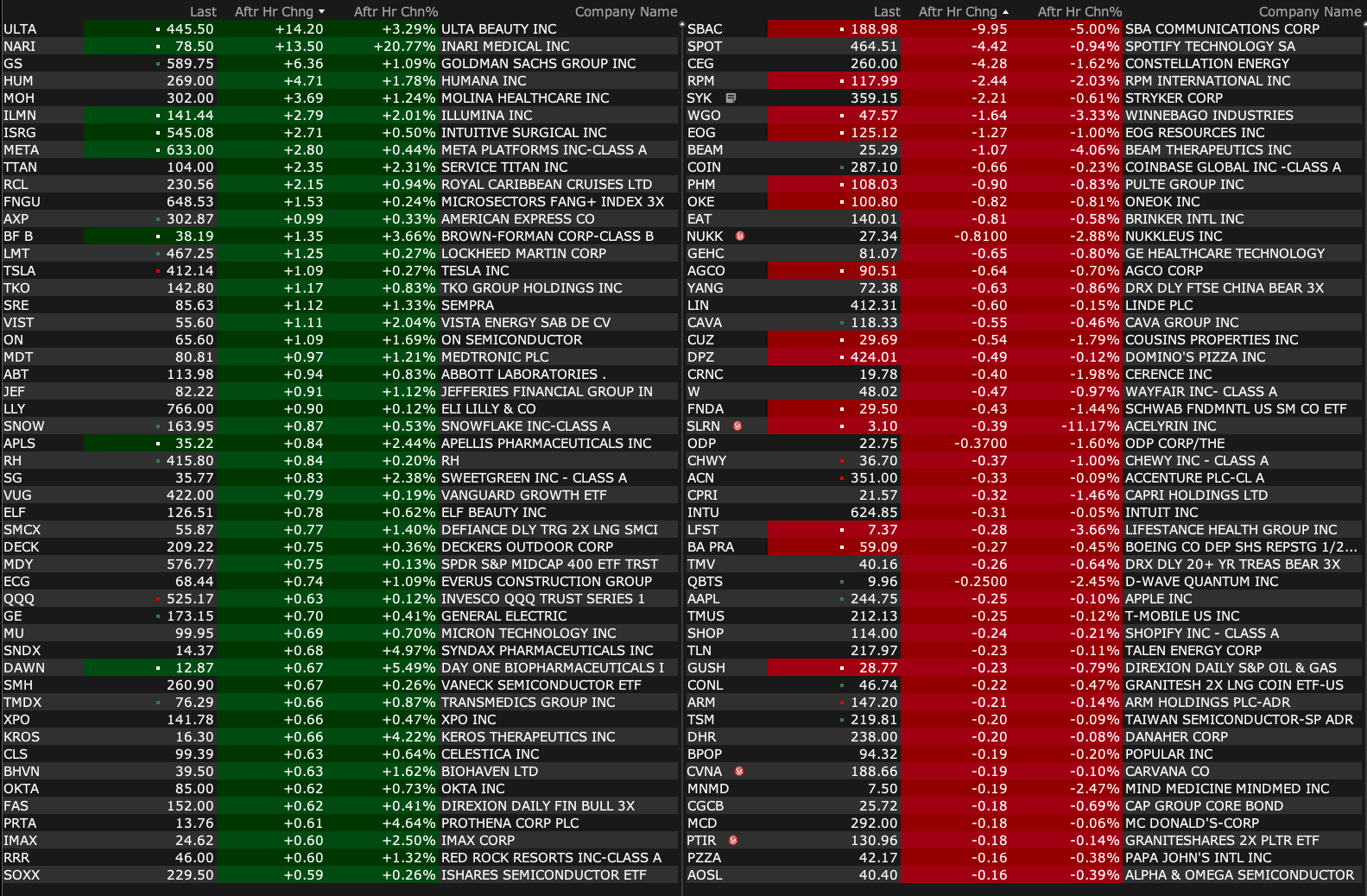

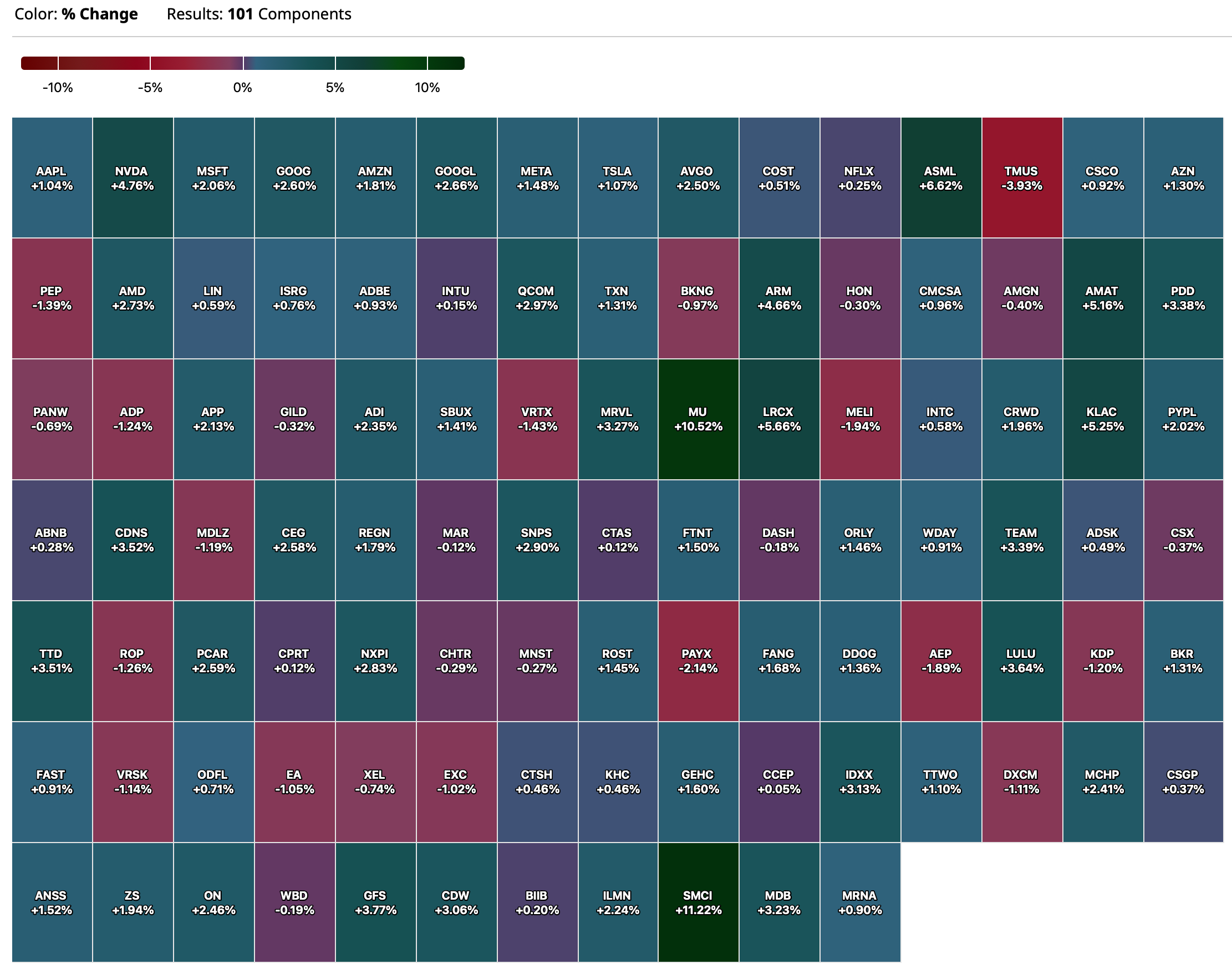

Monday's After-Hours Movers

At 4:18 p.m.:

BY Doug Kass · Jan 6, 2025, 4:26 PM EST

At 4:18 p.m.:

BY Doug Kass · Jan 6, 2025, 4:26 PM EST

BY Doug Kass · Jan 6, 2025, 4:23 PM EST

Allons, enfants de la patrie,

Le jour de gloire est arrivé!

Contre nous de la tyrannie

L’étendard sanglant est levé!1 (bis)

Entendez-vous, dans les campagnes

Mugir ces féroces soldats?

Ils viennent jusque2 dans nos bras

Égorger nos fils, nos compagnes!

Aux armes, citoyens! Formez vos bataillons!

Marchons, marchons! Qu’un sang impur abreuve nos sillons!

- La Marseillaise

If the market closes lower (highly unlikely) ....cue the La Marseillaise scene in Casablanca.

BY Doug Kass · Jan 6, 2025, 3:50 PM EST

* Much like the January 1972 market top?

I remain bearish on equities — in the belief that there is an asymmetric/unattractive ratio of risk to reward at current levels.

As expressed previously in my Diary, my theory has been that the December 2024 investing backdrop may resemble that of December 1972.

Let me, again, explain.

In both periods, we faced a combative President (Nixon/Trump), narrow leadership (it was the Nifty Fifty in the early 1970s and the Magnificent Seven in recent years), interest rates and inflation turned up (from the prior few decades) and public sector debt was climbing rapidly. Like in 1972, we lack visibility today (and a sense of fiscal responsibility on the part of our political leaders with regard to future fiscal policy).

In both periods the forward P/E was extremely elevated (today, at nearly 23x), the market advance was not broadening out, the "animal spirits" took stock prices higher without a commensurate change in future profit forecasts and the equity risk premium was paper thin.

An important market top occurred in January 1973. (1973 was a poor year for the S&P Index and marked the beginning of the end of the Nifty Fifty.)

I expect the same for January 2025 — an important market top, a down year for the averages and marked by the beginning of the end of the Mag 7, which could extend multiple years.

I plan to expand my short exposure on any further market strength.

BY Doug Kass · Jan 6, 2025, 3:00 PM EST

Added to Elanco Animal Health ELAN at $11.91, moving off medium-sized towards large-sized.

BY Doug Kass · Jan 6, 2025, 2:55 PM EST

BY Doug Kass · Jan 6, 2025, 2:50 PM EST

Again I converted my short common (SPY, QQQ) to short calls today.

BY Doug Kass · Jan 6, 2025, 2:41 PM EST

BY Doug Kass · Jan 6, 2025, 2:39 PM EST

I'm picking at individual cannabis names this afternoon.

BY Doug Kass · Jan 6, 2025, 12:58 PM EST

* More on "Peak Musk"...

Bingo99

Hi Doug happy new year ,there has been a lot in the UK press regarding the the current spat between Elon Musk and various politicians in the UK .Personally I have nothing against Mr Musk,he is free to comment on issues as he sees them (right or wrong) but first and foremost he is a business man and his day job is to run some very large companies. If one was a creditor of Musk's one might be concerned that his extra curricular activites might be starting to become something of a distraction (I am sure he can juggle a lot of balls) from his everyday job.A lot of store is set by the market cap of his companies but we know that can vanish in a heartbeat.People clearly feel he is teflon coated however when you start picking fights with Governments in Europe you are moving into a totally different sphere its easy to dissmiss the UK and Germany as sick but these things have a way of biting you in the ass.As you say and I am inclined to agree we might be approaching "peak Musk"

BY Doug Kass · Jan 6, 2025, 12:45 PM EST

BY Doug Kass · Jan 6, 2025, 12:32 PM EST

I have a routine medical examination between 1:30-2:30 p.m. today.

BY Doug Kass · Jan 6, 2025, 12:20 PM EST

BY Doug Kass · Jan 6, 2025, 12:10 PM EST

Tesla TSLA, after a morning gap higher, is now in the red...

BY Doug Kass · Jan 6, 2025, 11:30 AM EST

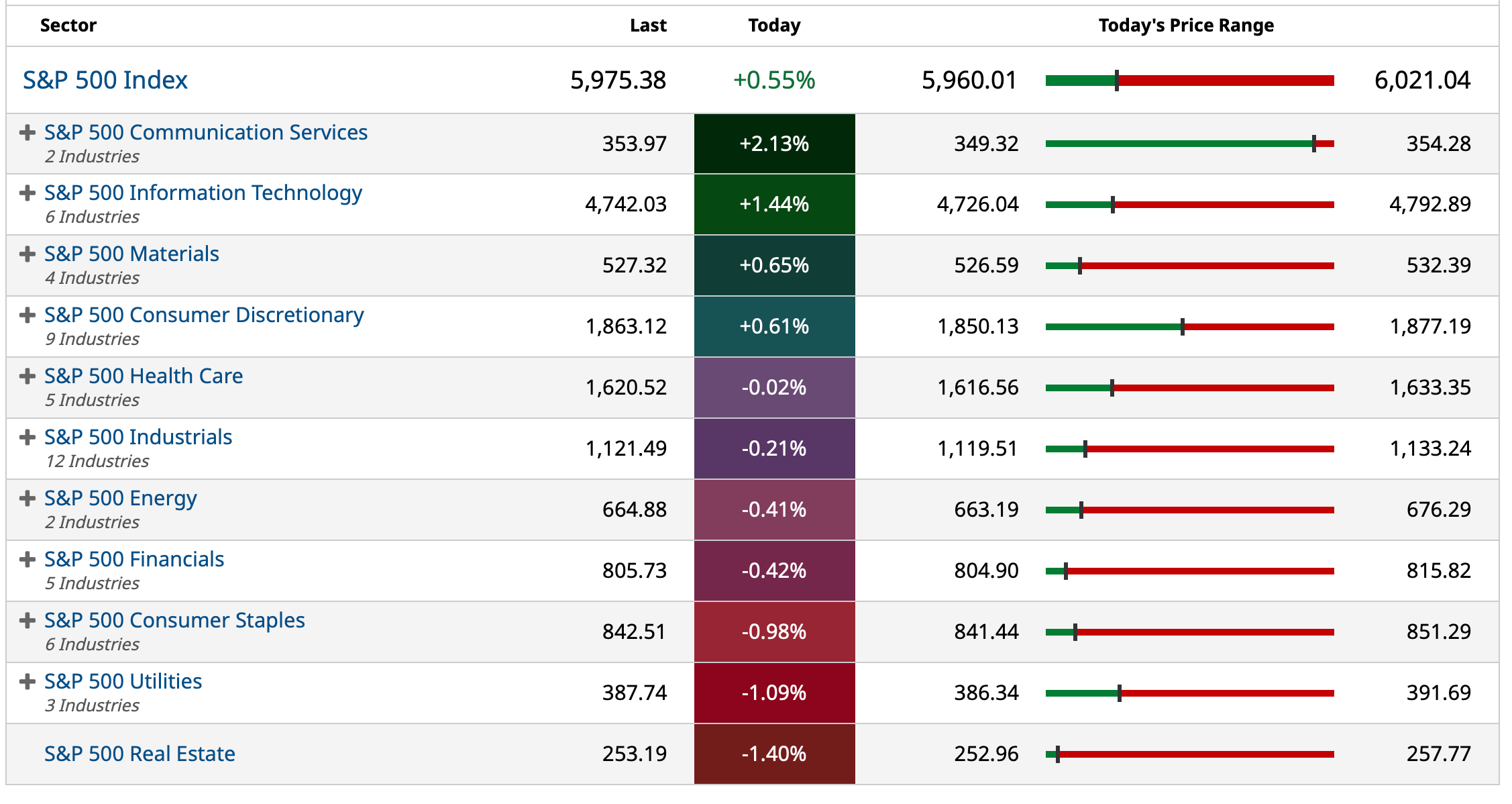

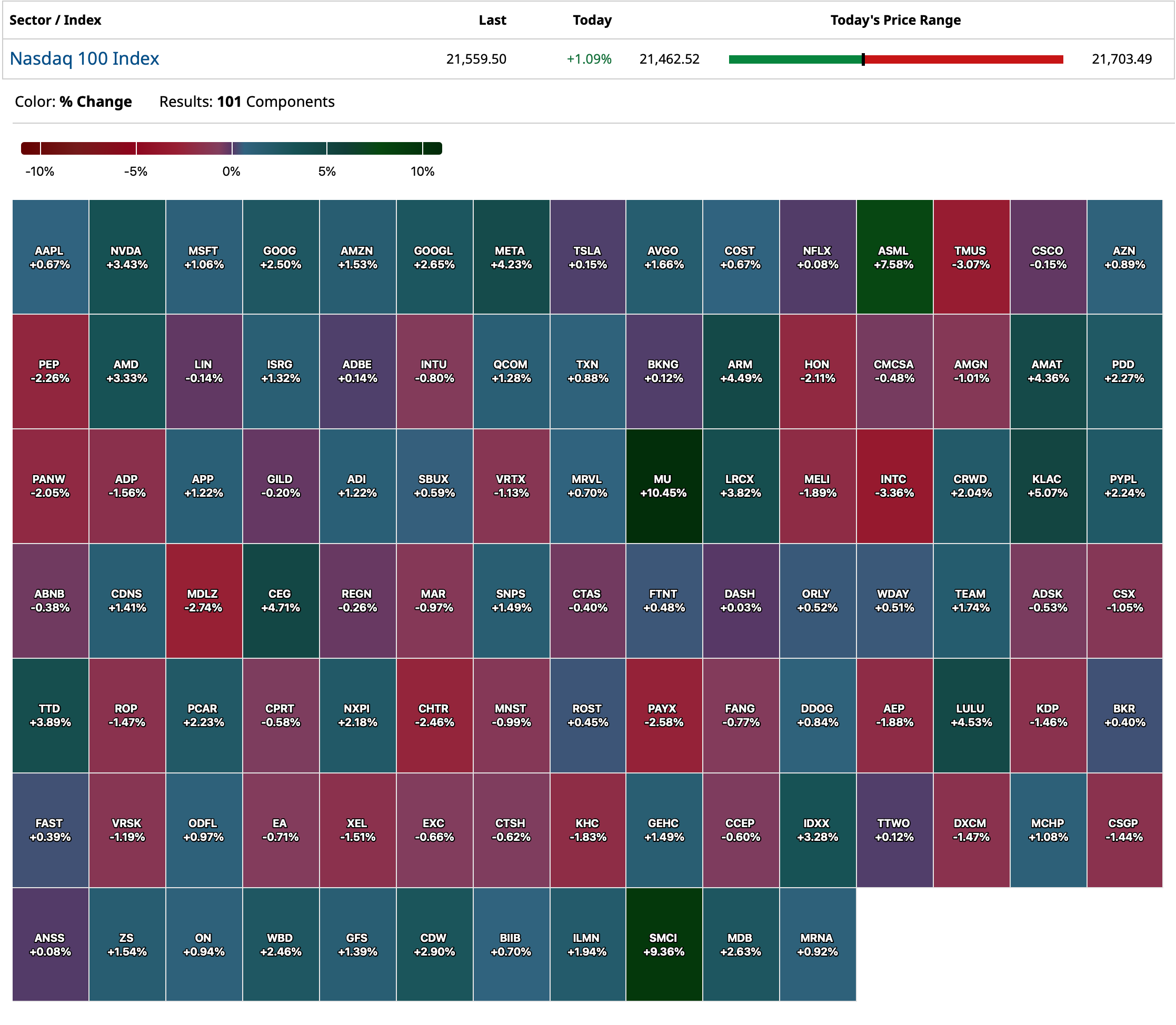

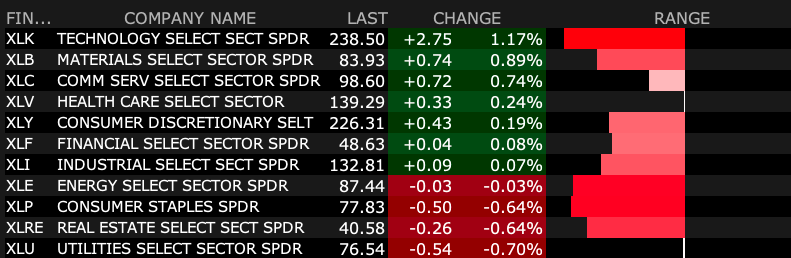

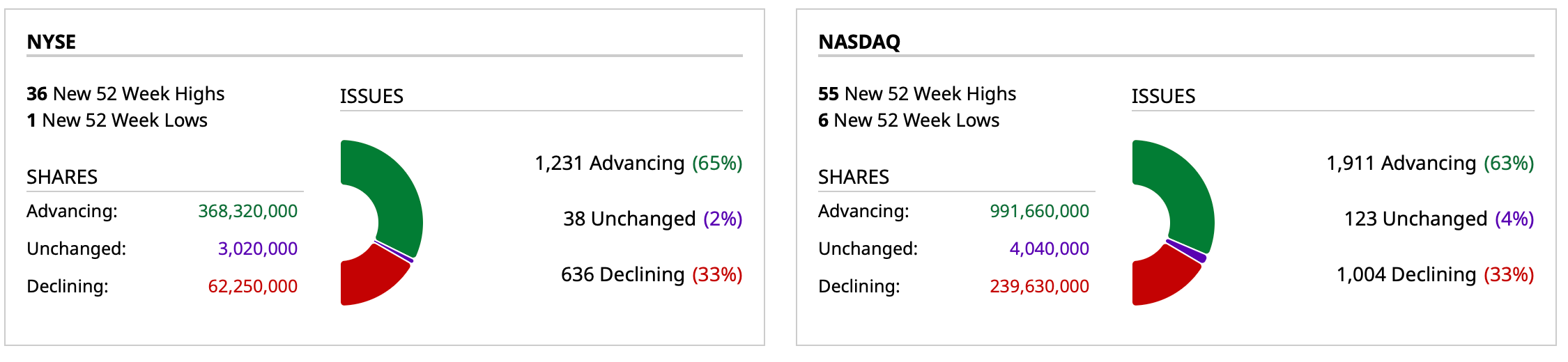

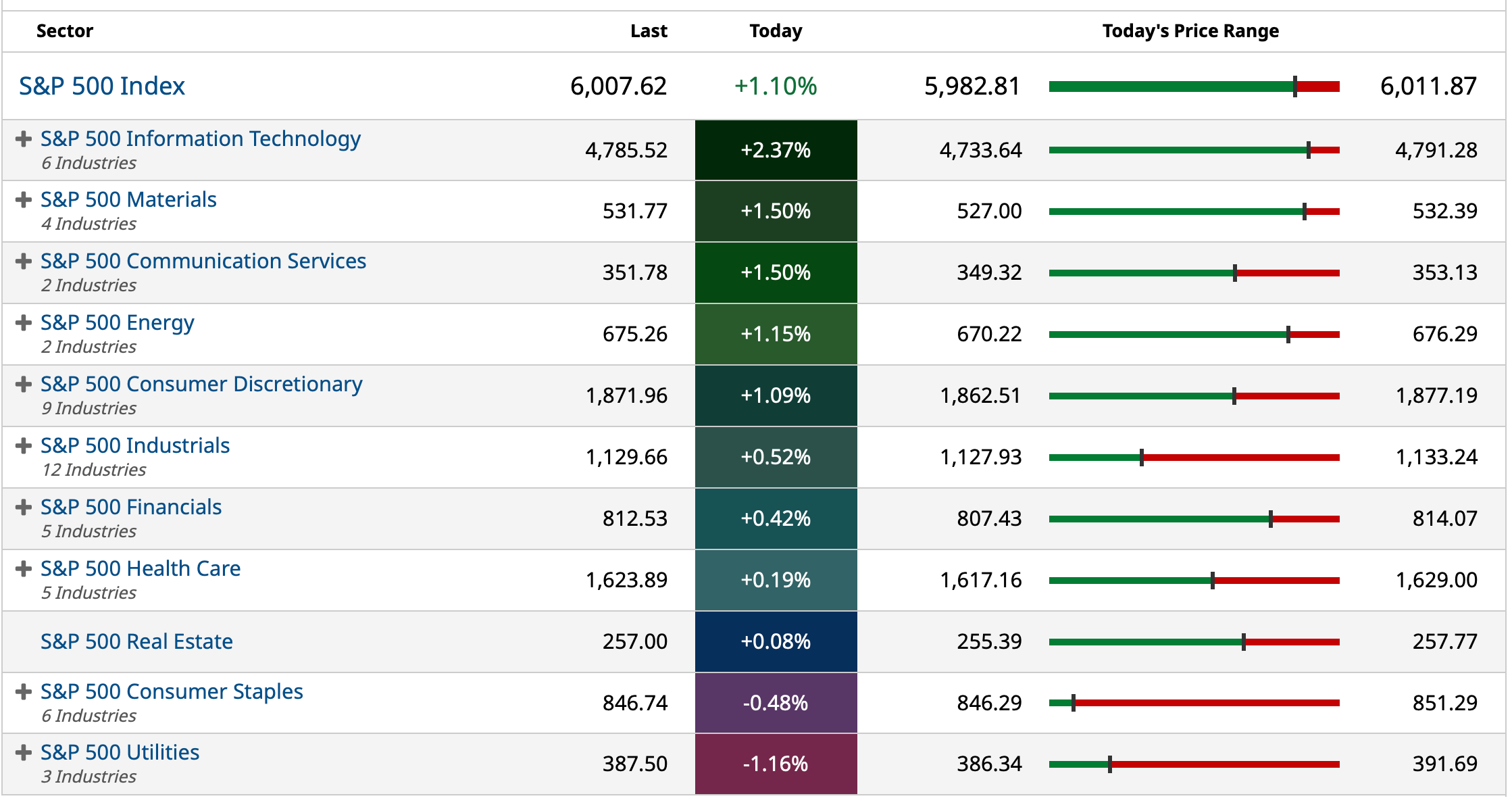

Charts from 10:40 a.m. ET

BY Doug Kass · Jan 6, 2025, 11:21 AM EST

BY Doug Kass · Jan 6, 2025, 11:00 AM EST

BY Doug Kass · Jan 6, 2025, 10:55 AM EST

The 10-year Treasury note yield is now at the day's high -- up by 4.5 basis points to yield 4.64%.

BY Doug Kass · Jan 6, 2025, 10:36 AM EST

* How much longer can this condition last?

Equities remain indifferent (and almost defiant) to the rise in interest rates, again, today.

With the 10-year Treasury note's yield back up to the day's highs (a gain of 3.5 basis points to yield 4.63%) I continue raise my short exposure.

BY Doug Kass · Jan 6, 2025, 10:15 AM EST

With S&P cash +62 handles, putting on my next tranche of Index shorts.

BY Doug Kass · Jan 6, 2025, 10:00 AM EST

From Peter Boockvar:

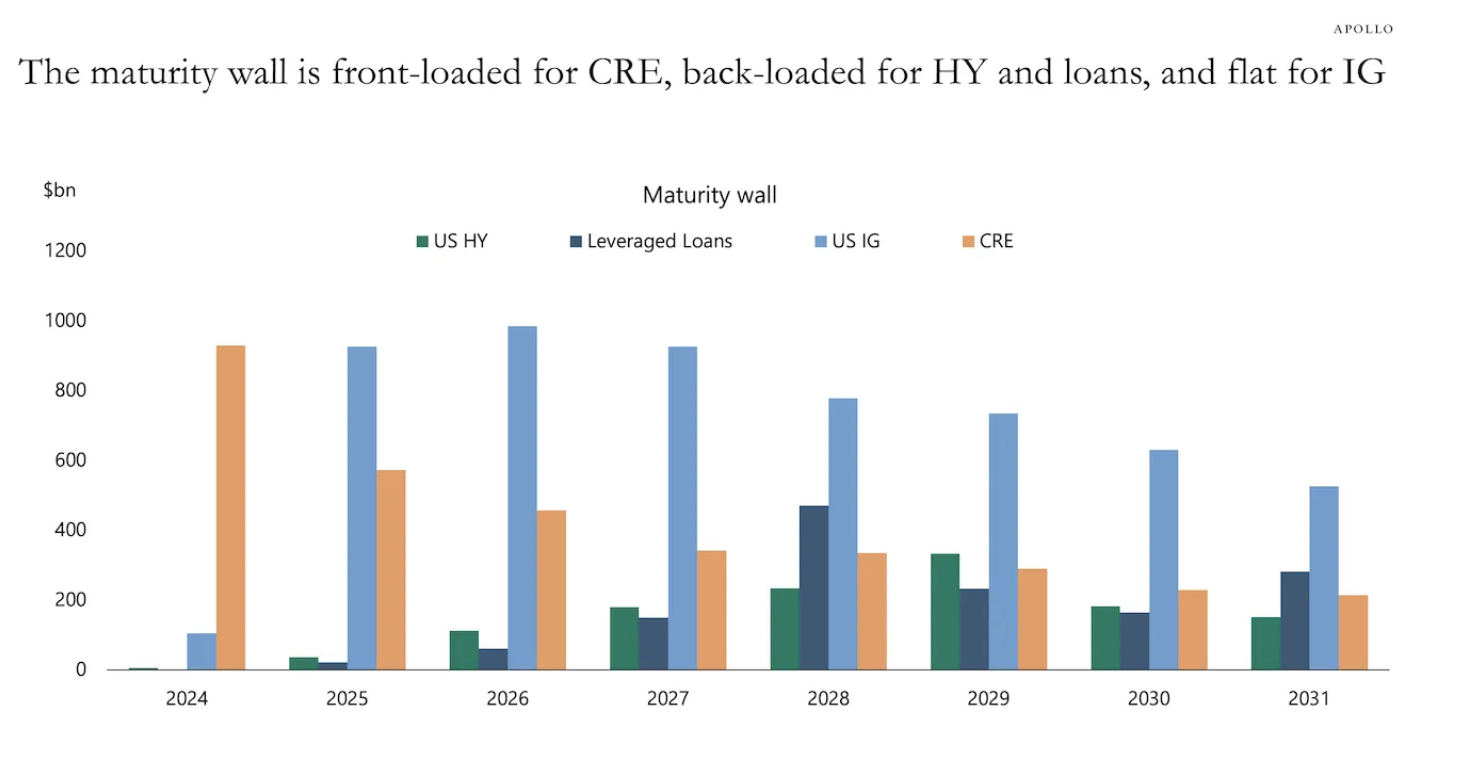

'Long and variable lags' when it comes to the impact of monetary policy on the economy is something we've heard all about for years with the only debate being how long and how variable. After 15 years of essentially zero interest rates preceding the 2022 rise in them, I still believe the impact will be very long and very variable as long as interest rates still stay higher for longer, which I believe they will. Below is a chart from my friend Torsten Slok back in October that he put out in his daily writings quantifying the maturity wall in coming years in high yield, leveraged loans, investment grade and commercial real estate. As seen, the biggest jump over the coming years is from investment grade companies.

Now we don't have to worry about the credit quality of these IG names but I do want to point out that the interest rate this debt will refi into will be a few hundred basis points above the rate on the maturing loan which was most likely priced pre 2022. Keep in mind that one of the key factors in the notable rise in corporate profit margins over the past 20 years has been artificially low interest expense. That along with the lower corporate tax rate and low labor costs.

With respect to the US government's maturity wall this year, my friend Stephanie Pomboy in a recent note mentioned the $10 trillion of maturing US debt this year with about $6 trillion being bills and $4 trillion being longer term notes. Those notes will likely refi also about 200 bps above the maturing rate. On $4 trillion, that's an added $80 billion of interest expense and doesn't include the about $2 trillion extra of debt the US government needs to sell just to finance the budget deficit. By the way, the US Treasury is issuing $119b of new debt just this week.

As for private equity and what higher for longer rates mean for them, this was an interesting tidbit I read over the weekend in the FT 'Long View' column from John Plender. He cites this from McKinsey, "that roughly two-thirds of the total return for buyout deals entered in 2010 or later and exited in 2021 or before can be attributed to broader moves in market valuation multiples and leverage, rather than improved operating efficiency." In other words, much of private equity's success during that time period was due to easy money and a low cost of funding deals.

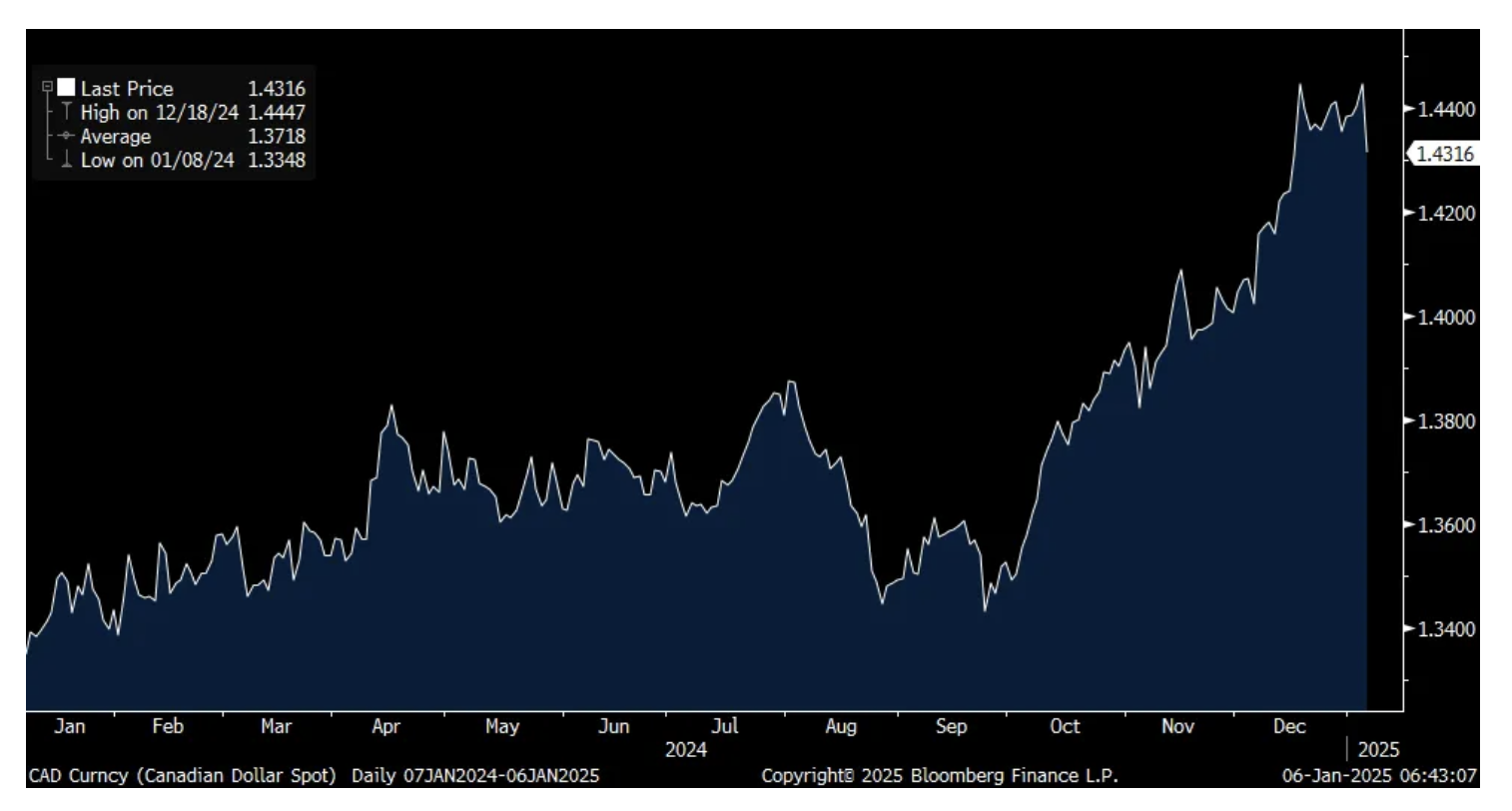

On the likelihood that Justin Trudeau resigns, the Canadian$ is rallying almost 1% and should rally further from here after really getting beaten up last year. It's like a stock rallying after an unliked CEO leaves.

CAD

In case you didn't see, the Washington Post is reporting that "President-elect Donald Trump's aides are exploring tariff plans that would be applied to every country but only cover critical imports, three people familiar with the matter said...If implemented, the emerging plans would pare back the most sweeping elements of Trump's campaign plans but still would be likely to upend global trade and carry major consequences for the US economy and consumers." This more targeted approach that this article is implying should be much more tolerable by the economy and markets rather than my concern of another scattershot repeat of 2017 and 2018. That said, there is no free lunch and will raise the cost of a variety of things. https://www.washingtonpost.com/business/2025/01/06/trump-tariff-economy-trade/

December vehicle sales seen Friday beat expectations with a count of 16.8mm seasonally adjusted annualized rate (SAAR) vs the estimate of 16.5mm. That compares with 15.83mm in December 2023 and 16.7mm in December 2019. Ward's said "The return to growth was aided by rising inventory, increased retail incentives and lower interest rates, while pull-ahead volume of electric vehicles from expectations of cuts in government incentives could have played a part." On the interest rate side, the rate for a 60 month auto loan on average was about 7.40% in December vs the average in 2024 of 7.74%. They fell with the lower fed funds rate.

Average Auto Loan Rate for 60 Month Term

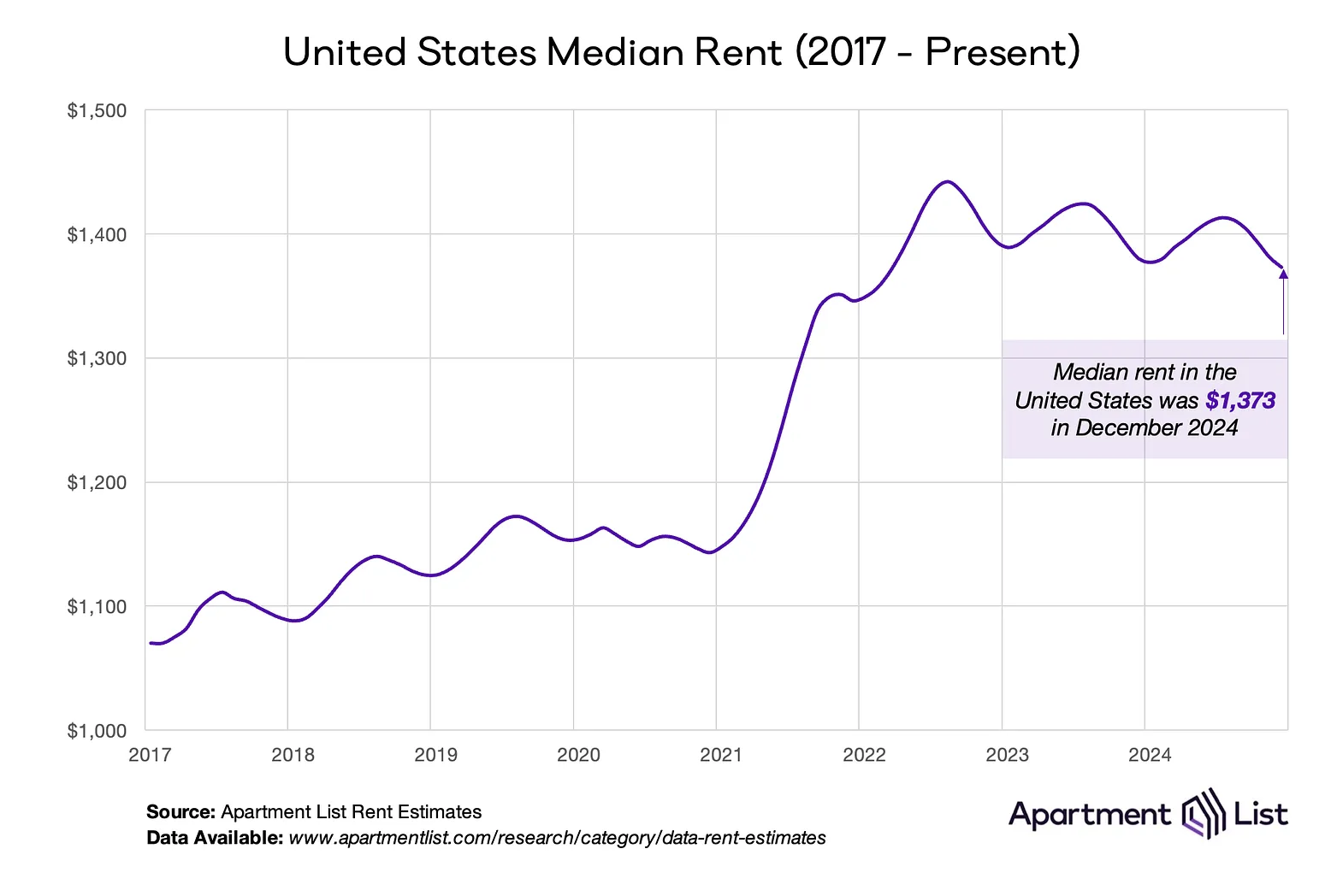

Apartment List on Friday released its December new lease national report and reflected a .6% m/o/m drop, which typically happens this time of the year. The y/o/y decline was also .6%. The vacancy rate continues to creep up slowly, now at 6.8%, up one tenth as a lot of supply mostly in the sunbelt gets absorbed. Apartment List said "2024 saw the most new apartment completions since the mid-1980s, and with nearly 800 thousand units still in the construction pipeline, the supply boom has runway to continue into 2025." That said, the pace of new multi family starts is slowing sharply. The sunbelt markets of Austin, Raleigh, and Jacksonville saw the deepest declines. Seasonally, overall new rents should rebound in the spring.

From what I saw from the publicly traded REITS, the renewal rates are rising about 2-3% in contrast.

Ahead of the US ISM services index at 10am est, we saw some more PMI's overseas. The private sector focused Caixin China services PMI rose to 52.2 from 51.5. This is what Caixin said, "Business activity and total new orders increased for the 24th month in a row, with the former growing at the fastest pace since May, while the latter grew at the fastest clip since July. Overseas demand fell, however, with the gauge dropping to the lowest level since December 2022." Also of note, "Market optimism weakened. The indicator for expectations of future activity stayed in expansionary territory, but fell by more than 3 pts compared with the previous month, leaving it just above September's 4 ½ yr low."

Hong Kong's December PMI was 51.1, little changed with November's print of 51.2. Singapore's slipped to 51.5 from 53.9. Japan's final read was 50.9 from 50.5 and India's services PMI remained strong at 59.3 from 58.4.

The services sector continues to keep the European economy afloat as its PMI was revised to 51.6 from 51.4 initially. That's up from 49.5 in November and vs the same 51.6 in October. An above 50 print for Germany offset the continued weakness in its manufacturing sector. Services in France remains weak but is strong in Spain and flat lining in Italy.

Services in the UK remained a bit above 50 at 51.1 vs 50.8 in November and 52 in October. We await the negative impact of the rise in employee insurance costs out of the new Rachel Reeves budget which is not well liked understandably by UK business.

Finally, keep your eye on those rising JGB yields. The 5 yr JGB yield closed at its highest level since 2009, up 5 bps overnight. The 10 yr yield at 1.14% is the highest since 2011. The bond bear market is global and this particular move up comes after BoJ Governor Ueda said today in his first comments in 2025, "Our stance is that we will raise the policy interest rate to adjust the degree of monetary easing if economic and price conditions keep improving." The yen reversed earlier weakness in response.

5 yr JGB Yield

10 yr JGB Yield

BY Doug Kass · Jan 6, 2025, 9:45 AM EST

With S&P cash +47 handles I am shorting more Index calls. I am also converting my early morning Index common shorts back into calls (with a premium).

BY Doug Kass · Jan 6, 2025, 9:36 AM EST

Trump refutes the "going easy on" tariff story... futures fall from highs.

BY Doug Kass · Jan 6, 2025, 9:32 AM EST

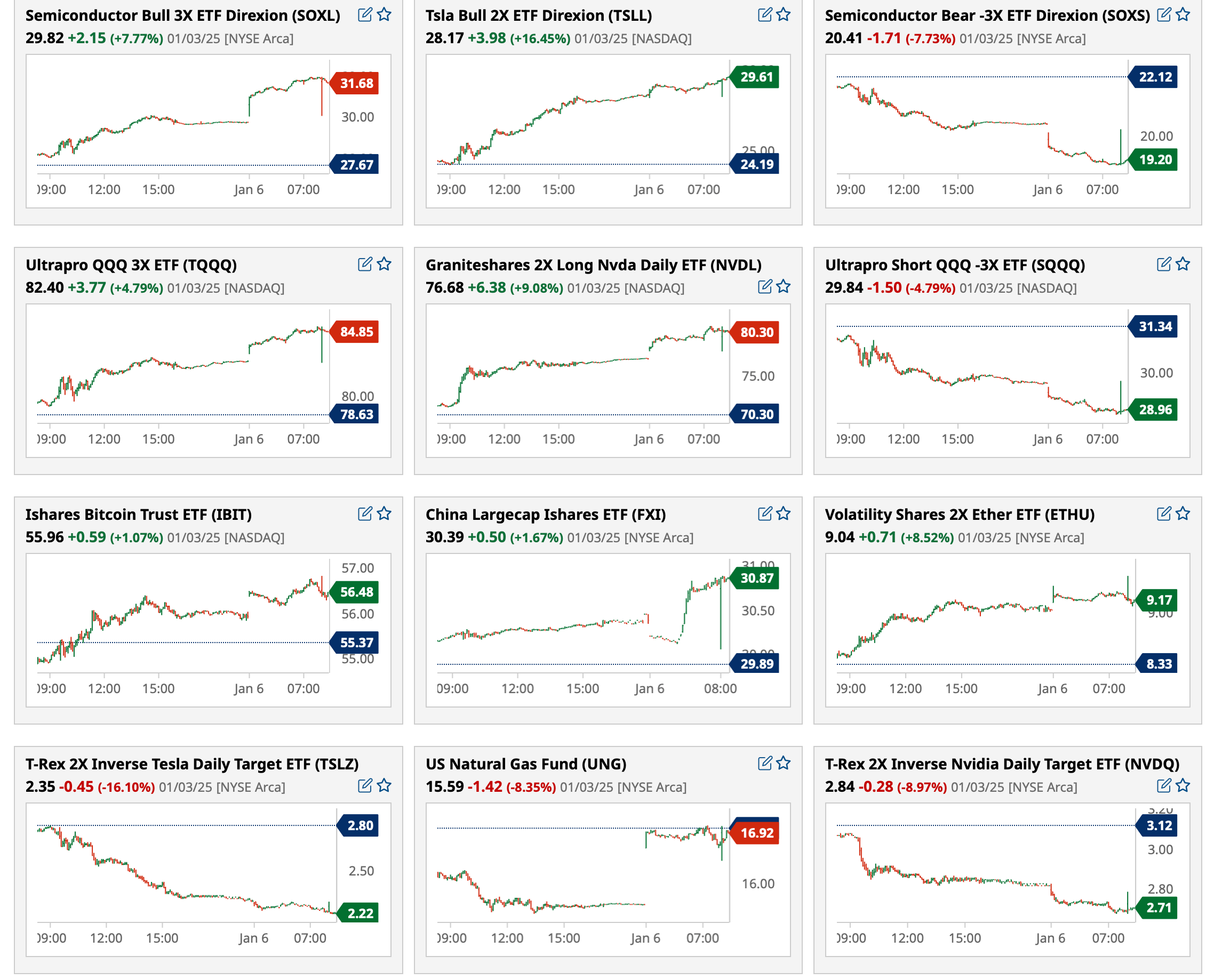

SPY does not make the Top 34 most active premarket ETFs rankings as of 8:19 a.m. ET:

BY Doug Kass · Jan 6, 2025, 9:05 AM EST

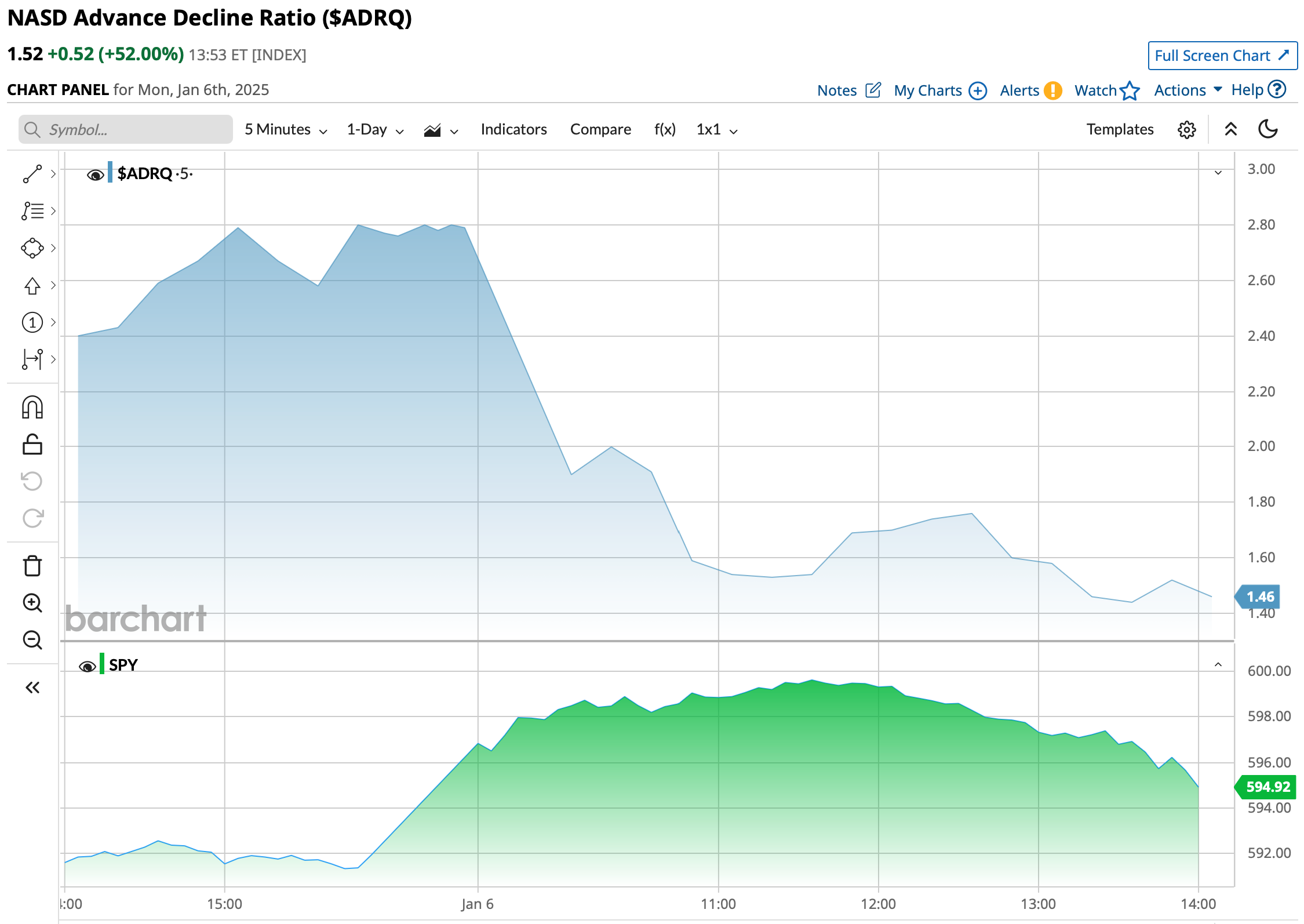

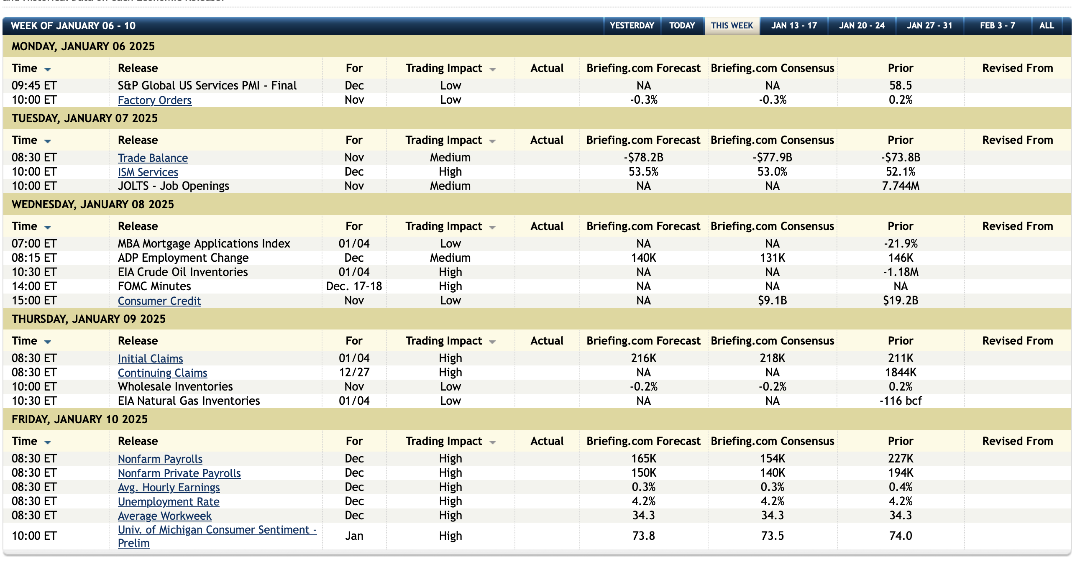

Chart from 8:36 a.m. ET:

BY Doug Kass · Jan 6, 2025, 8:52 AM EST

BY Doug Kass · Jan 6, 2025, 8:21 AM EST

S&P futures +43 handles (and +52 handles from last night's lows) likely based on Nvidia NVDA hopes (tomorrow's meeting), more Microsoft MSFT AI cap spending forecasts and the possibility of less-than-expected tariffs from the incoming administration.

BY Doug Kass · Jan 6, 2025, 7:27 AM EST

Morgan Stanley goes underweight on Palantir PLTR.

Barclays upgrades Citigroup C to overweight.

BY Doug Kass · Jan 6, 2025, 7:10 AM EST

BY Doug Kass · Jan 6, 2025, 7:00 AM EST

Bonus — Here are some great links:

BY Doug Kass · Jan 6, 2025, 6:45 AM EST

Doomberg on "Labor Laundering."

BY Doug Kass · Jan 6, 2025, 6:35 AM EST

BY Doug Kass · Jan 6, 2025, 6:25 AM EST

Wolf Street howls about the status of the U.S. dollar.

BY Doug Kass · Jan 6, 2025, 6:15 AM EST

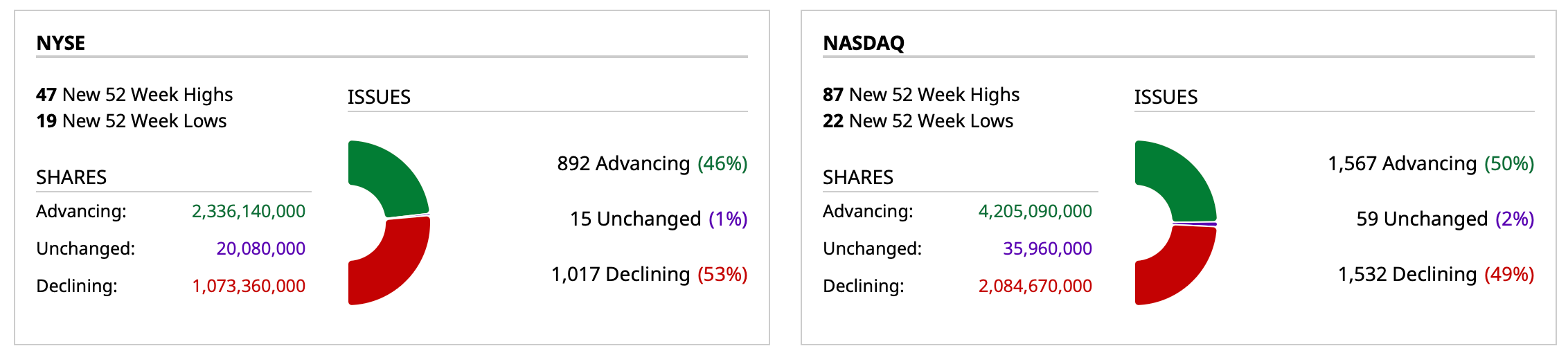

After days in an oversold, the S&P Short Range Oscillator has moved back into an overbought — now at 0.7% vs. -2.54%.

BY Doug Kass · Jan 6, 2025, 6:05 AM EST

BY Doug Kass · Jan 6, 2025, 5:55 AM EST

With bond yields continue to rise I am back re-shorting SPY and QQQ common at $595.01 and $522.80, respectively. (Options are not trading yet or I would have shorted more index calls!)

BY Doug Kass · Jan 6, 2025, 5:46 AM EST