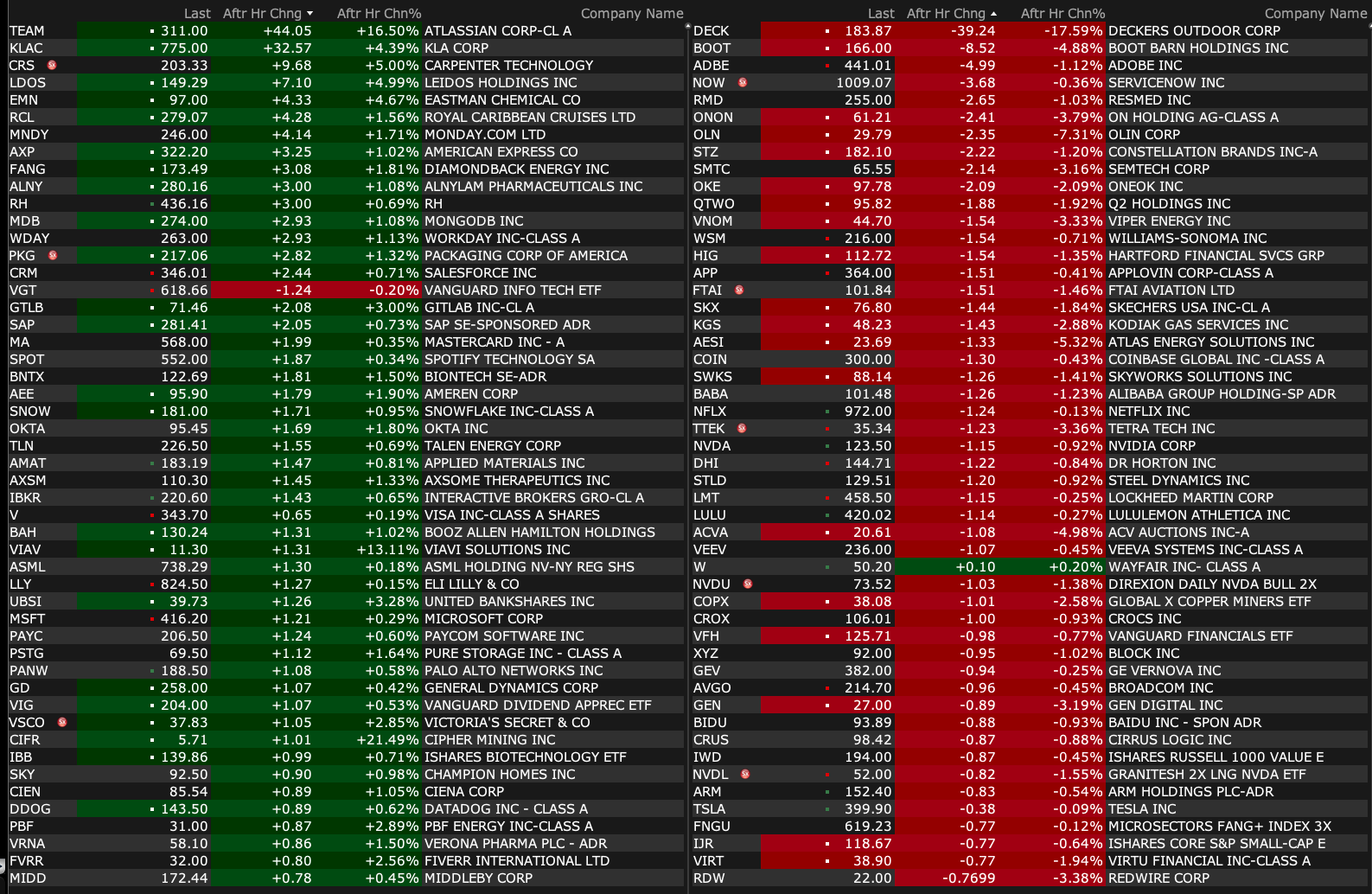

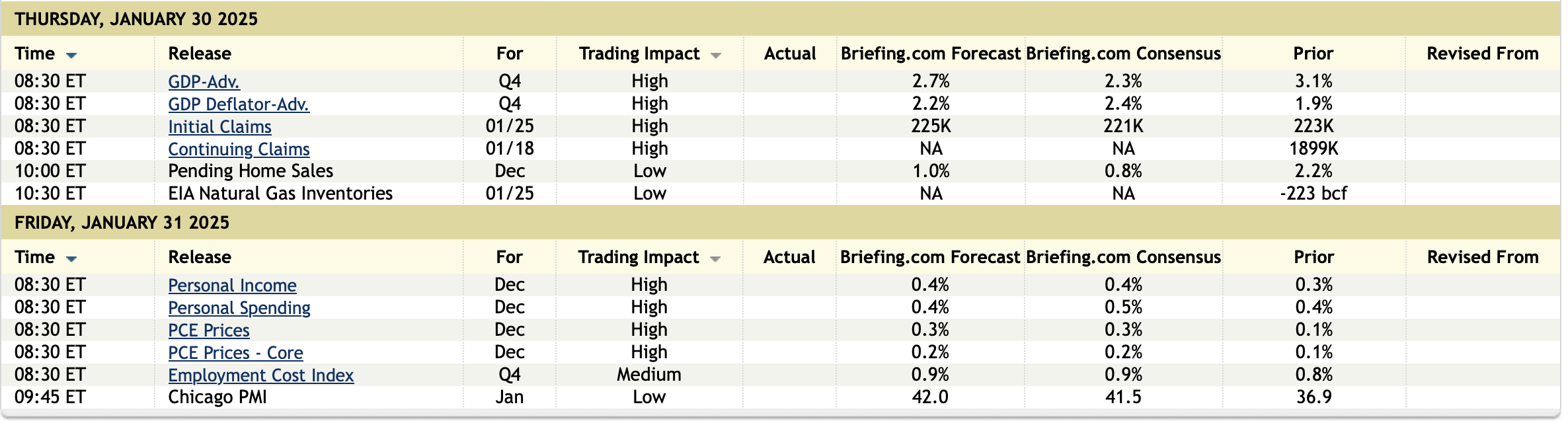

Thursday's After-Market Movers

At 4:36 p.m.:

BY Doug Kass · Jan 30, 2025, 5:10 PM EST

At 4:36 p.m.:

BY Doug Kass · Jan 30, 2025, 5:10 PM EST

BY Doug Kass · Jan 30, 2025, 4:55 PM EST

I have to leave early to an event a few minutes before the close.

I won't be writing tomorrow but you will be in the most capable hands of Sarge Guilfoyle.

Thanks for reading my Diary and enjoy the evening and the weekend.

BY Doug Kass · Jan 30, 2025, 3:04 PM EST

* Yesterday I brought back my daily "Things" column...

* Let's play two (Ernie Banks)! Ernie Banks 1977 Baseball Hall of Fame Induction Speech - YouTube

* 9 days, 10 hours, 23 minutes to Spring Training!!!

Once again, the market had more intraday moves than a shortstop batting .110 today!

It's a terrific market for opportunistic and disciplined traders — not so great for the buy-and-hold crowd.

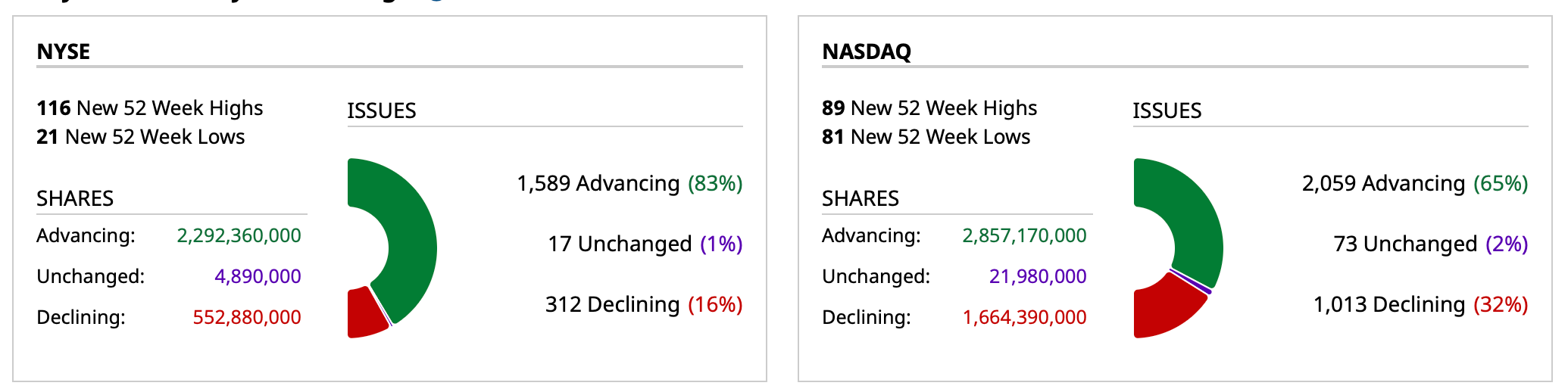

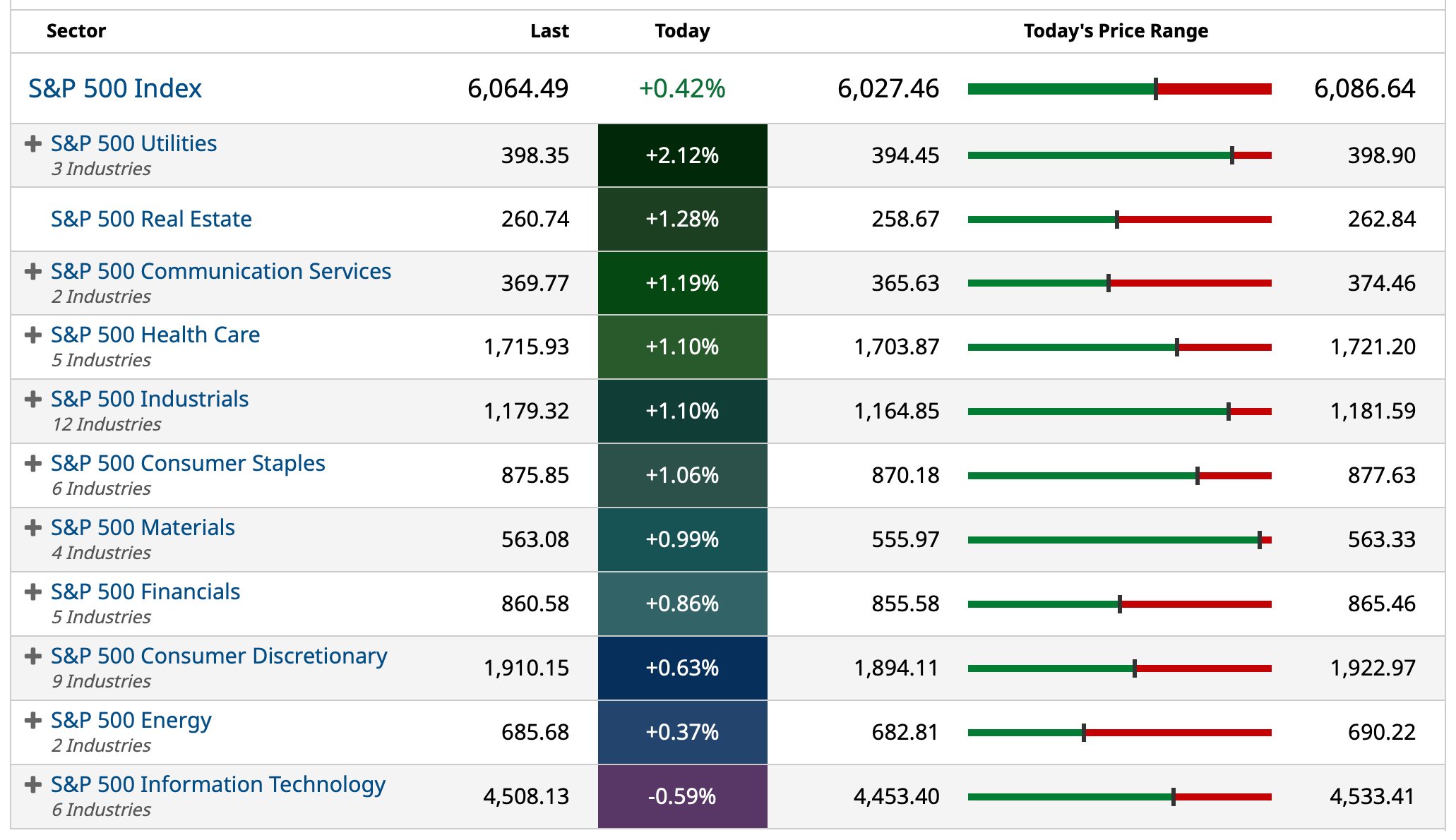

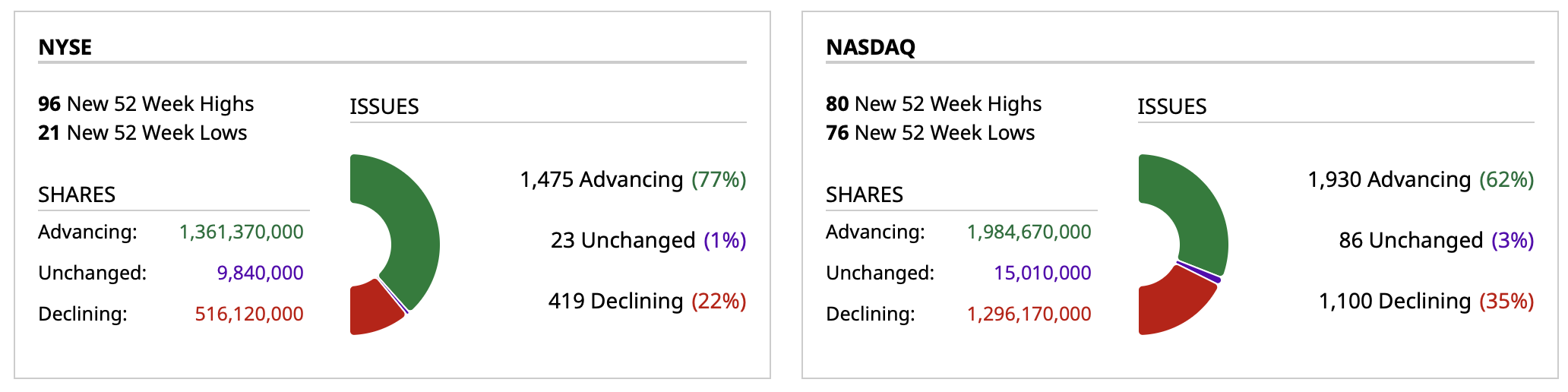

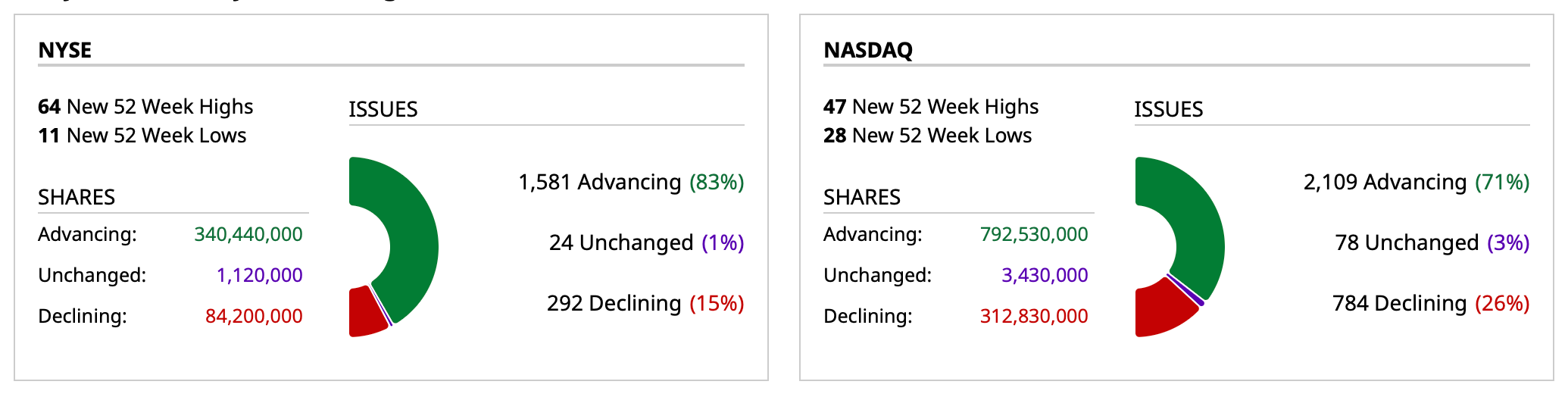

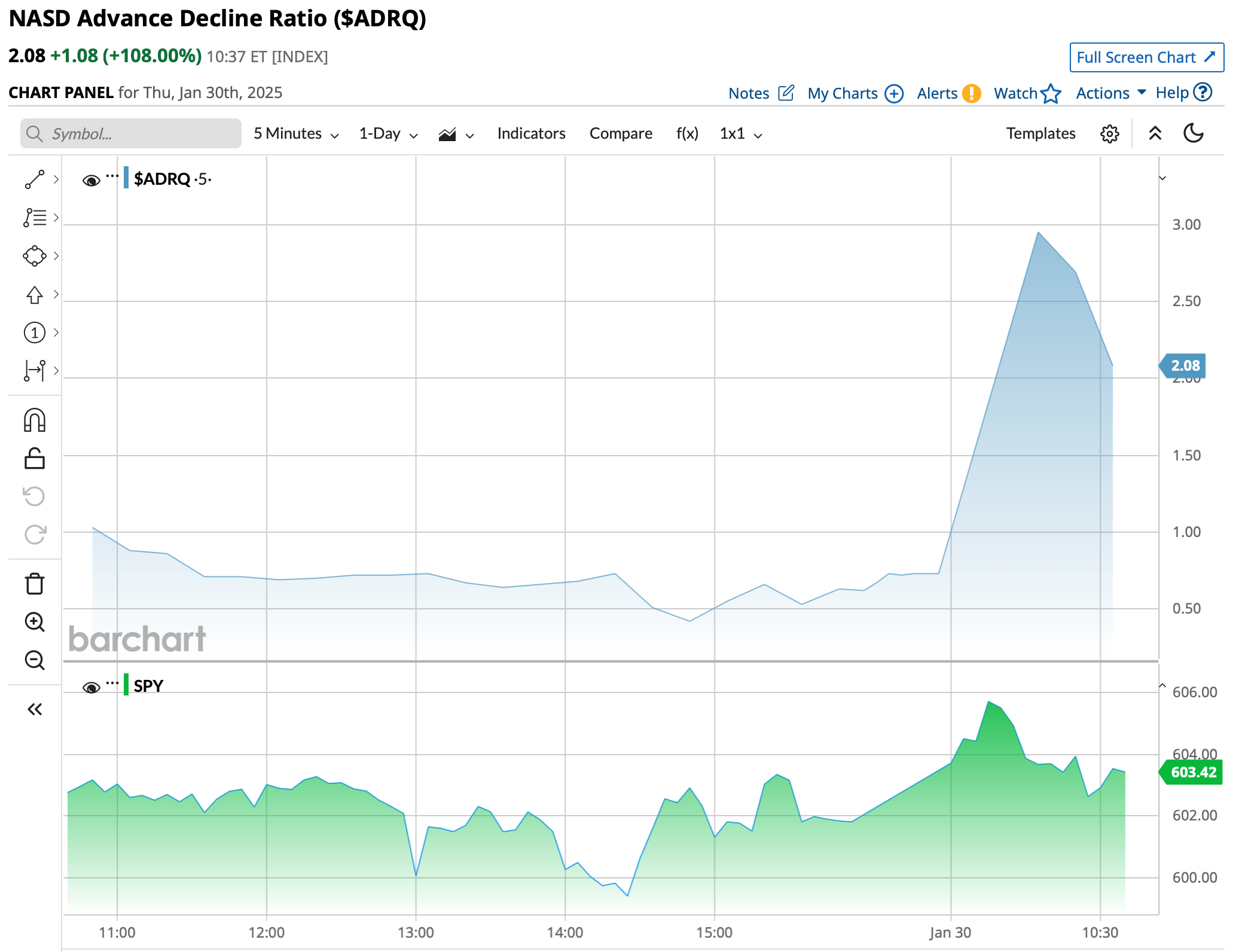

Breadth is very strong with 2.5 hours to go in the trading session:

At 1:40 p.m. S&P cash is up by about +30 handles and the equal weighted S&P Index (RSP) is 1.25%.

Here are today's "Things":

* This is a great trading market for opportunistic traders. Like yesterday, I made three individual swings (short and cover) in the Indices — all profitably. (I currently have no positions in the Indices.)

* I continue to add to cannabis longs.

* Shorted more SBUX at $109.15

It's been more of a research day than a trading day for me — with four separate research calls.

BY Doug Kass · Jan 30, 2025, 2:00 PM EST

I am still lugging my PPLT long — and not selling today's advance.

BY Doug Kass · Jan 30, 2025, 1:15 PM EST

BY Doug Kass · Jan 30, 2025, 12:39 PM EST

BY Doug Kass · Jan 30, 2025, 12:15 PM EST

BY Doug Kass · Jan 30, 2025, 11:50 AM EST

- NYSE volume 2% below its one-month average;

- Nasdaq volume 2.09 billion shares, 27% below its one-month average;

BY Doug Kass · Jan 30, 2025, 11:17 AM EST

From Peter Boockvar:

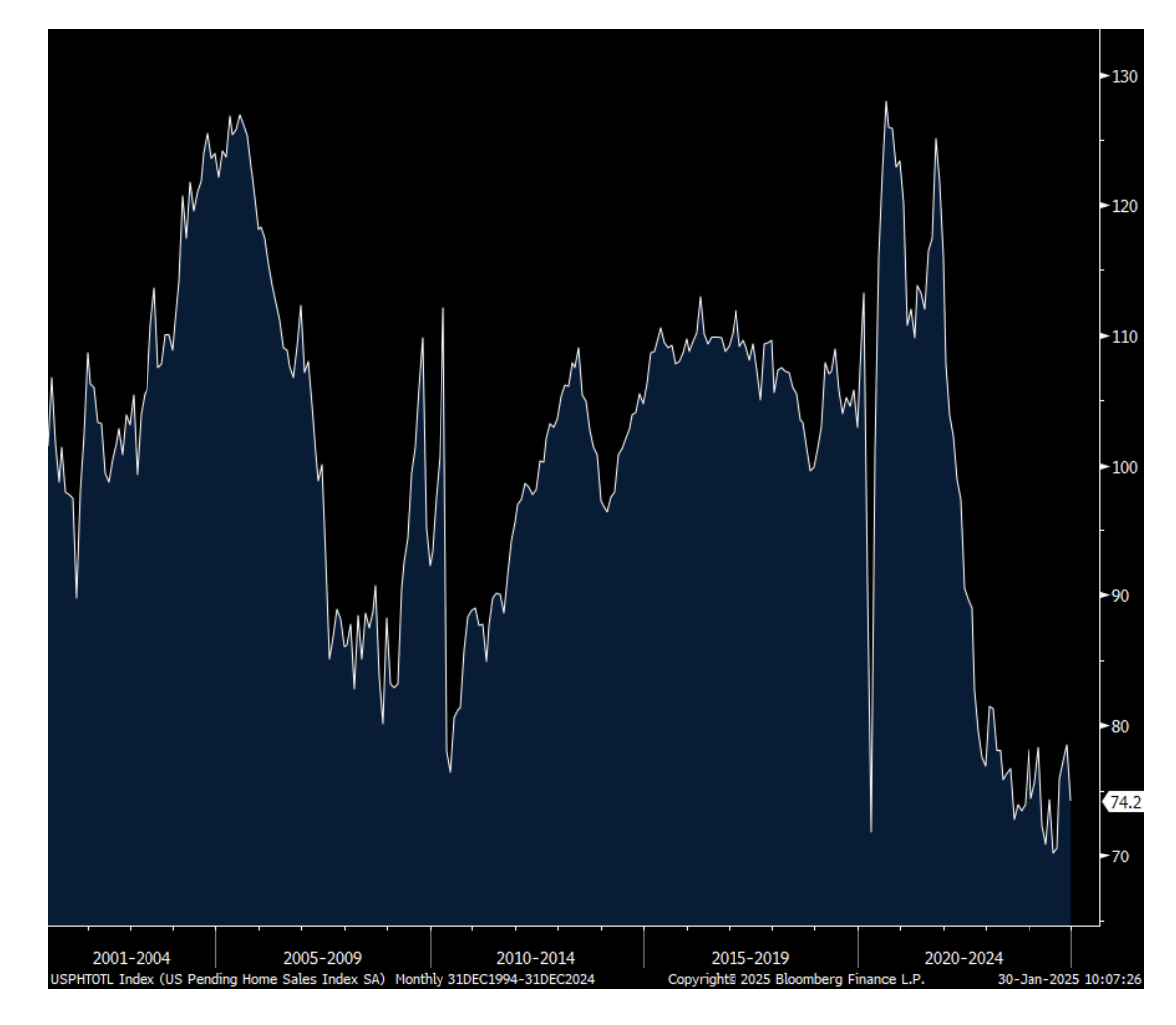

Pending home sales in December fell 5.5% m/o/m vs the estimate of on change and which followed a 1.6% rise in November. All four regions were lower, particularly in the Northeast and West. The NAR considers these two regions as having more higher priced homes and “where elevated mortgage rates have appreciably cut affordability.”

They also speculated whether “heavier than usual winter precipitation impacted the timing of purchases.” Maybe but winter is winter.

Bottom line, we know the upside down situation with the housing market with ever rising prices due to the lack of inventory that results in less sales but still higher prices, along with a 7% mortgage rate. The pace of transactions sits at 29 yr lows as seen with last week’s existing home figure for December.

Pending Home Sales Index

BY Doug Kass · Jan 30, 2025, 11:00 AM EST

From Peter Boockvar:

Q4 GDP grew 2.3% on a q/o/q annualized rate, below the estimate of 2.6% but again, always important to look under the hood. Nominal GDP was up 4.5% vs the estimate of 5.1% as a lower price deflator flattered the REAL figure. If the deflator was as expected, Real GDP would have printed 2%.

The consumer helped to drive the growth bus with a 4.2% gain driven by a 12.1% jump in durable goods spending with help from motor vehicles and recreation. Spending on services continues to be led by healthcare and leisure/hospitality. Consumption alone added 282 bps to the GDP figure. This was offset by a clip of 103 bps from gross private investment because of declines in equipment spending and non-residential structures (much of which is CRE). Spending on IP added 15 bps to GDP growth, and assume this is where AI spend is showing up in.

Inventories were a drag of almost 100 bps while government spending added 42 bps of economic growth with about half at the federal level and half from state/local governments. Trade was a push.

Bottom line, as stated here many times, the US economy is being held on the shoulders of upper income spending, AI CapEx and anything coming from Uncle Sam, whether directly via Medicare and Medicaid spend and transfer payments and via incentives seen in the IRA, Chips Act and infrastructure spend with the first two that shows up in ‘gross private investment.’

Initial jobless claims totaled 207k vs 223k in the week before but best to average the two because of the MLK holiday. The estimate was 225k. The 4 week average was 213k vs 214k in the week before. The pace of firing’s remains benign as measured here to say again. Continuing claims continue to be the issue with it totaling 1.858mm, though down from 1.90mm last week which was around the highest since November 2021.

From my morning note earlier, I will include this comment from Microsoft in yesterday’s call on their LinkedIn business, “In our talent solutions business, results were slightly below expectations driven by continued weakness in the hiring market in key verticals.”

No surprises with Christine Lagarde’s presser after they cut rates as fully expected. She’s not committing to cut again but the easing bias is still intact. European bonds are still up at the same level before the ECB news today and the euro is higher as are stocks. At a deposit rate of 2.75%, it now equals the December core CPI increase of 2.7% y/o/y. They consider this ‘restrictive’ according to Lagarde today. The headline rate is at 2.4%.

They say inflation is their sole mandate but growth right now is more of their focus that they somehow think can be solved via monetary policy.

BY Doug Kass · Jan 30, 2025, 10:30 AM EST

Dougie Kass

STAFF

Just Now

I scaled into more shorts (Index) on the rip.

On the dip I just covered my SPY $603.19 and QQQ $521.87 shorts - for a nice profit.

I plan to reshort strength.

BY Doug Kass · Jan 30, 2025, 10:15 AM EST

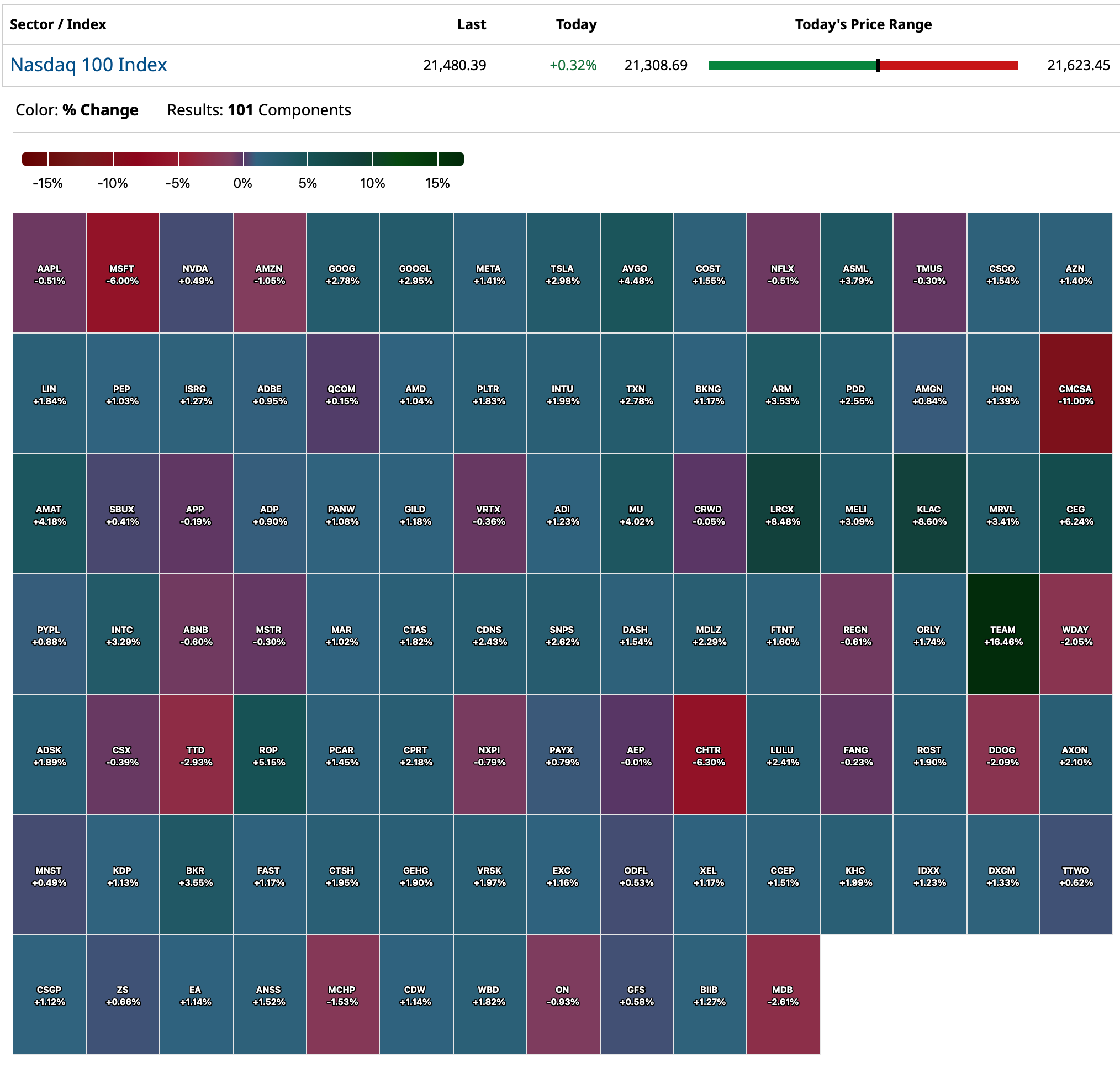

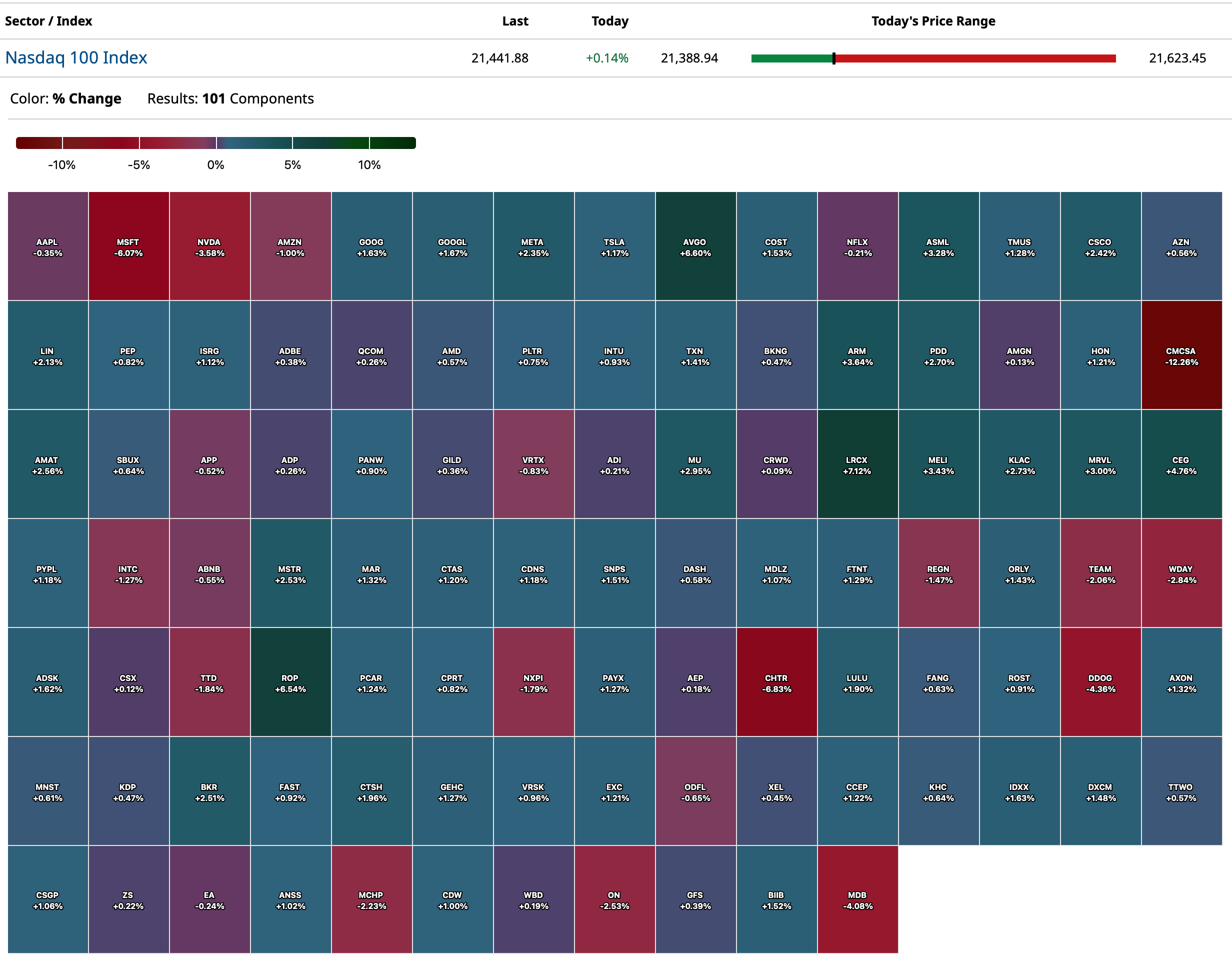

I am sure many saw the Alibaba BABA announcement yesterday morning: Alibaba Says It Has an Answer to DeepSeek: Superior AI.

Per my prior message on export controls, I strongly suspect Alibaba also has a treasure trove of Nvidia NVDA parts they are not supposed to have either. If the U.S. government is serious about this issue, they better get cracking:

Both Microsoft MSFT and Open AI are now whining about DeepSeek stealing their data. The same guys that apparently stole copyrighted material to train their models (and apparently broke their original contract to be a non-profit) are now complaining about DeepSeek doing a different version of the same thing? And if this is all so good for the sector, as Microsoft and Satya Nadella and numerous others are now trying to spin it, why then would they even care?

Microsoft and OpenAI are investigating if data output from OpenAI's technology was obtained in an unauthorized manner by a group linked to DeepSeek, Dina Bass and Shirin Ghaffary of Bloomberg reports. Microsoft's security researchers last year observed individuals they believe may be linked to DeepSeek exfiltrating a large amount of data using the OpenAI application programming interface, people told Bloomberg. Such activity could violate OpenAI's terms of service or indicate the group acted to remove OpenAI's restrictions on how much data can be obtained, the sources added.

These Investors Doubled Down When the AI Trade Faltered

Well that didn’t take long, and it should have been obvious this was coming. The new administration is now considering tighter curbs on Nvidia chip sales into China:

Trump administration officials are exploring additional curbs on the sale of Nvidia Corp. chips to China, according to people familiar with the matter….Commerce Secretary nominee Howard Lutnick, Trump’s pick to lead the agency that oversees chip trade curbs, said during a confirmation hearing Wednesday that he would be “very strong” on semiconductor controls, without providing more specifics.

* My guess, all the folks like Satya Nadella that are telling us how wonderful DeepSeek is going to be for the AI ecosystem, at the same time were all actually calling the White House and begging them to cut off all chip sales to China. Nadella, Altman, Google GOOGL, Facebook, Amazon AMZN, the whole lot of them. Calling and begging, shut it all down! If it is so good for their businesses, why do they want it all gone?

* Even though it was obvious this was going to happen, retail does not care, and they do not think about these things. These are the same folks that pile into things like GameStop GME, where there are zero in the way of fundamentals. They behave like religious zealots, but at some point, they are all in. Having said all of that, are institutional investors any better these days? They just chase price and a benchmark, which is also in part driven by retail, even for mega-cap stocks like the Magnificent 7. Then the algos, on top of all of this. Sadly, the algos don’t predict things like this obvious news that was going to happen, either. For all the technology, including the theoretical AI that the algos now have, they still can’t think, and cannot be predictive of things like this, which are obvious. What they can do, is react more quickly than anything else.

Microsoft just said they expect M365 and M365 copilot subscription growth to stall, which is normal due to the large installed base. They lumped in the small copilot base into the larger M365 base. Neat trick to try, I guess they think people are dumb (when really it is their AI that is dumb). Anyway, people don’t want it. Even the free version. Useless. If something is free, and people still do not want to use it because it does not provide value, there can be no elasticity to demand and no Jevons paradox, even if you can lower your costs of providing the service (useless) by 75%.

Here is an interesting article on hallucinations, and why they will never go away. Below that a link to a scientific paper saying similar:

“Because AI hallucinations are fundamental to how LLMs work, researchers say that eliminating them completely is impossible” Fundamentally, LLMs aren’t designed to pump out facts. Rather, they compose responses that are statistically likely, based on patterns in their training data and on subsequent fine-tuning by techniques such as feedback from human testers. Although the process of training an LLM to predict the likely next words in a phrase is well understood, their precise internal workings are still mysterious, experts admit. Likewise, it isn’t always clear how hallucinations happen.

As Large Language Models become more ubiquitous across domains, it becomes important to examine their inherent limitations critically. This work argues that hallucinations in language models are not just occasional errors but an inevitable feature of these systems. We demonstrate that hallucinations stem from the fundamental mathematical and logical structure of LLMs. It is, therefore, impossible to eliminate them through architectural improvements, dataset enhancements, or fact-checking mechanisms.

Meanwhile over at Facebook, ad impressions were only up 6% and continue to decelerate. But average price per ad is up +14% year over year and accelerating. Will be interesting how long the charging more for less works. Normally it does not. Which is probably part of why the revenue guidance was not good, and the expense guidance wasn’t good either. I also suspect they will start underspending their CAPEX projections again, which are likely just brinksmanship anyway.

Over at Tesla TSLA, automotive revenue was down -8% year over year (and total revenue badly missed estimates), 26% of their EPS came from unrealized gains on Bitcoin, and they also had $739 million in operating income from regulatory credits. And even with all of that, their operating income of $1.583 billion still badly missed estimates of $2.6 billion and was down -23% year over year.

I can see why folks are giddy about all things tech...

BY Doug Kass · Jan 30, 2025, 9:45 AM EST

From Peter Boockvar

So Jay Powell doesn't agree with Chris Waller who said a few weeks ago that we could see rate cuts "sooner than maybe the markets are pricing in." Powell said they are not in a hurry to cut again unless the unemployment rate jumps from here or inflation slows much further from here. That said, he still believes that policy is "meaningfully restrictive", and the fed funds rate is "meaningfully" above neutral even though he doesn't know what neutral even is. By saying this, he still seems to want to cut but doesn't see reason to do so anytime soon. Rate odds for a March cut is at 20% vs 32% yesterday morning.

On QT, Powell said that bank reserves are still "abundant" and thus implying that it will continue on but no time table was given on when and at what level they would stop.

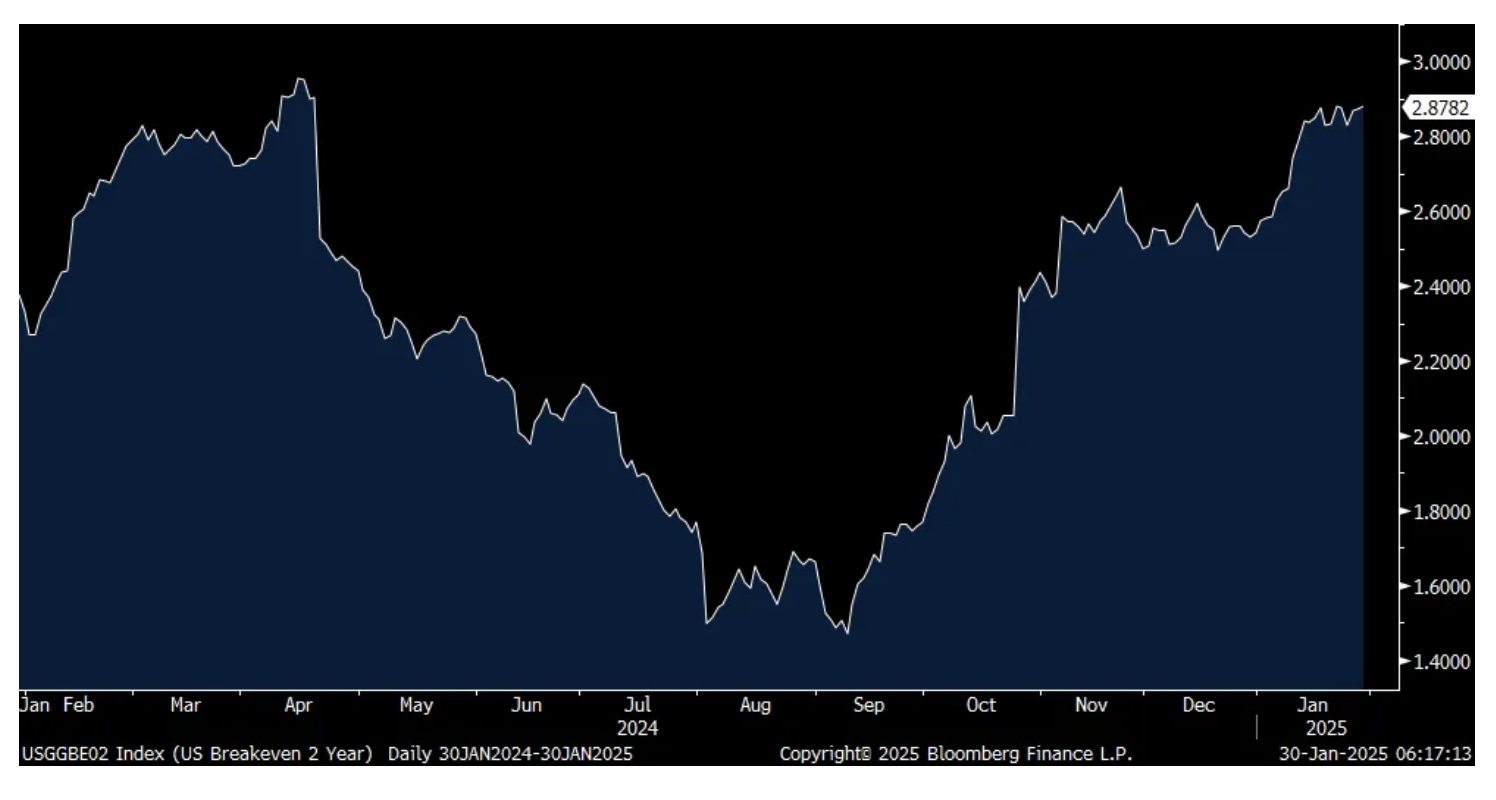

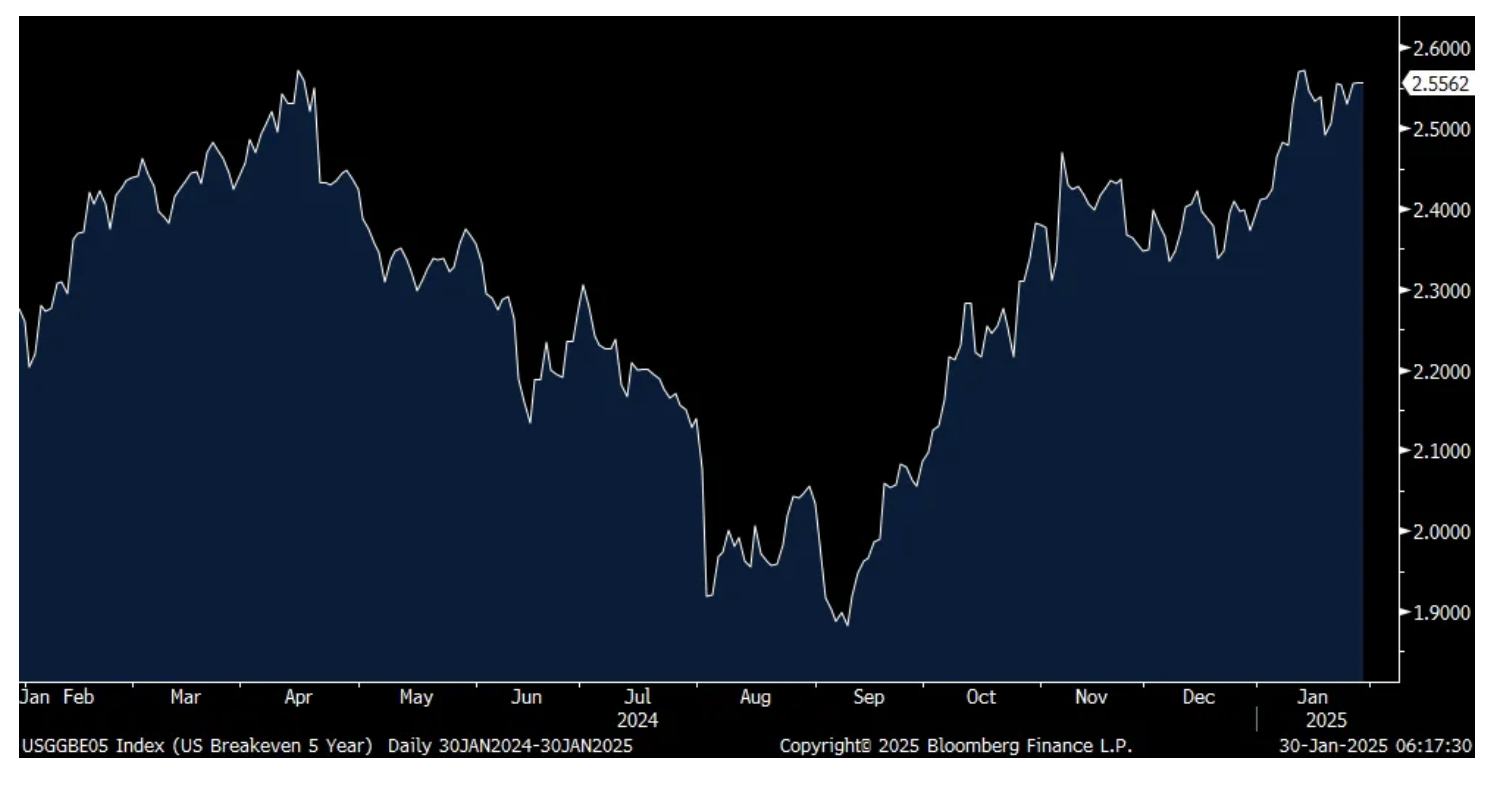

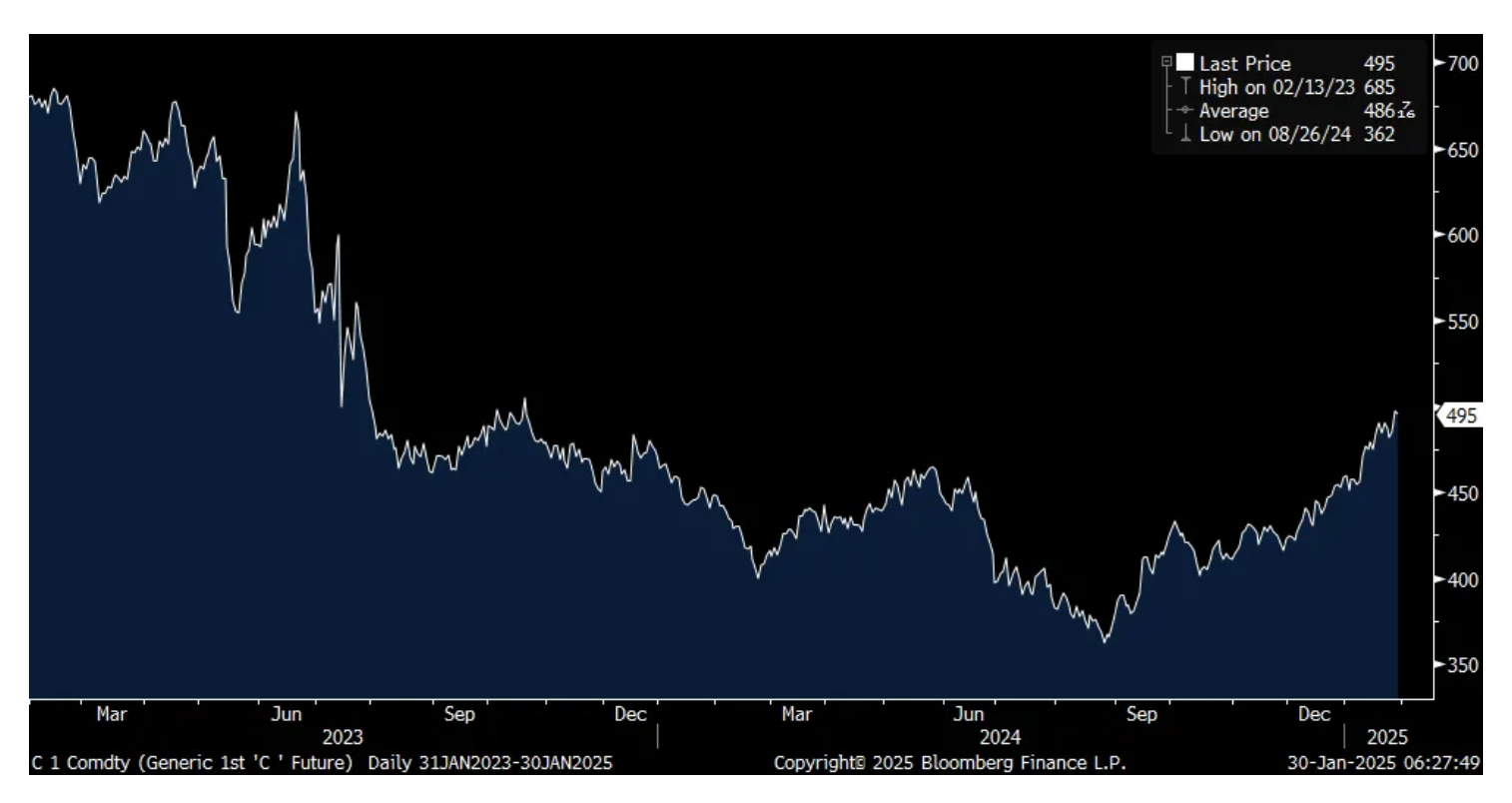

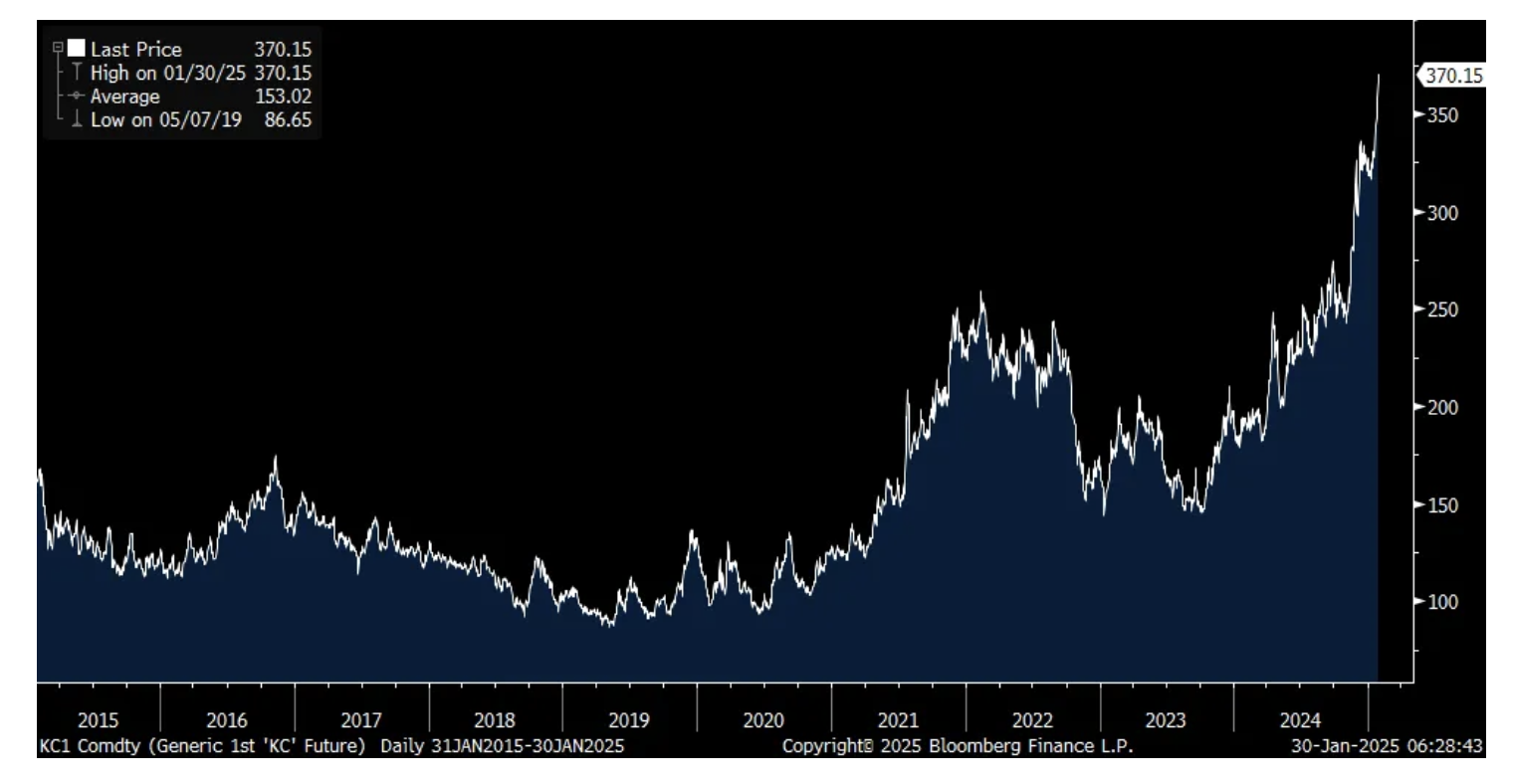

By the way, inflation breakevens out to 2 and 5 years closed yesterday at the highest level since April. Also, the price of gold is just a few dollars from a fresh all time record high. I've mentioned my bullishness on row crops like corn, soybeans and wheat and expressed through our long position in fertilizer stocks. Corn yesterday closed at the highest level since October 2023 at just under $5 per bushel. Coffee today is hitting a fresh record high.

2 yr Inflation Breakeven

5 yr Inflation Breakeven

Gold

Corn

Coffee

While the Bank of Canada cut rates again as expected to 3%, I think they left it somewhat uncertain as to their next move, in part due to the possibility of tariffs. In their statement they said "The economy is expected to strengthen gradually and inflation to stay close to target. However, if broad-based and significant tariffs were imposed, the resilience of Canada's economy would be tested." Governor Macklem did acknowledge though that yes, "A big increase in tariffs is a big disruption to the Canadian economy." But, "Monetary policy can't fix that."

On the flip side, the Brazilian central bank hiked its Selic rate by 100 bps to 13.25% as they deal with persistent weakness in the Real over spending concerns with the Lula government. It's now 275 of rate hikes since September and proving again that the Brazilian central bank doesn't mess around when it comes to inflationary/currency pressures. In response, the Brazilian Real closed at a 2 month high vs the US dollar.

Confirming the interest of the ECB to cut interest rates again today by 25 bps to 2.75%, the Eurozone economy saw no q/o/q growth in Q4 and the y/o/y increase was .9%. Versus Q3, both the German and French economies contracted. European bonds are rallying ahead of the meeting.

JGB yields are rising and the yen is weaker after Deputy Governor Ryozo Himino said the BoJ will raise rates again this year if things play out as they expect. "Looking ahead, it depends on the economy, prices and financial circumstances, but if our economic and price outlooks are realized, we'll hike rates accordingly." He acknowledged that money is still easy, "Given that real rates continue to be very much in the red, an easy monetary environment has been maintained."

On to the flood of earnings calls.

From Meta Platforms, Mark Zuckerberg was very optimistic:

"This is going to be a really big year. I know it always feels like every year is a big year, but more than usual, it feels like the trajectory for most of our long-term initiatives is going to be a lot clearer by the end of this year."

On its AI product, "I think this will very well be the year when Llama and open source become the most advanced and widely used AI models as well."

Around the world, "On a user geography basis, ad revenue growth was strongest in Rest of World at 27%, followed by Asia-Pacific and Europe at 23% and 22% respectively. North America grew 18%. In Q4, the total number of ad impressions served across services increased 6% and the average price per ad increased 14%."

They expect the strength in the US dollar to take 3% off their revenue growth based on current FX rates.

On CapEx, "We expect our full year 2025 capital expenses will be in the range of $60 billion to $65 billion. We expect CapEx growth in 2025 will be driven by increased investment to support both our generative AI efforts and our core business. The majority of our CapEx in 2025 will continue to be directed towards our core business."

Keep in mind, by capitalizing some of this huge spend, they are building in higher depreciation expenses and that was part of the reason they raised their overall expense guidance.

On the competition posed by DeepSeek and what that means for future CapEx spend, Mark said "I continue to think that investing very heavily in CapEx and infra is going to be a strategic advantage over time. It's possible that we'll learn otherwise at some point, but I just think it's way too early to call that. And at this point, I would bet that the ability to build out that kind of infrastructure is going to be a major advantage for both the quality of the service and being able to serve the scale that we want to."

From Microsoft:

"Enterprises are beginning to move from proof of concepts to enterprise wide deployments to unlock the full ROI of AI. And our AI business has now surpassed an annual revenue run rate of $13 billion, up 175% y/o/y."

"Azure is the infrastructure layer for AI. We continue to expand our data center capacity in line with both near term and long term demand signals. We have more than doubled our overall data center capacity in the last three years, and we have added more capacity last year than any other year in our history."

This was a macro comment on the labor market via their LinkedIn business. "In our talent solutions business, results were slightly below expectations driven by continued weakness in the hiring market in key verticals."

With CapEx, it totaled $22.6 billion which includes finance leases. "More than half of our cloud and AI related spend was on long lived assets that will support monetization over the next 15 years and beyond. The remaining cloud and AI spend was primarily for servers, both CPUs and GPUs."

Also worth listening to on the labor market is Robert Half, the staffing firm:

US Talent Solutions revenue fell 11% y/o/y and ex US was lower by 14% y/o/y.

That said, they remain bullish for this year. "As we move into the new year, we're very encouraged by the significant rise in US business confidence that followed the recent elections...Global labor markets remain resilient with US job openings significantly above historical averages. A clear indicator of substantial pent-up demand for talent. While we've seen a slight easing in the tightness of the labor supply, the overall unemployment rate in the US stands at only 4.1% with even lower rates for college students and those with in-demand accounting, finance and IT skills."

Notwithstanding the CEO's positivity, this is what is being seen right now. "And while the tone of client conversations are definitely better, clients are taking more of our calls, more of our requests for meeting, in addition to talking about their must have requirements, they're also talking about their backlog projects and talking about their like to have needs. The tone is clearly better, but it's still too early for an uptick in actual starts and placements."

Also, "As to the impact of AI, we've talked before. We're not seeing any meaningful impact as we speak on our business with SMBs (small and medium sized businesses) or otherwise."

From the always optimistic Elon Musk:

"And I've said this before, and I'll stand by it. I see a path, I'm not saying it's an easy path, but I see a path to Tesla being the most valuable company in the world by far. Not even close. Maybe several times more than... I mean there is a path where Tesla is worth more than the next top five companies combined. There's a path to that. I mean, I think it's like an incredibly, just like a difficult path, but it is an achievable path."

And how? "that is overwhelmingly due to autonomous vehicles and autonomous humanoid robots. So our focus is actually building towards that...very few people understand the value of full self-driving and our ability to monetize the fleet. Some of these things I've said for quite a long time and I know people have said, well, Elon is the boy who cried wolf like several times, but I'm telling you, there's a damn wolf at this time, and you can drive it. In fact, it can drive you. It's a self-driving wolf."

On tariffs, "There's a lot of uncertainty around tariffs. Over the years, we've tried to localize our supply chain in every market, but we are still very reliant on parts from across the world for all our businesses. Therefore, the imposition of tariffs, which is very likely, and any reciprocity will have an impact on our business and profitability."

From Group 1 Automotive, the car dealership:

Commenting on affordability, "I do know that our transaction prices held up and our grosses we were pleased with and our same store sales growth we were pleased with. So, our indication is the consumer is pretty healthy and we were pleased with those. So, I don't see anything that would lead me to believe it will get worse. I think, if anything, it could potentially get better if there's some stimulation on tax rates or something like that. Or interest rates for that matter."

From Ethan Allen the furniture company:

Sales fell 6% y/o/y as "the higher average retail ticket price and lower sales helped to offset lower backlogs, fewer contract sales and a lower delivered unit volume. Demand levels improved sequentially throughout the quarter and concluded with a strong December aided by our special promotion."

From Eagle Materials, the provider of many home related materials like wallboard:

"we've been in an environment where housing has been pretty tepid, pretty mediocre, and wallboard consumption reflects that. I think we finished calendar '24 around 27.3 billion square feet and that number has been consistent and so as you look forward, prior cycles, we've been well north of 30 billion square feet of consumption in the US. So we're still at pretty low levels of total consumption. We've just got the affordability issue, certainly interest rates are a part of that, but there's also good underlying demand."

Chili's continues to crush it for Brinker's International with items like the Big Smasher Burger:

"Chili's delivered another positive quarter in our turnaround and significantly outperformed the industry with same restaurant sales up 31% vs a year ago."

"Our strong performance is a direct result of staying focused on the fundamentals of food, services and atmosphere. Our investor growth strategy, combined with our industry leading value proposition continues to drive sustained growth in our business."

It's Maggiano's unit saw a 6.4% rise in price offset by negative 4.9% traffic.

They saw wage inflation of 3.5% and 1.5% commodity inflation.

From CH Robinson, the trucking broker:

"From a volume standpoint, the market continues to be in a prolonged freight recession...And Q4 continued to be a very competitive marketplace where demand is just not where the market needs it to be."

BY Doug Kass · Jan 30, 2025, 9:39 AM EST

BY Doug Kass · Jan 30, 2025, 9:27 AM EST

-ATHE +78% (ATH434-201 randomized, double-blind, placebo-controlled Phase 2 clinical trial in patients with early-stage multiple system atrophy (MSA) achieved Statistical Significance with up to 48% Slowing of Clinical Progression on UMSARS Rating Scale)

-KZIA +36% (announces the launch of a groundbreaking trial with paxalisib in combination with immunotherapy in women with advanced breast cancer)

-PCSA +13% (prices equity at-the-market offering at $0.615 for institutional investors and $0.7975 for the CEO and certain board members)

-CLS +12% (earnings, guidance)

-CALX +8.5% (earnings, guidance)

-IBM +8.5% (earnings, guidance)

-OSK +8.2% (earnings, guidance)

-LVS +6.6% (earnings)

-LRCX +6.1% (earnings, guidance)

-NTCT +5.8% (earnings, guidance)

-PHM +3.3% (earnings, guidance; raises share buyback program)

-TSLA +2.9% (earnings, guidance)

-MBUU +2.7% (earnings, guidance)

-DOV +2.5% (earnings, guidance)

-HONE +2.2% (earnings)

-ZENA +2.2% (Unit Spider Vision Sensors Collaborates with Suntek Global to Apply for First Blue UAS Certification of IQ Nano Drone Sensor for US Defense)

-CRGX -74% (to discontinue FIRCE-1 Phase 2 Study of Firi-cel)

-IKT -18% (Pauses Further Development of Risvodetinib)

-FLWS -15% (earnings, guidance)

-UPS -14% (earnings, guidance)

-WHR -11% (earnings, guidance)

-BFLY -10% (prices 24M shares at $3.15/share)

-IMNM -10% (prices 19.4M shares at $7.75/share)

-CI -9.9% (earnings, guidance)

-NOW -9.6% (earnings, guidance)

-DT -8.9% (earnings, guidance)

-MXL -8.5% (earnings, guidance)

-BFH -7.3% (earnings, guidance)

-IRWD -7.0% (initiates Apraglutide NDA Submission; issues FY25 guidance)

-LEVI -6.5% (earnings, guidance)

-RHI -4.8% (earnings, guidance)

-MSFT -4.1% (earnings, guidance)

-SIGI -4.0% (earnings, guidance)

-CAT -3.9% (earnings, guidance)

-SILC -3.9% (earnings, guidance)

-CMCSA -3.0% (earnings; raises buyback program, dividend)

-CLB -2.9% (earnings, guidance)

-DGX -2.9% (earnings, guidance; raises dividend)

-DOW -2.8% (earnings, guidance)

-FIBK -2.6% (earnings)

-SHW -2.6% (earnings, guidance)

-SXC -2.1% (earnings, guidance)

BY Doug Kass · Jan 30, 2025, 9:17 AM EST

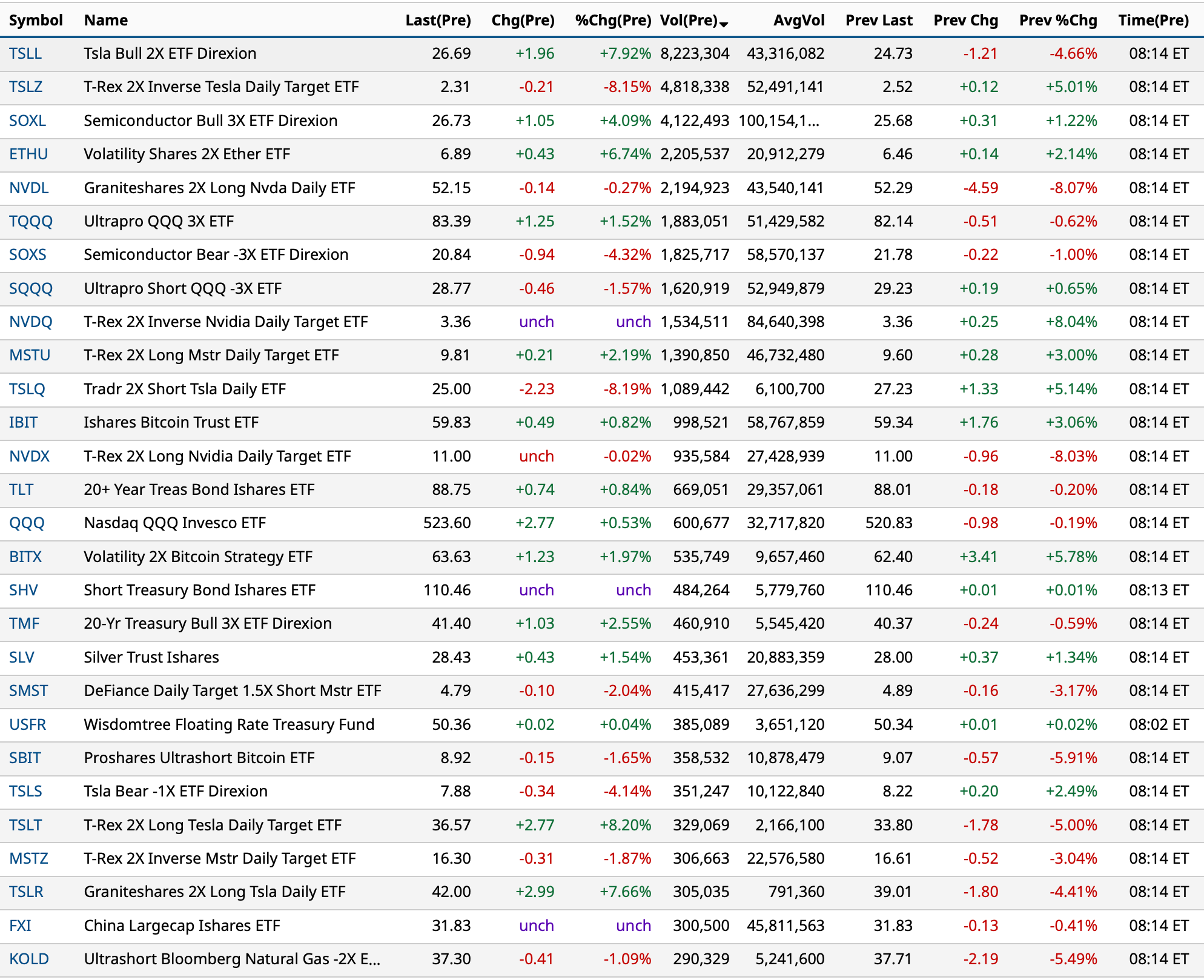

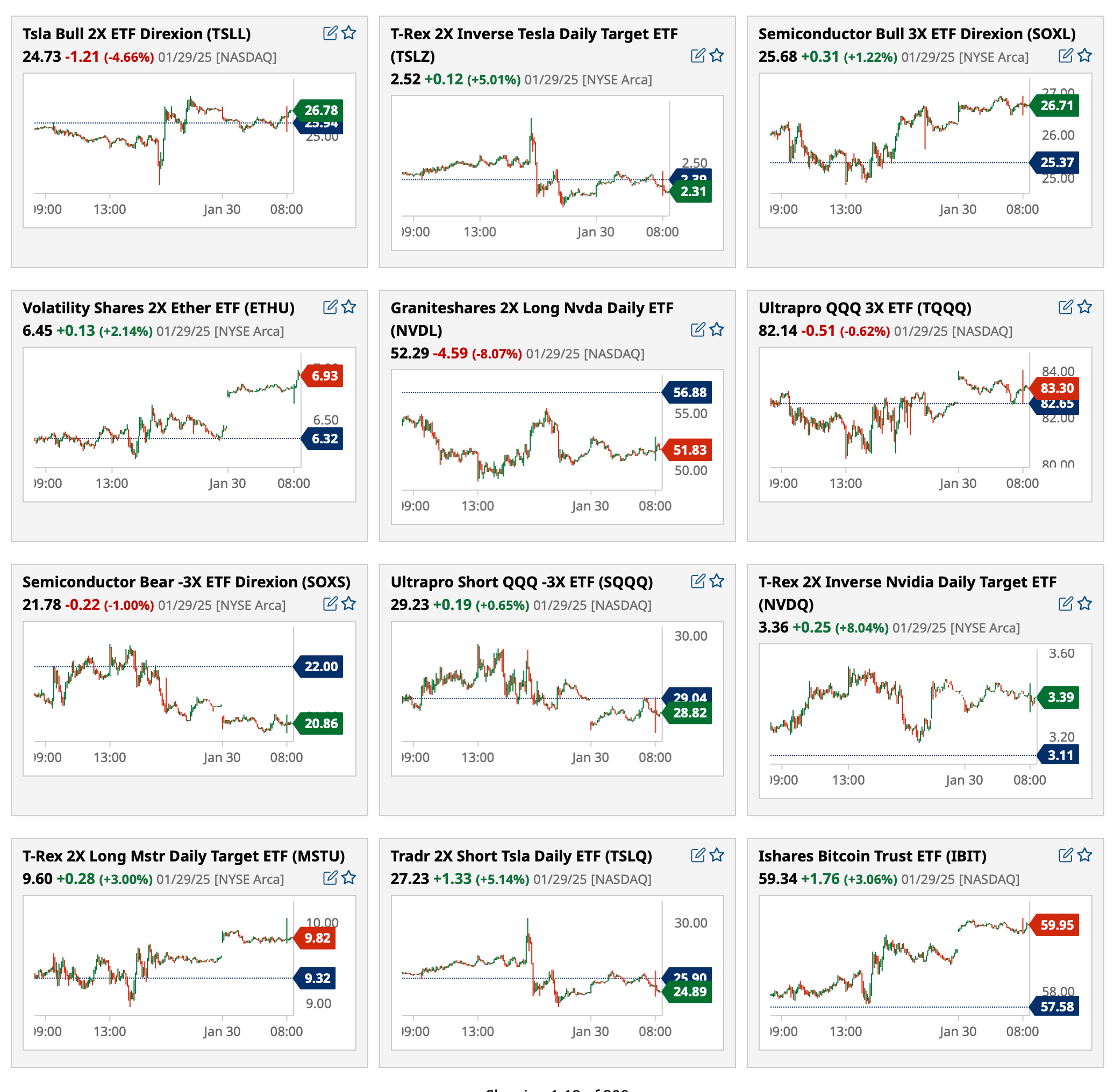

Most active premarket ETFs as of 8:14 a.m.:

BY Doug Kass · Jan 30, 2025, 9:08 AM EST

From the legendary Guap:

BY Doug Kass · Jan 30, 2025, 8:55 AM EST

Premarket percentage movers, lead by UPS UPS, Whirlpool WHR, Cigna CI downside; IBM IBM upside:

BY Doug Kass · Jan 30, 2025, 8:45 AM EST

On the rally off of the economic data I added to my QQQ short at $524.01

BY Doug Kass · Jan 30, 2025, 8:38 AM EST

BY Doug Kass · Jan 30, 2025, 8:29 AM EST

BY Doug Kass · Jan 30, 2025, 7:30 AM EST

BY Doug Kass · Jan 30, 2025, 7:20 AM EST

BY Doug Kass · Jan 30, 2025, 7:10 AM EST

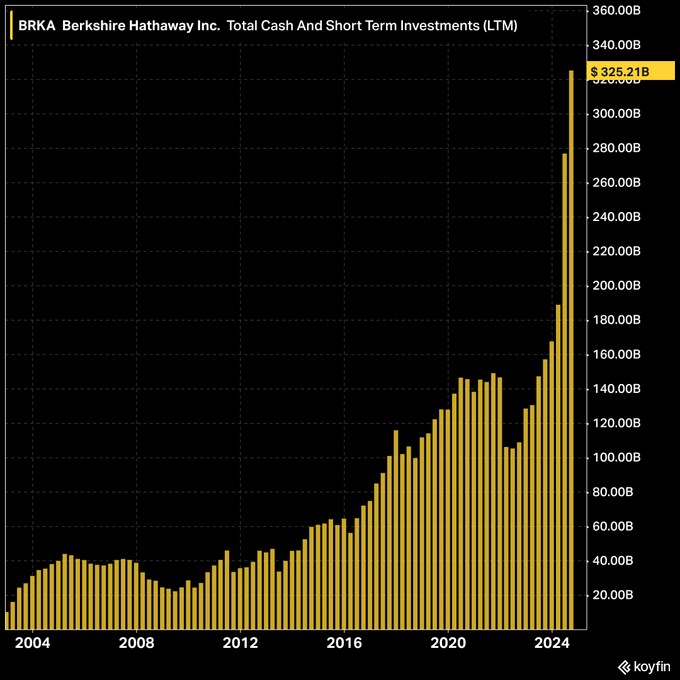

Berkshire Hathaway's BRK.A BRK.B cash hoard has now grown to over $325 billion.

Look at the (vertical ascent of the) chart below... if you thought it was a stock chart (and didn't know it represented Warren Buffett's cash position at Berkshire Hathaway) you would be concerned, thinking it was screaming "bubble."

In actuality it is a view of "lack of value" ascribed to one of the greatest investors of all time:

BY Doug Kass · Jan 30, 2025, 7:00 AM EST

Bonus — Here are some great links:

BY Doug Kass · Jan 30, 2025, 6:45 AM EST

BY Doug Kass · Jan 30, 2025, 6:35 AM EST

Doomberg reframing energy prices from the perspective of hard currency.

BY Doug Kass · Jan 30, 2025, 6:25 AM EST

From my friends at Miller Tabak:

Wednesday, January 29, 2025

Expect the Fed to Pause Until June

Expect the Fed to Pause Until JuneThe January FOMC meeting was slightly hawkish. Although Chairman Powell described it as simply “cleaning up” the FOMC statement, the removal of language about inflation making progress towards 2% and the labor market easing signals the start of a short pause. This was as expected. The Fed wants to wait out the current elevated policy uncertainty, and the labor market is still strong enough so that the Fed believes that it can move slowly. This is a mistake that will help cause GDP growth to slow to 1% by 4Q2025. Nevertheless, we still expect the Fed’s next move to be in June when it resumes one 25 bps rate cut each quarter. This will result in a year end Federal Funds rate of 350-375 bps.

Looking at the bigger picture, the Fed remains on course to cut rates to around 3% by late 2026. Cuts will resume if either inflation, looking past any temporary impacts from tariffs, starts to again fall or the labor market weakens. Both are likely. Powell correctly noted that shelter explains most of the gap between current inflation and its 2% target, and the most recent data (more on this later) continue to suggest that shelter inflation is about to drop. We also reiterate that as the elevated January -March 2024 reading fall out, core-PCE inflation will soon fall below the 2.6-2.8% y/y band where it has sat since May.

The bigger reason why we expect the Fed to resume cutting is that it is still too optimistic about the likely path of the labor market. The Fed’s last forecast put December 2025 unemployment rate at just 4.3%. This is inconsistent with the Fed’s policy plans and we instead expect unemployment to start rising in 2Q2025, reaching 4.5% by December. Powell was correct to note that a low hiring rate (and lower vacancies) make the labor market more sensitive to reduced demand than at any time since 2022. He underestimated, however, the threats to demand. Weakening household balance sheets, potential tariffs, and continuing high interest rates will be more damaging than the FOMC expects.

BY Doug Kass · Jan 30, 2025, 6:15 AM EST

Wolf Street howls about sticky inflation and Fed policy (on hold).

BY Doug Kass · Jan 30, 2025, 6:05 AM EST

* But slightly less so...

There was some slippage in the overbought signal, but we are still overbought.

The S&P Short Range Oscillator slipped from 7.29% to 5.43% overnight.

BY Doug Kass · Jan 30, 2025, 5:55 AM EST

I reestablished Index shorts on the META gap (which I shorted):

* SPY $604.02

* QQQ $523.93

BY Doug Kass · Jan 30, 2025, 5:45 AM EST