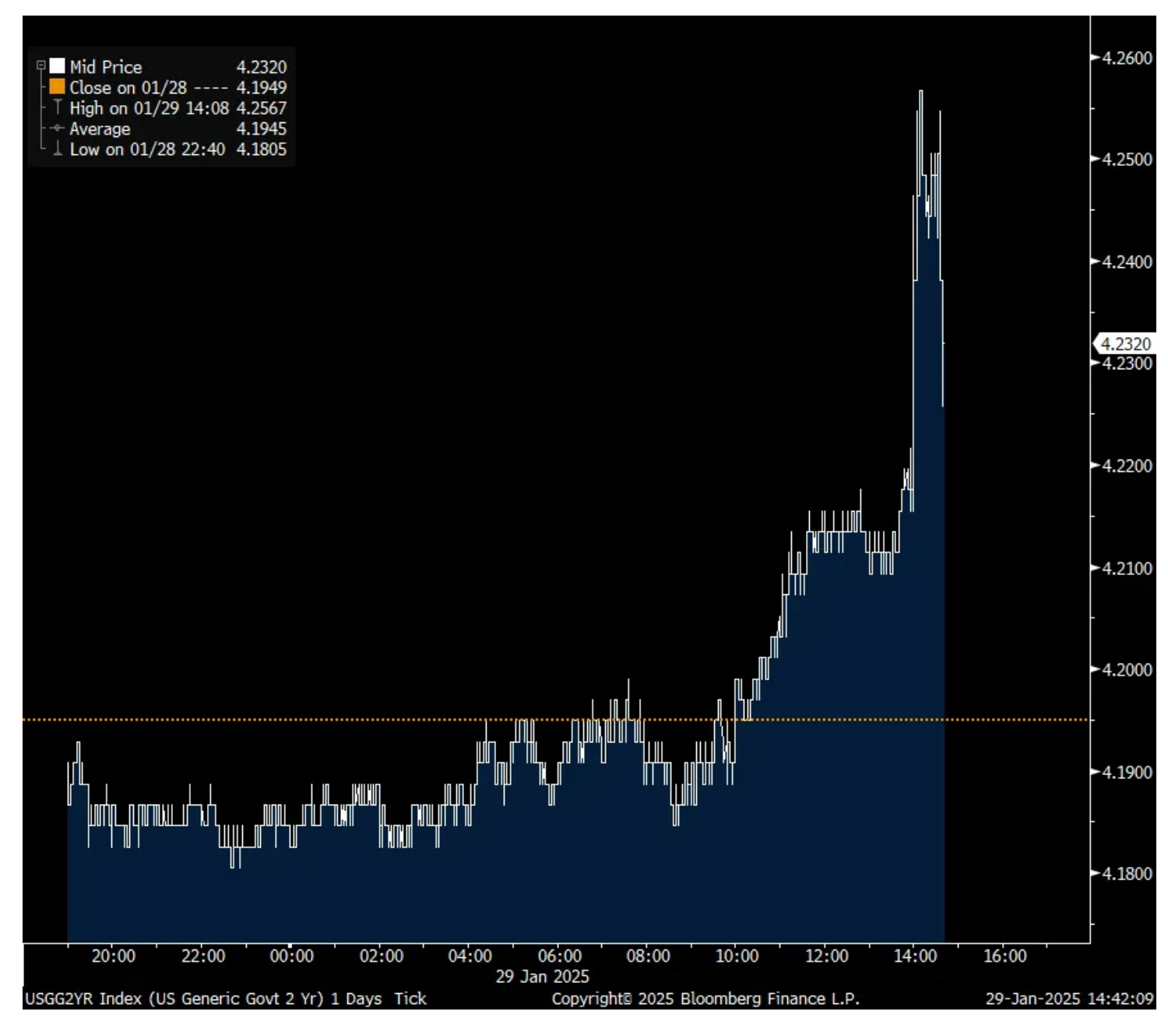

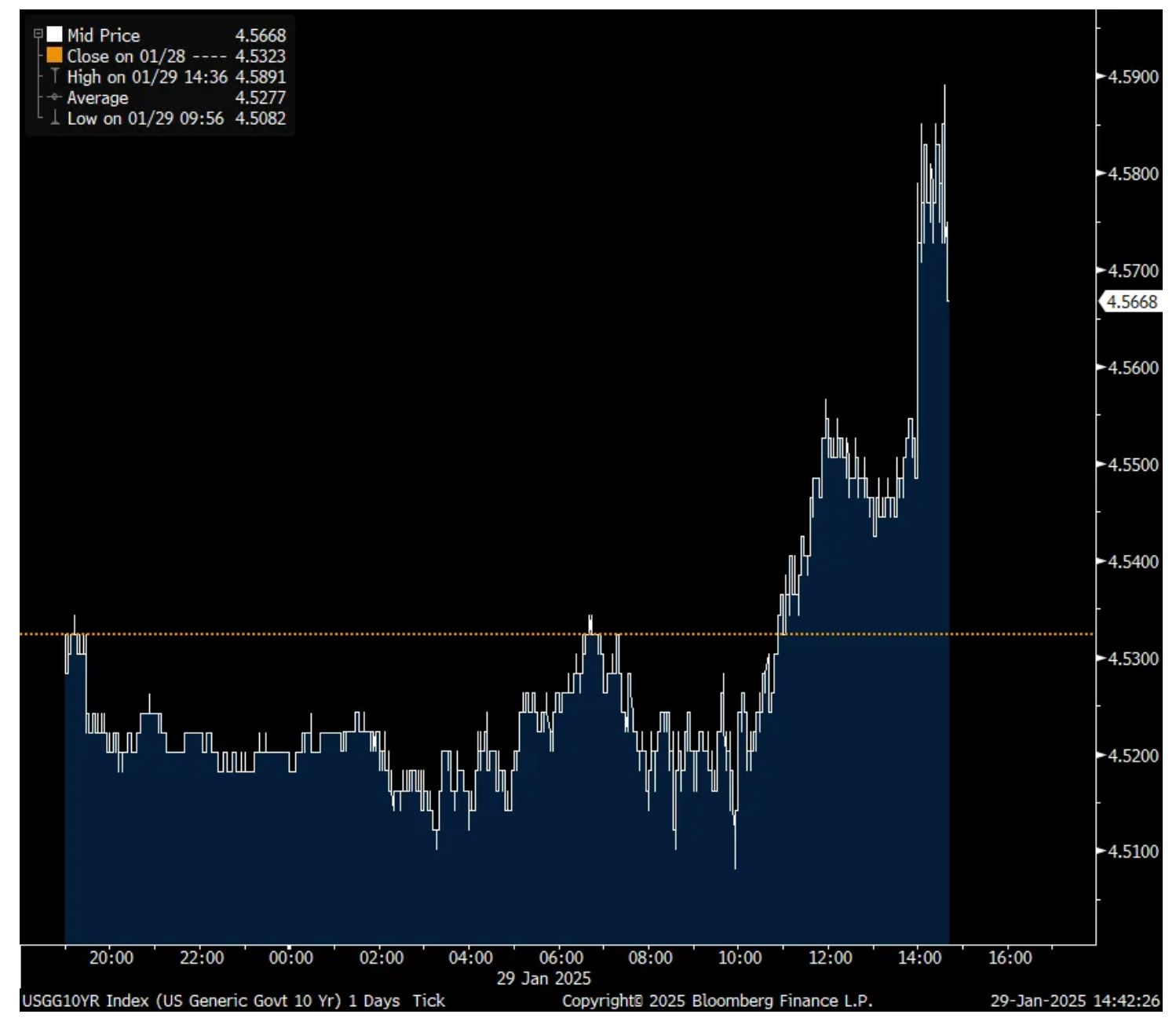

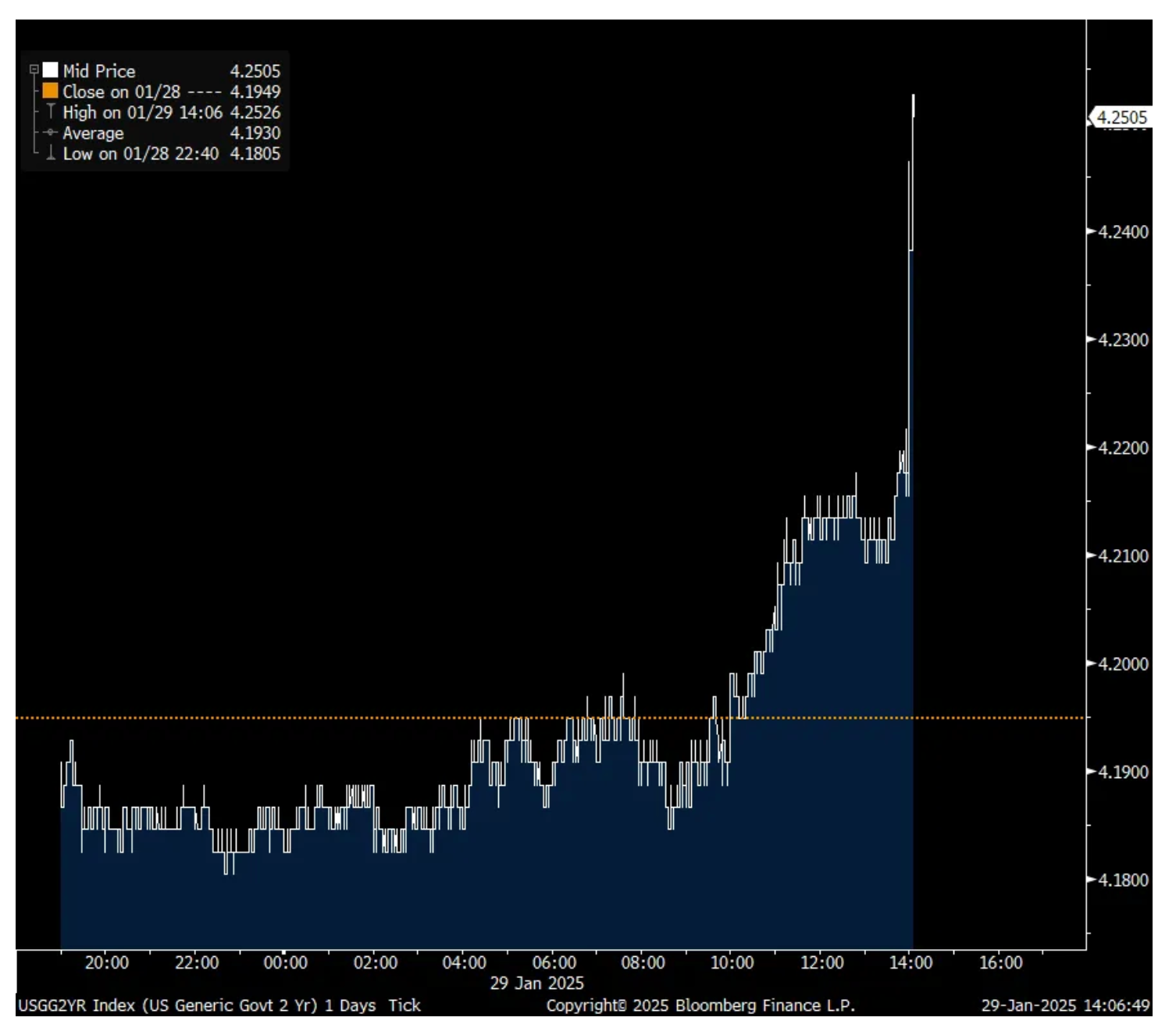

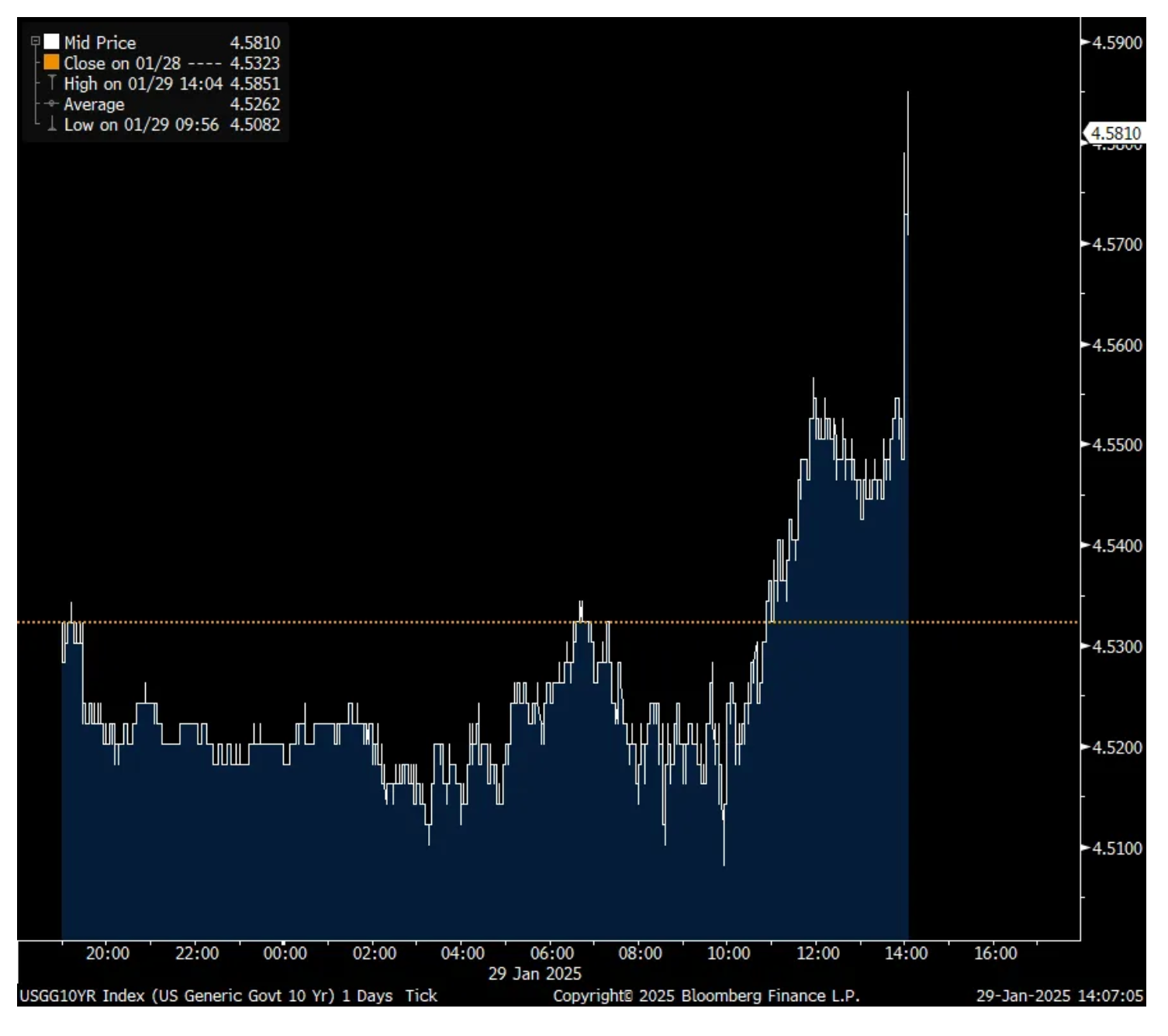

Jay Powell in his presser said the tweaks in comments on the labor market and inflation in the FOMC statement should not be interpreted as a signal. Here is an updated intraday chart in the 2 yr and 10 yr.

There were two changes in the FOMC statement relative to the one given in December of note. On the labor market they said “The unemployment rate has stabilized at a low level in recent months, and labor market conditions remain solid.” This compares to the previous statement that said “Since earlier in the year, labor market conditions have generally eased, and the unemployment rate has moved up but remains low.”

Today’s line would be a bit more hawkish way of describing things I’d say.

On inflation, all they said was “Inflation remains somewhat elevated.” They cut out half the sentence which included this line seen in December when they said “Inflation has made progress toward the Committee’s 2% objective but remains somewhat elevated.”

So, does that imply they think they’ve stopped making progress? A bit more hawkish here too.

In response, the 2 yr yield is at the highs of the day as is the 10 yr yield. As said this morning, does Jay Powell in his presser agree with what Chris Waller said a few weeks ago or does he push back. As seen just with this statement, it was a slight pushback I believe.

Either way, no cut was of course expected today and now they can sit back and absorb all the economic data and hopefully get more details of what Trumponomics will look like in terms of tax and tariff policy, among other things as the next meeting is not until March 18/19. That said, the longer end of the bond market has stolen the show since the Fed first cut rates in September and has really neutered the relevance, I believe, of Fed policy.

Before this meeting, the market was pricing in a 32% chance of a March cut. It stands as of this writing at just 12%. The first rate cut this year is now looking more like July than June as seen in the pricing in the fed funds market.

The market had more intraday moves than a shortstop batting .110 today!

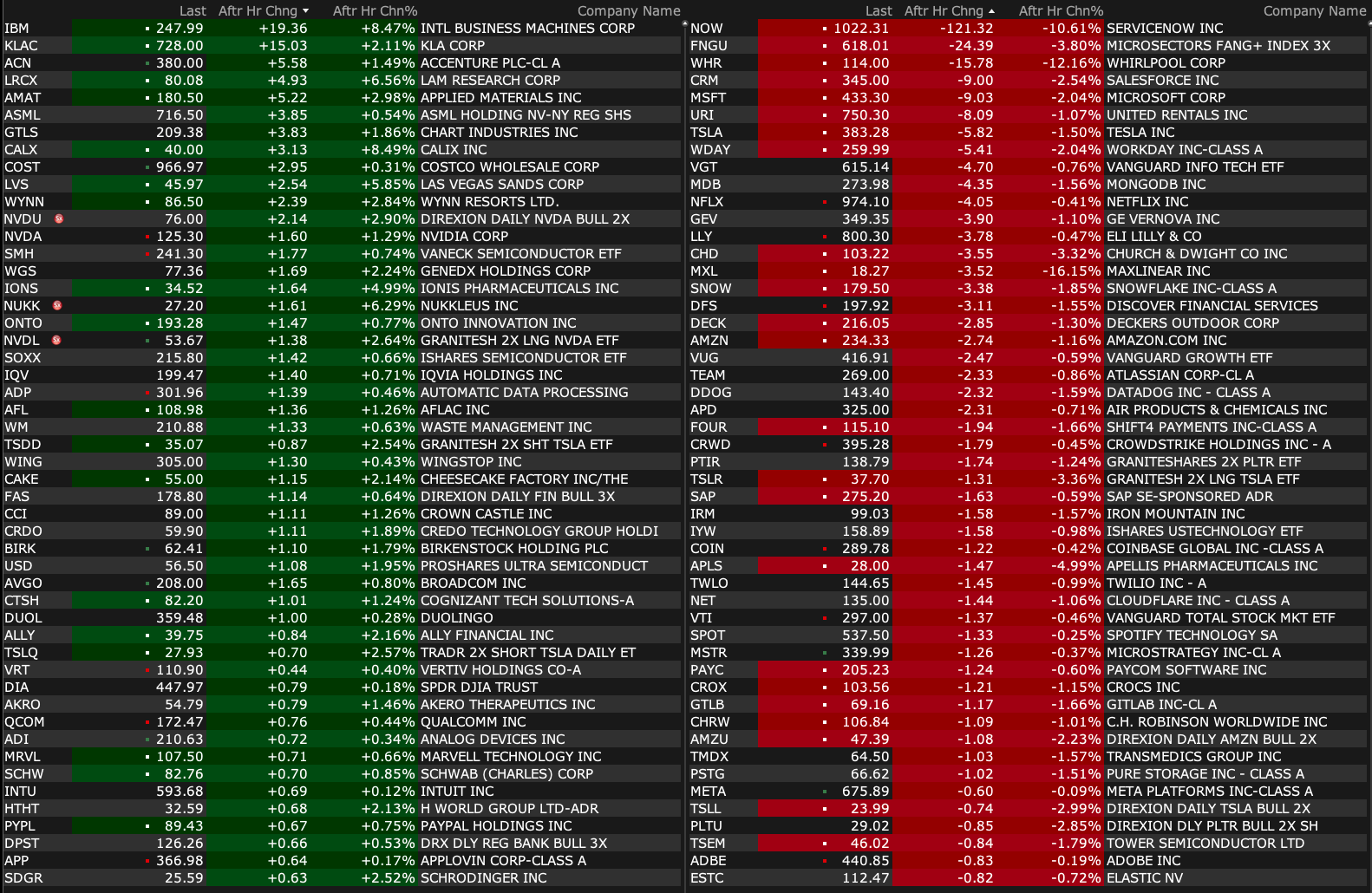

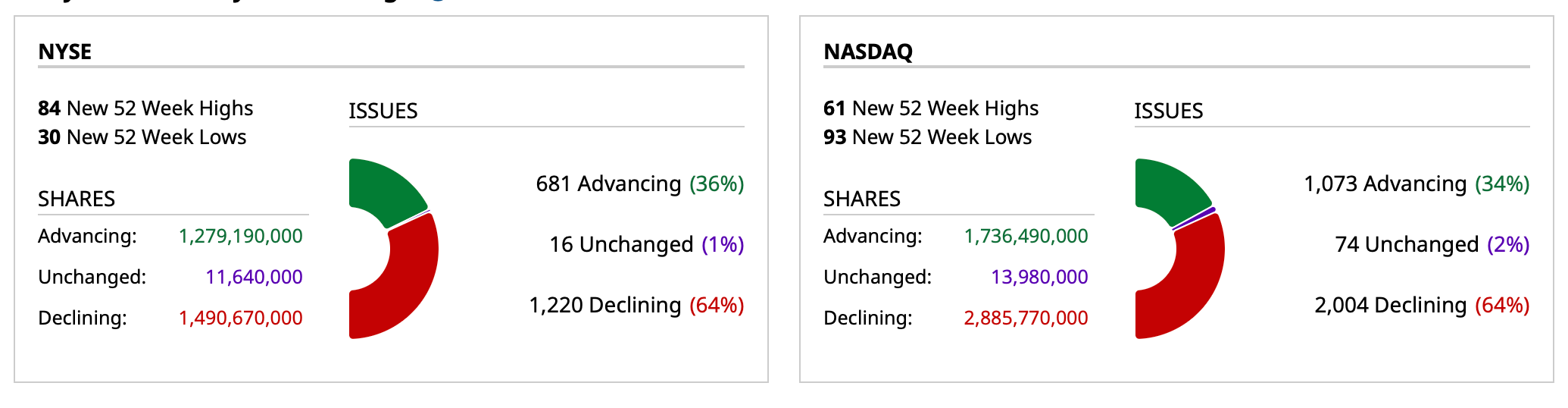

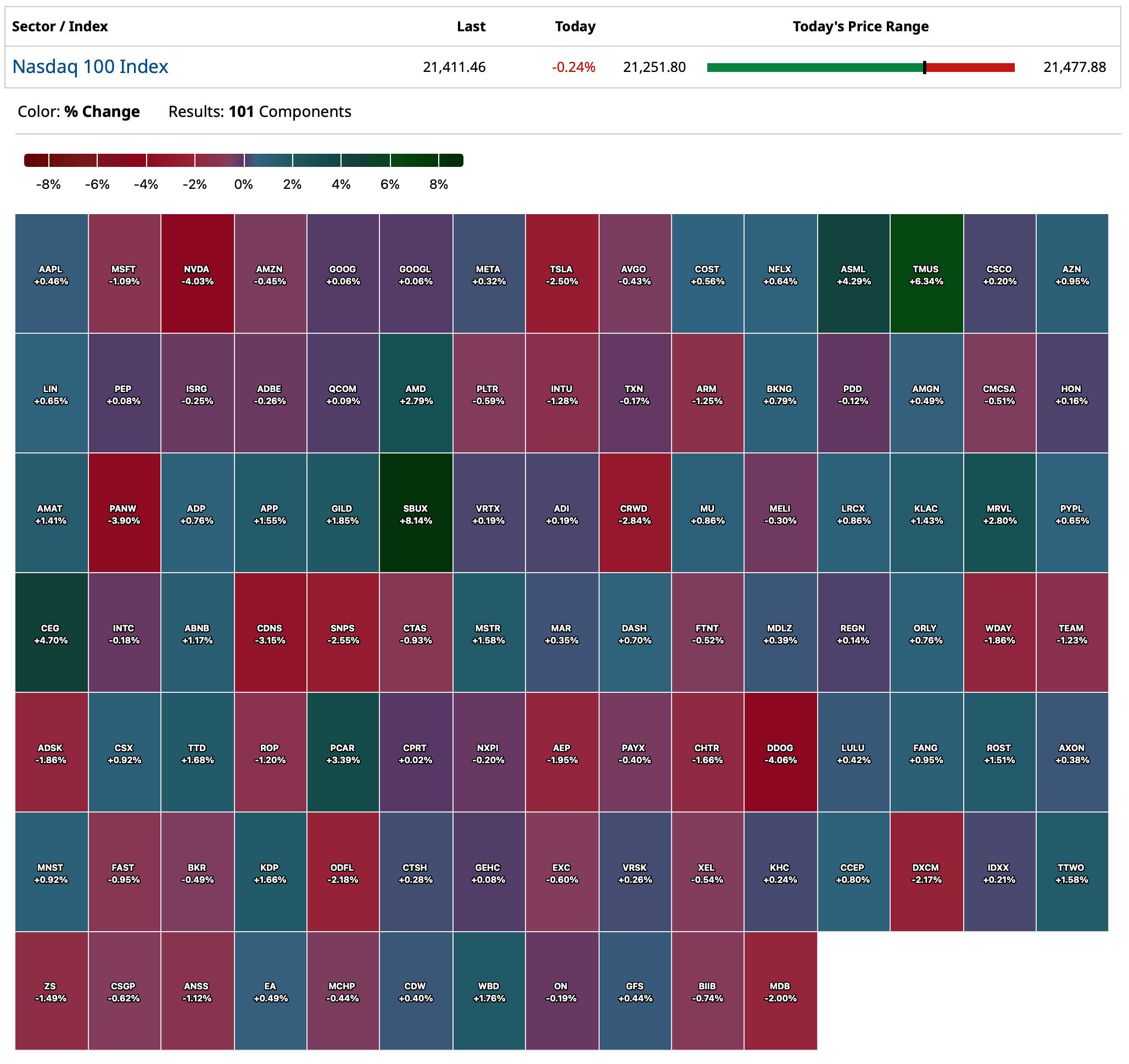

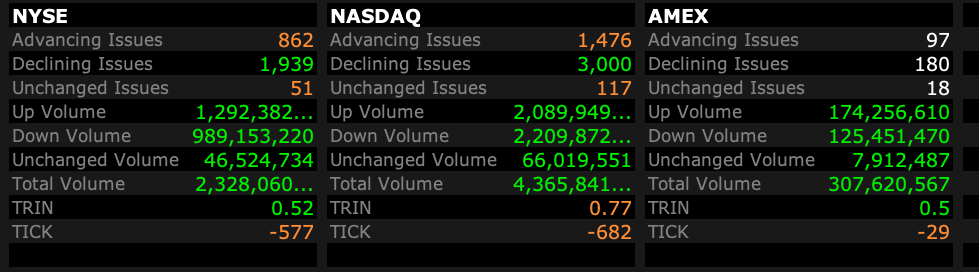

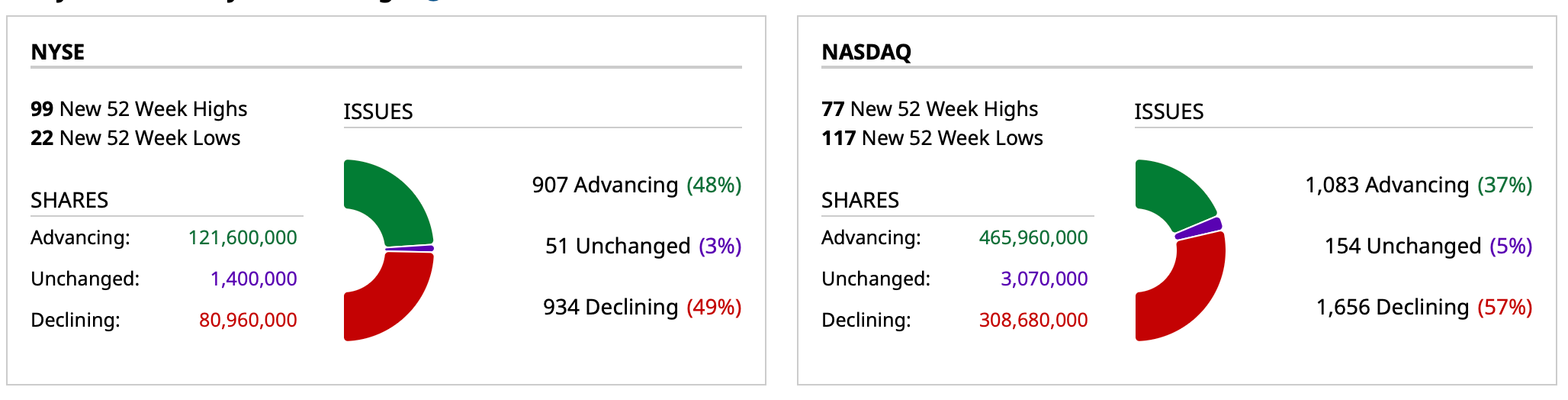

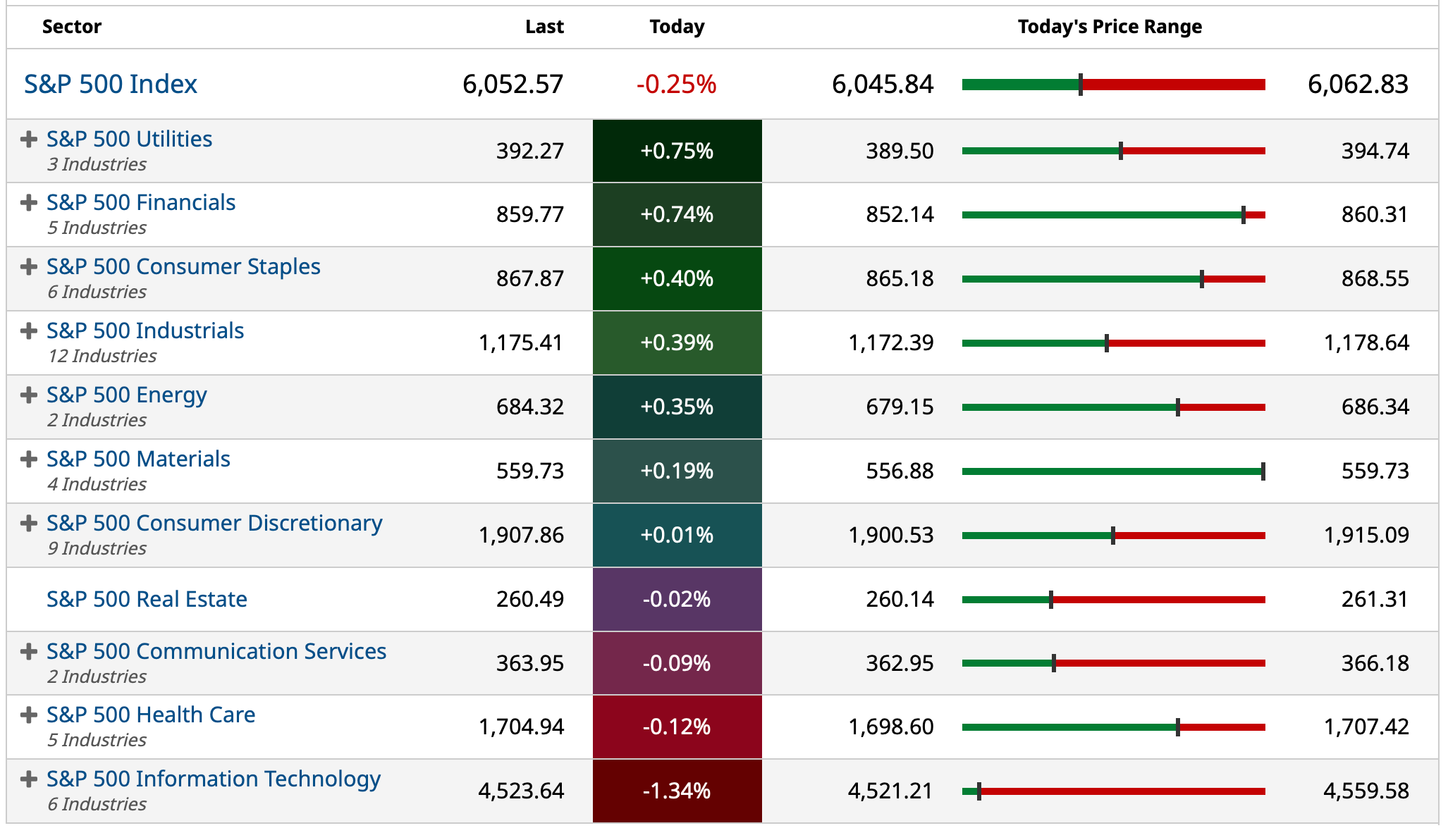

Breadth is weak (at around 2-1 negative on both the NYSE and Nasdaq) and the equal-weighed S&P is -0.53% (the second day in a row of relative underperformance in equal weighted):

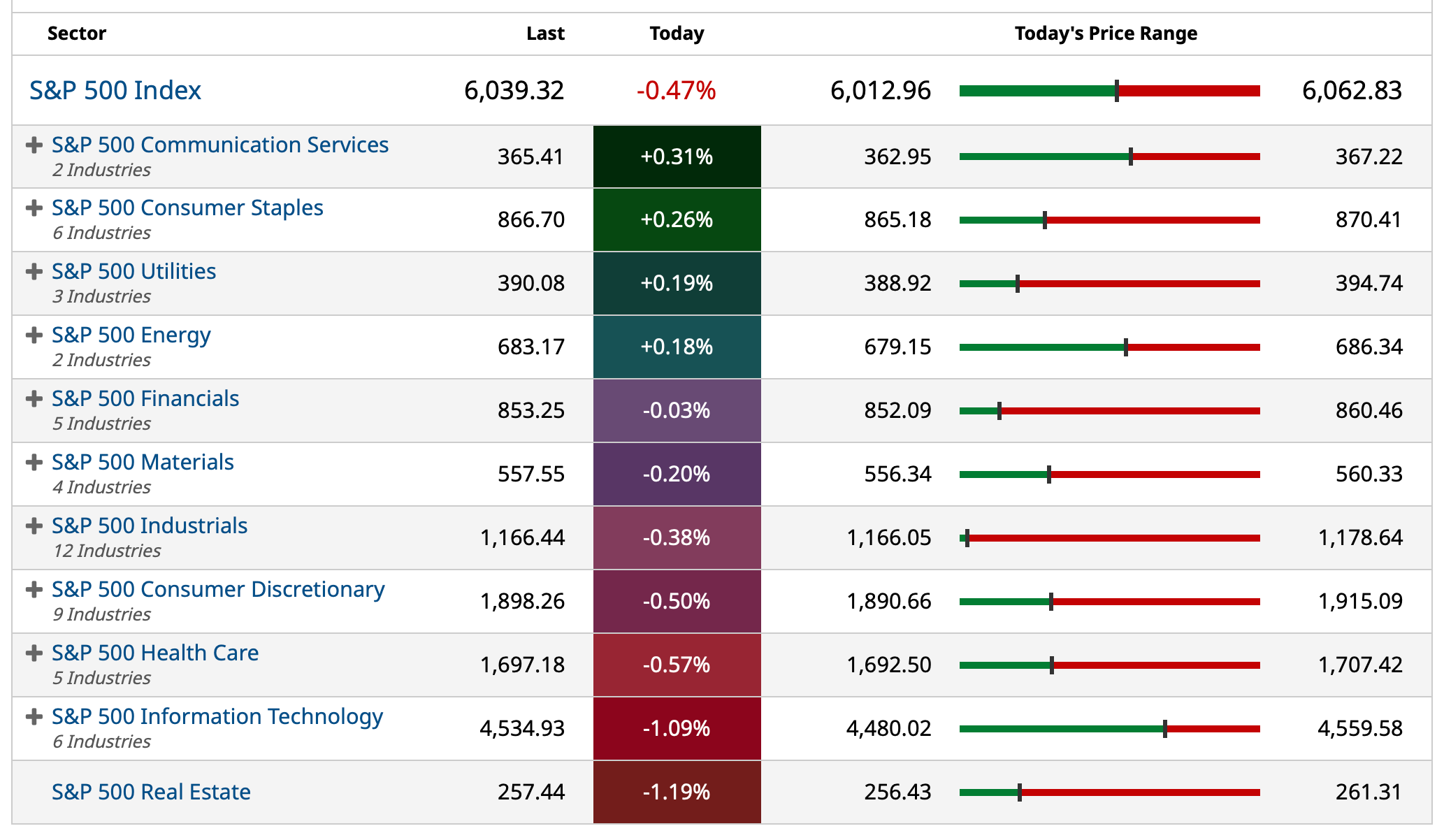

At 2:20 p.m. S&P cash is down by -50 handles.

Here are today's "Things":

* I traded Indices back and forth, profitably (making multiple points on SPY/QQQ shorts and covers, three times!). Out of all Index shorts now.

* I added across the board to MSOS at $3.39 and individual cannabis equities (TCNNF at $4.81, AYRWF at $0.46, CRLBF at $0.88, GTBIF at $6.97)

* I added to JPM $270.27 and XLF $51.72 shorts — and initiated shorts in MS at $140.42, GS at $646.80 and C at $81.53.

Market, volatile? Just look at Boeing BA intraday on Tuesday and this morning...

Yesterday I sold all of my BA at $186.32.

Today the shares are falling, trading at around $171!

That was quick!!

In response to some questions, I would be a buyer between $155 -$165.

From Tuesday:

Jumping Off Boeing

Boeing is trading +$12.50 on a release that was generally expected.

I just sold my remaining position at $186.32 - as it is nearly +$40 from my cost basis of a few months ago, substantially reducing the previously favorable reward v risk.

Boockvar on What to Watch from Fed, Earnings Calls

From Peter Boockvar:

Oh yeah, there is a Fed meeting today

Oh yeah, there is a Federal Reserve meeting today as I almost forgot with Trump 47 and the now DeepSeek news dominating the headlines. The statement seen at 2pm will be a non-event but I'm most interested in two things when it comes to the Powell press conference. Will Powell echo what Governor Chris Waller said a few weeks ago on CNBC when he said "As long as the data comes in good on inflation or continues on that path, then I can certainly see rate cuts happening sooner than maybe the markets are pricing in." Or was Waller just politicking for Powell's job when it frees up in May 2026 in being dovish and getting in the good graces of Trump who said he wants interest rates lower, immediately? Or will Powell, as I think he should, just be non-committal on rates from here, especially as headline GDP (goosed by both government spending and government incentives via infrastructure, IRA and Chips Act) continues to be around 2.5% and as we await what the tax/tariff policy will be from the new administration.

Also, will there be any questions and Powell comments on the Fed's balance sheet. Most expect QT to end this year but when and at what targeted level?

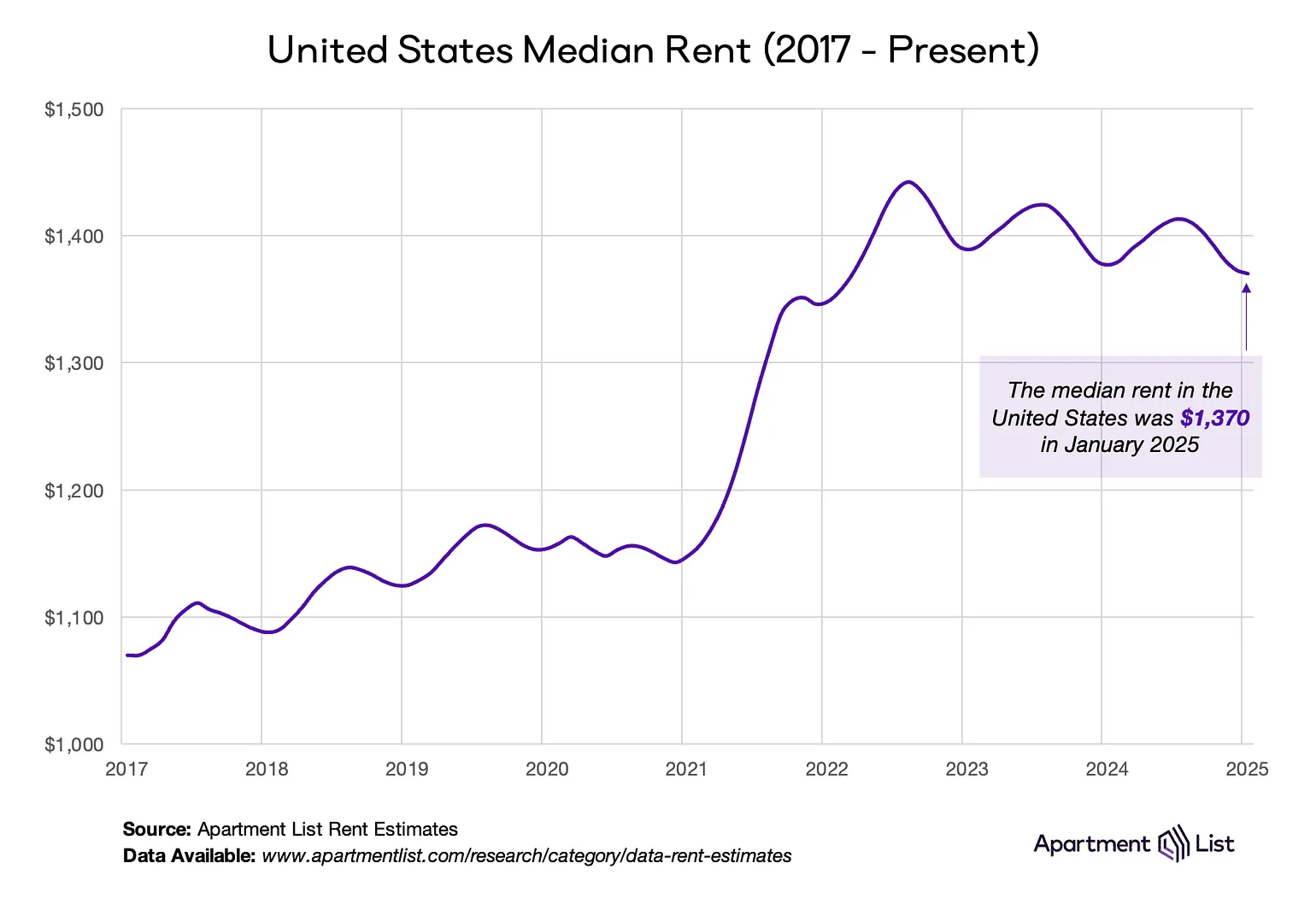

On inflation, the rental growth moderation should continue to filter thru the services component but with still many of the unknowns, I just don't see how Powell has any confidence on how things ultimately play out to commit to anything today. As for rents, Apartment List on Monday said that NEW rents fell .2% in January m/o/m in the seasonally slow rental period. They are down .5% y/o/y. The vacancy rate rose one tenth to 6.9% which is the highest dating back to 2017 when they first started collecting this data point. We know all about the big supply that came on line last year with almost all of it in the sunbelt with Austin, Texas leading the way on the price declines.

Apartment List also said this though, "Year-over-year growth has now been negative since June 2023, but in recent months, there are signs that we could see a return to positive growth this year...With the supply wave now getting past its peak, it appears that the era of declining rents could be nearing its end."

This is something I've been arguing about. We have to enjoy this rental deceleration while it lasts because it won't. With the huge affordability challenge in buying a new home for a first time buyer, rental demand will continue to be solid and as we digest the large amount of new supply, and as there will be very little new supply in the coming few years, rental prices will reaccelerate I believe in the back half of this year, into 2026.

To the many earnings calls.

From Starbucks whose global comps fell 4% and did the same in the US:

"US comparable store sales improved sequentially throughout the quarter, most evident in the morning day part as non-Starbucks Rewards customers grew from our strategic shift to broader marketing. Our ticket growth in the US remained strong at 4% due to the benefits from the prior year pricing, attach and fewer discounts. These drivers more than offset mix shift into lower priced beverages and removal of the extra charge for non-dairy milk customizations."

"Our US category share among QSRs also recovered in Q1 following two quarters of declines. These things tell us our actions are resonating with customers."

"In the US alone, we still see the potential to double our store count while improving the overall health of our portfolio."

In the face of record high coffee prices, Starbucks seemed to have done a good job in hedging this exposure but will clip earnings by one penny per share and they said "Although we can pass this cost to our business partners, higher prices to an already pressured consumer will likely impact our segment volumes and ultimate revenue and profitability."

From Houlihan Lokey, the investment bank and saying that higher interest rates are squeezing some businesses, as we know and M&A interest is picking up:

"Corporate finance and financial and valuation advisory continue to benefit from improvement in the M&A and financing markets, while financial restructuring had another solid quarter as it continues to benefit from record leverage and persistently higher interest rates."

From LVMH:

"2025 is starting well, and I will tell you all about it in a moment. A robust year, despite a challenging global environment, weaknesses in Asia, except Japan that reported strong growth thanks to its currency. The US, uncertainty because of an election year. Europe is fairing quite well. But all in all, the context was a little bit more challenging."

"Asia is still pretty difficult all year round. That's true across Asia, including mainland China. Roughly 10% drop over the year. As for Europe, it's similar to what you saw in the US, a slight improvement, and at the end of the year, mainly in Fashion & Leather goods.

From Polaris, the maker of snowmobiles, ATVs, boats and motorcycles and whose business is tough right now with higher rates and big ticket items just not selling so well in this demographic:

"2024 presented significant challenges across the powersports industry, leading to a prolonged down cycle driven by various factors affecting OEMs, dealers and consumers...We know these are challenging times for consumers in our industry."

"If I could sum up dealer sentiment right now, I would say they are cautious. They are closely watching inventory across all categories and OEMs. Dealers are seeing OEMs take different approaches in this prolonged down cycle and are therefore choosing to keep inventory light as they continue to experience low retail. Just this last quarter we've seen news of OEMs filing for bankruptcy or shutting down production for a prolonged period of time as well as OEMs putting part of their business up for sale which leads to many questions - many to question the future of some brands."

"Similar to dealers, we remain cautious about the industry. Retail trends have not given us a reason to change our outlook, nor do we see much change for the consumer in 2025."

Kimberly Clark had some interesting comments on birth rates where they are unfortunately falling in many places, as they sell diapers:

"I'd say the good news is birth rate declines are leveling off, and in some markets, notably Korea, we saw a positive birth rate in the third quarter, which continued in the fourth and that was the first time in 8 years and in China was positive in birth rate as well. So I'd say, one, on penetration, birth rate declines kind of inflecting a bit at least early signs."

By the way, the birth replacement rate in South Korea is the worst in the world at about .7.

From Sysco, the biggest food distributor into the restaurant business:

"Foot traffic to restaurants in the US was down approximately 2% for the 2nd quarter, which represents a moderate improvement from Q1. We expect to see continued improvement in traffic trends as we head into the 2nd half of the year."

"Inflation for the industry has maintained at approximately 2%, which is within the normal range, when we look at cost of goods sold inflation over the course of decades."

From GM:

"I think there's some speculation out there that we saw a big pull ahead in demand in the month of December, whether that was EV driven or just consumer driven ahead of inauguration. I think one of the things is we're adopting a little bit of a wait-and-see on that. January has been really noisy...about both the weather, the fires in California, etc...So it's tough to glean whether there was a big pull forward. So, we've kind of projected demand to be pretty similar to last year."

With mortgage rate still hovering around 7%, the MBA said purchases were flattish w/o/w, down .4% and lower by 7.3% y/o/y. Refi's fell 6.8% w/o/w, though up 5.2% y/o/y. Back to the Fed, as we know their 100 bps of rate cuts ended up worsening housing affordability with the jump back up in mortgage rates in response.

Australian bonds rallied overnight after Q4 CPI was one tenth below expectations, though the December print of 2.5% was in line. The Aussie$ is lower while stocks there rallied.

In Europe, the Swedish Riksbank cut rates by 25 bps to 2.25% as expected but said they are now on hold. The Governor said "Our best estimate is that we trough where we now are at 2.25%, but it is genuinely uncertain whether that view will hold."

An expected rate cut is expected to come from the Bank of Canada to 3% but that could be it for them for a bit too.

* Morgan Stanley confirms our channel checks on this pet company...

This morning Morgan Stanley lowered its price target on Elan ELAN from $15 to $14 - keeping equal weight:

After having met with several Animal Health management teams at VMX, the world's largest companion animal health conference, the Morgan Stanley analyst tells investors that "sentiment was cautious into 2025" on low compliance and deteriorating vet office visit trends.

In light of foreign exchange dynamics and "a continuing lackluster vet visit backdrop," the firm is trimming estimates and price targets for Zoetis ZTS, Idexx IDXX and Elanco.

From Morgan Stanley's report:

We met with several management teams and animal health industry professionals at VMX, notably Zoetis, Elanco Animal Health, IDEXX Laboratories, Covetrus, Patterson Companies, among other constituents. Some key takeaways from our conversations include: (1) vet office visits / compliance remain an enduring headwind across the industry likely continuing well into 2025; (2) innovation and leveraging across the industry likely continuing well into 2025; (2) innovation and leveraging alternative channels offer offsets for pharma in a lackluster demand backdrop (ELAN, ZTS); (3) dermatology and parasiticides may get more competitive (MRK AH potential '25 launches, covered by MS Pharma Analyst Terence Flynn), (4) price increases are only slightly more subdued than '24 (still +MSD across AH pharma); and (5) IDXX showcased its innovation lineup, detailing Cancer Dx, albeit offering limited insight into inVue traction (LT prospects remain favorable, in our view, see survey here).

Importantly, in light of FX dynamics and a continuing lackluster vet visit backdrop, we are trimming our estimates and Price Targets for ZTS, IDXX, and ELAN. Enclosed, we detail key model updates as well as takeaways by company across pharma, diagnostics, and services in Animal Health.

Two days ago I cautioned on ELAN:

ELAN Disappoints

Our channel checks for Elanco (ELAN) are a bit disappointing.

I was hopeful that the company would be street expectations, but that now appears challenging.

Though the quarter is not reported until February 24 (four weeks away), discretion is the better part of valor and I have sold most of my common holdings.

However, I am keeping my calls (as the pet company remains a bonafide takeover candidate).

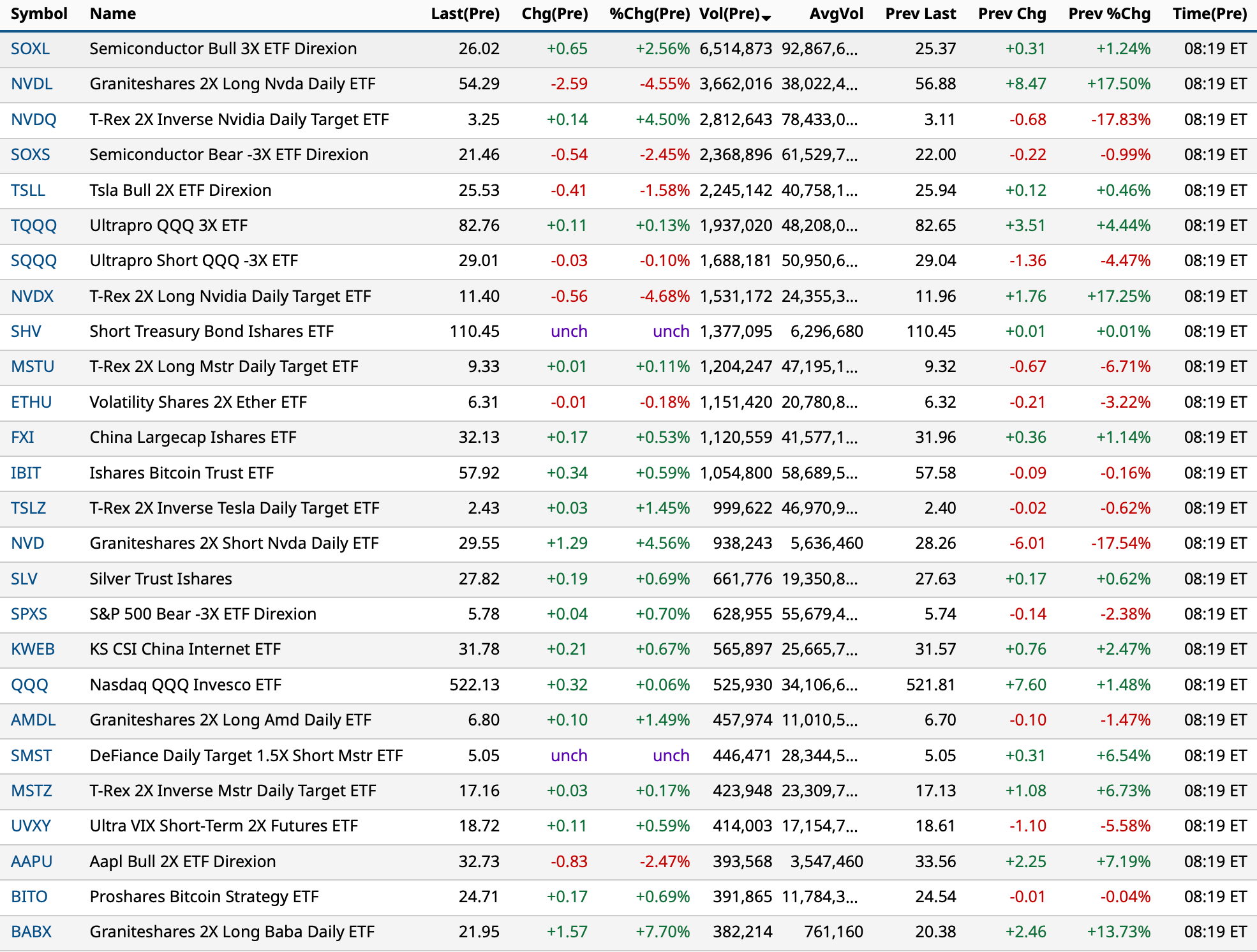

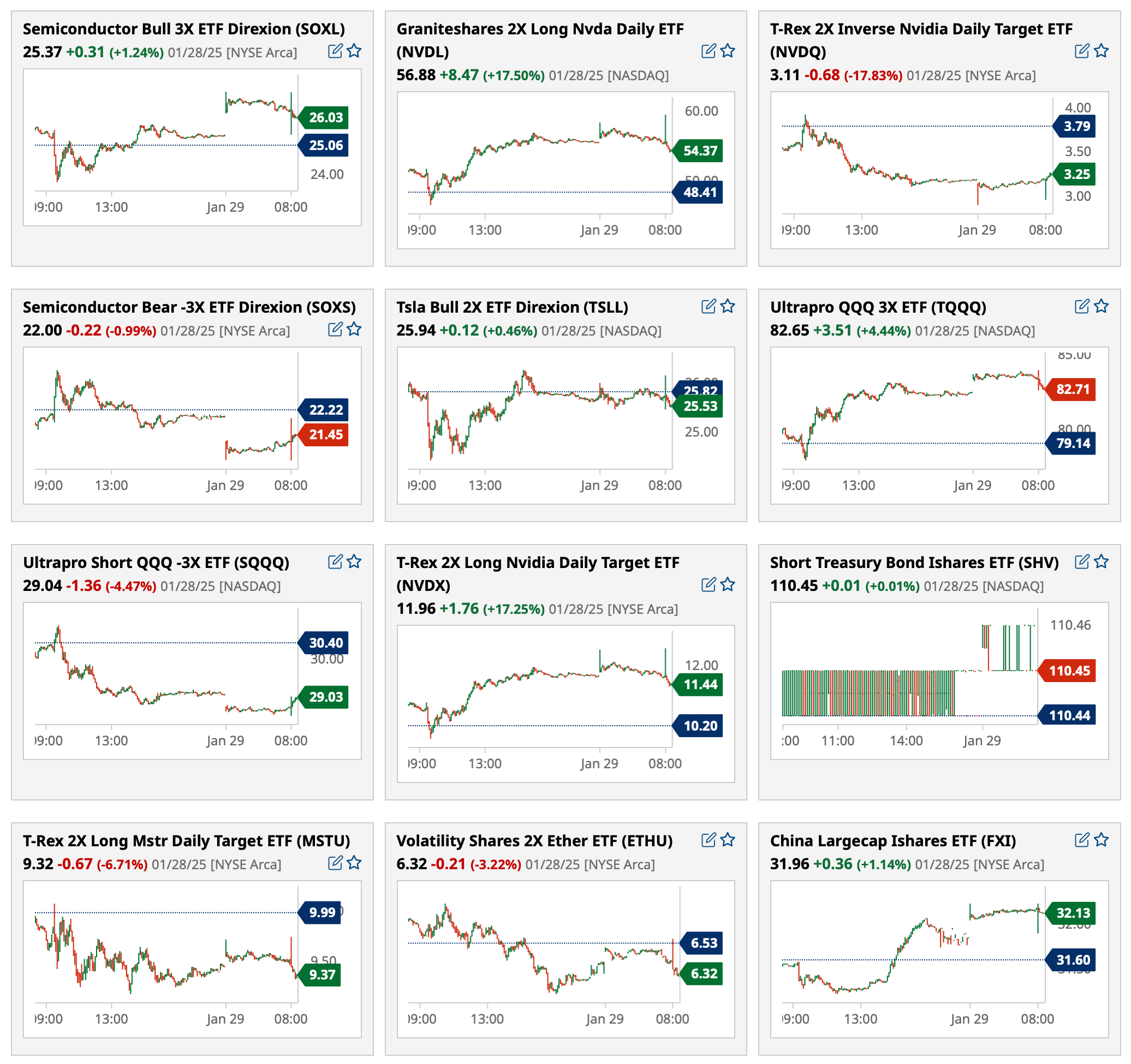

Let's start with this announcement early in the morning about potentially more AI competition from Alibaba BABA.

More snippets.

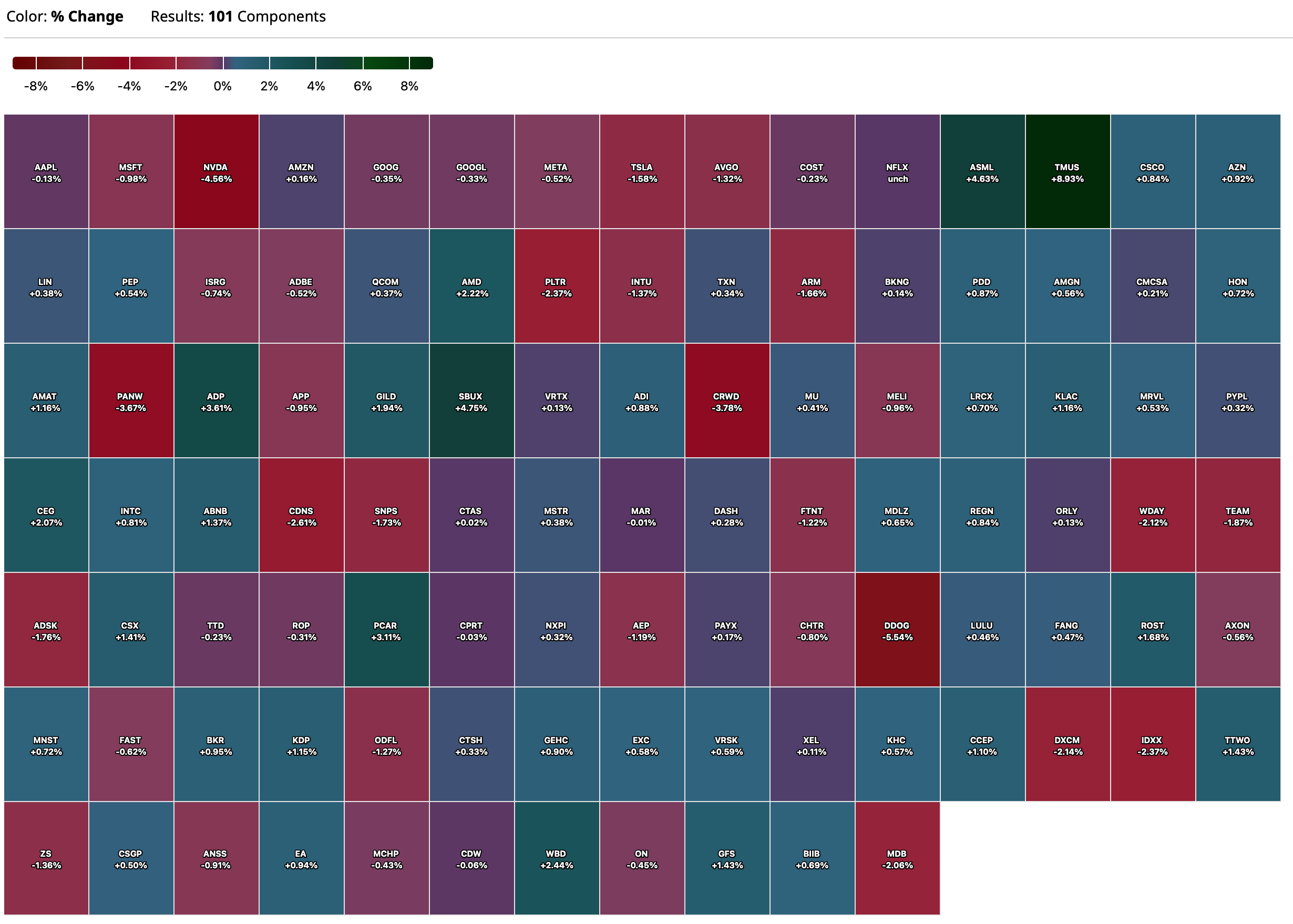

First, an observation. If you look at the amount of $ trading in Nvidia NVDA, and the amount of market cap involved, don't ever let anyone ever tell you again that when the government prints money it does not go into the economy and into the price of everything!

This information was all out there. Maybe if people would have done a little due diligence, as opposed to just blindly following what they are told by the guys selliing AI, none of this would have been a surprise. Second of all, given this stuff was all out there, it is very challenging for me to believe that people in the industry (Nvidia, Microsoft, Sam Altman, etc.), did not know about this. And per my prior "Tales" on the Satya Nadella tweet, we did not hear a peep about it from them. If it was such a positive development, they would have been touting this just like they tout everything else:

Plenty of Breadcrumbs

Breadcrumbs about the "cost-effectiveness" of what DeepSeek is doing have been dropped for MANY months, including this from July:

Next, a thoughtful piece of research by Julien Garran at MacroStrategy. All the lenders that took chips as collateral for their loans, whoa boy:

It has been an extraordinary week for Large Language Model (LLM) AI. First, we had Trump’s and Sam Altman’s announcement of the ‘Stargate’ US$500bn US LLM datacentre infrastructure build out. Then, with little fanfare, Deepseek released its R1 LLM as an opensource model. On Thursday Sam Altman launched Open AI’s first ‘agent’ called Operator, that is meant to order you pizzas, buy your groceries and tickets to a ball game. Then, by Friday, people started to realise that Deepseek was beating the best-in-class US LLM’s on their own test metrics, but that it had reportedly only cost a fraction to train, and you could run it on a high-end PC. This past week’s announcements put the nail in the coffin for LLM AI compute market this cycle. But they were simply the culmination of a series of developments, all in the public domain and discussed regularly on these pages, that had collapsed the market for LLM AI compute already, bringing H100 rental prices down from US$8/hour in Q2 2023, to 99c/hour as of last week. It is only this week that markets have noticed.

I estimate that Blackwells will have to rent for US$9.20/hour to make a 5% return on capital, and US$10.60/hour with tariffs. LLM developers will face a trade-off; run three H100s in parallel for US$3/hour or less, or run a Blackwell, to get the same compute. Well before Deepseek landed, I argued that Blackwells would struggle to rent for anything close to that and that there was a growing likelihood that we’d start to see order cancellations. The Deepseek launch and Trump’s tariffs have raised the likelihood of cancellations dramatically.

There are several major implications; first, you’d have to have a really good aesthetic or pollical reason to use something worse than Deepseek, and more expensive to run, like Chat GPT, Anthropic, Copilot etc. This renders the developers’ entire capex in LLMs to date close to valueless. It also raises the question why would you invest in training a next LLM if a competitor usurps you within three months with an opensource ap that is much cheaper to use? This should collapse future LLM training. Finally, if the cost of inference is also much lower, then the market for compute, which is already in the basement, and where rental for new chips doesn’t cover the cost of capital, will weaken even further.

At the same time, Open AI’s new ‘Operator’ agent is not fit for prime time, while multiple reports suggest that scaling, the improvement of LLMs with increased training, has hit a wall. In short, the LLM AI development and datacentre ecosystem is now fundamentally broken. At some point, the US$34bn+ credit in the ecosystem will head for the exit, and that suggests that the protagonists in LLM AI development, datacentres and chipsets, have a long way to fall. In the next cycle, cheap compute may open up opportunities for useful aps, but not in this one.

This tweet is interesting too regarding my point that the current export controls are a paper tiger. DeepSeek is using the highest end part that is not supposed to go to China:

The export controls, as currently structured, are meaningless, maybe purposefully and they were just PR from the prior administration to make it sound like they were tough on China. So many ways to get around them. Nvidia can ship to a legitimate destination, then whomever has the part can turn around and sell it into China. It is not complicated. I think Nvidia has even publicly owned up to the fact that they don't know where all their parts ultimately end up.

To whit, Nvidia U.S. revenue growth over the last three quarters is +21%. Nvidia's Singapore revenue in the last quarter was $7.7B (+185% YoY) — more than half its U.S. revenue in the same quarter. Seems rather strange given the export controls? Where does it go once it gets to Singapore? Also, the fact that U.S. growth has now slowed to 21pct y-y tells you something about underlying U.S. demand, and how it is flattening.

This remains a risk too. The current administration, if they behave in a way that is consistent with their behavior to date, and their public statements that AI is a national security issue, will find a way to cut this stuff off. I am sure they know what the food chain looks like, and the various ways parts can make it over to China. There is a way to stop it.

Holy Retail!

And once again per the point about money being put into the economy. The goofy thing is maybe the world has turned upside down, and institutions will chase retail now (retail seemingly is not afraid of catching falling knives), and the algos will frontrun and turbocharge all of it? It really is a brave new world out there.

US: Futs are flat with Tech/Small-caps big higher as the market looks to recover from Monday’s Tech Plunge. Pre-mkt, Mag7 names are mixed with Semis rallying but this may not mean the end of the Semis-to-Software rotation which is +10% this week (JPPQSFSM Index). Bond yields are flat to down 1bps ahead of what is expected to be a dovish pause by the Fed today. USD strength continues, given the likelihood of new tariffs announced this week or weekend. Cmdtys are mixed as Ags and Metals are bid.

and...

EQUITY AND MACRO NARRATIVE: What a difference a day makes … Retail investors were very active in the second largest buy-day since the Inauguration, buying ~$1.8bn vs. $512mm (1-month avg), +2.75z.NVDA retraced ~44% of its Monday loss.What changed? Not much actually. While there were some extreme moves on Monday, the equal-weighted SPX (SPW Index) closed +2bps and the moves in Credit did not match their Equity counterparts. So, if we take a step back and look at fundamentals, we remain in Goldilocks territory with an update on ISMs and NFP next week. While the market is not the economy, if the US remains in a 2.5% - 3% range for real GDP it will be difficult for stocks to move lower. Today, we enter a critical part of the earnings season with Mag7 kicking off (previews in the succeeding sections).

· FED –Feroli expects a dovish pause and maintains his call for 2x rate cuts in 2025, one in June and one in September.

·TREASURIES –Before the events of Monday, Jay Barry likes owning the 2Y but the 7bps move on Monday made the risk/reward less favorable and he took profits. Longer duration bonds are unlikely to see their yields decline materially given the uncertainty surrounding policy and the US fiscal outlook.

· USD – the dollar has been reactive to tariff headlines and we saw a jump overnight on suggested policy from Bessent and then additional Trump comments.

· FED BREAKEVENS FROM RATES TRADING (David Nadle) –In the last several sessions vols have softened (despite a brief pop yesterday in the rally) and the surface has steepened. Dealers remain long gamma across a wide range of strikes (+/- 20 bps in 10s) and program sellers have remained active in 1m10y, selling ~750mm 1m10y equivalents per day. In core gamma payer skew has softened driven selling from FM and AM both outright and via ladders in addition to yesterday’s sharp reversal of rate/vol directionality driven by a shift in equity/rate correlation. Payer skew now appears to offer quite attractive entry levels as dealers flip short gamma >4.75 in CT10y and points such as 1m10y +25 are merely +2.5 ABPV of skew. We continue to favor surface steepeners as realized vol is likely to remain somewhat suppressed given gamma positioning. On the LHS FM has continued to sell 1y tail vol, mostly as ATM straddles, as the vol slide remains attractive with the fed unlikely to be active in H1. VoV has richened in this sector as ATM vols have come lower, particularly on the call side of the distribution. We have seen FM buying risk off hedges in 1y tail low strikes driving this rotation Heavy gamma positioning and a fed that is expected to be quiet for the next several months results in tomorrow’s breakevens being the lowest FOMC breakevens since November of 2021.

o SFRH5: 2.25bp

o SFRH6: 5.50bp

o SFRH7: 5.75bp

o FV: 5.625bp

o 5y: 5.50bp

o TY: 5.125bp

o 10y: 4.625bp

o US: 4.50bp

o 30y: 4.25bp

o *the 1d terminal breakeven (premium/dv01) for a straddle struck at 3pm today, expiring at 3pm Wednesday