decliners as of 10:36 a.m.:

BY Doug Kass · Feb 11, 2025, 10:56 AM EST

With S&P cash basically breakeven I am adding to my short Index calls.

BY Doug Kass · Feb 11, 2025, 10:52 AM EST

From Peter Boockvar:

Sticking to what I believe was Jay Powell’s goal today with his prepared text, to say nothing new and reveal no breaking news, he reiterated what the Fed said at their January meeting as “With our policy stance now significantly less restrictive than it had been and the economy remaining strong, we do not need to be in a hurry to adjust our policy stance.”

The rest of the speech goes over the labor market and inflation but says nothing we don’t already know. We’ll have to now wait for the Q&A and hope he gets some smart questions, though many times that can be an elusive task.

BY Doug Kass · Feb 11, 2025, 10:41 AM EST

"Can maintain policy restraint for longer if the economy remains strong and inflation does not move toward 2%"

- Text release for semiannual address

- Conditions in the labor market are broadly in balance - Fed is attentive to risks on both sides of the mandate

- Policy is well positioned for risks and uncertainties

- The unemployment rate is low and steady; Labor market is solid and not a source of inflationary pressures

- We don't need to be in a hurry to adjust policy

- Framework review will not include a focus on inflation target, which will remain at 2%; Long term inflation expectations remain anchored; Framework review will wrap up by late summer

- U.S. economy is strong overall; Inflation is closer to 2% goal, but remains somewhat elevated

https://www.federalreserve.gov/newsevents/testimony/powell20250211a.htm

BY Doug Kass · Feb 11, 2025, 10:24 AM EST

*Glass House Brands...

The company said:

"Turning now to full year 2024 preliminary results, our updated guidance implies the following full year results: We expect that revenue will be a record high $200 to $202 million, up 25% year-over-year versus the midpoint of updated guidance and representing a compound average annual growth rate of 47% since 2021.

We project the full year average selling price for wholesale biomass to exceed $243 per pound, versus $312 per pound in 2023. We anticipate full year 2024 cost of production will be below $125 per pound, versus $136 in 2023. We expect combined 2024 Retail and Wholesale CPG revenue to exceed $61 million and we project that both business segments grew by over 10% year-on-year, respectively.

As regards retail, adjusting out the effect of our Turlock store which was opened in April 2023, we expect same store sales will grow around 10% outpacing the overall California retail market, which fell by 6% per Headset data, by an astonishing 16 percentage points. We anticipate that full year 2024 consolidated gross margin will be in the high 40% range, compared to 50.3% in 2023. We are very pleased with our team's performance, given the more than 20% decline in average wholesale biomass selling price and the deep discounts that characterized our retail dispensary strategic pricing plan. This performance has been enabled by reduced cultivation costs, tight cost management within the retail operation and the cost saving initiatives we applied in our CPG supply chain and manufacturing processes. We project that full year 2024 adjusted EBITDA will be $38 to $40 million, our second straight year of positive adjusted EBITDA and a 59% year-over-year increase at the midpoint of updated guidance, as well as a nearly $60 million increase versus 2022.

We started 2024 with $33 million in cash and restricted cash and expect to end it with approximately $37 million. This was accomplished with minimal fund-raising. We anticipate that operating cash flow will be between $27 million to $29 million, a 21% increase at the midpoint of updated guidance versus 2023 despite start-up working capital investment in Greenhouse 5. As previously announced, during December 2024 the Company implemented a new $25 million at-the-market share distribution program, intended to increase its financial flexibility and support its expansion plans.

During the fourth quarter of 2024, we made limited use of the facility as we felt market conditions were not well-suited to fund-raising. In all, we sold 10,000 common equity shares at an average price of $6.72 per share for aggregate net proceeds of approximately $65,600. We began Phase III expansion in the fourth quarter of last year, beginning the retrofit of Greenhouse 2 along with investment in ancillary support facilities. Consistent with prior guidance, we expect to start generating revenue from Greenhouse 2 by the fourth quarter of 2025, with production estimated at 275,000 pounds in its first full year. As regards the potential commercial sale and distribution of hemp-derived cannabis, we continue to closely monitor both state and federal regulatory developments with a view to announcing our hemp strategy during Q2 2025.

BY Doug Kass · Feb 11, 2025, 9:55 AM EST

Buying MSOS $3.54.

BY Doug Kass · Feb 11, 2025, 9:49 AM EST

With S&P cash rallying off the lows and now -13 handles I am averaging back into short Index calls.

BY Doug Kass · Feb 11, 2025, 9:42 AM EST

BY Doug Kass · Feb 11, 2025, 9:30 AM EST

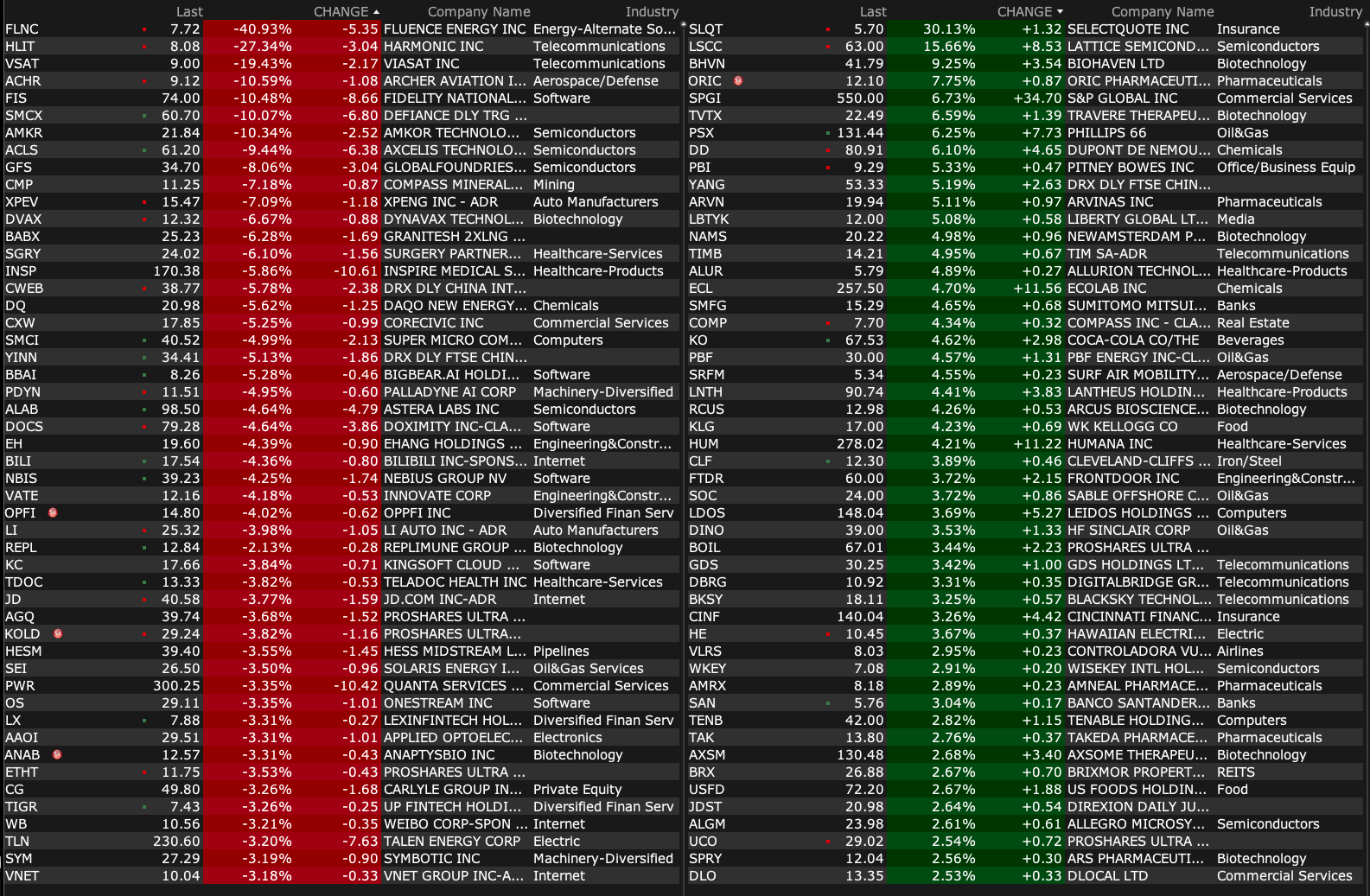

Premarket percentage movers at 8:54 a.m. ET:

BY Doug Kass · Feb 11, 2025, 9:21 AM EST

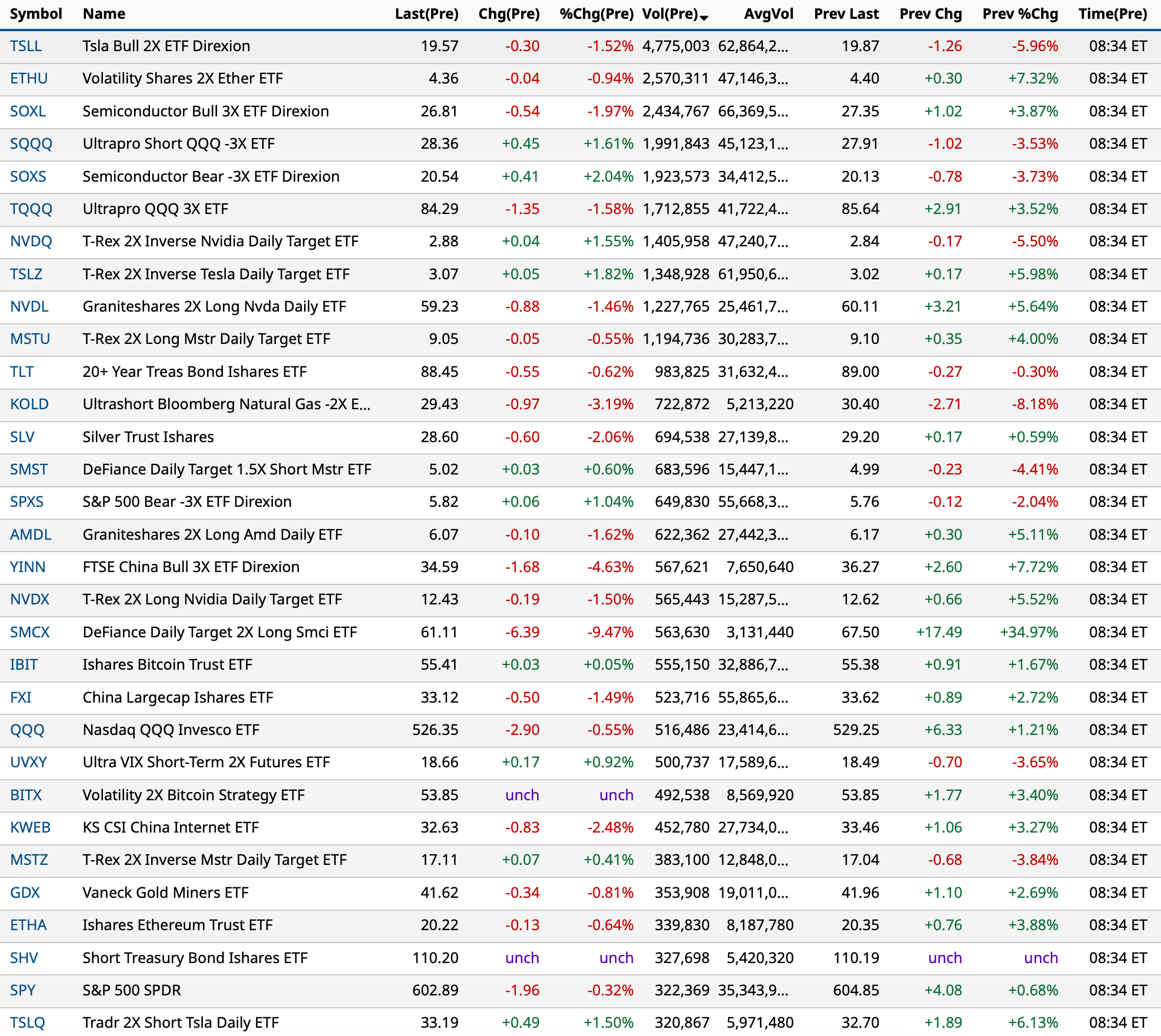

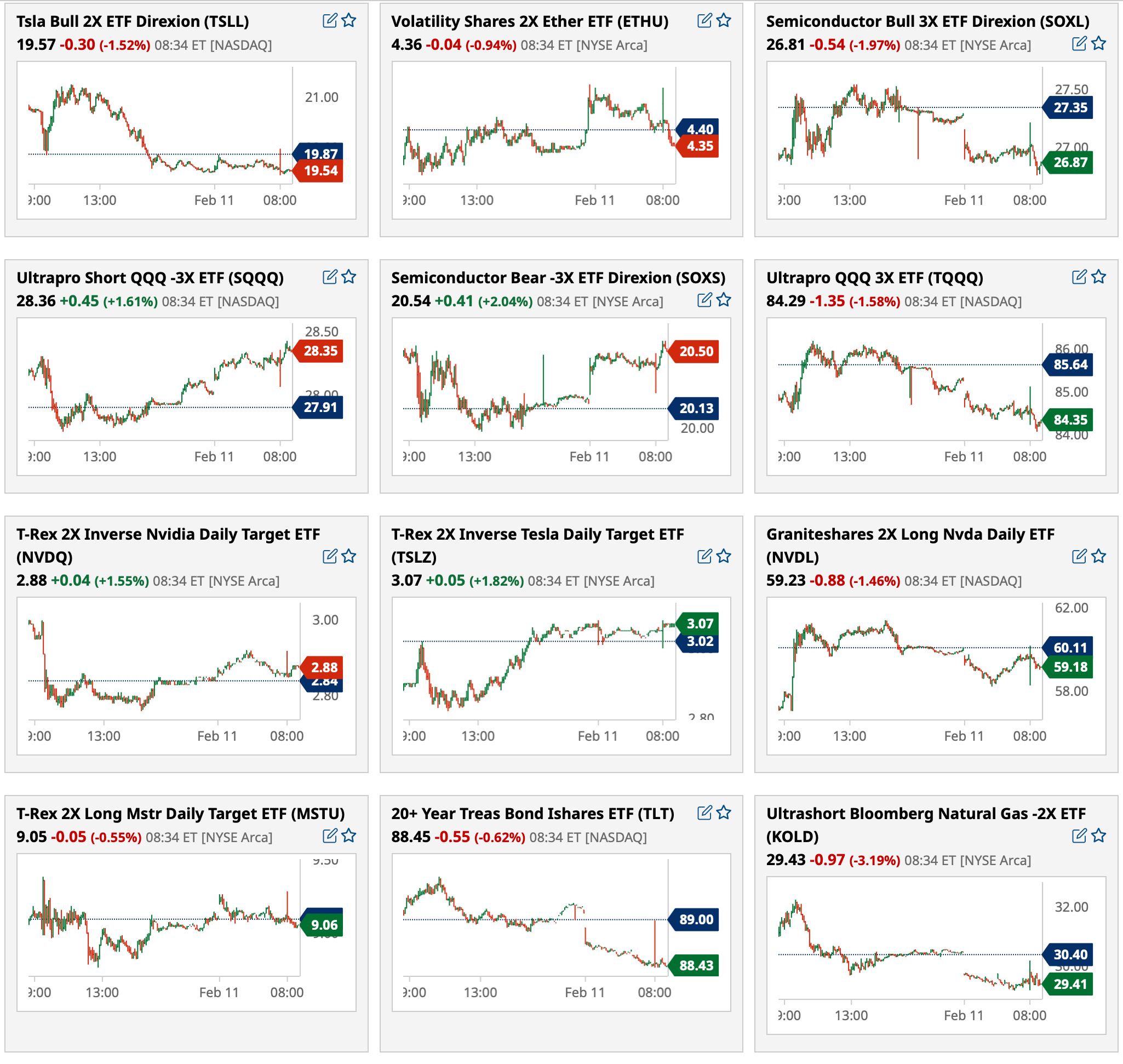

Most active premarket ETFs as of 8:34 a.m. ET:

BY Doug Kass · Feb 11, 2025, 9:09 AM EST

-SLQT +29% (earnings, guidance)

-LSCC +15% (earnings, guidance)

-ZBH +11% (files to sell 2-year, 5-year and 10-year notes)

-PSX +6.6% (Holder Elliott to push Co to spin off or sell midstream ops)

-ECL +4.5% (earnings, guidance)

-KLG +4.2% (earnings, guidance)

-SPGI +4.2% (earnings, guidance; announces share repurchase, raises dividend)

-KO +3.2% (earnings, guidance)

-BRX +2.7% (earnings, guidance)

-RLGT +2.7% (earnings)

-IONQ +2.6% (IonQ and General Dynamics Information Technology (GDIT) Partner to Develop Quantum Solutions for Customers in the U.S.)

-XRAY +2.5% (initiates review of Strategic Alternatives for Wellspect Healthcare)

-HUM +2.4% (earnings, guidance)

-HYPR -18% (files to sell 4.51M shares at $1.33/shr in $6.0M registered direct offering)

-PETS -18% (earnings)

-FIS -9.9% (earnings, guidance)

-AMKR -9.2% (earnings, guidance)

-ACLS -8.8% (earnings, guidance)

-GFS -5.6% (earnings, guidance)

-CXW -5.3% (earnings, guidance)

-MEDP -5.2% (earnings, guidance)

-ALAB -4.6% (earnings, guidance)

-JRSH -4.1% (earnings, guidance)

-INSP -3.9% (earnings, guidance)

-HESM -3.6% (prices 11M shares for selling stockholder [BlackRock] at $39.45/share; gross proceeds $434.0M)

-SHOP -3.3% (earnings, guidance)

-JD -3.2% (said to enter food delivery market in China with 'JD Takeaway')

-LCII -2.8% (earnings)

-COTY -2.4% (earnings, guidance)

-PDD -2.4% (reportedly Temu overhauls supply chain after tariffs, risking price hikes)

-WCC -2.3% (earnings, guidance)

BY Doug Kass · Feb 11, 2025, 9:00 AM EST

From Peter Boockvar:

I'm guessing that Jay Powell today in his testimony and Q&A in front of the Senate Banking Committee, is going to do his best to not lean in any one direction when it comes to rates, especially with still a month to go before the next FOMC gathering. Also, how can anyone have much confidence in forecasting growth and inflation trends in light of the weekly tariff possibilities, some threatened, some implemented at the same time we await the plans to extend the expiring tax cuts.

After a very optimistic response in November and December to the Trump win, the NFIB small business optimism index slipped back a bit in January to 102.8 from 105.1 and vs 101.7 in November though still well above the 93.7 in October. There were slight pullbacks in most of the categories. The one that stands out was the 7 pt drop in the 'Increased Capital Spending' category after the jump in the two prior months.

Also, higher for longer interest rates still really matters as the average rate paid on a loan was 9.4% vs 8.7% in December. For perspective, it averaged 6.2% over the past 20 years.

The bottom line from the NFIB, "Overall, small business owners remain optimistic regarding future business conditions, but uncertainty is on the rise. Hiring challenges continue to frustrate Main Street owners as they struggle to find qualified workers to fill their many open positions. Meanwhile, fewer plan capital investments as they prepare for the months ahead."

I'll add, in terms of visibility with tariffs, as we know they are here with more coming, ideally, they all come sooner rather than later so business can start planning around them now rather than being in complete limbo wondering if they get hit and when.

NFIB

Average Rate Paid on a Loan

On to some earnings comments where FX has become a bigger headwind and there is still a mixed macro environment.

From McDonald's whose stock had a nice day, up 4.8% but they were still cautious on their consumer:

"the QSR industry remained challenged and our performance in 2024 fell short of our expectations. Pressure on spending persists, in particular with two significant cohorts of our consumer base, low income and families, particularly in Europe."

"Throughout November and December, we saw sequential improvement in baseline traffic performance, including slightly positive comp guest count growth for the month of December and had a positive comp guest comp gap to most near end competitors for the 4th quarter. These results were driven by our marketing efforts to amplify traffic drivers."

They were also downbeat on the UK consumer. "There's a cost of living issue that exists in the UK, that is putting pressure on the low income consumers consistent with what we've seen in the US that's also putting pressure on families."

On the US dollar strength, "we expect foreign currency to be a full year headwind to 2025 EPS totaling in the range of $.20-$.30 based on current exchange rates."

From American Express whose stock fell to near a one month low after speaking at the UBS Financial Services conference:

In giving guidance, "I think Q1's expectations are too high." In part due to "the strength of the US dollar is a headwind to our growth. And the dollar is a bit stronger now than it was in late December."

They were otherwise positive on the travel and entertainment spend that drives a big part of their business.

Coca Cola, a stock we own, had a solid quarter even with FX headwinds. For full year 2025, "the company expects a 3% to 4% currency headwind based on the current rates and including the impact of hedged positions." They still expect organic revenue growth of 5% to 6%.

From Edgewell, the maker of everything from Schick razors, Banana Boat suntan lotion and Wet Ones and whose stock fell 9.5% yesterday:

They also talked about the FX headwind. They described "an external environment that has become increasingly more volatile and uncertain. Largely driven by the strengthening of the US dollar. Organic net sales were down slightly vs last year, but in line with our expectations with a sequential improvement over recent trend."

"Consumers remain resilient and at the same time cautious. Though in our categories, which are mostly non-discretionary and everyday use, we see no material signs of purchasing hesitancy nor trade down behavior. Having said that, the US wet shave and sun care categories remain highly competitive and promotional."

From Coty, the cosmetics and fragrance maker:

They saw revenue down 1% y/o/y which "included a 2% negative impact from FX" among other things.

Also, "The Q2 reported sales reflected the further slowing of the mass beauty market, particularly color cosmetics, together with continued headwinds in the APAC region, particularly China, travel retail Asia and Australia." They also cited pressure in their "Consumer Beauty US."

At the same time, "the global fragrance market remained robust."

From ON Semiconductor whose stock fell 8% and who doesn't have much AI end market exposure:

"As for the market environment, demand declined late in the quarter and continued into January...Regional revenue declined sequentially except North America, which remained flat with Japan seeing the sharpest decline. Q/o/q declines were driven primarily by our non-core market segments. Amid a backdrop of end market softness and geopolitical uncertainty, inventory digestion persists across our key end markets."

Specifically with their auto business, China was strong, growing revenue 18% q/o/q. That said, "Demand from all other regions weakened towards the end of the fourth quarter, which continued into Q1. In the US, Tier 1s have been impacted by lower global auto demand than expected in the fourth quarter, along with slower EV ramp than anticipated. Entering Q1, we expect persisting volatility due to the geopolitical uncertainty across all geographies as our customers assess their manufacturing footprints and the impact of tariffs." They also saw a slowdown in EV sales in Europe.

"Our industrial revenue decreased 5% sequentially, with weakness in the traditional parts of the business. The PMI across all major regions remained weak and the slowdown in manufacturing activity is further compounded by ongoing inventory digestion and we expect the weakness to persist into 2025."

AI data center and aerospace/defense is where they are seeing the fastest growth but is a smaller part of their overall business.

From Lattice Semi, who has similar end markets to ON but whose stock is jumping pre market because of a positive guide:

"On an end market basis, communications and computing was down 5% sequentially and industrial/automotive was down 9%, primarily due to continued inventory normalization."

"Looking ahead, as you heard during last quarter's earnings call, we expect more of a U-shaped recovery in 2025. We are very pleased to be guiding our Q1 EPS above the current consensus estimates in a quarter when other companies in our industry are expecting a guide down."

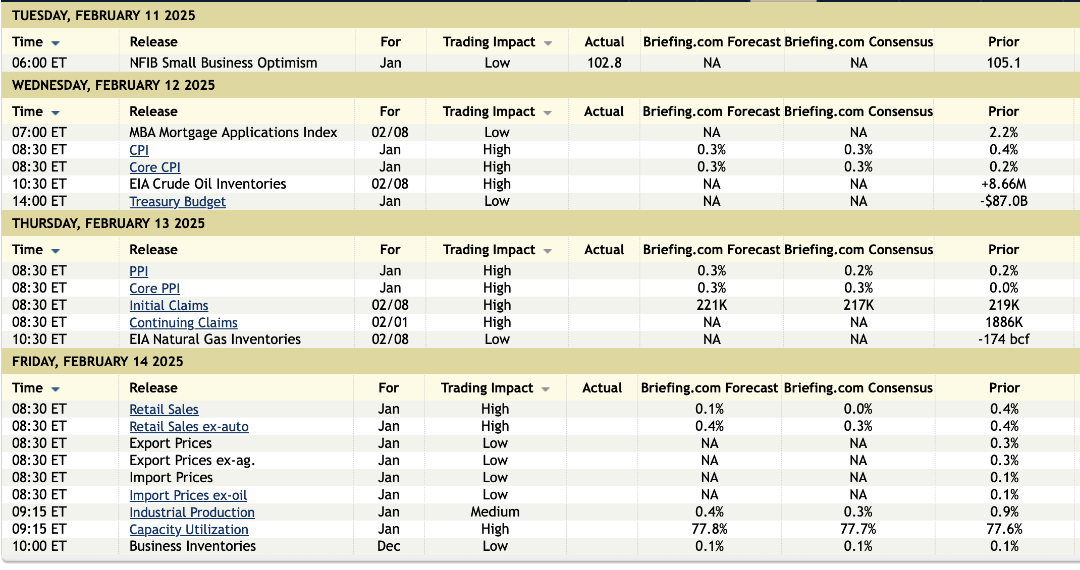

BY Doug Kass · Feb 11, 2025, 8:35 AM EST

8:50AM: Fed Bank of Cleveland President Hammack (Non-Voter) speaks on the economic outlook before the University of Kentucky Gatton School of Business and Economics 2025 Economic Outlook Conference, Lexington, KY

10:00AM: Fed Chair Powell hearing on "The Semiannual Monetary Policy Report to the Congress". before the Senate Banking Committee; NYC

3:30PM: Fed Bank of New York President Williams (Voter) gives keynote remarks before the Pace University Economics Society, NYC

3:30PM: Fed Board Governor Bowman (Voter) speaks on "Bank Regulation" before the2025 Iowa Bankers Association Bank Management and Policy Conference, Des Moines, IA

BY Doug Kass · Feb 11, 2025, 8:15 AM EST

BY Doug Kass · Feb 11, 2025, 8:04 AM EST

* And certainly not recommended without doing your homework!

I have a number (10-15!) positions in my hedge funds that have not been disclosed.

As noted in the past there are multiple reasons why this is the case:

* The positions may be small and analysis not complete.

* In the case of selected shorts I want to continue to have access to management. (If I disclosed a short and management became aware, I would likely lose that access!)

* The positions may be very speculative and not suitable in most portfolios.

Some holdings include shorts MSTR (very small,cost basis much higher) and PLTR (small, cost basis of $116.65 - put on very recently) and longs PSIL (small, cost basis $14) and BABA (small, cost basis around $92).

Speaking of weightings, here is a repost of my guidelines:

Subscriber ireadstock asked me a question about my weightings and size designations.

Here's a reposting of a previous column from October 2023:

I have been asked by several subscribers about my weightings strategies.

Here is a repost that explains my methodology:

Apr 25, 2023 ' 07:39 AM EDT DOUG KASS

Over the last two weeks I have gotten a number of questions about my weightings.

Here is an important repost that answers most of the related questions:

Feb 13, 2023 ' 06:10 AM EST DOUG KASS

A reminder, that going forward, I will be disclosing size positions:

Feb 09, 2023 ' 01:30 PM EST DOUG KASS

* Going forward I am going to reintroduce my weightings of individual stocks and indexes in order for subscribers to better gauge my confidence levels

* But remember, everyone has a different risk profile and appetite. I am laser focused on risk control and conservative in portfolio construction

As I mentioned yesterday, in two columns -- Know Your Sweet Spot and Check This Out, patience and sizing -- get little commentary but are essential parts of managing money and in controlling risk.

As well, most should not even sell short.

Given the conversation about Tesla (TSLA) in our Comments Section today I wanted to repeat an important post I originally delivered over two years ago on shorting and sizing.

Dec 09, 2020 ' 09:30 AM EST DOUG KASS

* It's not fun, it's not easy, and most should not bother!

* But if you immerse yourself in the more dangerous waters of short selling, consider some of my techniques

I have long written that most people should not short stocks:

* Stocks typically move higher over time. Depending on the time frame analyzed, the major Indices have historically risen by about seven to eight percent annually over the last six to seven decades. The gravitational pull of stocks higher is a formidable headwind to short selling.

* When longs go against an investor, their portfolio weighting moves lower. However, when shorts go against an investor, their portfolio weighting moves higher.

* Many shorts are crowded (in short interest terms) - so short squeezes are commonplace in some of the more popular short names. This means you will not likely short a top!

* Tops in individual stocks tend to be a process - while bottoms in individual stocks tend to be events.

* Above all, reward vs. risk is asymmetric between longs and shorts. Longs can theoretically rise by an infinite percentage, or amount, but shorts can only decline by 100% - in a bankruptcy.

My long weightings (for individual stocks or for Index positions), on average, are typically larger than my short weighting (for individual stocks or for Index positions) for the reasons listed above:

For Individual Stock Longs (Revised)

Very Small: Under 0.75%

Small: Between 0.75% and 1.5%

Medium: Between 1.5% and 3%

Large: Between 3% and 5%

Very Large: Over 5%

For Individual Stock Shorts (Revised)

Very Small: Under 0.25%

Small: Between 0.25% and 1.0%

Medium: Between 1.0% and 2.0%

Large: Between 2.0% and 2.5%

For Index Longs

Small: Under 5%

Medium: Between 5% and 15%

Large: More than 15%

For Index Shorts

Small: Under 5%

Medium: Between 5% and 10%

Large: More than 10%

I have been short them all - the "shiny speculative objects" and gewgaws of the time like Iomega, Snapple, LA Gear, Home Shopping, AOL/Time Warner, etc.

And, though I have the scars on my back to show for some of these shorts, in the main I have profited mightily by adopting a methodology towards speculative, high octane shorts.

My approach is four-fold:

The last point is an important one. I am currently short Tesla (TSLA) . Three months ago I shorted the stock and made well over $100/share in only a few days. In this rendition, the shares have moved dramatically higher, though less than $100/share. The previous large short term short gain has been forgotten by most - just look at the reaction the move has made on my Twitter thread!

I have approached the $100/share move higher as an opportunity to, dispassionately, short more - ignoring the financial media's hyperbolic coverage, sticking with my analysis of "intrinsic value" for Tesla and I have not treated the position differently in emotional terms than any other long or short position in my portfolio. Most can not be as "level headed" in shorts compared to longs - stated simply they often panic at the wrong time.

Bottom Line

Most should avoid short selling.

But if you elect to travel in these more dangerous investment waters, consider smaller weightings than long positions, and give a short a "wider berth" when adding and stay unemotional.

By Doug Kass Oct 11, 2023 1:43 PM EDT

BY Doug Kass · Feb 11, 2025, 7:30 AM EST

* And over the next several years...

EXECUTIVE SUMMARY:

Housing analyst Melody has just revised her forecast, now predicting a

national decline in U.S. home prices in 2025. She expects the National

Association of Realtors (NAR) price index to drop by 9% and the Census

Bureau’s home price index to decline by 6%, though some individual

markets could experience steeper declines of up to 20%. This

adjustment comes after analyzing December 2024 data, which showed an

unexpected increase in home sales but also indications of distress

selling. The long-held belief that home prices would remain stable or

appreciate due to limited inventory is now being questioned as new

market dynamics emerge.

The U.S. housing market saw stronger-than-expected sales activity in

December 2024, particularly in markets where a slowdown had been

anticipated. However, this increase in transactions was not due to

organic demand, but rather motivated selling, including early signs of

distress sales. In key regions such as Los Angeles, Richmond (VA),

Indianapolis, Charlotte, and Washington, D.C., there was a notable

increase in sales activity, but a simultaneous drop in prices,

suggesting sellers are becoming more willing to accept lower offers.

The primary drivers of these sales include rising mortgage

delinquencies, job relocations, and financial pressure from higher

interest rates and insurance costs.

Several indicators suggest an increase in financial stress among

homeowners. The mortgage delinquency rate has been rising since

mid-2023, and foreclosure starts increased by 50% month-over-month and

29% year-over-year according to Black Knight’s December data.

Additionally, real estate professionals are seeing more cases of

sellers falling behind on payments while trying to offload properties

that have been sitting on the market for months. This wave of distress

sales is occurring even before any significant economic downturn or

job losses, suggesting that affordability pressures alone are leading

to market stress. If economic conditions deteriorate further, the

situation could worsen significantly.

The long-standing narrative that the U.S. faces a severe housing

shortage is now being challenged by recent research from the Cato

Institute and Taylor & Francis, which argue that the U.S. has actually

built 3.3 million more homes than needed when accounting for household

formation. This surplus is being compounded by a large wave of

multifamily housing completions, with over 500,000 new apartments

scheduled for delivery in 2025. Additionally, millions of baby boomers

will either sell their homes or pass away in the coming decade,

further increasing housing supply. This shift in the supply-demand

balance is already being observed in cities like Nashville, Richmond,

and Washington, D.C., where inventory levels are rising rapidly.

Many homeowners postponed critical decisions in 2024, anticipating

Federal Reserve rate cuts that have not materialized. However, 2025 is

expected to see a significant increase in forced home sales due to

life events such as death, divorce, and financial distress. The

National Association of Realtors (NAR) and the Census Bureau are

expected to revise down home price estimates over time, just as they

did in 2011 when they had to correct four years’ worth of inflated

home price data. The reality is that many sellers will not be able to

continue waiting, especially as financial pressures mount.

The stock market boom since 2023, which helped some high-net-worth

buyers stay active in the housing market, may not provide the same

cushion going forward. Additionally, the cost of homeownership

continues to rise, with insurance costs in disaster-prone areas

increasing significantly. For example, State Farm has announced a 22%

rate hike due to the financial strain from natural disasters. This

could further discourage homeownership in key states like California,

Florida, and Texas, where property insurance is becoming prohibitively

expensive. Additionally, bankruptcies are rising in sectors tied to

the housing market, including remodeling firms, cabinetry

manufacturers, and home improvement services, signaling a slowdown in

discretionary spending.

The housing correction could play a central role in triggering a

broader economic downturn, much like the Great Financial Crisis (GFC)

of 2008, though for different reasons. Unlike the last crisis, which

was fueled by subprime mortgage lending, the current market faces a

sharp affordability crisis where many homeowners simply cannot sustain

their mortgage payments. If home prices decline as predicted, the

negative wealth effect could significantly impact consumer spending,

as homeowners perceive themselves as poorer when their property values

drop. This could lead to a broader economic contraction as households

cut back on discretionary spending, affecting businesses and

employment in multiple industries.

Homeowners considering selling should act sooner rather than later to

avoid a more competitive market with rising inventory and declining

prices. Listing now could provide an opportunity to lock in a buyer

before the full effects of distress selling and forced inventory

growth take hold. On the other hand, potential buyers, especially

first-time homebuyers, should exercise caution. While declining prices

may make homes seem more affordable, buying in a falling market

carries risks, particularly if there is uncertainty about future

employment or relocation. Investors in rental properties should also

reevaluate their portfolios, as many short-term rental markets are

oversaturated and suffering from declining occupancy rates. In short,

both buyers and sellers need to carefully assess their positions and

make decisions based on market realities rather than outdated

narratives.

BY Doug Kass · Feb 11, 2025, 6:55 AM EST

BY Doug Kass · Feb 11, 2025, 6:35 AM EST

BY Doug Kass · Feb 11, 2025, 6:25 AM EST

BY Doug Kass · Feb 11, 2025, 6:15 AM EST

* For now, but....

I ended yesterday with these observations:

With the equal weight Indices doing nothing, the Russell Index not crowing, the "generals" (e.g. (NVDA) , (GOOGL) and (AAPL) ) rolling over and volume rising on down days (and declining on up days)... where's the market's beef?

By Doug Kass Feb 10, 2025 12:25 PM EST

Bull markets die hard.

So, for now, I am shorting the rips and covering the dips — but I think a break in the rallies might soon be at hand.

S&P futures -21 handles at 5:45 PM.

BY Doug Kass · Feb 11, 2025, 6:05 AM EST

No real change in the S&P Short Term Oscillator — standing at 0.87% vs. 0.78%.

BY Doug Kass · Feb 11, 2025, 5:55 AM EST

In premarket trading (4:30 AM) I covered my short Indices (for a small gain from yesterday):

* SPY $602.95

* QQQ $527.11

On my short SPY/QQQ calls I bought stock (at prices above) to create a buy/write.

BY Doug Kass · Feb 11, 2025, 5:45 AM EST