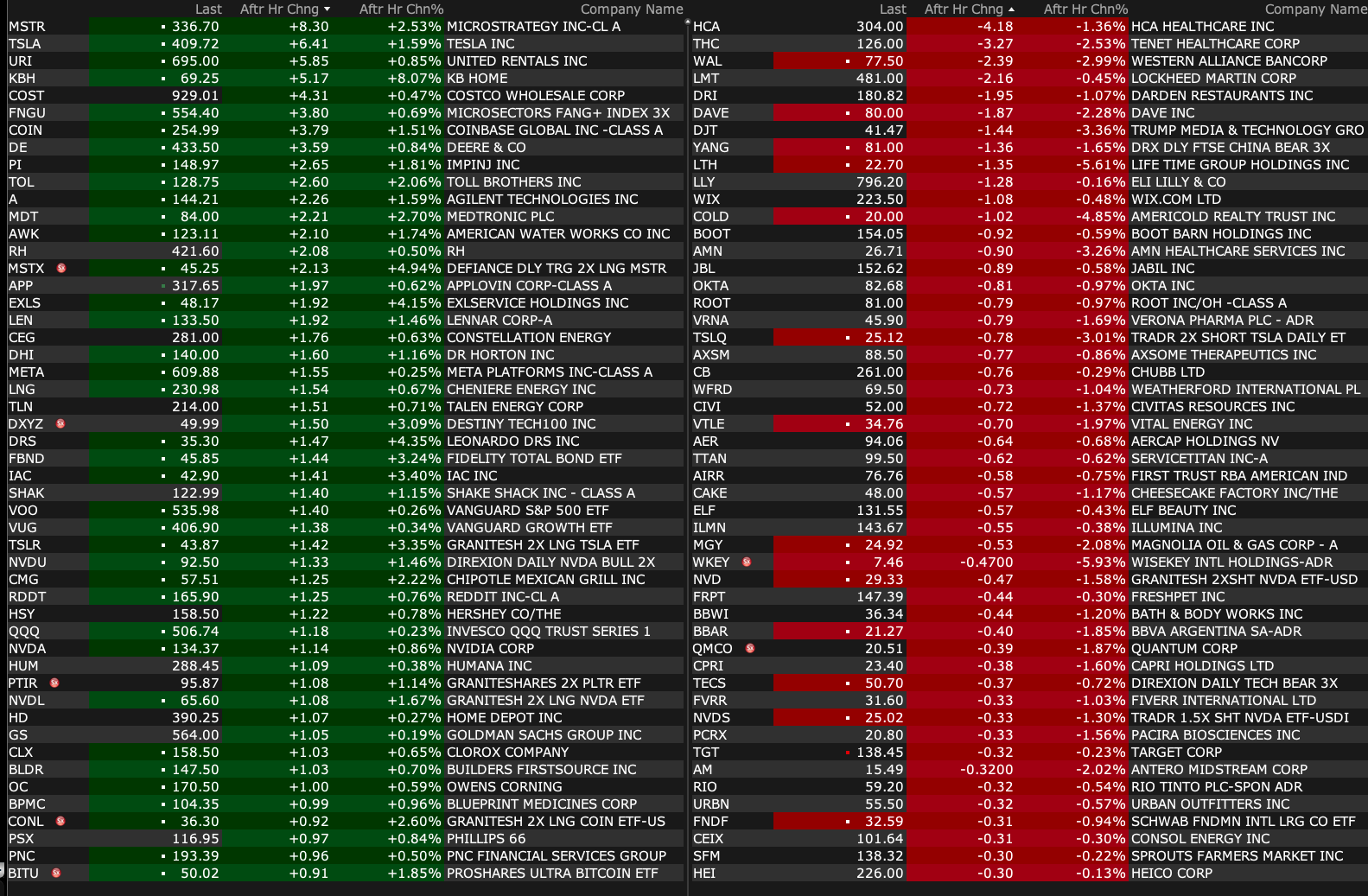

After-Hours Movers

At 5:30 p.m.:

BY Doug Kass · Jan 13, 2025, 5:42 PM EST

At 5:30 p.m.:

BY Doug Kass · Jan 13, 2025, 5:42 PM EST

Big beat at KB Home KBH, taking entire sector higher.

BY Doug Kass · Jan 13, 2025, 4:25 PM EST

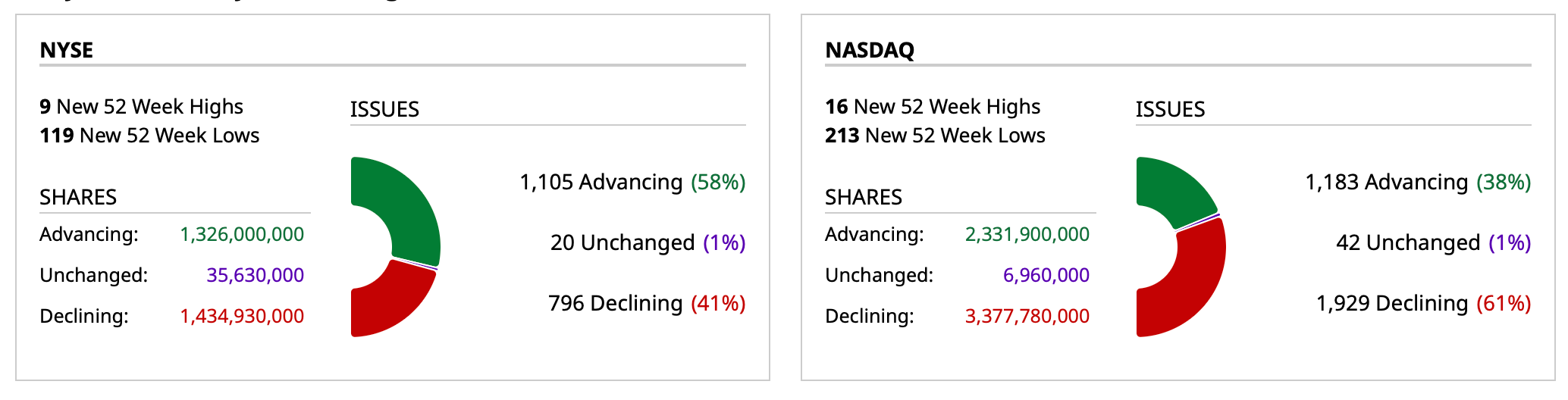

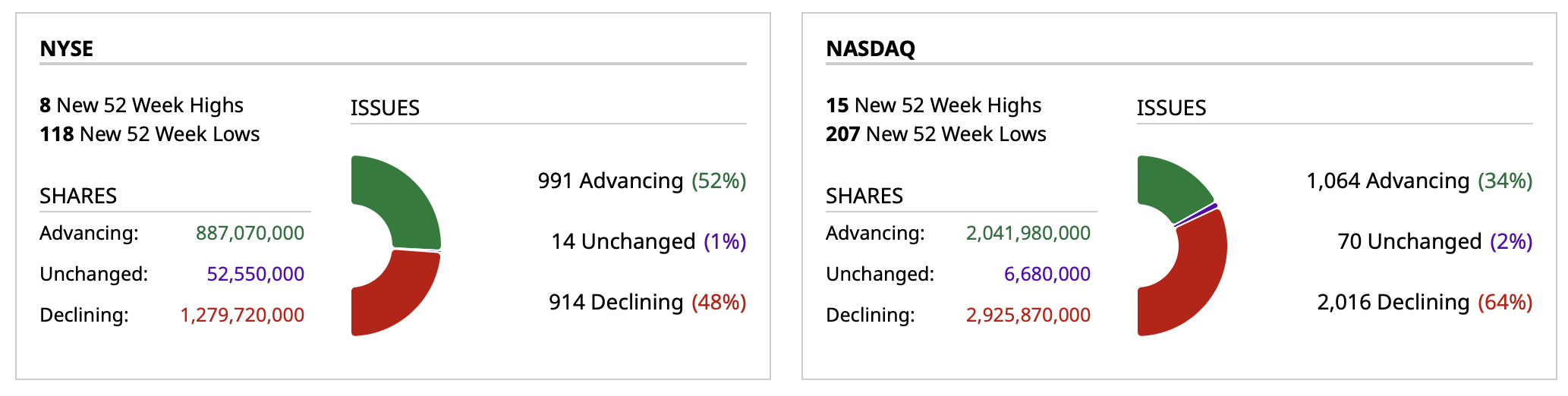

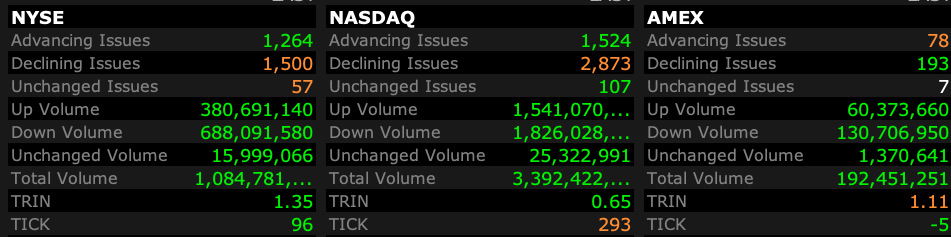

Close to the 4:00 p.m. close:

- NYSE volume 7% above its one-month average

- NASDAQ volume 6% below its one-month average

- VIX index: down 1.89% to 19.17

BY Doug Kass · Jan 13, 2025, 4:11 PM EST

A nice rally off the morning lows but breadth stinks up the joint and volatility continues apace.

Breadth is conspicuously weak on the Nasdaq (flat on the NYSE):

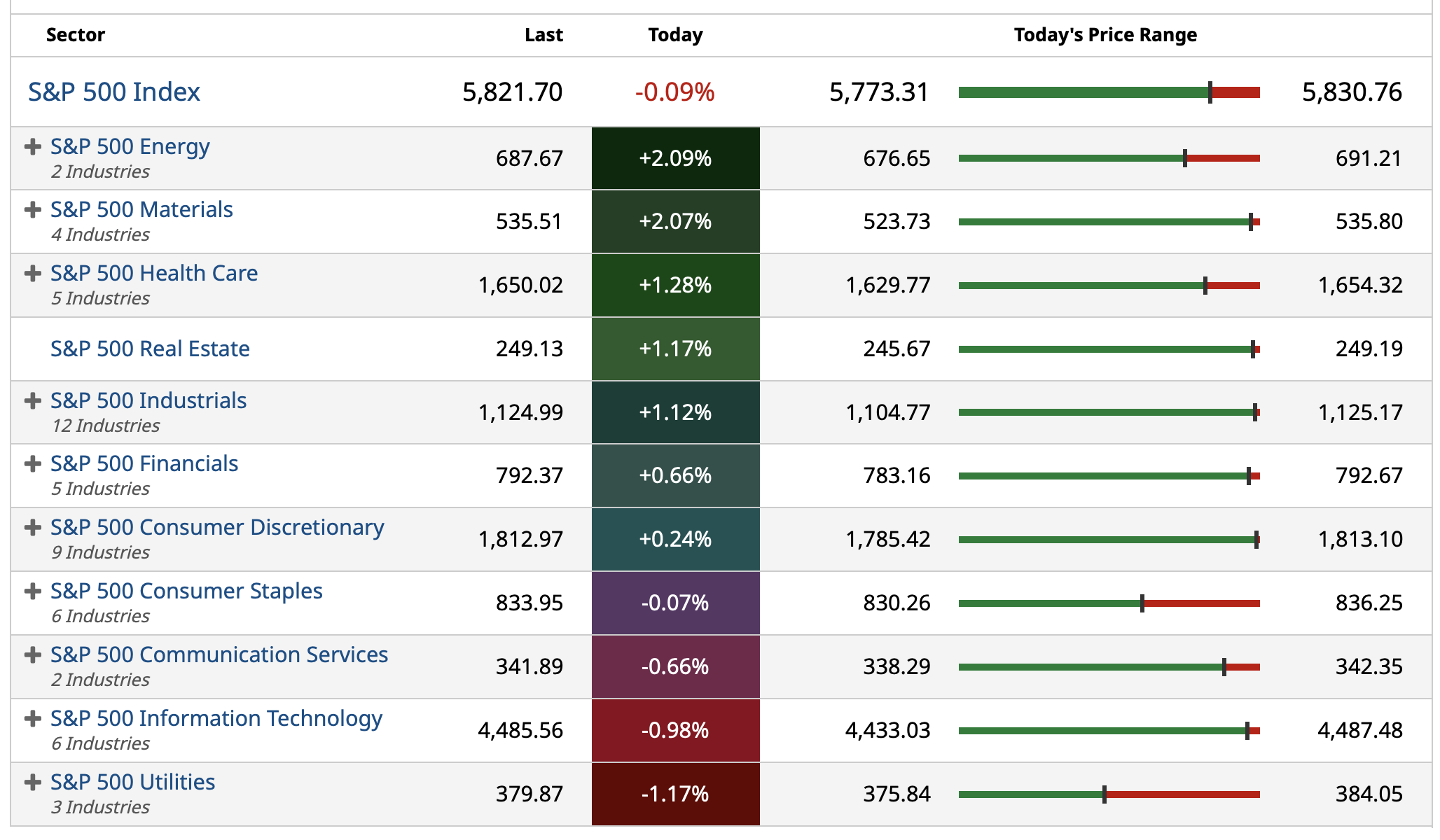

At 2:30 p.m. S&P cash is down by only -8 handles.

Here are today's "Things":

* I added across the board to early morning weakness in cannabis — MSOS at $3.44, TCNNF at $4.78, TSNDF at $0.535.

* I day traded SPY and QQQ for a gain.

* Initiated GRBK.

BY Doug Kass · Jan 13, 2025, 2:45 PM EST

I reinitiated a long position in Green Brick Partners GRBK today.

BY Doug Kass · Jan 13, 2025, 2:35 PM EST

I just go off the phone with one of "the "Goat(s)," Lee Cooperman.

Lee sees a parallel between President Reagan and former President Trump.

Reagan adopted three principles when elected:

1. Get government off the backs of Americans by cutting taxes and reducing red tape — ergo, simplifying the government.

2. Restore the lost prestige of our country by rebuilding our defense.

3. Balance the budget.

Reagen found he could not accomplish items #1 and #2 and keep the budget balanced — so he gave up #3 as an objective.

Similarly, Trump is trying to accomplish the same things that Reagan tried to.

But like Reagan, Trump will not be able to accomplish his goals and, he too, (when threatened by the bond vigilantes) will give up the concept of balancing the budget.

So, bond prices at risk and with interest rates likely climbing in the year ahead... equities will continue to be challenged.

Color Lee, cautious on both stocks and bonds.

BY Doug Kass · Jan 13, 2025, 1:40 PM EST

Bonds rallying (and at high of the day), adding to homebuilders.

BY Doug Kass · Jan 13, 2025, 1:27 PM EST

I'm adding to individual cannabis equities, bidding for more ELAN and a number of homebuilders.

BY Doug Kass · Jan 13, 2025, 12:25 PM EST

I have added to my already large MSOS long at $3.44.

BY Doug Kass · Jan 13, 2025, 12:20 PM EST

From Charlie!

BY Doug Kass · Jan 13, 2025, 12:10 PM EST

Getting my sea legs back.

BY Doug Kass · Jan 13, 2025, 12:00 PM EST

BY Doug Kass · Jan 13, 2025, 11:02 AM EST

I will be at a board meeting from 10 a.m. to about 11:30 a.m.

BY Doug Kass · Jan 13, 2025, 10:00 AM EST

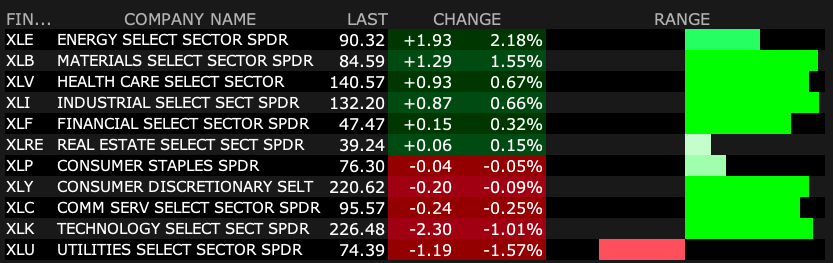

From Peter Boockvar

Many of the world's refiners, particularly those in China and India, that were previous to last week able to buy Russian oil are now scrambling to buy it from elsewhere after the newly implemented sanctions on the Russian energy space, particularly the ships that transport its oil. In response, the price of oil continues higher by almost $2 for both brent and WTI to a level last seen in July last year.

Helped by this rise in oil prices, along with natural gas, keep your eye on inflation expectations in the TIPS market as the 2 yr inflation breakeven as of Friday's close last fell on December 30th and is up 21 bps on this run to 2.74%. The move up in the 5 yr is higher in 8 out of the last 9 days and by 16 bps to 2.53%.

WTI

2 yr Inflation Breakeven

I argued a few times last year that central banks that were cutting rates, including the Fed and others, were all trying to catch the falling inflation knife. While inflation has decelerated notably, rather than wait until inflation was sustainably under control, many shifted their focus to their concerns with economic growth trends instead. Now of course they have a problem with the continued rise in long-term rates. This said, I do continue to believe that excessive debts and deficits are a key factor too in that the global bond police now are driving around the bad country neighborhoods with the stretched sovereign balance sheets.

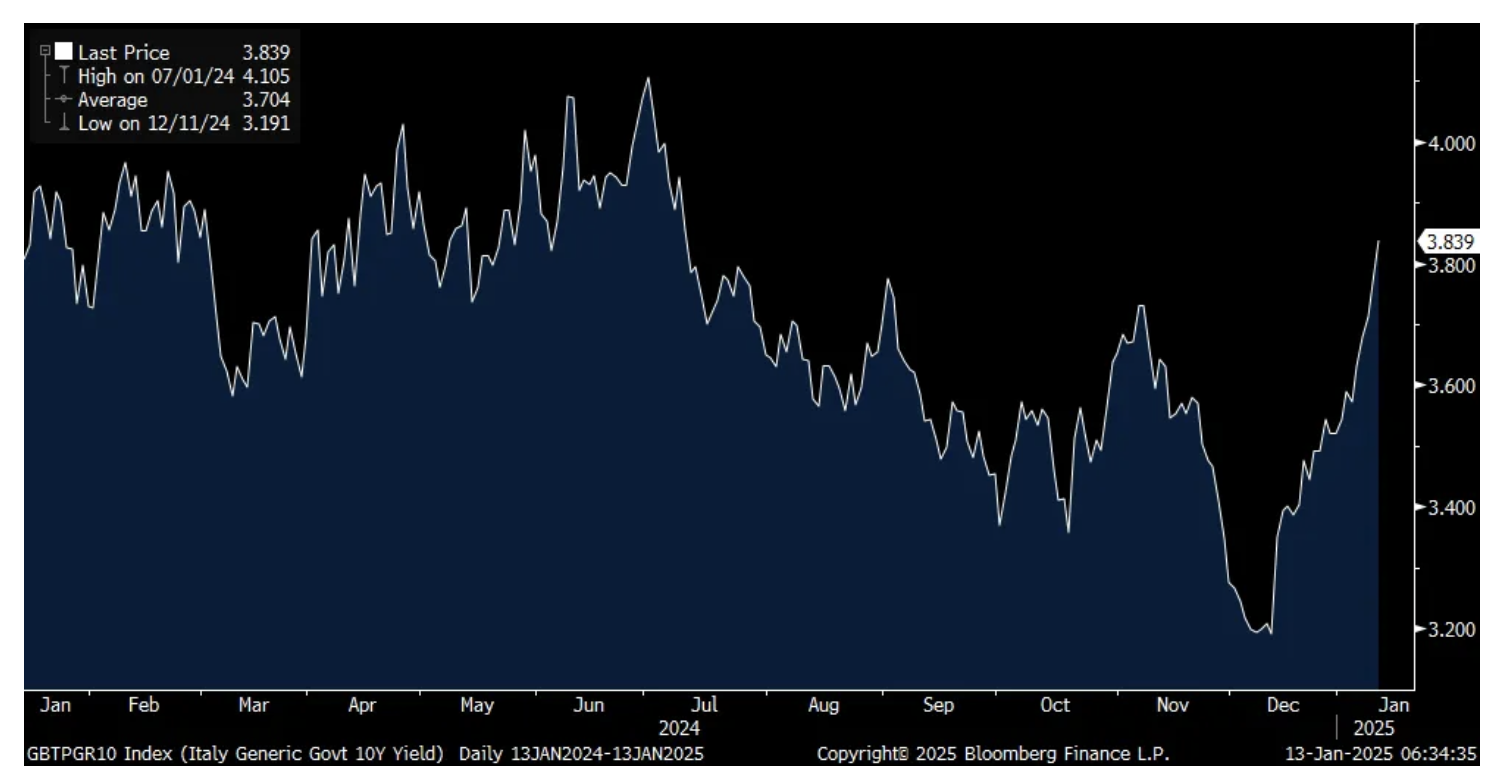

To highlight today, it is Italy's bonds which are selling off the most with its 10 yr yield up 7 bps to 3.84%, the highest level since July 2024.

Italy 10 yr BTP Yield

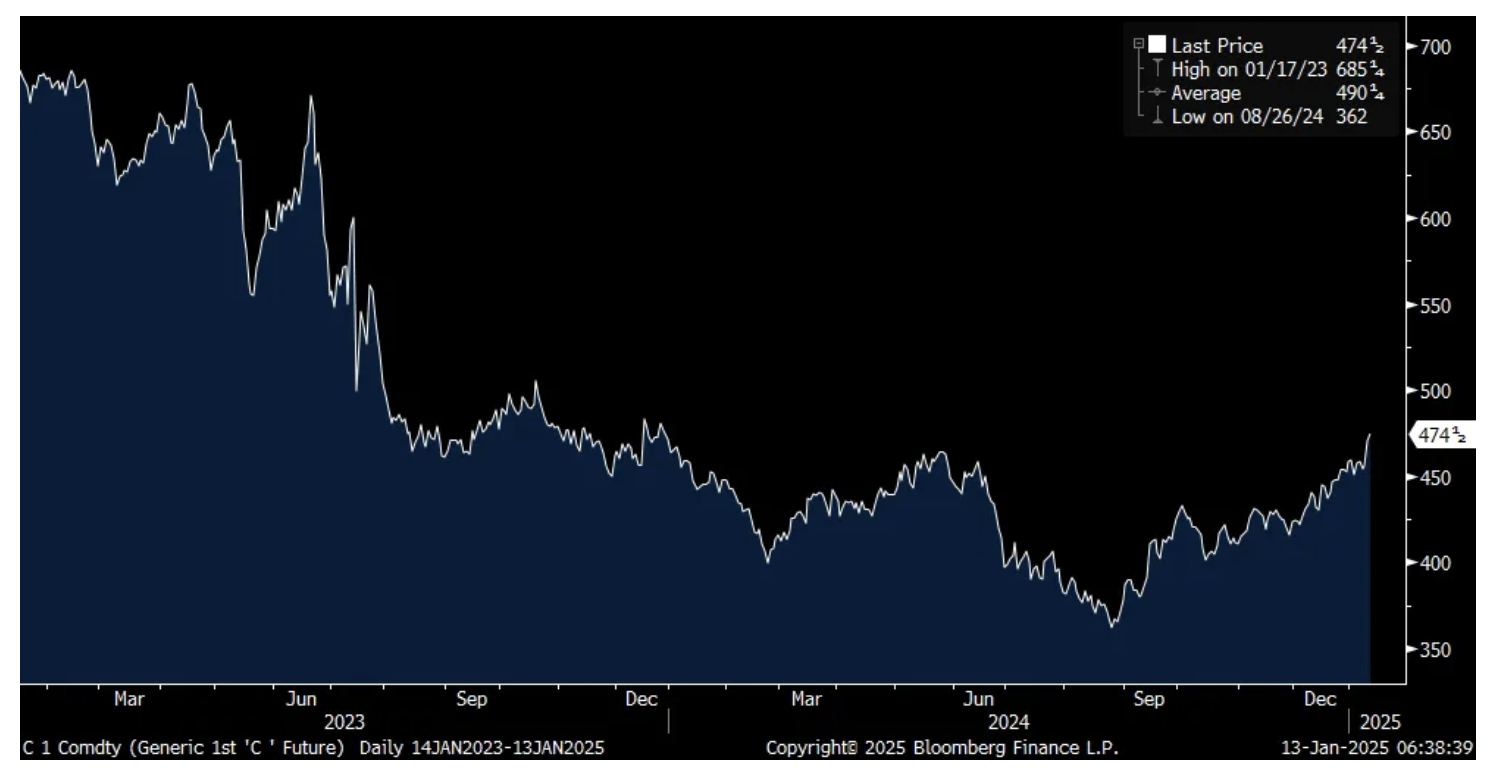

Over the last month we've seen record high prices in coffee and cocoa along with cattle too, helping to raise the price of beef. As I mentioned here just a few weeks ago, I've had my eye also on the main row crops of corn, soybeans and wheat to play catch up on the food upside. Today, corn is up 1% to the highest level since December 2023 and we continue to be long and bullish the fertilizer stocks that have been brow beaten. While corn is still well off its 2023 highs, as seen below, there is plenty of running room available.

Corn

Delta showed us last week that travel is still a bright spot in the US economy, and globally too. In Q4, they had "the largest December quarter profit in Delta's history (at $1.6 billion), improving more than $500 million over last year."

"The US consumer is financially healthy and continues to prioritize spending on experiences." I'll add, at least their customers are. "Closing out 2024, we saw an acceleration in air travel demand from corporates and consumers and co-brand card spending growth accelerated. This momentum is continuing into the March quarter, where we expect to grow the top line by 7% to 9%."

"Corporate sales grew 10% y/o/y, improving three points sequentially. Strength built through the quarter driven by both volume and fare with broad based strength geographically and across all sectors...Premium revenue performance outpaced main cabin throughout the year, up 8% over prior year with positive unit revenues in all four quarters of '24."

Of note on the pricing side, "Domestic demand remains robust with considerable improvement in the supply backdrop over the last few months as unprofitable supply is removed across the industry."

Finally, "We have good visibility into the spring and summer and expect another year of record profitability in our largest international entity."

From Walgreens and on their customer:

With respect to their retail business, "This has been made more challenging by the persistent deterioration in consumer discretionary spending. Our consumer remains under pressure from accumulated inflation and higher interest rates and we are seeing continued value seeking and channel shifting behavior."

Lululemon had a great holiday and raised guidance this morning. "During the holiday season, our guests responded well to our product offering, enabling us to increase our fourth quarter guidance."

Macy's lowered guidance.

Likely reflecting the rush ahead of the holidays and the pull forward before incoming tariffs, China's exports in December rose 10.7% y/o/y, above the estimate of 7.5%. Exports to the US rose almost 16% y/o/y, to the EU by 8.8%, to Southeast Asia by 19.2%, by 14% to Taiwan, 4% to South Korea but fell by 4.2% to Japan. Imports eked out a gain of 1% vs the forecast of a drop of 1%.

For the full year of 2024, China's trade surplus with the world rose to a record of $992 billion, helped by both strength in exports but also softness in imports. And China has continued to diversify their exports away from the US. The yuan is little changed in response and the strength of their exports shows that China does not need a weaker currency, though we'll see what happens after they get a new round of tariffs this year.

BY Doug Kass · Jan 13, 2025, 9:40 AM EST

-SAGE +37% (BIIB offers to acquire company for $7.22/shr or ~$469M total)

-ITCI +35% (confirms to be acquired by Johnson & Johnson at $132.00/shr in $14.6B deal)

-OPCH +15% (earnings, guidance)

-DCTH +12% (reports prelim Q4 revenue)

-HHH +9.9% (Bill Ackman: Propose Pershing Square holdco to acquire Howard Hughes at $85/shr in cash or cash/stock)

-ENFN +9.1% (to acquired by Clearwater for $11.25/shr in $1.5B cash and stock deal)

-FOLD +8.8% (reports Q4 revenue)

-DXCM +5.8% (guidance)

-LZ +5.7% (JPMorgan Chase and Co Raised LZ to Overweight from Underweight, price target: $9)

-NTRA +5.1% (earnings, guidance)

-X +4.1% (confirms Committee on Foreign Investment in the United States granted an extension of deadline to abandon the Merger Agreement to June 18, 2025)

-XENE +4.1% (outlines key milestone opportunities for 2025: Topline data from the first Phase 3 FOS study anticipated in H2 2025)

-AEO +3.9% (guidance)

-LULU +3.2% (guidance)

-FIVE +2.7% (reports holiday period SSS, issues guidance)

-AIRS -32% (cuts guidance)

-MRNA -20% (reports prelim FY24 product sales, cuts FY25 guidance)

-IRBT -13% (guidance)

-RGTI -13% (quantum computing weakness continues)

-ANF -11% (guidance)

-SWTX -11% (reports prelim Q4 revenue; Rappta Therapeutics enters into a global license agreement with SpringWorks Therapeutics for a pre-clinical first-in-class molecular glue targeting PP2A)

-TEM -6.0% (reports prelim Q4)

-IONQ -5.5% (announces new $21.1M project via Qubitekk, Inc. to work with the United States Air Force Research Lab)

-CAL -5.4% (cuts guidance)

-EW -4.4% (downside momentum)

-OSW -4.1% (guidance)

-REGN -3.9% (reports business updates, reports Eylea sales)

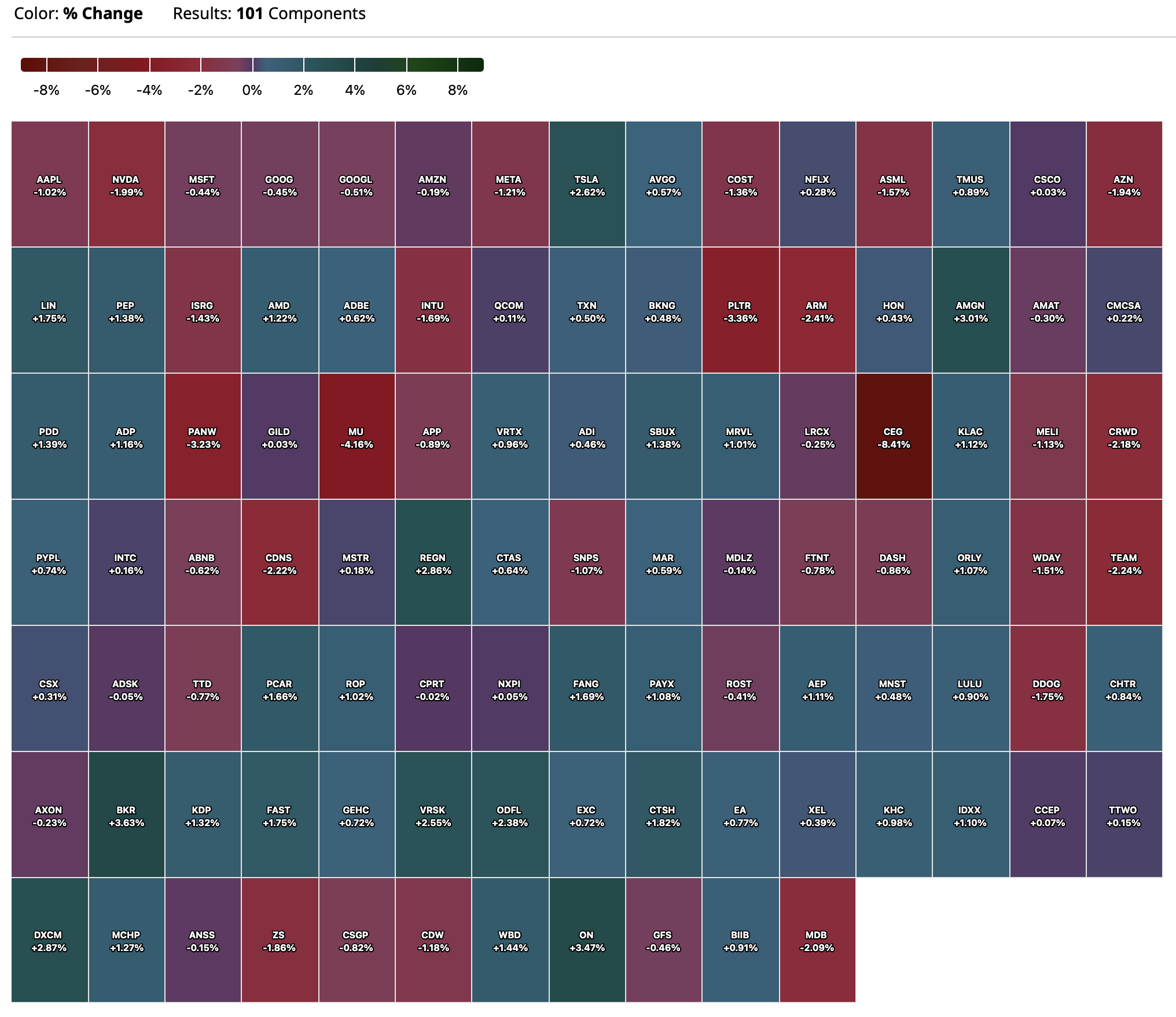

-NVDA -3.2% (White House confirms global curbs on exports of AI chips by Nvidia and its peers)

-M -2.5% (guidance)

-MU -2.5% (files to sell senior unsecured notes of indeterminate amount)

-PINS -2.5% (Jefferies Cuts PINS to Hold from Buy, price target: $32)

BY Doug Kass · Jan 13, 2025, 9:26 AM EST

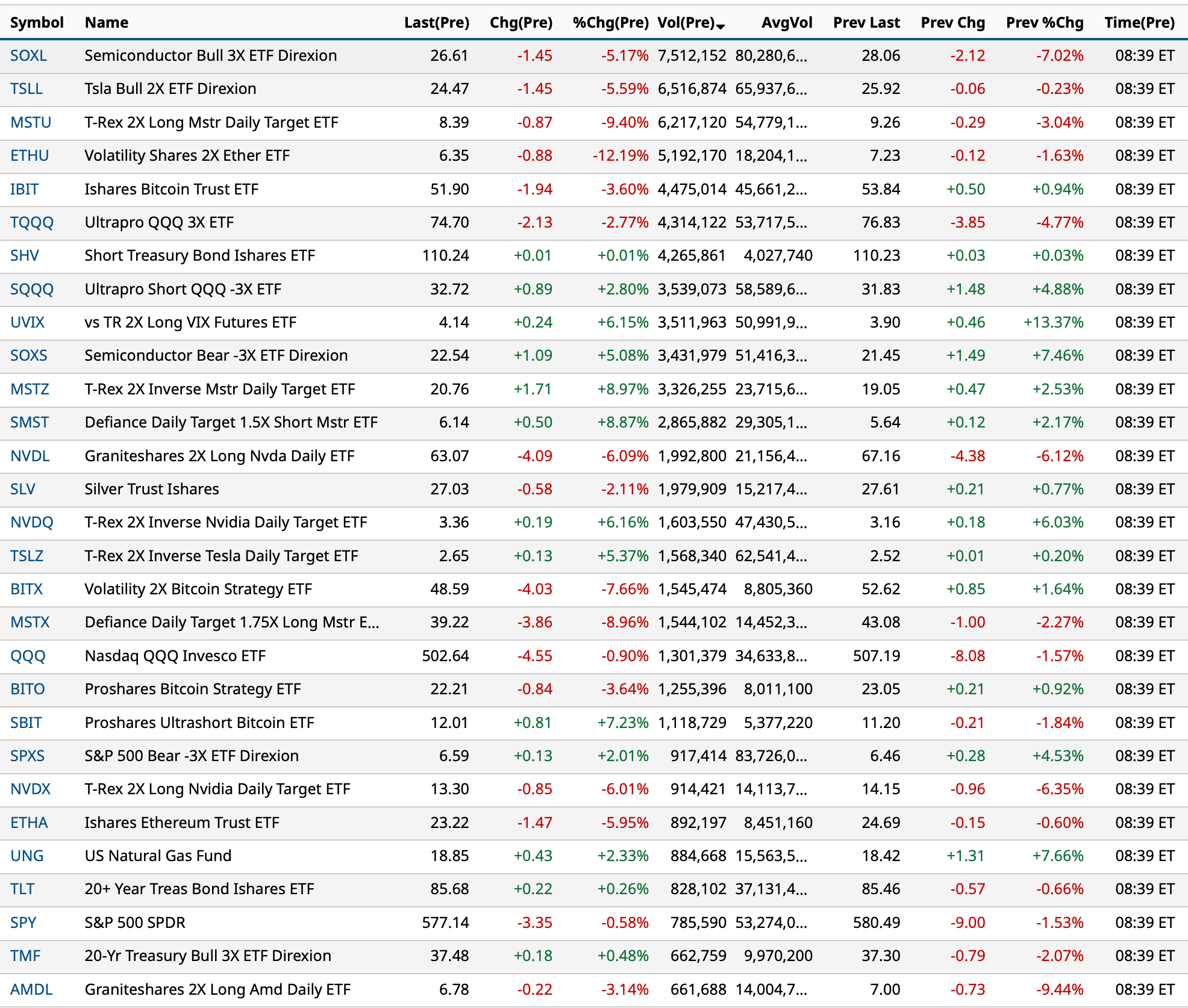

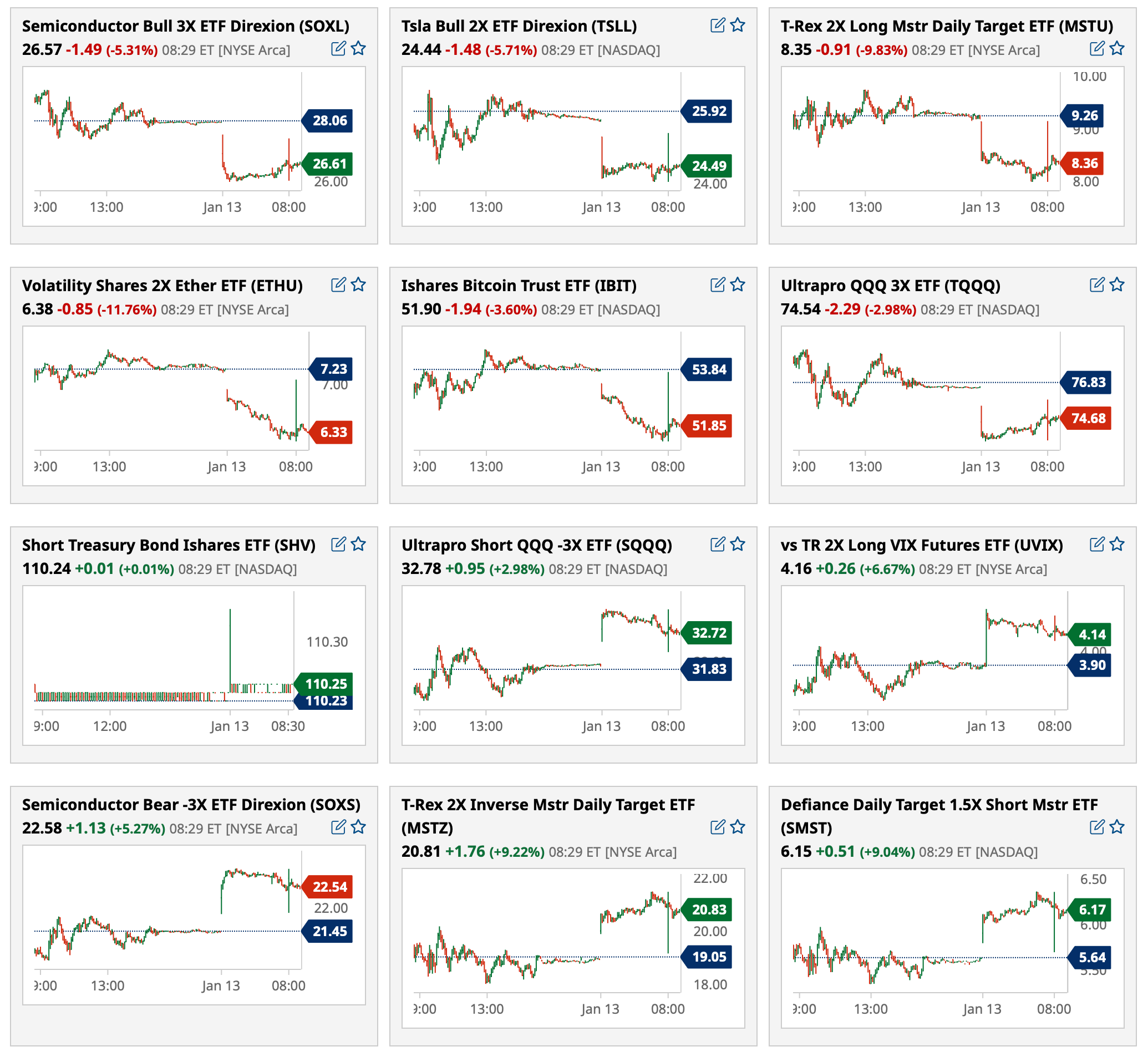

The most active premarket ETFs at 8:39 a.m. ET:

BY Doug Kass · Jan 13, 2025, 9:15 AM EST

Premarket percentage movers at 8:56 a.m. ET:

BY Doug Kass · Jan 13, 2025, 9:06 AM EST

* Back in 1992 while running the research and institutional equity departments at First Albany I wrote the first sell-side research report on St. Joe Paper.

* St. Joe is my largest individual equity long... and my choice for the "stock of the year."

* Praetorian Capital's Harris Kupperman attaches a very high NAV ($250/share) to this real estate company — compared to its current share price of $45.

I am always doing bottom up-analysis in the search for attractive long and shorts.

Ideally, especially with longs, I try to identify asymmetric opportunities in which upside reward dwarfs the downside risk.

If my and Kuppy's analysis are correct, The St. Joe Co. JOE is a vivid example of the fruits of that search.

St. Joe is now my largest individual long.

What follows is a recent JOE analysis from my pal Kuppy:

Since I’m doing book reports this quarter, I want to briefly mention JOE, which comprised 12.5% of our capital at year-end, and was our third largest detractor on a Dollar basis. I tend to focus on hard assets with strong tailwinds, as those assets offer downside protection, with plenty of upside in what I believe to be an inflationary decade. JOE has both of these aspects in spades (tailwinds and asset value).

Let’s look at the tailwinds.

As JOE owns a disproportionate percentage of the undeveloped land in Southern Bay, Gulf and Walton Counties, in Florida, along with substantial business operations there, let’s discuss those counties’ growth briefly, as real estate is tied to population and economic activity. I believe that there is no better, nor cleaner metric for both population and economic growth, than the growth in passenger traffic at Northwest Florida Beaches International Airport (ECP). Since 2019 when 1,275,488 people flew through the airport, traffic is up by 30.1% as of 2023 when 1,660,479 people flew through ECP, with traffic up an additional 13.5% this year over 2023, as of November. Clearly, this is impressive growth, and it doesn’t even track the rapid growth of private planes, which tend to be core JOE customers. The Florida Panhandle is a rapidly growing part of the nation, and JOE is in the driver’s seat in terms of how it is developed. By developing it intelligently, JOE doesn’t only add value to each development, but they add value to their massive landbank and all future developments that they undertake. There is a real multiplier effect here and I think that many investors miss this.

As a value investor, I always ask myself what something is worth today, and what it can be worth tomorrow. Valuing JOE’s income producing properties is relatively easy. I can get deep into the math here, but for the sake of simplicity, let’s assume their existing business operations (including full and partial ownership in 12 hotels with 1,298 rooms, multiple multi-family and senior living properties with 1,383 units, 1,179,000 square feet of other commercial space, a clubs business, marinas and a bunch of other assets like self-storage, a gas station and a shooting range) are worth approximately $2 billion, net of the cash and debt on the balance sheet. Then, at the year-end market cap of $2.6 billion, you’re buying approximately 168,000 acres of land in Florida, much of it waterfront, for approximately $3,600 an acre, net of the commercial real estate. I can assure you that this is the wrong price. In fact, I think there’s a genuine agreement amongst investors that this is the wrong price—the disagreement is in regard to the correct price.

I like to think in terms of big numbers. If you assume the Net Asset Value (NAV) of the company today is between $200 and $300 a share, then you can work backwards and calculate that I’m valuing the land at between $57,500 to $92,200 an acre, if you assume that everything else on the balance sheet nets to $2 billion. Looking around at recent transactions on the County Clerk’s website, I have pretty good confidence that this range of outcomes is directionally correct and could be on the low side of things. Of course, JOE has plenty of acres that are worth less than $57,500, but they also have acres that are worth a few million each, which drag the average up rapidly. For the sake of argument here, let’s just accept that my math is correct, and using $250 a share as a midpoint of NAV is accurate.

Having lived in Florida for 17 years, I have seen land in Florida appreciate rapidly. Maybe not every year, and there were a few down years during the GFC, but for the most part, land in Florida, especially land near the water, appreciates rapidly. As a shareholder, I assume this remains the case as the population of Florida, and particularly Bay, Gulf and Walton counties grows. If you assume that this collection of land and operating assets appreciates at 10% a year, which would be roughly the sum of the percentage changes in population growth and the CPI in the counties where JOE has investments, then it would imply that the NAV should appreciate by $25 next year, before the company earns a cent from running their recurring cashflow businesses, or reinvests a cent into new development.

Once you add in about two dollars of anticipated cash flow each year, and some value creation on the development side, I feel pretty confident in saying that the NAV can appreciate by $30 next year. Given the year-end share price of $45, that would represent an appreciation of 67%, which is quite attractive in my book. Naturally, this isn’t a one-and-done situation—I expect this sort of NAV appreciation to be an annual phenomenon, though it will be somewhat lumpy and track the economic cycle to a certain extent. Of course, as we’ve learned repeatedly over the past few years, the returns for the stock and the returns for the NAV can remain divergent.

While frustrating to us in 2024, I’m trying to predict long-term value creation, and I remain confident that the shares will one day accrete towards NAV. I’ve had frequent meetings with management, who I think are excellent, over the four years that we have owned our shares. I’ve implored them to close this discount to NAV with buybacks, and they’ve done some occasional buybacks, but they’ve mostly focused on developing the land that they have. At first, I found this frustrating, now I’m more accepting.

Let’s return to the math again. Let’s say they had bought back $100 million of shares during 2024 at an average price of $50, or at 20% of NAV, that would have been incredibly accretive. They would have created $400 million of incremental NAV value for everyone!! Amazingly, there’s something else that they could do that would be more accretive. Imagine if they instead spent $100 million on building a new hospital (the first in the region), along with a new marina, town center, restaurants, etc., all amenities that retired people likely desire when they are researching about where to retire (JOE built all of these things in 2024). To be more accretive than buybacks, JOE would need to add more than $400 million in value to their land through these investments.

Do I think these improvements have added approximately $2,400 per acre in incremental value to the 168,000 acres they have ($400 million / 168,000 acres = $2,400)?? Of course!! Their land has probably appreciated by far more than $2,400 an acre. How can you sell high-end homes to retired people when the nearest hospital is over an hour away?? Even better, these amenities are going to produce cash flow, allowing the company to continue to reinvest at an even more rapid pace in the future. In summary, buybacks are nice, but developing property is even nicer, as we get added cash flow, value uplift on successful developments (trust me, that concrete and steel is worth a lot more than the $100 million they spent on it), and value uplift on the surrounding 168,000 acres as well. The problem with this is that while the stock market is usually correct over long periods of time, it is lazy and downright stupid over short periods of time.

Since we started buying shares of JOE throughout 2020 at approximately $20 per share, the shares have appreciated by 122%, but I feel strongly that NAV per share has appreciated even more rapidly. One day, this valuation gap will close, but without more aggressive buybacks, this may take some time.

As noted in the case of Valaris, I’m perfectly fine to be patient and wait for the market to notice what I take for granted. Of course, nothing is ever linear, and you may be wondering why the shares of JOE have performed so poorly in the last few months of 2024. I can point you to rising interest rates, a US housing slowdown (which doesn’t appear to have really impacted JOE) and other macroeconomic factors, but the primary cause of the price decline is JOE specific.

Funds managed by Bruce Berkowitz currently own 29.7% of JOE. These funds have continually sold shares, and that has capped the price of JOE over the past few years. When Bruce chose to resign as Chairman of the company, after a 13-year stint where he successfully oversaw the turnaround at JOE, shareholders panicked that his funds would accelerate their pace of share sales. I see this as a short-term concern. Shareholders periodically sell shares. The long-term business prospects are not impacted by this. I focus on the long-term here. If Bruce chooses to sell additional shares after they’ve already declined by approximately 30% from the 2024 peak, then that just seems like a buying opportunity for us, and the company, should they choose to become more aggressive on their buyback. As this book report is now getting quite long-winded now,

Here is Kuppy's complete letter to investors. Q4 2024 Investor Letter

BY Doug Kass · Jan 13, 2025, 8:05 AM EST

* I have published about fifty "More Tales" thus far...

This article is interesting.

Healthcare oddly is one of the easier applications too for AI/Machine Learning, because there is quite a big dataset of if A, then B, which is also somewhat static. Human language and behavior, for example, has less logic and predictability to it than how the body behaves.

And yet healthcare AI works poorly, is very expensive, and frankly it seems dangerous if the output is poor, and it is not understood as being poor by the user. You cannot blindly follow it. At least for a query on ChatGPT, you can double check everything, if you are smart (and then you will find you have spent more time than just doing it the old-fashioned way while your query cost ChatGPT a bunch of money because they lose money hand over fist providing the output).

Can the AI be sued for malpractice? If it can, it is in big trouble based on its history of writing legal briefs. What is the point if it makes everything more expensive, and yields a poor/high risk output?

"Everybody thinks that AI will help us with our access and capacity and improve care and so on," said Nigam Shah, chief data scientist at Stanford Health Care. "All of that is nice and good, but if it increases the cost of care by 20%, is that viable?"

https://abcnews.go.com/Health/health-care-ai-intended-save-money-turns-require/story?id=117564598

BY Doug Kass · Jan 13, 2025, 7:55 AM EST

I sold my Index trading long rentals for small gains:

At:

* SPY $576.70

* QQQ $502.15

BY Doug Kass · Jan 13, 2025, 7:43 AM EST

BY Doug Kass · Jan 13, 2025, 7:15 AM EST

I wish I was not so prescient with this Surprise...

From my 15 Surprises for 2025 (written in December 2024):

Inflicting $250 billion-$500 billion in damages (roughly 10-times worse than Hurricane Katrina in 2005), the property and casualty industry is unprepared for such a catastrophic storm. With insufficient reserves and a move to forestall financial contagion, one of the top ten property and casualty companies is bailed out by the U.S. government.

The multi-year move to move away from globalization and towards reshoring in the U.S. backfires as another natural disaster (Covid being the first in early 2020) wrecks and disrupts supply chains in our country and causes another inflationary spike (already abetted by the wage inflation incurred from the deportation policy of the new Administration)).

A dramatic reset higher in natural disaster insurance pricing harms home prices across the country — serving to contain the rise in commodities and finished goods inflation. But with consumers questioning the value of their largest asset (their homes) coupled with a mortgage rate over 8%, consumer confidence collapses.

BY Doug Kass · Jan 13, 2025, 7:00 AM EST

Bonus — Here are some great links:

* Highest Bond Yields in a Year, Quantum Compute Rug Pull, & VIX at 20

BY Doug Kass · Jan 13, 2025, 6:41 AM EST

I was interviewed on Berkshire Hathaway BRK.A BRK.B in the Wall Street Journal over the weekend.

Warren Buffett Prepares His Middle Child for the Job of a Lifetime - WSJ

BY Doug Kass · Jan 13, 2025, 6:15 AM EST

* Trading opportunistically....

With S&P futures -52 handles (5:15 a.m.), I have taken a small trading long rental in the indices:

* SPY $575.51

* QQQ $500.52

BY Doug Kass · Jan 13, 2025, 6:05 AM EST

BY Doug Kass · Jan 13, 2025, 5:55 AM EST

Please read his entire thread:

BY Doug Kass · Jan 13, 2025, 5:45 AM EST