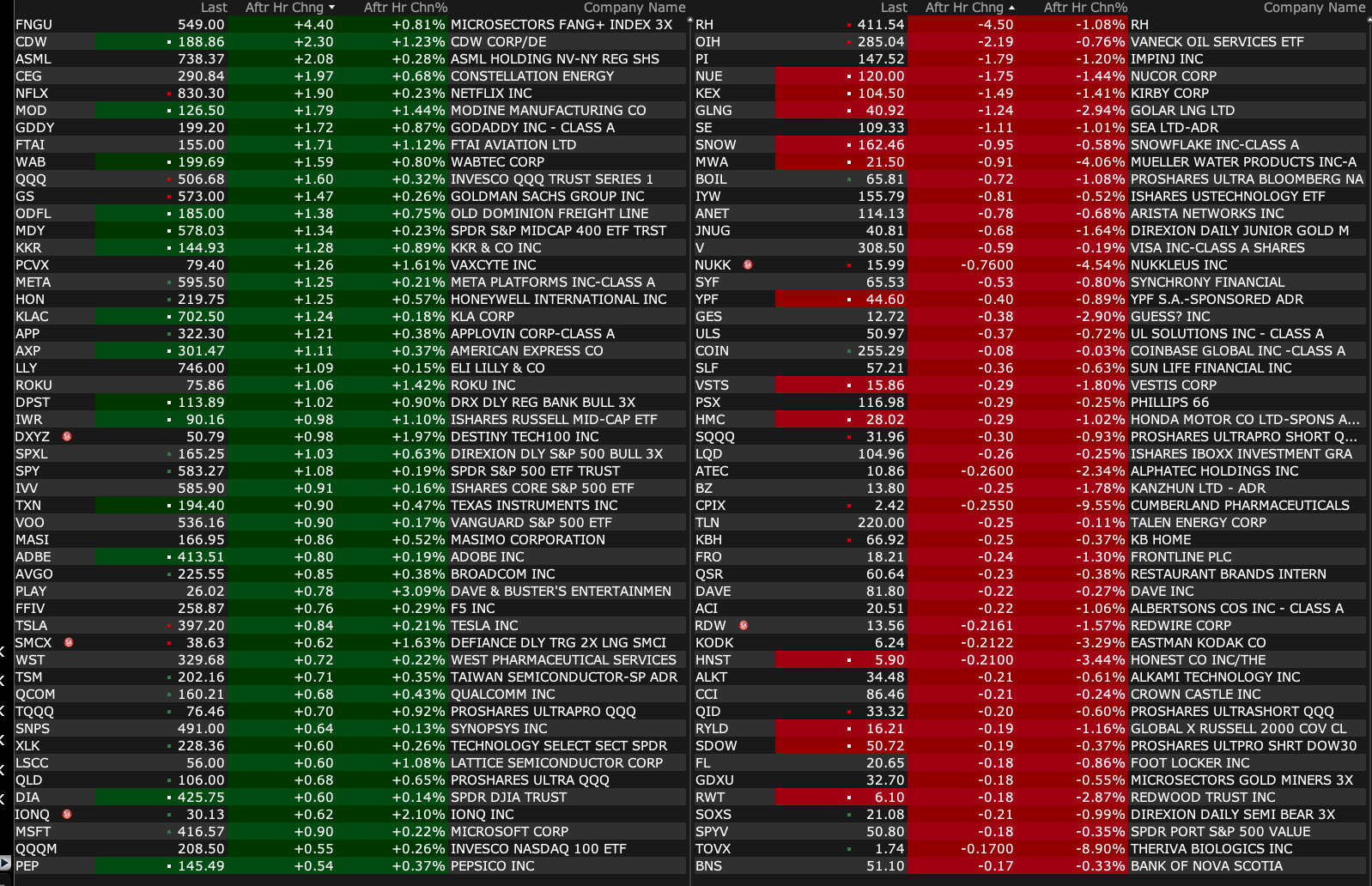

Tuesday's After-Hours Movers

At 4:19 p.m.:

BY Doug Kass · Jan 14, 2025, 4:55 PM EST

At 4:19 p.m.:

BY Doug Kass · Jan 14, 2025, 4:55 PM EST

BY Doug Kass · Jan 14, 2025, 4:45 PM EST

- NYSE volume 0.5% above its one-month average

- NASDAQ volume 3% below its one-month average

- VIX index: down 2.14% to 18.78

BY Doug Kass · Jan 14, 2025, 4:35 PM EST

Wolf Street howls about the PPI print this morning.

BY Doug Kass · Jan 14, 2025, 3:45 PM EST

The market had more intraday moves than a shortstop batting .110 today!

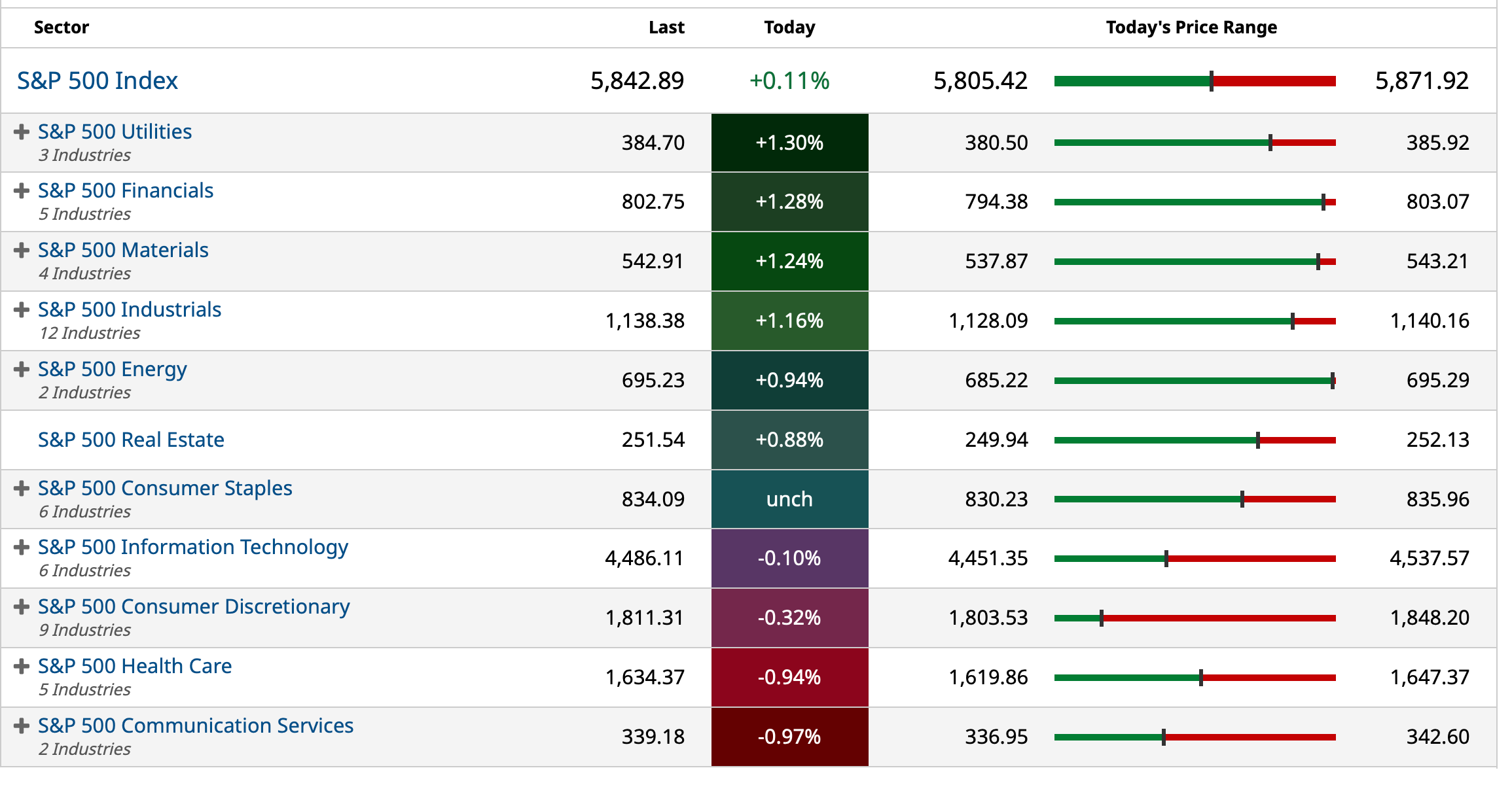

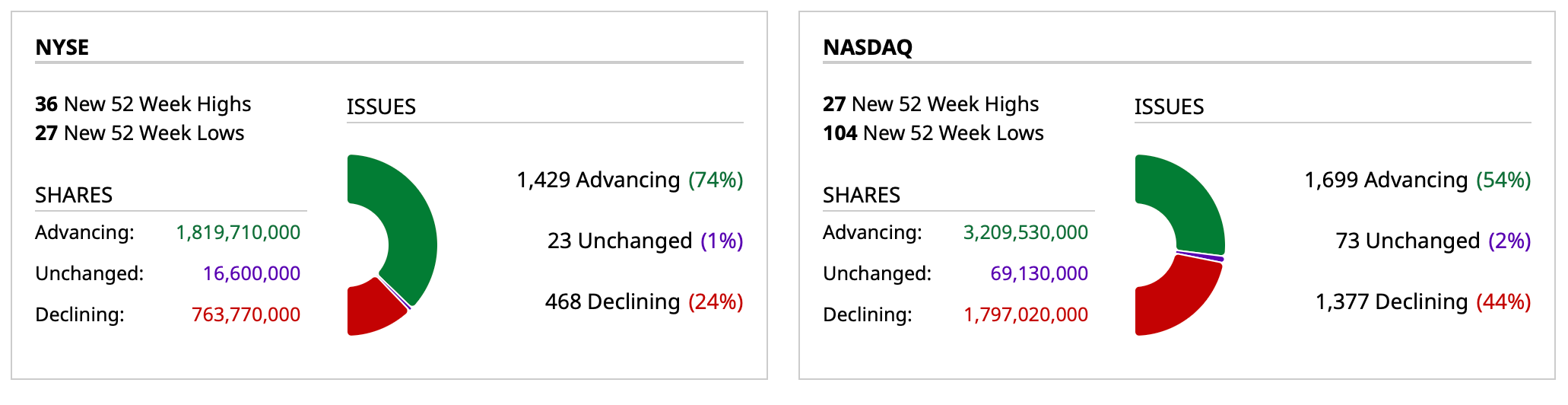

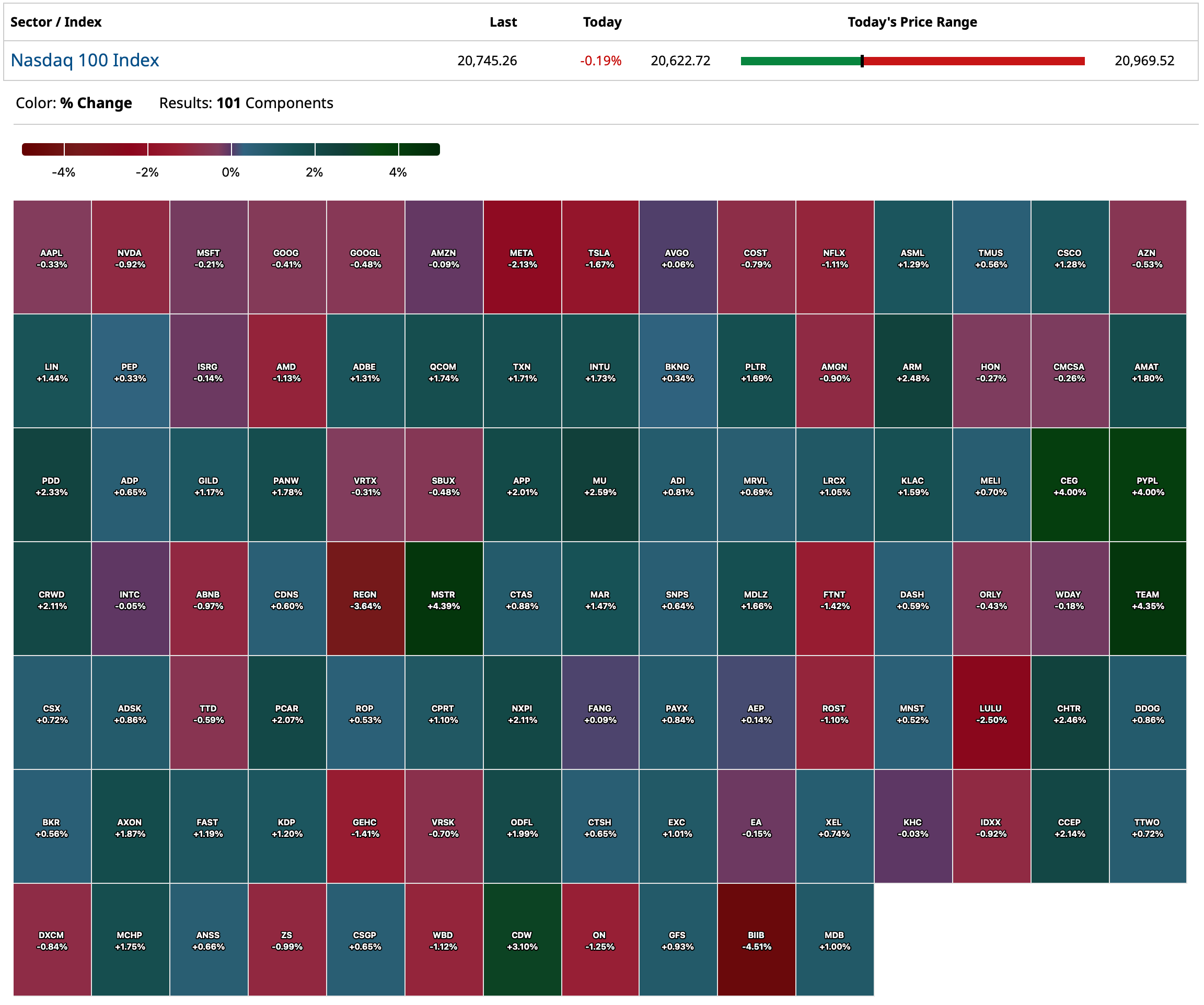

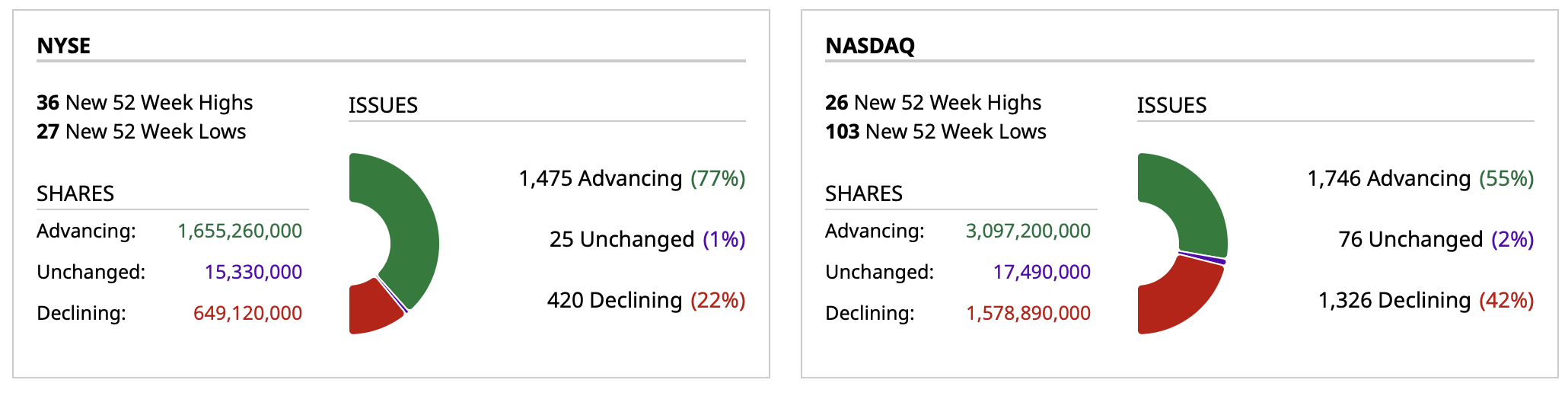

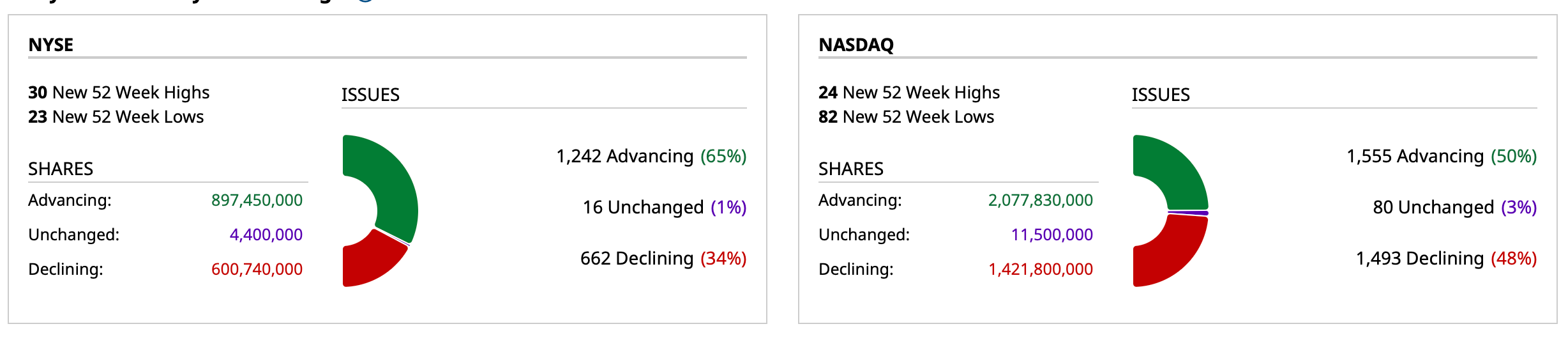

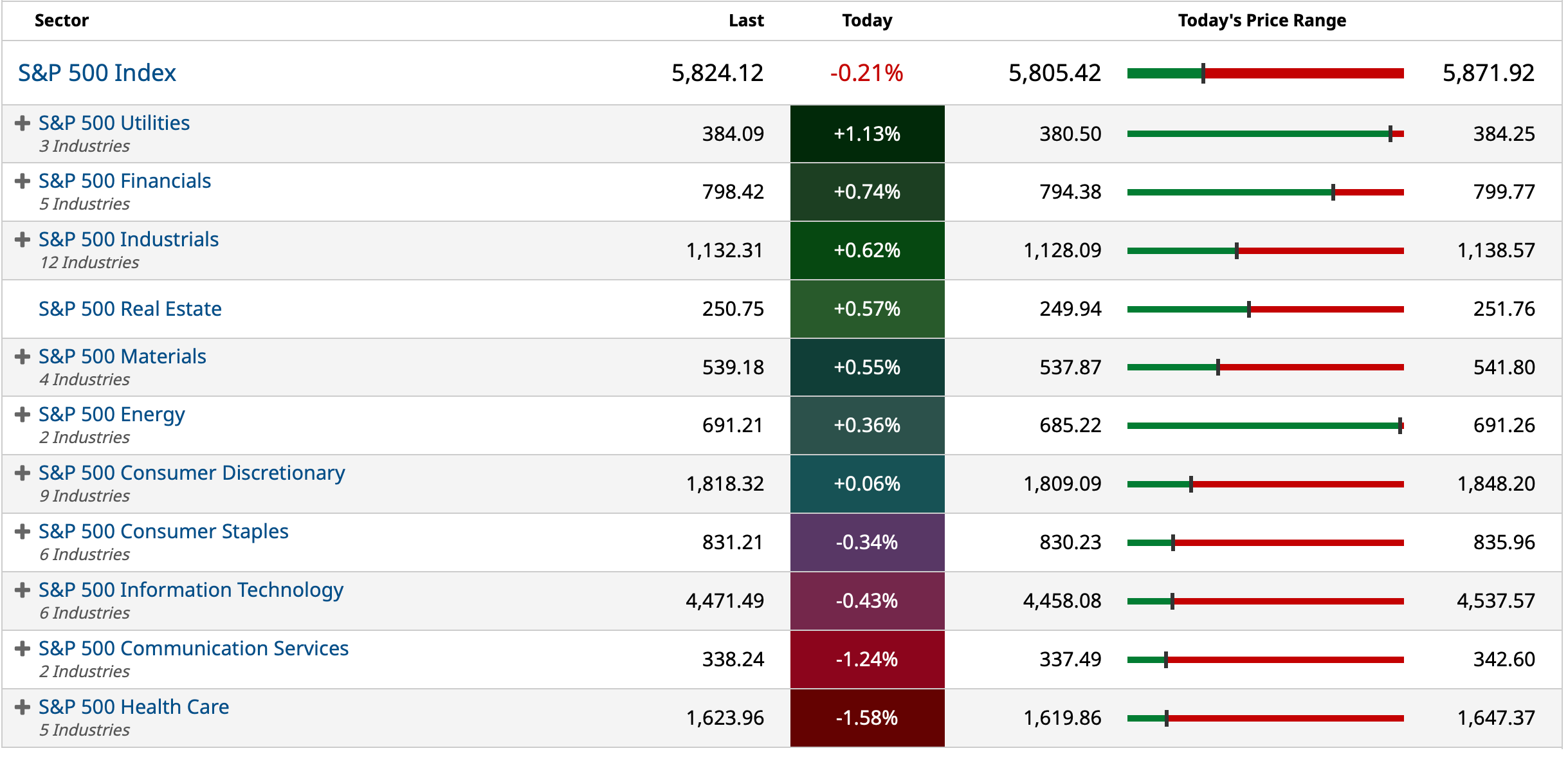

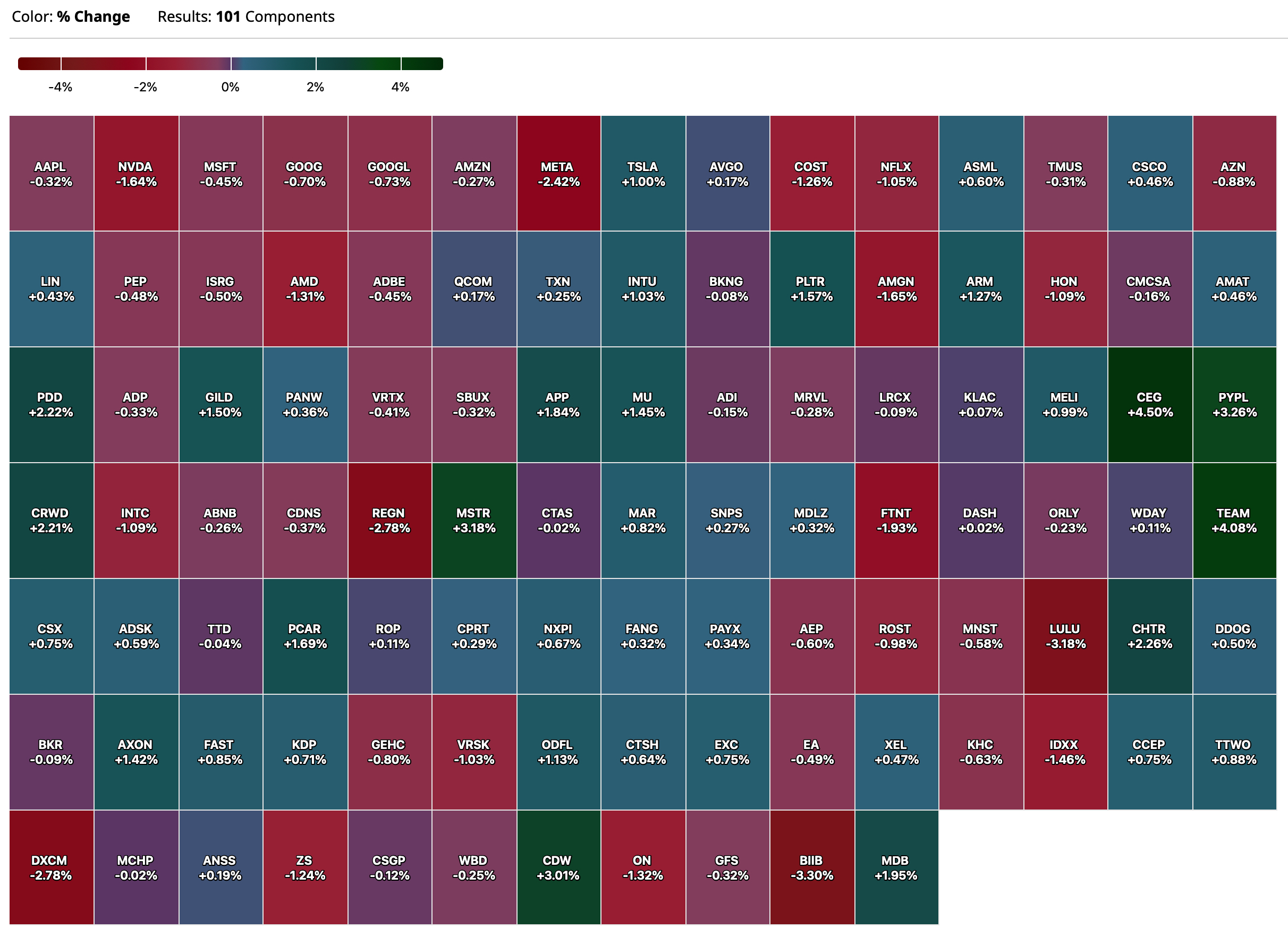

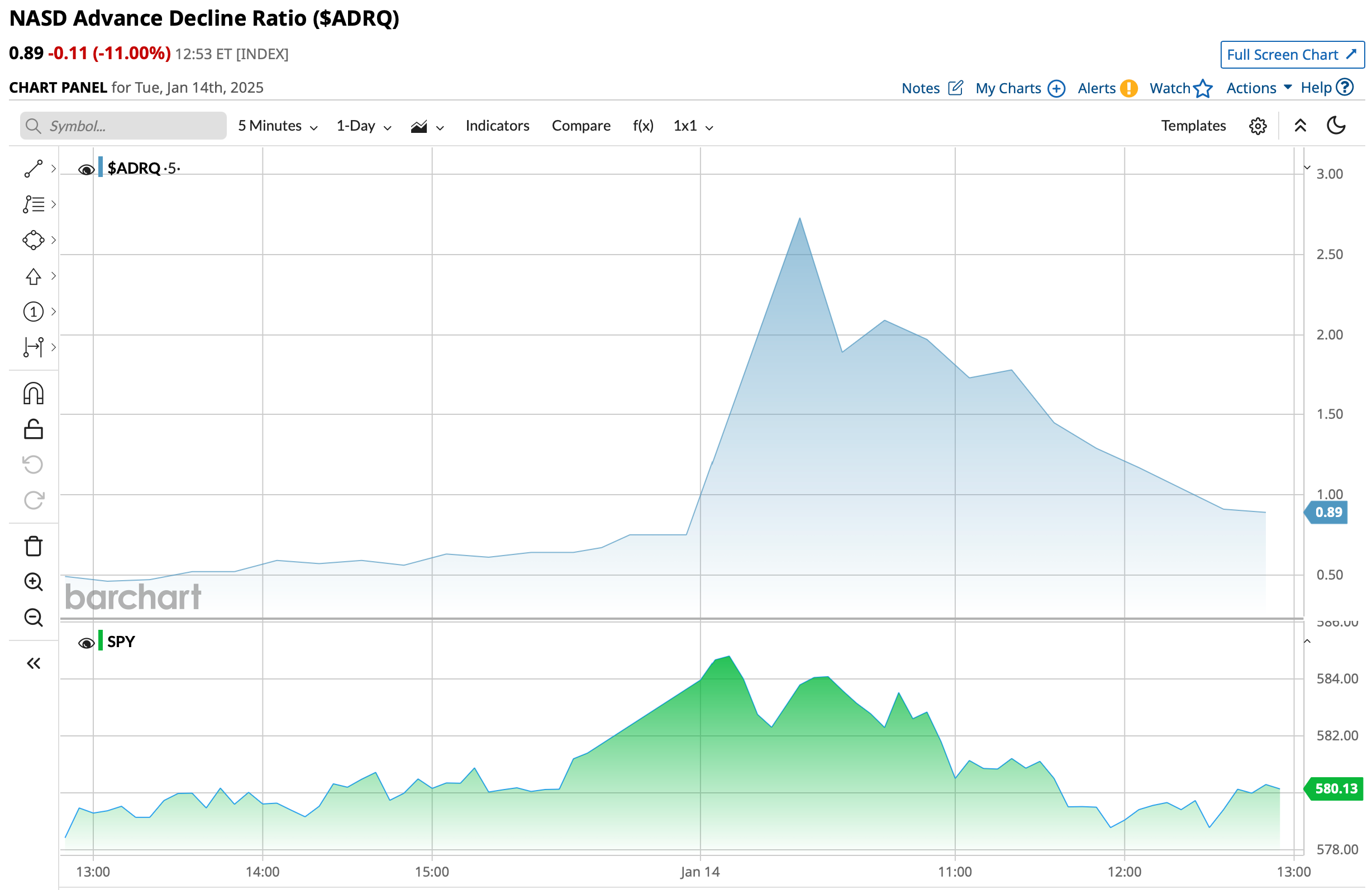

Breadth is fine (on both the NYSE and NASDAQ) and the equal-weighed S&P is +0.64%:

At 3:20 p.m. S&P cash is down by -13 handles.

Here are today's "Things":

* I purchased more MSOS at $3.46.

* I added to TSNDF at $0.54.

* I added to TCNNF at $4.94.

* I added to GTBIF at $7.04.

* I added to PG at $159.73.

* I started a new long in BA at $165.76.

BY Doug Kass · Jan 14, 2025, 3:35 PM EST

You're right, I am a coward!

I haven't any courage at all.

I even scare myself.

Look at the circles under my eyes.

I haven't slept in weeks.

- Cowardly Lion [while crying], Lions and Tigers and Bears, Oh my!

This is one of the best trading markets for quick-minded and unemotional traders.

But for the majority of investors (of a buy-and-hold school) — as Grandma Koufax used to say, "Dougie, rotzaruck!"

Do you suppose we will see some wild animals?

BY Doug Kass · Jan 14, 2025, 3:21 PM EST

All the girls and boys will sing

Come tomorrow we get everything

So as long as we survive today

Come tomorrow we gonna find a way

Yeah, as far as I can see

We should let the children lead the way

- Dave Matthews, Come Tomorrow

BY Doug Kass · Jan 14, 2025, 2:38 PM EST

I agree.

I continue to aggressively buy... for the longer term.

BY Doug Kass · Jan 14, 2025, 2:00 PM EST

BY Doug Kass · Jan 14, 2025, 1:40 PM EST

I'm back buying Green Thumb Industries GTBIF at $7.05.

BY Doug Kass · Jan 14, 2025, 1:30 PM EST

Amazon AMZN is having a real hard time making this stuff work. Amazon is about as well funded and as well resourced as anyone.

Amazon's AI lead says technical issues are holding back Alexa AI

When you see something like “no solid release date, not rolling out anytime soon,” that speaks volumes.

My two cents, if it is not working well yet, it will never work well. Nothing is really changing.

All the company is doing is throwing more processing power, more electricity, and more water (cooling) at an underlying technology that does not work well and does not scale. And the water would be better left in the empty reservoirs in California anyway!

BY Doug Kass · Jan 14, 2025, 1:20 PM EST

I added to ELAN at $11.54.

BY Doug Kass · Jan 14, 2025, 1:06 PM EST

As promised, I'm buying back Boeing BA at $165.35.

BY Doug Kass · Jan 14, 2025, 12:48 PM EST

The market action is awful.

I continue to err on the side of conservatism.

Most should have above-average cash reserves.

IMHO.

BY Doug Kass · Jan 14, 2025, 11:49 AM EST

Back in the saddle.

BY Doug Kass · Jan 14, 2025, 11:18 AM EST

From Peter Boockvar:

I argued last year and will again today, that one of the reasons for the rise in longer term US interest rates, and in other places too, is the increase in Japanese rates. I attribute last year's move to 5% in the US 10 yr yield to the Bank of Japan ending yield curve control and that the move began within days of the BoJ doing so. Ahead of the BoJ meeting next week and after today its Deputy Governor Ryozo Himino said "The board will have discussion to decide whether to raise the policy rate or not, based on the outlook compiled," the 40 yr JGB yield is rising to its highest level since it was first issued in 2007. The 2 yr JGB yield is at the highest level since October 2008 and the 10 yr yield was up another 4.4 bps overnight to 1.25%, nearing a 14 yr high.

Also of great importance and influence, the BoJ continues to trim its pace of asset purchases and by Q1 2026 will have cut the rate of buying in half from its peak early last year. To put numbers around this, I've seen estimates that the BoJ over a 2 yr time frame is expected to cut QE by about 45 trillion yen which at the current exchange rate equals about $286 billion. The BoJ was the architect of the current iteration of QE and has had its foot on the neck of rates for decades. I don't see how we can have a debate over the US 10 yr yield direction without discussing the moves of the BoJ.

Notwithstanding this, the yen still can't get out of its own way as it is lower today after a 3 day bounce. The FX market and those long yen do not want to hear about a possible rate hike from the BoJ, they want to actually see it.

The US dollar otherwise today is down after the recent voracious strength on the Bloomberg story that some incoming Trump officials are talking about phasing in the tariffs in a measured pace, "month by month, a gradual approach aimed at boosting negotiating leverage while helping avoid a spike in inflation, according to people familiar with the matter." We'll soon see.

2 yr JGB Yield

10 yr JGB Yield

The NY Fed's Consumer Expectations survey out yesterday was pretty mixed when trying to gauge the state of the US consumer. The one yr inflation guess remained at 3%, though lifted to 3% from 2.6% 3 years out and slipped to 2.7% from 2.9% at the 5 yr look. Expectations for the unemployment rate fell but "The mean perceived probability of finding a job if one's current job was lost declined sharply, to 50.2% from 54.1% in November 2024. This is the lowest reading since April 2021." Most came from those with a high school degree or less.

Income expectations fell but rose a touch for spending expectations. This also stood out, "The average perceived probability of missing a minimum debt payment over the next three months increased to 14.2% from 13.2%. The increase was broad based across income and education groups. This reading equals the September 2024 reading, which was the highest level of the series since April 2020." Rising delinquency rates we know are a growing issue, especially for the lower income cohort.

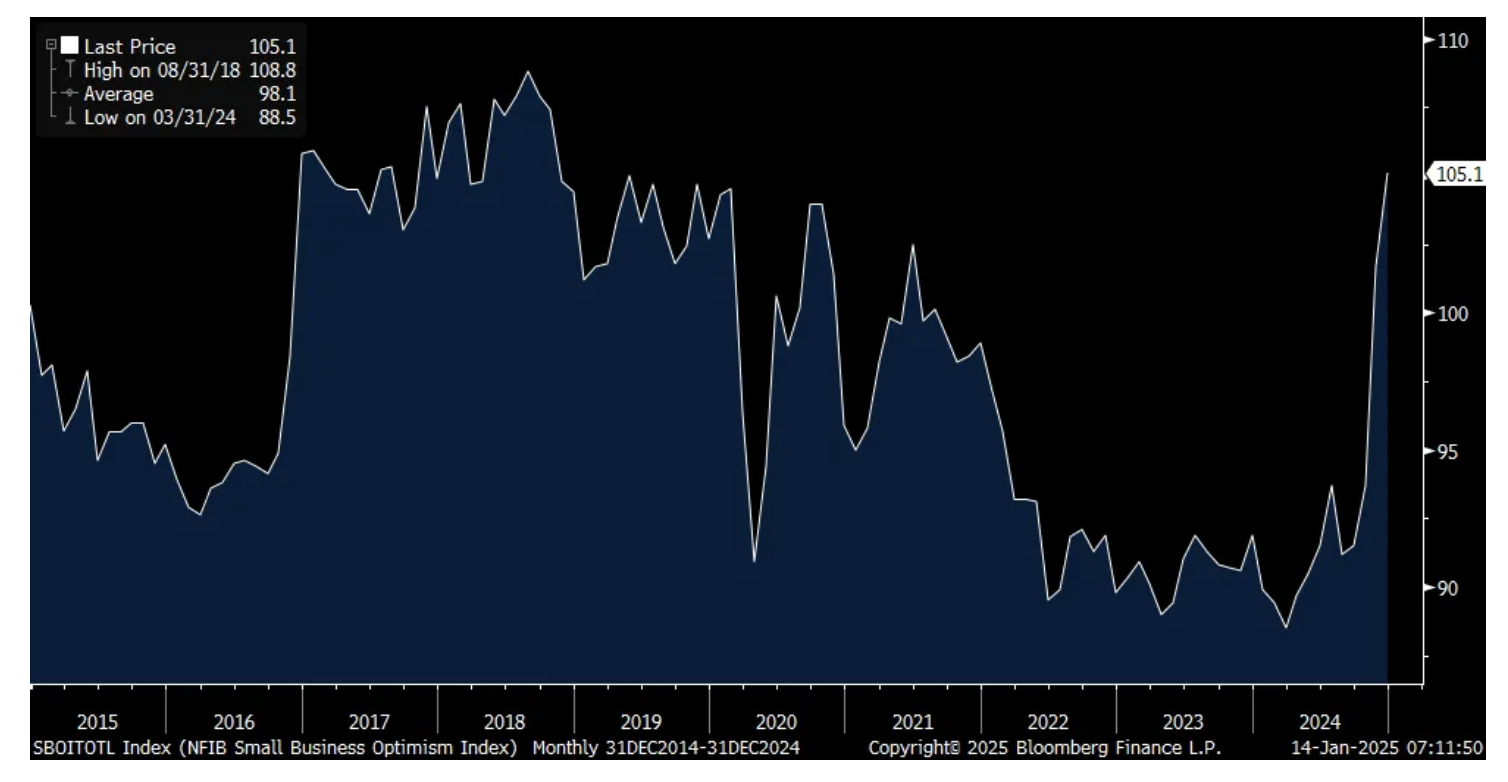

Small business also expressed its sentiment via the NFIB Small Business Optimism index for December and it jumped again to 105.1 from 101.7 and is now up 11.4 pts in the two months post election. Expectations are running high for Trump as those that Expect a Better Economy rose by 16 pts after gaining 41 pts in the month before. Those that Expect Higher Sales were up 8 pts after increasing by 18 pts in November. And Good Time to Expand was higher by 6 pts and by 14 pts over the past two months.

Plans to Hire rose 1 pt but fell 1 pt for job openings. Compensation plans fell. After rising by 6 pts last month, capital spending plans fell 1 pt but rose by 5 pts for Plan to Increase Inventory. Higher Selling Prices were unchanged at 24%. Lastly, the average rate paid on a loan fell one tenth m/o/m to 8.7%.

The bottom line from the NFIB is as you would expect it to be, "Optimism on Main Street continues to grow with the improved economic outlook following the election. Small business owners feel more certain and hopeful about the economic agenda of the new administration. Expectations for economic growth, lower inflation, and positive business conditions have increased in anticipation of pro-business polices and legislation in the new year." We now need to see these hopes and dreams realized.

Also of note, inflation remained the "single most important problem in operating their business (higher input and labor costs), unchanged from November and leading labor quality as the top issue by one point."

NFIB

KB Home is bouncing after reporting earnings last night but only after falling notably over the past 6 weeks with the rise in mortgage rates.

They remain big picture bullish on its business. "The housing market is benefiting from solid employment and wage increases. Demographics have been and we expect will continue to be a significant factor in driving housing demand with the largest generational cohorts, millennial and Gen Z buyers, demonstrating a strong desire for homeownership and contributing to the growth in household formations. As to supply, although existing home inventory has risen, it is still below historically normalized levels in most markets especially at our price points."

That said, "While longer term housing market conditions remain favorable, affordability constraints stemming from rising mortgage rates are influencing near term demand...we did miss our internal sales goals as rising mortgage rates tempered our selling base as the quarter progressed."

Also, "we continue to support our buyers during the fourth quarter with roughly 60% of our net orders having some form of mortgage concession, whether a rate lock or a buy down. This was a consistent level relative to the past four quarters despite the rise in rates."

Signet Jewelers gave us color on their holiday season and it was softer. They saw holiday comps down 2% "that were below forecast" and said "Engagement and Services sales were within expectations and we saw AUR increase in both Bridal and Fashion. However, fashion gifting underperformed as consumers gravitated to lower price points even more than anticipated in a continued competitive environment. Merchandise assortment gaps at key gifting price points impeded our ability to meet that trend. Merchandise margin expanded, but less than expected due to the lower fashion mix and a stronger customer response to promotional items."

BY Doug Kass · Jan 14, 2025, 9:39 AM EST

Premarket percentage movers at 8:33 a.m. ET:

BY Doug Kass · Jan 14, 2025, 8:45 AM EST

Upside:

-ANGI +9% IAC spin announcement

-HEES +100% URI deal

-INGN +6% prelim Q4

-KIDS +3% initial FY25 outlook

-KBH +8% earnings

-RILY +10% filed 10-Q

-DHR +1% guidance

-APLD +39% data center investment

-TDOC +10% Amazon announcement

-PCAR +2% upgrade

-AIFF +70% Discovers Breakthrough Cognitive Brain Age Biomarker

-SNGX +11% HyBryte Expanded Treatment Continues to Demonstrate Positive Outcomes in Early-Stage Cutaneous T-Cell Lymphoma

Downside:

-BTG -2% div cut; production update

-TTAN -2% quarterly results; guidance

-AEHR -10% earnings

-SIG -10% holiday sales update; cuts outlook

BY Doug Kass · Jan 14, 2025, 8:35 AM EST

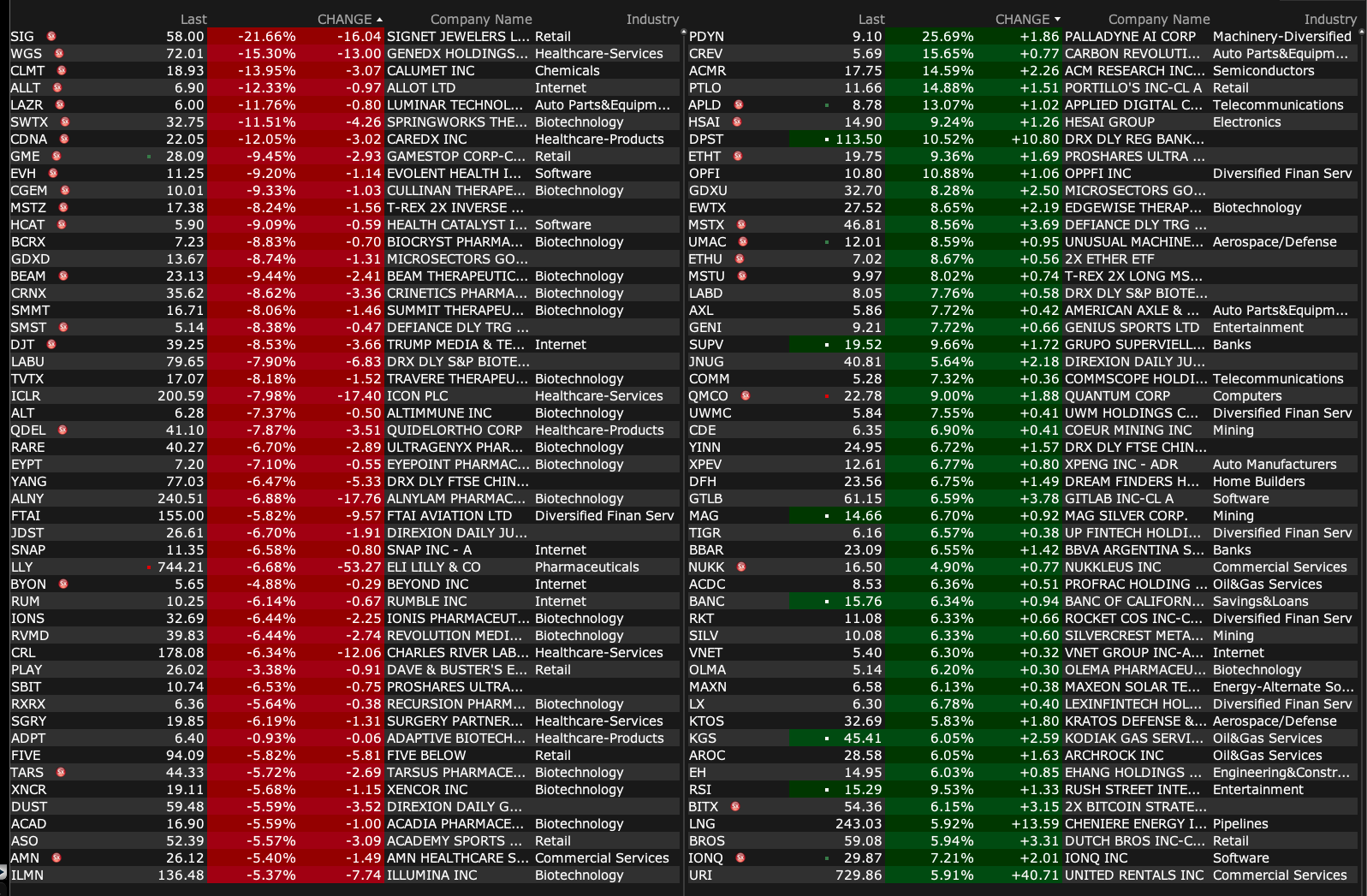

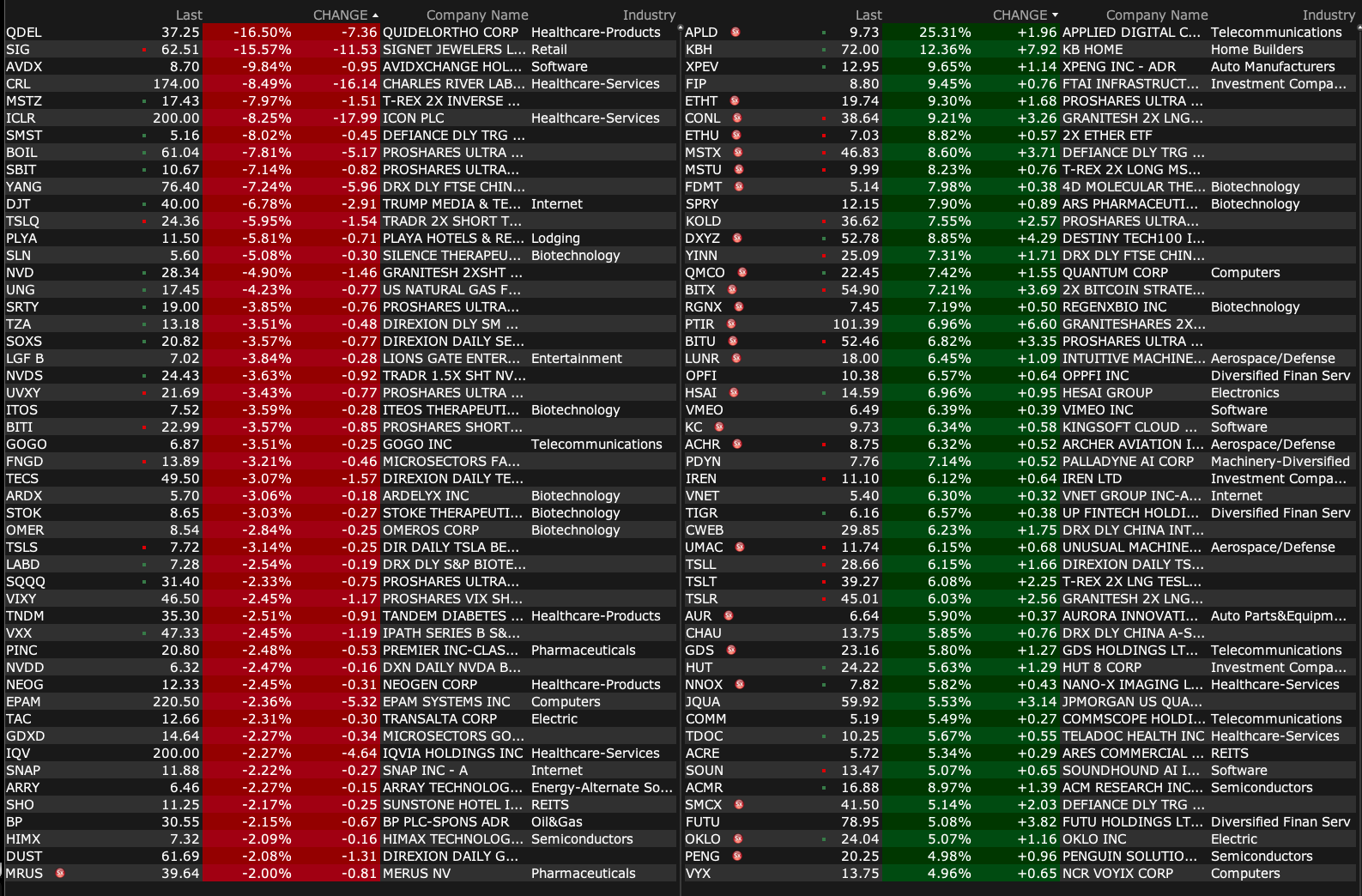

This is a valuable table for momentum-based short-term traders:

BY Doug Kass · Jan 14, 2025, 8:20 AM EST

From JPMorgan:

US: Futs are higher on reports that Trump may use a gradual approach rather than to tariff deployment, perhaps more scalpel than broad sword approach with the market seems to like. With bond yields flat and USD weaker, both NDX/RTY futures are outperforming with Mag7 names all higher along with Semis. It does appear to be a broad-based rally today, into PPI and tmrw’s CPI. Cmdtys are seeing some profit-taking today with Ags/Energy lower, but Metals still bid up. Today’s macro data focus includes NFIB Small Biz Optimism, PPI, Federal Budget Balance, and 2x Fedspeakers.

and...

EQUITY AND MACRO NARRATIVE: Yesterday was a choppy session with stocks opening on the lows and closing in the green, near their highs. While bond yields moved higher, the USD was flat. Bloomberg reports that Speculative Traders are the most bullish on USD since 2019, based upon CFTS. Commodity prices are also stoking inflation fears. Today gives the first batch of inflation data ahead of Wednesday’s CPI print and the kick off of bank earnings, which will be important to see if broadening of the rally, that characterized much of 24H2 rally, can resume.

BY Doug Kass · Jan 14, 2025, 8:05 AM EST

and...

BY Doug Kass · Jan 14, 2025, 7:50 AM EST

In the big gap higher, following KBH's strong numbers, I markedly reduced my homebuilder longs. (KBH climbed by +$7!)

I am uncertain whether this was the correct move as last night's momentum certainly could follow thru today and over the next couple of sessions.

I reduced my holdings (for a reasonably good-sized and quick profit) based on price and my weekend analysis (and discussion with several homebuilders) that suggests the major publicly held builders will not benefit to the degree and speed I initially thought in filling the void left by the Los Angeles fire disaster.

As well, I was using this sector as a leveraged proxy for a reversal lower in interest rates — but just the opposite is occurring (rates are rising further) and TLT looks like it may make a new 52-week low and undercut the October 2023 support:

Importantly, home insurance premium rates are destined to gap higher — dampening affordability on a nationwide basis — potentially dulling demand for new homes at a time in which the rate of domestic economic growth could begin to fall.

Finally, here are some thoughtful comments from one of our subscribers (that I agree with):

cjsolus

Hey Doug ...question for you as you are building positions in homebuilders in reaction to the LA Fires...First, I think the insurance companies will try to weasel every inch they can grab in not paying claims... and Second, I think no insurance company worth their salt will underwrite homeowners policies going forward without a revamp of building code to mitigate any future issues with wildfires,.... does the cost of rebuilding (and I'm not talking multi-millionaire celebrities homes) normal residences just balloon to beyond affordable between reconstruction under new and what I would deem much higher replacement cost building codes vs homeowners current policies and future insurance premiums?? And let's not forget that we are in an inflationary environment currently just for normal costs of construction....As well as considering the very soon increase in Property taxes in those areas most affected from these catastrophic fires..?? Hopefully food for thought......

BY Doug Kass · Jan 14, 2025, 7:35 AM EST

From my 15 Surprises for 2025 (written in December 2024):

Deion Sanders leaves the University of Colorado and, he too, becomes an NFL head coach - replacing Mike McCarthy of the Dallas Cowboys.

Yesterday ESPN reported that Deion Sanders has been interviewed to coach the Dallas Cowboys! Cowboys' Jerry Jones has talked to Deion Sanders regarding HC position; Sanders finds opportunity 'intriguing' - CBSSports.com

BY Doug Kass · Jan 14, 2025, 7:20 AM EST

Yesterday equities rallied smartly off the morning levels on lower volume:

BY Doug Kass · Jan 14, 2025, 7:05 AM EST

Doomberg on The Bitter End.

BY Doug Kass · Jan 14, 2025, 6:55 AM EST

BY Doug Kass · Jan 14, 2025, 6:40 AM EST

Wolf Street howls about tariffs.

BY Doug Kass · Jan 14, 2025, 6:30 AM EST

I will be out of the office from about 6 a.m. to 9 a.m. as I have to take a family member for some routine xrays.

BY Doug Kass · Jan 14, 2025, 6:15 AM EST

I suspect yesterday's gap fill and reversal in the S&P Index was technically and market-structure inspired:

I don't trust the reversal.... and I have moved my gross exposure lower.

I am very modestly net long in exposure. This will not be a permanent condition but I have learned that throughout the market's advance of the last two years, temporarily getting off the short train is a reasonable strategy in short-term and deepening oversolds.

That said, on Monday I will have an updated Market Outlook.

In that update I conclude/guesstimate that the S&P could have an upside of only 5% in 2025, while the downside may be in the -10% to -15% range. Therefore, downside exceeds upside by 2-3x over the next 12 months.

BY Doug Kass · Jan 14, 2025, 6:05 AM EST

BY Doug Kass · Jan 14, 2025, 5:50 AM EST

The S&P Short Range Oscillator remains oversold at -3.96% vs.-3.73%.

I currently have no Index positions on.

BY Doug Kass · Jan 14, 2025, 5:40 AM EST