My Tweet of the Day (Part Four)

BY Doug Kass · Feb 4, 2025, 5:00 PM EST

BY Doug Kass · Feb 4, 2025, 5:00 PM EST

"Just one more thing."

- Lt. Columbo

I forgot to mention that in the late afternoon I exchanged all my Index common shorts into short calls (taking in a premium).

BY Doug Kass · Feb 4, 2025, 4:45 PM EST

At 4:19 p.m.:

BY Doug Kass · Feb 4, 2025, 4:35 PM EST

BY Doug Kass · Feb 4, 2025, 4:24 PM EST

* Pennsylvania's governor endorses adult recreational uses of cannabis...

BY Doug Kass · Feb 4, 2025, 4:03 PM EST

KKR -$12!

BY Doug Kass · Feb 4, 2025, 3:45 PM EST

* 4 days, 8 hours to Spring Training!!! Spring Training Countdown

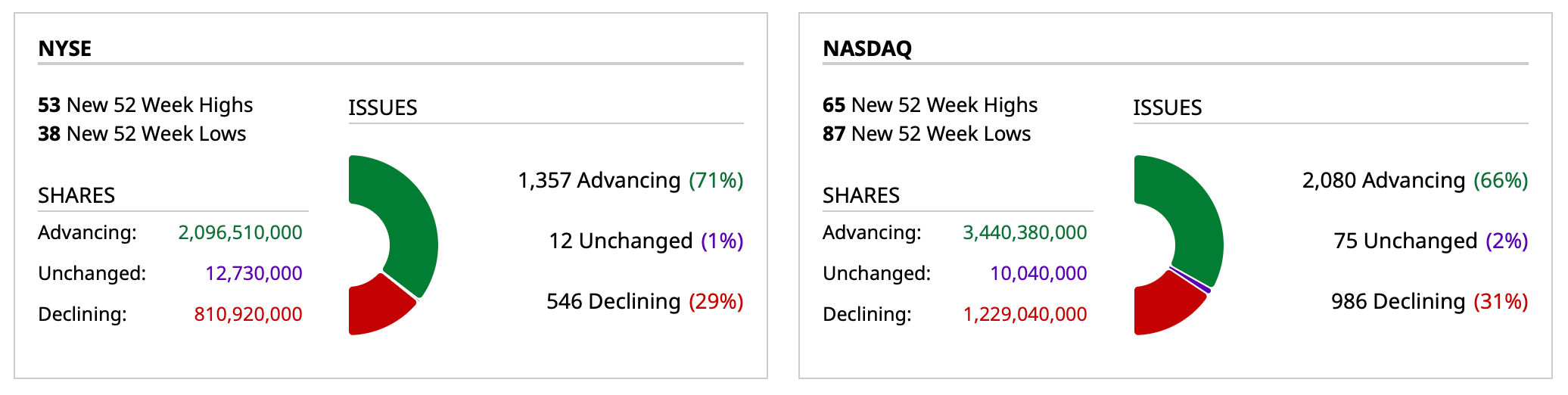

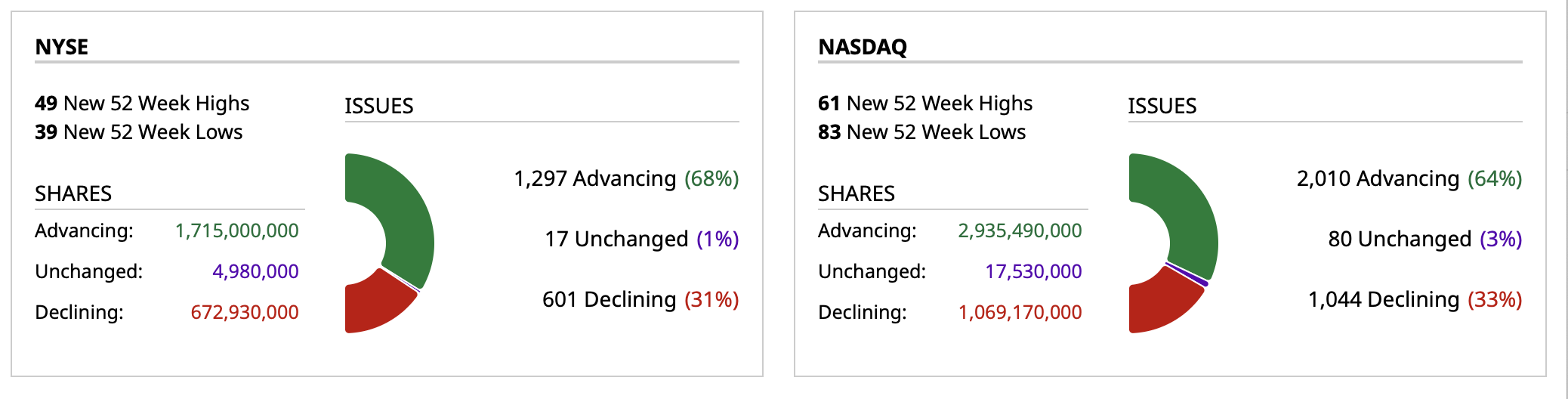

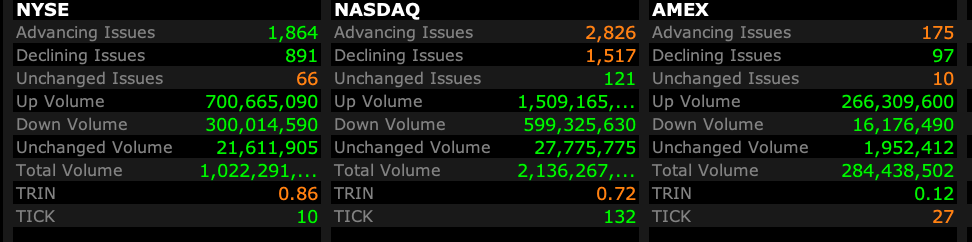

Breadth is improved today, at about 2-1 advancers over decliners:

Big research day — not too much on the trading side.

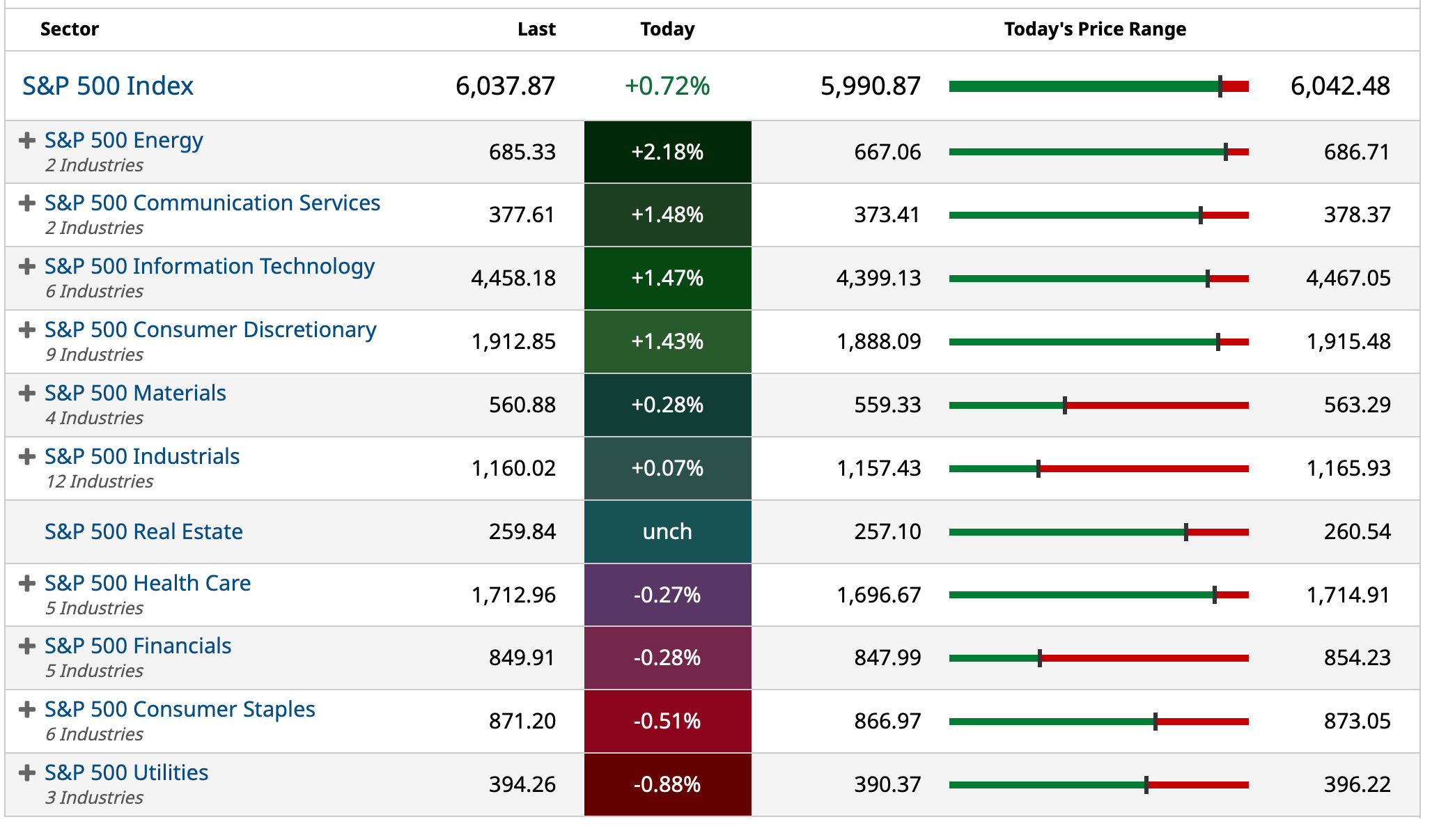

At 3:15 p.m. the S&P Index is +43 handles.

Here are today's "Things":

* I covered my SPY/QQQ shorts for a profit last evening.

* I re-established short common and short call Index positions. SPY at $600.72 and QQQ at $523.98.

* Added to MSOS at $3.35, TCNNF at $4.73 and VRNOF at $1.20.

* Added to SBUX $109.35 and JPM $268.20 shorts.

BY Doug Kass · Feb 4, 2025, 3:23 PM EST

* Bull markets, like the Mafia, die hard...

Monday morning's market schmeissing hinted of a market breakdown but it has given way to a steady and deliberate rally from that day's lows.

For now, it appears the hopes (and prayers) of the ursine crowd (that would be me!) will be delayed a bit in time.

Nonetheless, I remain tactically bearish and plan to use this afternoon's strength to up my short exposure.

Cue The Godfather theme song...

Tom, can you get me off the hook? For Old Time's Sake...

BY Doug Kass · Feb 4, 2025, 2:50 PM EST

BY Doug Kass · Feb 4, 2025, 2:34 PM EST

BY Doug Kass · Feb 4, 2025, 1:26 PM EST

Investment short PEP now -$7/share.

I have a 1 p.m. research call for about 45 minutes.

BY Doug Kass · Feb 4, 2025, 12:57 PM EST

The cost basis of today's Index shorts:

* SPY $600.72

* QQQ $522.98

I have a much better cost basis on my short calls!

BY Doug Kass · Feb 4, 2025, 12:34 PM EST

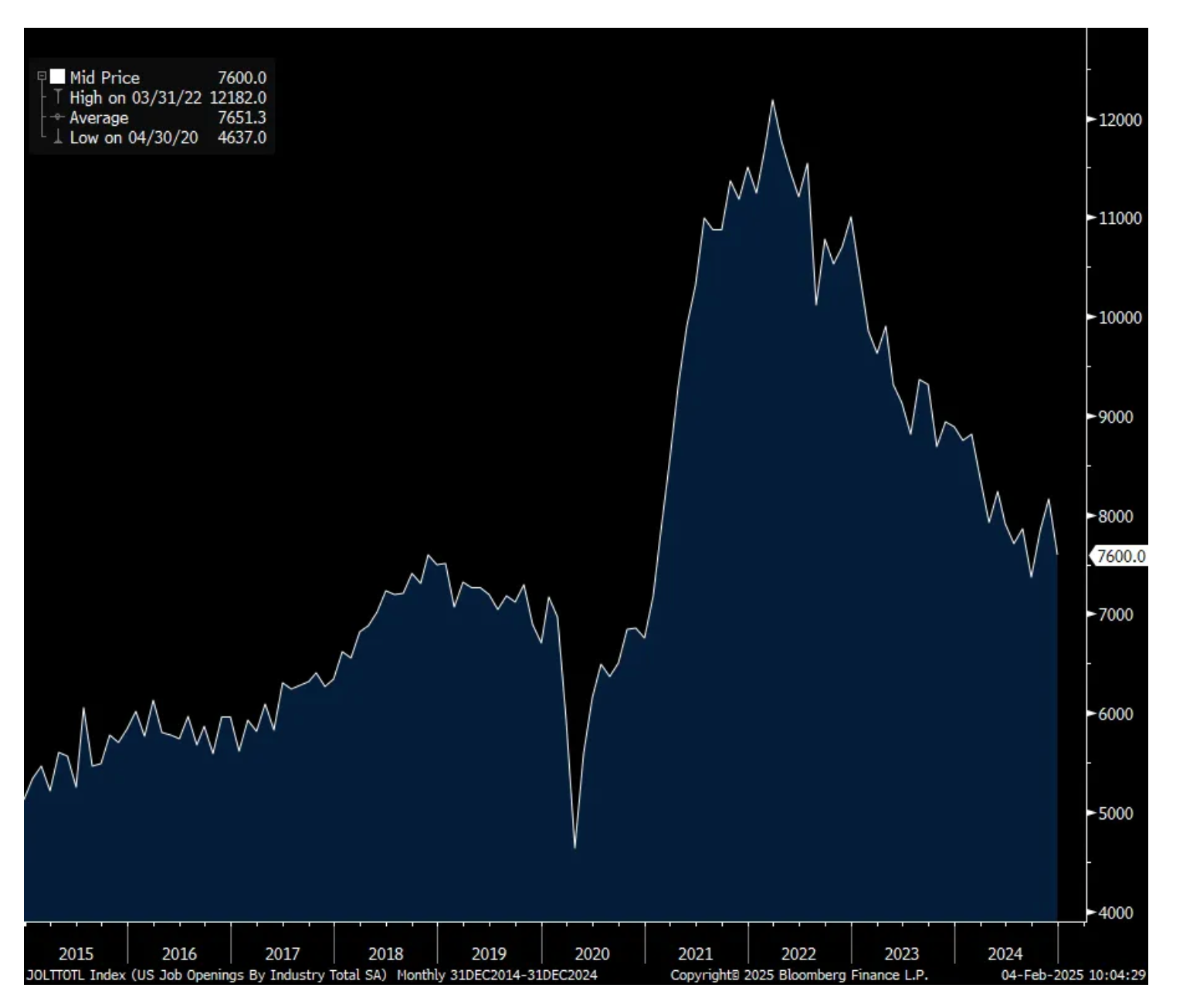

From Peter Boockvar:

Job openings shrink, particularly in mfr'g and construction

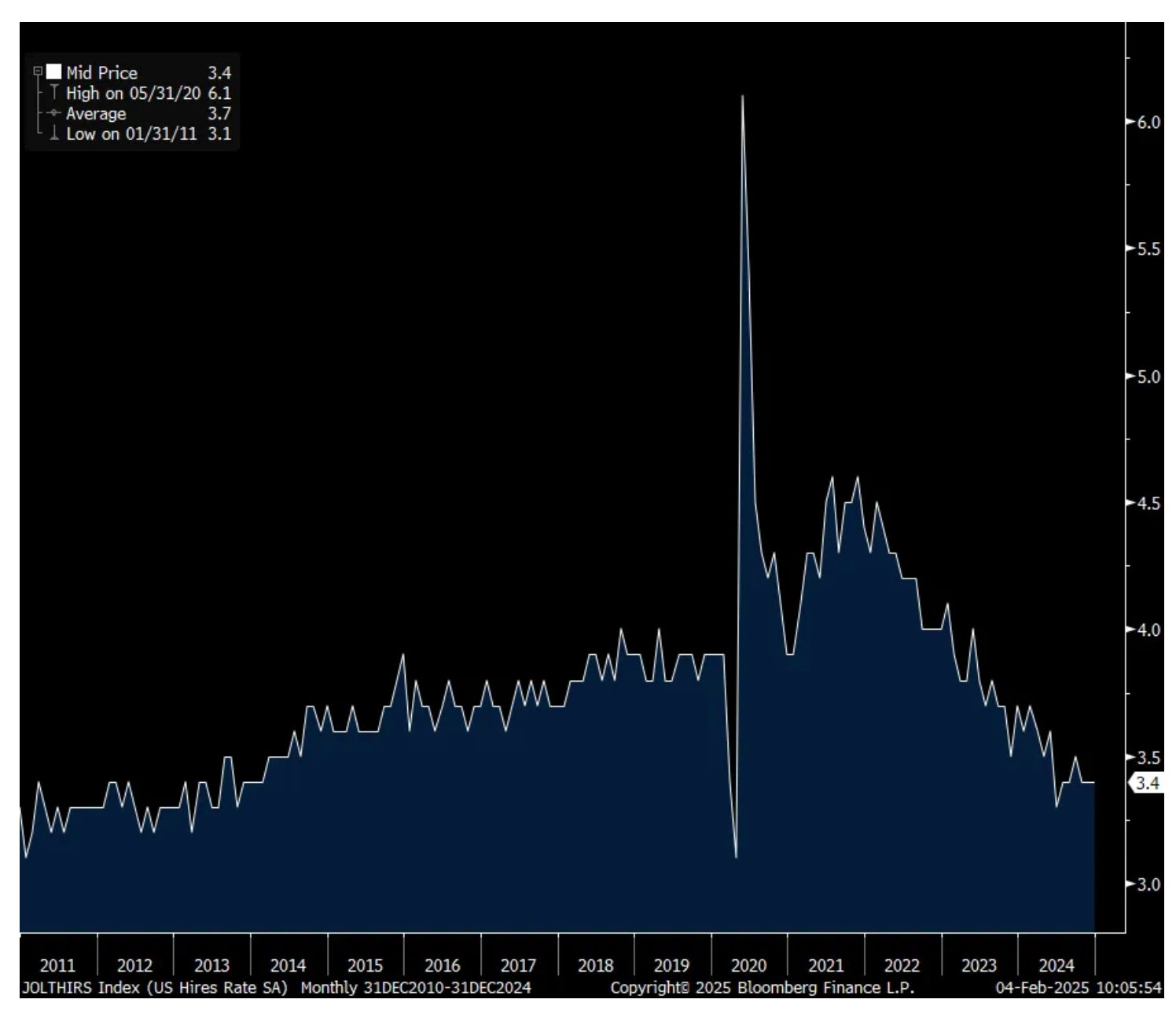

There was a notable reduction in the number of job openings in December to 7.6mm from 8.16mm in November. The estimate was 8mm. The hiring rate held at 3.4% for a 3rd straight month and one tenth off the lowest level since 2013 not including Covid. The quit rate was 2% for a 2nd month and also one tenth off the recent lows.

In terms of industry, what stood out was the 180k job opening drop in the health care/social assistance sector and we know this sector has been a key driver of job growth. Just maybe current staffing levels are finally back to some normality in healthcare? But also there was a 225k decline in openings in the professional/business service sector. After a jump in November there was a 166k fall in job openings in the financial services industry, which does include real estate leasing.

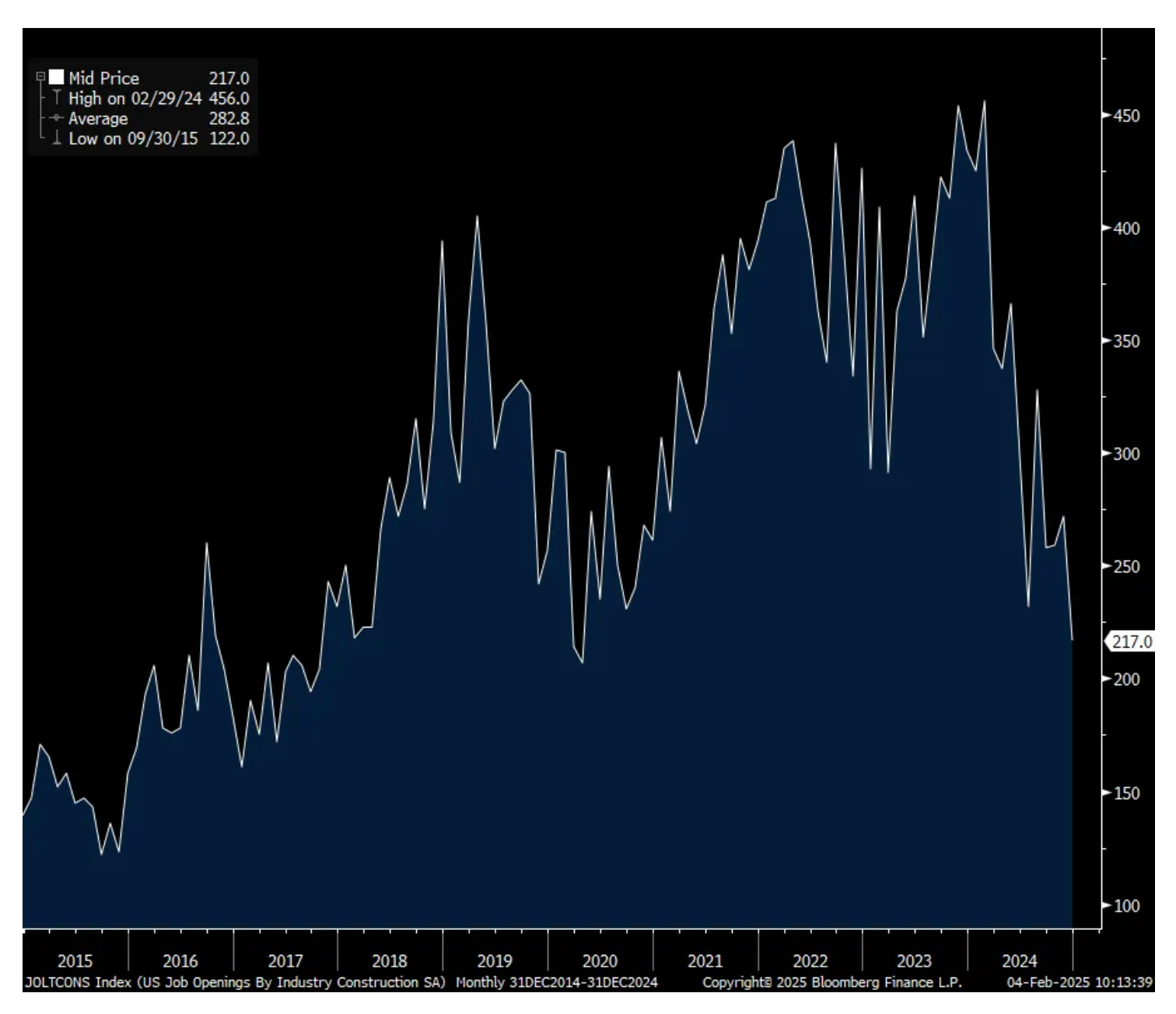

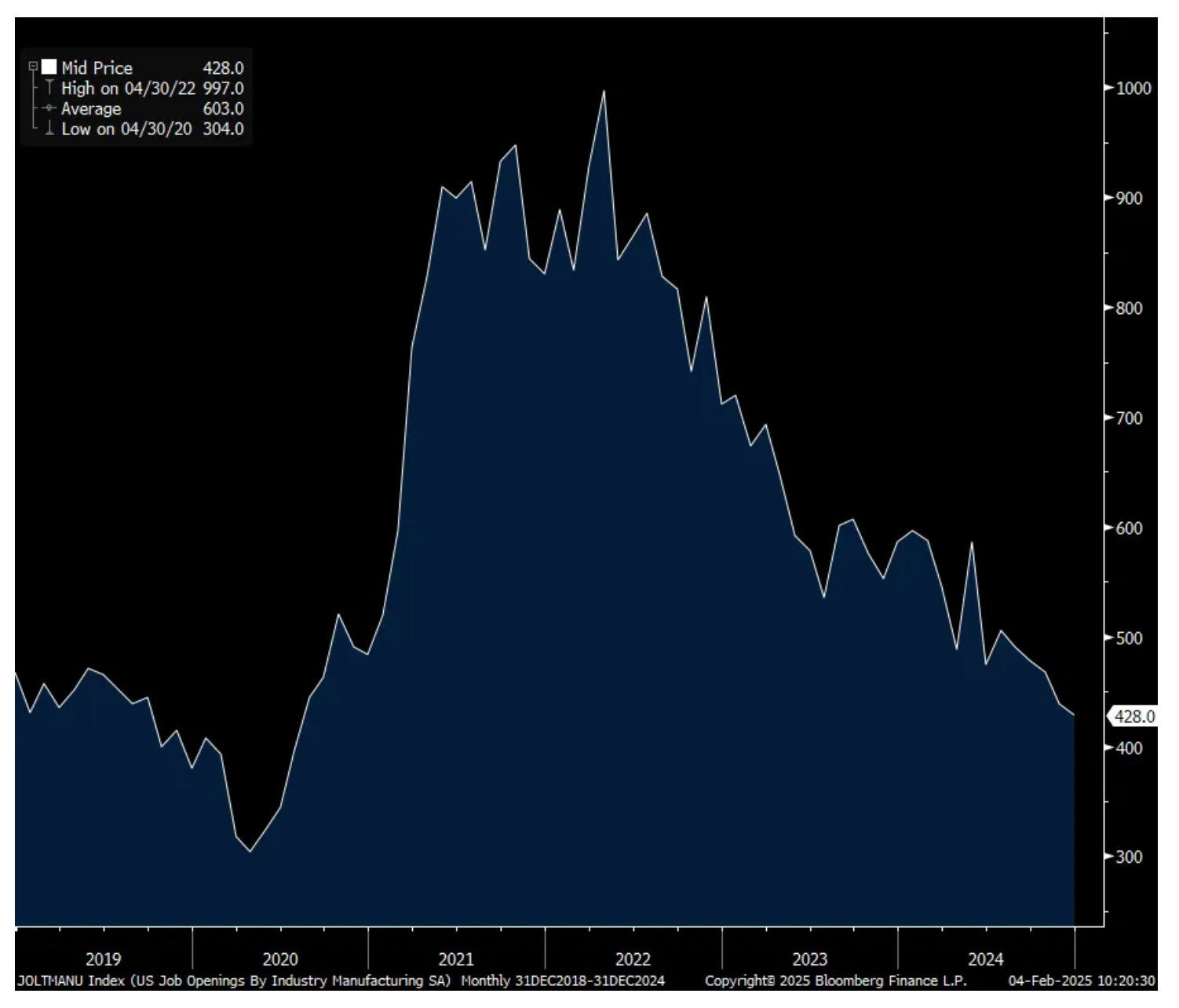

On the goods side, job openings in construction fell by 55k to the least since 2017 not including Covid. This is an interesting stat to watch because on one hand we have the demand for workers in building data centers and chip and EV battery factories but on the other hand, residential housing starts is well off its highs and building most things in commercial real estate is muted, not a surprise. Manufacturing job opening fell to the least since October 2019 not including Covid.

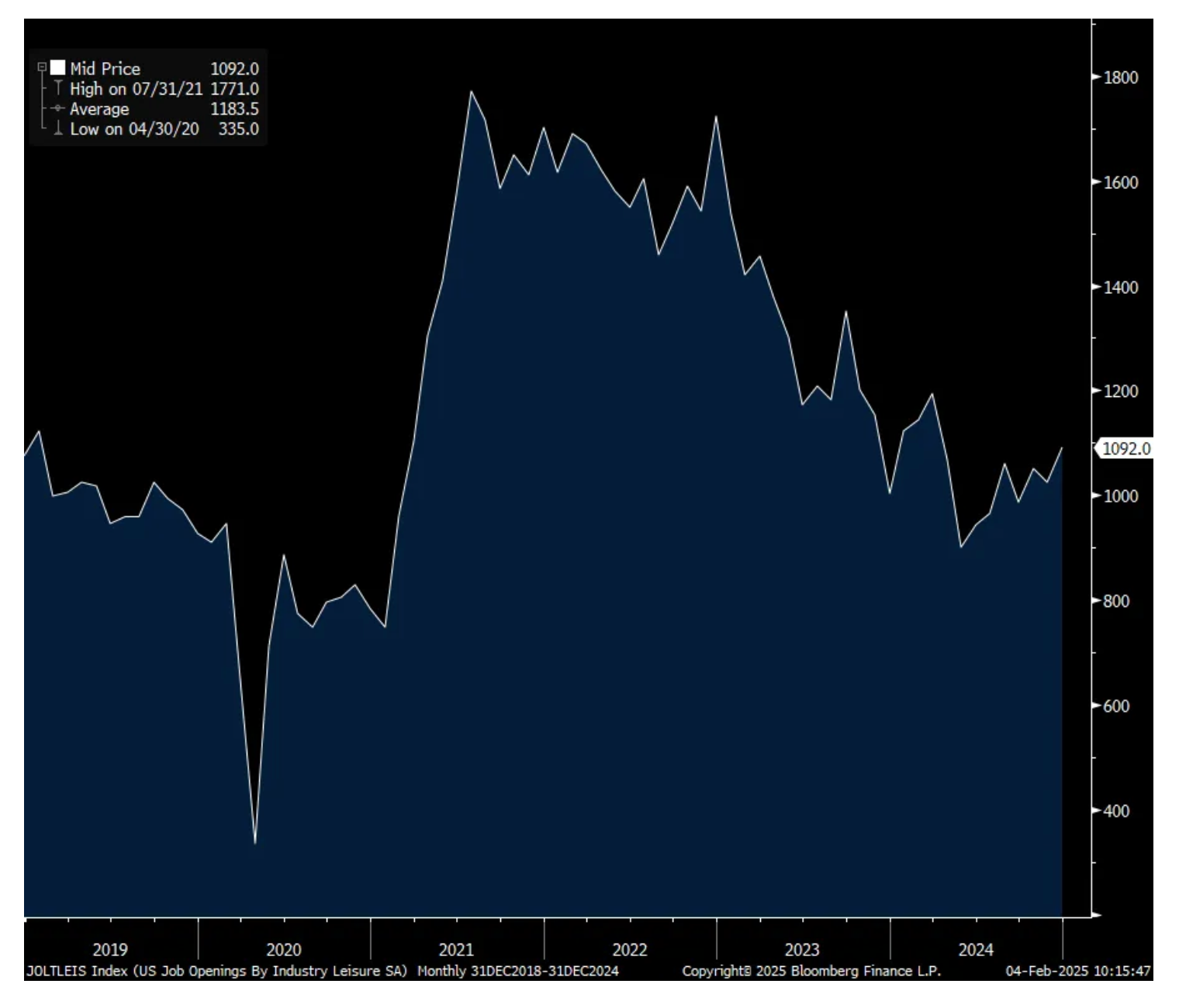

Leisure and hospitality increased the number of job openings to the most since March. They rose for retail and transportation too.

Bottom line, this data point squares with the slowing pace of hiring, though still good relative to the growth in the labor force. The service sector continues to carry the weight though as seen by the multi year low in job openings for construction and manufacturing workers.

Job Openings

Hiring Rate

Construction Job Openings

Manufacturing Job Openings

Leisure and Hospitality Job Openings

BY Doug Kass · Feb 4, 2025, 12:00 PM EST

As mentioned yesterday, Ayr Wellness AYRWF is an interesting speculative cannabis investment holding of mine — big reward, big risk.

I have recently been increasing my position of this security.

Yesterday Shadd Dales and Anthony Varrell had a great interview with the company's new President.

Cannabis Stock Ayr Wellness President Explains Future Plans | Trade to Black - YouTube

BY Doug Kass · Feb 4, 2025, 11:25 AM EST

- NYSE volume 3% below its one-month average

- NASDAQ volume 31% below its one-month average

BY Doug Kass · Feb 4, 2025, 11:14 AM EST

From Peter Boockvar:

Tariff strategy falling into 3 buckets/JGB yields continue higher/Earnings comments of note

It seems that the tariff strategy is falling into three buckets. One, what we've seen over the past few days where they are used as a cudgel in order to achieve a non-economic end, such as stopping fentanyl and migrants and which was successful in its aims with Mexico and Canada. China on the other hand is a different animal and at least for now we're back in a tariff battle with them as they retaliated, though seemingly measured, with a variety of measures including blacklisting PVH products from the country, Illumina too, 17% of the world's population PVH might not longer sell to. Also, limits were placed on the export of key raw materials that we need. Secondly, use tariffs to protect some domestic industries, like steel and aluminum that we saw in 2018 and also encourage manufacturers to bring production back to the US. Thirdly, use tariffs to raise money as part of the Trump income tax extension deal needed this year.

As for US Main Street businesses that are caught in the middle of all of this, I have to believe many are on edge, visibility is limited and we'll see what that means for hiring and capital investments. On the other hand, we anticipate major relief on the regulatory side and that will be the balancing act they are going to have to dance around.

The Hang Seng by the way rallied by 2.8% overnight as the 10% tariff on them is manageable in their eyes and in response to the more mild response back against us. The Hang Seng does house some cheap stocks that we own and whose businesses will benefit from growth throughout Asia, not just in China. The offshore yuan is up for a 2nd day on the same hopes that maybe the tariff back and forth between us and them can be smaller than last time.

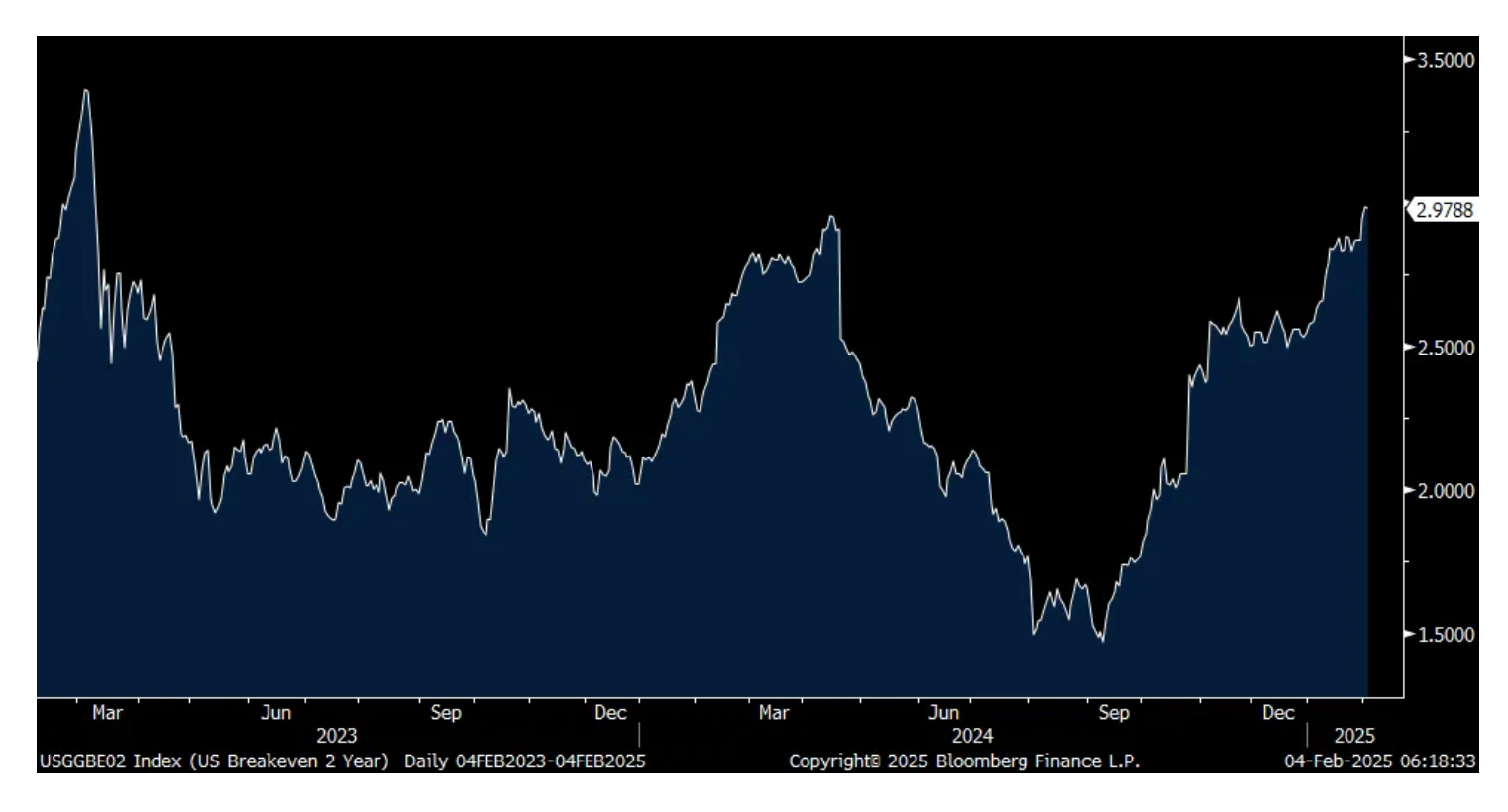

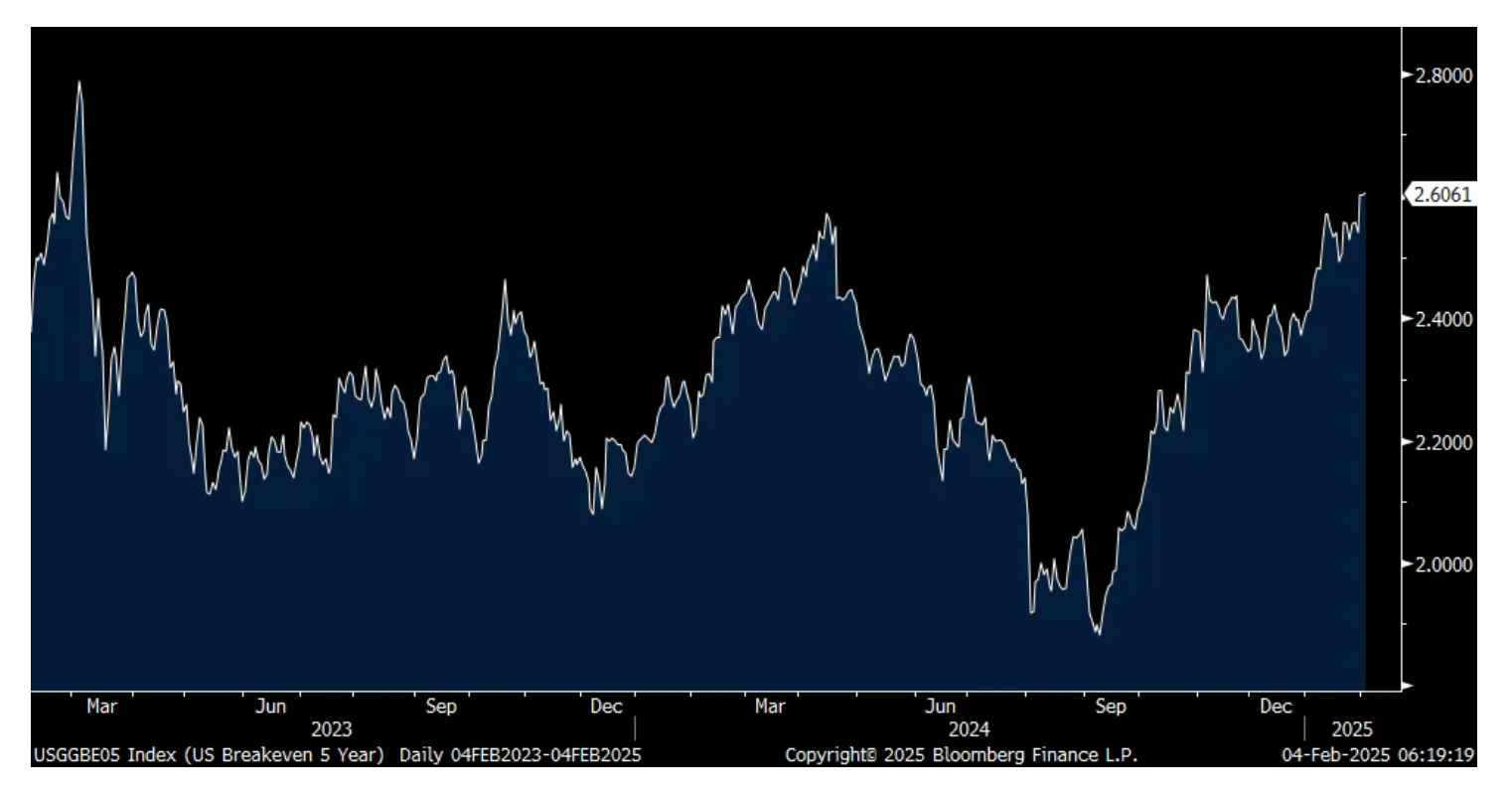

While maybe tariffs are not inflationary past the one time price set, the 2 yr inflation breakeven doesn't care as yesterday it closed at 2.98%, the highest since March 2023. The 5 yr did as well at 2.60%.

2 yr Inflation Breakeven

5 yr Inflation Breakeven

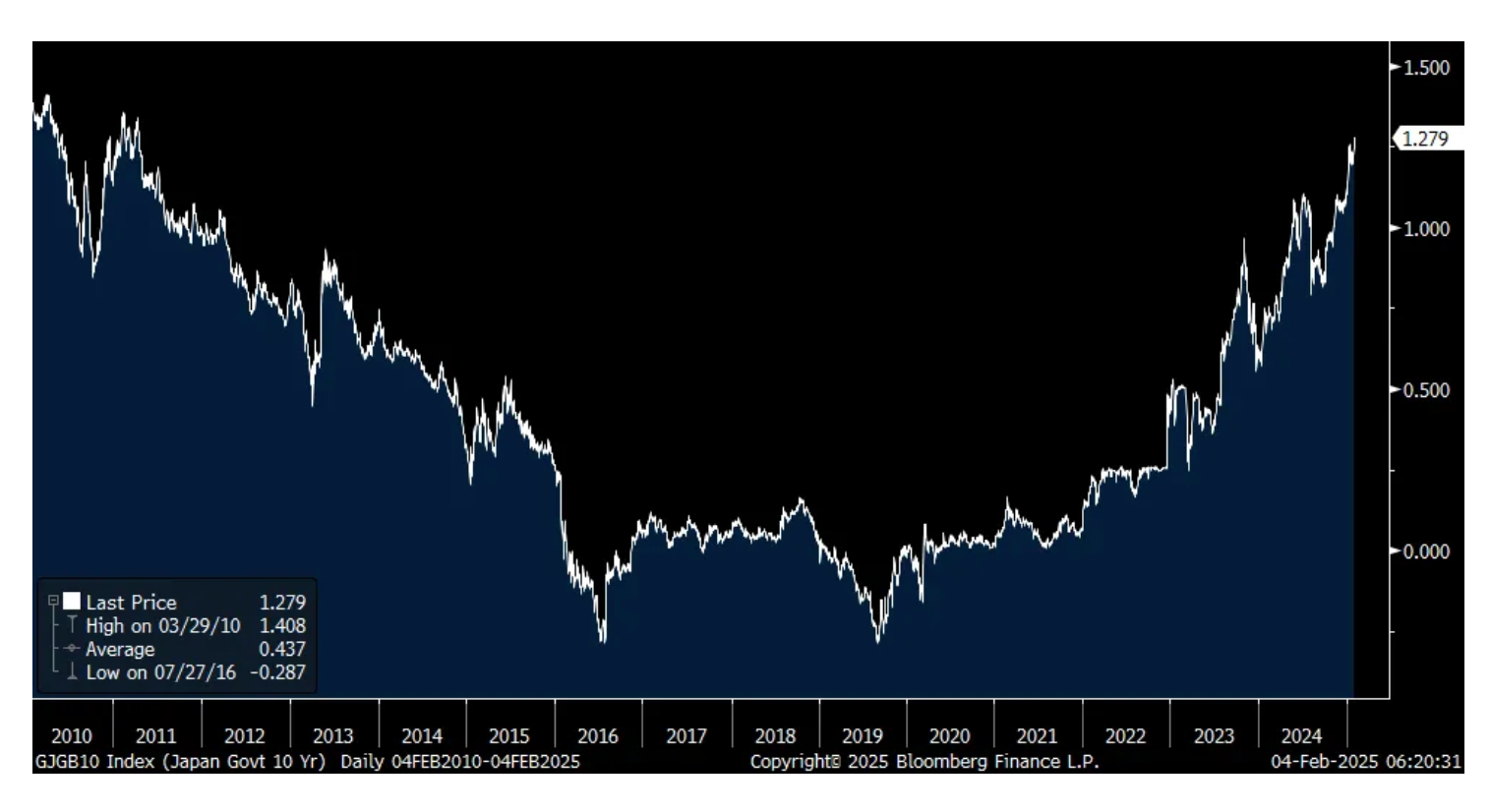

Take note too that Japanese JGB yields continue higher. The 10 yr yield rose almost 3 bps to 1.28% which is the highest since April 2011. The 2 yr yield at .75% was last seen in October 2008.

10 yr JGB Yield

2 yr Yield

US auto sales in January totaled 15.6mm at a SAAR, below the estimate of 16mm. That compares with 15mm in January 2024 and 16.6mm in 2019. WardsAuto said "There did not appear to be an end-of-month boost in demand, either as a rebound from the mid-month weather related losses or pull-ahead volume in case of still possible future tariff-related price increases. However, January's gain marked the fourth straight y/o/y increase in volume and fifth consecutive for the seasonally adjusted annual rate."

I'll add and say again, that auto sales are still trending below 2019 levels results in less than needed used car supply.

We know the largest swing factor in the CPI calculation are rents and we get to hear from companies directly in this earnings season rather than just relying on Fed surveys, Zillow and Apartment List to get our rental information. Equity Residential who has many properties on the coasts (Boston, NY, DC, Seattle, SF and Southern California) said its Q4 2024 blended rental rate was 1%, well below what CPI is telling us and means that services inflation should continue to decelerate this year. Seasonality is a factor though as it always slows in Q4 and they expect Q1's blended rate "to be between 1.4% and 2.2%."

From Cleveland Cliffs:

"Other than the Covid impacted 2020, 2024 was the worst year for domestic steel demand since 2010. As the largest supplier to the automotive industry in North America, we were especially impacted by muted demand from this sector in the 2nd half of the year. This was the primary driver of our weaker results, particularly in the fourth quarter, which we expect to be the trough as we look forward. So far into this new year, we have already seen improvements in our order book, both automotive and non-automotive, and are confident that the manufacturing friendly items on President Trump's agenda will have an outsized benefit on Cleveland-Cliffs. This includes the recently announced tariffs on Mexico, Canada, and China and the expectation that there is more to come on steel specifically."

From Clorox:

"Our category growth to date has generally been consistent with our expectations, despite period-to-period variability. As expected, consumers remain under pressure and are continuing to demonstrate value-seeking behaviors, including being very choiceful in their spending and shopping behaviors. That said, our categories are remaining resilient, our products are resonating with consumers and we are continuing to rebuild household penetration."

BY Doug Kass · Feb 4, 2025, 11:00 AM EST

Investment short PepsiCo PEP now -$6/share to day's lows.

I added to my PEP short this morning.

BY Doug Kass · Feb 4, 2025, 10:55 AM EST

BY Doug Kass · Feb 4, 2025, 10:45 AM EST

With S&P cash +32 handles I am back shorting SPY and QQQ calls (in the money for March).

BY Doug Kass · Feb 4, 2025, 10:35 AM EST

Back shorting Indices:

* SPY at $600.51.

* QQQ at $523.65.

BY Doug Kass · Feb 4, 2025, 10:30 AM EST

I am out of the Indices:

Dougie Kass

At 1015PM covered SPY $598.85 and QQQ $519.76 for the fourth intraday trading gain (this time a bit over +$2 on each) in the Indices.

BY Doug Kass · Feb 4, 2025, 10:25 AM EST

I pressed my SBUX and JPM shorts soon after the opening.

BY Doug Kass · Feb 4, 2025, 10:20 AM EST

I'm back at it buying MSOS.

BY Doug Kass · Feb 4, 2025, 10:15 AM EST

Inflation is expanding globally and slugflation lies ahead.

Not surprisingly, no outlet in the business media has even mentioned today's climb in bond yields, but I am:

* The yield on the 5-year Treasury note is +3 basis points to 4.39%.

* The yield on the 10-year Treasury note is +5 basis points to 4.59%.

* The yield on the 30-year Treasury bond is +5 basis points to 4.83%.

BY Doug Kass · Feb 4, 2025, 10:10 AM EST

BY Doug Kass · Feb 4, 2025, 10:00 AM EST

PepsiCo PEP remains an investment short as the weakness in the snack business is likely to be a secular headwind.

The shares are down in early trading.

BY Doug Kass · Feb 4, 2025, 9:55 AM EST

BY Doug Kass · Feb 4, 2025, 9:50 AM EST

Very quietly three generational compounders are in a correction mode:

Not much of a discussion of this in the business media...

BY Doug Kass · Feb 4, 2025, 9:40 AM EST

The equity market has been in a 6% range since the election.

High valuations are a petri dish for the transient volatility we have seen on the past two Mondays.

It will not always be transient.

People are being led to still greater levels of complacency that raises the level of risk.

No one (maybe just me?) can know what will be the straw that breaks the camel's back or when that will occur.

But it is likely out there in the ozone.

BY Doug Kass · Feb 4, 2025, 9:30 AM EST

BY Doug Kass · Feb 4, 2025, 9:20 AM EST

-EVAX +68% (strength following 13G filing discloses 20% stake by Merck)

-IVVD +25% (momentum following VYD2311 data for COVID-19)

-PLTR +24% (earnings, guidance)

-SPOT +8.7% (earnings, guidance)

-GRAB +7.9% (considering takeover of Goto at IDR100/shr in ~$7B valuation; HSBC Raised GRAB to Buy from Hold, price target: $5.45)

-ATI +7.1% (earnings, guidance)

-SER +6.9% (receives second $5M tranche ahead of Phase 1 clinical trial in Advanced Parkinson’s Disease patients)

-KITT +5.6% (announces movement of second Aquanaut Vehicle into the Acceptance Testing Phase; files $100M mixed shelf)

-ELAB +5.5% (Northstrive Biosciences, Inc., a subsidiary of PMGC Holdings Inc., reports positive updates for Obesity Drug Candidates targeting Fat Loss and Muscle Preservation used in Combination with GLP-1)

-AXTA +5.4% (earnings, guidance)

-VCSA +5.3% (confirms Special Committee of the Board will carefully review Davidson Kempner offer at $5.25/shr)

-SMCI +5.2% (will provide Q2 FY25 business update on Tuesday, February 11, 2025)

-FOXA +4.5% (earnings)

-RACE +4.2% (earnings, guidance)

-IT +3.6% (earnings, guidance)

-ARMK +3.5% (earnings, guidance)

-PYXS +3.3% (initiates new PYX-201 Combination Trial and Initiates Cohort Expansions of Ongoing Monotherapy Trial)

-LITE +3.2% (raises Q2 guidance)

-SLAB +2.4% (earnings, guidance)

-CMI +2.2% (earnings, guidance)

-QSI +2.2% (establishes Scientific Advisory Board to shape next-generation proteomic technologies)

-REGN +2.0% (earnings, guidance)

-ATKR -13% (earnings, guidance)

-OMGA -12% (discloses restructuring scheme)

-MRK -8.6% (earnings, guidance)

-TNXP -7.8% (downside momentum; names new CTO)

-CTS -6.2% (earnings, guidance)

-SYNA -5.1% (reports prelim Q3; CEO steps down)

-ENR -4.1% (earnings, guidance)

-PNR -3.1% (earnings, guidance)

-DKNG -2.9% (Ohio Governor DeWine proposes to double sports betting tax in 2025 budget; HOOD announces sports betting available for Super Bowl)

-MPC -2.7% (earnings, guidance)

-PEP -2.2% (earnings, guidance)

-ADM -2.0% (earnings, guidance)

BY Doug Kass · Feb 4, 2025, 9:10 AM EST

11:00AM: Fed Bank of Atlanta President Bostic (Non-Voter) speaks on housing in a moderated conversation before a National Housing Crisis Task Force Meeting, Atlanta, GA ( Livestream available. No embargoed text. Audience Q&A expected. No media Q&A).

2:00PM: Fed Bank of San Francisco President Daly (Non-Voter) participates in hybrid discussion, "The Economy 2025: the Impacts of Tariffs, Tax Cuts and Trump" before the Commonwealth Club World Affairs of California, San Francisco, CA (Audience Q&A expected. No prepared remarks. No group media interview).

7:30PM: Fed Vice Chair Jefferson (Voter) speaks on the U.S. economic outlook and monetary policy before the Lafayette College Economics Department Special Lecture (Text available. Audience Q&A expected. Livestream details forthcoming).

BY Doug Kass · Feb 4, 2025, 9:00 AM EST

At 8:09 a.m.:

BY Doug Kass · Feb 4, 2025, 8:50 AM EST

At 8:28 a.m.:

BY Doug Kass · Feb 4, 2025, 8:40 AM EST

BY Doug Kass · Feb 4, 2025, 8:30 AM EST

* Anything goes these days...

* Be forewarned and reduce your "VAR."

"Every so often, a decision is made that so defies the bounds of good sense, it leaves you with no other choice but to conclude that the decision really does make sense and the problem is you. Perhaps then it’s best to view the Luka Dončić trade not as the most shocking and bizarre in NBA history but as the standard-bearer for a post-historic era of inverted reality such as the one in which we are living. America in 2025: The less sense something makes, the more it proves its own validity. The wisdom of any action is secondary to the reaction it induces. The greatest of the virtues is to troll thy neighbor. The chaos is the point."

- Philadelphia Inquirer On Luka Doncic, Joel Embiid, and a wild start to the NBA trade deadline | Opinion and Sixers stunned by Luka Doncic-Anthony Davis blockbuster trade: ‘Anything can happen’

The only certainty in (fiscal, trade and monetary) policy, politics, in our capital markets, in our social lives and, even in sports, is the lack of certainty these days.

The tariff chaos, the Luka Doncic trade and both yesterday's and last night's volatile and unpredictable intraday and intra-evening stock futures price swings are symptomatic of these uncertain times.

Yesterday S&P futures bottomed at -130 handles and almost closed unchanged. Last night, S&P futures peaked at +50 handles and bottomed at -35 handles.

Be forewarned, the ride has gotten much bumpier.

Get used to it and consider your "value at risk." (Invest and trade with smaller positions given the aforementioned volatility.)

Importantly, keep your portfolios and children far away from the "talking heads" who overly simplify the complex investment equation and parade on the stage with hubris and false confidence.

BY Doug Kass · Feb 4, 2025, 7:45 AM EST

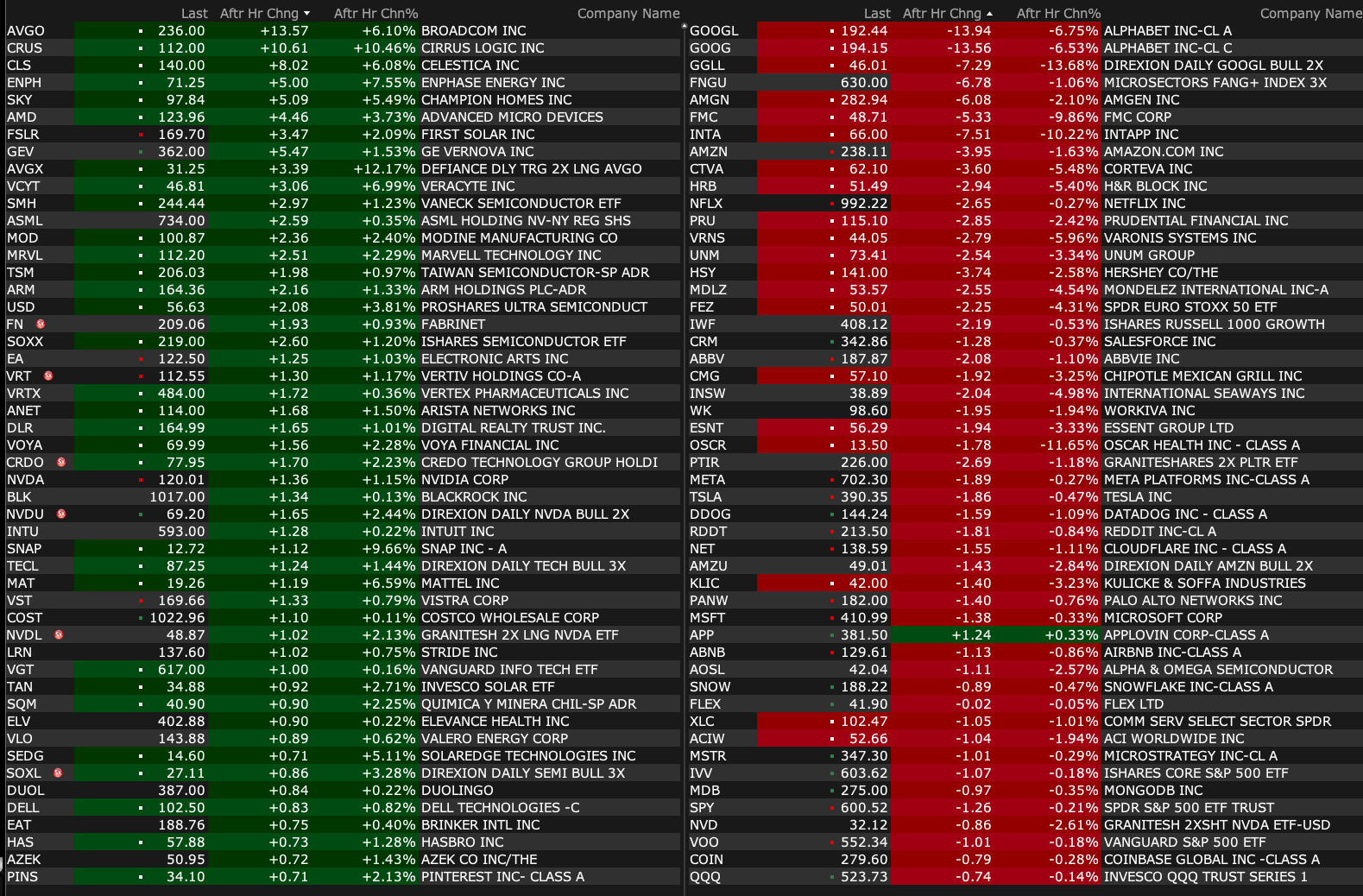

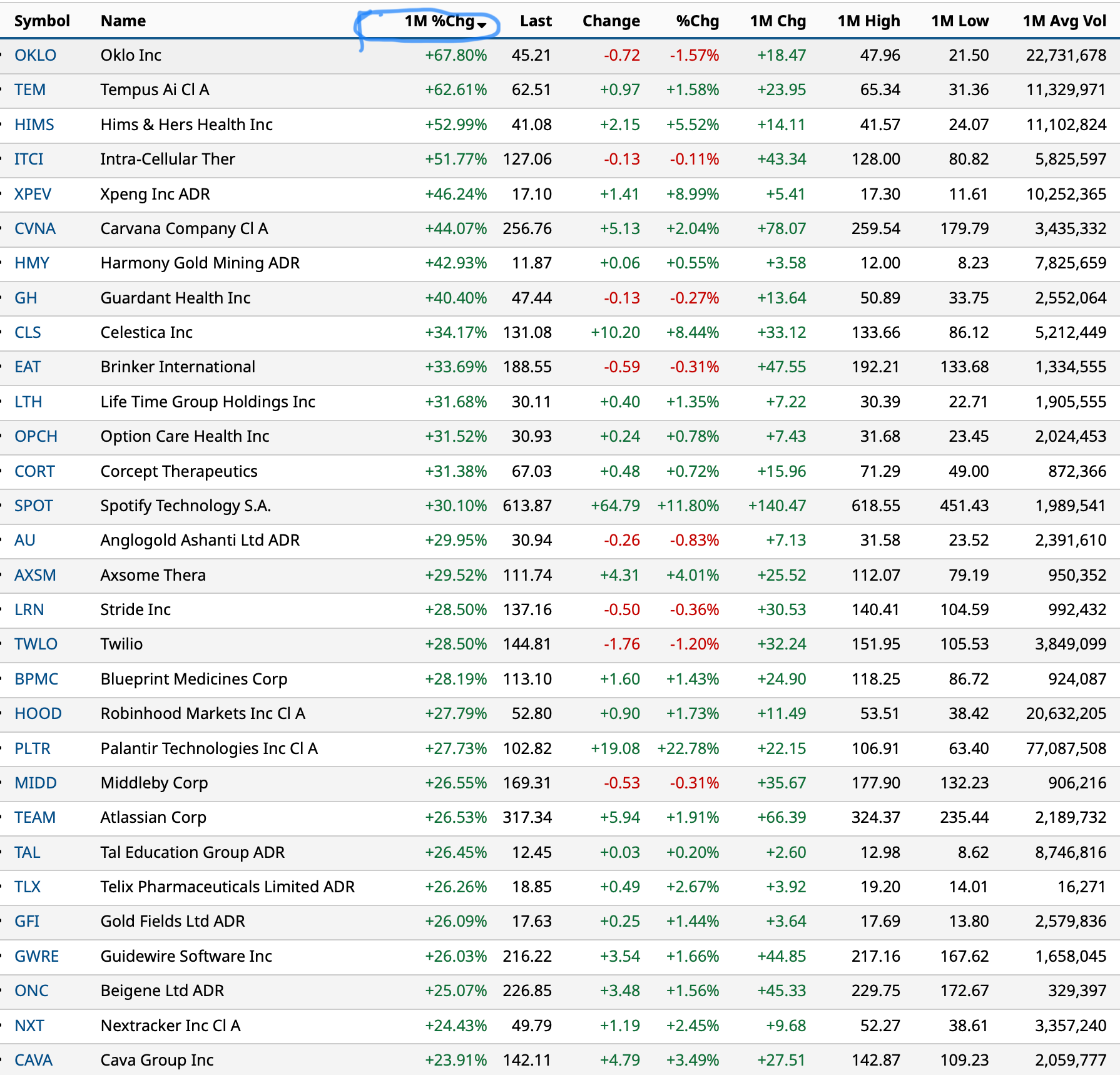

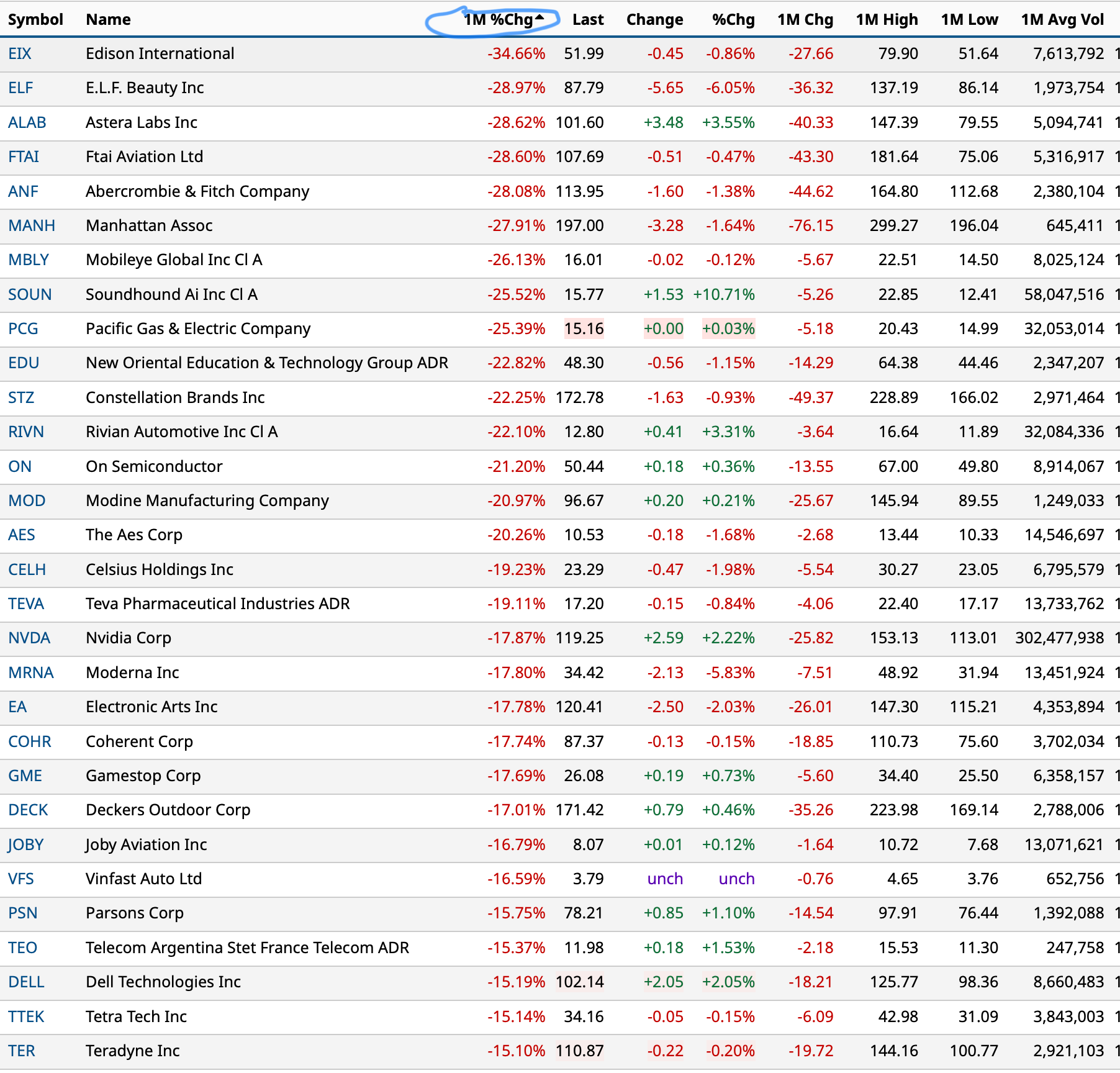

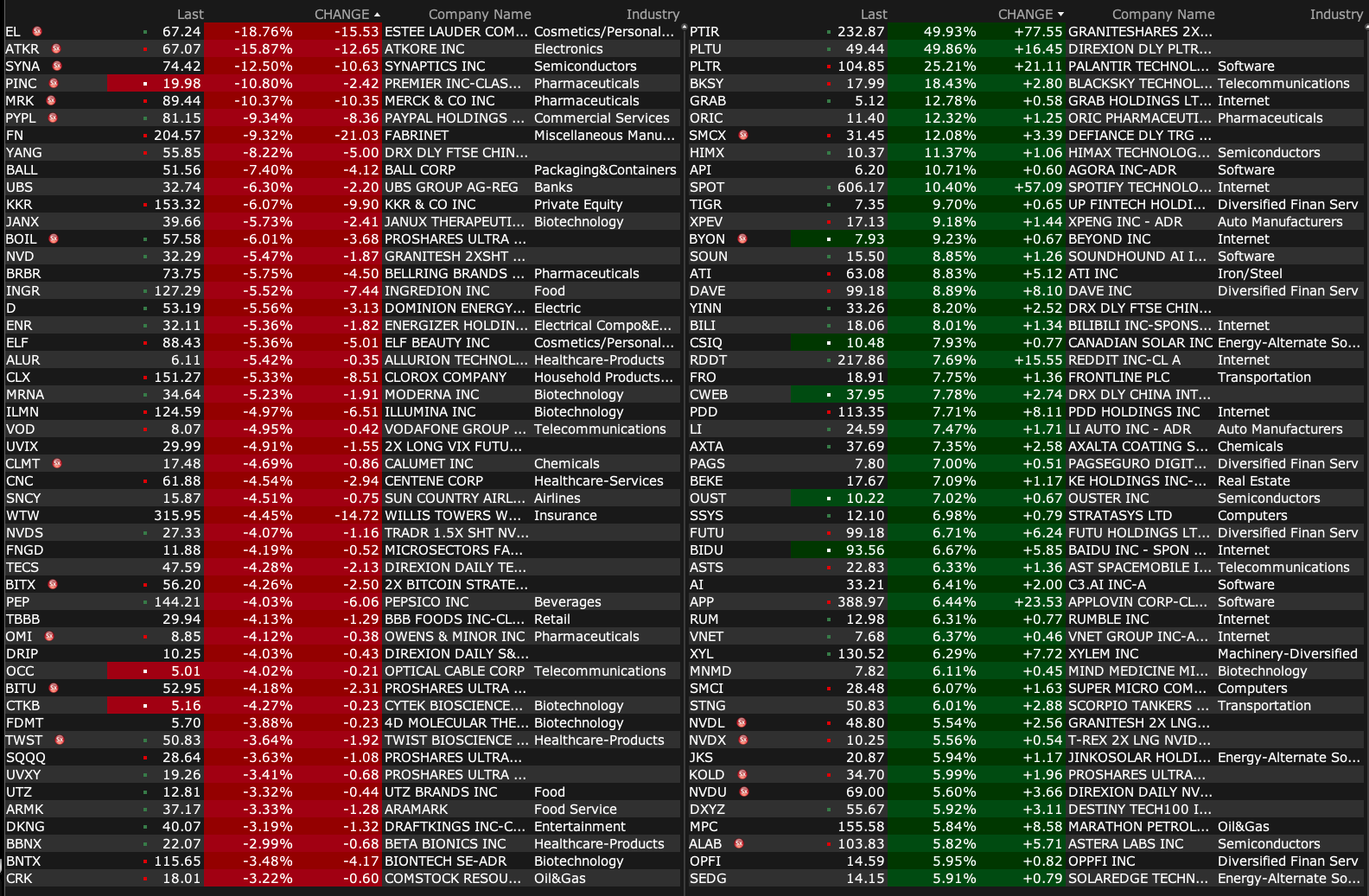

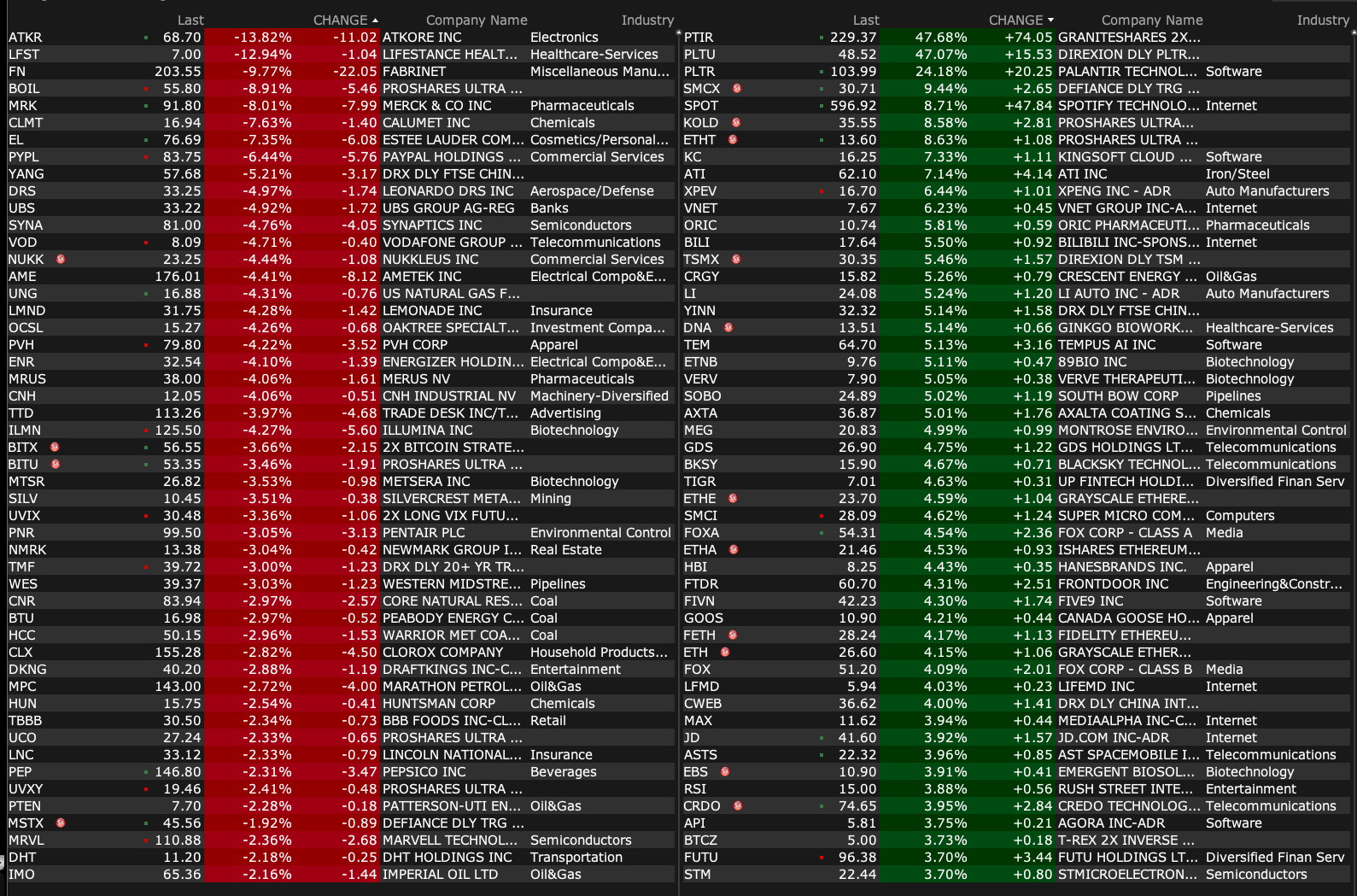

This is a valuable table for momentum-based short-term traders:

BY Doug Kass · Feb 4, 2025, 6:50 AM EST

From JPMorgan:

US: Futs are weaker after seeing a rallies following a delay of tariff implementation and then moved lower after China announced its retaliatory actions. Unlike yesterday, USD is weaker to start the session and the bond market reaction is muted, with the yield curve bear steepening 1-2bps. Pre-mkt, there is a bid for parts of Mag7/Semis. Cmdtys are lower with Energy getting hit but Base seeing a bid. Today’s macro focus is on JOLTS and Factory Orders.

and....

EQUITY AND MACRO NARRATIVE: We saw the opening salvo of Trade War 2.0 and though we saw delays, which multiple clients interpret as an eventual abandonment of the strategy. Now, we await any relief measures for China as well as whether the 30-day delay creates an overhang to US/DM stocks with EU the next, potential target.

· TARIFFS – The market is still debating the permanence of tariffs and several clients, plus the media, have highlighted the similarities to 2019, between the US and Mexico. The end game, at least for Mexico, may be increased border security. Later in the day, we saw a similar reprieve for Canada before China announced its countermeasures. From here, we may see a more moderate response until April when the tariff studies are expected to complete.

BY Doug Kass · Feb 4, 2025, 6:35 AM EST

BY Doug Kass · Feb 4, 2025, 6:25 AM EST

Wolf Street howls about Trump and the Fed.

BY Doug Kass · Feb 4, 2025, 6:15 AM EST

Wolf Street howls about Tesla.

BY Doug Kass · Feb 4, 2025, 5:55 AM EST

There has been a swift drop in the S&P Short Range Oscillator over the last 24 hours from 3.33% to 1.69%.

The market is far less overbought than it was a week ago.

BY Doug Kass · Feb 4, 2025, 5:45 AM EST