The dumb conversation about Trump and Melania meme coins on CNBC reminded me of the lame CNBC interview with Sam Bankman-Fried a month before he went to jail.

(In this fourth part of a four-part post that looks at a potential January top, we continue a compilation of recent commentary in my Daily Diary on the TheStreet Pro and comments delivered to my investors at my hedge fund, Seabreeze Partners.)

What We Failed To Expect in 2024

"A mistake that people often make is they compare themselves with others who are making more money than they are and conclude that they should emulate the others’ actions...after they’ve worked. This is the herd behavior that so often gets them into trouble."

- Howard Marks

"We derive no comfort because important people, vocal people, or great numbers of people agree with us. Nor do we derive comfort if they don't. A public opinion poll is no substitute for thought."

- Warren Buffett"

With the benefit of hindsight -- "animal spirits" and the fear of missing out -- were the key factors that contributed to the 2024 reset in valuations. Specifically, about $1 trillion of inflows into equity mutual funds/ETFs and an equivalent amount of company share buybacks spurred the advance in price earnings multiples.

I did not expect such a strong reset in valuations in the face of limited changes in profit expectations.

January 2025 Resembles January 1973

The conditions that exist today remind us of an important market top that took place in January 1973.

Like 52 years ago, today we face a combative President (Nixon/Trump), market leadership is narrow (it was The Nifty Fifty in the early 1970s and The Magnificent Seven in recent years), interest rates and inflation have turned up (from the prior few decades) and public sector debt has been climbing rapidly. Also, like in 1973, we lack visibility today with regard to any fiscal discipline by our government.

In both periods, the forward price-to-earnings was extremely elevated (today, at 23x, in the 96%-tile), the market advance was not broadening out, the "animal spirits" took stock prices higher without a commensurate change in future profit forecasts, and the equity risk premium was paper thin.

An epic market top was completed in January 1973 — leading to a poor year for the S&P Index, which marked the beginning of the end of the Nifty Fifty and several years of weak performance in the Indexes.

I expect something similar in January 2025 — an important market top, a down year for the averages and marked by the beginning of the end of the Mag 7, which could extend multiple years.

The Unexpected and Leveraged Corners of Speculation

* As we have already noted, the entirety of the recent market advance has been based on an expansion in price earnings multiples.

* As narratives multiply and fear/doubt disappear, guards and disciplines are dropped with many asset classes at all-time highs.

* But as asset prices rise, diligence and the assessment of reward vs. risk should take on greater irrelevance – unfortunately, just the opposite is occurring.

* And so should the concept of "a margin of safety" be evermore embraced - as it is an essential and integral ingredient to investing over a "market cycle."

* Expect the unexpected...in the corners of leverage and those that are endorsing the narrative of a "new paradigm" (of higher valuations).

Over history, market inflection points and economic dislocations often come from places not anticipated. Indeed, the most important turning points in markets (and in life) often come at the most unexpected times and in the most unexpected ways. In particular, leverage, as proven by history, is often uncovered in unexpected places. Think about the collapse of a generally unknown currency, the Thai Bhat that gripped Asia in 1997 and then spread to other countries (with a ripple effect), raising fears of financial contagion and a worldwide economic meltdown. Or the failure of the highly leveraged (and formerly successful) Long Term Capital hedge fund (managed by several Nobel Prize winners in economics) in the following year -- which was, in part precipitated by the Russian Debt crisis in 1998 and required a multibillion-dollar bailout by 14 banks (orchestrated by The New York Federal Reserve). But the best example of hidden leverage (where no one was looking) was seen in The Great Financial Crisis of 2007-09 when one overleveraged segment, real estate, proved to be the Achilles Heel for the global economy.

Indeed, what started out as what many believed to be only a few California mortgages underwater, multiplied geometrically and almost bankrupted our worldwide financial system -- as the layers of leverage were swiftly uncovered and spread rapidly.

Today’s commentary will highlight several significant market (and economic) risks that are not regularly discussed. The "failure" or combustion of any of these factors could have an adverse impact on equities and the domestic economy:

* The U.S. economy has never been more levered to the U.S. stock market. Indeed, one can argue that -- with household ownership of equities at an all-time high, with a chorus of "it’s different this time" and with dreams of a new investing paradigm (of higher valuations) dominating the narrative. As discussed below, it is almost as if the domestic economy is being collateralized by a foundation asset, equities.

From Tom Dyson:

"The US stock market is such a foundational asset. You could say, the US stock market has become the collateral that backs the world economy, and all its debt. As long as the stock market keeps rising, everything’ll be okay. But as soon as it turns down, things will start breaking. Employment, real estate values, consumption, trade… and even the government’s finances. It’s the wealth effect, when the stock market is such an important store of wealth. They all rely on a strong stock market to function. The fact that the world’s prosperity has one single point of failure – even as it rises day after day – should terrify you. The market’s function should be to allocate scarce capital efficiently… not collateralize the entire system. In effect, it’s become too big to fail, which is an acute fragility for our capitalist system. As allocators of capital ourselves, how should we approach our investment discipline in a market where expectations (and stock market values) are literally “off the charts”? The bears say "every other time this has happened, there's been a big wreck." The bulls say "this time is different, and besides, the trend is your friend and getting the timing wrong is the same as being wrong. “What do you do? Neither position is falsifiable. Which means there is no way to figure out the correct answer with logic… or research… or data. So it comes down to philosophy. Are you a contrarian? Or are you a trend-follower?... The global debt stock surged by over $12 trillion in the first three quarters of 2024 to a record high of nearly $323 trillion. It’s a huge wealth bubble and when it pops, $400 trillion or $500 trillion of (mostly) paper claims ($323 trillion in debt plus whatever owners’ equity the system has) will rush for the exits and seek safety. And policy makers won’t be able to stop it."

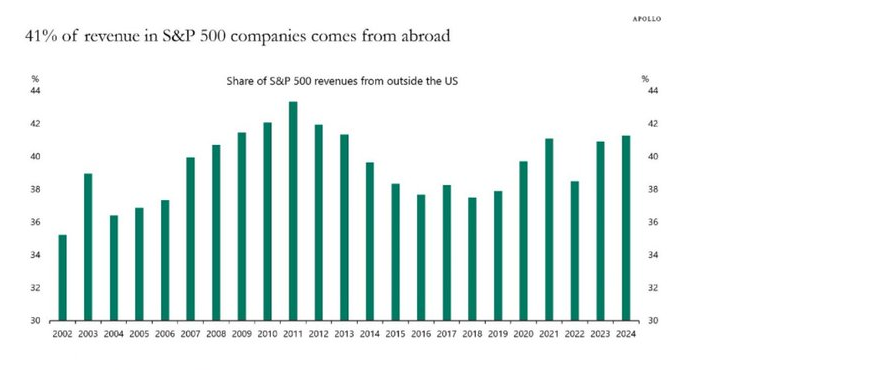

* No country is an island. The current narrative is that the outlook for the U.S. is great but the outlook for Europe, UK and China is not good. The problem with this optimistic line of thinking is that over 40% of revenues in the S&P 500 come from abroad:

* Elon Musk's health and business/innovative successes are critical to a continuation of economic growth and stock market gains. Musk's broad reach -- on the road, underground, in space, over the internet, in defense, in artificial intelligence -- has now advanced into Washington, and in the formulation and implementation of policy. To have one person so immersed and involved in all these critical areas could pose broad risks -- in many ways.

* An extremely leveraged cryptocurrency market represents potential systemic risks. It is my view that cryptocurrency is "the mother of all bubbles" perpetuated by a number of factors (including the rejection of fiat money) and developing digital narratives -- many of which have a weak foundation of logic. The absurd notion that the limiting of supply of bitcoin is as stupid as it is damning -- as there is no limit to the supply of other cryptocurrencies. To us, the sheer market size of Bitcoin and other cryptocurrencies is a manifestation of the risks.

When the cryptocurrency markets implode, which is my baseline expectation, the contagion effect will likely be pronounced on all of the capital markets.

* Both fiscal and monetary policy - which is needed to secure the foundation of growth -- are travesties. Neither political party has been fiscally responsible -- the profligate spending over the last few decades continues apace. (I do not, in any way, buy Elon Musk's objective of cutting $2 trillion from the U.S. budget, as when you go over the numbers only about $1.5 trillion can be cut (and that is if one cut all that was "available" to be cut in total). As well, the Federal Reserve has been guilty of reckless, feckless, and fatuous policy in its delayed response to inflation and then, in effecting a rapid rise in interest rates. I have little confidence in Powell's Fed steering clear of debris in his remaining time at that institution. Nor am I confident in any Fed chairman that might replace him.

* Changing market structure poses a significant market risk. Passive investing has engulfed the stock market landscape. We are all traders now, on the same side of the boat and worshiping at the altar of price momentum.

Massive inflows into passive strategies and products have been the straw that has stirred the market's drink. In part, those inflows, have contributed to a near-unprecedented narrowing in the equity risk premium (to 20-year lows) while the risk to earnings growth is at 20-year highs:

I can guarantee you (and history has proven) that these inflows -- as well as FOMO and the animal spirits -- will also not be permanent conditions. And when market momentum is broken and inflows turn into outflows, markets will likely suffer more meaningfully than most investors expect.

Bottom Line

As we enter the new year, we are of the view that stocks are increasingly vulnerable.

Specifically, we estimate that the market’s downside is probably between 2-times to 3-times the upside.

Despite heady valuations, the short-term headwinds are multiple, and the intermediate-term and other existential risks are considerable and growing.

On the latter point, as the New York Times columnist Ezra Klein writes today about existential (society) risks:

"Donald Trump is returning, artificial intelligence is maturing, the planet is warming, and the global fertility rate is collapsing.

"To look at any of these stories in isolation is to miss what they collectively represent: the unsteady, unpredictable emergence of a different world. Much that we took for granted over the last 50 years — from the climate to birthrates to political institutions — is breaking down; movements and technologies that seek to upend the next 50 years are breaking through.

"Any one of these challenges would be plenty on its own. Together they augur a new and frightening era. I find myself returning to a famous translation of a line from Antonio Gramsci: “The old world is dying, and the new world struggles to be born: Now is the time of monsters.”

That said, and as I have discussed in the past -- I am fully cognizant that short selling preserves capital (in tough times) and long buying creates capital (in good times).

As I have reminded my investors and our subscribers in the past, our cautious investment stance -- leading to a portfolio consisting of pairs trades and a sliver of a net short exposure -– is not permanent by any means. Equities tend to rise most of the time and being long has an inherent advantage over being short. (Longs theoretically have no limitation to the upside in percentage terms, while shorts can only return 100% (upon bankruptcy).

If I am correct in our ursine view, a top-heavy technology-based Mag7 led market should soon begin to topple, finally providing us with some long opportunities in the months ahead (or even sooner).

(What follows is more from my compilation of recent commentary in my Daily Diary on the TheStreet Pro and comments delivered to my investors at my hedge fund, Seabreeze Partners as we look at a possible January top).

Stocks Remain Defiant in the Face of Higher Yields and Sticky Inflation

Most recently interest rates have climbed much higher than consensus expectations - with the yield on the 10-year Treasury note approaching 4.75%, a multiple-month high.

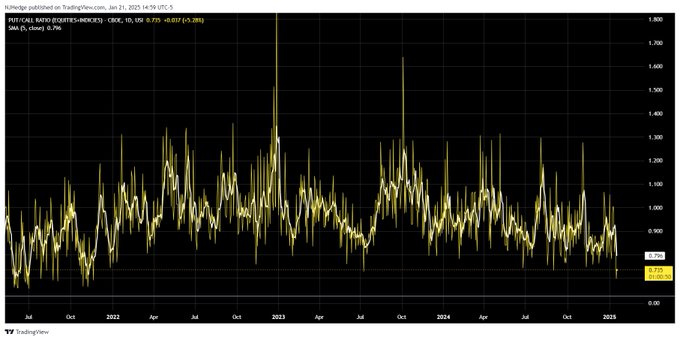

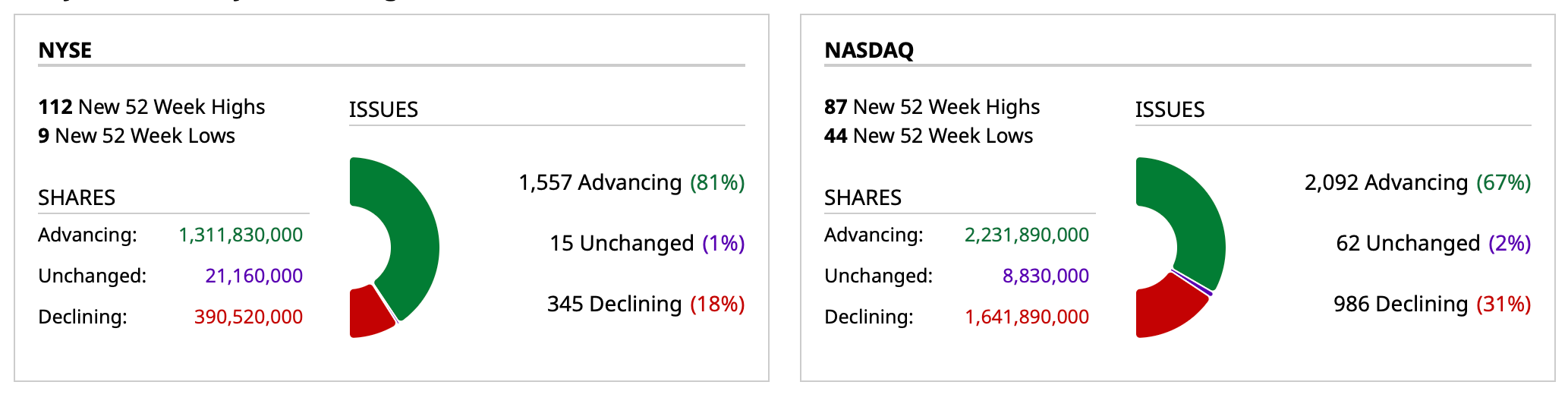

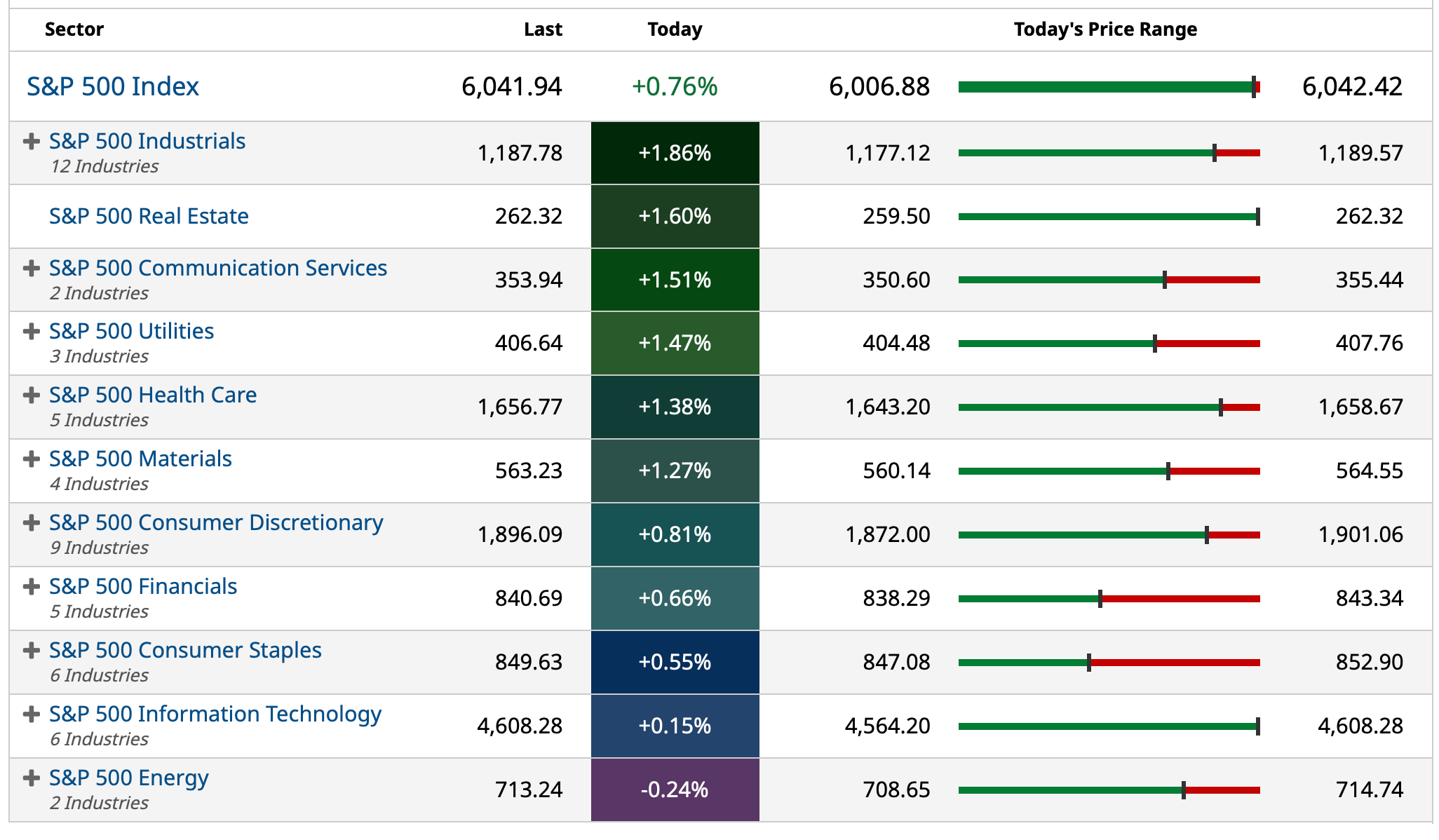

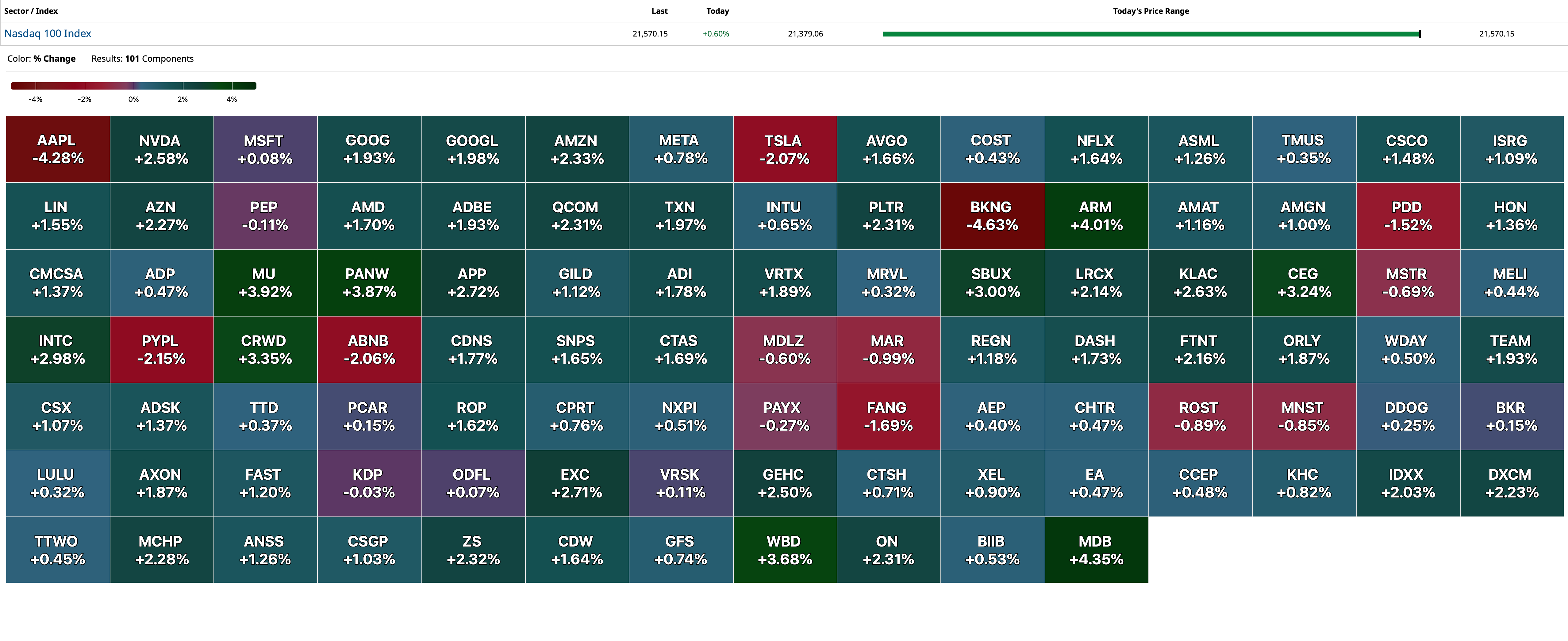

Investors have continued to ignore the signposts of continuing inflation:

Source: Hedgeye

The recent disaster in Los Angeles will likely serve to exacerbate inflationary pressures - as building material prices rise and insurance premiums are poised to take off.

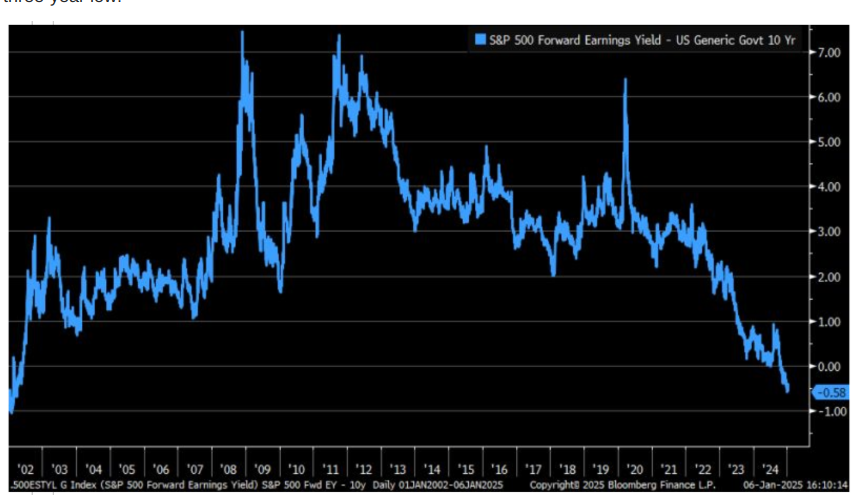

Importantly, the increase in interest rates and the absence of a more favorable EPS backdrop have contributed to an ever-thinning equity risk premium - in which the spread between the S&P Index's forward earnings yield and the ten-year Treasury yield has reached a twenty-three-year low:

David Rosenberg provides a succinct explanation to high valuation and for the equity market's indifference to the mounting concerns of sticky inflation, rising interest rates and other possible negative outcomes:

"Because I believe that earnings growth estimates are too lofty, even with the AI craze and how it will change the world, and because I believe that the ERP should be above zero (as risky assets should command a risk premium against riskless assets), I am still largely on the sidelines. I also believe that by the time the top is turned in, there will be a mad scramble to get out because the two extreme primal emotions of investing, fear and greed, never go out of style. Greed has been working, and may continue to work in 2025, but nothing lasts forever.

The problem is that because there is so much overexposure to equities on household balance sheets, everyone is going to be trying to bail out together with precious few buyers on the other side, because there aren’t exactly a whole lot of folks out there with a cash position like mine (oh, save for Warren Buffett… the two of us will be there, rest assured, to provide liquidity when the time comes). I don’t know when that time will be, but I do know it will come."

For now, it is clear that investors have lengthened their time horizons amid a perceived shift in the technology and productivity curves. This has meant that historical analysis of classic short-term valuations has not worked.

However, we can say with a fair degree of certainty that we don't expect this to be a permanent condition.

(What follows is more from my compilation of recent commentary in my Daily Diary on the TheStreet Pro and comments delivered to my investors at my hedge fund, Seabreeze Partners as we look at a possible January top.)

Other Cautionary Signs Pose Near-Term Risks

Besides the greatest degree of optimism that has prevailed since 2022, extended valuations, the likelihood that some (much?) of the appreciation in equities stems from automated buying by Index investors (without regard for their intrinsic value) and the multiple factors discussed in recent months -- there are other cautionary signposts:

* The enthusiasm surrounding quantum computing and AI.

* The implicit assumption that the constituents of the Magnificent Seven will continue to be successful.

* The relative valuations of US stocks compared to the rest of the world.

* Though unrelated to equities, the price of bitcoin (regardless of worthiness) has risen by over 450% over the last 24 months - this obviously doesn't suggest an overabundance of caution!

Looking Back on the Year

What differentiates our hedge fund, Seabreeze, from many "long/short funds" is that, in times of market concern, we run a bona fide "hedged" portfolio.

Most of the larger "long/short" hedge funds have abandoned short selling of individual equities altogether for a variety of reasons - not the least of which is that they can't get scale on the short side in specific names. Instead, these Funds often resort to shorting Indices, if they do anything on the short side at all.

As many recognize by now, I am as comfortable being short as being long.

A closer examination of our short book should make our differentiated approach apparent. We don't seek drama and beta in our shorts. Rather, we typically focus on non-crowded shorts (in which the short interest as a percent of float and average daily trading volume are low).

We don't short valuations. Our short selection is based on a bottom-up analysis; it's most often an assessment that companies' business models are deteriorating or broken relative to consensus expectations.

Here are examples of some of our individual shorts that we have held throughout most of the year:

The Coca-Cola Company KO, Starbucks SBUX, Chegg CHGG, Winnebago Industries WGO, FIGS FIGS, Medical Properties Trust MPW Blackstone Mortgage Trust BXMT, Inc, Sleep Number Corporation SNBR, Aegon AEG, Walgreens Boots Alliance, Inc. WBA, (now covered), Warner Bros. Discovery WBA, F45 Training Holdings Inc. FXLV, Petco Health and Wellness Company WOOF, B. Riley Financial RILY and Intuit INTU.

Our short book is hardly a "who's who" with regard to familiarity by most investors! You won't see a Mag7 short in our holdings. By staying away from high-risk popular and crowded shorts - despite the market's sea of green in 2024 -- our individual equity shorts contributed positively to last year's investment returns.

Price Is What You Pay, Value Is What You Get

"What the wise man does in the beginning, the fool does in the end."

- Warren Buffett

" A bull market is like sex, it feels best just before it ends."

- Barton Biggs

It should not come as a surprise that the return of an investment is significantly a function of the price paid for it. For that reason, investors clearly shouldn't be indifferent to today's heady market valuations.

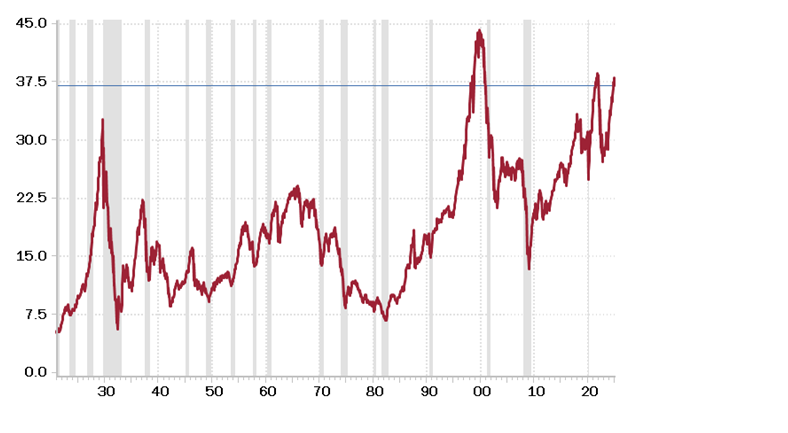

As expressed earlier, equities begin 2025 at an historically high level. The CAPE price-to-earnings multiple Cyclically adjusted price-to-earnings ratio (Wikipedia) developed by Yale University's Bob Shiller (I have lectured in his class since 2011!) is at 37-times, having expanded from 32-times a year ago and 27-times two years back. The last time valuations were so high was at the beginning of 2022 -- a year in which the S&P Index fell by 20%. Before the CAPE was that high in 2001 -- the start of a major Bear Market. In fact, in the last century the CAPE multiple has been this high only three percent of the time -- making the current ratio a 2.3 standard-deviation event.

S&P 500 CAPE Multiple

United States (ratio)

Shading indicates recession; Source: Haver Analytics, Robert Shiller, Rosenberg Research

Historically, a high CAPE is a launching pad for inferior returns:

United States

Source: Bloomberg, Rosenberg

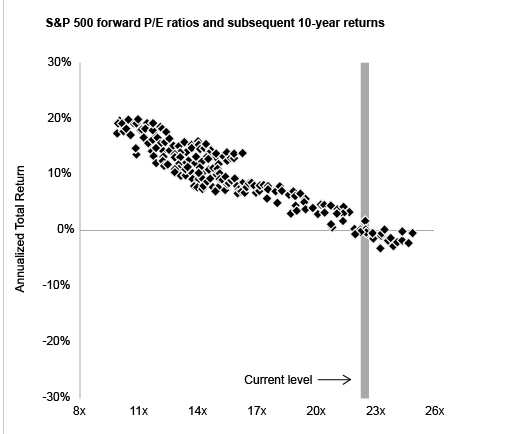

My friend, Oaktree's Howard Marks recently discussed this subject in one of his memorandums:

The above graph, from J.P. Morgan Asset Management, has a square for each month from 1988 through late 2024, meaning there are just short of 324 monthly observations (27 years x 12). Each square shows the forward p/e ratio on the S&P 500 at the time and the annualized return over the subsequent ten years. The graph gives rise to some important observations:

There’s a strong relationship between starting valuations and subsequent annualized ten-year returns. Higher starting valuations consistently lead to lower returns, and vice versa. There are minor variations in the observations, but no serious exceptions.

Today’s p/e ratio is clearly well into the top decile of observations.

In that 27-year period, when people bought the S&P at p/e ratios in line with today’s multiple of 22, they always earned ten-year returns between plus 2% and minus 2%.

In November, a couple of leading banks came out with projected ten-year returns for the S&P 500 in the low- to mid-single digits. The above relationship is the reason. It shouldn’t come as a surprise that the return on an investment is significantly a function of the price paid for it. For that reason, investors clearly shouldn’t be indifferent to today’s market valuation.

You might say, “making plus-or-minus-2% wouldn’t be the worst thing in the world,” and that’s certainly true if stocks were to sit still for the next ten years as the companies’ earnings rose, bringing the multiples back to earth. But another possibility is that the multiple correction is compressed into a year or two, implying a big decline in stock prices such as we saw in 1973-74 and 2000-02. The result in that case wouldn’t be benign.

This post that looks at a possible January top will be spread throughout the morning and early afternoon in four parts.

* The equity risk premium is at a two decade low - thus, stocks are materially overvalued relative to bonds.

* Almost every other traditional valuation metric is above the 95%-tile.

* The promises of a new Administration (deregulation, pro growth economic policies and lower corporate/individual tax rates) have been fueling the animal spirits since the November election.

* As well, the dominance of passive investing products and strategies (that worship at the altar of price momentum) have, in turn, propelled equities higher as that momentum builds.

* Company buybacks have added to investors' glee and upwards price momentum since early 2024.

* Nonetheless, based on history, today's valuations (statistically) represent a very poor launching pad for future equity returns.

* January 2025 (the end of The Nifty Fifty) resembles January 1973 (the possible end of The Magnificent Seven) in so many ways.

* Unexpected corners of speculation and leverage could lay the ground for a more significant market decline (than is represented by our baseline expectation (of about a -10% drop).

You're the top! You're the Coliseum You're the top! You're the Louver Museum You're a melody from a symphony by Strauss You're a Bendel bonnet A Shakespeare's sonnet You're Mickey Mouse You're the Nile You're the Tower of Pisa You're the smile on the Mona Lisa I'm a worthless check, a total wreck, a flop But if, baby, I'm the bottom, you're the top

What follows is a compilation of recent commentary in myDaily Diary on the TheStreet Pro and comments delivered to my investors at my hedge fund, Seabreeze Partners:

The December 2024/January 2025 period marks the beginning of what I expect to be a lower-trending market accompanied by rising volatility.

I expect 2025 to look far different than last year.

While, in managing my hedge fund, I predominantly focus on an assessment of reward vs. risk on individual stocks -- if I was forced to hazard a precise forecast I would project only about a 5% upside and a 10% to 15% downside for the S&P 500 Index in 2025 (or roughly 2-times to 3-times more risk than reward).

Today's commentary will explain why heady valuations are rarely a good launching pad for higher stock prices.

I will explore and summarize some of our fundamental near and intermediate-term concerns.

I will compare today with early 1973 (which marked the end of the Nifty Fifty era) and produced years of subpar returns for the major market averages. Then, I will highlight some longer-term existential market threats that few discuss, but that have a reasonable chance of emerging.

As I wrote to my Limited Partners several weeks ago:

"Many of our fundamental concerns (growing policy (fiscal and monetary) risks, sticky inflation, slowing economic growth and rising interest (higher for longer)) are finally beginning to be accepted by investors -- at a point in time in which valuations are elevated and consensus corporate profit estimates seem too optimistic. We are increasingly more confident that stocks will correct to more attractive levels than exist right now - at which time we can begin to accumulate selected stocks that meet our investing criteria and standards."

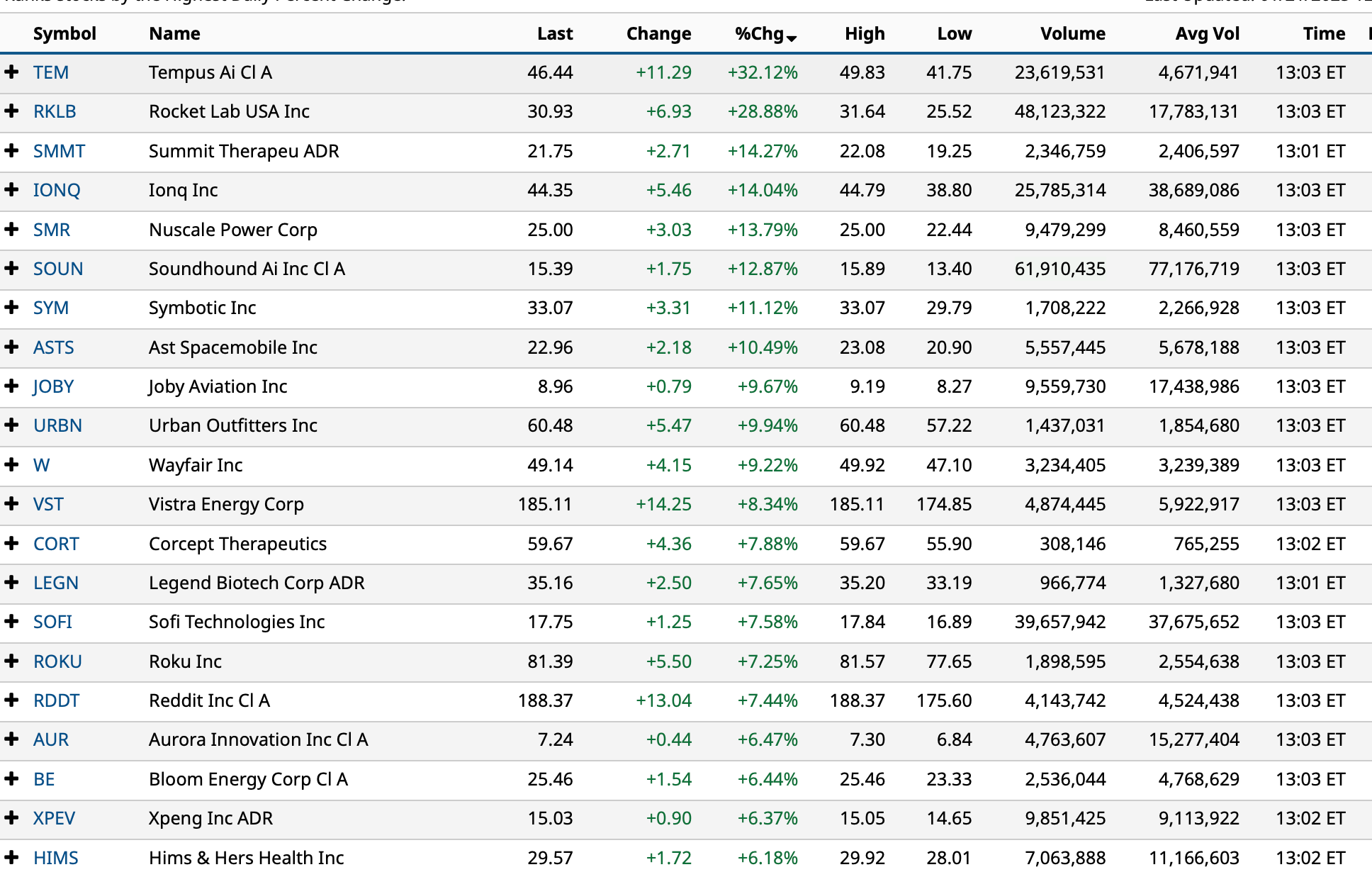

-XPEV +6.1% (President Trump did not target China in inauguration speech or impose tariffs immediately)

-MRNA +4.8% (HHS Provides ~$590M to MRNA to accelerate Pandemic Influenza mRNA-based Vaccine Development)

-TREE +4.6% (hearing Northland Capital Raised TREE to Outperform from Market Perform, price target: $60)

-MMM +4.4% (earnings, guidance)

-SCHW +4.0% (earnings)

-DHI +3.6% (earnings, guidance)

-URBN +2.7% (Morgan Stanley Raised URBN to Overweight from Equal Weight, price target: $63)

-QRVO +2.6% (Morgan Stanley Raised QRVO to Overweight from Equal Weight, price target: $106)

-ONB +2.5% (earnings, guidance)

-ROKU +2.3% (ADEA renews multi-year IP License Agreement)

-AEO +2.2% (Morgan Stanley Raised AEO to Equal Weight from Underweight, price target: $16)

-JD +2.2% (President Trump did not target China in inauguration speech or impose tariffs immediately)

-STX +2.2% (hearing Morgan Stanley names STX as Top Hardware selection)

Downside:

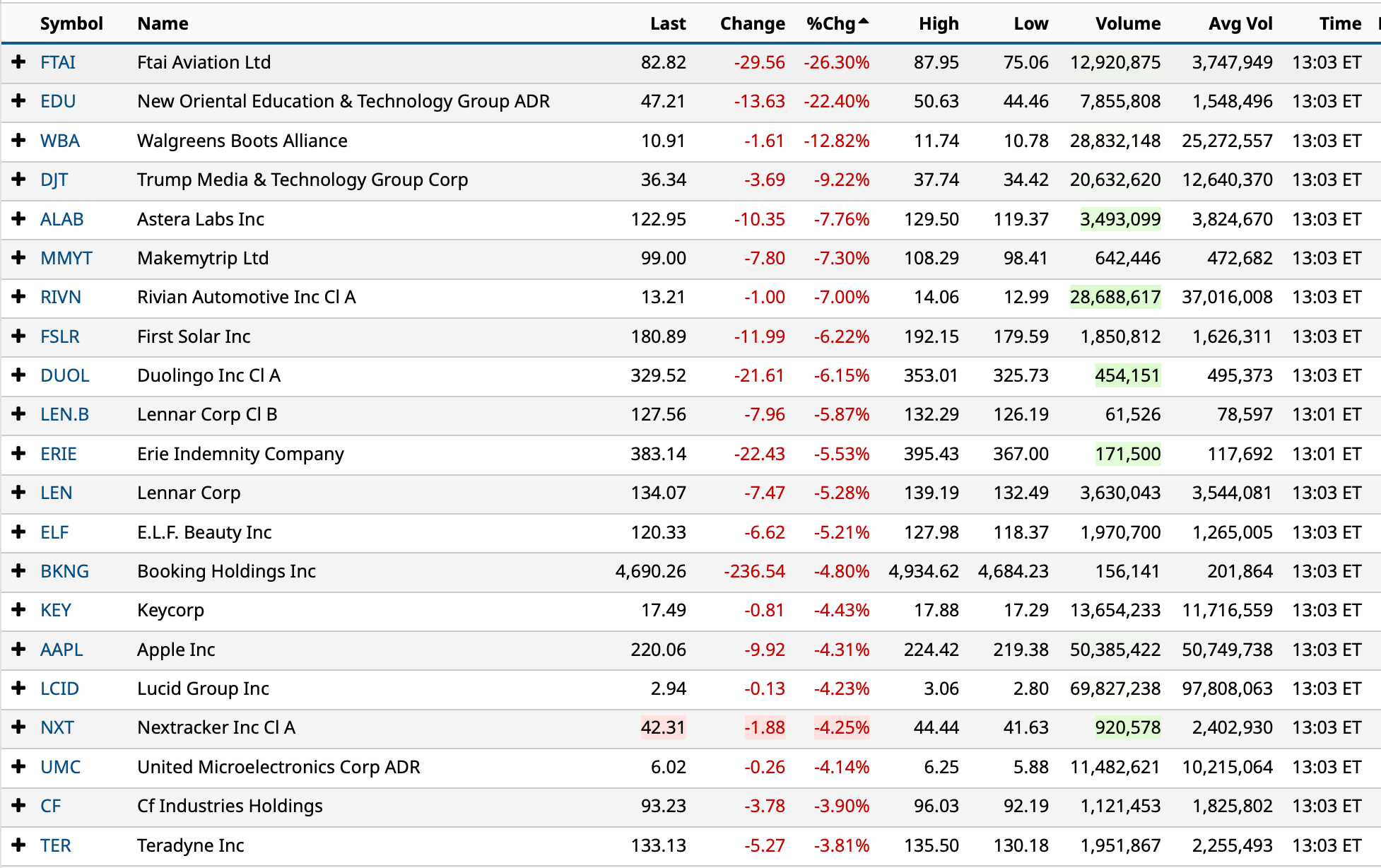

-FTAI -25% (Audit Committee of the Board of Directors of the Company determined to commence a review in response to the assertions alleged in the January 15, 2025 report issued by Muddy Waters Research)

-CBUS -17% (files to sell 9.0M shares at $2.50/shr in $22.6M registered direct offering)

-EDU -13% (earnings, guidance)

-LEN -6.2% (lower ahead of Millrose spin-off)

-WBA -6.2% (DOJ files suit against Walgreens for allegedly dispensing unlawful prescriptions)

-DJT -5.6% (profit-taking following rally into Trump inauguration last week)

-TER -3.9% (Morgan Stanley Cuts TER to Underweight from Equal Weight, price target: $117)

-KEY -3.8% (earnings, guidance)

-ATRA -2.7% (US FDA places Clinical Hols on EBVALLO (tabelecleucel) and ATA3219 IND applications)

-ALAB -2.5% (Morgan Stanley Cuts ALAB to Equal Weight from Overweight, price target: $142)

Boockvar on Presidential Timing, Earnings Comments and More

From Peter Boockvar:

Some things to think about/Some earnings comments/Some data

If there is one thing that anyone involved in markets gets to know is that markets sometimes don't always reflect the economy and the state of the economy at times separates itself from markets. How many times have we seen stocks rally on disappointing economic data on the belief it would give us a Fed rate cut? And vice versa? Also, markets are sometimes dispassionate but other times highly emotional. They don't care what you think, they don't care about your politics, they don't always do what you think they should and much more often than not, it does the opposite of what most people think it will do.

I say all this as we digest the likely incoming policies of Trump 2.0 which from an economic perspective, business should benefit greatly on the regulatory side in relieving its seemingly nonstop intense pressure, particularly on small business. On the tax side, a 21% corporate tax rate remaining in place (will be tough to lower further though I wish it did in order to better able US companies to compete globally and the corporate taxes are passed on to consumers anyway), along with the extension of the expiring tax legislation of the TCJA will meet up with the desire for tariffs, aka taxes that someone has to eat. I'm stating all the obvious things to think about but want to bring this all together.

We have had bull markets most of the time and under both Republican and Democratic presidents. We've had bear markets under both Republican and Democratic presidents too. And market behavior under either administration many times is just a victim or beneficiary of circumstance. Quickly on this, George H. W. Bush was unlucky becoming president after a long Reagan expansion and a recession and a bear market came on his watch. Clinton was lucky to be elected just as the recession was ending and benefited too from the epic tech stock bubble that happened to crash on George W. Bush's watch who then devastatingly presided over 9/11. He then experienced an economic recovery but ended his presidency with the housing market crash that Obama was lucky enough to have caught the bottom of when his presidency began. Trump 1.0 saw a pick in growth post Obama and the sharp corporate tax cut but ended with the disaster of Covid 19 that Biden was fortunate enough to have been president with the reopening and recovery. Inflation though, self-inflicted, was the curse of his administration but yes, sometimes being in the right place at the right time dictated market performance and vice versa.

All throughout too, we have had a growingly active Federal Reserve that continued to flex its monetary muscles and it itself became a major factor in how the economy and markets behaved, both in blowing bubbles and then figuring out how to recover from the aftermath.

Bottom line, the US economy will hopefully be helped by business supportive policies (tariffs are up for debate though and I still don't like them as I think the negatives outweigh the perceived positives) but we still must be thick skinned as living in markets we know s**t happens and other factors sometimes drive the bus. High valuations along with higher for longer interest rates will be the current administration's challenge when it comes to market's I believe.

To some earnings comments.

From Truist Financial:

"End of period loans experienced a little over 1% growth as we saw an increase in loan demand due to the results of our focused initiatives in the latter half of the quarter." Consumer loan growth in indirect auto, residential mortgage and other consumer offset weakness on the commercial side.

"Average commercial loans decreased $1.5b or .8%, primarily due to a decline in CRE and C&I balances driven by lower production in CRE."

"Credit metrics remained relatively stable and new consumer loan production spreads are accretive to the overall portfolio."

On the optimism post election, "I think clients are certainly more expansionary...So we've seen more increasing commitment. So I think clients are telling us that they're building for the future in terms of opportunities to invest. I think the real linchpin or the fulcrum point will come in M&A."

Regions Financial had similar commentary on its customers post election:

"client optimism is improving, and further clarity surrounding tax reform and tariffs is expected to be a catalyst for business activity and lending. As a result, it will probably be the 2nd half of the year before we see the impact filter through to the economy."

They are also benefiting from government largess as "within our footprint there is $77 billion of federal infrastructure spending already approved and allocated at the state level, which will benefit customers in infrastructure and infrastructure adjacent industries. We're also encouraged that pipelines and commitments are trending up. As a result, we expect a notable pickup in C&I lending in 2025, but this will be partially offset by continued softness in CRE origination."

"Average consumer loans remained stable in the fourth quarter as modest growth in credit card was offset by declines in other categories."

From DR Horton's earnings release this morning:

"Although the level of new and existing home inventories has increased from historically low levels, the supply of homes at affordable price points is generally still limited, and demographics supporting housing demand remain favorable. Despite continued affordability challenges and competitive market conditions, incentives such as mortgage rate buydowns have helped to address affordability and spur demand. Additionally, given our focus on affordable product offerings, we have continued to start and sell more of our homes with smaller floor plans to meet homebuyer demand."

Taiwan, as seen with the numbers last week from Taiwan Semi, continues to be a tech powerhouse and it helped to drive a 20.8% y/o/y export order increase, just above the estimate of up 18.8%.

The mood on the German economy remains challenged as seen with the January ZEW expectations index which fell to 10.3 from 15.7 and vs the estimate of 15.1. The only respite was the Current Situation component that was slightly less negative at -90.4 vs -93.1. The ZEW said "A lack of private household spending and subdued demand in the construction sector continue to stall the German economy. If these trends continue in the current year, Germany will fall further behind the other countries of the Eurozone. There is also greater political uncertainty, driven by a potentially difficult coalition building process in Germany and the unpredictability of the economic policy pursued by the new Trump administration." We also know their manufacturing sector is under major stress.

The UK said that the number of employed fell by 47k in December and is the first jobs number post the new Rachel Reeves budget that raised payroll taxes and likely drove the employment drop. This then puts pressure on the BoE to respond but who is still dealing with high services inflation.

The euro is weaker again after yesterday's rally on the WSJ tariff article saying the implementation of tariffs might be delayed. We heard from two ECB members Peter Kazimir and Francois Villeroy today who were both dovish and told us to expect more rate cuts with another cut to come next week. Rather than take a pause, see how the tariff situation works itself out, the ECB is trying to save its economy via cheap money again.

Petco WOOF price target lowered to $5 from $6 at Morgan Stanley Morgan Stanley lowered the firm's price target on Petco to $5 from $6 and keeps an Equal Weight rating on the shares. In the hardline, broadline and food retail space, the analyst's preferred stocks for 2025 are companies leveraging their scale to invest in next-generation retail tech that have revenue upside, are market share leaders within their sub segments, or are executing into a cyclical inflection in their category, the analyst tells investors in a 2025 outlook note for the group.

Blackstone Mortgage BXMT price target lowered to $17.50 from $18.50 at JPMorgan JPMorgan lowered the firm's price target on Blackstone Mortgage to $17.50 from $18.50 and keeps a Neutral rating on the shares as part of a Q4 earnings preview for the mortgage real estate investment trust group. Commercial real estate borrowers and lenders "have collectively kicked the can down the road," awaiting a more favorable rate environment, the analyst tells investors in a research note. However, the firm says the higher rate outlook "may dampen the budding optimism" that emerged in mid-2024. With the 10-year Treasury rate now projected above 4% until at least 2027, carrying costs will remain elevated and commercial real estate participants may be forced to resolve deals at "undesirable valuations," contends JPMorgan. It views Claros Mortgage Trust's (CMTG) December dividend cut to zero as potentially cautionary for the sector.

Apple's AAPL smartphone sales fell sharply in Q4 in China, Counterpoint Research Apple's smartphone sales in China fell 18% in Q4, putting it in third place behind Huawei and Xiaomi, Counterpoint Research said. Huawei's phone sales rose 15.5% y/y during the quarter. Commenting on the market dynamics, Associate Director Ethan Qi said, "The country's smartphone market saw a rebound in the first three quarters of the year, with positive YoY growth each quarter. However, momentum began to slow in Q4 as consumers adopted cautious spending behavior." Amid intensifying market competition from Huawei and other Chinese OEMs expanding into the premium market, Apple captured a 17.1% market share. Reference Link

Apple price target lowered to $260 from $265 at JPMorgan JPMorgan lowered the firm's price target on Apple to $260 from $265 and keeps an Overweight rating on the shares as part of a fiscal Q1 earnings preview. The concern heading into the earnings print is less about the quarter itself, and more so about the outlook, the analyst tells investors in a research note. The firm says Apple's share loss in China to likely continue with the company already past its product cycle peak and with the consumer subsidies from the local administration to enable smartphone replacement for low to mid-tier phones, which excludes high-end smartphones. In addition, Apple is seeing limited traction for the artificial intelligence features rolled out, increasing the likelihood of flattish unit sales through the upcoming quarters, contends JPMorgan. However, it feels downside to unit sales remain limited "given trough replacement rates already." The stronger U.S. dollar will also increase headwinds for Apple to navigate in the coming quarters, adds JPMorgan.

US: Futs are higher. Trump’s Day-1 executive orders took central stage during the holiday weekend: the most impactful headlines on Monday morning was Trump holding off immediately China tariff, pointing to a more cautious view from Trump on tariff implementation. With immediately tariff risks off the table, USD/CNY fell -0.7%. However, the possibility of 25% tariff on Canada and Mexico on Feb. 1 weigh on futures yesterday evening. This week, key macro focus will be Q4 earnings and headlines from the Washington. Today, we will hear from COF, DHI, MMM, NFLX and SCHW.

and...

EQUITY AND MACRO NARRATIVE: Last week, SPX added +2.9%, the best performing week since Nov 8; the index now sits only 1.4% below its ATH. The equities rally was primarily driven by both lower bond yields and a robust start to the Q4 earnings. 10Y yield fell 13bps last week to close the week at 4.6% amid dovish US CPI. Combining the December CPI and employment report, US data point to Goldilocks macro backdrops that continues to support economic growth and earnings delivery. On earnings, banks kicked off Q4 earnings with solid results across large-cap banks, with both revenue performance and credit metrices remaining healthy. Conference calls from banks earnings highlighted the healthy US consumer and benign credit conditions. In addition, TSMC earnings last week helped set a bullish narrative on semis and AI demand. Richemont’s solid Q4 results showed recovery in European domestic demand.

Over the holiday weekend, Trump’s inauguration took central stage. The initial WSJ article on no immediate tariff implementation was a relief to global risk assets, but it was offset by headlines on possible Mexico/Canadia tariff in February. You may find the full list of presidential actions from the White House (here). Overall, as we move past immediate tariff risks and a slew of December macro data, investors’ focus will return to micro as we will hear from the majority of SPX companies over the next few weeks.