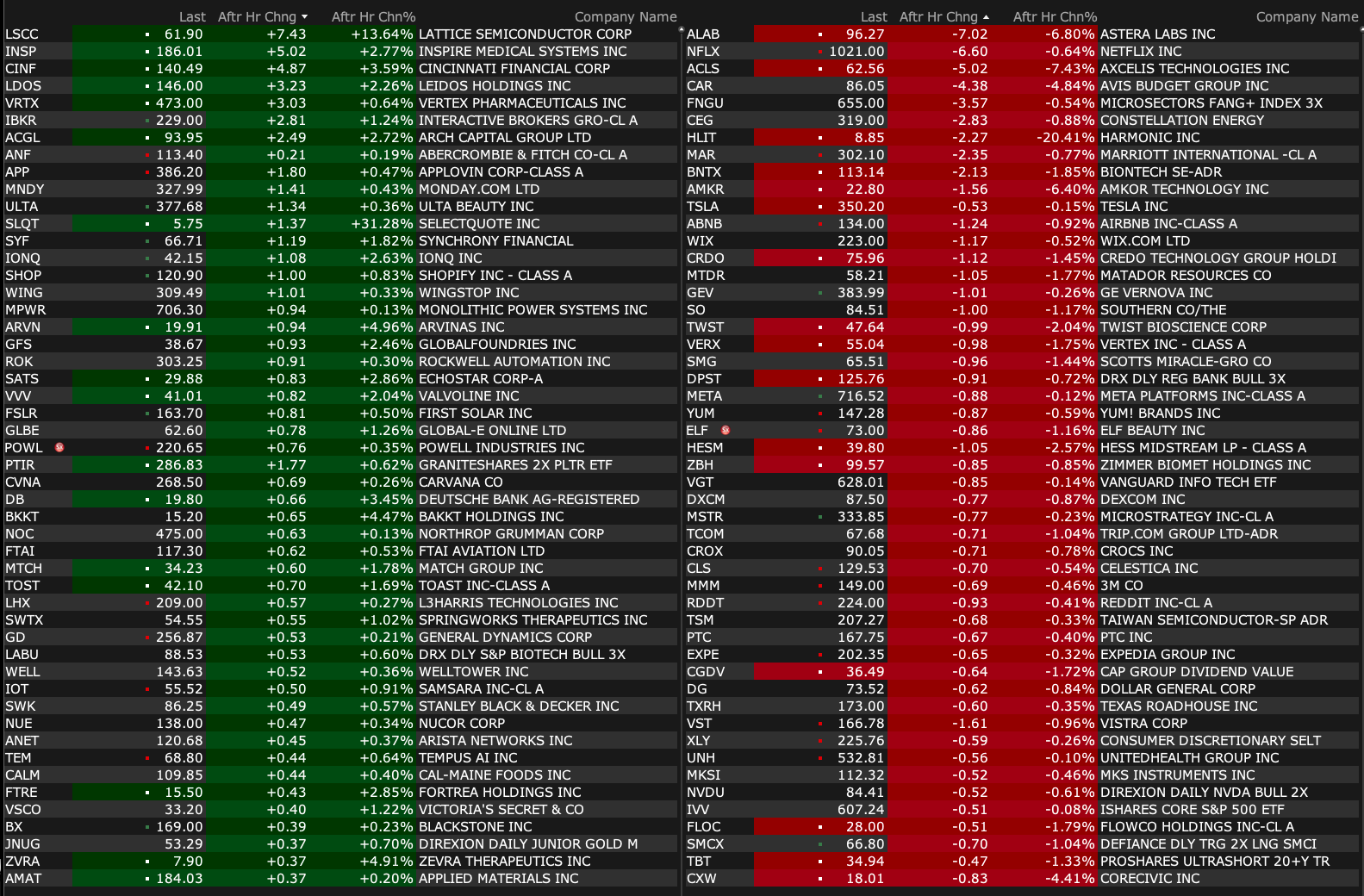

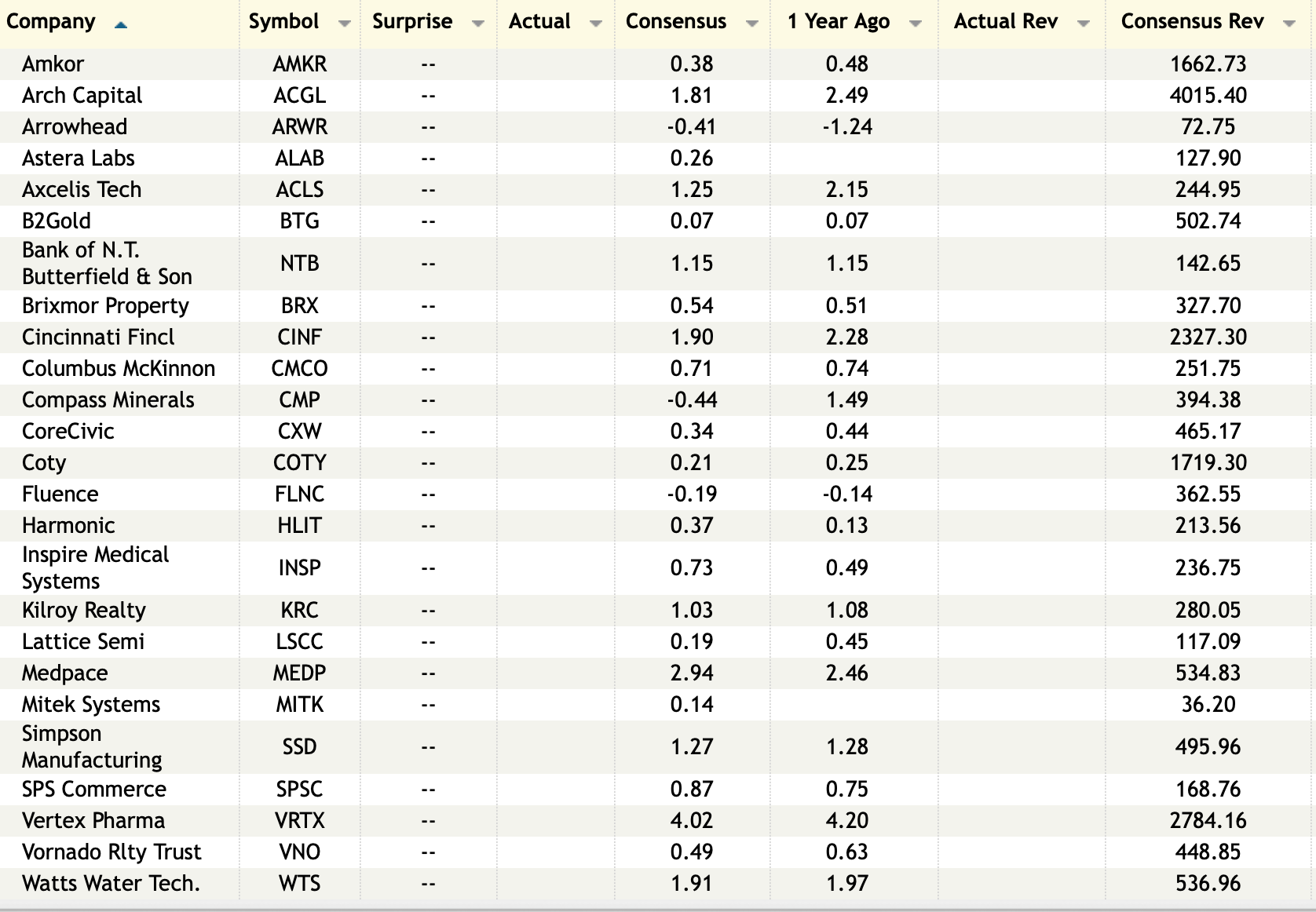

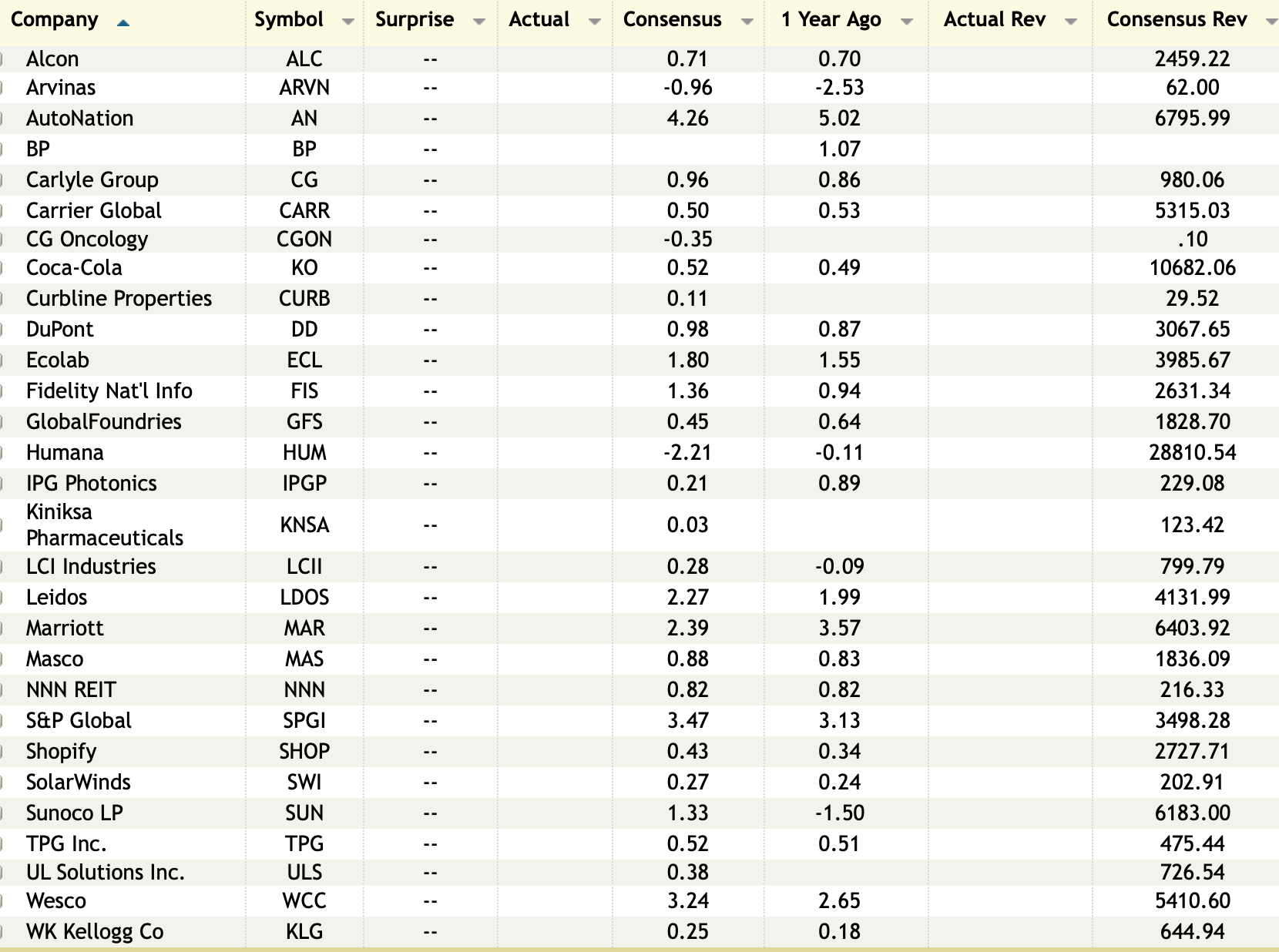

Monday's After-Hours Movers

At 4:20 p.m.:

BY Doug Kass · Feb 10, 2025, 4:55 PM EST

At 4:20 p.m.:

BY Doug Kass · Feb 10, 2025, 4:55 PM EST

BY Doug Kass · Feb 10, 2025, 4:38 PM EST

BY Doug Kass · Feb 10, 2025, 3:54 PM EST

This news created a bid in MSOS.

DEA Official Says Marijuana Rescheduling Is “Delayed, But Certainly Not Dead”

BY Doug Kass · Feb 10, 2025, 3:51 PM EST

I have a 3:15 PM research call.

I will back at the close.

BY Doug Kass · Feb 10, 2025, 3:20 PM EST

skeptcl

NVDA: Nvidia added to 'Tactical Outperform' list at Evercore ISI ahead of earnings later this month

Evercore ISI is a buyer of Nvidia into the company's earnings call scheduled for February 26, noting that the stock had underperformed the S&P 500 by 9% over the past month as of February 7, which Evercore attributes to three investor concerns, namely that: 1) DeepSeek lowers AI demand in aggregate, 2) DeepSeek shifts AI compute-cycles away from NVDA GPUs and to ASICs, 3) Blackwell delays. Evercore conducted a dozen channel checks with senior AI engineers at the top hyperscalers, and found the following: 1) Related to concerns that DeepSeek developments lowers aggregate demand: consensus amongst the AI community is that DeepSeek cost improvements are evolutionary rather than revolutionary, and that lower cost/compute cycle or cost/token likely translates to increased demand for those tokens, which likely manifests in more accurate larger parameter models and/or an acceleration in the development of “multi-mode” models that train on images and videos. 2) Related to concern that DeepSeek shifts AI compute-cycles away from NVDA GPUs and to ASICs: a. NVDA remains the platform of choice for hyperscalers' customers, the robustness of its software ecosystem and breadth of its development community put it 5-10 years ahead of anything else in the market. b. ASICs will play a role for high-volume internal workloads, but external workloads like cloud and enterprise on-prem likely to remain dominated by NVDA

BY Doug Kass · Feb 10, 2025, 2:10 PM EST

I am working with a $3.55 limit in buying more MSOS now.

BY Doug Kass · Feb 10, 2025, 2:00 PM EST

With S&P cash +41 handles I am back shorting Index calls (in-the-money March monthlies) to complement my small Index common shorts.

BY Doug Kass · Feb 10, 2025, 1:49 PM EST

PPLT was $82 at the end of 2024 and is now trading a $91.

I sold my small position for a profit because it is up on "newsy" President Trump comments about monetizing the U.S. gold position.

I will buy back on weakness.

BY Doug Kass · Feb 10, 2025, 1:22 PM EST

Cannabis company ACB is bubbling up again (on very large volume). Will its meme status become contagious with the other weed stocks?

BY Doug Kass · Feb 10, 2025, 1:07 PM EST

BY Doug Kass · Feb 10, 2025, 12:54 PM EST

BY Doug Kass · Feb 10, 2025, 12:35 PM EST

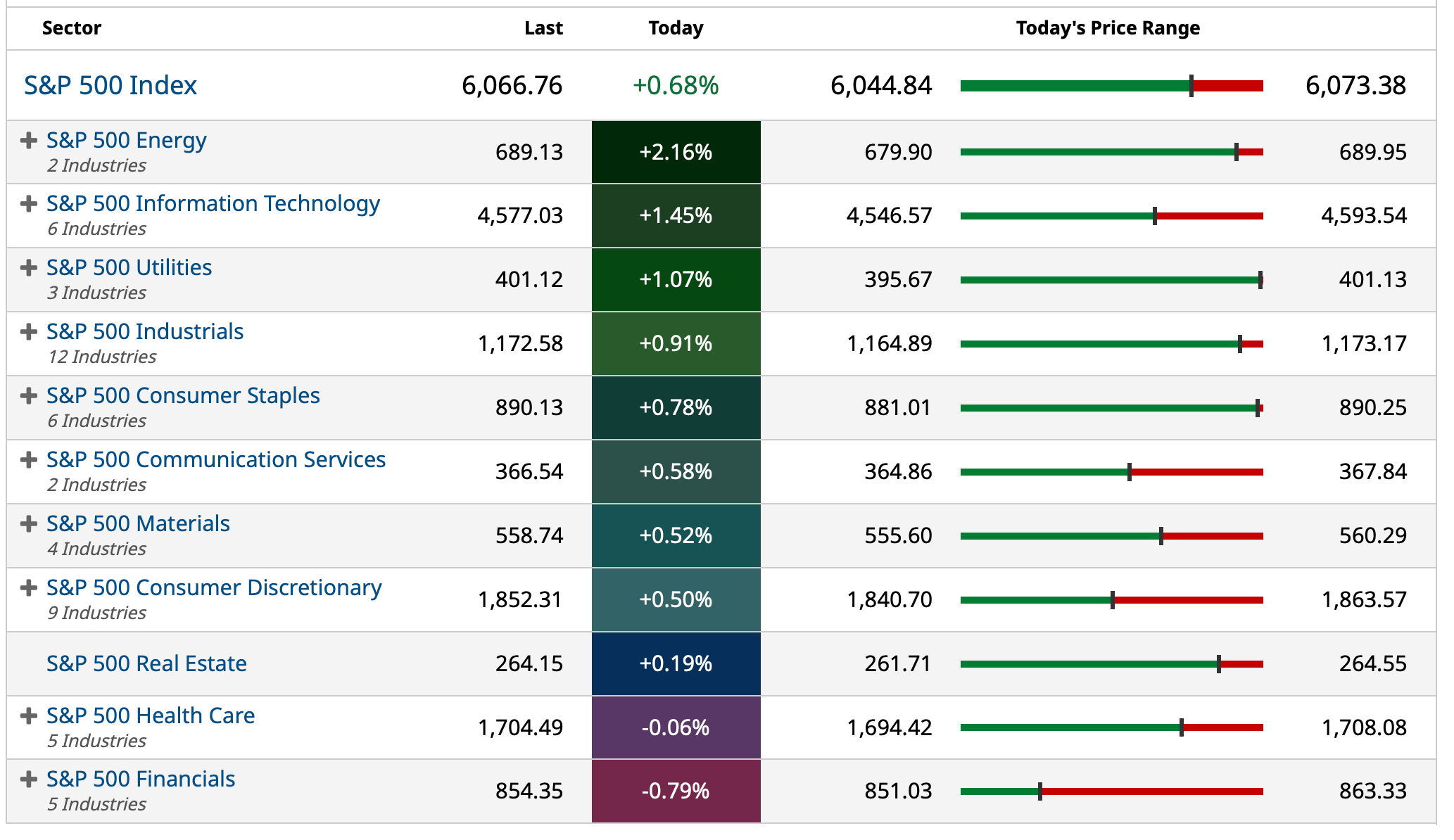

With the equal weight Indices doing nothing, the Russell Index not crowing, the "generals" (e.g. NVDA, GOOGL and AAPL) rolling over and volume rising on down days (and declining on up days)... where's the market's beef?

BY Doug Kass · Feb 10, 2025, 12:25 PM EST

My intention is now to move to very large in MSOS — on the bid side.

BY Doug Kass · Feb 10, 2025, 12:00 PM EST

I covered small JPMorgan Chase JPM at $269.95 (-$5.80).

BY Doug Kass · Feb 10, 2025, 11:40 AM EST

BY Doug Kass · Feb 10, 2025, 11:35 AM EST

* Based on a divergence... "not broadening"

I am prompted to add to my short exposure given this divergence:

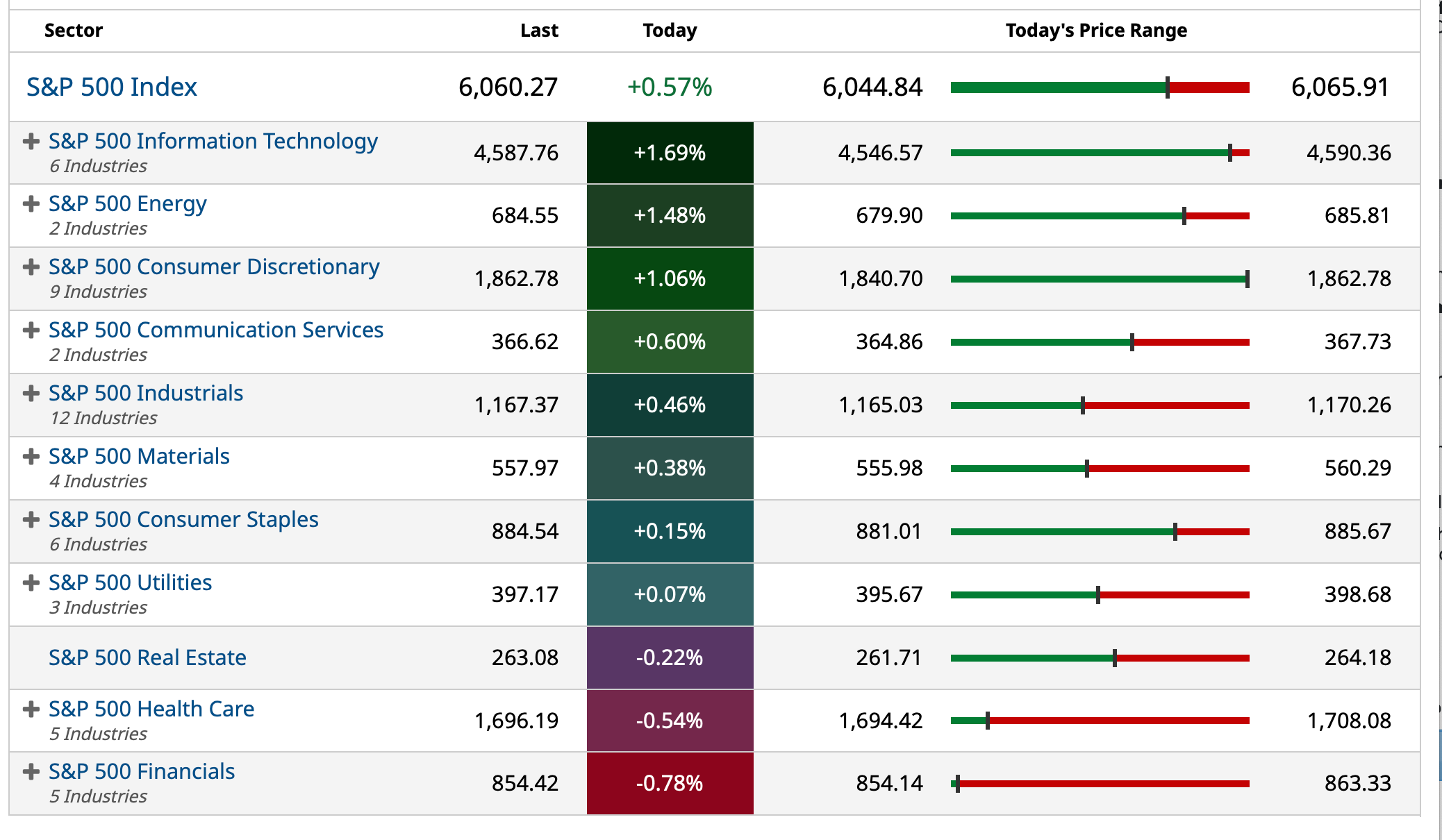

SPY +0.65%

QQQ +1.30%

RSP (equal weighted S&P) +0.08%

BY Doug Kass · Feb 10, 2025, 11:20 AM EST

* SPY $605.11

* QQQ $529.97

BY Doug Kass · Feb 10, 2025, 11:10 AM EST

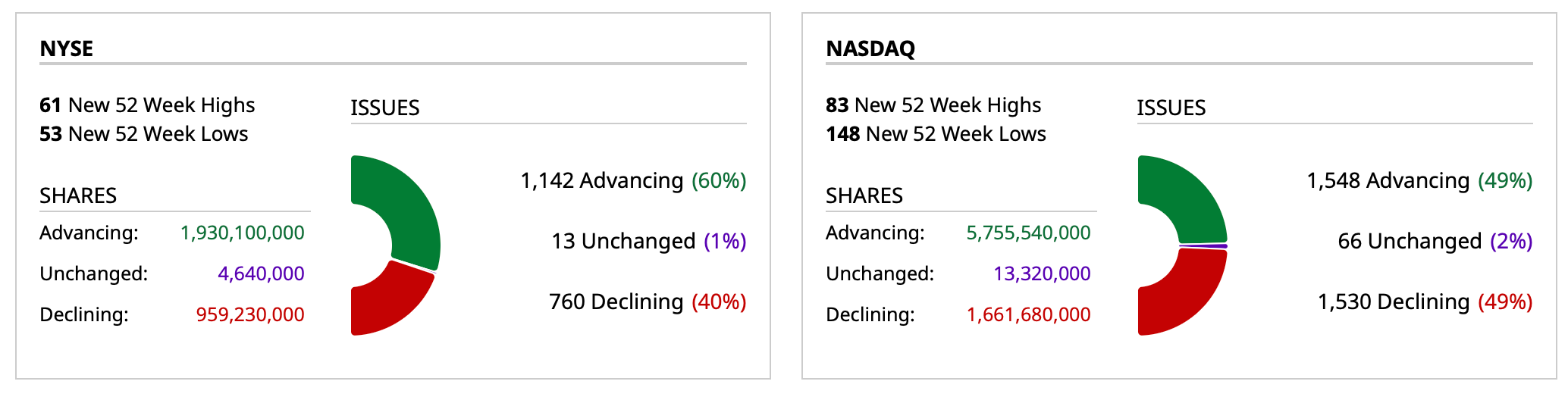

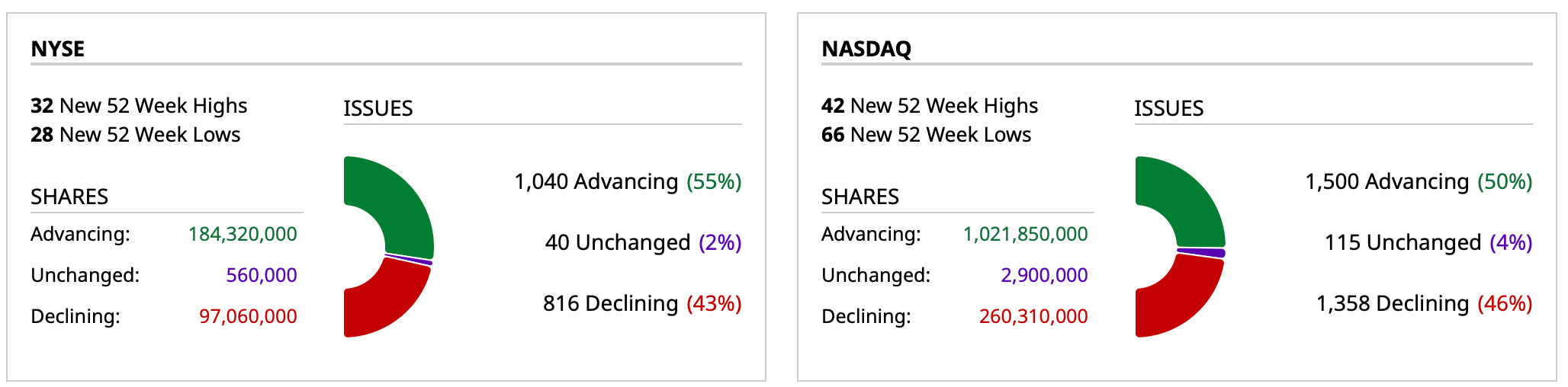

- New York Stock Exchange volume is 3% below its one-month average;

- Nasdaq volume is 22% above its one-month average:

BY Doug Kass · Feb 10, 2025, 10:48 AM EST

I will be in a board meeting from 9:30 AM to 11 AM.

BY Doug Kass · Feb 10, 2025, 9:35 AM EST

-MNDY +24% (earnings, guidance)

-FPAY +15% (experienced the highest level of January lease originations in 4 years, new customer application volume +130% y/y)

-TALK +9.1% (momentum)

-AIOT +8.4% (earnings)

-NSP +7.8% (earnings, guidance)

-NUE +7.1% (to announce 25% tariffs on all steel and aluminum imports)

-OCX +7.0% (prices $29.1M equity offering at $2.05/shr)

-BP +6.9% (Activist Elliott has taken a 'significant' stake in BP and to push for transformational changes to improve the company's performance)

-ROK +5.5% (earnings, guidance)

-X +4.2% (to announce 25% tariffs on all steel and aluminum imports; Ancora Issues Letter to U.S. Steel’s Board of Directors Following Failed Attempts to Resurrect the Dead Nippon Transaction)

-AA +3.8% (to announce 25% tariffs on all steel and aluminum imports)

-TMUS +3.6% (introduced T-Mobile Starlink Beta)

-PDD +3.4% (Chinese ADR strength; China Cabinet Meeting: Reiterates stance to place greater emphasis on increasing consumption)

-SHOP +3.3% (Benchmark Company Raised SHOP to Buy from Hold, price target: $150)

-HOOD +3.1% (Mizuho Securities Reiterates HOOD with Outperform, price target: $65 from $60)

-JSPR +2.8% (announces Briquilimab Presentations at the American Academy of Allergy, Asthma, and Immunology (AAAAI) Annual Meeting)

-PLYA +2.7% (confirms to be acquired by Hyatt Hotels at $13.50/shr in cash in $2.6B deal)

-JCI +2.5% (UBS Raised JCI to Buy from Neutral, price target: $103)

-PLRX -64% (following DSMB recommendation, Company voluntarily paused enrollment and dosing in BEACON-Idiopathic Pulmonary Fibrosis (IPF) Phase 2b trial and will monitor current patients while data is reviewed)

-SMTC -26% (gives update on CopperEdge product sales)

-INVZ -13% (prices 28.8M units at $1.39/unit in $40M registered direct offering)

-HAIN -9.4% (earnings, guidance)

-EPC -8.2% (earnings, guidance)

-MBOT -7.1% (announces $13M Registered Direct Offering Priced At-The-Market under Nasdaq Rules at $2.13.shr)

-ON -4.4% (earnings, guidance)

-TSEM -3.0% (earnings, guidance)

-SCHW -2.9% (TD announces Intent to Sell its Equity Investment in Schwab, who has agreed to repurchase $1.5B of its shares from TD conditional on completion of the offering)

BY Doug Kass · Feb 10, 2025, 9:16 AM EST

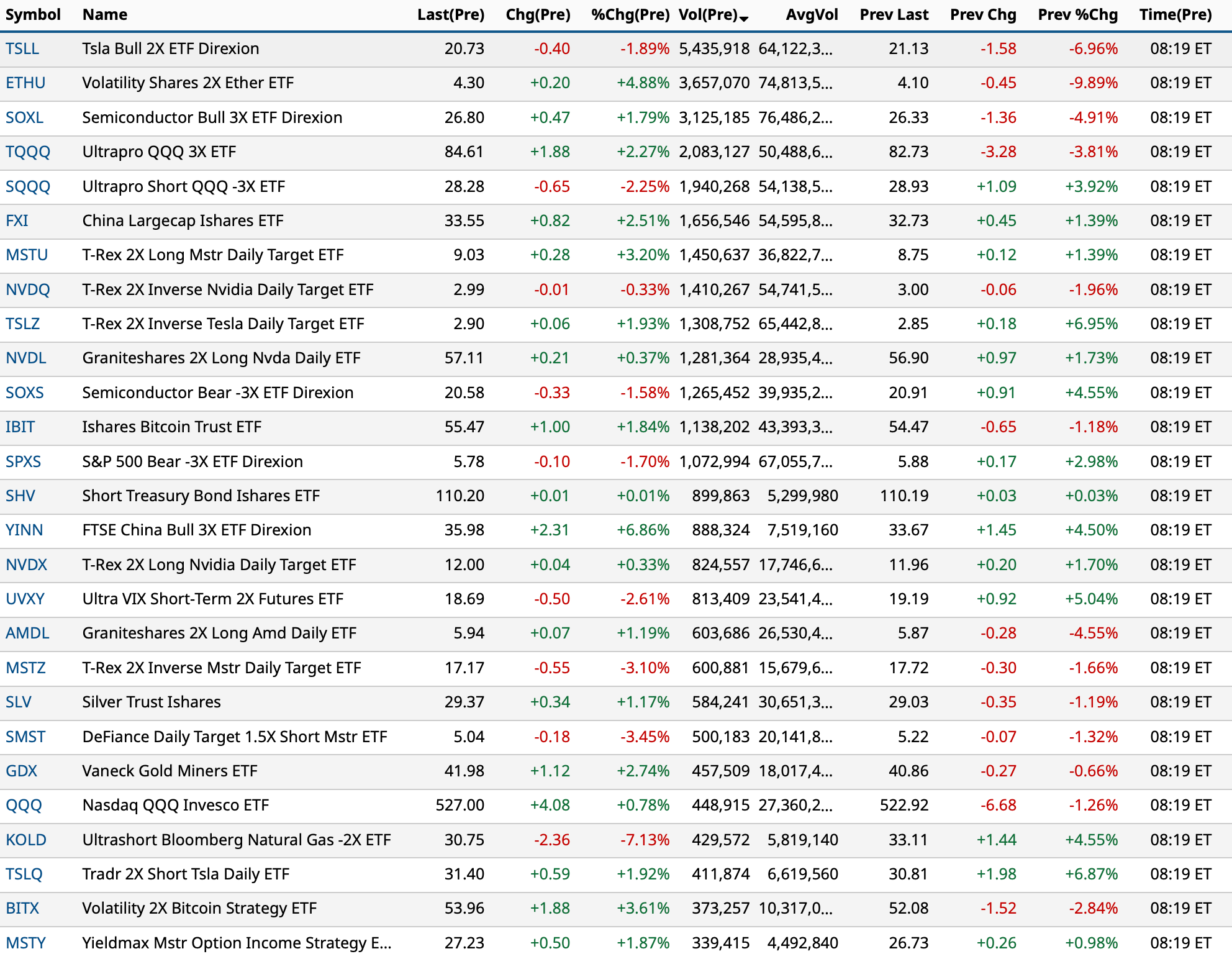

Most active premarket exchange-traded funds as of 8:19 a.m. ET:

BY Doug Kass · Feb 10, 2025, 9:08 AM EST

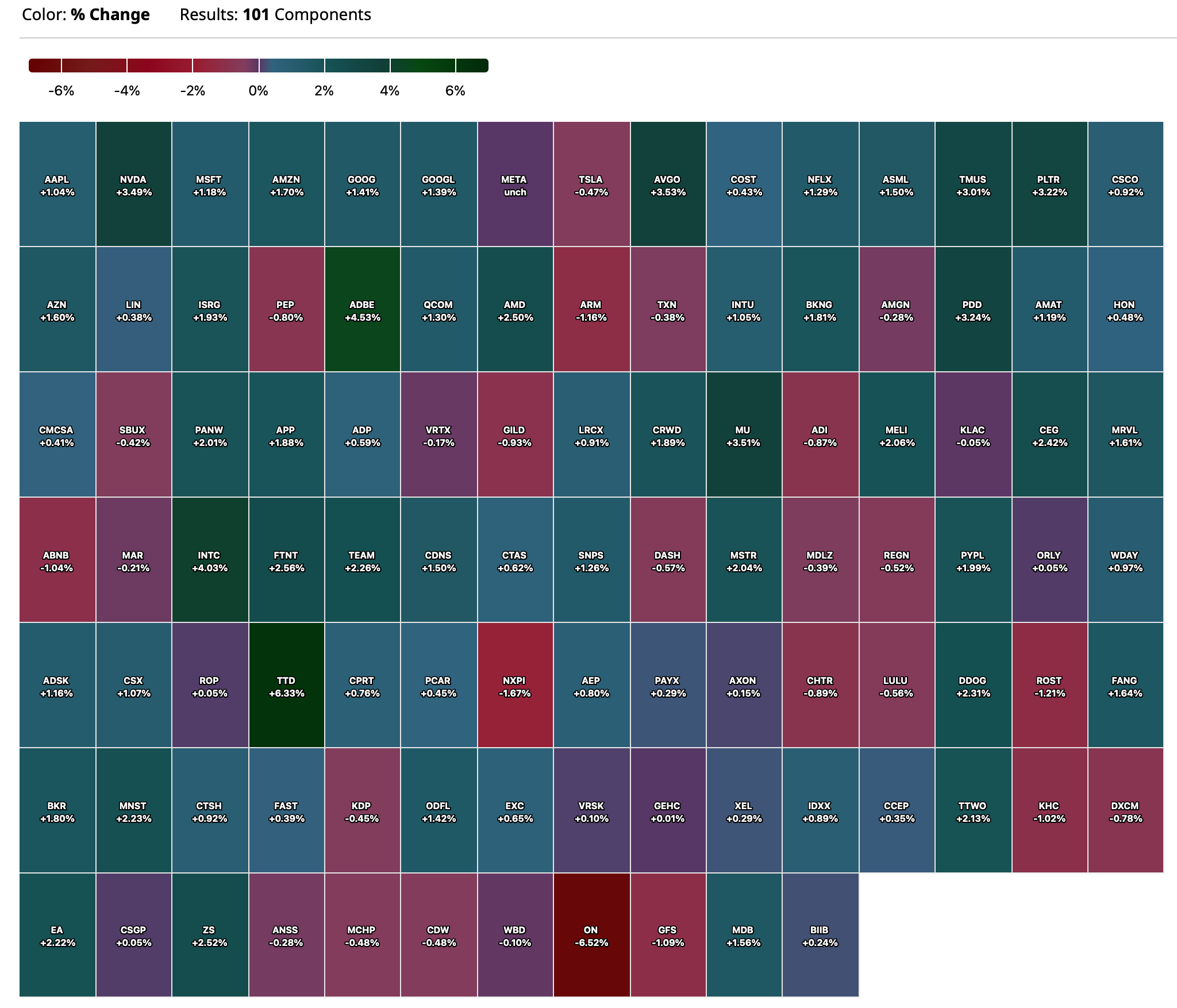

Premarket percentage movers at 8:37 a.m. ET:

BY Doug Kass · Feb 10, 2025, 8:55 AM EST

From Peter Boockvar:

I was at a private conference last month and heard two really interesting ideas that were supposedly being discussed at the US Treasury and inside the White House but wondered whether it was just talk or actually had a chance of happening. One, the US Treasury would revalue to the market the 8,133 metric tons/261 million troy ounces of gold that they hold and currently marked at just $42 per ounce. Via a relationship with the Fed that holds gold certificates in return as they handed over the gold to Treasury many years ago, this maybe can be monetized via a repo deal with Fed or something else, giving Treasury about $800b-900b in cash in the snap of a finger.

The second was the US Treasury would give some of our foreign friends that own US Treasuries an offer that they could not refuse, to swap some of them for much longer term bonds, like 50 to 100 year bonds that would allow us to term out our debt and maybe even make them zero coupon.

Then I hear last week comments from Scott Bessent who at the White House said he is looking about monetizing some things on the balance sheet of the US Government. Interesting in light of what I said above. Also, President Trump made some comments yesterday about potential problems in the Treasury market where maybe we don't have as much as debt as we thought, though there was no further color or clarification on exactly what he was referring to.

I wasn't intending on mentioning any of this until news actually came of it but what got me to write this today and reveal what I heard last month and after the Bessent comment, was the Gillian Tett article over the weekend in the Financial Times titled "The Unimaginable is Now Imaginable as Gold Glitters" where she seems to be on to this story.

She goes through some of the reasons for the record high price in gold that we're all aware of but then said, "some hedge fund contemporaries of Scott Bessent, the hedgie-turned US Treasury secretary, are speculating about a revaluation of America's gold stocks."

"Currently, these are valued at just $42 an ounce in national accounts. But knowledgeable observers reckon that if these were marked at current values - $2,800 an ounce - this could inject $800 billion into the Treasury General Account, via a repurchase agreement. That might reduce the need to issue quite so many Treasury bonds this year."

Now this would only be a one-time reset but something that apparently is being debated.

Also, on point number two. She cites an investor memo that Stephen Miran, the head of Trump's Council of Economic Advisors wrote last year. In addition to talking about the use of tariffs and eventually weakening the US dollar via "voluntary co-operation from the Federal Reserve and a multilateral dollar devaluation accord...he also contends that the dollar's reserve status and American military dominance are so tightly entwined that the White House could force countries who enjoy the US security umbrella to finance its deficit by buying very long-dated treasury bonds."

Bottom line from Gillian, "Such ideas might seem mad. And Miran acknowledges that the policy 'path' to implement tactics like these 'without material adverse consequences' is 'narrow'...But what Miran's memo shows is that once unimaginable ideas are now becoming entirely imaginable."

"Thus it is no surprise that gold is outperforming bitcoin right now; nor that traders are flying gold bars from London vaults to New York. Welcome to a financial Alice in Wonderland world where buying bullion seems almost sane."

I'll add, it is clear that at Treasury and in the White House, some really creative, outside the box thinking is taking place in dealing with the overload of US debts and deficits. Who knows if any of this takes place, the legal ability to do so, etc... but these are all things to now be thinking about and considering as possibilities.

https://www.ft.com/content/f6459ed1-8a65-4d89-8bd8-40e8546912f0

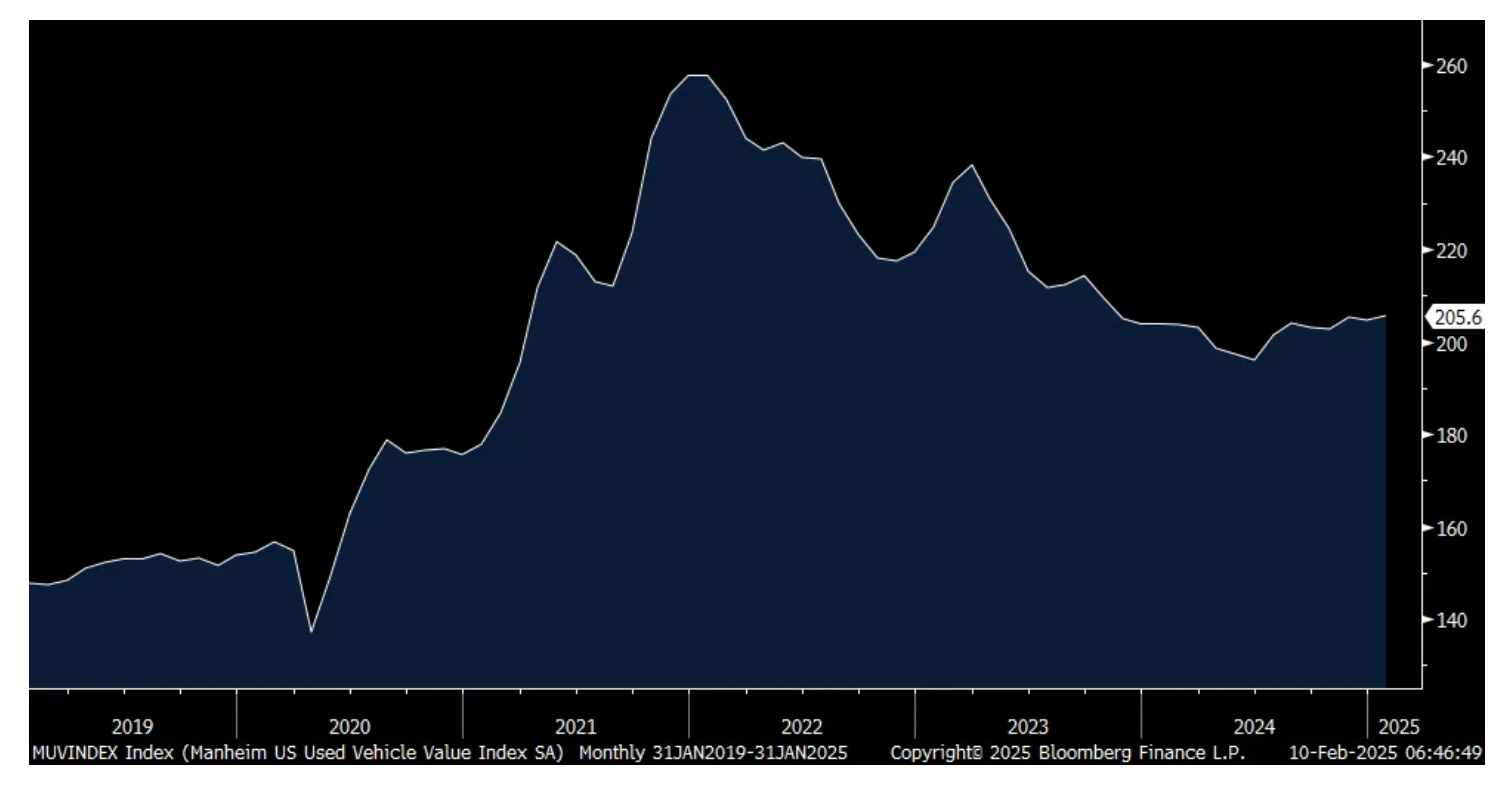

Moving on. Quietly, the Manheim Used Vehicle Index is at its highest level since October 2023. Their January index rose .4% m/o/m and .8% y/o/y. "While it's not yet spring, wholesale values increased more than we usually see in the month of January, with particular strength at the end of the month...Currently, retail days' supply at used dealerships sits nine days lower than last year, and we are just now on the cusp of starting the spring wholesale market."

I'll say for the umpteenth time, we are now 5 years into selling new vehicles at a pace below the 2019 rate. That means a continued below trend pace of used cars entering the market. Goods price inflation is not dead and now we have more tariffs coming.

Manheim Used Vehicle Index

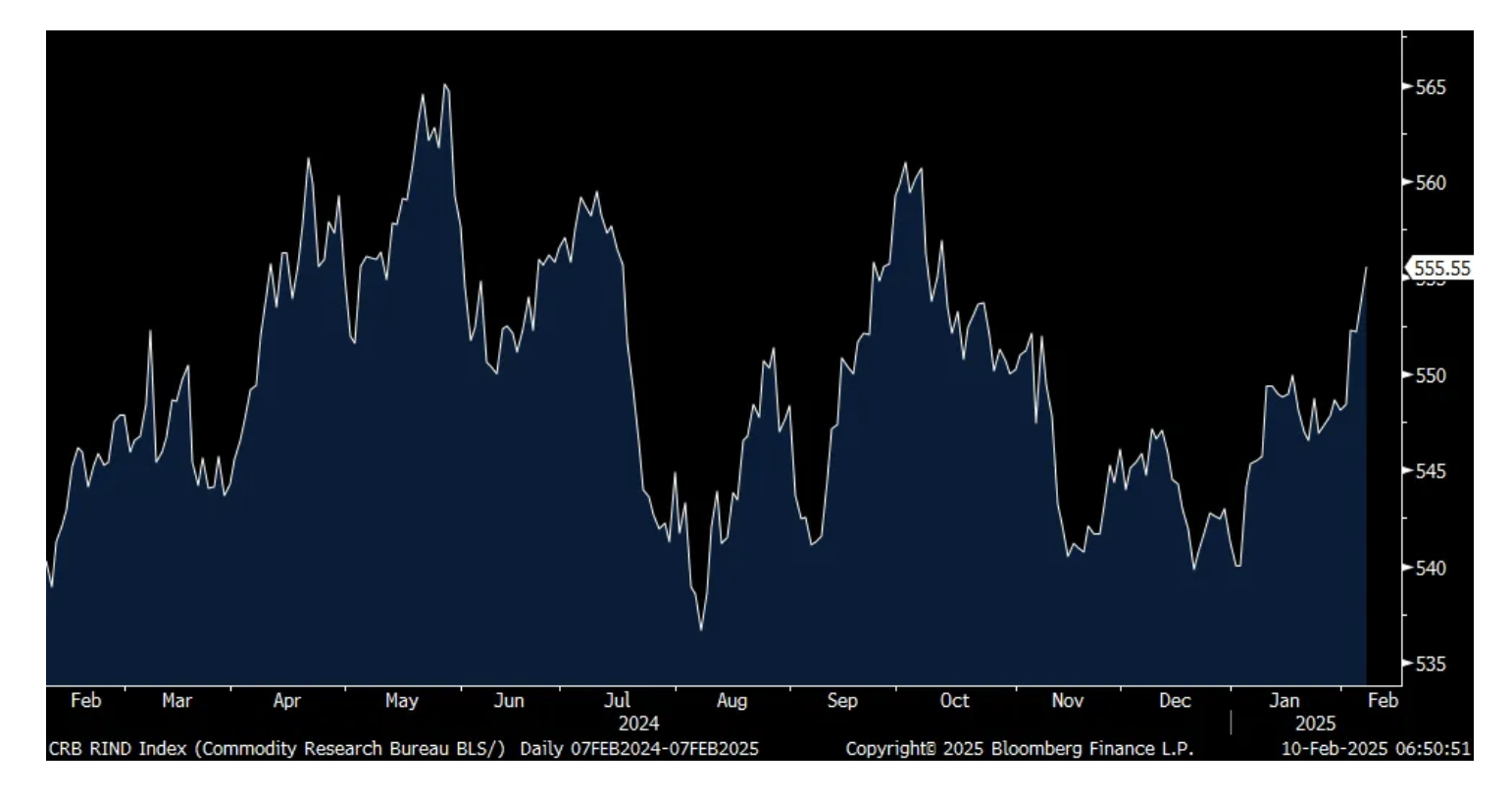

By the way, the CRB Raw Industrials index closed Friday at the highest level since mid October.

CRB Raw Industrials Index

I'll add this, the 2 yr and 5 yr inflation breakevens closed Friday at the highest levels since March 2023 and the 10 yr breakeven is just below the highest since October 2023. While never take this as an accurate predictor, it is what the market is pricing in right now in their inflation view.

On the flip side, the sunbelt states continue to see decelerating apartment rental growth. I mentioned on Friday what we heard from Mid America Communities and Camden Property Trust (a stock we own) in their earnings call expects same property revenue growth of just 1% "within the majority of our markets." But, they also said "Our top five markets should see revenue growth in the range of 2% to 2.5%, and these markets account for over 40% of our budgeted revenue." Either way, it's a slowdown from what the CPI is currently calculating. Their most challenged markets are Austin and Nashville where rents are down about 3% y/o/y.

As for new supply in their markets, "We reviewed supply forecasts from several third party data providers, and their projections ranged from 160,000 to 230,000 completions across our 15 markets over the course of 2025, compared with 230,000 to 280,000 apartments delivered in 2024."

From Expedia, whose stock popped by 17% Friday on healthy travel trends:

"Our fourth quarter results exceeded our expectations, with room nights, gross bookings and revenue all growing double-digits. This top line strength reflects our continued strong execution, along with better than expected travel demand."

"Travel demand remained healthy in Q4, despite price increases in hotels, vacation rentals and air. Like last quarter, international demand was stronger than the US with booked room nights growing high single digits in the US, low double digits in Europe and high teens in the rest of the world."

From Newell Brands, the maker of so many things like Sharpie, Graco, Rubbermaid, Yankee Candle, Paper Mate, Elmer's Glue, etc... And whose stock was down 26% after earnings:

"Turning to 2025, we expect the macroeconomic backdrop to be dynamic. Lower income consumers remain under pressure from the cumulative impact of inflation over the last several years. The recent substantial appreciation of the US dollar, along with evolving tax policies and potential tariffs and trade regulations in the US, contribute to a fluid and complex operating environment."

BY Doug Kass · Feb 10, 2025, 8:30 AM EST

* Gary Marcus ("Deep Learning Is Hitting A Wall"), the slowing is more than DeepSeek and more...

Interesting article below from Gary Marcus – “Deep Learning Is Hitting A Wall.”

In third-grade terms, there is no scaling, it doesn’t work, and it will always hallucinate and have reasoning errors.

Does the market actually believe AI works? It sure has capitalized things that way. But the market, as it often does, seems to be speaking out of both sides of its mouth. If the market really believed the LLMs worked well and were an economic solution to a real problem, shouldn’t Google GOOGL stock be zero? Open AI, Anthropic, Perplexity, DeepSeek, all of them are just a different form of search. Search (and paid search) are almost the entirety of Google’s business model and profit pool. If the LLMs worked well, the bulk of Google’s revenue stream should be at risk to these other services. Therefore Google’s market cap should reflect that issue. But that is not what is happening. So I can only conclude that the market doesn’t really believe in the LLMs either as much as it believes in the short-term momentum of the stock prices and the theme. Or, like AI, the market doesn’t really think anymore. Frankly, I am a bit surprised that Google hasn’t yet come out and said there are real limitations to what LLMs can do, just to protect themselves. But I guess for the time being, they probably feel like they have no need to address a question that nobody is asking, especially because over the short term the AI theme counterintuitively has only been a lift for their stock price as well.

As to why all these guys continue to throw massive dollars at a broken solution to a problem that doesn’t exist and therefore can only be lighting money on fire, I guess nobody likes to admit they were wrong.

Five ways in which the last three months — and especially the DeepSeek era — have vindicated “Deep learning is hitting a wall"...

A demonized paper from three years ago that has stood the test of time:

Feb 08, 2025

No other essay I have ever written has been ridiculed by as many people, or as many famous people, from Sam Altman and Greg Brockman to Yann LeCun and Elon Musk, as Deep Learning is Hitting a Wall, published nearly three years ago.

In hindsight, I wrote the essay too soon; the world wasn’t ready for what I had to say. But an awful lot of what it had to say has borne out, and the last three months, especially the last few weeks, have been especially in line with the essay’s conclusions.

Here are five observations:

I think it is fair to say that “Deep Learning is Hitting a Wall” didn’t anticipate how well a system like Deep Research might work, but in most other respects, ranging from anticipating the slowing of pure LLMs to the need for neurosymbolic AI to the continued troubles with reasoning and hallucination, the paper was bang on. The ridicule, on the other hand, was deeply misplaced, and emblematic of a new regime in which oligarchs try to impose their beliefs on a science, moving markets but not actually solving the underlying research challenges that still loom before us.

Speaking of the devil re Google. Oh my lord. Apparently they think their sh*t doesn’t stink (like Gouda cheese) and never bothered to fact check their own ad which was based on the output from their own AI. Kool-aid drinking morons. This one might be more precious than Anthropic asking their job applicants not to use AI in their application:

Finally, I don’t think it was DeepSeek. That news broke all of two weeks ago. There was one week left in January. And it takes time to hit the brakes. This slowing is due to something else.

DeepSeek will be a convenient excuse for a lot of other issues, both accounting and business related:

https://finance.yahoo.com/news/tsmc-january-sales-growth-slows-054551367.html

BY Doug Kass · Feb 10, 2025, 7:30 AM EST

Bonus — Here are some great links:

BY Doug Kass · Feb 10, 2025, 7:00 AM EST

BY Doug Kass · Feb 10, 2025, 6:45 AM EST

The S&P Short Range Oscillator slipped back toward neutral — falling from 2.39% to 0.76%.

BY Doug Kass · Feb 10, 2025, 6:30 AM EST

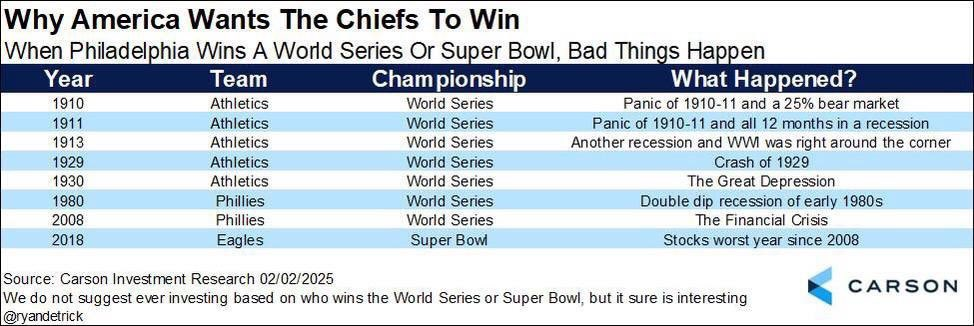

Speaking of the Super Bowl, my column was inserted into Sarge's posts on Friday. I case you missed it, here it is:

BY Doug Kass · Feb 10, 2025, 6:05 AM EST

BY Doug Kass · Feb 10, 2025, 5:55 AM EST

* I was off by a couple of playoff games, but the Kansas City Chiefs were blown out in Super Bowl VIX by the Philadelphia Eagles....

* The heavily favored Super Bowl contender, the Kansas City Chiefs, get blown out in the first round of the NFL Playoffs. Shortly thereafter, similar to the famous 1973 wife swap It's 50th anniversary of Yankees' most insane swap ever of New York Yankees pitchers Fritz Peterson and Mike Kekich, Kansas City Chiefs' Patrick Mahomes and Travis Kelce switch partners ((Patrick Mahomes marries Taylor Swift and Travis Kelce marries Brittany Mahomes).

BY Doug Kass · Feb 10, 2025, 5:45 AM EST