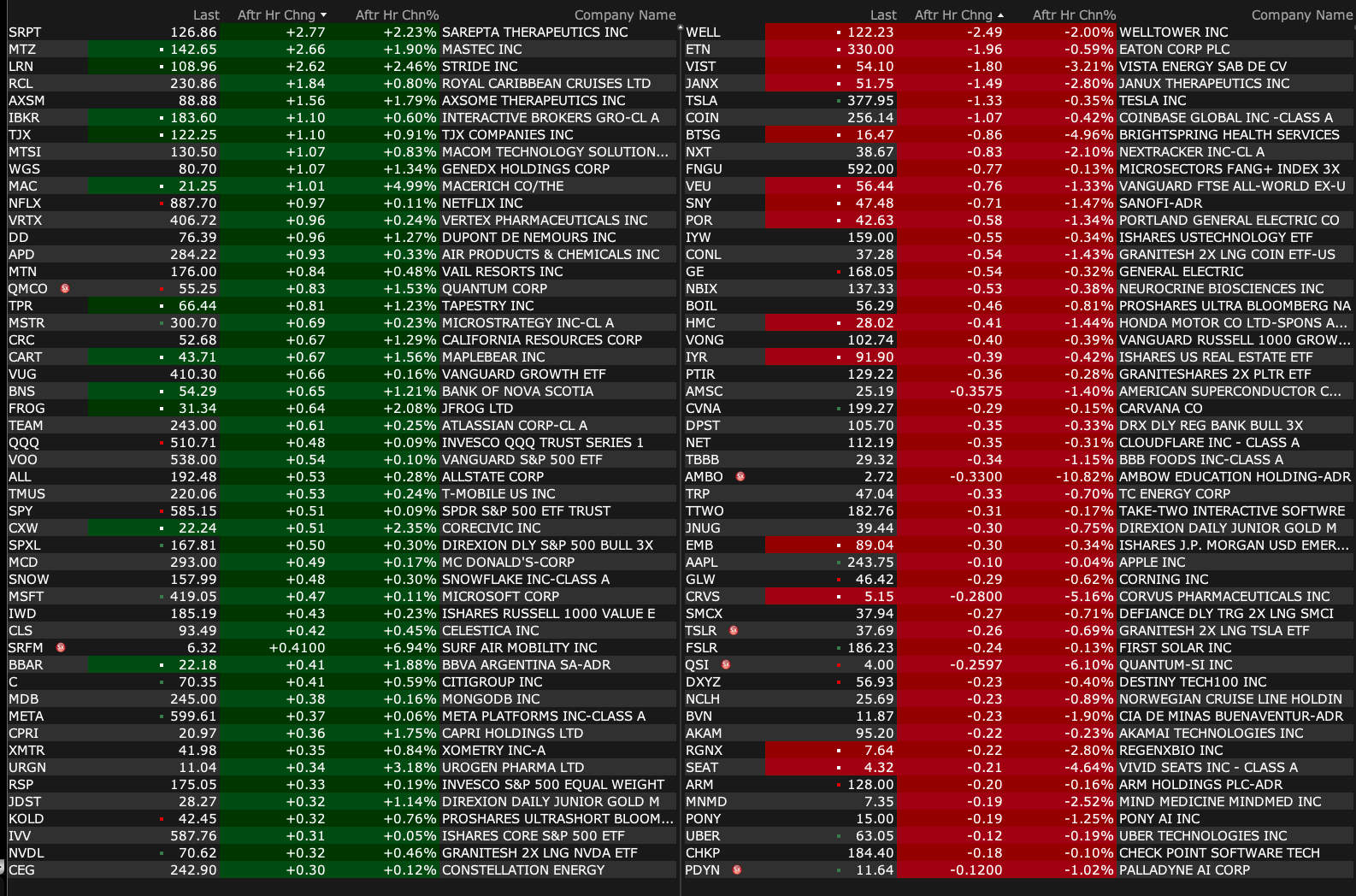

Thursday's After-Hours Movers

As of 4:19 p.m.:

BY Doug Kass · Jan 2, 2025, 5:20 PM EST

As of 4:19 p.m.:

BY Doug Kass · Jan 2, 2025, 5:20 PM EST

BY Doug Kass · Jan 2, 2025, 5:10 PM EST

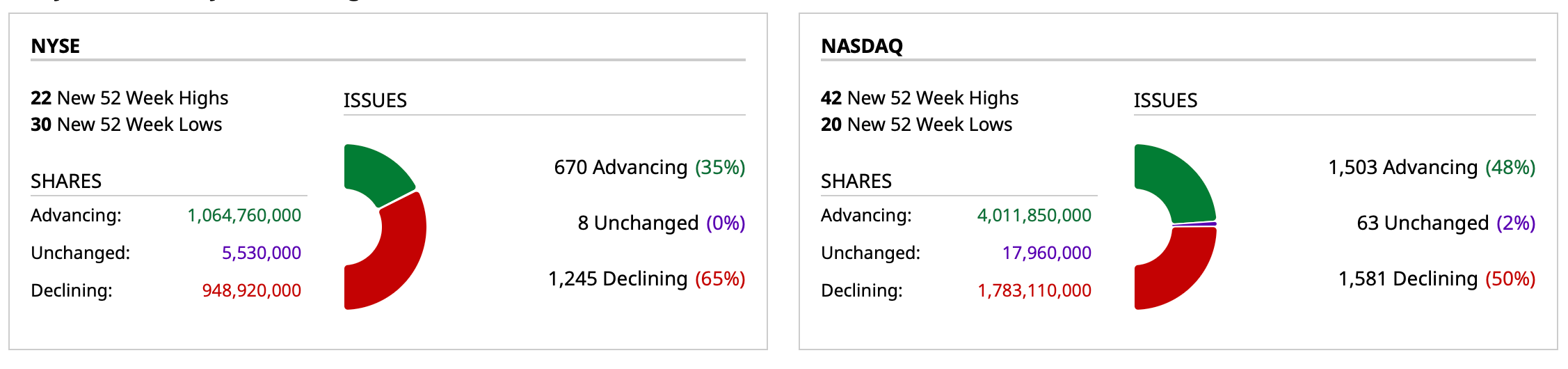

- NYSE volume 10% below its one-month average

- NASDAQ volume 75% above its one-month average

- VIX: up 3.46% to 17.95

BY Doug Kass · Jan 2, 2025, 4:57 PM EST

I took back my short Index calls for a small profit.

This is just a wonderful market for opportunistic traders willing to trade with and against the machines.

BY Doug Kass · Jan 2, 2025, 3:56 PM EST

From my pal Daryl at Hedgeye:

BY Doug Kass · Jan 2, 2025, 3:50 PM EST

With S&P cash down only -10 handles, I am back shorting Index calls.

But baby steps...

BY Doug Kass · Jan 2, 2025, 3:37 PM EST

BY Doug Kass · Jan 2, 2025, 3:30 PM EST

BY Doug Kass · Jan 2, 2025, 3:20 PM EST

Buying more ELAN under $12 and also purchasing calls.

BY Doug Kass · Jan 2, 2025, 3:10 PM EST

I have a research call between 2:30 and the close so there will be no "Things I Did Today" this afternoon.

I will recap in the morning!

BY Doug Kass · Jan 2, 2025, 3:05 PM EST

jesus is here

Serious question: I have hundreds of thousands of dollars in unrealized gains for 2025. Assuming things remain the same or even better what are my options to reduce my tax bill?

Dougie Kass

sell deep in the money calls for early 2026 - against your stock positions!

BY Doug Kass · Jan 2, 2025, 2:53 PM EST

BY Doug Kass · Jan 2, 2025, 2:25 PM EST

BY Doug Kass · Jan 2, 2025, 2:15 PM EST

2 January 2025 | 1:12PM EST

Tesla reported preliminary 4Q24 vehicle deliveries of about 496k (up 7% qoq and up 2% yoy), and production of about 459k (down 2% qoq and down 7% yoy). 2024 deliveries of ~1.79 mn were down 1% yoy.

Deliveries of about 496k were below consensus estimates in the ~500k-510k range (with Visible Alpha at 512k, FactSet at 498k, and GSe at 510k). Recall that in order for Tesla to have met its objective to grow vehicle deliveries in 2024, it would have required ~515k or more units in 4Q.

We believe weakness in Europe (down double digits yoy in 4Q) was offset by growth in China (mid to high teens growth yoy), and that US deliveries were down modestly yoy. Relative to our 510K estimate, the downside was driven by S/X/Cybertruck, and similarly we believe the US market was softer than we had expected.

We expect key focus items from here to include vehicle delivery volumes (and if they can accelerate in 2025), automotive non-GAAP gross margins, progress with FSD, the Energy segment (with strength in storage deployments in the quarter), and progress with Optimus. Please see our note for details.

BY Doug Kass · Jan 2, 2025, 2:01 PM EST

BY Doug Kass · Jan 2, 2025, 12:55 PM EST

On Fin TV you will predominantly hear made-up narratives and feels.

In my Diary you will predominantly read analysis. That said I am often wrong and always in doubt.

You won't get feels but you may get fears.

And I remain fearful of the risks associated with market structure (that you never hear about in the business media).

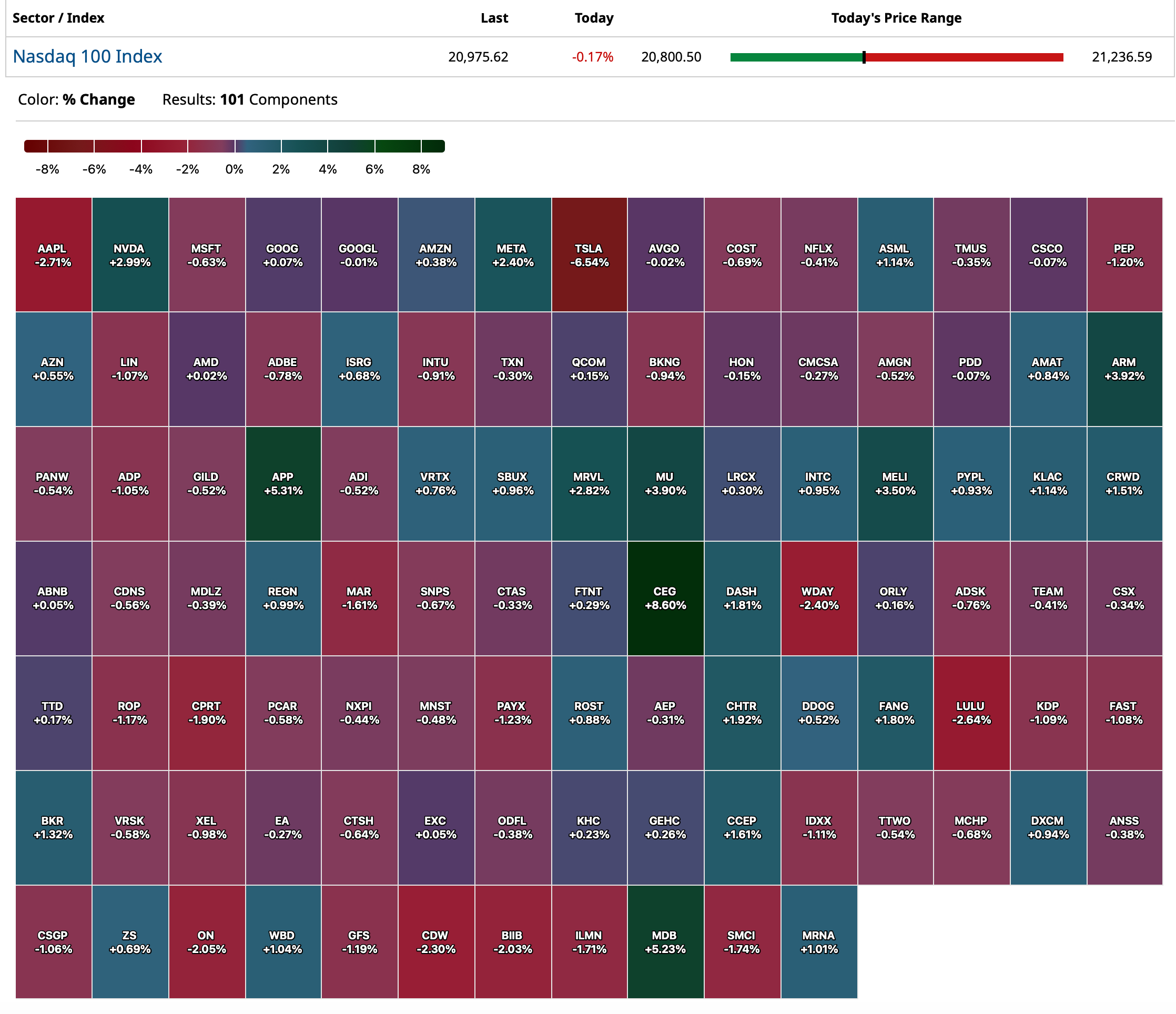

Just look at today's intraday chart of the S&P Index.

I don't think you have seen anything yet!

BY Doug Kass · Jan 2, 2025, 12:45 PM EST

Moved to medium-sized TLT at $87.28.

BY Doug Kass · Jan 2, 2025, 12:20 PM EST

I collapsed my long SPY/QQQ common against short SPY/QQQ calls for a profit just now.

I have no Index exposure now.

BY Doug Kass · Jan 2, 2025, 12:15 PM EST

Back long TLT at $87.34.

BY Doug Kass · Jan 2, 2025, 12:02 PM EST

Adding to JOE with a $45 limit now.

BY Doug Kass · Jan 2, 2025, 11:29 AM EST

From my Surprise List:

Surprise #2: The "other" romance, between Trump/Musk, doesn't make it past Spring, 2025

National protests and demonstrations emerge and demands from a wide array of members of both the Republican and Democratic parties (including conservatives and liberals) call for "ousting" Elon Musk, an unelected official, from playing such a dominant role in the U.S. government.

Bernie Sanders, taking the Senate's mantle of opposition to Musk, tweets about Elon Musk's and other billionaires' outsized role in the government:

"The precedent set in the last few months should upset every American who believes in our democratic form of government. In 2024, just 150 billionaire families spent almost $2 billion to purchase political candidates. Since the election in November, Elon Musk, Jeff Bezos and Mark Zuckerberg got $300 billion richer and are now worth $1 trillion combined. It appears that from now on no major legislation can be passed without the approval of Elon Musk, the wealthiest person in our country. That's not Democracy, it's Oligarchy. We must fight for an economy that works for all, not just the few. Elon Musk is an unelected official that is essentially acting a the President of the United States. We must pass legislation that changes this!"

Funded by George Soros, the law firm Boies, Schiller & Flexner launches a suit restricting the role of unelected officials without official positions in the Administration (like Elon Musk and Vivek Ramaswamy). The suit ends up going to the Supreme Court but is unresolved by year-end.

Reading the room (and increasingly uncomfortable with Musk's nororiety), President Trump begins to be openly critical of Musk and finally abandons him entirely.

Musk lashes out and retaliates by forming his own party and has a nervous breakdown.

Separately, Tesla makes little progress in "full self driving." The U.S. government takes away the $7,500 tax credit, competition from China intensifies, unit sales drop by double digits and Tesla's profits collapse. In addition, an "accounting issue" (related to warranties) is uncovered by a short-oriented research boutique. All these factors cause the shares of (TSLA) to drop to $100/share.

Elon Musk's non-Tesla investments suffer from reduced U.S. government support.

Musk grows ever more unhinged throughout 2025 - his mother attempts a family intervention.

BY Doug Kass · Jan 2, 2025, 11:05 AM EST

Tesla is lower after reporting below consensus fourth quarter deliveries.

BY Doug Kass · Jan 2, 2025, 10:52 AM EST

* Wow!

* Ideal for opportunistic traders....

On whoosh lower to only +12 handles from +46 handles (only minutes ago!) I evened up my short Index calls by purchasing SPY $586.79 and QQQ $511.44.

Delta equivalent neutral in indexes.

BY Doug Kass · Jan 2, 2025, 10:38 AM EST

With S&P cash +46 handles I am shorting some Index calls for February (in the money).

BY Doug Kass · Jan 2, 2025, 10:21 AM EST

What differentiates my hedge fund from many "long/short funds" is that we run a bona fide "hedged" portfolio.

Most of the larger "long/short" hedge funds have abandoned short selling of individual equities all together -- for a variety of reasons. Not the least of which is that they can't get scale on the short side in specific names... they often resort to shorting Indices, if they do anything on the short side at all.

As many recognize by now, I feel as comfortable being short as I feel being long. (I often take trading short rentals in the indexes, for a "cash register" impact).

But, when you look at my bread and butter individual short names, it should be clear that I don't seek drama (and beta!) -- as, I am, in the main, a conservative investor. Rather, I typically focus on non-crowded shorts (in which the short interest as a percent of float and average daily trading volume are low).

Our short selection is based on a bottom-up analysis; it's most often an assessment that companies' business models are deteriorating or broken relative to consensus expectations.

By staying away from popular and crowded, high risk shorts, we see that net-net our short positions -- despite the market's sea of green in 2024 -- contributed positively to our year's investment performance.

Here is a partial list of my holdings in my hedge fund (Seabreeze Partners):

Longs: MSOS, AYRWF, CURLF, TSNDF, VRNOF, ELAN, DKNG, PG, FRPT, VVV, AMZN, AMZN and JOE

Shorts: DJT, KO, PEP, SBUX, BXMT, SNBR, CHGG, WGO,FIGS, AEG, WBA, WBD,MPW, FXLV, WOOF, ABR, RILY, INTU and WMT

BY Doug Kass · Jan 2, 2025, 10:00 AM EST

BY Doug Kass · Jan 2, 2025, 9:49 AM EST

From Peter Boockvar:

Good,

1)Headline GDP continues on with about 2.5% growth.

2)Inflation further decelerates led by rents that reflect reality on the ground.

3)The Fed feels they have more space to cut short rates a few more times.

4)Other central banks, including the ECB, BoE, RBA, BoC and others, cut rates again.

5)Earnings growth meets expectations of around mid teens growth and current high P/E multiples hold.

6)Trump extends the expiring 2017 tax cuts.

7)Regulatory relief on business takes hold, DOGE works some magic with government and tariffs implemented are targeted with pinpoint precision and not widespread.

8)Credit spreads remain tight and companies maintain a high level of refinancing maturing debt.

9)With a new FTC Chair, the M&A and IPO window opens wide.

10)The AI excitement and trade continues and many companies find success in integrating the tools into their businesses, enhancing productivity and efficiency.

11)The war in Ukraine ends as it does in Gaza and the Houthis are also destroyed.

12)China’s economy bottoms out as home prices stop going down and consumer spending rebounds.

13)Germany gets a new president that thru fiscal policy initiatives and a China economic rebound experiences a lift in growth which in turn helps other European economies.

Not Good,

1)The economy remains very split with upper income spending, AI CapEx and government largess the only main areas of growth.

2)The slowdown in rent growth is offset by a bottoming out in goods prices and lift in commodity prices leaving inflation stuck around 3%.

3)The Fed cuts a few more times but because of rising unemployment and long rates rise anyway. The increase in unemployment leads to less tax revenue, enhancing worries about U.S. debts and deficits.

4)The rate cuts only further worry long end bond investors and globally rates rise further in the long end. The BoJ hikes rates a few more times and the sovereign bond bear market continues on. The US 10 yr yield retests 5% and breaks through it.

5)Mid teens earnings growth is just not realistic with rates staying elevated, fiscal spending’s influence slowing down and Mag 7 profit growth slows. Also, profit margins shrink as Corporate America continues to digest higher interest expense. Lower interest expense over the 15 yrs pre 2022 was a key driver of profit margin expansion. The P/E multiple on the broad market falls as higher for longer interest rates finally matter.

6)Trump relies too heavily on tariffs as the pay-for needed to extend the tax cuts.

7)Tariff policy becomes scattershot and retaliatory tariffs back are widespread. The manufacturing recession deepens in response and helps to reaccelerate inflation that is not just a one time price adjustment.

8)Default rates on loans continue higher as the current cost of capital becomes overwhelming for some as debt comes due. It starts to infect the high yield market. In the FT last week, "US companies are defaulting on junk loans at the fastest rate in four years, as they struggle to refinance a wave of cheap borrowing that followed the Covid-19 pandemic. Defaults in the global leveraged loan market - the bulk of which is in the US - picked up to 7.2% in the 12 months to October, as high interest rates took their toll on heavily indebted businesses, according to a report from Moody's. That is the highest rate since the end of 2020."

9)Private equity continues to have difficulty unloading holdings as IPO window continues to remain mostly shut because of the still high cost of capital. According to an FT article last week, "Cambridge associates, a leading advisor to large institutions on their private equity investments, estimated that funds had fallen about $400b short in payments to their investors over the past three years compared with historical averages."

10)All the AI spend weighs on profitability for the hyperscalers and the use of Gen AI tools are slow to catch on and enhancements and uses of it for business are only around the edges.

11)The war of attrition in Ukraine continues on and energy prices, particularly natural gas, moves much higher as the pipeline deal via Ukraine with Russian gas ends and is not renegotiated. What we saw in New Orleans and maybe in Vegas is just a dress rehearsal for more attacks from Islamic jihadists.

12)Either China’s economy does continue to slow or it rebounds which leads to a rise in commodity prices, particularly oil and industrial metals prices.

13)Higher energy prices continue to make the German economy less competitive and/or China’s slowdown puts a continued lid on their economy.

Moving to some economic data, we got a slew of manufacturing PMI's for December and they were mixed overall. China's Caixin manufacturing index fell to 50.5 from 51.5. Caixin said "Exports dragged on demand amid mounting uncertainties stemming from the overseas economic environment and global trade. The corresponding indicator was in contractionary territory for the fourth time in the past five months." Also, "business confidence eased in the latest survey period. Chinese manufacturers were the least upbeat since September. This was as concerns about the outlooks for growth and trade, especially amidst the US tariffs threat, challenged hopes for new product and policy driven sales growth in the new year."

Taiwan's PMI rose to 52.7 from 51.5, Indonesia's was 51.2 from 49.6, Thailand's 51.4 fro, 50.2, and the Philippines saw a lift to 54.3 from 53.8. On the flip side, South Korea's PMI fell back under 50 at 49 from 50.6, Vietnam's was 49.8 from 50.8 and the Malaysia's was 48.6 vs 49.2. The final India read was 56.4 vs 56.5. Japan's was 49.6 vs 49 while Australia's fell to 47.8 from 49.4.

The revisions to the Eurozone and UK manufacturing PMI's were each down slightly and the recession for each rolls on. The Eurozone index stands at 45.1 with Germany down at 42.5 and France at 41.9. The UK's manufacturing PMI was 47. Spain is the bright spot, with its PMI at 53.3.

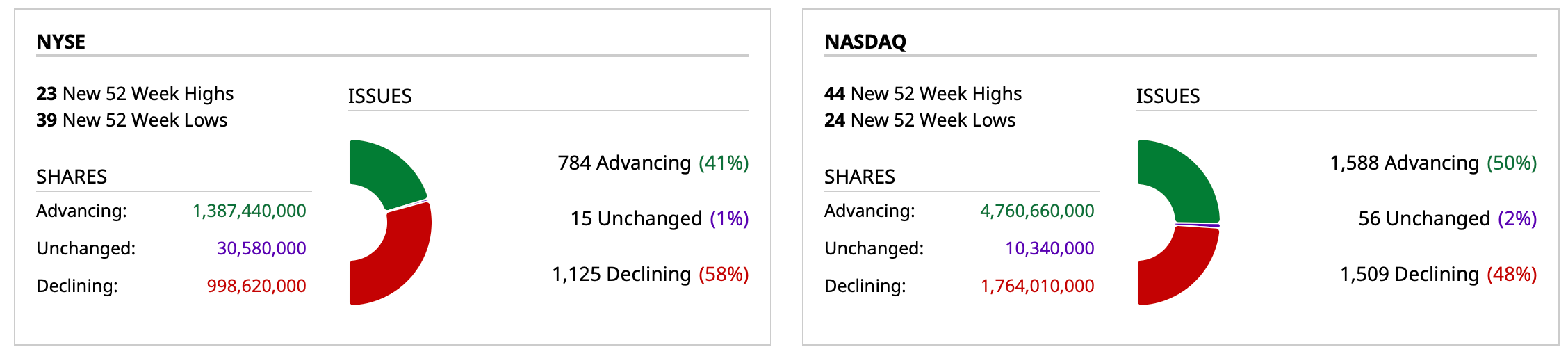

BY Doug Kass · Jan 2, 2025, 9:30 AM EST

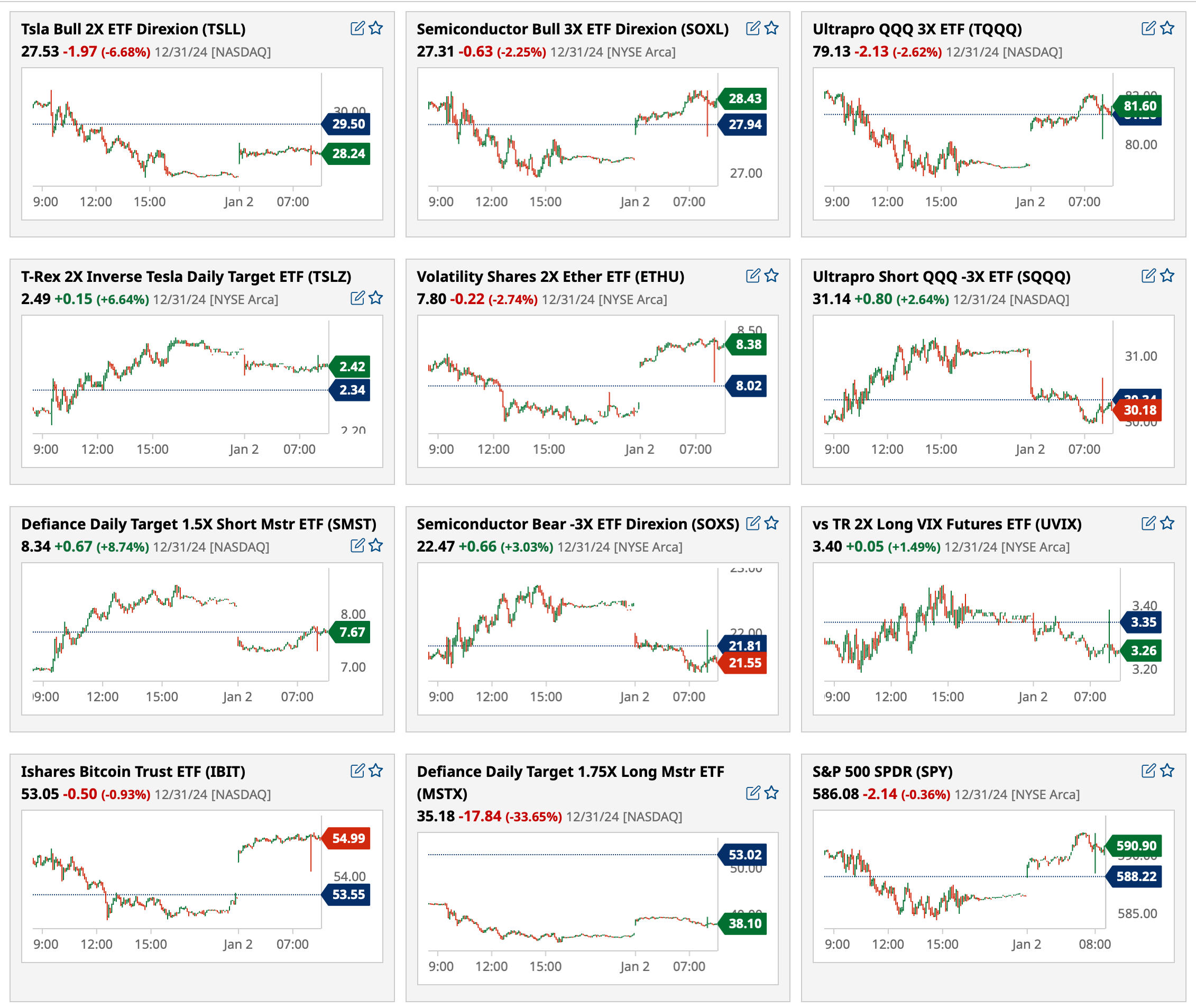

Charts from 8:29 a.m. ET.

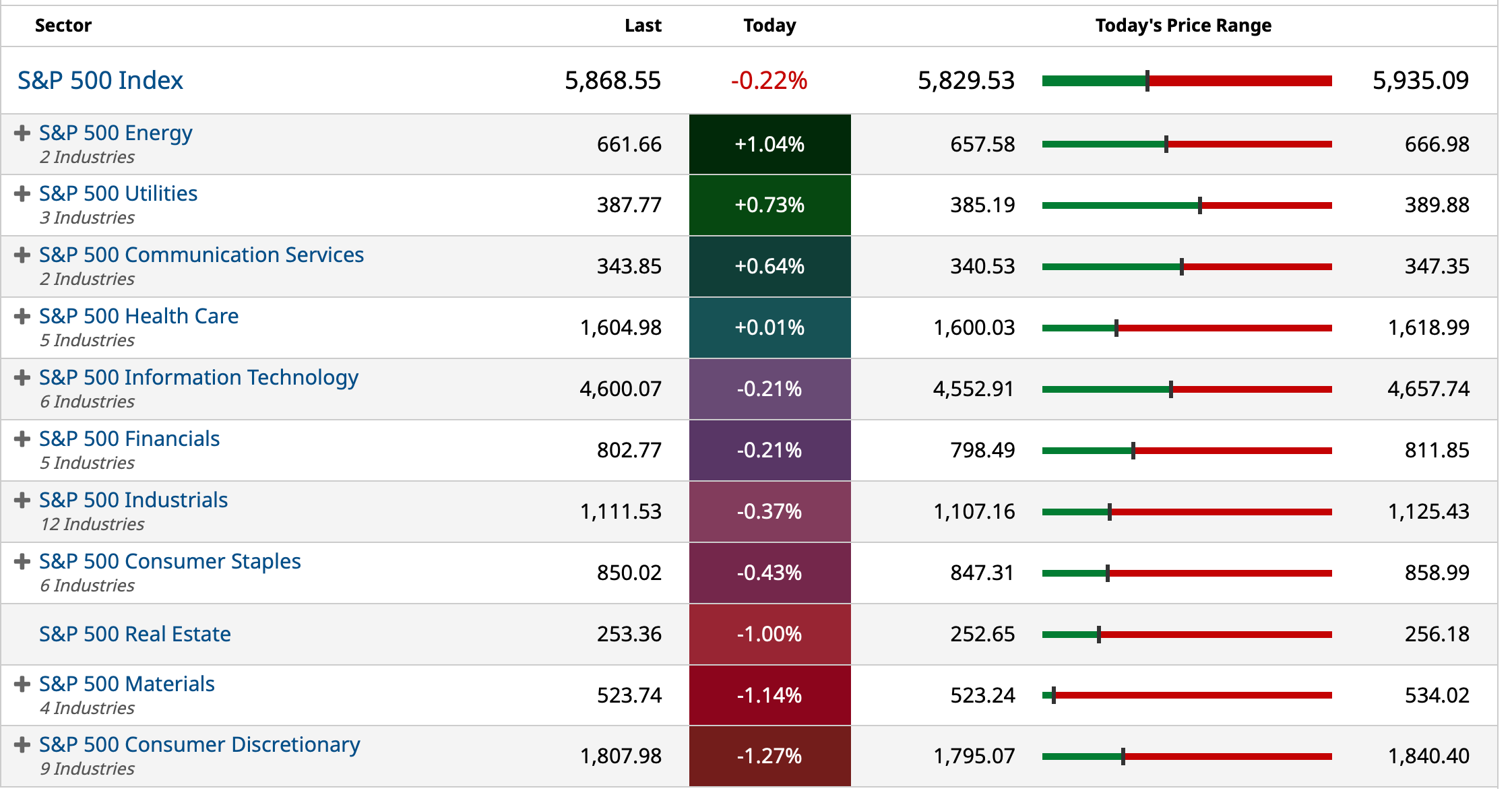

BY Doug Kass · Jan 2, 2025, 9:17 AM EST

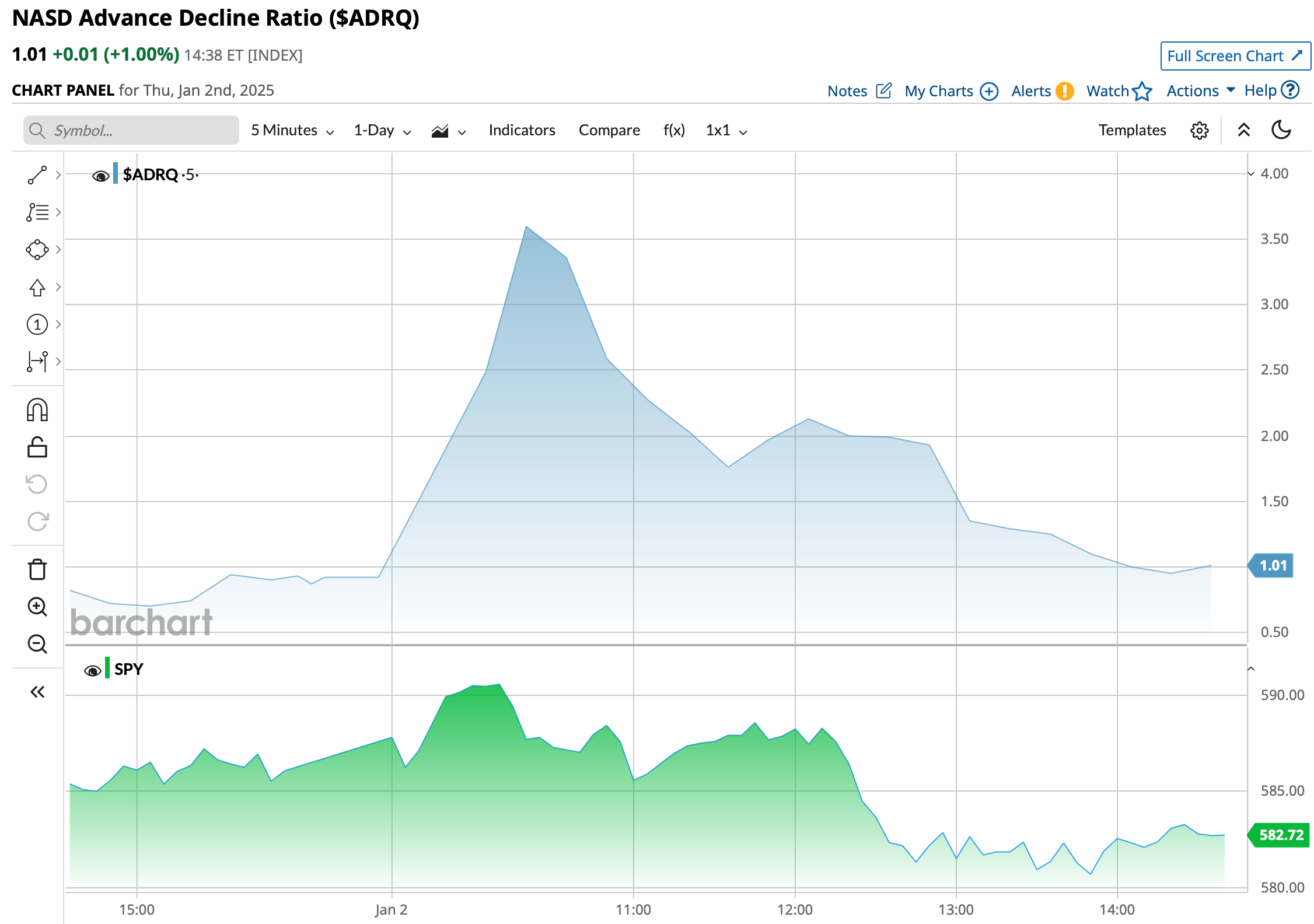

Chart from 8:49 a.m. ET:

BY Doug Kass · Jan 2, 2025, 9:09 AM EST

I ended the year with about a 95% gross exposure in Seabreeze Partners, my hedge fund.

However, in net terms I was approximately market neutral at Tuesday's close.

BY Doug Kass · Jan 2, 2025, 9:00 AM EST

-U +9% Roaring Kitty post

-NIO +1% deliveries

-MODG +10% upgrade

-HOOK +6% M&A speculation

-SOFI -3% downgrade

-VERI -23% secondary

-MKFG -3% litigation update

BY Doug Kass · Jan 2, 2025, 8:45 AM EST

BY Doug Kass · Jan 2, 2025, 8:31 AM EST

BY Doug Kass · Jan 2, 2025, 6:50 AM EST

BY Doug Kass · Jan 2, 2025, 6:40 AM EST

BY Doug Kass · Jan 2, 2025, 6:15 AM EST

The S&P Short Range Oscillator slipped to less oversold as of Tuesday evening — at -3.79% vs. -4.88%.

BY Doug Kass · Jan 2, 2025, 6:05 AM EST

BY Doug Kass · Jan 2, 2025, 5:55 AM EST

Wolf Street howls about 2024.

BY Doug Kass · Jan 2, 2025, 5:45 AM EST