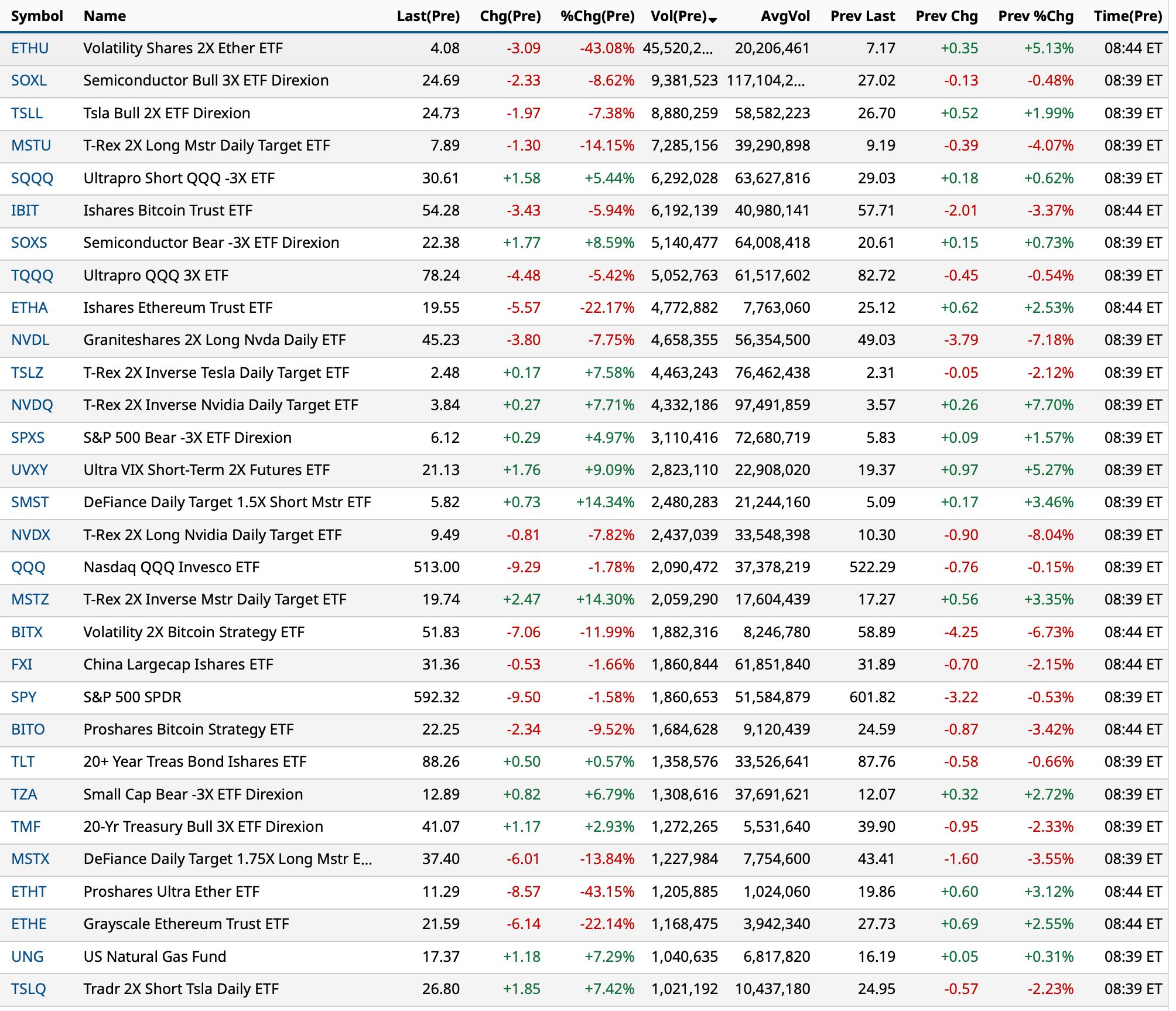

Back Shorting the Indexes

On the Canada tariff pause I am reestablishing my Index shorts in the after hours:

* SPY$601.20

* QQQ $521.92

BY Doug Kass · Feb 3, 2025, 5:05 PM EST

On the Canada tariff pause I am reestablishing my Index shorts in the after hours:

* SPY$601.20

* QQQ $521.92

BY Doug Kass · Feb 3, 2025, 5:05 PM EST

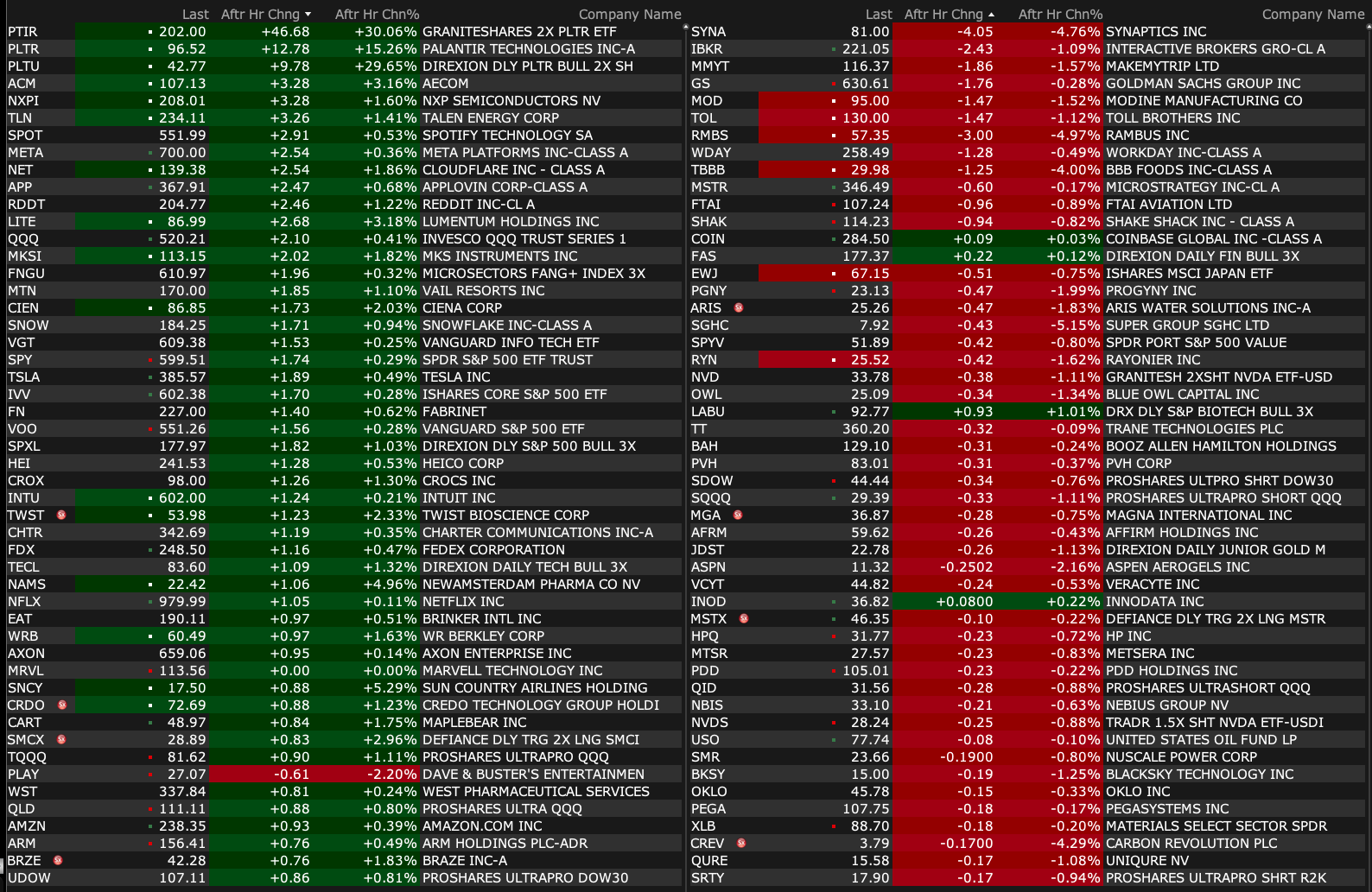

At 4:20 p.m.:

BY Doug Kass · Feb 3, 2025, 4:40 PM EST

BY Doug Kass · Feb 3, 2025, 4:27 PM EST

I just took a $2 profit in SPY $597.75 and QQQ $518.25 trading short rentals. That's the fourth profitable intraday trade in the day.

Out of the Indices.

BY Doug Kass · Feb 3, 2025, 4:08 PM EST

BY Doug Kass · Feb 3, 2025, 4:03 PM EST

Elanco ELAN continues to move lower.

We recently eliminated most of our common holdings. We remain short WOOF and long FRPT in the space:

* Morgan Stanley confirms our channel checks on this pet company...

This morning Morgan Stanley lowered its price target on Elan (ELAN) from $15 to $14 - keeping equal weight:

After having met with several Animal Health management teams at VMX, the world's largest companion animal health conference, the Morgan Stanley analyst tells investors that "sentiment was cautious into 2025" on low compliance and deteriorating vet office visit trends.

In light of foreign exchange dynamics and "a continuing lackluster vet visit backdrop," the firm is trimming estimates and price targets for Zoetis (ZTS) , Idexx (IDXX) and Elanco.

From Morgan Stanley's report:

We met with several management teams and animal health industry professionals at VMX, notably Zoetis, Elanco Animal Health, IDEXX Laboratories, Covetrus, Patterson Companies, among other constituents. Some key takeaways from our conversations include: (1) vet office visits / compliance remain an enduring headwind across the industry likely continuing well into 2025; (2) innovation and leveraging across the industry likely continuing well into 2025; (2) innovation and leveraging alternative channels offer offsets for pharma in a lackluster demand backdrop (ELAN, ZTS); (3) dermatology and parasiticides may get more competitive (MRK AH potential '25 launches, covered by MS Pharma Analyst Terence Flynn), (4) price increases are only slightly more subdued than '24 (still +MSD across AH pharma); and (5) IDXX showcased its innovation lineup, detailing Cancer Dx, albeit offering limited insight into inVue traction (LT prospects remain favorable, in our view, see survey here).

Importantly, in light of FX dynamics and a continuing lackluster vet visit backdrop, we are trimming our estimates and Price Targets for ZTS, IDXX, and ELAN. Enclosed, we detail key model updates as well as takeaways by company across pharma, diagnostics, and services in Animal Health.

Two days ago I cautioned on ELAN:

Our channel checks for Elanco (ELAN) are a bit disappointing.

I was hopeful that the company would be street expectations, but that now appears challenging.

Though the quarter is not reported until February 24 (four weeks away), discretion is the better part of valor and I have sold most of my common holdings.

However, I am keeping my calls (as the pet company remains a bonafide takeover candidate).

By Doug Kass Jan 29, 2025 9:43 AM EST

BY Doug Kass · Feb 3, 2025, 3:52 PM EST

From Charlie!

BY Doug Kass · Feb 3, 2025, 3:45 PM EST

My average on the most recent dive into short Indices over the last few minutes are:

* SPY $600.04.

* QQQ $520.55.

BY Doug Kass · Feb 3, 2025, 3:24 PM EST

I've added to Index shorts, moved to small from very small.

BY Doug Kass · Feb 3, 2025, 3:00 PM EST

On the big rally from the lows and with S P cash now only -21 I am back short SPY at $599.90 and QQQ at $520.51.

BY Doug Kass · Feb 3, 2025, 2:35 PM EST

* 5 days, 10 hours to Spring Training!!! Spring Training Countdown

Once again, the market had more intraday moves than a shortstop batting .110 today!

It's a terrific market for opportunistic and disciplined traders not so great for the buy-and-hold crowd.

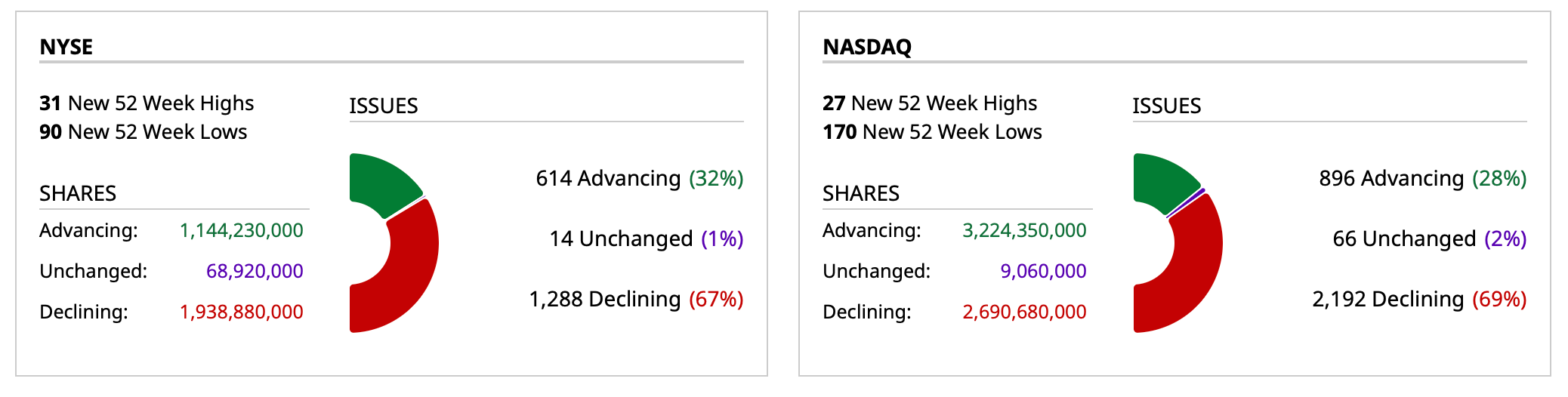

Breadth is weak but improved from earlier in the morning:

At 2:00 p.m. S&P cash is down by about -30 handles and the equal weighted S&P Index (RSP) is down by only -0.47%:

Here are today's "Things":

* I added to shorts in JPM at $257.03, GS at $637.4 and SBUX at $107.66.

* I added to MSOS at $3.31. Also CRLBF at $0.87, AYRWF at $0.46, GLASF at $5.43, CURLF at $1.26, TCNNF at $4.64, GTBIF at $6.81 and VRNOF at $1.22.

* I day traded (three times) the Indices — all for small profits. (I currently have no Index positions on).

BY Doug Kass · Feb 3, 2025, 2:25 PM EST

* Anthony and Shadd at 4 p.m. today...

Cannabis Stock Ayr Wellness President Explains Future Plans

AYRWF - high risk, high reward.

BY Doug Kass · Feb 3, 2025, 1:55 PM EST

I am on a roll:

BY Doug Kass · Feb 3, 2025, 12:45 PM EST

From Peter Boockvar:

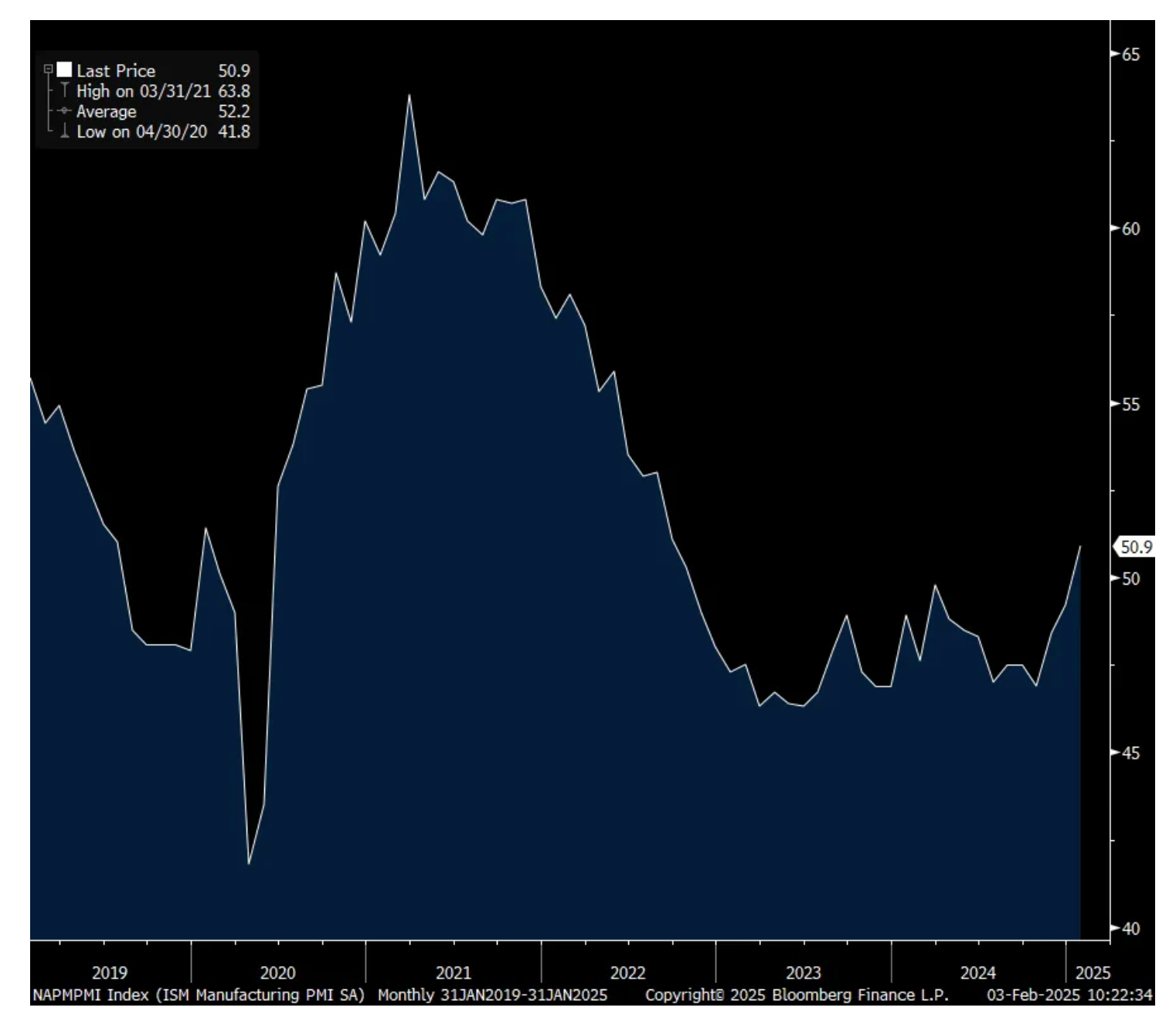

US mfr'g sees some positive light after 26 months of contraction

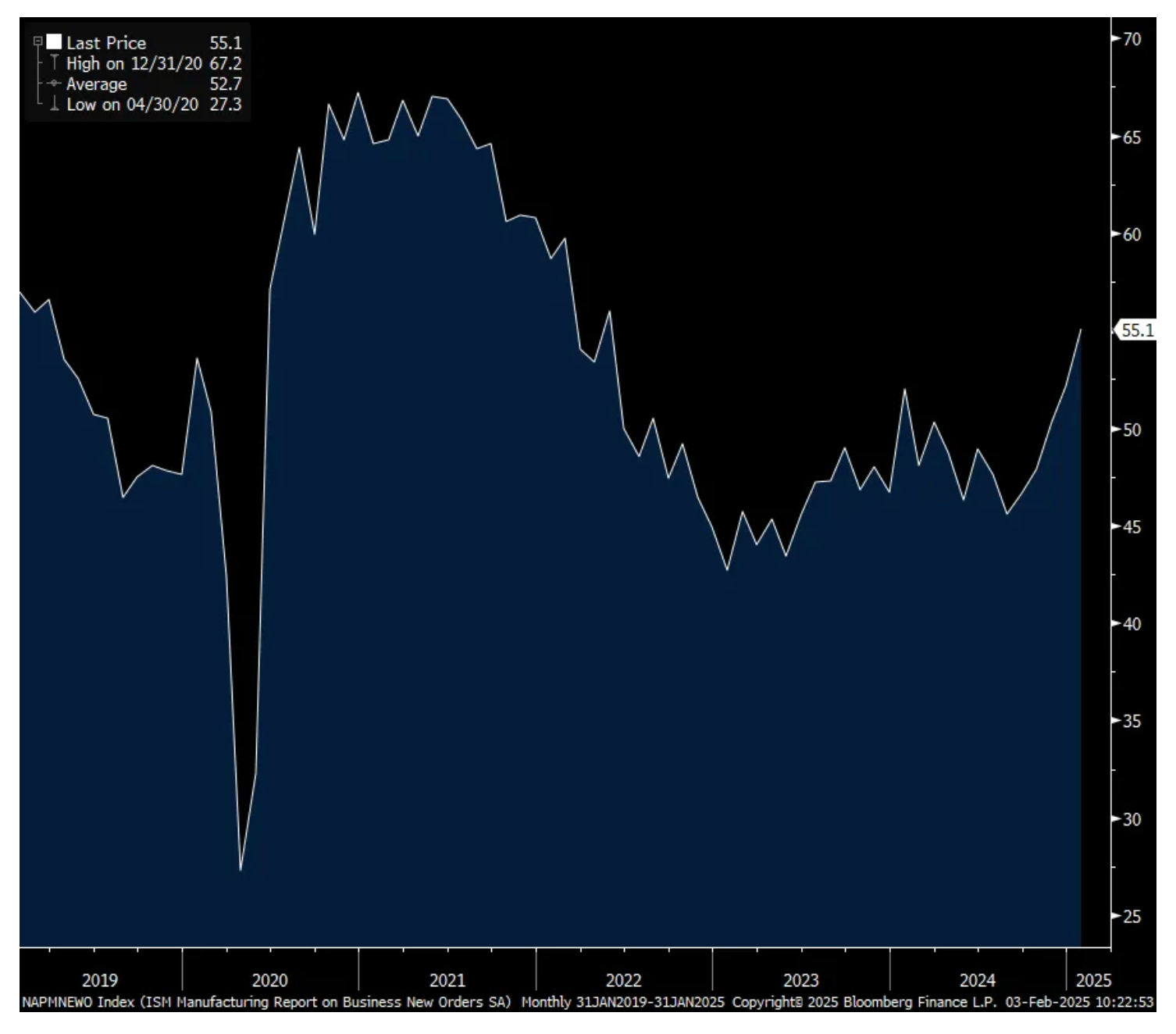

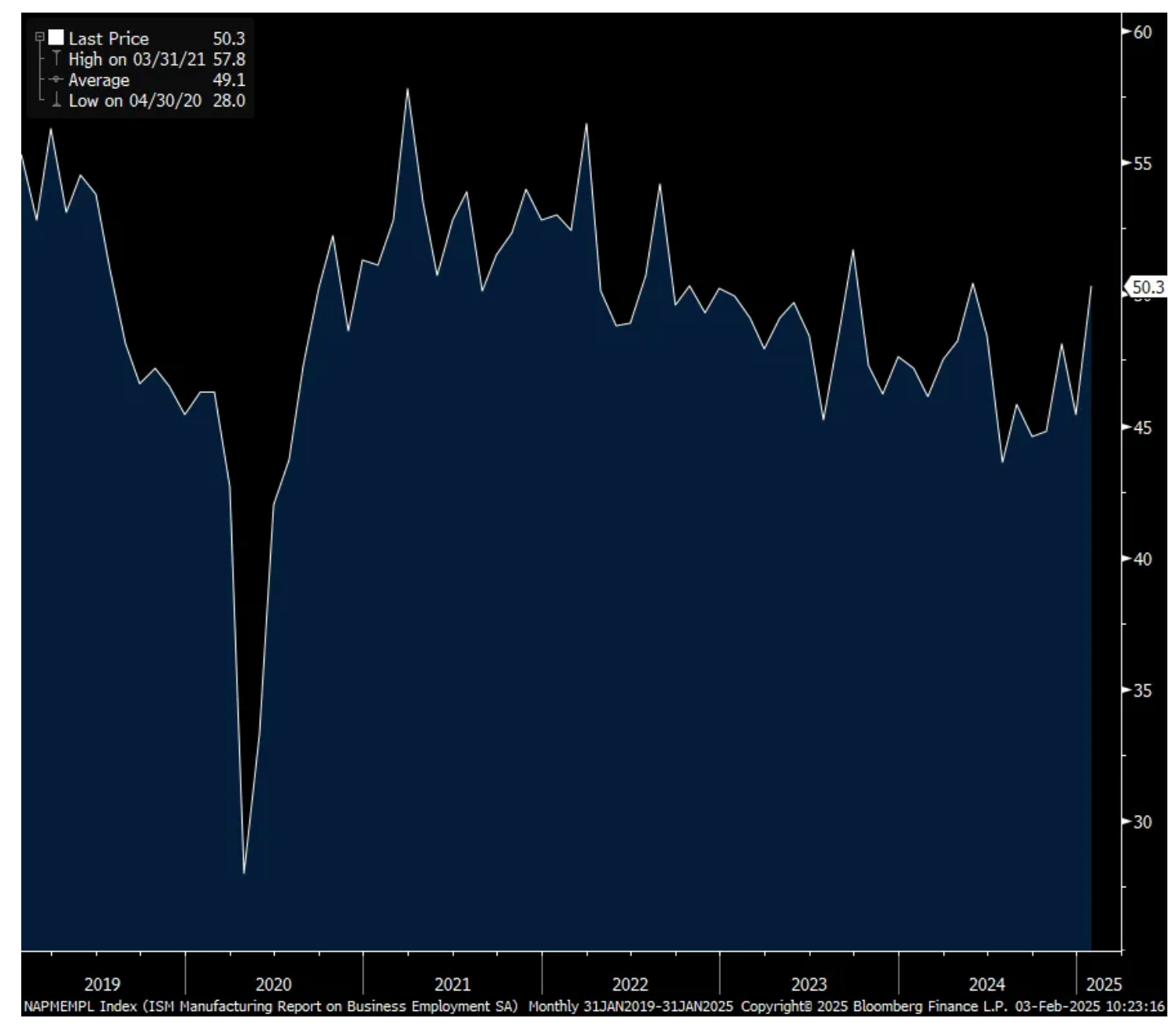

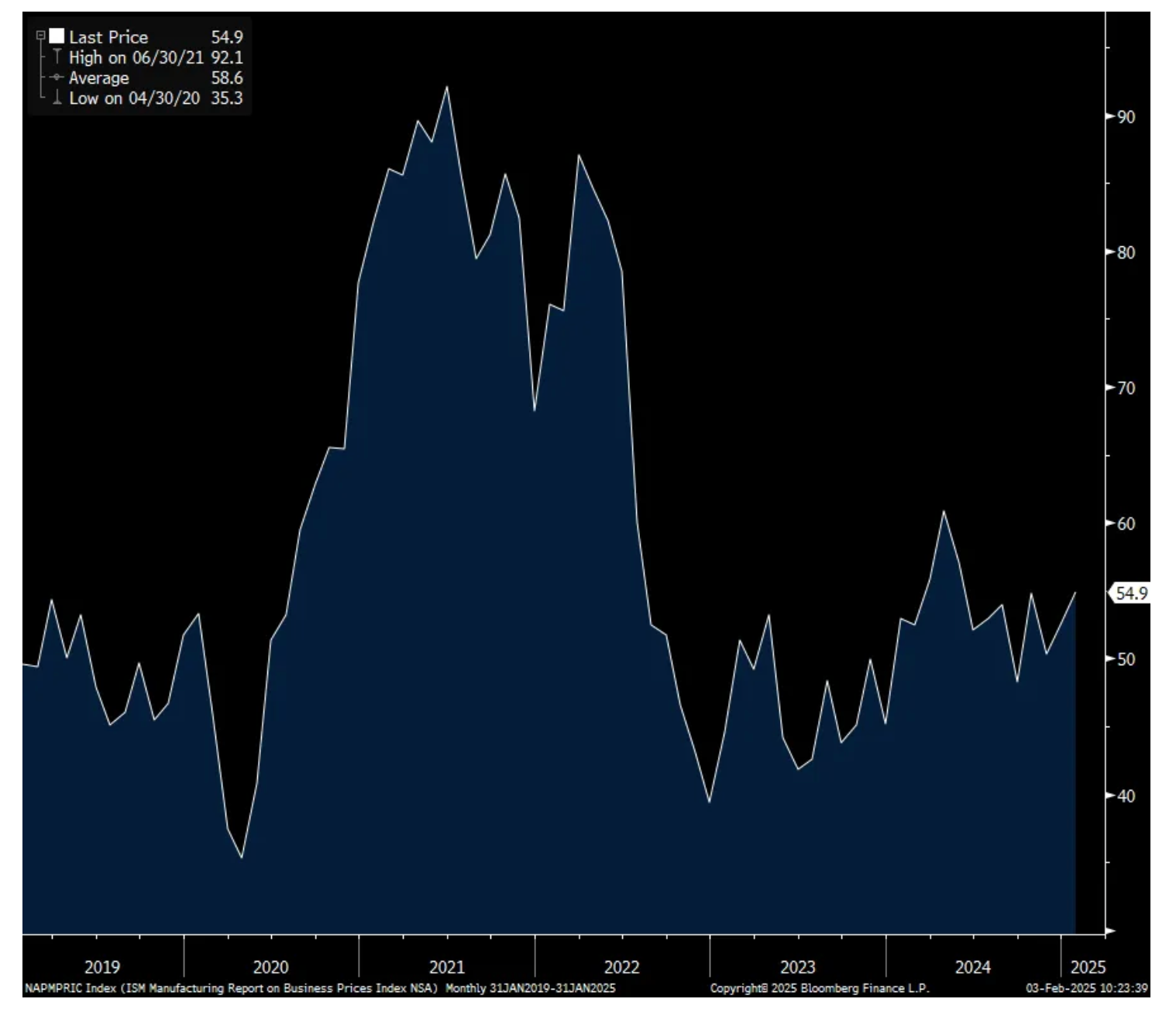

The January ISM manufacturing index was 50.9, just above the estimate of 50 and finally expressing some level of expansion/optimism after about two years of contraction. It’s the best level since September 2022 and helped by new orders which increased to 55.1 from 52.1 on the heels of inventories falling to a 3 month low. Employment was a bright spot too, rising to 50.3 from 45.4 and the first time above 50 since May of last year. Export orders rose 2.4 pts and is above 50 for a 2nd month. Backlogs remained sluggish though, falling 1 pt to 44.9. Supplier deliveries rose almost 1 pt and is above 50 for a 2nd straight month but around 50 at 50.9. Prices paid rose by 2.4 pts m/o/m to 54.9 which is the highest since May 2024.

Breadth was mixed as 8 of 18 industries saw growth vs 7 seen in December. Eight too experienced a contraction, also vs 7 in the month before. The balance saw no change in their business.

Bottom line, after 26 straight months of below 50 prints, implying manufacturing contraction, we finally see some stabilization. That said, there are still a bunch of things to think about on where we go from here. The obvious is tariffs and its impact, along with the US dollar strength for those exporting but also understanding that at the end of 2024, there was a bunch of ordering and inventory drawdowns (as seen in the Q4 GDP report) as buyers rushed to procure products before the oncoming tariffs. It’s likely that the new orders rise follows that inventory shelf clearing.

And in order to sustain a manufacturing recovery we need to see a pick up in end demand for goods and that remains to be seen as consumers both focus on spending money on services/experiences and the high cost of money limits big ticket items. The area of manufacturing we should see a rebound in is stuff related to the home as LA and the hurricane hit parts of North Carolina, Georgia and Florida rebuild what was destroyed.

Here are some anecdotes from respondents in some specific industries:

“Customer orders slightly stronger than expected. Seeing more general price increases for chemicals/raw materials. No International Longshoremen’s Association strike is a tremendous help.” [Chemical Products]

“Alleviating supply chain conditions are noticeably pivoting back into acute shortage situations, with headwinds following. For aerospace and defense companies, critical minerals supply chains are tightening dramatically due to Chinese restrictions. Concerns are growing of an environment of more supply chain shortages.” [Transportation Equipment]

“As the U.S. administration transfers, we will continue to monitor impact of tariffs on materials used for manufacturing. China stimulus is helping us win orders and increase use of services and consumables. Cost pressures remain for all materials and parts but are starting to stabilize.” [Computer & Electronic Products]

“Volume in 2025 is targeting 2-percent growth. The organization is mindful of potential tariffs and what to do with re-routing or cost increases in supply chains that are impacted.” [Food, Beverage & Tobacco Products]

“Although we are in our busy season, our demand for the first two weeks of 2025 has outpaced normal levels for this period of time.” [Machinery]

“Business is slowly improving.” [Electrical Equipment, Appliances & Components]

“Capital equipment sales are starting 2025 off strong. Normally, we see a soft start to the year, so this strong start is unusual.” [Fabricated Metal Products]

“New orders are still good but decreasing compared to previous quarters. Working through current backlog.” [Miscellaneous Manufacturing]

“Automotive order demand continues to be consistent and on a steady pace. Beginning to look at hiring additional team members once again. Pricing is holding firm. Having to work overtime to cover plant inefficiency to date.” [Primary Metals]

“Looking forward to a year of strong customer demand and higher sales than 2024.” [Textile Mills]

ISM Mfr’g

New Orders

Employment

Prices Paid

BY Doug Kass · Feb 3, 2025, 12:15 PM EST

BY Doug Kass · Feb 3, 2025, 12:00 PM EST

I'm adding to the following shorts:

* JPM $266.84

* SBUX $107.63

* GS $637.55

BY Doug Kass · Feb 3, 2025, 11:36 AM EST

BY Doug Kass · Feb 3, 2025, 11:30 AM EST

SPY at $596.35 and QQQ at $517.31 - for a small gain.

Too volatile for this guy right now!

BY Doug Kass · Feb 3, 2025, 11:23 AM EST

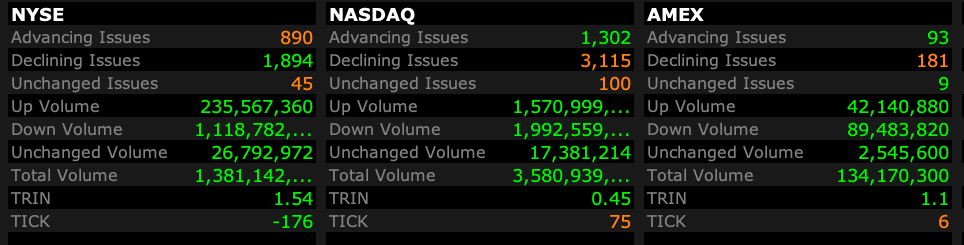

- NYSE volume 36% above its one-month average

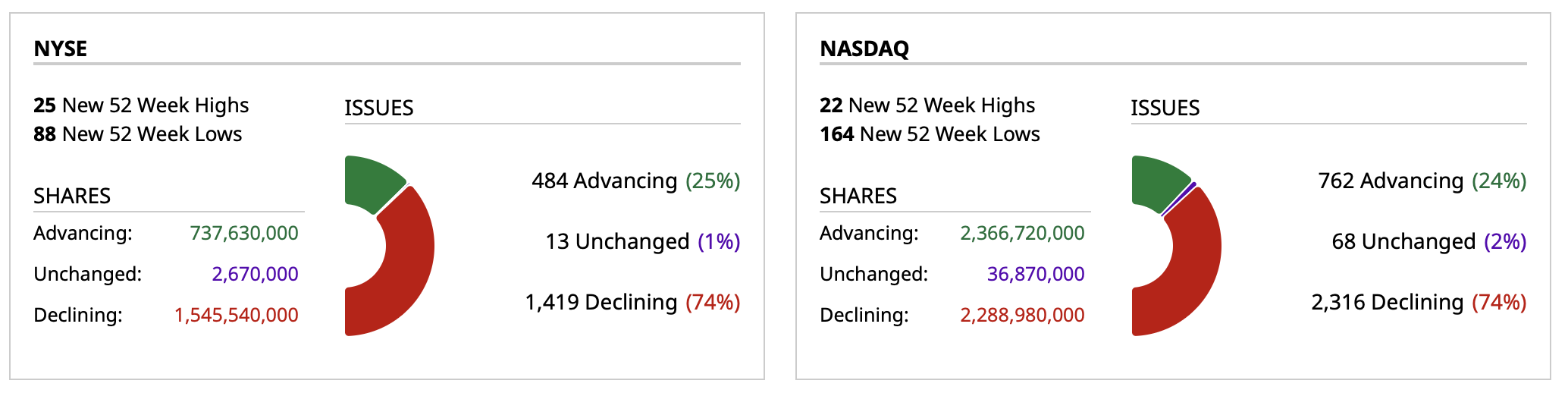

- NASDAQ volume 17% above its one-month average

- VIX: up 7.91% to 17.73

BY Doug Kass · Feb 3, 2025, 11:15 AM EST

BY Doug Kass · Feb 3, 2025, 11:00 AM EST

Small shorts SPY and QQQ at $598.36 and $518.93, respectively.

BY Doug Kass · Feb 3, 2025, 10:49 AM EST

BY Doug Kass · Feb 3, 2025, 10:33 AM EST

From Peter Boockvar:

"The Dumbest Trade War in History"

Not a surprise to my long time readers as I'm going with the WSJ editorial page on this one titled, "The Dumbest Trade War in History." They said, "This reminds us of the old Bernard Lewis joke that it's risky to be America's enemy but it can be fatal to be its friend. Leaving China aside, Mr. Trump's justification for this economic assault on the neighbors makes no sense."

It went on, "Mr. Trump sometimes sounds as if the US shouldn't import anything at all, that America can be a perfectly closed economy making everything at home. This is called autarky, and it isn't the world we live in, or one that we should want to live in, as Mr. Trump may soon find out."

They quote the Cato Institute's Scott Lincicome who specifically says about the auto industry, "Thousands of good paying auto jobs in Texas, Ohio, Ilinois and Michigan owe their competitiveness to this ecosystem, relying heavily on suppliers in Mexico and Canada." By the way, I saw today that Nomura estimates the hit to the operating profit of the US auto industry at $33 billion with these tariffs.

And then lastly, "Then there's the prospect of retaliation, which Canada and Mexico have shown they know how to do for maximum potential impact."

I'm on board with the rest of the economic policies of Trump 2.0, particularly what is to come on the regulatory side but just not on this tariff approach as said here many times since 2018 under both Trump and Biden.

As for the defenders of the tariffs, all we hear is that it doesn't cause inflation as it's a one time price set and we didn't see it after the 2018 tariffs. Fine but what we did see after that tariff battle was a US manufacturing recession that resulted in Jay Powell and the Fed cutting interest rates in 2019. We don't seem to hear about that now when debating tariffs.

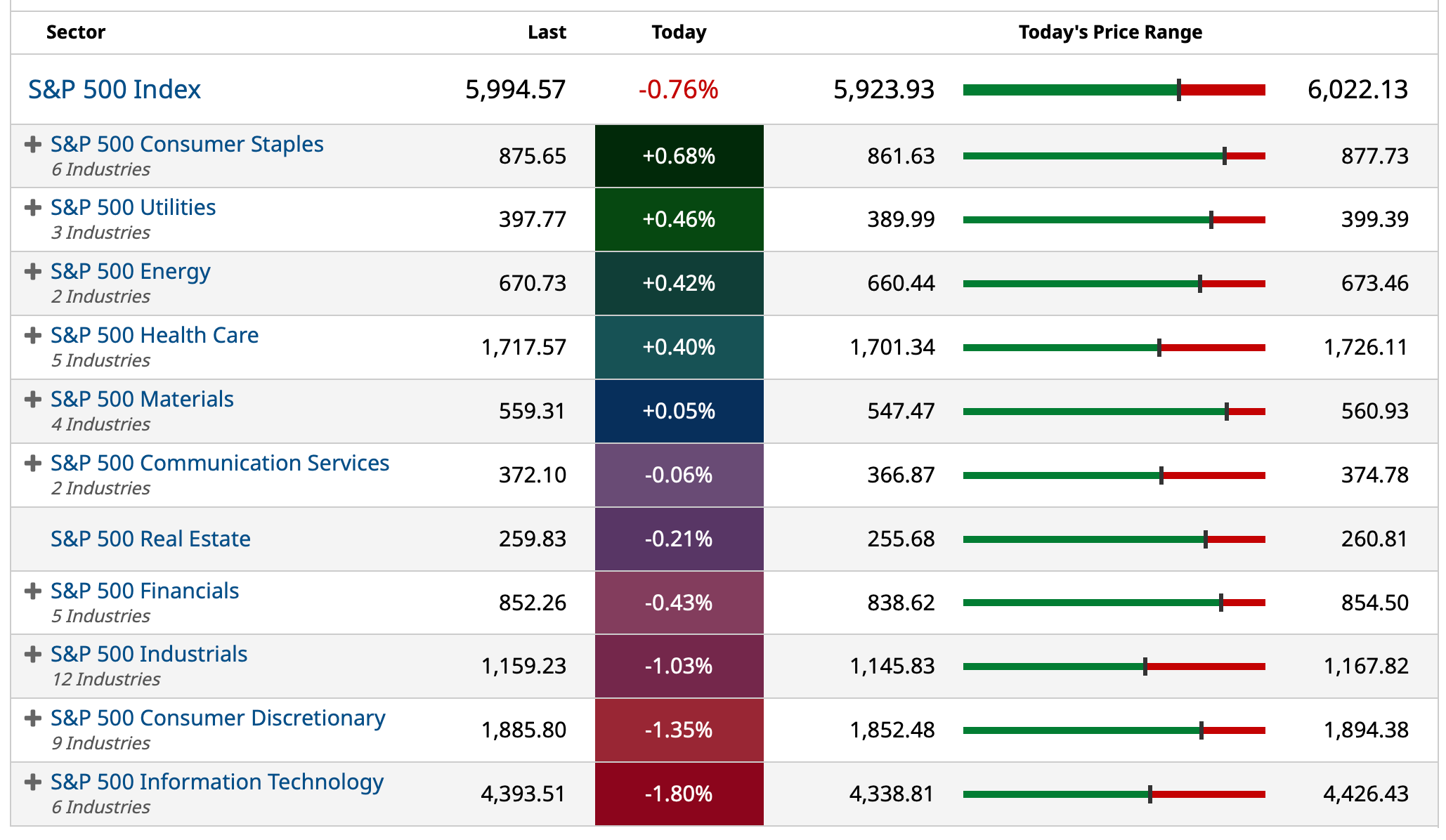

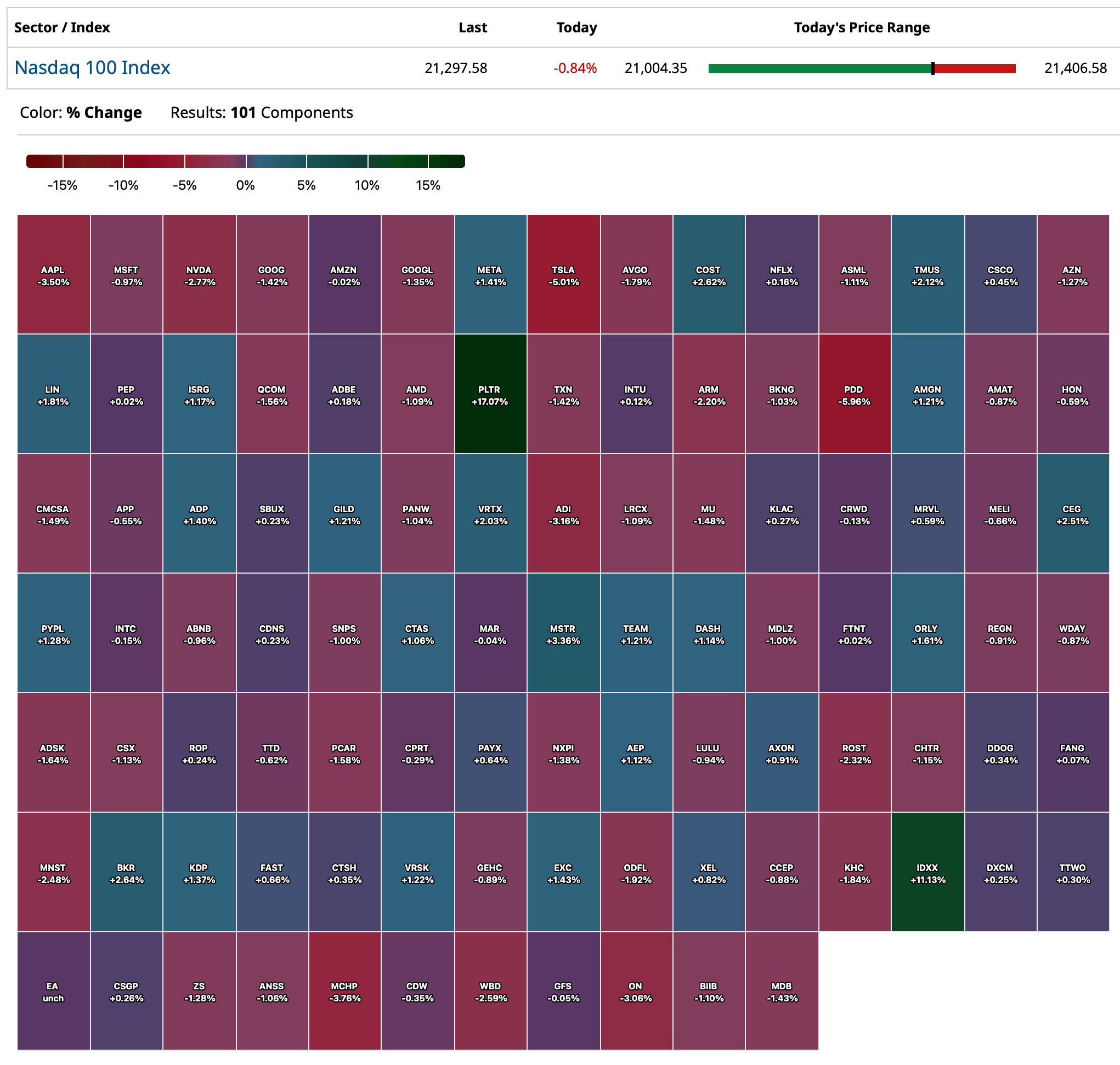

Here is a chart of the ISM manufacturing index and you can see it peaked in February 2018 just as the tariff battle was getting underway and that 2019 weakness saw Fed rate cuts as said. I've also included below the manufacturing component of US industrial production. It peaked in September 2018 and we've yet to surpass that level.

ISM Manufacturing Index during 2017, 2018 and 2019

US Manufacturing component of industrial production, still waiting to exceed Sept 2018 level

With regards to the Federal Reserve, in answer to a question Jay Powell was again dismissive of the easy financial conditions we currently have and how it influences their policies even though he historically reacted to the tightening of financial conditions. As heard on Friday, Michelle Bowman has a different take. She said "I continue to be concerned that easier financial conditions over the past year may have contributed to the lack of further progress on slowing inflation. In light of the ongoing strength in the economy and with equity prices substantially higher than a year ago, it seems unlikely that the overall level of interest rates and borrowing costs are exerting meaningful restraint."

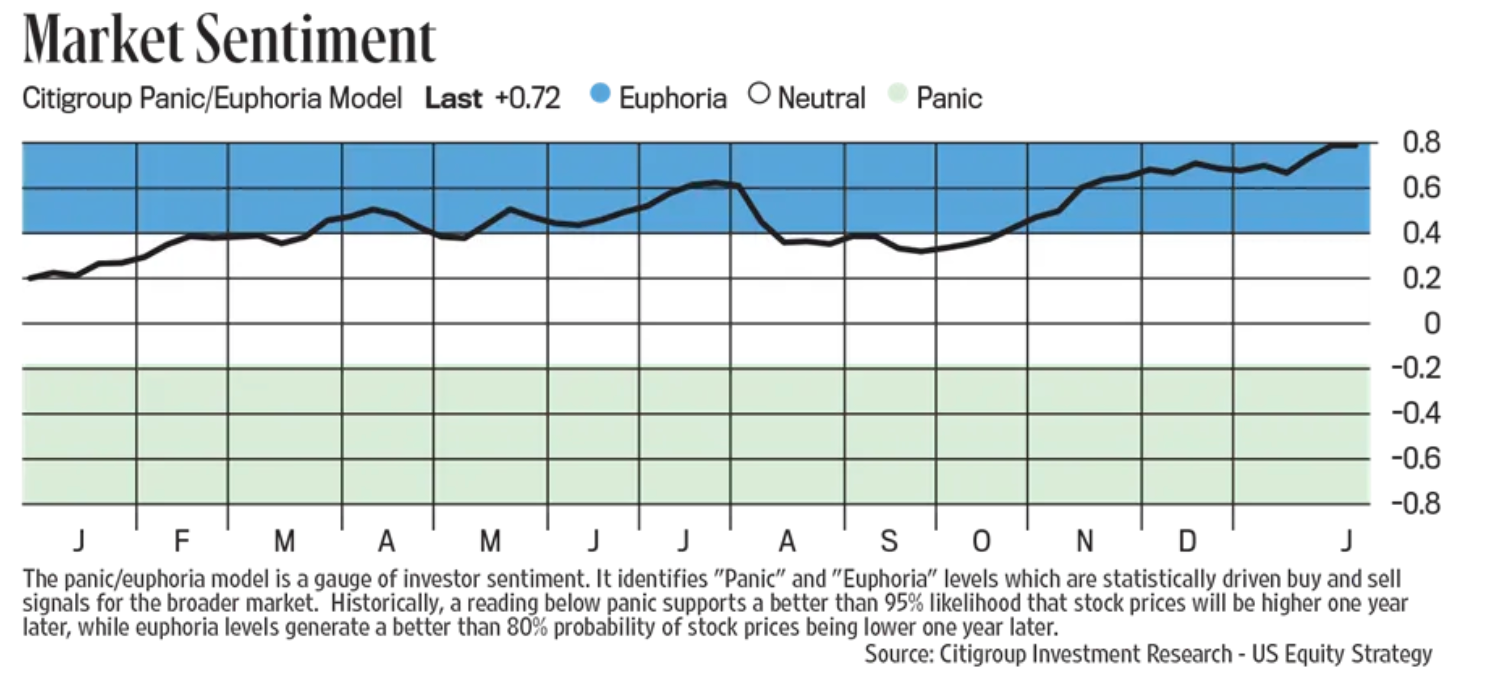

All this news just as the Citi Panic/Euphoria index continues to get more euphoric and to a multi year high at .72, well above the .41 threshold that classifies as such.

I read something positively about the sclerotic European economy over the weekend and it was the realization of it and the need to do something about it. ECB president Christine Lagarde and European Commission president Ursula von der Leyen both penned an opinion piece in the Financial Times titled "Europe has got the message on change...We can no longer squander our strengths with self-imposed handicaps. There is too much at stake." They propose three cures, "First, we need to make the EU an easier place for innovative companies to grow...Second, we need to make Europe a better place to invest. Two out of three EU companies say that regulation is a key obstacle to investment, while just 14% of them are using AI...Third, we need to make doing business in Europe cheaper, especially in terms of energy costs." Amen.

These are very important acknowledgments and hopefully we'll see actions addressing them as the world needs a more economically vibrant European economy. https://www.ft.com/content/fba6b27a-3a72-4451-8c75-ea8533c62681

Here's a rundown of the January manufacturing PMI's from overseas but obviously doesn't capture the tariff news and still reflects global sluggishness when it comes to this important sector. China's Caixin 50.1 vs 50.5, Taiwan 51.1 vs 52.7, South Korea 50.3 vs 49, Thailand 49.6 vs 51.4, Vietnam 48.9 vs 49.8, Malaysia 48.7 vs 48.6, Philippines 52.3 vs 54.3. Japan was revised to 48.7 from 48.8, Australia's to 50.2 from 49.8 and India's to 57.7 from 58 initially.

The Eurozone manufacturing index was revised up a touch to 46.6 from 46.1 initially and vs 45.1 in December. The last time it was above 50 was in June 2022. The UK manufacturing index was 48.3, up from 47 last month.

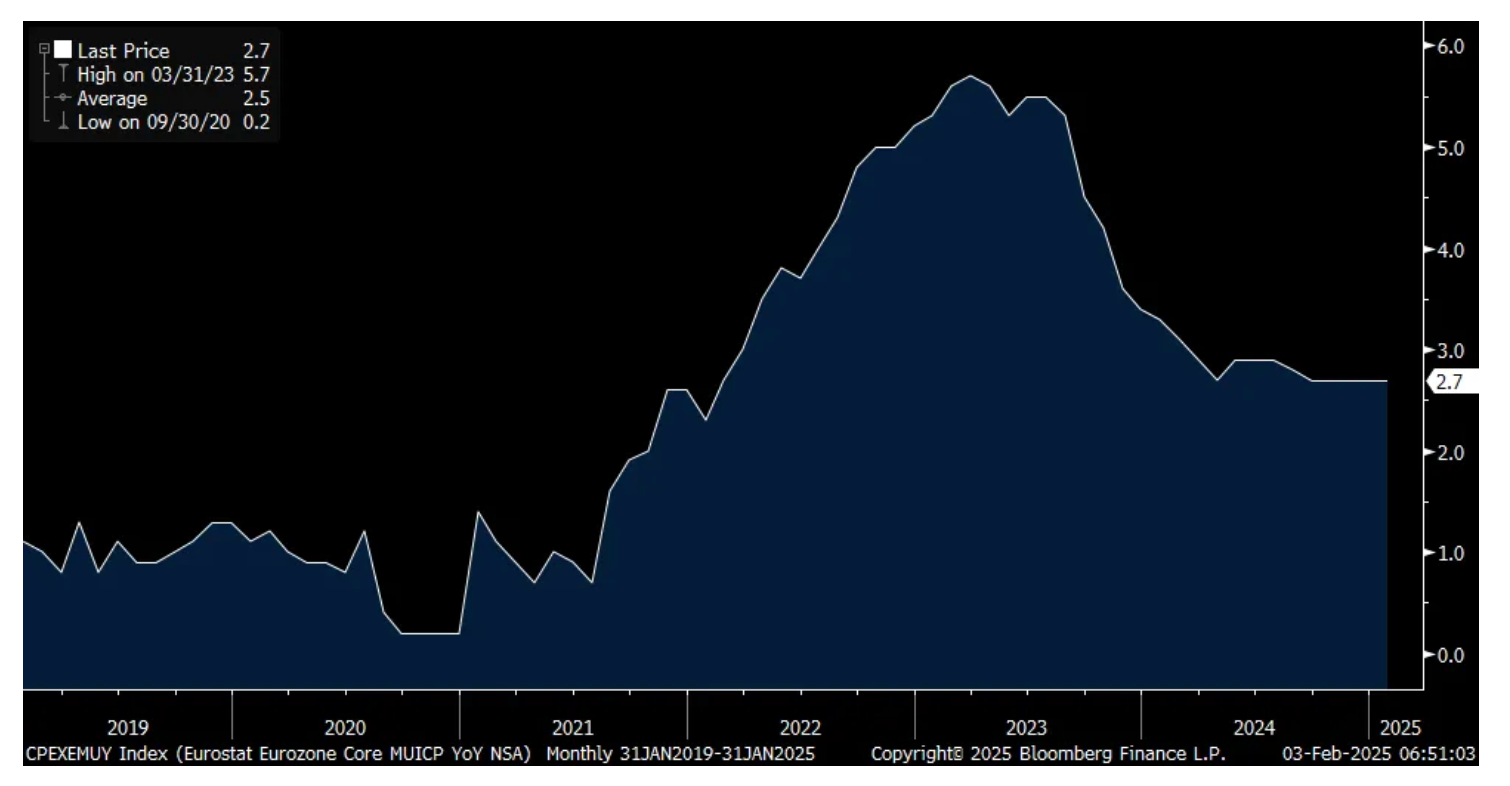

The Eurozone also reported its January CPI and it rose 2.5%, up one tenth from the December pace and one tenth more than expected. The core rate was higher by 2.7%, also one tenth above what was estimated and vs 2.7% in December. With an ECB deposit rate of now 2.75%, the ECB is back to ZERO real rates again but at least not yet is it negative. The ECB has obviously shifted their focus to regenerating economic growth rather than stick to its sole mandate of price stability.

Core CPI y/o/y in Eurozone

A few earnings call comments of note from Friday.

From Eaton and after seeing the 'electrical equipment' category within US industrial production last week showing strength:

"In electrical, our end markets performed better than expectations due to strength in data centers and in the Americas market."

Also, "In aerospace, markets grew nicely and in line with plan, and this was despite the Boeing strike.

"And our vehicle markets were a bit of a mixed bag, with better than planned performance in commercial vehicles, offsetting weakness in the light vehicle market, which includes eMobility."

From WW Grainger, the big distributor of many things selling into the industrial/manufacturing space:

"In the US, we expect market volume for the full year to remain muted. This is consistent with what we're seeing in the current short cycle environment and does not assume a step change macro recovery that some are projecting for the back half of the year."

From Lyondell, the big specialty chemical company:

"Across our key businesses, fourth quarter industry margins are about 60% of historical averages, underscoring the depth of the current downturn."

"We recognize that current dynamics represent more than just typical cyclical pressures. They also reflect some structural shifts in the industry relative to prior cycles. Slower global growth, particularly in China, structurally higher energy costs, regulatory impacts in Europe and other regions, along with the potential for capacity additions to outpace demand have introduced sectoral challenges. These shifts are contributing to the depth and duration of the current downturn and will likely moderate future mid-cycle margins relative to the prior decades."

BY Doug Kass · Feb 3, 2025, 10:30 AM EST

I am again buying across-the-board in cannabis stocks this morning.

I am making no "mainstream" long purchases and have not shorted a thing.

BY Doug Kass · Feb 3, 2025, 10:15 AM EST

Regarding export controls, the lightbulb finally seems to be going off in the heads of the U.S. government.

This has been obvious for a long time. Better late than never, I guess?

Export controls, the way currently implemented, are a paper tiger and were just done for publicity. So easy to evade, by shipping to a legal party in a legal domicile, who then turns around and ships to China. Some of whom may be shell companies. I have been referencing this issue for a long time, and it has been patently obvious for a long time:

Did DeepSeek Use Shell Companies In Singapore To Procure Nvidia Blacklisted Chips?

Now... from my prior "Tales" from a few days ago, although I have been referencing this for months:

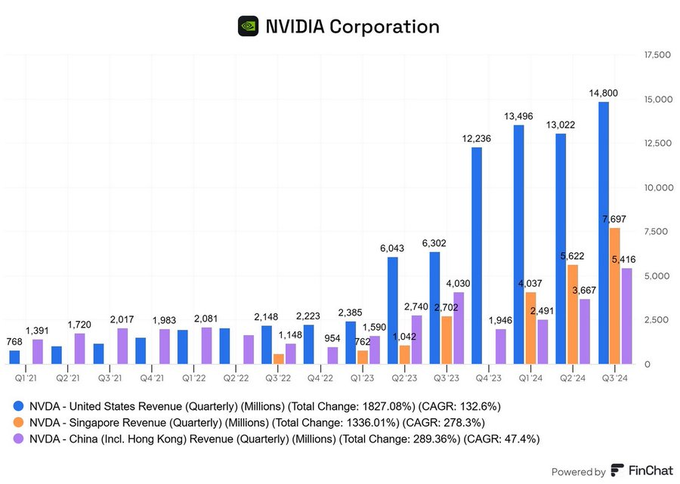

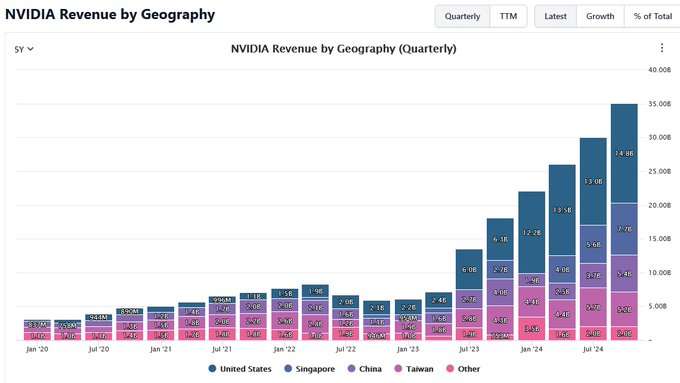

Interestingly, all the recent growth has been coming from Singapore. U.S. growth has already really slowed, which tells you something. To whit, NVDA U.S. revenue growth over the last 3 quarters +21%. NVDA's Singapore revenue in the last quarter was $7.7B (+185% YoY) - more than half its U.S. revenue in the same quarter. Seems rather strange given the export controls? Where does it go once it gets to Singapore? Also the fact that U.S. growth has now slowed to 21pct y-y tells you something about underlying U.S/ demand, and how it is flattening.

Oops, one more little bit on this issue. It can go beyond China/China affiliated entities procuring chips they are not meant to be able to get. They can also theoretically use hosted capacity that is hosted in an offshore legal domicile (Saudi, UAE, Dubai, etc.) which is running the chips and other technology China is not meant to have access to. This is functionally not much different than procuring the chips. Although I guess it could be possible to shut this stuff down by not allowing China/China affiliated entities to access it. My guess, the chip sales alone into China, understate by a fair bit, the actual amount of practical capacity that China is consuming of chips and technology that they are not meant to have access to.

If the U.S. government is serious, they will have to curtail Chinese access to this hosted offshore stuff too, somehow.

And one more small follow-up.

The U.S. shouldn’t really care about access to chips because of the front end (consumer-facing side) of applications like DeepSeek. Who cares? That is free competition.

My view also is the chatbots will never work that well anyway until there is an entirely new approach, which does not yet exist. Let them flush their money down the toilet too. That is good for us. Less money there, more money paid to a U.S. company. However, there are other real issues and reasons why the U.S. should not let these chips go there:

* What these LLMs do on the back end is a concern. Who knows, just like with TikTok, what they will ultimately do with the data, and what type of information they will serve. Something tells me, none of it will be in our interest.

* More importantly, there are other things that can be done with these chips, that have nothing to do with LLMs, but everything to do with machine learning/pattern recognition technologies that existed well prior to the LLMs. Watch this video. China is already well out ahead of us with regard to this stuff, especially the hardware technologies. They also control the supply chain for what is used to make these things. The dumb drones out there are already problems for advanced militaries. Russia is having a tough time with Ukrainian drones. A few have also snuck through into Israel, and also past the defenses of U.S. ships on patrol in the Middle East. We cannot just keep handing China the keys to steal our IP and then use our own technology against us in this capacity, and all sorts of other ways with regard to data analysis and data mining.

BY Doug Kass · Feb 3, 2025, 9:30 AM EST

Tom Lee never met a market he didn't like.

He is fantastic in bull markets....

BY Doug Kass · Feb 3, 2025, 9:23 AM EST

BY Doug Kass · Feb 3, 2025, 9:15 AM EST

At 9:00 a.m.:

BY Doug Kass · Feb 3, 2025, 9:07 AM EST

-HCWB +188% (receives clearance of Investigational New Drug Application from US FDA to initiate a first-in-human Phase 1 dose escalation clinical trial to evaluate one of its lead drug candidates, HCW9302, in patients with moderate-to-severe alopecia areata)

-TGI +34% (confirms to be acquired at $26.00/shr by affiliates of Warburg Pincus and Berkshire Partners in $3.0B all-cash transaction)

-IVVD +21% (reports Q4 prelim PEMGARDA revenue; announces Positive Phase 1/2 Clinical Data for VYD2311, a Monoclonal Antibody Designed to be a Superior Alternative to COVID-19 Vaccination for the Broad Population)

-MX +16% (Magnachip said to again pursue sale)

-RSLS +13% (granted Key International Patent in Israel for Its Proprietary Diabetes Neuromodulation Technology)

-SSYS +13% (announces $120M equity investment from Fortissimo Capital; earnings, guidance)

-IDXX +6.6% (earnings, guidance)

-MGRX +4.6% (executes Exclusive Distribution Agreement with Propre Energie for Clinically Proven Dermytol Skincare Treatment Targeting Hyperpigmentation)

-TSN +4.4% (earnings, guidance)

-SAIA +3.7% (earnings, guidance)

-TECX +2.0% (places 3.7M shares at $50M in $185M private placement to fund TX45, TX2100 and other working capital purposes)

-TNXP -46% (earnings; terminates Loan and Guaranty Agreement and announces 1-for-100 reverse stock split)

-NSSC -20% (earnings)

-OMI -8.7% (prelim earnings)

-UMAC -7.8% (enters into a Definive Agreement to acquire drone software company Aloft Technologies)

-GM -7.6% (US president Trump announces blanket tariffs on China, Mexico, Canada)

-MSTR -7.6% (did not buy any Bitcoin from Jan 27 to Feb 2nd)

-MTLS -6.1% (KBC Cuts MTLS to Accumulate from Buy, price target: $10)

-BRZE -5.2% (President and Chief Commercial Office Myles Kleeger will be stepping down, effective June 1st)

-DJT -4.7% (to adopt secure payment processing with vendor Moov)

-BWB -4.6% (files to sell $150M mixed securities shelf)

-STLA -4.6% (announces internal reorganization according to the changes communicated in Dec 2024)

-DOOO -4.4% (CitiGroup Cuts DOO.CA to Neutral from Buy, price target: C$70)

-F -4.2% (US president Trump announces blanket tariffs on China, Mexico, Canada)

-VSAT -4.0% (Unit Inmarsat Government (dba Viasat) received initial $3.5M Task Order award from U.S Space Force under the Proliferated Low Earth Orbit (PLEO) Satellite-Based Services (SBS)

-ARLP -3.6% (earnings, guidance)

-CSIQ -3.5% (downside momentum with new administration)

-CLF -3.3% (earnings, guidance)

-AA -2.7% (US president Trump announces blanket tariffs on China, Mexico, Canada)

-FSLR -2.7% (downside momentum with new administration)

-BABA -2.4% (US president Trump announces blanket tariffs on China, Mexico, Canada)

-FCX -2.1% (downside momentum with new administration)

BY Doug Kass · Feb 3, 2025, 9:04 AM EST

From Rosie:

BY Doug Kass · Feb 3, 2025, 8:45 AM EST

BY Doug Kass · Feb 3, 2025, 8:35 AM EST

From Barron's (attach attachment below):

BY Doug Kass · Feb 3, 2025, 8:22 AM EST

BY Doug Kass · Feb 3, 2025, 7:51 AM EST

Nobel Laureate Eugene Fama Predicts Bitcoin Will Become Worthless - ProMarket

From my recent commentary:

* An extremely leveraged cryptocurrency market represents potential systemic risks. It is my view that cryptocurrency is "the mother of all bubbles" perpetuated by a number of factors (including the rejection of fiat money) and developing digital narratives — many of which have a weak foundation of logic. The absurd notion that the limiting of supply of bitcoin is as stupid as it is damning — as there is no limit to the supply of other cryptocurrencies. To us, the sheer market size of Bitcoin and other cryptocurrencies is a manifestation of the risks. When the cryptocurrency markets implode, which is my baseline expectation, the contagion effect will likely be pronounced on all of the capital markets.

BY Doug Kass · Feb 3, 2025, 7:35 AM EST

BY Doug Kass · Feb 3, 2025, 7:10 AM EST

Bonus — Here are some great links:

BY Doug Kass · Feb 3, 2025, 6:50 AM EST

BY Doug Kass · Feb 3, 2025, 6:35 AM EST

Some of my long book: AMZN, DKNG, ELAN common and calls, PG, FRPT, VVV, PPLT, JOE and MSOS (AYRWF, TCNNF, VRNOF, CURLF, GLASF, CRLBR, GTBIF, TSNDF).

Some of my short book: AAPL, KO, PEP, BXMT, ROAD, AEG, SNBR, GS, MS, C, JPM, WGO, FIGS, CHGG, WOOF, ABR, MPW, FXLV, RILY and INTU.

BY Doug Kass · Feb 3, 2025, 6:25 AM EST

The S&P Short Range Oscillator slipped from 5.09% to 3.33% — so the market is less overbought.

BY Doug Kass · Feb 3, 2025, 6:15 AM EST

Given the magnitude of this morning's decline, let's revisit my four-part January 2025 market top columns:

A January 2025 Market Top? (Part One)

A January 2025 Market Top? (Part Deux)

BY Doug Kass · Feb 3, 2025, 6:05 AM EST

BY Doug Kass · Feb 3, 2025, 5:55 AM EST

Wolf Street howls about the last bout of Trump tariffs.

BY Doug Kass · Feb 3, 2025, 5:45 AM EST