After-Hours Trading

"Just one more thing."

- Lt. Columbo

I covered my Index shorts after the close for a breakeven on the trade rental:

* SPY at $606.00

* QQQ at $530.99

BY Doug Kass · Jan 22, 2025, 5:15 PM EST

"Just one more thing."

- Lt. Columbo

I covered my Index shorts after the close for a breakeven on the trade rental:

* SPY at $606.00

* QQQ at $530.99

BY Doug Kass · Jan 22, 2025, 5:15 PM EST

At 4:21:

BY Doug Kass · Jan 22, 2025, 5:00 PM EST

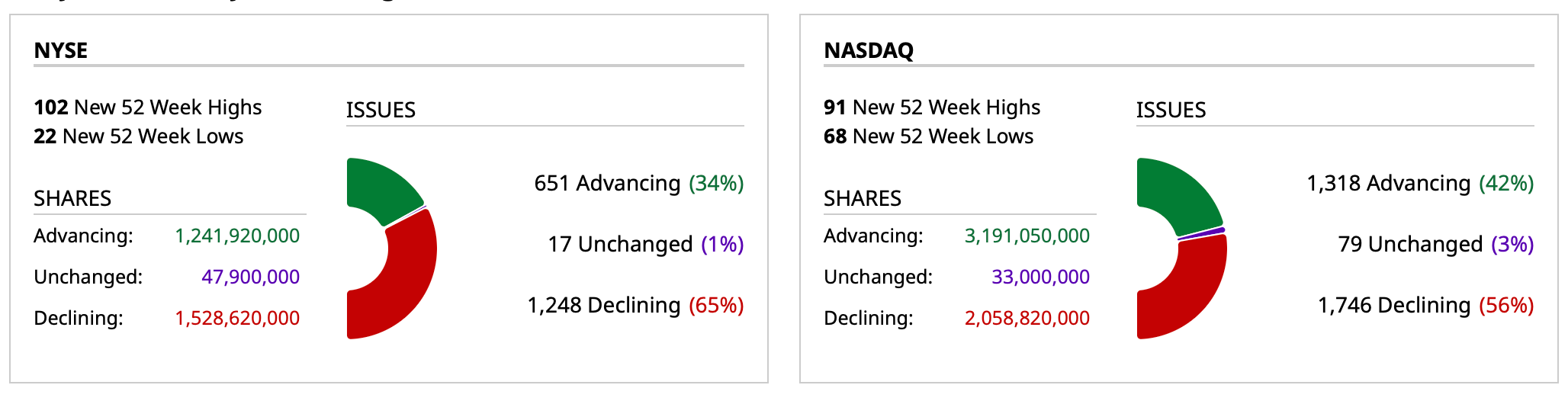

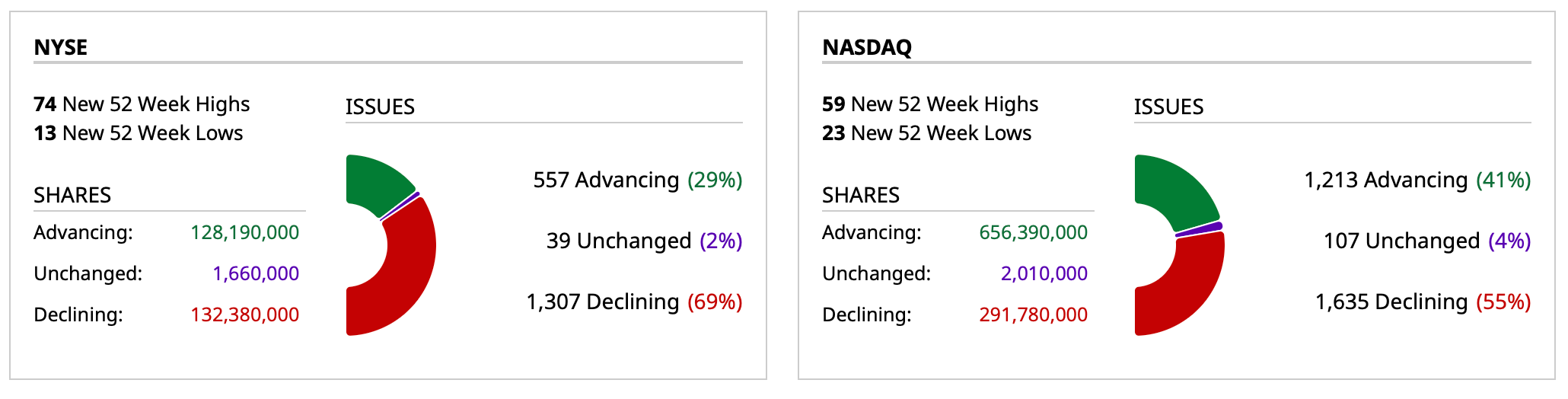

- NYSE volume 3% below its one-month average.

- NASDAQ volume 14% below its one-month average.

BY Doug Kass · Jan 22, 2025, 4:50 PM EST

I am still a bit sick so I am going to call it a day earlier than usual.

Thanks for reading.

Be safe.

BY Doug Kass · Jan 22, 2025, 3:46 PM EST

BY Doug Kass · Jan 22, 2025, 1:56 PM EST

BY Doug Kass · Jan 22, 2025, 1:49 PM EST

BY Doug Kass · Jan 22, 2025, 12:55 PM EST

BY Doug Kass · Jan 22, 2025, 12:28 PM EST

This article modifies my Promises, Promises post.

BY Doug Kass · Jan 22, 2025, 11:57 AM EST

- NYSE volume is 3% below its one-month average;

- Nasdaq volume is 13% below its one-month average;

- VIX: down 1.33% to 14.86

BY Doug Kass · Jan 22, 2025, 11:15 AM EST

BY Doug Kass · Jan 22, 2025, 11:00 AM EST

I have been averaging on a scale higher into more Index shorts:

Cost basis SPY $606.45 and QQQ $531.01

BY Doug Kass · Jan 22, 2025, 10:32 AM EST

The company expects stronger results in H2, despite recent consumer trends and FX rates making the balance of the year more challenging:

- Despite a 2-week global services outage, P&G achieved 3% organic sales growth in Q2, overcoming the disruption with strong late December customer orders ahead of early January merchandising events.

- The 2-week outage resulted in incremental costs of approximately $0.02 per share, mostly in cost of goods sold, impacting gross margin by 30 basis points and core operating margin by 80 basis points.

- P&G expects stronger results in the second half of fiscal year 2025, despite recent consumer trends and FX rates making the balance of the year more challenging; they remain committed to delivering within full fiscal year guidance ranges.

- Greater China organic sales declined 3% in Q2, a significant improvement from a 15% decline last quarter, indicating a trend back toward growth in this key market.

- SK-II in Greater China grew 5%, with strong performance during the 11/11 key consumption period and modest growth in travel retail, despite underlying market softness.

- P&G continues to invest in innovation across all five vectors of superiority, with successful product launches like Charmin Smooth Tear, Swiffer Power Mop, and Oral-B iO2 driving market share growth and expected to contribute to future revenue.

- The company remains disciplined in its portfolio management, making moves over the past year to strengthen its ability to generate U.S. dollar-based returns, including doubling down on product superiority and innovation plans.

- While first half results were below the guidance ranges set for the full year, P&G maintains its expectation of stronger results in the second half, supported by continued strategy execution and a strong innovation pipeline.

- P&G returned over $4.9 billion of cash to shareholders in the quarter, distributing $2.4 billion in dividends and repurchasing $2.5 billion in shares.

BY Doug Kass · Jan 22, 2025, 10:23 AM EST

Berkshire -$10/share today.

From yesterday:

BY Doug Kass · Jan 22, 2025, 10:22 AM EST

From Peter Boockvar:

As we'll possibly get tariff threats and possibilities each day/week, until we actually see details and what might actually happen, I'm not going to comment on it each time I hear something. That said, on the refresh of the 10% proposal on China, across the board, resulted in Chinese stocks trading down overnight and the yuan is a hair weaker. The FX market has really been the main absorber of the tariff comments, particularly with the Mexican peso and Canadian dollar in addition to the yuan.

As there is no data of significance overseas, I'll get right to some notable earnings comments.

From MMM which rose 4% after earnings:

For the full year they expect organic sales growth of 2% to 3%.

They said "the macro recovery continues to be uneven." They expect auto builds "to be slightly negative, but down 3% to 4% in Europe and the US, where we have better penetration and flat in China and up across Asia, where our content per vehicle is lower."

"Consumer electronics is expected to be up low to mid single digits and consumer discretionary spend remains soft, especially in the US where retail sales are expected to be relatively flat."

They saw strength in their aerospace business.

DR Horton traded down almost 3% as people focused on their discounting and lower margins:

"Our gross profit margin on home sales revenues in the first quarter was 22.7%, down 90 bps sequentially from the September quarter as expected due to higher incentive costs."

"Our incentive costs are expected to increase further on homes closed over the next few months, so we expect our home sales gross margin to be lower in the 2nd quarter compared to the 1st quarter. Our incentive levels and home sales gross margin for the full year of fiscal 2025 will be dependent on the strength of demand during the spring selling season, in addition to changes in mortgage interest rates and other market conditions."

Prologis, the largest industrial warehouse owner in the US and whose stock rallied 7% post earnings:

"In our business, the bottoming process across our markets continues to progress. Leasing in our portfolio accelerated following the US election and the pipeline has started the year at healthy levels...Looking ahead, we believe market vacancy is topping out and rents will inflect later this year."

They also saw rent growth in some of their international markets like Japan, UK, Southern Europe and Latin America...Customer engagement is improving and we saw a notable increase in activity amongst our larger global customers who often lead in the recovery of demand as we've seen in past cycles."

After a huge amount of Covid overbuild in their industry, they expect supply growth of industrial real estate to continue to slow dramatically "which will pave the way for rent growth."

From Keycorp, another bank seeing no loan growth:

"Average loans declined 1.4% sequentially and ended the quarter just north of $104 billion. The decline reflects tepid client demand, active capital markets, our disciplined approach as to what we're willing to put on the balance sheet, and the intentional runoff of low yielding consumer loans as they pay down and mature."

On some macro and where loan growth goes from here, "My personal view is that the economy is actually starting to accelerate a bit. My personal view is also that inflation isn't necessarily under complete control yet. It's also apparent that if we do have tariff policy, there'll be people kind of buying ahead on that from an inventory perspective. I'll give you a couple of other data points. Our M&A backlogs right now is about as large as it's ever been, and there's still a whole bunch of capital on the sidelines. So, for all those reasons, we think we will see loan growth."

"Non-performing assets are peaking, and assuming the macro environment remains constructive for the balance of the year, we expect non-performing loans to begin to decline by mid-year."

From Capital One:

"We delivered another quarter of top-line growth in domestic card loans, purchase volume and revenue. In the auto business, we posted growth in originations for the 4th consecutive quarter and the return to y/o/y growth in loan balances and consumer credit trends remained stable."

Here was their macro commentary, "So the US consumer continues to be a source of strength in the overall economy. The labor market remains strong and we saw signs of softening in the first half of 2024, but in the 2nd half of the year, the unemployment rate has been stable and job creation data has shown renewed strength. Incomes are growing steadily in real terms as inflation settles out a bit."

Some more, "Consumer debt servicing burdens are stable near pre-pandemic levels. Consumers have higher bank account balances than before the pandemic. Now, of course, the circumstances of individual consumers and households are highly variable and so talking in averages doesn't always fully cover what's going on. We do see some pockets, as I've been saying for some time now, we do see some pockets of pressure related to the cumulative effects of inflation and elevated interest rates among consumers whose incomes have not kept up with inflation or who have high debt servicing burdens. And of course, there's still some inflation pressure and longer term interest rates strikingly have increased since the Fed started lowering rates in September. So we do see a bit of a disconnect between the average consumer and the folks closer to the margin."

After a good quarter UAL said this, "Looking ahead to 2025 United sees robust demand trends in the first quarter with domestic RASM (revenue per available seat mile) expected to turn solidly positive y/o/y, as well as continued improvement in international RASM."

Their earnings call is this morning and we know travel, both leisure and business, has been pretty solid.

Netflix continues to rock and roll as it stretches itself further away from the competition but I didn't read anything macro other than they are raising prices again by about 15%.

Finally, with still the average 30 yr mortgage rate above 7%, purchases were flattish, up by .6% w/o/w while refi's fell by 2.9%. Always, mortgage apps fall at the end of the year and rebound in the first few weeks of the year even though the data is seasonally adjusted. Now though it normalizes.

BY Doug Kass · Jan 22, 2025, 10:00 AM EST

I just covered my Oracle ORCL trading short rental at $184.84 for a quick +$5+ gain in a few minutes.

BY Doug Kass · Jan 22, 2025, 9:39 AM EST

I have been scaling into small shorts in the indexes:

* SPY $605.75

* QQQ $529.47

BY Doug Kass · Jan 22, 2025, 9:30 AM EST

As noted in my Diary, I have been accumulating Procter & Gamble PG on weakness.

Good results this morning and the shares are +$5.

From Morgan Stanley:

Beat, Unchanged FY Guidance Positive Stock Reaction:

PG reported slightly above-consensus Q2 EPS of $1.88 vs the $1.87/1.86 VA/SA consensus, but OSG of 3.0% (un-rounded was also 3.0%) was better then the 2.5%/2.3% VA/SA consensus and the rounded 2% bar we think was in sentiment, which should be viewed positively. PG also kept FY OSG/EPS guidance, but given H1 OSG trends and incremental FX pressure on profit ($300M worse in FY guidance), we assume will acknowledge the low-end is more reasonable on the call.

With the $6.95 FY25 consensus already towards the low-end of PG's $6.91-7.05 implied range, the low-end should be viewed positively vs a group that is likely to have greater negative revisions, and lack of a full guidance (bottom-end) cut at PG. We do assume ad spend cutbacks are enabling FY EPS delivery, but this is not a big deal from our vantage point given much higher ad spend last year. Slight F2Q EPS but Solid OSG Upside: PG fiscal Q2 core EPS of $1.88 was slightly above the $1.87/1.86 VA/SA consensus, with a 1.4% reported topline beat and 0.9% gross profit beat (30 bps GM miss), but SG&A was 2.2% above consensus (20 bps higher as % of sales), driving roughly in-line (-0.4% below consensus) operating income. Gross profit was likely hurt modestly by Blue Yonder expenses, with FQ2 EPS upside driven by below the profit line items. Organic sales growth (rounded and unrounded) of 3% was ahead of the 2.5%/2.3% VA/SA consensus and market expectations. Organic volumes increased 2% vs consensus of +1.3%, pricing was flat vs the +0.7% consensus, and mix was +1% vs the +0.4% consensus. Organic sales growth of 3% was above the ~2.5% consensus and rounded 2% market expectation. The OSG CAGR vs a pre-Covid 2019 was +5.2%, slightly below +5.7% in F1Q25 and +6.0% in FY24. Core gross margins decreased 30 bps versus the prior year or 20 bps ex FX, with gross productivity savings of 150 bps, and 30 bps from pricing, fully offset by 110 bps of unfavorable mix, 50 bps of unfavorable commodity costs, 40 bps of product reinvestments and transportation services costs. PG likely modestly missed GM's on direct Blue Yonder costs and less ability to drive savings (indirectly). Core SG&A increased 50 bps yoy and 30 bps ex FX on a solid 210 bps of reinvestments, partially offset by 110 bps of productivity savings, 60 bps of net sales growth leverage, and 10 bps of other savings.

FY25 OSG and EPS Guidance Maintained, But We Would Expect the Low-End to Be Blessed on the Call Given FX is Now Expected to be Worse and Given H1 OSG

BY Doug Kass · Jan 22, 2025, 9:22 AM EST

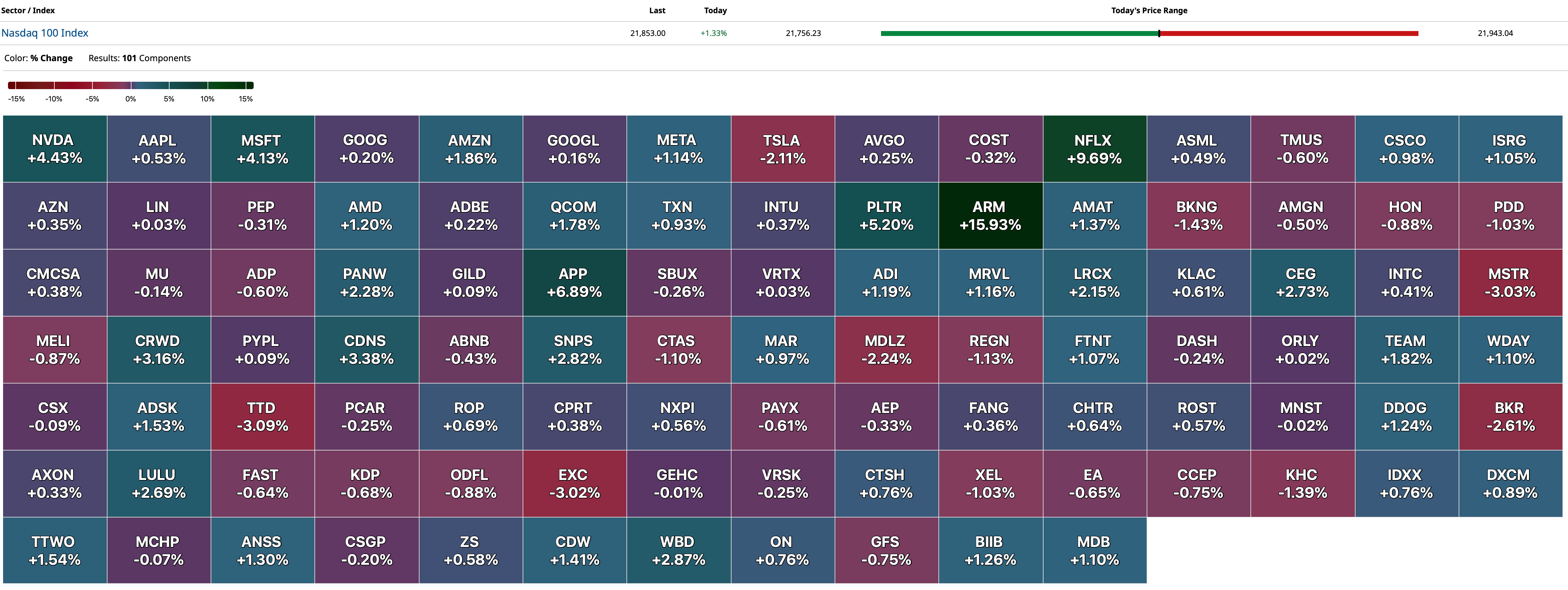

-NFLX +15% (earnings, guidance)

-MDAI +13% (anticipates reporting ARR exceeding its $28M market guidance)

-ORCL +11% (announces new AI agents and generative AI capabilities in Oracle Cloud Sales)

-USEG +10% (prices underwritten public offering of common stock at $2.65/shr)

-LOBO +9.9% (announces strategic collaboration with Roundtree Lab, LLC to manufacture advanced e-Hospital beds)

-ALLY +8.7% (earnings, guidance)

-SGHC +7.1% (reports prelim Q4 Rev, EBITDA)

-APTV +6.8% (to separate Its Electrical Distribution Systems Business; affirms FY24 guidance)

-STX +6.2% (earnings, guidance)

-TRV +5.4% (earnings, color)

-UAL +5.0% (earnings, guidance)

-APH +4.0% (earnings, guidance)

-IBKR +3.9% (earnings)

-OFG +3.4% (earnings)

-PG +3.3% (earnings, guidance)

-MP +2.0% (restores US production of NdPr and NdFeB magnets)

-LSTA -36% (reports preliminary Cohort A data from AGITG-led Phase 2 ASCEND trial evaluating Certepetide with Standard-of-Care Chemotherapy in Metastatic Pancreatic Ductal Adenocarcinoma)

-HUSA -21% (files to sell $4.4M registered direct offering)

-AGYS -20% (earnings, guidance)

-TXT -3.3% (earnings, guidance)

-IRON -2.5% (files to sell $200M proposed public offering of common stock and pre-funded warrants)

-JNJ -2.4% (earnings, guidance)

-PRGS -2.4% (earnings, guidance)

-CMA -2.2% (earnings, guidance)

-ABT -2.1% (earnings, guidance)

-CELH -2.1% (TD Cowen Cuts CELH to Hold from Buy, price target: $29 from $40)

BY Doug Kass · Jan 22, 2025, 9:22 AM EST

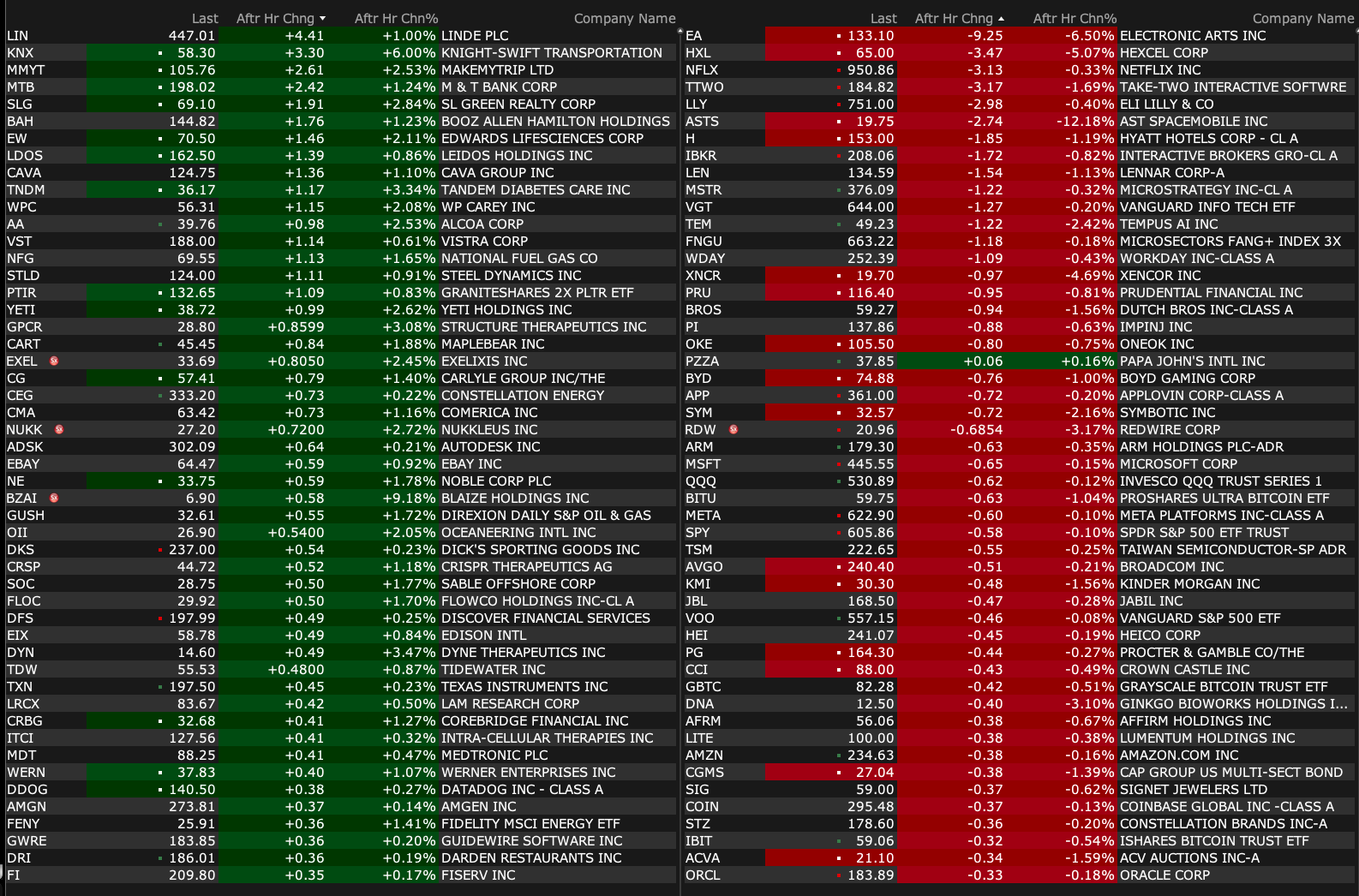

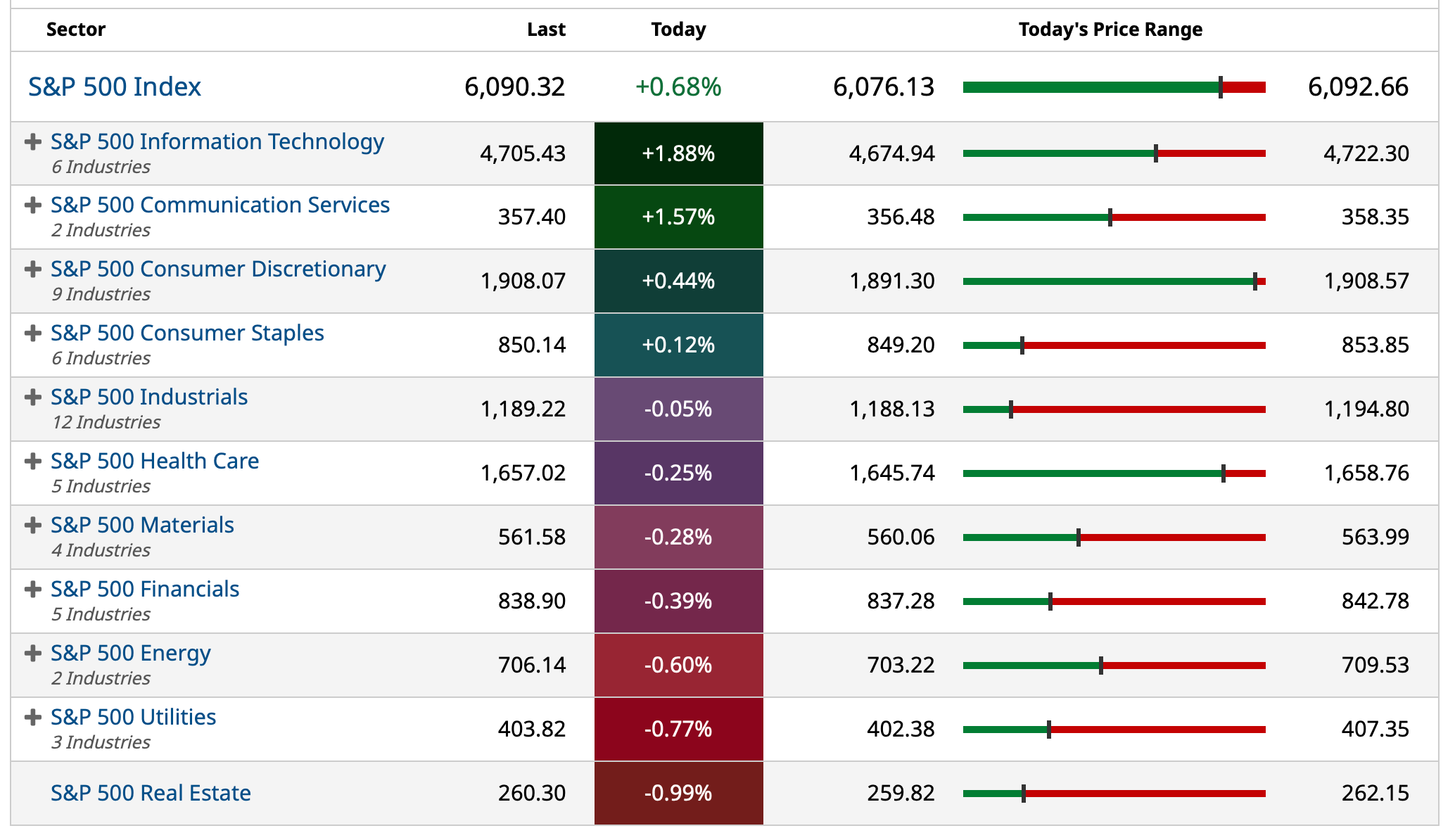

Chart from 8:40 a.m. ET:

BY Doug Kass · Jan 22, 2025, 9:15 AM EST

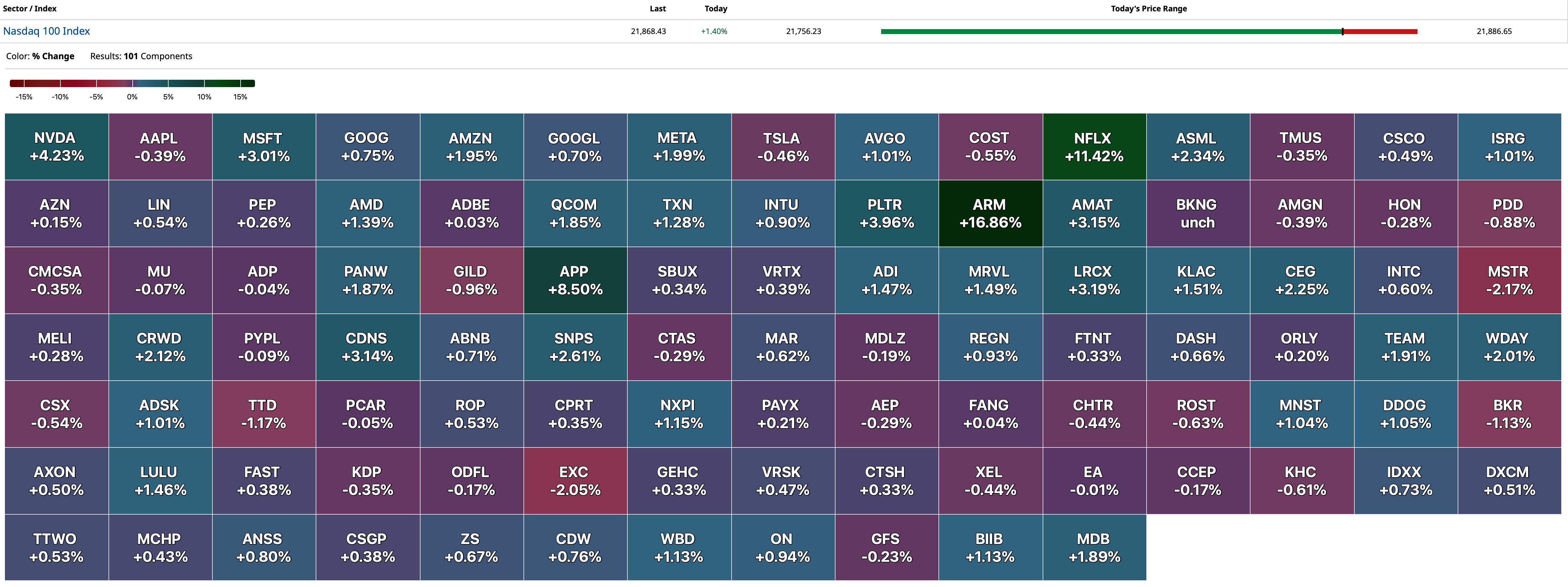

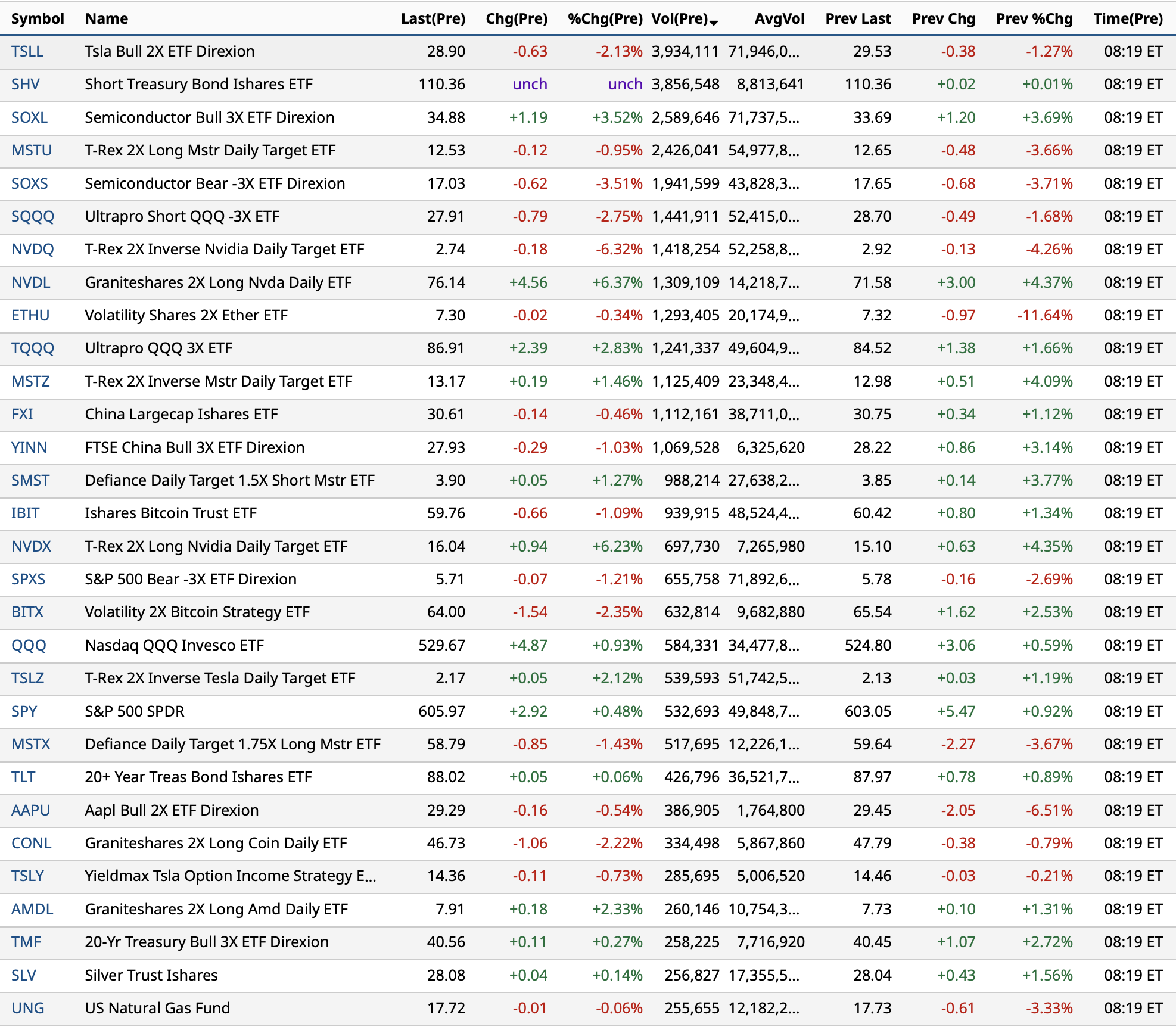

Most active premarket ETFs as of 8:19 a.m.:

BY Doug Kass · Jan 22, 2025, 9:05 AM EST

From my pal Anthony:

BY Doug Kass · Jan 22, 2025, 8:57 AM EST

BY Doug Kass · Jan 22, 2025, 8:45 AM EST

Today:

11:30 a.m: Treasury hosts a $64B 17-Week Bill Auction;

1:00 p.m.: Treasury hosts a $13B 20 Year Bond Auction;

2:00 p.m.: Treasury's Buyback (Liquidity Support)

BY Doug Kass · Jan 22, 2025, 8:28 AM EST

BY Doug Kass · Jan 22, 2025, 7:59 AM EST

Knowledge@Wharton on U.S. fiscal policy:

BY Doug Kass · Jan 22, 2025, 7:40 AM EST

BY Doug Kass · Jan 22, 2025, 7:00 AM EST

This is called a valuation reset:

BY Doug Kass · Jan 22, 2025, 6:50 AM EST

Bonus — Here are some great links:

The U.S. Is The Nicest House on the Block

BY Doug Kass · Jan 22, 2025, 6:35 AM EST

From JPMorgan:

US: Stocks finished higher led by RTY. Earnings and Trump’s agenda remain the focus for investors. SCHW rallied +5.8% on robust revenue growth and margin; XLF continued last week’s strong rally and added 84bp. Trump’s AI announcement drove a +7.5% rally in ORCL; SOXX added 1.5%. Price actions feel squeezy with High Short Interest and High Retail Activity all added over +3%. Post-market, NFLX soared 11% amid revenue beat and higher 2025 revenue guidance

and...

EQUITY AND MACRO NARRATIVE: Earnings and Trump’s agenda remain the focus for investors today. Robust Q4 results, from banks to NFLX today, supported the view of above-trend Q4 growth in the US and drove equities higher.

· NFLX EARNINGS FIRST TAKE (JACK ATHERTON) - NFLX (+10% post): Subscriber Smackdown! Netflix going out with a bang on subs reporting (+18.9m vs whisper +12-13m)... raising 2025 revenue and OPM guide despite the FX headwinds... announcing price adjustments to “most plans” in US, Canada, Portugal and Argentina... and board has approved another $15B buyback.

o Q4: +18.9m paid adds (whisper +12-13m). Geographically: UCAN +4.8m vs St +2.0m, EMEA +5.0m vs +2.9m, LATAM +4.2m vs +1.4m, APAC +4.9m vs +2.5m. Revenue $10.25b (+19% FXN) vs guide $10.1b, OPM 22.2% vs guide ~21.6%, and FCF $1.38b vs St $1.06b.

o Q1 Guide: Revenue $10.4b (+14% y/y FXN) vs buyside looking for ~$10.5B (St $10.6%), OPM 28.2% vs St 29.6%. Co no longer guiding/reporting subs so this is kinda irrelevant but i’ve heard buyside expects ~5-6m.

o 2025 Guide: Guiding to $43.5-44.5b (+14-17% FXN) based on FX at 1/1/25, prior guide was for $43-44b (+11-13%). Raising the OPM guide too to 29% (prev 28%) despite the FX headwind. Guiding to $8B 2025 FCF (St $8.5B).

· ENERGY – Trump made several executive orders on energy, including (i) “Unleashing American Energy” (here) and (ii) “Declaring a National Energy Emergency” (here). The supply side policies and tariff risks weigh on oil prices today with WTI and XLE losing -2.6% and -64bp, respectively. Despite this aggressive move, we remain the view that structural tailwinds to US producers from Trump’s pro-oil and gas policies could be limited as (i) fundamental/economic signals remain the primary driver for production guidance, rather than policy incentives; (ii) the current restrictions on drilling only impact about 16% of total US oil and gas production, per Natasha. In other words, even if Trump lifts all restrictions, it is less likely to materially change the production outlooks. Overall, we do not view Trump’s victory to be a structural tailwind for the energy sector given the mixed outlooks on oil prices in 2025.

THOUGHTS ON STARGATE (JOSHUA MEYERS)

· A few hours ago, CBS reported that this afternoon Trump will announce “billions of dollars in private sector investment to build artificial intelligence infrastructure in the US in a joint venture by OpenAI, Softbank and Oracle called Stargate.” Heads of these three companies will attend a White House meeting with Trump today to announce the “$100b investment which could scale up to $500b over the next four years.”

· From Oracle’s perspective, Jack views it as a Trump “headline-grabber,” rather than something we’re putting in our models. It follows the recent $100B, 4-year Softbank-led US investment announcement and Trump’s $20B DC investment announcing coming from the Middle East. Jack: “What many are focused on is the implications that there could be a deeper partnership brewing between OpenAI and Oracle… I won’t confess to have any insight here but I continue to think that Microsoft & OpenAI are wedded to each other at this stage. OpenAI needs capital, infrastructure & distribution (which Oracle can really supply at this stage); Microsoft needs AI tech and an anchor AI customer for Azure. This is a clearly a fast evolving space that we’ll need to pay attention to but the 7% ORCL-MSFT spread feels like a lot to me.”

· And here’s what I’ve pieced together on the hardware side from news and conversations:

o A few clients with long memories noted that last March Reuters reported “Stargate” as a $100b project between MSFT and OpenAI, with a 2028 launch schedule. This was meant to be the 5th phase in their cooperation, and the biggest supercomputer the two would produce together. Reuters reported that “the new project would be designed to work with chips from different suppliers” (italics are mine). The Information reported something similar at that time, but made it sound like it was contingent on certain OpenAI performance milestones, and might use custom ASIC. And a TechRadar article reported the project was specifically to “reduce the two companies’ reliance on Nvidia”(italics mine).

o Lots of folks asking… would they start with NVDA chips? Seems they would have to if they wanted to launch soon (given new political imperatives). We believe OpenAI has been working with AVGO on an ASIC, but they’re 12~18 months away from production, at a minimum. Ditto Softbank, which is even farther behind. And no, ORCL does not have any ASIC programs that we are aware of.

o Folks also nothing that $100b incremental capex potentially helps ease concerns around 2026 AI capex. Good signal for chip demand, but obviously depends a lot on the timetable. Of course, this still only tells the story of datacenter capex, not of real end-demand.

o Are there implications of a deeper partnership between OpenAI and Softbank? Do OpenAI and Softbank still each produce their own ASICs, or do they cooperate on one? (One less chip is one less opportunity for AVGO/MRVL). And remember, Softbank owns ARM.

BY Doug Kass · Jan 22, 2025, 6:25 AM EST

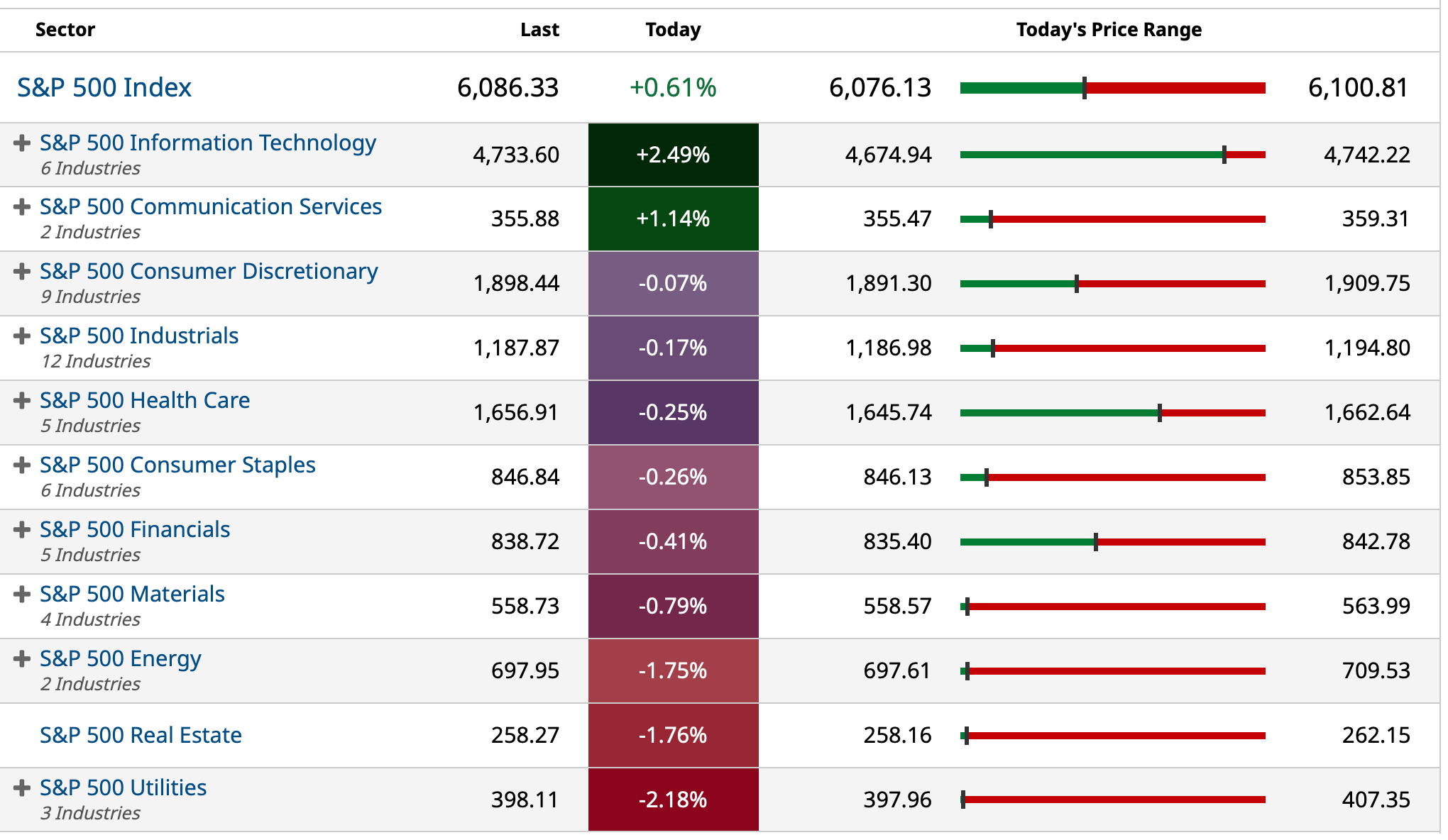

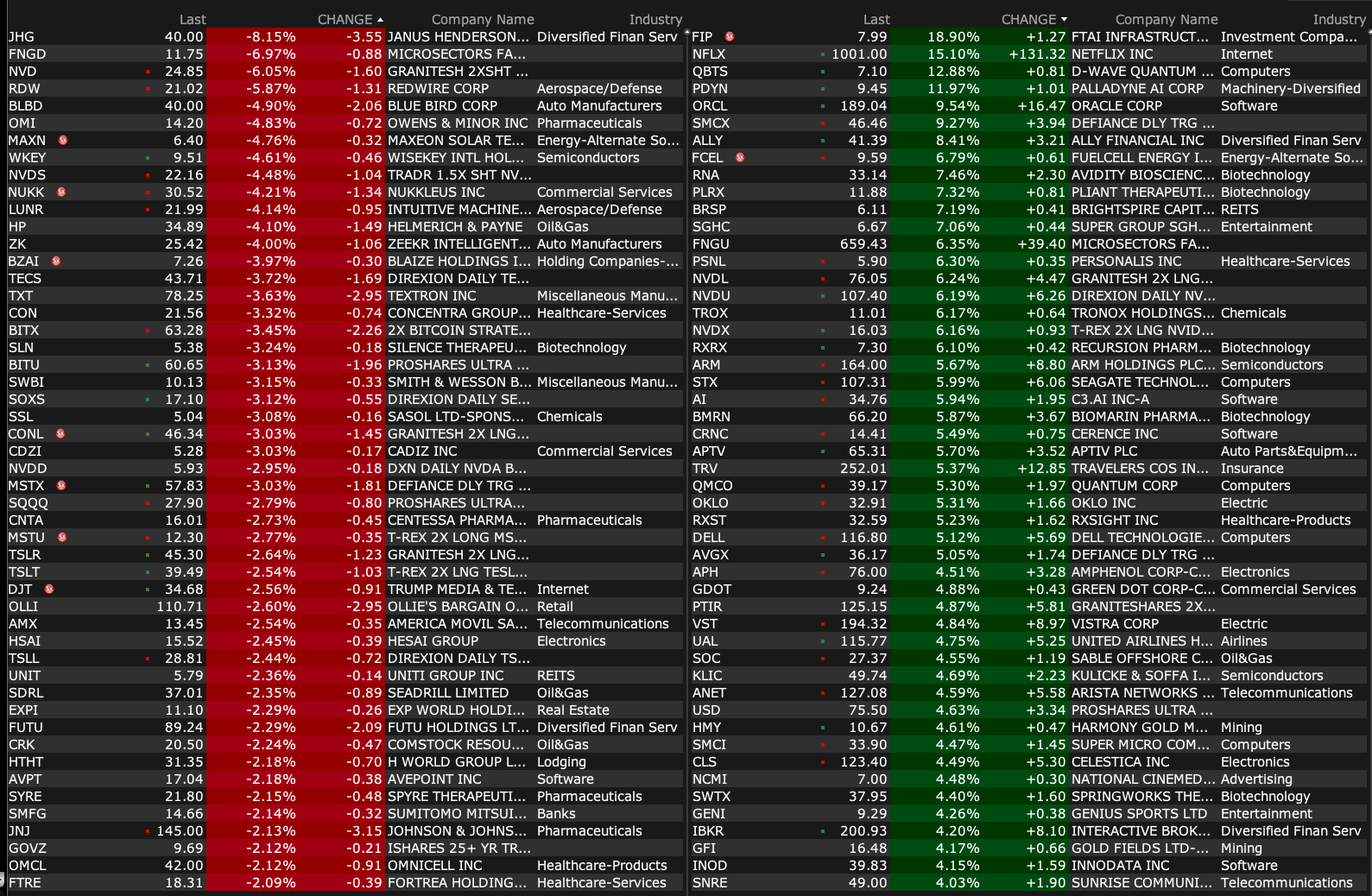

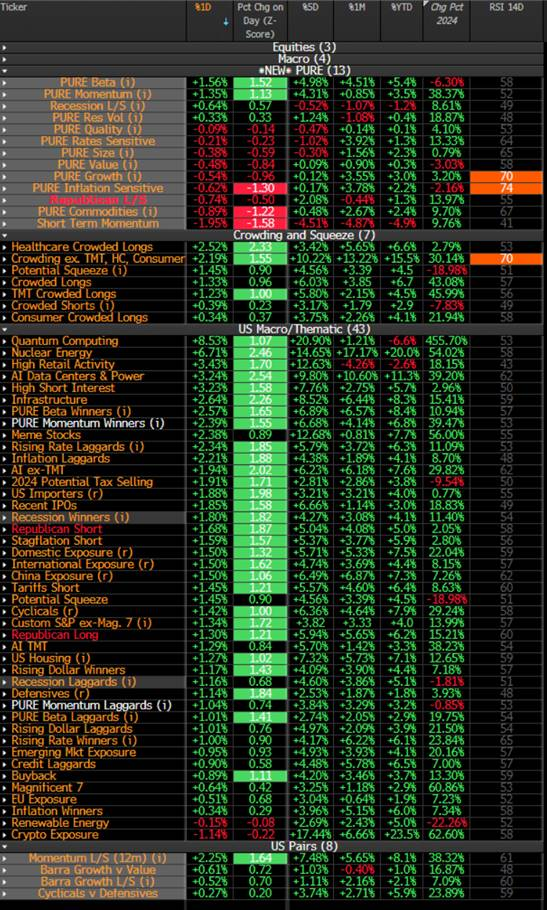

This is a valuable table for momentum-based short-term traders:

BY Doug Kass · Jan 22, 2025, 6:15 AM EST

The S&P Short Range Oscillator rose from 2.64% to 3.3% — representing a further overbought.

BY Doug Kass · Jan 22, 2025, 6:05 AM EST

In the very early going (around 4:15 a.m.):

* I took a trading short rental in ORCL ($187.43) — see first post.

* With SPOOs +30 handles, I shorted SPY $605.75 and QQQ $529.35.

BY Doug Kass · Jan 22, 2025, 5:55 AM EST

* With "animal spirits" high and in these new eras — announcements of capital commitments to technology seem to be enough for the investment community (who don't wait around for the inevitable failure to follow up).

* Never let the truth get in the way of a good story.

* Here we go again — the bubble grows (on the way to bursting) in a backdrop of share-price momentum, limited analysis and in the absence of questioning...

Promises, promises

I'm all through with promises

Promises now

I don't know how

I got the nerve to walk out

If I shout

Remember, I feel free

Now, I can look at myself

And be proud

I'm laughing out loud

Oh, promises, promises

This is where those promises

Promises end

- Burt Bachrach and Hal David, Promises Promises

Never let the truth get in the way of a good story.

A lot of hoopla.

A lot of promises about President Trump "marketing" AI investments and how it is going to drive the U.S. economy:

and

By the way, the same idle promises (and B.S.) were made by President Clinton at the end of the dot-com boom — regarding large government expenditues and how it would help drive the U.S. to economy prosperity and deliver large productivity gains:

BY Doug Kass · Jan 22, 2025, 5:45 AM EST