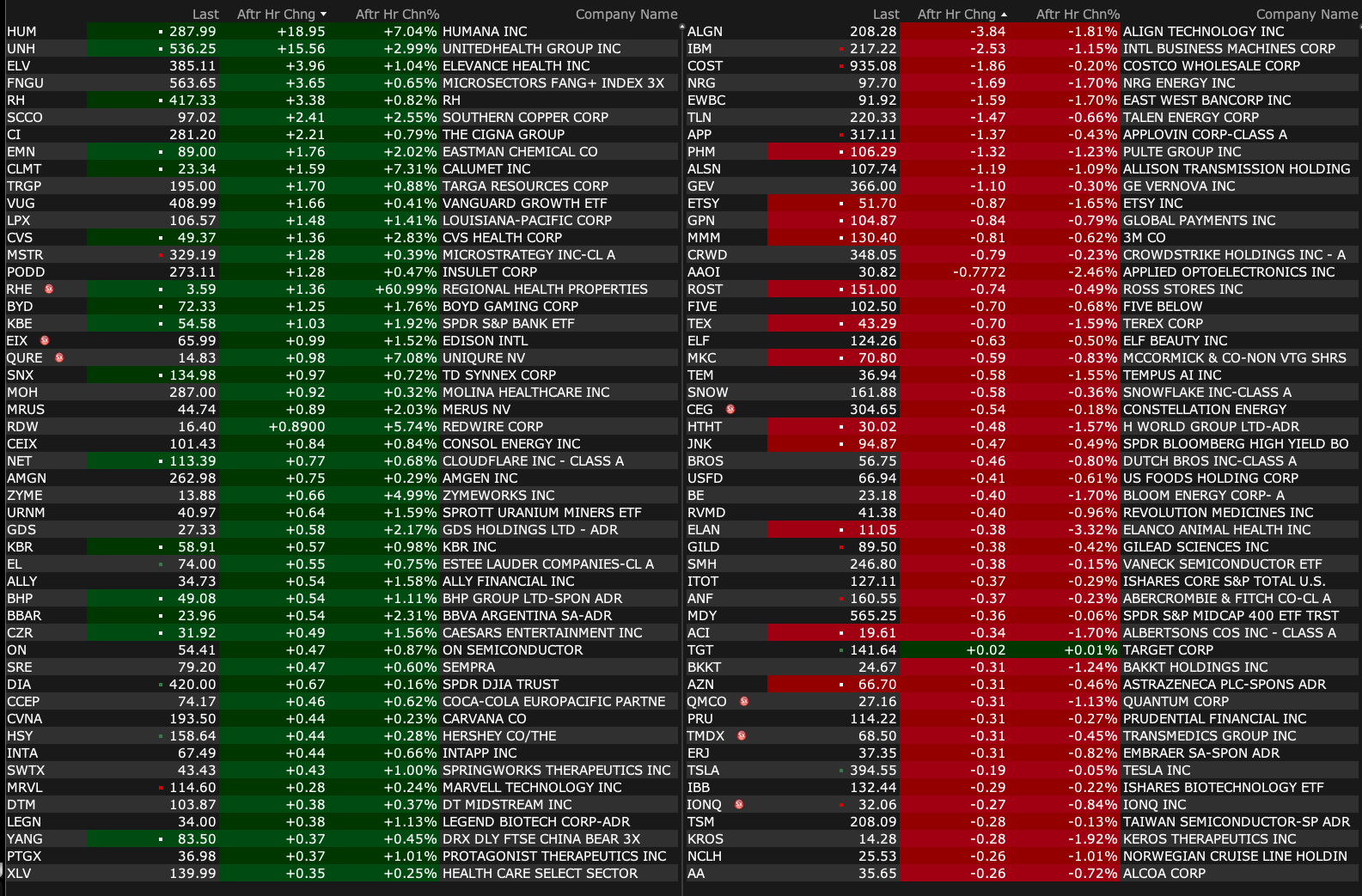

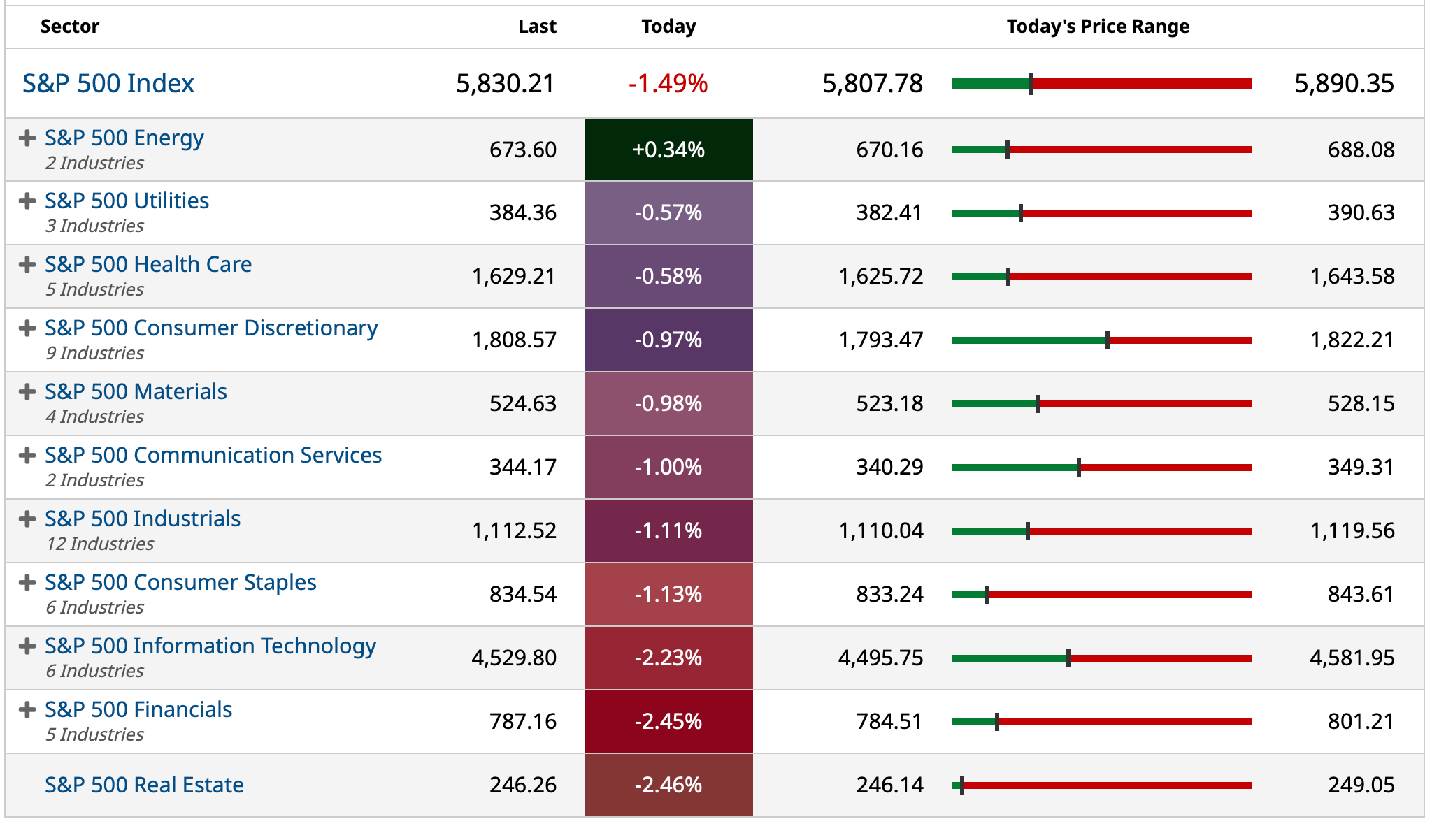

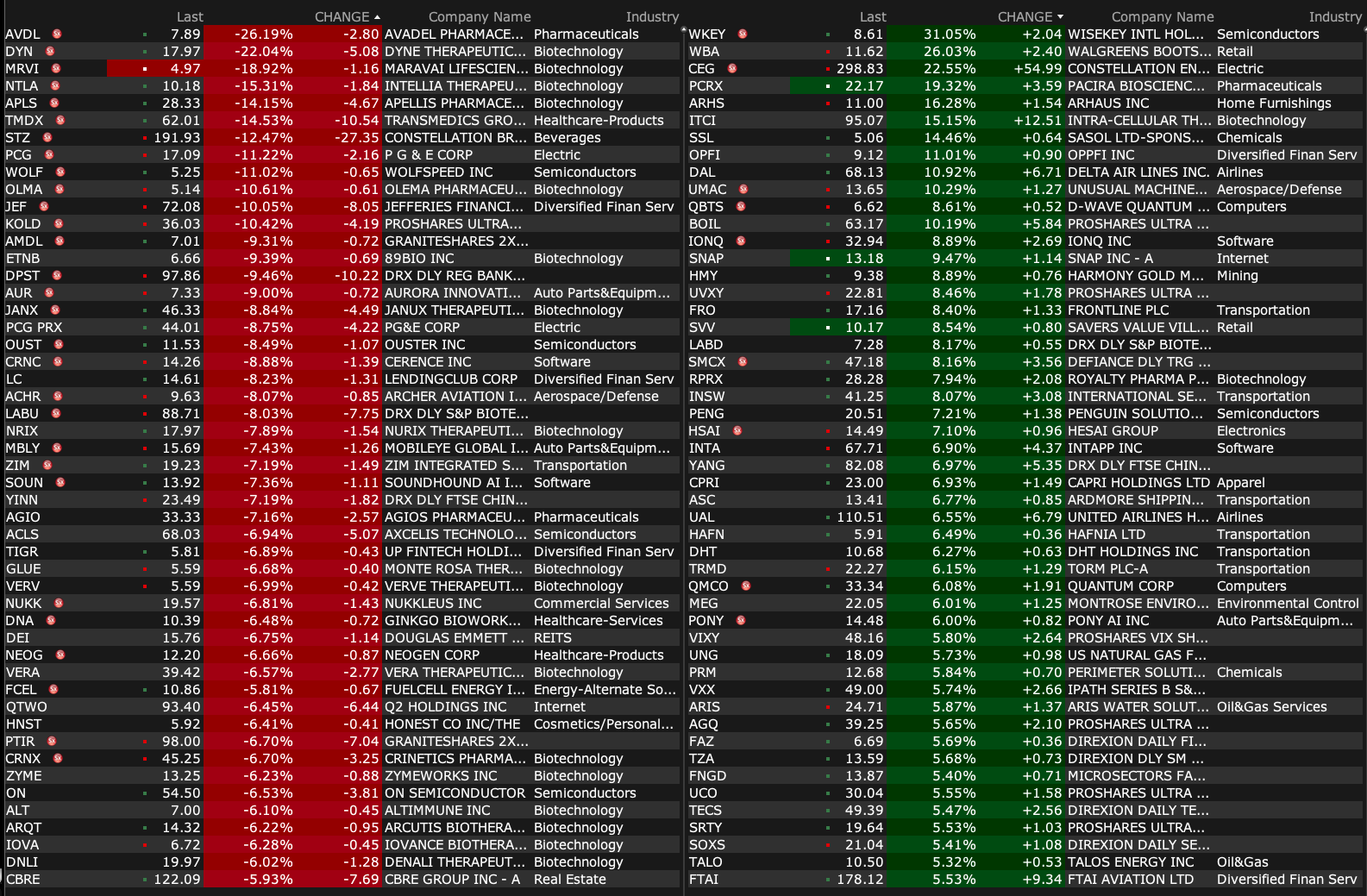

Friday's After-Hours Movers

BY Doug Kass · Jan 10, 2025, 4:50 PM EST

BY Doug Kass · Jan 10, 2025, 4:50 PM EST

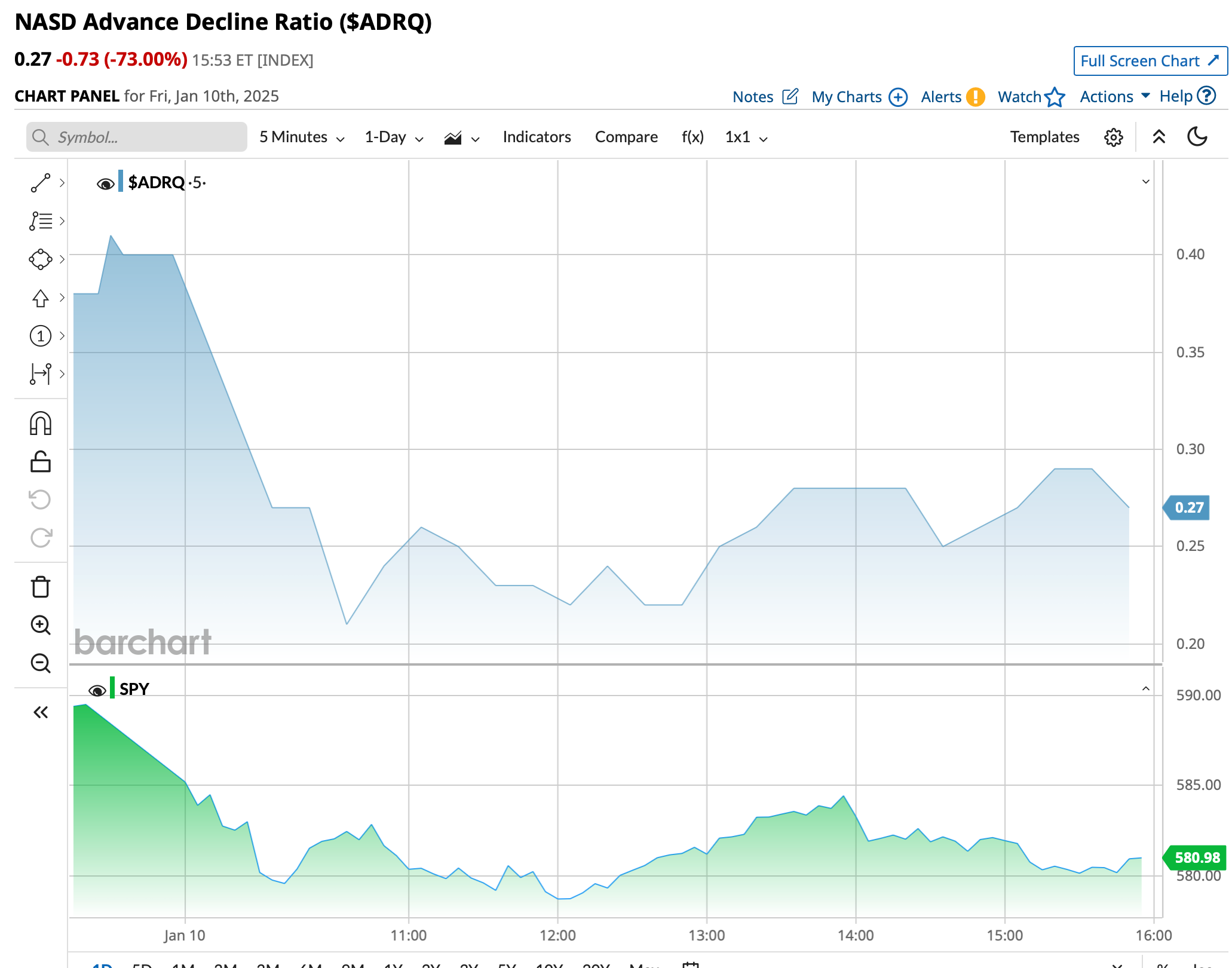

Advance-Decline vs SPY (intraday through closing)

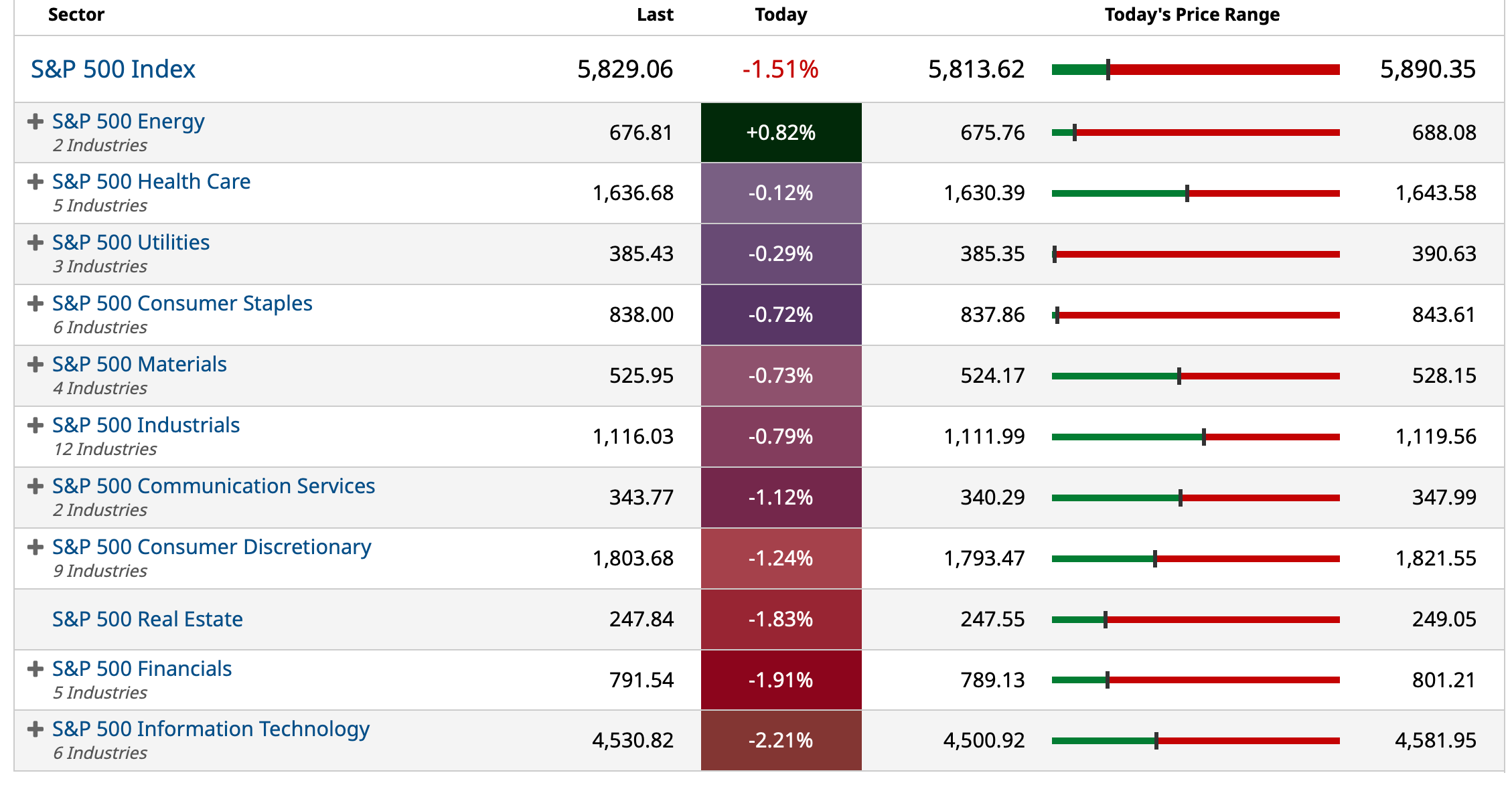

BY Doug Kass · Jan 10, 2025, 4:40 PM EST

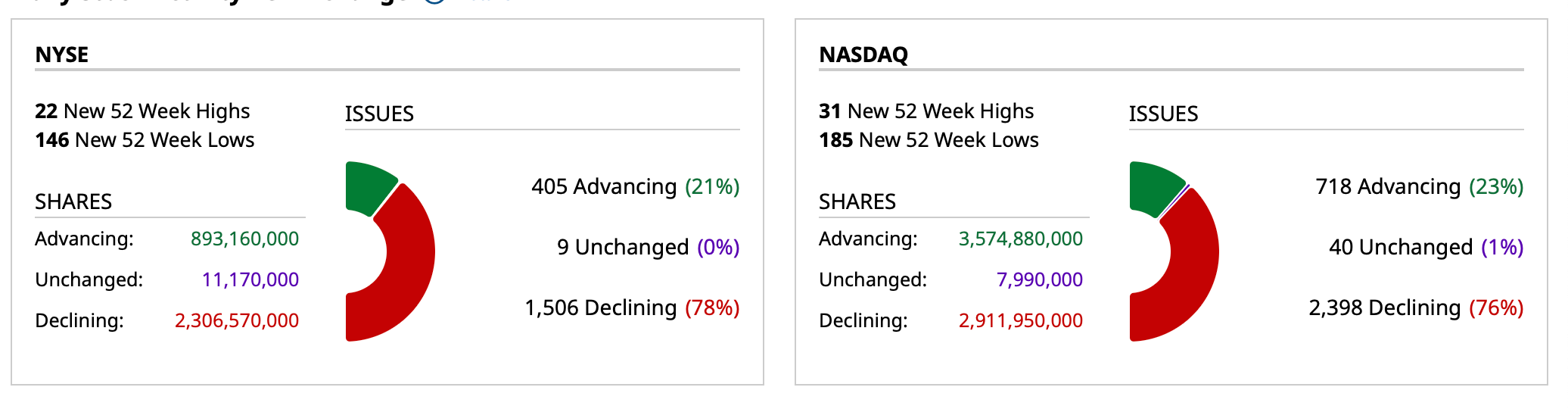

- NYSE volume 18% above its one-month average

- NASDAQ volume 6% above its one-month average

- VIX: up 8.14% to 19.54

BY Doug Kass · Jan 10, 2025, 4:27 PM EST

Thanks for reading my Diary today and all week.

Enjoy the weekend.

Be safe.

BY Doug Kass · Jan 10, 2025, 4:13 PM EST

The decimation in the consumer non-durable space over the last few weeks has been staggering,

I remain short Coca-Cola KO and made a mistake in covering my PepsiCo PEP short.

BY Doug Kass · Jan 10, 2025, 2:53 PM EST

From Peter Boockvar:

Positives

1)Job growth surprised to the upside with a headline gain of 256k vs the estimate of 165k with the private sector adding 223k of this. The two prior months were revised down by a total of 8k. Also, in the household survey, after very choppy hiring trends in the prior months, 478k net saw new jobs and exceeded the rise of 243k in the labor force which is why the unemployment rate fell to 4.1% from 4.2%. Almost half of this figure came from the 16-19 yr age cohort. The all in rate fell two tenths m/o/m to 7.5% which is the lowest since June. Hours worked at 34.3 was as expected as was the 62.5% participation rate. The rate for the 25-54 key age group was 83.4%, down from 83.5% last month. Average hourly earnings gains of .3% m/o/m were too as forecasted and the y/o/y gain was 3.9%.

2)Please take the jobless claims data with a grain of salt in the last week of December and the first week of January. That said, initial claims totaled 201k vs the estimate of 215k and vs 211k last month. Continuing claims were 1.867mm, about as expected.

3)Job openings got back above 8mm in November at 8.1mm from 7.84mm in October.

4)The December ISM services index rose to 54.1 from 52.1 and just above the estimate of 53.5. That compares with 56 in October. Notwithstanding the headline lift, in part because of the rise in Business Activity and supplier deliveries, the breadth of growth softened. Of 18 industries surveyed, 9 saw growth vs 14 in November and that is the least since June while 6 said their business is contracting vs 3 last month. The bottom line from ISM, “Many industries noted that end-of-year and seasonal factors were helping drive business activity or impact inventory management. Some of the increased business activity seems to have been driven by preparation for demand in the new year, or risk management for impacts from ports strikes and potential tariffs. There was general optimism expressed across many industries, but tariff concerns elicited the most panelist comments.”

5)From Commercial Metals: "A meaningful shift in business sentiment gives us hope that we may be nearing a turning point in our markets...optimism across many sectors has improved sharply over the last two months, driven by expectations for an improved regulatory environment, tax reforms, and policies to support US manufacturing and job creation. In particular, the outlook among construction firms has improved notably as evidenced by ENR's Construction Confidence Index, which recently hit its highest reading in over two years. I would also note that our recent conversations with customers indicate similar optimism about the future. Outside of the construction industry, both large and small businesses are feeling more confident about the months and quarters ahead."

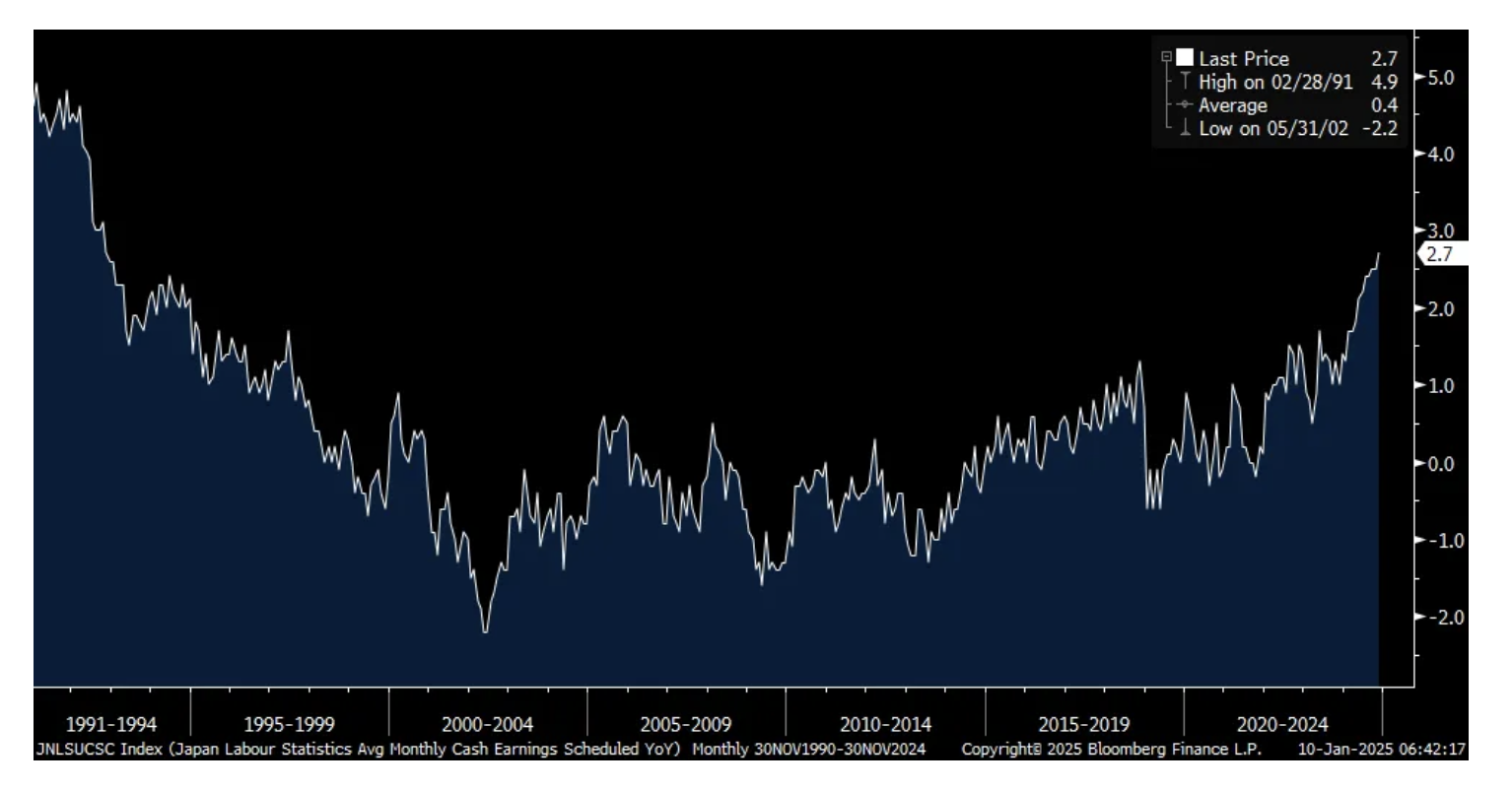

6)Base pay in Japan rose 2.7% y/o/y in November vs 2.5% in October and that is the quickest pace since November 1992.

7)The private sector focused Caixin China services PMI rose to 52.2 from 51.5. This is what Caixin said, "Business activity and total new orders increased for the 24th month in a row, with the former growing at the fastest pace since May, while the latter grew at the fastest clip since July. Overseas demand fell, however, with the gauge dropping to the lowest level since December 2022." Also of note, "Market optimism weakened. The indicator for expectations of future activity stayed in expansionary territory, but fell by more than 3 pts compared with the previous month, leaving it just above September's 4 ½ yr low."

8)Japan's final services PMI December read was 50.9 from 50.5 and India's services PMI remained strong at 59.3 from 58.4.

9)The services sector continues to keep the European economy afloat as its PMI was revised to 51.6 from 51.4 initially. That's up from 49.5 in November and vs the same 51.6 in October. An above 50 print for Germany offset the continued weakness in its manufacturing sector. Services in France remains weak but is strong in Spain and flat lining in Italy.

10)Services in the UK remained a bit above 50 at 51.1 vs 50.8 in November and 52 in October.

11)German industrial production in November surprised to the upside while exports were as expected.

12)China continues to see actual price stability in December with CPI up .1% y/o/y.

Negatives

1)The heartbreaking devastation to parts of LA.

2)The global interest rate rise continues.

3)ADP said a net 122k private sector jobs were created in December, below the estimate of 140k and vs 146k in November. They also said “The labor market downshifted to a more modest pace of growth in the final month of 2024, with a slowdown in both hiring and pay gains.”

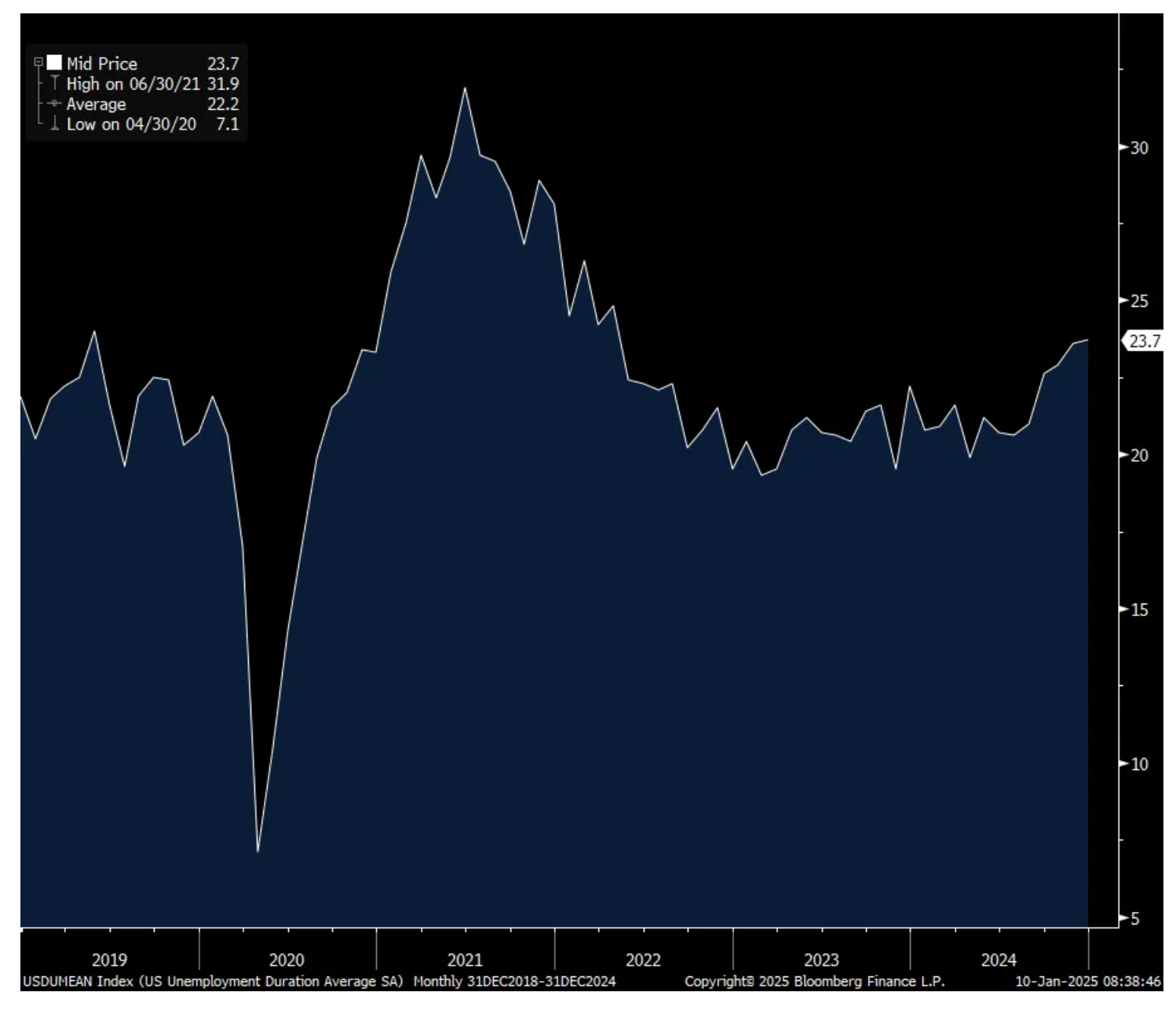

4)A fly in the BLS jobs data for December is that it’s taking longer to find work as the average duration of unemployment rose to 23.7 weeks, the highest since April 2022.

5)In the November JOLTS report, the hiring rate fell to just 3.3% from 3.4% and that is the lowest since 2013 not including Covid. Also of note, the quits rate fell to 1.9% which matches the lowest since 2014, also not including Covid.

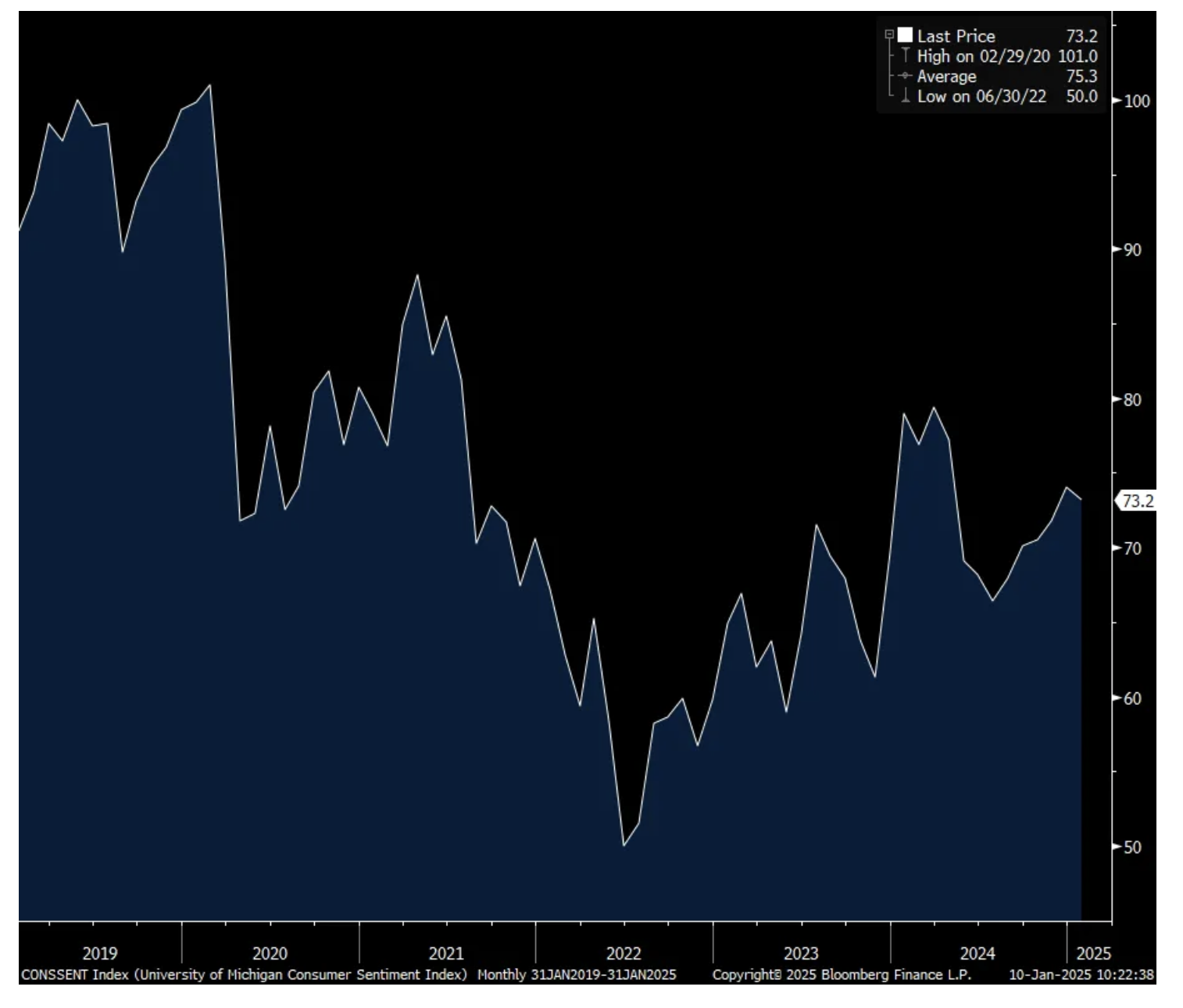

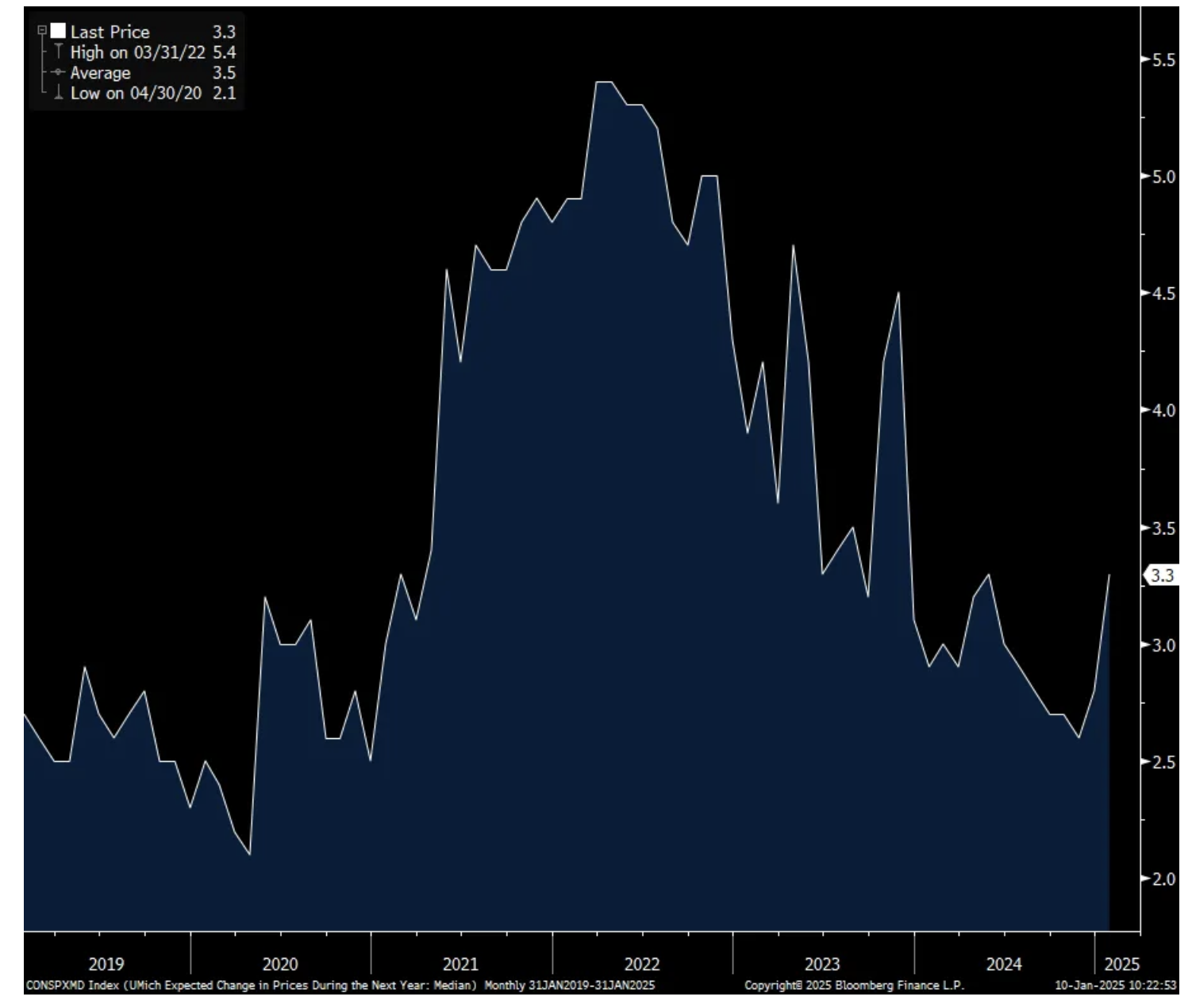

6)The first UoM consumer confidence read of the year comes in at 73.2 vs 74 in December and just below the estimate of no change of 74. The two key internals were mixed as Current Conditions rose 4.8 pts m/o/m but were offset by a 3.1 pt drop in Expectations. One yr inflation expectations jumped to 3.3% from 2.8% . That’s the highest since November 2023 and the 5-10 yr look also went to 3.3% from 3%. That’s the highest since 2008 and we can blame expectations for tariffs. The thing that stands out the most, especially in light of the big upside surprise in the December jobs report, was the employment expectations component which plunged by 17 pts to 66. The last time it was lower was in July 2009. Spending intentions were little changed m/o/m with 1 pt upticks for vehicles and homes and a 4 pt rise for a major household item.

7)With the continued rise in mortgage rates, purchase applications fell sharply for the 3rd straight week, by 6.6% and now down 15% y/o/y. That said, at the end and beginning of the year, the holidays always seasonally skew this data and I'd rather wait until next week for a cleaner read. Refi's stabilized after falling off a cliff in the last two weeks of 2024. Again, seasonally distorted.

8)From Helen of Troy: "We also continue to see the widely reported bifurcation in spending between higher income and lower income households. While holiday spending overall is up y/o/y, its driven by higher income consumers purchasing higher priced items, while lower income consumers continue to struggle, prioritizing necessities over discretionary goods."

9)From MSC Industrial Direct: "While it was a good start to the year, we're mindful that the near-term environment remains soft and our company remains in a transition period during fiscal '25…Automotive and heavy truck, primary metals, fabricated metals and machinery and equipment continue to be soft. Aerospace, while a net positive for us in the quarter, experienced a step down related to strikes that have since been resolved. Additionally, manufacturing and metal working related softness continues to be reflected in manufacturing index readings, which have now been contracting for 22 consecutive months."

10)From Apogee Enterprises: "non-residential construction remains challenging. Leading indicators such as the Architectural Billings Index have pointed to a contracting market for 20 plus months. We have and continue to see this softness in framing systems over the past several quarters and more recently with awards slowing in our Architectural Glass segment…The picture across different building types within non-res construction remains mixed. Interest rate sensitive sectors like office, commercial, lodging and multifamily housing have been weaker while verticals like education, healthcare and transportation continue to see growth."

11)From Commercial Metals: "Results in our North America Steel Group were impacted by economic uncertainty that has weighed on new construction activity and pressured steel pricing and margins. This was partially offset by strong late season demand for Rebar as job sites worked to catch up from days lost to weather disruptions earlier in the year…Though uncertainty related to the outcome of the US election has been resolved, questions remain about the future path of interest rates and the nature and speed of policy implementation by the incoming presidential administration. As a result of new construction projects being fewer and slower to award, competition has increased for the work that does come to the market, putting pressure on pricing and margins for our steel products. This hesitancy is widespread across most segments of the construction markets with the notable exception of publicly funded work such as infrastructure."

12)Economic confidence in the Eurozone in December weakened further to 93.7 from 95.6 and the estimate was for no change. That matches the lowest since November 2020. Manufacturing confidence led the decline, only partly offset by a gain in services confidence. Consumer confidence fell to the lowest since February and retail and construction were little changed.

13)The December Eurozone CPI rose from November but as expected. The headline rise was 2.4% y/o/y, up two tenths from the 2.2% seen in November. The core rate was higher by 2.7% y/o/y, no change with the prior month. Services inflation remains their issue as it was up 4% y/o/y vs 3.9% in November and 4% in October.

14)German factory orders dropped by 5.4% m/o/m, well worse than the estimate of a .2% decline. Weakness in big ticket items were the main culprit. Retail sales in Germany fell for a 2nd straight month in November.

15)Hong Kong's December PMI was 51.1, little changed with November's print of 51.2. Singapore's slipped to 51.5 from 53.9.

16)Reflecting price competition and challenges in parts of its manufacturing sector, PPI in China fell 2.3% y/o/y in December but about as expected.

BY Doug Kass · Jan 10, 2025, 2:09 PM EST

BY Doug Kass · Jan 10, 2025, 1:35 PM EST

I have a late lunch, back at 2:30 p.m.

BY Doug Kass · Jan 10, 2025, 1:25 PM EST

I'm now long another cannabis name, Trulieve TCNNF (under $5).

BY Doug Kass · Jan 10, 2025, 12:15 PM EST

Short report on TMDX this morning.

BY Doug Kass · Jan 10, 2025, 12:05 PM EST

From Peter Boockvar:

The first UoM consumer confidence read of the year comes in at 73.2 vs 74 in December and just below the estimate of no change of 74. The two key internals were mixed as Current Conditions rose 4.8 pts m/o/m but were offset by a 3.1 pt drop in Expectations. One yr inflation expectations jumped to 3.3% from 2.8% . That’s the highest since November 2023 and the 5-10 yr look also went to 3.3% from 3%. That’s the highest since 2008.

The thing that stands out the most, especially in light of the big upside surprise in the December jobs report, was the employment expectations component which plunged by 17 pts to 66. The last time it was lower was in July 2009 and yes, you should not believe the BLS report today as gospel as it will be revised many more times. Net income views did lift 3 pts but after being at -1 last month.

Spending intentions were little changed m/o/m with 1 pt upticks for vehicles and homes and a 4 pt rise for a major household item.

This is what the UoM said on the pop in inflation expectations, “inflation expectations rose across multiple demographic groups, with particularly strong increases among lower-income consumers and Independents…Inflation expectations are being shaped by beliefs about future policy. The share of consumers worried about the prospect of tariff hikes continues to rise. Nearly one-third of consumers spontaneously mentioned tariffs, up from 24% in December and less than 2% prior to the election. These consumers generally report that tariff hikes will pass through to consumers in the form of higher prices, thus pushing up their inflation expectations.”

The positive, “About 32% of consumers spontaneously cited high prices are weighing down their personal finances, down from 47% in August 2024 and the lowest seen since February 2022.”

On employment, “Half of consumers expect unemployment rates to rise in the year ahead, up from 40% last month and 31% a year ago.”

Bottom line, consumer confidence still remains almost 30 pts below where it stood in February 2020 when it printed 101 and we can of course blame the cumulative rise of almost 30% in inflation and now we have the inflation antenna still up as seen with the inflation answers. Also, that huge drop in employment expectations should temper those who actually believe in the headline BLS survey. Hiring is ok, it is just not as strong as the BLS says it is and I expect the future revisions to reflect this.

UoM

One yr Inflation Expectations

BY Doug Kass · Jan 10, 2025, 11:45 AM EST

- New York Stock Exchange volume is 30% above its one-month average;

- Nasdaq volume is 16% above its one-month average

- VIX is up 7.19% to 19.37

BY Doug Kass · Jan 10, 2025, 11:35 AM EST

Break in!

I have exchanged my entire TLT long position (selling at $85.7, I essentially broke even) and replaced with my growing homebuilder long.

While I still like the reward vs. risk in TLT, I believe I have more upside leverage if I am correct in my view of moderating U.S. economic growth... and, as noted earlier, I get the rebuild kicker in California.

BY Doug Kass · Jan 10, 2025, 11:25 AM EST

"Today's jobs report was strong makes me comfortable employment market is stabilizing at something near full employment"

- Federal Reserve Bank of Chicago Pres. Austan Goolsbee

More thoughts:

- Should not over index on single month

- Reiterates do not see jobs market as source of inflation

- Long rates moving up can't really be explained by an expected uptick in inflation; Would look at higher growth expectations and uncertainty around fiscal policies

- If conditions are stable and no uptick in inflation and full employment, rates should go down

- Reiterates that 12-18 months from now rates will be a fair bit lower if current expectations are met

- Fed does have to think about tariffs, and other nations' responses that impact prices; Will have to wait and see for concrete proposals on tariffs

- The issue would be determining if tariffs are a one-time shock or a persistent one

- Inflation looks sticky now due to the jump in CPI one year ago

- So far, don't see evidence of overheating in recent months

- Interest-rate sensitive parts of the economy do show the impact of Fed restraint, even if that is offset by things like business confidence

- If long interest rates started rising on the basis of inflation expectations, that would be a cause for concern

- Aggregate numbers like jobs are hard to interpret when productivity is moving around

BY Doug Kass · Jan 10, 2025, 11:20 AM EST

Buys: DHI $138.99, JOE $43.12, KBH $65.11, PHM $109.50,TOL $135.98/

Also TLT $85.03, ELAN $11.17, VRNOF $1.20, TSNDF $0.58

BY Doug Kass · Jan 10, 2025, 10:52 AM EST

* From a very very low base... I am taking advantage of this week's weakness and adding to my long positions

* More than just a January bounce?

"You can't get killed by falling off the curb."

-Grandma Koufax

I purchased cannabis equities in December for a January (tax-related) bounce.

Since then a number of factors have conspired to put continued pressure on the space:

* On Wednesday, a $70 million cannabis exchange-traded fund MJUS has announced its liquidation: "Amplify to Shutter Cannabis ETF as Industry Struggles Continue"

* Industry product price compression accelerated (in large measure due to the failure of Amendment 3 to pass in Florida. As previously noted, due to excess supply and disappointing demand, CuraLeaf (among others) discounted prices by 70% in December and by 40% in January (TheStreet Pro).

* Uncertainty about rescheduling: Read "New Evidence Shows DEA Opposes Marijuana Rescheduling And Should Be Removed From Hearings, Cannabis Groups Say - Marijuana Moment"

and...

* Analyst coverage is evaporating

Here is an important and thoughtful discussion between Shadd Dales, Anthony Farrell and CuraLeaf's Boris:

The fears and concern about forced selling of cannabis stocks may be overstated - especially as it relates to the ETF liquidation which precipitated Wednesday's share price weakness:

1.

2.

Today the cannabis industry faces an existential crisis.

For a number of years investors, analysts and managements have overstated the business opportunities, have grossly misinterpreted cannabis' total addressable market and have poorly forecast the industry's top- and bottom-line growth. For a number of years investors, analysts and management leaders have mistakenly anticipated the timing and substance of legislative breakthroughs.

As a reflection, the share price of the largest exchange-traded fund is now more than 95% lower than its all-time high. Indeed, there is no sector that has come near to performing as badly as cannabis equities have.

With dour investor sentiment, weak fundamentals, growing legislative concerns, lack of coverage and structural fears (of forced liquidations) -- cannabis share prices are falling to new lows. Remarkably, the industry's five top players now have a combined equity capitalization of under $5.5 billion. The next 10 largest market players are virtually all penny stocks. I am buying, because the factors at work above are clear events and developments that occur at or near important sector bottoms.

My trades might now become investments, because you can't get killed falling off the curb.

BY Doug Kass · Jan 10, 2025, 10:05 AM EST

I added to TLT at $85.03.

BY Doug Kass · Jan 10, 2025, 9:52 AM EST

From Peter Boockvar:

The bottom line with all the Fed speak this week along with the FOMC minutes is that their rhetoric matches up with no expected rate cut this month. In fact, you have to go out to the June fed funds contract to fully price in another rate reduction.

If this continues, we'll see if it impacts what the Powell says at the January presser. 'This' being the notable rise in some commodities of late.

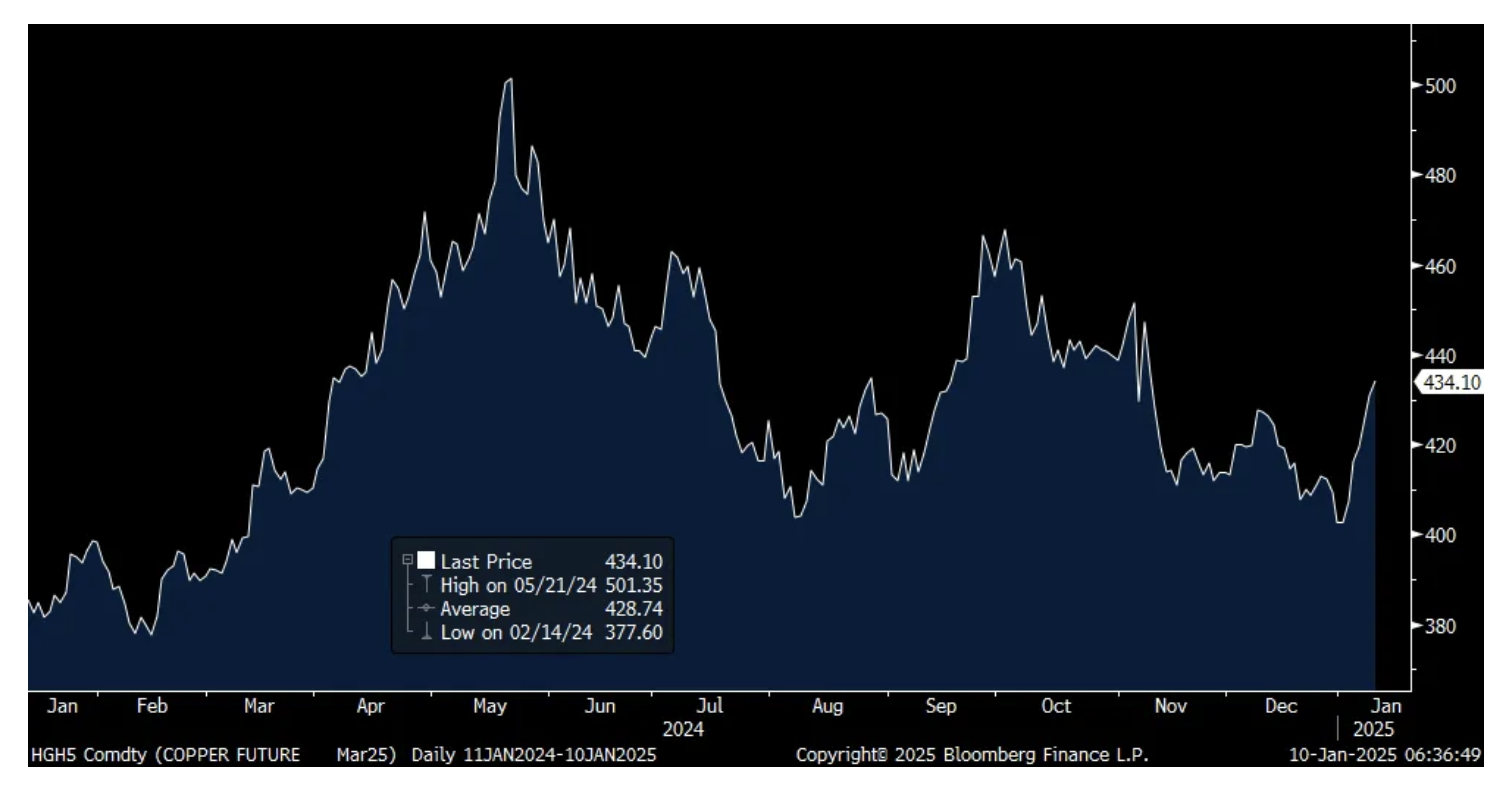

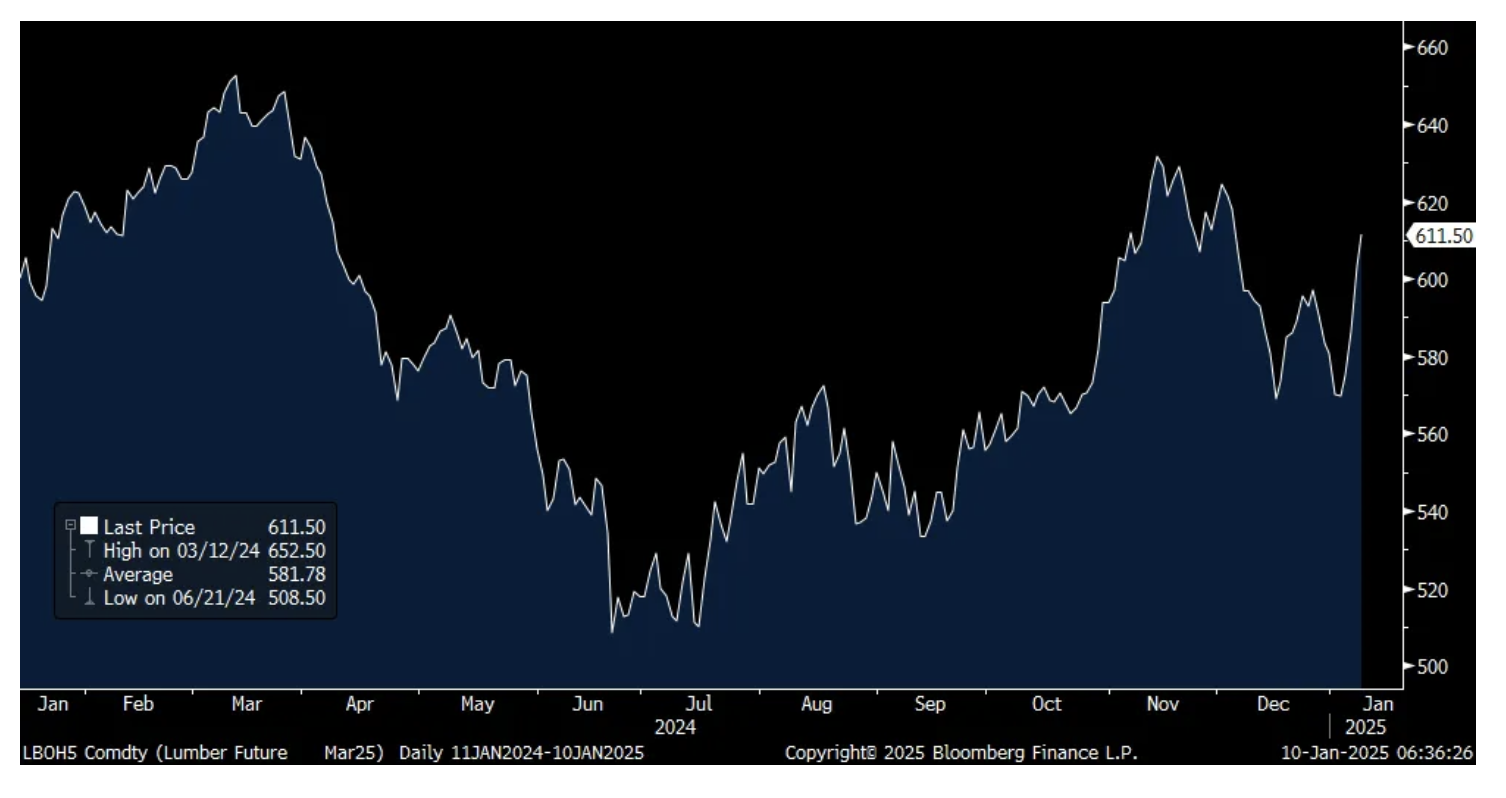

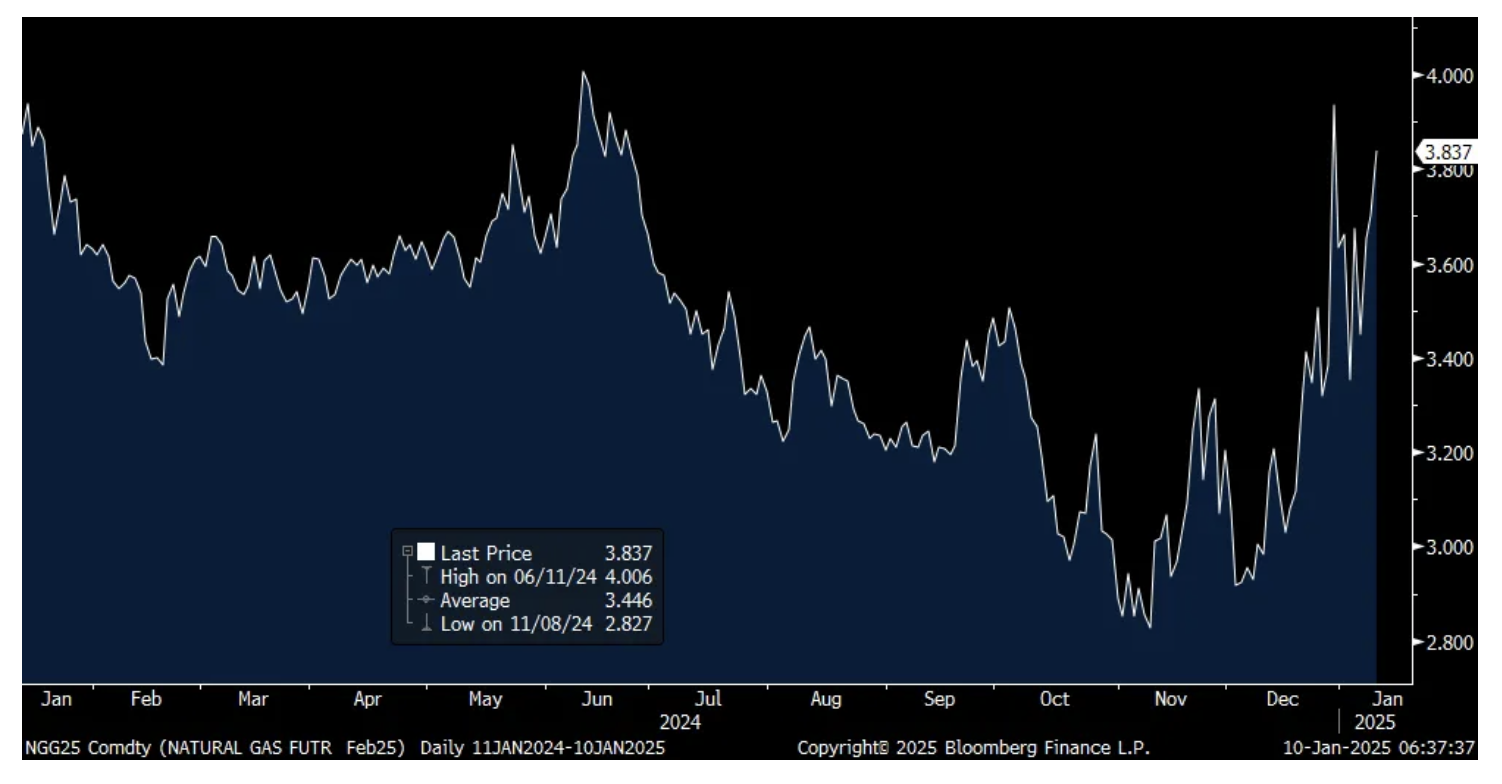

I'm guessing the 3.5% rise in copper prices over the past 3 trading days which followed a 3.3% rise in the previous 3 days to that, bringing the 5 day gain to 7% is in part due to the expected rebuilds in the devastated parts of LA. Lumber prices are up 7.4% this week too. Natural gas by the way because of the cold weather is again approaching $4 per bcf. Oil is getting dragged up too, now above $76, the highest since July. We remain bullish and long oil and gas stocks.

Copper

Lumber

Natural Gas

Bond yields are certainly the big market story this week and we're ending it with further gains. The 10 yr JGB yield rose another 2 bps to 1.20%, up 10 bps on the week. In case you didn't see yesterday, base pay in Japan rose 2.7% y/o/y in November vs 2.5% in October and that is the quickest pace since November 1992. The Australian 10 yr yield jumped 16 bps this week to 4.55%. The UK saw it the worst with the 10 yr gilt yield higher by 25 bps to 4.84%, up each day this week. France has budget challenges too and the 10 yr oat yield rose by 12 bps to 3.41%. German yields rose 16 bps and in the US, the 10 yr yield is now up 10 bps to 4.70% on the week.

There is a common theme here of many countries now getting caught up in the dragnet of the bond police because of excessive borrowing needs relative to the demand of lenders. And throw in the expected rate increase by the BoJ this month and their slowing of QE.

Base Pay Growth y/o/y in Japan

In order to stem the continued fall in the yuan, the PBOC said they were going to halt its purchases of Chinese bonds and their 10 yr yield went up for the 4th day after a pretty persistent decline where it was the only major bond market to see a rally over the past few months. The offshore yuan is finishing the week higher after 3 weeks of declines.

While both sides of the US political aisle have fallen in love with tariffs, this was the headline in Wednesday's FT, "Milei slashes tariffs to bring down high prices." In the piece it says, "Argentines are ordering from Amazon for the first time and supermarkets are beginning to stock Tide Laundry detergent and Ecuadorean tinned tuna, as the libertarian president dismantles a web of duties and regulations that have made many imported products near unaffordable."

"Aiming to lower consumer prices and speed the decline of Argentina's triple digit annual inflation, Milei has slashed tariffs on dozens of products, from acne cream to funeral urns."

Milei told a business event in October, "We are lowering tariffs that underpin the disastrous scheme to replace imports with domestic production. It has punished the whole of society with goods and services of worse quality at a higher price, for the benefit of a privileged few." Isn't it ironic, don't you think?

https://ft.pressreader.com/v99e2025010800000000001001

Here were some important earnings comments this week from those who reported on Wednesday.

From Helen of Troy, the maker of hair style appliances and other personal care products:

"We are pleased with our third quarter results that are within the outlook range we provided in October, despite continued cautious consumer spending on discretionary purchases and a weak cough, cold, and flu season globally."

"We also continue to see the widely reported bifurcation in spending between higher income and lower income households. While holiday spending overall is up y/o/y, its driven by higher income consumers purchasing higher priced items, while lower income consumers continue to struggle, prioritizing necessities over discretionary goods."

Costco reported strong comps in December but said some of it was due to the later Thanksgiving, Black Friday and Cyber Monday vs last year.

In terms of products, "Food and sundries were positive mid single digits, better performing departments included cooler, candy and foods. Fresh foods were up high single digits, better performing departments included meat and produce. Nonfoods were positive high teens, better performing departments included jewelry, gift cards and toys and seasonal." In their ancillary business, "Pharmacy, optical and food court were the top performers."

From MSC Industrial Direct, the large distributor of many things into the industrial/manufacturing end markets:

"While it was a good start to the year, we're mindful that the near-term environment remains soft and our company remains in a transition period during fiscal '25."

They had expected daily sales to be down 4.5-5.5% y/o/y but fell instead by 2.7% y/o/y and said "Growth in the public sector and sustained momentum in solutions were the primary drivers of our top line performance."

On the macro, "Automotive and heavy truck, primary metals, fabricated metals and machinery and equipment continue to be soft. Aerospace, while a net positive for us in the quarter, experienced a step down related to strikes that have since been resolved. Additionally, manufacturing and metal working related softness continues to be reflected in manufacturing index readings, which have now been contracting for 22 consecutive months."

BY Doug Kass · Jan 10, 2025, 9:45 AM EST

Buying homebuilders on early weakness. I am long DHI, TOL, KBH and PHM. Adding to JOE.

BY Doug Kass · Jan 10, 2025, 9:44 AM EST

From Peter Boockvar:

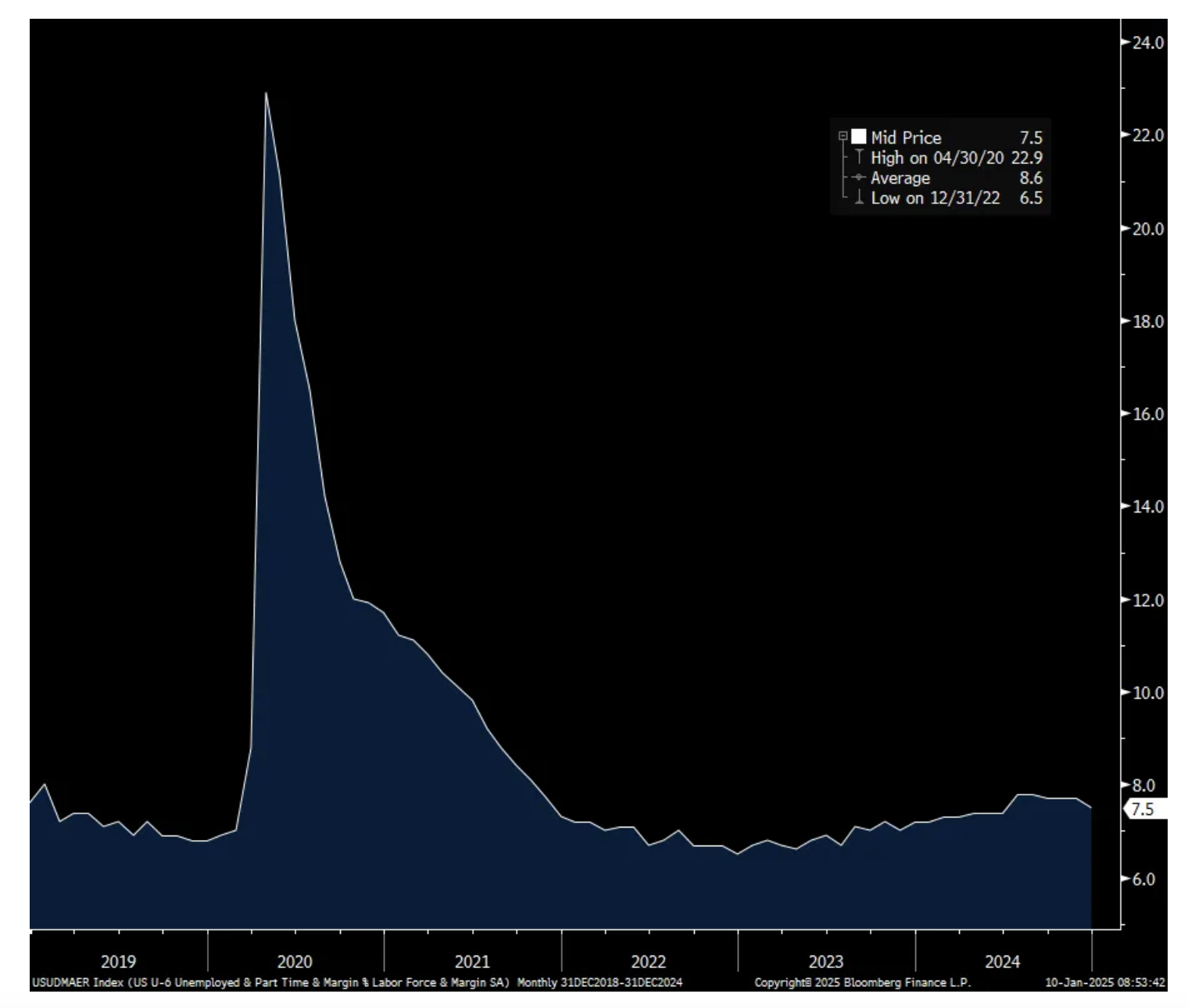

Job growth surprised to the upside with a headline gain of 256k vs the estimate of 165k with the private sector adding 223k of this. The two prior months were revised down by a total of 8k. Also, in the household survey, after very choppy hiring trends in the prior months, 478k net saw new jobs and exceeded the rise of 243k in the labor force which is why the unemployment rate fell to 4.1% from 4.2%. The all in rate fell two tenths m/o/m to 7.5% which is the lowest since June.

In that household gain of 478k, 224k came from those aged 16-19 yrs old with 151k from the 25-54 yr old cohort. I can’t explain the big jump for high schoolers and post graduation hiring. Employment for those aged 55 and older fell slightly m/o/m.

Hours worked at 34.3 was as expected as was the 62.5% participation rate. The rate for the 25-54 key age group was 83.4%, down from 83.5% last month. Average hourly earnings gains of .3% m/o/m were too as forecasted and the y/o/y gain was 3.9%. Of note also, ‘job leavers’ as a % of the unemployed rose to 13.8%, a measure of the quit rate essentially and that is the highest since July 2023.

Industry wise, all of the private sector job growth came from services with the biggest contributor being private education/healthcare of 80k. Leisure/hospitality added 43k and retail too hired a net 43k after losing 29k last month. Professional business services added 28k.

With goods, manufacturing lost 13k and no surprise here while construction hiring rose by 8k while mining lost 3k. So a net loss in the ‘goods producing’ sectors.

A fly here is that it’s taking longer to find work as the average duration of unemployment rose to 23.7 weeks, the highest since April 2022.

Nothing unusual in the birth/death model in that the drop of 52k was the same seen in December 2023 and similar to the drop of 60k in December 2019. That said, if the labor force hiring rate has really changed and we’re at an inflection point, this would be overstating job gains.

Bottom line, because as we know these numbers are subject to big revisions multiple times, I don’t think anyone can say with confidence that the labor market in terms of net hiring is as strong as the headlines today say. I say this when we look at all the labor market information in totality. Just looking at the ISM services index this week, the employment component was at just 51.4 with only 9 of 18 industries surveyed adding people. Continuing Claims remain near 3 yr highs. ADP said just 122k private sector jobs were added in December.

That all said, markets are only focused on today’s data and why yields are popping higher and we get ever closer again to the 5% 10 yr yield. In terms of the rate cuts that is now priced in. We’ve just about taken out any odds of a 2nd cut and the first one is now fully priced in for November vs June before today’s figure.

U6 Unemployment Rate

Average Duration of Unemployment in weeks

BY Doug Kass · Jan 10, 2025, 9:35 AM EST

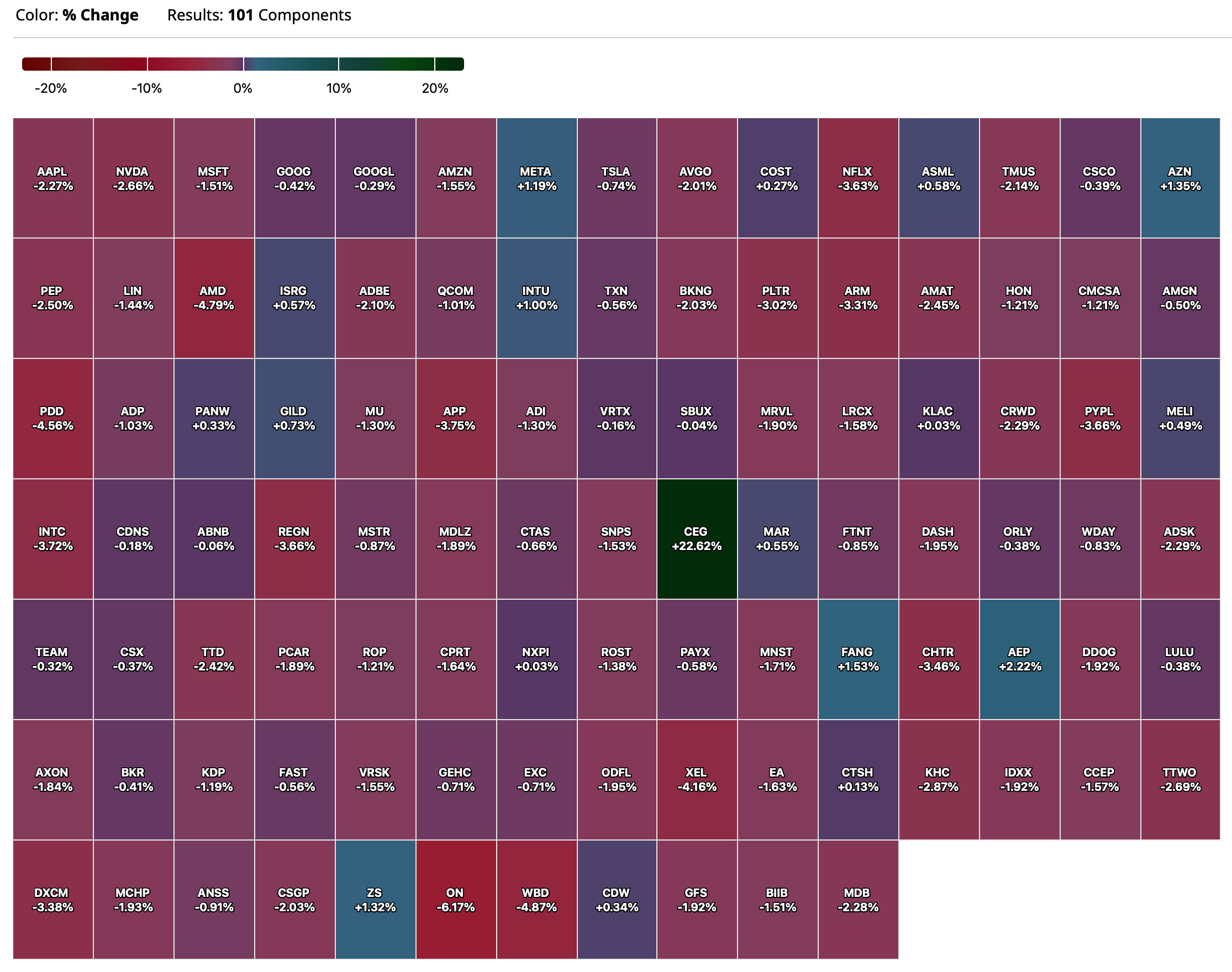

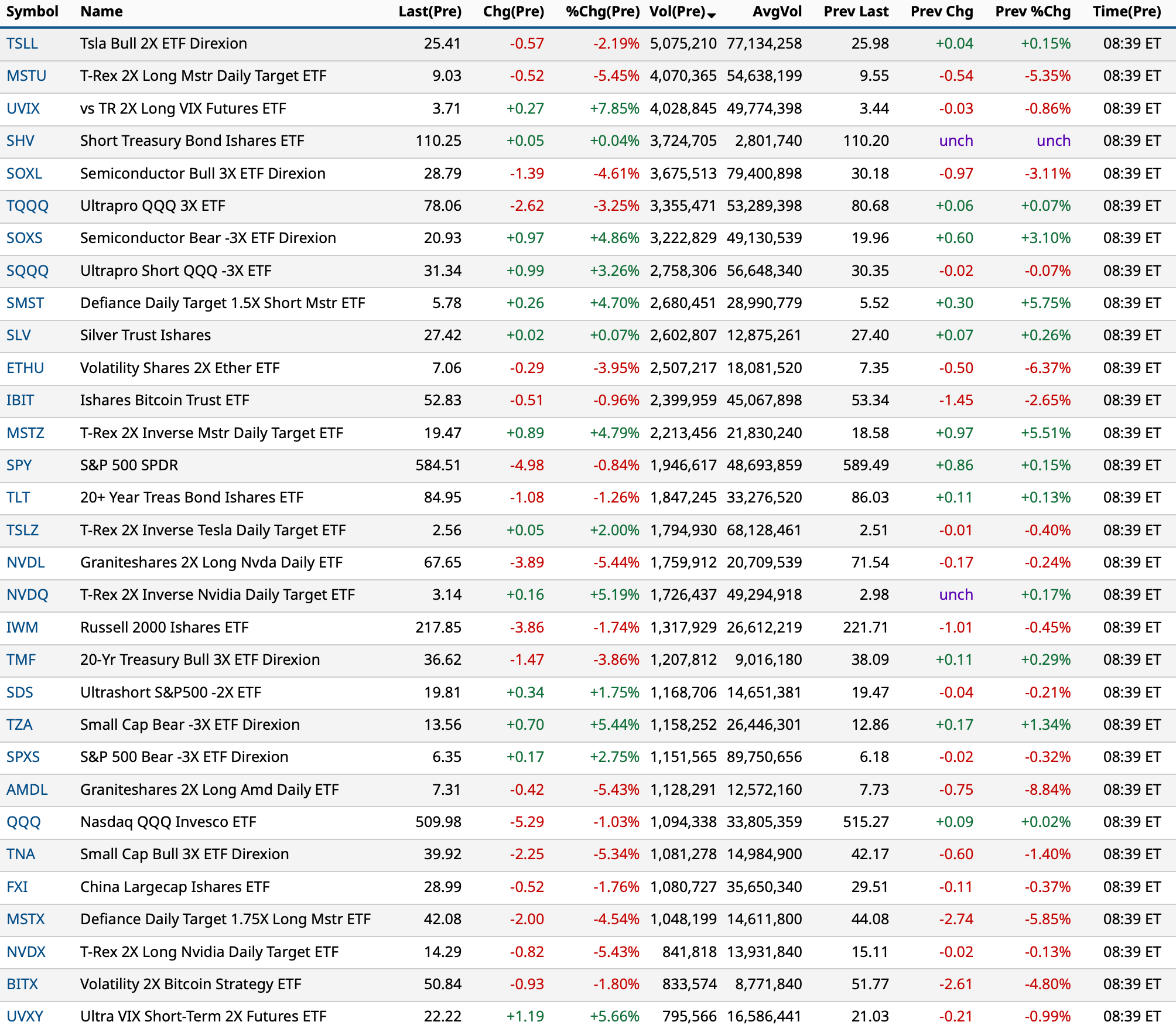

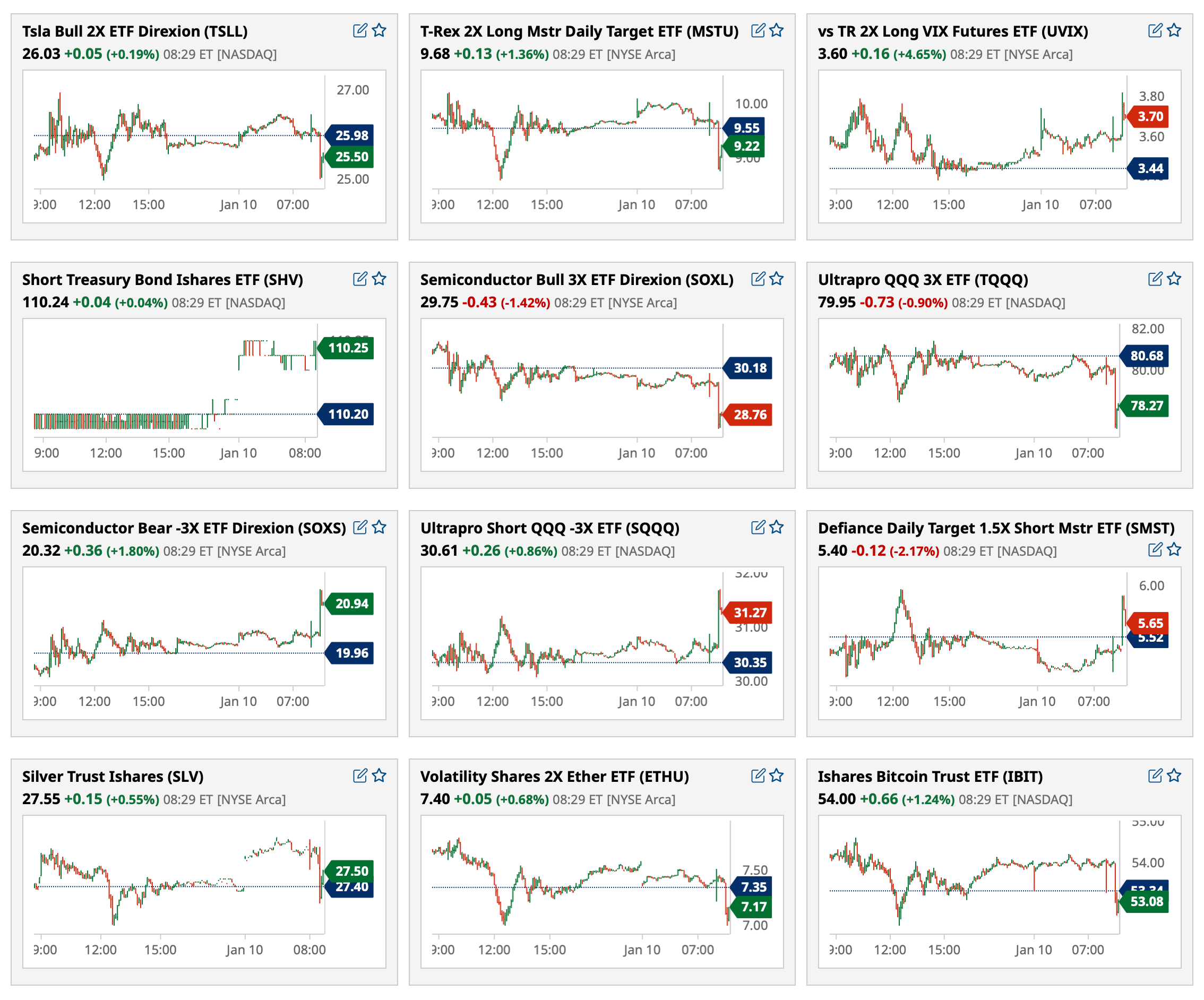

Charts from 8:39 a.m. ET:

BY Doug Kass · Jan 10, 2025, 9:15 AM EST

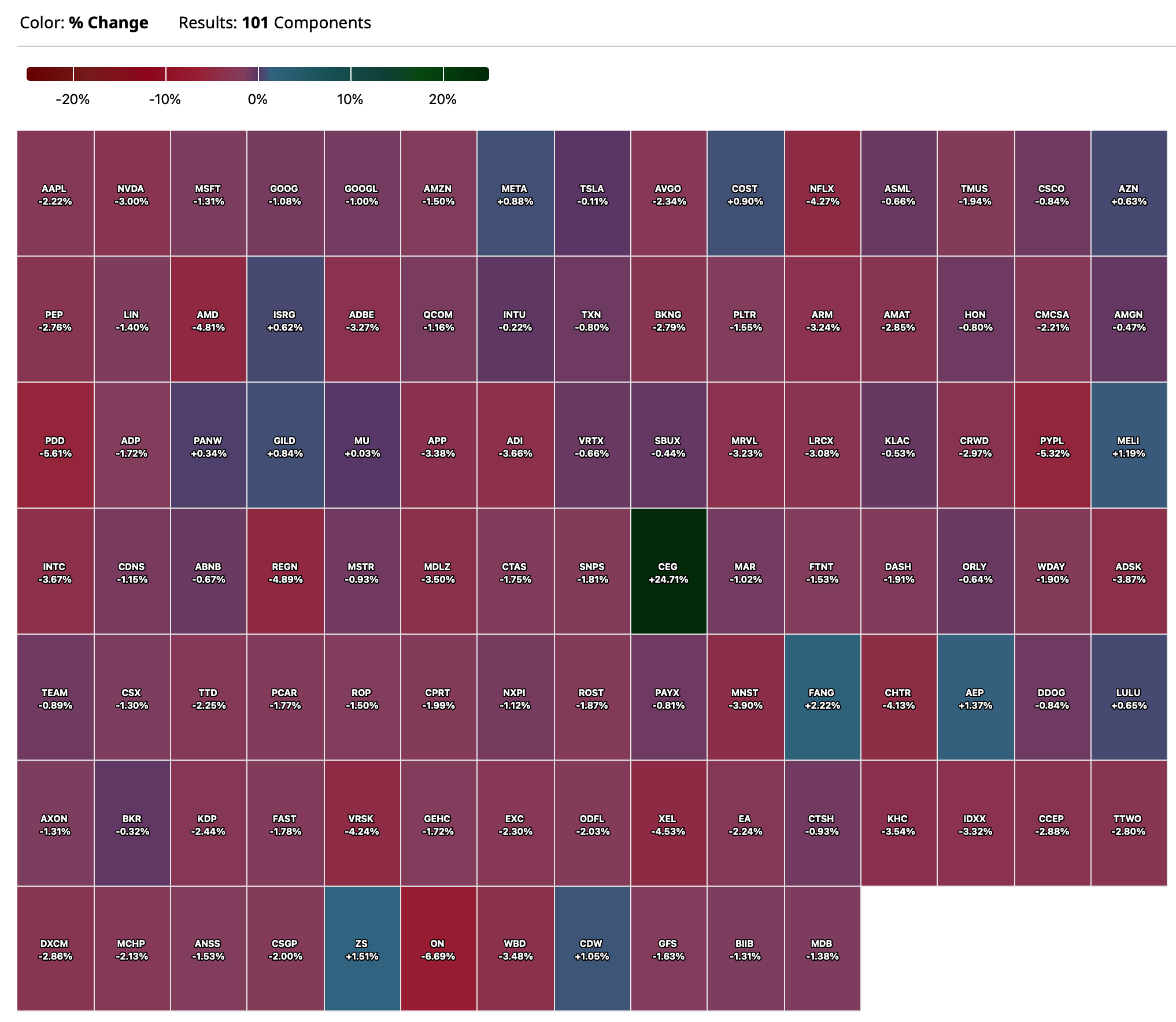

-MVST +43% (announces significant milestone in the development of its True All-Solid-State Battery (ASSB) technology)

-AKYA +24% (confirms to be acquired by Quanterix in all-stock deal)

-ABOS +13% (momentum)

-CEG +13% (confirms to acquire the largest U.S. producer of energy from low-emission natural gas generation, Calpine in stock-cash deal based on EV of $29.1B)

-INTS +11% (provides business update highlighting key achievements with Lead Drug Candidate INT230-6)

-WBA +11% (earnings, guidance)

-DAL +7.5% (earnings, guidance)

-ATRO +7.4% (prelim earnings, guidance)

-CMPS +6.0% (prices 24.0M ADSs and pre-funded warrants for 11.0M ADSs at $4.275/ADS and $4.2649/pre-funded warrant)

-IONQ +5.8% (2024 results will be at the high end of our bookings and revenue guidance; issues long-term targets)

-IINN +5.0% (preparing production ramp-up of INSPIRA ART100 device in response to spread of human metapneumovirus (hMPV) in China)

-RPRX +5.0% (to acquire its external manager, RP Management, LLC; Board has approved a new $3B share repurchase program with $2B of shares intended to be repurchased in 2025)

-W +4.8% (to exit the German market, effective immediately)

-ITCI +2.9% (settles CAPLYTA (lumateperone) Patent Litigation with Sandoz)

-FDMT +2.7% (announces Positive Interim Data from 4D-150 SPECTRA Clinical Trial in DME and Alignment with FDA on Registrational Path)

-BCRX +2.6% (guidance)

-CLDI -28% (announces pricing of $4.25M Public Offering of Common Stock at $0.85/shr)

-LVTX -9.7% (doses first patient in Phase 1 LAVA-1266 study in Hematological Cancers; initial phase 1 data read-out expected by YE25)

-TLRY -8.8% (earnings, guidance)

-NKTR -4.4% (completes target enrollment in REZOLVE-AD Phase 2b Clinical Trial of Rezpegaldesleukin in Patients with Moderate-to-Severe Atopic Dermatitis)

-ROKU -3.1% (MoffettNathanson Research Cuts ROKU to Sell from Neutral, price target: $55)

-NEO -3.0% (CEO Chris Smith to retire; affirms guidance)

-JEF -2.9% (earnings)

-NTLA -2.8% (anticipated 2025 Milestones and Strategic Reorganization to include ~27% workforce reduction in 2025 in effort to prioritize advancement of Late-Stage Programs, NTLA-2002 and Nexiguran Ziclumeran)

-HURC -2.1% (earnings)

-AMD -2.0% (earnings, guidance)

-STZ -2.0% (earnings, guidance)

BY Doug Kass · Jan 10, 2025, 9:01 AM EST

Premarket percentage movers as of 8:35 a.m. ET:

BY Doug Kass · Jan 10, 2025, 8:47 AM EST

BY Doug Kass · Jan 10, 2025, 6:30 AM EST

From my friends at Miller Tabak:

Thursday, January 9, 2025

Tariffs Will Be a Double Blow to the Economy

For over two years, strong growth in consumption and government spending have offset weakness in interest rate sensitive sectors, especially housing. This has allowed overall U.S. growth to beat expectations. Consumption’s performance has not been a surprise. It resulted from exceptionally strong household balance sheets which underpinned our call that high interest rates would not cause a recession. The consensus has, however, now shifted to not just expecting this trend to continue, but for demand to accelerate in 2025. This is the basis for renewed inflation concerns that, for now, have driven up long-term yields to unsustainable levels. We disagree and instead expect growth to slow throughout 2025 with tariffs being the likely catalyst.

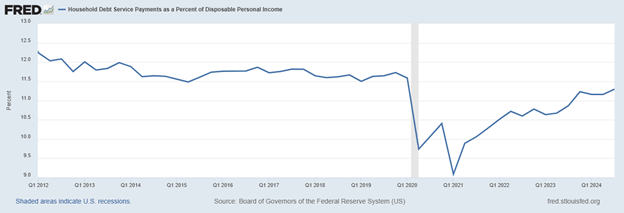

Government spending may continue to prop up demand if President Trump does enact new spending or tax cuts. We maintain, however, that his fiscal policy is likely to be less expansionary than expected. Extending tax cuts that are set to expire will not boost demand, and spending cuts through the Department of Government Efficiency may offset other new spending. So far, President Trump has been more conscious of the budget deficit than we expected. Consumption growth, however, will almost surely sag this year for two reasons. First, new tariffs will reduce households’ spending power enough to switch consumption growth from strong to weak. Second, households’ balance sheets are no longer strong. The Fed’s latest data on household debt puts household debt service at 11.3% of disposable income as of 3Q2024 and we estimate that it is now close to 11.5%. This rate is back in its 2014-2019 range. Households are now in an average financial position and an adverse shock will likely cause them to pull back. Expect tariffs to be that shock, amplifying their direct effect and causing consumption growth to slow by 2Q2025. We reiterate that we are predicting slow growth, not a recession. The odds of a recession starting in 2025 are 15% and the chances of one beginning by the end of 2026 are 40%.

Figure 1: Household Debt Service as a Share of Disposable income

Aggregate debt measures, like that in Figure 1, mask that lower income households are already in a below average financial position. This concern came up at last month’s FOMC meeting “low and moderate-income households continued to experience financial strains, which could damp their spending.” The FOMC also note that delinquency rates continue to creep up, another headwind for upcoming growth.

BY Doug Kass · Jan 10, 2025, 6:05 AM EST

I expect homebuilders to rally smartly in the aftermath of the tragic California fires.

Here is a list of the top homebuilders in California:

KB Home, PulteGroup Top Pro Builder's Ranking of Largest Builders in California | Pro Builder

BY Doug Kass · Jan 10, 2025, 5:55 AM EST

The S&P Short Range Oscillator moved to slightly more oversold at -0.97% from -0.80%.

BY Doug Kass · Jan 10, 2025, 5:45 AM EST

whispers that the DEA is deliberately sabotaging the marijuana rescheduling process are getting louder. case in point: DEA chief Anne Milgram ignored Colorado Gov. Jared Polis's request to provide data on traffic safety after legalization. mjbizdaily.com/biased-dea-kep…

whispers that the DEA is deliberately sabotaging the marijuana rescheduling process are getting louder. case in point: DEA chief Anne Milgram ignored Colorado Gov. Jared Polis's request to provide data on traffic safety after legalization. mjbizdaily.com/biased-dea-kep…

that sounds like a closed end thing. MJ simply needs to put in a sell order for it's MJUS shares, then same day put in a similar dollar value purchase order to buy shares of CNBS, and at the end of the day, MJUS can sell/transfer it's swap exposure to CNBS. (or MJ can start using Show more

that sounds like a closed end thing. MJ simply needs to put in a sell order for it's MJUS shares, then same day put in a similar dollar value purchase order to buy shares of CNBS, and at the end of the day, MJUS can sell/transfer it's swap exposure to CNBS. (or MJ can start using Show more

Biggest takeaway from yesterday’s livestream with @Boris_Jordan? Unity among the top 5 MSOs in lobbying efforts. Next 2 yrs are crucial, big numbers being put up, aiming for a $50M PAC in DC. 💪 $MSOS #CannabisIndustry #Lobbying @TheDalesReport @V_arrell

▶️💯 Dan Ahrens @InvestinginCan1, $MSOS PM & @AdvisorShares COO, offers up some plausible scenarios for how $MJUS could be absorbed by $MJ &/or $CNBS 🎦 WATCH the full explanation (starting @ minute 35:02): youtube.com/live/DHKjsOoWk… 🇺🇸🇨🇦🌎⚕️🌿🥦🧺 ETFs: $TOKE $WEED $YOLO $MSOS