Much More Overbought

"Just one more thing."

- Lt Columbo

The S&P Short Range Oscillator moved much higher— to 5.61% from 4.73%.

BY Doug Kass · Jan 24, 2025, 5:30 PM EST

"Just one more thing."

- Lt Columbo

The S&P Short Range Oscillator moved much higher— to 5.61% from 4.73%.

BY Doug Kass · Jan 24, 2025, 5:30 PM EST

At 4:18 p.m.:

BY Doug Kass · Jan 24, 2025, 4:40 PM EST

BY Doug Kass · Jan 24, 2025, 4:30 PM EST

Finally some common sense — from Barron's.

Persistent Deficits Mean High Interest Rates May Be Here to Stay - Barron's

Thanks for reading my Diary today and all week.

I hope it held value to you.

Enjoy the weekend.

Be safe.

BY Doug Kass · Jan 24, 2025, 4:17 PM EST

Rojizo

Doug, as we consider the possibility of January being a top in the market, it would be great to get a list of your shorts before we potentially start down. Even for times sake if it is just a quick dump of names and doesn’t have the exact short levels.

Dougie Kass

The point I made in Tuesday's four part market update is that I made money short in 2024 by shorting (on bottoms up basis) non drama shorts that had broken business models or that investors' had unrealistic expectations RILY CHGG MPW FIGS< FXLV WGO WBA SNBR KO PEP etc.

Now with broad market possibly topping (this month) my focus is on the liquid and overvalued Indices (SPY, QQQ).

Dougie

BY Doug Kass · Jan 24, 2025, 4:03 PM EST

Dr. Scott Galloway's No Mercy No Malice.... "American For Sale."

BY Doug Kass · Jan 24, 2025, 2:35 PM EST

I just covered this morning's Index shorts for a profit:

* SPY $607.11

* QQQ $528.32

From the opening:

Right after the opening I added to SPY and QQQ shorts at $610.01 and $532.78.

Position: Short SPY S QQQ S

By Doug Kass Jan 24, 2025 9:37 AM EST

BY Doug Kass · Jan 24, 2025, 2:25 PM EST

Back from a rest.

Getting my sealegs back.

BY Doug Kass · Jan 24, 2025, 2:18 PM EST

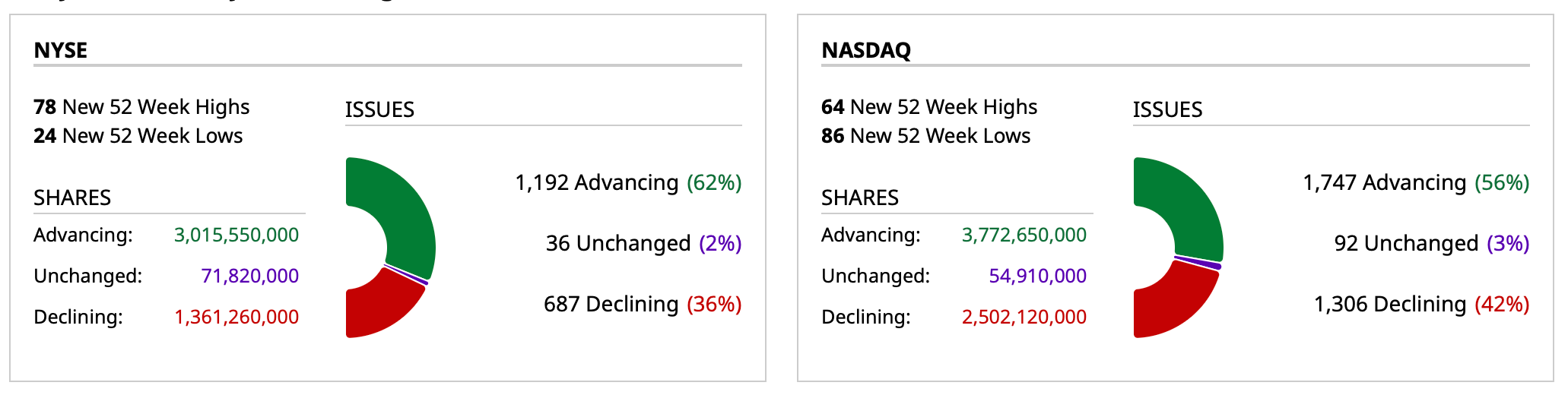

BY Doug Kass · Jan 24, 2025, 11:15 AM EST

I still have the flu so I will likely taking it easy today - probably go down for a nap at lunchtime.

My posts will be infrequent over the balance of the day.

BY Doug Kass · Jan 24, 2025, 10:39 AM EST

I have added to MSOS , Terrascend Corp (TSNDF) and CURLF this morning.

BY Doug Kass · Jan 24, 2025, 10:28 AM EST

Apple AAPL target lowered to $253 at BofA Securities ahead of earnings, cites mixed iPhone outlook and Services growth potential:

BofA Securities lowers their AAPL tgt to $253 from $256. Analyst Wamsi Mohan commented, "Apple reports F1Q25 (December quarter) after market on Thursday, January 30. We expect a strong report driven by initial demand for the iPhone 16. Our/Street revenues are $126bn/$124bn, and we model iPhone units of 79mn vs. Street at 77mn. However, partly due to the weak macro and partly due to the staggered launch of Apple Intelligence features, which we see as yet to gain widespread adoption, we lower our F2Q (March quarter) iPhone units estimate to 49mn (from 56mn) vs. Street at 52mn. For F25/F26, we now model 229mn/246mn iPhones vs. prior 239mn/257mn. We see Services as a growth driver for Apple and model revenue growth of 13% y/y for F1Q and 14% for the rest of the FY. Recent data on developer revenues indicates that App Store revenue grew 15% y/y in F1Q25. In our opinion, weaker iPhone sales are well understood by investors, and we reiterate our Buy rating on margin resiliency, tailwinds to gross margin, and strong cash flow. Investors will likely soon shift focus to WWDC, increased AI partnerships (Gemini, etc), launch of iPhone 17.”

BY Doug Kass · Jan 24, 2025, 10:25 AM EST

Bonds continue to rise in yield (and move lower in price) -- the yield on the 10 year Treasury is up by over two basis points this morning.

Equities continue to be unconcerned as the S&P makes an all-time high.

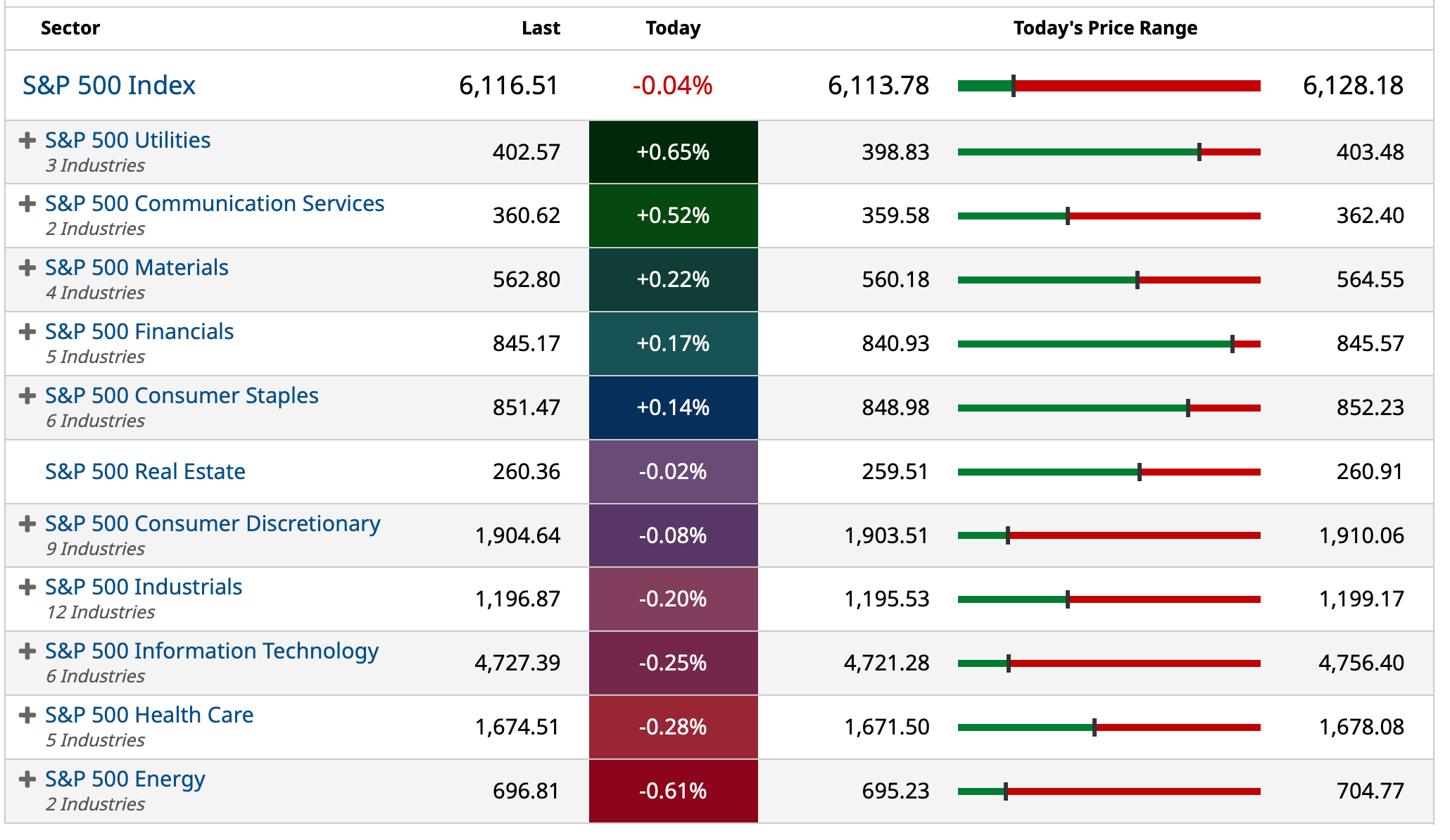

BY Doug Kass · Jan 24, 2025, 10:10 AM EST

One of the most expensive markets in history based on price to sales ratio and the equity risk premium:

BY Doug Kass · Jan 24, 2025, 9:45 AM EST

Right after the opening I added to SPY and QQQ shorts at $610.01 and $532.78

BY Doug Kass · Jan 24, 2025, 9:37 AM EST

BY Doug Kass · Jan 24, 2025, 9:30 AM EST

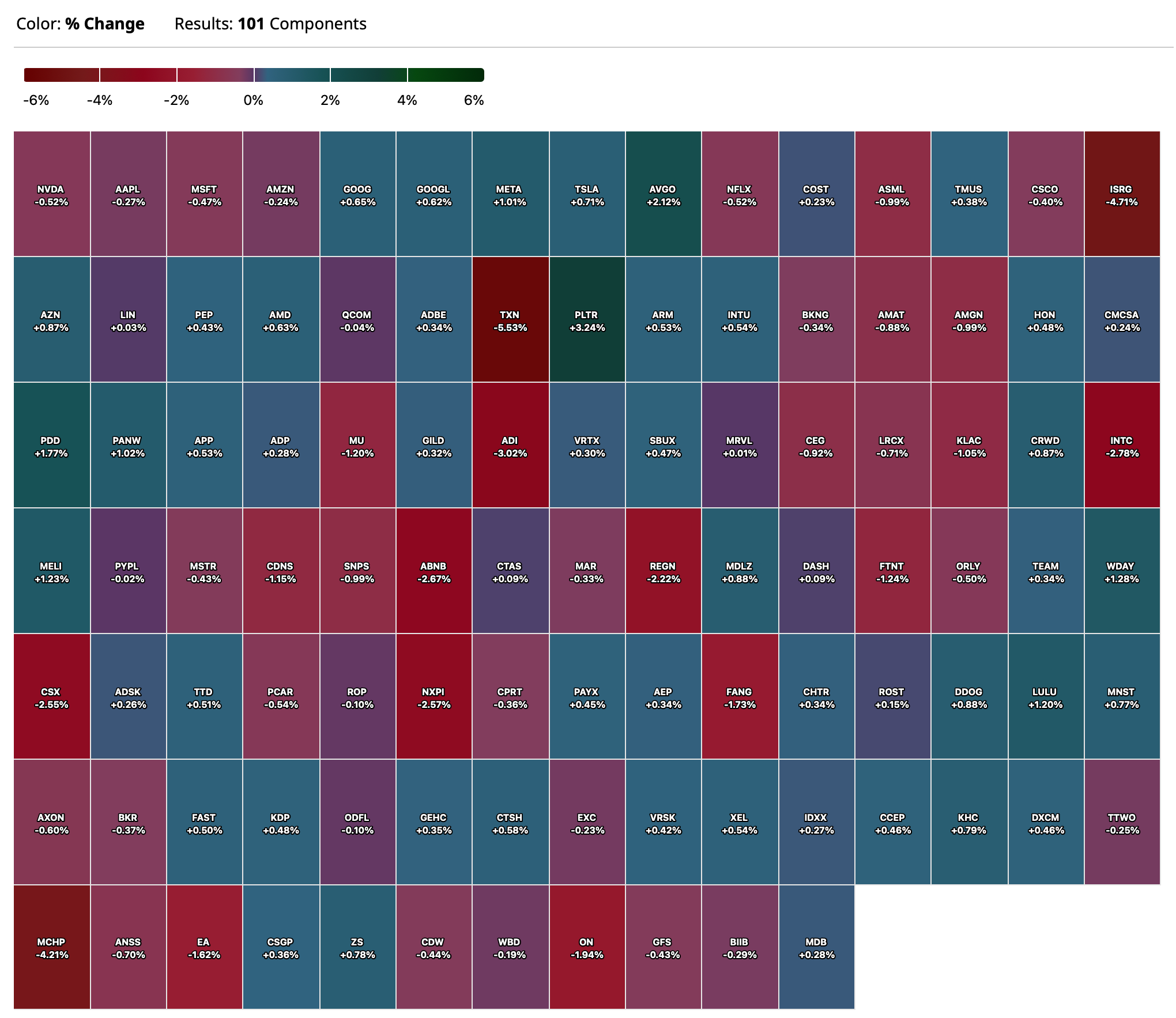

-TWLO +18% (guidance from Investor Day)

-FPH +13% (earnings)

-DDD +12% (in partnership with Daimler Truck announced a revolutionary solution to facilitate remote spare part printing)

-NVO +12% (successfully completes phase 1b/2a trial with subcutaneous Amycretin in people with overweight or obesity)

-GRND +7.0% (raises guidance)

-AFRM +4.5% (reportedly to receive $750M in funding from Liberty Mutual)

-ATHE +4.2% (Topline data for ATH434-201 randomized, double-blind Phase 2 clinical trial on track for expected release by early February 2025)

-CUBI +2.8% (earnings, guidance)

-EBC +2.3% (earnings)

-SMLR -12% (reports prelim Q4 Rev; announced a $85M offering of 4.25% convertible senior notes due 2030, upsized from $75M)

-EONR -8.6% (holder Pogo Royalty discloses sale of 1.1M common shares)

-TXN -4.0% (earnings, guidance)

-CSX -3.6% (earnings)

-EWBC -3.6% (earnings, guidance)

-ISRG -2.2% (earnings, guidance)

BY Doug Kass · Jan 24, 2025, 9:25 AM EST

Added small to index shorts in premarket trading:

* SPY $609.35

* QQQ $532.87

BY Doug Kass · Jan 24, 2025, 9:21 AM EST

META shares drop on news that it is planning to invest $60 billion-$65 billion in 2025 capex (mostly AI-related) vs. prior guidance of $38 billion-$40 billion.

BY Doug Kass · Jan 24, 2025, 9:14 AM EST

BY Doug Kass · Jan 24, 2025, 9:05 AM EST

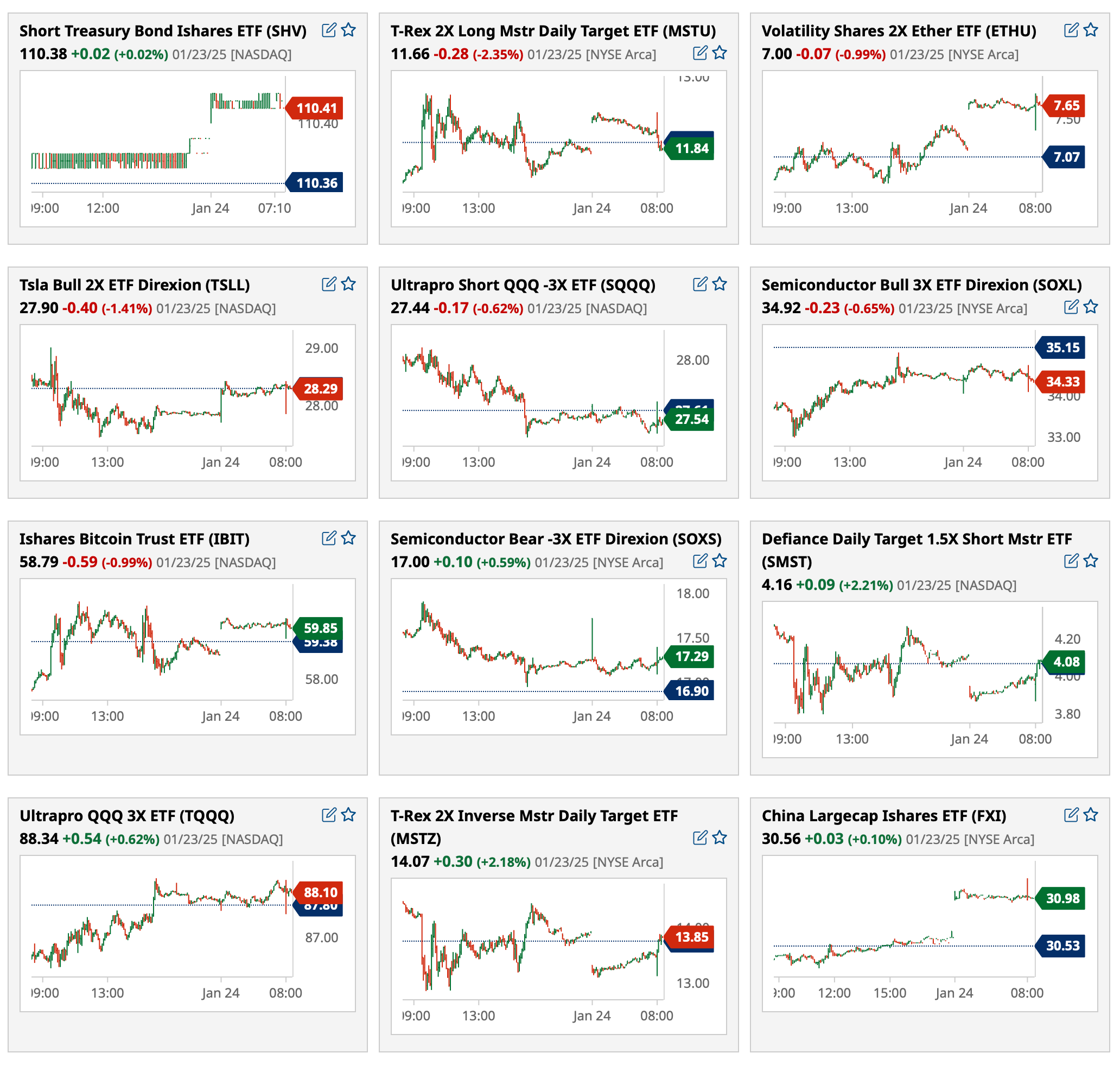

The S&P 500 exchange-traded fund SPY absent from most active premarket ETFs; QQQ ranks 30th:

BY Doug Kass · Jan 24, 2025, 8:50 AM EST

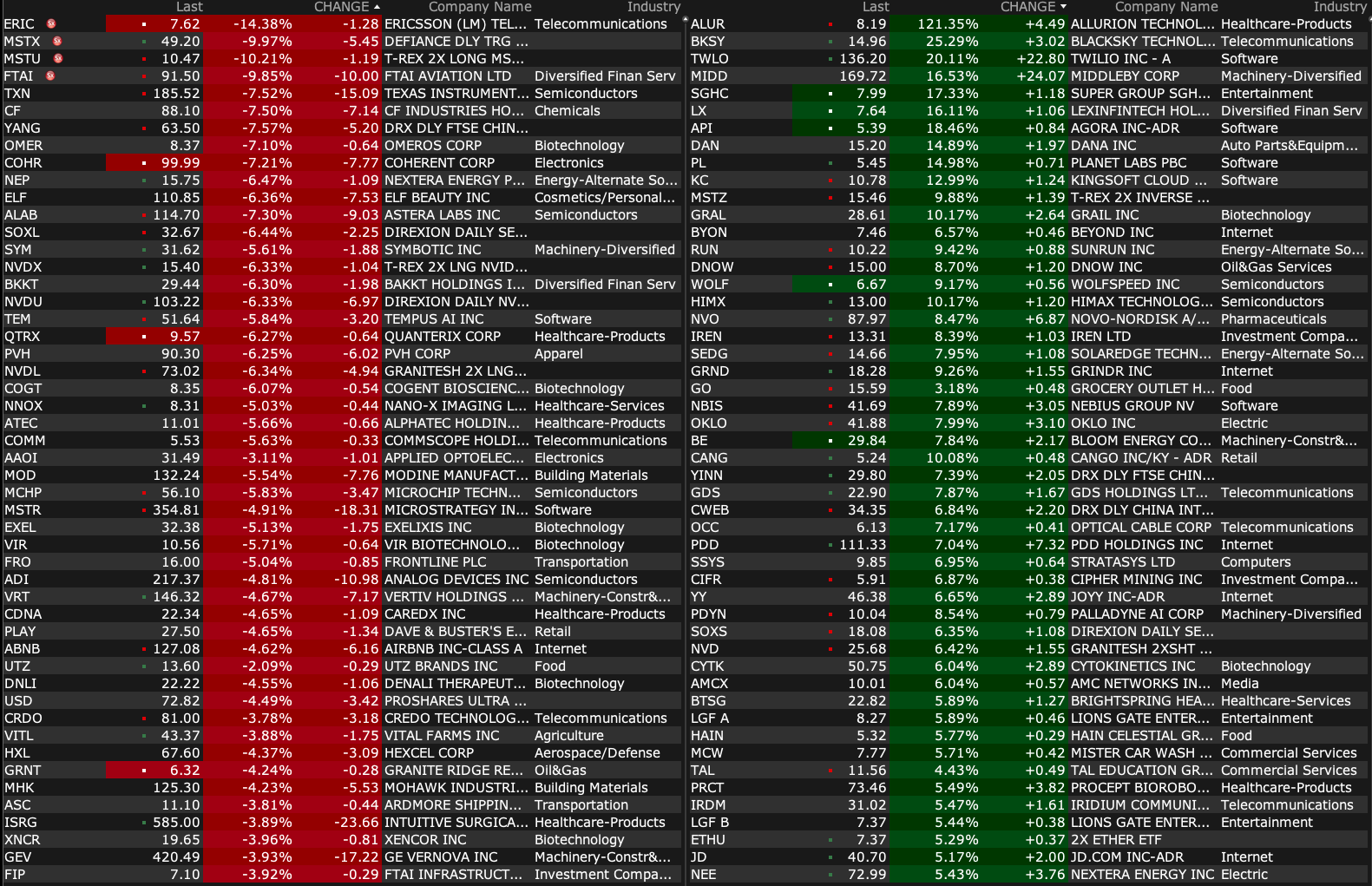

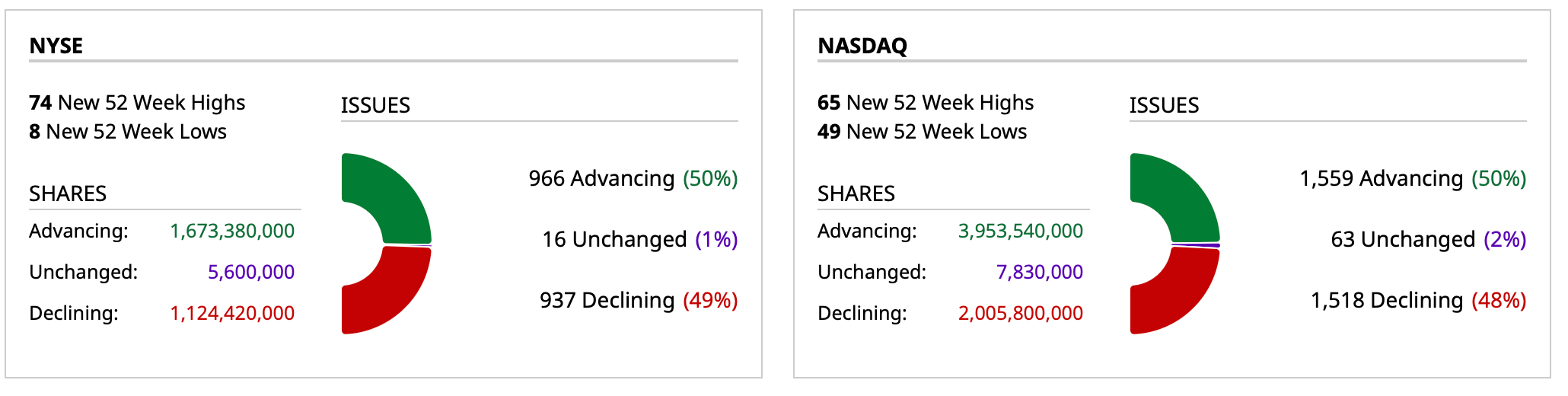

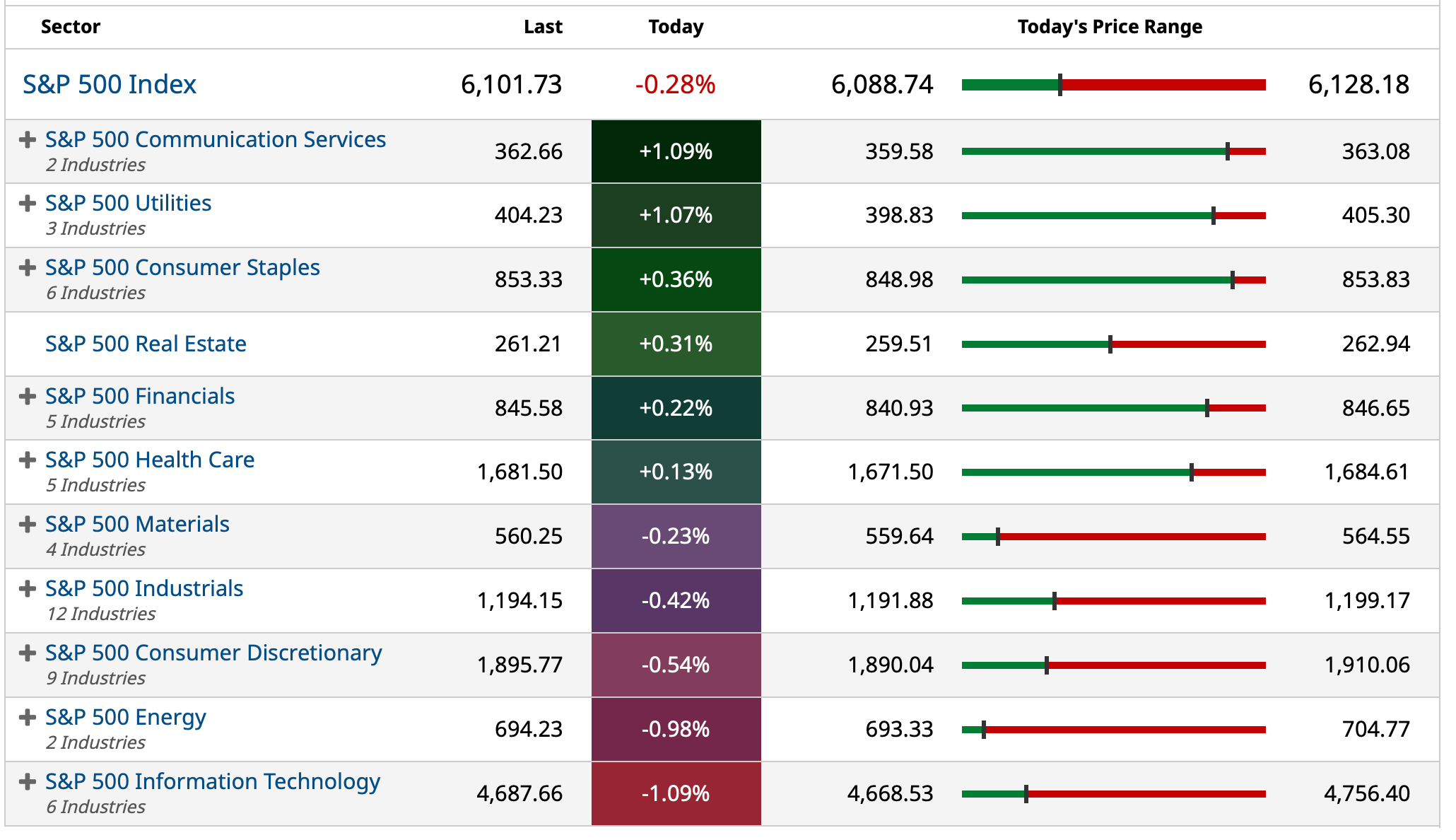

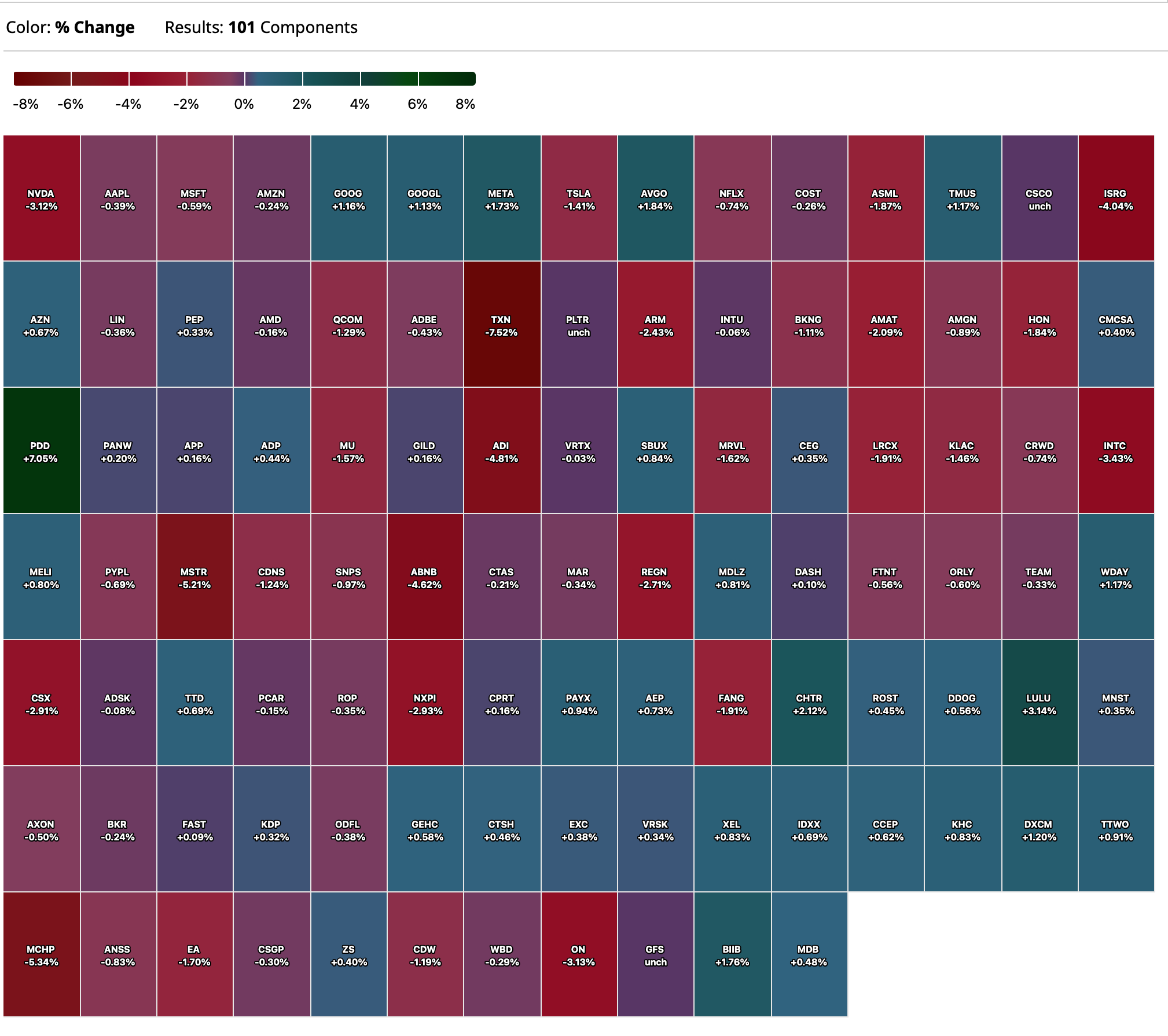

Premarket percent movers at 8:27 a.m. ET:

BY Doug Kass · Jan 24, 2025, 8:37 AM EST

From Peter Boockvar:

So the BoJ did follow through with an interest rate hike of 25 bps to .50%, the highest since 2008, which by meeting time was expected. The question then was what Governor Ueda would say about future hikes. "We don't have any preset idea. We'll make a decision at each policy meeting by looking at economic and price developments as well as risks." That said, "We'll raise rates and adjust policy if our outlook is realized." Not really discussed was the BoJ balance sheet where they continue to reduce the pace of their asset purchases.

Also of note, and pointing to more rate increases, Ueda said "The BoJ's estimate shows the neutral rate, in nominal terms, is in a range of 1%-2.5%. There's still some distance to that range, given the short-term rate is .5%."

Those last few comments is why yields across the JGB yield curve rose further overnight with the 2 yr yield up almost 2 bps to 72% and the 10 yr yield by a like amount to 1.23%. The 40 yr yield was unchanged. The yen initially rallied on the news but is back to unchanged. The Nikkei is flat and we still like and own Japanese stocks.

I still think what the BoJ does from here is a really big deal for global bond yields and liquidity.

Also out today and confirming why the BoJ raised rates to a still microscopic level of .50% was the December CPI print which came in up 2.4% ex food and energy as expected. The headline gain was 3.6%, two tenths above expectations because of the rise in both energy and food prices. While well above the BoJ overnight rate, Ueda said "I don't think we are seriously behind the curve in dealing with inflation." I scratch my head on that one but no central banker would admit to being so.

Japan's composite PMI for January rose to 51.5 from 50.5 and all because of a rise in services to 52.7 while manufacturing remained under pressure below 50. Australia's PMI was little changed just above 50 at 50.3 with also services above 50 and manufacturing below.

The Monetary Authority of Singapore, which uses its FX rate to tweak policy, slightly lowered its policy band for the first time in 5 years. Not a suprise.

India's PMI remained solid at 57.9 but did slip from 59.2 with both components well above 50.

The January Eurozone PMI got back above 50 at 50.2 from 49.6 and that was higher than the estimate of 49.7. The reason was a slightly less bad manufacturing print of 46.1, up 1 pt m/o/m while services came in at 51.4. While Germany's manufacturing sector remains very much under pressure, its services PMI was above 50 at 52.5. France though has both its key components under 50.

On inflation, while the ECB will likely keep cutting rates, S&P Global said this, "Cost inflation has increased in the services sector, which ECB president Christine Lagarde has said to monitor closely. Selling prices in the sector have risen at a similar rate to the previous month. Worryingly, input prices in manufacturing have increased, ending four months of stable or decreasing costs. This higher price pressure might be due to the weaker euro and the increased CO2 tax in Germany. In the services sector, it's likely due to wage increases, which rose in the eurozone at the highest rate since the euro's inception during the third quarter of 2024, according to Eurostat."

The UK PMI saw the same thing as manufacturing was up 1.2 pts m/o/m to 48.2 while services was 51.2 vs 51.1 in the month before. Combining the two has the composite index at 50.9 from 50.4 and vs the estimate of 50.1. S&P Global on pricing said "Inflation pressures have meanwhile reignited, pointing to a stagflationary environment which poses a growing policy quandary for the Bank of England." It does indeed.

The better than expected PMI's, along with Trump's tariff comments on China, does have the euro and the pound, with other currencies too, higher vs the US dollar after the extreme bout of weakness post election. Bond yields are higher in Europe while stocks are mixed.

Finally before I get to some earnings calls, the Israel/Hamas truce for now which led to the Houthi's saying they were going to stop targeting ships in the region, for now, resulted in the Shanghai to Rotterdam container route price fall by 19% w/o/w to the lowest since October. They also fell for the trips to NY and LA but less so. Maersk though did say today, "Due to the continued tensions in the region, the security risk of commercial vessels transiting the Red Sea and Bab-el-Mandeb strait remains high." And why they aren't going back their just yet.

Texas Instruments, a business where industrial and automotive contribute 70% of its revenue saw a 2% y/o/y drop in revenue:

"First, the industrial market was down low single digits. The automotive market was down mid-single digits. Personal electronics (20% of their business) grew mid-single digits. Next, enterprise systems declined low single digits. And lastly, communications equipment grew upper single digits."

In their industrial market, "most of the sectors are kind of hovering at the bottom, maybe found the bottom. And then there are a couple of sectors that are still showing larger declines, especially industrial automation and the energy infrastructure market that is still not found, I believe, at the bottom."

Also, "We haven't seen yet the start of the cyclical growth again in industrial across all of our geographies."

"And on the automotive market, similar to Q3, we did see kind of a pretty significant weakness, maybe outside of China. So it declined about mid single digits, about 5% sequentially, but China did grow, but not enough to offset the declines in Europe, the US and Japan."

The fast growing EV business in China is really strong for them and that has a higher content of their chips.

SL Green was optimistic on its main NYC market:

"On job creation, the city's OMB is forecasting about 38,000 new office using jobs in 2025. Those jobs will be coming out of the finance, business services and IT sectors. That translates into millions and millions of square feet of new absorption for each one of those bodies and those are not work from home bodies for the most part."

"Combine that with the fact that onsite attendance is rising every month as companies are calling people back to the office four and five days a week, we expect to see very strong demand for office space throughout 2025."

On the supply side, "there's real scarcity of well located amenitized space in Manhattan. I said in the December investor conference, there are zero new ground up office projects currently underway in core midtown and with 4 to 7 yr timelines for major projects, the reality is that inventory is only going to get scarcer in the coming years due to that imbalance between timeline for demand and the realities of when the space can be delivered in a best case."

I'll chime in here on that last comment. Counter to the Fed's desires, when money is free, with the purpose of stoking inflation, sometimes it sows the seeds for deflation as excess capacity is built. On the flip side, right now higher interest rates, meant to cool inflation, is sowing the seeds for higher inflation because it is crimping capacity in parts of real estate, here stated in office, and in other sectors of the economy too.

While American Airlines stock fell about 9% yesterday, because of higher than expected costs, they are still benefiting from the bull market in travel:

"Passenger revenue strength throughout the fourth quarter was broad based. In the fourth quarter, American's y/o/y Domestic, Atlantic, Pacific and total passenger unit revenue results led US network carriers."

"I see continued strength domestically and the strong dollar is absolutely going to have an impact on buying and travel to Europe this summer. So we take a look to March and as we look to some of our peak periods, spring break and getting into the summer, I see robust demand across the board."

Also, "We continue to expect full year capacity to be up low single digits, in line with expected economic growth and our prior guidance." Over the past few quarters, all the airlines have cut capacity from its peak and its why pricing has firmed up.

McCormick, the spice maker said this about some of their end markets:

"In flavor solutions, in both Americas and EMEA, some of our CPG (consumer packaged goods) customers experienced continued softness in volumes within their own businesses. And in EMEA, some of these customers were impacted by geopolitical boycotts in the region related to the Middle East conflict."

"In addition, QSR traffic remains soft in EMEA and in the Americas. We have seen this pressure impact our results for several quarters. It's difficult to predict QSR traffic."

BY Doug Kass · Jan 24, 2025, 8:17 AM EST

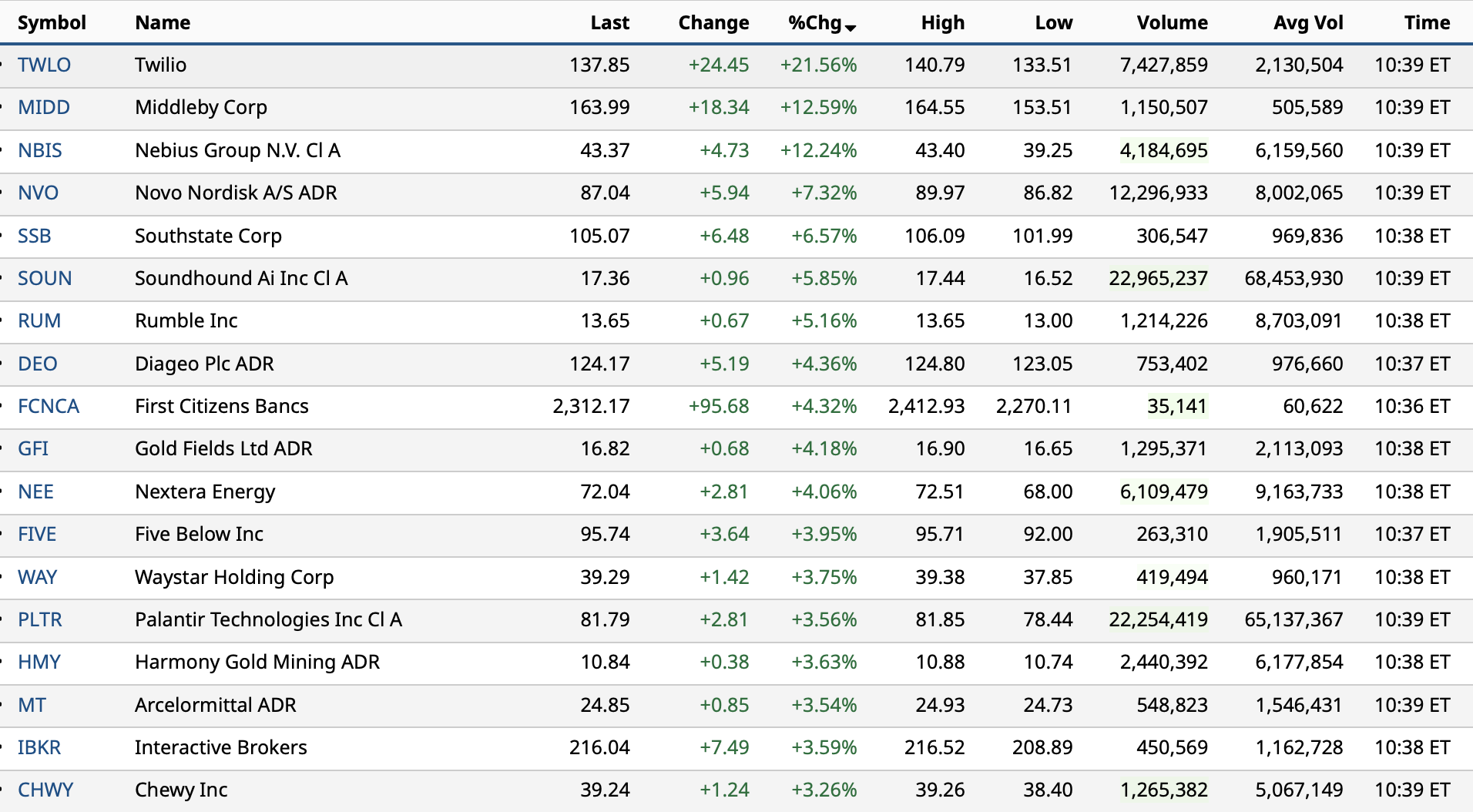

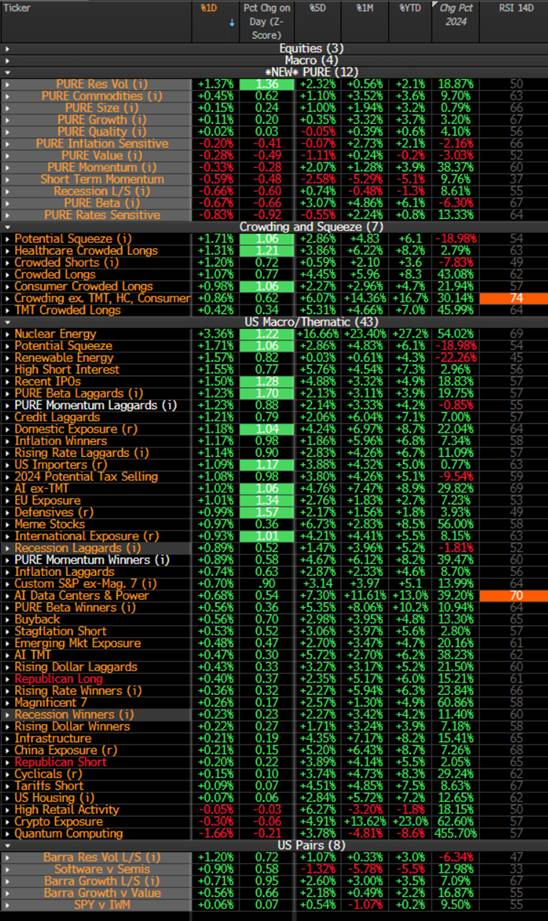

This is a valuable table for momentum-based short-term traders:

BY Doug Kass · Jan 24, 2025, 7:55 AM EST

From JPMorgan:

US: Futs are lower. MegaCap Tech were largely unchanged this morning; TSLA +57bp. Bond yields are flat, and USD is modestly lower. Commodities are mixed; precious metals are higher while Ags are mostly lower. Overnight, BOJ hiked 25bp, as widely expected; USD/JPY was mostly flat. Today, the key focus will be global PMIs and earnings, with AXP and VZ being the most important ones to provide further color on consumer demand and economic growth. Feroli expects PMI-Mfg and PMI-Srvcs to print at 50.0 and 57.0, largely in line with the Street estimates of 49.8 and 56.5, respectively.

and...

EQUITY AND MACRO NARRATIVE: Yesterday, equities finished at another all-time high amid healthy underlying price actions: 65% of SPX stocks finished higher, and SPX outperformed both NDX and RTY. Macro catalysts were mostly quiet: initial jobless claims were largely in line with expectations; Trump’s Davos speech did not provide many details on tariffs and reiterated several key agenda items we already knew. Overnight, BOJ hiked 25 basis points, in line with expectations, and pointed out that real interest rates still remain significantly negative. JPM Economist Ayako Fujita sees two additional rate hikes this year with the policy rate reaching 1% by year-end. Today, the key focus will be global PMIs and earnings, with AXP and VZ being the most important ones to provide further color on consumer demand and economic growth. Feroli expects PMI-Mfg and PMI-Srvcs to print at 50.0 and 57.0, largely in line with the Street estimates of 49.8 and 56.5, respectively.

BY Doug Kass · Jan 24, 2025, 7:45 AM EST

American Express AXP shares were +$4 in premarket.

After the company reported fourth-quarter results, the shares are now -$11.

BY Doug Kass · Jan 24, 2025, 7:25 AM EST

BY Doug Kass · Jan 24, 2025, 7:16 AM EST

Bonus — Here are some great links:

Post-Election Best Year Since 1985 Is Bullish

BY Doug Kass · Jan 24, 2025, 6:34 AM EST

The S&P Short Range Oscillator grew more overbought yesterday — moving from 3.23% to 4.73%.

Along with so-so breadth over the last two trading sessions and a drop to recent lows in the CBOE put/call ratio coupled with a rise in interest rates — one would think some sort of correction seems more likely.

That said, yesterday's late-day ramp (or jam!) was unsettling to the ursine crowd.

BY Doug Kass · Jan 24, 2025, 6:12 AM EST

Doomberg on the 'whiplash' of executive orders and the energy industry.

BY Doug Kass · Jan 24, 2025, 5:55 AM EST

Wolf Street howls about the collapse of solar stocks.

BY Doug Kass · Jan 24, 2025, 5:45 AM EST