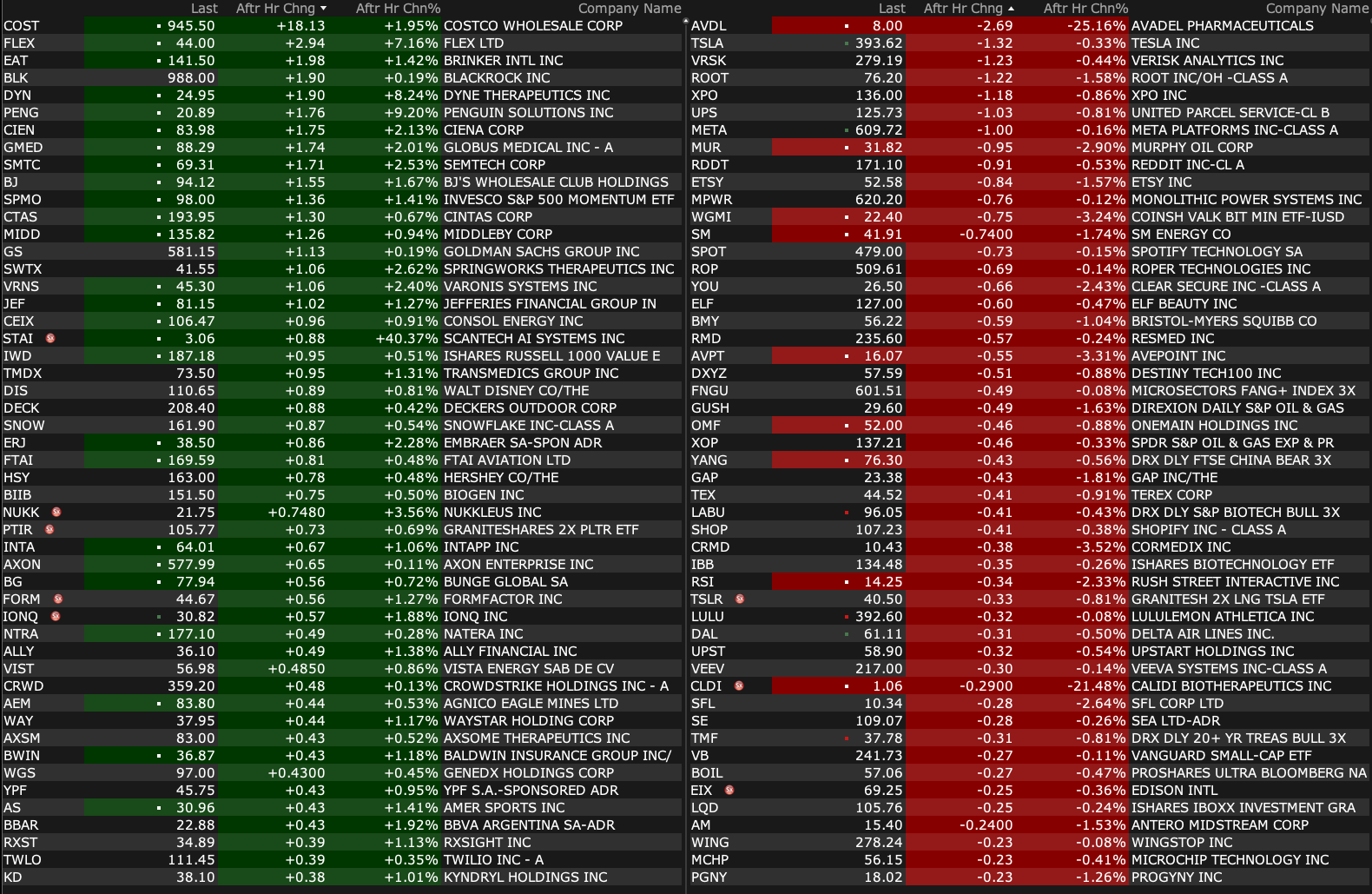

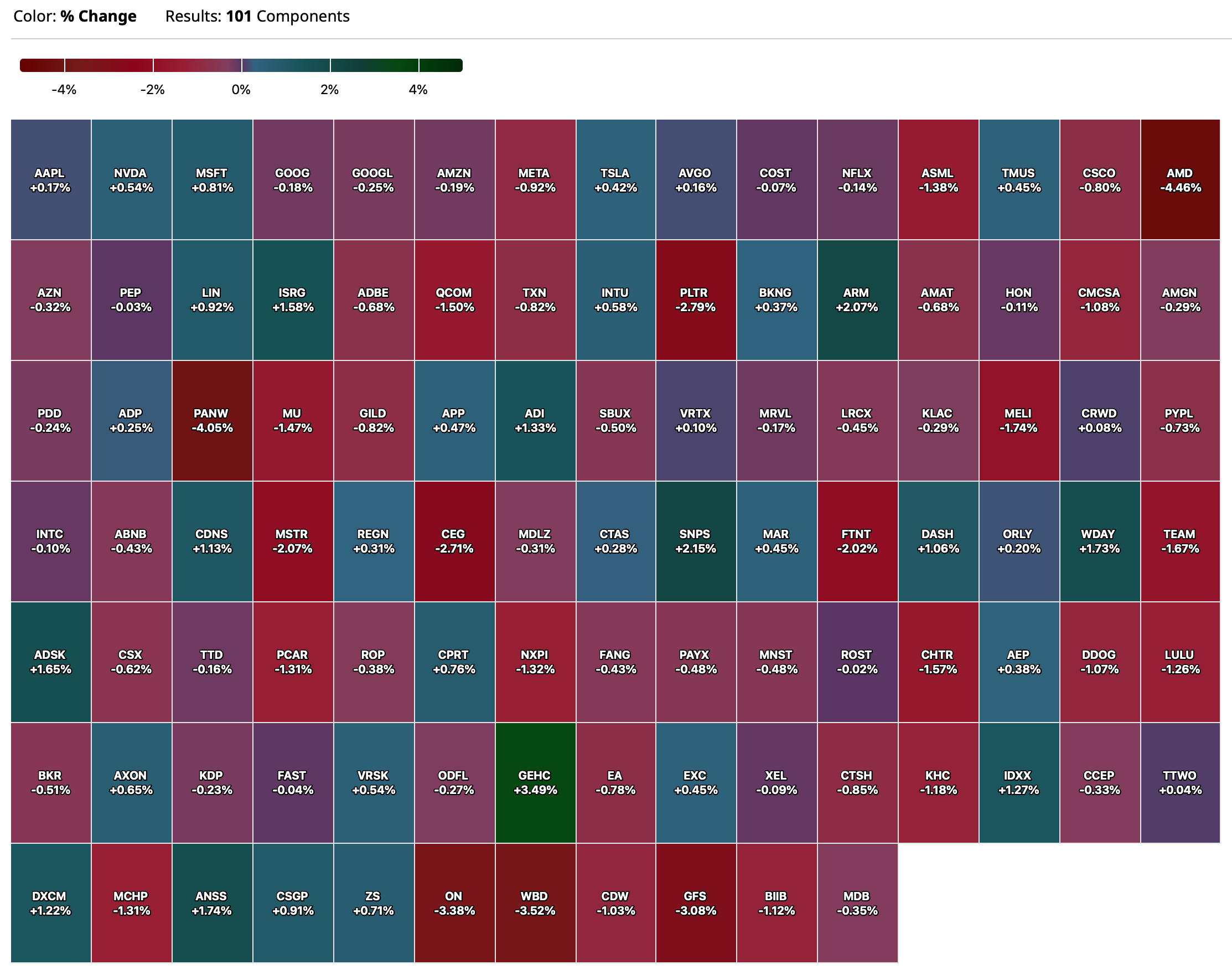

Wednesday's After-Hours Movers

As of 4:30 p.m.:

BY Doug Kass · Jan 8, 2025, 5:15 PM EST

As of 4:30 p.m.:

BY Doug Kass · Jan 8, 2025, 5:15 PM EST

BY Doug Kass · Jan 8, 2025, 5:01 PM EST

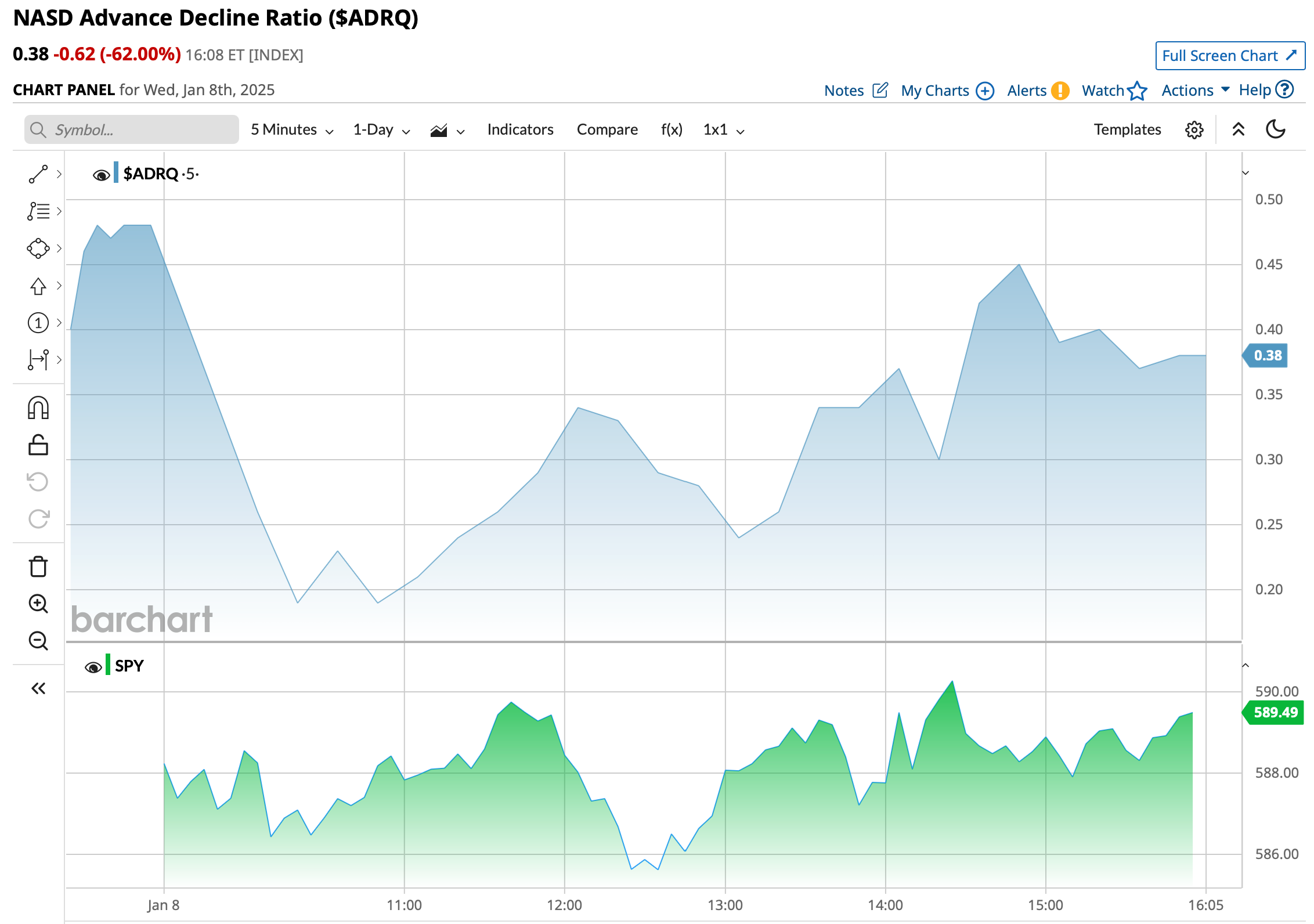

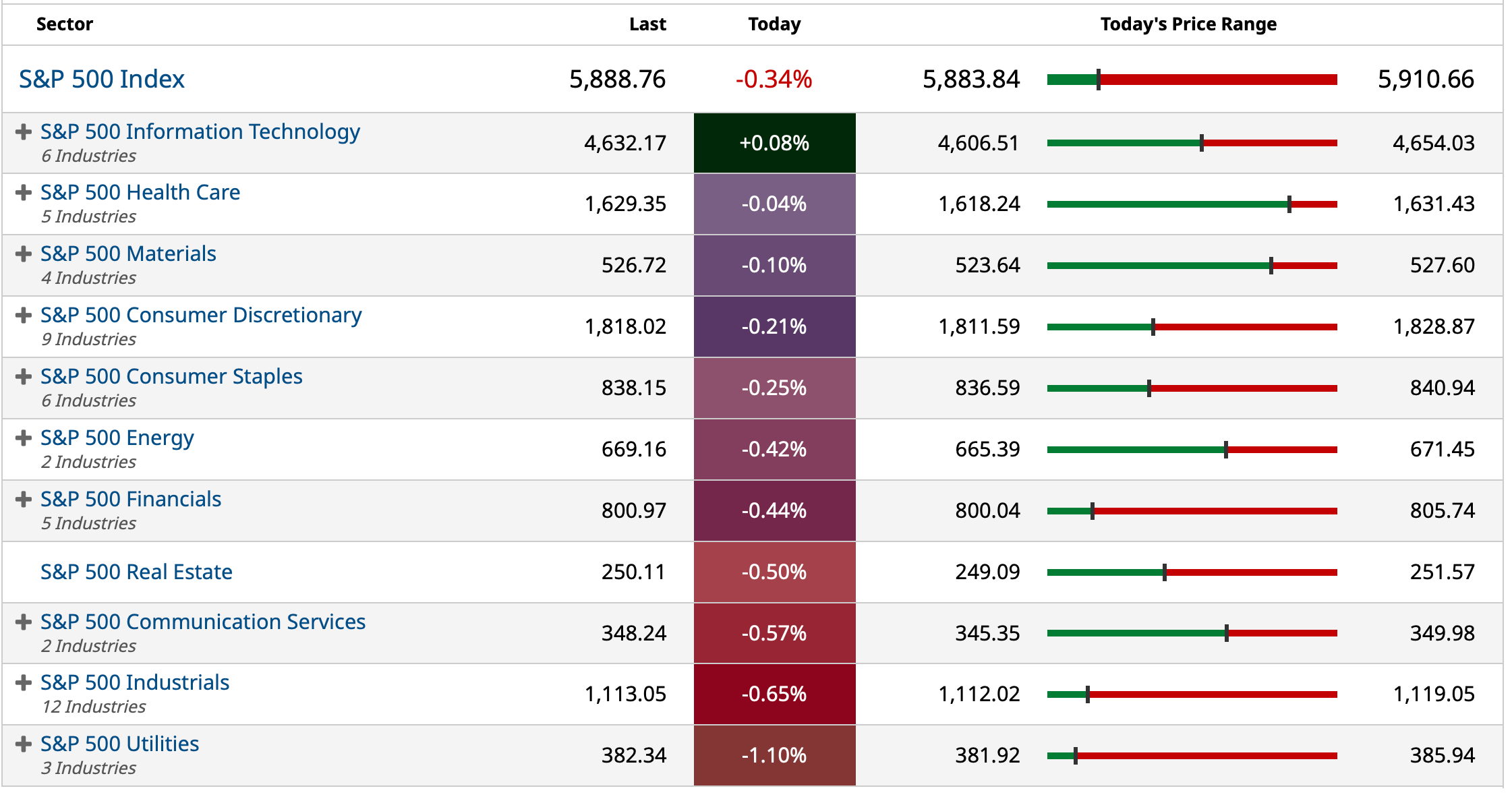

- NYSE volume 6% above its one-month average

- NASDAQ volume 10% above its one-month average

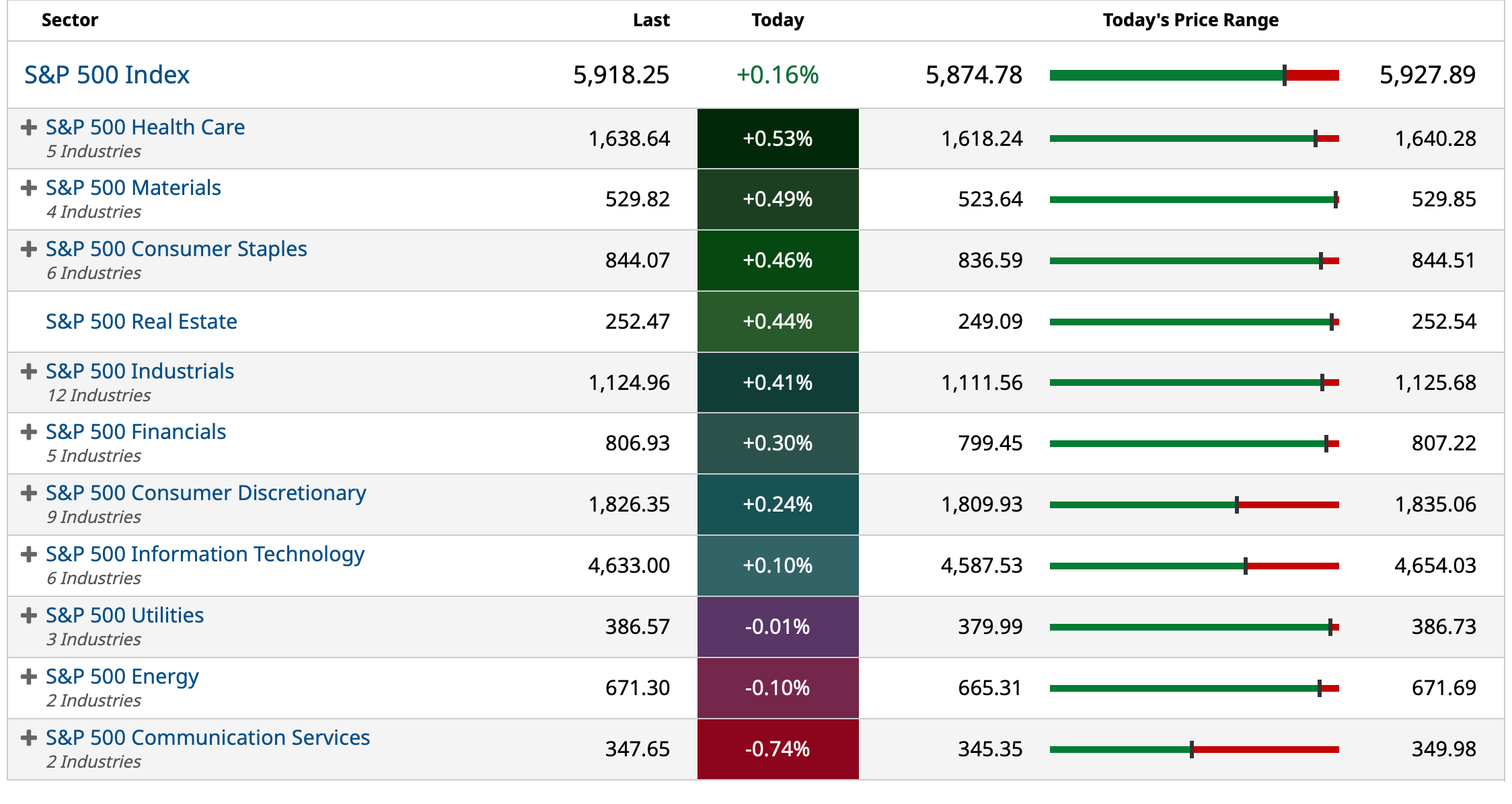

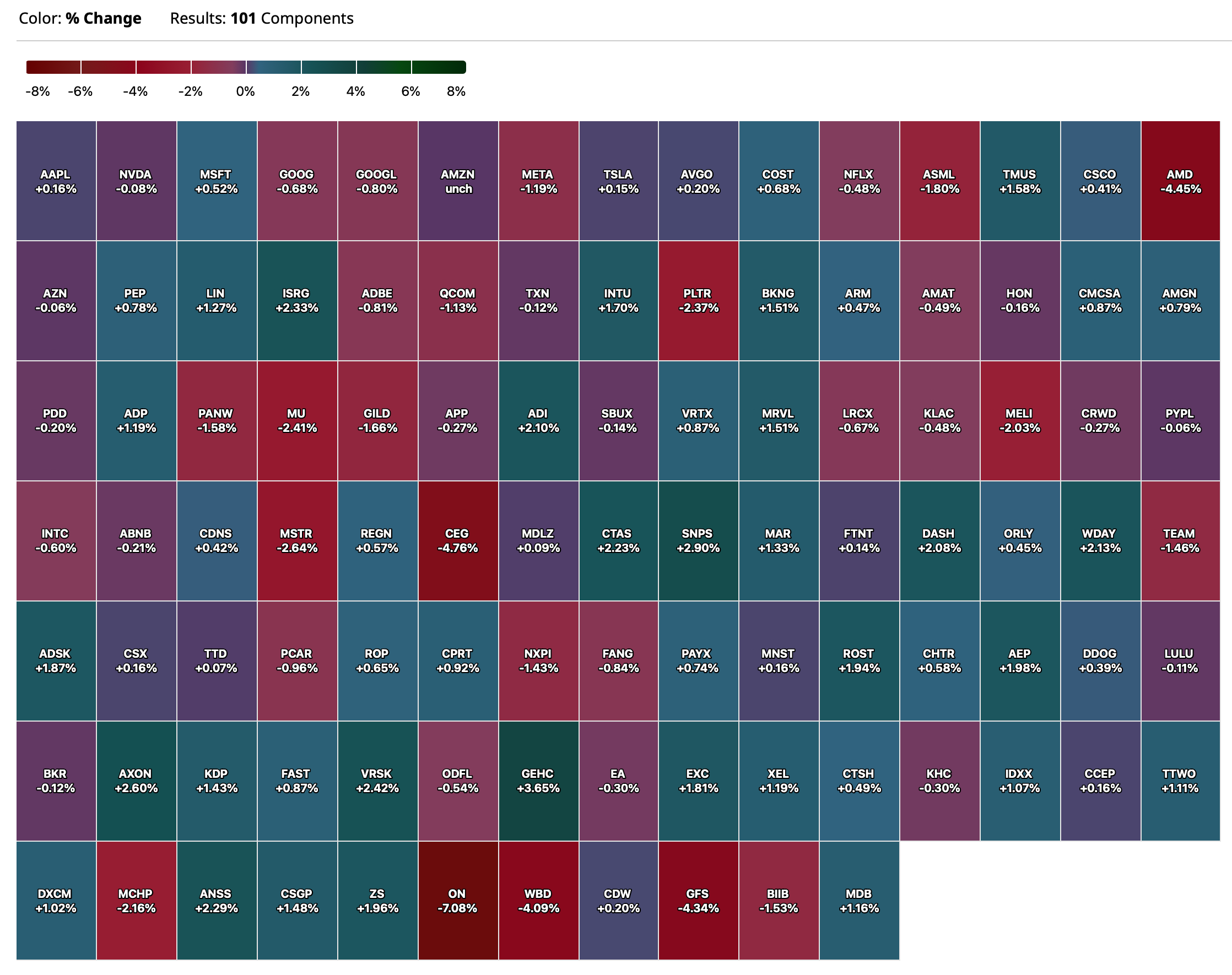

Nasdaq 100 Heat Map

BY Doug Kass · Jan 8, 2025, 4:04 PM EST

I paid $87.59 for more TLT.

Out to a meeting for about 1 1/2 hours.

BY Doug Kass · Jan 8, 2025, 2:10 PM EST

Break in!

Good 30-year Treasury auction moves TLT over $86.

BY Doug Kass · Jan 8, 2025, 1:10 PM EST

BY Doug Kass · Jan 8, 2025, 12:53 PM EST

* Many fail to recognize that long opportunities are often an outgrowth of extremely dour investor sentiment and weak fundamentals...

I added further to AYWF, CURLF, TSNDF and VRNOF today.

From yesterday:

I continue to add to individual cannabis stocks.

This, despite the heavy wind of discounted product prices.

Price compression is most visible in Florida, where Amendment 3 failed to be passed. In that state, cultivation capacity was expanded vigorously ahead of the November vote (the consensus anticipated passage) based on the expectation that adult recreational use would increase.

Now, Florida is faced with surplus weed. Curaleaf (CURLF) (which I am buying), as an example, had a December special in which most products were discounted by 70%. That discount has been reduced to a still healthy 40% this month, which does not spell healthy short-term profits.

I think this is already discounted in the share prices.

Doug Kass Jan 7, 2025 12:40 PM EST

BY Doug Kass · Jan 8, 2025, 12:25 PM EST

From Jazzy Jeff:

JeffI

I agree with Dougie that stocks are vulnerable- high valuations, long term interest rates trending higher, upcoming presidency with Trump’s unsettling stated intentions (good or bad) and the uncertainty which is typically market unfriendly.

It doesn’t matter how many people agree with this or how many articles or posts one writes. Being right is not a popularity contest.

The most valuable stock- APPL has had 40%+ drawdowns many times along way to the top of the market cap pile- it is part and parcel of individual stock ownership. Definitely tests one’s conviction. One must understand why one owns the stock- as such sell offs should be bought or sold.

I have done something new. I have collared almost every position (no cost- as the sale of the calls pay for the long puts) to limit my downside to 10- 15% (also limits upside- but better that 1 to 1) for various time frames. It’s a lot of work. I have outperformed the S&P yet I wonder if this is another reason to own index funds and spend time with the family instead. It would be much less work to simply collar the index. Note: The longer the collar the better the set up as you have more upside than downside as the ratio improves with time.

Maybe I’m just rattled? I did find the first Trump presidency painful. I’m also getting older and less comfortable with large drawdowns at this stage of my life.

I’d like to think I value my time- but considering most investors (including professionals) under perform the index- I must question all of our decisions to play a game that’s stacked against us.

BY Doug Kass · Jan 8, 2025, 12:05 PM EST

* As the spectre of "slugflation" (and sticky inflation) comes ever closer into sight...

The wildfires in California pose a bonafide threat to inflation over the next twelve months.

Insurance premiums already were ridiculously expensive — the wildfires will exacerbate the general inflation "issue."

As premium prices are likely to go even further thru the roof (excuse the pun!), there might even be (at some point of time) a move to nationalize homeowners insurance in certain geographies.

BY Doug Kass · Jan 8, 2025, 11:53 AM EST

TLT green.

BY Doug Kass · Jan 8, 2025, 11:29 AM EST

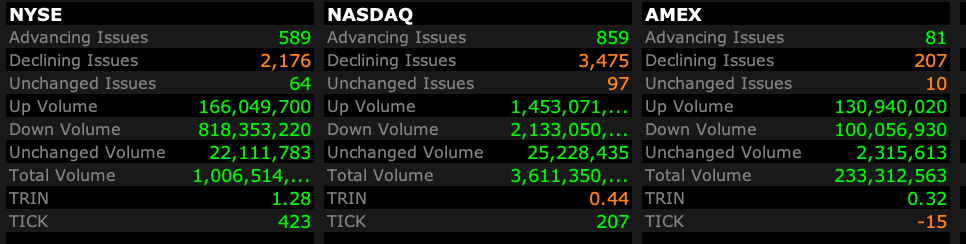

- NYSE volume is 3% above its one-month average;

- Nasdaq volume is 27% above its one-month average

- VIX is up 5.78% to 18.85

BY Doug Kass · Jan 8, 2025, 10:56 AM EST

There has been a broad and healthy discussion and debate of long term investing in our Comments Section.

At any time I have over 20 investment longs and shorts, as a perspective -- so I have plenty of longer-term investments in my portfolio.

Ergo, I fully recognize the value of longer-term investing.

Trading, augments (in theory) my longer-term investing.

The decision on long-term gross exposure is primarily a function of my market view and my ability to find (on a bottoms up basis) individual equities that provide me with asymmetric reward v risk and provide me with a margin of safety. I, for one, have been incorrectly negative over the last year. So that governs my gross exposure (on both longs and shorts).

My decision on long-term exposure is importantly a function of my risk profile and appetite. Many long term investors (like Jazzy Jeff) are willing to experience 20%-30% drawdowns because they are confident about the longer term prospects. By contrast, I am risk averse and I am unwilling to experience such drawdowns -- this is fundamental to the way in which I manage money and it helps to explain my tight net positions.

Finally, when I am negative or I don't see a trending market I emphasize more greatly the trading function, which I have been doing successfully in recent months. (Note: I have made money while being negative). This is not, however, expected to be a permanent condition.

But I will never compromise the core notions of buying at a discount to intrinsic value, having a favorable reward v risk and having a "margin of safety" on all of my purchases.

More on this later ...

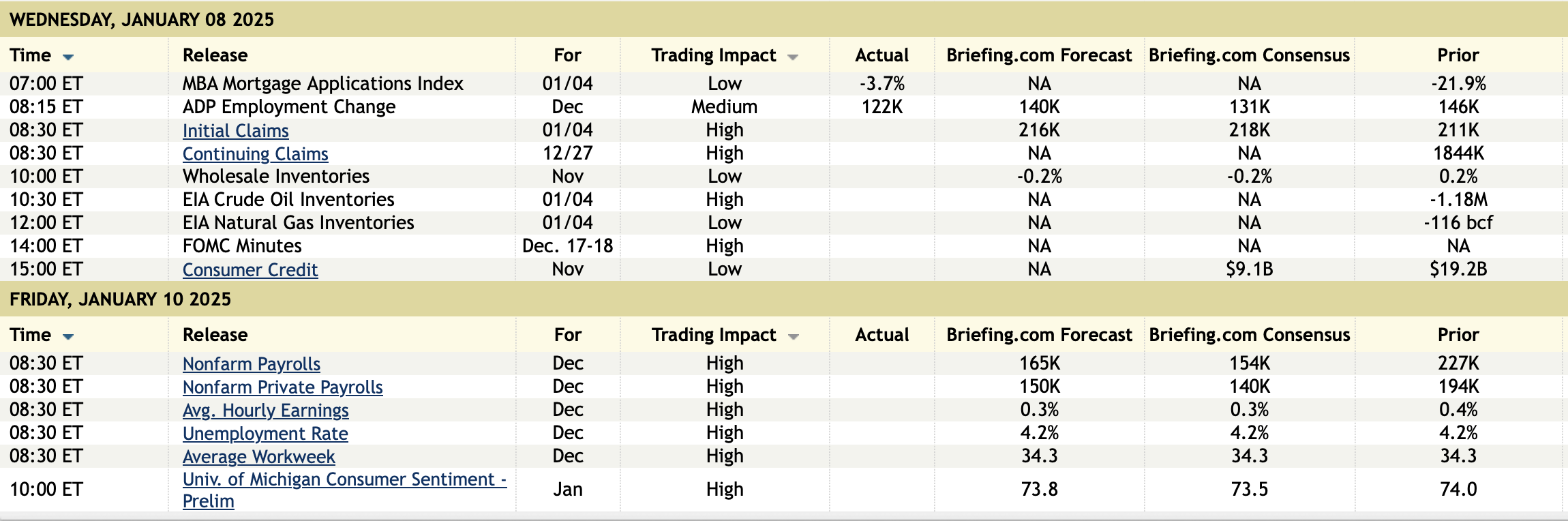

BY Doug Kass · Jan 8, 2025, 10:00 AM EST

From Peter Boockvar:

ADP said a net 122k private sector jobs were created in December, below the estimate of 140k and vs 146k in November. Small businesses, those with less than 50 employees, continued to slow the pacing of hiring’s. After losing 17k in November, just 5k were added in December. Those with 50-499 employees added just 9k after 42k last month. Large companies continued to drive most of the job growth, hiring 97k vs 120k last month.

Most of the deceleration took place in services as 112k jobs were hired in this sector vs 140k in the month before. Education/health continues to be consistent with its job adds, contributing 57k. Leisure/hospitality added 22k and with smaller gains in trade/transportation/utilities, information, financial activities and other services. Jobs were shed in professional/business services.

On the goods side, construction hired 27k, partly offset by a drop of 11k in manufacturing, down for a 3rd straight month. The natural resource/mining industry lost 6k jobs.

On the wage side, ‘job stayers’ saw a 4.6% rise in y/o/y growth vs 4.8% in the month before. ‘Job changers’ saw a 7.1% y/o/y wage gain vs 7.2% in the month before. Still solid gains.

ADP said “The labor market downshifted to a more modest pace of growth in the final month of 2024, with a slowdown in both hiring and pay gains.” To quantify the downshift, it’s really vs the 2023 gains as the 3 month average is now 151k vs the 6 month average of 138k, the 12 month average of 152k and vs the 2023 average of 209k. The private sector estimate for Friday’s BLS report is 140k.

Please take the jobless claims data with a grain of salt in the last week of December and the first week of January. That said, initial claims totaled 201k vs the estimate of 215k and vs 211k last month. Continuing claims were 1.867mm, about as expected.

With respect to Fed Governor Waller’s comments today, the first thing that came to mind is that he’s jockeying to be the next Fed Chair after Trump yesterday said interest rates were too high. Waller in a prepared speech said “As always, the extent of further easing will depend on what the data tell us about progress toward 2% inflation, but my bottom line message is that I believe more cuts will be appropriate.” He believes in this because he expects inflation to continue to decelerate and he laid out his reasons for that belief. He’s also not worried about tariffs impacting his views. He could very well be right on his inflation guess but I think he should be more non-committal on more cuts from here as long rates continue to rise and we wait to see the new Trump policies, particularly on tariffs.

The 2 yr yield rallied on his comments but as seen since the Fed first cut 50 bps in September, long rates are still higher with the 10 yr at 4.70% as of this writing.

BY Doug Kass · Jan 8, 2025, 9:48 AM EST

From Peter Boockvar:

Having very close friends in LA who left their home yesterday not knowing if it would be there when they came back, my heart and prayers go out to those living in the area, especially those who lost their houses.

With market interest rates continuing to rise in many parts of the world with today seeing another jump in UK gilt yields in particular with its 10 yr jumping by 12 bps to 4.80%, the highest since 2008, everyone has their own theory and/or questions on why this is happening. I think it's all of the above in that rates are rising because the world is now flooded with too much sovereign bond supply and that the laws of supply and demand now matter for those countries that have excessive debt, which means many. Rates are now rising because we're seeing the unwind of the largest financial bubble in the history of bubbles that took place in sovereign bonds that culminated in $18 trillion dollars of negative yielding securities in December 2020. Rates are rising because maybe central banks (outside of the BoJ) are likely going to slow the pace of rate cuts from here because of still inflation above their targets.

I will again also point to the Japanese, the BoJ and the JGB market as a reason for the rise in rates there and elsewhere. I believe it was the BoJ ending yield curve control in July 2024 as the catalyst for the rise in the US 10 yr yield to 5%. Now, we have a likely rate hike this month from the BoJ and each and every quarter stretching out to Q1 of 2026, the BoJ is slowing its bond buying by 400 billion yen per quarter and will eventually cut in half the amount they are buying by then. That liquidity spigot is turning down big time.

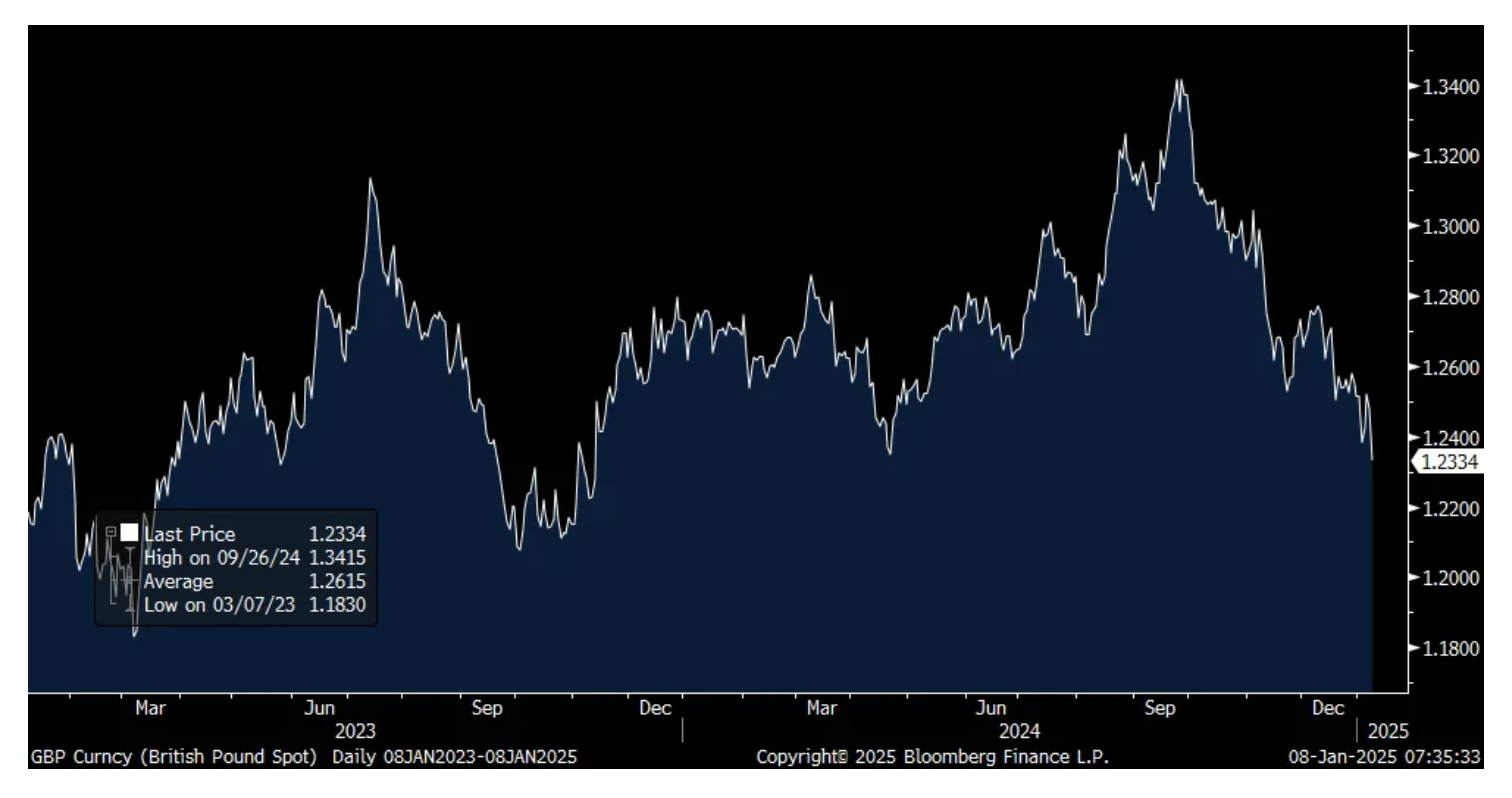

By the way, back to the UK, even with the continued rise in yields, the pound continues to weaken and this market response is something you usually see historically in emerging markets. It's also a big thumbs down on the new Starmer government.

UK 10 yr Gilt Yield

British Pound vs USD

These comments were from Apogee Enterprises yesterday whose stock fell 19%. They are a $1.3b revenue company making glass for commercial windows and framed art.

"Revenue in the quarter was in line with last year, despite seeing continued pressure from soft end market demand in non-residential construction. As expected, this softness is primarily impacting our Framing and Glass segments."

"non-residential construction remains challenging. Leading indicators such as the Architectural Billings Index have pointed to a contracting market for 20 plus months. We have and continue to see this softness in framing systems over the past several quarters and more recently with awards slowing in our Architectural Glass segment."

"The picture across different building types within non-res construction remains mixed. Interest rate sensitive sectors like office, commercial, lodging and multifamily housing have been weaker while verticals like education, healthcare and transportation continue to see growth."

With the continued rise in mortgage rates, purchase applications fell sharply for the 3rd straight week, by 6.6% and now down 15% y/o/y. That said, at the end and beginning of the year, the holidays always seasonally skew this data and I'd rather wait until next week for a cleaner read. Refi's stabilized after falling off a cliff in the last two weeks of 2024. Again, seasonally distorted.

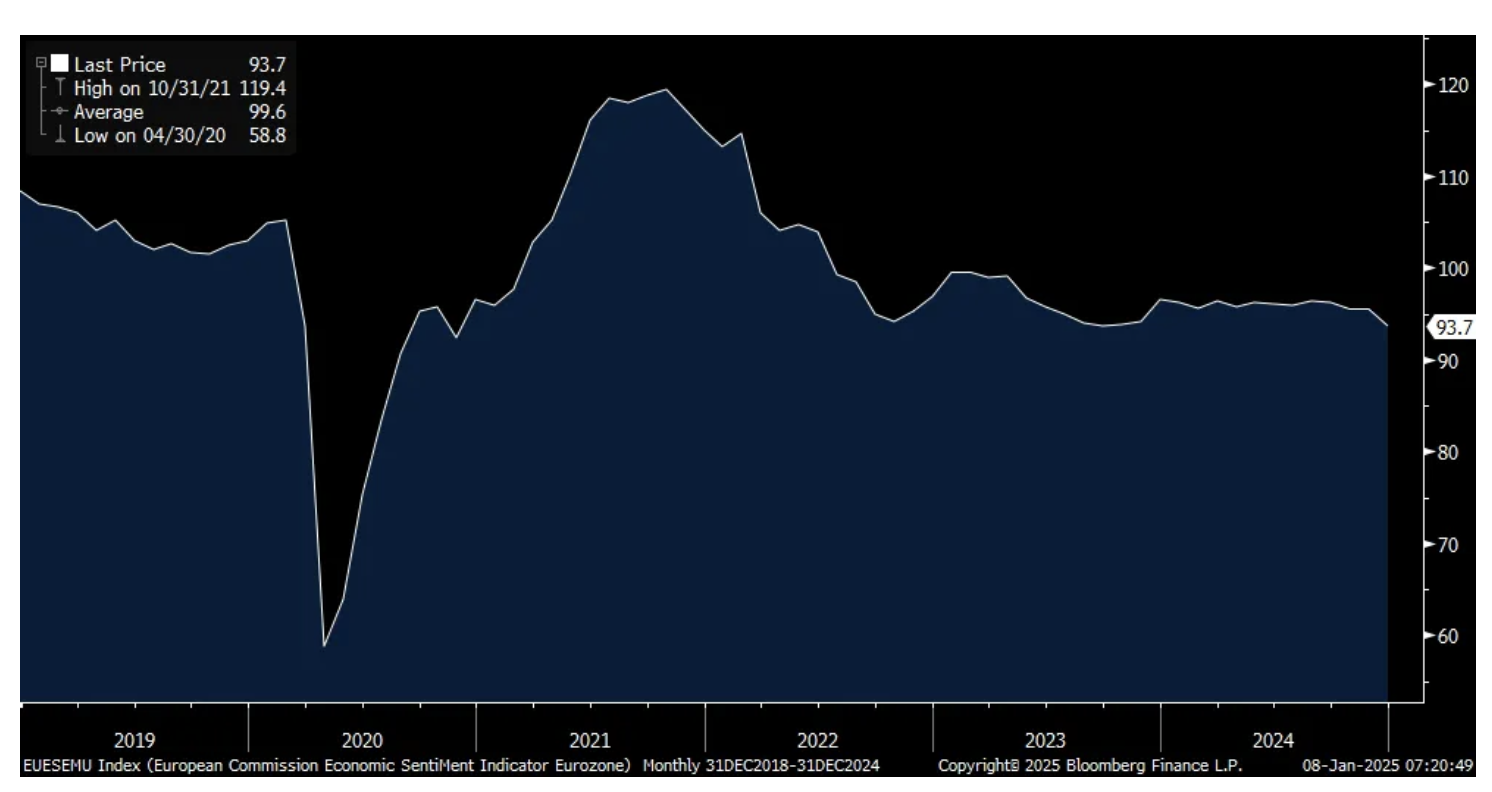

Economic confidence in the Eurozone in December weakened further to 93.7 from 95.6 and the estimate was for no change. That matches the lowest since November 2020. Manufacturing confidence led the decline, only partly offset by a gain in services confidence. Consumer confidence fell to the lowest since February and retail and construction were little changed. Bottom line, Europe's economy is barely growing and with the weak euro too, it will be very interesting to hear what Corporate America says during earnings season about their business in this region.

Eurozone Economic Confidence

German factory orders dropped by 5.4% m/o/m, well worse than the estimate of a .2% decline. Weakness in big ticket items were the main culprit. Retail sales in Germany fell for a 2nd straight month in November.

BY Doug Kass · Jan 8, 2025, 9:33 AM EST

-SANA +234% (announces Positive Clinical Results from Type 1 Diabetes Study of Islet Cell Transplantation without Immunosuppression)

-ABSI +47% (AMD makes $20M investment)

-LFVN +34% (prelim earnings, guidance)

-ANGO +16% (earnings, guidance)

-SLDB +16% (announces FDA IND Clearance for First-In-Industry Dual Route of Administration Gene Therapy to Treat Both Neurologic and Cardiac Manifestations of Friedreich’s Ataxia)

-CMPX +11% (provides corporate update and announces advancement of a new drug candidate; continue to expect initiation of tovecimig and CTX-471 clinical trials in mid-2025 and to submit CTX-10726 IND by year-end with initial proof-of-concept clinical data in 2026)

-EBAY +7.7% (Meta to launch test in Germany, France and US that will enable buyers to browse Ebay listings on Marketplace platform)

-CALM +5.1% (earnings)

-HALO +5.0% (raises FY25 guidance)

-AIR +3.6% (earnings)

-MATW +3.3% (to sell SGK Brand Solutions for $350M total consideration including $250M cash)

-KMDA +3.2% (affirms FY24 guidance, provides initial FY25 guidance)

-ACCD +3.0% (to be acquired at $7.03/shr in cash by Transcarent)

-NEOG +2.9% (names current CFO David Naemura as new COO (to maintain CFO role as well), effective immediately)

-WINT +2.6% (announces new corporate strategy seeking to identify and acquire FDA-approved revenue assets while advancing Its Cardiovascular and Oncology Pipeline; Company will seek to use equity to acquire subsidiaries)

-EDBL +2.1% (achieves >45% y/y increase in preliminary Herbs and Produce sales results during holiday time period)

-KRUS +2.0% (earnings, guidance)

-DATS -50% (announces pricing of $5.1M Registered Direct Offering at $4.25/shr)

-RCEL -24% (guidance)

-CTXR -17% (announces $3M Registered Direct Offering Priced At-The-Market under Nasdaq Rules at $4.035/shr)

-INMD -13% (Q4 guidance)

-QSI -13% (Quantum computing related names lower following NVDA CEO comments)

-SLP -12% (earnings, guidance)

-MBRX -11% (highlights Development Progress of Annamycin)

-KRP -6.0% (announces $231M Midland Basin acquisition in cash and unit transaction; prices 10M shares at $14.90/share)

-AZZ -4.5% (earnings, guidance)

-QURE -3.7% (priced 4.4M share secondary at $17.00/shr)

-HELE -3.0% (earnings, guidance)

-PLTR -2.3% (downside momentum)

-DKNG -2.1% (lower in sympathy with Flutter)

BY Doug Kass · Jan 8, 2025, 9:21 AM EST

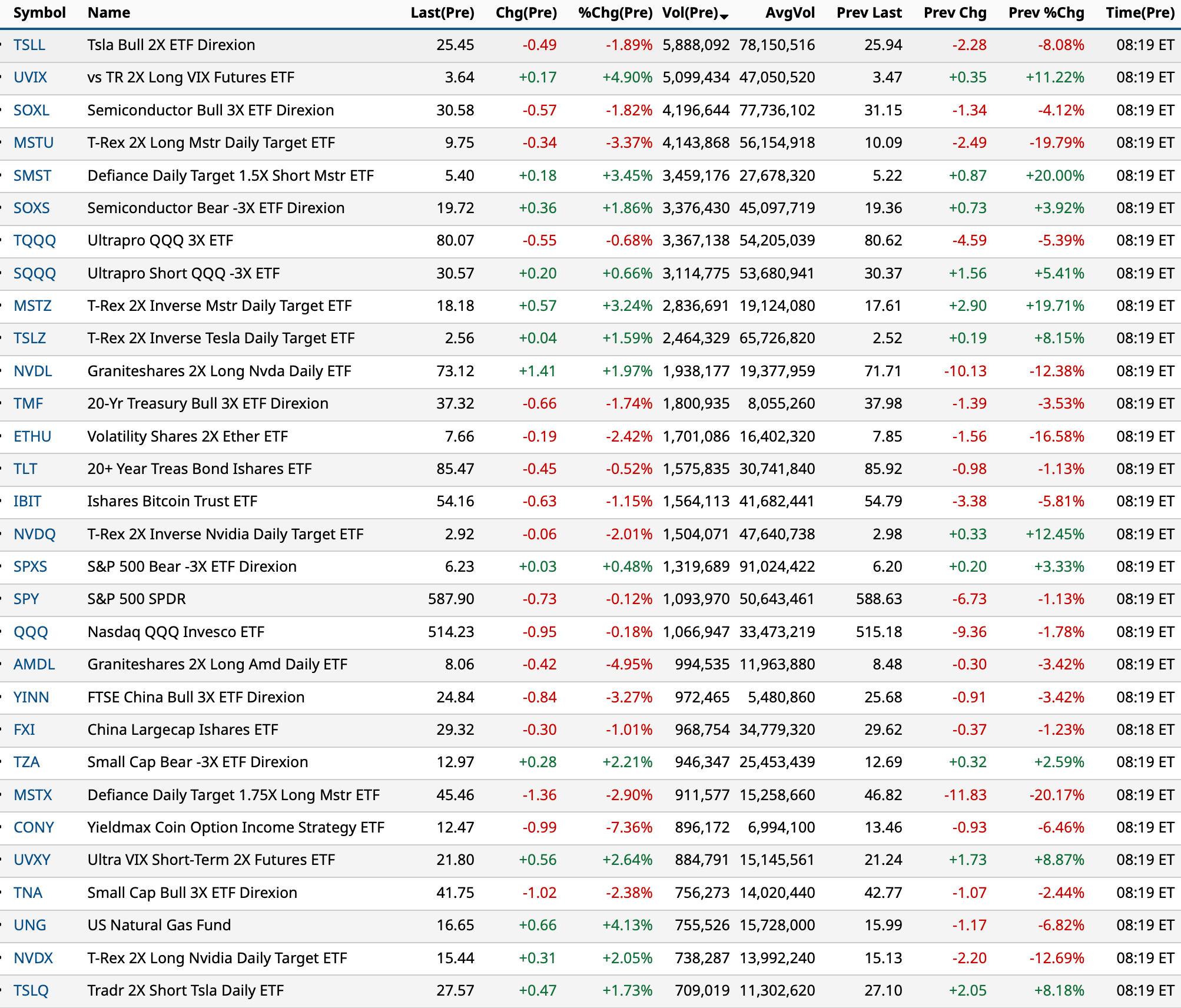

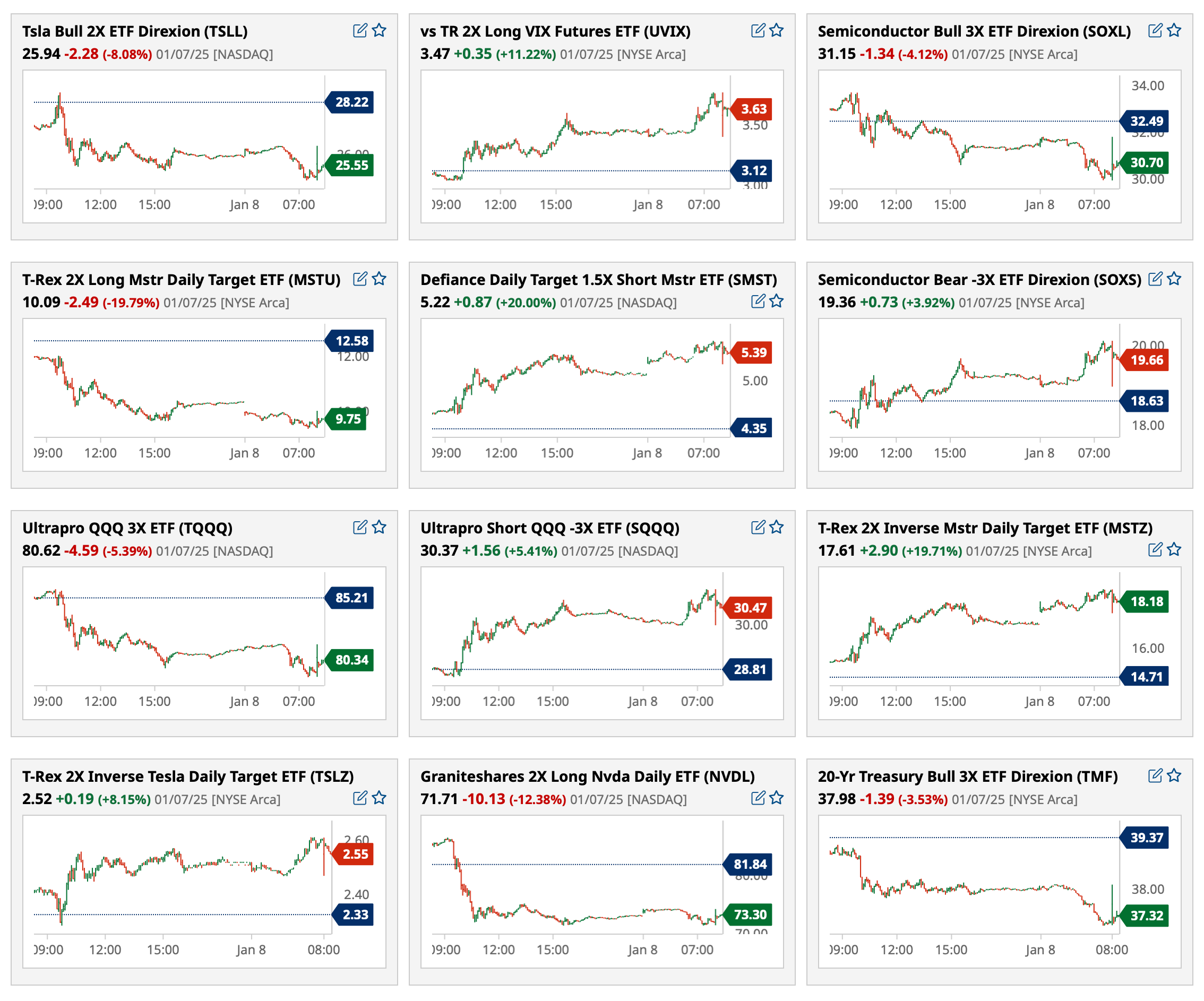

Most active premarket ETFs as of 8:19 A.M. ET:

BY Doug Kass · Jan 8, 2025, 9:09 AM EST

The premarket percentage movers as of 8:37 a.m. ET:

BY Doug Kass · Jan 8, 2025, 8:57 AM EST

BY Doug Kass · Jan 8, 2025, 8:37 AM EST

At $85.30, I have moved very large into TLT.

BY Doug Kass · Jan 8, 2025, 8:12 AM EST

BY Doug Kass · Jan 8, 2025, 8:05 AM EST

Knowledge@Wharton interviews Dr Jeremy Siegel.

Jeremy Siegel: 2025 Outlook for Stocks and the Economy - Knowledge at Wharton

BY Doug Kass · Jan 8, 2025, 7:45 AM EST

1. Not only is service inflation percolating (from yesterday's data), but commodities inflation ripping higher in last few months:

2. Interest rates are climbing fast:

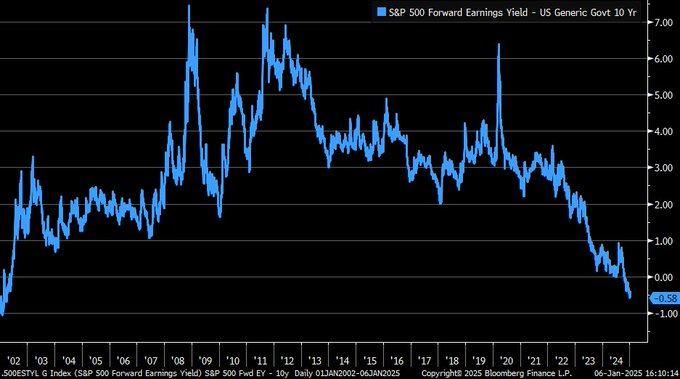

3. As interest rates rise and corporate profits are little changed, the equity risk premium falls to the lowest level in over two decades:

Slugflation lies ahead and, at 23x forward EPS, stocks are vulnerable.

BY Doug Kass · Jan 8, 2025, 7:30 AM EST

What bottoms are made of:

BY Doug Kass · Jan 8, 2025, 7:00 AM EST

Added to TLT at $85.72 in premarket trading.

BY Doug Kass · Jan 8, 2025, 6:50 AM EST

Bonus — Here are some great links:

What Happens When Stocks Gain 20%

A Prerequisite for a Correction

BY Doug Kass · Jan 8, 2025, 6:35 AM EST

The S&P Short Range Oscillator slipped back into oversold at -0.8% vs. 1.17%.

BY Doug Kass · Jan 8, 2025, 6:25 AM EST

BY Doug Kass · Jan 8, 2025, 6:15 AM EST

The equity risk premium made a new multi-decade low yesterday.

BY Doug Kass · Jan 8, 2025, 6:05 AM EST

BY Doug Kass · Jan 8, 2025, 5:55 AM EST

Wolf Street howls about job openings.

BY Doug Kass · Jan 8, 2025, 5:45 AM EST