From JPMorgan:

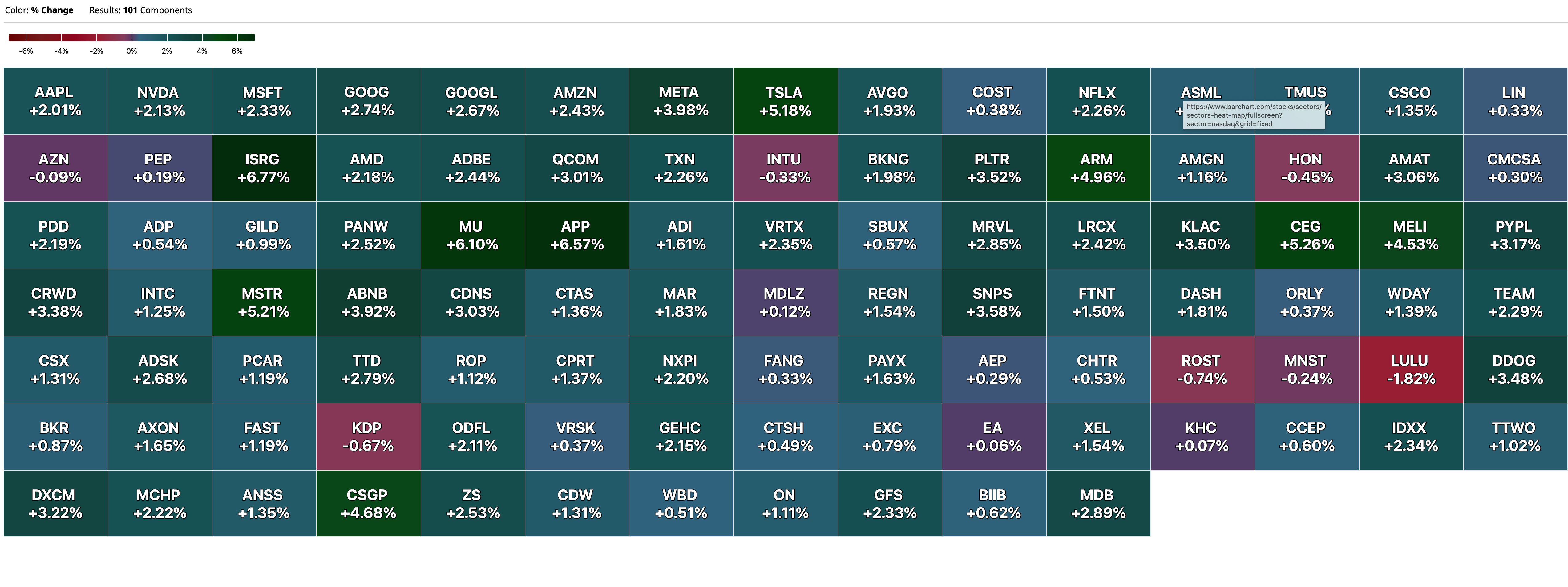

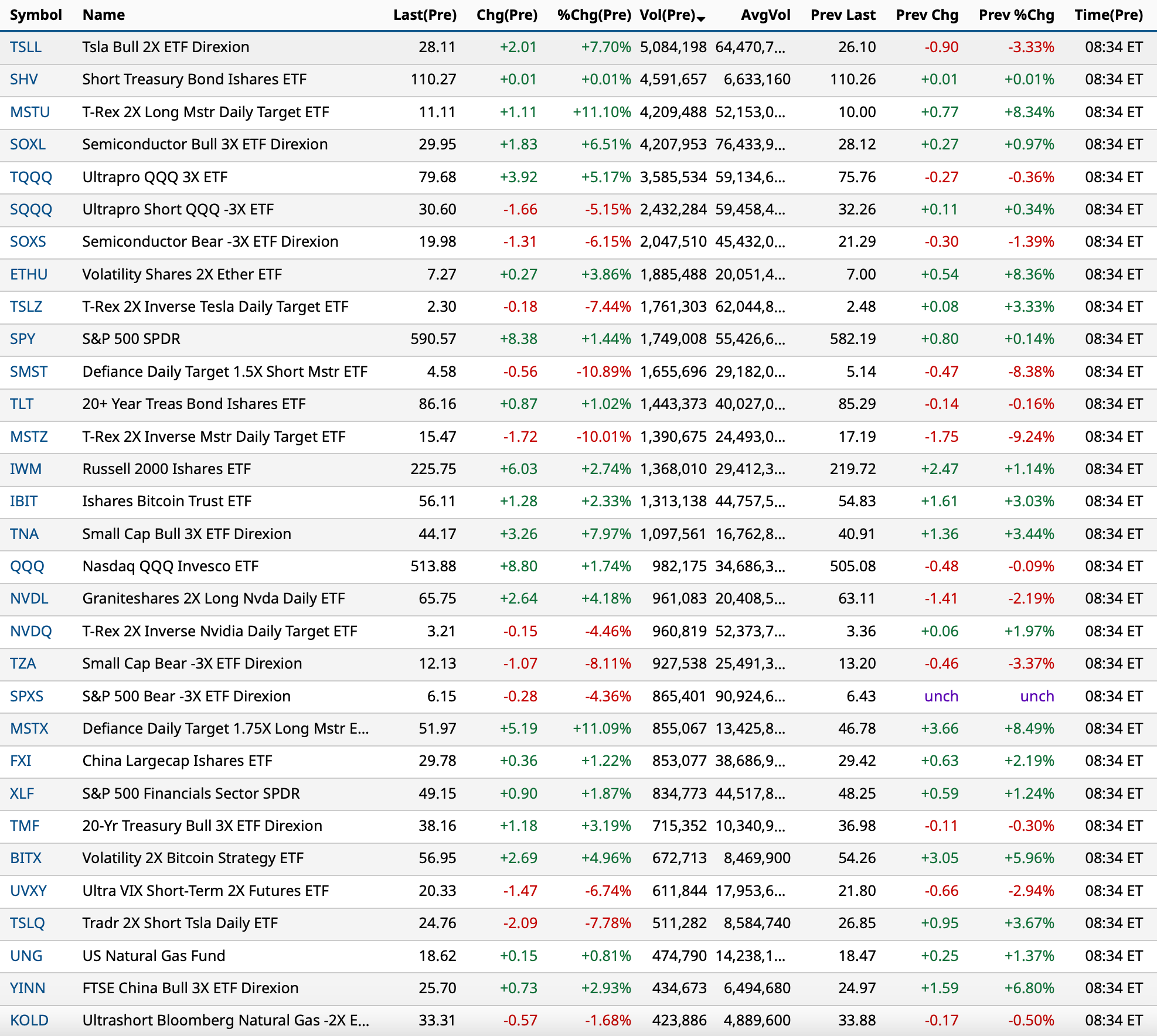

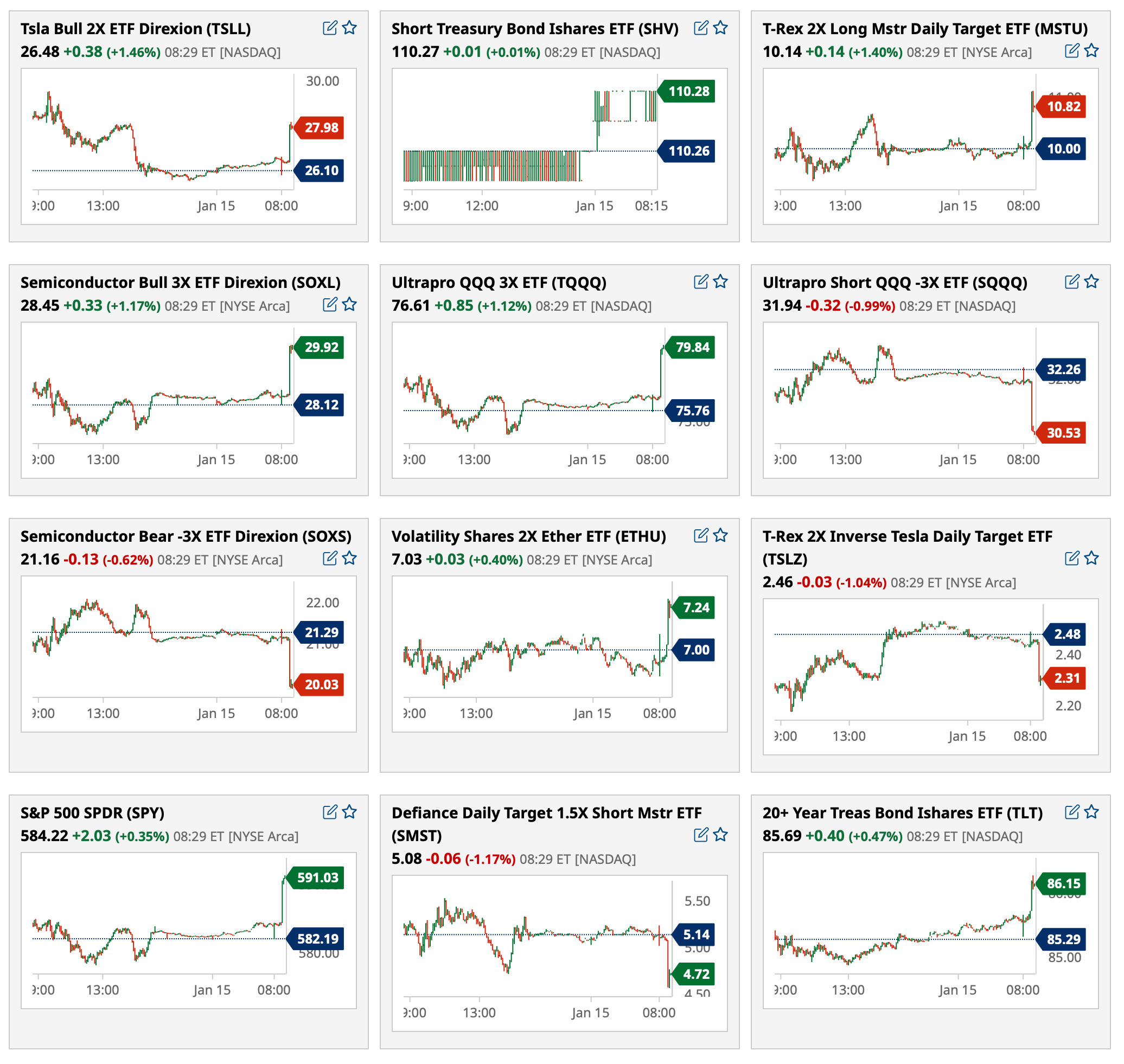

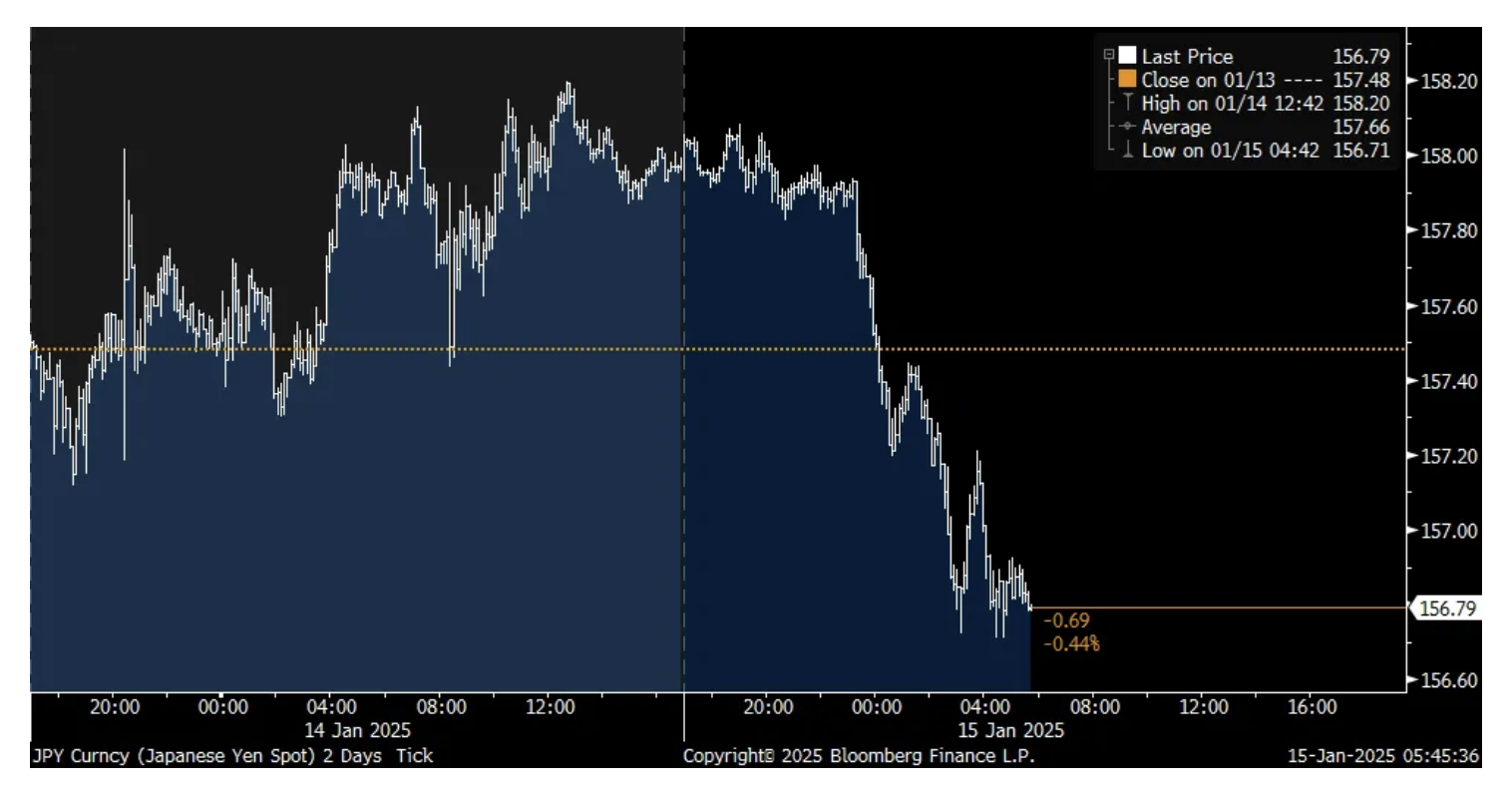

US: Futs are higher pre-mkt led by small-caps with the rally strengthening after the cooler than expected UK CPI print. Bond yields are down 1-2bps as USD is being offered. All Mag7 names are higher, ex-NVDA. Banks are seeing a pre-mkt bid ahead of earnings releases. In cmdty space, Energy and Metals are leading the complex higher. Today’s focus is on CPI/Bank Earnings but keep an eye on the Beige Book release.

and...

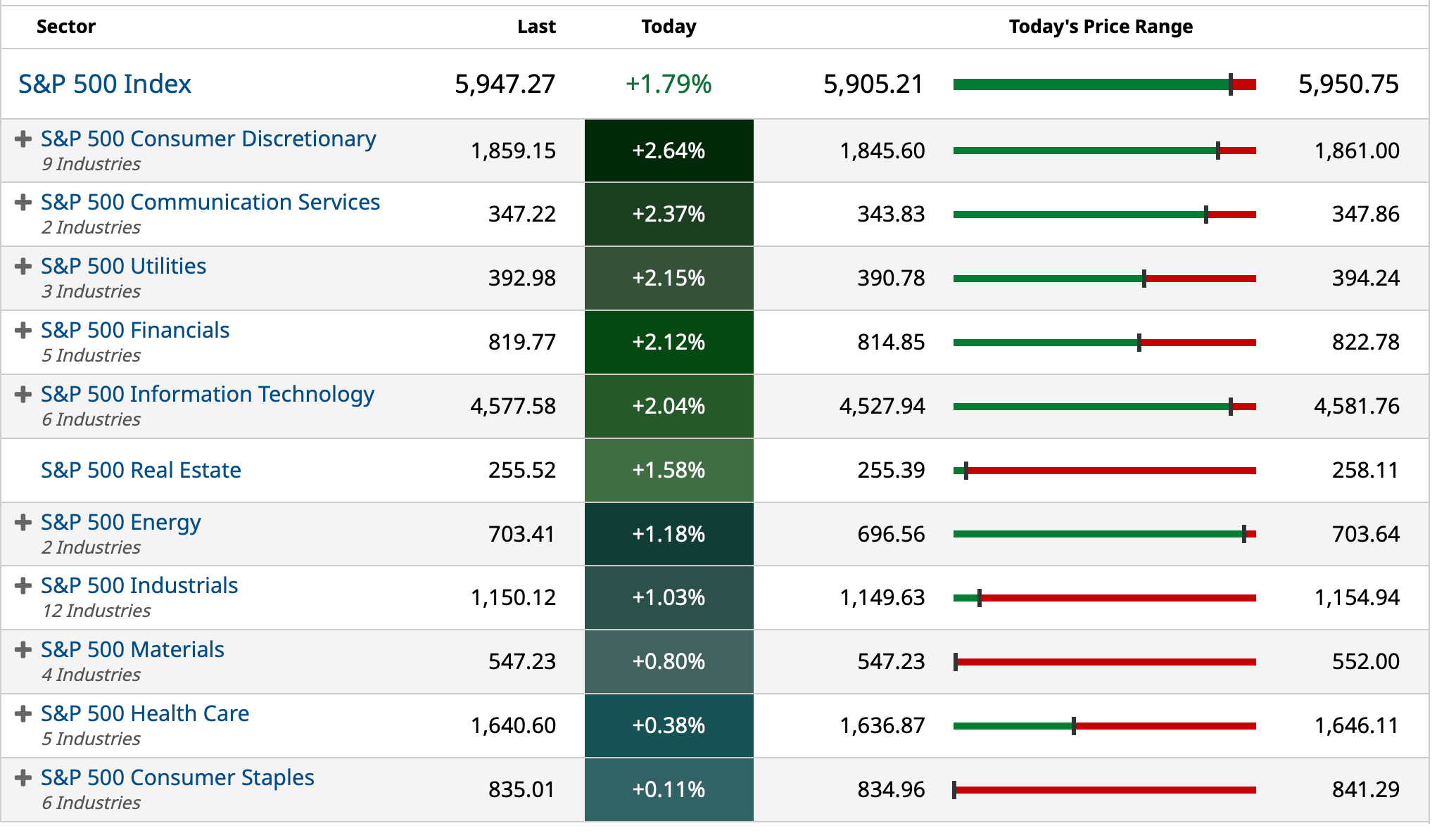

EQUITY AND MACRO NARRATIVE: As we prep for today, the SPX has fallen ~4.1% from its all-time, set on Dec 6, 2024; SPW -4.8%, NDX -4.0%, NDXW -4.0%, RTY -7.9%. This occurred with the yield curve bear steepening; the 10Y yield move from 4.15% to 4.77% (yesterday, a 52-week high). While it does appear that bond yields have overshot their fundamentals, today’s CPI is the catalyst and would take bond bids following yesterday’s PPI print as evidence for this, despite that bid lacking durability in the trading session.

My colleague Jack Atherton on yesterday’s Mag7 moves, “Market rolling into the close ahead of CPI tomorrow 0830aET, led by Mag7 (-1.7% today). It’s only Tuesday but this week has felt eerily quiet given we’re on the cusp of tech earnings (JPM tomorrow, TSM 1/16, NFLX 1/21)… both on the desk and in terms of client inbounds. Into earnings, feels like traders are happy to “wait and see” with the macro backdrop making any earnings / guidance wobbles hard to defend. Rates the primary driver of price action at the moment and there is a LOT of moving parts that tech investors + myself don’t really have a view on (CPI tomorrow, multiple Fed updates, Trump inauguration, China/TikTok, Bessent confirmation hearing, Tariffs noise). Additionally, tech investors are generally coming off a very good year so likely leaning more defensively... valuations are not that easy (for Mag7 or for the market overall)… Mag7 is possibly facing the first round of EPS downgrades in a few years through earnings (FX, depreciation, equity investments).”

CPI SCENARIO ANALYSIS – updated with Rates color from David Nadle

Feroli’s CPI preview is here. For CPI he sees Headline MoM printing +0.4% (0.44% unrounded) and Core MoM printing +0.3% (+0.28% unrounded), both numbers are above the Street. This equates to 3.0% YoY for Headline and 3.3% YoY for Core.

The following scenario analysis is NOT A PRODUCT OF JPM RESEARCH, this is a trading desk view from JPM US Market Intelligence. This month we focus on Core MoM outcomes and 1-days SPX moves.

· [5.0%] Above 0.30%. The first tail outcome with this outcome stemming from strong consumption and a potential move higher in housing prices. SPX loses 1% - 2%.

· [30.0%] Between 0.23% - 0.30%. This hawkish outcome likely comes to fruition if Core Goods deflation flips to being inflationary and/or loss of disinflation momentum from housing. SPX loses 75bps – 1.25%.

· [40.0%] Between 0.17% - 0.23%. The base case scenario. SPX gains 25bps – 1%.

· [22.5%] Between 0.10% - 0.17%. This dovish outcome is likely achieved via a combination of cooler home inflation and an increase in the deflationary impulse from Core Goods. SPX gains 1% – 1.5%.

· [2.5%] Below 0.10%. Similar to the previous bullet point, but you also likely see a reversal in categories experiencing recent gains such as Transportation. SPX gains 1.75% – 2.50%.

· WHAT ARE OPTIONS PRICING? Options that expire on Friday are pricing ~1.6% move.

· RATES COLOR (David Nadle) – Since NFP intermediate LHS vols have richened vs the rest of the surface while ULC has sunk. With the market pricing no fed action in H1 ULC continues to offer strong carry and slide, assuming that the market will not press a further selloff in front whites on the back of strong data. We have seen buying if 5y tails across the expiry surface both outright and vs RHS, mostly as straddles switches. Locally 5y realized/implied ratios still appear cheap and as 5s will function as a pivot point on the curve given how much pricing has been taken out of the whites. Realized vol has come down materially outside of Tier 1 data releases, making long gamma positions challenging to hold. Skew has continued to rotate towards receivers on the LHS, accompanied with a broader richening in VoV across shorter tails (last week’s strong NFP print has re-opened the upside of the distribution). We have reduced our long vol position as we have turned bearish on the forward path of realized vol.

o RATES BREAKEVENS:

o SFRH5: 2.5bp

o SFRH6: 9.875bp

o SFRH7: 9.50bp

o FV: 9.25bp

o 5y: 9.00bp

o TY: 8.125bp

o 10y: 7.375bp

o US: 6.75bp

o 30y: 5.75bp

o *the 1d terminal breakeven (premium/dv01) for a straddle struck at 3pm today, expiring at 3pm Wednesday.